Strategic mean-variance investing under mean-reverting stock returns

Abstract

In this report we derive the strategic (deterministic) allocation to bonds and stocks resulting in the optimal mean-variance trade-off on a given investment horizon. The underlying capital market features a mean-reverting process for equity returns, and the primary question of interest is how mean-reversion effects the optimal strategy and the resulting portfolio value at the horizon. In particular, we are interested in knowing under which assumptions and on which horizons, the risk-reward trade-off is so favourable that the value of the portfolio is effectively bounded from below on the horizon. In this case, we might think of the portfolio as providing a stochastic excess return on top of a “guarantee” (the lower bound).

Deriving optimal strategies is a well-known discipline in mathematical finance. The modern approach is to derive and solve the Hamilton-Jacobi-Bellman (HJB) differential equation characterizing the strategy leading to highest expected utility, for given utility function. However, for two reasons we approach the problem differently in this work. First, we wish to find the optimal strategy depending on time only, i.e., we do not allow for dependencies on capital market state variables, nor the value of the portfolio itself. This constraint characterizes the strategic allocation of long-term investors. Second, to gain insights on the role of mean-reversion, we wish to identify the entire family of extremal strategies, not only the optimal strategies. To derive the strategies we employ methods from calculus of variations, rather than the usual HJB approach.

Keywords: Deterministic strategies, mean-variance optimization, mean-reverting stock returns, calculus of variations.

1 Introduction

This is a technical document providing the theoretical foundation for a study of the risk-reward trade-off on long horizons in a capital market under which equity returns are mean-reverting. The problem is stated and solved in continuous-time based on the model analyzed in Jarner and Preisel (2017), see also Munk et al. (2004).

We are particularly interested in studying how the risk-reward trade-off depends on the degree of mean-reversion and the horizon, and under which assumptions the trade-off is so favourable that the (optimal) portfolio is effectively bounded from below. In this case, one might argue that the portfolio can be used as a “hedge” for a guaranteed payment, equal to the lower bound of the portfolio.

The optimal strategy itself is of course also of interest. In a model without mean-reversion it is optimal to hold a constant share of equities over time. This is intuitively clear, since under this assumption a given equity return has the same probability and the same effect on the (final) portfolio value regardless of when it occurs. In other words, it is equally likely and equally bad to lose, say, 10% of your investment on the first day as it is to lose it on the last day.

Under mean-reverting equity returns the situation is more complicated. Intuitively we would expect early losses to have a smaller effect than late losses, since an early loss has a higher chance of being “reverted” than a late loss. Qualitatively, this ought to imply a higher (optimal) equity exposure in the beginning of the period and a lower equity exposure at the end of the period. Quantitatively, however, we need to take account of the fact that we only benefit from mean-reversion if we maintain an equity exposure throughout. Loosely speaking, to benefit from the assumed mean-reversion we need to hold equities when they (hopefully) rebound later on. Essentially, “early” risk is better rewarded than “late” risk, but only if we take “late” risk. Mathematically, the optimal strategy needs to balance early and late risk taking account of the benefit late risk has on early risk.

We are looking for optimal strategies depending on time only. More precisely, the strategy is allowed to depend on the initial value of the state variables only. In particular, the strategy is not allowed to depend on the unobservable, stochastic excess return on equities as it changes over the period, nor on the value of the portfolio. This assumption makes the strategy less tailored to the specific capital market model used to derive it, and it is therefore reasonable to expect that the strategy is also close to optimal under other, less stylized, types of mean-reversion. The assumption also ensures that the strategies can be implemented and tested in practice, without the need to identify latent variables. Christiansen and Steffensen (2015, 2018) find optimal, deterministic strategies motivated by the fact that marketed life-cycle products are deterministic, but apart from their work only few results exist in the literature.

Focusing on deterministic strategies implies that the portfolio is log-normally distributed on all horizons, in the model employed. The problem can thereby be stated as optimizing the mean for given variance of the (log) portfolio value on the horizon of interest. We focus primarily on optimal equity strategies, but we also consider optimal rate strategies and jointly optimal strategies. The optimal equity strategies are derived by methods from calculus of variations in three steps. First, we derive an integral equation characterizing the optimal strategy. Second, we use the integral equation to derive a second order differential equation, which gives us the general solution. Finally, we derive and solve a system of equations for determining the constants of the general solution. The solution is explicit up to the presence of a Lagrange multiplier, which when varied gives the entire family of extremal, including optimal, strategies for varying levels of variance. We also provide illustrations of the results, discussing in particular the role of mean-reversion.

1.1 Outline

The rest of the paper is organized as follows. In Section 2 we set up the model and provide the distributional results on the portfolio value on future horizons needed for the optimization, in Section 3 we formulate and solve three optimization problems, finding optimal rate and equities strategies, both separately and jointly. The results are illustrated and discussed in Section 4, and Section 5 summarizes and concludes on the findings. All proofs and technical details are in the appendices.

2 Preliminaries

In this section we state the underlying capital market model. We refer to the model as a factor model due to its intended use as a sparse representation of generic “rates” and ”equities”. Accordingly, we interpret the resulting strategies as profiles for generic interest and equity risk, respectively. How to obtain this risk in practise, i.e., the selection of specific bonds and stocks, is outside the scope of the model.

After introducing the capital market model, we state a distributional result for portfolios resulting from time-dependent strategies of the kind we will be considering. The formulation and solution of the optimization problem rely on this result and the accompanying integral representation.

2.1 Capital market model

The capital market model is described in Jarner and Preisel (2017), see also Munk et al. (2004), but for ease of reference we restate it here. The model of Jarner and Preisel (2017) also contains realized inflation and break-even inflation (BEI) curves for pricing inflation-indexed bonds, and inflation swaps. Here, however, we disregard inflation and include only nominal interest rates and equities in the model.

Hence, the model features

-

•

A stochastic short rate ()

-

•

A bond market of all maturities with stochastic risk premium ()

-

•

A stochastic equity index ()

-

•

A mean-reverting equity risk premium ()

Since we are interested in portfolio optimization we need the so-called ’real world’ dynamics of the state variables of the model (sometimes referred to as the -dynamics as opposed to the -dynamics used for pricing). In addition to these, we also need the evolution of the term structure of interest rates (the yield curve) for pricing bonds.

We assume that the short (nominal) interest rate follows an Ornstein-Uhlenbeck process,

| (1) |

where is the long-run mean of the short interest rate, describes the degree of mean reversion, is the interest rate volatility, and is a standard Brownian motion.

The stock index (total return index) is assumed to evolve according to the dynamics

| (2) |

where is the short rate from (1), is the time-varying risk premium (expected excess return) from investing in stocks, is the stock index volatility, and is a standard Brownian motion. We further assume that the risk premium follows an Ornstein-Uhlenbeck process,

| (3) |

where denotes the long-run equity risk premium, describes the degree of mean reversion towards this level, and is the risk premium volatility. We assume joint normality of the two Brownian motions and with correlation coefficient .

Note that the stock index and the risk premium processes are locally perfectly negatively correlated, i.e., a stock return above or below its expected value will “cause” a change in the (future) risk premium in the opposite direction. This interaction induces a mean-reversion in the stock returns over time.

Finally, we assume that the term structure of interest rates is of the form considered by Vasicek (1977). Specifically, we assume that the (arbitrage free) price at time of a zero-coupon bond maturing at time is given by

| (4) |

with ,

| (5) | ||||

| (6) |

and where and are parameters controlling the slope and level of the yield curves.111The price of a zero-coupon bond can be obtained by the usual risk-neutral valuation formula, , where with being a -Brownian motion. The specification corresponds to the market price of interest rate risk being equal to

| (7) |

As shown in Section 5.1 of Jarner and Preisel (2017), the price dynamics of for fixed has the form

| (8) |

where

| (9) |

From (8) we see that the (negative) market price of interest rate risk, , can be interpreted as the risk-reward trade-off at a given point in time, i.e., as the excess return per unit of volatility. It is the continuous-time analogue to the Sharpe ratio used in portfolio construction and benchmarking, cf. Sharpe (1966, 1994). In general, the market price of interest rate risk depends on the current short rate, in particular, the market price of interest rate risk is stochastic. For subsequent use, we define the market price of equity risk as the excess return per unit of volatility when investing in equities,

| (10) |

2.2 Portfolio dynamics

We now consider the dynamics of a portfolio exposed to (interest) rate and equity risk. In general, the dynamics of the portfolio value, , is given by

| (11) |

where is the vector of (factor) exposures to rate and equity risk, respectively, is the vector of market prices of risk given by (7) and (10), and is the vector of driving Brownian motions.

The exposures are measured in volatility and formula (11) succinctly states that the excess return, i.e., the return in excess of the short rate, is the market prices of risk weighted by the exposure. As an example, if and we get

| (12) |

which is equal to the dynamics of the equity index, as expected.

In general, assuming only that the strategies are adapted and sufficiently regular, we have the following integral representation of the portfolio process

| (13) |

where is the (instantaneous) correlation matrix given by

| (14) |

This follows by an application of the multi-dimensional version of Itô’s lemma, see e.g. Proposition 4.18 of Björk (2009). Let , and use Itô’s lemma to calculate the differential of , where ,

which is the same as (11). Since the right-hand side of (13) equals for we conclude (under standard regularity conditions) that (13) is the solution to (11) as claimed. In the second equality of the above calculations we have used the formal multiplication rules: and .

