Difference-in-Differences for Continuous Treatments and Instruments with Stayers††thanks: We are very grateful to Alberto Abadie, Federico Bugni, Ivan Canay, Matias Cattaneo, Daniel Herrera, Brian Jacob, Joel Horowitz, Thierry Mayer, Isabelle Méjean, Jean-Marc Robin, Jeffrey Wooldridge, and seminar participants at Bank of Portugal, IFAU, the International Panel Data Conference, Michigan, Northwestern, Reading, Sciences Po, 2023 North American Summer Meeting of the Econometric Society, the Stockholm School of Economics, Université Paris Dauphine, and York University for their helpful comments. Clément de Chaisemartin was funded by the European Union (ERC, REALLYCREDIBLE,GA N°101043899).

Abstract

We propose difference-in-differences estimators for continuous treatments with heterogeneous effects. We assume that between consecutive periods, the treatment of some units, the switchers, changes, while the treatment of other units does not change. We show that under a parallel trends assumption, an unweighted and a weighted average of the slopes of switchers’ potential outcomes can be estimated. While the former parameter may be more intuitive, the latter can be used for cost-benefit analysis, and it can often be estimated more precisely. We generalize our estimators to the instrumental-variable case. We use our results to estimate the price-elasticity of gasoline consumption.

Keywords: differences-in-differences, continuous treatment, two-way fixed effects regressions, heterogeneous treatment effects, panel data, policy evaluation, instrumental variable.

JEL Codes: C21, C23

1 Introduction

A popular method to estimate the effect of a treatment on an outcome is to compare over time units experiencing different evolutions of their exposure to treatment. In practice, this idea is implemented by estimating regressions that control for unit and time fixed effects. de Chaisemartin and D’Haultfœuille (2023a) find that 26 of the 100 most cited papers published by the American Economic Review from 2015 to 2019 have used a two-way fixed effects (TWFE) regression to estimate the effect of a treatment on an outcome. de Chaisemartin and D’Haultfœuille (2020), Goodman-Bacon (2021), and Borusyak et al. (2021) have shown that under a parallel trends assumption, TWFE regressions are not robust to heterogeneous effects: they may estimate a weighted sum of treatment effects across periods and units, with some negative weights. Owing to the negative weights, the TWFE treatment coefficient could be, say, negative, even if the treatment effect is positive for every unit period. Importantly, the result in de Chaisemartin and D’Haultfœuille (2020) applies to binary, discrete, and continuous treatments.

Several alternative heterogeneity-robust difference-in-difference (DID) estimators have been proposed (see Table 2 of de Chaisemartin and D’Haultfœuille, 2023b). Some apply to binary and staggered treatments (see Sun and Abraham, 2021; Callaway and Sant’Anna, 2021; Borusyak et al., 2021). Some apply to designs where all units start with a treatment equal to , and then get treated with heterogeneous, potentially continuously distributed treatment intensities (see de Chaisemartin and D’Haultfœuille, 2023a; Callaway et al., 2021). By contrast, here we allow the treatment to be continuously distributed at every period, as may for instance be the case of trade tariffs (see Fajgelbaum et al., 2020) or gasoline taxes (see Li et al., 2014). Note that de Chaisemartin and D’Haultfœuille (2023a) extend our approach to models with dynamic effects (see Section 1.10 of their Web Appendix), while this paper focuses on models where past treatments do not affect the current outcome.111de Chaisemartin and D’Haultfœuille (2023a) cover that extension in the November 2023 version of their paper, which is posterior to the first version of this paper. Allowing for dynamic effects may be appealing, but in designs with continuous treatments, doing so may lead to hard-to-interpret and noisy estimators (see de Chaisemartin and D’Haultfœuille, 2023a).

We assume that we have a panel data set, whose units could be geographical locations such as counties. We start by considering the case where the panel has two time periods. From period one to two, the treatment of some units, hereafter referred to as the switchers, changes. On the other hand, the treatment of other units, hereafter referred to as the stayers, does not change. We propose a novel parallel trends assumption on the outcome evolution of switchers and stayers with the same period-one treatment, in the counterfactual where switchers’ treatment would not have changed. Under that assumption, we show that two target parameters can be estimated. Our first target is the average slope of switchers’ period-two potential outcome function, from their period-one to their period-two treatment, hereafter referred to as the Average Of Switchers’ Slopes (AOSS). Our second target is a weighted average of switchers’ slopes, where switchers receive a weight proportional to the absolute value of their treatment change, hereafter referred to as the Weighted Average Of Switchers’ Slopes (WAOSS).

Economically, our two parameters can serve different purposes, so neither parameter dominates the other. Under shape restrictions on the potential outcome function, we show that the AOSS can be used to infer the effect of other treatment changes than those that took place from period one to two. Instead, the WAOSS can be used to conduct a cost-benefit analysis of the treatment changes that effectively took place. On the other hand, when it comes to estimation, the WAOSS unambiguously dominates the AOSS. First, we show that it can be estimated at the standard parametric rate even if units can experience an arbitrarily small change of their treatment between consecutive periods. Second, we show that under some conditions, the asymptotic variance of the WAOSS estimator is strictly lower than that of the AOSS estimator. Third, unlike the AOSS, the WAOSS is amenable to doubly-robust estimation.

Then, we consider the instrumental-variable (IV) case. For instance, one may be interested in estimating the price-elasticity of a good’s consumption. If prices respond to demand shocks, the consumption trends of units experiencing and not experiencing a price change may not be parallel. On the other hand, the consumption trends of units experiencing and not experiencing a tax change may be parallel. Then, taxes may be used as an instrument for prices. In such cases, we show that the reduced-form WAOSS effect of the instrument on the outcome divided by the first-stage WAOSS effect is equal to a weighted average of the slopes of switchers’ outcome-slope with respect to the treatment, where switchers with a larger first-stage effect receive more weight. The ratio of the reduced-form and first-stage AOSS effects is also equal to a weighted average of slopes, with arguably less natural weights, so in the IV case the WAOSS seems both economically and statistically preferable to the AOSS.

We consider a few other extensions. First, we extend our results to applications with more than two time periods. Second, we propose a placebo estimator of the parallel trends assumption underlying our estimators. Third, we discuss how our estimators can be applied to discrete treatments taking a large number of values.

Finally, we use the yearly, 1966 to 2008 US state-level panel dataset of Li et al. (2014) to estimate the effect of gasoline taxes on gasoline consumption and prices. Using the WAOSS estimators, we find a significantly negative effect of taxes on gasoline consumption, and a significantly positive effect on prices. The AOSS estimators are close to, and not significantly different from, the WAOSS estimators, but they are also markedly less precise: their standard errors are almost three times larger than that of the WAOSS estimators. For gasoline consumption, the AOSS estimator is marginally significant, and for prices it is insignificant. Thus, even if one were interested in inferring the effect of other tax changes than those observed in the data, a policy question for which the AOSS is a more relevant target, a bias-variance trade-off may actually suggest using the WAOSS. We also compute an IV-WAOSS estimator of the price elasticity of gasoline consumption, and find a fairly small elasticity of -0.76, in line with previous literature (for instance, Hausman and Newey, 1995, find a long-run elasticity of -0.81). Our estimated elasticity is 30% smaller than, but not significantly different from, that obtained from a 2SLS TWFE regression. Our placebo estimators are small, insignificant, and fairly precisely estimated, thus suggesting that switchers and stayers may indeed be on parallel trends in this application.

