From Rough to Multifractal volatility: the log S-fBM model

Abstract

We introduce a family of random measures , namely log S-fBM, such that, for , where is a Gaussian process that can be considered as a stationary version of an -fractional Brownian motion. Moreover, when , one has (in the weak sense) where is the celebrated log-normal multifractal random measure (MRM). Thus, this model allows us to consider, within the same framework, the two popular classes of multifractal () and rough volatility () models. The main properties of the log S-fBM are discussed and their estimation issues are addressed. We notably show that the direct estimation of from the scaling properties of , at fixed , can lead to strongly over-estimating the value of . We propose a better GMM estimation method which is shown to be valid in the high-frequency asymptotic regime. When applied to a large set of empirical volatility data, we observe that stock indices have values around while individual stocks are characterized by values of that can be very close to and thus well described by a MRM. We also bring evidence that unlike the log-volatility variance whose estimation appears to be poorly reliable (though used widely in the rough volatility literature), the estimation of the so-called ”intermittency coefficient” , which is the product of and the Hurst exponent , appears to be far more reliable leading to values that seem to be universal for respectively all individual stocks and all stock indices.

Keywords— Rough volatility, Multifractal volatility, fractional Brownian motion, GMM estimation, Intermittency coefficient

1 Introduction

During the past few years, new insights on stochastic volatility models have been obtained after the observation by Gatheral et al. [16] (see also [8, 9]), that the logarithm of the realized volatility is rough, i.e., is less regular than a standard Brownian motion. Rough volatility models have become very popular not only because they allow one to account for main empirical realized volatility properties but also because, when they are considered in asset price models, they provide a very good fit of option prices and notably their ATM skew power-law behavior close to maturity [20, 6, 11]. The first empirical evidence reported in [16] suggests that the logarithm of the asset price stochastic variance can be represented by a fractional Brownian motion (fBM) of Hurst exponent close to . More recent studies based either on quasi-likelihood approach [14] or GMM-approach [10], consistently suggest the is even closer to , i.e., for a large panel of equity data. In that respect, it is natural to consider the limit in the rough process driving the volatility logarithm. Even if one cannot plug in the power-law expression of the fractional Brownian motion covariance, formally, it corresponds to a logarithmic behavior.

Such a logarithmic behavior is precisely the one that characterises the so-called continuous random cascade models introduced two decades ago by Bacry et al. [26, 1]. Indeed, in 2000, these authors proposed the “Multifractal Random Walk” (MRW) as a model for asset prices in order to account for their multifractal properties, i.e., the fact observed by various authors (see e.g. [18, 17, 21]) that asset return empirical moments obey non-trivial scaling properties. The MRW model relies on a multifractal stochastic volatility model, namely the “Multifractal Random Measure” (MRM) model [26, 1], in which the log-volatility is provided by a log-correlated Gaussian field. Such a class of processes, also referred to as Gaussian multiplicative chaos, has been at the heart of many studies in a large variety of applications [29]. Gaussian multiplicative chaos and the associated log-normal random cascades have been extended to any infinitely divisible distribution by Bacry and Muzy in [24, 4].

Recovering a multifractal volatility model as the limit of a rough volatility model or, from a more general perspective, defining a meaningful limit of a fractional Brownian motion and one of its variants has been the subject of various recent studies. In [15], the authors build an - fBM by considering a regularisation from the harmonizable representation of fBM’s while in [27, 19] a limiting process is obtained using a peculiar normalisation and centering of the fBM. In [13] (see also [12]), the authors consider the limit of the exponential of a rescaled Riemann-Liouville fBM and its relationship with Gaussian multiplicative chaos. Finally, in [7], Bayer et al. propose a new class of rough models that consists in modulating the Riemann-Liouville fBM power-law kernel by a logarithmic factor. The so-obtained ”super-rough” stochastic volatility remains well-defined as a continuous process when .

In this paper, our goal is to add a contribution to this problem by introducing a new version of rough volatility models based on the so-called “stationary” fBM (S-fBM). S-fBM is a variant of fBM whose covariance function is exactly the one obtained when considering the small-time approximation of the correlation of the fractional Ornstein-Uhlenbeck process considered in [16]. We prove that when , one recovers the exact self-similar multifractal measure defined in [26, 1]. Our construction is based on the same approach proposed in [24, 4] where the log-volatility is obtained from the integration of a 2D Gaussian white noise over a triangular domain in a time-scale plane. It turns out such an approach corresponds to the same method defined by Takenaka to build the fractional Brownian motion [30]. Our model therefore provides a unified framework to consider both rough and multifractal stochastic volatility models. Beyond defining the main statistical properties of the model, we aim at estimating its parameters on a large panel of market data. For that purpose, we extend the GMM method proposed in [3] that is based on a “small intermittency” expansion of the moments of the measure logarithms.

The paper is organized as follows: in section 2, after recalling the basic notions underlying usual rough volatility models and the definition of the multifractal random measure (MRM), we introduce the log S-fBM random measure as the exponential of the S-fBM random process which is nothing but a “stationary” version of the fractional Brownian motion of Hurst parameter . We show that one recovers the celebrated Mandelbrot-Van Ness fBM when , the correlation parameter of our model, tends to infinity. In this section, we also show that the log S-fBM converges, when , towards a Multifractal Random Measure, consequently leading to a unified framework for rough volatility models (, for ) and multifractal volatility models (by extension, ). In section 3, we establish, within this unified framework, analytical expressions for the second-order moments of respectively and its logarithm, while in section 4 we define two GMM parameter estimation methods based on these expressions. Our approach is illustrated by various numerical examples. Application to empirical data, namely the daily volatility of many individual stocks as well as market indices is provided in section 5. Section 6 summaries our findings while technical material and mathematical proofs are provided in Appendices.

2 The log Stationary fractional Brownian Motion (log S-fBM) stochastic volatility model

2.1 Multifractal and rough volatility models

Before introducing our new model of stochastic volatility measure (log S-fBM), let us briefly walk through the two popular former classes of stochastic volatility models it is notably designed to unify, namely the Rough Fractional Stochastic Volatility (RFSV) model and the Multifractal Random Walk (MRW) or Multifractal Random Measure (MRM) models.

The MRM/MRW models

The MRW was firstly introduced in 2001 by Bacry et al. [26, 1] as a model for log-prices that has exact (log-normal) multifractal properties, i.e., such that the moment of price returns obeys exact scaling properties:

| (1) |

where the multifractal scaling spectrum is a non-linear (namely parabolic) concave function that only depends on a single positive parameter (which quantifies the level of non linearity of ) and such that . Let us point out that the parameter is generally referred to as the intermittency coefficient since it governs the degree of multifractality of the model, i.e., the range of the Hölder exponents that characterise the paths . It consequently controls the degree of appearance of volatility bursts. When , the model is said to be monofractal, then simply corresponds to a Brownian motion which is almost everywhere of Hölder regularity .

The MRW model involves a log-normal stochastic volatility, that is a multifractal random measure (MRM) , obtained as the weak limit

| (2) |

where is defined by

where stands for the weak convergence and the process is Gaussian and stationary with a logarithmic covariance vanishing for lags greater than (see Eq. (75)). Let us point out that multifractality of the limit process is obtained in the Gaussian multiplicative chaos context [29] which implies that, at the same time goes to 0, the mean (resp. variance) of has to go to (resp. ). Thus though the stochastic measure has a weak limit, the Gaussian process does not have a limit. We refer the reader to the beginning of Appendix A.3 for detailed construction of the log-normal MRM.

Since such a logarithmic decreasing covariance can be interpreted using random multiplicative cascades as the limit case where the scale ratio goes to , one often refers to such a model as “continuous cascade” [3] models. In [24, 4], MRM measures have been extended from log-normal statistics to any log-infinitely divisible law so that they obey the exact scaling law:

| (3) |

where is the cumulant generating index of the infinitely divisible law (let us point out that it is parabolic only in the Gaussian case).

