remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \newsiamthmassumptionAssumption \newsiamremarkexampleExample \headersRisk sensitive portfolio optimizationM. Pitera and Ł. Stettner

Discrete-time risk sensitive portfolio optimization with proportional transaction costs

Abstract

In this paper we consider a discrete-time risk sensitive portfolio optimization over a long time horizon with proportional transaction costs. We show that within the log-return i.i.d. framework the solution to a suitable Bellman equation exists under minimal assumptions and can be used to characterize the optimal strategies for both risk-averse and risk-seeking cases. Moreover, using numerical examples, we show how a Bellman equation analysis can be used to construct or refine optimal trading strategies in the presence of transaction costs.

keywords:

Risk sensitive portfolio, risk sensitive criterion, risk sensitive control, long time horizon, Bellman equation, portfolio optimization, transaction costs93E20, 91G10, 91G80, 49N60

1 Introduction

Quantitative portfolio management is an important part of mathematical finance. Stimulated by the seminal work [31], this field has been consistently evolving during the last 70 years for both discrete and continuous time settings, see [28, 12, 35] and references therein for an overview. Among the considered portfolio optimisation frameworks, the risk sensitive portfolio optimisation is among the most recognised ones, see [18, 6, 24]. Given a wealth process and the risk-averse parameter , the long-run version of risk sensitive criterion is defined as

| (1) |

where is the entropic utility. The optimality criterion presented in (1) measures the long-run normalised entropy of the log-wealth and could be seen as a non-linear extension of the Kelly’s criterion, see [30, 10, 19]. It should be noted that the extension (1) is in fact unique within the class of cash-additive and strongly time-consistent certainty equivalents which explains why the usage of entropy is so common in multiple stochastic control applications, see [29, 14] for details. In fact, the risk sensitive criterion appears naturally in many portfolio investment problems and is linked to various optimality frameworks. For completeness, let us provide some examples. First, by considering the second order Taylor’s expansion of the entropic utility, around , we get

which shows that, for , the risk sensitive framework might be considered as an extension of the mean-variance Markowitz portfolio optimisation that allows time-consistent utility treatment, see [7]. Second, (1) is directly linked to so called equivalent safe rate, which reflects the minimal hypothetical safe rate that would encourage the investor to invest in the risky portfolio, see [25]. Third, for the risk-averse case , the risk-sensitive criterion is dual to the downside risk, which is a common investment criterion in the long-run portfolio optimisation, see [32] or [33] for details. Fourth, for , the maximization of (1) is related to the studies of power utility asymptotics and can be considered as a dual problem to upside chance probability, see [33] and [39]. Finally, let us remark that risk sensitive criterion is an acceptability indicex (also called performance measure) and has many economically desirable properties, see e.g. [13, 5]. We refer to [7] for an overview of economic properties of risk sensitive criterion made in reference to portfolio management.

The main aim of this paper is to show that under the i.i.d. property imposed on asset’s log-returns one can solve a suitable risk-sensitive Bellman equation under proportional transaction cost and lack of short selling; see [20, 16] for a discussion about transaction cost impact on portfolio management. We emphasize that the set of additional assumptions imposed on log-returns in this paper is minimal, i.e. we only require that asset’s log-returns have finite mean and entropy. While this might be counter-intuitive on the first sight, as one typically impose strong ergodic assumption on the process in order to get the existence of risk-sensitive Bellman equation solution, the i.i.d. property proves to be a plausible alternative. For an overview of the key results, we refer to Theorem 4.3, Theorem 4.5, and Theorem 5.4.

The results of this paper are presented in a self-contained entropy based way to streamline the economic context; we hope this makes the paper more transparent and accessible to the generic mathematical finance community. That saying, the results presented here are in fact linked to an extensive literature on the risk sensitive stochastic control optimisation, and are expanding this framework in reference to portfolio management, see [6, 34]. That is why in some cases we decided to present alternative formulations of the Bellman equations, to link them more directly with the (controlled) Multiplicative Poisson Equation framework.

Our work is also linked to a variety of problems studied for Markov decision processes (see e.g. [3]) and recently studied continuous time risk sensitive problems with regime switching over finite time horizon, see [8, 27, 17]. In particular, we want to mention that the proof techniques presented in this paper are based on some novel ideas applied to vanishing-discount and span-contraction approaches, cf. [11, 36]. For instance, we were able to weaken the typical assumption imposed on the negative value of the log-process, by replacing Schwarz’s inequality based approximation with a tail-based argument in one of the key steps of local contraction property proof, see Proposition 32. Also, by incorportaing Arzela-Ascoli theorem into the vanishing discount approach, we were able to show the existence of a regular Bellman solution.

Apart from theoretical results, we present two numerical examples. They might be interesting to a reader who is not familiar with the risk sensitive stochastic control but wants to better understand why the study of Bellman equation could improve trading performance even in a very simplistic case. In particular, by using simple approximation schemes, one can directly recover no-action strategies that are important aspect of portfolio management in the presence of transaction costs, see [16]. This shows why the development of efficient risk sensitive approximation algorithms in the dynamic context can help to develop or benchmark trading strategies; see [23, 2, 9, 1] where practical aspects linked to risk sensitive policy iteration algorithms are studied.

