Well-Conditioned Linear Minimum Mean Square Error Estimation

Abstract

Linear minimum mean square error (LMMSE) estimation is often ill-conditioned, suggesting that unconstrained minimization of the mean square error is an inadequate approach to filter design. To address this, we first develop a unifying framework for studying constrained LMMSE estimation problems. Using this framework, we explore an important structural property of constrained LMMSE filters involving a certain prefilter. Optimality is invariant under invertible linear transformations of the prefilter. This parameterizes all optimal filters by equivalence classes of prefilters. We then clarify that merely constraining the rank of the filter does not suitably address the problem of ill-conditioning. Instead, we adopt a constraint that explicitly requires solutions to be well-conditioned in a certain specific sense. We introduce two well-conditioned filters and show that they converge to the unconstrained LMMSE filter as their truncation-power loss goes to zero, at the same rate as the low-rank Wiener filter. We also show extensions to the case of weighted trace and determinant of the error covariance as objective functions. Finally, our quantitative results with historical VIX data demonstrate that our two well-conditioned filters have stable performance while the standard LMMSE filter deteriorates with increasing condition number.

I Introduction

We investigate the problem of designing linear filters to minimize the mean square error under a constraint that the filter be well-conditioned. Without this constraint, the optimal filter depends on the condition number of the input covariance matrix, often large. This makes the filter numerically unreliable to compute. Incorporating a suitable constraint on the minimization ensures a well-conditioned solution, i.e., the computed filter is reliable. (We use estimator and filter interchangeably.)

We first show that, under an appropriate assumption on the constraint set, constrained optimal filters have a particular structure involving a certain prefilter, and optimality of a filter is invariant under invertible linear transformations of the prefilter. So, all constrained optimal filters are parameterized by equivalence classes of prefilters. We then consider a well-studied constraint on the rank of the filter. Based on the prefilter parameterization, a closed-form optimal solution is easy to derive, called the low-rank Wiener (LRW) filter [1]. However, it turns out that constraining the rank still does not ameliorate the problem of ill-conditioning. A related rank-constrained estimator, the cross-spectral Wiener (CSW) filter [2], suffers from the same ill conditioning.

To properly address the ill-conditioning issue, we explicitly constrain the solution to be well-conditioned. No closed-form optimal solution is currently known to exist. Instead, we introduce two approximately optimal solutions: JPC and LSJPC. We analyze their asymptotic performance and show that, just like the LRW filter, they converge to the unconstrained LMMSE solution as the truncation-power loss goes to zero. To illustrate our results, we also show empirical comparisons based on real data: historical daily VIX values.

The practical consequences of ill-conditioning are well-known, but solutions for it in filtering applications are limited. In [3] and [4], the authors study the numerical behavior related to ill-conditioning of Kalman filters and their extensions. In [5], the authors investigate the stability and sensitivity of the condition number of convolution neural network filters for image processing. Though these studies are related to ill-conditioning, they do not include the design of well-conditioned LMMSE filters of the kind we seek. Because LMMSE filtering is a component of Kalman filters, our filter designs are relevant to Kalman filtering.

Our contributions are summarized as follows:

1. We develop a unifying framework for studying constrained LMMSE estimation problems (Section II) and show that they all involve a prefiltering structure that is invariant under invertible linear transformations of the prefilter. This parameterizes all such filters by their equivalence classes of prefilters.

2. We clarify that the rank-constrained optimal solution, the LRW filter (Section II-D), is generally ill-conditioned (Section II-E). The same holds for the CSW filter.

3. We introduce two new filters (Section III), JPC and LSJPC, and show that as their truncation-power loss goes to zero, they converge to the unconstrained LMMSE filter at the same rate as the LRW filter (Section IV).

4. We show how to extend our formulation to the case of weighted trace and determinant of the error covariance as objective functions (Section V).

5. We use historical VIX data to demonstrate that the performance of JPC and LSJPC remains stable as we increase the size of the input covariance matrix, while the unconstrained LMMSE filter and LRW filter deteriorate significantly as expected (Section VI).

II LMMSE Estimation

II-A The unconstrained case

Let and be zero-mean random vectors taking values in and respectively. We wish to estimate from using a linear estimator (or filter) ( matrix) such that the estimate minimizes the mean square error , where represents either expectation or empirical mean (from data), and is the standard -norm. In other words, solves the following optimization problem, called the LMMSE estimation problem:

| (1) |

To express the optimal solution, define the covariance matrix of , (), covariance of , (), and crosscovariance of and , (), where the superscript prime represents Hermitian transpose. Assume that has full rank. The problem yields a simple closed-form unique solution , henceforth called the unconstrained LMMSE filter (or Wiener filter, though the same name appears in other filters too).

II-B The constrained case

Suppose that we now impose an explicit constraint on the estimator in terms of a constraint set . The constrained LMMSE problem is then

| (2) | ||||

Our primary motivation is the difficulty in numerically computing unconstrained LMMSE estimates. Specifically, it involves the inverse (i.e., solving linear equations), which often precludes practically computing the solution, for two reasons. If is very large, then the computational burden might be practically infeasible. But more important, the large condition number of —the ratio of its largest eigenvalue to its smallest eigenvalue—causes numerical problems. In this case, we say that the computation is ill-conditioned; otherwise, it is well-conditioned. Ill-conditioning exists regardless of computational execution time or finite-precision arithmetic. The problem lies instead in the amplification of errors inherent in solving linear equations.

According to [7], if the condition number is and the data have significant figures, then a small data perturbation can affect the solution in the th place. In practice, empirical covariance matrices often have significant errors in even the fourth significant figure. