Multi-portfolio internal rebalancing processes

Linking resource allocation models and biproportional matrix techniques to portfolio management

Abstract

This paper describes multi-portfolio internal rebalancing processes used in the finance industry. Instead of trading with the market to externally rebalance, these internal processes detail how portfolio managers buy and sell between their portfolios to rebalance. We give an overview of currently used internal rebalancing processes, including one known as the banker process and another known as the linear process. We prove the banker process disadvantages the nominated banker portfolio in volatile markets, while the linear process may advantage or disadvantage portfolios.

We describe an alternative process that uses the concept of market-invariance. We give analytic solutions for small cases, while in general show that the -portfolio solution and its corresponding ‘market-invariant’ algorithm solve a system of nonlinear polynomial equations. It turns out this algorithm is a rediscovery of the RAS algorithm (also called the iterative proportional fitting procedure) for biproportional matrices. We show that this process is more equitable than the banker and linear processes, and demonstrate this with empirical results.

The market-invariant process has already been implemented by industry due to the significance of these results.

1 Introduction

This paper describes and extends multi-portfolio rebalancing processes currently used in the financial industry. Rebalancing processes are the strategy or rules that a portfolio manager undertakes to maintain their portfolios of assets around certain target allocations, as in Bernstein [6, pg. 167]. In this paper, we will classify rebalancing processes into two types: the external ones, where rebalancing of the portfolios occurs by trading with the market, and the internal ones, where rebalancing of the portfolios occurs through reallocation of current assets between the different portfolios. The focus of this paper will be on internal processes, which are only applicable for multi-portfolio managers, although we survey both in §2.

Internal rebalancing processes are a type of resource allocation problem. In general, resource allocation problems have been well studied in the literature, and are considered a core problem of economics as in Conrad [14]. Some questions that economists study include how resources are currently allocated, forecasting how they may be allocated in the future, and determining how best to allocate. Internal rebalancing processes consider the third point of how a portfolio manager should best allocate assets, although much of the connected literature considers the first two points, focusing on estimation and forecasting.

Optimisation and game theory techniques may be used to consider how best to allocate resources as in Nisan et al. [44, §5]. In the game theory setting, utility functions determine payoffs for individuals for allocating resources and solutions are usually in the form of equilibria. Such equilibra may not guarantee the optimal solution for each individual as in the Prisoner’s Dilemma, see for example Leyton-Brown and Shoham [34, pg. 4]. In contrast, the optimisation perspective defines a collective objective function that is required to be optimised subject to a set of constraints, as in [19, §II].

While many problems can be considered from both perspectives, our analysis of internal rebalancing processes in §3 will start by examining the existing processes and their properties, such as the market-invariant property. We will show that each rebalancing process can be formulated in terms of objective and utility functions in §4.3.1, although this is not required to formulate these processes.

More specifically, internal rebalancing processes seek an allocation of assets to all portfolios such that all assets are allocated, all portfolios have the required total assets, and this allocation is as ‘close to’ the target asset allocation (usually written as a matrix ) as possible. The asset allocation is usually written as a matrix and the target allocation as a matrix . It is called a process as at each point in time there may be a different amount of assets, a different total required for each portfolio and potentially a different target , and one requires a systematic way of allocating the assets to the portfolios. This process then determines the definition of ‘close to’.

It turns out there are many solutions to this problem, infinitely many as we discuss in §3 depending on the notion of ‘close to’. We will show that the property of market-invariance will determine such a definition of ‘close to’, giving us a well-defined process and an algorithm to calculate the allocation matrix . This market-invariant property is particularly important for our analysis, as the internal rebalancing process with this property does not advantage or disadvantage portfolios due to market movements. These notions of ‘close to’ usually determine an objective function and allow us to write these processes from an optimisation perspective, which we do in §4.3.1.

While internal rebalancing problems are well known in practical settings of portfolio management, the theory behind them is quite general. For instance, finding such a matrix is a requirement of estimating input-output matrices as in Bacharach [4], and a similar matrix must be found to describe powerflows along electricity lines as we discuss in Remark 3.4 and Appendix A. These different applications usually determine what ‘close to’ should mean.

After undertaking this research independently, we found that the market-invariance property is related to the problem in the economics literature of finding a biproportional matrix as in Bacharach [3], and the market-invariant algorithm is a rediscovery of the RAS algorithm from Stone et al. [50] (see also Lahr and De Mesnard [32] for a survey of this work). This algorithm is also known by various other names including the biproportional fitting algorithm and the iterative proportional fitting procedure (see Lomax and Norman [35] or Lovelace et al. [36] for example). We are not unique in this rediscovery, with early independent works by Kruithof [31] for telephone traffic, Deming and Stephan [17] for census data, and Sheliekhovskii and Bregman as in [10] for convex optimisation.

In particular, in Bacharach [4] the target allocation matrix is known as an input-output matrix for a closed Leontief System (see Wassily [60], Ryan [48], and Berman [5]), and it was used to describe the structure of economic systems. In this case, instead of portfolios composed of assets, the system describes production of goods from different proportions of commodities.

Taking this goods and commodities example from [4], the idea of finding a biproportional matrix is as follows. Over a given period of time there should be a matrix that describes how the commodities are being used by each industry to produce each good. However, there may be several unknowns — the biproportional case considers that the total number of commodities being used and the total output of the commodities is known, along with the matrix which is some known measure of how much of each commodity is required for each good (which may be estimated for example from a previous period of time). The matrix is the true proportion used by each industry to produce each good, and this is unknown, and the problem becomes that of how to estimate . The solution in [4] proposes that the matrix can be estimated by a matrix of the form of a product where and are positive diagonal matrices. This matrix is then called biproportional to .

We note that the literature seems to use these biproportional approaches for estimating or forecasting purposes. There is subsequent discussion how well these estimates fit, including how to generate confidence intervals, as in Bacharach [4, § 1]. Our problem is not to estimate or forecast a matrix, instead we are using these techniques to decide how best to allocate assets, so the discussion of confidence intervals and other measures of estimation do not apply here. However, these biproportional techniques and their extensions can be used to determine internal rebalancing processes.

More recently, the literature has broadened these biproportional studies to consider when different information is known or unknown. For instance if one or more entries of the matrix are known or include negative elements, as in the GRAS algorithm from Junius and Oosterhaven [28] and its extensions detailed in Huang et al. [22], or one or more entries of the column or row totals , are unknown, as in Temursho et al. [55]. See also Miller and Blair [41, § 7.4.1] or [56, Ch. 18] for a detailed summary.

There are also multi-dimensional examples (that is, dimensional matrices and tensors) as studied in Sugiyama et al. [52] and Valderas-Jaramillo and Rueda-Cantuche [59]. We do not study these here, although these extensions can be meaningful for internal rebalancing processes. For example, the multi-dimensional case could be used to consider other types of asset exposures, including exposures across different currencies, countries or industries. We also discuss interpreting negative entries for internal rebalancing processes in §3.1.1.

In general, the literature on biproportional problems is extensive. There are theoretical studies as in Bregman [10], de Mesnard [16] and Bacharach [4]; there are motivations from statistics as in Ireland and Kullback [25] for contingency tables and from economics as in Bacharach [3] for input-output models; and there are a wide range of applications. The research in this paper was undertaken without knowledge of this literature nor the techniques within, and has now been updated to include references to this research.

This paper adds much to the literature. From the perspective of an interested portfolio manager, the work is entirely self-contained, surveying the existing portfolio management rebalancing practices, and discussing alternative techniques and results.