This paper is organized as follows. In Section 2, we provide the general setup, state the assumptions, and formulate suitable Bellman equations. Next, in Section 3 we focus on the discounted version of the problem, that paves the ground for the usage of the vanishing discount approach. In Section 4 we follow the vanishing discount approach in order to show the key results of this paper. Then, in Section 5 we switch to the span-contraction approach in order to strengthen the results presented in Theorem 4.5 and show how to utilise the local contraction property in the i.i.d. setting. Finally, in Section 6 we present numerical examples.

2 Problem formulation

Let be a discrete-time filtered probability space, where . Let denote the number of available risky assets and let denote the positive vector price process, where denotes the price of the th risky asset at time . For a given trading strategy, we use to denote the portfolio asset volume vector at time after the portfolio is rebalanced, i.e. denotes how much asset we hold in our portfolio at time after the rebalancing is executed. Also, we use

| (2) |

where is the standard scalar product, to denote portfolio wealth process at time before and after the rebalancing, respectively. Throughout the paper we assume absence of short selling and follow the proportional transaction cost framework. This is partly encoded in the self-financing condition that is given by

| (3) |

where denotes vector point-wise product, function is the proportional transaction cost penalty given by

for a fixed cost rates such that , , and denotes (component-wise) positive/negative part of . To ease the notation, we introduce portfolio loading factors (portions of the capital invested in the assets, weights) vectors given by

| (4) |

Note that due to the absence of short selling, for any and , we have , where . Before we introduce the objective function, let us present a short technical lemma which shows that capital decay can be expressed as a function of factor loadings.

Lemma 2.1.

There is and continuous function such that

Proof 2.2.

Let be a function given by and let . Noting that is continuous, strictly increasing in , , and , we know that there exists function such that . On the other hand, using self-financing condition (3) we get

Since is strictly increasing with respect to we know that . It remains to show that is continuous. Let be such that and , as . Recalling that is continuous, strictly increasing in its first argument and satisfies as well as , we conclude that for any subsequence such that , for some , we get . Since the same limit is achieved for any subsequence , we get continuity of .

From Lemma 2.1 we see that the trading strategy could be represented via the loading factors (4). For any given -valued (adapted) strategy we use to denote the corresponding wealth process.

The main goal of this paper is to find strategy that maximizes long run risk sensitive objective function, applied to log-wealth process. Namely, we fix a risk-sensitivity parameter and consider the objective function given by

| (5) |

where is the entropic utility function; for consistency, we also use limit notation . Note that (5) is measuring time averaged entropy of portfolio’s log-return; see [7] for the economical context.

Since we are interested in optimising portfolio’s log-growth, throughout this paper we assume that the assets log-return vector , where , is an i.i.d. vector satisfying conditions

| (A.1) |

which means that log-returns are integrable and have finite entropy for the prefixed risk sensitive parameter .

Remark 2.3.

From assumption (A.1), using monotonicity of entropic risk with respect to risk-sensitivity parameter, we get that for any between and , we have . Also, note that assumption (A.1) could be rephrased using non-entropy notation as and , which could be linked to log-returns moment generating function finiteness.

For transparency, we also introduce an asset relative shift process given by

Let us now show how to re-express inner part of as a -controlled process. Let be given by . Noting that

and rewriting the objective criterion (5) as

| (6) |

we essentially get direct restatement of the controlled log-wealth process using control process and independent shifts .

In order to solve (6), we introduce the associated Bellman equation. Ideally, given , we are looking for a function and a constant which satisfy equation

| (7) |

for . Note that, with a slight abuse of notation, in (7) we use in reference to a deterministic pre-rebalancing and post-rebalancing weights rather than the whole rebalancing strategy; this convention is often used in the paper when optimality equations are considered.

For technical reasons, instead of considering (7) directly, in this paper we consider its slightly modified version given by

| (8) |

where and . In particular, we use instead of to emphasize the dependency between risk-parameter choice and Bellman’s equation solution, and to embed (7) into vanishing discount framework. Note that if and solves (8), then and solves (7). Also, Bellman’s equation (8) could be directly restated in a more classical form. Namely, for the risk-averse case we can rephrase (8) as

| (9) |

while for the risk-seeking case we get

| (10) |

For transparency, if not stated otherwise, we use in reference to equation (8).

In the following sections, we study the existence of the solution to the initial problem and its link to Bellman’s equation (7). For risk-averse case , we will show that under general assumption (A.1) and can solve the recursive version of (7) in order to get the optimal constant and optimal strategy. Moreover, by imposing additional condition on that is related to mixing, one can show that (7) could be directly solved without relying on the recursive scheme. On the other hand, for risk-seeking case assumption (A.1) alone imply existence of solution to (7).

For completeness, we will also show that selectors to the Bellman equation determine an optimal strategy in both cases. As already said, the results will be obtained using both vanishing discount approach as well as span-contraction approach.

3 Discounted problem

Before we apply the vanishing discount approach, let us provide a few remarks for the discounted version of problem (5). Consider and the discounted risk sensitive objective problem given by

The associated discounted analogue of Bellman equation (8) is given by

| (11) |

Note that (11) is in fact linked to a series of equations which effectively should provide the formula for . Nevertheless, for simplicity, we are looking for a stronger condition, i.e. a function that satisfies (11) for any value of risk sensitive parameter between and 0. In other words, we want (11) to hold on , for

where and . Nevertheless, with slight abuse of notation, if no ambiguity arise, we often use to denote a generic choice from .