Stata and R packages computing our estimators will be available soon. Some of our estimators can already be computed by the did_multiplegt Stata and R packages (see the earlier versions of this paper for details).

Related Literature.

On top of the aforementioned papers in the recent heterogeneity-robust DID literature, our paper builds upon several previous papers in the panel data literature. Chamberlain (1982) seems to be the first paper to have proposed an estimator of the AOSS parameter. Under the assumption of no counterfactual time trend, the estimator therein is a before-after estimator. Then, our paper is closely related to the work of Graham and Powell (2012), who also propose DID estimators of the AOSS when the treatment is continuously distributed at every time period. Their estimators rely on a linear treatment effect assumption (see their Equation (1)) and assume that units experience the same evolution of their treatment effect over time, a parallel-trends-on-treatment-effects assumption (see their Assumption 1.1(i) and (iii)). By contrast, our estimator of the AOSS does not place any restriction on treatment effects. But our main contribution to this literature is to introduce, and propose an estimator of, the WAOSS.

de Chaisemartin and D’Haultfœuille (2018) and de Chaisemartin and D’Haultfœuille (2020) also compare switchers and stayers with the same baseline treatment, to form heterogeneity-robust DID estimators of the effect of binary or discrete treatments. Those papers have shown that comparing switchers and stayers with the same period-one treatment is important: unconditional comparisons implicitly assume constant treatment effects over time, and are therefore not robust to time-varying effects. With a continuous treatment, the sample does not contain switchers and stayers with the exact same baseline treatment, so this paper’s contribution is to use non-parametric regression or propensity-score reweighting to compare switchers and stayers “with the exact same baseline treatment”.

D’Haultfœuille et al. (2023) also consider a DID-like estimator of the effect of a continuous treatment, but their estimator relies on a common change assumption akin to that in Athey and Imbens (2006), rather than on a parallel trends assumption.

Finally, our estimators require that there be some stayers, whose treatment does not change between consecutive time periods. This assumption is unlikely to be met when the treatment is say, precipitations: for instance, US counties never experience the exact same amount of precipitations over two consecutive years. In de Chaisemartin et al. (2023), we discuss the (non-trivial) extension of the results in this paper to applications without stayers.

Organization of the paper.

In Section 2, we present the set-up, introduce notation and discuss our main assumptions. In Section 3, we introduce the AOSS and discuss its identification and estimation. Section 4 then turns to the WAOSS. Section 5 extends our previous results to an instrumental variable set-up. We consider other extensions in Section 6. Finally, our application is developed in Section 7. The proofs are collected in the appendix.

2 Set-up and assumptions

A representative unit is drawn from an infinite super population, and observed at two time periods. This unit could be an individual or a firm, but it could also be a geographical unit, like a county or a region.222In that case, one may want to weight the estimation by counties’ or regions’ populations. Extending the estimators we propose to allow for such weighting is a mechanical extension. All expectations below are taken with respect to the distribution of variables in the super population. We are interested in the effect of a continuous and scalar treatment variable on that unit’s outcome. Let (resp. ) denote the unit’s treatment at period 1 (resp. 2), and let (resp. ) be the set of values (resp. ) can take, i.e. its support. For any , let and respectively denote the unit’s potential outcomes at periods 1 and 2 with treatment .333Throughout the paper, we implicitly assume that all potential outcomes have an expectation. Finally, let and denote their observed outcomes at periods 1 and 2. Let be an indicator equal to 1 if the unit’s treatment changes from period one to two, i.e. if they are a switcher.

In what follows, all equalities and inequalities involving random variables are required to hold almost surely. For any random variables observed at the two time periods , let denote the change of from period to .

We make the following assumptions.

Assumption 1

(Parallel trends) For all , .

Assumption 1 is a parallel trends assumption. It requires that be mean independent of , conditional on . It has one key implication we leverage for identification: the counterfactual outcome evolution switchers would have experienced if their treatment had not changed is identified by the outcome evolution of stayers with the same period-one treatment:

| (1) |

Accordingly, the DID estimators we propose below compare switchers and stayers with the same period-one treatment.444As it imposes parallel trends conditional on prior treatment, Assumption 1 is connected to the sequential ignorability assumption, another commonly-used identifying assumption in panel data models (see, e.g., Robins, 1986; Bojinov et al., 2021). Sequential ignorability requires that treatment be randomly assigned conditional on prior treatment and outcome, which implies parallel trends conditional on prior treatment and outcome.

Instead, one could propose DID estimators comparing switchers and stayers, without conditioning on their period-one treatment. On top of Assumption 1, such estimators rest on two supplementary conditions:

-

(i)

.

-

(ii)

For all , .

(i) requires that all units experience the same evolution of their potential outcome with treatment , while Assumption 1 only imposes that requirement for units with the same baseline treatment. Assumption 1 may be more plausible: units with the same period-one treatment may be more similar and more likely to be on parallel trends than units with different period-one treatments. (ii) requires that the trend affecting all potential outcomes be the same. Rearranging, (ii) is equivalent to assuming

| (2) |

the treatment effect should be constant over time, a strong restriction on treatment effect heterogeneity. Assumption 1, on the other hand, does not impose any restriction on treatment effect heterogeneity, as it only restricts one potential outcome per unit.

Assumption 2

(Bounded treatment, Lipschitz and bounded potential outcomes)

-

1.

and are bounded subsets of .

-

2.

For all and for all , there is a random variable such that , with .

Assumption 2 is a technical condition ensuring that all the expectations below are well defined. It requires that the set of values that the period-one and period-two treatments can take be bounded. It also requires that the potential outcome functions be Lipschitz (with an individual specific Lipschitz constant). This will automatically hold if is differentiable with respect to and has a bounded derivative.

For estimation and inference, we assume we observe an iid sample with the same distribution as :

Assumption 3

(iid sample) We observe , that are independent and identically distributed vectors with the same probability distribution as .

3 Estimating the average of switchers’ slopes

3.1 Target parameter

In this section, our target parameter is

| (3) |

is the average, across switchers, of the effect on their period-two outcome of moving their treatment from its period-one to its period-two value, scaled by the difference between these two values. In other words, is the average of the slopes of switchers’ potential outcome functions, between their period-one and their period-two treatments. Hereafter, is referred to as the Average Of Switchers’ Slopes (AOSS). Note that with a binary treatment such that all units are untreated at period 1 and some units get treated at period 2, the AOSS reduces to the standard average treatment effect on the treated. Thus, the AOSS generalizes that parameter to non-binary treatments and more complicated designs.

