Information-Based Trading

Abstract

We consider a pair of traders in a market where the information available to the second trader is a strict subset of the information available to the first trader. The traders make prices based on information concerning a security that pays a random cash flow at a fixed time in the future. Market information is modelled in line with the scheme of Brody, Hughston & Macrina (2007, 2008, 2011) and Brody, Davis, Friedman & Hughston (2009). The risk-neutral distribution of the cash flow is known to the traders, who make prices with a fixed multiplicative bid-offer spread and report their prices to a game master who declares that a trade has been made when the bid price of one of the traders crosses the offer price of the other. We prove that the value of the first trader’s position is strictly greater than that of the second. The results are analyzed by use of simulation studies and generalized to situations where (a) there is a hierarchy of traders, (b) there are multiple successive trades, and (c) there is inventory aversion.

Key words: Information-based asset pricing, information processes, trading models, informed traders, Brownian bridge, nonlinear filtering, signal to noise ratio, bid-offer spread, inventory aversion.

I Introduction

We step outside the standard framework for arbitrage-free pricing and consider a situation that conforms more closely to that of reality, namely that where traders with access to superior information dominate those who are less well informed. The principle that the more well informed should be better placed to trade successfully is intuitively satisfactory and generally accepted, but there remains the problem of embodying this principle in the context of a specific set of models, and within this context giving a precise mathematical characterization of the mechanics of statistical arbitrage when the arbitrage is based on informational advantage. That is the goal of the present investigation. Our approach to the problem is to adapt the methods of information-based asset pricing BHM2022 to the dynamical setting of a hierarchy of traders stratified by the level of information that they can access.

Before embarking upon details we give an overview of the arguments we propose to develop. In Section II we recall the construction of the information-based price in a market with a single source of information concerning a security that delivers a single random cash flow at a fixed time . The price process is presented in Proposition 1 and is worked out by filtering techniques based on the methods of references BHM2007 ; BHM2008 . Here we reformulate that work in a rather general setting in which the cash flow is represented by an integrable random variable.

The setup is then generalized to the situation where prices are made by a hierarchy of traders, wherein a tier- trader has at their disposal the filtration generated by a collection of information processes, the tier- trader works with the filtration made by the first of these processes, and so on. In Proposition 2 we work out the price made by a tier- trader, and in Proposition 3 we show that this price can be expressed in terms of a reduced “effective” information process with a higher information flow rate given by the square root of the sum of the squares of the flow rates of the various component information sources.

The arguments of Section II are developed within the framework of a hierarchy of specific models for market information. The restriction to the case of a single random cash flow is merely for simplicity and can be generalized in a straightforward way to the situation where one has multiple cash flows dependent on multiple market factors and multiple associated sources of information BHM2007 ; BHM2008 ; Macrina2006 . In Section III the discussion is lifted to the general set up of a pair of traders where the filtration of Trader is a sub-filtration of that of Trader . See BDFH2009 ; BHM2011 for similar trading schemes. In the setting we consider, a game master monitors the prices made by the two traders and declares the terms under which a trade takes place.

There is a fixed multiplicative spread , and in Scenario 1, the trades take place at a predesignated time and occur whenever the bid price of one of the traders exceeds that of the offer price of the other. There is a pricing kernel that determines a pricing measure, and hence a value can be assigned to Trader ’s position as he enters the arena. We assume the bank accounts of both traders are empty at the initiation of trading. Then under a mild non-triviality condition we prove in Proposition 4 that Trader ’s position has a strictly positive value in this scenario. The method of proof extends that of reference BDFH2009 . In Scenario 2 we consider the same trading setup and specialize to the case where Trader accesses a single information process of the Brownian bridge type and Trader is an uninformed trader with only the a priori distribution of at his disposal and no updating. In that case we proceed in Proposition 5 to establish an exact lower bound on the value of Trader ’s position.

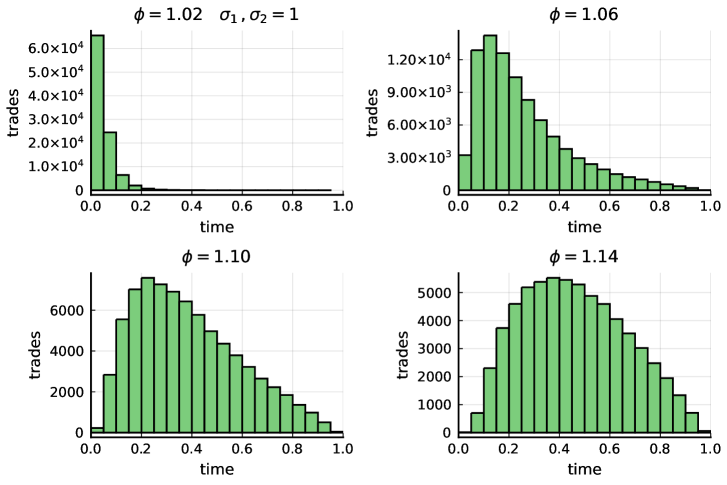

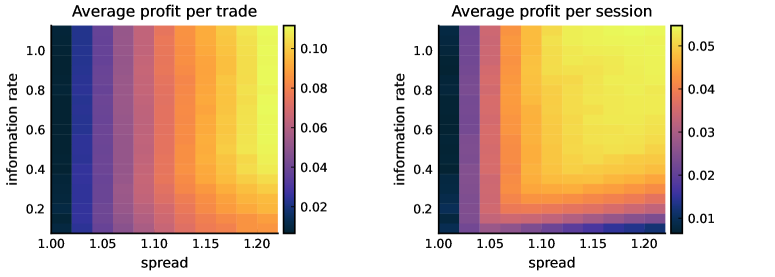

In Section IV we return to the general setting and consider the situation where a trade takes place on the first occasion over the trading interval when the spreads cross, that is, when the bid price of reaches the offer price of or the bid price of reaches the offer price of . The theory of stopping-time -algebras is well suited for this kind of analysis (Lemma 1) and we are able to make novel use of the optional sampling theorem for uniformly integrable martingales for the proof of Proposition 6, which shows that the profitability of the informed trader in such a scenario is strictly positive. Figure 1 shows how the distribution of the trading times is concentrated in the early part of the trading session for smaller spreads and shifts towards the middle part of the trading session for larger spreads. Figure 2 shows the rather surprising result that the informed trader’s average profit per trading session is a concave function of the spread factor at a given level of the information flow rate.