As before, Equation (11) could be rephrased in a classical way, i.e. for we can restate (11) as

while for we can rewrite (11) as

Let us now introduce a lemma that will be helpful for establishing existence of solutions to Bellman’s equation (8). For brevity, we introduce supplementary notation

Note that and are finite due to (A.1).

Lemma 3.1.

Let and let us assume (A.1). Then, for any and we have .

Proof 3.2.

First let us consider the case where and . Using monotonicity and translation invariance of entropic utility we get

| (12) |

and

| (13) |

Now, for and , using similar calculations, we get

| (14) |

We are now ready to present the main theorem of this section.

Theorem 3.3.

Proof 3.4.

For brevity we only show the proof for ; the proof for is analogous. Fix and consider the Bellman operator linked to (11) that is given by

for any . First, let us show that is -Feller, i.e. it transforms bounded and continuous functions into themselves. Using Lemma 3.1 we immediately get

where denotes the standard supremum norm, which shows that boundedness is preserved. Now, let us show that continuity is also preserved for continuous bounded functions. First, since is continuous, for any sequence , where and , satisfying , we get

Now, using similar reasoning as in Lemma 3.1 we know that

Thus, noting that due to (A.1), and using dominated convergence theorem, we get

which in turn implies continuity of the mapping

| (15) |

Now, noting that is compact, we get continuity of . This concludes the proof of the -Feller property.

Now, we show that for , the iterated sequence of operators satisfies the Cauchy condition. For any and , we get

For brevity, and with slight abuse of notation, let us introduce the abbreviated notation . For any and (i.e. ), noting that entropic risk is additive for independent random variables and doing similar calculations as in Lemma 3.1, we get

| (16) |

Similarly, we get

| (17) |

Consequently, combining (16) and (17), for any we get

which shows that the sequence of functions satisfies the Cauchy condition. Now, note that for any , function is continuous and bounded due to Feller property. Consequently, as the space of bounded and continuous functions on is a Banach space, we know that there exists a bounded and continuous function such that

| (18) |

Now, noting that , we get that as well as , which shows that is a fixed point of operator .

Remark 3.5.

In the end of this section let us show a supplementary result linked to .

Lemma 3.6.

4 Vanishing discount approach

Fix and for any and define

| (20) | ||||

| (21) | ||||

| (22) |

where is a solution to the discounted Bellman equation (11). First, let us show that sequence introduced in (21) is uniformly bounded.

Lemma 4.1.

Proof 4.2.

We only show the proof for ; the proof for is analogous. Let us fix and . Using Lemma 3.6, for any and , we get

| (23) |

Consequently, recalling that is a solution to the discounted Bellman equation, rewriting using (11), applying (23), and then Lemma 3.1, we get

Similarly, we get . Noting that both upper and lower bound is independent of and , we conclude the proof.

Now, we present two main results of this section, which shows that under (A.1) one could find a sequence of functions solving the iterated Bellman equation. These functions could be used to find optimal strategy and related optimal value for the problem (5). While Theorem 4.3 is in fact true under both risk-averse () and risk-seeking () case, in the latter case we can show that iteration is not required, i.e. we can directly solve (8); this is stated in Theorem 4.5.

Theorem 4.3.

Let and let us assume (A.1). Then, there exists a sequence of constants , , and a sequence of continuous bounded functions , , such that the recursive Bellman equation

is satisfied for any . Moreover, the constant is the optimal value for the problem (5), i.e. we get , and the optimal (iterated) strategy is defined by the selectors to the recursive Bellman equation.

Proof 4.4.

Fix . First, observe that the family of functions , indexed by and is both uniformly bounded and equicontinuous. Indeed, both uniform boundedness and equicontinuity follows directly from Lemma 3.6 since for any we get

Thus, by the Arzela-Ascoli theorem, we know that there exists a decreasing sequence , such that , as , and for any , we have

| (24) |

for some continuous and bounded function . Second, from Lemma 4.1, we know that the sequence , can be chosen in such a way that for any we also have

| (25) |

where is some sequence of real numbers. Third, by combining Bellman equation (11) with (20) and (21), for any , we get

| (26) |

Now, noting that the limit values are also bounded, for each , we can take the limit in (26), as , and get

| (27) |

which concludes the first part of the proof. Now, iterating the sequence (27), starting from , and using tower property of entropic utility, for any , we get

where . Dividing both sides by , noting that the sequence of functions is uniformly bounded by , and taking the limes inferior of both sides, we get

which concludes the proof. Also, note that for any admissible strategy we get , while for the strategy determined by the iterated sequence we get .

Now, let us show that for , the result in Theorem 4.3 could be strengthened in a sense that recursive scheme is not required and one can solve directly (8).

Theorem 4.5.

Proof 4.6.

