Optimal Estimation and Computational Limit of Low-rank Gaussian Mixtures

Abstract

Structural matrix-variate observations routinely arise in diverse fields such as multi-layer network analysis and brain image clustering. While data of this type have been extensively investigated with fruitful outcomes being delivered, the fundamental questions like its statistical optimality and computational limit are largely under-explored. In this paper, we propose a low-rank Gaussian mixture model (LrMM) assuming each matrix-valued observation has a planted low-rank structure. Minimax lower bounds for estimating the underlying low-rank matrix are established allowing a whole range of sample sizes and signal strength. Under a minimal condition on signal strength, referred to as the information-theoretical limit or statistical limit, we prove the minimax optimality of a maximum likelihood estimator which, in general, is computationally infeasible. If the signal is stronger than a certain threshold, called the computational limit, we design a computationally fast estimator based on spectral aggregation and demonstrate its minimax optimality. Moreover, when the signal strength is smaller than the computational limit, we provide evidences based on the low-degree likelihood ratio framework to claim that no polynomial-time algorithm can consistently recover the underlying low-rank matrix. Our results reveal multiple phase transitions in the minimax error rates and the statistical-to-computational gap. Numerical experiments confirm our theoretical findings. We further showcase the merit of our spectral aggregation method on the worldwide food trading dataset.

1 Introduction

The recent decade has witnessed a burgeoning demand in processing and analyzing large-scale matrix-variate data which routinely arise in diverse fields. In gene expression analysis, e.g., the BHL (brain, heart and lung) dataset (BHL, ; Mai et al., 2021), the measurement of gene expression on different types of tissues is often repeated for multiple times. The resultant observation for each tissue becomes a matrix and thus the cluster analysis is operated on matrix-valued observations. A multi-layer network (Le et al., 2018; Jing et al., 2021; Lyu et al., 2021; Paul and Chen, 2020) usually consists of multiple networks on the same set of vertices. Since each observed layer is equivalently represented as an adjacent matrix, problems such as community detection (Paul and Chen, 2020), layer clustering (Jing et al., 2021) and common probability matrix estimation (Le et al., 2018) are generally attacked by statistical analysis on a collection of adjacency matrices. Other notable examples include brain image clustering (Sun and Li, 2019; Wang et al., 2017), EEG data analysis (Hu et al., 2020; Gao et al., 2021), etc. Oftentimes, the dimensions of observed matrices are ultra-large or the number of matrix-valued observations is relatively small, which has motivated the exploration of hidden low-dimensional structures, e.g. sparsity and low-rankness, in matrix-valued observations. All the aforementioned works assumed, among others, certain types of low-rank structures for the underlying parameters of interest and have delivered fruitful outcomes in real-world applications.

Inspired by those foregoing works, throughout this paper, we assume that each matrix-valued observation has a low-rank expectation which might vary for different observations. Towards that end, several specific low-rank statistical models, tailored for concrete applications, and respective estimating procedures have been proposed. For instance, a mixture multi-layer stochastic block model (SBM) was introduced in Jing et al. (2021) for uncovering the global and local communities in multi-layer networks. At the core of this model is the assumption that every layer has a low-rank expected adjacency matrix. Their estimator was based on the (regularized) low-rank tensor decomposition. A special multi-layer SBM was proposed by Paul and Chen (2020) and estimated by a spectral method. In order to analyze the brain fMRI data, Sun and Li (2019) proposed a tensor Gaussian mixture model and designed an estimator via (fusedly-)truncated low-rank tensor decomposition. Despite these prior efforts, usually motivated by particular applications, on the low-rank estimates from a mixture of matrix-valued observations, many fundamental questions remain unanswered. What is the role and benefit of low-rankness? How do the sample size and signal strength (see the definition after eq.(2)) characterize the intrinsic difficulty, i.e., are there any phase transitions? What is the statistically optimal rate, which estimator can achieve the rate and is this estimator computationally feasible? What is the fastest error rate achievable by estimators requiring only polynomial-time complexity? This paper aims to answer all these questions and provides a complete picture for the statistical and computational limits in the low-rank estimation from a mixture of matrix-valued observations.

We now introduce the low-rank Gaussian mixture model (LrMM) to formalize the questions. For simplicity, we focus on the mixture of two components and will briefly discuss the case of multiple components in Section 7. The matrix is said to follow an isotropic matrix normal (Gupta and Nagar, 2018) distribution if , where represents the identity matrix and is a deterministic matrix. Clearly, this implies that is equal to in distribution where has i.i.d. standard normal entries. Denote222With a slight abuse of notation, we also denote the associated probability density function.

| (1) |

the symmetric mixture of two-component Gaussian mixture model. Then means that is sampled from and with probability both , respectively. Put it differently, equals in distribution with being a Rademacher random variable, called the label of , satisfying . Throughout the paper, we assume that has a small rank, i.e., . Note that, under model (1), the marginal expectation of is actually zero. The former claim of low-rank expectation in the last paragraph actually refers to the conditional expectation which is low-rank. We remark that the condition of equal prior probabilities is not essential and can be slightly relaxed. The assumption of symmetry of the two components is only for ease of exposition. If the two components have distinct mean matrices, say and , respectively, one can first estimate the average , subtract it from all observations and reduce the problem to the symmetric case. Similarly, the assumption of isotropic noise is relaxable as long as the covariance tensor is known. The case of unknown covariance is much more challenging (Davis et al., 2021; Bakshi et al., 2020; Belkin and Sinha, 2010; Cai et al., 2019; Ge et al., 2015; Moitra and Valiant, 2010) even in the vector case and is beyond the scope of the current paper.

Given i.i.d. observations sampled from the mixture distribution in (1), our goals are to estimate the latent low-rank matrix , establish the minimax error rates and design computationally efficient estimators. We assume meaning that there exist absolute constants satisfying . The parameter space of interest is, for any ,

| (2) |

where denotes the -th largest singular value of a matrix. For notational brevity, we shall write for short. The signal strength of low-rank models is usually determined by the smallest non-zero singular value (Koltchinskii and Xia, 2016; Zhang and Xia, 2018; Xia, 2021; Cheng et al., 2021; Gavish and Donoho, 2014). The set is the collection of all rank- matrices whose signal strength is of order . For simplicity, we only focus on the well-conditioned matrices, i.e., with a bounded condition number. The minimax error rate of estimating is defined by , where the infimum is taken over all possible estimator constructed from the i.i.d. observations and the loss function is with standing for the Frobenius norm. Note that, due to the symmetry of model (1), is estimable up to a sign flip.

If has a full rank with , model (1) reduces to the canonical two component isotropic Gaussian mixture model (GMM) in the dimension , which has been extensively investigated in the literature. See Balakrishnan et al. (2017); Chen (1995); Ho and Nguyen (2016a); Xu et al. (2016); Wu and Yang (2020) and references therein. For instance, Wu and Zhou (2019) proved that the minimax rate 333Note that there is an additional term derived in Wu and Zhou (2019) which is actually negligible if inspecting all other terms carefully. is

| (3) |

, and showed that a simple spectral method, together with a trivial estimate for the case of small , is minimax optimal. This rate implies intriguing phenomenons of phase transitions concerning the sample size and signal strength . For instance, if the sample size , their result reveals three different minimax rates: for , for and for . Interestingly, it also implies that non-trivial estimate is impossible, i.e., information-theoretically impossible, if the signal strength is smaller than . Undoubtedly, if is low-rank with , one can naturally foresee the existence of multiple phase transitions for the minimax error rates. Establishing these rates becomes more challenging for several reasons. On the methodological front, a naive spectral method cannot attain the minimax optimal rate and thus additional procedures are necessary. On the theoretical front, the low-rank structure dictates a smaller intrinsic dimension and brings about new behaviors to the phase transitions of the minimax error rates. See, e.g. Koltchinskii and Xia (2015); Ma and Wu (2015) and references therein. On the computational front, it is well recognized that the low-rankness sometimes bears a so-called statistical-to-computational gap (Barak and Moitra, 2016; Zhang and Xia, 2018) in the sense that there exist regimes where statistically optimal estimators can be computationally infeasible, e.g., requiring an exponential-time complexity.

The summary of our contributions is as follows. We establish the minimax rate of estimating the rank- matrix for the LrMM model that reads as

| (4) |

where the infimum is taken over all possible estimators, regardless of their computational feasibility. This rate implies that, when the sample size , it is information-theoretically impossible to estimate if the signal strength is smaller than . Under minimal conditions, we prove that the maximum likelihood estimator (MLE) can achieve the rate (4) up to a logarithmic factor. Unfortunately, there are no known polynomial-time algorithms with guaranteed performance to solve MLE. Earlier works (Tosh and Dasgupta, 2017; Sanjeev and Kannan, 2001) show that solving MLE is generally NP-hard. We then propose a computationally fast estimator based on spectral aggregation. This approach can be viewed as a modified method of second moment (Pearson, 1894; Wu and Yang, 2020) adapted with a spectral projection to leverage the low-rank structure. We prove that this computationally efficient estimator can achieve the minimax rate (4) as long as the signal strength is larger than , which is much stronger than the information-theoretical requirement for the minimal signal strength. This difference unveils the statistical-to-computational gap in LrMM. Lastly, we adopt the low-degree likelihood ratio framework (Kunisky et al., 2019) to conjecture that no polynomial-time estimator is consistent if is smaller than . The minimax rates, phase transitions and statistical-to-computational gaps are illustrated in Figure 1.

Our results are closely related yet crucially different from several existing works. In Chen et al. (2021), a low-rank mixture model was proposed for linear regression which is generally more challenging than our model (1). They designed a computationally efficient estimator but provided no results respecting the statistical optimality or computational limits. A multi-graph network model was introduced by Wang et al. (2019) which allows heterogeneous structure on each matrix-valued observation. However, their model has no mixture nature and there is no guarantee on minimax optimality. More recently, Jing et al. (2021) proposes a mixture multi-layer SBM and establishes the minimax error rate of spectral estimate only for the special regime when the sample size is smaller than and the signal strength, reflected by the network sparsity, is strong enough. In addition, our LrMM is directly related to low-rank tensor literature. By stacking the matrix observations slice by slice, we end up with a tensor of size whose expectation, under model (1), has a low Tucker rank . See, e.g., Zhang and Xia (2018); Jing et al. (2021) and references therein. Minimax rates for low-rank tensor denoising and noisy tensor completion have been investigated by Zhang and Xia (2018) and Xia et al. (2021), respectively. However, they both require the sample size to be of the same order of , which becomes unrealistic in the low-rank mixture model. Finally, it worths to remark that our bound (4) reduces to the minimax bound of GMM (3) if we let be full-rank. To see this, one can just replace and in our bound (4) by and , respectively.