The AOSS averages effects of discrete rather than infinitesimal changes in the treatment as in Hoderlein and White (2012), for instance. But if one slightly reinforces Point 2 of Assumption 2 by supposing that is differentiable on , by the mean value theorem,

for some . Then, the AOSS is an average marginal effect on switchers:

| (4) |

The only difference with the usual average marginal effect on switchers is that the derivative is evaluated at instead of . Note that (4) implies that unlike TWFE regression coefficients, the AOSS satisfies the no-sign reversal property. If for all , meaning that increasing the treatment always increases the outcome of every switcher, .

However, the AOSS is a local effect. First, it only applies to switchers. Second, it measures the effect of changing their treatment from its period-one to its period-two value, not of other changes of their treatment. Still, the AOSS can be used to identify the effect of other treatment changes under shape restrictions on the potential outcome function. First, assume that the potential outcomes are linear: for ,

where is a slope that may vary across units and may change over time. Then, : the AOSS is equal to the average, across switchers, of the slopes of their potential outcome functions at period 2. Therefore, for all ,

under linearity, knowing the AOSS is sufficient to recover the ATE of any uniform treatment change among switchers. Of course, this only holds under linearity, which may not be a plausible assumption. Assume instead that is convex. Then, for any ,

can be identified following the same steps as those we use to identify the AOSS below. Accordingly, under convexity one can use the AOSS to obtain a lower bound of the effect of changing the treatment from to a larger value than . For instance, in Fajgelbaum et al. (2020), one can use this strategy to derive a lower bound of the effect of even larger tariffs’ increases than those implemented by the Trump administration. Under convexity, one can also derive an upper bound of the effect of changing the treatment from to a lower value than . And under concavity, one can derive an upper (resp. lower) bound of the effect of changing the treatment from to a larger (resp. lower) value than .555See D’Haultfœuille et al. (2023) for bounds of the same kind obtained under concavity or convexity. Importantly, the AOSS is identified even if those linearity or convexity/concavity conditions fail. But those conditions are necessary to use the AOSS to identify or bound the effects of alternative policies.

3.2 Identification

To identify the AOSS, we use a DID estimand comparing switchers and stayers with the same period-one treatment. This requires that there be no value of the period-one treatment such that only switchers have that value, as stated formally below.

Assumption 4

(Support condition for AOSS identification) , .

Assumption 4 implies that , meaning that there are stayers whose treatment does not change. While we assume that and are continuous, we also assume that the treatment is persistent, and thus has a mixed distribution with a mass point at zero.

To identify the AOSS, we also start by assuming that there are no quasi-stayers: the treatment of all switchers changes by at last from period one to two, for some strictly positive .

Assumption 5

(No quasi-stayers) : .

We relax Assumption 5 just below.

Intuitively, the effect of changing a switcher’s treatment from its period-one to its period-two value is identified by a DID comparing its outcome evolution to that of stayers with the same period-one treatment. Then, this DID is normalized by , to recover the slope of the switcher’s potential outcome function.

If there are quasi-stayers, the AOSS is still identified. For any , let be an indicator equal to one for switchers whose treatment changes by at least from period one to two.

If there are quasi-stayers whose treatment change is arbitrarily close to (i.e. ), the denominator of is very close to for them. On the other hand,

so the ratio’s numerator may not be close to . Then, under weak conditions,

Therefore, we need to trim quasi-stayers from the estimand in Theorem 1, and let the trimming go to 0 to still recover , as in Graham and Powell (2012) who consider a related estimand with some quasi-stayers. Accordingly, while the AOSS is still identified with quasi-stayers, it is irregularly identified by a limiting estimand.

3.3 Estimation and inference

With no quasi-stayers, can be estimated in three steps. First, one estimates using a non-parametric regression of on among stayers. Second, for each switcher, one computes , its predicted outcome evolution given its baseline treatment, according to the non-parametric regression estimated among stayers. Third, one lets

where .

To estimate , we consider a series estimator based on polynomials in , . We make the following technical assumption.

Assumption 6

(Conditions for asymptotic normality of AOSS estimator)

-

1.

is continuously distributed on a compact interval , with .

-

2.

and is bounded on .

-

3.

and .

-

4.

The functions , and are four times continuously differentiable.

-

5.

The polynomials , , are orthonormal on and , .

Point 3 is a slight reinforcement of Assumption 4. In Point 5, requires that , the order of the polynomial in we use to approximate , goes to when the sample size grows, thus ensuring that the bias of our series estimator of tends to zero. ensures that does not go to infinity too fast, thus preventing overfitting.

Theorem 3 shows that without quasi-stayers, the AOSS can be estimated at the rate, and gives an expression of its estimator’s asymptotic variance. With quasi-stayers, we conjecture that the AOSS cannot be estimated at the rate. This conjecture is based on a result from Graham and Powell (2012). Though their result applies to a broader class of estimands, it implies in particular that with quasi-stayers,

cannot be estimated at a faster rate than . The estimand in the previous display is closely related to our estimand

in Theorem 2, and is equal to it if . Then, even though the assumptions in Graham and Powell (2012) differ from ours, it seems reasonable to assume that their general conclusion still applies to our set-up: here as well, owing to ’s irregular identification, this parameter can probably not be estimated at the parametric rate with quasi-stayers. This is one of the reasons that lead us to consider, in the next section, another target parameter that can be estimated at the parametric rate with quasi-stayers.

4 Estimating a weighted average of switchers’ slopes

4.1 Target parameter

In this section, our target parameter is

is a weighted average of the slopes of switchers’ potential outcome functions from their period-one to their period-two treatments, where slopes receive a weight proportional to switchers’ absolute treatment change from period one to two. Accordingly, we refer to as the Weighted Average Of Switchers’ Slopes (WAOSS). All slopes are weighted positively, so the WAOSS satisfies the no-sign reversal property, like the AOSS.

It is easy to see that if and only if

| (5) |

the WAOSS and AOSS are equal if and only if switchers’ slopes are uncorrelated with .

Economically, the AOSS and WAOSS serve different purposes. As discussed above, under shape restrictions on the potential outcome function, the AOSS can be used to identify or bound the effect of other treatment changes than the actual change switchers experienced from period one to two. The WAOSS cannot serve that purpose, but under some assumptions, it may be used to conduct a cost-benefit analysis of the treatment changes that took place from period one to two. To simplify the discussion, let us assume in the remainder of this paragraph that . Assume also that the outcome is a measure of output, such as agricultural yields or wages, expressed in monetary units. Finally, assume that the treatment is costly, with a cost linear in dose, uniform across units, and known to the analyst: the cost of giving units of treatment to a unit at period is for some known . Then, is beneficial relative to if and only if or, equivalently,

Then, comparing to the per-unit treatment cost is sufficient to evaluate if changing the treatment from to was beneficial.

4.2 Identification

Let , and

Hereafter, units with are referred to as “switchers up”, while units with are referred to as “switchers down”. Thus, is the WAOSS of switchers up, and is the WAOSS of switchers down. One has

| (6) |

To identify (resp. ) we use DID estimands comparing switchers up (resp. switchers down) to stayers with the same period-one treatment. This requires that there be no value of such that some switchers up (resp. switchers down) have that baseline treatment while there is no stayer with the same baseline treatment, as stated in Point 1 (resp. 2) of Assumption 7 below.