In Section V we allow for the possibility of multiple trades under the assumption that following a trade each trader will take the value at which the trade was carried out to be their new quoted mid-price. Thus the quoted mid-prices are equalized and are made by adjusting the associated information based prices upward or downward by the spread factor. The new quoted mid-prices of the two traders then develop onward from there with the information subsequently received, and the associated bid and offer prices are determined by a further unit of the spread factor. Another trade takes place when the spreads cross again. In Scenario 4 we look at the case where the game master allows for trading to continue for up to a maximum of two trades over a given trading session, and then in Proposition 7 we show that the profitability of the informed trader is strictly positive in such a scenario.

In Section VI, under Scenario 5, we develop a theory of inventory aversion to take into account the fact that in many trading situations traders prefer, everything else being the same, to run fairly flat books, moving in and out of positions in accordance with the arrival of favorable trading opportunities. We allow for this by keeping track of a trader’s inventory and adjusting the quoted mid-price up or down by an inventory aversion adjustment factor for each unit of inventory. The two traders can have distinct inventory aversion adjustment factors, reflecting the fact that inventory aversion is an individual characteristic of a trader, unlike the spread factor, which is a market convention determined by the game master. Nevertheless there are some global constraints: in particular, in Lemma 2 we show that the inventory aversion risk factors are bounded from above by the spread factor. In the situation where the game master admits a maximum of two trades to take place, our Proposition 8 establishes that even with the presence of inventory aversion (possibly asymmetric) the profitability of the informed trader remains strictly positive.

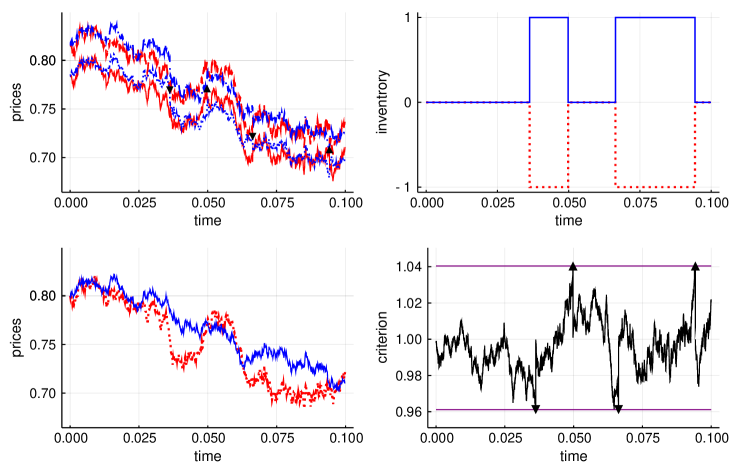

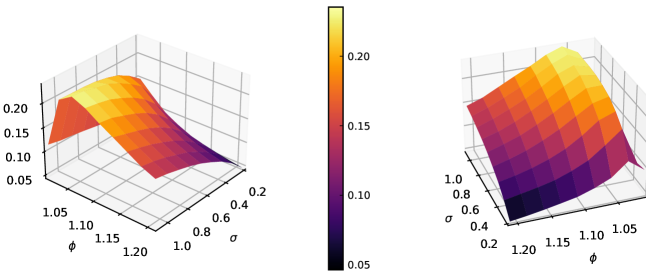

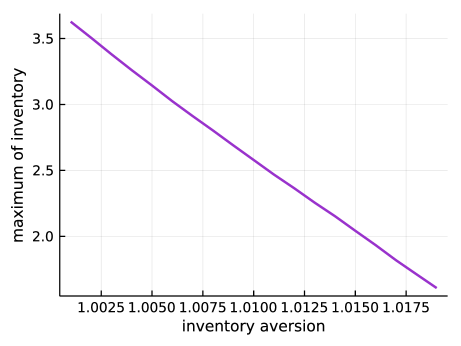

In Section VII under Scenario 6 we examine the situation when more than two trades are admitted under the condition of inventory aversion. We prove a combinatorial identity in Lemma 3, a result that is of interest in its own right, illustrated in Figures 3 and 4. This paves the way to Proposition 9, establishing in a rather general setting the positivity of the informed trader’s profitability when there are multiple trades. Figure 5 allows one to see in some detail examples of the trading dynamics when there are up to ten trades allowed in a given trading session. We see the bid and offer prices quoted by both traders, and the points at which the spreads cross are flagged with pointers to show whether the trade is buy or a sell. The inventories are tracked in the second panel, and the third panel plots the underlying information-based prices. The fourth panel shows the ratio of the quoted mid prices, and we show the boundaries at which trades are triggered. Then in Figure 6 we plot the average profitability of the informed trader as a function of the spread, which turns out to be concave, illustrating the fact that there is an ideal level for the spread, at a given level of the information flow, at which the profitability is maximized. Figure 7 then presents this result in the form of a profitability surface parametrized by the spread factor and the information flow rate. Figure 8 shows the effect of inventory aversion and makes it clear that with increased levels of inventory aversion the average value of the magnitude of the inventory decreases. Finally, in Section VIII we show that if the trader with inferior information is allowed the strategic flexibility of an adapted spread and an adapted risk aversion, this makes no difference qualitatively to the outcome that the trader with superior information will dominate. We conclude in Section IX.

II The model

We fix a probability space and consider a trading model with stratified information. We look at several different variants of the model with increasing layers of complexity. An interval of time is fixed over which the trading takes place. The trading is in a contract that at time pays a single non-negative dividend, which we model by an integrable random variable . We assume that interest rates are deterministic and that is the pricing measure (the risk-neutral measure), so the value of one contract at time (the present) is given by

| (1) |

Here denotes the discount factor out to time . For simplicity, we assume that traders have the same information and same beliefs at time and that the position of each trader is initially flat.

We introduce a hierarchy of traders as follows. By a tier-0 trader, we mean a trader whose only information is that implicit in the set-up described. Thus, he knows the a priori measure of the random variable under , but has no other information. As a consequence, the prices made at later times are given by

| (2) |

where . Knowledge of the distribution of is equivalent to knowledge of the time- prices of all derivative securities with a payout at time of the form for some . Note that for since the contract pays a single random dividend at and nothing thereafter. With this convention the price process has the càdlàg property.

By a tier-1 trader we mean a trader who has access to a so-called information process . The information takes the form

| (3) |

for and for . Here is a non-negative parameter, called the information flow rate, and is a Brownian bridge over the interval . The Brownian bridge can be modelled by setting for and for , where is a standard Brownian motion. The information available at time can be thought of as a signal , corresponding to the upcoming cash flow, obscured by market noise. For some applications one can treat more generally as a market factor with the property that the cash flow is given by a function of . Here for simplicity we stick to the case where represents the cash flow itself, but the reader will be readily able to see how the more general situation can be accommodated. The theory of information processes along with a variety of applications is set out in references BHM2007 ; BHM2008 ; BDFH2009 ; BHM2011 ; BHM2022 ; see also HSB2020 ; Macrina2006 ; Rutkowski Yu .

