Multi-purpose open-end monitoring procedures for multivariate observations based on the empirical distribution function

Abstract

We propose nonparametric open-end sequential testing procedures that can detect all types of changes in the contemporary distribution function of possibly multivariate observations. Their asymptotic properties are theoretically investigated under stationarity and under alternatives to stationarity. Monte Carlo experiments reveal their good finite-sample behavior in the case of continuous univariate, bivariate and trivariate observations. A short data example concludes the work.

keywords:

[class=MSC2010]keywords:

, and

1 Introduction

From an historical perspective, monitoring is often associated with control charts also known as Shewart charts. Such graphical tools central to statistical process control (see, e.g., Lai, 2001; Montgomery, 2007, for an overview) are usually calibrated in terms of the so-called average run length (ARL) controlling how many monitoring steps are necessary on average before the data generating process is declared out of control. The fact that this conclusion (that is, that the probabilistic properties of the monitored observations have changed) is reached with probability one could be regarded as a drawback of this type of procedure, in particular if false alarms are very costly. To remedy this situation, Chu, Stinchcombe and White (1996) have proposed to treat the issue of monitoring from the point of view of statistical testing. The main advantage is that, when observations arise from a stationary time series, monitoring procedures à la Chu, Stinchcombe and White (1996) will lead to the conclusion that a change has occurred in the data generating process only with a small probability controlled by the user. For a recent nicely written literature review comparing monitoring as carried out in statistical process control to approaches based on statistical tests à la Chu, Stinchcombe and White (1996), we refer the reader to the introduction of Gösmann et al. (2022).

In addition to being statistical tests, the monitoring procedures investigated in this work are nonparametric and deal with -dimensional observations, . In that respect, as we continue, we use the superscript [ℓ] to denote the th coordinate of a vector (for instance, . As is customary in the sequential testing literature, we assume that we have at hand observations from the initial data generating process. Monitoring starts immediately thereafter. To be more precise, we assume that we have at our disposal a stretch , , from a -dimensional stationary time series with unknown contemporary distribution function (d.f.) given by , . These available observations will be referred to as the learning sample as we continue. Once the monitoring starts, new observations arrive sequentially and the aim is to issue an alarm as soon as possible if there is evidence that the contemporary distribution of the most recent observations is no longer equal to .

Most approaches in the literature are of a closed-end nature: the monitoring eventually stops if stationarity is not rejected after the arrival of a final observation , . Our focus in this work is on the more difficult scenario in which the monitoring can in principle continue indefinitely: this is called the open-end setting. From a practical perspective, it can be argued that the fact that the monitoring horizon does not need to be specified is a great advantage of open-end procedures. The price to pay for open-endness is however a significantly more complicated theoretical setting. Indeed, as discussed for instance in Remark 2.2 of Gösmann, Kley and Dette (2021), while the asymptotics of closed-end procedures can usually be derived using functional central limit theorems, such results are insufficient in the open-end case and need to be either combined with Háyék-Réyni type inequalities (see, e.g., Kirch and Weber, 2018, and the references therein) or replaced by approximations of the form of forthcoming Condition 2.5 (see Aue and Horváth, 2004; Aue et al., 2006).

The null hypothesis of the sequential testing procedures studied in this work is

| (1.1) |

When , starting from the work of Gösmann, Kley and Dette (2021), Holmes and Kojadinovic (2021) have recently introduced a detection procedure that is particularly sensitive to changes in the mean. Because it uses the retrospective cumulative sum (CUSUM) statistic as detector, it turns out to be more powerful then existing procedures as long as changes do not occur at the very beginning of the monitoring. As noted in Section 6 of the latter reference, this approach can be adapted to obtain alternative procedures that are particularly sensitive for instance to changes in the variance or some other moments. The goal of this work is to generalize the method of Holmes and Kojadinovic (2021) in order to obtain open-end monitoring procedures that can be sensitive simultaneously to all types of changes in the d.f. . Although such procedures already exist in a closed-end setting (see, e.g., Kojadinovic and Verdier, 2021), to the best of our knowledge, they are unavailable in the open-end setting.

This paper is organized as follows. In the second section, starting from the work of Gösmann, Kley and Dette (2021) and Holmes and Kojadinovic (2021), we propose a detector that can be sensitive to all types of changes in the contemporary d.f. of multivariate observations. We additionally introduce a suitable threshold function and study the asymptotics of the resulting monitoring procedure under in (1.1) and under sequences of alternatives to . In the third section, we focus on the case of continuous observations and provide additional asymptotic results under the null. In the fourth section, using asymptotic regression models, we address the estimation of high quantiles of the distributions appearing in the asymptotic results under which are necessary in practice to carry out the sequential tests. The fifth section summarizes the results of numerous Monte Carlo experiments for whose aim is to study the finite-sample behavior of the monitoring procedures under and under alternatives to . A data example and concluding remarks are gathered in the last section.

Unless mentioned otherwise, all convergences are as . Also, as there are many discrete intervals appearing in this work, we will conveniently use the notation , , , and for the sets of integers , , , and , respectively. Note that all mathematical proofs are gathered in a series of appendices and a non-optimized implementation of the monitoring procedures studied in this work is available in the package npcp (Kojadinovic and Verhoijsen, 2022) for the R statistical environment (R Core Team, 2022).

2 A first detector, the threshold function and related asymptotics

2.1 A first detector and the threshold function

One of the two main ingredients of a monitoring procedure à la Chu, Stinchcombe and White (1996) is a statistic, also called a detector, that is potentially computed after the arrival of every new observation , . This statistic is typically positive and quantifies some type of departure from stationarity. Once computed, it is compared to a positive threshold, possibly also depending on . If greater, evidence against in (1.1) is deemed significant and the monitoring stops. Otherwise, a new observation is collected.

For sensitivity to changes in the mean of univariate () observations, Holmes and Kojadinovic (2021) used among others the detector

| (2.1) |

where , . Some thought reveals that, for any fixed , is akin to the so-called retrospective CUSUM statistic frequently used in offline change-point detection tests (see, e.g., Csörgő and Horváth, 1997; Aue and Horváth, 2013).

When , to be sensitive to changes in the d.f. at a fixed point , a straightforward adaptation of the previous approach would be to compute (2.1) from the stretch of univariate observations , where inequalities between vectors are to be understood componentwise. The detector can then be equivalently expressed as

| (2.2) |

where, for any integers ,

| (2.3) |

is the empirical d.f. of evaluated at . Our aim is to extend the previous approach using points in , where the integer and the points are chosen by the user. Let and, for any , let , which is a -dimensional random vector. Combining the approach of Gösmann, Kley and Dette (2021) with the one of Holmes and Kojadinovic (2021), the first detector considered in this work is defined by

| (2.4) |

where, for any integers , , is an estimator (based on ) of the long-run covariance matrix

| (2.5) |

of the -dimensional time series and, for any , denotes a weighted norm of induced by a positive-definite matrix and the integer .

Remark 2.1.

The role of the matrix when using the Mahalanobis-like norm in (2.4) is, roughly speaking, to standardize and decorrelate under the null vectors of the form before computing their norm (scaled by ). As shall become clearer from Theorem 2.6 below, a consequence of that step is that a key limiting null distribution playing a central role in the testing procedure will not depend on the characteristics of the underlying time series but only on the number of points chosen by the user. The latter desirable property from a practical perspective is also the reason why we did not consider, instead of in (2.4), alternative detectors that evaluate differences of empirical d.f.s at all the points in . One natural such alternative detector is

| (2.7) |

Such a detector was actually considered in a closed-end setting by Kojadinovic and Verdier (2021) and required in practice the use of bootstrapping when monitoring serially dependent observations. The major practical obstacle related to its use in an open-end setting will be discussed in Remark 2.13.

The second key ingredient of a monitoring procedure is a threshold function. In the considered open-end setting, given a significance level , the aim is to define a deterministic function such that (ideally) under in (1.1),

| (2.8) |

where the supremum is over integers . Because the detector in (2.4) or in (2.6) can be regarded as a multivariate generalization of the detector in (2.1), one can use the same reasoning as in Section 2 of Holmes and Kojadinovic (2021) to suggest that a meaningful threshold function in the considered case is

| (2.9) |

where is a positive real parameter and is the -quantile of , the weak limit of under , assuming that is continuous. In that case, under , by the Portmanteau theorem,

| (2.10) |

which can be regarded as an “asymptotic version” of (2.8). As far as is concerned, as a consequence of Proposition 2.10 below, it needs to be chosen strictly positive so that is almost surely finite. In practice, we follow the recommendation made in Holmes and Kojadinovic (2021) and set to 0.001.

Remark 2.2.

Proceeding for instance along the lines of Horváth et al. (2004), Fremdt (2015), Kirch and Weber (2018), Gösmann, Kley and Dette (2021) or Holmes and Kojadinovic (2021), instead of in (2.9), one could alternatively consider as a threshold function defined by , , where

with a real parameter and a technical constant that can be taken very small in practice. The multiplication of a candidate threshold function by was initially considered in Horváth et al. (2004) and Aue and Horváth (2004) for the so-called ordinary CUSUM detector in order to study, under suitable alternatives, the limiting distribution of the detection delay (the time delay after which the detector exceeds the threshold function). From a practical perspective, as discussed in Holmes and Kojadinovic (2021), an appropriate choice of may improve the finite-sample performance of the sequential test at the beginning of the monitoring. The multiplication of a candidate threshold function by does not however affect the asymptotics of the underlying monitoring procedure.

2.2 Asymptotics under the null

One of the first assumptions required to be able to study the asymptotics (as , of the monitoring procedure based on in (2.4) and in (2.9)) concerns the long-run covariance matrix in (2.5) of the -dimensional time series , under the null. As we shall see later in this section, it will be necessary to consider both its inverse and its square root . The following assumption guarantees that these two matrices exist (and are unique).

Condition 2.3 (On the long-run covariance matrix ).

Remark 2.4.

Under and when the time series consists of independent observations, the elements of in (2.5) are simply

where denotes the element-wise minimum operator. Hence, in the case of serially independent observations, by definition of positive-definiteness, Condition 2.3 will hold if the points appearing in are chosen such that any linear combination of the , , has a strictly positive variance. A necessary condition for this is that all belong to the support of and are all distinct. Since the law of is unknown, the user could in practice rely on the learning sample to choose . If the learning sample seems to be a stretch from a discrete time series, a natural possibility consists of choosing from a subset of frequently occurring observations. The choice of when the observations in the learning sample seem to arise from a continuous time series will be discussed in Section 3.

