[2]

Profit Shifting of Multinational Corporations Worldwide

Abstract

We exploit the new country-by-country reporting data of multinational corporations, with unparalleled country coverage, to reveal the distributional consequences of profit shifting. We estimate that multinational corporations worldwide shifted over $850 billion in profits in 2017, primarily to countries with effective tax rates below 10%. Countries with lower incomes lose a larger share of their total tax revenue due to profit shifting. We further show that a logarithmic function is better suited for capturing the non-linear relationship between profits and tax rates than linear or quadratic functions. Our findings highlight effective tax rates’ importance for profit shifting and tax reforms.

Keywords — multinational corporation, corporate taxation, profit shifting, effective tax rate, country-by-country reporting, global development

JEL — F23, H25, H26, H32

1 Introduction

Corporate tax avoidance contributes to the view of globalisation as inequitable. Publicised case studies, such as those based on the Panama and Paradise Papers, have detailed how little some large multinational corporations (MNCs) pay in corporate income tax as a result of their profit shifting to low-tax jurisdictions or tax havens. The case studies are not exceptions, with MNCs estimated to shift up to 40% ($600 billion–$1.1 trillion) of their foreign profits to tax havens such as the Netherlands, Switzerland or Bermuda [94, 152]. Corporate tax avoidance is problematic because it affects the efficiency and equity of financial markets and societies [148]. For example, large MNCs in the United Kingdom pay lower taxes than domestic firms [88]. Despite recent growth in research interest in tax havens generally [161, 135, 82] and profit shifting in particular [96, 107, 125, 139, 120, 156, 151], we still lack reliable estimates on the origin and destination of profit shifting for many countries worldwide, which is necessary to understand the potential effects of international tax reforms.

In this paper, we exploit a new dataset and develop a novel methodology to address the question of the distributional consequences of profit shifting of MNCs worldwide. Specifically, we answer the following four research questions: (i) What is the scale of profit shifting? (ii) Which tax havens are the largest? (iii) Which MNCs are the most aggressive in profit shifting? (iv) Which countries lose the most relative to their total tax revenues? These intrinsically linked research questions lack definitive answers due to both data-related and methodological challenges. Profit shifting as a form of tax avoidance cannot be directly observed and it is not clear how economists should estimate it. However, the data utilised as well as the choice of function to model the relationship between tax rates and profits have crucial implications for answers to our research questions. In this paper, we address these challenges by using a new country-by-country reporting (CBCR) dataset with vastly improved country coverage and by modelling the extreme non-linearity of that relationship—two contributions that we now outline before proceeding to our main findings.

Our first contribution is to pioneer the use of CBCR by MNCs, alongside several other concurrent studies. These unique data were first made available in 2020 thanks to a new regulation, which emerged from the Base Erosion and Profit Shifting project by OECD, that requires all large MNCs to report profits and taxes in every country, including tax havens and low-income countries. For example, the US CBCR data include 25 African countries, while the frequently used US Bureau of Economic Analysis data only include three. We provide our own estimates of profit shifting for a total of 214 countries using data from 38 headquarter countries, including the major economies of the United States, China and India. While CBCR data include the most reliable country-level information on tax payments and profits of MNCs worldwide, CBCR data aggregate small countries into categories (e.g. “Other Africa”), and might be prone to double-counting of profits due to a lack of clarity in reporting of intercompany dividends and so-called stateless entities. We address the double-counting of profits by developing a method for estimating missing data, disaggregating categories into individual countries, and eliminating double-counting of dividends.

Our second contribution is a methodological one: we propose to model the extremely non-linear relationship between profit location and MNCs’ tax rates using a logarithmic function. We build on literature that confirmed the existence of profit shifting, pioneered by [124, 129]. The headline specification of that approach assumes a linear semi-elasticity, which [113] show to underestimate profit shifting to low-tax jurisdictions. [113] instead introduce a quadratic semi-elasticity, which does constitute an improvement. However, we show that not even the quadratic model is capable of capturing the empirically observed extreme non-linearity in the data: 85% of profit shifted takes place towards countries with tax rates below 10%. In this paper, we therefore introduce a logarithmic model to fully capture the extreme non-linearity of the semi-elasticity of profits to tax rates. Although estimates of the global scale of profit shifting are similar for linear, quadratic and logarithmic functions as well as a simpler misalignment model measuring the difference between locations of profits and economic activity, they differ substantially at the country level: the logarithmic function and the misalignment model point to profits being shifted relatively more to countries with zero or very low effective tax rates. This naturally has implications for the estimated distributional consequences of profit shifting to tax havens.

We apply the logarithmic model to the CBCR data to establish the scale and distribution of profit shifting in many countries worldwide, revealing four main findings that answer the four research questions outlined above. First, MNCs shifted over $850 billion in profits to tax havens in 2017, which in turn implies $200–300 billion in revenue losses for other countries. Our total estimates of profit shifting are broadly comparable to existing estimates such as [152] and [159], who estimate profit shifting to be $616 billion in 2015 and $969 billion in 2019—see Table A25 for a more detailed comparison with [152] and Table A13 for a comparison with additional studies. By combining our modelling approach with the extreme non-linearity and exceptionally high coverage of our dataset (214 countries), we arrive at semi-elasticity estimates that are consistent with higher shares of profits in tax havens.

Second, we proceed to estimating which tax havens are the largest. The large majority of shifted profits are shifted to a small group of countries with extremely low effective tax rates (ETRs), defined as the ratio of accrued taxes over profits. We find that the Cayman Islands, Luxembourg, Singapore, Canada, the Netherlands, Switzerland, Hong Kong, Bermuda, Puerto Rico and Ireland are the largest destination of profits. In contrast with the consistent estimates across models of the overall scale, the largest tax havens—as well as the countries affected by them—differ substantially between models. The United Kingdom is seen as a source of profits in the misalignment model, while a recipient of profits (given its low tax rate) in other models. The misalignment and logarithmic model agree that the vast majority of profits in small tax havens (e.g., the Cayman Islands or Luxembourg) are shifted there, while the quadratic and linear models are not able to capture the extent of profit shifting. Moreover, high-income countries capture most of the tax revenue gains due to being destinations of profit shifting.

Third, among headquarter countries reporting on over 20 jurisdictions, MNCs headquartered in the United States, Brazil and Singapore are the most aggressive in terms of profit shifting. In contrast, we find no evidence of profit shifting towards tax havens by MNCs headquartered in South Africa and Malaysia. While a great deal of previous research has been carried out on US-headquartered MNCs due to data availability, our results highlight that they are not necessarily representative of all MNCs and that there are important differences across countries. Consequently, policymakers might negotiate international agreements differently if they know how aggressive their own MNCs are in comparison with other countries’ MNCs with respect to profit shifting.

Fourth, we contribute to the ongoing discussion of which countries lose more tax revenue due to profit shifting. CBCR data has much higher country coverage (214 countries) and includes many lower-income countries for the first time. We find that it is precisely these lower-income countries that tend to lose more tax revenue due to profit shifting relative to their total tax revenue, directly contravening one of the goals of the 2030 Agenda for Sustainable Development, namely to: “Strengthen domestic resource mobilization, including through international support to lower-income countries, to improve domestic capacity for tax and other revenue collection”. In absolute terms, the United States is estimated to suffer the most from profit shifting while other high-income countries such as Germany and France are estimated to lose up to half of their profit base in this manner.

Overall, our paper’s enhanced methodology and data provide a possible resolution to the inconsistency between so-called micro and macro estimates of profit shifting found in existing literature. Specifically, the relatively low (micro) estimates of tax semi-elasticity in earlier studies [86, 128] could not explain the (macro) estimates of the high shares of profits reported by MNCs in tax havens [162, 109]. In this paper, we show that one explanation for the apparent inconsistency is the manner in which the relationship between profits and tax rates has been modelled using mostly linear and, far less frequently, quadratic functions [113, 140]. When we instead use a logarithmic function to allow for the relationship’s extreme non-linearity, we arrive at high estimates of tax semi-elasticity at low levels of ETRs and, consequently, a very high share of profits in a number of tax havens with low ETRs. While the CBCR data may need to be provided at firm level or for several years to facilitate even more nuanced findings, such as on the incidence or industry heterogeneity of profit shifting worldwide, our improved methodology and dataset do help reconcile the micro and macro estimates.

We structure the rest of the paper as follows. In Section 2, we introduce the new logarithmic model designed to estimate the scale and distribution of profit shifting to tax havens and compare it with existing specifications of the semi-elasticity model. We then describe how we reallocate the shifted profit from tax havens to other countries, as well as including the so-called misalignment model as an alternative to the semi-elasticity model. In Section 3, we discuss the available datasets used to estimate profit shifting, mainly the CBCR data. In Section 4, we show how our methodology improves profit shifting estimation using the US CBCR data, applies the methodology to the OECD CBCR data to obtain global estimates, and describes how profit shifting differs by countries’ per capita income. In Section 4, we also summarise several robustness checks and sensitivity analyses with which we show that our findings are robust to changes in the methodology. In Section 5, we conclude the paper.

2 Methodology for estimating profit shifting

In this section we first introduce the traditional methodology for estimating profit shifting using linear and quadratic specifications (Section 2.1). We then detail our logarithmic specification as this paper’s preferred way of estimating the scale of profit shifting to tax havens (Section 2.2). We proceed to describe how the shifted profit is reallocated from tax havens to other countries on the basis of economic activity (Section 2.3). Finally, we describe how we apply this logic of shifted profit reallocation to estimate the scale of profit shifting itself using the so-called misalignment model (Section 2.4).

2.1 Semi-elasticity model

MNCs can, and many of them do, engage in shifting profit to tax havens where they seek lower taxation of their profits—a recent review of existing literature is provided by [86]. The profit booked in a jurisdiction by MNCs () can be expressed as a sum of the ”real unobserved profits” () and profits shifted into the jurisdiction () minus the cost of profit shifting incurred by the MNCs ():

| (1) |

While various methodologies have been used to estimate profit shifting (e.g. [131, 157, 83, 110, 102, 84]), profit shifting is most frequently modelled using the method proposed by [129]. This method assumes that the cost of profit shifting increases quadratically with the fraction of profit shifted (this assumption and other theory-related issues are discussed in more detail in section A.2). The booked profits () are maximised subject to the existence of profit shifting. Subsequently, theoretical profits are identified with the Cobb-Douglas production function, yielding equation 2 for the first-order Taylor expansion and equation 3 for the first-order Taylor expansion around the two values of the Lagrange multiplier where profit shifting becomes zero (it is worth noting that the points where profit shifting becomes zero are far from the most interesting cases: tax havens, see section A.2):

| (2) |

| (3) |

where represents profits booked in country , including both real profit and profit shifted, and and are the capital and labour components of the Cobb-Douglas production function, usually operationalised with total tangible assets and wages. is either the tax rate of the subsidiary, the difference of tax rates between the subsidiary and the parent, or, less frequently (due to lacking data), between the subsidiary and other subsidiaries, and are controls including e.g. GDP per capita and population.

Both equations are currently viewed as traditional methods. However, follow-up studies use equation 2 and its modifications much more than equation 3, even though [129] noted that the results of 3 suggest that the effect is strongest at low tax rates. Recent research has revisited the possibility of significant curvature in the relationship between tax rates and reported profits. In particular, [113] apply equation 3 to a panel dataset of US tax returns spanning the 2002–2012 period and find that the effect of tax on profit shifting is not linear, namely that incentive to shift profits from a country with a tax rate of 20% to one with a tax rate of 0% is more than double compared to incentive to shift profits from a country with a tax rate of 20% to one with a tax rate of 10%. [113] account for this non-linearity by including a quadratic term.

