dsgDSG papers

[1]JPMorgan Chase Bank, N.A., New York, NY, USA — {dylan.a.herman,yue.sun,marco.pistoia}@jpmorgan.com \affil[2]University of Chicago, Chicago, IL, USA — codygoogin@uchicago.edu \affil[3]University of Delaware, Newark, DE, USA — {joeyxliu,isafro}@udel.edu \affil[4]Menten AI, San Francisco, CA, USA — alexey.galda@menten.ai \affil[5]Argonne National Laboratory, Lemont, IL, USA — yuri@anl.gov

A Survey of Quantum Computing for Finance

Abstract

Abstract. Quantum computers are expected to surpass the computational capabilities of classical computers during this decade and have transformative impact on numerous industry sectors, particularly finance. In fact, finance is estimated to be the first industry sector to benefit from quantum computing, not only in the medium and long terms, but even in the short term. This survey paper presents a comprehensive summary of the state of the art of quantum computing for financial applications, with particular emphasis on stochastic modeling, optimization, and machine learning, describing how these solutions, adapted to work on a quantum computer, can potentially help to solve financial problems, such as derivative pricing, risk modeling, portfolio optimization, natural language processing, and fraud detection, more efficiently and accurately. We also discuss the feasibility of these algorithms on near-term quantum computers with various hardware implementations and demonstrate how they relate to a wide range of use cases in finance. We hope this article will not only serve as a reference for academic researchers and industry practitioners but also inspire new ideas for future research.

⋆These authors contributed equally to this work.

1 Introduction

Quantum computation relies on a fundamentally different means of processing and storing information than today’s classical computers use. The reason is that the information does not obey the laws of classical mechanics but those of quantum mechanics. Usually, quantum-mechanical effects become apparent only at very small scales, when quantum systems are properly isolated from the surrounding environments. These conditions, however, make the realization of a quantum computer a challenging task. Even so, according to a McKinsey & Co. report [1], finance is estimated to be the first industry sector to benefit from quantum computing (Section 2), largely because of the potential for many financial use cases to be formulated as problems that can be solved by quantum algorithms suitable for near-term quantum computers. This is important because current quantum computers are small-scale and noisy, yet the hope is that we can still find use cases for them. In addition, a variety of quantum algorithms will be more applicable when large-scale, robust quantum computers become available, which will significantly speed up computations used in finance.

The diversity in the potential hardware platforms or physical realizations of quantum computation is completely unlike any of the classical computational devices available today. There exist proposals based on vastly different physical systems: superconductors, trapped ions, neutral atoms, photons, and others (Section 3.3), yet no clear winner has emerged. A large number of companies are competing to be the first to develop a quantum computer capable of running applications useful in a production environment. In theory, any computation that runs on a quantum computer may also be executed on a classical computer—the benefit that quantum computing may bring is the potential reduction in time and memory space with which the computational tasks are performed [2], which in turn may lead to unprecedented scalability and accuracy of the computations. In addition, any classical algorithm can be modified (in a potentially nontrivial way) such that it can be executed on a universal quantum computer, but without any speedup. Obtaining quantum speedup requires developing new algorithms that specifically take advantage of quantum-mechanical properties. Thus, classical and quantum computers will need to work together. Moreover, in order to solve a real-world problem, a classical computer should be able to efficiently insert and obtain the necessary data into and from a quantum computer.

This promised efficiency of quantum computers enables certain computations that are otherwise infeasible for current classical computers to complete in any reasonable amount of time (Section 3). In general, however, the speedup for each task can vary greatly or may even be currently unknown (Section 4). While these speedups, if found, can have a tremendous impact in practice, they are typically difficult to obtain. And even if they are discovered, the underlying quantum hardware must be powerful enough to minimize errors without introducing an overhead that counteracts the algorithmic speedup. We do not know exactly when such robust hardware will exist. Thus, the goal of quantum computing research is to develop quantum algorithms (Section 4) that solve useful problems faster and to build robust hardware platforms to run them on. The industry needs to understand the problems that can best benefit from quantum computing and the extent of these benefits, in order to make full use of its revolutionary power when production-grade quantum devices are available.

To this end, we offer a comprehensive overview of the applicability of quantum computing to finance. Additionally, we provide insight into the nature of quantum computation, focusing particularly on specific financial problems for which quantum computing can provide potential speedups compared with classical computing. The sections in this article can be grouped into two parts. The first part contains introductory material: Section 2 introduces computationally intensive financial problems that potentially benefit from quantum computing, whereas Sections 3 and 4 introduce the core concepts of quantum computation and quantum algorithms. The second part—the main focus of the article—reviews research performed by the scientific community to develop quantum-enhanced versions of three major problem-solving techniques used in finance: stochastic modeling (Section 5), optimization (Section 6), and machine learning (Section 7). The connections between financial problems and these problem-solving techniques are outlined in Table 1. Section 8 covers experiments on current quantum hardware that have been performed by researchers to solve financial use cases.

Overview of Earlier Surveys

Although the field of quantum computing is one of the most dynamic today and some scientific conclusions, approaches, and technologies become obsolete relatively quickly, we reiterate the importance of getting information from different perspectives. Here we emphasize the difference between our survey and several existing surveys that have recently been published or appeared in open domain. One of the key differences is that in our survey we not only summarize the recent achievements but also discuss the limitations of quantum devices and algorithmic approaches that are currently subject to massive abuse in the media.

In [3], Egger et al. focus on covering the hardware and algorithmic work done by IBM. We take a much broader view and survey the entire landscape of quantum technologies and their applicability in the finance domain. For example, we believe it is beneficial to also discuss the quantum annealing-based approaches and other gate-based devices. Also, with regard to optimization applications, we discuss a much wider variety of financial applications that make use of optimization and may take advantage of quantum hardware development.

The article by Bouland et al. [4] focuses on works done by the QC Ware team with a central emphasis on quantum Monte Carlo integration. Some more recent work has been done in that area and is included in our survey. Also Bouland et al. focus on portfolio optimization. While this is an important financial problem that we also cover, we have tried to include other financial applications that use optimization as well. Moreover, we tried to delve deeper into the various quantum machine learning approaches for generative modeling and neural networks.

The survey by Orus et al. [5] does an excellent job at highlighting financial applications that make use of quantum annealers. However, we believe the quantitative finance and quantum computing communities would also benefit from hearing about other quantum optimization approaches and devices. We also tried to delve a little bit deeper into how quantum annealing works and discuss universal adiabatic computation. Given that the field of quantum computation is so dynamic, we believe the community can benefit from seeing more recent work.

A recent survey by Pistoia et al. [6] covers a variety of quantum machine learning algorithms applicable to finance. In our review, we discuss a broader array of applications outside the realm of machine learning, such as financial applications that make use of stochastic modeling and optimization.

2 Applicability of Quantum Computing to Finance

Numerous financial use cases require the ability to assess a wide range of potential outcomes. To this extent, financial institutions employ statistical models and algorithms to predict future outcomes. Such techniques are fairly effective but not infallible. In a world where huge amounts of data are generated daily, computers that can perform predictive computations accurately are becoming a predominant need. For this reason, several financial institutions are turning to quantum computing, given its promise to analyze vast amounts of data and compute results faster and more accurately than any classical computer has ever been able to do. Financial institutions believe that once they are capable of leveraging quantum computing, they are likely to see important benefits. This section introduces financial use cases that are projected to lend themselves to a quantum computing approach.

2.1 Macroeconomic Challenges for Financial Institutions

The financial services industry is expected to reach a market cap of $28.53 trillion by 2025, with a compound annual growth rate of 6% [10]. While this industry is often considered incredibly stable and insulated from change, shifting government regulations, new technologies, and customer expectations present challenges that require the industry to adapt. We discuss here three key macroeconomic financial trends that can be impacted by quantum computing: keeping up with regulations, addressing customer expectations and big data requirements, and ensuring data security.

2.1.1 Keeping Up with Regulations

The Third Basel Accord, commonly known as Basel III, is an international regulatory framework set up in response to the 2008 financial crisis. Basel III sets requirements on capital, risk coverage, leverage, risk management and supervision, market discipline, liquidity, and supervisory monitoring [11]. These regulations require computing numerous risk metrics, such as value at risk (VaR) and conditional value at risk (CVaR). Because of the stochastic nature of the parameters involved in these computations, closed-form analytical solutions are generally not available, and hence numerical methods have to be employed. One of the most widely used numerical methods is Monte Carlo integration, since it is generic and scalable to high-dimensional problems [12]. Quantum Monte Carlo integration (Section 5.1) has been shown to offer up to a quadratic speedup over the performance of its classical counterpart. Engaging in ways to determine risk metrics with higher levels of accuracy and efficiency will enable financial institutions to make better-informed loan-related decisions and financial projections.