In §2 we survey the existing literature on rebalancing process, particularly external rebalancing process, and discuss their importance for portfolio managers. While we would have preferred to focus on internal rebalancing process in this review, the author has found no existing literature that covers this other than the theoretical connection to the biproportional literature described above. In §3 we seek to rectify this, where we define internal rebalancing problems in general and describe the processes used in practice. These include the banker process in §3.2, the linear process in §3.3, and hybrid processes in §3.4. We also discuss the relationships to optimisation problems in §3.5 and how supply and demand problems, including electricity power flow constraints, can be considered as rebalancing processes in Remark 3.4 and Appendix A.

In §4 we discuss the market-invariant rebalancing process. We initially give the definition in terms of the market-invariant property, and then we show how this results in a well defined process. We then determine analytic solutions in small cases including where the dimension of the matrix is , then discuss what happens in the case and higher order cases in §4.1 and §4.2. While the market-invariant process is related to the RAS algorithm, the presentation of defining it in terms of a property is novel and the analytic solutions have not appeared in the literature so far.

In general, we show that the market-invariant algorithm in §4.3 gives the process for of arbitrary dimension. This algorithm is a rediscovery of the RAS algorithm. We present our own proof of convergence. We then compare the market-invariant process to the banker and linear processes in §5. We show that under certain market conditions the banker process disadvantages the banker portfolio and the linear process may advantage or disadvantage each portfolio, while the market-invariant process does not disadvantage any portfolio over another. This is in contrast to the general understanding in practice that these different rebalancing strategies have little effect on portfolio returns over time. This motivates using the market-invariant process for internal portfolio rebalancing to minimise any inequities from market movements.

This research is a significant contribution to the financial industry, and has already been implemented in the Superannuation industry in Australia. Funds have responded to this research by discontinuing the use of banker and linear rebalancing process or hybrids, and instead using the market-invariant process to minimise inequity between portfolios due to market movements.

2 Rebalancing processes in the finance industry

A core problem for portfolio managers is to maintain exposures as markets fluctuate and as they contribute to or redeem from their investments. Some portfolio managers employ a ‘buy and hold’ strategy, where after the initial purchase of assets they continue to hold the assets and never correct for market movements or cash flows (also called a drift-weight portfolio as in Granger et al. [20]). However, portfolio managers usually have target allocations for their assets (or collections of assets called asset classes) that contribute to maximising returns while achieving a certain level of risk, as first motivated by Markowitz [38]. Portfolio managers then undertake a process of rebalancing, where they buy or sell assets to maintain their desired market exposures.

An example to keep in mind would be a simple portfolio consisting of two different asset classes, say shares and bonds. There may be a target asset allocation of, say, shares (which we call a weight to shares) while the rest is bonds. We would say that this portfolio aims to be (directly) exposed to the share market and (directly) exposed to the bond market. We call the collection of shares the shares asset class, and similarly for bonds. If the shares’ market value increases, the weight of the share asset class increases and we say that the portfolio is overweight shares and underweight bonds. At this point the portfolio manager holding this portfolio must make a decision whether or not to rebalance their portfolio back to the target asset allocations. To do so, they would need to sell shares and buy bonds by trading with the market.

A portfolio manager with a single portfolio may manage these rebalancing decisions manually or may use pre-determined rules to trade with the market to maintain their exposures close to their target allocations. This may improve risk characteristics as in Ilmanen and Maloney [24]. We call such rules (external) rebalancing processes.

Such rebalancing processes have been well studied throughout the literature. They are often extensions of ‘buy low, sell high’ rules that give conditions on the extent of the buy and sell, and what is considered low or high. They also suggest how frequently to apply such rules particularly given the costs involved in their implementation. For example, Zilbering et al. [63] suggest rebalancing back to the target allocations whenever there are deviations or larger on an annual or semi-annual basis, and Bernstein [6, pg. 167] suggests rebalancing even less frequently for tax reasons. While rebalancing is considered an important part of a portfolio manager’s strategy as in Weinstein et al. [61], there does not appear to be any consensus on which processes to apply, with different strategies perform optimally in different conditions as in Tsa [57].

More advanced rebalancing processes tend to use optimisation techniques (such as minimising cost and/or minimising (conditional) value-at-risk as in MacLean et al. [37] and Meghwani and Thakur [39]); consider derivatives as in Israelov and Tummala [26]; use stochastic probability theory, dynamic programming and heuristic approximations such as machine learning algorithms as in Kritzman et al. [30], Perrin and Roncalli [45] and Sun et al. [53]; or use fuzzy logic models as in Fang et al. [18]. In general, these processes rely on the ability for a portfolio manager to be able to buy and sell with the market — in particular, they rely on a reasonable level of liquidity of their assets. Much of the statistical data required to implement these processes also relies on the ability of such data to be collected (or predicted) and may not have the same meaning for illiquid assets — for example, how does one understand daily or weekly volatility of an asset class whose assets only price monthly or quarterly? See Ang [1, Ch. 13.4] for details on issues with illiquid asset data.

When a portfolio manager has more than one portfolio under management with potentially different target allocations, the literature has concentrated on managers pooling together the assets and applying these processes to the collective totals. More recently, the literature has begun to consider the interrelationships between the portfolios and how to distribute the assets and costs between the rebalanced portfolios ‘fairly’, as in Stubbs and Vandenbussche [51], Iancu and Trichakis [23] and Zhang and Zhang [62].

The focus in this paper is not on external rebalancing processes, but instead on what we call internal rebalancing processes, which exist for multi-portfolio managers. These rebalancing processes do not consider buying and selling with the market and are purely concerned with the distribution of assets (and costs) fairly to all portfolios. They do not currently rely upon historical or predicted statistics, such as expected returns or variances, and they resemble the resource allocation problems detailed in §1. Such processes are used for funds with multiple portfolios that use portions of one or more of the same pooled assets in each of the portfolios’ asset allocations.

Extending our simple example above to consider this, say an investment manager is managing two portfolios, both worth , one with a target exposure of shares and bonds and cash, and the other with a target exposure of shares and bonds and cash. To manage this, the portfolio manager thinks in aggregate: they need a total of in a shares asset class and in a bonds asset class. The investment manager has selected a collection of shares and bonds that they think will do well, so they buy a total of worth in shares and in bonds to form the asset classes. They then distribute worth of the shares asset class to the first portfolio and the rest to the second portfolio, and distribute of the bonds asset class to the first portfolio and the rest to the second portfolio, leaving the remaining as cash.

Now say the second portfolio has a large withdrawal so that it is left with only cash, however at the same time the shares portfolio has a large distribution of cash from its investments. This would result in the first portfolio becoming overweight cash (and underweight shares and bonds) while the second portfolio is underweight cash (and over weight shares and bonds). Without trading with the market, the portfolio manager notices that they can redistribute the asset classes between the portfolios to correct for some of these overweights and underweights. How the manager decides to do this would require an internal rebalancing process.

While the portfolios in this example involved liquid222By liquidity we mean market liquidity as opposed to funding liquidity. See Mehrling [40, pg. 5] and Brunnermeier and Pedersen [11] for further details. asset classes, where the assets can be bought or sold in the time required at the volume required without moving the price, internal rebalancing process are particularly important for portfolios with asset classes that are illiquid. These asset classes cannot be bought or sold in the short time frames desired by the asset managers. They are also important as buying or selling with the market incurs fees or buy/sell spreads that managers are often incentivised to reduce.