2.3 Portfolio distribution

As mentioned in the introduction, we are aiming at finding the optimal risk-reward trade-off for a deterministic strategy, i.e., a strategy that depends on time only. We are aided in this task by the fact that under this restriction, the portfolio is log-normally distributed at every horizon. In this section we derive the necessary distributional results.

We need the following integral representations for the risk premium, the short rate and the integrated short rate from Section 3 of Jarner and Preisel (2017):

| (15) | ||||

| (16) | ||||

| (17) |

where is given by (9). Since and are linear in and , respectively, it follows from the expressions above that the integrals at the right-hand side of (13) are either deterministic, or stochastic integrals with deterministic integrands and Brownian integrators. From this observation, the claimed log-normality follows; the mean and variance are given by the following theorem.

Theorem 2.1.

Assume that is deterministic (depends on time only). For given , the portfolio value at time can be expressed as

| (18) |

where

| (19) | ||||

| (20) | ||||

| (21) | ||||

| (22) | ||||

| (23) |

In particular, is log-normally distributed with mean and variance given by

| (24) | ||||

| (25) |

Note that the weight functions and , which measure the impact of the risk sources and on the horizon value of the portfolio, contain both a direct and an indirect effect. Due to mean-reversion, the risk (innovation) at time measured by and , respectively, has both a direct effect which depends on the exposure at time (the terms and in and , respectively) and an indirect effect which depends on the subsequent exposure to the risk source (the integrals from to ). The direct effect depends only on the current exposure, while the indirect effect depends over the (future) exposure on the remaining horizon.

We also note that the indirect effect for rates disappears if , which corresponds to the case where the market price of interest rate risk is constant, . Thus, it is not the mean-reverting nature of the short rate process itself, but rather the state dependent market price of risk, that causes the indirect effect for rates. For equities, the indirect effect is caused by the feedback mechanism from equity risk to (future) equity risk premia. The size of this effect depends on the “loading” ratio and the degree of persistence, , in the equity risk premium process.

In principle, Theorem 2.1 can be used for joint optimization of the mean-variance trade-off at a given horizon. However, to make the computations easier to follow and to highlight the structure of the solution in special cases, we solve the problem in stages under various simplifying assumptions. We are primarily interested in the effect of mean-reverting equity returns and consequently we keep this feature, while we make the simplifying assumptions that the market price of interest rate risk is constant () and that rate and equity factors are independent ().

We state without proof a simplification of Theorem 2.1 to be used in the following.

3 Optimal mean-variance strategies

We are now ready to state the optimization problem(s) and derive the solution. As previously announced we proceed in stages: rates only, equities only, and finally combined rates and equities assuming independence of the two factors.

3.1 Optimal rate strategies

We first want to find the deterministic, rates only investment strategies that lead to the optimal (log) mean-variance trade-off on a given horizon. We consider only the case of a constant market price of interest rate risk, corresponding to . Clearly, a constant market price of interest rate risk is a mathematical simplification. However, at this stage we are primarily interested in getting an intuition for the structure of the optimal strategies in a simple setup.222The solution technique developed in the next section for handling mean-reverting stock returns can be used to solve the rates only problem for general , but the resulting strategies are less intuitive and harder to interpret.

Corollary 2.2 gives the mean and variance of the log portfolio value and the problem can therefore be phrased as

For given horizon, , the solution to Problem 3.1 takes the form of a family of strategies, one for each value of the variance . Members of this family are referred to as optimal bond strategies. More generally, we refer to bond strategies maximizing, or minimizing, (26) for given value of (27) as extremal bond strategies.

Theorem 3.1.

Assume such that the market price of interest rate risk is constant, . For given horizon , let for . The extremal bond strategies on horizon are of the form

| (28) |

where depends on the prescribed value of the variance .

The optimal bond strategies have , and the bond strategies minimizing the mean for given value of the variance have .

For , Theorem 3.1 yields , which is the strategy (globally) maximising (26). Recall from (8) that long positions in bonds correspond to negative exposures to the underlying Brownian motion, , and that positive excess returns for bonds correspond to . Thus, the maximizing strategy, , is long in bonds when bonds have positive excess returns, and short in bonds when bonds have negative excess returns. We typically expect positive excess returns for bonds, but we cannot rule out the possibility of negative excess returns, , neither mathematically, nor in practise. Also note, that the maximising strategy amounts to a constant exposure to interest rate risk over time; this is the only constant, optimal strategy.

The proof of Theorem 3.1 is a variational argument where plays the role of a Lagrange multiplier introduced to handle the variance constraint. At an extremal point (strategy) the gradients of the mean functional (the objective) and the variance functional (the constraint) are parallel with proportionality coefficient . If we are at a point where relaxing the constraint, i.e., allowing a larger variance, leads to a larger mean. Conversely, if we are at a point where a larger variance leads to a smaller mean. With this in mind, we can categorize the optimal strategies of Theorem 3.1 as follows.

In the limit tending to minus (or plus) infinity, we have the strategy , which corresponds to the buy-and-hold strategy of a bond that matures at time , cf. (8). This strategy has , and it is the optimal (and only) strategy with no variance on the horizon. For we obtain optimal strategies where added risk is rewarded, i.e., as is increased from minus infinity to zero we get optimal strategies with higher variance and higher mean. For we obtain the maximal mean possible. For , we have optimal strategies where added risk is penalized, i.e., strategies where the prescribed value of the variance can only be achieved by exposures so high that the quadratic term in (26) impairs the mean. Mathematically, these strategies are optimal in the sense that they achieve the highest possible mean given the variance, but in practice they are sub-optimal: for each of these strategies there exist strategies with lower variance and identical or higher mean. Hence, for practical purposes we are interested only in strategies of form (28) with .

3.1.1 Interpretation of the optimal bond strategy

The optimal strategy of Theorem 3.1 can be written , where . For , we have , and hence we can interpret the strategy as a convex combination of two optimal strategies: -bonds and constant risk exposure of size . It is natural to interpret the -bonds as a risk-free hedging component, and the constant risk exposure as a return-seeking component. This interpretation is supported by the fact that we always hold a long, unlevered position in -bonds, while the constant risk exposure is obtained by either a long or short bond position depending on the sign of the market price of interest rate risk.

Strictly speaking, this is only one possible way to interpret the optimal strategy. Since we are using a single factor rate model, all bond returns are fully correlated and only the net interest rate exposure matters. Furthermore, the exposure can be taken using bonds of any maturity (with varying degrees of leverage). Still, interpreting (28) as a combination of variance reducing -bonds ("hedging") and additional long, or short, return-seeking bond positions ("investments") provides a useful intuition. The structure and the interpretation closely resemble the classic two-fund separation theorem of modern portfolio theory, see Markowitz (1952); Tobin (1958); Merton (1972).

For we still have a linear, but no longer a convex, combination of "hedging" and "investment" strategies. More precisely, for we have and . Hence, in this situation we have a short position in -bonds and a long return-seeking position, larger than the optimal level of . Thus we are borrowing risk-free funds (as seen from time ) and investing these in the optimal return-seeking strategy. Finally, the extremal strategies minimizing the mean have which correspond to and . Essentially, we are spending the variance budget on borrowing funds as expensively as possible and investing them in risk-free -bonds.

3.1.2 Closed form expressions for the extremal mean and variance

For given , we can find the portfolio mean and variance by computing the integrals of (26) and (27), respectively, after substituting with the extremal strategy of (28). Due to the simple form of the extremal strategy it is possible to evaluate these integrals analytically, and we will do so here. However, apart from special cases, e.g., , or , the resulting expressions are hard to interpret. Instead, in Section 4.1 we will investigate numerically the risk-reward profile obtained by varying .

To express the results we introduce the function given by

| (29) |

Using this notation we can express the zero-coupon bond price as

| (30) |

where , cf. Section 5.1 of Jarner and Preisel (2017). This expression is valid for all values of . However, recall that the extremal strategies of Theorem 3.1 are derived under the simplifying assumption , such that is constant.

We can now evaluate (26) with given by (28)

| (31) | ||||

| (32) |

where we have used that . Evaluation of the integral in (27) with given by (28) gives us the extremal variance

| (33) |

It follows from (33) that there are two extremal strategies for any positive specification of the variance, with the pair of Lagrange multipliers characterising the strategies being of the form for . The strategy with is mean optimizing, and the strategy with is mean minimizing. In the limit for tending to plus or minus infinity, we have , i.e., is constant, and

| (34) |

where the first equality follows from Corollary 2.2, the second equality follows from (31)—(32), and the last equality follows from (30) with . Thus, as expected, the return on the risk free strategy equals the return on a zero-coupon bond maturing at the horizon.

3.2 Optimal equity strategies

In this section we set out to find the equity exposure strategy that leads to the optimal (log) mean-variance trade-off for excess returns on a given horizon. One might think of this as an overlay strategy to an underlying bond strategy, e.g., one of the strategies derived in Section 3.1. In particular, the equity strategy can act as an overlay to the hedging -bond strategy.

For reasons stated earlier, we are interested in deterministic, or strategic, equity exposure profiles only, i.e., we allow the strategy to depend on time and the initial equity risk premium only. In contrast to Problem 3.1, we solve the equity problem in full generality taking account of the mean-reverting risk premia. Mathematically, this makes the present problem much harder. The solution is presented in three steps: an integral equation characterizing the strategy, a general solution, and explicit formulas for the coefficients in the general solution.