2.2 Addressing extreme non-linearity: A logarithmic model

In this paper, we argue that the non-linearity of tax semi-elasticity is too extreme to be adequately accounted for using linear or quadratic models. We argue that the assumption of the quadratic relationship between the fraction of profit shifted and the cost of profit shifting, while suitable for the transfer pricing of physical goods where arm-length prices are more readily available, is not suitable for profit shifting strategies based on financial assets such as intellectual property or intra-group lending. In these strategies, the costs of profit shifting are largely fixed and do not differ significantly with profits. As such, the cost as a fraction of profits shifted is high for low fractions of profit shifted and subsequently decreases [111]. Once a tax avoidance structure is in place (e.g. intellectual property located in a tax haven), we assume that the costs do not increase much with each additional dollar of profit shifted through it. Consequently, since they constitute a small share of their overall costs and are typically much lower than the tax avoided through profit shifting, these costs are minor for large MNCs (and only those are included in the CBCR data). By contrast, smaller companies may not find it viable to set up such tax avoidance structures at all and this dichotomy has been observed previously [134, 104]; indeed, large MNCs tend to be responsible for the bulk of profit shifting [158]. Moreover, these costs are comparable regardless of which tax haven profits are shifted to. Firms thus have an incentive to shift profits to tax havens with the lowest effective taxation available, not merely to countries with lower ETRs, and, therefore, models including a logarithmic semi-elasticity would more effectively model profit shifting.

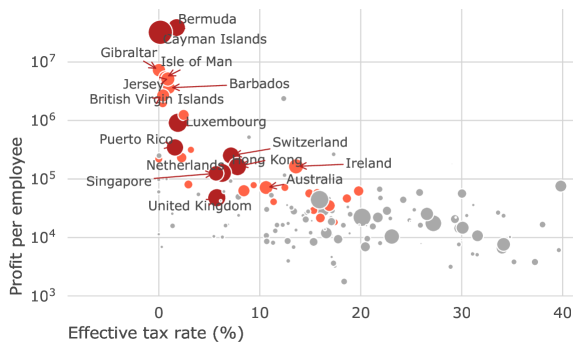

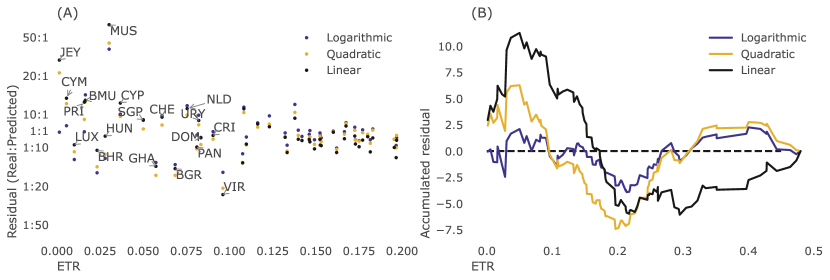

This theoretical prediction is empirically backed by three observations. The first takes into account the extreme non-linearity of the profitability of firms in tax havens. The reported profit per employee is relatively constant around $30,000 to $50,000 per employee in all countries with an ETR over 10%, and exponentially increases as the ETR falls below that level (Fig. 1). The second observation focuses on the empirical results by [113]. Their discontinuity model yields semi-elasticities for ETRs below 10% which are twice as large as those yielded by their quadratic model, indicating that the extreme non-linearity is not fully captured using a quadratic term. The third observation is derived from our data-driven exploration of the data (see Appendix A.5), where we use symbolic regression to obtain models which best fit the data. All of these models include a term which allows for extreme non-linearity semi-elasticities: a logarithmic term.

Notes: Profit per employee as a function of the ETR using the OECD data. Colour indicates the ETR (below or above 10%). Note that the horizontal axis is logarithmic, and as such the effect of effective tax rate on the profitability per employee, which is driven in a large part by profit shifting, is extremely non-linear. The horizontal axis is cut at 40% to increase readability. Only nine countries have a tax rate above 40% (Angola, Guyana, Malawi, Niger, Nigeria, Pakistan, Reunion, Rwanda, Tonga).

We argue that including a logarithmic term enables us to capture the extreme non-linearity better than the inclusion of a quadratic term, and we show this empirically in the results section. In order to model the extreme non-linearity, we propose to modify the equation as follows:

| (4) |

where is the tax rate faced by the subsidiary which we proxy by ETRs (and is an offset parameter, which we discuss below). Likewise, three recent influential profit shifting studies all use ETRs to estimate profit shifting in one way or another [96, 125, 152]. ETRs are superior to statutory rates because they are capable of better capturing the actual tax rate faced by MNCs and are more likely to be used by MNCs for profit shifting decision-making. A great deal of existing literature (e.g. [108]) uses statutory rates, arguing that they are determined by governments and are thus generally exogenous to firms’ choices (and mostly for comparability, we present estimates using statutory rates for both data sets in Tables A16 and LABEL:tab:cit_etr_oecd, which show that these models generally perform worse than those with ETRs: for the US data, they have lower R-squared in every case and the BIC values are higher with the exception of the linear model). Such endogeneity might be of importance for the research question of whether MNCs shift profits to countries with low tax rates, of which there is now abundant evidence [86]. However, once we move on to the scale, destinations and origins of profit shifting, the informativeness about the actual rates MNCs face becomes more important. In particular, statutory rates are not very informative about the taxes MNCs face (e.g. what [108] highlighted as some possibility of mismeasurement of actual tax rates), correlate only weakly with various measures of ETRs [119] and do not seem to sufficiently explain the location of profits (e.g. Section A.5). For example, Luxembourg had a statutory rate of 29.22% in 2017, whereas our ETR estimate for the same year is 1% (Table 2) and is in line with ETR estimates from other data sources [121].

In equation 4, is an offset parameter, included in order to avoid obtaining extremely high differences in the tax semi-elasticity for countries with similar but extremely low tax rates. We obtain the optimal value of the offset (0.0011 for US data and 0.0023 for OECD data) numerically by iterating over the range 0–0.2 and keeping the value that minimises the Bayesian Information Criterion. In section 4.4 we show that our results are highly robust to the choice of the offset, and that including this parameter in the linear and quadratic models does not increase their predictive power. We further include headquarter-country fixed effects to account for differences in profitability and data reporting methods between MNCs headquartered in different countries, and interaction terms between the country fixed effects and , which capture differences in the profit shifting aggressiveness of the MNCs of different reporting countries.

Consistently with literature, we operationalise capital () using tangible assets, and labour () using wages. A limitation of the operationalisation of the capital component through tangible assets is that tangible assets are affected by profit shifting strategies. For example, US MNCs in Luxembourg report the second highest value of tangible assets in Europe according to the CBCR data, with a combined value of $223 billion (equal to values reported by US MNCs in the rest of the European Union, excluding tax havens). As a consequence, the use of tangible assets yields conservative estimates of the tax semi-elasticity. Since the data does not include wages, we model them using the product of employees and the average salary in each country, obtained from the International Labour Organization. Missing values in the average salary are estimated using a linear model containing log-GDP and log-Population ().

After estimating the tax semi-elasticities using equation 4, we calculate for each pair of countries (headquarter country and jurisdiction of operation) the underlying profits without profit shifting, . To do this we remove the effect of tax rates by comparing the profits reported in country i with profits in a hypothetical scenario where the country’s ETR is 25%:

| (5) |

This ETR threshold of 25% corresponds roughly to a zero marginal effect of the ETR on profits in the quadratic and logarithmic models, as explored further in the results section. Since MNCs do not appear to shift profits to countries with ETRs above 15%, and our threshold is 25%, is almost always larger than . The results are robust to changes in this threshold. A threshold of 20% reduces the estimate of profit shifting using the logarithmic model by 8%, the estimate using the quadratic model by 11% and the estimate using the linear model by 19%. This is expected, since the vast majority of profits are shifted towards countries with extremely low tax rates, which the logarithmic models can account for. In addition, we observe in Orbis that most MNCs indeed have opportunities to shift profits to tax havens. Specifically, 3,804 out of 5,391 (70%) corporate groups, accounting for 89.7% of profits in Orbis, have a subsidiary in one of the following tax havens: Bermuda, Ireland, Luxembourg, Netherlands, Switzerland, Cayman Islands, British Virgin Islands, Hong Kong, and Singapore.

2.3 Reallocating shifted profits

We now proceed to describe how the shifted profit is reallocated from tax havens to other countries and start by discussing how it is linked with the equation 1 above. Profit shifting is calculated as the difference of the booked profits and the estimated profits, assuming that the cost of profit shifting is negligible (as discussed in section 2.2 above):

| (6) |

Since is almost always larger than , does not correspond to profit shifted in or out of the country (i.e. ). For this to happen, we need to redistribute shifted profits to where real economic activity takes place:

| (7) |

where the change in profits due to profit shifting, , is defined as the profits shifted out of the country, (we reverse its sign since measures profits shifted into a country), plus the share of total profit shifted redistributed back to the country.

We define the redistribution formula, , operationalising real economic activity, as

| (8) |

where 25% of the weight is given to employees (), 25% to wages () and 50% to unrelated party revenues (). We use unrelated party revenues, which are less affected by tax-planning strategies than, for example, tangible assets. This is the same formula used by the misalignment model described in section 2.4. The reallocation of shifted profits to the jurisdictions where economic activity takes place is also used in the impact assessment of the [143] BEPS plan in both pillar one (excess profit allocation) and pillar two (operationalization of the undertaxed payments rule), as well as by [87]—i.e., it is common to use a formulary approach to identify where the economic activity takes place. In the sensitivity analysis, we test that our results are robust to changes in the redistribution formula. The alternative redistribution of using bilateral balance of payments data [152] is not feasible due to the poor coverage of that data for many countries worldwide [98].

After the redistribution, the sum of the change in profits due to profit shifting, , sums to zero.

Finally, tax revenue loss, , is the product of the change in the profit base and the ETR (and we use the statutory rate as a robustness check):

| (9) |

2.4 Misalignment model

In addition to various semi-elasticity model specifications, we estimate the scale of profit shifting based on profit misalignment. The misalignment model applies basic arithmetic to the data to observe how well the location of reported profits are aligned with the location of economic activity, typically approximated by a combination of labour (measured using wages and employees), capital (often approximated with tangible assets) and revenue. Profit misalignment is then calculated as the difference between reported profits () and estimated theoretical profits (()). In our version of this method, and as in equation 8, we calculate giving 25% of the weight to employees, 25% of the weight to wages, and 50% of the weight to unrelated party revenues (eq. 10). Since the majority of profits are shifted towards a small number of tax havens, the exact formula has little impact on the aggregated estimation of profit shifting, although can affect the results for individual countries (which we explore in section 4.4).

| (10) |

Profit shifting is again calculated as the difference between booked profits and the estimated profits (eq. 6). In a pure misalignment model, the sum of profit shifting is equal to zero ( and ). We, however, add one extra constraint, similarly to [143]. We set the profit misalignment of all foreign observations (pairs of reporting and investment countries where the reporting and investment countries are different) with a tax rate higher than 25% to zero, since we assumed that an MNC would not shift profits to a country with a tax rate over 25%. This corrects for extreme outliers, such as the high profits of of MNCs in resource-rich countries compared with the economic activity in the countries. In order to ensure that , we redistribute the profits as in section 2.3.

The logarithmic and misalignment models have different advantages. The logarithmic model explicitly models the observed extremely non-linear relationship between profits and tax rates (Fig. 1), and as such provides an estimate on the tax semi-elasticities (which we later visualize in Figures 2 and A16). In contrast, the misalignment model provides a better estimate of the origin and destination countries of profit shifting because it takes into consideration the current distribution of profits. The logarithmic model is agnostic to this fact, and redistributes the profits only as a function of the location of economic activity.