Now, let us write for the smallest right-continuous complete filtration containing the natural filtration of . Thus, we let denote the set whose elements are subsets of the null sets of , and for each we set

| (4) |

We refer to as the filtration generated by . Then the price of the asset at time is

| (5) |

and we have the following:

Proposition 1.

The information-based price of a contract that pays a non-negative integrable random cash flow at time takes the form

| (6) |

Proof.

One can show that the information process has the Markov property BHM2007 , from which it follows that

| (7) |

Now write for the distribution of , where , and let be a continuous random variable with distribution and density . Then there is a generalized Bayes theorem (HSB2020 , Lemma 3) to the effect that for all at which it holds that

| (8) |

where denotes the conditional distribution , and

| (9) |

It follows that for any outcome of chance we have

| (10) |

where denotes the value of at . Then if we let the random variable play the role of in the setup described above and use the fact that is conditionally Gaussian with mean and variance , it is straightforward to work out the conditional distribution of given by use of (10), and (6) follows. ∎

We refer to as the information-based price made at time by a tier-1 trader. Note that , whereas . By a higher-tier trader we mean a trader who has one or more additional information processes at his disposal in such a way that the filtration accessible to the tier- trader is a sub-filtration of that accessible to the tier- trader. We adapt the notation above to the case where we have information processes and write

| (11) |

for , . Here denotes the information flow rate for the information process , and the are independent Brownian bridges. In principle, one could look at the seemingly more general situation where the Brownian bridges are correlated, but after suitable linear transformations this can be reduced to the case under consideration. We recall that a tier-0 trader has no information available other than that which is available a priori to all traders. A tier-0 trader thus makes the price

| (12) |

A tier-1 trader makes the price

| (13) |

a tier-2 trader makes the price

| (14) |

and a tier- trader makes the price

| (15) |

Then, it becomes an exercise to prove the following:

Proposition 2.

The tier- price is given by

| (16) |

Proof.

It will suffice to look at the case to illustrate the method of proof. We wish to show that

| (17) |

We observe that

| (18) |

from which one deduces that

| (19) |

where

| (20) |

In fact, can be interpreted as the “effective information” generated jointly by and . One can check that is an information process and that is an independent Brownian bridge. Indeed, we have

| (21) |

where

| (22) |

and the process defined by

| (23) |

is a standard Brownian bridge over . The fact that is itself a Brownian bridge and that and are independent can be deduced from covariance relations. Moreover, it should be evident that the -algebras and are independent.

Now, we recall the following from Williams williams1991 , §9.7(k) in his well-known list of properties of conditional expectation. Suppose that is an integrable random variable on a probability space and that and are sub--algebras of . Then if and are independent, we have

| (24) |

It follows in the case under consideration that

| (25) |

That is to say, the tier-2 price only depends on the effective information associated with the two given information processes. Thus, we have

| (26) |

Then if we substitute (21) into (26), a straightforward calculation gives the result (17). The proof for higher values of is similar. ∎

It is interesting to note, as we have pointed out above, that the tier-2 price (26) can be expressed as a function of a single effective parcel of information, given by (21), with effective flow rate (22). This property generalizes to higher . In particular, we have:

Proposition 3.

The tier-n price of an asset paying at time can be put in the form

| (27) |

where the effective information is defined by

| (28) |

Proof.

We observe that

| (29) |

where is the effective information at and the , defined for by

| (30) |

constitute a family of independent Brownian bridges. For each value of the -dependence cancels in the terms on the right and hence we can write

| (31) |

The fact that the are indeed independent Brownian bridges can be then checked by the use of covariance relations. The -algebras and are therefore independent and thus

| (32) |

as claimed. ∎

We observe that as a consequence of these relations the effective information flow rate for a tier- trader takes the form

| (33) |

a relation that might appropriately be referred to as a Pythagorean law of information flow: when there are multiple sources of information, the square of the effective information flow rate is equal to the sum of the squares of the information flow rates of the sources BDFH2009 ; BHM2011 .

III Deterministic trading time

It will be useful to establish some general principles regarding trading with information. As in the previous section, we consider a market where a single risky security is traded that pays a random dividend at a fixed time . As before, we take interest rates to be deterministic and we let denote the pricing measure. In a more extended treatment we might enter into a discussion of how the pricing measure is determined, but that is not our goal here.

We look at the situation where there are two traders, a higher-tier Trader who has the information generated by at his disposal, and a lower-tier Trader who has the information generated by at his disposal, where . Then clearly at each time we have , reflecting the fact that the higher-tier trader has more information at his disposal than his lower-tier counterparty. Equivalently, we say that the filtration is finer than the filtration and that is courser than . The key point is that at the outset of the trading the traders have identical information and identical beliefs, both embodied in . After time and up to time the traders gain information and make prices based on this information in such a way that the information gained by Trader is always a subset of the information gained by Trader .

Let us assume that the market conventions are such that traders make prices with a fixed multiplicative spread. We refer to the information-based price computed by a given trader at time as his mid-price at that time. The spread factor is taken to be a fixed real number that is strictly greater than unity. Then the trader’s offer price (the price at which he is willing to sell the asset) will be , and his bid price (the price he is willing to buy the asset at) will be .

The so-called bid-offer (or bid-ask) spread is then given by . The discussion can be easily adjusted to accommodate the case of a fixed additive spread, but we shall leave that to the reader and stick with multiplicative spreads here. The mid-price is then given by the geometric mean of the bid price and the offer price.

We shall assume in what follows that the market is overseen by a game master (e.g., an exchange or central planner). The traders report their mid-prices to the game master (but not to one another) on a continuous basis, and the game master determines, in accordance with certain conventions, when a trade is deemed to have taken place. Neither trader is aware of informational status of the other trader. Trader receives the information that Trader receives, but he is not aware of the fact that this is the only information being received by Trader . There are various situations that can be envisaged, and we refer to these as trading scenarios, several examples of which we proceed to examine.