Assuming independence between the two risk sources (), or alternatively no interest rate exposure (), the excess return due to equity exposure is well-defined. The (excess) mean and variance due to equity exposure is given by the terms and , respectively, of Theorem 2.1.

For ease of notation and in this section only, we drop superscript on all quantities relating to equities. We also introduce a short-hand notation for the expected market price of equity risk at future times

| (35) |

Using this notation we obtain from Theorem 2.1 the following corollary, which serves to formulate the problem.

Corollary 3.2.

Assume . For given , the excess return of due to equity exposure, , is log-normally distributed with mean and variance given by

| (36) | ||||

| (37) |

The problem of this section can now be phrased as

Similarly to Problem 3.1, for given horizon, , the solution to Problem 3.2 takes the form of a family of strategies, one for each value of the variance . Members of this family are referred to as optimal equity strategies. More generally, we refer to equity strategies (locally) maximising, or minimizing, (36) for given value of (37) as extremal equity strategies.

Before discussing the solution to Problem 3.2 in detail we start by noting that the global (unconstrained) maximum of is achieved for yielding ; the maximum is obtained by optimizing the integrand in (36) at each individually. In particular, the maximal excess return is finite and generally also strictly positive (except in the degenerate cases , or ). Let us denote by the variance associated with the optimal mean, i.e., (37) evaluated with . Since is the global maximum it is also the constrained maximum under the variance constraint . In particular, is an optimal equity strategy.

We typically expect a positive risk-reward trade-off, meaning that the larger the risk (variance) the larger the reward (mean). Hence, we typically expect that as we increase the prescribed value of the variance the associated optimal mean also increases. This however is true only up to a certain point, namely . As we vary the variance from to the optimal mean increases from to , but if we increase the prescribed value of the variance further the optimal mean starts to decrease. In other words, demanding a variance beyond is counter-productive in the sense that it can only be achieved by investing so much in equities that it impairs the mean log-return. Mathematically we can characterize the optimal strategies for any prescribed non-negative variance, but in practise we are interested only in optimal strategies with variance at most .

3.2.1 Characterization of extremal equity strategies

The double integral in (37) is a manifestation of the global nature of the problem by which later equity exposure reduces the variance arising from earlier exposure. The double integral also implies that Problem 3.2 does not immediately conform with problems solvable by the Euler-Lagrange equation of calculus of variations. However, we can still use a variational argument to arrive at the following integral characterization of the extremal equity strategies.

Extremal strategies are defined as stationary points (strategies) for the constrained optimization problem. These strategies are candidates for the optimal strategies, since optimal strategies are also extremal. However, extremal strategies can also be minimizing strategies, or local extremal strategies.

Lemma 3.3.

For given , the extremal equity strategies satisfy

| (38) |

where

| (39) |

and is a Lagrange multiplier.

The extremal strategies are characterized by having the same mean-variance trade-off for all (infinitesimal) perturbations of the strategy, i.e., if we alter an extremal strategy slightly such that the variance changes by , say, then the mean changes by , say, regardless of how we alter the strategy. The Lagrange multiplier, , is equal to minus the (common) value of the mean-variance trade-off for the corresponding extremal strategy; loosely speaking, . In principle, there could be more than one solution to (38) for given , but we will show later that the solution (if it exists) is unique. Hence, the extremal strategies are uniquely identified by their mean-variance trade-off.

Assuming sufficient regularity, differentiating (38) twice leads to a second-order differential equation in from which the general form of the solution can be inferred.

Lemma 3.4.

For given , the extremal equity strategies satisfy

| (40) |

where

| (41) |

Lemma 3.4 gives a surprisingly simple characterization of the extremal strategies as solutions to a differential equation with constant coefficients which do not depend on , nor . In general, the solution space to (40) is two-dimensional, and it remains to identify the specific solution also satisfying (38).

3.2.2 Optimal equity strategies with positive mean-variance trade-off

As noted in the introductory remarks to this section, the unconstrained maximum to (36) is achieved by and this strategy is an optimal strategy. We note that is also the (unique) solution to (38) when ; this is to be expected, since a Lagrange multiplier vanishes at a global maximum.

In the limit tending to minus infinity, we get the strategy with . It is not obvious that this is the limiting solution to (38), but it follows from the explicit solution given in Theorem 3.5 below. It also conforms with the intuition that the size of reflects the investor’s risk aversion. Although, as we shall see in Section 4.2.4, this intuition is only partly true.

Strategies satisfying (38) with correspond to extremal strategies with a positive mean-variance trade-off, i.e., strategies where added risk is rewarded in terms of higher mean. Varying in this range gives us all the strategies of practical relevance, ranging from the risk free strategy to the strategy achieving the global maximum. In this section we give an explicit expression for these strategies.333Strictly speaking, we only know that the strategies are extremal and with rewarded risk. However, we cannot rule out the possibility that for certain values of the variance constraint, there could exist both an extremal strategy with rewarded risk and a better (optimal) extremal strategy with unrewarded risk. This is conceivable because whether or not risk is rewarded is a local property applying only to infinitesimal changes in risk. A formal proof for the non-existence of this possibility would require an analysis of the global structure of the solution space, which is outside the scope of the present paper. In practise, however, it is easily verified that extremal strategies with positive mean-variance trade-off are indeed optimal; this can be observed from a mean-variance plot of the family of all extremal strategies for given model parameters, cf. Section 4

Hence, assume . Under this assumption, and . Note, that the strict negativity of holds even if (assuming and ). From standard theory we know that the general solution to (40) takes the form of a specific solution plus the general solution to the associated, homogeneous differential equation, . The characteristic polynomial of the latter is , which, under the current assumption, has two distinct, real roots and , say, and it follows that the general solution to the homogeneous differential equation is of the form . Regarding the specific solution, we note that solves (40), since is non-zero. Thus, the general solution to (40) is given by

| (42) |

where . This leaves the determination of the two coefficients and . To determine those we insert the general form of given by (42) into the left-hand side of (38). In general, this results in a linear combination of four exponential functions with different exponents, and a constant term. The requirement that all terms vanish gives us five equations for determining the five constants in (42), in particular and . This programme is carried out in Appendix A. For ease of reference, the following theorem summarizes the results (with superscript reintroduced).

Theorem 3.5.

Assume independent risk factors (). For given horizon , the optimal equity strategies with positive mean-variance trade-off are of the form

| (43) |

where , , with , , and given by (41), and depends on the prescribed value of the variance .

For , the exponents satisfy , and

| (44) |

For , the exponents are and , with

| (45) |

Note that the equity risk premium process is transient for , and exploding for , so for practical purposes we would consider using the model only for . Nevertheless, it is interesting to learn that the solution has the same structure regardless of the value of . Recall that the global maximum is achieved by with given by (35). This strategy is also of form (43) with either or equal to , and .

For tending to minus infinity, the exponents approach . In particular, the exponents have a finite limit. Further, for the -coefficients all tend to for tending to minus infinity, while for the sum of the -coefficients tends to in the same limit.444We here give an outline of the argument. Write (44) as . Using the established limits of and , we have that for , one of the bottom entries of diverges while the other three entries have finite, non-zero limits. Under the same condition on , the top entry of tends to , while the bottom entry has a finite limit. From this we can conclude that and both tend to . For the special case, , both and tend to for tending to minus infinity. It follows that the top row of converges to , while the top entry of equals . From this we can conclude that tends to . We leave it to the reader to handle the last special case, . Thus, in either case the limiting strategy is the risk-free strategy, , as previously claimed.

3.2.3 Extremal equity strategies with negative mean-variance trade-off

From a practical point of view, we are only interested in pursuing optimal strategies with a positive mean-variance trade-off, and these are therefore the main focus of the paper. However, it is very instructive to also study extremal strategies with a negative mean-variance trade-off, corresponding to . These strategies include both optimal strategies with "excessive" variance, minimizing strategies with lowest possible mean for given variance, but also "interior" strategies, where the mean is strictly between the minimal and maximal value for given variance. The latter class of strategies displays an intriguing variety of equity profiles, exemplified in Section 4.2.4. In this section we briefly discuss the different types of solution that can occur for . The actual strategies can be found in Appendix B, with Theorem B.1 giving an overview of the full set of extremal strategies.

Depending on the type of roots to the characteristic polynomial, , the extremal strategy takes one of three forms. For distinct, real roots we get the exponential solution already covered, for complex roots we get a trigonometric solution of form

| (46) |

where and , and in the special case where zero is a double root we get a quadratic solution

| (47) |

where .

The solution is exponential if and are of opposite signs, it is trigonometric if and are of the same sign, and it is quadratic in the special case and . In general, there is no extremal equity strategy for (). The domains for the respective solution types are illustrated in Figure 11 of Appendix B. We know that the exponential solution applies for , but we see from the figure that it is in fact also the "typical" solution for .

The quadratic solution defines the border between the exponential and trigonometric solutions. For given model parameters, there is (at most) one value of for which the extremal strategy is quadratic. Of course, one is unlikely to encounter this solution in applications, but it is interesting to note that quadratic solutions bridge the two main domains. This suggests that extremal strategies in general might be well approximated by quadratic strategies.