The redistribution of shifted profits works differently in the two methods, as we illustrate in the following example. Assume that $9 million profits are located in the US, $0 million are located in India and $1 million are located in the Cayman Islands. In contrast, the wages and sales in the United States add up to $9 million, $1 million in India and in $0 million in the Cayman Islands. Both the logarithmic and the misalignment models would find that the shifted profit or the total misalignment is approximately $1 million (located in the Cayman Islands), but the redistribution would differ. The logarithmic model would redistribute 90% of those shifted profits to the US and 10% to India. Since the profits in the US are comparable to the economic activity, the misalignment model would redistribute 0% of those profits to the US and 100% to India. Since the misalignment model takes into consideration the degree of profit shifting out of a country—as our example illustrates—the redistribution of profits is more accurate and realistic under the misalignment model than under the logarithmic specification.

3 Data

Our paper exploits the CBCR dataset that became available in July 2020, and is of unprecedented quality. The dataset was created thanks to a CBCR regulation that stems from OECD Base Erosion and Profit Shifting (BEPS) Action 13, and requires all large MNCs to report how much tax they pay in individual countries, including tax havens. The regulation impacts MNCs with consolidated annual group revenue of €750 million and above, headquartered in any country that has adopted the CBCR regulation. The firm-level data is collected by the headquarter country (a template is depicted in Fig. A8), aggregated by country of operations, and published by the OECD. The published data, which we use in this paper, is thus aggregated at the country level for each reporting country — for example, India publishes data on the operations of India-headquartered MNCs in Ghana, Switzerland and many other countries.

To our knowledge, there are now several concurrent research papers using CBCR data from the US [105, 97, 96, 119, 122, 141], Italy [91], Germany [118] and, most recently, Germany and other countries [116], and this has been the first paper using the OECD CBCR data.

We use the 2017 OECD CBCR data, which contains data for 38 headquarter countries (see Table A4). The US IRS has been publishing CBCR data approximately one year before it is published by the OECD, which has allowed previous researchers to compare US CBCR with other sources [96, 119], and established a good correlation between various types of data sources. Moreover, the CBCR data is outstanding in at least three dimensions.

First, one of the most obvious advantages of CBCR data over other data sources is its much more substantial country coverage. This is especially relevant for lower-income countries and for selected parts of the world, for which coverage from other data sources is notoriously limited [119]. For example, US CBCR data includes information on taxes and profits for US MNCs in 25 African countries, while the frequently used data from the Bureau of Economic Analysis of the United States Department of Commerce only covers 3. CBCR data includes data on large MNCs’ profits and tax payments in, for example, up to 145 (United States) and 198 (Japan) jurisdictions in the full dataset. The exceptional data coverage of up to 214 countries enables us to estimate the scale of profit shifting for lower-income countries. This country coverage is one reason why [154] propose to use this CBCR data for the Sustainable Development Goals indicator of illicit financial flows, likely in a similar way that we implement the profit misalignment method outlined in Section 2.4.

Second, CBCR ensures that profits and taxes are defined consistently with the concepts of corporate profits and taxes. By contrast, this is not the case with, for example, Bureau of Economic Analysis data, where profits are imputed from a combination of net profits, intra-group dividends, interest paid and other variables, as recently discussed by [96, 95, 89, 119]. Consequently, CBCR data excludes double-counting in revenue.

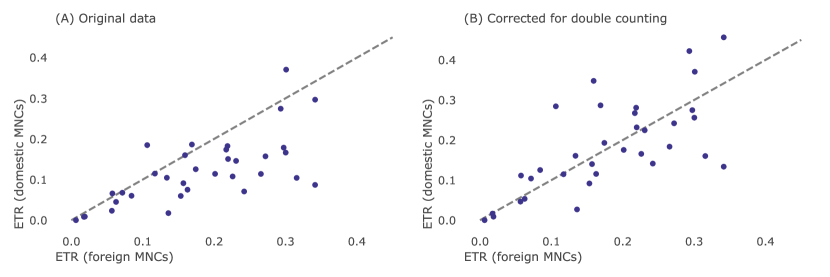

However, a certain extent of double counting in profit due to intercompany dividends, for which we correct, and stateless entities, which we drop from our analysis, is inevitable and confirmed by existing evidence on which we build. Specifically, we correct for double counting in profit in five ways that we briefly summarise here and discuss in more detail in the Appendix A.1. First by excluding stateless entities. Second, some countries such as the Netherlands investigated the extent of double counting in domestic profits and we use their corrections. Third, we remove double counting of US profits, as estimated by [122]. Fourth, we remove 10% of profits in tax havens for non-US MNCs (a similar ratio that the one found by [122] for US MNCs). Fifth, we remove certain domestic profits in other countries depending on the relative difference between ETR on domestic and foreign profits. When corrected for double-counting in profits, CBCR data offers the best available information on MNCs’ tax payments for many countries, it thus provides us with the first suitable dataset for a high-quality cross-country comparison—until now various proxies for profits were used, for example, by [126], [90] or [103].

Third, CBCR data is provided in two separate datasets, for all subsidiaries (“All Sub-Groups”), as well as for those subsidiaries that had positive profits and so not losses (“Sub-Groups with Positive Profit”). While the data on affiliates with positive profits has lower coverage (Table A4), it allows for more accurate estimates of the ETRs.

3.1 Use of data in the logarithmic and misalignment models

We use different subsets of the data for different parts of the methodology. We estimate ETR as the ratio of accrued taxes over profits, using the data on “sub-groups with positive profits”. By using the data with positive profits only, we avoid offsetting firms with losses and firms with profits, and we can thus estimate ETRs more precisely. Since taxes are typically paid by companies earning profits, including companies making losses would overstate ETRs. We use ETRs in two parts of the paper: to calculate profit shifting in the semi-elasticity models, and to calculate tax revenue losses. For the semi-elasticity models we remove outliers—country dyads with tax rates above 50%. This eliminates outliers and allows for a more efficient estimation of the semi-elasticities. To calculate tax revenue losses we use the average ETR in the country, using the average ETR paid by foreign MNCs and the statutory tax rate as robustness checks. The average ETR is weighted by profits booked: . For countries that are only available in the data on all sub-groups but not in the data on sub-groups with positive profit, we used the statutory corporate income tax rate (which was the case for Anguilla, Antigua and Barbuda, Cuba, Djibouti, French Guiana, Guadeloupe, Haiti, Kiribati, Kosovo, Kyrgyz Republic, Sao Tome and Principe, St. Lucia, St. Vincent & Grenadines, Syria, Turkmenistan, Turks and Caicos Islands). The ETRs are reported in Table LABEL:tab:n_ETR_country.

First, we estimate the semi-elasticity model (detailed in section 2.1) using data on “sub-groups with positive profits”. In addition, we run a robustness check and find no significant differences with the full sample, see section 4.4 for more information. Table LABEL:tab:stats shows the summary statistics of the CBCR data for the countries in this sample, distinguishing between domestic and foreign activities of MNCs—domestic ones are those in the reporting (i.e. headquarter) countries, while foreign ones are those in all other countries (i.e. except for the domestic one). For most countries domestic profits and activities are higher than foreign ones. The observed balance between domestic and foreign activities provides useful guidance for when we estimate missing data in Section A.1.

Second, we reallocate profits shifted (equation 8) using the dataset including all sub-groups for the 38 countries that reported some information. Using the complete dataset allow us to more accurately measure information on real economic activities of MNCs regardless of whether the affiliates are profit- or loss-making. Since MNCs prefer to report losses in countries with high taxes while locating their profits in countries with low taxes, excluding loss-making affiliates would exclude an important component of profit shifting (see Figure A9 for a visualisation of this behaviour in the CBCR data, and [106] for an empirical confirmation using tax returns data in the United Kingdom). The dataset on all sub-groups is also more suitable for comparison with other datasets (e.g. from the Bureau of Economic Analysis).

Finally, and for the same reasons explained in the previous paragraph, we used data on all sub-groups for the misalignment model. The ETRs (used to calculate tax revenue losses) are still calculated from the data on sub-groups with positive profit. Since the misalignment method is not affected by outliers we keep all observations in the sample.

While we make use of the substantial country coverage and other advantages of CBCR data, we carefully deal with several remaining challenges associated with the new data source, particularly missing data and double counting of profits. We describe how we address the data limitations in detail in Appendix A.1.

4 Results

The results section is composed of four parts. In the first part we demonstrate the advantage of our methodology using the US CBCR data. In the second part we apply our methodology to the OECD CBCR data, and compare it to estimates generated using other methodologies. In the third part we test whether the scales of profit shifting and associated tax revenue loss are higher or lower in some country groups. In the fourth part, we present a series of robustness tests and sensitivity analyses.