The rest of paper is organized as follows. We establish the minimax lower bound in Section 2 and prove that the maximum likelihood estimator, albeit computationally infeasible in general, achieves the minimax optimal rates. A computationally fast estimator based on spectral aggregation is proposed in Section 3 which attains minimax optimal rates as long as the signal strength is strong. Section 4 justifies the statistical-to-computational gap by showing that there exists some regime where the MLE can attains minimax optimal rates but no-polynomial time algorithms can consistently recover the underlying low-rank matrix. We then showcase results of numerical simulations in Section 5, present a real-world data experiment in Section 6, and discuss open questions and potential directions in Section 7.

2 Maximum likelihood estimator and minimax optimality

We slightly abuse the notation and denote the probability density function of under the LrMM model (1). The family of density functions parameterized by is written as (note that we assume )

which is indexed by rank- matrices with the signal strength . Given observations sampled from , the maximum likelihood estimator (not necessarily unique) is defined by

| (5) |

While the MLE estimator (5) is generally NP-hard to compute, it often serves as a benchmark for understanding the information-theoretical limit of a statistical model.

We begin with the regime 444Here, stands for the standard big- notation up to a logarithmic factor., which falls into the typical low-dimensional setting555The low-dimensional setting here refers to the case that dimension is allowed to grow with sample size , while the order of still dominates.. The convergence rate of MLE in this regime has been thoroughly investigated for Gaussian mixture model. See, for instance, Leroux (1992); Van de Geer (1993); Chen (1995); Genovese and Wasserman (2000); Ghosal and Van Der Vaart (2001). The standard tool, e.g. Van de Geer (1993) and (Van de Geer, 2000, Theorem 7.4), establishes the convergence rate of MLE in the Hellinger distance defined by for two density functions and . According to this tool, it suffices to bound the bracketing entropy number of a class of square root density functions around the truth . While existing literature (Ho and Nguyen, 2016a, b; Maugis and Michel, 2011) have developed respective bracketing entropy bounds for Gaussian mixture model, they only focus on the fixed dimension and their method is inapplicable to matrix-variate observations with a planted low-rank structure. By a covering argument and the construction of bracket functions, we establish such a bracketing entropy bounds for LrMM and derive the upper bound in Hellinger distance for .

To bridge the density estimation and parameter estimation, we resort to a sharp characterization for the total variation distance (similarly, the Hellinger distance) between Gaussian mixture densities established recently by Davies et al. (2021).

Lemma 1.

(Lower bound of Hellinger distance) Let and be two matrices, and denote and the two density functions defined by (1). There exists absolute constants such that, if then

Otherwise

where .

Together with the upper bound of Hellinger distance and Lemma 1, we obtain the error rate of the maximum likelihood estimator when , namely the first part of Theorem 1.

However, the above argument fails when it comes to the regime 666Again, stands for the standard big- notation up to a logarithmic factor., corresponding to an ultra high-dimensional setting. The reason is that the minimax lower bound, as we will see later in Theorem 2, suggests that the optimal error rate should be of order , which can be larger than 1. Consequently, the Hellinger distance is no longer an appropriate metric777The error rate of other bounded metric, say, the Wasserstein distance considered in Doss et al. (2020), also becomes trivial when ., for instance, the lower bound in Lemma 1 becomes trivial. To this end, we turn to Kullback-Leibler (KL) divergence defined by . Though KL divergence is not a metric itself, in many cases its convergence also implies consistency of parameter estimate in some metric of interest (Van de Geer, 2000). Moreover, the KL divergence in its form is closely related to MLE and its unboundedness property is beneficial for our purpose since possibly diverges. By carefully characterizing the distribution of and exploiting the concentration inequality of suprema of an empirical process (Adamczak, 2008, Theorem 4), we are able to derive an upper bound for the KL divergence . We also establish the following lower bound relating KL divergence to the distance in the parameter space. Combining Lemma 2 with the upper bound of leads to the desired error rate in the regime , i.e., the second part of Theorem 1.

Lemma 2.

(Lower bound of KL divergence) Let and be two matrices, and denote and the two density functions defined by (1). There exists absolute constants such that if and , then

Collecting two pieces, the error rate of the maximum likelihood estimator is summarized in the following theorem.

Theorem 1.

Suppose and let denote the maximum likelihood estimator by (5).

-

(1)

If , then there exist absolute constants such that the following bound holds with probability at least ,

(6) If further assume , then

-

(2)

If , then there exist absolute constants such that if

, then the following bound holds with probability at least ,(7) And the following bound in expectation holds,

We note that the logarithmic factor in (6) emerges from the bracketing entropy bound and that in (7) arises from the tail inequality for suprema of empirical processes of unbounded functions. The high probability bound in the first part of Theorem 1 is proved without conditions on the sample size , the rank or on the signal strength . It suggests intriguing phase transitions in the regime . When , the MLE attains the rate , growing with respect to the rank , which is the best achievable rate even if the labels of observations are all known, namely in the oracle scenario. On the other hand, if , the MLE attains the rate that is free of the underlying rank . Moreover, a trivial estimate by attains the error rate . Therefore, the MLE becomes pointless if is smaller than , which is referred to as the information-theoretically impossible regime. In the second statement of Theorem 1, a more stringent condition is imposed on signal strength () for technical difficulty, though we believe that MLE could attain the optimal rate in a wider range of via more sophisticated analysis. On the other hand, as long as , a computationally efficient estimator (see Section 3) is already able to attain the optimal rate. As we intend to reveal the optimal estimation rate under different signal strength, we only appeal to MLE when the signal strength is not strong enough. Therefore, the technical condition of for MLE is not essential.

The next theorem demonstrates the minimax optimality of the MLE by establishing a matching minimax lower bound up to the logarithmic factor. We note that the minimax lower bound (8) is a statistical lower bound because it takes no considerations of the computational feasibility. In Section 3, we introduce a computationally fast estimator that achieves these lower bounds but requires much more stringent conditions.

Theorem 2.

There exists an absolute constant such that

| (8) |

where the infimum is taken over all possible estimators and .

3 Computationally efficient estimator by spectral aggregation

Since the MLE (5) is generally computationally infeasible, it is of crucial importance to design an estimator which is polynomial-time computable. While existing works have demonstrated the optimality of spectral method for both estimation (Wu and Zhou, 2019) and clustering (Löffler et al., 2019) under the GMM, it turns out that a naive spectral estimate is statistically sub-optimal for our LrMM and additional subsequent treatments are necessary.

For technical simplicity, we adopt the sample splitting in our estimating procedure. It will inevitably affect the constant factor in the error rate, e.g., the as in Theorem 1. Since our main interest concerns only the convergence rate in terms of the model parameters, we spare no efforts to improve the constant factor.

Without loss of generality, assume the sample size . We randomly split the original sample into four disjoint subsets of equal size, denoted by for . Our estimating procedure consists of three major steps:

-

-

Step 1 (Spectral initialization). Stack the observations column by column into a matrix , extract its leading left singular vector, denoted by . Then, construct the matrix and extract its left singular vector, denoted by .

-

-

Step 2 (Spectral refinement). Extract the top- left and right singular vectors of

(9) -

-

Step 3 (Aggregation). Denote the best rank- approximation of

(10) Compute the scaling factor by

The final estimator is defined by .

Due to eq. (10), we refer to this procedure as the spectral aggregation. Note that (10) is, in spirit, similar to the method of second moment as in Gaussian mixture model (Wu and Yang, 2020). The additional projection onto and serves the purpose of denoising to leverage the low-rank structure. In this regard, our estimating procedure can also be viewed as a method of projected moments. The spectral initialization in Step 1 is very similar to the tensor literature. See, for instance, Montanari and Richard (2014); Zhang and Xia (2018); Xia and Zhou (2019) and references therein. A crucial difference here is that the estimate relies on the estimate to ensure that they are properly correlated in the sense that is bounded away from zero, which is a critical requirement for the refinement step (9).

Note that the expectation of the RHS of eq. (10), with respect to the randomness of , is . Therefore, its best rank- approximation needs to scaled to serve as a valid estimator for . The quantity is an estimate of this scaling factor. The performance of the final estimator is guaranteed by the following theorem where we assume defined in (2) and .

Theorem 3.

There exist absolute constants such that if the signal strength and , then with probability at least ,

, if we further assume , then

By Theorem 2 and Theorem 3, we conclude that the estimator can attain the minimax optimal error rate as long as the signal strength is larger than , which we refer to as the strong signal phase. This is much more stringent than the information-theoretical limit suggested by the maximum likelihood estimator and minimax lower bound in Section 2.

4 Statistical and computational tradeoffs

Section 2 and Section 3 indicate the existence of a gap in the signal strengths required by the, in general, computationally infeasible maximum likelihood estimator and the computationally fast spectral-based estimator. Gap of this type is usually called the statistical-to-computational gap. In this section, we provide evidences claiming that no polynomial-time algorithm can consistently estimate if the signal strength is smaller than . Our evidence is built on the low-degree likelihood ratio framework for hypothesis testing (Kunisky et al., 2019; Löffler et al., 2020; Hopkins, 2018). This framework delivered convincing evidences justifying the statistical-to-computational gap for sparse Gaussian mixture model (Löffler et al., 2020) and tensor PCA model, and demonstrated the sharp phase transitions for the spiked Wigner matrix model (Kunisky et al., 2019).

The low-degree likelihood ratio framework aims to test two sequences of hypothesis. For our purpose, consider the following hypothesis testing:

| (11) |

where denotes the sample size. By observing i.i.d. matrices sampled from the mixture model (1), the interest is to test whether the data is pure noise or there is a planted low-rank matrix. Without loss of generality, it suffices to focus on the rank-one case since the “information” strength increases if the rank is larger and, as a result, the hypothesis testing becomes easier for larger ranks.

Classical textbook results, say, by Neyman-Pearson Lemma, dictate that the likelihood ratio test has preferable power and is uniformly most powerful under some scenarios. Direct computation of the likelihood ratio for testing (11) is rather involved due to the composite hypothesis in . For simplicity, under the alternative hypothesis, we impose a prior distribution on assuming that with a fixed and the entries of and independently taking the values and , respectively, with probability . Denote , treated as the alternative hypothesis, the distribution of under LrMM (1) with sampled from the aforementioned prior distribution. Note that, for brevity, we suppress the dependence of on . Let be the distribution of under the null hypothesis, i.e., each is sampled from LrMM (1) with . Instead of (11), we consider the following hypothesis testing

| (12) |

Denote the likelihood ratio, where is constructed by stacking data matrices. A well-recognized fact is that the two distributions and are statistically indistinguishable if remains bounded as . Here statistically indistinguishable means that no test can have both type I and type II error probabilities vanishing asymptotically.

Let denote the orthogonal projection of onto the linear subspace of polynomials of degree at most . Similarly, define . At the core of low-degree likelihood ratio framework is the following conjecture888We note that a recent work Zadik et al. (2021) introduces a very special counter-example to Conjecture 1. However, our LrMM is more closely related to the spiked matrix and tensor model where Conjecture 1 has contributed convincing evidences to the computational hardness. Therefore, we still postulate the correctness of Conjecture 1 for our LrMM., adapted to the matrix-variate case for our purpose. Here, a test taking value means rejecting the null hypothesis and takes value if the null hypothesis is not rejected.