Fix . The first part of the proof is analogous to the proof of Theorem 4.5. Applying similar reasoning, we get that there exists sequence of constants and bounded continuous functions , such that

| (28) |

Now, let us show that for the sequence is non-decreasing. First, note that for any random variable , the mapping is convex.111This could be easily shown using Hölder inequality by considering and , for , with , such that and , and taking logarithm of both sides. Consequently, since supremum of a family of convex functions is convex, we get that for any and the mapping is also convex. In particular, for any , we get

| (29) |

which implies . Now, letting in the decreasing sequence defined in the proof of Theorem 4.3, we get

which concludes this part of the proof. Second, from (29) we get

Again, taking the limit , for the decreasing sequence defined in the proof of Theorem 4.3, we get

Consequently, the sequence of functions is increasing wrt. . As the sequence is equicontinuous and bounded, there exists a continuous bounded function such that , as . Now, since for some , as , we get

Now, note that for any we get as otherwise, the sequence , that could be represented by

would be unbounded which would lead to contradiction as , for . This implies

| (30) |

Due to Arzela-Ascoli theorem, as the mapping is equicontinuous and uniformly bounded, we can choose a subsequence and continuous bounded function such that

Finally, as , , recalling (30), and letting in (27) we get

which concludes the proof.

5 Span-contraction approach

In Section 4 we have shown that for one can solve directly Bellman equation (8); see Theorem 4.5. On the other hand, for , we were only able to obtain the recursive scheme as presented in Theorem 4.5. In this section, we show that the solution to (8) exists also for under relatively weak ergodic assumptions imposed on asset log-returns. We follow the span-contraction approach; see e.g. [34]. In the span-contraction approach the parameter is kept fixed in a sense that we do not need to introduce the discounting scheme. Consequently, to ease the exposition, rather than using notation from (8), we revert to the one from (7): we fix one and write rather than . As usual, we use to denote the space of continuous and bounded functions . For any we introduce supremum norm and span semi-norm notation

Note that those norms are bound by relation

| (31) |

see [34] or [26] for details. Now, we introduce additional assumption that relates to ergodicity and plays a central role in the span-contraction approach. Namely, for any , we assume that

| (A.2) |

where identifies a set of strategies in which we allocate at least proportion of capital to each asset. This assumption is related to mixing and states that whatever our initial (non-degenerated) allocation is, we expect to be in some common set with positive probability.

Remark 5.1 (Ergodicity/mixing assumption relevance).

Recalling that , for any we get which shows that (A.2) is in fact related to assumptions imposed on . Nevertheless, we decided to present (A.2) in its classical form, to show the connection to mixing. One can show that assumption (A.2) is satisfied by any log Levy process, even with ergodic economic factors, see [22, Proposition 1] for details. Also, one can notice that if has full support, then the assumption (A.2) is automatically satisfied.

Now, for any we introduce operator

It is relatively easy to show that operator is -Feller. In particular, using similar reasoning as in Lemma 3.6, for any we get

| (32) |

which implies boundedness of , for any . Let us now show that is a local contraction.

Proposition 5.2.

Proof 5.3.

Let us fix . For any and let

denote the projection measure for with rebalancing , and let

denote the optimal rebalancing (induced by operator ) given and initial state . First, let us show that for any and we get

| (33) |

where is a signed measure and is the total variation norm given by

for being the total variation of ; see [34] for details. Using dual representation for entropic risk, and performing similar calculations as in [34, Lemma 1] we get

Now, recalling that for any we have , we know there exists such that

Consequently, for denoting the positive set of measure , we get

which concludes this step of the proof. Now, let us fix and show that there exists constant such that for any satisfying and , and , we get

| (34) |

Suppose that (34) is not satisfied. Recalling that

we get that there exists a sequence of sets , functions satisfying and , and weights such that

| (35) |

Now, let and . For any , and , we get

| (36) |

Let us now assume there exists , such that and let , where is the generalised (lower) quantile function of . First, if there exists such that and , then we have

| (37) |

Second, let us assume there is no such that and . Then, we have and consequently, for , we get

| (38) |

Combining (36), (37) and (38), for any , , , and , such that , there exists such that

| (39) |

From (A.1), both and are finite for any . Also, note that is increasing and the choice of in (37) depends only on the choice of , i.e. given condition , the choice of is independent of the choice of , and . Consequently, combining (35) with (39), recalling that and , for , we get and , as . Therefore, as , we have

| (40) |

Noting that , we get that (40) contradicts (A.2), which concludes the proof of (34). Combining (33) with (34) we conclude the proof.

Finally, we are ready to show the main result of this section; note that while in Theorem 5.4 we adjusted notation from to , the presented conclusions are consistent with those presented in Theorem 4.5 (for instead of ).

Theorem 5.4.

Proof 5.5.

For any fixed , combining (32) with Theorem 5.4 we get that there exists a unique (up to an additive constant) function and a constant such that

| (41) |

Now, let and for ; note that also solves (41) and we get due to (32) and property . Thus, the family of functions is uniformly bounded and equicontinuous since, by (41), we get

| (42) |

Consequently, using Arzela-Ascoli theorem, we know that there exists a function and a subsequence , , such that (uniformly) and , as . Thus, due to uniform convergence, we get

| (43) |

where . Now, since right hand side of (43) is a continuous function of , we also get

which concludes the proof.