Assumption 7

(Support conditions for WAOSS identification)

-

1.

, and implies that .

-

2.

, and implies that .

Theorem 4

Point 1 of Theorem 4 shows that , the WAOSS of switchers-up, is identified by two estimands, a regression-based and a propensity-score-based estimand. Point 2 of Theorem 4 shows that , the WAOSS of switchers down, is identified by two estimands similar to those identifying , replacing by . Finally, if the conditions in Point 1 and 2 of Theorem 4 jointly hold, it directly follows from (4.2) that , the WAOSS of all switchers, is identified by a weighted average of the estimands in Equations (7) and (9), and by a weighted average of the estimands in Equations (8) and (10). Those weighted averages simplify into the expressions given in Point 3 of Theorem 4. Point 3 of Theorem 4 also implies that is identified by the following doubly-robust estimand:

| (13) |

4.3 Estimation and inference

The regression-based estimands identifying and can be estimated following almost the same steps as in Section 3.3. Specifically, let

where and , and where is the series estimator of defined in Section 3.3 of the paper. Then, let

and let

be the corresponding estimator of .

We now propose estimators of the propensity-score-based estimands identifying and in Equations (8) and (10). Let (resp. , ) be an estimator of (resp. , ). Let (resp. , ) be a non-parametric estimator of (resp. , ) using a series logistic regression of (resp. , ) on polynomials in . We make the following technical assumption.

Assumption 8

(Technical conditions for asymptotic normality of propensity-score WAOSS estimator)

-

1.

is continuously distributed on a compact interval , with .

-

2.

and is bounded on

-

3.

, , and .

-

4.

The functions , , and are four times continuously differentiable.

-

5.

The polynomials , are orthonormal on and where .

Let

and let

be the corresponding estimator of . Let

Based on (13), we can also estimate using the following doubly-robust estimator:

Finally, we now show that under some assumptions, the asymptotic variance of the WAOSS estimator is lower than that of the AOSS estimator. While the assumptions under which this result is obtained are admittedly strong, this still suggests that one may often expect an efficiency gain from using the WAOSS.

Proposition 1

If Assumption 1 holds, for some real number , for some real number , , and , then

with equality if and only if .

5 Instrumental-variable estimation

There are instances where the parallel-trends condition in Assumption 1 is implausible, but one has at hand an instrument satisfying a similar parallel-trends condition. For instance, one may be interested in estimating the price-elasticity of a good’s consumption, but prices respond to supply and demand shocks, and therefore do not satisfy Assumption 1. On the other hand, taxes may not respond to supply and demand shocks and may satisfy a parallel-trends assumption.

5.1 Notation and assumptions

Let denote the instrument’s values at period one and two and be the support of . For any , let and respectively denote the unit’s potential treatments at periods 1 and 2 with instrument . Let be an indicator equal to 1 for switchers-compliers, namely units whose instrument changes from period one to two and whose treatment is affected by that change in the instrument. We make the following assumptions.666Note that with our notation where potential outcomes do not depend on , we also implicitly impose the usual exclusion restriction.

Assumption 9

(Reduced-form and first-stage parallel trends) For all ,

-

1.

.

-

2.

.

Point 1 of Assumption 9 requires that , units’ outcome evolutions in the counterfactual where their instrument does not change from period one to two, be mean independent of , conditional on . Point 2 requires that units’ treatment evolutions under be mean independent of , conditional on . de Chaisemartin (2010) and Hudson et al. (2017) consider IV-DID estimands and also introduce “reduced-form” and “first-stage” parallel trends assumptions.

Assumption 10

(Monotonicity) For all , .

Assumption 10 is a monotonicity assumption similar to that in Imbens and Angrist (1994). It requires that increasing the period-two instrument weakly increases the period-two treatment.

Assumption 11

(Bounded instrument, Lipschitz and bounded reduced-form potential outcomes and potential treatments)

-

1.

and are bounded subsets of .

-

2.

For all and for all , there is a random variable such that , with .

-

3.

For all and for all , there is a random variable such that , with .

Assumption 12

(iid sample) We observe , that are independent and identically distributed with the same probability distribution as .

5.2 Target parameter

In this section, our target parameter is

is a weighted average of the slopes of compliers-switchers’ period-two potential outcome functions, from their period-two treatment under their period-one instrument, to their period-two treatment under their period-two instrument. Slopes receive a weight proportional to the absolute value of compliers-switchers’ treatment response to the instrument change. is just equal to the reduced-form WAOSS effect of the instrument on the outcome, divided by the first-stage WAOSS effect of the instrument on the treatment. Hereafter, we refer to as the IV-WAOSS. We could also consider a reduced-form AOSS divided by a first-stage AOSS. The resulting target parameter is a weighted average of the slopes , with weights proportional to . It may be more natural to weight compliers-switchers’ slopes by the absolute value of their first-stage response than by the slope of their first-stage response.

5.3 Identification

Let , , and .

Assumption 13

(Support conditions for IV-WAOSS identification)

-

1.

, and implies that .

-

2.

, and implies that .

The regression-based (resp. propensity-score-based) estimand identifying is just equal to the regression-based (resp. propensity-score-based) estimand identifying the reduced-form WAOSS effect of the instrument on the outcome, divided by the regression-based (resp. propensity-score-based) estimand identifying the first-stage WAOSS effect.

5.4 Estimation and inference

Let

| (16) |

where and are series estimators of and defined analogously to the series estimator in Section 3.3.

Let , and let

| (17) |

where , and (resp. , ) is a series logistic regression estimator of (resp. , ) defined analogously to the series logistic regression estimators in Section 4.3.

6 Extensions

In this section, we return to the case where the treatment, rather than an instrument, satisfies a parallel-trends condition. Combining the extensions below with the IV case is possible.

6.1 Discrete treatments

While in this paper we focus on continuous treatments, our results can also be applied to discrete treatments. In Section 4 of their Web Appendix, de Chaisemartin and D’Haultfœuille (2020) already propose a DID estimator of the effect of a discrete treatment. The plug-in estimator of one can form following Theorem 4 and using simple averages to estimate the non-parametric regressions or the propensity scores is numerically equivalent to the estimator therein. This paper still makes two contributions relative to de Chaisemartin and D’Haultfœuille (2020) when the treatment is discrete. First, the estimator based on Theorem 1 was not proposed therein. Second, with a discrete treatment taking a large number of values, the estimator in de Chaisemartin and D’Haultfœuille (2020) may not be applicable as it requires finding switchers and stayers with the exact same period-one treatment, which may not always be feasible. Instead, one can use the estimators proposed in this paper.

6.2 More than two time periods

In this section, we assume the representative unit is observed at time periods. Let denote the unit’s treatments and for all . For any , and for any let denote the unit’s potential outcome at period with treatment . Finally, let denote their observed outcome at . For any , let be an indicator equal to 1 if the unit’s treatment switches from period to . Let also and . We assume that the assumptions made in the paper, rather than just holding for and , actually hold for all pairs of consecutive time periods . For instance, we replace Assumption 1 by:

Assumption 14

(Parallel trends) For all , for all , .