Conjecture 1.

Consider and defined in (12). If there exists and for which , then there is no polynomial-time test such that the sum of type-I error and type-II error probabilities

Basically, Conjecture 1 means that the two distributions and are indistinguishable by polynomial-time algorithms if . Under the low-degree framework, we now state the computational lower bound of our signal strength for testing (12).

Theorem 4.

Consider and defined in (12). If , then .

By Theorem 4, conditioned on Conjecture 1, detecting the signal matrix in LrMM as in (12) becomes computationally hard as long as the signal strength is at a smaller order of . In principle, the estimation of signal matrix is at least as hard (computationally) as detection as in (12), as the latter one only concerns the mere existence thereof, and hence we would expect, at least, the same lower bound also holds for estimation problem in LrMM. Notably, if , LrMM reduces to the typical matrix perturbation model (Cai and Zhang, 2018; Xia, 2021) where there exists no statistical-to-computational gap and the signal strength requirement is both the statistical and computational limit. Interestingly, if is at the order of , the computational hardness occurs at the signal strength which coincides with the prior literature on spiked tensor model. See Zhang and Xia (2018); Kunisky et al. (2019) and references therein.

5 Numerical simulations

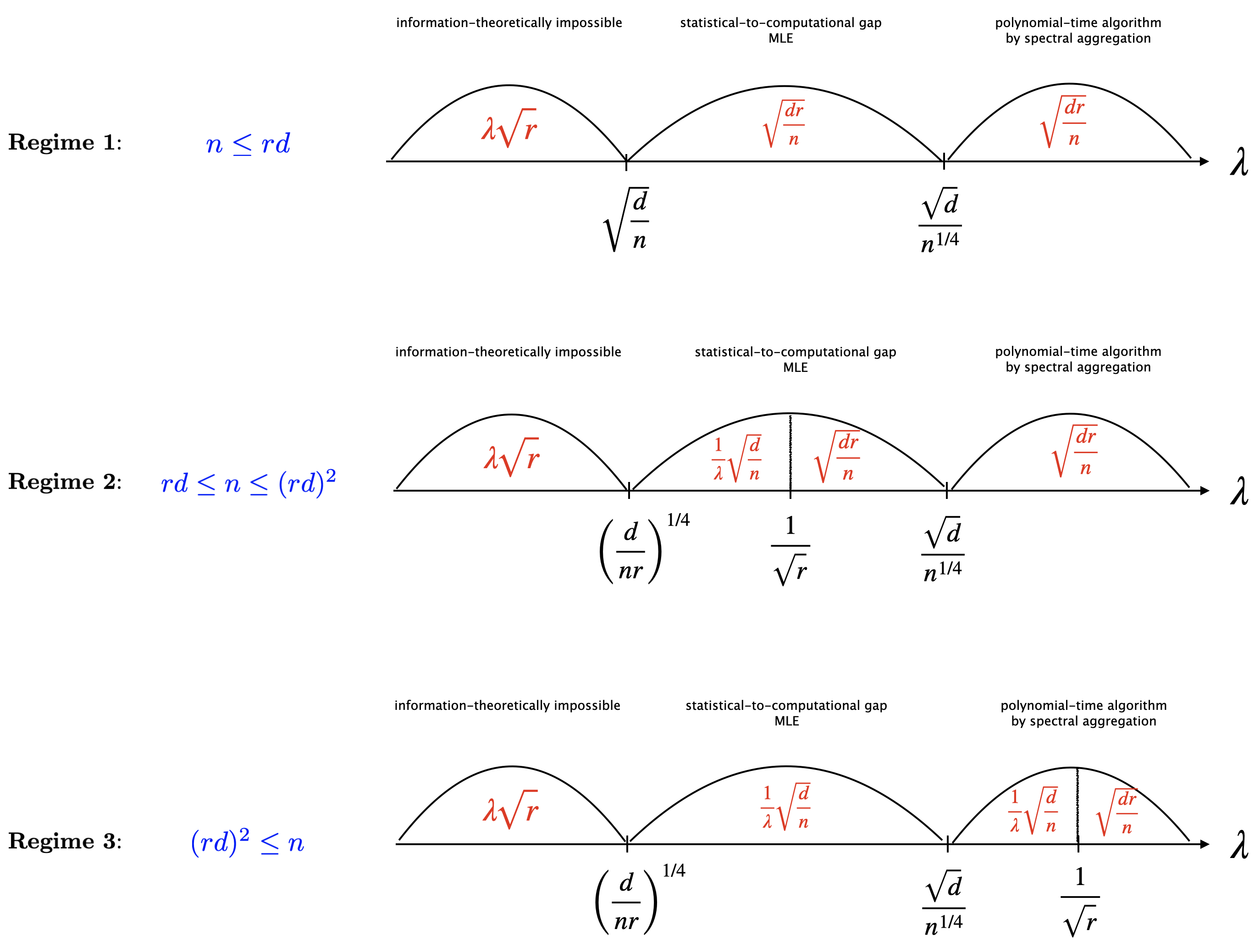

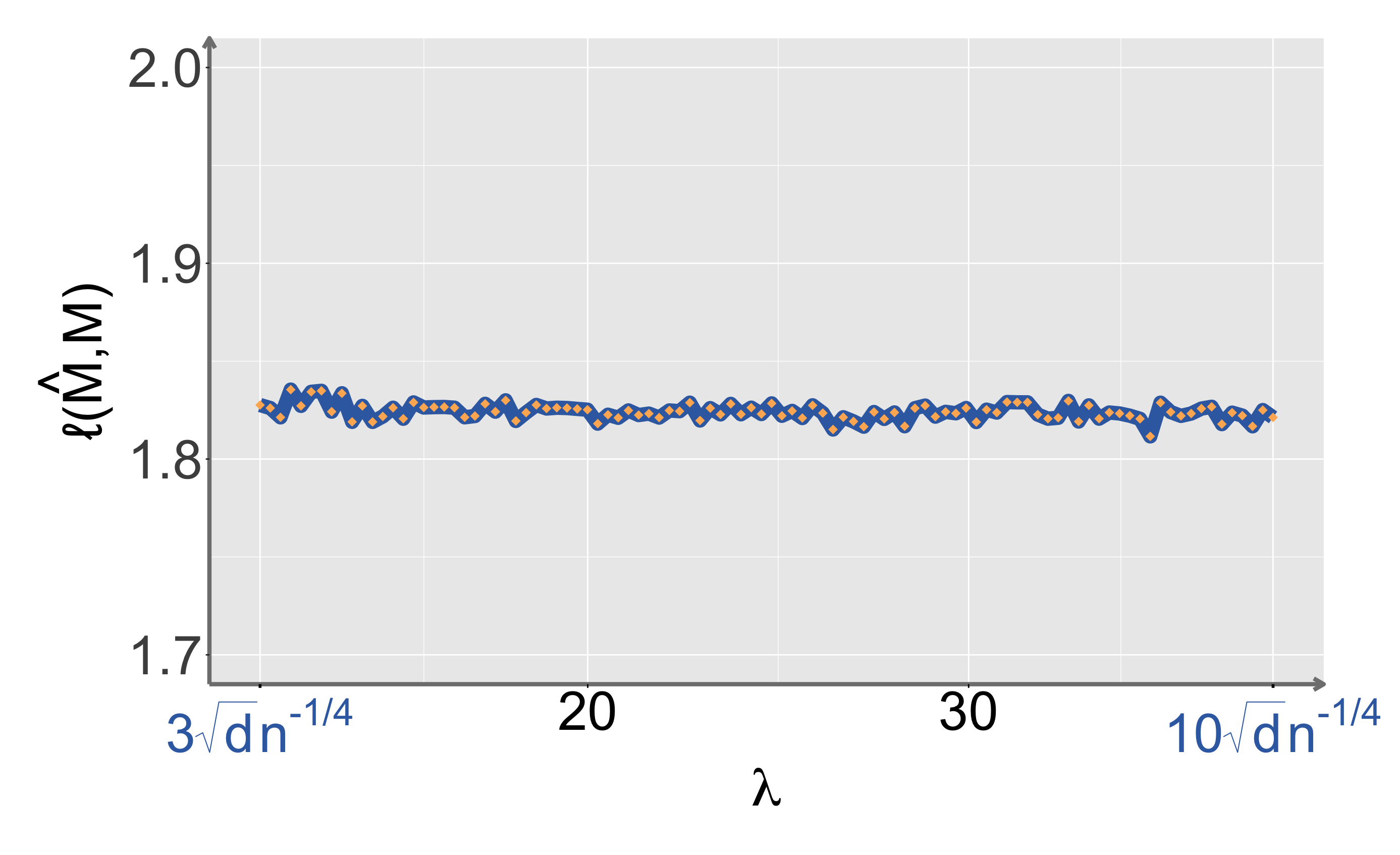

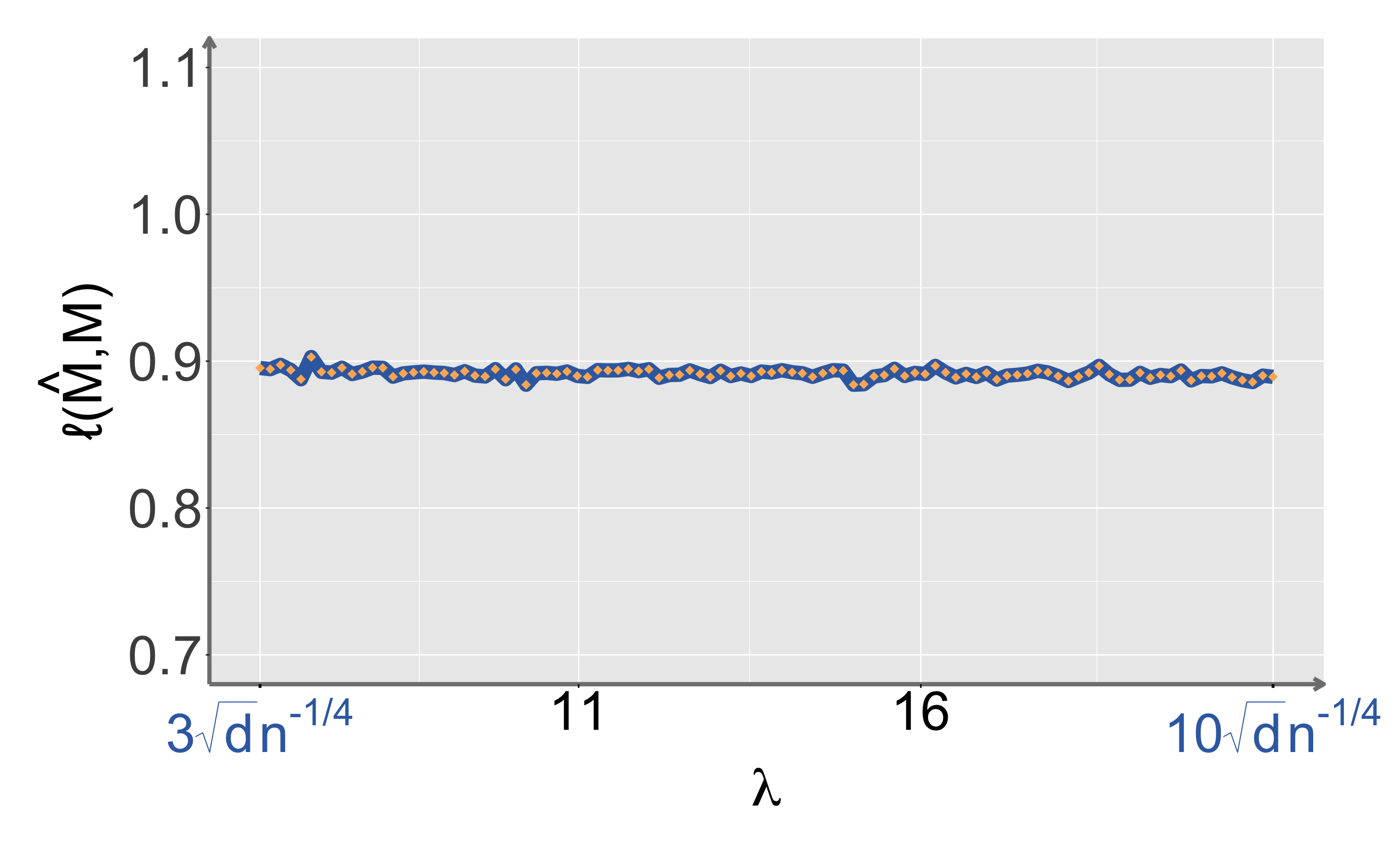

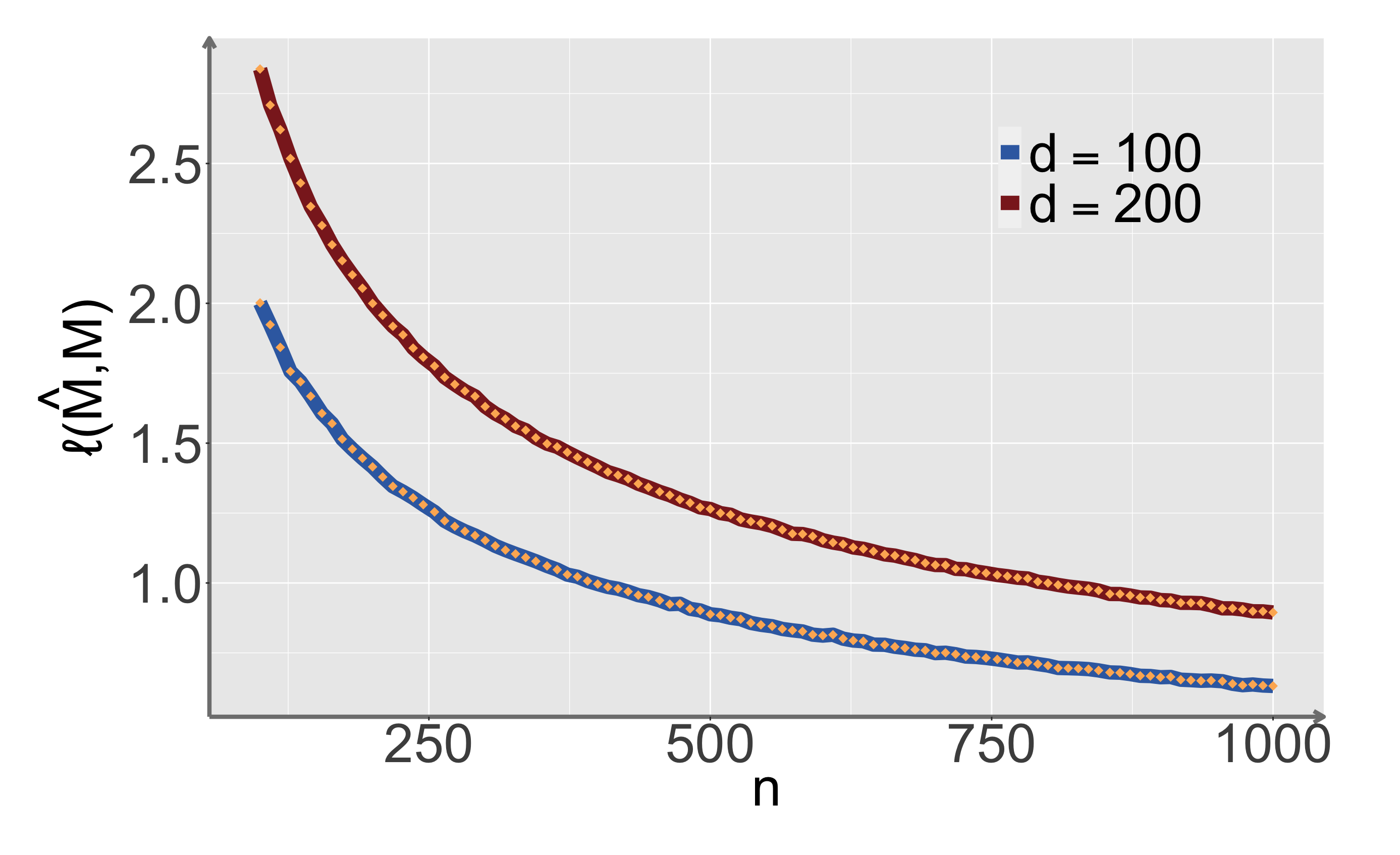

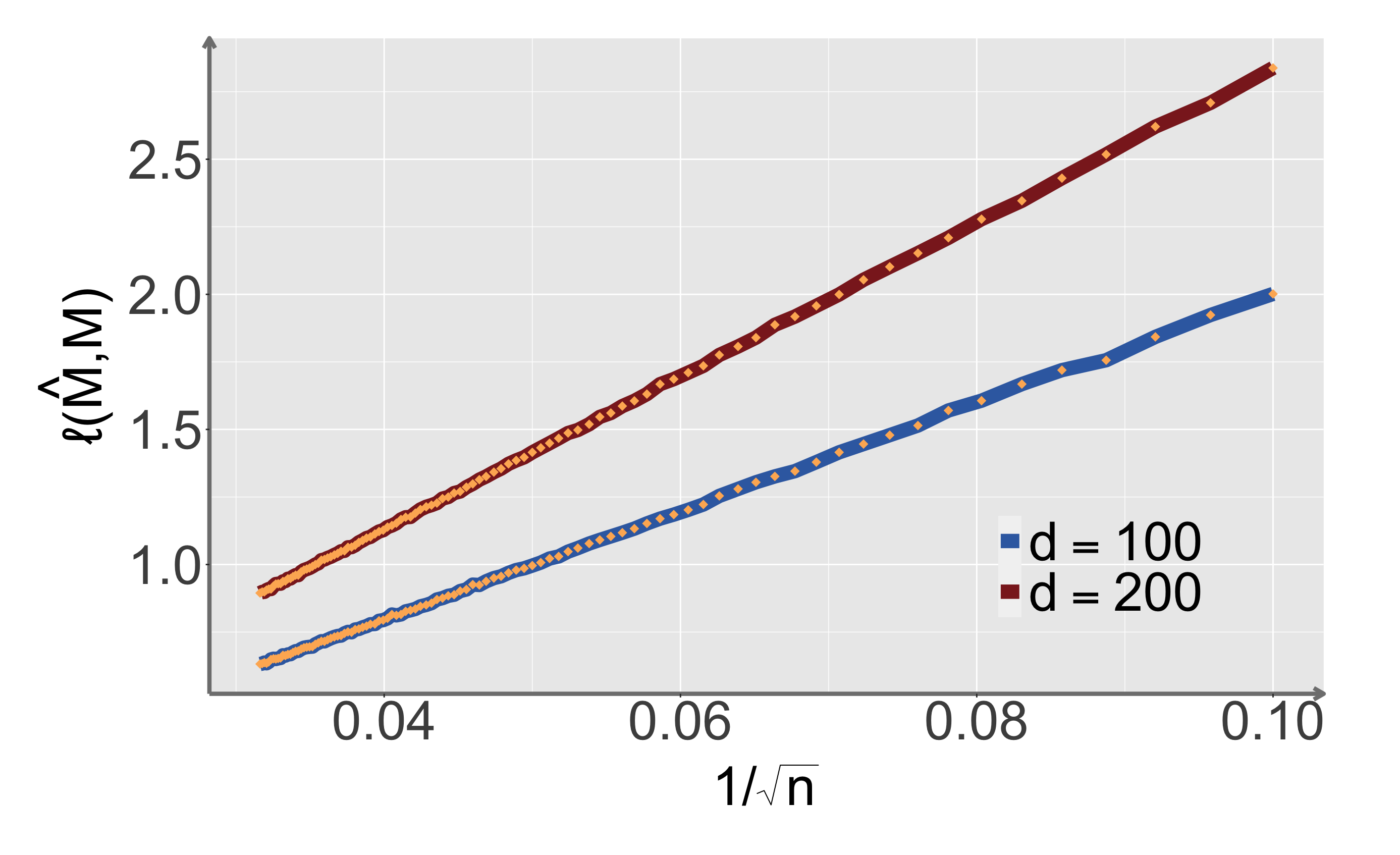

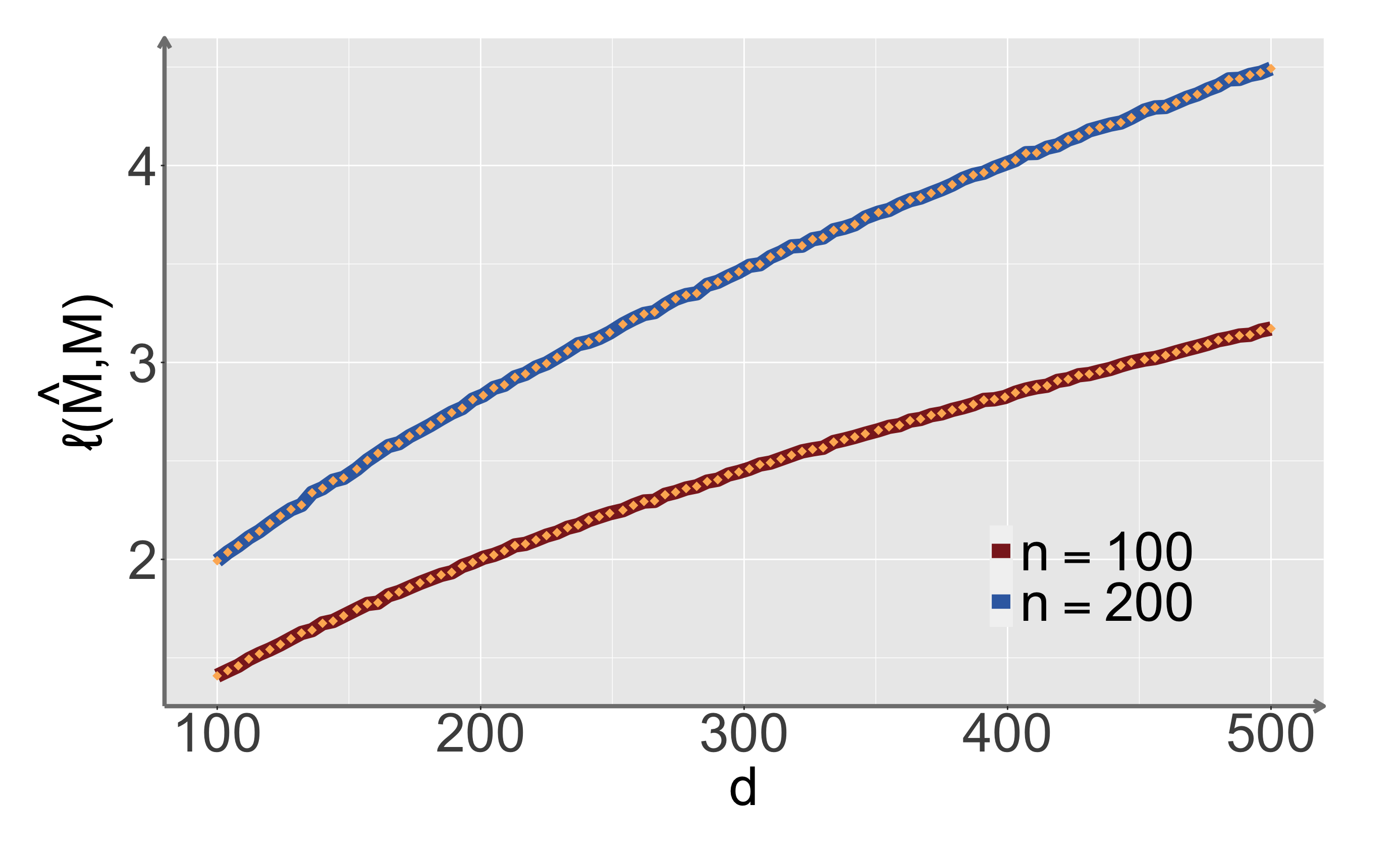

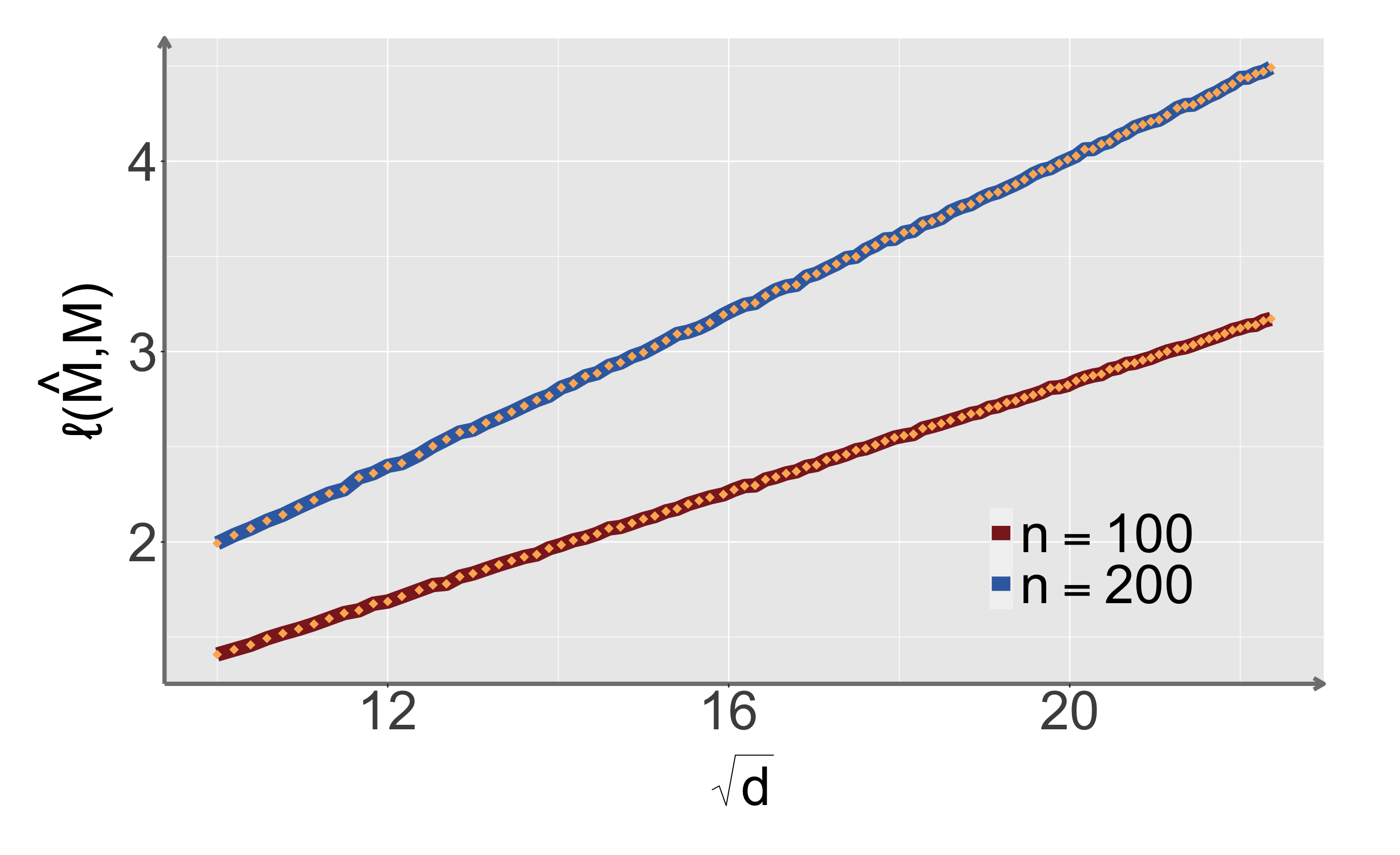

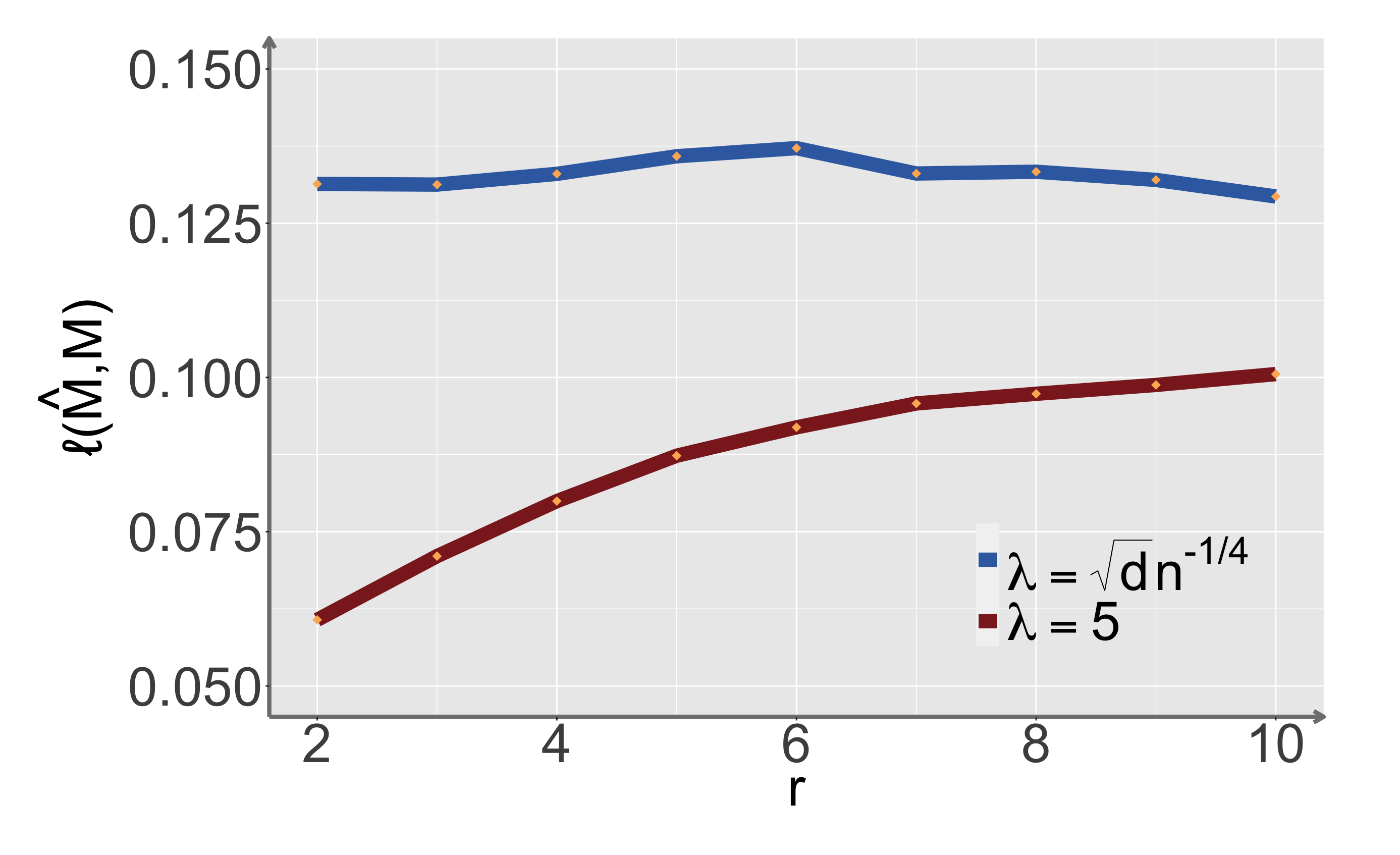

In this section, we present numerical experiments to confirm our theoretical findings in the strong signal phase and showcase the performance of our algorithm. Particularly, we apply the spectral aggregate algorithm on independent data matrices generated from LrMM model in (1), with a signal matrix of rank constructed as follows. We first generate two uniformly random orthonormal matrices and , say, by computing the column span (i.e. the image) of a random Gaussian random matrix with i.i.d. entries. Then we fix the smallest and the largest singular value to be and , respectively, and form a diagonal matrix where the values of the diagonal terms are equally spaced in a decreasing order. Finally we get our signal matrix . We study the effect of parameters on the error via varying one/two parameters while fixing the rest of them. In each experiment (for a given parameter group ), the value of the error is the average based on 100 independent simulations with the same signal matrix . As the aim of sample splitting step is to facilitate the theoretical analysis, we apply the spectral aggregation algorithm on all samples without sample splitting in all numerical experiments. For brevity, Regime 1 is referred to the case when , Regime 2 is referred to the case when and Regime 3 is referred to the case when . The information are summarized as follows:

-

•

Experiment 1: , , (Regime 1). is varying from to .