Scenario 1. The game master selects a fixed time at which a trade can take place. The traders each initially have flat positions. We shall write

| (34) |

for the mid-price made by Trader at time , and let and denote his bid price and offer price, respectively. For the mid-price of Trader at , we write

| (35) |

with bid price and offer price . The game master declares that Trader sells one unit of the asset to Trader at time if ; the game master declares that Trader buys one unit of the asset from Trader at time if ; if neither of these conditions hold then no trade takes place. By convention, the game master assigns the mean price to the trade if sells to ; the game master assigns the mean price to the trade if buys from . In fact, these prices are the same, both being equal to the geometric mean of the mid-prices made by and . The overall profit (or loss) accruing to Trader at time is thus given by

| (36) |

where payments made or received at are future-valued to . The profit (or loss) of Trader is clearly . Now, since is the risk neutral measure, it is meaningful to assign an overall value to Trader ’s strategy, given by

| (37) |

Here we have taken the -expectation of Trader ’s profit when that profit is expressed in units of the money-market account at time , which in a deterministic interest-rate system is given by . Armed with (37), we are now in a position to say more specifically in what sense the additional information possessed by Trader gives him a financial advantage. To this end, let us say that a trading model is non-trivial if the probability of a trade occurring over a given trading session is non-vanishing. Note that we do not require that a trade should definitely occur, merely that it might occur. Since the pricing measure and the physical measure share the same null sets, it follows that a trading model is non-trivial if and only if the probability of a trade occurring in any given trading session is non-zero under the measure . Then we have:

Proposition 4.

The value of Trader A’s position under Scenario 1 is strictly positive in any non-trivial trading model.

Proof.

If sells then and hence ; whereas if buys then and hence . It follows that

| (38) |

Then if we take into account the fact that and hence that is -measurable, as are the two indicator functions in the expression above, it follows by use of (34), (35), (37), (38) and the tower property that

| (39) |

which gives us a strictly positive lower bound on the value of Trader ’s position, providing that at least one of the two indicator functions takes the value unity on a set that is not of measure zero, which is the condition that the model is non-trivial. ∎

The idea of the proof of Proposition 4 is deceptively simple. We only require that should be -measurable. If the information available to is marginally better than that available to , then their mid-prices will not tend to diverge much, and the probability of a trade occurring will be relatively low; whereas if the information available to is of significantly better quality, then the prices will tend more to diverge, and hence the probability of a trade occurring will be higher, and the price at which the trade occurs will tend to be more advantageous to than . It should be emphasized that in setting the trading time to be a fixed time we are not suggesting that such a scenario is representative of the way in which real trades are carried out. The point is rather that under that simplifying assumption we are able to identify how Trader can take advantage of his informational superiority. By stripping away some of the clutter associated with more realistic trading scenarios, we can focus on the mathematical principle that allows the informationally superior trader to succeed. Of course, we must check that the advantage is not spoiled in the setting of more elaborate trading scenarios, and this is what we do in subsequent examples. We observe that the value of Trader ’s position at the beginning of the trading session is strictly positive. This means that he can in principle monetize his advantage by selling off some or all of his stake in the eventual outcome of the trading session to a third party at the market price given by (37). The fact that such a monetization is feasible is what we mean by statistical arbitrage. There is no guarantee that in any particular trading session Trader will prevail.

Scenario 2. Continuing with a deterministic trading time, we remark that in the situation where is a tier-1 trader and is a tier-0 trader (only having knowledge of the a priori distribution of ) one can work out the lower bound on Trader ’s position exactly if we use the model of Section 2 when the payout is that of a defaultable discount bond, thus allowing for an explicit realization of the effects of the spread and the flow rate on the profitability of the informed trader’s market activity. In the case of a defaultable discount bond with no recovery we assume that takes the values (no default) and (default) with probabilities and respectively. Then the mid-prices made by the two traders are given by

| (40) |

A straightforward calculation shows that

| (41) |

and

| (42) |

The indicator function in (42) is able to take the value unity only if . This is because under Scenario 2 a trade can take place where Trader is a buyer only if this condition is satisfied. Otherwise Trader can only be a seller. In the following we let denote the standard normal distribution function.

Proposition 5.

The lower bound on the value of Trader ’s position under Scenario 2 is

| (43) |

Proof.

We need to work out the right hand side of (39) when we substitute (40), (41) and (42) into it. This gives

| (44) |

Here we have used the fact that in a deterministic interest system. It may not be obvious how to take the expectations in (III), but these can be worked out in closed form. The trick is to observe that the process defined by

| (45) |

is a unit-initialized martingale under with respect to the filtration generated by , and hence can be used to change measure to a new measure under which is a Brownian bridge. In fact, is an example of the so-called bridge measure introduced in reference BHM2007 . Thus for any event we define

| (46) |

and we obtain

| (47) |

where the expectation is now taken under . Finally, we use that fact that is a normally distributed random variable with mean zero and variance , and the problem reduces to evaluating a Gaussian integral of a standard type, leading to (5). ∎

IV Trading when the spreads cross

Scenario 3. We consider a setup like that of Scenario 1, but where the game master declares that a trade occurs the first time the spreads cross. To make the ideas precise we need a few results from the theory of stopping times (see, e.g., Dothan1990 ; Protter2004 ; Cohen2015 ). We recall that by a stopping time on a filtered probability space we mean a random variable taking values in with the property that for all . It follows that if and are stopping times, then is also an stopping time. This is because . We recall that in our model the filtration accessed by Trader is strictly finer than the filtration accessed by Trader . Thus the mid-prices made both by Trader and Trader are adapted to . Now, for any càdlàg process adapted to , and for any Borel set the random variable is an stopping time. We can therefore introduce the following stopping times:

| (48) |

and we set , the minimum of and . Here for any index set and any collection of elements of we write for the random variable . We observe that is the first time the bid price of hits the offer price of , that is the first time the offer price of hits the bid price of , and that is the first time the spreads cross. We recall that the prices made by both traders drop to zero at time . Therefore if takes the value for some outcome of chance, then no trade has taken place in that outcome of chance.

We assume that once a trade has been made then the position will be held until maturity and no further trades will take place. With this setup in mind, we see that the overall profit accruing to Trader at time in Scenario 3 is

| (49) |

As in Scenario 1, we can work out the value of Trader ’s position by use of the risk-neutral pricing relation (37). For this purpose, we need a few additional mathematical tools. For any stopping time on a filtered probability space , the so-called stopping-time -algebra is defined by

| (50) |

Given a pair of stopping times and , one can show that if then . The following is fundamental:

Lemma 1.

If and are stopping times based on the filtration , then each of the events , , , , belongs to and to .

Proof.

Let us demonstrate that . The other cases then follow analogously. Thus by (50) we need to show that . Now,

| (51) |

and hence for any it holds that

| (52) |

for rational. But each of the events and is in . Thus we have expressed as a countable union of sets in . ∎

Continuing with our discussion of stopping times, we recall that a collection of random variables on a probability space is said to be uniformly integrable (UI) if given such that , . A martingale on a filtered probability space is said to be closed by a random variable if and for . If a right-continuous martingale is UI, then exists almost surely, , and closes . In what follows, we need the optional sampling theorem, which states that if a right-continuous martingale is closed by a random variable , and if and are stopping times such that almost surely, then and are integrable and

| (53) |

This relation holds in particular in the case of a UI martingale. These results can be applied as follows:

Proposition 6.