The motivating example for this process comes from Superannuation funds in Australia, which invest on behalf of working Australians and provide a pension income for these Australian workers in retirement. They hold various portfolios with different mixes of asset classes to provide for different investment desires of their members. These funds are incentivised to hold illiquid assets to meet return and volatility targets, however must also minimise fees such as transaction costs. These cost pressures incentivise funds to minimise their external rebalances and their illiquid holdings prevent frequent rebalancing of these assets classes. However they can and do internally rebalance as frequently as needed, as this is comparatively cost-less and there are no issues for illiquid assets. Superannuation funds usually undertake these internal rebalancing processes daily, weekly or monthly in a systematised way.

In the next section we discuss rebalancing processes common in Superannuation funds, for which there are no published references. The author knows of no published research on these internal processes nor their properties, and this paper will begin to fill this gap in the literature.

3 Internal rebalancing processes

We start this section with necessary definitions before describing internal rebalancing processes known in industry. We will generally drop the word ‘internal’ as all rebalancing processes described in the following will be internal unless labeled by ‘external’.

3.1 Definitions and feasibility

Here we define rebalancing problems and processes, as well as discuss the feasibility of a rebalancing problem and the degrees of freedom that constrain the possible processes.

Definition 3.1.

A rebalancing problem consists of the following:

-

•

A non-negative column vector (asset class totals) and a non-negative column vector (portfolio totals) where .

-

•

A real non-negative matrix (target asset allocation) with entries and with columns sums . Here, is the target proportion of portfolio required from asset class .

-

•

The problem of finding a real non-negative matrix (actual asset allocation as a proportion) with entries and with column sums for all such that and is ‘close to’ .

For a given problem there might not exist an without violating one of the constraints. We call such a problem infeasible, and otherwise it is called feasible. We may apply additional constraints such as requiring whenever , and we discuss when this is feasible in Lemma 3.3. A rebalancing process is a process used to find for any given feasible rebalancing problem that defines a notion of ‘close to’. That is, a rebalancing process is a function for feasible .

While is the asset allocation as percentages, we will also consider the matrix with entries

This is the actual asset allocation as values (often monetary values) and we have that the conditions

are equivalent to requiring and for all .

Note that given we can scale each column to sum to 1 by dividing by to construct provided is positive. If is zero, we can set for all .

An immediate question that comes to mind is how many different rebalancing process are there? Or how many different ways to choose are available? We discuss this in the following remark. Note also that both and are possible and appear in practice.

Remark 3.2.

In general, a matrix with elements has degrees of freedom in the choice of the elements. In our case, the requirement that gives constraints and that for all gives constraints to the matrix . However, knowing that means that one of these constraints is redundant. This means we expect

degrees of freedom for the possible values of . That is, in general we can determine of the elements of before the constraints imply what the rest of the elements must be.

The requirement that is non-negative means that we consider a subset (with non-empty interior) of these possible values, so we still have degrees of freedom but on a smaller space. In general, other than the trivial case or , this means we have an infinite number of solutions to the rebalancing problem. The requirement of finding an ‘close to’ will mean that we want a process that can determine uniquely for each given within this infinite solution space.

Say we have such a process, so that given any we can determine a unique . Then consider that we can construct infinitely many more rebalancing processes by the following: for this given process and a given determine and by the original process. Then take a matrix consisting of the elements such that all rows and columns sum to (if has any zero elements, require that has a zero in the same positions). Then take the number and a scaling element . Then define the new process by constructing the allocation to be

As the rows and columns of sum to zero, it is follows that satisfies the constraints and that this is a valid rebalancing process. That is a minimum and ensures all elements remain non-negative.

The choice of shows that given any rebalancing process we can construct infinitely many more rebalancing process, with at least one degree of freedom. In fact, can be chosen so that it has zeros in the same position as but otherwise so that it contains values between and so that its maximum element is or its minimum element is and each column and row sum to . This gives significantly more degrees of freedom in the cases where and either or is greater than .

For a given process, we usually require that whenever to be part of the definition of ‘close to’. Given such a process exists, we can still construct infinitely many other processes by defining in the above to be a function of , where say

We may wish to add additional requirements such as imposing that whenever . This will reduce the degrees of freedom depending on the number of zeros in and knowing if this property holds beforehand can reduce the complexity of finding the solutions.

We now discuss conditions on and that ensure there are always feasible solutions to a rebalancing problem so that it is possible to construct a rebalancing process. We then give examples of rebalancing processes, showing that they do exist.

Lemma 3.3.

Let be a rebalancing problem. If there are no additional constraints on then all problems are feasible.

If we impose that must have zeros where has zeros then there are feasible solutions to this problem provided the following conditions hold:

-

(1)

For any given distinct list then for each we define the collection

and we require that

This ensures there are enough assets to allocate to the portfolio requirements.

-

(2)

Similarly for a given distinct list then for each we define the collection

and we require that

This ensures there is enough portfolio capacity to allocate all assets.

Note that these conditions hold trivially in the case that has no zero elements.

Proof.

In the first case, we can define a rebalancing process that does not depend on at all and instead behaves in a ‘greedy’ way. That is, we can define

by starting at , then iterating over and then incrementing and iterating again over etc. Here we define the sums to be zero if or respectively. By induction one can show that

and

Induction of the first equation on and the second one on gives that

for all and

for all , so that this is a valid rebalancing process. We call it greedy as it allocates the largest amount possible for the first element and the subsequent largest amount possible in the next element, completely ignoring the information in .

In the case where has zeros, we require that whenever . Say an is feasible and such an exists, however that the conditions in the lemma are not satisfied. Then without loss of generality there is a collection with corresponding such that

Given such an exists, we must have and we also know that

This gives

Putting these together we see that

which is a contradiction. This means that for to exist in this case the conditions in the lemma must be satisfied. Conversely, if the conditions in the lemma are satisfied, we do have a feasible rebalancing problem and the greedy process can be modified to be as before however forcing the -th element to be zero whenever . The greedy process then constructs a feasible solution to the rebalancing problem.

Note that in the case that has all elements positive, then regardless of we have for all and regardless of we have for all . This means the requirements in Lemma 3.3 reduce to simply checking that any subset of elements of must sum to something less than or equal to the sum of all elements of , and any subset of elements of must sum to something less than or equal to the sum of all elements of . Both of these conditions are trivially true due to the non-negativity of and which means any with having all entries positive is feasible. ∎

In general, these conditions are not restrictive and matrices with zeros are usually feasible, although more zeros makes the problem more restrictive. In the sequel, we usually require that if has zeros then must have zeros in the same locations, and then feasible rebalancing problems satisfy conditions (1) and (2) from Lemma 3.3.

3.1.1 Non-negativity conditions

Before we proceed to give examples of rebalancing process that are used in practice, we should discuss the non-negativity conditions and, if we relaxed these conditions, what the interpretation of a negative solution would be in our context. We note that Lahr and De Mesnard [32, pg. 15] suggest negative solutions in economics contexts are not easy to interpret in economic terms.

In the portfolio management context we can however interpret negative elements as follows. If one of the elements of contained a negative value, one could interpret this as a class of debt or liabilities to the portfolio holder rather than assets, for example a loan taken to fund the portfolio. If one of the elements of contained a negative value, one could interpret this to mean that this portfolio has been used to fund a loan (i.e. is a liability of someone, a form of leverage) where they owe the contents of the portfolio plus the interest it would have earned on the underlying investments, which is currently attributed to the other portfolios.

If one of the elements in (or equivalently in ) is negative, this would mean that the corresponding portfolio is leveraging this asset class to increase its exposure to the other asset classes. For example, if the target allocation to portfolio was shares, and bonds, then any positive movement for bonds would mean this portfolio paid the other portfolios the corresponding movements, and similarly positive movements for the shares would result in the other portfolios paying this portfolio the corresponding movements.