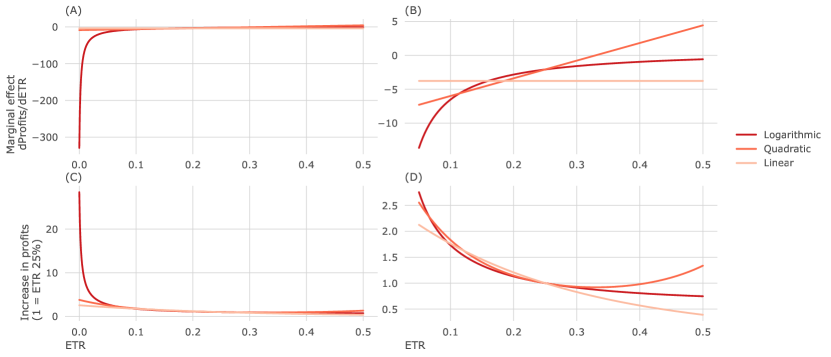

4.1 Estimation of profit shifting (US data): the logarithmic model versus other models

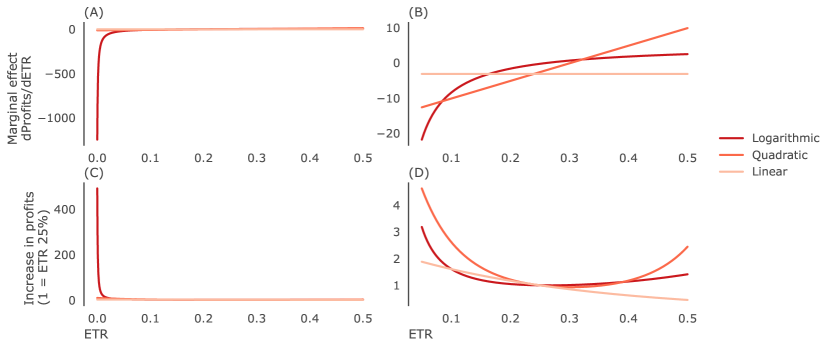

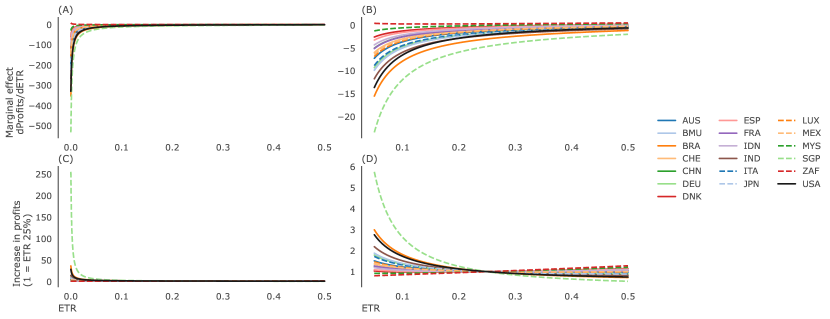

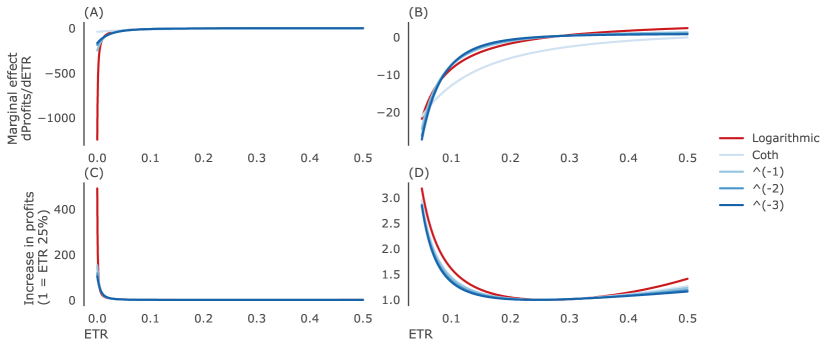

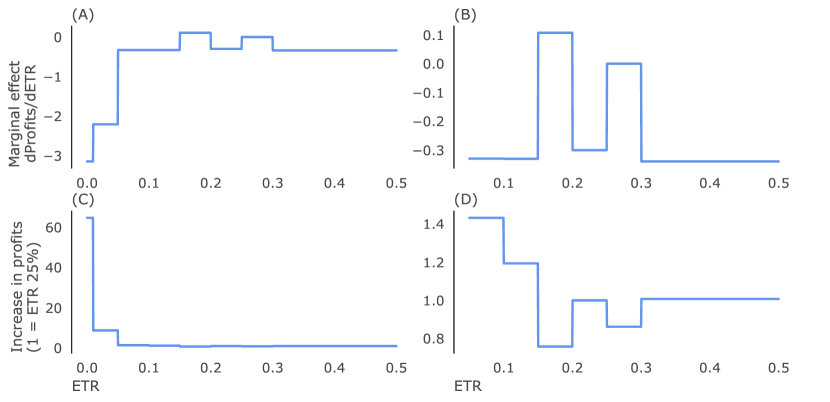

We first test our methodology using only US CBCR data. Restricting our analysis to US data allows us to compare with previous analysis, including one of the best-regarded papers on profit shifting using tax semi-elasticities, [113]. The results of our regressions (Table 1) shows that the logarithmic model fits the data better than any other model. This not only involves a higher R-square and lower Bayesian information criteria, but also a better disaggregation of the origin and destination of profits shifted. Fig. 2 shows a graphical interpretation of the coefficients. The logarithmic model is capable of accounting for extreme ratios of profit shifted in small countries with low ETRs, while at the same time avoiding the overestimation of profit shifted in countries with tax rates above 15%. For a country with a tax rate of 15% (e.g. Australia), the logarithmic model estimates that 16% of the profits are shifted in, while the quadratic and linear models estimate that number to be 40 and 26% respectively. Importantly, the logarithmic model and the misalignment model clearly identify that the majority of profits in small countries with extremely low tax rates are shifted there. This effect is less pronounced for the quadratic model, and especially so for the linear model (Table 2). For an ETR of 1.7% (e.g. Bermuda), the logarithmic and quadratic model estimates that 91% and 86% of the booked profits have been shifted into the country (and 98.5% with the misalignment method below), while the linear model estimates that only 52% have.

| Log | Quad | Log+Quad | Linear | |

| ETR | 5.1998*** | -15.1545*** | 8.4752 | -3.1654*** |

| (1.4324) | (3.0356) | (5.2472) | (1.0062) | |

| ETR2 | 24.9745*** | -5.0609 | ||

| (6.0246) | (7.7973) | |||

| log(0.0011 + ETR) | -1.3813*** | -1.5210*** | ||

| (0.1959) | (0.2915) | |||

| log(Tangible assets) | 0.5456*** | 0.6745*** | 0.5412*** | 0.7595*** |

| (0.0751) | (0.0815) | (0.0756) | (0.0861) | |

| log(Wages) | 0.2481*** | 0.1163 | 0.2541*** | 0.0442 |

| (0.0885) | (0.0977) | (0.0893) | (0.1049) | |

| log(Population) | 0.1638* | 0.1094 | 0.1602* | 0.0200 |

| (0.0859) | (0.0983) | (0.0863) | (0.1046) | |

| log(GDP per capita) | 0.1664 | 0.2132 | 0.1638 | 0.2347 |

| (0.1316) | (0.1510) | (0.1322) | (0.1646) | |

| N | 91 | 91 | 91 | 91 |

| R-squared | 0.8850 | 0.8481 | 0.8856 | 0.8170 |

| R-squared Adj. | 0.8768 | 0.8372 | 0.8759 | 0.8062 |

| BIC | 230.48 | 255.83 | 234.53 | 268.26 |

Notes: Comparison of semi-elasticities for the logarithmic (Log), quadratic (Quad), the combination of the two (Log+Quad) and linear (Linear) models using the 2017 US CBCR data. The dependent variable for all models is profits booked in country in logarithm. (We include the combination of the two (Log+Quad) models in this and other regression tables as a robustness check to test whether the Log model was not better because it was more complex; the results show that adding a Quad term to the Log model does not improve the model.)

Notes: Graphical representation of Table 1 for the logarithmic, quadratic, linear models. (A, B) Marginal effect of ETR on profits. (C,D) Relative increase in profits due to profit shifting, compared with a country with an ETR of 25%. Plots B and D are close-ups of plots A and C respectively, constraining ETRs between 5 and 50%. Note that the marginal effects for the logarithmic model decreases (becomes more negative) faster than other models as the ETR approaches 0%.

| Country | ETR | Profits (+) | Profits (all) | Misal. | Log | Quad | Linear |

|---|---|---|---|---|---|---|---|

| Jersey | 0.1% | $12.8 bn | $10.5 bn | 97.3% | 99.4% | 89.0% | 54.5% |

| Cayman Islands | 0.6% | $56.1 bn | $52.7 bn | 98.8% | 97.6% | 88.3% | 53.9% |

| Other Europe | 0.8% | $13.6 bn | $0.0 bn | - | 96.5% | 87.9% | 53.6% |

| Luxembourg | 1.0% | $54.4 bn | $22.4 bn | 92.0% | 95.2% | 87.5% | 53.2% |

| Puerto Rico | 1.6% | $31.7 bn | $30.9 bn | 94.9% | 91.8% | 86.4% | 52.3% |

| Bermuda | 1.7% | $31.9 bn | $29.2 bn | 98.5% | 91.4% | 86.2% | 52.2% |

| Other America | 2.4% | $12.2 bn | $-0.1 bn | - | 86.4% | 84.7% | 51.1% |

| Singapore | 5.0% | $51.1 bn | $49.2 bn | 78.2% | 68.6% | 78.4% | 46.9% |

| Switzerland | 6.1% | $53.3 bn | $44.4 bn | 79.4% | 61.3% | 75.3% | 45.0% |

| Netherlands | 7.5% | $63.0 bn | $36.0 bn | 79.2% | 51.9% | 70.7% | 42.4% |

| United Kingdom | 11.6% | $81.7 bn | $18.1 bn | - | 29.8% | 55.2% | 34.5% |

| Hong Kong | 12.3% | $12.2 bn | $11.1 bn | 48.0% | 26.8% | 52.3% | 33.1% |

| Ireland | 13.8% | $30.8 bn | $26.5 bn | 54.3% | 20.9% | 45.8% | 29.9% |

| Canada | 15.2% | $40.1 bn | $31.7 bn | 7.5% | 15.8% | 39.2% | 26.6% |

| Australia | 15.3% | $18.1 bn | $14.8 bn | 27.8% | 15.6% | 38.9% | 26.4% |

| Japan | 20.5% | $25.5 bn | $24.9 bn | 44.9% | 3.8% | 15.6% | 13.2% |

| China | 23.0% | $28.5 bn | $26.8 bn | - | 1.1% | 6.1% | 6.1% |

| Germany | 24.9% | $19.8 bn | $6.8 bn | - | - | 0.3% | 0.4% |

| Brazil | 25.5% | $12.0 bn | $5.9 bn | - | - | - | - |

| Nicaragua | 26.7% | $17.7 bn | $0.1 bn | - | - | - | - |

| India | 33.0% | $13.7 bn | $11.8 bn | - | 3.3% | - | - |

| United States | 42.8% | $602.8 bn | $542.8 bn | - | 16.9% | 27.0% | - |

Notes: Profit shifted into countries estimated using a variety of models and the US CBCR data. The table shows the percentage of profits shifted for the misalignment (Misal.) model using data on all sub-groups, and—using data on affiliates with positive profits—logarithmic (Log), quadratic (Quad), and linear (Linear) models. The column “profits (+)” indicates the profits of affiliates with positive profits, the column “profits (all)” indicates the profits of all affiliates.

Figure 2 shows a U-shaped relationship in the effect of ETRs on profits. The semi-elasticity is negative until the ETR reaches approximately 25%, thereafter becoming positive. This is due to high profits in countries rich in natural resources, such as Angola, the United Arab Emirates, Qatar, Norway and Nigeria. These countries levy resource taxes while carrying out activities that produce vast amounts of profit in relation to the labour and capital costs. In order to correct for this in our estimates of profit shifting, we assume a tax semi-elasticity of zero if the ETR is higher than 25%. This approach is also used in the Impact Assessment of the BEPS plan [143].

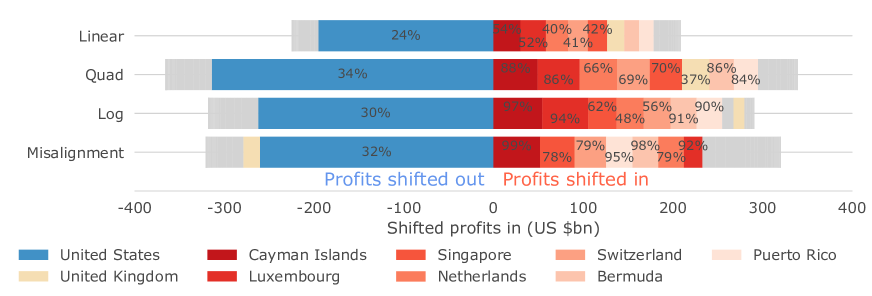

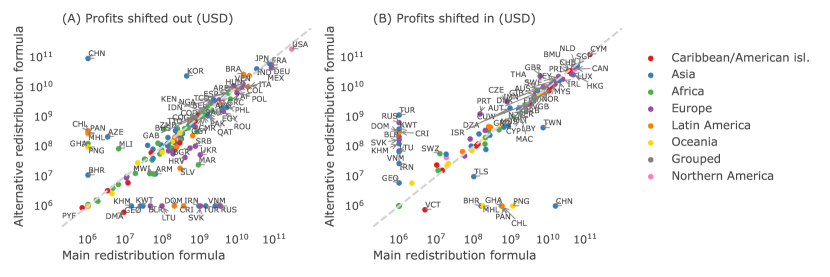

Next, we redistribute the profits shifted according to equation 8 to calculate global profit shifting. The logarithmic model yields an estimate of $364 billion of profit shifted, comparable to the $323 billion of profit shifted found by the misalignment strategy (Figure 3). Since our objective in this section is to compare the different methodologies and not to present the scale of profit shifted for individual countries, we do not try to disaggregate categories, such as “Other Europe”, into individual countries, as detailed in section A.1 and as applied in section 4.2. The destination of shifted profits is similar between models (Figure 3 and A10). The majority of these profits are in a small group of tax havens. The large majority of profits shifted, are shifted to the top 10 countries shown in Table 2. Moreover, over 75% of the profits booked in those 10 countries are artificially shifted there. The Cayman Islands, Luxembourg, the Netherlands, Switzerland, Singapore, Bermuda and Puerto Rico are the largest destinations. However, several differences may be observed. Profit shifted to Luxembourg is more than two times larger in the logarithmic rather than misalignment model, because of the presence of many companies with losses and different data used for the two models. Compared with the $22 billion of profits found in Luxembourg in the data on “All Sub-Groups” (used for the misalignment model), there is $54 billion of profits in the data “Sub-Groups with positive profits”. Similarly, while the “Other Europe”, “Other Asia&Oceania” and “Other America” groups appear as profit destinations in the logarithmic model, they appear as places of profit origin in the misalignment. This is due to the higher granularity of the data with “All Sub-Groups” used for the misalignment model. There, “Isle of Man”, “Barbados”, “Gibraltar”, “Macao” and “the British Virgin Islands” appear as standalone countries, with $22 billion booked into those countries.