The MRM process has been used in various works since 2001 for volatility modeling. Not only it has stationary increments but it reproduces most stylized facts of volatility (including scale invariance and self-similarity properties). Moreover, it also benefits from a concise geometric construction, which allows one to easily obtain the auto-covariance function in the desired form.

The original RFSV model.

In 2018, Gatheral et al. [16] introduced a new (but related) class of models called “rough” fractional stochastic volatility (RFSV) models. Instead of focusing on the scaling properties of price increments, Gatheral et al. examined the regularity properties of the log-volatility and observed (as the case for a multifractal model) that volatility appears to be far less regular than a Brownian motion. RFSV model quickly became a popular model. Within the RSFV framework, the volatility measure of some given interval is supposed to be provided by a density measure corresponding to a log-normal stationary process:

| (4) |

where is a fractional Ornstein-Uhlenbeck (fOU) process that satisfies, for some , the equation

| (5) |

where is a fractional Brownian motion with Hurst parameter . The parameter (resp. ) is the variance (resp. mean) of and , where represents a characteristic correlation time that accounts for the typical mean reversion length of the process. Indeed, Gatheral et al. show that, for small enough, the covariance function of can be approximated as:

| (6) |

where represents the Gamma function. In [16], it is also shown that when , behaves locally as a fractional Brownian motion in the sense that, :

| (7) |

This result can be of practical importance for application in finance since empirically it appears that is very large and consequently can be used as a volatility model instead of the associated fOU process as long as .

Let us point out that, since the original work [16], many other versions of RFSV models have been introduced in the literature, each of them serving some specific purposes (making some explicit computations or estimations simpler) while keeping the main feature of the original RFSV model, i.e., the ”roughness” of the volatility modelled using a fBM-like process. In the next section, we will introduce a new version that will enable us to unify in the same framework an RFSV model and the MRM framework.

2.2 The log S-fBM random measure : a common framework for RFSV and MRM models

In this section, we build the main model of this paper. This model allows us to define a common framework for RFSV and MRM models. It is built in three steps. First we introduce a stationary version of a fractional Brownian motion, namely the S-fBM process for . Then using this S-fBM process, we define the log S-fBM stochastic measure () which can be seen as a new version of a rough volatility model (RFSV). Finally, we prove that this process converges when goes to to a measure that we will refer to as , which is shown to be an MRM.

Step 1/3 : Defining the S-fBM process for

The S-fBM process is a stationary Gaussian process and can thus be defined by its mean and its covariance function. In Appendix A.1, we provide the details of its construction by following the one proposed by Bacry & Muzy ([24, 4]) for building log-infinitely divisible Multifractal Random Measures (MRM). Let us point out that such a construction can also be related to the original approach proposed by Takenaka to build correlated fields (see [30] and Appendix A.2).

Thus, following the construction detailed in Appendix A.1, the S-fBM process is defined for as a stationary Gaussian process whose covariance function is:

| (8) |

The parameter is analog to the Hurst parameter of the fBM process since it controls the “roughness” of the model. The variance parameter controls the average amplitude of the process and the constant is a large time scale that corresponds to the correlation scale. Let us point out that the approximated covariance provided by Eq. (6) of the fOU process , involved in the construction of the RFSV model, holds exactly for the S-fBM (up to a rescaling of ) for lags smaller than . Both the S-fBM process and the fOU could then be regarded as stationary versions of a fBM process but, unlike the fOU process, the correlation function of S-fBM exactly vanishes for lags greater than , i.e., the S-fBM values at different timestamps are independent when the distance between timestamps is large enough (i.e., greater than ).

It is noteworthy that, when , one recovers the original Takenaka construction of the fBM [30] by proving that . More precisely, in Appendix A.2 we show that, when , the analog of Eq. (7) holds for :

Proposition 1.

There exists a fractional Brownian motion of Hurst index and unit variance at such that, , one has:

| (9) |

A direct result from the similarity in auto-covariance function is that S-fBM has the same scaling property as RFSV. According to Appendix A.1, for ,

| (10) |

It leads to the following scaling property of generalized moments, :

| (11) |

This means that is linear against with slope . From Kolmogorov continuity theorem it results that the paths of are continuous functions. More precisely, is Hölder continuous for all regularity exponents . We especially point out that the calibration of the Hurst parameter of the log-volatility process in [16] is based on the obtained scaling behavior (11).

Step 2/3 : Defining the log S-fBM stochastic measure for

The log S-fBM stochastic measure is then defined as:

| (12) |

Then for any interval , one has:

| (13) |

Under this setting, we retrieve the so-called stationarity of volatility process, i.e.:

| (14) |

with

where (resp. ) is the mean (resp. variance) of . The quantity can be regarded as the variance of the price fluctuations on a unit-time interval.

Step 3/3 : Convergence of towards an MRM when goes to 0

As shown in Appendix A.3, the MRM measure can be recovered from the log S-fBM by taking

the limit . More precisely, the following proposition holds true:

Proposition 2.

Let be the log S-fbm process defined by (13) and define the intermittency coefficient,

| (15) |

Considering both and the variance of the price fluctuations

are fixed, then, when (and consequently, and ), one has

| (16) |

where stands for the weak convergence and is a log-normal MRM (as defined by (2)) with the intermittency coefficient and integral scale .

The proof is provided in Appendix A.3. This result indicates that the MRM can be considered as a limit case of a log S-fBM and therefore could be regarded as an ”extremely rough” case. Let us remark that very much like the scale parameter involved in the regular construction of the MRM, the parameter in the context of Proposion 2 can be considered as regularization parameter. However, such a regularization through impacts observations at all (time) scales since it explicitly breaks scale-invariance that is not the case of regularization through as defined in Appendix A.1.

Conclusion and notations for the remaining of the paper

For the sake of simplicity, in the following, the MRM will be referred to as .

Thus, we can consider that we have built a class of models , which correspond for to an RFSV model and for to an MRM model.

3 Second order properties of and its logarithm

In section 4, we will consider the problem of estimating the parameters of the S-fBM, namely (or equivalently ) and through the expression of various “statistical moments” of the process. Among these moments, the correlation function of or of are particularly interesting since, as emphasized below, they can be approximated by simple analytical expressions.

Let us first remark that in [16], Gatheral et al. proposed to estimate the roughness exponent of the RFSV model (equivalently in the log-SfBM model) by considering the scaling of the increments of as in Eq. (11). However, since cannot be directly observable, they consider as a proxy of , the observable moments:

| (17) |

where is the so-called integrated variance over an interval of size :

| (18) |

Thus, the exponent is measured from the scaling behavior in of this proxy of using the Eq. (11).

However, as emphasized below (see Section 4.1), the estimation of based on Eq. (11) can be highly biased. In order to obtain an unbiased estimation of H in the framework of an RFSV model, Ref. [10] introduces a totally different framework. The authors provide a GMM method that is based on the correlation function of :

| (19) |

More precisely, they show that under peculiar conditions, its asymptotic behavior when can be obtained and then a GMM formula can be derived. Within the framework of various RFSV models (namely the one involving an fBM or its Riemann-Liouville variant), the authors advocate the use of this GMM method and show that it provides reliable estimates for both the roughness parameter and the variance parameter .

Following this latter path, in this work, we aim at defining a GMM method for the log-SfBM framework, that works for both (the RFSV case) and (the MRM case). We thus need to establish exact or good approximations of correlation function of . This is the purpose of the next section (Section 3.1).

Moreover, as we will see, the process is, in some sense, close to be a Gaussian process, consequently it is also natural to operate the GMM not on the process itself but on its logarithm . We therefore also need to establish exact or good approximations of the correlation function of , which is defined by :

| (20) |

This is the purpose of Section 3.2.