6 Numerical examples

In this section we illustrate the implications of Theorem 4.5 and Theorem 5.4. Namely, for exemplary dynamics, we approximate the optimal strategies and maximise the objective function (5) using the associated Bellman’s equations. For brevity, we study only the risk-averse case and focus on a simple low-dimensional setting in which one can directly approximate optimal policies following the standard policy iteration algorithm under known dynamics, see [40] for details. It should be noted that the policy iteration scheme could be also applied to a more realistic high-dimensional market setting in which transition kernel might be unknown, change in time, etc. For an overview of more advanced methods based on Reinforced Learning, -learning, etc., we refer to [23, 2, 9, 1]. The goal of this section is to illustrate how to numerically approximate the solution (7) and recover the optimal policy used to construct optimal trading strategy. Namely, by considering iterations of operator given by

| (44) |

we get a series of functions , , , that should converge in the span norm, as , to the solution of the Bellman’s equation (7). By studying the difference of the consequent iterations, we have control over so called regret that can tell us how far from the optimal policy we are, see [23]. Le us now present two illustrative examples that show why detailed look into Bellman’s equation could lead to a more optimal trading choice under transaction costs when confronted with plausible alternatives.

First, we introduce a two-dimensional toy example based on finite state-space dynamics. Its aim is to show that even under simplistic setting, one can meaningfully increase the trading performance by solving a Bellman’s equation and easily recover optimal barrier-hit strategy with a simple numerical scheme.

Second, we introduce a three dimensional example based on correlated Gaussian noise with drift. Note that while in this paper we follow an i.i.d. framework under which very generic assumptions (A.1) and (A.2) are sufficient to guarantee the existence to Bellman’s equation (7), similar reasoning could be applied to a more generic Markovian setting, see e.g. [34] where the discrete-time version of the Merton’s inter-temporal capital asset pricing model (CAPM) is considered.

Example 6.1 (Toy example).

To illustrate how to approximate Bellman equation’s solution and how the solution is linked to portfolio performance let us present a simple two-dimensional example based on finite state-space dynamics. Let , , and let , , where is an i.i.d. sequence of log-returns such that

| (45) |

Note that the sequence satisfies assumption (A.1). Let us assume that the proportional transaction cost penalty is antisymmetric with 10%/20% costs, i.e let the penalty function be given by , , for and . Noting that for any we get and using notation as well as we can rewrite operator given in (44) as

| (46) |

For the dynamics introduced in (45), we get that (46) is equal to

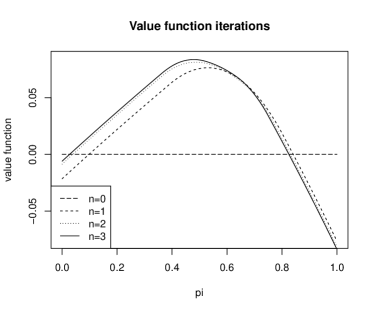

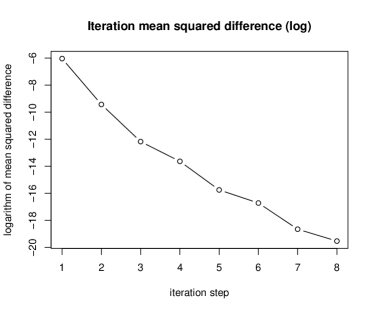

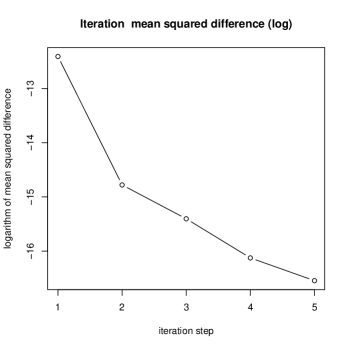

so that a simple univariate iterration scheme could be applied to recover the value of given . In fact, simple numerical calculations show that the value of iterated value function (centered with constant from (31) to increase calculation robustness) stabilizes relatively fast. This is illustrated in Figure 1

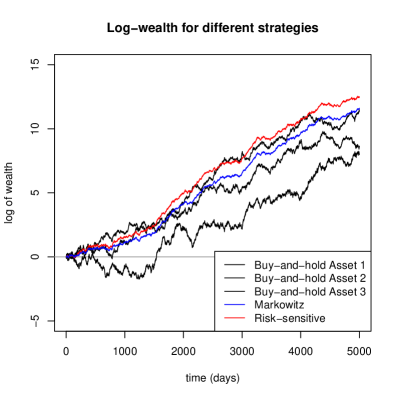

Noting that the convergence rate is fast, we decided to set and use optimal strategy induced by in the optimisation. To illustrate the usefulness of risk-sensitive approach we study the asymptotic dynamics of the wealth function under various trading strategies for the dynamics introduced in (45). Namely, we consider four trading strategies: (1) Static buy-and-hold asset 1 strategy; (2) Static buy-and-hold asset 2 strategy; (3) Dynamic proportion strategy; (4) Dynamic strategy induced by risk-sensitive framework.