2.1.2 Addressing Customer Expectations and Big-Data Requirements

Customer personalization has become increasingly important in finance. For example, financial technology (FinTech), in contrast to traditional finance, thrives on providing personalized services. A Goldman Sachs report has highlighted the necessity for financial institutions to provide new big-data-driven services to align with changing consumer behavior [13]. According to a Salesforce 2020 publication [14], 52% of customers expect companies to always personalize offers, while only 27% of customers feel that the financial services industry provides great service and support [14]. Financial institutions must meet this expectation in order to continue to retain their customers. The current classical techniques for analyzing data have large computational demands and require significant time to train algorithms, whereas quantum algorithms may be able to speed up these computationally intensive and time-consuming components. As financial institutions continue to generate data, they must be able to employ that data in a functional way to improve their business strategy. Additionally, data organization can allow financial institutions to engage with customers’ finances more specifically and effectively, supporting their customer service and keeping customers engaged despite other options such as FinTech. Much of this data analysis is done by dealing with large matrices, which can be computationally demanding for classical computers.

2.1.3 Ensuring Data Security

Ensuring data security is one of the most pressing concerns for the financial services industry, according to an article by McKinsey [15] discussing rising cybersecurity issues. An increase in digitization has occurred due to the rise of FinTech. Additionally, as a result of the COVID-19 pandemic, substantially more financial activity is performed online. According to the McKinsey article, 95% of board committees discuss cyber and tech risks four or more times a year. Financial institutions must stay up to date with online security and remain vigilant against attackers. Quantum computing data modeling and machine learning techniques could allow financial institutions to identify potential risks with higher accuracy. Furthermore, even if one does not plan to use quantum computation, one must be knowledgeable about it because of its ability to break current public-key cryptographic standards [16, 17, 2], such as RSA and Diffie–Hellmann, including the common variants based on elliptic curves [18]. This is due to quantum computing’s ability to efficiently solve the Abelian hidden subgroup problem [19]. Although current quantum computers cannot achieve this task, financial institutions need to become ready by investigating how to utilize quantum-safe protocols [20] and, potentially, quantum-enhanced cryptography [21], each of which has its own potential usages in the layers of a network. While the situation is by no means as serious for cryptographically-secure hash functions or symmetric-key ciphers, it is important to be aware of the potential quantum-enhanced attacks [22, 23, 24, 25]. Here, however, we are going to focus on quantum algorithms that have direct applications in finance, so protocols for quantum-enhanced cryptographic attacks, quantum-safe cryptography, and quantum-enhanced cryptography are all out of the scope of this survey.

2.2 Financial Use Cases for Quantum Computing

As discussed earlier, finance is one of the first industry sectors expected to benefit from quantum computing, largely because financial problems lend themselves to be solved on near-term quantum computers. Since many of the financial problems are based on stochastic variables as inputs, they are, more often than not, relatively more tolerant to imprecisions in the solutions compared with problems in chemistry and physics. Arguably, certain problems in chemistry and physics also can benefit from quantum computing. In this survey, however, we aim to review common financial problems that can benefit from quantum computing and to discuss the associated quantum algorithms applicable to solving them. We group these problems and quantum algorithms into three broad categories: stochastic modeling, optimization, and machine learning.

Stochastic modeling is concerned with the study of the dynamics and statistical characteristics of stochastic processes. In finance, one of the most commonly seen problems that involves stochastic modeling, using numerical techniques, is estimating the prices of financial assets and their associated risks, whose values may depend on certain stochastic processes. In Section 5, we will discuss two of the most used techniques for modeling stochastic processes in finance—Monte Carlo methods and numerical solutions of differential equations, and the corresponding quantum approaches for them, namely, quantum Monte Carlo integration (QMCI) and quantum partial differential equation (PDE) solvers. We will also demonstrate the applicability of the two quantum approaches to financial problems through examples of derivative pricing (Section 5.3.1) and risk modeling (Section 5.3.2). Stochastic modeling with quantum machine learning (QML) techniques will be discussed in Sections 7.9.2 and 7.9.3.

Optimization involves finding optimal inputs to a real-valued function so as to minimize or maximize the value of the function. In Section 6 we will review prevailing quantum techniques for combinatorial and convex optimization problems. We will cover adiabatic and variational quantum algorithms, as well as other quantum-classical hybrid approaches. A large variety of financial problems that involve optimization could potentially benefit from these quantum techniques, in particular, portfolio optimization (Section 6.4.1), hedging and swap netting (Section 6.4.2), optimal arbitrage (Section 6.4.3), credit scoring (Section 6.4.4), and financial crash prediction (Section 6.4.5).

Machine learning has become an essential aspect in modern business and research across various industries. It has revolutionized data processing and decision-making, empowering organizations large and small with unprecedented ability to leverage the ever-growing amount of easily accessible information. Using quantum machine learning techniques can potentially speed up the training of the algorithm or certain parts of the whole process. We will explore these techniques in Section 7. In finance, some of the most common use cases for machine learning are anomaly detection (Section 7.9.1), natural language modeling (Section 7.8), asset pricing (Section 7.9.2), and implied volatility calculation (Section 7.9.3). Applications of quantum machine learning in these use cases will be discussed in the respective sections.

In Table 1 we present a summary of the quantum techniques and their applicable financial use cases covered in this survey.

| Problem Category | Example Use Cases | Classical Solutions | Quantum Solutions |

|---|---|---|---|

| Stochastic Modeling |

Derivative Pricing (Section 5.3.1),

Risk Analysis (Section 5.3.2) |

Monte Carlo Integration,

Numerical PDE Solver, Machine Learning |

Quantum Monte Carlo Integration (Section 5.1),

Quantum PDE Solver (Section 5.2), Quantum Machine Learning (Section 7) |

| Optimization | Portfolio Optimization (Section 6.4.1), Hedging, Swap Netting (Section 6.4.2), Optimal Arbitrage (Section 6.4.3), Credit Scoring (Section 6.4.4), and Financial Crash Prediction (Section 6.4.5) |

Branch-and-Bound (with cutting -planes, heuristics, etc.) for non-convex cases [26]

and Interior-Point Methods for certain convex cases [27] |

Quantum Optimization (Section 6) |

| Machine Learning |

Anomaly Detection (Section 7.9.1),

Natural Language Modeling (Virtual Agents, Analyzing Financial Documents, Section 7.8), Risk Clustering (Section 7.3) |

Deep Learning,

Cluster Analysis |

Quantum Machine Learning (Section 7),

Quantum Cluster Analysis (Sections 7.3.1 and 7.3.2) |

3 Quantum Computing Concepts

Quantum computing is an emerging and promising field of science [28]. Global venture capital funds, public and private companies, and governments have invested millions of dollars in this technology. Quantum computing is driven by the need to solve computationally hard problems efficiently and accurately. For decades, the advancement of classical computing power has been remarkably following the well-known Moore’s law. Initially introduced by Gordon Moore in 1965, Moore’s law forecasts that the number of transistors in a classical computer chip will double every two years, resulting in lower prices for manufacturers and consumers. Today, transistors are already at the size at which quantum-mechanical effects become apparent and problematic [29]. These effects will only become more difficult to manage as classical chips decrease in size. This problem is partially circumvented by alternative forms of computing that do not use conventional transistors, such as photonic computing, neuromorphic computing, biocomputing, and special-purpose chips. However, these techniques still use classical algorithms and are subject to the scaling of them. Thus, it is imperative to investigate quantum computing, which provides scaling advantages no classical architectures can achieve.

Google has demonstrated an enormous computational speedup using quantum computing for the task of simulating the output of pseudo-random quantum circuits [30]. Specifically, Google claimed that what takes its quantum device, Sycamore, 200 seconds to accomplish would take Summit, one of the most powerful supercomputers, approximately 10,000 years. Thus, quantum supremacy has been achieved. As defined by John Preskill [31], quantum supremacy is the promise that certain computational (not necessarily useful) tasks can be executed exponentially faster on a quantum processor than on a classical one. The decisive demonstration of quantum devices to solve more useful problems faster and/or more accurately than classical computers, such as large-scale financial problems (Section 2.2), is called quantum advantage. Quantum advantage is more elusive and, arguably, has not been demonstrated yet. The main challenge is that existing quantum hardware does not yet seem capable of running algorithms on large enough problem instances. Current quantum hardware (Section 3.3) is in the noisy intermediate-scale quantum (NISQ) technology era [32], meaning that the current quantum devices are underpowered and suffer from multiple issues. The fault-tolerant era refers to a yet unknown period in the future in which large-scale quantum devices that are robust against errors will be present. In the next two subsections we briefly discuss quantum information (Section 3.1) and models for quantum computation (Section 3.2). In the last subsection (Section 3.3) we give an overview of the current state of quantum hardware and the challenges that must be overcome.