3.1 Integrated variance correlation function

In Appendix A.4 we prove the following Proposition that gives an explicit analytic formula for :

Proposition 3.

For any , one has

| (21) |

with

| (22) |

where stands for the (lower) incomplete Gamma function,

and where we have denoted

Let us notice that when , since and are independent, one has:

Moreover, using the equality:

where is the Kummer’s confluent hypergeometric function, the function can be simply rewritten as:

| (23) |

where is the covariance of provided by Eq. (8). Since, when , and finally, when , the following approximation for holds:

| (24) |

3.2 Small approximation of the logarithm integrated variance moments

In this section, our goal is to obtain analytical expressions for the moments of instead of . In [3] a GMM method to estimate the parameters of the MRM has been proposed relying on the expression of such logarithmic moments that were obtained within a small intermittency, i.e. , asymptotic behavior. In fact, it is straightforward to check that all proofs and results established in [3] in the limit for the log-normal MRM measure remain valid for for , i.e. in the log S-fBM framework introduced in this paper. Indeed, in particular by simply checking that all conditions required for MRM also hold for the log S-fBM measure , a direct consequence of Proposition 13 in [3] is the following result:

Proposition 4.

Let be arbitrary times. The generalized moments of the logarithm of admit the following Taylor series expansion around :

| (25) |

where is the Gaussian process defined by

| (26) |

Within this approximation, one can directly compute the correlation function of as defined in (20). From the definition of and the expression (8) for the covariance of , it results:

Proposition 5.

To the first order in , the covariance function of , reads:

| (27) | |||||

| (28) |

Let us first start with two direct consequences of these propositions

Using this last consequence, Proposition 4 can also be used to obtain an approximation to the first order in of the moments defined in (17). Indeed, if one supposes that is a Gaussian random variable of variance , then,

| (29) |

in which indicates that equality holds in the first order of .

The final expression for the moments of the increments of the measure logarithm reads, in the first oder in ,

| (31) |

Let us remark that we have the following asymptotic relation:

| (32) |

and when , one recovers that when one has, to the first oder in ,

| (33) |

which is the expression used to estimate in [16] where corresponds to the logarithm of the (daily) realized volatility.

4 Estimation

This section is devoted to the estimation of in the framework of log-SfBM. We first show (in Section 4.1) that if is measured from the scaling behavior of against using Eq. (11) (as advocated in [16]), the estimation of can be highly biased.

In order to obtain an unbiased estimation of , we consider two GMM based estimators in Sections 4.2 and 4.3. The first one is based on the use of the moments of the log-SfBM process itself mainly relying on the explicit covariance formula in Eq. (21). The second one is based on the use of moments of the logarithm of the log-SfBM process and involves the explicit covariance provided by Eq. (28).

We show that both estimators are expected to be reliable even in the ”high-frequency regime” when data are only available over an interval that is smaller than the overall correlation scale , i.e. in a regime when one does not expect any ergodic hypothesis to hold.

4.1 Bias of the moment scaling method proposed in Ref. [16]

In [16], the parameter is estimated from the scaling behavior of against as described in Eq. (11). More precisely, the unobservable quantity is substituted by its observable proxy as defined in Eq. (17), whose explicit form is worked out in Eq. (31). Then, a linear regression of against is performed in order to estimate .

We can show see that this approach can lead to a significantly biased estimation of . Indeed, by taking logarithm on both sides of Eq. (31), one has (using again the notation for equality up to the first order of )

| (34) |

where the expression of is provided in Eq. (30). Since the term also depends on , assuming, on a given range of , that

| (35) |

the measured slope in the relation against is biased as:

| (36) |

and the bias depends on both the considered range of and the value of .

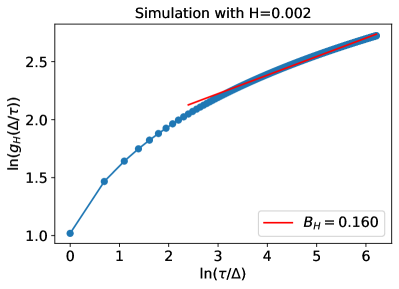

Let us illustrate this phenomenon on some numerical simulations. For that purpose, let us consider an arbitrary value and . For the specific value , Fig. 1 plots as a function of . We note that the behavior is, to a first approximation, assumed to be linear in the range when is sufficiently large in front of . A linear regression leads to a slope value of which dominates the (highly biased) estimation of : . Using the same procedure, we checked that for different values of in the range , one systematically overestimates with a bias that decreases from to . It is noteworthy that the same kind of bias analysis has been considered by the author of Ref. [16] themselves (see their Appendix C).

4.2 Low versus high frequency regime for GMM estimations

As already explained, our purpose is to build two GMM estimators based on the second order moments of the log-SfBM process or its logarithm. More precisely, we will consider respectively the correlation function of (using the explicit covariance formula (21)) and , the covariance function of (using the explicit covariance formula (28)). If denotes the overall size of the interval where the empirical data are available at scale , one can measure (or equivalently ) for where and the estimators of previous correlation functions read:

| (37) | |||||

| (38) | |||||

| (39) |

In general, GMM methods rely on some ergodic hypothesis that ensures the convergence of previous empirical means towards the expected values. As advocated in [3] or in [10], these approaches allow one to build efficient parameter estimator in the limit , which, when is kept fixed, corresponds to . When (recall that is the correlation length of ), this ergodicity assumption can be proven to hold. We refer to such a situation as the “low-frequency regime”.

However, as first remarked in [3], one can alternatively consider the asymptotic regime when , while is fixed. This is the “high-frequency regime”. Thus, whereas the low-frequency regime corresponds to , the second one corresponds to .

Let us point out that, as emphasized in [3] and motivated by the empirical results reported in [25] (see also Sec. 5 below), in many practical situations and notably for financial time series, the high-frequency regime appears to fit more precisely the empirical conditions. Notably, it appears that the correlation scale of the realized volatility always seems to be larger than the observation size . For instance, in Fig. 6(b) of [25], the authors plotted the logarithm of Dow-Jones realized daily volatility from 1928 to 2011 and observed deviations far from the “mean value” that are lasting for decades. The same kind of observation can be done in Fig. 8(a) below. In [25], it is also observed that the estimated correlation scale increases linearly with the observation size from a few days to several years in agreement with the hypothesis that the true correlation scale is extremely large. In such a situation, assuming that the low-frequency regime is reachable and consequently that the ergodic hypothesis holds, is clearly unrealistic.

These remarks call for developing GMM estimations in the high-frequency regime . Let us first start by noticing that from the expression of the covariance of (Eq. (8)), for (where is any interval such that ), one has

| (40) |

where means an equality of all finite dimensional distributions and is a Gaussian random variable independent of and of variance . It thus results that we have, in any interval of size ,

| (41) | |||||

| (42) |

As already discussed in [3] for the case of the MRM measure , these properties show that one cannot measure the parameters and over an interval of size since by redefining as , one can always assume that . It can also be seen on expression (22) that, when , the large correlation scale can be absorbed in a redefinition of the variance parameter .

If one seeks to consider correlation function based GMM estimators in the high frequency regime, one thus needs to study the behavior of respectively the estimators, , in the limit . A rigorous study of this problem is beyond the scope of the present paper, but we can refer to Theorem 10 of [3] where the authors proved that, in the multifractal case (), the behavior of can be used to build an asymptotically unbiased and consistent estimator of in the high frequency regime. In the present paper, we just give a sketch of proof that one can build moments functions with vanishing fluctuations in the limit .

First, let us notice that, without loss of generality, one can always perform an overall change of scale, , , . This amounts to assume that while the limit becomes and with .