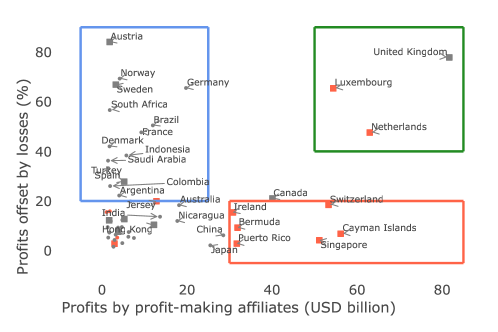

Notes: Profits shifted in and out of countries using the US data, estimated with with the linear, quadratic (Quad), logarithmic (Log) and misalignment models. MNCs shift profits from countries with negative shifted profits to countries with positive shifted profits. The largest origins of the profits are visualised in blue, and the largest destinations in red. All other countries are visualised together in grey. The annotations indicate the percentage of profit shifted out of the country (compared to estimated profits) or into the country (compared to booked profits).

The origin of shifted profits is, however, considerably different across the models. We observe that 72% of the employees, wages and sales of US MNCs are located in the United States and the ETR of the United States is 43%. This together implies that no profits are shifted into the US, and approximately 72% of the global shifted profits are redistributed back to the United States in the models relying on semi-elasticity. In the misalignment model a similar level of profits are shifted out of the USAsince 48% of the profits are already reported there. In addition to the US, the UK also seems to lose out in the misalignment model, but not in the other models (Fig. 3). In the tax semi-elasticity models, the low ETR of the UK (12%) implies that profits are expected to be shifted into the country. In the misalignment model profits are found to be shifted out of the country, since the profits reported in the UK (1.5% of the total) are lower than their share of the economy (3.3% of the total). The low aggregated profits recorded in the UK are a consequence of MNCs reporting zero or negative profits [88].

Overall, while we consider the logarithmic specification to be more accurate with respect to estimating the global scale of profit shifting, the misalignment method might provide more accurate estimates of the redistribution of these shifted profits. The misalignment method takes into consideration the current distribution of profits, and in this respect provides a more accurate way of redistributing profits, as we have discussed at the end of the methodology section 2. The location of profits and economic activity is often more balanced (i.e. less misaligned) in countries with high per capita income (Fig. A10 in the Appendix). The logarithmic model is agnostic to this fact, and redistributes the profits only as a function of the location of economic activity. As a consequence, the misalignment model typically redistributes more profits back to lower-income countries.

4.2 Estimation of profit shifting (OECD data)

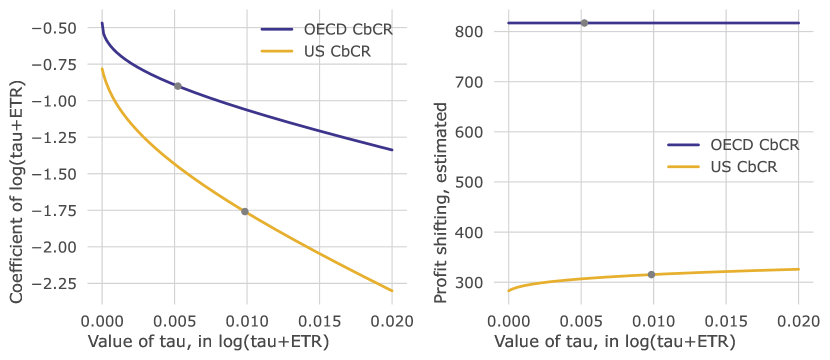

Having shown that the logarithmic model is superior to both the quadratic and linear models, we apply it to the OECD CBCR data. We use the same methodology as in the previous section, but add fixed effects for the reporting countries to correct for differences in profitability due to the location of headquarters, and add an interaction between the reporting country and either , or in our logarithmic, quadratic and linear models.

Table 3 shows the estimates of tax semi-elasticity using the OECD data (with an interpretation of the coefficients given visually in Figure A16). The US is used as the reference group for country comparisons. We again observe that the logarithmic model fits the data better than the quadratic and linear specifications. The logarithmic model estimates that over 40% of profit shifting takes places towards countries with an ETR below 1% (Table 4). The quadratic and linear models are not able to capture this fully (Table 4). The misalignment model yields similar results to the logarithmic model, reinforcing the accuracy of the logarithmic model.

| Logarithmic | Quadratic | Log*FE + Quad | Log + Quad*FE | Linear | |

| ETR | 0.9313 | -8.5950*** | 1.5638 | 0.6666 | -3.7698*** |

| (0.7316) | (2.0412) | (1.8934) | (2.0052) | (0.3623) | |

| ETR2 | 13.0086*** | -1.1865 | -1.2082 | ||

| (3.9734) | (3.2164) | (3.5384) | |||

| log(0.0023 + ETR) | -0.7626*** | -0.7817*** | -0.4012*** | ||

| (0.0788) | (0.0848) | (0.0930) | |||

| Australia:tax | 0.3816*** | 4.2074*** | 0.3807*** | 2.7669** | 1.6438*** |

| (0.0471) | (1.2526) | (0.0484) | (1.2730) | (0.4634) | |

| Bermuda:tax | 0.2434*** | -0.9764 | 0.2439*** | -1.3191 | -0.9521*** |

| (0.0259) | (1.0674) | (0.0262) | (1.1076) | (0.3177) | |

| Brazil:tax | -0.0517 | -1.5007 | -0.0505 | -2.8834* | -2.0144*** |

| (0.0341) | (1.5443) | (0.0346) | (1.4777) | (0.3989) | |

| Switzerland:tax | 0.4475*** | 2.7625*** | 0.4485*** | 2.7460*** | 2.9171*** |

| (0.0244) | (0.3537) | (0.0235) | (0.3293) | (0.1867) | |

| China:tax | 0.4961*** | 3.3578*** | 0.4957*** | 2.5759*** | 1.8940*** |

| (0.0192) | (0.6916) | (0.0196) | (0.6705) | (0.1017) | |

| Germany:tax | 0.2750*** | 0.8763*** | 0.2765*** | 0.7850*** | 1.3159*** |

| (0.0294) | (0.2102) | (0.0291) | (0.2001) | (0.1539) | |

| Denmark:tax | 0.6250*** | 8.0680*** | 0.6245*** | 7.5109*** | 3.6067*** |

| (0.0350) | (0.7957) | (0.0351) | (0.7826) | (0.1935) | |

| Spain:tax | 0.5907*** | 3.9825*** | 0.5889*** | 2.8803*** | 2.4847*** |

| (0.0235) | (0.8224) | (0.0257) | (0.7778) | (0.1168) | |

| France:tax | 0.4934*** | 3.0331*** | 0.4952*** | 2.4200*** | 3.5035*** |

| (0.0721) | (0.4119) | (0.0734) | (0.4265) | (0.1727) | |

| Indonesia:tax | 0.5351*** | 0.7934 | 0.5397*** | 2.4612 | 1.9278** |

| (0.0453) | (1.5095) | (0.0481) | (1.5396) | (0.7508) | |

| India:tax | 0.1467*** | -3.3621*** | 0.1489*** | -2.8247*** | -1.5550*** |

| (0.0416) | (0.8267) | (0.0415) | (0.9031) | (0.3596) | |

| Italy:tax | 0.2978*** | 3.3342** | 0.2930*** | 0.4478 | 0.4584** |

| (0.0352) | (1.6581) | (0.0425) | (1.4797) | (0.1807) | |

| Japan:tax | 0.2457*** | -1.7402* | 0.2462*** | -2.1359** | -0.6353** |

| (0.0315) | (1.0264) | (0.0311) | (1.0368) | (0.2695) | |

| Luxembourg:tax | 0.4013*** | 11.3447*** | 0.4014*** | 9.5510*** | 1.7322*** |

| (0.0385) | (2.3111) | (0.0387) | (2.3102) | (0.2663) | |

| Mexico:tax | 0.4254*** | 3.0125* | 0.4268*** | 3.3186** | 1.9125** |

| (0.0843) | (1.6854) | (0.0837) | (1.6929) | (0.8231) | |

| Malaysia:tax | 0.6954*** | 19.4704*** | 0.6960*** | 19.3316*** | 4.0391** |

| (0.0805) | (7.2946) | (0.0801) | (7.3789) | (1.5871) | |

| Singapore:tax | -0.4671*** | -6.1132*** | -0.4660*** | -5.6146*** | -4.2840*** |

| (0.0361) | (0.7610) | (0.0352) | (0.7757) | (0.3474) | |

| South Africa:tax | 0.7822*** | 12.0999*** | 0.7831*** | 12.2542*** | 5.0063*** |

| (0.0497) | (1.4844) | (0.0491) | (1.5910) | (0.3831) | |

| log(Tangible assets) | 0.3379*** | 0.3389*** | 0.3381*** | 0.3416*** | 0.3395*** |

| (0.0454) | (0.0439) | (0.0453) | (0.0440) | (0.0455) | |

| log(wages) | 0.1847*** | 0.1623*** | 0.1847*** | 0.1744*** | 0.1544*** |

| (0.0462) | (0.0455) | (0.0464) | (0.0465) | (0.0472) | |

| log(Population) | 0.1668** | 0.1588** | 0.1661** | 0.1596** | 0.1396* |

| (0.0768) | (0.0776) | (0.0776) | (0.0773) | (0.0748) | |

| log(GDPpc) | 0.3505*** | 0.3686*** | 0.3503*** | 0.3618*** | 0.3679*** |

| (0.0957) | (0.0940) | (0.0960) | (0.0918) | (0.0970) | |

| N | 1430 | 1430 | 1430 | 1430 | 1430 |

| R-squared | 0.7314 | 0.7142 | 0.7314 | 0.7196 | 0.7115 |

| R-squared Adj. | 0.7178 | 0.6997 | 0.7176 | 0.7051 | 0.6971 |

| BIC | 5267.72 | 5356.36 | 5274.88 | 5336.68 | 5362.54 |

Notes: Regression table for the OECD data. Clustered standard errors are shown in parenthesis. Country:tax represents the interaction effect between the country and , and for our three specifications (logarithmic, quadratic and linear). The intercept and country fixed effects are not shown and are generally negative and significant at the 0.1% significance level; since the treatment group is the US, this indicates the higher profitability of US MNCs. Only countries reporting in over 20 partner jurisdictions are shown.

| ETR | Misalignment | Logarithmic | Quadratic | Linear |

|---|---|---|---|---|

| Below 5% | 40.0% | 40.6% | 33.5% | 31.6% |

| 5-10% | 30.0% | 43.1% | 40.6% | 39.8% |

| 10-15% | 15.4% | 11.8% | 16.4% | 17.2% |

| 15-25% | 9.7% | 2.7% | 4.1% | 6.1% |

| Above 25% | 4.9% | 1.7% | 5.4% | 5.3% |

Notes: Share of profit shifted into countries, grouped by the average foreign ETR in the country. The quadratic and linear models are not able to account for the large share of profits shifted into countries with ETRs below 1%. Since profit shifting is estimated at the bilateral level (reporting:partner) for the semi-elastictiy methods, a country can (rarely) have an average ETR above 25% and an ETR below 25% for some of those reporting:partner relationships.