3.1 Fundamentals of Quantum Information

All computing systems rely on the fundamental ability to store and manipulate information. Today’s classical computers operate on individual bits, which store information as binary or states. In contrast, quantum computers use the physical laws of quantum mechanics to manipulate information. At this fundamental level, the unit of information is represented by a quantum bit, or qubit. Physically, a qubit is any two-level quantum system [33, 2]. Mathematically, the state space of a single qubit can be associated with the complex projective line, denoted [34].111Generally, quantum states live in a projective Hilbert space, which can be infinite-dimensional [33]. However, one commonly considers qubit states as elements , called state vectors, of a two-dimensional complex-vector space but restrict consideration to those that satisfy and allow for and to be used interchangeably (i.e., consider specific elements of the equivalence classes in ). A state vector is usually denoted by using Dirac’s “bra-ket” notation: is represented by the “ket” . Examples of two single-qubit kets are the states and , which are analogous to the classical bits and .

Multiqubit state spaces are expressed through the use of the vector space tensor product [35], which results in a -dimensional complex vector space for qubits. The tensor product of two state vectors is denoted as , , or and extends naturally to multiple qubits. Entanglement is a quantum phenomenon that can be present in multiqubit systems in which the states of the subsystems cannot be described independently. This results in correlated observations (measurement results) even when physical communication between qubits, which would correlate them in a classical sense, is impossible [2]. Entangled states are mathematically expressed as tensors that are not factorable over the involved subsystems, in other words, non-simple tensors. A quantum state is a product state of certain subsystems if those subsystems can be described independently and it is a simple tensor with respect to those subsystems. Qubits are in a superposition state with respect to a given basis for the state space if their state vector can be expressed as a nontrivial linear combination of basis states. Thus, a qubit can be in a state that is an arbitrary superposition of and , whereas a classical bit can be in only one of the analogous states or . The coefficients of the superposition are complex numbers called amplitudes. Although multiplying a state by a phase , called a global phase, has no physical significance, the relative phase between the amplitudes of two basis states in a superposition does.

A measurement in quantum mechanics consists of probing a system to obtain a numerical result. Measurement of a quantum system is probabilistic. A projective measurement of a system with respect to a Hermitian operator , called an observable, results in the state vector of the system being orthogonally projected onto an eigenspace, with orthogonal projector , and the observable quantity is the associated eigenvalue, . A potential projective measurement result is observed with probability equal to . The expected value of the measurement is equal to , where , called a “bra,” is the Hermitian adjoint. In physics, the quantum Hamiltonian is the observable for a system’s energy. A ground state of a quantum Hamiltonian is a state vector in an eigenspace associated with the smallest eigenvalue and thus has the lowest energy. Any physical transformation of a quantum system can be represented by a completely positive non-trace increasing linear operator. Two important special cases of such operations are unitary operators and measurements, which are not unitary. The dynamics of a closed quantum system follow the Schrödinger equation, , where is the reduced Planck constant and is the system’s quantum Hamiltonian. The unitary operator , which transforms a solution to the Schrödinger equation at one point in time into another one at a different point in time , is called the time-evolution operator or propagator. There can also be a time-dependent Hamiltonian, , where the operator changes over time. However, the propagator is computed by the product integral [36] to take into account that and may not commute for all in the specified evolution time interval [33]. The simulation of time evolution on a quantum computer is called Hamiltonian simulation. For quantum algorithms, the Hamiltonian can be an arbitrary observable with no connection to a physical system, and is often assumed. Three important observables on a single qubit are the Pauli operators: , , and , where , and , where denotes the vector outer product.222The Pauli operators are also sometimes denoted as , , and , respectively. For qubits, the set forms the computational basis. Measuring in the computational basis probabilistically projects the quantum state onto a computational basis state. A measurement in the context of quantum computation, without further clarification, usually refers to a measurement in the computational basis.

A positive semi-definite operator on the quantum state space with is called a density operator, where is the trace operator. The classical probabilistic mixture of pure states , in other words, state vectors, with probabilities has density operator and is called a mixed state. In general, a density operator represents a mixed state if and a pure state if . Fidelity is one of the distance metrics for quantum states and , defined as [2]. The fidelity of an operation refers to the computed fidelity between the quantum state that resulted after the operation was performed and the expected state. Decoherence is the loss of information about a quantum state to its environment, due to interactions with it. Decoherence constitutes an important source of error for near-term quantum computers.

3.2 Models of Quantum Computation

A qubit-based333There are other models of quantum computation that are not based on qubits, such as -level quantum systems, for , called qudits [38], and continuous-variable, infinite-dimensional systems [39]. This article discusses only quantum models and algorithms based on qubits. model of quantum computation is, simply, a methodology for performing computations on qubits. A model can realize universal quantum computation if it can be used to approximate any -qubit unitary, for all , with arbitrarily small error [2, 40]. Two universal models are polynomial-time equivalent if they can simulate each other with only a polynomially-bounded overhead in computational resources [41, 40]. We briefly discuss two polynomial-time-equivalent models that can be used to realize universal quantum computation: gate-based quantum computing and adiabatic quantum computing. There are others based on qubits [40] that we will not review since current quantum devices do not implement them, even in a non-universal fashion.

When running an algorithm on quantum hardware, one must contend with errors that can occur during computation. In the near term, quantum error mitigation techniques are commonly used to reduce (mitigate) errors, rather than eliminate them. However, error correction will be required in the long term. Techniques for quantum error correction [42] or fault tolerance have been developed to construct logical qubits and operations that tolerate errors. This strategy has been extensively studied for gate-based quantum computing [43].

3.2.1 Gate-Based Quantum Computing

Gate-based quantum computing, also known as the quantum circuit model, composes a countable sequence of unitary operators, called gates, into a circuit to manipulate qubits that start in a fixed state [2, 37]. A circuit can be viewed as a directed acyclic graph tracking the operations applied, which qubits they operate on, and the time step at which they are applied. Typically, the circuit ends with measuring in the computational basis. However, measurements of subsets of qubits before the end of the circuit and operations conditioned on the results of measurements are also possible [44]. Sequences of gates that act on separate sets of qubits can, if hardware supports it, be applied in parallel. The circuit depth is the longest sequence of gates in the circuit, from initial state until measurement, that cannot be made shorter through further parallelization. The quantum circuit model is analogous to the Boolean circuit model of classical computation [37]. An important difference with quantum computation is that because of unitarity all gates are invertible, i.e., computation involving only quantum gates is reversible. A shot is a single execution of a quantum circuit followed by measurements. Multiple shots are required if the goal is to obtain statistics.

This model can be utilized to realize universal quantum computation by considering circuits with qubits built by using any type of single-qubit gate and only one type of two-qubit gate [2]. Any -qubit unitary can be approximated in this manner to arbitrarily small error. The two-qubit gates can be used to mediate entanglement. A discrete set of gates that can be used for universal quantum computation is called a basis gate set. The basis gate set realized by a quantum device is called its native gate set. The native gate set typically consists of a finite number of (parameterized and non-parameterized) single-qubit gates and one two-qubit entangling operation. An arbitrary single-qubit gate can be approximately decomposed into the native single-qubit gates.

Some common single-qubit gates are the Hadamard gate (), the Phase () and -Phase () gates, the Pauli gates (, , ), and the rotation gates generated by Pauli operators (). Examples of two-qubit gates are the controlled-NOT gate denoted or and the gate. The , , and gates generate, under the operation of composition, the Clifford group, which is the normalizer of the group of Pauli gates [2]. The time complexity of an algorithm is measured in terms of the depth of the circuit implementing it. This is in terms of native gates when running the circuit on hardware. The majority of commercially available quantum computers implement the quantum circuit model.

We note that quantum circuits generated for gate-based quantum computers can also be simulated on classical hardware. It is generally a computationally inefficient process, however, with enormous memory requirements scaling exponentially with the number of qubits [45, 46, 47, 48]. But for certain types of computations such as computing the expectation values of observables, these requirements can be dramatically reduced by using tensor network simulators [49, 50, 51]. Classical simulation is commonly used for the development of algorithms, verification, and benchmarking, to name a few applications.