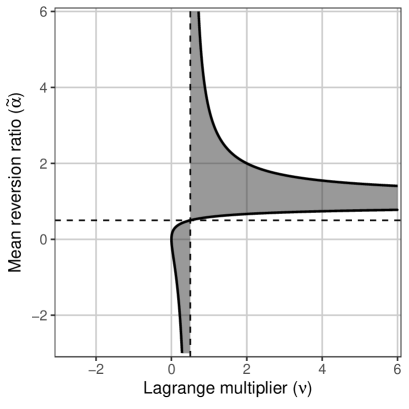

Finally, we note that the solution type depends only on and the mean reversion ratio , where can be interpreted as the volatility of the market price of equity risk, . Thus, apart from , the determining factor for the type of solution is the ratio of mean reversion strength to noise in the market price of equity risk process,

| (48) |

where denotes the long-run market price of equity risk.

3.3 Optimal joint strategies

Assuming independent risk factors (), the effects of rate and equity exposures can be separated and joint maximization can be performed based on the results of the preceding two sections.

To phrase the problem, let us first state a simplified version of Theorem 2.1.

Corollary 3.6.

The problem of this section can now be phrased as

For given horizon, , the solution to Problem 3.3 takes the form of a family of pairs of rate and equity strategies, one for each value of the variance . Members of this family are referred to as optimal pairs of strategies. More generally, we refer to pairs of strategies (locally) maximising, or minimizing, (49) for given value of (50) as extremal pairs of strategies.

We note that the mean and variance of Corollary 3.6 are the sum of the means and variances, respectively, of Corollaries 2.2 and 3.2. Further, the interest rate strategy, , and the equity strategy, , affect separate terms. This implies that the solutions to Problem 3.3 consist of the previously derived, optimal strategies to Problems 3.1 and 3.2. A fortiori, the extremal pairs consist of extremal bond strategies and extremal equity strategies with the same Lagrange multiplier, . Heuristically, the argument is as follows.

Assume is an extremal pair of strategies. This implies that the mean-variance trade-off is the same for all (infinitesimal) perturbations of the strategy. Since if this were not the case, it would be possible to combine two changes with different trade-offs to change the mean, while preserving the variance, contradicting the assumed extremity. In particular, the mean-variance trade-off is the same for all (infinitesimal) perturbations of only the rate strategy, or only the equity strategy. But since the mean-variance trade-off associated with is the same in Problem 3.3 as it is in Problem 3.1, we conclude that is in fact an extremal bond strategy. Similarly, is in fact an extremal equity strategy. Moreover, the mean-variance trade-off of and must match, and since the trade-off equals (minus) the Lagrange multiplier, , we conclude that the extremal strategies and must have the same value of . The argument can be made formal, but it is useful to keep the heuristic argument in mind.

Theorem 3.7.

Assume independent risk factors (), and constant market price of interest rate risk (). For given horizon , the extremal pairs of strategies consist of pairs with given by Theorem 3.1, and given by Theorem 3.5 (Theorem B.1) for the same value of .

For , the pairs are optimal strategies with positive mean-variance trade-off.

We note from Theorem 3.7 that all extremal rate and equity strategies belong to one, and only one, extremal pair. For the rate strategies, we can compute a priori the variance contribution by formula (33), but we have no similar (simple) formula for the variance contribution of the equity strategies. Thus, we cannot a priori say anything about the relative size of the variance contributions from rates and equities in the extremal pairs. In particular, we do not know in general whether the optimal pairs are balanced regarding rate and equity risk, or whether one of the risk sources dominates. Of course, we can answer this question numerically on a case by case basis by computing the family of extremal pairs and the variance contribution from each risk source.

In addition to the optimal pairs of strategies, it is also of interest to consider strategies with the same amount of rate and equity risk. Such risk parity, or balanced, strategies might be considered more robust as they do not rely on assumed differences in risk premia. In the present context, one could consider pairs of strategies with the same variance contribution on the horizon, i.e., pair up strategies solving Problems 3.1 and 3.2 for the same value of given by, respectively, (27) and (37). Again, this pairing has to be done numerically on a case by case basis. We do not pursue these ideas further in this paper.

3.3.1 Dependent risk factors

The case of dependent risk factors () is mathematically rather more challenging. In full generality, the problem amounts to maximising (24) for given value of (25). We see from Theorem 2.1, that for the mean and variance of are affected by terms depending on both and . Thus we cannot hope to solve the general problem by "stitching" together partial solutions. In fact, it is not even clear how to separate the mean and variance contributions arising from, respectively, the rate and equity exposures.

Apart from the mathematical difficulties, we also argue that the resulting strategies—if we were able to obtain them—are unlikely to be of much value in practice. An assumed correlation between rate and equity risk factors is very hard to verify in practice, and we therefore might be reluctant to pursue strategies which exploit this correlation. From that perspective, the independence assumption is the "neutral" assumption most often used in practice.

Rather than deriving the general solution, we can alternatively test the robustness of strategies derived under no correlation in an environment with correlation. We can, e.g., establish the correlation range for which the derived strategies are better than constant strategies. This in turn can be used as a guide for when the derived strategies are near-optimal without the need for an exact value of the correlation coefficient. We do not, however, pursue this idea further.

As an indication of the complexity of the optimal strategies under dependent risk factors we derive the optimal rate strategy for given equity exposure . Assuming , this amounts to maximizing the mean

| (51) |

for given value of the variance

| (52) |

These expressions follow from Theorem 2.1, see also Corollary 2.2 and Problem 3.1 for the original optimization problem. By a straightforward extension of the proof of Theorem 3.1 we find that the optimal rate strategies on horizon are of the form

| (53) |

with and . We see that, although computable, the strategy is complicated and with explicit reference to the given equity exposure via both and . This indicates that the optimal pais of strategies are presumably very complicated indeed, and we will not try to find them.

4 Numerical illustrations

In this section we provide numerical illustrations of the optimal risk-reward profiles and the underlying optimal strategies. We cover optimal rate and equity strategies separately, with an emphasis on the latter. Assuming independent risk factors, the jointly optimal pais of strategies consist of optimal rate and equity strategies with the same value of , cf. Theorem 3.7. Thus, joint optimization consists of pairing the illustrated optimal rate and equity strategies. We do not, however, explicitly consider joint optimization in this section.

4.1 Optimal rate strategies

In the following we consider the optimal strategies of Section 3.1, i.e., optimal strategies when we are allowed to invest only in the interest rate market. For illustrative purposes we consider two parameter sets, corresponding to moderate and low market prices of interest rate risk, cf. Table 1. For these parameter sets we show the risk-reward profile for the entire family of extremal strategies and we give examples of optimal rate strategies and the resulting portfolio distributions. We also consider alternative risk and reward statistics connected to the portfolio distributions.

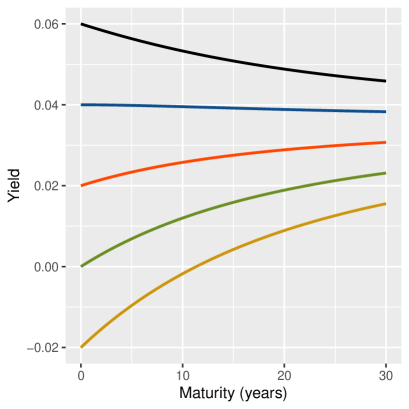

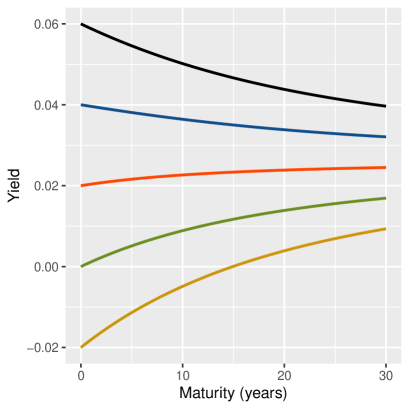

4.1.1 Yield curves

First, we visualize the interest rate assumptions. The continuously compounded zero-coupon yield for the period , , is defined by the relation . From (30) it follows

| (54) |

where , and and are defined by continuity. The yield as a function of is referred to as the yield curve. The yield curve and the corresponding curve of zero-coupon bond prices are equivalent ways of representing the bond market, but we typically prefer the former due to its more intuitive interpretation.

| Parameter set | ||||||

|---|---|---|---|---|---|---|

| Moderate | 0.08 | 0.02 | 0.007 | 0.08 | 0.04 | 0.2286 |

| Low | 0.08 | 0.02 | 0.007 | 0.08 | 0.03 | 0.1143 |

Figure 1 shows yield curves corresponding to different values of the short rate, , for the two parameter sets in Table 1. The yield curves represent the yield that can be locked in today (time ) by purchasing a zero-coupon bond. In the left plot interest rate risk is rewarded higher than in the right plot, and consequently the yields are higher. For example, if (green curves) we can lock in a return of per year on a 20-year horizon when the market price of risk is moderate (left plot), and a return of when the market price of risk is low (right plot). Note that since the short-rate -dynamics are the same in the two cases, a money-market account will give rise to the exact same return distribution on any horizon in the two cases, while bond strategies will yield higher returns in the "moderate" parameter set than in the "low" parameter set.