-

•

Experiment 2: , , (Regime 2). is varying from to .

-

•

Experiment 3: , , (Regime 3). is varying from to .

-

•

Experiment 4: , . is varying from to with .

-

•

Experiment 5: , . is varying from to with .

-

•

Experiment 6: , , (Regime 3). is varying from to .

In Experiment 1 & 2 (Regime 1 & 2), the error stays almost constant as increases. Both cases fall into the strong signal phase and an optimal rate of can be attained, suggested by Theorem 3. While in Experiment 3 (Regime 3) with the same range of , the phase transition effect is clearly demonstrated in the bottom panel of Figure 2: when varies from to , the optimal rate is linear in ; when , the optimal rate is again independent of .

In Experiment 4 & 5, we screen the effect of varying and , respectively in Figure 3. As expected, the error becomes smaller as grows (or decreases). The linearity between the error rate and (or ) can be verified in the right panels, which is in accordance with Theorem 3.

In Experiment 6, we let vary with other parameters fixed and focus on Regime 3, which is the most interesting case due to the phase transition effect in terms of rank . As shown in Figure 5, the error rate is constant in with and when , the error rate increases with .

6 Real data experiment

We present an application of our algorithm on a real-world dataset, which is a collection of multiple layers of worldwide food trading networks (De Domenico et al. (2015)), recording the trade flows of 30 food products between 99 countries. We pre-process the data the same as in Jing et al. (2021) and end up with a 3-rd order binary tensor of dimension . Each layer of this tensor represents the adjacency matrix of one specific type of food product , and nodes are different countries/regions which are common across all layers. As shown in Jing et al. (2021), the layers could be clustered into two groups, one of which mainly consists of raw or unprocessed food and another is made of processed food. We adopt this clustering result as ground truth and assume all layers are generated independently according to two expected adjacency matrices . Note that though throughout the paper the noise matrix is assumed to be Gaussian , we believe the spectral aggregation can be applied to more general setting (for instance, observations with sub-gaussian noise). Our goal is to recover and . To make it adapted to our framework (as mentioned in Section 1), we first construct centered observations , where is the sample average of adjacency matrices over all layers. Here, serves as an estimate of . Then we apply the spectral aggregation algorithm with rank to to get . It turns out that the final result is not sensitive to choice of rank . Finally we can construct and . To appropriately visualize our result, we rearrange the order of columns and rows of and in the same way as in Jing et al. (2021), which is based on the community labels estimated by tensor method therein, in order to have a glance of community structures. In Figure 6, the mean matrix in the left panel demonstrates a strong trend of global trading, while the other one shows the dominance of regional trading. These findings coincides with results in Jing et al. (2021), whereas we are estimating the difference of two center matrices instead of clustering all observations. Note that the results in Jing et al. (2021) require layer clustering before producing but our method does not.

7 Discussion

Our main focus in this paper is on the optimal estimation and computational limits for the two-component low-rank Gaussian mixtures. It is of great interest to investigate the minimax optimal estimation when the number of components is greater than two. Unfortunately, our spectral aggregation method is inapplicable and we cannot immediately see an easy generalization of the maximum likelihood estimator to the multi-component case. There are several possibilities. For instance, unlike the two-component case, it might be necessary to, at least partially, recover the latent labels before estimating the underlying low-rank components. Indeed, the linear regression low-rank mixture model (Chen et al., 2021) was treated by this way. However, it is well recognized that consistent clustering often requires a much stronger condition on the signal strength. See, for instance, Löffler et al. (2019); Wu and Zhou (2019) and references therein. For the two-component symmetric case as in model (1), consistent clustering requires a signal strength at least999To see this, one can simply assume the singular vectors and are available before hand. in the order of when is a constant, which can be much more stringent than the condition required by the spectral aggregation method in Regime 3. It therefore indicates another possibility: there might exist some method that can reliably estimate the multiple low-rank components without the prerequisite of meaningful clustering. We leave this for future works.

References

- (1) https://www.ncbi.nlm.nih.gov/sites/GDSbrowser?acc=GDS1083.

- Abramowitz and Stegun (1948) Milton Abramowitz and Irene A Stegun. Handbook of mathematical functions with formulas, graphs, and mathematical tables, volume 55. US Government printing office, 1948.

- Adamczak (2008) Radoslaw Adamczak. A tail inequality for suprema of unbounded empirical processes with applications to markov chains. Electronic Journal of Probability, 13:1000–1034, 2008.

- Bakshi et al. (2020) Ainesh Bakshi, Ilias Diakonikolas, He Jia, Daniel M Kane, Pravesh K Kothari, and Santosh S Vempala. Robustly learning mixtures of arbitrary gaussians. arXiv preprint arXiv:2012.02119, 2020.

- Balakrishnan et al. (2017) Sivaraman Balakrishnan, Martin J Wainwright, and Bin Yu. Statistical guarantees for the em algorithm: From population to sample-based analysis. The Annals of Statistics, 45(1):77–120, 2017.

- Barak and Moitra (2016) Boaz Barak and Ankur Moitra. Noisy tensor completion via the sum-of-squares hierarchy. In Conference on Learning Theory, pages 417–445. PMLR, 2016.

- Belkin and Sinha (2010) Mikhail Belkin and Kaushik Sinha. Toward learning gaussian mixtures with arbitrary separation. In COLT, pages 407–419, 2010.

- Cai and Zhang (2018) T Tony Cai and Anru Zhang. Rate-optimal perturbation bounds for singular subspaces with applications to high-dimensional statistics. The Annals of Statistics, 46(1):60–89, 2018.

- Cai et al. (2013) T Tony Cai, Zongming Ma, and Yihong Wu. Sparse pca: Optimal rates and adaptive estimation. The Annals of Statistics, 41(6):3074–3110, 2013.

- Cai et al. (2019) T Tony Cai, Jing Ma, and Linjun Zhang. Chime: Clustering of high-dimensional gaussian mixtures with em algorithm and its optimality. The Annals of Statistics, 47(3):1234–1267, 2019.

- Chen (1995) Jiahua Chen. Optimal rate of convergence for finite mixture models. The Annals of Statistics, pages 221–233, 1995.

- Chen et al. (2021) Yanxi Chen, Cong Ma, H Vincent Poor, and Yuxin Chena. Learning mixtures of low-rank models. IEEE Transactions on Information Theory, 2021.

- Cheng et al. (2021) Chen Cheng, Yuting Wei, and Yuxin Chen. Tackling small eigen-gaps: Fine-grained eigenvector estimation and inference under heteroscedastic noise. IEEE Transactions on Information Theory, 67(11):7380–7419, 2021.

- Davies et al. (2021) Sami Davies, Arya Mazumdar, Soumyabrata Pal, and Cyrus Rashtchian. Lower bounds on the total variation distance between mixtures of two gaussians. arXiv preprint arXiv:2109.01064, 2021.

- Davis et al. (2021) Damek Davis, Mateo Diaz, and Kaizheng Wang. Clustering a mixture of gaussians with unknown covariance. arXiv preprint arXiv:2110.01602, 2021.

- De Domenico et al. (2015) Manlio De Domenico, Vincenzo Nicosia, Alexandre Arenas, and Vito Latora. Structural reducibility of multilayer networks. Nature communications, 6(1):1–9, 2015.

- Do (2003) Minh N Do. Fast approximation of kullback-leibler distance for dependence trees and hidden markov models. IEEE signal processing letters, 10(4):115–118, 2003.

- Doss et al. (2020) Natalie Doss, Yihong Wu, Pengkun Yang, and Harrison H Zhou. Optimal estimation of high-dimensional location gaussian mixtures. arXiv preprint arXiv:2002.05818, 2020.

- Gao et al. (2021) Xu Gao, Weining Shen, Liwen Zhang, Jianhua Hu, Norbert J Fortin, Ron D Frostig, and Hernando Ombao. Regularized matrix data clustering and its application to image analysis. Biometrics, 77(3):890–902, 2021.

- Gavish and Donoho (2014) Matan Gavish and David L Donoho. The optimal hard threshold for singular values is . IEEE Transactions on Information Theory, 60(8):5040–5053, 2014.

- Ge et al. (2015) Rong Ge, Qingqing Huang, and Sham M Kakade. Learning mixtures of gaussians in high dimensions. In Proceedings of the forty-seventh annual ACM symposium on Theory of computing, pages 761–770, 2015.

- Genovese and Wasserman (2000) Christopher R Genovese and Larry Wasserman. Rates of convergence for the gaussian mixture sieve. The Annals of Statistics, 28(4):1105–1127, 2000.

- Ghosal and Van Der Vaart (2001) Subhashis Ghosal and Aad W Van Der Vaart. Entropies and rates of convergence for maximum likelihood and bayes estimation for mixtures of normal densities. Annals of Statistics, pages 1233–1263, 2001.

- Golub and van Loan (2013) Gene H. Golub and Charles F. van Loan. Matrix Computations. JHU Press, fourth edition, 2013. ISBN 1421407949 9781421407944. URL http://www.cs.cornell.edu/cv/GVL4/golubandvanloan.htm.

- Gupta and Nagar (2018) Arjun K Gupta and Daya K Nagar. Matrix variate distributions, volume 104. CRC Press, 2018.

- Ho and Nguyen (2016a) Nhat Ho and XuanLong Nguyen. Convergence rates of parameter estimation for some weakly identifiable finite mixtures. The Annals of Statistics, 44(6):2726–2755, 2016a.

- Ho and Nguyen (2016b) Nhat Ho and XuanLong Nguyen. On strong identifiability and convergence rates of parameter estimation in finite mixtures. Electronic Journal of Statistics, 10(1):271–307, 2016b.

- Hopkins (2018) Samuel Hopkins. Statistical inference and the sum of squares method. PhD thesis, Cornell University, 2018.

- Hu et al. (2020) Wei Hu, Weining Shen, Hua Zhou, and Dehan Kong. Matrix linear discriminant analysis. Technometrics, 62(2):196–205, 2020.

- Jing et al. (2021) Bing-Yi Jing, Ting Li, Zhongyuan Lyu, and Dong Xia. Community detection on mixture multilayer networks via regularized tensor decomposition. The Annals of Statistics, 49(6):3181–3205, 2021.