The value of Trader A’s position under Scenario 3 is strictly positive in any non-trivial trading model.

Proof.

We observe that if is the price process of an asset that pays a single dividend at time , then the so-called deflated gain process defined by

| (54) |

is a -martingale. The deflated gain process is obtained by taking the current value of the asset, expressed in units of the money market account, and adding to it the cumulative dividend process, where each dividend is expressed in units of the money-market account at the time the dividend is paid. In the case of a single dividend payment and a deterministic interest rate system, the result is given by (54). Thus, by (34) it holds, in fact, that

| (55) |

and we see that the deflated gain process is a UI martingale under , closed by . It follows by the optional sampling theorem that

| (56) |

and hence

| (57) |

Then, since is measurable and is measurable we can use the tower property alongside (49) and (57) to deduce that

| (58) |

It should be evident that both of the terms on the right side of (IV) are non-negative. Then since by assumption it holds that or , or equivalently , we deduce that . ∎

Now, the information-based model described in Section 2 based on Brownian bridge information is evidently non-trivial, so Proposition 6 is applicable, and we should be able to work out the profitability of Trader by use of simulation studies. In Figure 1, we show the distribution of trading times over the interval under Scenario 3. The information flow rates for both information processes are set at unity. Charts are shown for four different values of the spread factor.

One observes that for relatively low spreads, e.g. , the bulk of the trades occur relatively early on in the trading session, whereas as the spread is increased to higher levels such as the trades tend to take place later in the session. This is because it takes more time on average in the case of large spreads for the prices to diverge sufficiently for the spreads to cross.

In Figure 2 below we plot a heat map showing the average profits taken by Trader under Scenario 3 as a function of the information rate and the spread factor. We look both at average per-trade profits and average per-session profits. In the latter case, we allow for the fact that a trade may or may not actually occur in a given trading session. We consider 100,000 trading sessions in each case, using the same outcomes of chance. The average profit is plotted as a function of the spread (-axis) and the information rate (-axis).

We note that the per-trade profits is an increasing function of the spread factor. On the other hand, the per-session profit is for each value of the information flow rate a concave function of the spread factor, over the range of parameters considered. This allows us to conclude that from the perspective of the better informed trader there is an optimal market spread at which to be trading for any given level of the information flow rate, if the objective is to optimize the per-session profitability.

These conclusions are of course based on a relatively simple trading model, but nevertheless give a useful qualitative picture of the interplay of information and market convention in the determination of trading profits. Our philosophy is not to present the most elaborate trading models possible, with bells and whistles, but rather the simplest versions of the models that illustrate the underlying mathematical principles that guarantee the success of the more well-informed trader.

V successive random trades

Scenario 4. In this scenario we consider the situation where trading occurs when spreads cross, as in Scenario 3, but where additionally prices are adjusted following each trade in such a way that the mid prices are equalized and trades occur when the spreads cross again. The setup is as follows. As before, we consider a contract that pays a random dividend at time . Let and denote the mid-prices computed by Trader and Trader on the basis of the information they have gained, respectively, from the information processes at their disposal, and let be the spread factor. The filtration available to Trader is assumed to be a strict sub-filtration of that available to Trader . Then we define a collection of stopping times as follows. First we write

| (59) |

and set . Thus is the time at which the first trade occurs, with the understanding that corresponds to the situation where no trade takes place in the given trading session. Trader buys if and Trader sells if . Next we introduce an indicator function for Trader taking the values plus one, minus one, or zero, to tell us whether the trade was a buy or sell or if there was no trade. We set

| (60) |

After a trade has taken place, the seller adjusts his mid-price up by one unit of the spread factor, whereas the buyer adjusts his price down by one unit of the spread factor. In this way, the two new mid-prices are equalized. One might envisage that the traders would adjust their prices by taking into account the additional information gained by knowledge of the fact that another trader must have made a price in such a way that the spreads would cross. But since neither trader has knowledge of the other’s informational status, it is not so obvious how this could be achieved. We shall assume that it is simply a market convention that the prices are adjusted in line with the procedure stated. Thus each trader adjusts his mid-price to the price at which the trade just took place. This is not unreasonable. Once the prices have been equalized, the traders create bid and offer prices by multiplying or dividing the new mid-prices by a further unit of the spread factor. The game master then declares the time at which the second trade occurs, where

| (61) |

with the understanding that corresponds to the situation where there is no second trade. The profits made by Trader over the course of the first two trades are given in total by the following expression:

| (62) |

By use of the tower property, the optional sampling theorem, and measurability properties of the stopping times involved, we deduce that the value of Trader ’s position is

| (63) |

One notes that the terms involving a pair of opposite trades, that is to say, a buy followed by a sell, or a sell followed by a buy, generate no value for Trader , and hence do not appear in the formula above. But the single trade positions, and the positions involving two buys or two sells, have strictly positive value, assuming that the events in question take place with nonzero probability. Thus we arrive at:

Proposition 7.

The value of Trader A’s position under Scenario 4 is strictly positive in any non-trivial trading model.

VI Inventory Aversion

Scenario 5. We consider the situation where traders prefer to keep a low profile in the market and thus wish to avoid taking excessively long or short positions. This is not unusual: it is often the case that traders are market-neutral and tend to keep their position flat on average. This situation can be modelled as follows. Suppose in the context of the general setup of the last two sections that a trade has just been undertaken, and the new mid-price now shared by both traders is where is the time of the trade. Thus if the initial trade was a purchase by Trader , and if the initial trade was a sale by Trader . Now let be the inventory of Trader at time . By inventory, we mean the number of contracts held by . Then the inventory of Trader is given by since the initial positions of each trader are assumed to have been flat. We shall assume now that at the time the new mid-price is determined there is a further small adjustment of the mid-price set in such a way as to discourage the development of excessively large long or short positions – that is to say, to keep the absolute inventory relatively small. The required adjustment, which holds with effect from time , takes the form

| (64) |

for Trader , where the adjustment factor is taken to be strictly greater than unity. Thus, if the inventory is positive (long position), the mid-price is knocked down by a factor , hence lowering both the bid price and the offer price a bit. This will tend to suppress further purchases by the trader and will encourage sales. But if the inventory is negative (short position), the mid-price is bumped up by a factor of , and this will raise the bid price and the offer price, encouraging purchases by the trader and discouraging sales.

We have assumed so far that traders have the same initial beliefs and initial knowledge, and hence the same initial mid-price; at this stage we can allow for the possibility that they have different levels of inventory aversion. Then Trader adjusts his mid-price after the first trade by the prescription

| (65) |

where is the inventory aversion adjustment factor for Trader .