Then, Appendix A.5 provides an heuristic proof of the following result:

Proposition 6.

Suppose that . Then, for any , , when , then, to the first order in , one has for all :

| (43) |

where means that the convergence holds in “in probability” and where

| (44) |

Moreover, numerical experiments (see Fig. 2 below) also suggest that an equivalent result holds for , i.e.,

| (45) |

with

| (46) |

where is defined in Eq. (22).

The consequence of Eqs. (43), (45) is that, for large enough, there exist two positive random variables and such that, in the first order of ):

| (47) | |||||

| (48) |

Numerical illustrations of these relations are given in Figs. 2 and 3.

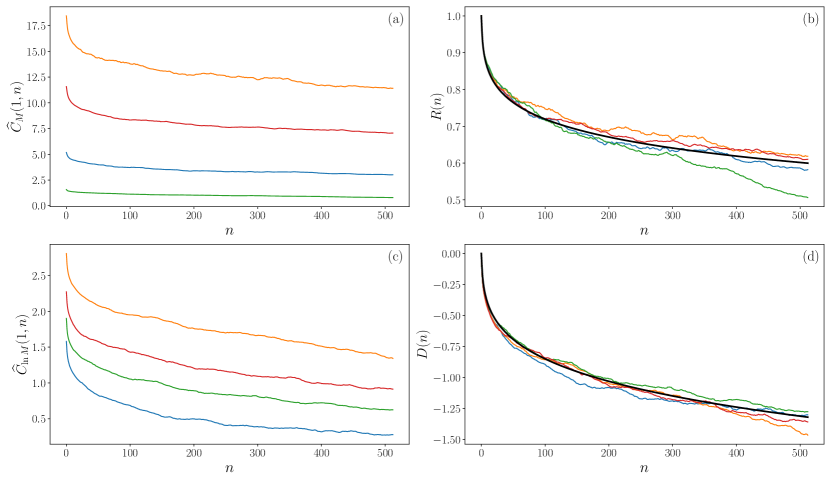

In Fig. 2, we have displayed the estimated correlation functions and for 2 sets of 4 realisations of over an interval of size with , , and (for ) or (for ). One clearly sees in Fig. 2(a) that each estimate seems to differ from the other one by a significant geometric random factor while estimates of appear to be randomly shifted in Fig. 2(c). In order to check these assertions, we have plotted respectively the ratios and the differences in Figs 2(b) and 2(d). As expected, all the curves appear to collapse to a single curve that is well described by analytical expressions obtained from respectively Eq. (44) and (46) (represented by bold curves).

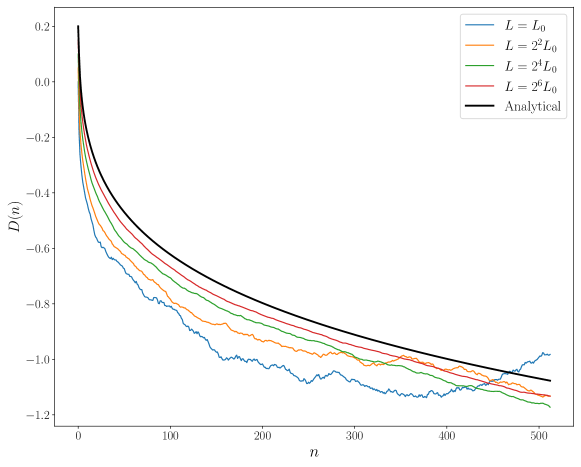

The asymptotic convergence of Proposition 6 is illustrated in Fig. 3 where we have plotted as defined in Eq. (43) as obtained from random samples of with , , , and . All the curves are shifted by an arbitrary small constant for clarity purpose. As predicted by Eq. (43), one sees that, as increases, the empirical curves become less and less noisy and increasingly close to the analytical expectation (44) (black curve).

4.3 Defining two GMM estimators for and

We are now ready for defining two GMM estimators for based respectively on the moments of or its logarithm in the high-frequency limit. By using the previously established expressions (44) and (46) for the empirical correlation function and , one can devise two GMM methods along the same line as the methods proposed respectively in [3] and [10].

As explained in the previous section (Section 4.2), in the high-frequency regime, estimations of or are unreachable. Thus, hereafter, we consider exclusively the problem of estimating the values of the parameters and (or alternatively ) using one of the following two sets of moments:

where is the number of moments, different time indices, and are the empirical estimators of respectively and and the following analytical expressions:

| (49) | |||||

| (50) |

where and are 3 random positive constants and stands for the Kronecker function. Notice that the term allows one to account for the eventual presence of a white noise (of variance superimposed to as described in ref. [10].

4.4 Numerical illustrations and empirical performances of the GMM methods

In order to verify our approach and compare the performances of and , we have carried out various numerical experiments. However, since historical volatility is not directly observable in financial markets, in order to consider a more realistic scenario, we decided to run the experiments directly on a price model. We consider that a “price” is modelled by a Brownian motion whose variance is a log S-fBM measure , i.e.,

| (51) |

where is the log-fBM defined in (12) while is a Brownian motion independent of . Let us notice that, when , is precisely the MRW process introduced in [26, 1]. Let us also remark that, in many respects (e.g., by rewriting as a stochastic integral of the form ), the model (51) can be seen as a peculiar non skewed variant a the rough Bergomi model introduced in [6].

Alternatively, an equivalent definition of can be obtained using a time-warp of the Brownian motion:

| (52) |

Within this framework, is called the (stochastic) volatility of . If one does not observe directly but only the process , as emphasized notably in [5], a proxy of the integrated volatility over an interval of size is provided by an estimation of the quadratic variation of :

| (53) |

As shown in [5] (see also [10]), as , under mild conditions, while even for moderate , and provide excellent approximations of the integrated volatility and its logarithm. For the purpose of this paper, we have checked that is sufficient to disregard any significant difference between and .

We simulated independent samples of S-fBM processes and the associated processes with , and , with 2 different values of , namely and . We chose , and fixed arbitrary .

For all these parameters we run both and estimators with and . Our GMM implementations closely follow the one detailed in [10] and notably the error covariance is estimated using the Newey-West HAC type estimator with a lag and the initialisation is performed using the scaling estimator provided in [16]. We used the L-BFGS-B minimisation algorithm as provided by scipy.optimize library in Python but we find similar results using alternative methods.

In Fig. 4, are displayed a fit of respectively and using expressions (44) and (46) with the estimated GMM parameters for a sample of length with and or . Our estimation results are summarised in Table 1 where we reported the obtained mean values and standard deviation of estimated and for each set of parameters.