The location of MNCs’ headquarters have been shown both theoretically and empirically to be an important consideration in the profit shifting carried out by MNCs [112, 88]. A significant number of existing studies observed profit shifting in the case of US headquartered MNCs [125, 113, 96]. For example, the ETR paid on foreign profits by US MNCs in sectors other than oil has fallen by half since the late 1990s and nearly half of this decline is estimated to be the outcome of the rise of profit shifting to tax havens [160].

The introduction of the interaction term between the country fixed-effect and , or allows us to understand the aggressiveness of each country’s MNCs with respect to profit shifting. We find that MNCs from Singapore, Brazil and the United States are the most aggressive (the magnitude of the interaction is more negative). This is in contrast with a recent paper by [88] that studies headquarter location heterogeneity for MNCs active in the United Kingdom and finds US MNCs to have a similar size of the estimated profit ratio gap as French and German MNCs. Furthermore, we find that the difference is statistically significant for all countries (Table 3). In fact, the relationship completely disappears for South Africa and Malaysia (Fig. A17). Japan is an interesting case to study due to its historically perceived distinct attitude towards tax planning [132]. Our results show that profit shifting by Japanese MNCs are similar to other MNCs.

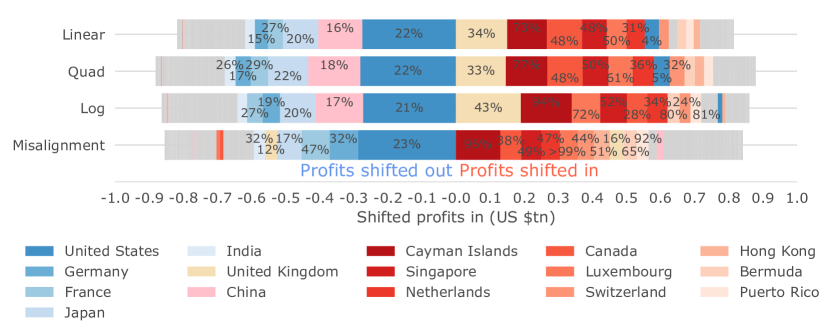

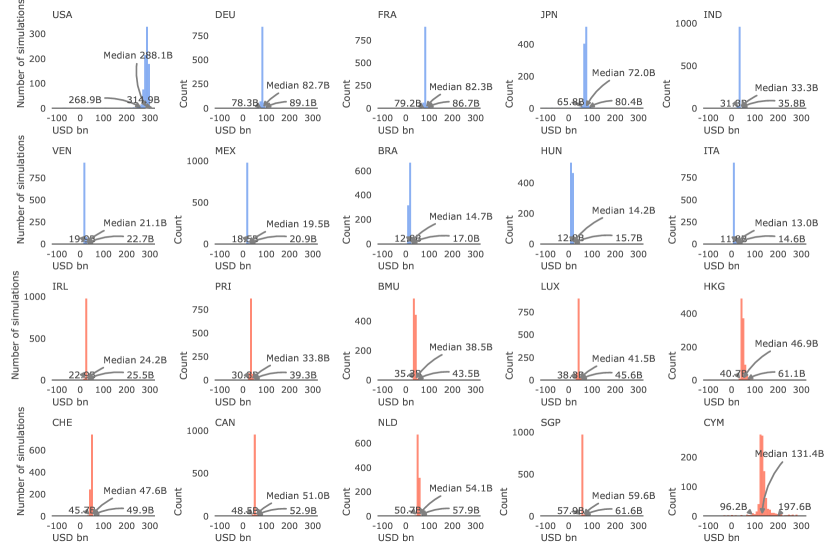

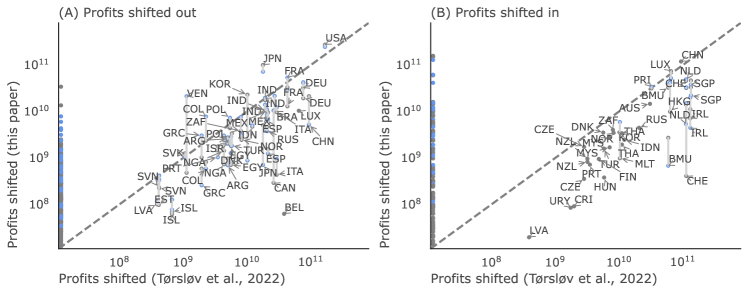

Next, we calculate the extent of profit shifting for all models. We reach an estimate of $862 billion shifted for the logarithmic model and a 95% confidence interval of $838–1,022 billion for the misalignment model, of which we use the median, $867 billion (Table A12 and Fig. 4).111Note that the sum of the median misalignment for each country is different from the median of the total misalignment. We use the median misalignment for each country which adds up to a positive misalignment of $841 billion and negative of 854B. We compare the results obtained using both methodologies in Figure A10 in the Appendix. In general, there is a good correlation between the origin and the destination of profit shifted, albeit with some outliers (the United Kingdom, Brazil, Malaysia, China), with the United Kingdom previously discussed in section 4.1. Our total estimates are comparable to existing estimates such as [152] and [159], who estimate profit shifting to be $616 billion in 2015 and $969 billion in 2019, albeit using a smaller sample of countries ((see Figure A25 for a detailed comparison)). Our findings imply that revenue losses total approximately $200–300 billion. This is comparable with recent leading estimates of revenue losses which range from $100 to $300 billion, as compared in Table A13. Furthermore, it is important to keep in mind that some aspects of our methodological approach are conservative. For example, we aggregate at the country level and as such offset profits shifted in with profits shifted out. The estimated scale of profit shifting and tax revenue loss would be higher if we would not net gains and loses.

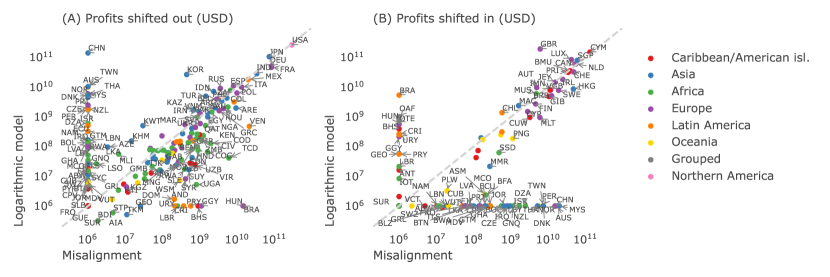

In addition to outlining the overall scale of the practice, Figure 4 provides an overview of the origins and destinations of profit shifting. Using both the logarithmic model and misalignment methods, we estimate that the Cayman Islands and the Netherlands have 94–96% and 34–47% of their respective booked profits shifted in from other countries, while also ranking among countries most benefiting from profit shifting in absolute terms. The US is estimated to suffer the most from profit shifting in absolute terms according to most of the methods, while France is affected to a substantially greater degree relative to estimated profits, with an estimate ranging from 47% (misalignment method) to 27% (logarithmic model). Table 5 and 6 shows the largest destinations and sources of profit shifting respectively.222Perhaps surprising is the inclusion of Canada as one of the top destinations. This is mostly driven by Canadian MNCs shifting profits towards the headquarters. However, this may be explained by the relatively low ETR of 12.9% observed in the data, and the characteristics of its tax system [155, 93]. Figure A11 in the Appendix shows profit shifting at the country level for all countries, 214 countries for the log and 210 for the misalignment model, and for the misalignment model we show results in Table LABEL:tab:winners_mis and we visualise the uncertainty in Figure A12.

| ETR | Misalignment | Logarithmic | |||||

|---|---|---|---|---|---|---|---|

| Country | (%) | P (all groups) | PS (B) | PS (%) | P (groups>0) | PS (B) | PS (%) |

| United Kingdom | 7.3 | 260,194 | 6,041 | 2.3 | 441,372 | 190,160 | 43.1 |

| Cayman Islands | 0.2 | 136,292 | 130,276 | 95.6 | 159,811 | 149,000 | 93.2 |

| Luxembourg | 1.8 | 48,845 | 41,520 | 85.0 | 116,346 | 83,360 | 71.6 |

| Singapore | 5.3 | 121,237 | 59,602 | 49.2 | 151,568 | 79,058 | 52.2 |

| Canada | 12.9 | 162,820 | 51,011 | 31.3 | 215,831 | 59,342 | 27.5 |

| Netherlands | 6.0 | 114,845 | 54,029 | 47.0 | 172,608 | 59,256 | 34.3 |

| Switzerland | 8.1 | 107,476 | 47,639 | 44.3 | 136,177 | 32,231 | 23.7 |

| Hong Kong | 7.8 | 91,630 | 46,727 | 51.0 | 86,695 | 8,567 | 9.9 |

| Bermuda | 1.8 | 58,903 | 55,853 | 96.0 | 43,618 | 35,089 | 80.4 |

| Puerto Rico | 1.6 | 36,570 | 33,815 | 92.5 | 38,546 | 31,090 | 80.7 |

| Ireland | 10.6 | 51,363 | 24,163 | 47.0 | 65,284 | 18,124 | 27.8 |

| Malaysia | 18.7 | 44,027 | 19,628 | 44.6 | 50,721 | -4,513 | -8.9 |

| Sweden | 10.9 | 52,014 | 18,785 | 36.1 | 61,060 | 7,729 | 12.7 |

| Australia | 19.7 | 111,334 | 17,055 | 15.3 | 126,229 | -9,854 | -7.8 |

| China | 25.9 | 583,000 | 15,511 | 2.7 | 683,371 | -139,394 | -20.4 |

| Jersey | 0.9 | 16,493 | 15,329 | 92.9 | 15,989 | 14,529 | 90.9 |

| Norway | 26.5 | 41,225 | 15,037 | 36.5 | 47,853 | -5,859 | -12.2 |

| Gibraltar | 0.0 | 12,373 | 12,248 | 99.0 | 5,511 | 5,082 | 92.2 |

| Isle of Man | 0.6 | 11,624 | 11,486 | 98.8 | 8,639 | 7,954 | 92.1 |

| British Virgin Islands | 0.4 | 12,480 | 11,100 | 88.9 | 13,759 | 7,868 | 57.2 |

| Barbados | 1.0 | 10,540 | 10,441 | 99.1 | 6,842 | 4,776 | 69.8 |

Notes: The table shows the top destinations of profit shifting (PS (B)) for misalignment and logarithmic models and as a percentage of the total profits booked in the jurisdiction (PS (%)). All countries with at least $10 bn shifted are included. The total profits for all groups ((P (all groups)) and groups with positive profits (P (groups>0) are shown for comparison. The full table can be found in Tables LABEL:tab:winners_mis and LABEL:tab:winners_log for misalignment and logarithmic models, respectively.