In fact, one can derive an upper bound for the inventory aversion factors. The argument is as follows. Let us assume that at some given time in the trading session Trader buys (resp., sells) the contract paying (resp., receiving) the amount (resp., ). Then, the trader’s new mid price becomes (resp., ). Now, this new mid-price has to satisfy the condition that the associated new offer price (resp., bid price ) based on it, should be strictly greater than (resp., strictly less than) the price just paid (resp., received). In other words, has to satisfy an inequality of the form (resp., ). For it would be irrational, or at least inefficient, in the absence of further information, for Trader to be willing to immediately sell the contract for less than or the same as what he has just bought it (resp., buy the contract for more than or the same as what he has just sold it). For such actions would at the very least lead to some loss of shoe leather and in general would lead to opportunists taking advantage of him by arbitrage. Hence we obtain:

Lemma 2.

The inventory aversion adjustment factors and are strictly bounded from above by the spread factor .

With this scheme in mind we return to the setup of Scenario 4 but we allow now for inventory aversion in our Scenario 5. The profit made by Trader on the first trade remains the same as in Scenario 4, whereas the inventory aversion adjustments begin to take effect in relation to the prices made in anticipation of a second trade. In particular we now set

| (66) |

and

| (67) |

where for convenience we write for and for . Assuming that trading stops after two trades, we see that the profit made by Trader when both traders have inventory aversion takes the form

| (68) |

The value of Trader ’s position can be worked out by the methods already discussed, and the result is as follows:

| (69) |

Here the first two terms represent the profits from the first trade, whereas the remaining terms represent the profits from the second trade, allowing for the different possible ways in which the history of the second trade might evolve.

Proposition 8.

The value of Trader A’s position under Scenario 5 is strictly positive in any non-trivial trading model with inventory risk.

VII Multiple trades

Scenario 6. When multiple successive trades take place in a given trading session one can adapt the notation of the previous sections by recursively defining the stopping times

| (73) |

and

| (74) |

where , with the convention that . Here, the inventory of Trader after the first trades is given by

| (75) |

and it should be evident that . With this notation in mind, let us consider the situation where the game master permits up to trades in the trading session. We introduce a collection of indices for that take the values . Thus, for the index ranges over the set . To analyze the profitability of Trader over the given trading session it will be useful to have a compact expression for the trading profits. We note that in the case of a single trade, the profit can be written

| (76) |

and it can be verified that this reduces to formula (49), with which we are already familiar. A little less obviously, one can check that for we have

| (77) |

Here we have separated the profits resulting from the first trade from the profits resulting from the second trade. Alternatively, we an write

| (78) |

which splits the profits into those deriving from the situation where there is a single trade and those deriving from situations where there are two trades. The advantage of (VII) is that this expression, when taken with (76), readily generalizes to the -trade case. To this end, it will be useful to define the random variables

| (79) |

for . Thus, and . Let us write

| (80) |

One can then check that the total profitability of Trader over the given time frame in a multiple trade situation is given by

| (81) |

The profits registered in (VII) are those for the first trades, allowing for the possibility that there may be fewer than trades. The first term on the right takes into account the situation where there are (or fewer) trades, and the second term on the right gives the profitability when there are exactly trades. Here, to ease the notation we have written in place of , since enters only indirectly, via the stopping times. As a step towards establishing Proposition 9 below, we introduce the following:

Lemma 3.

Let , let , and let the series be chosen such that for each . Then

| (82) |

Proof.

We proceed by induction. It is straightforward to check that (82) holds for and for . Our goal is to show that if (82) holds for then it holds for . Let the index series be given. Define the series by setting and for . We observe that (82) can be written

| (83) |

We consider the case , the case being analogous. Within the chosen case, we observe that if a negative value is taken by an element of the series , then such that and . Define the series by and for . Then we have

| (84) |

Since and , it holds by the inductive hypothesis that both terms on the right hand side of (84) are positive. Thus, it suffices to restrict our attention to the case where all elements of the series are non-negative. Now let be the number of times is negative for . That is to say,

| (85) |

where denotes the cardinality of the set . If , then for all and (82) holds. Thus, we turn to the case . Let denote the first for which is negative, let denote the second for which is negative, and so on up to , which denotes the -th for which is negative. Let be , and for set

| (86) |

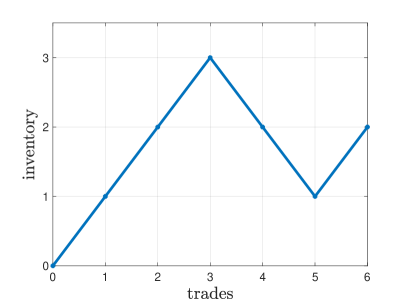

It should be evident that for each such that there exists a number satisfying (86). To fix ideas, in Figure 3 we present an example of the trajectory of Trader ’s inventory over six trades, where we work out and for .

Define . Then

| (87) |

which is strictly greater than zero. In particular, we note that the first term of the right hand side of (87) is strictly positive, since and . Furthermore, since by construction for , we have , and hence

| (88) |

from which we deduce that the second term on the right side of (87) is strictly positive. ∎

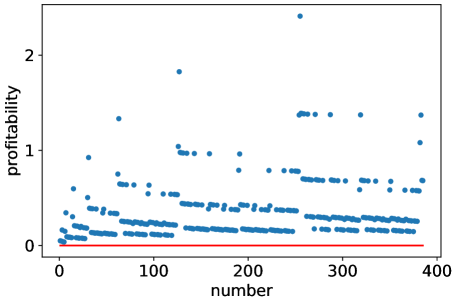

Figure 4 provides a visual representation of the inequality (82) for sequences up to .

Armed with Lemma 3 we are now in a position to assert the following:

Proposition 9.

The value of Trader A’s position under Scenario 6 is strictly positive in any non-trivial trading model with inventory risk.

Proof.

We wish to show that the expectation of the total profitability (VII) is positive for any . By use of the optional stopping theorem we observe that the value of Trader ’s position under Scenario 6 is strictly positive if

| (89) |

for any choice of the parameters and for any sequence such that for all . We conclude the proof by use of Lemma 3. ∎

With the framework of Scenario 4 in mind, we conduct simulation studies for the case when the game master allows up to ten trades. Figure 5 illustrates the trading mechanism. To make the various features of the model apparent to the naked eye, we have shown the first one-fifth of the time frame of the trading session. The lower right-hand panel shows the trajectory of the ratio of the quoted mid-prices, given by

| (90) |

In the figure below we plot the profitability of Trader as a function of the spread factor , based on 100,000 simulations. The concavity of the profitability as a function of the spread is clear.

Figure 6 provides the insight that as the spread is decreased information is transferred to the less informed trader at a lower cost. This means that there is a duality for Trader , at least regarding the average profitability, between (i) acquiring more information while remaining less-informed than Trader , and (ii) trading in a market where the game master declares a smaller spread.