3.2.2 Adiabatic Quantum Computing

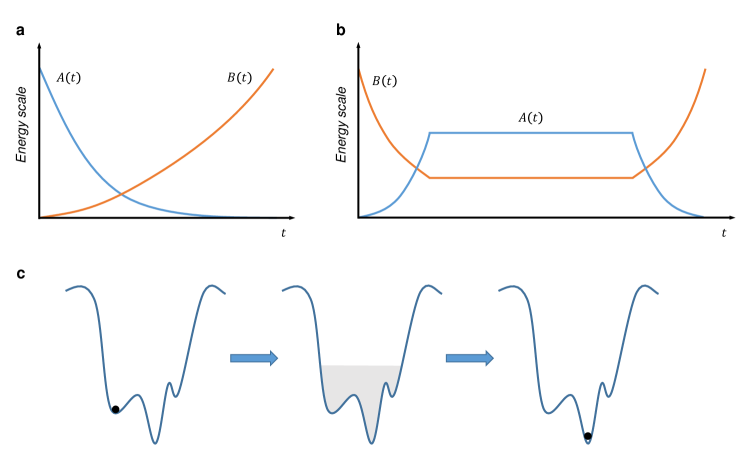

Adiabatic quantum computing (AQC) is a model for quantum computation that relies on the quantum adiabatic theorem. This theorem states that as long as the evolution of a time-dependent Hamiltonian, , is sufficiently slow (defined in references) from an initial th eigenstate of the time-dependent Hamiltonian at , it will remain in an instantaneous th eigenstate throughout the evolution for all [52]. A unitary operation can be applied by following an adiabatic trajectory from an initial Hamiltonian whose ground state is easy to prepare (e.g., a product state of qubits) to the final Hamiltonian whose ground state is the result that would be obtained after applying the unitary. A computation consists of evolving a time-dependent Hamiltonian for time according to a schedule , which interpolates between the two (non-commuting) Hamiltonians: [52]. The time required for an adiabatic algorithm to produce the result to some specified error is related to the minimum spectral gap among all instantaneous Hamiltonians. The spectral gap of the Hamiltonian at time is the difference between the th eigenvalue and the next closest one (e.g., difference between the ground-state energy and the first excited level). This quantity helps define how slow the evolution needs to be in order to remain on the adiabatic trajectory—although it is notoriously difficult to bound in practice [52]. One example of where this has been done is for the adiabatic version of Grover’s algorithm (Section 4.1) [53]. There exist classes of time-dependent Hamiltonians that through adiabatic evolution can approximate arbitrary unitary operators applied to qubits [52, 54]. Thus AQC can realize universal quantum computation. As of this writing, there does not exist a commercially available device for universal AQC. By polynomial equivalence to the circuit model, however, gate-based devices can efficiently simulate it. There are commercially available devices that implement a specific AQC algorithm for combinatorial optimization, called quantum annealing, discussed in Section 4.8. It is believed to be unlikely that the transverse-field Ising (stoquastic [52]) Hamiltonian used for quantum annealing is universal [54].

3.3 Quantum Hardware Challenges

As mentioned, the quantum computers available today are called NISQ devices. Multiple physical realizations of qubit-based quantum computation have been developed over the past decade. The majority of efforts to develop quantum technologies at this time are driven by industry and, to a lesser degree, by academia. Superconducting-based quantum computers [55] are manufactured by IBM, Google, D-Wave, and Rigetti, among others. Quantum computers using trapped atomic ions [56] have been developed, for example, by IonQ, Quantinuum, and AQT. These two technologies are currently the most widely available and thus, have been frequently utilized for research. However, other promising technologies also are under development, including photonic systems by PsiQuantum and Xanadu; neutral-atoms by ColdQuanta, QuEra Computing, Atom Computing and Pasqal, spins in silicon by Silicon Quantum Computing; quantum dots; molecular qubits; and topological quantum systems. As mentioned in Section 3.2, most of the current quantum devices and those that are in development, with the exception of the D-Wave quantum annealers, follow the quantum circuit model. All of the mentioned quantum devices have system-level attributes, which need to be considered in multiqubit systems. Significant scientific and engineering efforts are needed to improve and optimize these devices. The most important attributes are discussed in the remainder of this section.

The technical challenges of NISQ devices discussed below have a major impact on the current state of quantum algorithms. The algorithms can be roughly split into two camps: () near-term algorithms designed to run on NISQ devices and () algorithms that have a theoretically proven advantage for when hardware advances enough but require a large number of logical qubits with extremely high-fidelity quantum gates. In this work we cover both types of algorithms. One should keep in mind that arguably none of the discussed algorithms implemented on NISQ devices provide a decisive advantage over classical algorithms yet.

3.3.1 Noise

Qubits lose their desired quantum state or decohere (Section 3.1) over time. The decoherence times of each of the qubits are important attributes of a quantum device. Various mechanisms of qubit decoherence exist, such as quantum amplitude and phase relaxation processes and depolarizing quantum noise [2]. One potentially serious challenge for superconducting systems is cosmic rays [57]. While single-qubit decoherence is relatively well understood, the multiqubit decoherence processes, generally called crosstalk, pose more serious challenges [58]. Even two-qubit operations have an order of magnitude higher error rate than do single-qubit operations. This makes it difficult to entangle a large number of qubits without errors. Various error-mitigation techniques [59, 60] have been developed for the near term. In the long term, quantum error correction using logical operations, briefly mentioned in Section 3.2, will be necessary [61, 43]. However, this requires multiple orders of magnitude more physical qubits than available on today’s NISQ systems, and native operations must have sufficiently low error rates. Thus, algorithms executed on current hardware must contend with the presence of noise and are typically limited to low-depth circuits. In addition, current quantum error correction techniques theoretically combat local errors [61, 43, 58]. The robustness of these techniques to non-local errors is still being investigated [62].

3.3.2 Connectivity

Quantum circuits need to be optimally mapped to the topology of a quantum device in order to minimize errors and total run time. With current quantum hardware, qubits can interact only with neighboring subsets of other qubits. Existing superconducting and trapped-ion processors have a fixed topology that defines the allowed connectivity. However, trapped-ion devices can change the ordering of the ions in the trap to allow for, originally, non-neighboring qubits to interact [63]. Since this approach utilizes a different degree of freedom from that used to store the quantum information for computation, technically the device can be viewed as having an all-to-all connected topology. For existing superconducting processors, the positioning of the qubits cannot change. As a result, two-qubit quantum operations between remote qubits have to be mediated by a chain of additional two-qubit gates via the qubits connecting them. Moreover, the two-qubit gate error of current NISQ devices is high. Therefore, quantum circuit optimizers and quantum hardware must be developed with these limitations in mind. Connectivity is also a problem with current quantum annealers, which is discussed in Section 6.1.1.

3.3.3 Gate Speed

Having fast quantum gates is important for achieving quantum supremacy and quantum advantage with NISQ devices in the quantum circuit model. However, some types of quantum devices are particularly slow, for example trapped-ion quantum processors, compared with superconducting devices, although these devices typically have lower gate error rates. There is a well-known trade-off between space, speed, and fidelity. Execution time is particularly relevant for algorithms that require a large number of circuit execution repetitions, such as variational algorithms (Section 4.7) and sampling circuits. Error rates typically increase sharply if the gate time is reduced below a certain duration. Thus, one must find the right balance, which often requires tedious calibrations and fine-tuning.

3.3.4 Native Gates

Another important attribute, specific to gate-based quantum devices, is the set of available quantum gates that can be executed natively, namely, those that map to physical operations on the system (Section 3.2.1). The existence of a diverse universal set of native gates is crucial for designing short-depth high-fidelity quantum circuits. Developing advanced quantum compilers is, therefore, critical for efficiently mapping general quantum gates to the native gates of a particular device.

4 Foundational Quantum Algorithms

In this section we discuss foundational quantum algorithms that are the building blocks for more sophisticated algorithms. These algorithms have been extended to address problems in different domains, particularly finance, as described in Sections 5, 6, and 7. We briefly review the concepts from computational complexity theory that are relevant to the discussions in this survey. We refer the reader to the references for more rigorous discussions on the topic.

Computational complexity, the efficiency in time or space with which computational problems can be solved, is presented by using the standard asymptotic “Big-O” notation [64]: the set for an upper bound on complexity (worst case) and the set for a lower bound on complexity (best case). Also, if and only if and .444Let signify , , or . It is common practice to abuse notation and use the symbol instead of to signify is in [64]. Similarly, it is common to interchange the phrases “the complexity is ” and “the complexity is in .” Computational problems, which are represented as functions, are divided into complexity classes. The most common classes are defined based on decision problems, which can be represented as Boolean functions. denotes the complexity class of decision problems that can be solved in polynomial time (i.e., the time required is upper bounded, in “Big-O” terms, by a polynomial in the input size) by a deterministic Turing machine (TM), in other words, a traditional classical computer [37, 2]. An amount of time or space required for computation that is upper bounded by a polynomial is called asymptotically efficient, whereas, for example, an amount upper bounded by an exponential function is not. However, asymptotic efficiency does not necessarily imply efficiency in practice; the coefficients or order of the polynomial can be large. denotes the class of decision problems for which proofs of correctness exist, called witnesses, that can be executed in polynomial time on a deterministic TM [37].