While all of these negativity conditions are possible, in practice the last one would likely be the most useful in this setting, and can also arise from some of the rebalancing processes we detail below. Also relevant here is the Superannuation regulations which strictly prevent leveraging in almost all situations, as in the SIS Act [13, §67 &§97]. However, leveraging is a common financial concept and therefore all of these interpretations have merit in the general portfolio management context.

We now detail specific rebalancing processes, beginning with the banker process.

3.2 Banker rebalancing process

This common rebalancing process selects a specific portfolio to be called the banker. In this process, all portfolios except the selected ‘banker’ portfolio are given their target asset allocations, and the banker portfolio is given the remaining funds. There are limitations on this, as the banker must be able to contain all the asset classes, and there must be enough of each asset class so that there are no negative exposures for the banker. This usually means the banker portfolio is chosen to be the largest portfolio in the fund.

In the case of Superannuation funds, they have default portfolios that often contain the largest proportion of their assets and this is usually the portfolio chosen to be the banker.

Specifically, this process works as defined in Algorithm 1.

We can check that by the following calculation

We additionally require

for each for this process to be well defined and give a non-negative solution for . This means there is enough of each asset class to satisfy the target allocation for all portfolios but the banker and for there to be a non-negative amount left over for the banker.

While there is usually a non-negative solution for , extreme market events can cause this requirement to fail and the banker process would return an infeasible, negative solution. In practice funds usually manually adjust for this, either readjusting the asset allocations or changing the target allocations so that a feasible solution exists. However, if negative allocations are allowed, this process could be used without adjustment.

The amount is called the linear overweight or underweight for this asset allocation compared to the target for the asset class and portfolio . The justification of this process is that the largest portfolio can absorb the overweights or underweights of an asset class more easily, and choosing the banker to be the largest portfolio means that the linear overweights for this asset class will be the smallest of all other possible choices of banker. However, this tends to ignore the target asset allocation of the banker altogether.

It can also create inequity, as, for instance, if an asset class falls in value then applying this process will result in the banker effectively ‘selling’ its assets in this asset class to the other portfolios, and vice versa when markets rise. This is contrary to the usual ‘buy low, sell high’ external rebalancing process rules, which means that this process is disproportionately affecting the banker portfolio with respect to market movements. We discuss this further in Section 5.

3.3 Linear rebalancing process

This process involves calculating the linear overweight of all of the portfolios compared to what they would be at their targets, and distributing this to each of the portfolios. No specified banker portfolio is required. The calculations are not complex, as in the following algorithm.

This process distributes the linear overweights/underweights for each asset class compared to the target asset allocation to all portfolios. Here we have

where is the linear overweight/underweight

We can check that by the following calculation

using that .

This process creates some sense of equity, as it means all portfolios receive these linear underweights and overweights evenly. However, it may be undesirable as it can mean some portfolios significantly change their allocations compared to others.

For example, consider a portfolio that has a small allocation to an asset class, say , compared to another portfolio that has a larger allocation at say to that asset class. If the asset class has a linear overweight of , then the first portfolio will be rebalanced to an allocation of which is double its target asset allocation, while the second portfolio will be rebalanced to an allocation of which is only a increase. If the market then falls so that this asset class is at a neutral weight, the portfolios must be rebalanced to their target.

In practice, this will have been achieved by the first portfolio ‘buying’ from the the other portfolio at the top of the market for that asset class, and ‘selling’ at the bottom of the market, contrary to usual ‘buy low, sell high’ rules, and can disadvantage such a portfolio in the long run. The doubling of the exposure may also cause other asset allocation issues, such as significantly increasing the risk profile of some portfolios compared to others.

3.4 Hybrid and proportional processes

Many funds use hybrid banker and linear processes. Here, funds may group portfolios into categories, and, for example, apply the linear process to each category, and then select a banker portfolio within each category and apply the banker process within the categories. Another approach is to apply a process up to a certain limit to portfolios before resorting to a banker process, for example applying the linear process until a portfolio reaches a percentage linear overweight/underweight of a certain asset class (or group of asset classes, for example, a group consisting of all of the illiquid asset classes).

Funds have also considered trying to distribute the overweights/underweights proportionally instead of linearly. Here instead of the linear overweight/underweight , the proportional overweight/underweight is calculated

and the aim is to give the portfolios the values . However, this does not ensure that . Some funds have opted to avoid this issue by subsequently applying a banker process. In general however, the market-invariant rebalancing process we study in §4 is a way to resolve this issue.

3.5 Optimisation

The rebalancing problem can be phrased as an optimisation problem. This could be the problem of minimising some objective function with output in written in terms of , , and the output allocation . This forms an optimisation program as follows

| such that | |||

The choices of are numerous — an easy example is to take to be the sum of the squared differences of the elements of and . Solving by standard methods including Lagrange multipliers and convex optimisation as in Boyd and Vandenberghe [9], or Newton-Raphson methods as in [8, Chpt. 4], is usually feasible for different choices of and they can improve on the issues mentioned in the banker and linear rebalancing process.

The previous two processes can be converted into optimisation problems. In the banker process, one choice of objective function which would give the same solution would be

Here, any metric to compute the distance between and would do, as given that the banker is not included in the sum, the optimisation process would set for all portfolios except the banker. For the linear case, the optimisation problem could have objective function

and here the optimisation process would set for each . This means that for each for the linear overweight/underweight .

In general, is there a natural choice of objective function and would we interpret it? The squared differences are a usual first guess in optimisation as it can be interpreted as a least-squares estimator. This and several extensions are discussed in Lahr and De Mesnard [32, §4], noting that there are interpretations as the Person’s statistic or as the Neyman’s statistic, and Senata [49, §2.6] discusses the squared differences as a second order Taylor series approximation. These objective functions make sense when the focus is to estimate or forecast , but have little intuitive meaning for our rebalancing processes.

As mentioned in the introduction, market data such as momentum overlays and risk measures including Variance at Risk (VaR) used in [51], [23] and [62] could also be introduced to determine an optimisation problem, but we do not do this here. We will return to the question of what might be a natural choice of objective function in §4.3.1. A summary of other optimisation techniques documented in the literature is available in [56, Ch. 18].

Remark 3.4.

The requirement that means this problem is a supply equal to demand problem. An interpretation of this is that the supply of each asset class is sufficient to meet the total demand from the portfolio, and that all assets are fully allocated. There are many such problems that require supply to equal to demand.

One example is from electricity networks, where supply of electricity must equal demand of electricity and certain properties of powerlines determine how much electricity flows along each line. We detail this further in Appendix A.

4 The market-invariant rebalancing process

We now present the market-invariant rebalancing process. The aim of this process is to minimise or indeed eliminate any inequitable treatment that may occur between portfolios due to market fluctuations. For example, if a market shock event occurred where only one asset class declined in value, then each time the rebalancing process was undertaken no portfolio should need to buy or sell between other portfolios to balance this, which may advantage or disadvantage portfolios upon further market movements. Note that such a market event would be an opportunity for an external rebalance instead.

In the following sections, we will use the operation to mean multiplication element-wise, for example

while the operation will mean to divide element-wise, for example

In practice we will want to be able to take a row vector and a matrix and multiply each column of by the corresponding element in , then we will write this as follows

Here is a row vector of length with entries all ones. Note that and would result in each row of being multiplied by the corresponding element of provided the number of rows in is the same as the number of element of (so in the example above).

We now define the property of market-invariance, which precisely captures the idea that no portfolio should need to buy or sell from other portfolios due to market movements.

Definition 4.1.