In Figure 7 we show the profitability surface as the spread factor and the information flow rate change. Figure 8 demonstrates how the average inventory decreases as the inventory aversion parameter is rachetted up. It is interesting to observe that the dependence is essentially linear.

VIII Information Dominates Strategy

Scenario 7. In this scenario Trader has a fixed spread and a fixed ambiguity aversion parameter satisfying . But Trader now employs an adapted multiplicative spread , assumed to be càdlàg, such that for all . Trader also uses an adapted ambiguity aversion , assumed to be càdlàg, satisfying for all . We define the stopping times

| (91) |

and

| (92) |

where , with the convention that . Here, the inventory of Trader after the first trades is given by

| (93) |

and one has . Then we obtain the following.

Proposition 10.

The value of Trader A’s position under Scenario 7 is strictly positive in any non-trivial trading model with inventory risk and where Trader makes use of an adapted multiplicative spread and an adapted inventory aversion.

Proof.

As in Proposition 9, we wish to show that the expectation of Trader ’s profitability (VII) is positive for any . Given that and only enter (VII) indirectly, via stopping times, it follows by use of the optional stopping theorem that the value of Trader ’s position under Scenario 7 is strictly positive if (89) holds for any choice of the parameters and satisfying and for any sequence such that for all . Lemma 3 then applies and leads to the desired result. ∎

Proposition 10 offers an interesting insight: superior information trumps strategy – in other words, regardless of the strategy that Trader uses, the superiority of Trader ’s information ensures that Trader ’s profitability is positive.

IX Conclusions

That superior information leads to superior trading need not come as a surprise, for who would have thought otherwise? But it is one thing to speculate so in general terms with waving hands, and it is another thing to embody the principle in mathematical terms underpinned with explicit models. Our examples illustrate the variety of venues under which the informed trader will practice his trade, and the professionals will realize that strategy is but of little impact, that knowledge exceeding that of {greek}o¡i pollo’i is what is required. When the traded instrument admits a single payout, as in the case of the defaultable discount bond considered, the advantage taken by the informed trader diminishes as the terminal date is approached, and at the point of reckoning traders of either class are equally knowledgeable. This is an artefact of the simple structure of the example, and not representative of the situation in general; for in reality the informed trader will have already taken his profit and moved on to the next presented opportunity. With coupon bonds and dividend paying stocks, by the time Trader has caught up with Trader ’s knowledge of some coupon or dividend, the intention is already on the next. We do regard it significant that the filtration accessed by Trader is a strict sub-filtration of that of Trader . For we assign a value to a trader’s strategy and for that we require a pricing kernel adapted to the filtration of the larger mass of the less-informed represented by Trader . The change of measure thus induced allows one to work with risk-neutral pricing for all traders, whose differences in pricing are due to differences in knowledge – not, in the main, in our scheme, to differences in behavioral characteristics or issues of supply and demand.

Throughout the analysis we have worked at two different levels, which we might call the general and the specific. For some considerations we look at general trading models based on a market with a pricing kernel and a hierarchy of filtrations. For other considerations we construct specific examples of market information flows. It is a general feature of the information-based approach that quantification of the magnitude of the information is left as an abstraction, and one might be left wondering what the information flow rate signifies. This issue has been addressed in references BHM2007 ; BHM2008 , where it is pointed out that one can back out an implied information flow rate from option prices, alongside the implied -distributions of the cash flows. Whether or not such options are actually traded is not the point; rather, we emphasize that the flow rate parameters and the a priori -distributions can in principle be determined from market data. We envisage a variety of practical applications of the trading scenarios that we have considered in this paper. Both in-house risk managers and market regulators may find our model useful to stress market conditions such as volatility and spread and to look at average profitability, volume traded, and other variables of interest. More generally, our model can be readily extended to the situation where there are more than two traders in which the traders are stratified into hierarchies. Such scenarios may form the basis for viability studies for large markets and eventually new approaches to the vexing issues of systemic risk in such markets Hurd . In the specialized aspects of our analysis we have confined our studies to the consideration of Brownian bridge information processes of the type set out and studied in BHM2007 ; BHM2008 ; BDFH2009 ; BHM2011 ; FHM2012 ; HM2012 ; BHM2022 ; Macrina2006 ; Rutkowski Yu ; Aydin2017 ; FKT2019 . This can be justified on the basis of the high degree of analytic tractability found in such models. But it should be clear that the more general aspects of our analysis extend into the categories of information processes admitting jumps, and hence it would also be worth exploring trading models based on Lévy processes and Lévy-Ito processes Applebaum ; BHJS2021 ; BH2013 ; BHM2008dam ; BHMackie2012 ; BHY2013 ; Hoyle2010 ; HHM2012 ; HHM2015 ; HMM2020 ; HSB2020 ; MS2019 ; Menguturk 2013 ; Sato 1990 .

The information-based trading models that we set out here can be placed in the context of the distinct and overlapping contributions made by various authors, including those of the present paper, to the development of the trading mechanisms built on information-based asset pricing. The early work BHM2007 ; BHM2008 ; BHM2008dam ; Macrina2006 ; Rutkowski Yu in this area was concerned with applications to asset pricing, derivatives risk management, and insurance markets. The story of how these collaborations came about can be found in the preface to BHM2022 where a bibliography of later work on the topic by a host of authors can be found. The first applications to trading mechanisms appear in reference BDFH2009 . In that paper, the trading involves (i) a large homogeneous market with access to a single flow of information, together with (ii) a single “informed” trader, who has access to an additional flow of information. Since the informed trader also has access to the information flow available to the general market, his filtration is strictly larger than that of the market as a whole.

In the language of the present paper, the market as a whole in BDFH2009 can be represented by a tier-1 trader, whereas the informed trader is a tier-2 trader. In reference BDFH2009 one also finds a version of the “Pythagorian” formula as well as elements of the statistical arbitrage argument that we use in the present paper. In reference BHM2011 one sees the first applications of the information-based approach to trading in a truly heterogeneous market. In that work each trader has access to a distinct information process and it is assumed for simplicity that the Brownian bridges are independent. The traders make prices with bid-ask spreads and trades occur when the spreads cross. Some of the traders have informational superiority in the sense that their information flow rates are higher than those of other traders, but the relationship of the traders to one another is not “hierarchical” in the way that it is in the present paper. The model of BHM2011 was extended and analyzed in great depth in the work of Aydın Aydin2017 and has been further extended (with the inclusion of noise correlations and extensive numerical analysis) by Fukuda, Kondo & Takada FKT2019 . All in all, one sees two distinct lines of development in the construction and analysis of trading models making use of the information-based framework. On the one hand, there are the heterogeneous models of BHM2011 ; Aydin2017 ; FKT2019 , and on the other hand there are the hierarchical models of BDFH2009 and the present paper. These two classes of models apply to different types of markets and each can be generalized in various ways. An open problem in the theory of heterogeneous markets, in the situation where each trader has his own supply of information, is to show rigorously (or else provide a counterexample) that informational superiority – that is, having a higher information flow rate – is advantageous in the sense that it leads to a statistical arbitrage.