As shall become clearer in the forthcoming paragraphs, studying the asymptotics under the null (of the monitoring procedure as ) actually amounts to establishing the weak limit of under in (1.1). The following assumption on the time series (a type of “strong approximation” condition) is typical of the kinds of assumptions in the sequential change-point literature; see, e.g., Assumption 2.3 in Gösmann, Kley and Dette (2021), Condition 3.1 in Holmes and Kojadinovic (2021) and the corresponding discussions in these references. Let denote the Euclidean norm.

Condition 2.5 (Approximation).

There exists a probability space on which:

-

•

is a -dimensional stationary time series satisfying Condition 2.3,

-

•

for each , and are two independent -dimensional standard Brownian motions,

such that, for some ,

| (2.11) |

and

| (2.12) |

We use the notation ‘’ to denote convergence in distribution (weak convergence) and to denote the identity matrix. The following result, proven in Appendix A, can be regarded as a multivariate extension of Theorem 3.3 of Holmes and Kojadinovic (2021).

Theorem 2.6.

Note that in Theorem 2.6 the supremum on the left is over integers while the supremum on the right is over real numbers .

Remark 2.7.

It is important to note that the limiting random variable depends neither on the characteristics of the underlying time series (such as its dimension , its serial dependence properties or the unknown d.f. ), nor on the user-chosen points involved in the definition of . It only depends on the integer and on the real . The latter is due to the use of the Mahalanobis-like norm in (2.4) as hinted at in Remark 2.1. As shall become clearer below, an important practical consequence of this is that the monitoring procedure can be used as soon as it is possible to compute or estimate quantiles of for the chosen parameters and . This important aspect will be investigated in Section 4 in more detail.

For a given serial dependence scenario under in (1.1), it is hoped that Condition 2.5 will hold for many different vectors of points . The following proposition shows that this is for instance the case when the time series is strongly mixing under . Given a time series and for any , denote by the -field generated by and recall that the strong mixing coefficients corresponding to are defined by

The sequence is then said to be strongly mixing if as .

The following result, proven in Appendix B, is a consequence of Theorem 4 of Kuelbs and Philipp (1980).

Proposition 2.8.

The previous proposition leads to the following immediate corollary of Theorem 2.6.

Corollary 2.9.

Assume that the time series is stationary and strongly mixing, and that its strong mixing coefficients satisfy as with . Then, for any fixed and any vector of points such that Condition 2.3 holds,

The strong mixing conditions in the previous corollary are for instance satisfied (with much to spare) when is a stationary vector ARMA process with absolutely continuous innovations (see Mokkadem, 1988).

The following result, proven in Appendix B, can be regarded as a multivariate extension of Proposition 3.4 of Holmes and Kojadinovic (2021). It shows that imposing that is strictly positive in Theorem 2.6 and Corollary 2.9 is necessary and sufficient for ensuring that the limiting random variable is almost surely finite.

Proposition 2.10.

For any fixed ,

Remark 2.11.

In relation to the previous result, note that in (2.9) could actually be replaced by , where when and when . Indeed, as explained in Remark 3.5 of Holmes and Kojadinovic (2021), by the law of the iterated logarithm for Brownian motion, all the results stated before Proposition 2.10 should continue to hold with such a modification which could be considered optimal in the sense that, as , diverges slower to infinity than for any . We did not however consider such a change as it is unwieldy from a practical perspective as shall become clearer from Section 4.

The next proposition, also proven in Appendix B, shows that the weak limit appearing in Theorem 2.6 and Corollary 2.9 is absolutely continuous. The proof is an application of Theorem 7.1 of Davydov and Lifshits (1984) together with an argument allowing us to reduce the problem to compact sets.

Proposition 2.12.

For any and , is an absolutely continuous random variable.

Let us finally explain how Theorem 2.6 can be used to carry out the monitoring in practice for a chosen vector of points for which Condition 2.3 is assumed to hold. Given a significance level , suppose that we are able to compute , the -quantile of . Then, under in (1.1) and Condition 2.5, from the Portmanteau theorem, (2.10) holds. Hence, for large , we can expect that, under and Condition 2.5,

In practice, after the arrival of observation , , is computed from and compared to the threshold (or, equivalently, is computed and compared to ). If greater, the null hypothesis is rejected and the monitoring stops. Otherwise, is collected and the previous iteration is repeated using the available observations.

Remark 2.13.

Under a suitable transformation of Condition 2.5, we suspect that it is possible to obtain an analogue of Theorem 2.6 for the detector in (2.7). From the closed-end results obtained in Proposition 2.5 of Kojadinovic and Verdier (2021), we can actually guess the form of the corresponding weak limit. This leads us to believe that, under in (1.1) and a suitable version of Condition 2.5,

| (2.13) |

where the limit is almost surely finite and is a Kiefer process, that is, a two-parameter centered Gaussian process whose covariance function is given, for any and , by

| (2.14) |

Thus, it appears that in general, the weak limit in (2.13) depends on the characteristics of the underlying time series . This implies that in general, to carry out monitoring based on the detector , one would need to be able to estimate high quantiles of the weak limit in (2.13) prior to every execution of the procedure. Given the unwieldy form of the weak limit, this seems to be a major obstacle to the use of the detector . One exception may be when the monitored observations are univariate (), continuous and serially independent. In that case, using a change of variable (as is classically done for instance when dealing with a Brownian bridge), it can be verified that the weak limit in (2.13) no longer depends on the characteristics of the underlying time series . To estimate high quantiles of the resulting weak limit, one could then proceed as in forthcoming Section 4 where the estimation of high quantiles of the weak limit appearing in Theorem 2.6 is addressed. Due to the apparently rather limited scope of application of an open-end monitoring procedure based on , we do not pursue the investigation of such a sequential test in this work and leave this for future research.

2.3 Asymptotics under alternatives

To complement the previously stated asymptotic results, it is necessary to study the asymptotics of the monitoring procedure under sequences of alternatives to in (1.1). Because it is based on the detector in (2.4), the studied monitoring procedure is expected to be particularly sensitive to alternative hypotheses of the form

corresponding to a change in the d.f. at one or more of the chosen evaluation points. Note that this can be interpreted as a change in mean since by rewriting in terms of the univariate time series , we get the following equivalent statement

| (2.15) |

As already mentioned at the beginning of Section 2, monitoring procedures designed to be particularly sensitive to changes in the mean were studied in Holmes and Kojadinovic (2021). Theorem 3.7 and Condition 3.7 in the latter reference specifically provide conditions under which, for a sequence of alternatives to related to in (2.15), , where is defined as in (2.2) with . For the sake of brevity, we do not restate these conditions with the notation used in this work as they are lengthy to write. Very roughly speaking, they imply that for “early” or “late” changes in the d.f. of the observations at , the scaled detector will end up exceeding any fixed threshold provided is sufficiently large. The following result, proven in Appendix C, shows that, as , the same will hold for the scaled detector , where is defined in (2.4).

Proposition 2.14.

Let and assume that for some , . Then, if , where is positive-definite and is positive-definite almost surely for all ,

3 The case of continuous observations: practical implementation and additional asymptotic results under the null

Prior to using the monitoring procedure based on the detector in (2.4), the user needs to choose the points . Following the discussion initiated in Remark 2.4, using the learning sample to do so seems meaningful. As mentioned in the latter remark, when the observations are discrete, a natural possibility consists of choosing from a subset of frequently occurring observations. We focus in this section on the more complicated situation when the learning sample seems to be a stretch from a continuous time series.

Fix and assume that is large. Having Theorem 2.6 as well as Remark 2.7 and Corollary 2.9 in mind, one can hope that, under in (1.1), has roughly the same distribution as the random variable for all vectors of points such that Condition 2.3 holds. A user who is interested in very specific changes in the d.f. may choose accordingly. Otherwise, one natural possibility is to select the vector of points such that the coordinates of each of the points are empirical quantiles computed from the coordinate samples of the learning sample . As we continue, for any , let be the univariate margins of defined in (2.3). Also, for any univariate d.f. , let denote its associated quantile function (generalized inverse) defined by , , with the convention that . Finally, let denote the points when chosen automatically from the learning sample and let .

3.1 The univariate case

When , a natural instantiation of the previous generic strategy for choosing consists of setting , , that is, the ’s are merely taken as the -empirical quantiles of the learning sample . As we will see in Section 5, this strategy seems to lead to powerful multi-purpose open-end monitoring procedures in the case of univariate observations.

3.2 The multivariate case

A natural first idea when is simply to apply the univariate strategy above to each component sample of the learning sample , yielding sets of size for all . For each dimension , each selected coordinate , , typically corresponds to a unique -dimensional vector of the learning sample. One could then define to be the union of the corresponding sets of -dimensional points, which implies that . A preliminary implementation of this strategy showed however that (among other things) this approach can sometimes lead to the selection of points in the learning sample that are too close to the “border” of the point cloud , resulting in numerical difficulties when computing the inverse or the square root of (see also Remark 2.4).

Another natural adaption of the strategy considered in the univariate case would be to choose an integer , consider the uniformly-spaced grid (containing points)

| (3.1) |

and define as consisting of the points

| (3.2) |

This strategy needs however to be refined because some of the above points might not belong to the support of which, as hinted at in Remark 2.4, is a necessary condition for Condition 2.3 to hold. Let be the unobservable sample obtained from the learning sample by probability integral transformations, that is, let

| (3.3) |

where are the unknown univariate margins of . Note in passing that can be regarded as a stretch from a -dimensional time series of continuous random vectors with contemporary d.f. , where is the (unique) copula of (see, e.g., Sklar, 1959) satisfying

and

Adapting the approach briefly described in Section 4.2 of Li and Genton (2013), we propose to keep in only those points in (3.2) constructed from grid points in (3.1) whose “neighborhood” contains a sufficiently large proportion of the ’s. As are unknown, we follow one of the classical approaches used in the copula literature (see, e.g., Hofert et al., 2018, and the references therein) and use as a proxy for , where

| (3.4) |

For any such that , let . Furthermore, let be the empirical measure of and let . Given and if the components of are independent, it is expected that the proportion of ’s in be approximately equal to . This motivates the following strategy: we choose to retain in only the points in (3.2) constructed from grid points , where

| (3.5) |

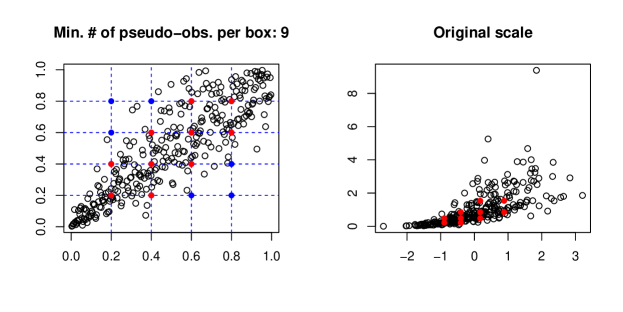

is defined in (3.1) and is a user-chosen parameter. The number of automatically chosen points depends on . Figure 1 illustrates the automatic choice of in the bivariate case for and . Values for and appearing to lead to powerful multi-purpose open-end monitoring procedures will be recommended in the case in Section 5.

We end this section by stating an asymptotic property of the proposed selection procedure. Let be the measure on associated with the copula of and let

| (3.6) |

Also, recall the definition of in (3.5) and, as classically done in the literature (see, e.g., Hofert et al., 2018, Chapter 4 and the references therein), let the empirical copula of be defined as the empirical d.f. of the “pseudo-observations” defined in (3.4). Of course, one hopes that is close to the deterministic (but unknown) set when is large. Proposition 3.2 below (proven in Appendix D) makes this statement rigorous under the following mild condition.

Condition 3.1.

-

(i)

For each , , and

-

(ii)

.

Proposition 3.2.

Assume that Condition 3.1 holds. Then, almost surely, for all sufficiently large, .

3.3 Additional asymptotic results under the null

The asymptotic results stated in Sections 2.2 and 2.3 concern the monitoring procedure based on the detector in (2.4) where the chosen evaluation points are fixed (they are not allowed to change in the asymptotics with ). To fully asymptotically justify the use of the detector resulting from the automatic choices of points considered in Sections 3.1 or 3.2, one needs an analogue of Theorem 2.6 in which the points at which the empirical d.f.s are evaluated are allowed to change with .

In the rest of this section, we assume that the automatically chosen points in are of the form

| (3.7) |

for some vectors of probabilities not depending on . This is clearly the case for the univariate selection strategy proposed in Section 3.1. From Proposition 3.2, it is also the case for the multivariate strategy proposed in Section 3.2 upon additionally assuming that Condition 3.1 holds and that is sufficiently large.

Next, set , write and notice that the points in are unobservable since are unknown. The -dimensional random vectors are also unobservable. Since with given by (3.7) is an estimator of , the long-run covariance matrix in (2.5) of the unobservable -dimensional time series may still be estimated from the sample which is a proxy for the sample .

We first state a condition under which the monitoring procedure based on and the unobservable monitoring procedure based on in (2.4) are asymptotically equivalent.

Condition 3.3 (For the asymptotic equivalence of and ).

For any ,

| (3.8) |

The following result, proven in Appendix D, shows that the previous condition can be satisfied under the null and absolute regularity. Given a time series , recall that, for , denotes the -field generated by , that the absolute regularity coefficients corresponding to are defined by

| (3.9) |

and that the sequence is said to be absolutely regular if as . Also, note that absolute regularity is known to imply strong mixing (see, e.g., Dehling and Philipp, 2002) and that an independent sequence is clearly absolutely regular since in this case for every and as in (3.9), almost surely.

Proposition 3.4 (Condition 3.3 can hold under the null).

Assume that the underlying time series is stationary and absolutely regular, and that its absolute regularity coefficients satisfy as with . Then, if the univariate margins of are continuous and if, for each , , Condition 3.3 holds.

Remark 3.5.

Assumptions related to Condition 3.3 appear in Dette and Gösmann (2020) in the context of the study of the asymptotics of closed-end sequential tests designed to be sensitive to changes in the mean, the variance or certain quantiles. In an open-end setting, related conditions are stated in Assumption 2.5 of Gösmann, Kley and Dette (2021) and in Condition 6.1 of Holmes and Kojadinovic (2021) under an “almost sure” form. As an inspection of the proof of Proposition 3.4 reveals, Condition 3.3 is essentially a consequence of the continuity of the margins of and Theorem 3.1 of Dedecker, Merlevède and Rio (2014) which provides an adequate strong approximation result for the empirical process under absolute regularity (but not under strong mixing).

Remark 3.6.

In the statement of Proposition 3.4, it is assumed that, for each , . This condition can actually be dispensed with provided additional conditions of the true unobservable quantile functions are assumed instead. Indeed, from Rio (1998), we know that the condition on the absolute regularity coefficients in Proposition 3.4 implies that, for any , in , where denotes the space of bounded functions on equipped with the uniform metric. From Lemma 21.2 in van der Vaart (1998), this is then equivalent to the fact that at every at which is continuous. Consequently, the condition that, for any , could be replaced by the condition that, for any , is continuous at , for all .

The next proposition, also proven in Appendix D, states that, under Conditions 2.5 and 3.3, the monitoring procedures based on and are asymptotically equivalent.

The last claim of the previous proposition suggests to carry out the monitoring procedure based on the detector exactly as the procedure based on the detector when the points are hand-picked by the user (see the last paragraph of Section 2.2).

3.4 The monitoring procedure based on is margin-free under the null

We end this section by verifying that, under the considered assumption that the true unknown marginal d.f.s are continuous, the procedure based on the detector is margin-free under in (1.1), that is, it does not depend on under the null. To see this, let be the unobservable sample obtained from the available observations using (3.3) and let be the empirical d.f. of . Notice that we can recover the from the by marginal quantile transformations, that is, . Furthermore, for any , by (right) continuity of , we have that for all and ; see, e.g., Proposition 1 (5) in Embrechts and Hofert (2013). Then, it can be verified that, for every , and ,

which implies that, under the null and the current setting, the detector at can be rewritten to depend only on .

4 Estimation of high quantiles of the limiting distribution

From the two previous sections, we know that, to carry out the studied monitoring procedures, it is necessary to be able to accurately estimate high quantiles of the random variable , , , appearing first in the statement of Theorem 2.6. The underlying estimation problem was empirically solved in Holmes and Kojadinovic (2021) for using asymptotic regression modeling. We choose to use the same approach when and refer the reader to Section 4 of the aforementioned reference where the motivation for this way of proceeding is explained in detail.

Fix , , and let be the -quantile of . Furthermore, let , let be an infinite sequence of independent standard normals and let where , and is the d.f. of the standard normal. According to Theorem 2.6, for large the distribution of should be close to that of . If for a given realization of we could compute the corresponding realization of , then could be estimated by , the -empirical quantile of a large sample of realizations of . As this is not possible because of the supremum over , the idea taken from Holmes and Kojadinovic (2021) is to model the relationship between and , the -empirical quantile of , using an asymptotic regression model.

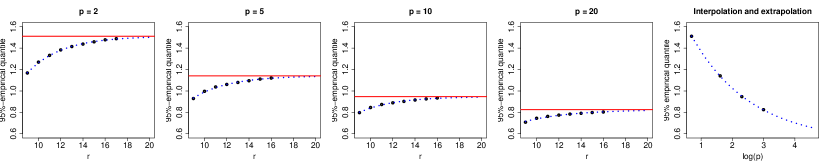

To begin with, using a computer grid, we computed the empirical quantiles , , from 10,000 simulated trajectories of the scaled detector for and . In a next step, an asymptotic regression model was fitted to the points , . The considered model is a three-parameter model with mean function

where is the equation of the upper horizontal asymptote of . Its fitting was carried out using the R package drc (Ritz et al., 2015). A candidate estimate of , the -quantile of , is then the resulting estimate of the parameter . The previous steps were carried out for , and (following the practical recommendation made in Holmes and Kojadinovic (2021)), and can be visualized in the first four panels of Figure 2 for . The corresponding estimates of the quantiles are given in columns two to five of Table 1.

| 2 | 5 | 10 | 20 | ||||

|---|---|---|---|---|---|---|---|

| 0.99 | 1.654 | 1.234 | 1.010 | 0.860 | -0.126 | 1.535 | 2.080 |

| 0.95 | 1.511 | 1.141 | 0.946 | 0.825 | 0.060 | 1.475 | 1.921 |

| 0.90 | 1.450 | 1.099 | 0.921 | 0.806 | 0.140 | 1.462 | 1.870 |

In a last step, to be able to carry out the monitoring procedures for some values of different than those in , we fitted asymptotic regression models to the points , , for and . The estimates of the parameters , and are reported in the last three columns of Table 1. We make no claim regarding the theoretical adequacy of this type of model. The aim is only to be able to interpolate (resp. extrapolate) the value of for (resp. for slightly larger than 20). Note that, since as (as a consequence of the definition of the norm ), a fitted two-parameter submodel with fixed to 2 is expected to behave better for large . We have nonetheless decided to keep the fitted three parameter model because its accuracy for values of slightly larger than 20 was found to be better in our Monte Carlo experiments summarized in the forthcoming section.

5 Monte Carlo experiments

We carried out rather extensive numerical experiments in the case of low-dimensional () continuous observations to investigate the finite-sample behavior of the monitoring procedure based on the detector introduced in Section 3. Specifically, for , recall from Section 3.1 that the real points at which the (univariate) empirical d.f.s are evaluated are chosen as empirical quantiles of order , , computed from the learning sample . For , the approach is slightly more involved: as explained in Section 3.2, the evaluation points are chosen using a point selection procedure which relies on two parameters: an integer specifying the maximal value of and the constant controlling how many of the initial grid points will actually be retained.

From the definition of the detector , we see that an underlying unknown long-run covariance matrix needs to be estimated from the sample . In practice, for , we used the estimator of Andrews (1991) based on the quadratic spectral kernel with automatic bandwidth selection as implemented in the function lrvar() of the R package sandwich (Zeileis, 2004; Zeileis, Köll and Graham, 2020). Note that we did not however use prewhitening as suggested in Andrews and Monahan (1992). The fact that the monitoring procedure studied in this work is available in the R package npcp (Kojadinovic and Verhoijsen, 2022) not only makes all our experiments fully reproducible but also allows a user to change the long run covariance estimator (for instance to that of Newey and West, 1987) by passing parameters to the main function which will be passed to the function lrvar().

Before we present our empirical findings, it is important to keep in mind that, in the case of open-end approaches, numerical experiments only provide a biased view of their behavior as finite computing resources impose that monitoring has to be stopped eventually. From the point of view of statistical testing, the main consequence of this is that all rejection percentages are underestimated.