- Koltchinskii and Lounici (2017) Vladimir Koltchinskii and Karim Lounici. Concentration inequalities and moment bounds for sample covariance operators. Bernoulli, 23(1):110–133, 2017.

- Koltchinskii and Xia (2015) Vladimir Koltchinskii and Dong Xia. Optimal estimation of low rank density matrices. J. Mach. Learn. Res., 16(53):1757–1792, 2015.

- Koltchinskii and Xia (2016) Vladimir Koltchinskii and Dong Xia. Perturbation of linear forms of singular vectors under gaussian noise. In High Dimensional Probability VII, pages 397–423. Springer, 2016.

- Koltchinskii et al. (2011) Vladimir Koltchinskii, Karim Lounici, and Alexandre B Tsybakov. Nuclear-norm penalization and optimal rates for noisy low-rank matrix completion. The Annals of Statistics, 39(5):2302–2329, 2011.

- Kunisky et al. (2019) Dmitriy Kunisky, Alexander S Wein, and Afonso S Bandeira. Notes on computational hardness of hypothesis testing: Predictions using the low-degree likelihood ratio. arXiv preprint arXiv:1907.11636, 2019.

- Laurent and Massart (2000) Beatrice Laurent and Pascal Massart. Adaptive estimation of a quadratic functional by model selection. Annals of Statistics, pages 1302–1338, 2000.

- Le et al. (2018) Can M Le, Keith Levin, and Elizaveta Levina. Estimating a network from multiple noisy realizations. Electronic Journal of Statistics, 12(2):4697–4740, 2018.

- Ledoux and Talagrand (1991) Michel Ledoux and Michel Talagrand. Probability in Banach Spaces: isoperimetry and processes, volume 23. Springer Science & Business Media, 1991.

- Leroux (1992) Brian G Leroux. Consistent estimation of a mixing distribution. The Annals of Statistics, pages 1350–1360, 1992.

- Löffler et al. (2019) Matthias Löffler, Anderson Y Zhang, and Harrison H Zhou. Optimality of spectral clustering in the gaussian mixture model. arXiv preprint arXiv:1911.00538, 2019.

- Löffler et al. (2020) Matthias Löffler, Alexander S Wein, and Afonso S Bandeira. Computationally efficient sparse clustering. arXiv preprint arXiv:2005.10817, 2020.

- Lyu et al. (2021) Zhongyuan Lyu, Dong Xia, and Yuan Zhang. Latent space model for higher-order networks and generalized tensor decomposition. arXiv preprint arXiv:2106.16042, 2021.

- Ma and Wu (2015) Zongming Ma and Yihong Wu. Volume ratio, sparsity, and minimaxity under unitarily invariant norms. IEEE Transactions on Information Theory, 61(12):6939–6956, 2015.

- Mai et al. (2021) Qing Mai, Xin Zhang, Yuqing Pan, and Kai Deng. A doubly enhanced em algorithm for model-based tensor clustering. Journal of the American Statistical Association, pages 1–15, 2021.

- Maugis and Michel (2011) Cathy Maugis and Bertrand Michel. A non asymptotic penalized criterion for gaussian mixture model selection. ESAIM: Probability and Statistics, 15:41–68, 2011.

- Moitra and Valiant (2010) Ankur Moitra and Gregory Valiant. Settling the polynomial learnability of mixtures of gaussians. In 2010 IEEE 51st Annual Symposium on Foundations of Computer Science, pages 93–102. IEEE, 2010.

- Montanari and Richard (2014) Andrea Montanari and Emile Richard. A statistical model for tensor pca. arXiv preprint arXiv:1411.1076, 2014.

- Paul and Chen (2020) Subhadeep Paul and Yuguo Chen. Spectral and matrix factorization methods for consistent community detection in multi-layer networks. The Annals of Statistics, 48(1):230–250, 2020.

- Pearson (1894) Karl Pearson. Contributions to the mathematical theory of evolution. Philosophical Transactions of the Royal Society of London. A, 185:71–110, 1894.

- Sanjeev and Kannan (2001) Arora Sanjeev and Ravi Kannan. Learning mixtures of arbitrary gaussians. In Proceedings of the thirty-third annual ACM symposium on Theory of computing, pages 247–257, 2001.

- Sun and Li (2019) Will Wei Sun and Lexin Li. Dynamic tensor clustering. Journal of the American Statistical Association, 114(528):1894–1907, 2019.

- Tosh and Dasgupta (2017) Christopher Tosh and Sanjoy Dasgupta. Maximum likelihood estimation for mixtures of spherical gaussians is np-hard. J. Mach. Learn. Res., 18:175–1, 2017.

- Van de Geer (1993) Sara Van de Geer. Hellinger-consistency of certain nonparametric maximum likelihood estimators. The Annals of Statistics, pages 14–44, 1993.

- Van de Geer (2000) Sara Van de Geer. Empirical Processes in M-estimation, volume 6. Cambridge university press, 2000.

- Van Der Vaart et al. (1996) Aad W Van Der Vaart, Adrianus Willem van der Vaart, Aad van der Vaart, and Jon Wellner. Weak convergence and empirical processes: with applications to statistics. Springer Science & Business Media, 1996.

- Vershynin (2010) Roman Vershynin. Introduction to the non-asymptotic analysis of random matrices. arXiv preprint arXiv:1011.3027, 2010.

- Wainwright (2019) Martin J Wainwright. High-dimensional statistics: A non-asymptotic viewpoint, volume 48. Cambridge University Press, 2019.

- Wang et al. (2019) Lu Wang, Zhengwu Zhang, and David Dunson. Common and individual structure of brain networks. The Annals of Applied Statistics, 13(1):85–112, 2019.

- Wang et al. (2017) Xiao Wang, Hongtu Zhu, and Alzheimer’s Disease Neuroimaging Initiative. Generalized scalar-on-image regression models via total variation. Journal of the American Statistical Association, 112(519):1156–1168, 2017.

- Wu and Yang (2020) Yihong Wu and Pengkun Yang. Optimal estimation of gaussian mixtures via denoised method of moments. The Annals of Statistics, 48(4):1981–2007, 2020.

- Wu and Zhou (2019) Yihong Wu and Harrison H Zhou. Randomly initialized em algorithm for two-component gaussian mixture achieves near optimality in iterations. arXiv preprint arXiv:1908.10935, 2019.

- Xia (2021) Dong Xia. Normal approximation and confidence region of singular subspaces. Electronic Journal of Statistics, 15(2):3798–3851, 2021.

- Xia and Zhou (2019) Dong Xia and Fan Zhou. The sup-norm perturbation of hosvd and low rank tensor denoising. The Journal of Machine Learning Research, 20(1):2206–2247, 2019.

- Xia et al. (2021) Dong Xia, Ming Yuan, and Cun-Hui Zhang. Statistically optimal and computationally efficient low rank tensor completion from noisy entries. The Annals of Statistics, 49(1):76–99, 2021.

- Xu et al. (2016) Ji Xu, Daniel Hsu, and Arian Maleki. Global analysis of expectation maximization for mixtures of two gaussians. arXiv preprint arXiv:1608.07630, 2016.

- Zadik et al. (2021) Ilias Zadik, Min Jae Song, Alexander S Wein, and Joan Bruna. Lattice-based methods surpass sum-of-squares in clustering. arXiv preprint arXiv:2112.03898, 2021.

- Zhang and Xia (2018) Anru Zhang and Dong Xia. Tensor svd: Statistical and computational limits. IEEE Transactions on Information Theory, 64(11):7311–7338, 2018.

Appendix A Proofs for main results

A.1 Proof of Theorem 1

For technical reasons discussed in Section 2, we split our proof into two cases, corresponding to the first and second statement in Theorem 1.

Case 1:

In this regime, the standard tool to establish the convergence rate of MLE is applicable. To this end, we need to introduce the following notations. Define

and for any small , define a Hellinger ball centered at with radius by

We refer to as the -bracketing entropy of under metric with Lebesgue measure and view as the entropy integral of , which is defined as

Now we state Theorem 7.4 in Van de Geer (2000) (adapted to our notation), which establishes the rate of convergence of MLE.

Lemma 3 (Van de Geer (2000)).

Take in such a way that is a non-increasing function of . Then for a universal constant , and for

we have for all

A combination of Lemma 1 and Lemma 3 implies that the convergence rate of would entail an upper bound on the -bracketing entropy . Notice that for any ,

| (13) |

where (a) is due to , (b) follows from the definition of Hellinger distance and (c) is due to the following fact (cf. Lemma 4.2 in Van de Geer (2000), Ho and Nguyen (2016a)): for any

In view of (A.1), it suffices to bound . The following lemma characterize the size of bracketing entropy of .

Lemma 4.

Assume then we have

Using relation (A.1) and Lemma 4 we can arrive at

Now we can take for some absolute constant and , then we have is a non-increasing function of and that

By Lemma 3, with probability at least we have

It suffices to use Lemma 1 to connect the density estimation and parameter estimation. Notice that . By Lemma 1, if , with probability at least :

If , note that in this case (), we have with probability at least :

implying that . Combining two pieces we conclude that with probability at least :

We can further have a bound in expectation:

provided that .

Case 2:

In this regime, our ultimate goal is to have with high probability and in expectation and hence we can assume for some absolute constant (otherwise we have the desired result). Without loss of generality, we assume . Unlike Case 1, we resort to KL divergence instead of Hellinger distance to establish the convergence rate. Let denote the distribution of (1) and recall the definition of KL divergence, for any we have

Note that for fixed and , we simply have for . On the other hand, by the definition of the maximum likelihood estimator , we have

Therefore, we can have that

| (14) |

Now we give an upper bound of RHS of (14). To this end, we consider a ball in with radius , i.e., . Our aim is to bound the following quantity:

Observe that

By log-sum-exp inequality, we have

Hence we have

which implies , where

To get a high probability bound for , we first upper bound its expectation. By symmetrization (see, e.g., in (Van Der Vaart et al., 1996, Lemma 2.3.1)), we have

where are independent Rademacher random variables, which is independent of . Denote , for any we have

which means is -Lipschitz in . By comparison theorem ((Ledoux and Talagrand, 1991, Theorem 4.12)), we deduce that

Hence we proceed as

where in (a) we’ve used , in (b) we have a simple bound for by Jensen’s inequality, and (c) is due to the assumption . Define , notice that

Observe that , we have , the last inequality is due to in this regime. Moreover, by Lemma 2.2.2 in Van Der Vaart et al. (1996), we have

It suffices to note that for each ,

where in the last inequality we’ve used and . By random matrix theory, we know and is sub-gaussian, then . Hence

Now we can invoke concentration inequality for suprema of empirical processes of unbounded functions (Adamczak, 2008, Theorem 4), we have for any :

| (15) |

Note that (15) only holds for any given . Consider any , let for with , then . By construction, for any , we have . Hence for fixed , (15) holds for any up to change in constants and . Take a union bound over all , we have (15) holds for any and any . Combined with (14), we conclude that

| (16) |

where the last inequality holds with probability at least , due to the facts that . Since and in this regime, it turns out that we can apply Lemma 2 to get a lower bound of , hence we have with probability at least that

Finally, we can have a bound in expectation

given that . ∎

A.2 Proof of Theorem 3

In the proof, we consider the conditional model with sample splitting, i.e., for and . Let denote the thin SVD of the signal matrix and recall that .