A problem is hard for a complexity class if any problem in that class can be reduced in polynomial time to it, and it is complete if it is both hard and contained in the class [65]. Problems in can be solved efficiently on a classical or quantum device. While contains , it also contains many problems not known to be efficiently solvable on either a quantum or classical device. # is a set of counting problems. More specifically, it is the class of functions that count the number of witnesses that can be computed in polynomial time on a deterministic TM for problems [65]. , which contains , denotes the class of decision problems solvable in polynomial time on a quantum computer with bounded probability of error [2]. A common way to represent the complexity of quantum algorithms is by using query complexity [66]. Roughly speaking, the problem setup provides the algorithm access to functions that the algorithm considers as “black boxes.” These are represented as unitary operators called quantum oracles. The asymptotic complexity is computed based on the number of calls, or queries, to the oracles.

The goal of quantum algorithms research is to develop quantum algorithms that provide computational speedups, a reduction in computational complexity. In practice, however, one commonly finds algorithms with improved efficiency without any proven reduction in complexity. These algorithms typically utilize heuristics. As mentioned in Section 3.3, a majority of algorithms for NISQ fall into this category. When one can theoretically show a reduction in asymptotic complexity, the algorithm has a provable speedup for the problem. In the discussions that follow, we emphasize the category into which each algorithm currently falls.

4.1 Quantum Unstructured Search

Grover’s algorithm [67] is a quantum procedure for solving unstructured search with an asymptotic quadratic speedup, in terms of the number of oracle queries made, over the best known classical algorithm. The goal of unstructured search is as follows: Given an oracle , find such that . Sometimes is also called a marked element. More specifically, the algorithm amplifies the probability of measuring the state encoding such that . In Grover’s algorithm, a marked state is identified by utilizing a phase oracle, , which can be a composition of an oracle computing into a register and a conditional phase gate. One can represent by a unitary utilizing techniques for reversible computation [2]. Classically, in the worst case will be evaluated on all items in the set, queries. Grover’s algorithm makes . The complexity stated for this algorithm is said to be in terms of quantum query complexity. In fact, this algorithm is optimal for unstructured search [68].

Along with an efficient unitary simulating , the algorithm requires the ability to query uniform superpositions of states representing elements of . This criterion is typically referred to as quantum access to classical data [69]. The general case can be achieved by using quantum random access memory (qRAM) [70]. As of this writing, the problems associated with constructing a physical qRAM have not been solved. However, a uniform superposition over computational basis states (i.e., with Hadamard gates, Section 3.2.1) can be used for the simple case where . Moreover, hybrid techniques have been developed to deal with larger classical data sets without qRAM [71]. Ambainis [72] developed a variable-time version of the algorithm that more efficiently handles cases when queries can take different times to complete. We note that loading data onto a quantum computer is generally exponentially expensive. It is believed that a quantum computer may help with computing small but complex datasets, which are computationally easy to load onto a quantum computer.

4.2 Quantum Amplitude Amplification

The quantum amplitude amplification (QAA) algorithm [73] is a generalization of Grover’s algorithm (Section 4.1). Suppose an oracle exists that marks a quantum state (e.g., only acts nontrivially on , say, by adding a phase shift by ). Also, assume there is a unitary and for some input state . In addition, if has nonzero overlap with the marked state , namely, , then without loss of generality , where and . For example, in the case of Grover’s algorithm, is a uniform superposition over states corresponding to the elements of , and is the marked state. QAA will amplify the amplitude and as a consequence the probability of measuring (using an observable with as an eigenstate) to 555 probability means the probability that the event occurs is at least some constant. This is used to signify that the desired output of the algorithm occurs with a probability that is independent of the variables in the algorithm’s time complexity or query complexity. In addition, this implies an asymptotically efficient amount of repetitions (classical probabilistic boosting) can be used to increase the probability of success close to (e.g., see Section 4.3). using queries to and . This is done utilizing a series of interleaved reflection operators involving , , and [73].

This algorithm can be understood as a quantum analogue to classical probabilistic boosting techniques and achieves a quadratic speedup [73]. Classically, samples would be required, in expectation, to measure with probability. QAA is an indispensable technique for quantum computation because of the inherit randomness of quantum mechanics. Improvements to the algorithm have been made to handle issues that occur when one cannot perform the required reflection about [74], the number of queries to make (which requires knowing ) is not known [75, 76], and is imperfect with bounded error [77]. The last two improvements are also useful for Grover’s algorithm (Section 4.1). A version also exists for quantum algorithms (i.e., a unitary ) that can be decomposed into multiple steps with different stopping times [78].

4.3 Quantum Phase Estimation

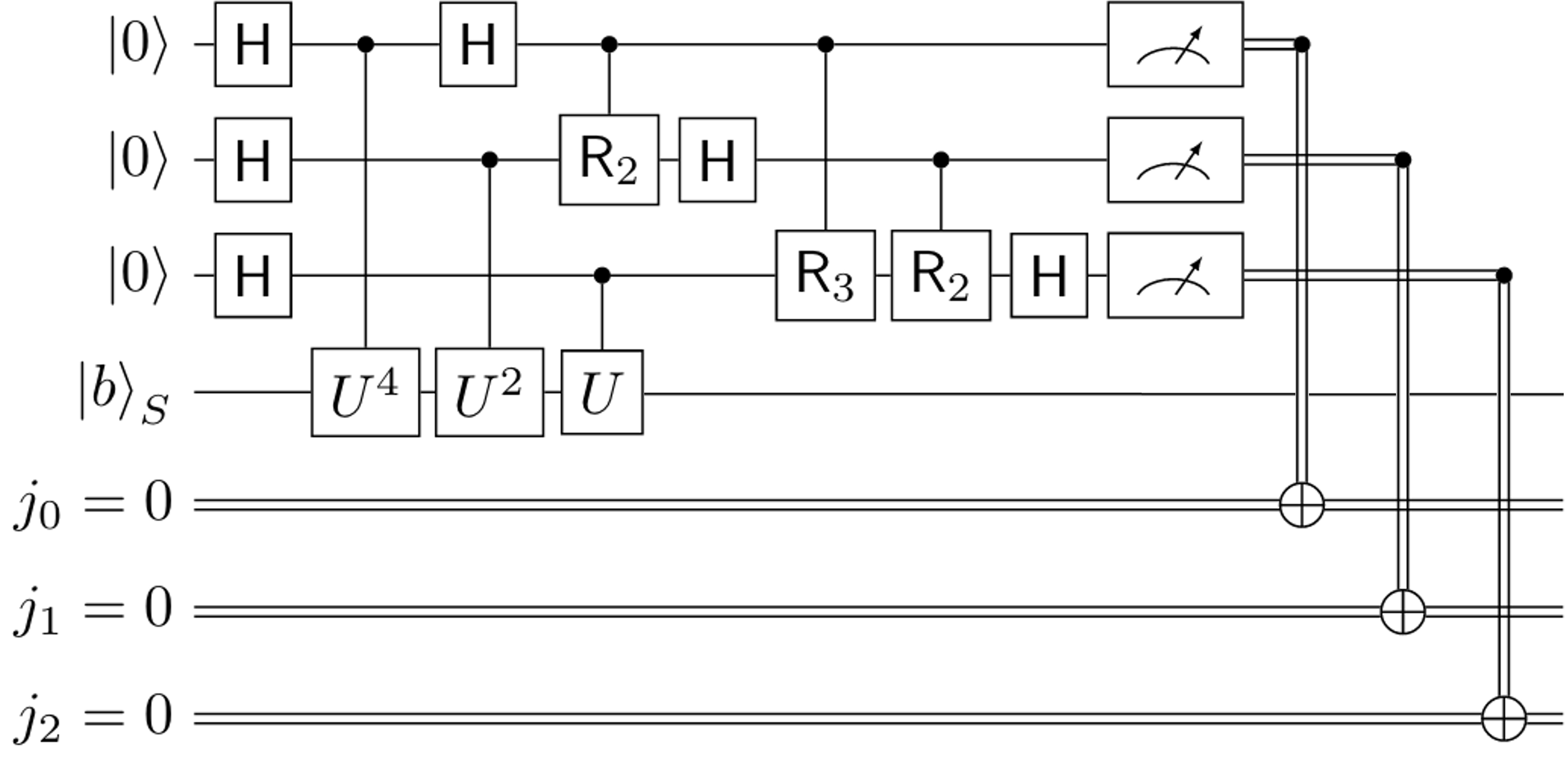

The quantum phase estimation (QPE) algorithm [79] serves as a critical subroutine in many quantum algorithms such as HHL (Section 4.5). Given a desired additive error of , QPE makes queries to a unitary to produce an estimate of the phase of one of the eigenvalues of , , such that . The probability of successfully measuring an estimate to the actual eigenvalue phase within error is and can be boosted to by adding and then discarding ancillary qubits [2, 80]. Alternatively, it can be boosted to by using repetitions of QPE and taking the most frequent estimate, according to standard Chernoff bounds [81]. This brings the overall query complexity to and , respectively. In the cases where the actual eigenvalue phase can be represented with finite precision, QPE can perform the transformation , when is an eigenvector of . A more detailed explanation of the algorithm and what happens when the eigenvalue phases cannot be perfectly represented with the specified precision, , is provided by Nielsen and Chuang [2].