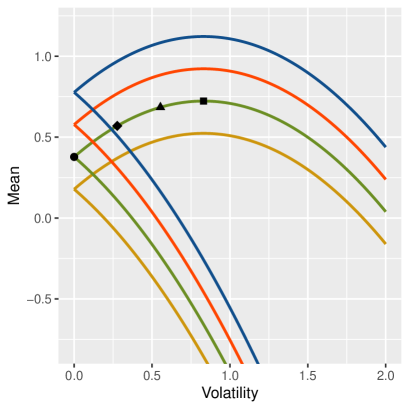

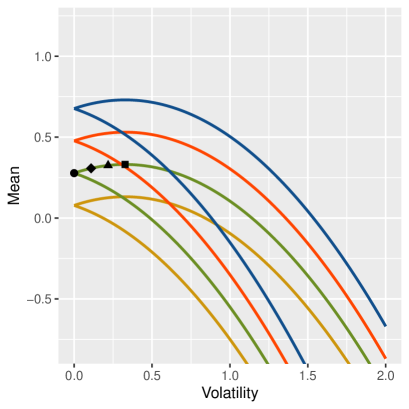

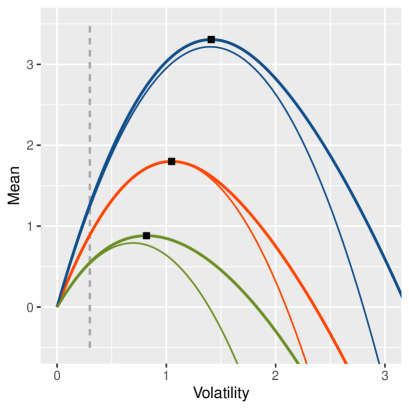

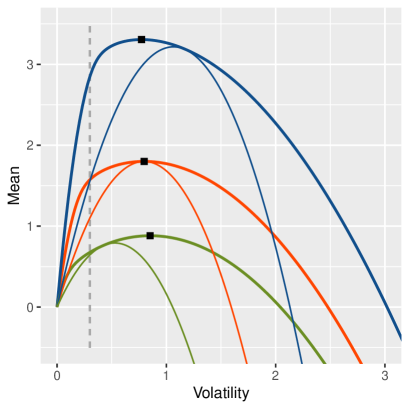

4.1.2 Risk-reward profiles

Section 3.1.2 provides formulas for the extremal mean and variance, i.e., the log-portfolio mean, , and the log-portfolio variance, , arising from following the extremal rate strategies of Theorem 3.1. Figure 2 plots against for for four different values of the initial short-rate, , using the same colour scheme as in Figure 1. We refer to the curves as risk-reward profiles. The upper part of the profiles represent maximizing strategies (), and the lower part of the profiles represent minimizing strategies (), where is the Lagrange multiplier of Theorem 3.1. The upper part of the profiles consists of an initial upward-sloping part () where adding risk increases the mean until the global maximum is achieved (), and a downward-sloping part () where risk is so high that adding further risk decreases the mean. Of course, for practical purposes only strategies with are of interest.

It follows from Corollary 2.2 and expressions (31)—(33) that,

| (55) |

where is a standard normal variate. Thus, the portfolio value on the horizon can be interpreted as the amount that can be locked in with certainty at time times a stochastic factor, . The stochastic factor depends on the -dynamics of the short-rate process, the market price of interest rate risk, and , but not on the initial value of the short-rate, . From this observation and (55) it follows that the profiles in Figure 2 are (vertical) translations of each other, with the (vertical) distance between two profiles being equal to the difference in log bond prices.

4.1.3 Portfolio distributions

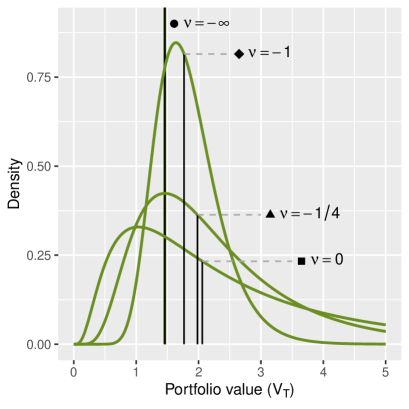

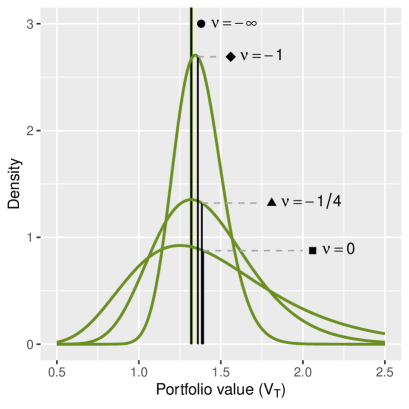

We have marked four points on each of the profiles in Figure 2 for . Figure 3 illustrates the underlying distribution of (for ); alternatively, we can interpret the plots as showing , i.e., the stochastic multiplier scaled by the 20-year bond return that can be obtained when . The thin black lines show the median, , of each distribution. As is increased from to the median increases, but the volatility also increases markedly. In particular, when the market price of risk is low (right plot) the increase in median is very modest compared to the additional risk. It follows from (55) that, apart from scaling, these plots will look the same for other values of .

In Appendix D, Tables 5 and 6 quantify various risk and reward statistics for for a range of optimal rate strategies. The tables show the median as a measure of the reward, along with three different risk measures:

-

•

The probability that we earn less than the risk-free investment, ;

-

•

The expected size of the loss given that we experience a loss, ;

-

•

The expected size of the loss, .

Since can be obtained with no risk by holding only -bonds, we interpret as a loss relative to this risk-free strategy. The risk measures therefore focus on the event . We see that for given , the probability of earning less than the risk-free investment is substantially higher when the market price of interest rate risk is low (Table 6) than when it is moderate (Table 5), but both the conditional and unconditional losses are smaller. This is due to the fact that the exposure depends on the market price of risk, see Figure 4. Thus, when risk is less rewarded the exposure is decreased and therefore as the distribution of moves "to the right" it also becomes more narrow.

4.1.4 Illustration of optimal strategies

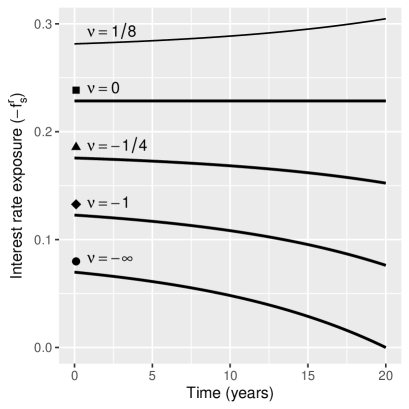

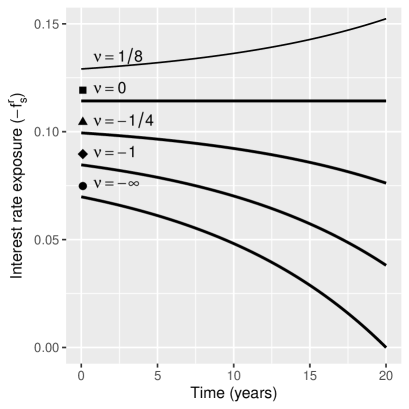

Figure 4 shows the underlying strategies for the portfolio distributions of Figure 3. The strategies are given by (28) of Theorem 3.1. The strategies give rise to the stochastic multiplier, , which acts on the risk-free bond return that can be locked in initially. The bond return depends on the initial yield curve which in turn depends on the initial short-rate, . The strategies themselves, however, do not depend on . In particular, Figure 4 is valid for all interest rate levels. In other words, an investor with a relative risk tolerance will choose the same strategy regardless of the interest rate level and thereby obtain the same (stochastic) multiplier on the risk-free investment. Conversely, an investor with an absolute risk tolerance will choose a strategy that depends on the interest rate level, but still within the family of optimal strategies.

In Figure 4 we plot the negated interest rate exposure () as a function time, rather than the interest rate exposure itself. The optimal exposure is negative (corresponding to holding bonds) and the negated exposure therefore gives a more intuitive plot with higher exposures implying larger bond holdings. Also, for the optimal strategies the negated exposure is equal to the (instantaneous) volatility of the portfolio.555It follows from (11) that, in general, the (instantaneous) volatility of the portfolio at time is given by . With no equity risk, , this reduces to , which equals when is negative.

Recall from Section 3.1 that corresponds to the risk-free, buy-and-hold strategy where is fully invested in -bonds, while corresponds to a constant risk exposure of which is the strategy achieving the (unconstrained) maximal mean. For we get a convex combination of these two strategies. Holding only -bonds corresponds to a (negated) exposure of with an initial volatility of , decreasing to zero over time. This (hedging) strategy does not depend on the market price of interest rate risk, and it is therefore the same for the two parameter sets. All other optimal strategies, however, depend on the market price of interest rate risk: The higher the market price of risk, the higher the optimal exposure (for given ).

Finally, Figure 4 also shows an example of an optimal strategy on the "wrong" side of the risk-reward profile () where risk is so excessive that the quadratic term in (26) impairs the mean. The exposure is still negative, however, i.e., we are long in bonds. In contrast, for mean minimizing strategies the exposure is fully or partly positive, corresponding to shorting bonds; if drawn these strategies would lie below the risk-free strategy.