The full details of our simulations are available in Appendix E. We provide hereafter a summary of our findings:

-

•

For monitoring univariate data, taking evaluation points and choosing them as suggested in Section 3.1 seems a good choice in general. Unless serial dependence is very strong, a learning sample of size seems to lead to a procedure that holds its level well and displays good power against several alternatives involving a change in the mean or the variance, or such that the d.f. changes with the mean and variance remaining constant. In the case of very strong serial dependence (such as for an AR(1) model with autoregressive parameter 0.7), a larger learning sample (for instance ) seems necessary for the monitoring procedure to hold its level reasonably well.

-

•

For monitoring low-dimensional data (), using if , if and in the point selection procedure of Section 3.2 seems to be a reasonable choice in general. As for , in the case of mild serial dependence, taking seems sufficient to obtain a sequential test that holds its level reasonably well. With such settings, the procedure seems powerful against various alternatives involving changes in one margin or in the copula of the contemporary d.f.

6 Data example and concluding remarks

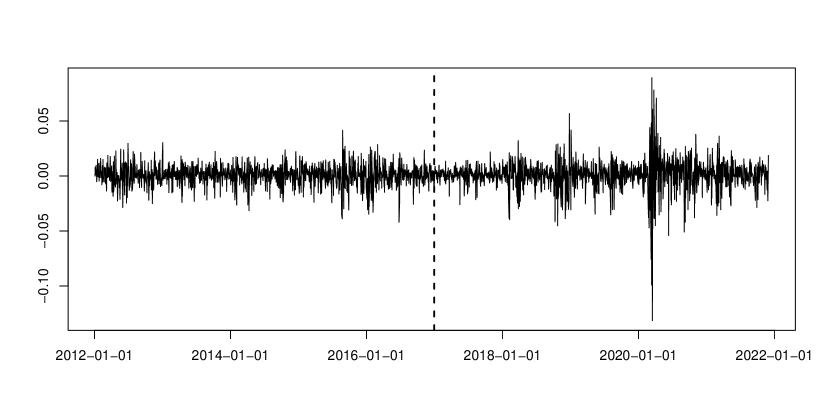

Let us briefly illustrate how the procedure based on the detector considered in Section 3 could be used for monitoring changes in the contemporary distribution of daily log-returns of a financial index. In our fictitious example, the learning sample (whose stationarity would need to be tested) corresponds to 1257 trading days of the NASDAQ for the period January 3rd 2012 – December 30th 2016. Monitoring starts on the first trading day of 2017. The corresponding daily log-returns are represented in Figure 3, where the dashed vertical line represents the start of the monitoring.

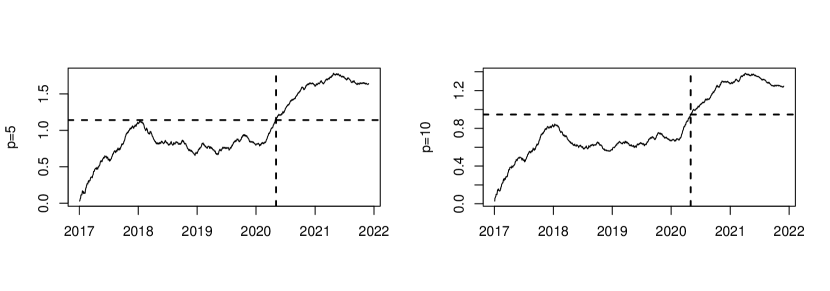

The sample paths of are represented in Figure 4 for . The horizontal dashed line in each panel represent one of the 95%-quantiles given in the second row of Table 1. The dashed vertical lines mark the first time that the threshold is exceeded (corresponding to May 2020). A change in the data generating process slightly prior to this date seems likely as an inspection of Figure 3 reveals: the first months of 2020 are indeed characterized by a period of very high volatility.

We end this section by stating a few remarks:

-

•

One important practical advantage of the monitoring procedure proposed in this work comes from its open-end nature and is that the monitoring horizon does not need to be specified. As a consequence, monitoring could theoretically run forever. This is however not possible from a practical perspective because of the form of the detector in (2.4): it is indeed clear that the cost of computing the detector at time increases with . The latter implies that its computation will become impossible for large enough. Some other detectors, such as the ordinary CUSUM, will not be affected by such a practical issue. Yet, as empirically observed in Gösmann, Kley and Dette (2021) and in Holmes and Kojadinovic (2021), the ordinary CUSUM is substantially less powerful than more computationally costly detectors similar to the ones considered in this work. In a related way, let us mention that the implementation of the studied monitoring procedure available in the R package npcp is merely a proof of concept and is not optimized for very long-term monitoring.

-

•

The price to pay for open-end monitoring is that the detection power decreases as time elapses. For the studied class of procedures, this is due to the parameter as discussed in Section 4 of Holmes and Kojadinovic (2021). On one hand, the smaller the value of , the weaker the power decrease. On the other hand, the smaller , the more conceptually difficult and computationally costly it is to estimate high quantiles of the distribution appearing in Theorem 2.6. The latter suggests to devote more research to the estimation of high quantiles of .

-

•

The type of monitoring procedure used in this work could also be used to detect changes in the serial dependence. For instance, to detect such changes “at lag 1” from an initial sequence of univariate observations , the could be formed as .

Acknowledgments

The authors would like to thank a co-editor and two anonymous referees for their very constructive comments on an earlier version of this manuscript. MH was supported in part by Future Fellowship FT160100166 from the Australian Research Council. AV is supported by a University of Melbourne Research Scholarship.

Appendix A Proof of Theorem 2.6

The proof of Theorem 2.6 is based on four lemmas which we prove first. Throughout the remainder of the proof, we let

| (A.1) |

which is the version of the detector in (2.6), in which the estimated long-run variance is replaced by the true long-run variance .

On the probability space of Condition 2.5 (assuming that this condition holds), we may define

| (A.2) |

where we recall that for each , and are independent -dimensional standard Brownian motions.

Lemma A.1.

Assume that Condition 2.5 holds. Then, for any ,

Proof.

Fix . Applying the reverse triangle inequality for suprema

| (A.3) |

to the maximum over below gives

Next, we rewrite as

Hence, using the triangle inequality, we have that

where (using the convention that empty sums are equal to 0)

It suffices to show that , , , and are . Since when , we have that and . So it suffices to consider and . Let be as in Condition 2.5. Then,

Hence, by equivalence of norms on , (2.12) and the fact that , converges in probability to zero as . Next, since the norm in is zero when and using the fact that , we see that is equal to

The supremum over above is less than 1 since . The supremum over is bounded in probability by (2.11) and equivalence of norms. Since , this proves that converges to 0 in probability. ∎

Given -dimensional independent standard Brownian motions and and , define the random function by

| (A.4) |

Lemma A.2.

For any , the function is almost surely bounded and uniformly continuous.

Proof.

Fix . For and , define to be the -th coordinate of

and note that . From Lemma A.2 in Holmes and Kojadinovic (2021), we know that is almost surely bounded and uniformly continuous for each . It follows that each is also bounded and uniformly continuous, almost surely. Now note that

So is almost surely bounded and uniformly continuous since each is. ∎

Proof.

Fix . The random variable is equal in distribution to

where we note that the norm is equal to zero when , which has allowed us to include the cases and in the maximum and supremum, respectively. Using Brownian scaling, this is equal in distribution to

In the above, and are integers. Letting and (where and ), the above display becomes

Using (A.3) with the supremum over , we have

which converges to zero almost surely as since is almost surely uniformly continuous and . ∎

For a matrix , denote the operator norm of by

| (A.5) |

Lemma A.4.

Proof.

Fix . Applying (A.3) to the maximum over and using the inequality for , we obtain that

| (A.6) |

For and , we have that by the Cauchy-Schwarz inequality. By (A.5), , so that . From (A.6), we therefore obtain

It is well-known that the mapping that maps an invertible square matrix to its inverse is continuous. Since and Condition 2.3 holds, the continuous mapping theorem immediately implies that , which in turn implies that by equivalence of norms. Furthermore, from Lemmas A.1 and A.3, we have that converges weakly, which implies that it is bounded in probability. By equivalence of norms on , we immediately obtain that

and therefore the desired result. ∎

Proof of Theorem 2.6.

From Lemmas A.1–A.4, we have that

where is defined in (A.4). It remains to be shown that

| (A.7) |

Let and be two -dimensional Gaussian processes defined, for any , by

Since , , and are -dimensional standard Brownian motions, it follows that the coordinates of the Gaussian processes and are centered. Thus, to show that the random functions and are equal in distribution (which will immediately imply (A.7)), it suffices to establish equality of their covariance functions at any with and . On one hand, the covariance function of the Gaussian process at is

while, on the other hand, the covariance function of the Gaussian process at is

which concludes the proof. ∎

Appendix B Proofs of Propositions 2.8, 2.10 and 2.12

Proof of Proposition 2.8.

Let be such that Condition 2.3 holds. Since , it is immediate that as . Furthermore, as all the components of the are bounded in absolute value by 1, from Theorem 4 of Kuelbs and Philipp (1980), we can redefine the sequence on a new probability space together with a -dimensional standard Brownian motion such that, almost surely,

for some that depends on , and . Let . Then, almost surely,

| (B.1) |

Let be another -dimensional standard Brownian motion independent of and define as

and as , . Then, for each , and are independent -dimensional standard Brownian motions.

For each , let

and note that the sequence consists of identically distributed random variables. Therefore, to show that (2.11) holds, it is sufficient to show that . From the previous definition, can be rewritten as

and, from (B.1), it is the supremum of an almost surely convergent sequence. It follows that is an almost surely finite random variable, so and therefore (2.11) holds. Finally, (B.1) and the definition of immediately imply (2.12). ∎

Proof of Proposition 2.10.

It is immediate that

where is the first component of the -dimensional Brownian motion . Hence, for any fixed ,

where the last equality is a consequence of Proposition 3.4 of Holmes and Kojadinovic (2021). ∎

Proof of Proposition 2.12.

Fix and . Note first that is a -variate continuous Gaussian process, which implies that almost surely. For , let be defined by

and, similarly, let be defined by

Notice that and that for every .

Next, for any , we equip with the uniform distance, which is then a separable (and locally convex) metric space. Furthermore, as we shall verify below, is continuous and convex for any . We can then apply Theorem 7.1 of Davydov and Lifshits (1984) to obtain that, for any , the distribution of is concentrated on and absolutely continuous on . In addition, some thought reveals that, for any ,

since is a centered multivariate normal random vector with covariance matrix . Hence, for any , the distribution of has no atom at 0 and is therefore absolutely continuous.

Proof of the continuity of : To show (uniform) continuity on (equipped with the uniform distance), let be given and let . Let be such that . Then,

This shows that . Similarly (or just by symmetry of the above argument), . Thus, as required.