4.4 Quantum Amplitude Estimation

The quantum amplitude estimation (QAE) algorithm [73] estimates the total probability of measuring states marked by a quantum oracle. Consider the state , oracle , unitary , and amplitude as defined in Section 4.2. QAE utilizes ) queries to and to estimate to relative additive error [81]. The algorithm utilizes QPE (Section 4.3) as a subroutine, which scales as , for desired additive error . Some variants of QAE do not make use of QPE [82, 83, 84], including a variational (Section 4.7) one [85], and are potentially more feasible on near-term devices. An important application of QAE to finance is to perform Monte Carlo integration, discussed in Section 5.1. Other applications of QAE include estimating the probability of success of a quantum algorithm and counting.

4.5 Quantum Linear System Algorithms

The quantum linear systems problem (QLSP) is defined as follows Given an –sparse invertible Hermitian matrix and a vector , output a quantum state that is the solution to up to a normalization constant with bounded error probability [86]. While this definition requires the sparsity to be independent of the dimensions of the matrix, the quantum linear system algorithms (QLSAs) have a polynomial dependence on sparsity. As can be understood by viewing the time complexities of these algorithms, we can allow for –sparse matrices, which is what is meant when we simply say “a sparse matrix” [87]. The -sparsity specification comes from the decision problem version of QLSP that is BQP-complete [86, 88].

The Harrow–Hassidim–Lloyd (HHL) algorithm [88] is the first algorithm invented for solving the QLSP. It provides an exponential speedup in the system size for well-conditioned matrices (for QLSP this implies a condition number in ) [89], over all known classical algorithms for a simulation of this problem. For matrix sparsity and condition number , HHL runs with worst-case time complexity , for desired error . This complexity was computed under the assumption that a procedure based on higher-order Suzuki–Trotter methods [90, 91] was used for sparse Hamiltonian simulation. However, a variety of more efficient techniques have been developed since the paper’s inception [92, 93]. These potentially reduce the original HHL’s quadratic dependence on sparsity. HHL’s query complexity, which is independent of the complexity of Hamiltonian simulation, is [94].

Alternative quantum linear systems solvers also exist that have better dependence on some of the parameters, such as almost linear in the condition number from Ambainis [78] and polylogarithmic dependence on for precision from Childs, Kothari, and Somma (CKS) [87]. In addition, Wossnig et al. [95] utilized the quantum singular value estimation (QSVE) algorithm of Kerenedis and Prakash [69] to implement a QLS solver for dense matrices. This algorithm has dependence on and hence offers no exponential speedup. However, it still obtains a quadratic speedup over HHL for dense matrices. Following this, Kerenedis and Prakash generalized the QSVE-based linear systems solver to handle both sparse and dense matrices and introduced a technique for spectral norm estimation [96]. In addition, the quantum singular value transform (QSVT) framework provides methods for QLS that have the improved dependencies on and mentioned above [97, 98]. The QSVT framework also provides algorithms for a variety of other linear algebraic routines such as implementing singular-value-threshold projectors [99, 69] and matrix-vector multiplication [97]. As an alternative to QLS based on the QSVT, Costa et al. [94] devised a discrete-time adiabatic approach [100] to the QLSP that has optimal [88] query complexity: linear in and logarithmic in . Since QLS algorithms invert Hermitian matrices, they can also be used to compute the Moore–Penrose pseudoinverse of an arbitrary matrix. This requires computing the Hermitian dilation of the matrix and filtering out singular values that are near zero [88, 99].

While solving the QLSP does not provide classical access to the solution vector, this can still be done by utilizing methods for vector-state tomography [101]. Applying tomography would no longer allow for an exponential speedup in the system size . However, polynomial speedups using tomography for some linear-algebra-based algorithms are still possible (Section 6.2). In addition, without classical access to the solution, certain statistics, such as the expectation of an observable with respect to the solution state, can still be obtained without losing the exponential speedup in . Providing quantum access to and is a difficult problem that can, in theory, be dealt with by using quantum models for data access. Two main models of data access for quantum linear algebra routines exist [97]: the sparse-data access model and the quantum-accessible data structure. The sparse-data access model provides efficient quantum access to the nonzero elements of a sparse matrix. The quantum-accessible data structure, suitable for fixed-sized, non-sparse inputs, is a classical data structure stored in a quantum memory (e.g., qRAM) and provides efficient quantum queries to its elements [97].

For problems that involve only low-rank matrices, classical Monte Carlo methods for numerical linear algebra (e.g., the FKV algorithm [102]) can be used. These techniques have been used to produce classical algorithms that have an asymptotic exponential speedup in dimension for various problems involving low-rank linear algebra (e.g., some machine learning problems) [103, 104]. As of this writing, these classical dequantized algorithms have impractical polynomial dependence on other parameters, making the quantum algorithms still useful. In addition, since these results do not apply to sparse linear systems, there is still the potential for provable speedups for problems involving sparse, high-rank matrices.

4.6 Quantum Walks

Formally, random walks are discrete-time stochastic processes formed through the summation of independent and identically distributed random variables [105] and play a fundamental role in finance [106]. In the limit, such discrete-time processes approach the continuous-time Wiener process [107]. One type of stochastic process whose logarithm follows a Wiener process is geometric Brownian motion (GBM), commonly used to model market uncertainty. Random walks have also been generalized to the vertices of graphs [108]. In this case they can be viewed as finite-state Markov chains over the set of vertices [109]. Quantum walks are a quantum mechanical analogue to the processes mentioned above [110]. Generally, quantum walks in discrete time can be viewed as a Markov chain over its edges (i.e., a quantum analogue of a classical bipartite walk) [111, 112] and consist of a series of interleaved reflection operators. This approach generalizes QAA (Section 4.2) and Grover’s algorithm (Section 4.1) [113, 114]. Discrete-time quantum walks have be shown to provide polynomially faster mixing times [115, 116, 117] as well as polynomially faster hitting times for Markov-chain-based search algorithms [111, 118, 112, 119, 120, 121, 122]. Alternatively, there are quantum walks in continuous time [123, 124], which have certain provable advantages [125], using a different notion of hitting time. A similar result, using this notion, has also been shown for discrete-time quantum walks [126]. In addition, the various mixing operators used in the Quantum Approximate Optimization Algorithm (QAOA, Section 6.1.2) can be viewed as continuous-time quantum walks connecting feasible solutions [127]. There have been multiple proposed unifications of quantum walks in continuous and discrete time [128, 129], something that is true for the classical versions [107]. For a comprehensive review of quantum walks, see the survey by Venegas–Andraca [129]; and for an overview and a discussion of connections between the various quantum-walk-based search algorithms, see the work of Apers et al. [119].

4.7 Variational Quantum Algorithms

Variational quantum algorithms (VQAs) [130], also known as classical-quantum hybrid algorithms, are a class of algorithms, typically for gate-based devices, that modify the parameters of a quantum (unitary) procedure based on classical information obtained from running the procedure on a quantum device. This information is typically in the form of a cost function dependent on the expectations of observables with respect to the state that the quantum procedure produces. Generally, the training of quantum variational algorithms is -hard [131] which withholds us from reaching arbitrarily good approximate local minima. In addition, these methods are heuristic. The primordial quantum-circuit-based variational algorithm is called the variational quantum eigensolver (VQE) [132] and is used to compute the minimum eigenvalue of an observable (e.g., the ground-state energy of a physically realizable Hamiltonian). However, it is also applicable to optimization problems (Section 6.1.3) and both linear (e.g., quantum linear systems [133, 134]) and nonlinear problems (Section 5.2.2). VQE utilizes one of the quantum variational principles based on the Rayleigh quotient of a Hermitian operator (Section 6.1.3). The quantum procedure that provides the state, called the ansatz, is typically a parameterized quantum circuit (PQC) built from Pauli rotations and two-qubit gates (Section 3.2.1). For VQAs in general, finding the optimal set of parameters is a non-convex optimization problem [135]. A variation of this algorithm, specific to combinatorial optimization problems, known as the quantum approximate optimization algorithm (QAOA) [136], utilizes the alternating operator ansatz [137] and is typically used for observables that are diagonal in the computational basis. There are also variational algorithms for approximating certain dynamics, such as real-time and imaginary-time quantum evolution that utilize variational principles for dynamics [138] (e.g., McLachlan’s principle [139]). Furthermore, variational algorithms utilizing PQCs and various cost functions have been applied to machine learning tasks (Section 7.6) [140]. Problems using VQAs are seen as one of the leading potential applications of near-term quantum computing.