Let be a rebalancing problem. We say that a rebalancing process has the property of market-invariance if it produces the asset allocation such that

-

(1)

If then ; and

-

(2)

Say solves the rebalancing problem so that . Let represent a proportional change in the value of assets to

and corresponding changes to the portfolio values where becomes with

Then the rebalancing process applied to the rebalancing problem must give the asset allocation

(where here is a row vector with elements). As indices we have

From the outset, this definition seems to give us neither existence nor uniqueness of the solution , or even a way to find . In Proposition 4.3 we will show this definition is equivalent to solving a system of polynomial equations, so that solving these polynomial equations for a non-negative solution will determine . In Theorem 4.7 and Corollary 4.8 we will show that these equations always have a non-negative solution, so existence is guaranteed, and we see this explicitly for in §4.1. Finally, we see that Theorem 4.9 determines uniqueness. This means this property uniquely determines a rebalancing process, which we call the market-invariant rebalancing process. It turns out that this process also gives a way to distribute asset overweights/underweights proportionally, which we mentioned in §3.4.

Remark 4.2.

The property of market-invariance can be used to define an equivalence relation as follows for matrices. We say for matrices and that if there are and diagonal matrices and respectively, with positive diagonal, such that . We can see this relation is reflexive, that is , by setting and to the identity matrices; it is reflexive (if then ) by considering and ; and it is transitive by considering if , and then , so that and implies .

In our case, we have , where we take to be the diagonal matrix with along the diagonal, and to be the diagonal matrix with along its diagonal. Similarly , with the same however has elements on its diagonal. As the relation is an equivalent relation, there is a set of all matrices that are related to (called an equivalence class). We will use this equivalence relation to discuss how the property of market-invariance gives a unique set of polynomial equations as in Proposition 4.3.

Proposition 4.3.

For each rebalancing problem , if a rebalancing process has the property of market-invariance from Definition 4.1 then determining asset allocation is equivalent to finding non-negative column vectors , , to give

Here we require that and solve the following system of polynomial equations, divided into the asset class equations

| (1) |

and the portfolio equations

| (2) |

As matrices, we can rewrite these equations as

We can see that any non-negative solution to Equation 1 and Equation 2 can be extended to a 1-dimensional space of solutions, and , where is a scaling factor. That is, , and . These all have the same corresponding asset allocation .

Note that negative solutions can be created by taking , although this still results in the same value of . Also, these equations are not independent, as we have , so one equation can be removed from the set Equation 1 and Equation 2 without changing the solutions.

In the literature, the matrix is called biproportional to (or to ), as in Bacharach [3, pg. 296–297].

Proof.

Say we have a rebalancing problem and we do not have that . We want to be able to use both points of Definition 4.1 to determine .

Say there exists another set of portfolio values and asset class values such that , and we also have asset class movements such that

Then we can solve using the solution by Definition 4.1(1) and then we can solve by setting

and

using Definition 4.1(2). This means we need to find such that and

which are the asset class and portfolio equations. This means that if Definition 4.1 gives a well defined rebalancing process implies there exists that solve the asset class and portfolio equations.

For the reverse argument, it is clear that if then , , solve the asset class equations, and if this is unique then the asset class and portfolio equations imply Definition 4.1(1). Using the notation from Definition 4.1(2), if solves using the asset class and portfolio equations, then where has along the diagonal and has along the diagonal as in Remark 4.2, so . Then if solves using the asset class and portfolio equations using , then where has along the diagonal and has . As we have shown that is an equivalence relation, we must have that . This means that being able to solve the asset class and portfolio equations for a unique implies that the property of market-invariance from Definition 4.1 gives a well defined rebalancing process.

This means that Definition 4.1 is well defined if and only if for each rebalancing problem there exists such that give the solution uniquely. This is equivalent to saying that for each feasible there exists a unique element in the -equivalence class of that has row sums equal to and column sums equal to . ∎

This result implies that our market-invariant rebalancing process is well defined provided there exists a (unique up to scaling) solution that solves the system of equations in Proposition 4.3. However, systems of polynomial equations are notoriously hard to solve analytically. They often reduce to solving a single high order polynomial equation, and the Abel-Ruffini theorem (see [2, 15]) tells us that there is no general analytic solution for polynomial equations above order 4. Instead, numerical methods such as Newton-Raphson methods (see [8, Chpt. 4]) can be used to solve for solutions where they exist.

In the cases we can write down an analytic solution, which we do next, as well as consider the case and higher order cases. We then proceed to prove such solutions exist in general and give an algorithm to find these solutions. We also remark on uniqueness of solutions.

4.1 Solution for

Here we determine the analytic formula for the market-invariant process in the case where the dimension of is .

Proposition 4.4.

Let be a feasible rebalancing problem. When the asset class and portfolio equations from Proposition 4.3 result in a unique solution to this rebalancing problem, and a one-dimensional solution set .

Proof.

If an element of is zero, the solution is trivial. For example, if , then , , , , and . Then we can define such that , and such that for , which implies , and . Multiplying by and by for gives the full solution set for values of and , while the unique positive solution occurs for all values of .

If we assume that all elements of are positive then we can consider the asset class equations

and the portfolio equations

We can write

| (3) | |||

then we find that

We can rewrite as

Both equations have the same right-hand sides, so we can equate their left hand sides as follows

So this is now just a polynomial of degree two in our two unknowns and . Expanding and collecting like terms we have

Applying the quadratic formula we have

where

So we have that one of and is free, and the other is a multiple of the first.

We now show that we always get a unique positive solution for and , despite having a free variable. We have that

so that

This means that is independent of the choice of or , and only depends on the choice of sign for or

We will show only results in a non-negative solution for . Note that the discriminant is non-zero unless one or more elements of are zero, which reduces back to the first case. We have that regardless of , and then we have , so that and , regardless of the values of . This means we always have a unique positive solution, corresponding to and , giving the unique solution to the rebalancing problem. We note that

∎

Example 4.5.

Say we have the rebalancing problem of where

Using the market-invariant rebalancing process for we have solution

If we include the negative solutions as well, we see that there is another solution for corresponding to the negative sign in front of the square root in the scaling factor between and . This solution is

For both solutions, we can allow to vary in and this means the solutions give two lines through the origin with the origin removed. This is a real smooth algebraic variety with four disconnected components each isomorphic to and these correspond to each quadrant in .

We attach the Matlab code for these calculations in Appendix B.

4.2 More small cases

We can extend the results of the previous section to more small cases.

Proposition 4.6.

Let be a feasible rebalancing problem. When or solutions to the asset class and portfolio equations in Proposition 4.3 can be written analytically.

Proof.

Starting with the case , we will assume all are non-zero else this reduces to the previous case. Note that the case is analogous.

We can consider the asset class equations

and the portfolio equations

Given our previous discussions, to solve for positive solutions we can assume the scale parameter is equal to 1. Also, given the linear dependence of one of the equations, we will exclude from the calculations.

Now, rewrite the portfolio equations as follows

and substitute these into to give

Rearranging and factorising in terms of we have the following cubic equation

with coefficients

We can now apply the cubic formula (see for example Neumark [43]) for solving cubic polynomials in terms of as follows. Define

Then the solutions to the cubic are , and we can use the previous equations to find . If we use , then all of the above still works however the formulae for and must be multiplied by .

As cubics always contain one real root, then there are at least two real solutions corresponding to and . There may be up to solutions, however there may be fewer real solutions. For example, if for all , , and , then we find

and the cubic for becomes

This has a double root for , and a single root , which gives a positive solution. In §4.3 we show that there always exists a positive real root for the general case, so this formula must give this solution, and we have observed this in practice with the positive real root appearing for , and solution .

The case (and analogously ) is very similar, however uses the quartic formula. Applying the same method results in a quartic

with coefficients

We can now apply the quartic formula, where we define

The solutions are . Similarly if we consider the case, the formulae for must be multiplied by .