To preserve space, we do not restate our other assumptions with more than two periods.

Let

Let

be generalizations of the AOSS and WAOSS effects to applications with more than two periods. Note that in line with the spirit of the two effects, we propose different weights to aggregate the AOSS and WAOSS across time periods. For the AOSS, the weights are just proportional to the proportion of switchers between and . For the WAOSS, the weights are proportional to the average absolute value of the treatment switch from to .

Theorem 8

Theorems 7 and 8 are straightforward generalizations of Theorems 1 and 4 to settings with more than two time periods.

Let

After some algebra, one can show that the influence function of the AOSS estimator with is several periods is

| (18) |

while the influence function of the WAOSS estimators with several periods is

| (19) |

Importantly, those influence functions allow the unit’s treatments and outcomes to be arbitrarily serially correlated.

6.3 Testing for pre-trends

With several time periods, one can test the following condition, which is closely related to Assumption 14:

Assumption 15

(Testable parallel trends) For all , for all , .

To test that condition, one can compute a placebo version of the estimators described in the previous subsection, replacing by , and restricting the sample, for each pair of consecutive time periods , to units whose treatment did not change between and . Thus, the placebo compares the average of the -to- switchers and stayers, restricting attention to -to- stayers.

7 Application

Data and research questions.

We use the yearly 1966-to-2008 panel dataset of Li et al. (2014), covering 48 US states (Alaska and Hawaii are excluded). For each stateyear cell , the data contains , the total (state plus federal) gasoline tax in cents per gallon, , the log tax-inclusive price of gasoline, and , the log gasoline consumption per adult. Our goal is to estimate the effect of gasoline taxes on gasoline consumption and prices, and to estimate the price-elasticity of gasoline consumption, using taxes as an instrument. Instead, Li et al. (2014) jointly estimate the effect of gasoline taxes and tax-exclusive prices on consumption, using a TWFE regression with two treatments. Between each pair of consecutive periods, the tax-exclusive price changes in all states, so this treatment does not have stayers and its effect cannot be estimated using the estimators proposed in this paper. Thus, our estimates cannot be compared to those of Li et al. (2014).

Switching cells, and how they compare to the entire sample.

Let be the set of switching cells such that but for some . The second condition drops from the estimation seven pairs of consecutive time periods between which the federal gasoline tax changed, thus implying that all states experienced a change of their tax. includes 384 cells, so effects of taxes on gasoline prices and consumptions can be estimated for 19% of the 2,016 stateyear cells for which can be computed. Table 1 below compares some observable characteristics of switchers and stayers. Switchers seem slightly over-represented in the later years of the panel: is on average 2.5 years larger for switchers than for stayers, and the difference is significant. On the other hand, switchers are not more populated than stayers, and their gasoline consumption and gasoline price in 1966 are not significantly different from that of stayers. Thus, there is no strong indication that the cells in are a very selected subgroup.

| Dependent Variables: | Adult Population | log(quantity)1966 | log(price)1966 | |

|---|---|---|---|---|

| Constant | 1,986.7 | 3,691,608.0 | -0.5161 | 3.471 |

| (0.2739) | (577,164.0) | (0.0210) | (0.0054) | |

| 2.481 | 39,588.0 | -0.0099 | 0.0014 | |

| (0.7519) | (320,342.1) | (0.0096) | (0.0029) | |

| N | 2,016 | 2,016 | 2,016 | 2,016 |

Notes: The table show the results of regressions of some dependent variables on a constant and an indicator for switching cells. The standard errors shown in parentheses are clustered at the state level.

Distribution of taxes.

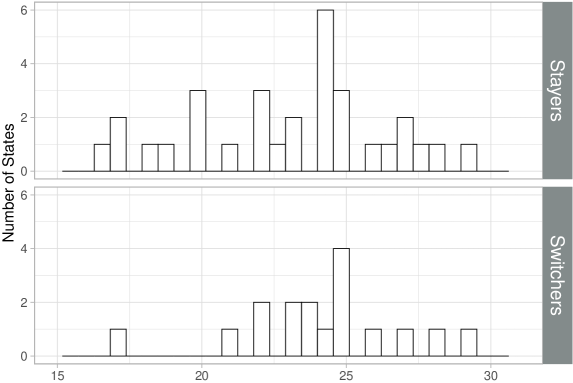

As an example, the top panel of Figure 1 below shows the distribution of for 1987-to-1988 stayers, while the bottom panel shows the distribution for 1987-to-1988 switchers. The figure shows that there are many values of such that only one or two states have that value, so is close to being continuously distributed. Moreover, all switchers are such that

Thus, Assumption 4 seems to hold for this pair of years. is not atypical. While varies less across states in the first years of the panel, there are many other years where is close to being continuously distributed. Similarly, almost 95% of cells in are such that . Dropping the few cells that do not satisfy this condition barely changes the results presented below.

Distribution of tax changes.

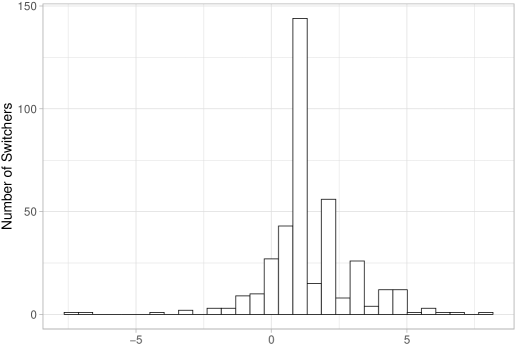

Figure 2 below shows the distribution of for the 384 cells in . The majority experience an increase in their taxes, but 38 cells experience a decrease. The average value of is equal to 1.61 cents, while prior to the tax change, switchers’ average gasoline price is equal to 112 cents: our estimators leverage small changes in taxes relative to gasoline prices. Finally, : some switchers experience a very small change in their taxes. Their slope receives a weight equal to 1/384 in the AOSS estimators, and a weight 32.2 () times smaller in the WAOSS estimators.

Reduced-form and first-stage AOSS and WAOSS estimates.