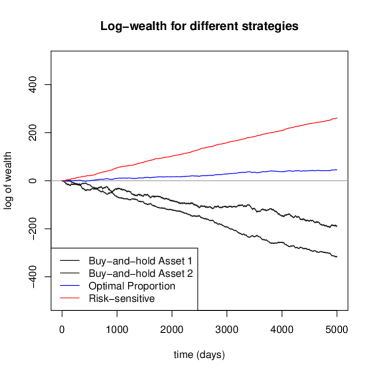

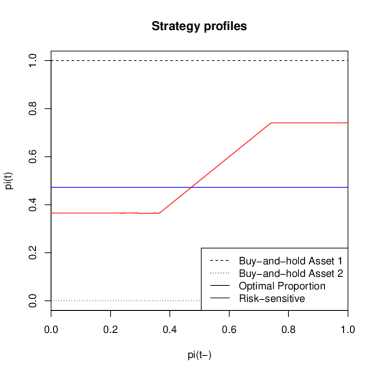

To compare the performance of trading strategies on a single long trajectory, we simulate a single realisation of , for , with initial capital , Then, we apply the trading strategies to the dataset; the proportion in strategy (3) have been chosen in such a way that the final portfolio value is the highest, i.e. we decided to choose the trajectory-optimal proportion. The log-wealth evolution as well as trading strategy profiles could be found in Figure 2.

From the plot a couple of things can be deduced. First, the risk-sensitive strategy outperforms all other strategies and shows the benefits of dynamic rebalancing. In particular, while the static strategies lead to losses, the dynamic risk-sensitive strategy produces relatively stable gains. Second, as expected, the risk-sensitive induced strategy is a barrier-trading strategy. In other word, if for a given day the (proportion) value falls outside of some interval (ca. ), then the trading strategy push it into this interval with cost-efficient approach. On the other hand, if the value is inside the interval, then it is optimal to not impose any trading. Third, we see that it is advised to study dynamic trading strategies even in the most simplistic transaction-cost setting – the performance improvement coming from applying risk-sensitive strategy to the problem looks material even when confronted with optimal proportion strategy.

Next, to fully understand the balance between the pay-off and the risk, we decided to calculate cumulative log-wealth for multiple trajectories and check their performance using assessment metrics. Namely, we consider the (time-normalised) mean, standard deviation, and entropy function ; note the time-averaged entropy of log-wealth corresponds directly to the risk-sensitive objective function (5). For completeness, we also added values for entropy second-order Taylor expansion based on mean and variance which illustrates the link between risk-sensitive framework and mean-variance framework. Note that while mean-variance trading might lead to time-inconsistency, the risk-sensitive trading is time-consistent, see [7, 4] for details. Also, to better understand the difference between risk-sensitive and risk-neutral frameworks, we decided to include the results for strategy similar to (4) but with risk-sensitivity parameter set to , which approximates the risk-neutral setting, see [21]. With slight abuse of notation, we call it the risk-neutral strategy. The aggregated results are presented in Figure 3.

| Strategy | Mean | Std | Mean+ Variance | Entropy () |

|---|---|---|---|---|

| Buy-and-hold asset 1 | -0.053 | 0.029 | -0.106 | -0.101 |

| Buy-and-hold asset 2 | -0.053 | 0.041 | -0.156 | -0.146 |

| Optimal proportion | 0.005 | 0.009 | 0.000 | 0.000 |

| Risk-sensitive | 0.049 | 0.009 | 0.044 | 0.044 |

| Risk-neutral | 0.050 | 0.012 | 0.042 | 0.043 |

By looking at Figure 3 we see that the risk-sensitive trading strategy outperforms trading strategies (1)-(3). While the normalised log-mean for the risk-neutral strategy is higher compared to risk-sensitive strategy (which is in fact expected as the log-mean reflects directly the objective function in the risk-neutral setting), it also results in higher variance. In other words, in the risk-sensitive case, the smaller mean (ca. 2% decrease) is compensated by risk decrease (ca. 25% variance reduction) which seems like a plausible trade-off. This suggests that the risk-sensitive strategy might be the optimal choice among all considered strategies. Also, as expected, the risk-sensitive strategy has the highest entropy among all strategies.

Example 6.2 (Gaussian noise with a drift).

In this example, we focus on a three dimensional correlated Gaussian noise with a positive drift. Let , and let , , where is an i.i.d. sequence of log-returns such that , where

| (47) |

Next, let and let the penalty function be given by , , for and . The parameters are fixed in such a way that we have both positive and negative correlation in assets; note the correlation coefficients for are (ca.) equal to , and . Also, the transaction costs reflect pay-off between return (mean) and risk (variance). The assumption (A.1) is satisfied for as the moment generating function for Gaussian random variables exists and assumption (A.2) is satisfied as the support of is full.

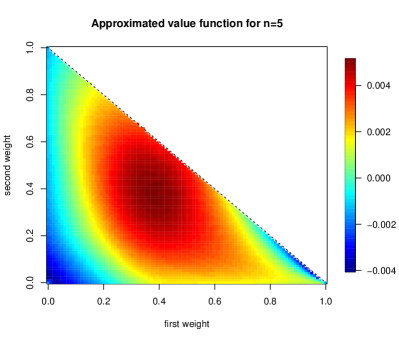

First, as in Example 6.1, we approximate the solution to Bellman’s equation. The approximation was made on a discrete -grid of step-size 0.02. By analysing the consequent differences and the shape of the approximated value functions, we decided to set , i.e use approximated value of to determine the trading strategy. The approximation results are illustrated in Figure 4; note that for any we get , so it is sufficient to analyse a two-dimensional graphs.