Proof of the convexity of : To show convexity, let and . Then and

as required.

To complete the proof of the proposition, it suffices to fix and show that . Notice first that, for any , almost surely,

Since according to Theorem 2.6, is almost surely finite, we see that

Hence, there exists (depending on ) such that

| (B.2) |

Now, if , then either or the supremum () in the definition of is attained for some with . Absolute continuity of shows that the former has probability 0, while (B.2) shows that the latter has probability at most . ∎

Appendix C Proof of Proposition 2.14

Proof of Proposition 2.14.

Let be a symmetric positive-definite matrix. Then, there exits a diagonal matrix with ,…, on its diagonal and a orthogonal matrix such that the columns of are the eigenvectors of with corresponding eigenvalues and . Starting from the definition of given below (2.5), for any ,

where we have used the fact that orthogonal matrices preserve the dot product.

Let be the map from the set of symmetric positive-definite matrices to such that, for any , . Since eigenvalue decomposition is a continuous operation and since the minimum is a continuous function, the map is continuous. Hence, and the continuous mapping theorem imply that .

From the previous derivations and the assumptions of the proposition, we thus have that, for all , almost surely. Therefore, for any and , almost surely,

which immediately implies that since and . ∎

Appendix D Proofs of Propositions 3.2, 3.4, and 3.7

Proof of Proposition 3.2.

Proof of Proposition 3.4.

Let

From Theorem 3.1 part 2(b) in Dedecker, Merlevède and Rio (2014), without changing its distribution, the empirical process can be redefined on a richer probability space on which there exists a Kiefer process, that is, a two-parameter centered continuous Gaussian process with covariance function given by (2.14), and a random variable such that, almost surely (a.s.),

| (D.1) |

for some only depending on and . Let . Then,

From (D.1), with probability one, the first two terms on the right-hand side of the last display are smaller than

The third term is smaller than

| (D.2) |

where . To complete the proof, it thus suffices to show that .

From Theorem 3.1 part 2(a) in Dedecker, Merlevède and Rio (2014), we know that the sample paths of the Gaussian process are almost surely uniformly continuous with respect to the pseudo-metric on defined by

We will use this fact to show that . To this end, define , where

Since implies that , we have that

where with

Let . By almost sure uniform continuity of the sample paths of the process , there exists such that, for all , almost surely. Since the univariate margins of are (uniformly) continuous, there exists such that, for all , . Therefore

Since by assumption, this shows that which completes the proof since . ∎

Proof of Proposition 3.7.

The second claim is immediate from the first claim and Theorem 2.6, so we need only prove the first claim.

First, we assert that, for any ,

| (D.3) |

Indeed, the left-hand side of (D.3) is equal to

so the assertion holds by (3.8). Using the fact that all norms on are equivalent, (D.3) implies that

| (D.4) |

where and (similarly for ).

Recall the definition of in (A.1) which can be rewritten as

and define the unobservable detector by changing the norm in the definition of as

Using the reverse triangle inequality for the maximum norm and the norm , we then obtain that, for any ,

Therefore,

We claim that both terms on the right hand side converge to 0 in probability. For example, since and , the second term is at most

which converges to 0 in probability by (D.4). The first term is similar. Hence,

| (D.5) |

From Lemma A.4, we have that . Therefore, it remains to prove that

Proceeding as in the proof of Lemma A.4, we have that

We claim that this converges to zero in probability (which completes the proof). By Condition 2.3 and the fact that , we have that . To prove this final claim, it therefore suffices to show that

Indeed, by equivalence of norms on , this follows from the fact that , itself a consequence of (D.5), Lemma A.4, and Theorem 2.6. ∎

Appendix E Details of Monte Carlo experiments

In this section, we provide the implementation details of the Monte Carlo experiments that we carried out in the case of low-dimensional () continuous observations and whose main findings are summarized in Section 5. In all experiments, the sequential tests were carried out at the nominal level.

E.1 Univariate experiments for the procedure based on under the null

To investigate the empirical levels of the sequential test based on when , we considered 9 data generating models, denoted M1, …, M9. Models M1, …, M6 are AR(1) models with independent standard normal innovations whose autoregressive parameter is equal to 0, 0.1, 0.3, 0.5, 0.7 and , respectively. Model M7 is a GARCH(1,1) model with independent standard normal innovations and parameters , and to mimic SP500 daily log-returns following Jondeau, Poon and Rockinger (2007). Models M8 and M9 are the nonlinear autoregressive model used in Paparoditis and Politis (2001, Section 3.3) and the exponential autoregressive model considered in Auestad and Tjøstheim (1990) and Paparoditis and Politis (2001, Section 3.3), respectively. The underlying generating equations are

and

respectively, where the are independent standard normal innovations. Note that, for all time series models, a burn-out sample of 100 observations was used.

| Model | |||||

|---|---|---|---|---|---|

| M1 | 200 | 3.4 | 3 | 3.3 | 5.4 |

| 400 | 1.9 | 2.1 | 3.2 | 2.8 | |

| 800 | 1.5 | 1.3 | 2 | 1.3 | |

| 1600 | 1 | 0.9 | 0.9 | 1 | |

| M2 | 200 | 4.4 | 4.3 | 8.1 | 13.8 |

| 400 | 3.2 | 2.7 | 3.6 | 5.6 | |

| 800 | 1.8 | 2.8 | 2.1 | 3.2 | |

| 1600 | 1.3 | 1 | 1.7 | 1 | |

| M3 | 200 | 6.9 | 10.6 | 21.5 | 53.9 |

| 400 | 3.4 | 4.1 | 7.2 | 16.7 | |

| 800 | 3 | 2.5 | 3 | 5.6 | |

| 1600 | 1.5 | 1.3 | 1.5 | 1.4 | |

| M4 | 200 | 9.5 | 18.1 | 44.6 | 93.2 |

| 400 | 5.3 | 7.1 | 16.5 | 42.9 | |

| 800 | 3 | 3.6 | 5.3 | 12.3 | |

| 1600 | 2.2 | 2.3 | 2.8 | 2.2 | |

| M5 | 200 | 18.9 | 39.4 | 82.1 | 100 |

| 400 | 9.6 | 17.5 | 40.3 | 87 | |

| 800 | 5.7 | 6.7 | 14.4 | 34.5 | |

| 1600 | 2.4 | 2.7 | 4.4 | 7.5 | |

| M6 | 200 | 7.3 | 8.6 | 14.1 | 26.7 |

| 400 | 3.7 | 4.6 | 6.4 | 11 | |

| 800 | 2.6 | 2.8 | 3 | 3.6 | |

| 1600 | 1.2 | 1.5 | 1.3 | 1.2 | |

| M7 | 200 | 9.1 | 14.8 | 17.2 | 16.8 |

| 400 | 8 | 12 | 12.6 | 9.9 | |

| 800 | 7.5 | 9.8 | 9.2 | 5.2 | |

| 1600 | 4.6 | 6.1 | 4.8 | 2.9 | |

| M8 | 200 | 7.8 | 13 | 30.6 | 74.3 |

| 400 | 4.7 | 5.5 | 10.8 | 30.8 | |

| 800 | 2.8 | 3.4 | 4.7 | 7.9 | |

| 1600 | 1.8 | 1.8 | 1.9 | 2.1 | |

| M9 | 200 | 15 | 29 | 61.1 | 95.6 |

| 400 | 8.6 | 12.9 | 25.5 | 57.9 | |

| 800 | 5.5 | 6.7 | 10.1 | 17.3 | |

| 1600 | 2.1 | 2.4 | 3.4 | 5.3 |

For each of the nine models, the probability of rejection of in (1.1) was estimated from 1000 samples of size with and for . The empirical levels are reported in Table 2. As one can see, for any fixed , reassuringly, they decrease as increases. For , it is mostly for the models with strong serial dependence such as M5, M8 and M9 that the empirical levels are not below the 5% nominal level. The latter is not so surprising and highlights the difficulty of the estimation of the long-run covariance matrix using the estimator in the case of strong serial dependence. It may be slightly more surprising for the GARCH(1,1) model M7 for which seems necessary to obtain a reasonably good estimate of . The fact that for most other models, the empirical levels are all below the 5% nominal level when is a consequence of the fact that they are underestimated in all settings. Indeed, the monitoring was stopped after 5000 steps whereas it would theoretically be necessary to monitor “indefinitely” to compute empirical levels accurately. For any fixed , we see that increasing tends in general to increase the empirical level. This is again a consequence of the difficulty of the estimation of the long-run covariance matrix which is a matrix. Note that, since the monitoring procedure based on is margin-free (as verified in Section 3.4), it is not necessary to empirically study the influence of the contemporary distribution on the empirical levels.

| 200 | 2.4 | 2.4 | 2.3 | 3.1 |

|---|---|---|---|---|

| 400 | 1.7 | 1.9 | 3.1 | 2.3 |

| 800 | 1.3 | 1.3 | 1.6 | 0.7 |

| 1600 | 0.8 | 0.9 | 0.9 | 0.6 |

In a second experiment, we briefly investigated the effect of the estimation of on the empirical levels in the case of independent observations. Instead of estimating from the learning sample, we used its true value whose elements, in the considered setting (see Remark 2.4), are given by

for . The empirical levels were then estimated from 1000 random samples of size from the standard normal distribution. The results are reported in Table 3. By comparing the results with the first horizontal block of Table 2, we see, as could have been expected, that for the same value of , the use of the true long-run covariance matrix leads to lower empirical levels than when it is estimated.

| 1.0 | 0.9 | 0.9 | 1.0 | 0.4 | 0.3 | 0.5 |

As a last experiment under the null, we investigated the quality of the model fitted at the end of Section 4 to extrapolate the values of the quantiles of the distribution of for and . Using and 1000 random samples of size from the standard normal distribution, we estimated rejection percentages for . These are given in Table 4 and suggest that the quality of the model for extrapolating the values of the quantiles may be acceptable when (although it may lead to some slightly more conservative tests).