| ETR | Misalignment | Logarithmic | |||||

|---|---|---|---|---|---|---|---|

| Country | (%) | P (all groups) | PS (B) | PS (%) | P (groups>0) | PS (B) | PS (%) |

| Sorted by total profit shifted (average of the two models) | |||||||

| United States | 29.6 | 954,310 | 287,971 | 23.2 | 997,467 | 259,263 | 20.6 |

| Japan | 27.4 | 346,261 | 71,961 | 17.2 | 414,662 | 104,218 | 20.1 |

| Germany | 18.3 | 175,971 | 82,717 | 32.0 | 223,988 | 51,277 | 18.6 |

| France | 25.0 | 92,626 | 82,377 | 47.1 | 122,962 | 45,784 | 27.1 |

| China | 25.9 | 583,000 | -15,511 | -2.7 | 683,371 | 139,404 | 16.9 |

| India | 41.7 | 70,523 | 33,269 | 32.1 | 88,394 | 28,086 | 24.1 |

| Mexico | 33.9 | 56,136 | 19,479 | 25.8 | 49,351 | 17,762 | 26.5 |

| South Korea | 23.0 | 102,984 | 441 | 0.4 | 130,052 | 26,236 | 16.8 |

| Italy | 21.1 | 54,621 | 13,024 | 19.3 | 71,412 | 9,984 | 12.3 |

| Spain | 14.8 | 63,375 | 7,923 | 11.1 | 72,889 | 10,976 | 13.1 |

| Brazil | 22.7 | 80,658 | 14,666 | 15.4 | 113,266 | -5,332 | -4.9 |

| Taiwan | 13.1 | 58,112 | -7,240 | -14.2 | 15,269 | 10,320 | 40.3 |

| Sorted by percentage of total profits shifted (average of the two models) | |||||||

| Kenya | 37.3 | 714 | 1,412 | 66.4 | 727 | 509 | 41.2 |

| Greece | 23.9 | 2,485 | 3,266 | 56.8 | 2,013 | 1,599 | 44.3 |

| Colombia | 34.0 | 5,258 | 8,241 | 61.0 | 5,052 | 3,143 | 38.3 |

| Nigeria | 47.8 | 10,061 | 5,627 | 35.9 | 1,269 | 2,129 | 62.6 |

| Iran | 11.1 | 4,968 | 940 | 15.9 | 487 | 1,504 | 75.5 |

| Saudi Arabia | 17.8 | 10,737 | 3,826 | 26.3 | 3,304 | 3,362 | 50.4 |

| France | 25.0 | 92,626 | 82,377 | 47.1 | 122,962 | 45,784 | 27.1 |

| Romania | 14.8 | 5,500 | 4,232 | 43.5 | 6,223 | 1,893 | 23.3 |

| Philippines | 20.5 | 13,304 | 5,276 | 28.4 | 7,714 | 4,261 | 35.6 |

| Pakistan | 41.9 | 4,501 | 1,603 | 26.3 | 2,285 | 1,379 | 37.6 |

| Egypt | 27.2 | 6,514 | 2,079 | 24.2 | 2,963 | 1,444 | 32.8 |

| India | 41.7 | 70,523 | 33,269 | 32.1 | 88,394 | 28,086 | 24.1 |

| Ukraine | 12.8 | 2,277 | 1,015 | 30.8 | 1,985 | 590 | 22.9 |

| Poland | 16.6 | 20,457 | 9,799 | 32.4 | 23,370 | 6,286 | 21.2 |

| Germany | 18.3 | 175,971 | 82,717 | 32.0 | 223,988 | 51,277 | 18.6 |

| Kazakhstan | 25.3 | 11,566 | 657 | 5.4 | 2,466 | 1,676 | 40.5 |

| Russia | 22.9 | 35,355 | 3,514 | 9.0 | 18,552 | 9,032 | 32.7 |

| Turkey | 17.1 | 18,641 | 1,432 | 7.1 | 9,695 | 4,909 | 33.6 |

| Taiwan | 13.1 | 58,112 | -7,240 | -14.2 | 15,269 | 10,320 | 40.3 |

Notes: The table shows the top sources of profit shifting (PS (B)) for misalignment and logarithmic models and as a percentage of the total profits in the jurisdiction (PS (%)). Note that the total profits is the sum of the profits booked and the profits shifted. All countries with at least $10 bn shifted out (top table) or $1bn and 20% of the total profits (bottom table) are included. The total profits for all groups ((P (all groups)) and groups with positive profits (P (groups>0) are shown for comparison. The full table can be found in Tables LABEL:tab:lossers_mis and LABEL:tab:lossers_log for misalignment and logarithmic models, respectively.

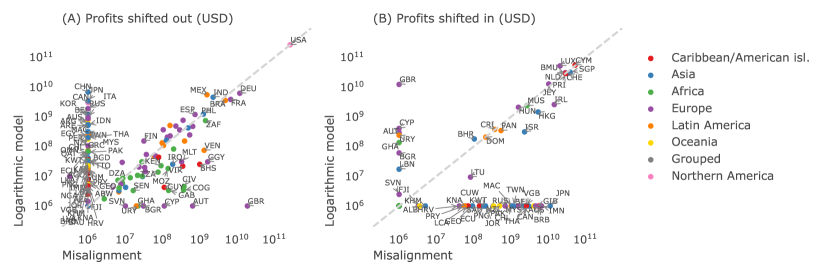

Notes: Profits shifted in and out of countries using the OECD CBCR data, estimated with the linear quadratic (Quad), logarithmic (Log) and misalignment models. MNCs shift profits from countries with negative shifted profits to countries with positive shifted profits. The largest origins of the profits are visualised in blue, and the largest destinations in red. All other countries are visualised together in grey. The annotations indicate the percentage of profit shifted out of the country (compared to estimated profits) or into the country (compared to booked profits). Tables 5 and 6 show the top sources and destinations.

4.3 Profit shifting and tax revenue loss by income groups

The analysis presented above compares different methodology approaches and establishes the largest origins and destinations of profits in absolute terms. In this section, we focus on the distribution effects of profit shifting, and find that lower-income countries tend to lose more tax revenue relative to their total tax revenue (i.e. total tax revenue collected by government, from across all types of taxes), which is in line with some of the earlier estimates (e.g., [117, 102].

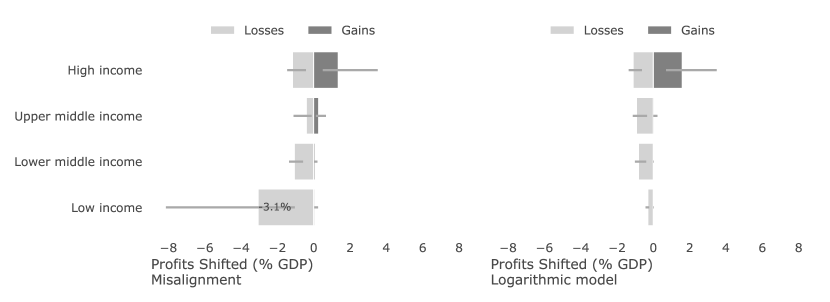

We first focus on profit shifting. While countries from all income groups lose similarly relative to their GDP, profit shifting takes place predominantly to high-income countries (Figure A18). This is expected, since the majority of tax havens are included in this group (see, e.g., [101, 152]). Although we present results for both the misalignment and the logarithmic model, we argue that the results of the misalignment model might be more accurate for two reasons. First, we use all available data in the misalignment model, imputing missing data. As previously mentioned, countries often do not report on small countries, but group them together into categories (e.g. “Other Africa”). For example, only Germany, Japan and India report operations on Gambia (three, two and two MNCs respectively), while the remaining reporting countries with operations in the country group Gambia with other African countries. For the logarithmic model this leads to an underestimation of the losses of lower-income countries. For the misalignment model, we estimate the expected employees and revenue of all country pairs, and use this information to correct the amount of profit shifted more accurately (Section 2.4). While this only increases total profit shifted by 30%, it is key to estimating profit shifting in lower-income countries accurately. A second, closely related, reason in favour of the misalignment model is its observation that profits are less aligned with economic activity in lower-income countries (discussed in Section 4.1).

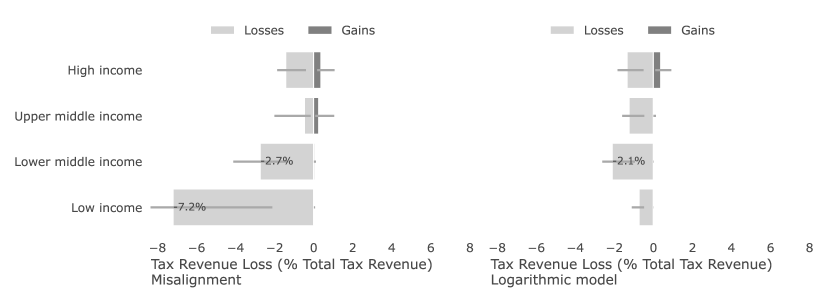

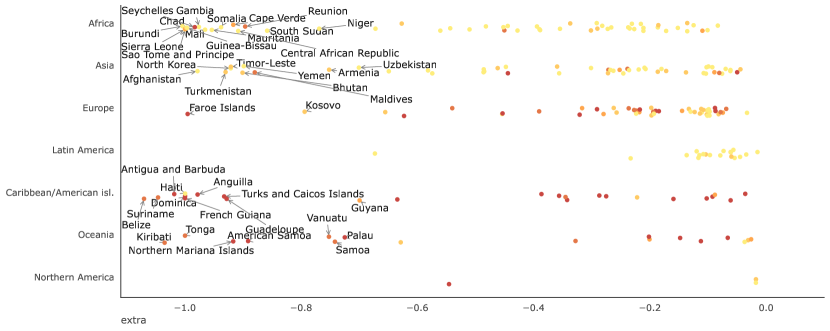

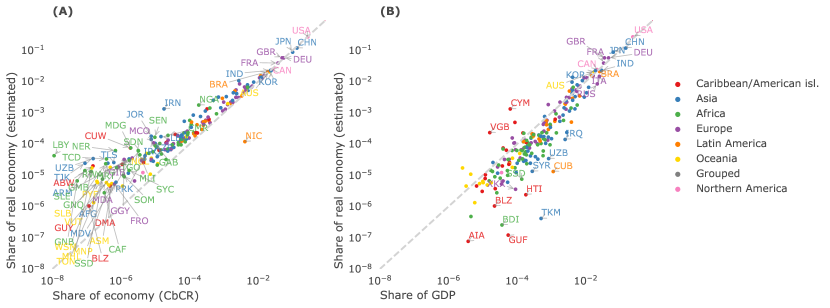

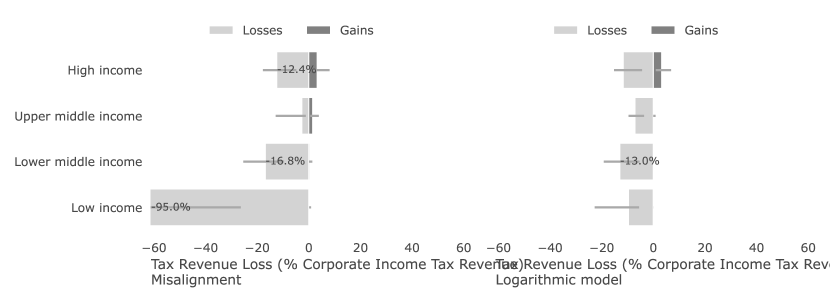

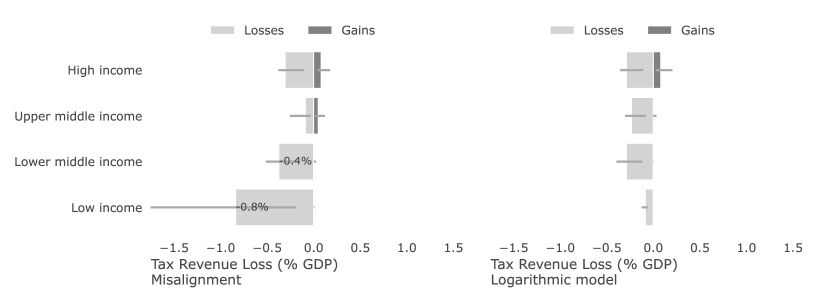

We continue by looking at tax revenue loss (the product of profits shifted and the ETR) as a function of the total tax revenue in each income group and region (Figure 5). In general, we find that lower-income-countries – those in Africa and Latin America—tend to lose more tax revenue relative to their total tax revenue. Countries with low and middle per capita incomes (Figure 5), are thus the largest profit-shifting losers. MNCs shift an equivalent of 7.19% (95% CI; 2.12–17.42) of their total tax revenue out of low-income countries, while receiving influxes equivalent to 0.02% (0.01–0.07). On the other hand, high-income countries lose an equivalent of 1.43% (0.40–1.87), while gaining 0.37% (0.18–1.07). These low tax revenue gains for high-income countries contrast with the high volume of profits shifted in those countries (Figure A18). Furthermore, losses for lower-middle-income countries (1.29–4.11) are also significantly higher than those of higher-income countries, while upper-middle-income countries exhibit only moderate loses (0.15-2.01).