From Figure 4 we see that the approximated value function is regular with maximal value around point . Recalling that entropy utility function has a second order Taylor expansion , one would expect that this point (approximatelly) corresponds to an optimal allocation obtained using Markowitz portfolio optimization. This could be easily verified by solving a quadratic programming problem of the form

| (48) |

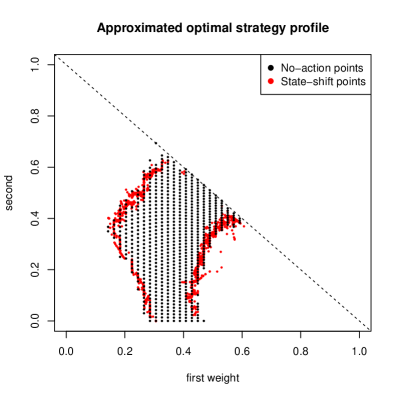

for which we get . Let us now confront the (approximated) trading strategy with other alternative strategies as in Example 6.1. Namely, we consider five trading strategies: (1) Static buy-and-hold asset 1 strategy; (2) Static buy-and-hold asset 2 strategy; (3) Static buy-and-hold asset 3 strategy; (4) Dynamic Markowitz proportion strategy; (5) Dynamic strategy induced by risk-sensitive framework. In strategy (4) we shift the allocation to the state induced by (48), i.e. we follow the optimal Markowitz strategy for risk aversion under no transaction costs. While the full illustration of the trading strategy obtained via Bellman’s equation approximation (as presented in Figure 2) is problematic (it would require four-dimensional plot) we can analyse strategy structure by looking at no-action points as well as shift points, i.e. sets of ’s such that no trading is executed if we are in the state and sets of all ’s that are the target state for some pre-trading initial state. The trading results for an exemplary long single trajectory as well as simplified strategy profile is presented in Figure 5.

Next, we analyse trading performance by looking into (time-averaged) performance metrics introduced in Example 6.1. The aggregated results are presented in Figure 6.

| Strategy | Mean | Std | Mean+ Variance | Entropy () |

|---|---|---|---|---|

| Buy-and-hold asset 1 | 0.0025 | 0.0031 | -0.00358 | -0.00561 |

| Buy-and-hold asset 2 | 0.0015 | 0.0022 | -0.00149 | -0.00147 |

| Buy-and-hold asset 3 | 0.0020 | 0.0025 | -0.00203 | -0.00193 |

| Markowitz proportion | 0.0024 | 0.0012 | 0.00144 | 0.00143 |

| Risk-sensitive | 0.0026 | 0.0013 | 0.00151 | 0.00151 |

From Figure 6 we see that risk-sensitive trading strategy is outperforming all other strategies and has the highest entropy, as expected. While the variance for Markowitz strategy is slightly smaller, the Markowitz allocation leads to smaller mean – the payoff between the two is better for risk-sensitive strategy as could be seen by looking into both Entropy and performance criterions. To better understand the difference between risk-sensitive strategy and Markowitz strategy it is best to look into trading intensity. While the Markowitz strategy has homogeneous trading intensity (as expected, as the strategy should always push the allocation back to the fixed point), the risk-sensitive strategy shows more intense trading on rare occasions, i.e. when the process falls outside of the zone presented in Figure 5. In fact, while the trading for Markowitz strategy was initiated for almost all of the considered days, the trading for risk-sensitive strategy was initiated in only 176 days (ca. 3.5% of sample size). Moreover, the aggregated trading intensity for risk-sensitive strategy, measured e.g. by cumulative product of capital decays, is much smaller. This shows that intense re-balancing could in fact negatively impact performance, especially in the transaction cost regime.

References

- [1] A. Arapostathis, A. Biswas, and S. Pradhan, On the policy improvement algorithm for ergodic risk-sensitive control, Proceedings of the Royal Society of Edinburgh Section A: Mathematics, 151 (2021), pp. 1305–1330.

- [2] A. Basu, T. Bhattacharyya, and V. S. Borkar, A learning algorithm for risk-sensitive cost, Mathematics of operations research, 33 (2008), pp. 880–898.

- [3] N. Bäuerle and A. Jaśkiewicz, Stochastic optimal growth model with risk sensitive preferences, Journal of Economic Theory, 173 (2018), pp. 181–200.

- [4] T. R. Bielecki, T. Chen, and I. Cialenco, Time-inconsistent markovian control problems under model uncertainty with application to the mean-variance portfolio selection, International Journal of Theoretical and Applied Finance, 24 (2021), p. 2150003.

- [5] T. R. Bielecki, I. Cialenco, S. Drapeau, and M. Karliczek, Dynamic assessment indices, Stochastics, 88 (2016), pp. 1–44.

- [6] T. R. Bielecki and S. R. Pliska, Risk-sensitive dynamic asset management, Applied Mathematics & Optimization, 39 (1999), pp. 337–360.

- [7] T. R. Bielecki and S. R. Pliska, Economic properties of the risk sensitive criterion for portfolio management, Review of Accounting and Finance, 2 (2003), pp. 3–17.

- [8] L. Bo, H. Liao, and X. Yu, Risk sensitive portfolio optimization with default contagion and regime-switching, SIAM Journal on Control and Optimization, 57 (2019), pp. 366–401.

- [9] V. S. Borkar, Learning algorithms for risk-sensitive control, in Proceedings of the 19th International Symposium on Mathematical Theory of Networks and Systems–MTNS, vol. 5, 2010.

- [10] J. Y. Campbell and L. M. Viceira, Strategic asset allocation: portfolio choice for long-term investors, Clarendon Lectures in Economic, 2002.