4.2 Optimal equity strategies

We now turn attention to the optimal strategies of Section 3.2, i.e., optimal strategies where we are allowed to invest only in the equity market. Recall that we are optimizing excess returns on a given horizon and that we interpret the resulting strategies as overlay strategies, i.e, strategies where the exposure is financed by a corresponding short money-market position. In our setup, an equity strategy acts as a stochastic multiplier to (the portfolio value of) the underlying rate strategy, which in turn acts as a stochastic multiplier to the risk-free, -bond hedging strategy.

4.2.1 Volatility profiles and calibration of mean-reversion

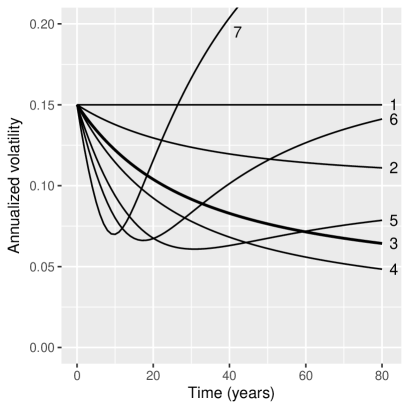

We begin with an investigation of the model for equity returns (2)—(3). The rationale for the model is that equity returns above/below the expected return leads to a decrease/increase in the future risk premium, . Thus, there is a tendency for gains to follow losses, and vice versa, and this mean-reversion feature effectively compresses the equity process, and prevents both extreme loses and extreme gains over longer periods. The model is simple, yet it can produce a variety of different volatility profiles for the equity process. In fact, the simplicity of the model is deceptive and counter-intuitive volatility profiles can easily arise even for "innocent looking" parameter values.

There are two parameters of interest in the risk premium process: controlling the degree of mean reversion, and controlling the size of feedbacks. At first sight, we are free to choose these parameters as we please. A larger/smaller causes a larger/smaller correction of the equity premium, while a larger/smaller value of causes a shorter/longer "corrective" period. While mean-reversion decreases the volatility of the equity process in the short term, excessive mean-reversion ( too large and/or too small) actually increases volatility in the long term. Intuitively, if mean-reversion parameters are set too aggressively, the uncertainty that builds up in the risk premium process can overshadow the short-term volatility reductions and lead to an overall increase in volatility.

In the following we study this phenomenon more formally and give recommendations on the degree of mean-reversion. We are interested in the process of excess equity returns, which we denote by . It follows from Section 3 of Jarner and Preisel (2017) that

| (56) |

and, further, from Section 6 ibid. it follows that

| (57) |

where is given by (29) on page 29 of the present report, and is given by

| (58) |

the interested reader is referred to Appendix A of Jarner and Preisel (2017) for background information on the expression for the variance. We note that the variance expression in (57) contains both a positive (first) term arising from the stochasticity of the risk premium itself, and a negative (last) term due to the link between innovations and risk premia. The asymptotic rate of increase of these two terms determine whether mean-reversion leads to an increase or a decrease of the long-term variance—compared to a (Black-Scholes) model with constant risk premium, .

For , we have from Section 6 of Jarner and Preisel (2017) that the asymptotic (rate of) variance is given by

| (59) |

where is the mean-reversion ratio encountered in Section 3.2.3. It follows from (59) that the asymptotic variance is the same, or below, the variance of the Black-Scholes model if and only if .

| Par. set | Asym. vol. | SD() | ||||

|---|---|---|---|---|---|---|

| 1 | 0.15 | 0 | 0.06 | 0.15 | 0 | |

| 2 | 0.15 | 0.003 | 0.06 | 3.00 | 0.10 | 0.0087 |

| 3 | 0.15 | 0.007 | 0.06 | 1.30 | 0.033 | 0.020 |

| 4 | 0.15 | 0.009 | 0.06 | 1 | 0 | 0.026 |

| 5 | 0.15 | 0.015 | 0.06 | 0.60 | 0.10 | 0.043 |

| 6 | 0.15 | 0.020 | 0.06 | 0.45 | 0.18 | 0.058 |

| 7 | 0.15 | 0.030 | 0.06 | 0.30 | 0.35 | 0.087 |

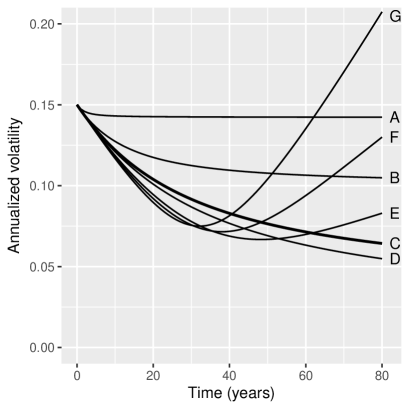

| Par. set | Asym. vol. | SD() | ||||

|---|---|---|---|---|---|---|

| A | 0.15 | 0.007 | 0.90 | 19.3 | 0.14 | 0.0052 |

| B | 0.15 | 0.007 | 0.14 | 3.00 | 0.10 | 0.013 |

| C | 0.15 | 0.007 | 0.06 | 1.30 | 0.033 | 0.020 |

| D | 0.15 | 0.007 | 0.047 | 1 | 0 | 0.023 |

| E | 0.15 | 0.007 | 0.020 | 0.43 | 0.20 | 0.035 |

| F | 0.15 | 0.007 | 0.010 | 0.21 | 0.55 | 0.049 |

| G | 0.15 | 0.007 | 0 | 0 |

The asymptotic volatility, i.e., the square-root of (59), is given by . For , and the effect of mean-reversion can be interpreted as reducing the (local) volatility. Conversely, for , and the volatility reduction due to mean-reversion in a sense "overshoots" the (local) volatility; if the overshoot is large enough mean-reversion in fact increases, rather than reduces, volatility. Also note, that for the two terms are equal and stocks are asymptotically risk free!

Figure 5 shows the annualized volatility, i.e, , as a function of time for the parameter sets in Tables 3 and 3. The highlighted, third parameter set is inspired by the empirical estimates reported in Table 1 of Munk et al. (2004) and it is the same in the two tables. With this parameter set as a starting point, we vary the values of and in Tables 3 and 3, respectively. In each case, we see that increased mean-reversion lowers the asymptotic volatility, but only up to a certain point (given by ). Beyond that point the asymptotic volatility starts to increase again and it eventually diverges as tends to zero. As mentioned above, this is due to the uncertainty that accumulates in the risk premium process. In the last column of each table, the standard deviation of the stationary distribution of the risk premium process is shown as a measure of this uncertainty.

Clearly, not every volatility profile in Figure 5 is suitable for modelling equity returns. It is noteworthy, that all parameter values appear reasonable and in fact they all (except set A) are within one standard error of their empirical estimates, cf. Munk et al. (2004). Thus, some kind of expert judgment is needed in the calibration process. The theoretical foundation for the model seems strongest for , and as a rule of thumb we recommend using parameter sets satisfying this constraint. Parameter sets with might be useful on shorter horizons, but on longer horizons they can lead to counter-intuitive results, as illustrated later.

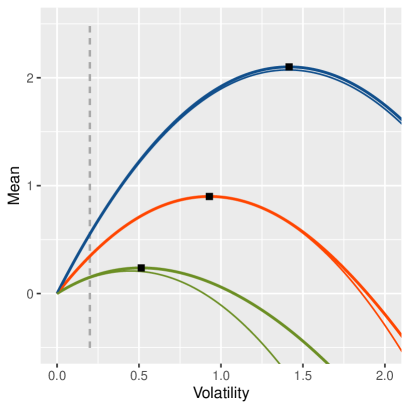

4.2.2 Risk-reward profiles

In this section we illustrate the optimal risk-reward trade-off that can be obtained by equity strategies, and we give examples of the optimal strategies. We also compare the optimal strategies with constant strategies; constant strategies provide a natural benchmark due to their optimality in the Black-Scholes model. In particular, it is instructive to see how the horizon and the degree of mean-reversion affect the performance of optimal and constant strategies differently.

We consider the two parameter sets given in Table 4, corresponding to a moderate () and high () degree of mean-reversion. The two sets are the same as sets 3 and 5 of Table 3 with an added assumption on the risk premium in stationarity, . For both parameter sets, the (expected) market price of equity risk in stationarity is . This is higher than the market price of interest rate risk used in Section 4.1, cf. Table 1, but lower than values typically used for equities.666Munk et al. (2004) reports on empirical estimates of and of and , respectively. This corresponds to a market price of equity risk in stationary of , which is more in line with levels typically used. However, we do not wish to overstate the return potential on stocks going forward, and therefore we use more conservative return assumptions in this paper. Note, that the market price of equity risk is stochastic, with sizeable variations both between paths and within paths. This stochasticity is part of the optimization problem and the main driver of the different (optimal) strategies that arise.

| Parameter set | ||||||

|---|---|---|---|---|---|---|

| Moderate | 0.045 | 0.015 | 0.007 | 0.06 | 1.30 | 0.30 |

| High | 0.045 | 0.015 | 0.015 | 0.06 | 0.60 | 0.30 |

It follows from Corollaries 2.2 and 3.2, that we can represent the portfolio value as

| (60) |

where and are independent, and determined by the rate and equity strategies, respectively. Further, is log-normally distributed, , where and are given by (36) and (37), respectively. Due to (60), we can study the effect of the rate and equity strategies separately. In Appendix D, Tables 7 and 8 show risk and reward statistics for for a range of optimal equity strategies.