| () | 0.010 (0.01) | 0.007 (0.015) | 0.077 (0.033) | 0.146 (0.05) |

| () | 0.010 (0.01) | 0.018 (0.015) | 0.082 (0.02) | 0.153 (0.02) |

| () | 0.010 (0.01) | 0.010 (0.01) | 0.018 (0.006) | 0.021 (0.005) |

| () | 0.019 (0.001) | 0.020 (0.001) | 0.019 (0.002) | 0.020 (0.002) |

| () | 0.010 (0.02) | 0.018 (0.02) | 0.11 (0.22) | 0.16 (0.26) |

| () | 0.010 (0.01) | 0.02 (0.01) | 0.078 (0.02) | 0.16 (0.02) |

| () | 0.08 (0.03) | 0.08 (0.02) | 0.09 (0.045) | 0.08 (0.07) |

| () | 0.095 (0.001) | 0.10 (0.005) | 0.10 (0.008) | 0.10 (0.008) |

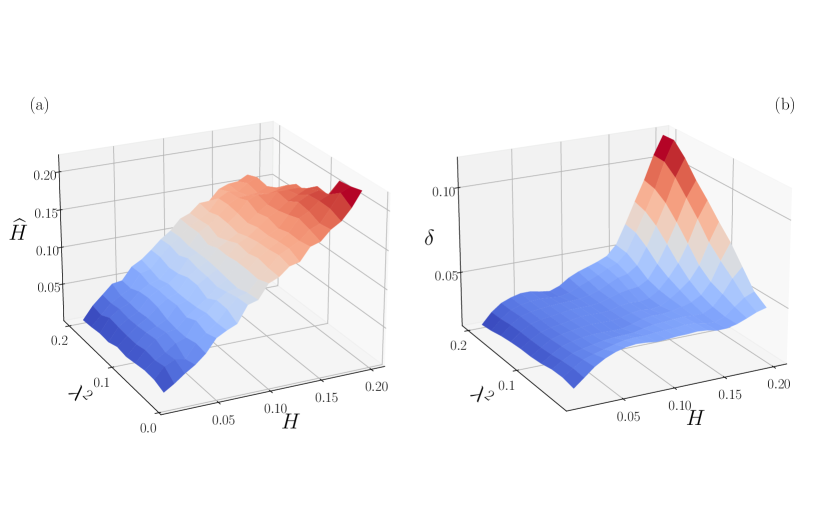

We clearly see that the method relies on logarithms of integrated volatilities outperforms the method built on integrated volatilities. This latter approach appears to have significantly larger bias and variance errors notably for very small values. method provides more reliable estimates and in particular one sees that the error on is very small for all sets of parameters. In order to better illustrate the variations of , the estimation error on , as a function of the S-fBm parameters, we have displayed it as a surface plot in Fig. 5 for a size comparable to ones of the empirical time series considered in section 5. One can see that the error increases when both increases and increase but remains rather small in the domain and . As far as the estimation error of is concerned, we have observed similar results though with a relative error smaller than over the whole domain.

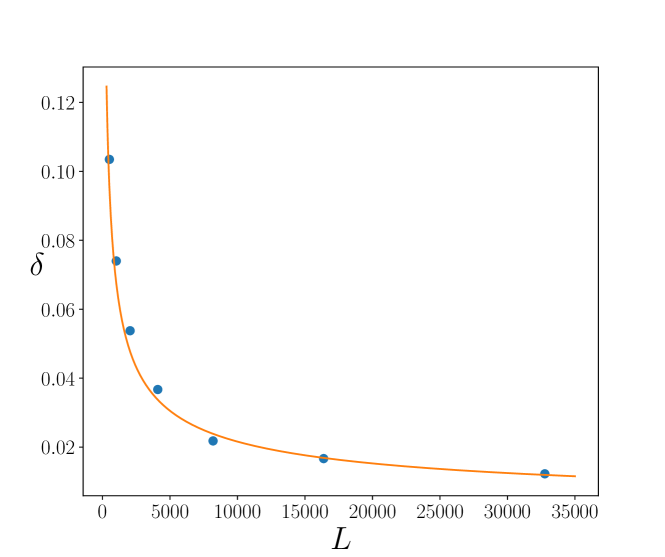

Regarding the scaling of the error with respect to the sample size , by considering, besides as in Fig. 5 or as in Table 1), various sample lengths () with , we checked that, as predicted by Prop. 6, the estimation errors vanishes when increases. As illustrated in Fig. 6, empirically, it appears that, even in the high-frequency regime, the error behaves as .

Finally, let us emphasise that the reported estimations were obtained by estimating and the variance parameter from which is estimated using Eq. (15). We checked that estimating directly instead of deriving it from , provides the same results. However we observed that the errors on are much larger than the errors on . More precisely, it appears that, for a fixed , the measured bias is strongly related to as precisely expected from :

| (54) |

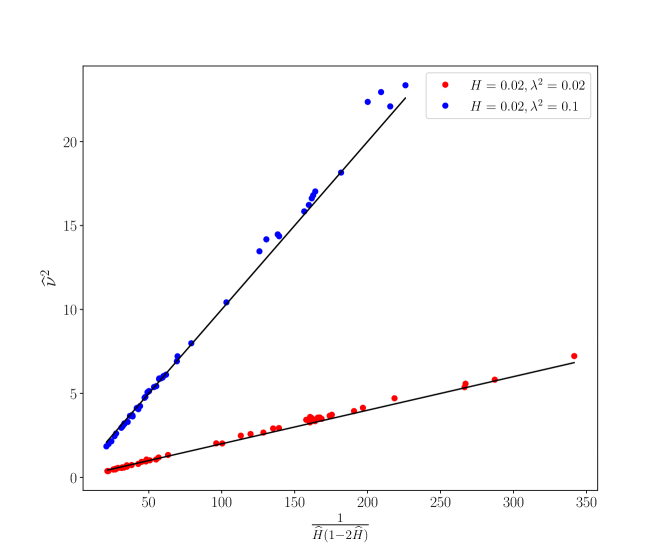

This is illustrated in Fig. 7 in which two experiments where run with . For the first one we chose and for the other one we chose .

For each sample, we have reported as a function of estimated by method. One can easily see that in each case ( or ), one observes a very large dispersion on (whose expected values should be respectively and ) that, however, strikingly appears to be proportional to (which, when is very small, has a large dispersion). As shown by the linear fits predicted by Eq (54) (continuous line in Fig. 7), the proportionality constant is precisely the value of the intermittency coefficient for which the estimation is quite accurate. These observations suggest that while can be estimated with a very small error, this is not at all the case of , when . The intermittency coefficient appears to be a much more reliable quantity than the variance of the log volatility. This can be easily explained by the fact that, in order for the S-fBM measure to converge when (towards the MRM ), one has to choose a variance proportional to . Therefore, in the moment estimation method, in order to match the empirical covariance values when the estimated is very small, the parameter must scale as .

5 Application to realized volatility of asset returns

In this section we consider the application of the estimator of the former section to characterise the roughness exponent and the intermittency coefficient of realized volatility associated with various assets. Section 4 suggests that the GMM estimator outperforms the other candidate . This is why we exclusively consider the applied to various empirical daily volatility data. Our study is based on 2 datasets containing respectively stock market indices and individual stock prices:

Oxford-Man Institute of Quantitative Finance Realized Library (OM)

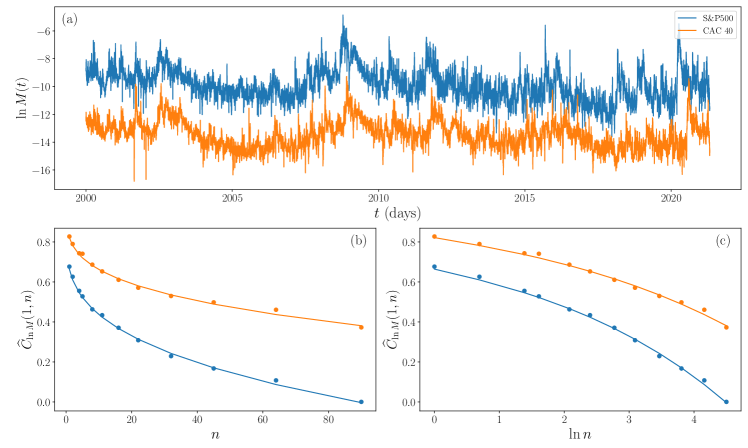

The Oxford-Man Institute’s Realized Library111http://realized.oxford-man.ox.ac.uk/data, contains historical records of various estimators of daily realized volatility of several stock indices. This dataset is widely used in various empirical studies and in particular, it was used as a benchmark database in many former studies on rough volatility (see e.g. [16, 10]). So we apply estimator to analyse the daily volatility time series associated with 24 major stock market indices considered in [10]. Following this latter work, in the following, we only report obtained results when using bipower variation volatility estimator but we have checked that the same results are obtained when using realized variance estimators at scale min or min. Two estimations are illustrated in Fig. 8 : one on CAC40 data and one on S&P500 data. The corresponding daily historical volatilities (using bipower-variation estimator) are illustrated in Fig. 8(a). We observe that over the 20-years period, the volatilities of S&P 500 and CAC40 are strongly correlated. One can also notice that some of the correlated departures from the mean value are lasting several years. This observation seriously questions any ergodic hypothesis that would result from short-term correlations as assumed in many papers (see, e.g., [16, 10]). Figs 8(b) (resp. (c)) displays the corresponding estimated correlation functions as a function of (resp. ) and their fits. The so-obtained estimations for are (for S&P) and (for CAC40). For both indices, we estimate .