Columns (1) and (3) of Table 2 below show the AOSS and doubly-robust WAOSS estimates of the reduced-form and first-stage effects of taxes on quantities and prices. First, the estimators are computed using a polynomial of order 1 in to estimate and the propensity scores , , and . Second, as a robustness check, the estimators are computed using a polynomial of order 2 in those estimations. With 48 states, and only 20 to 30 stayers for many pairs of consecutive time periods, fitting higher order polynomials could lead to overfitting. Columns (2) and (4) show standard errors clustered at the state level, computed following (18) and (19). Column (5) shows the p-value of a test that the AOSS and WAOSS effects are equal. All estimations use 1632 (48 35) first-difference observations: 7 periods have to be excluded as they do not have stayers. In Panel A, the AOSS estimates indicate that increasing gasoline tax by 1 cent decreases quantities consumed by 0.5-0.6 percent on average for the switchers. That effect is significant at the 5% level when one uses linear models to estimate the aforementioned conditional expectations, and at the 10% level when one uses quadratic models. The WAOSS estimates are slightly lower than, but close to, the AOSS estimates. As predicted by Proposition 1, the standard errors of the WAOSS estimators are almost 3 times smaller than that of the AOSS estimators. Equality tests that the AOSS and WAOSS effects are equal are not rejected, thus suggesting that (5) may hold in this application. At least, the correlation between switchers’ tax changes and their slopes is not large enough to generate a detectable difference between the two parameters. In Panel B, the AOSS estimates of the first-stage effect are insignificant. The WAOSS estimates are significant, and they indicate that if gasoline tax increases by 1 cent on average, prices increase by around 0.5 percent on average for the switchers. Again, the differences between the AOSS and WAOSS effects of taxes on prices are insignificant.

| Panel A: Reduced-form effect of taxes on quantities consumed. | ||||||

| AOSS | s.e | WAOSS | s.e. | p-value | N | |

| (1) | (2) | (3) | (4) | (5) | (6) | |

| log(quantity) - Linear model | -0.0058 | 0.0026 | -0.0039 | 0.0009 | 0.357 | 1632 |

| log(quantity) - Quadratic model | -0.0050 | 0.0026 | -0.0038 | 0.0010 | 0.573 | 1632 |

| Panel B: First-stage effect of taxes on quantities consumed. | ||||||

| AOSS | s.e | WAOSS | s.e | p-value | N | |

| log(price) - Linear model | 0.0028 | 0.0023 | 0.0054 | 0.0009 | 0.154 | 1632 |

| log(price) - Quadratic model | 0.0024 | 0.0024 | 0.0050 | 0.0009 | 0.182 | 1632 |

Notes: All estimators in the table are computed using the data of Li et al. (2014). Columns (1) and (3) show the AOSS and doubly-robust WAOSS estimates of the reduced-form and first-stage effects of taxes on quantities and prices. First, the estimators are computed using a polynomial of order 1 in to estimate and the propensity scores , , and . Second, the estimators are computed using a polynomial of order 2 in those estimations. Columns (2) and (4) show estimated standard errors clustered at the state level and following (18) and (19). Column (5) shows the p-value of a test that the AOSS and WAOSS effects are equal.

Placebo analysis.

Table 3 below shows placebo AOSS and doubly-robust WAOSS estimates of the reduced-form and first-stage effects. The placebo estimators are analogous to the actual estimators, but they replace by , and they restrict the sample, for each pair of consecutive time periods , to states whose taxes did not change between and . The placebo WAOSS estimates are small and insignificant, both for quantities and prices. Those placebos are fairly precisely estimated, and their confidence intervals do not contain the actual WAOSS estimates. The placebo AOSS estimates are larger for quantities, but they are insignificant, and less precisely estimated. This placebo analysis shows that before switchers change their gasoline taxes, switchers’ and stayers’ consumption of gasoline and gasoline prices do not follow detectably different evolutions.

| Panel A: Reduced-form placebo effect of taxes on quantities consumed. | |||||

| AOSS | s.e | WAOSS | s.e | N | |

| (1) | (2) | (3) | (4) | (5) | |

| log(quantity) - Linear model | 0.0038 | 0.0023 | -0.0001 | 0.0011 | 1059 |

| log(quantity) - Quadratic model | 0.0039 | 0.0026 | -0.0003 | 0.0011 | 1059 |

| Panel B: First-stage placebo effect of taxes on prices. | |||||

| AOSS | s.e | WAOSS | s.e | N | |

| (1) | (2) | (3) | (4) | (5) | |

| log(price) - Linear model | -0.0008 | 0.0047 | 0.0015 | 0.0013 | 1059 |

| log(price) - Quadratic model | -0.0011 | 0.0045 | 0.0011 | 0.0013 | 1059 |

Notes: The table shows the placebo AOSS and doubly-robust WAOSS estimates of the reduced-form and first-stage effects of taxes on quantities and prices. The estimators and their standard errors are computed as the actual estimators, replacing by , and restricting the sample, for each pair of consecutive time periods , to states whose taxes did not change between and .

IV-WAOSS estimate of the price-elasticity of gasoline consumption.

The first two lines of Table 4 show doubly-robust IV-WAOSS estimates of the price-elasticity of gasoline consumption. The third line shows a 2SLS-TWFE estimator, computed via a 2SLS regression of on and state and year fixed effects, using as the instrument. As the instrument’s first stage is not very strong and the sample effectively only has 48 observations, asymptotic approximations may not be reliable for inference. In line with that conjecture, we find that the bootstrap distributions of the three estimators in Table 4 are non-normal, with some very large outliers. Therefore, we use percentile bootstrap for inference, clustering the bootstrap at the state level. Reassuringly, these confidence intervals have nominal coverage in simulations taylored to our application.777Here is the DGP used in our simulations. We estimate TWFE regressions of on state and year fixed effects and , and of on state and year fixed effects and . We let and denote the resulting regression decompositions. In each simulation, the simulated instrument is just the actual instrument, while the simulated outcomes and treatments are respectively equal to and where the vector of simulated residuals is drawn at random and with replacement from the estimated vectors of residuals . Thus, the first-stage and reduced-form effects, the correlation between the reduced-form and first-stage residuals, and the residuals’ serial correlation are the same as in the sample. The IV-WAOSS estimates are negative, significant, and larger than -1, though their confidence intervals contain -1. The 2SLS-TWFE is 42% larger in absolute value, though Column (3) of the table shows that the IV-WAOSS and 2SLS-TWFE estimators do not significantly differ. Interestingly, the confidence interval attached to the 2SLS-TWFE estimator is about 27% wider than that of the IV-WAOSS estimators, thus showing that using a more robust estimator does not always come with a precision cost.

| Estimator | 95% CI | P-value | N | |

|---|---|---|---|---|

| (1) | (2) | (3) | (4) | |

| IV-WAOSS - Linear Model | -0.726 | [-1.349,-0.328] | 0.358 | 1632 |

| IV-WAOSS - Quadratic Model | -0.761 | [-1.566,-0.068] | 0.394 | 1632 |

| 2SLS-TWFE | -1.084 | [-2.015,-0.502] | 1632 |

Notes: The table shows the doubly-robust IV-WAOSS and 2SLS-TWFE estimates of the price-elasticity of gasoline consumption, computed using the data of Li et al. (2014). Percentile bootstrap confidence intervals are shown in Column (2). They are computed with 500 bootstrap replications, clustered at the state level. The p-value of an equality test of the IV-WAOSS and 2SLS-TWFE estimators, also computed by percentile bootstrap, is shown in Column (3).