Figures 6 and 7 plot against on horizons 20 and 40 years, respectively, for the optimal equity strategies. The profiles are constructed by varying from to , both values excluded. For each of the selected values of , the corresponding optimal strategy is found by Theorem B.1, and and are then computed by numeric integration of (36) and (37), respectively, with the optimal strategy inserted.777In fact, since for the two parameter sets under consideration and since the optimal strategies are all of exponential form (type I), cf. Figure 11 of Appendix B, and Theorem 3.5 also applies.

Each plot also shows the risk-reward trade-off for constant strategies, . For constant strategies the log-mean and log-variance of can be calculated explicitly as

| (61) | ||||

| (62) |

assuming both and are non-zero. The dedicated reader is encouraged to implement the variance formula and compare its behaviour as a function of time to the variance of a constant strategy in a Black-Scholes model, .

We see from Figures 6 and 7 that for moderate levels of mean-reversion the optimal strategies improve the mean only slightly compared to constant strategies, at least for the strategies of interest, i.e., strategies with . However, for high levels of mean-reversion substantial improvements are obtained on the 40-year horizon. Indeed, the optimal risk-reward profile in the right plot of Figure 7 is surprising. The profile is very steep initially meaning that substantial equity gains can be achieved on long horizons with very little risk. Mathematically, the high degree of mean-reversion allows a very effective netting of equity fluctuations—but only on long horizons, and only if the exposure is taken in the right way.

4.2.3 Illustration of optimal strategies

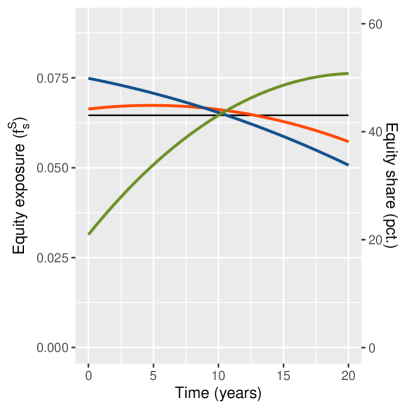

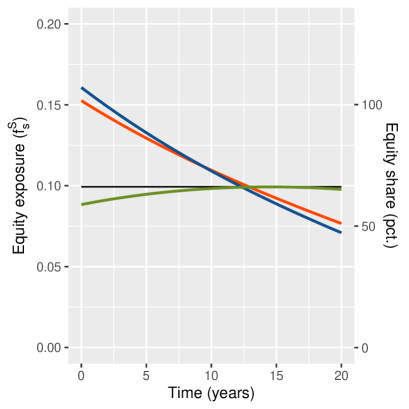

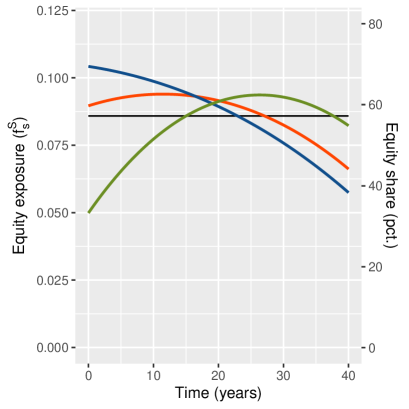

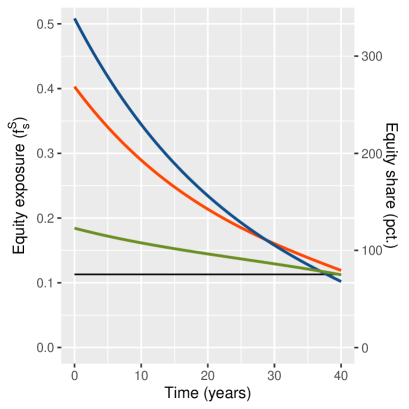

In Figures 8 and 9 we illustrate the optimal equity strategies with on 20 years horizon and on 40 years horizon, respectively. The optimal strategies exploit the dynamics of the risk premium process, and different strategies will therefore be employed depending on the initial value of the risk premium. Therefore, there are three optimal strategies in each plot, corresponding to the three different values of . In contrast, we see from (62) that the volatility of a constant strategy does not depend on . Consequently, for given volatility target the same constant strategy will be used regardless of ; the horizontal, black line in each plot shows this strategy.

The natural scale (left axis) for the strategies is the exposure, , to the Brownian motion driving equity returns. When positive, the exposure can be interpreted as the (local) volatility due to equity investments. To aid interpretation we also show (right axis) the exposure in terms of the corresponding equity share, i.e., . An equity share of, say, 50 pct. means that the equity exposure should equal the exposure obtained from investing half the portfolio in equities. Note, since all equity exposures are financed by equivalent short positions in cash, there is no upper limit on the equity exposure/share.

The optimal strategies are generally decreasing over time, except when the initial risk premium is sufficiently low. We also know that for moderate mean-reversion only little is gained from following the optimal strategy compared to a constant strategy, even though the strategies are quite different. However, with high mean-reversion and a long horizon optimal strategies substantially outperform constant strategies. We see from the right plot of Figure 9 that the optimal exposure is initially very high and declines rapidly thereafter. When mean-reversion is high, this profile is very effective at netting equity fluctuations over time, and constant strategies can only obtain the same volatility target by having a much smaller exposure.

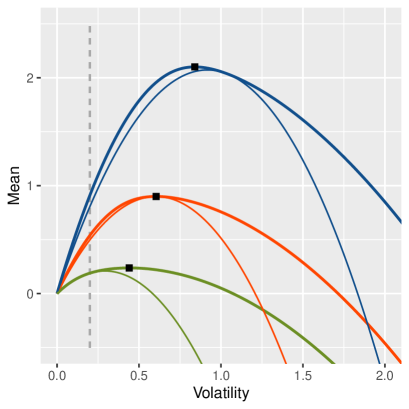

4.2.4 Interior wedges of extremal strategies

We conclude the numerical section with an illustration of a surprising phenomenon due to excessive mean-reversion. The risk-reward profiles shown in Section 4.1.2 have two branches. An upper branch consisting of optimal rate strategies and a lower branch consisting of minimizing rate strategies. From the calculations in Section 3.1.2 it follows that there can be no other extremal rate strategies. For extremal equity strategies the situation is considerably more complex.

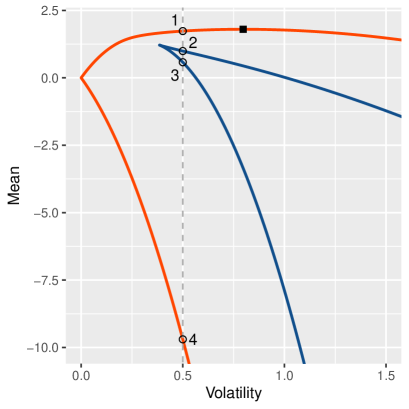

The left plot of Figure 10 shows the risk-reward profile for the entire family of extremal equity strategies () for the parameter set of Table 4 with high mean-reversion. We show the profile for a horizon of years and , but other horizons and initial risk premiums give similar plots. The upper branch of the profile is formed by ; this part is also shown in the right plot of Figure 7 (orange thick line). The remaining extremal strategies, however, do not all line up in a lower branch, as might be expected. Instead, an interior wedge of strategies is formed, in addition to the lower branch of minimizing strategies. The wedge consists of locally minimizing and maximizing strategies, i.e., strategies where, for given variance target, the mean cannot be improved, either upwards or downwards, in a vicinity of the strategies (in the underlying function space of strategies). A similar wedge does not occur for the parameter set of Table 4 with moderate mean-reversion.

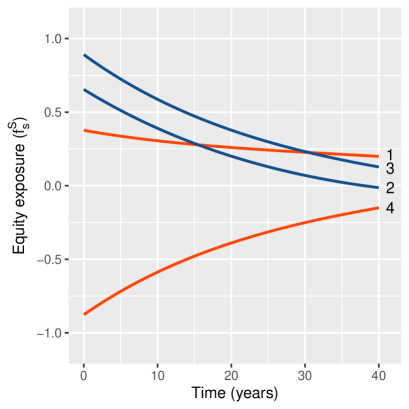

To investigate further this phenomenon, the right plot of Figure 10 shows the four different extremal strategies with . The optimal strategy (1) is similar to the optimal strategy shown in Figure 9 for (orange thick line). The "drastic" change in exposure over time of the optimal strategy is, however, dwarfed by the radical change in exposure of the minimizing strategy (4). Without a high degree of mean-reversion such a strategy would lead to a very high variance, but high mean-reversion in combination with declining (absolute) exposure all but cancel aggregate return fluctuations.

The locally minimizing strategy (3) is essentially the mirror strategy of the globally minimizing strategy: The same glidepath is used to control the variance, but with positive rather than negative exposure. The reason this strategy has a relatively low mean, is that the extreme leverage results in a large quadratic term that impairs the mean, cf. (36). The locally maximizing strategy (2) uses a dampened version of the same glidepath, but with an overall lower exposure resulting in a lower quadratic term and a higher mean.

In summary, high degrees of mean-reversion implies the existence of very aggressive glidepaths with low aggregate variance. Depending on the sign of the exposure, these glidepaths can be used as building blocks to create either very low, or high, but not optimal, portfolio means. It is the presence of these glidepaths that generates a richer set of extremal strategies than typically seen. Apparently, it requires a high degree of mean-reversion before the interior wedge appears. We conjecture that is a necessary condition, but we leave this as an open research question.