Step 1:

Denote . A key observation is that is also the leading eigenvector of . Then we have

| (17) |

where

Note that () is a () matrix of independent centered Gaussian entries with variance , then by random matrix theory (e.g. Vershynin (2010)) with probability at least , we have:

Furthermore, since

where is the -th column of . By concentration of sample covariance operator (e.g. Koltchinskii and Lounici (2017)), we have with probability at least :

By (17) and eigenvalue perturbation theory (e.g. Corollary 8.1.6 in Golub and van Loan (2013)), we have101010With slight abuse of notation, we use to denote the -th largest eigenvalue of a given matrix, while ’s themselves are singular values of .

Therefore, we obtain

| (18) |

Hence with probability at least we have

| (19) |

where the last inequality holds provided that for some large absolute constant .

Step 2:

Observe that is the leading eigenvector of and we have the following decomposition:

| (20) |

where

Due to the independence of and , we conclude that , hence with probability at least :

Notice that , where and ’s are independent. Again, by concentration of sample covariance operator, with probability at least :

Therefore, (20) and eigenvalue perturbation theory imply that

Combined with the decomposition (20), we can arrive at

| (21) |

Thus, we get

| (22) |

with probability at least , provided that .

Step 3:

We proceed our analysis by conditioning on the event . Observe that

| (23) |

where

Now we give an upper bound for . By random matrix theory we know with probability at least :

Next, notice that , we have with probability at least :

It remains to bound . Notice the following decomposition:

where is the projection matrix onto the column space of and is the projection matrix onto orthogonal complement of the column space of . Since , by concentration for chi-square random variable with degrees of freedom (see Laurent and Massart (2000)), we have with probability at least :

By property of Gaussian matrices we have , where and is independent of . Hence we have

| (24) |

In addition, by concentration for chi-square random variable we have with probability at least . Combined with (24), we arrive at

with probability at least . Similar arguments can be applied to and . Collecting four parts we can bound the last term of as

| (25) |

with probability at least . Hence we have the following bound for with probability at least :

| (26) |

For any , denote is the -th largest singular value of and the corresponding left and right singular vectors. By (A.2) and perturbation theory for singular values we have

| (27) |

By definition of singular value and singular vectors, we have that

which implies

| (28) |

Using (22), it follows that with probability at least such that for all :

| (29) |

given that . Notice that this implies with overwhelming probability, we have

-

1.

-

2.

share the same sign with

As a consequence, with probability at least . These facts will be used in the following derivations.

Step 4:

We proceed by conditioning on the event . Consider the rank- approximation of , which admits the following decomposition:

| (30) |

where

Similar to that in step 3, we need to upper bound , the spectral norm of the perturbation term. The following bound is clear, which holds with probability at least :

Due to the rotation invariance of Gaussian and the orthogonality of ’s and ’s, we have with probability at least :

The following decomposition is similar to that in step 3:

| (31) |

By the property of Gaussian matrices, we have

where are independent matrices of dimension with i.i.d standard normal entries. Hence

The following lemma gives the concentration inequality of the above term.

Lemma 5.

Let be independent matrices with i.i.d standard normal entries. Then there exists a constant such that, for all , with probability at least :

By Lemma 5, if , we take , then we have with probability at least , provided that . If , we can take , then we have with probability at least , provided that . In summary, we have with probability at least :

In addition, we have , where and is independent of . Hence we have

Note that by concentration for chi-square random variable with probability at least . Then we can conclude that with probability at least :

The bounds for and can be obtained similarly. We have with probability at least :

| (32) |

Step 5:

Again, we continue on the event . In this step, we first construct , which is an estimator for the pre-factor of the signal part in (A.2). Notice that

| (33) | ||||

| (34) |

The second term , with being standard normal. Therefore, with probability at least :

The third term , where , hence we have with probability at least :

Therefore, we have with probability at least :

where we’ve used the fact . Hence by definition of , with probability at least :

| (35) |

The concentration inequalities of second and third term of (33) also imply that with probability at least :

| (36) |

Since the RHS of (36) is of order , we have with probability at least . Next, denote , the left and right leading singular vectors of, then the best rank- approximation is given by

The error of low-rank approximation is characterized by the perturbation term, given by the following lemma.

Lemma 6.

Consider a rank- matrix with its thin-SVD form , where and , , let be a perturbation matrix and . Denote the best rank- approximation of . Suppose that , then there exists some absolute constant such that

By Lemma 6, we have

Recall that . Denote , hence we have the following bound

| (37) |

Using (32) and (36), the first term can be bounded with probability at least :

Using (36), the second term can be bounded with probability at least :

where we’ve used the fact . Take union bound over all events that we’ve conditioned on in previous steps, we conclude that with probability at least :

| (38) |

Bound in expectation:

Denote the event . Then we have the following bound in expectation:

| (39) |

Note that by Von Neumann’s trace inequality, we have

| (40) |

Since is a rank- projection of and is lower bounded by , we have the following upper bound using (40):

| (41) |

Now we turn to bound , note that by definition we have

| (42) |

The first term of (A.2) can be bounded as

The second term of (A.2) can be bounded as

For the last term of (A.2), recall the decomposition (31), we have

Similar bounds hold for and . It remains to find . For simplicity, denote , then using Lemma 5 we can get

Hence we can conclude that

| (43) |

provided that . By (41), we have

Hence

Then (39) implies that

provided that and .

A.3 Proof of Theorem 2

The main idea is to construct a set of sufficiently dissimilar hypotheses to apply Fano’s method. To this end, we fix some and consider the ball centered at with radius of under the chordal Frobenius-norm metric :

By Lemma 1 in Cai et al. (2013) and the equivalence between and , we have for any , there exists , a packing of such that for some absolute constant :

Denote . Fix with and , we can construct for . Notice that

Let denote the distribution of and let denote the distribution of , i.e, the -th model parametrized by for . When , since has a Rademacher prior, using the log-sum inequality (see, e.g., Do (2003)) we have

When , by Lemma 27 in Wu and Zhou (2019), there exists a universal constant , such that for any :

which implies that

Hence we have

By Fano’s lower bound on minimax risk (see, e.g., Proposition 15.12 in Wainwright (2019)), we have

By choosing for some large absolute constant and , we can guarantee that . Hence

∎

A.4 Proof of Theorem 4

Denote the prior distribution for defined in (12) as , where is the latent label vector. Let be two independent copies from prior distribution . By Theorem 2.6 in Kunisky et al. (2019), we have the following formula for under the additive Gaussian noise model:

The last inequality is due to the fact that in distribution equals to the sum of i.i.d. Rademacher random variables, denoted by , and hence for odd . Hence we have

| (44) |

Moreover, , where for are two independent copies of i.i.d. Rademacher random variables. Since the even moment of standard normal is lower bounded by , denote i.i.d. standard normal random variables by and then we have the following simple bound for the combination number:

Hence we have

| (45) |

Combining (44) and (45), we arrive at

Notice that

provided that . Together with , we have

∎

Appendix B Proofs for technical lemmas

B.1 Proof of Lemma 1

Our result is an application of the following lemma.

Lemma 7 (Theorem 1 in Davies et al. (2021)).

Define

For , define sets , , and vectors for . Let with being the span of the vectors . If and , then

and otherwise, we have that

In our setting, , , and . For any , we have , , and . Notice that always holds. By Lemma 7, if , then

Otherwise, we have

The result immediately follows by noting that the total variation distance is bounded by Hellinger distance.

B.2 Proof of Lemma 2

By definition of KL divergence, we have

where . By log-sum-exp inequality, we have

It follows that

Recall that , and for brevity denote the expectation over . Then we have that

where the third equality is due to and denotes the cumulative distribution function (cdf) of standard normal. Likewise, we obtain that

Thus we have that

| (46) |

Without loss of generality, we assume . Using the upper and lower bound for cdf of standard normal (see, e.g., Abramowitz and Stegun (1948)), we obtain

| (47) |

| (48) |

It follows from (B.2) (47) and (48) that

where . Observe that

Now we need to show

| (49) |

It suffices to show

If , then the inequality is trivial. If for some constant , then

as long as

Since , the inequality holds provided that . If , then

Therefore, we conclude that (49) holds and hence we obtain that

provided that and . Due to symmetry, we can apply the same argument to and the proof is completed.∎

B.3 Proof of Lemma 5

The idea is to apply Berstein’s type matrix inequality, e.g., Proposition 2 in Koltchinskii et al. (2011), and check the conditions therein are satisfied. To begin with, it’s easy to verify that . Then we check that is sub-exponential, which can be seen via the following derivation:

where the second inequality follows from the fact that and . In addition, we need to bound . Notice that

The -th diagonal entry of can be computed as

For -th entry of such that , we have

Hence we have

Applying matrix Berstein’s inequality, we complete the proof.∎

B.4 Proof of Lemma 6

We first prove a symmetric version of this lemma and then extend it to the desired non-symmetric version using standard dilation technique. Now we restate the symmetric version.

Lemma 8.

Consider a rank- matrix with eigen-decomposition , where and , , let be a symmetric perturbation matrix and . Denote the best rank- approximation of . Suppose that for any constant , then there exists some absolute constant such that

Proof of Lemma 8

Denote the leading (in absolute value) eigenvectors of . First, by Theorem 1 in Xia (2021), we have the following identity holds:

| (50) |

where

Here contains non-negative indices, is the number of positive indices in and and . By definition of , utilizing (50) we have

| (51) | ||||

| (52) |

We are going to bound each term of (B.4). Notice that for any

where in (a) we used the fact . Therefore, for the first term of (B.4) we have

Since , we have

The second term of (B.4) can bounded as

For the third term in (B.4), we have

It remains to bound the last term of (B.4), which can be done as follows

Collecting all pieces, by (B.4) we arrive at

∎

Proof of Lemma 6

Now we turn to the proof of Lemma 6. Define

Also define

Notice that and are the eigenvectors of and , respectively. By construction we have and . Then applying Lemma 8 we have

∎

B.5 Proof of Lemma 4

Consider a -net for endowed with metric , denoted by , we have its cardinality (see, e.g., Zhang and Xia (2018)). Then for any , we can have a ball centered at with radius , that is, . Hence . Now for any with , there exists such that , we consider the following functions with :

We first check the bracket contains , which follow from the following observation:

where the inequality follows from the inequality for any and the fact that . Hence we have . It remains to calculate . Note that by definition of Hellinger distance, we have

Hence we can take , then . Since , the cardinality of brackets becomes

∎