E.2 Univariate experiments for the procedure based on under alternatives

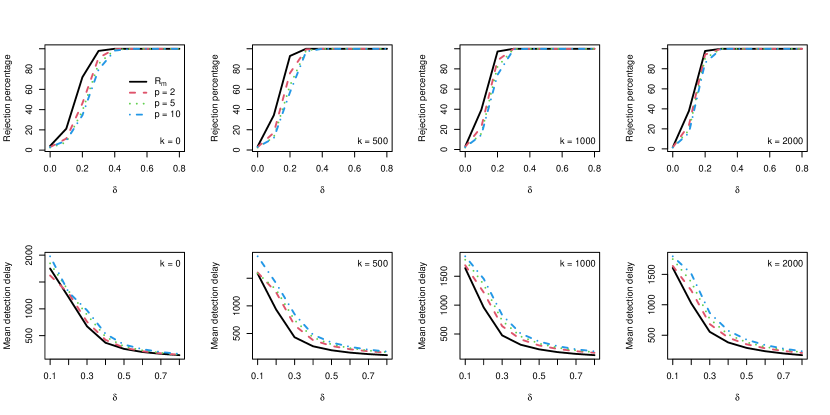

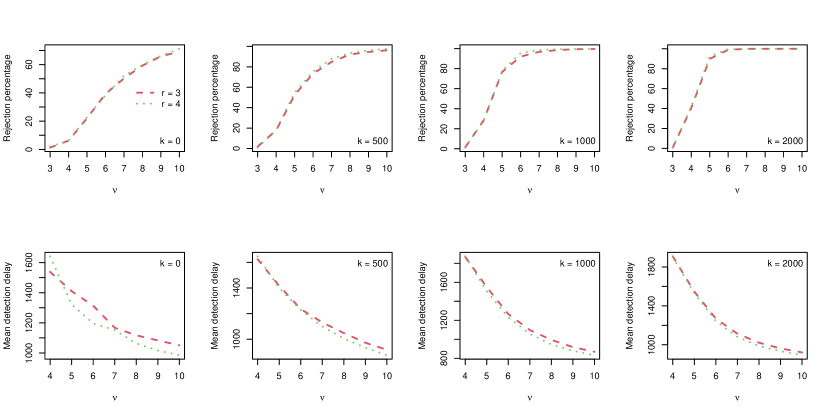

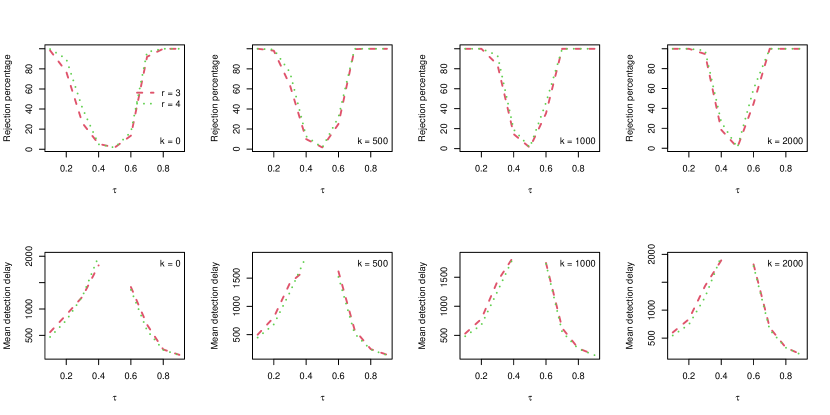

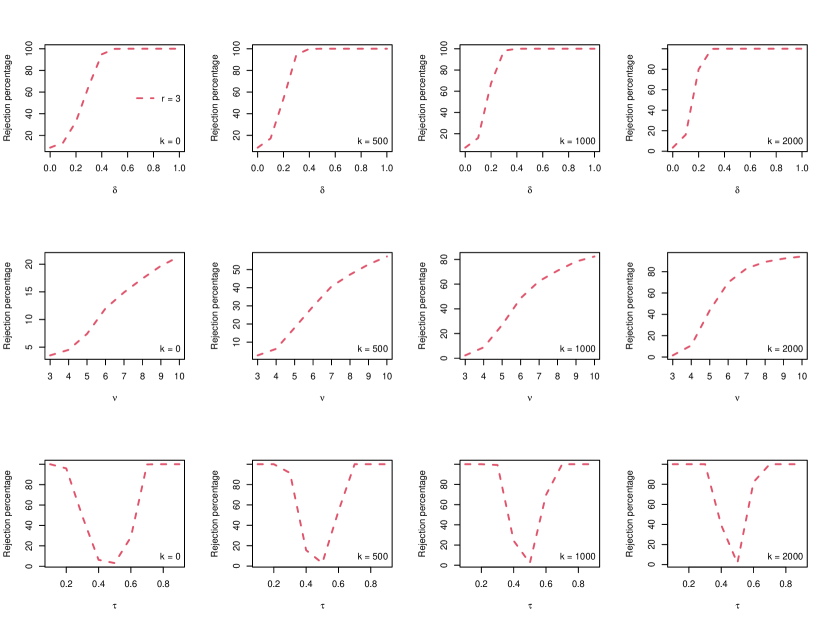

In order to understand the behavior of the monitoring procedure based on the detector considered in Section 3.1 under alternatives to in (1.1), we considered successively changes in the expectation of the ’s, in their variance and in their d.f. (while keeping their expectation and variance constant). As a first experiment, we studied the finite-sample behavior of the sequential test under a change in the expectation of an AR(1) model with autoregressive parameter equal to 0.3 (Model M3). Specifically, to estimate rejection percentages, we generated 1000 samples of size from Model M3 with and, for each sample, added a positive offset of to all observations after position with . The results are reported in Figure 5. Notice that only the exceedences (of the detectors with respect to their thresholds) after position are taken into account when calculating the rejection percentages.

As one can see from the top row of graphs in Figure 5, as expected, the power of all procedures increases as increases. Furthermore, for the procedure based on and a fixed value of the offset , increasing the number of evaluation points slightly lowers the power of the test. We also see that the procedure based on in (2.1) is always the most powerful. This was to be expected as the latter was specifically designed to be sensitive to changes in the mean. Similarly, from the second row of plots in Figure 5, we see that mean detection delays are smallest for the procedure based on and increase for the procedure based on as increases. Note finally that the power of every procedure becomes larger as the time at which the offset is added becomes closer to half of . This is a consequence of using of CUSUM statistics to define the detectors.

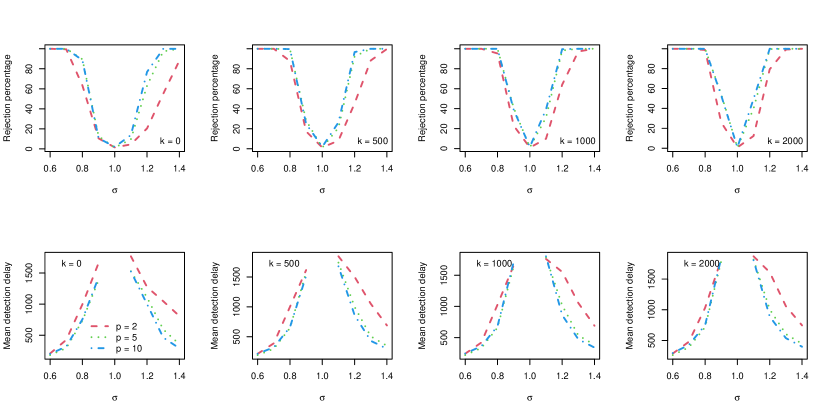

As a second experiment, we considered a change in the variance of independent centered observations. To estimate the power of the sequential test, we generated 1000 samples of size with such that, observations up to position with are from the standard normal distribution while observations after position are from the distribution. The results are reported in Figure 6. As expected, the power of the procedure based on increases as deviates further away from one. In contrast to the first experiment however, the rejection percentages (resp. mean detection delays) increase (resp. decrease) as the number of evaluation points increases. Notice that the improvement as increases from 5 to 10 appears to be rather small.

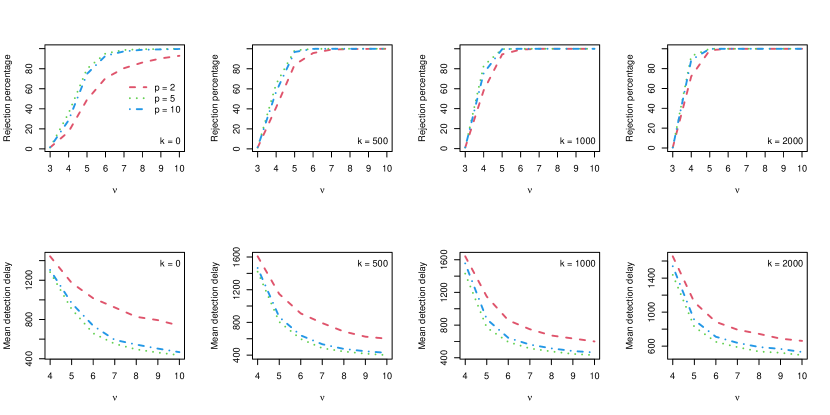

As a final experiment, we considered a change in the contemporary distribution of independent observations that keeps the expectation and the variance constant. To estimate the rejection percentages, we generated 1000 samples of size with such that observations up to position with are from the scaled Student distribution with 3 degrees of freedom (where the scaling is performed so that the variance is equal to one) while observations after position are from the scaled Student distribution with degrees of freedom. The results are reported in Figure 7. As expected, the power of the procedure based on increases as increases. Furthermore, as in the previous experiment, the rejection percentages (resp. mean detection delays) are larger (resp. smaller) when . Somehow surprisingly however, the results seem slightly better when .