8 Conclusion

We propose new difference-in-difference (DID) estimators for continuous treatments. We assume that between pairs of consecutive periods, the treatment of some units, the switchers, changes, while the treatment of other units, the stayers, does not change. We propose a parallel trends assumption on the outcome evolution of switchers and stayers with the same baseline treatment. Under that assumption, two target parameters can be estimated. Our first target is the average slope of switchers’ period-two potential outcome function, from their period-one to their period-two treatment, referred to as the AOSS. Our second target is a weighted average of switchers’ slopes, where switchers receive a weight proportional to the absolute value of their treatment change, referred to as the WAOSS. Economically, the AOSS and WAOSS serve different purposes, so neither parameter dominates the other. On the other hand, when it comes to estimation, the WAOSS unambiguously dominates the AOSS. First, it can be estimated at the parametric rate even if units can experience an arbitrarily small treatment change. Second, under some conditions, its asymptotic variance is strictly lower than that of the AOSS estimator. Third, unlike the AOSS, it is amenable to doubly-robust estimation. In our application, we use US-state-level panel data to estimate the effect of gasoline taxes on gasoline consumption. The standard error of the WAOSS estimator is almost three times smaller than that of the AOSS estimator, and the two estimates are close. Thus, even if one were interested in inferring the effect of other tax changes than those observed in the data, a policy question for which the AOSS is a more relevant target, a bias-variance trade-off may actually suggest using the WAOSS estimator.

References

- Athey and Imbens (2006) Athey, S. and G. W. Imbens (2006). Identification and inference in nonlinear difference-in-differences models. Econometrica 74(2), 431–497.

- Bertrand et al. (2004) Bertrand, M., E. Duflo, and S. Mullainathan (2004). How much should we trust differences-in-differences estimates? The Quarterly Journal of Economics 119(1), 249–275.

- Bojinov et al. (2021) Bojinov, I., A. Rambachan, and N. Shephard (2021). Panel experiments and dynamic causal effects: A finite population perspective. Quantitative Economics 12(4), 1171–1196.

- Borusyak et al. (2021) Borusyak, K., X. Jaravel, and J. Spiess (2021). Revisiting event study designs: Robust and efficient estimation. arXiv preprint arXiv:2108.12419.

- Callaway et al. (2021) Callaway, B., A. Goodman-Bacon, and P. H. Sant’Anna (2021). Difference-in-differences with a continuous treatment. arXiv preprint arXiv:2107.02637.

- Callaway and Sant’Anna (2021) Callaway, B. and P. H. Sant’Anna (2021). Difference-in-differences with multiple time periods. Journal of Econometrics 225, 200–230.

- Cattaneo (2010) Cattaneo, M. D. (2010). Efficient semiparametric estimation of multi-valued treatment effects under ignorability. Journal of Econometrics 155(2), 138–154.

- Chamberlain (1982) Chamberlain, G. (1982). Multivariate regression models for panel data. Journal of econometrics 18(1), 5–46.

- de Chaisemartin (2010) de Chaisemartin, C. (2010). A note on instrumented difference in differences.

- de Chaisemartin and D’Haultfœuille (2018) de Chaisemartin, C. and X. D’Haultfœuille (2018). Fuzzy differences-in-differences. The Review of Economic Studies 85(2), 999–1028.

- de Chaisemartin and D’Haultfœuille (2020) de Chaisemartin, C. and X. D’Haultfœuille (2020). Two-way fixed effects estimators with heterogeneous treatment effects. American Economic Review 110(9), 2964–2996.

- de Chaisemartin and D’Haultfœuille (2023a) de Chaisemartin, C. and X. D’Haultfœuille (2023a). Difference-in-differences estimators of intertemporal treatment effects. arXiv preprint arXiv:2007.04267.

- de Chaisemartin and D’Haultfœuille (2023b) de Chaisemartin, C. and X. D’Haultfœuille (2023b). Two-way fixed effects and differences-in-differences with heterogeneous treatment effects: A survey. Econometrics Journal 26(3), C1–C30.

- de Chaisemartin et al. (2023) de Chaisemartin, C., X. D’Haultfœuille, and G. Vazquez-Bare (2023). Difference-in-differences estimators with continuous treatments and no stayers.

- D’Haultfœuille et al. (2023) D’Haultfœuille, X., S. Hoderlein, and Y. Sasaki (2023). Nonparametric difference-in-differences in repeated cross-sections with continuous treatments. Journal of Econometrics 234(2), 664–690.

- Fajgelbaum et al. (2020) Fajgelbaum, P. D., P. K. Goldberg, P. J. Kennedy, and A. K. Khandelwal (2020). The return to protectionism. The Quarterly Journal of Economics 135(1), 1–55.

- Goodman-Bacon (2021) Goodman-Bacon, A. (2021). Difference-in-differences with variation in treatment timing. Journal of Econometrics 225, 254–277.

- Graham and Powell (2012) Graham, B. S. and J. L. Powell (2012). Identification and estimation of average partial effects in “irregular” correlated random coefficient panel data models. Econometrica 80(5), 2105–2152.

- Hausman and Newey (1995) Hausman, J. A. and W. K. Newey (1995). Nonparametric estimation of exact consumers surplus and deadweight loss. Econometrica: Journal of the Econometric Society, 1445–1476.

- Hoderlein and White (2012) Hoderlein, S. and H. White (2012). Nonparametric identification in nonseparable panel data models with generalized fixed effects. Journal of Econometrics 168(2), 300–314.

- Hudson et al. (2017) Hudson, S., P. Hull, and J. Liebersohn (2017). Interpreting instrumented difference-in-differences. Metrics Note, Sept.

- Imbens and Angrist (1994) Imbens, G. W. and J. D. Angrist (1994). Identification and estimation of local average treatment effects. Econometrica 62(2), 467–475.

- Li et al. (2014) Li, S., J. Linn, and E. Muehlegger (2014). Gasoline taxes and consumer behavior. American Economic Journal: Economic Policy 6(4), 302–342.

- Newey (1994) Newey, W. K. (1994). The asymptotic variance of semiparametric estimators. Econometrica 62(6), 1349–1382.

- Newey (1995) Newey, W. K. (1995). Convergence rates for series estimators. In G. Maddala, P. Phillips, and T. Srinivasan (Eds.), Advances in Econometrics and Quantitative Economics: Essays in Honor of Professor C. R. Rao. Basil Blackwell.

- Newey (1997) Newey, W. K. (1997). Convergence rates and asymptotic normality for series estimators. Journal of econometrics 79(1), 147–168.

- Robins (1986) Robins, J. (1986). A new approach to causal inference in mortality studies with a sustained exposure period-application to control of the healthy worker survivor effect. Mathematical modelling 7(9-12), 1393–1512.

- Sun and Abraham (2021) Sun, L. and S. Abraham (2021). Estimating dynamic treatment effects in event studies with heterogeneous treatment effects. Journal of Econometrics 225, 175–199.

9 Proofs

Hereafter, denotes the support of . Note that under Assumption 2, one can show that for all , exists.

9.1 Theorem 1

9.2 Theorem 2

First, observe that the sets are decreasing for the inclusion and . Then, by continuity of probability measures,

| (20) |

where the inequality follows by Assumption 4. Thus, there exists such that for all , . Hereafter, we assume that .