Yahoo Finance database (YF)

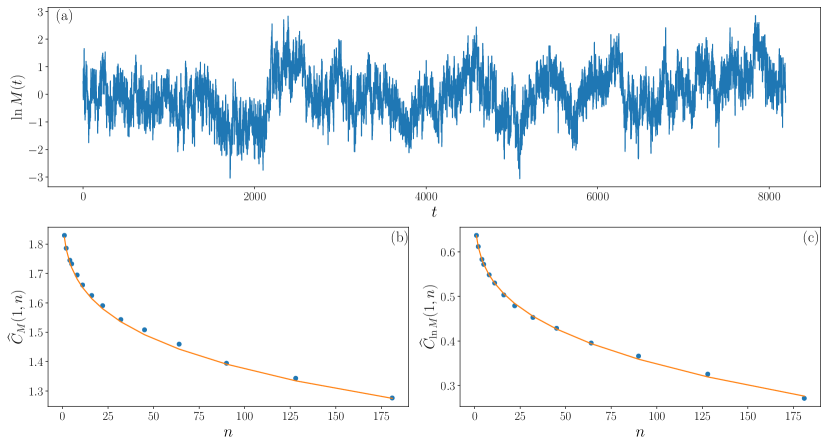

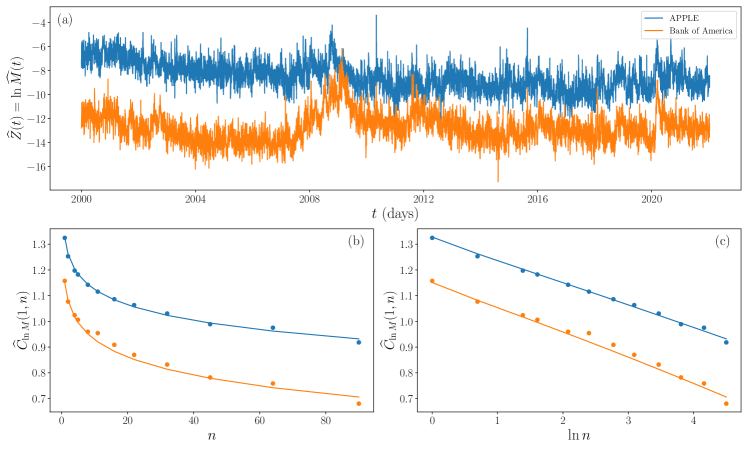

We collected historical daily open, high, low, and close price time-series of 296 individual stocks and also of a set of 24 stock indices from Yahoo Finance222http://YahooFinance.com. Stocks were taken from either the S&P 500 index (historical data from 1985-01-01 to 2021-12-31) or the CAC 40 index ((historical data from 2000-01-01 to 2021-12-31) while the indices were chosen as being those we considered in the OM database (over the period 200-01-01 to 2021-12-31). For each asset, we constructed a proxy of the daily volatility using Garman-Klass (GK) estimator described in [22]. This allows us, for any individual stocks or any index, to perform a estimation of and from the estimated log-volatility time series. As illustrated in Figs 10 and 11 below, on stock indices our results using Oxford-Man realized volatility and GK volatility estimation from YF data provide results that are fully consistent. In Fig. 9, following the exact same structure as Fig. 8, we illustrated the estimation procedure with the examples of Apple and Bank of America realized volatility. Again, we observe that volatility fluctuations seem to be long-term correlated. For the selected two stocks, the estimated values of are respectively and .

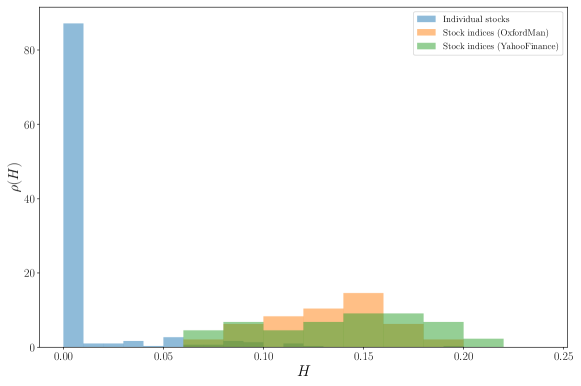

The estimations on all the 24 stock indices from both OM and YF databases and the 296 individual stocks from the YF database are summarized in Figures 10 and 11. In Fig. 10, we have reported the normalized histograms of the estimation for the Hurst exponents of the stock indices and the individual stocks of the two datasets. We can observe that the two distributions are quite different: while the Hurst exponents of the stock market indices are spread around with a rather large dispersion (corresponding to a rms of 0.03), the distribution of values of individual stocks is mainly peaked around a very small average value (with a rms of 0.015). It therefore clearly appears that the log-volatility of stock indices is much more regular than the log-volatility of individual stocks which turns out to be well described by a multifractal model characterized by . Moreover, in agreement with the findings of [16] (and in contrast with the results reported in [10]), Stock indices are confirmed to be well described by a ”rough volatility” model with a typical value of the Hurst exponent close to . Notice that that estimation from either OM bipower variation realized volatility (orange bars) or YF Garman Klass realized volatility (green bars) provides a similar result333To be more precise, empirically the find a correlation coefficient of 0.7 between the two series of Hurst index estimates (i.e., from OM and YF data) over the 24 indices..

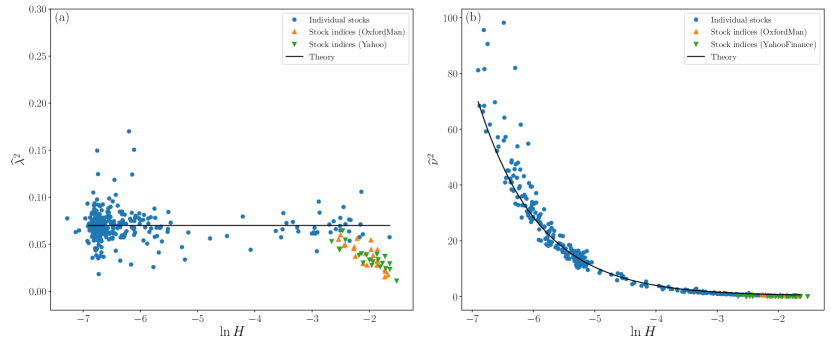

As far as the intermittency coefficient is concerned, we reported in Fig. 11(a) the estimated values for the 296 individual stocks (blue bullets) and the 24 stock indices (orange and green triangles for respectively OM and YF data) as a function of the logarithm of the estimated exponent . First, we can remark in both figures that OM and YF index data provide close estimations and therefore lead to the same conclusions. We can see that all the points are distributed around the value for stocks and for indices. In contrast, if one estimates the variance parameter , one observes a very large dispersion of its values. Actually, as it can be checked in Fig. 11(b), the data closely follow the curve as represented by the solid line. Whether varies because itself is varying or because of estimation errors, it appears that is related to through the relationship (54). This suggests that the intermittency coefficient is more likely to be the pertinent parameter to account for volatility fluctuations. Moreover, this latter quantity appears to be “almost universal” with a value for stocks and for indices. Let us remark that, because of data dispersion due to estimation errors, one can not exclude in Fig. 11(a), a direct relationship between and , since one can observe that slightly decreases as the Hurst exponent increases. A possible explanation could be that a linear combination of multifractal processes with some particular correlations in their increments or in their volatilities (the individual stock prices) may appear as a rough volatility process with an intermittency that depends on (some market index). This question will be considered in future work.