E.3 Multivariate experiments for the procedure based on under the null

Given and a -dimensional copula , we used a multivariate AR(1) model to generate potentially serially dependent observations under in (1.1). Let , , be a -dimensional i.i.d. sample from a copula . Then, set , where is the d.f. of the standard normal distribution, and . Finally, for any and , compute recursively

| (E.1) |

| 400 | 0.00 | 8.9 | 9.1 | 15.4 | 14.8 | 9.0 | 10.4 | 15.9 | 18.4 | 9.0 | 10.4 | 16.0 | 21.6 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.30 | 8.6 | 7.4 | 14.3 | 13.2 | 8.9 | 8.4 | 15.3 | 16.6 | 9.0 | 9.4 | 15.9 | 20.5 | |

| 0.60 | 7.0 | 7.7 | 10.7 | 10.0 | 7.1 | 8.0 | 11.7 | 11.3 | 7.7 | 8.1 | 13.4 | 13.6 | |

| 0.90 | 3.0 | 4.0 | 5.8 | 3.7 | 3.4 | 3.6 | 7.8 | 4.6 | 5.9 | 4.5 | 9.8 | 12.9 | |

| 800 | 0.00 | 9.0 | 4.5 | 15.9 | 6.6 | 9.0 | 4.7 | 16.0 | 7.6 | 9.0 | 4.7 | 16.0 | 7.6 |

| 0.30 | 8.7 | 4.6 | 14.5 | 3.7 | 9.0 | 4.9 | 15.6 | 4.9 | 9.0 | 5.0 | 16.0 | 5.6 | |

| 0.60 | 7.0 | 3.6 | 10.3 | 4.4 | 7.0 | 3.7 | 11.9 | 3.5 | 7.8 | 3.5 | 13.8 | 5.9 | |

| 0.90 | 3.0 | 2.1 | 5.2 | 1.8 | 3.2 | 2.2 | 8.4 | 3.1 | 6.3 | 3.0 | 10.0 | 7.5 | |

| 1600 | 0.00 | 9.0 | 2.2 | 16.0 | 2.7 | 9.0 | 2.2 | 16.0 | 2.7 | 9.0 | 2.2 | 16.0 | 2.7 |

| 0.30 | 8.9 | 1.8 | 14.7 | 2.8 | 9.0 | 2.2 | 15.8 | 2.6 | 9.0 | 2.2 | 16.0 | 2.7 | |

| 0.60 | 7.0 | 1.2 | 10.1 | 1.1 | 7.0 | 1.2 | 12.0 | 1.1 | 7.6 | 1.3 | 14.0 | 1.8 | |

| 0.90 | 3.0 | 1.2 | 4.9 | 1.3 | 3.0 | 1.3 | 8.8 | 2.0 | 6.5 | 0.9 | 10.0 | 3.3 | |

Recall that, when , the evaluation points of the monitoring procedure based on are chosen from the learning sample using the point selection procedure described in Section 3.2. To evaluate the behavior of the procedure when with and under the null, in a first experiment, we computed its rejection percentages from 1000 bivariate samples of size generated from the time series model (E.1) with and the bivariate Gumbel–Hougaard copula with a Kendall’s tau of . The empirical levels are reported in the columns of Table 5. The columns report the average number of grid points retained by the point selection procedure of Section 3.2. As one can see, reassuringly, the empirical levels improve in all settings as increases. Unsurprisingly, they are higher for than for since a larger value of tends to result in a larger number of selected points and thus in a more difficult estimation of the underlying long run covariance matrix. Also unsurprisingly, the number of selected points tends to increase as increases and to decrease as increases, that is, as the cross-sectional dependence in the underlying time series changes from independence to stronger positive association.

| 400 | 0.00 | 7.6 | 12.5 | 20.8 | 32.0 | 7.9 | 14.6 | 24.1 | 43.6 | 8.0 | 16.0 | 26.0 | 55.6 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0.30 | 7.4 | 10.4 | 18.3 | 22.4 | 7.8 | 12.2 | 21.4 | 33.7 | 8.0 | 15.4 | 24.0 | 49.2 | |

| 0.60 | 6.5 | 6.5 | 14.6 | 18.4 | 7.5 | 10.9 | 15.4 | 22.3 | 8.0 | 16.5 | 16.5 | 25.4 | |

| 0.90 | 2.0 | 3.9 | 6.4 | 4.4 | 2.0 | 3.8 | 8.5 | 6.7 | 3.2 | 3.4 | 11.2 | 14.9 | |

| 800 | 0.00 | 7.9 | 5.6 | 24.1 | 11.7 | 8.0 | 6.6 | 26.3 | 18.1 | 8.0 | 6.8 | 26.9 | 22.6 |

| 0.30 | 7.6 | 4.1 | 19.9 | 9.8 | 8.0 | 5.7 | 23.1 | 14.3 | 8.0 | 6.1 | 25.6 | 19.8 | |

| 0.60 | 6.7 | 2.8 | 15.0 | 7.8 | 7.9 | 5.2 | 15.3 | 9.1 | 8.0 | 6.7 | 16.5 | 8.8 | |

| 0.90 | 2.0 | 2.7 | 6.6 | 3.0 | 2.0 | 2.7 | 9.2 | 4.7 | 2.5 | 1.9 | 12.2 | 6.7 | |

| 1600 | 0.00 | 8.0 | 2.4 | 26.2 | 3.8 | 8.0 | 2.4 | 27.0 | 5.7 | 8.0 | 2.4 | 27.0 | 6.0 |

| 0.30 | 7.8 | 1.9 | 20.7 | 2.5 | 8.0 | 2.6 | 24.3 | 4.2 | 8.0 | 2.6 | 26.4 | 6.3 | |

| 0.60 | 6.9 | 1.0 | 15.0 | 2.2 | 8.0 | 1.8 | 15.1 | 2.3 | 8.0 | 2.2 | 16.2 | 2.4 | |

| 0.90 | 2.0 | 1.6 | 6.8 | 1.4 | 2.0 | 1.6 | 9.5 | 2.3 | 2.1 | 1.4 | 13.0 | 4.3 | |

We additionally considered a trivariate version of the previous experiment under the null based on the Clayton copula. The results, reported in Table 6, are qualitatively the same.

E.4 Multivariate experiments for the procedure based on under alternatives

In a last series of bivariate and trivariate experiments, we investigated the power of the procedure based on .

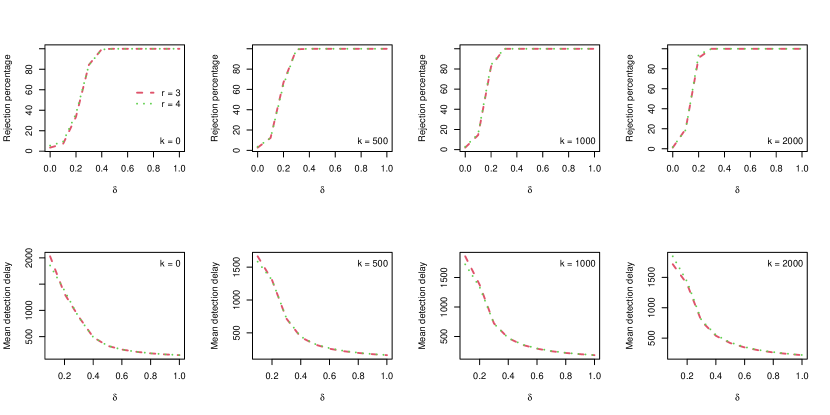

We first estimated its rejection percentages and corresponding mean detection delays for and from 1000 samples of size with generated from the time series model (E.1) with and the bivariate Frank copula with a Kendall’s tau of such that, for each sample, a positive offset of was added to the first component of all bivariate observations after position . The results are represented in Figure 8. As one can see, the value of has hardly any influence on the power or on the mean detection delay.

We next considered a similar experiment where the change affects only the first margin which changes from the scaled Student with 3 degrees of freedom to the scaled Student distribution with degrees of freedom. The copula (the bivariate Frank with a Kendall’s tau of ) and the second margin (the Student with degrees of freedom) remain constant. The results are displayed in Figure 9. As one can see, using rather than leads to a slightly more powerful procedure which detects the change faster on average.

In a third experiment, we focused on the effect of a change of the dependence parameter of the copula in the case of serially independent data. Before the change, observations are generated from the bivariate Normal copula with a Kendall’s tau of , while after the change they come from the bivariate Normal copula with a Kendall’s tau of . The rejection percentages and corresponding mean detection delays are represented in Figure 10. As in the previous experiment, the results for are slightly better than for .

In a fourth bivariate experiment, we considered the situation where the copula changes while the strength of association measured in terms of Kendall’s tau remains constant. Specifically, before the change, observations are generated from the bivariate Clayton copula with a Kendall’s tau of (which is lower tail dependent), while after the change they arise from the bivariate Gumbel–Hougaard copula with a Kendall’s tau of (which is upper tail dependent). The results are reported Table 7. The procedure with is again slightly more powerful and detects the change faster than the procedure with .

| m.d.d. | m.d.d. | |||||

|---|---|---|---|---|---|---|

| 0 | 6.8 | 72.3 | 1063.9 | 10.7 | 74.4 | 1007.7 |

| 500 | 6.8 | 92.9 | 967.9 | 10.8 | 94.8 | 936.4 |

| 1000 | 6.8 | 99.0 | 990.1 | 10.7 | 98.9 | 905.6 |

| 2000 | 6.9 | 99.8 | 1002.3 | 10.7 | 99.8 | 965.1 |

We concluded our multivariate simulations under alternatives by considering trivariate versions of the previous bivariate experiments. We used and . The results are reported in Figure 11 and Table 8 and are qualitatively the same as in the bivariate case. Notice however the rather low estimated rejection percentages for the trivariate version of the second bivariate experiment reported in the second row of graphs of Figure 11.

| 0 | 15.3 | 95.2 |

|---|---|---|

| 500 | 15.2 | 99.8 |

| 1000 | 15.2 | 100.0 |

| 2000 | 15.2 | 100.0 |

References

- Andrews (1991) {barticle}[author] \bauthor\bsnmAndrews, \bfnmD. W. K.\binitsD. W. K. (\byear1991). \btitleHeteroskedasticity and autocorrelation consistent covariance matrix estimation. \bjournalEconometrica \bvolume59 \bpages817–858. \endbibitem

- Andrews and Monahan (1992) {barticle}[author] \bauthor\bsnmAndrews, \bfnmD. W. K.\binitsD. W. K. and \bauthor\bsnmMonahan, \bfnmJ. C.\binitsJ. C. (\byear1992). \btitleAn Improved Heteroskedasticity and Autocorrelation Consistent Covariance Matrix Estimator. \bjournalEconometrica \bvolume60 \bpages953–966. \endbibitem

- Aue and Horváth (2013) {barticle}[author] \bauthor\bsnmAue, \bfnmAlexander\binitsA. and \bauthor\bsnmHorváth, \bfnmLajos\binitsL. (\byear2013). \btitleStructural breaks in time series. \bjournalJ. Time Series Anal. \bvolume34 \bpages1–16. \bdoi10.1111/j.1467-9892.2012.00819.x \bmrnumber3008012 \endbibitem

- Aue and Horváth (2004) {barticle}[author] \bauthor\bsnmAue, \bfnmA.\binitsA. and \bauthor\bsnmHorváth, \bfnmL.\binitsL. (\byear2004). \btitleDelay time in sequential detection of change. \bjournalStatistics and Probability Letters \bvolume67 \bpages221 – 231. \bdoi10.1016/j.spl.2004.01.002 \endbibitem

- Aue et al. (2006) {barticle}[author] \bauthor\bsnmAue, \bfnmA.\binitsA., \bauthor\bsnmHorváth, \bfnmL.\binitsL., \bauthor\bsnmHušková, \bfnmM.\binitsM. and \bauthor\bsnmKokoszka, \bfnmP.\binitsP. (\byear2006). \btitleChange-point monitoring in linear models. \bjournalThe Econometrics Journal \bvolume9 \bpages373-403. \bdoi10.1111/j.1368-423X.2006.00190.x \endbibitem