Again, if for all , , and , then we find

and the cubic for becomes

This has a triple root for , and a single root , which gives the positive solution we are looking for. Again §4.3 we show that there always exists a positive real root for the general case, so this formula must give this solution. ∎

The next smallest case is . However, unless there are one or more zeros in , this in general results in a quintic polynomial or higher, for which there is no analytic form of the solution.

4.2.1 Further comments on hybrid solutions

While in the next section we will describe an algorithm to find a non-negative solution to the equations in Proposition 4.3, we note that these analytic solutions can be used to form approximate solutions to this. For example, if we want to use the formula only, we can aggregate the portfolios and asset classes into groups. This works as follows.

Set to be a non-empty partition of the asset classes , and and a non-empty partition of the portfolios . Set

which is like an aggregated target allocation for that group of asset classes and portfolios. Similarly aggregate the portfolio totals to

Then apply the analytic rebalancing process solution for to . Call the resulting asset allocation and then define

This allocates the proportions of and to each group. We then apply this process again, but now we partition each and further into two groups. If any partition only contains one element, we do not partition this further. We repeat this process until all partitions contain only one element, resulting in a final proportion for each asset class to each portfolio.

This gives an approximate solution to the general case, although the choices of partitions give different solutions. Care must be taken if there are zeros in , and this must be adjusted for appropriately, by, for instance, picking partitions that isolate the zeros first. In general, this approach might be most useful if there are certain asset classes that have high correlation, for example two categories of shares. Then picking partitions that groups these asset classes together can increase the effectiveness of the approximation, although we do not prove this here. In general, any rebalancing solutions can be integrated in this way to create new rebalancing processes, and at each time step a different process can be used if required.

4.3 General case

In this section we prove that for any given feasible rebalancing problem there exists a natural solution and that solve the asset class and portfolio equations in Proposition 4.3. This means that the market-invariant rebalancing process is well defined. From this, we describe an algorithm that can be implemented efficiently to find a unique solution for any rebalancing problem.

Here we will often replace the index with and the index with when there are multiple summations present.

An intuitive way to interpret this next theorem is as follows. Say we have a feasible rebalancing problem and we want to distribute the asset overweights/underweights proportionally.

We suggested in §3.4 that the proportional overweight/underweight

should be used to distribute assets to each portfolio, where portfolio should receive

However, this does not ensure that the row sums of are equal to , although the column sums are equal to . The following theorem is a way to use this intuition but to ensure that , and it turns out that this gives a non-negative solution to Proposition 4.3.

Theorem 4.7.

Construct two sequences of matrices , , such that

and

for . We have the relationship

At each step we have and , and as we have that

The sequences , converge to and respectively, and we have . We define for all , and for which implies , and . Then is a solution to the rebalancing problem and satisfy the equations in Proposition 4.3.

Corollary 4.8.

The market-invariant rebalancing process from Proposition 4.3 applied to a rebalancing problem has a natural non-negative solution with .

Proof.

Proof of convergence of is as follows. Convergence of is analogous.

We show that for each . We see that

| (4) |

Here we define to be any for this such that is non-zero, and we use that to go from the second line to the third.

Now consider such that attains its minimum. Then we have

Substituting this into Equation 4 we have

| (5) | ||||

| (6) | ||||

| (7) |

As this is true for all this means that

and so for each is an increasing sequence in .

Similarly, we can swap all of the maximums and minimums to get a bound

Then for all , is a decreasing sequence in .

Iterating over we see by induction that

| (8) |

for all . This means that is a decreasing sequence in bounded below and is an increasing sequence in that is bounded above, so both converge by the Monotone Convergence Theorem (see [29, Chpt.1 §1 Cor 1.6] or any standard real analysis text book).

As sequences to converge, by the Squeeze theorem for sequences (see for example [47, Thm. 3.19] or [29, Chpt. 1 § 1 Prop. 1.7]) we must have that Equation 6 converges to Equation 7. This implies that

From this we can conclude that and must both converge to the same value, and by Equation 8 and the Squeeze theorem for sequences again, this means also converges and converges to the same limit.

Due the symmetry between and we have the corresponding result that , and all converge to the same limit.

Using this, we have

for some constant which must not depend on . Then

Taking the sum over we have

and as there is no dependence on in the right hand or left hand side, we have that . So indeed , , and converge to 1, and similar for the corresponding terms. Then we must have

Similarly

This in turn means that and must also converge, as they are defined by multiplying by and .

Note that for all and for all . Then we have the difference

This means the limits are , and we know that , and .

The proof that the limit solves the equations in Proposition 4.3 is by induction to find and as follows.

We will show for each there exist non-negative , such that for all . The initial case is , so this is true with .

Assume it is true for for some . Then

as required, with

A similar proof shows that there are and for , with , and , . We see that at each iteration then solve the portfolio equations and and solve the asset class equations. As then we have and converge to the same value , and and converge to the same value . This convergence implies we solve both equations simultaneously, giving the solution to the equations in Proposition 4.3 as required.

Finally we define such that for all , and such that for which implies . Then we have allocation with . These solve the rebalancing problem and satisfy the equations in Proposition 4.3, so they are a solution to the market-invariant rebalancing process. ∎

This theorem shows the existence of solutions to Proposition 4.3 by constructing such a non-negative solution. We can then describe a rebalancing process by using this.

We can use this theorem to construct Algorithm 3 that finds this natural solution and we call this the market-invariant rebalancing algorithm. This algorithm directly calculates a finite number of elements in the sequence , , , , as described in Theorem 4.7. As it only constructs a finite number of elements in the sequence, then it is unlikely to have fully converged upon termination. At this point, it takes the last element calculated in the sequence which has columns summing to and determines any difference between its row sums and (note that the sum of these differences is ). It then adds these into in a way proportion to . This then enforces that the columns still sum to and now the rows also sum to . Note that the differences could be added back to in many different ways, for example they could be all added to the largest portfolio, just like the banker process.

We also give a Matlab code example of this algorithm, available in Appendix B. Note that this algorithm converges extremely quickly, with iterations already giving the solution to 3 decimal places.

It turns out that this algorithm has been discovered previously and is known by many names including the RAS algorithm, raking, the biproportional fitting algorithm, and the iterative proportional fitting procedure, see [50, 35, 32, 3, 4, 31, 17, 10] for further details. This algorithm can be applied to more general cases, for example, there is no requirement that the columns of sum to 1, but instead requiring that no row or column entirely consists of zeros.

Note that Bezout’s theorem tells that if the solution space to Proposition 4.3 has dimension 0, then there are at most solutions for the reduced solution set (in , as ). We have shown that that for there are precisely real solutions with , and for there are at most real solutions with , and there may be only solutions in some cases. In the case , there are at most real solutions, although there may be only 2 in some cases. However, in the case, there was only one non-negative solution for and , and we have empirically found the same in the cases. It turns out that the following holds, as in Bacharach [3, Cor. 1].

Theorem 4.9.

For every feasible rebalancing problem the equations in Proposition 4.3 have a unique non-negative solution, and it is therefore given by the market-invariant algorithm.

This means the market-invariant algorithm gives this unique solution, and the market-invariant rebalancing process from Definition 4.1 is well defined and equivalent to the output of the algorithm.

Note that Bacharach [3, Thm. 3] (see also Senata [49, § 2.6]) determines that the algorithm only converges provided certain conditions hold. These conditions are equivalent to the feasibility conditions from Lemma 3.3.

In the next section we will show that we can formulate the market-invariant rebalancing process as convex optimisation problem. As the objective function is a strictly concave function (refer to Boyd and Vandenberghe [9, §3.1.4–1.5,§3.2] for details), then this directly implies Theorem 4.9.