6 Conclusion

We have introduced the log S-fBM, a class of log-normal “rough” random measures that converge, when , to the log-normal multifractal random measure. This model allows us to consider, within the same framework, the two popular classes of multifractal () and rough volatility () models. Besides the roughness exponent , the model involves 3 supplementary parameters: that provides the mean value of , the intermittency coefficient which is related to the variance of and the correlation length (also referred to as the ”integral scale” in the multifractal literature) above which the process values are independent. The second-order properties are studied and notably, we have computed the correlation function of to the first order in . By studying the self-similarity properties of when one changes the correlation length , it appears that one cannot estimate and in the “high-frequency” estimation regime, i.e., if one observes, at a small scale , a single sample of over an interval of length .

We design two efficient GMM estimation methods, and based on the expressions of respectively and correlation functions. We provide theoretical arguments and numerical evidence showing that very much like the method introduced in [3], provides an efficient estimation of and even in the high-frequency asymptotic regime.

We illustrate on various numerical examples that, when , the most pertinent parameter for accounting for volatility fluctuations is not, as it is always used in the rough volatility literature [16, 10], the variance parameter , but the intermittency parameter . Indeed the estimation of the variance parameter is shown to have large fluctuations and to strongly depend on the estimation error on .

Finally, when calibrating the log S-fBM model on a large set of empirical daily volatility data, we observe that stock market indices have values around (close to a rough volatility behavior) whereas individual stocks are characterized by values of that can be very close to (close to a multifractal volatility behavior). The conclusions of section 4 concerning the Hurst estimation errors for the typical sample sizes we considered ( corresponding to 20 years of daily data) and the agreement of the estimated values from two very different volatility estimators associated with YF and OM databases, make it unlikely that such an observation is caused by a statistical bias. Furthermore, nothing guarantees that a linear combination (indices) of multifractal processes (individual stocks) appears to be itself multifractal. It may simply appear as a ”rougher” volatility process with eventually a smaller intermittency coefficient. This specific question will be addressed in future work. Finally, we pointed out that the estimations of the intermittency coefficient are much more robust than the ones of the variance parameter . Its value seems to be quite universal and spread around for stocks and for stock market indices in agreement with the values formerly reported for the multifractal model [3].

In a future work, we will consider the issue of defining a faithful model for asset and option prices within the log S-fBm framework. To that end, the problem of introducing a specific skewness in our model will be considered along the same line as in Ref. [2]

Appendix A Appendix

A.1 Construction of the S-fBM process

In this Appendix, we explain in every details how the S-fBM process is defined. It depends on three parameters :

-

•

the (Hurst) parameter ,

-

•

the decorrelation time scale

-

•

and the coefficient which is linked to the variance parameter by

This parameter will be referred to as the intermittency parameter since it controls the intensity of intermittent “bursts” observed in and it is the name given to that quantity in the framework of MRM.

Construction of the S-fBM process

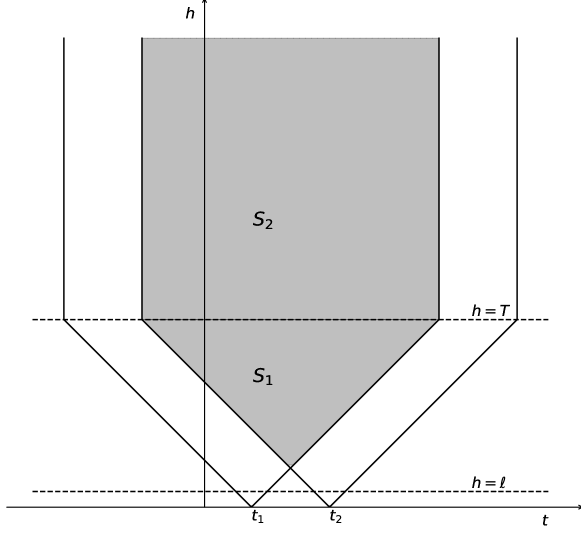

In the upper half-plane , we first consider the area illustrated in Fig. 12 which is defined as:

| (55) |

For , we will use the notation .

We then consider in a non homogeneous Gaussian white noise of variance:

| (56) |

We will see below that is the analog of the Hurst parameter of the fBM process.

We then define the Gaussian process as:

| (57) |

where is a normalising constant such that

| (58) |

Covariance function of the S-fBM process

As a Gaussian process, the S-fBM is mainly characterised by its covariance function.

This covariance can be directly calculated as the variance of integral of the random measure on the overlapping area of and displayed in Fig. 13:

| (59) |

Let us assume, without loss of generality, that and denote . When , and thus . For , we have, using the notations of Fig. 13,

| (60) | ||||

Using (56), we have for the first term,

| (61) | ||||

For the second term,

| (62) | ||||

By composing the results above,

| (63) |

Similarly, if we consider a strictly positive and , direct calculation shows:

| (64) |

A.2 Takenaka fBM and proof of Proposition 1

Let us denote by the full cone obtained by considering in :

| (65) |

and consider the domain:

| (66) |

where stands for the symmetric difference between two sets and , are the two disjoint sets:

Along the same line as definition (57), let us define the Gaussian processes:

| (67) |

Notice that and therefore . It is easy to show that, after a little algebra that, for :

It directly results that:

| (68) |

with . Since , we see that is nothing but a fractional Brownian motion. This construction corresponds to the 1D version of Takenaka fractional Brownian fields as discussed in [30].

In order to prove Proposition 1, let us first work out

This amounts to compute the ”areas” of the intersections of with and respectively. After a little algebra, one obtains, for any :

where is a positive constant depending on and . Similarly, if

one has if :

| (69) |

Let

and

By expanding the square one directly obtains:

Therefore, , , we have when :

| (70) |

On can consider as a metric and define as the number of boxes of radius need to cover the set . Let . Then, according to Dudley inequality [23], there exists a positive universal constant such that:

| (71) |

From Eq. (70), one has . Moreover, one has

where stands for the largest integer not greater than . We then have when is small with respect to :

Thus

since for , when . Proposition 1 follows directly from inequality (71).

A.3 The case : Convergence towards the MRM log-normal measure

We now examine the case in the geometric construction above. The definition of remains unchanged and we consider the Gaussian random noise when , of variance:

| (72) |

Then we define a random process as previously

| (73) |

As proven in [4], provided is chosen such that , when we have

| (74) |

where stands for the weak convergence and where is the so-called log-normal ”Multifractal Random Measure” (MRW), a non trivial singular continuous random measure with exact multifractal properties [24, 4, 3].

| (75) |

We can remark that this expression of the covariance of in the range , can be recovered from Eq. (63), (64) when .

Let us show a strong mean square convergence of S-fBM to MRM when as claimed in Proposition 1.

Since is regular enough, in order to establish the weak convergence we just have to prove that ,

| (76) |

Before starting, it is useful to calculate the covariance between and . Following similar computation as in Appendix A.1,

| (77) |

By expanding the square in Eq. (76), we have:

| (78) |

Since, for a symmetric function , one has:

Then the previous expression becomes:

| (79) |

Let us split this integral as a sum of two integrals, and according to whether one considers the integration domains and respectively. In the first case, by replacing the covariance by their expressions, one has:

| (80) |

Since , one can the safely take in the lower integral bound and then, thanks to dominated convergence theorem, observe that converges to 0 when since the expression inside the integral vanishes in this limit. The second integral, when is:

| (81) |

For , the first and last terms inside the integral can be bounded by a constant that does not depend on while the second term can be bounded by . Therefore we can see that, if , when . This concludes the proof.