- Auestad and Tjøstheim (1990) {barticle}[author] \bauthor\bsnmAuestad, \bfnmB.\binitsB. and \bauthor\bsnmTjøstheim, \bfnmD.\binitsD. (\byear1990). \btitleIdentification of nonlinear time series: First order characterization and order determination. \bjournalBiometrika \bvolume77 \bpages669–687. \endbibitem

- Chu, Stinchcombe and White (1996) {barticle}[author] \bauthor\bsnmChu, \bfnmC-S. J.\binitsC.-S. J., \bauthor\bsnmStinchcombe, \bfnmM.\binitsM. and \bauthor\bsnmWhite, \bfnmH.\binitsH. (\byear1996). \btitleMonitoring Structural Change. \bjournalEconometrica \bvolume64 \bpages1045–1065. \endbibitem

- Csörgő and Horváth (1997) {bbook}[author] \bauthor\bsnmCsörgő, \bfnmM.\binitsM. and \bauthor\bsnmHorváth, \bfnmL.\binitsL. (\byear1997). \btitleLimit theorems in change-point analysis. \bseriesWiley Series in Probability and Statistics. \bpublisherJohn Wiley and Sons, \baddressChichester, UK. \endbibitem

- Davydov and Lifshits (1984) {bincollection}[author] \bauthor\bsnmDavydov, \bfnmYu. A.\binitsY. A. and \bauthor\bsnmLifshits, \bfnmM. A.\binitsM. A. (\byear1984). \btitleThe fibering method in some probability problems. In \bbooktitleProbability theory. Mathematical statistics. Theoretical cybernetics, Vol. 22. \bseriesItogi Nauki i Tekhniki \bpages61–157, 204. \bpublisherAkad. Nauk SSSR, Vsesoyuz. Inst. Nauchn. i Tekhn. Inform., Moscow. \bmrnumber778385 \endbibitem

- Dedecker, Merlevède and Rio (2014) {barticle}[author] \bauthor\bsnmDedecker, \bfnmJ.\binitsJ., \bauthor\bsnmMerlevède, \bfnmF.\binitsF. and \bauthor\bsnmRio, \bfnmE.\binitsE. (\byear2014). \btitleStrong approximation of the empirical distribution function for absolutely regular sequences in . \bjournalElectronic Journal of Probability \bvolume19 \bpages1 – 56. \bdoi10.1214/EJP.v19-2658 \endbibitem

- Dehling and Philipp (2002) {bincollection}[author] \bauthor\bsnmDehling, \bfnmH.\binitsH. and \bauthor\bsnmPhilipp, \bfnmW.\binitsW. (\byear2002). \btitleEmpirical process techniques for dependent data. In \bbooktitleEmpirical process techniques for dependent data (\beditor\bfnmH.\binitsH. \bsnmDehling, \beditor\bfnmT.\binitsT. \bsnmMikosch and \beditor\bfnmM.\binitsM. \bsnmSorensen, eds.) \bpages1–113. \bpublisherBirkhäuser, \baddressBoston. \endbibitem

- Dette and Gösmann (2020) {barticle}[author] \bauthor\bsnmDette, \bfnmH.\binitsH. and \bauthor\bsnmGösmann, \bfnmJ.\binitsJ. (\byear2020). \btitleA Likelihood Ratio Approach to Sequential Change Point Detection for a General Class of Parameters. \bjournalJournal of the American Statistical Association \bvolume115 \bpages1361–1377. \bdoi10.1080/01621459.2019.1630562 \endbibitem

- Embrechts and Hofert (2013) {barticle}[author] \bauthor\bsnmEmbrechts, \bfnmP.\binitsP. and \bauthor\bsnmHofert, \bfnmM.\binitsM. (\byear2013). \btitleA note on generalized inverses. \bjournalMathematical Methods of Operations Research \bvolume77 \bpages423–432. \endbibitem

- Fremdt (2015) {barticle}[author] \bauthor\bsnmFremdt, \bfnmS.\binitsS. (\byear2015). \btitlePage’s sequential procedure for change-point detection in time series regression. \bjournalStatistics \bvolume49 \bpages128-155. \bdoi10.1080/02331888.2013.870568 \endbibitem

- Gösmann, Kley and Dette (2021) {barticle}[author] \bauthor\bsnmGösmann, \bfnmJ.\binitsJ., \bauthor\bsnmKley, \bfnmT.\binitsT. and \bauthor\bsnmDette, \bfnmH.\binitsH. (\byear2021). \btitleA new approach for open-end sequential change point monitoring. \bjournalJournal of the Time Series Analysis \bvolume42 \bpages63–84. \bdoihttps://doi.org/10.1111/jtsa.12555 \endbibitem

- Gösmann et al. (2022) {barticle}[author] \bauthor\bsnmGösmann, \bfnmJ.\binitsJ., \bauthor\bsnmStoehr, \bfnmC.\binitsC., \bauthor\bsnmHeiny, \bfnmJ.\binitsJ. and \bauthor\bsnmDette, \bfnmH.\binitsH. (\byear2022). \btitleSequential change point detection in high dimensional time series. \bjournalElectronic Journal of Statistics \bvolume16 \bpages3608 – 3671. \bdoi10.1214/22-EJS2027 \endbibitem

- Hofert et al. (2018) {bbook}[author] \bauthor\bsnmHofert, \bfnmM.\binitsM., \bauthor\bsnmKojadinovic, \bfnmI.\binitsI., \bauthor\bsnmMaechler, \bfnmM.\binitsM. and \bauthor\bsnmYan, \bfnmJ.\binitsJ. (\byear2018). \btitleElements of copula modeling with R. \bpublisherSpringer. \endbibitem

- Holmes and Kojadinovic (2021) {barticle}[author] \bauthor\bsnmHolmes, \bfnmM.\binitsM. and \bauthor\bsnmKojadinovic, \bfnmI.\binitsI. (\byear2021). \btitleOpen-end nonparametric sequential change-point detection based on the retrospective CUSUM statistic. \bjournalElectron. J. Statist. \endbibitem

- Horváth et al. (2004) {barticle}[author] \bauthor\bsnmHorváth, \bfnmL.\binitsL., \bauthor\bsnmHušková, \bfnmM.\binitsM., \bauthor\bsnmKokoszka, \bfnmP.\binitsP. and \bauthor\bsnmSteinebach, \bfnmJ.\binitsJ. (\byear2004). \btitleMonitoring changes in linear models. \bjournalJournal of Statistical Planning and Inference \bvolume126 \bpages225 - 251. \bdoihttps://doi.org/10.1016/j.jspi.2003.07.014 \endbibitem

- Jondeau, Poon and Rockinger (2007) {bbook}[author] \bauthor\bsnmJondeau, \bfnmE.\binitsE., \bauthor\bsnmPoon, \bfnmS. H.\binitsS. H. and \bauthor\bsnmRockinger, \bfnmM.\binitsM. (\byear2007). \btitleFinancial modeling under non-Gaussian distributions. \bpublisherSpringer, \baddressLondon. \endbibitem

- Kirch and Weber (2018) {barticle}[author] \bauthor\bsnmKirch, \bfnmC.\binitsC. and \bauthor\bsnmWeber, \bfnmS.\binitsS. (\byear2018). \btitleModified sequential change point procedures based on estimating functions. \bjournalElectron. J. Statist. \bvolume12 \bpages1579–1613. \bdoihttps://doi.org/10.1214/18-EJS1431 \endbibitem

- Kojadinovic and Verdier (2021) {barticle}[author] \bauthor\bsnmKojadinovic, \bfnmI.\binitsI. and \bauthor\bsnmVerdier, \bfnmG.\binitsG. (\byear2021). \btitleNonparametric sequential change-point detection for multivariate time series based on empirical distribution functions. \bjournalElectron. J. Statist. \bvolume15 \bpages773–829. \bdoi10.1214/21-EJS1798 \endbibitem

- Kojadinovic and Verhoijsen (2022) {bmanual}[author] \bauthor\bsnmKojadinovic, \bfnmI.\binitsI. and \bauthor\bsnmVerhoijsen, \bfnmA.\binitsA. (\byear2022). \btitlenpcp: Some Nonparametric Tests for Change-Point Detection in Possibly Multivariate Observations \bnoteR package version 0.2-4. \endbibitem

- Kuelbs and Philipp (1980) {barticle}[author] \bauthor\bsnmKuelbs, \bfnmJ.\binitsJ. and \bauthor\bsnmPhilipp, \bfnmW.\binitsW. (\byear1980). \btitleAlmost Sure Invariance Principles for Partial Sums of Mixing -Valued Random Variables. \bjournalThe Annals of Probability \bvolume8 \bpages1003 – 1036. \bdoi10.1214/aop/1176994565 \endbibitem

- Lai (2001) {barticle}[author] \bauthor\bsnmLai, \bfnmT. L.\binitsT. L. (\byear2001). \btitleSequential analysis: some classical problems and new challenges. \bjournalStatistica Sinica \bvolume11 \bpages303–351. \endbibitem

- Li and Genton (2013) {barticle}[author] \bauthor\bsnmLi, \bfnmB.\binitsB. and \bauthor\bsnmGenton, \bfnmM. G.\binitsM. G. (\byear2013). \btitleNonparametric Identification of Copula Structures. \bjournalJournal of the American Statistical Association \bvolume108 \bpages666-675. \bdoi10.1080/01621459.2013.787083 \endbibitem

- Mokkadem (1988) {barticle}[author] \bauthor\bsnmMokkadem, \bfnmA.\binitsA. (\byear1988). \btitleMixing properties of ARMA processes. \bjournalStochastic Processes and Applications \bvolume29 \bpages309–315. \endbibitem

- Montgomery (2007) {bbook}[author] \bauthor\bsnmMontgomery, \bfnmD. C.\binitsD. C. (\byear2007). \btitleIntroduction to statistical quality control. \bpublisherJohn Wiley & Sons. \endbibitem

- Newey and West (1987) {barticle}[author] \bauthor\bsnmNewey, \bfnmW. K.\binitsW. K. and \bauthor\bsnmWest, \bfnmK. D.\binitsK. D. (\byear1987). \btitleA Simple, Positive Semi-Definite, Heteroskedasticity and Autocorrelation Consistent Covariance Matrix. \bjournalEconometrica \bvolume55 \bpages703–708. \endbibitem