4.3.1 Interpretation as an optimisation program

The market-invariant algorithm can be interpreted as an optimisation program. The following is adapted from Lahr and De Mesnard [32, § 3.2] as first described in Uribe et al. [58] using tools from information theory. Here the objective function is known as the information inaccuracy of , which is also called the Kullbaclk-Leibler divergence (see for example [56, pg. 552]). The program can be written as

| (9) | ||||

| subject to |

Note for a given if is equal to 0, we set and the objective function does not sum over this pair.

Using Lagrange multipliers, we can solve the above optimisation problem. We have the Lagrangian

with . Taking the derivative with respect to and setting equal to zero gives

This implies that

for all . So we have that and , using the notation from Proposition 4.3. This shows that the optimisation program is equivalent to the market-invariant rebalancing process.

As the optimisation program is convex, then convex optimisation algorithms can be used to solve this numerically, as in Boyd and Vandenberghe [9].

We note that program is equivalent to following

| subject to |

Here the objective function is a weighted geometric mean. This looks very similar to Fisher’s market model, as in Nisan et al. [44, pg. 106], where unlike our model the objective function is geometric mean of a linear sum of utilities. However, we can equivalently write the optimisation problem as

| subject to |

Then we could define utility functions by

and then define the product utility for each portfolio as

Then this is almost in the form of a Eisenberg–Gale-type convex program, as defined in Jain and Vazirani [27, § 5]. This is a class of convex optimisation programs that include Fisher’s market model, as in Nisan et al. [44, § 5.2]. Note however that this class of algorithms generally only uses one of the two sets of constraints, and usually relaxed to an inequality, say . So while these resource allocation problems are related to this, they are not quite the same.

Finally we can consider the convex dual of Equation 9, which is the following program

| (10) | ||||

| subject to | ||||

| (11) |

We see that there is an invariance up to scale, were for a solution then for any we have that is also a solution. Making large enough would ensure that is positive for all and is negative for all . Then we could interpret this optimisation program as minimising the prices and (up to scale) of supplying the assets and portfolios respectively. This is similar to the way the dual variables are considered prices in the Eisenberg–Gale-type convex programs, [27, § 5].

Of course, in general we do not expect that the objective function has a minimum of zero, which would only occur in the rare case that the solution is . If we interpret the and as prices, the objective function could then be considered the total cost of the solution for .

4.3.2 Interpretation of the R and S in the RAS algorithm

The RAS algorithm is equivalent to our market-invariant algorithm as it seeks to find a matrix of the form where and are square diagonal matrices. Here corresponds to our , while corresponds to a diagonal matrix with our along the diagonal, and corresponds to a diagonal matrix with our along the diagonal. There are some questions around how to interpret and , with Lahr and De Mesnard [32, §2.1-2.2] discussing several alternatives.

Bacharach [4, pg. 23] suggests in particular that while Leontief [33] and Neisser [42] propose interpreting these matrices as proportional changes in either the asset classes or the portfolios, that this seems implausible in practice.

We think our interpretation in Proposition 4.3 is an important addition to this discussion: consists of portfolio values that would allow , i.e. that give a solution that is exactly equal to the target . On the other hand, represents the increase or decrease in asset class values only that, given and , would result in the current and .

Note that the invariance under scale property of these solutions would allow us to write such that . Then could be interpreted as how much the portfolio values would need to change (increasing or decreasing) relative to as a linear difference to get exactly to the target for each portfolio, and represents the same for the asset classes but the proportional increase or decrease. We can also rescale so that , then would be how much the asset classes would need to change to get exactly to the target relative to to be at the target. These representations can be helpful for external rebalancing, as this determines how much would be required to trade with the market to return an asset allocation closer to the target .

We should also point out here the symmetry between the asset classes and portfolios: we have used the convention from industry that the matrix (or ) has the column sums equal to , so it represents the proportion of the portfolio value that is made up of each asset class. One can rescale each row of (or ) to (and ) so that instead the rows sum to 1, which is then the proportion of each asset class that is allocated to each portfolio. If one then applied all of the same theory following this symmetry, determining the corresponding , and , we would have , and this would represent the proportional increase in each portfolio to achieve . This is less relevant for our application but may be relevant for interpreting and in other areas.

In summary, contrary to Bacharach [4], we suggest interpreting these matrices as proportional changes in the asset classes or the portfolio values is appropriate for this application.

5 Comparisons of different processes

In this section we compare the performance of the different rebalancing processes as they are used in practice in portfolio management. We start with a theorectical result.

5.1 Theoretical results

Recall that we are motivated by the following scenario: a portfolio manager has a series of portfolios with values that use asset classes with values . These asset classes need to be fully allocated to the portfolio and each portfolio has a target proportion for asset class .

At any given time, the manager allocates the asset classes to the different portfolios according to their chosen rebalancing process. Over time, market movements and cash flows change the allocation of each of the portfolios. The manager then reapplies the rebalancing process to rebalance the portfolios closer to their targets — usually on a weekly or monthly basis.

Portfolio managers have not previously studied how the different process may advantage or disadvantage their portfolios with respect to market movements. In particular, we note that the banker process is often used as it is said to balance out any advantages or disadvantages to any particular portfolio overtime. The following theorem contradicts this, showing that the banker portfolio is always disadvantaged during ‘volatile’ periods. Specifically, we take any series of returns that result in the same asset allocation as started with and, ignoring all cash flows, show that the banker process is always disadvantaged by this process. This means that market fall and recovery events disadvantage the banker portfolio, as does any period of increased market volatility. This theorem motivates using the market-invariant process instead of the banker or linear process.

Theorem 5.1.

Let be a rebalancing problem. Take any series of returns for the asset classes over time periods such that the total return for each asset class over the time period is zero, so

Here we say that the returns are tethered so that total return is zero.

For a given rebalancing process, proceed by first applying the rebalancing process to allocate the assets to the portfolios. Then apply the returns for the asset classes for the first time period, resulting in performance of the portfolio corresponding to the ratio of asset classes it contains. Then apply the rebalancing process again to redistribute the assets, then calculate the performance again, and continue through all time periods. Then we have that

-

1.

The market-invariant rebalancing process applied at each time period will result in all the portfolios having the same return of 0%, aligning with the asset classes returning 0%. No portfolio is advantaged over another.

-

2.

The linear rebalancing process applied at each time period will result in all the portfolios having slightly different total returns, depending on the order of the returns. This means that some portfolios are advantaged while others are disadvantaged.

-

3.

The banker rebalancing process applied at each time period will result in the banker portfolio returning negative returns and all other portfolios returning positive returns. That is, the banker is disadvantaged compared to all other portfolios, regardless of the returns.

We show this matches empirical results.

Proof.

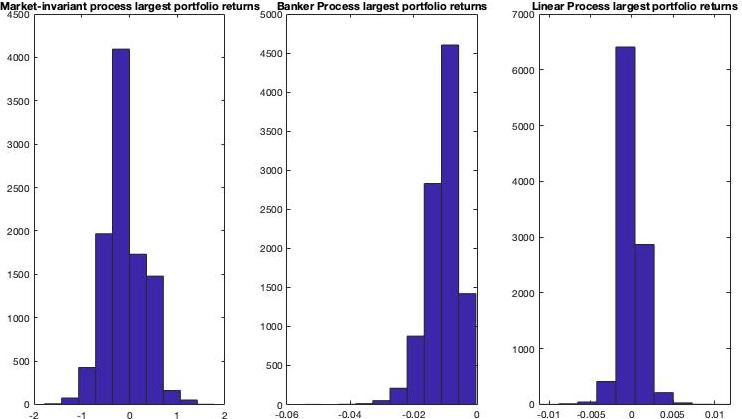

For point 1, this results by definition of the market-invariant rebalancing process. In fact, at each time period other than the first, no reallocation is necessary. Empirically using the code in Appendix B, simulations show that the return is zero to 15 decimal places, which are due to rounding errors. This means that no portfolio is advantaged over another portfolio when using this process.