4.8 Adiabatic Quantum Optimization

Adiabatic quantum optimization [141], commonly referred to as quantum annealing (QA), is an AQC (Section 3.2.2) algorithm for quadratic unconstrained binary optimization (QUBO). QUBO is an -hard combinatorial optimization problem. These problems are discussed in Section 6.1. The main reason behind the interest in QA is that it provides a nonclassical heuristic, called quantum tunneling, that is potentially helpful for escaping from local minima. Its closest classical analogue is simulated annealing [142], a Markov chain Monte Carlo method that was inspired by classical thermodynamics and uses temperature as a heuristic to escape from local minima.666Somma et al. [120] produced a quantum algorithm with provable speedup, in terms of the spectral gap, for simulated annealing using quantum walks (Section 4.6). So far QA has proven useful for solving QUBOs with tall yet narrow peaks in the cost function [143, 144]. The overall benefit of QA is still a topic of ongoing research [144, 145]. However, the current scale of quantum annealers allows for potential applicability in the near term [146].

5 Stochastic Modeling

Stochastic processes are commonly used to model phenomena in physical sciences, biology, epidemiology, and finance. In finance, stochastic modeling is often used to help make investment decisions, usually with a goal of maximizing return and minimizing risks. Quantities that are descriptive of the market condition, including stock prices, interest rates, and their volatilities, are often modeled by stochastic processes and represented by random variables. The evolution of such stochastic processes is governed by stochastic differential equations (SDEs), and stochastic modeling aims to solve the SDEs for the expectation value of a certain random variable of interest, such as the expected payoff of a financial derivative at a future time, which determines the price of the derivative.

Although analytical solutions for SDEs are available for a few simple cases, such as the well-known Black–Scholes equation for European options [106], a vast majority of financial models involve SDEs of more complex forms that have to resort to numerical approaches.

In the following subsections, we review two commonly used numerical methods for solving SDEs, namely, Monte Carlo integration (MCI, Section 5.1) and numerical solutions of differential equations (ODEs/PDEs, Section 5.2), and we discuss respective quantum solutions and potential advantages. Then, in Section 5.3, we show example financial applications for these quantum solutions.

5.1 Monte Carlo Integration

Monte Carlo methods utilize sampling to approximate the solutions to problems that are intractable to solve analytically or with numerical methods that scale poorly for high-dimensional problems. Classical Monte Carlo methods have been used for inference [147], integration [148], and optimization [149]. Monte Carlo integration (MCI), the focus of this subsection, is critical to finance for pricing and risk predictions [12]. These tasks often require large amounts of computational power and time to achieve the desired precision in the solution. Therefore, MCI is another key technique, heavily used in finance, for which a quantum approach is appealing. Interestingly, there exists a quantum algorithm with a proven advantage over classical Monte Carlo methods for numerical integration.

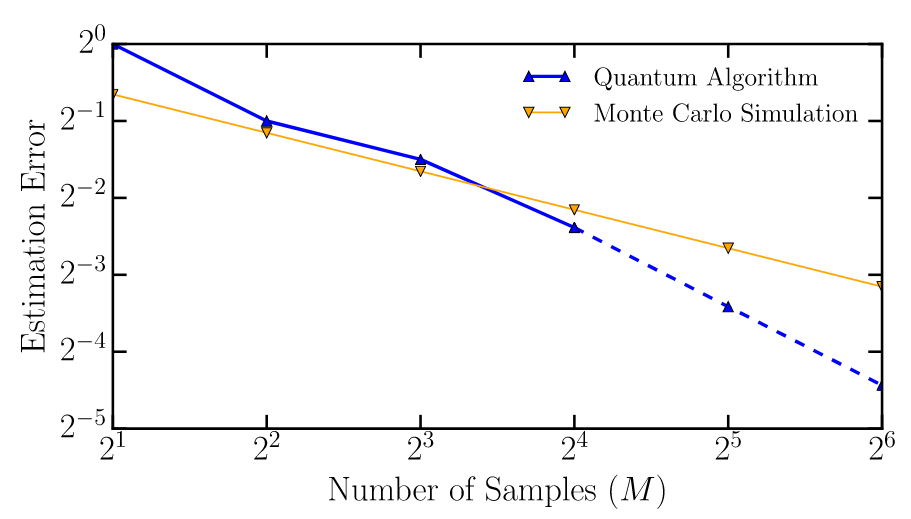

In stochastic modeling, MCI typically is used to estimate the expectation of a quantity that is a function of other random variables. The methodology usually starts with a stochastic model (e.g. SDEs) for the underlying random variables from which samples can be taken and the corresponding values of the target quantity subsequently evaluated given the samples drawn. For example, consider the following sequence of random variables, . These random variables are often assumed to follow a diffusion process [107], where each with represents the value of the quantity of interest at time , and the collective values of the random variables from the outcome of a single drawing are known as a sample path. Suppose the quantity whose expectation we want to compute is a function of this process at various time points: . In order to estimate the expectation, many sample paths are drawn, and sample averages of are computed. The estimation error decays as independent of the problem dimension, where is the number of paths taken. This is in accordance with the law of large numbers and Chebyshev’s inequality [148].

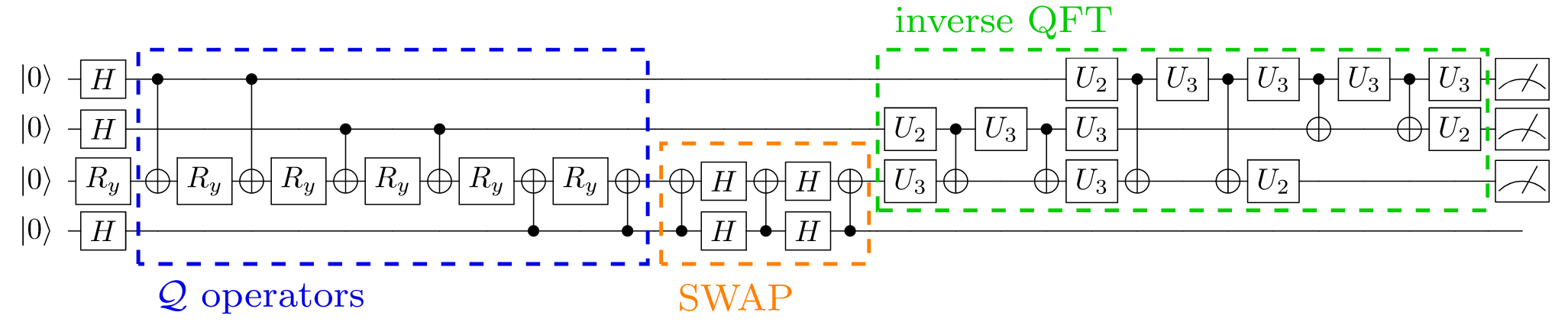

Quantum MCI (QMCI) [150, 151, 152] provides a quadratic speedup for Monte Carlo integration by making use of the QAE algorithm (Section 4.4).777To disambiguate, there are classical computational techniques called quantum Monte Carlo methods used in physics to classically simulate quantum systems [153]. These are not the topic of this discussion. With QAE, using the example from the previous paragraph, the error in the expectation computation decays as , where is the number of queries made to a quantum oracle that computes . This is in contrast to the complexity in terms of the number of samples mentioned earlier for MCI. Thus, if samples are considered as classical queries, QAE requires quadratically fewer queries than classical MCI requires in order to achieve the same desired error.

The general procedure for Monte Carlo integration utilizing QAE is outlined below [154]. Let be the set of potential sample paths of a stochastic process that is distributed according to , and is a real-valued function on , where is bounded. The task is to compute [152], which can be achieved with QAE in three steps as follows.

-

1.

Construct a unitary operator to load a discretized and truncated version of . The probability value translates to the amplitude of the quantum state representing the discrete sample path . In mathematical form, it is

(1) -

2.