A.4 Proof of Eqs. (21) and (22)

Let us compute the analytical expression of and establish expressions (21) and (22). For that purpose, let us first remark that from the definition (18) of and from the expression (8) of the covariance of , we have (when ):

| (82) |

with and .

Moreover, let us prove that, if is a symmetric function, then

| (83) |

Indeed, as shown in [28], we have, when :

In the l.h.s. of (83), let us set and use respectively symmetry argument and previous expression to obtain

By using (83) in (82), we have:

where we have denoted

If one considers the lower-incomplete Gamma function ,

and makes the change of variable in previous integrals, one obtains the following exact expression for :

which corresponds to Eq. (22). When , i.e. for , one can show that the former expression reduces to:

A.5 Proof of proposition 6

In this section we provide a proof of Proposition 6 based on small intermittency approximation of Proposition 4. Let and be the number of samples in the interval . We will suppose that with , so that we are in the high frequency regime. Let us consider the empirical mean:

| (84) |

and define the “centered” random variable:

| (85) |

If , one has obviously:

| (86) |

One can use Proposition 4 to compute, to the first order in , all terms in Eq. (86). Indeed, the expression of is provided by Proposition 5 (Eq. (28)) and order to compute , one can use Prop. 4 to show that, to the first order in ,

and therefore, from expression (28), one has:

| (87) |

It thus results that:

| (88) |

Let us consider the empirical covariance:

| (89) |

Since one has (as defined in Eq. (44)), in order to prove Eq. (43), it is sufficient to show that

To that end, remark that, from the definition of ,

| (90) | |||||

| (91) |

where we have denoted

From proposition 4, because is a Gaussian process, we have, to the first order in ,

Thereby, from the expression (88) of , after a little algebra, one can show that there exists a constant such that

Then, Eq. (91) gives:

Acknowledgement

This research is partially supported by the Agence Nationale de la Recherche as part of the “Investissements d’avenir” program (reference ANR-19-P3IA-0001; PRAIRIE 3IA Institute).

References

- [1] E. Bacry, J. Delour, and J. F. Muzy. Multifractal random walk. Phys. Rev. E, 64:026103, Jul 2001.

- [2] E. Bacry, L. Duvernet, and J.F. Muzy. Continuous-time skewed multifractal processes as a model for financial returns. Journal of Applied Probability, 49(2):482 – 502, 2012.

- [3] E. Bacry, A. Kozhemyak, and J. F. Muzy. Log-normal continuous cascade model of asset returns: aggregation properties and estimation. Quantitative Finance, 13(5):795–818, 2013.

- [4] E. Bacry and J.F. Muzy. Log-infinitely divisible multifractal processes. Communications in Mathematical Physics, 236(3):449–475, 2003.

- [5] O.E. Barndorff-Nielsen and N. Shephard. Econometric analysis of realized volatility and its use in estimating stochastic volatility models. J.R. Statist. Soc. B, 64, 2002.

- [6] C. Bayer, P. Friz, and J. Gatheral. Pricing under rough volatility. Quantitative Finance, 16(6):887–904, 2016.

- [7] C. Bayer, F.A. Harang, and P. Pigato. Log-modulated rough stochastic volatility models. SIAM Journal on Financial Mathematics, 12(3):1257–1284, 2021.

- [8] M. Bennedsen. Semiparametric estimation and inference on the fractal index of gaussian and conditionally gaussian time series data. Econometric Reviews, 39(9):875–903, Feb 2020.

- [9] M. Bennedsen, A. Lunde, and M.S. Pakkanen. Decoupling the Short- and Long-Term Behavior of Stochastic Volatility. Journal of Financial Econometrics, Jan 2021.

- [10] A.E. Bolko, K. Christensen, M.S. Pakkanen, and B. Veliyev. Roughness in spot variance? A gmm approach for estimation of fractional log-normal stochastic volatility models using realized measures. arXiv:2010.04610, 2020.

- [11] Masaaki F. Volatility has to be rough. Quantitative Finance, 21(1):1–8, 2021.

- [12] M. Forde, M. Fukasawa, S. Gerhold, and B. Smith. The rough bergomi model as skew flattening/blow up and non-gaussian rough volatility, 2020.

- [13] M. Forde and B. Smith. The riemann-liouville field as a limit- sub, critical and super critical gmc, decompositions and explicit spectral expansions, 2020.

- [14] M. Fukasawa, T. Takabatake, and R. Westphal. Is volatility rough ? arXiv:1905.04852v2, 2019.

- [15] Y. V. Fyodorov, B. A. Khoruzhenko, and N. J. Simm. Fractional Brownian motion with Hurst index and the Gaussian Unitary Ensemble. The Annals of Probability, 44(4):2980 – 3031, 2016.

- [16] J. Gatheral, T. Jaisson, and M. Rosenbaum. Volatility is rough. Quantitative Finance, 18(6):933–949, 2018.

- [17] S. Ghashghaie, W. Breymann, J. Peinke, and P. Talkner. Turbulence and financial markets. In S. Gavrilakis, L. Machiels, and P. A. Monkewitz, editors, Advances in Turbulence VI, pages 167–170, Dordrecht, 1996. Springer Netherlands.

- [18] S. Ghashghaie, W. Breymann, J. Peinke, P. Talkner, and Y. Dodge. Turbulent cascades in foreign exchange markets. Nature, 381:767––770, 1996.

- [19] P. Hager and E. Neumann. The multiplicative chaos of fractional brownian fields. Technical report, 2021.

- [20] G. Livieri, S. Mouti, A. Pallavicini, and M. Rosenbaum. Rough volatility: Evidence from option prices. IISE Transactions, 50(9):767–776, 2018.

- [21] B. B. Mandelbrot, A. J. Fisher, and L. E. Calvet. A multifractal model of asset returns. Cowles Foundation Discussion Paper No. 1164, Sauder School of Business Working Paper, Available at SSRN, Sep 1997.

- [22] Garman M.B and Klass M.J. On the estimation of security price volatility from historical data. The Journal of Business, 53:67–78, 1980.

- [23] Y. Mishura and M. Zili. Gaussian processes. In Y. Mishura and M. Zili, editors, Stochastic Analysis of Mixed Fractional Gaussian Processes, pages 1–29. Elsevier, 2018.

- [24] J.F. Muzy and E. Bacry. Multifractal stationary random measures and multifractal random walks with log infinitely divisible scaling laws. Physical Review E, 66(5), Nov 2002.

- [25] J.F. Muzy, R. Baïle, and E. Bacry. Random cascade model in the limit of infinite integral scale as the exponential of a nonstationary 1/f noise: Application to volatility fluctuations in stock markets. Physical Review E, 87(4), 2013.

- [26] J.F. Muzy, J. Delour, and E. Bacry. Modelling fluctuations of financial time series: from cascade process to stochastic volatility model. Eur. Phys. J. B, 17(3):537–548, 2000.

- [27] E. Neuman and M. Rosenbaum. Fractional brownian motion with zero hurst parameter: a rough volatility viewpoint. Electronic Communications in Probability, 23, 2018.

- [28] M. Rambaldi, E. Bacry, and J.F. Muzy. Disentangling and quantifying market participant volatility contributions. Quantitative Finance, 19(10):1613–1625, 2019.

- [29] R. Rhodes and V. Vargas. Gaussian multiplicative chaos and applications: A review. Probability Surveys, 11:315–392, 05 2013.

- [30] G. Samorodnitsky and M.S. Taqqu. Stable Non-Gaussian Random Processes: Stochastic Models with Infinite Variance: Stochastic Modeling. 1994.