When mean reversion is even higher, e.g., parameter set 7 in Table 3, a multitude of interior wedges can appear with locally minimizing/maximizing exposure profiles of trigonometric form (not illustrated). These periodic profiles constitute yet another type of building block for obtaining (relatively) low variance even when the absolute exposure is very high. The structural richness of the extremal strategies is intriguing and further insights about the role of mean-reversion can undoubtedly be uncovered, but we leave that for others to explore.

5 Concluding remarks

In this report we have derived the mean-variance optimal investment strategies in a two-factor model with stochastic interest rates and mean-reverting equity returns, with the constraint that the strategies are allowed to depend on time only. Such deterministic strategies are closer to practical use than their state-dependent counterparts typically considered in the literature. We have used techniques from calculus of variations to obtain explicit solutions for optimal rate and equity strategies separately, and discussed how to combine these strategies. For equity strategies a complete solution has been provided, while optimal rate strategies have been derived under the simplifying assumption of constant market price of interest rate risk. We have also provided illustrations of the results, and discussed the calibration of the mean-reversion component in detail.

Assuming independent risk factors, the distribution of the portfolio on the horizon can be succinctly represented as

| (63) |

where and are independent, log-normally distributed random variates depending on the rate and equity strategies, respectively. Holding only -bonds and no equity risk corresponds to and thereby no risk on the horizon. All rate and equity strategies, or combination of these, deviating from this hedging strategy, entail a non-trivial risk-reward trade-off captured by the distribution of the stochastic multipliers, and . Appendix D contains tables with risk and reward statistics that can be used to assess this trade-off. The strategies are parameterized by , which can be interpreted as a risk-aversion parameter, with corresponding to the strategy with maximal log-mean.

We conclude from Appendix D that on long horizons, say, 30 years and above there exist equity strategies with substantial upside and very little risk of accumulated losses (). When mean-reversion is high the strategies are essentially risk free (Table 8), but also for moderate levels of mean-reversion the risk is low for all but the most aggressive strategies (Table 7). In other words, on long horizons, (optimal) equity strategies can function as return generating overlays with very low risk of performing below the risk-free, hedging strategy.

The optimal equity strategies are typically decreasing over time. This conforms with our intuitive understanding of the effect of mean-reversion. Essentially, "early" exposure is better rewarded than "late" exposure, since early losses are more likely to be (partly) compensated by subsequent excess returns than losses towards the end of the period. However, we have demonstrated numerically, that for moderate levels of mean-reversion constant strategies perform close to optimally. Indeed, under no mean-reversion, i.e., the Black-Scholes model, constant strategies are optimal. Conversely, with high levels of mean-reversion the optimal strategies outperform constant strategies significantly, but they rely on rather extreme glidepaths which may be hard to implement in practice.

Appendix A Optimal equity strategies with positive mean-variance trade-off

In this appendix we derive the (unique) solution to (38) of Lemma 3.3 for . These strategies correspond to the optimal equity strategies with positive mean-variance trade-off, as discussed in the main text. We assume throughout that and , while and can have any real value.

It follows from Lemma 3.4 that for the solution to (38), if it exists, must be of form

| (64) |

The plan therefore is to rewrite (38) using this form of , and from this derive the values of the five constants. We first carry out this programme, assuming and . The two special cases for are handled separately afterwards. Proof of uniqueness of the stated solutions is given at the end of the appendix. We begin with the following lemma, the conclusion of which we will need throughout.

Lemma A.1.

Assume and . Let , where and . Then, and . Further, the equation

| (65) |

has two distinct solutions given by .

Proof.

In the expression for , at least one of the terms and will be strictly positive, with coefficients and , respectively, which are both strictly negative. This implies , and since we have , and thereby also .

For the second statement, we first note that the assumption implies that . Now, consider

| (66) |

where with . Equation (66) expresses as a strict convex combination of two distinct values. In particular, , which is equivalent to .

Considering equation (65) we note that the right-hand side is finite, while the left-hand side diverges for approaching . In the search for a solution we can therefore assume . Under this assumption and introducing the short-hand notation , we can rewrite the left-hand side of (65) as follows

| (67) |

Equating this to the right-hand side of (65) and rearranging terms, we see that this is equivalent to with solution . Finally, since the solutions are distinct. ∎

The next two lemmas establish the (general) form of and as defined in Lemma 3.3.

Lemma A.2.

Proof.

This follows from inserting and evaluating integrals of the form for , , and . By assumption, all three exponents are different from , and the integral evaluates to . We get,

from which the result follows after expanding and collecting terms. ∎

Lemma A.3.

Proof.

This follows by the same argument as in the proof of Lemma A.2 using that, by assumption, all exponents are different from . We leave the details to the reader. ∎

Note, that the assumption of Lemma A.2 is slightly weaker than in Lemma A.3. In the former, we need to ensure that the exponents of are different from , while in the latter we need to ensure that the exponents of are also different from . Both assumptions are typically satisfied, except in certain special cases.

Proposition A.4.

Proof.

By Lemma A.1 we have that , and thereby also . The assumptions of Lemmas A.2 and A.3 are thereby satisfied, and we can use the conclusions of these lemmas to recast the left-hand side of condition (38) as

| (76) | ||||

| (77) | ||||

| (78) |

Condition (38) states that the expression above should equal for all . Since the exponents in (76)–(78) are all non-zero and distinct, this is satisfied if (and only if) the five expressions in square brackets in (76)–(78) are all . It remains to be shown that this is fulfilled if (and only if) the parameters take the stated values. For the current result we only need the "if"-part, but for the later uniqueness result we also need the "only if"-part; to facilitate this argument we show slightly more than needed below.

By Lemmas A.2 and A.3, we have that the expression in (76) is if and only if

| (79) |

and that the two expressions in square brackets in (77) are zero if and only if

| (80) | ||||

| (81) |

Further, assuming (80)–(81) hold and using , the two expressions in square brackets in (78) are zero if and only if

| (82) |

To reach the desired conclusion, we need to verify that (79)–(82) all hold. Clearly, satisfies (79), while (80) and (81) are satisfied by Lemma A.1. Finally, with , the right-hand side of (82) is equivalent to the rightmost column of (75), and it follows that (82) is also satisfied. ∎

Proposition A.4 leaves two cases to be handled separately. These are covered by the following propositions. The line of argument is the same, but the specific calculations differ slightly from those in the proof of Proposition A.4.

Proposition A.5.

Proof.

We will only give a sketch of the proof. By computations similar to those of Lemmas A.2 and A.3 we first obtain expressions for and ; the computations are left to the reader. Using these expressions we recast the left-hand side of condition (38) as

| (85) | ||||

| (86) |

where

As in the proof of Proposition A.4, it follows that condition (38) is satisfied if and only if the four terms in square brackets in (85) and (86) are zero. This in turn is equivalent to the following set of conditions,

| (87) | ||||

| (88) |

Since , we can use Lemma A.1 to conclude that (87) is satisfied, while it follows from (84) that (88) is satisfied. ∎

Note that the solution stated in Proposition A.5 is in fact the same as in Proposition A.4 with ; it is only the argument for verifying the solution that differs. This is due to the fact that in both cases the exponents, and , differ from . For the other special case, , the exponents equal which change the conditions somewhat.

Proof.

For use in the later uniqueness result, we will prove a bit more than needed to establish the current result. Consider of the form

| (91) |

By computations similar to those of Lemmas A.2 and A.3 we recast the left-hand side of condition (38) as

| (92) | ||||

| (93) |

where

Note that, compared to previous calculations there is apparently missing factors of in the -coefficients. These, however, are being absorbed by the (also missing) factors proportional to .

Collectively, Propositions A.4, A.5, and A.6 provide a solution to condition (38) of Lemma 3.3 for . The proofs of the propositions consist of deriving an equivalent set of conditions characterizing the constants in (64). Since we know that is of form (64), it might seem as if we have also shown uniqueness. However, there is a caveat. In deriving the equivalent set of conditions we make a priori assumptions on the value of the exponents, and , and of the constant (in Proposition A.5). To prove uniqueness we also need to check that condition (38) cannot be satisfied if and take values initially ruled out by assumption. This amounts to deriving alternative sets of equivalent conditions and showing that these cannot be satisfied. In principle, this is possible, but it is rather laborious. Fortunately, there is a shortcut to this brute force approach.

Proposition A.7.

Proof.

For , it follows from Lemma 3.4 that is of form (64) with . Moreover, it follows from general theory on ordinary differential equations (ODE) that the exponents are given by , since .

Revisiting the proof of Proposition A.4, the initial assumptions on and , and the recasting of condition (38) are thus justified, not by assumption, but as a consequence of Lemma 3.4. A fortiori, we can restrict attention to candidate solutions of form (64) with , , and , and for these candidate solutions the derived conditions are valid. In fact, conditions (79)–(81) are automatically satisfied, and a candidate solution is therefore an actual solution if and only if it satisfies condition (82). Finally, since (82) has a unique solution, the claimed uniqueness follows, in the case and . The same argument applies to the proofs of Propositions A.5 and A.6 showing uniqueness also for the cases , or . ∎

Appendix B Overview of extremal equity strategies