Acknowledgements.

We are grateful for comments by participants at the 16th Research in Options conference (RIO 2021), where this work was presented in November 2021, co-hosted by the Department of Mathematics, Khalifa University, UAE, by the School of Applied Mathematics, Fundação Getulio Vargas, Rio de Janeiro (FGV EMAp), by Universidade Federal Fluminense, Brazil (UFF), and by Universidade Federal de Santa Catarina, Brazil (UFSC). We are grateful to seminar participants in the Department of Mathematics and Statistics at McMaster University, Ontario, November 2022, for their input. The authors wish to thank A. Macrina, and the anonymous referees, for helpful comments on earlier drafts. This work was carried out in part while LBS was based at Imperial College London and at King’s College London.References

-

(1)

Applebaum, D. (2009) Lévy Processes and

Stochastic Calculus, second edition. Cambridge University Press.

- (2) Aydın, N. S. (2017) Financial Modelling with Forward-Looking Information. Cham, Switzerland: Springer.

- (3) Bouzianis, G., Hughston, L. P., Jaimungal, S. & Sánchez-Betancourt, L. (2020) Lévy-Ito Models in Finance. Probability Surveys 18, 132-178.

- (4) Brody, D. C., Davis, M. H. A., Friedman, R. L. & Hughston, L. P. (2009) Informed Traders. Proceedings of the Royal Society A 465, 1103-1122.

- (5) Brody, D. C. & Hughston, L. P. (2013) Lévy Information and the Aggregation of Risk Aversion. Proceedings of the Royal Society A 469, 20130024:1-19.

- (6) Brody, D. C., Hughston, L. P. & Macrina, A. (2007) Beyond Hazard Rates: a New Framework for Credit-Risk Modelling. In Advances in Mathematical Finance (M. C. Fu, R. A. Jarrow, J.-Y. J. Yen & R. J. Elliot, eds.) Basel: Birkhäuser.

- (7) Brody, D. C., Hughston, L. P. & Macrina, A. (2008a) Information-Based Asset Pricing. International Journal of Theoretical and Applied Finance 11 (1), 107-142b.

- (8) Brody, D. C., Hughston, L. P. & Macrina, A. (2008b) Dam Rain and Cumulative Gain. Proceedings of the Royal Society A 464, 1801-1822.

- (9) Brody, D. C., Hughston, L. P. & Mackie, E. (2012) General Theory of Geometric Lévy Models for Dynamic Asset Pricing. Proceedings of the Royal Society A 468, 1778-1798.

- (10) Brody, D. C., Hughston, L. P. & Macrina, A. (2011) Modelling Information Flows in Financial Markets. In Advanced Mathematical Methods for Finance (G. Di Nunno & B. Øksendal, eds.) Berlin: Springer-Verlag.

- (11) Brody, D. C., Hughston, L. P. & Macrina, A., eds. (2022) Financial Informatics: an Information-Based Approach to Asset Pricing. Singapore: World Scientific Publishing Company.

- (12) Brody, D. C., Hughston, L. P. & Yang, X. (2013) Signal Processing with Lévy Information. Proceedings of the Royal Society A 469, 20120433:1-23.

- (13) Cohen, S. N. & Elliot, R. J. (2015) Stochastic Calculus and Applications, second edition. New York: Birkhäuser.

- (14) Dothan, M. U. (1990) Prices in Financial Markets. Oxford, New York: Oxford University Press.

- (15) Filipović, D., Hughston, L. P. & Macrina, A. (2012) Conditional Density Models for Asset Pricing. International Journal of Theoretical and Applied Finance 15 (1), 1250002:1-24.

- (16) Fukuda, K., Kondo, K. & Tadaka, H. (2019) Price Dynamics under the Information-Based Dealer Model. Journal of Mathematical Finance 9, 726-746.

- (17) Hoyle, E. (2010) Information-Based Models for Finance and Insurance. PhD Thesis, Imperial College London.

- (18) Hoyle, E., Hughston, L. P. & Macrina, A. (2011) Lévy Random Bridges and the Modelling of Financial Information. Stochastic Processes and their Applications 121, 856-884.

- (19) Hoyle, E., Hughston, L. P. & Macrina, A. (2015) Stable-1/2 Bridges and Insurance. In Advances in Mathematics of Finance (A. Palczewski & L. Stettner, eds.) Banach Center Publications 104, 95-120. Warsaw: Polish Academy of Sciences.

- (20) Hoyle, E., Macrina, A. & Mengütürk, L. A. (2020) Modulated Information Flows in Financial Markets. International Journal of Theoretical and Applied Finance 23 (4), 2050026.

- (21) Hughston, L. P. & Macrina, A. (2012) Pricing Fixed Income Securities in an Information Based Framework. Applied Mathematical Finance 19 (4), 361-379.

- (22) Hughston, L. P. & Sánchez-Betancourt, L. (2020) Pricing with Variance-Gamma Information. Risks 8 (4), 105.

- (23) Hurd, T. R. (2016) Contagion ! Systemic Risk in Financial Networks. Springer Briefs in Quantitative Finance.

- (24) Macrina, A. (2006) An Information-Based Framework for Asset Pricing: X-factor Theory and its Applications. PhD Thesis, King’s College London.

- (25) Macrina, A. & Sekine, J. (2019) Stochastic Modelling with Randomized Markov Bridges. Stochastics 19, 1-27.

- (26) Mengütürk, L. A. (2013) Information-Based Jumps, Asymmetry and Dependence in Financial Modelling. PhD Thesis, Imperial College London.

- (27) Protter, P. E. (2004) Stochastic Integration and Differential Equations, second edition. Berlin, Heidelberg, New York: Springer-Verlag.

- (28) Rutkowski, R. & Yu, N. (2007) An Extension of the Brody-Hughston-Macrina Approach to Modeling of Defaultable Bonds. International Journal of Theoretical and Applied Finance 10 (3), 557-589b.

- (29) Sato, K. (1999) Lévy Processes and Infinitely Divisible Distributions. Cambridge University Press.

- (30) Williams, D. (1991) Probability with Martingales. Cambridge University Press.

- (2) Aydın, N. S. (2017) Financial Modelling with Forward-Looking Information. Cham, Switzerland: Springer.