We have and by Assumption 4, . Thus, for all , , so is well-defined. Moreover, for almost all such ,

| (21) |

where the first equality follows from Assumption 1. Now, by Point 2 of Assumption 2, admits an expectation. Moreover,

| (22) |

where the first equality follows from the law of iterated expectations, the second follows from (21), and the third again by the law of iterated expectations. Next,

Moreover,

where the second inequality follows by Assumption 2. Now, by (20) again, a.s. Moreover, with . Then, by the dominated convergence theorem,

We finally obtain

| (23) |

9.3 Theorem 3

Let , , , . In what follows we let . From Theorem 1, the parameter is characterized by the condition:

Define:

where . Also define:

We verify conditions 6.1 to 6.3, 5.1(i) and 6.4(ii) to 6.6 in Newey (1994). Following his notation, we let and represent the true parameters, and .

Step 1.

We verify condition 6.1. First, since is binary . On the other hand, by part 2 of Assumption 6. Thus, condition 6.1 holds.

Step 2.

We verify condition 6.2. Since is a power series, the support of is compact and the density of is uniformly bounded below, by Lemma A.15 in Newey (1995) for each there exists a constant nonsingular matrix such that for , the smallest eigenvalue of is bounded away from zero uniformly over , and is a subvector of . Since the series-based propensity scores estimators are invariant to nonsingular linear transformations, we do not need to distinguish between and and thus conditions 6.2(i) and 6.2(ii) are satisfied. Finally, because for all , for a vector we have that for all . Since is nonsingular, letting , is a non-zero constant for all and thus condition 6.2(iii) holds.

Step 3.

We verify condition 6.3 for . Since is a power series, the support of is compact and the functions to be estimated have 4 continuous derivatives, by Lemma A.12 in Newey (1995) there is a constant such that there is with , where in our case since the dimension of the covariates is 1 and the unknown functions are 4 times continuously differentiable. Thus, condition 6.3 holds.

Step 4.

Step 5.

We verify condition 6.4(ii). First, . For power series, by Lemma A.15 in Newey (1995), so setting ,

since , and . Finally,

since and for , . Hence condition 6.4(ii) holds.

Step 6.

We verify condition 6.5 for and where . Since ,

Next, the same linear transformation of as in Step 2, namely is, by Lemma A.15 in Newey (1995), such that . As a result, . Then, for ,

since and for . Thus, condition 6.5 holds.

Step 7.

We verify condition 6.6. Condition 6.6(i) holds for

Because the involved functions are continuously differentiable, by Lemma A.12 from Newey (1995) there exist and such that:

and

were we recall that . Thus, the first part of condition 6.6(ii) follows from

Next,

and finally

and

Thus, condition 6.6 holds.

By inspection of the proof of Theorem 6.1 in Newey (1994), condition 6.4(ii) implies 5.1(ii) therein, conditions 6.5 and 6.2 imply 5.2 therein, and condition 6.6 implies 5.3 therein. Then, conditions 5.1-5.3 inNewey (1994) hold, and thus by his Lemma 5.1,

where

and . Finally note that:

and the result follows defining . □

9.4 Theorem 4

We only prove the first point, as the proof of the second point is similar and (11)-(12) follow by combining these two points. Moreover, the proof of (7) is similar to the proof of Theorem 1 so it is omitted. We thus focus on (8) hereafter.

For all , by Point 1 of Assumption 7, . Thus, is well-defined. Then, using the same reasoning as that used to show (21) above, we obtain

Now, let be the complement of . For all , . Then, with the convention that ,

Combining the two preceding displays implies that for all ,

Hence, by repeated use of the law of iterated expectation,

The result follows after some algebra. □

9.5 Theorem 5

We prove the result for the propensity-score-based estimator and drop the “ps” subscript to reduce notation. Let , , and . The logit series estimators of the unknown functions are given by where is the logit function and

for equal to , or . Under Assumption 8, there exists a constant that satisfies:

and we let . We suppress the subscript on to reduce notation and let and . Under Assumption 8 part 1, Lemma A.15 in Newey (1995) ensures that the smallest eigenvalue of , is bounded away from zero uniformly over . In addition, Cattaneo (2010) shows that under Assumption 8, the multinomial logit series estimator satisfies:

and

where . Newey (1994) also shows that for orthonormal polynomials, is bounded above by for some constant , which implies in our case that . Throughout the proof, we also use the fact that by a second-order mean value expansion, there exists a such that:

where both and are bounded.

We start by considering the parameter and omit the “ps” superscript to reduce notation. Recall that

Thus,

Define:

Let be the influence function defined in the statement of the theorem. Using the identity:

we have, after some rearranging,

which we rewrite as:

where each represents one term on the above display. We now bound each one of these terms.

Term 1.

For the first term, we have that:

Now, by a second-order mean value expansion,

Next note that

Now, . Let

We have and

| (24) |

since the polynomials can be chosen such that , see Newey (1997), page 161. Hence,

Therefore, by Markov’s inequality,

Next,

where the first inequality follows by Cauchy-Schwarz inequality, the second by Markov’s inequality and the third by the same reasoning as to obtain (24). Hence,

Finally, for we have that

and

and therefore

Term 2.

This follows by the same argument as that of Term 1 and we obtain:

Term 3.

For the third term, since is uniformly bounded and converges uniformly to , for large enough

Term 4.

For the fourth term,

Term 5.

For the fifth term, since is uniformly bounded and converges uniformly to , for large enough

Term 6.

For the sixth term, let be the population coefficient from a (linear) series approximation to the function . Then we have that

because the last term in the second line equals zero by the first-order conditions of the logit series estimator. Next, we have that

Now, for , we have that

and

so that

On the other hand, for , we have that

from which

Term 7.

This follows by the same argument as that of Term 6 and we obtain

Collecting all the terms, if follows that under the conditions

we obtain

Setting , this implies

These conditions are satisfied when for or in this case .

By an analogous argument, we can show that under the same conditions

and the result follows by a multivariate CLT. Finally, notice that letting and , and using that and , after some simple manipulations:

which is analogous to replacing by and the denominator by . Thus, under the same conditions

where is defined in the statement of the theorem □

9.6 Proposition 1

If and ,

If , then , and , so after some algebra the previous display simplifies to

Then, under Assumption 1,

Then, using the law of total variance, the fact that , and some algebra,

and

The inequality follows from the convexity of , the convexity of on and , Jensen’s inequality, and increasing on , which together imply that

Finally, Jensen’s inequality is strict for strictly convex functions, unless the random variable is actually constant. The last claim of the proposition follows.

9.7 Theorem 6

The parameter can be written as:

The regression-based estimand is:

Following previous arguments, the conditional expectations are well-defined under Assumption 13. For the denominator,

because

by Assumption 9. On the other hand,

where the last equality follows from monotonicity (Assumption 10) and using the definition of switchers-compliers. Next, the numerator is:

using the parallel trends assumption as before. Then,

and thus

For the propensity-score estimand, notice that

and using that , by the law of iterated expectations,

as required. The same argument replacing by completes the proof □

9.8 Theorem 7

Using the same steps as in the proof of Theorem 1, one can show that for all ,

This proves the result □

9.9 Theorem 8

The proof is similar to that of Theorem 7, and is therefore omitted.