For point 2 we show this empirically through simulations. Note that if all assets moved the same amount at each time period, no reallocation is necessary. In general however, the return will depend on the order of the returns. This means that using the linear rebalancing process, some portfolios are advantaged and some portfolios are disadvantaged due to market movements.

For point 3 we will take an arbitrary portfolio such that it is not the banker. We want to consider the ratio

where is the value of the portfolio at time , and . If this ratio is greater than 1, this portfolio has made money while less than one means this portfolio has lost money. Then consider that at time

Iterating, we see that we have

We want to prove that this is greater than or equal to 1 for this portfolio to not have been disadvantaged through applying the banker process. This is trivially true for , as then and the performance is exactly equal to 1.

The proof can be derived from using to show

| (12) |

for all choices of . Here is the set of all distinct permutations of and is the total number of permutations. Note that this is equal to the multinomial coefficient

where is the number of distinct elements in the list , and is the number of times that element appears in the list. For example, if we have then and and .

We can then prove Equation 12 as we have

where the first line uses that arithmetic means are greater than or equal to geometric means, as in Hardy et al. [21, § 2.5]. Note that equality occurs if and only if all terms of the form

are equal.

If we write that

then we have that

as required, where the last line uses the Multinomial Theorem (see Tauber [54] or Riordan [46] for details).

Equality only occurs if all terms are equal for all possible . This only occurs if every for all and for all . This means that unless all asset classes move in unison in every time period, every portfolio except banker portfolio will be advantaged by applying the banker process.

Unfortunately, this then implies that the banker’s performance is

whenever the asset classes do not move in unison, so that the banker process always disadvantages the banker portfolio. In effect, the banker process is giving returns to the other portfolios.

In Figure 5.1 we have empirically tested this result for . We see that the banker process results in negative returns for the banker, while the market-invariant process results in zero return (up to rounding errors in order of ) and the linear process returns in both positive and negative returns. ∎

An initial question from this theorem is to what extent is the banker portfolio disadvantaged? Another observation of the previous theorem is that the tethered return series described appears theoretical and unlikely to be observed in practice. In the following section we address these points.

5.2 Simulation results

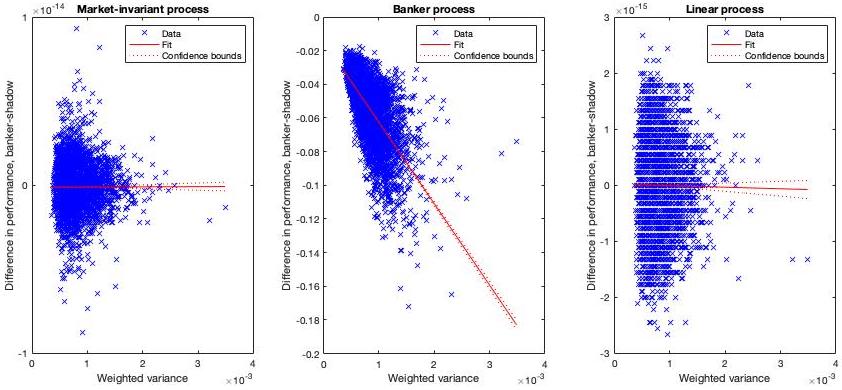

We first consider the situation of the previous theorem where the returns are tethered to zero to understand how much the banker portfolio is disadvantaged. To do this, we set up a shadow portfolio, which is a portfolio that has the same target asset allocation as the banker. We then want to measure the difference between the returns of the shadow portfolio and the banker portfolio over the time series. As we proved in Theorem 5.1, this will always be negative when the returns are tethered unless all the returns are the same. However, we may want to understand what contributes to the extent of the negative returns.

To do this we plotted the difference between the performance of the banker portfolio and the shadow portfolio against the weighted variance of the return series of the asset classes. The weighting here is by the starting value of the asset classes. Using the banker process, we see that a linear regression model is statistically significant with higher variance resulting in lower performance of the banker compared to the shadow portfolio. The R-squared value is 0.464, suggesting nearly half of the trend in performance is explained by the weighted variance of the asset classes.

We are aware that having the returns tethered exactly to zero may seem unlikely to occur in practice. However, we expect this to be illustrative of a market fall and recovery event. More generally, an observed return series could be considered as a decomposition into a volatile tethered series and an increasing or decreasing trend, so there is some merit in considering the volatile tethered series separately. However, the process of rebalancing is not so easily decomposed in this way.

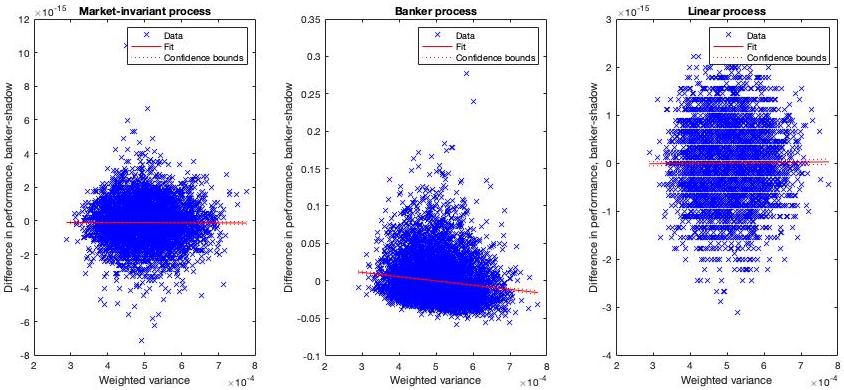

Running the same analysis on untethered data, so that the end values of the asset classes are random and may be higher or lower than their starting values, we observe similar but more noisy results. There is still a statistically significant linear trend between the difference in performance of the banker and the shadow portfolio against the weighted variance of the asset classes for the banker process. The R-squared value has lowered to 0.0174, suggesting only around of the difference in performance is explained by the variance. Interestingly, the difference in performance is now both positive and negative, although we note that of the time the difference remained negative and the banker portfolio was disadvantaged in these cases.

We see that the weighted variance is in the order of , yet the difference in performance is between -10 to +30 basis points. This is a sizeable enough difference that funds would want to mitigate to maintain equity between the different portfolios. This is another reason to prefer the market-invariant process where the difference is a rounding error in the order of .

Finally, we also analysed whether the weighted performance of the asset classes is also a predictor of the performance differences between the banker and shadow portfolio. We indeed found this is the case, with positive performance contributing to banker outperforming the shadow portfolio. This matches intuition, where increasing markets will benefit the banker by overweighting the banker to the positive performing asset classes. While the banker portfolio is benefited in these markets, the other portfolios are disadvantaged and we see the shadow portfolio under perform.

The model with the best fit we found to be the following

| (13) |

where is the performance of the banker, is the performance of the shadow, is the weighted variance and is the weight return of the asset classes. The full results are in Appendix C. The R-squared is slightly higher at .

This is the beginning of larger analysis that would be needed to understand exactly how the banker process impacts returns of the different portfolios. However, these results tell us that the banker process does indeed impact the returns of the portfolios. It may advantage or disadvantage the banker portfolio, and increasing the volatility in general disadvantages the banker’s performance while increasing performance advantages the banker’s performance.