Convert into a normalized function , and construct a unitary that computes and loads the value onto the amplitude of . 888In general, quantum arithmetic methods [155] can be used to load into a register and perform controlled rotations to load onto the amplitudes [154]. The resultant state after applying and is

(2) -

3.

Using the notation from Section 4.4, perform quantum amplitude estimation with and an oracle, , that marks states with the last qubit being . The result of QAE will be an approximation to . This value can be estimated to a desired error utilizing evaluations of and its inverse [152]. Then scale to the original bounded range, , of to obtain .

Variants [152] of QMCI also exist that can be applied when has bounded norm and bounded variance (both absolutely and relatively). The problem of estimating a multidimensional random variable is called multivariate Monte Carlo estimation. Quantum algorithms that obtain similar quadratic speedups in terms of error have been proposed by Cornelissen and Jerbi [156]. They solved this problem in the framework of Markov reward processes, and thus it has applicability to reinforcement learning (Section 7.7).

As mentioned earlier (Section 4.1), preparing an arbitrary quantum state is a difficult problem. In the case of QMCI, we need to prepare the state in (2). The Grover–Rudolph algorithm [157] is a promising technique for loading efficiently integrable distributions (e.g., log-concave distributions). It requires the ability to compute the probability mass over subregions of the sample space. However, it has been shown that when numerical methods such as classical MCI are used to integrate the distribution, QMCI does not provide a quadratic speedup when using this state preparation technique [158]. Additionally, variational methods (Section 4.7) have been developed to load distributions [159], such as normal distributions [154]. Geometric Brownian motion (GBM) is an example of a diffusion process whose solution is a series of log-normal random variables. These variables can be implemented by utilizing procedures for loading standard normal distributions, followed by quantum arithmetic [155, 154].

While GBM is common for modeling stock prices, it is often considered unrealistic [160] because it assumes a constant volatility. In addition, unlike realistic models, the SDE of GBM can be solved in closed form; that is, the distribution at every point in time is known, which avoids the need to use approximations involving the SDE to simulate the process. The local volatility (LV) model is one approach for accounting for a changing volatility by making it a function of the current price and time step. However, the corresponding SDE does not have a closed-form solution, and hence this means numerical methods such as Euler–Maruyama schemes [161] need to be used to simulate paths of the SDE with discretized time steps. Kaneko et al. [162] proposed quantum circuits implementing the required arithmetic for simulating the LV model, namely, the operation , based on improved techniques for simulating stochastic dynamics on a quantum device [163]. However, the discretized simulation of the SDE introduces additional error and complexities when computing expectations of functions of the stochastic process the SDE defines. Popular classical approaches to this problem are known as Multilevel Monte Carlo (MLMC) methods [164], which can be used to approximately recover the error scaling of classical single-level MCI. An et al. [165] proposed a quantum-enhanced version of MLMC that utilizes QMCI as subroutine to compute all expectations involved. This allowed them to approximately recover the error scaling of QMCI, and the approach benefits from being applicable to a wider variety of stochastic dynamics beyond GBM and LV. With regard to implementing payoff functions, Herbert [166] developed a near-term technique for functions that can be approximated well by truncated Fourier series. Furthermore, if fault tolerance (Section 3) is to be taken into account, advancements in the field of quantum error correction are required in order to realize quantum advantage [167].

Also worth noting are non-unitary methods for efficient state preparation [168, 44, 169]. These methods are usually incompatible with QAE, however, because of the non-invertibility of the operations involved. The methods would be more useful in a broader context where the inverse of the state preparation operation is not required; this topic is out of the scope of this survey.

5.2 Numerical Solutions of Differential Equations

While Monte Carlo methods are widely used for modeling stochastic processes, other numerical methods are also commonly used to calculate properties of stochastic systems. In fact, according to the Feynman–Kac formula [170, 171], the expectation of certain random variables, whose evolution is described by SDEs, can be formulated as the solution to parabolic partial differential equations (PDEs). This connection between SDEs and PDEs allows one to study stochastic processes using deterministic methods. Specifically, this enables an alternative to Monte Carlo methods for studying SDEs. A prime example of an alternative to MCI, applicable to certain problems, is the Black–Scholes PDE, which forms the keystone for pricing financial derivatives.

Classical numerical methods 999For details on numerical methods for PDEs, see, for example, [172]. for solving PDEs and ordinary differential equations (ODEs) usually require discretization of the domain on which solutions are sought. Specifically, the finite difference method (FDM) solves a PDE by approximating the solution and its derivatives on a predefined grid in both space and time and advancing it in time on the grid. Similarly, the finite volume method (FVM) employs a grid to divide the space into volumes, on which the function to be solved is integrated and the volume integrals are converted to surface integrals using the divergence theorem. These surface integrals are then connected by the original PDE. Another grid-based method, the finite element method (FEM), uses functions to form a basis of solutions on the subdomains divided by the grid. These basis functions are then assembled into an approximate for the solution in the entire domain.

In addition to grid based methods mentioned above, spectral methods may also be used to solve PDEs. Spectral methods [173] expand the solution into a linear combination of basis functions in the entire domain, whose spatial derivatives can be computed exactly. Although spectral methods do not require a grid when computing the spatial derivatives, numerical solution on a computer still requires evaluation of the functions on a grid. Moreover, spectral methods are often expensive to implement for PDEs with nonlinear terms. The reason is that spectral methods often require Fourier transforms, which have a computational cost of , with being the number of points on which the solution is evaluated. In contrast, grid-based spatial differentiation methods usually have a complexity of .

All these techniques can easily become computationally intractable for complex and high-dimensional problems, since they often require extremely large grid sizes to achieve desired accuracy and numerical stability in the solution. Specifically, these algorithms have complexities that scale at least linearly with the number of points on which the solution is to be evaluated and exponentially in the number of dimensions of the spatial variable.

On the other hand, quantum algorithms often address the same problem by representing a vector of size using space, and operating on it in potentially time.

5.2.1 Quantum-linear-system-based algorithms

Since classical algorithms for numerical solutions of PDEs such as the ones mentioned above often resort to the solution of linear systems, a natural candidate for quantum algorithms for PDEs is to employ the quantum linear system algorithms as mentioned in Section 4.5.

Because of the linear nature of QLS, QLSAs have been used to solve linear PDEs and ODEs [174, 175, 176, 177, 178]. These algorithms often consider differential equations with the following form:

where is a -dimensional vector, is a scalar function that accounts for the inhomogeneity in the PDE, is the scalar function that we are solving, and is a linear differential operator. The differential equations are transformed into a set of linear equations by using the same approaches as the classical algorithms mentioned above for computing numerical derivatives given a discretization. The resultant linear system can then be solved by QLSAs. This approach will potentially give the PDE solver algorithm a complexity of , where is the error tolerance, which is an exponential improvement in compared with that of the best-known classical algorithms.

In particular, FDM-based quantum algorithms [174, 175, 176, 179, 177] use quantum states and to encode the functions and (up to a normalization factor), with the computational basis states representing the discretized points in and amplitudes proportional to the scalar values of the functions at the respective points. A finite-difference scheme that defines how the derivatives are approximated using values from neighboring grid points is then used to convert into an matrix operator acting on , and hence the solution of the differential equations becomes a QLSP:

where is the solution we would like to obtain.

Similarly, quantum versions of FVM [180] and FEM [178] also use amplitude-encoded quantum states to represent the solution or the basis functions used to approximate the solution, and generate the matrix based on the relation of the grid points as defined by differential equations and the respective methods. The same applies to quantum algorithms based on spectral methods, in which the discretization is done in the spectral space [177].

To extend the QLSA-based algorithms to the solution of nonlinear differential equations, linearization of the equations is usually required. One approach is Carleman linearization [181, 182], which approximates the nonlinear functions in an ODE with truncated Taylor expansions of them, so that the nonlinear ODE can be approximated by a system of linear ODEs of the different powers of the solution. Specifically, Liu et al. [183] utilize Carleman linearization to convert dissipative quardratic ODEs into linear ODEs, which are then solved by QLSA. The overall complexity achieved by this algorithm is , where is the evolution time requested for the solution, measures the decay of the solution, and and are the same as defined earlier.

Another approach for implementing nonlinearity is to build multiple copies of the quantum state representing the solution, apply linear transformations in the expanded space to simulate the nonlinearities in the differential equations, and then trace out the additional copies to achieve the effective nonlinear transformation on a single copy of the quantum state [184, 185]. In particular, Lloyd et al. [185] combined the methods for simulating the dynamics of the nonlinear Schrödinger equation with QLSA-based quantum linear differential equation solvers to solve nonlinear ODEs with an -th order polynomial nonlinear term. It was shown that by using a sufficiently large number of copies, , of the quantum state that scales quadratically with the evolution time , the approximation error is suppressed by a factor of .