- [11] R. Cavazos-Cadena and D. Hernández-Hernández, Vanishing discount approximations in controlled Markov chains with risk-sensitive average criterion, Advances in Applied Probability, 50 (2017), pp. 204–230.

- [12] P. Chandra, Investment analysis and portfolio management, McGraw-hill education, 2017.

- [13] A. S. Cherny and D. B. Madan, New measures for performance evaluation, The Review of Financial Studies, 22 (2009), pp. 2571–2606.

- [14] A. S. Cherny and V. P. Maslov, On minimization and maximization of entropy in various disciplines, Theory of Probability & Its Applications, 48 (2004), pp. 447–464.

- [15] S. Christensen, A. Irle, and A. Ludwig, Optimal portfolio selection under vanishing fixed transaction costs, Advances in Applied Probability, 49 (2017), pp. 1116–1143.

- [16] C. Czichowsky and W. Schachermayer, Duality theory for portfolio optimisation under transaction costs, The Annals of Applied Probability, 26 (2016), pp. 1888–1941.

- [17] M. K. Das, A. Goswami, and N. Rana, Risk sensitive portfolio optimization in a jump diffusion model with regimes, SIAM Journal on Control and Optimization, 56 (2018), pp. 1550–1576.

- [18] M. H. A. Davis and S. Lleo, Risk-sensitive investment management, vol. 19, World Scientific, 2014.

- [19] M. H. A. Davis and S. Lleo, Risk-sensitive benchmarked asset management with expert forecasts, Mathematical Finance, 31 (2021), pp. 1162–1189.

- [20] M. H. A. Davis and A. R. Norman, Portfolio selection with transaction costs, Mathematics of operations research, 15 (1990), pp. 676–713.

- [21] G. B. Di Masi and Ł. Stettner, Remarks on risk neutral and risk sensitive portfolio optimization, in From Stochastic Calculus to Mathematical Finance, Springer, 2006, pp. 211–226.

- [22] T. Duncan, B. Pasik-Duncan, and Ł. Stettner, Growth optimal portfolio selection under proportional transaction costs with obligatory diversification, Applied Mathematics & Optimization, 63 (2011), pp. 107–132.

- [23] Y. Fei, Z. Yang, and Z. Wang, Risk-sensitive reinforcement learning with function approximation: A debiasing approach, in International Conference on Machine Learning, PMLR, 2021, pp. 3198–3207.

- [24] W. H. Fleming and S. J. Sheu, Risk-sensitive control and an optimal investment model, Mathematical Finance, 10 (2000), pp. 197–213.

- [25] P. Guasoni, A. Tolomeo, and G. Wang, Should commodity investors follow commodities’ prices?, SIAM Journal on Financial Mathematics, 10 (2019), pp. 466–490.

- [26] M. Hairer and J. C. Mattingly, Yet another look at Harris’ ergodic theorem for Markov chains, in Seminar on Stochastic Analysis, Random Fields and Applications VI, Springer, 2011, pp. 109–117.

- [27] H. Hata, Risk-sensitive portfolio optimization problem for a large trader with inside information, Japan Journal of Industrial and Applied Mathematics, 35 (2018), pp. 1037–1063.

- [28] P. N. Kolm, R. Tütüncü, and F. J. Fabozzi, 60 years of portfolio optimization: Practical challenges and current trends, European Journal of Operational Research, 234 (2014), pp. 356–371.

- [29] M. Kupper and W. Schachermayer, Representation results for law invariant time consistent functions, Mathematics and Financial Economics, 2 (2009), pp. 189–210.

- [30] L. C. MacLean, E. O. Thorp, and W. T. Ziemba, The Kelly capital growth investment criterion: Theory and practice, World Scientific, 2011.

- [31] H. Markowitz, Portfolio selection, The journal of finance, 7 (1952), pp. 77–91.

- [32] H. Nagai, Downside risk minimization via a large deviations approach, The Annals of Applied Probability, 22 (2012), pp. 608–669.

- [33] H. Pham, Long time asymptotics for optimal investment, in Large deviations and asymptotic methods in finance, Springer, 2015, pp. 507–528.

- [34] M. Pitera and Ł. Stettner, Long run risk sensitive portfolio with general factors, Mathematical Methods of Operations Research, 83 (2016), pp. 265–293.

- [35] J.-L. Prigent, Portfolio optimization and performance analysis, CRC Press, 2007.

- [36] Y. Shen, W. Stannat, and K. Obermayer, Risk-sensitive Markov control processes, SIAM Journal on Control and Optimization, 51 (2013), pp. 3652–3672.

- [37] Ł. Stettner, Discrete time risk sensitive portfolio optimization with consumption and proportional transaction costs, Applicationes Mathematicae, 4 (2005), pp. 395–404.

- [38] Ł. Stettner, Long time growth optimal portfolio with transaction costs, in Optimality and Risk – Modern Trends in Mathematical Finance, Springer, 2009, pp. 237–250.

- [39] Ł. Stettner, Asymptotics of HARA utility from terminal wealth under proportional transaction costs with decision lag or execution delay and obligatory diversification, in Advanced Mathematical Methods for Finance, Springer, 2011, pp. 509–536.

- [40] P. Whittle, Risk-sensitive optimal control, Wiley New York, 1990.