Notes: Tax revenue loss as a percentage of total tax revenue for countries in different income groups (top row) and different geographical regions (bottom row), as estimated by the misalignment (left side of graph) and logarithmic (right side of graph) models. Confidence intervals show 95% intervals, calculated via bootstrapping.

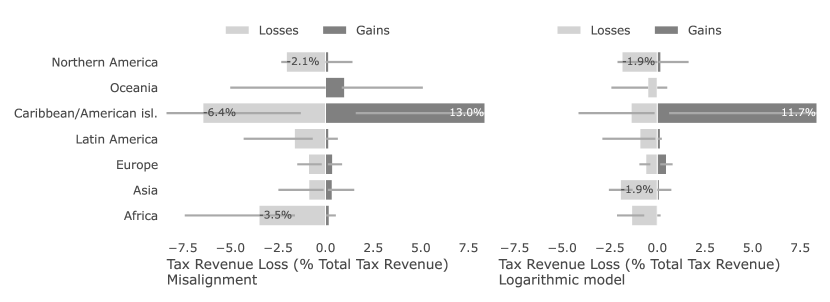

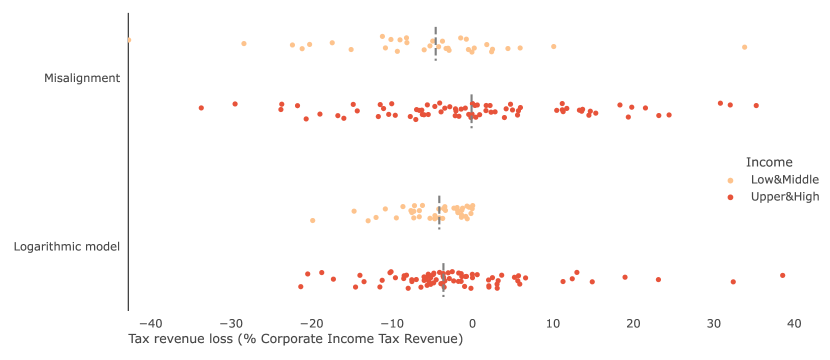

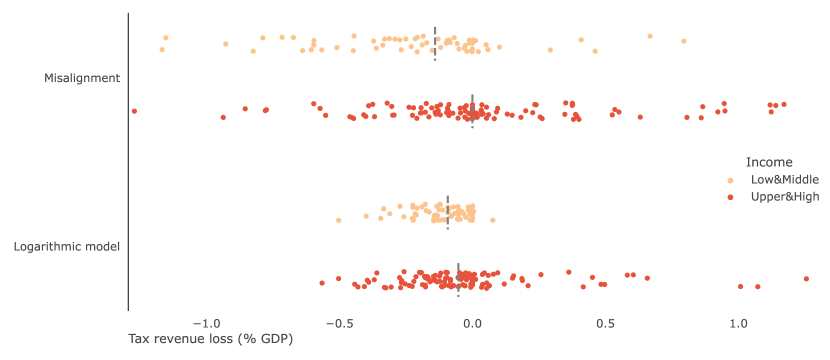

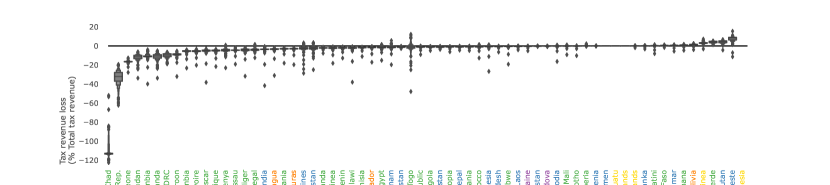

When analysing each country separately (Figure A19), we once again find that lower-income countries lose significantly more tax revenue than high- and upper-middle-income countries. Similar results are found for comparisons of tax revenue losses with corporate income tax revenue (Figure A20) and GDP (Figure A21). There are, however, differences within lower-income countries. In general, African countries tend to lose the higher share of their tax revenue to profit shifting (Figure A22). Overall, our analysis shows that only a small number of countries gain any tax revenue. Profit shifting is thus a phenomenon where the majority of countries lose, and especially so lower-income countries.

With this finding on lower-income countries we contribute to the ongoing discussion of which countries lose more to profit shifting. Few existing studies identify how countries in various income groups are distinctly affected by profit shifting, and the nature of these differences varies across the studies. On the one hand, the theoretical case for such countries’ higher vulnerability is strong [127], and several studies indicate that low- and lower-middle-income countries (which we label as lower-income countries) are more vulnerable to profit shifting by MNCs than countries at higher levels of income [117, 134]. On the other hand, [133] compare five sets of country-level estimates—[152, 94, 99, 100] and their own estimates—and four of the five do not suggest that lower-income countries are disproportionately affected by profit shifting. These five studies rely on data from a different number of countries (25, 102, 34, 37, 79), which are all small in comparison with our results for up to 214 countries.

4.4 Robustness checks and sensitivity analyses

We address the data and methodology limitations of this paper by testing the consistency of the main results to our methodological choices. In total, we carry out 10 robustness checks and sensitivity analyses. We briefly summarise them here. Overall, these robustness checks and sensitivity analyses show how our results are robust to changes in the methodology and data.

First of all, we discuss the main sensitivity analyses of our methodology that are not related to the data. (i) We use a variety of models based on linear, quadratic and logarithmic semi-elasticities, as well as the misalignment method. The scale of profit shifting is estimated to be similar across all models—$817 (linear), $880 (quadratic), $862 (logarithmic), and $867 (misalignment) billions (Sections 4.1 and 4.2). (ii) We test the robustness of the 25% ETR threshold in equation 5. Reducing the threshold to 20% would reduce our estimate of profit shifting by the logarithmic model by 6%. Increasing the threshold to 30% would increase the estimate of profit shifting by 8%. (iii) We compare our results to those of [152] and [159], observing a high correlation with a much increased country sample (Figure A25). (iv) We compare the tax revenue loss with other benchmarks, corporate tax revenue (Figure A20) and GDP (Figure A21). We find that lower-income countries lose comparatively the most in all specifications, as discussed above in section 4.3.

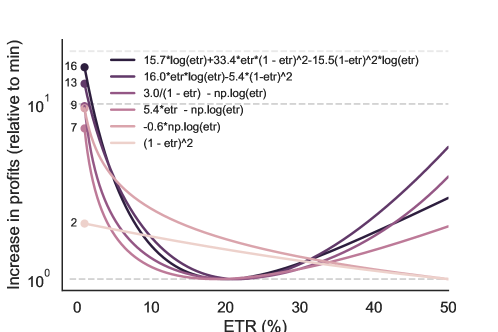

We further test the consistency of the main results to other methodological choices in three additional ways: (v) We analyse the sensitivity of our results to the offset in the logarithmic model, showing a robust estimation of the coefficients for a wide range of offsets (Figure A26). (vi) We compare the logarithmic specification with other specifications that can accommodate extreme non-linearities, including , , and . The logarithmic specification allows for higher non-linearities, and exhibits a higher R2 and lowest Bayesian Information Criteria (see Table A14 and Figs. A27 and A28). (vii) We test a different redistribution formula. For this, we first regressed the share of profits booked in a country against the shares of employees, capital, sales and wages (Table A15). We then used the coefficients as our new redistribution formula, after normalising them to sum to one. Profit shifting is reduced by 9%, with a similar distribution of the origin and destination of profits (Figure A30).

Additional robustness checks and sensitivity analyses focus on the data itself and, in particular, on missing data imputation. In accordance with the design of the individual methods, this missing data imputation does not affect our preferred semi-elasticity methods of estimating the scale of profit shifting, but only influences the measures of misalignment and the subsequent redistribution of the shifted profit for all methods: (viii) We estimate missing data using 1,000 bootstrapped data samples (Section A.1) to show the consistency of our results in relation to variations in data coverage. In the main results we use the median of the samples. The confidence intervals are included in Figure A12. (ix) We compare the location of employees and revenue according to our missing data model with the information in the original data as well as GDP, showing how our method addresses the limitations of these two alternatives (Figure A13). (x) Finally, we compare our missing data imputation method with other models, including with penalised linear regression (Appendix A.1.2), showing that our method has higher predictive power.

5 Conclusion

Exploiting the combination of a new methodology and a new dataset, we establish that MNCs shifted around $900 billion in profits to tax havens in 2017. Our results show that existing linear and quadratic models underestimate profit shifting to countries with extremely low tax rates while simultaneously overestimating it for countries with moderate rates. However, the new logarithmic model as well as the misalignment model are able to capture this behaviour accurately. Using these two preferred models, we show that 40–41% and 70–83% of profit shifted is shifted to countries with an ETR below 1% and 10%, respectively. Overall, our findings are consistent with the hypothesis that MNCs exploit the combination of globalisation and the sovereignty of individual countries, in particular tax havens, to avoid paying taxes at the expense of countries worldwide regardless of income level.

Our findings provide two key insights. First, the extremely non-linear relationship between the location of profits and tax rates has implications for both research and policy. In research, we show that accurately accounting for this relationship affects the estimated scale and distribution of profit shifting. In policy, this modelling choice can significantly influence the assessment of international tax reform, as may be the case with the global minimum tax rate agreement reached in 2021, so-called Pillar Two. While this assessment assumes that profit shifting incentives decrease in linear fashion as the minimum ETR increases, we show in this paper that this linearity assumption is unlikely to hold. Our findings indicate the importance of the specific value of the minimum ETR, which is 15% in the case of Pillar Two.

Our second key insight is based on our finding that lower-income countries tend to lose more tax revenue relative to total tax revenue due to profit shifting. This could nudge their governments into using confidential tax return data for more detailed analyses—as South Africa recently did, thus learning that profit shifting is highly concentrated among a few large MNCs [158]. In policy, our results indicate that the current international tax system may be hindering the achievement of one of the goals of the 2030 Agenda for Sustainable Development: to strengthen domestic resource mobilisation [153, 114]. This supports the arguments of lower-income countries that they should be represented on an equal footing at reform discussions and that such reforms should be geared towards creating a level playing field in the corporate taxation of MNCs.

The findings presented in this paper open up additional avenues for future research. We see two such research directions as especially fruitful. The first is obtaining more accurate estimates as new CBCR data become available in the future. For example, the guidelines to report intra-company dividends have been updated and the 2020 data, which should be published no later than in 2024, will thus contain no double counting. The second research avenue is obtaining more accurate estimates of tax semi-elasticity using firm-level data. An increasing number of MNCs (e.g. Vodafone and Shell) are voluntarily publishing their own CBCR data, and more are likely to do so in the future, either of their own accord or due to government pressure. For example, in 2021 the European Union approved a regulation whereby companies will be required to publish parts of their CBCR data, to be available from around 2025. If firm-level CBCR data become available for a large number of MNCs, it would enable us to understand even more accurately the extent of profit shifting, as well as which MNCs are responsible for the bulk of profit shifting worldwide.

References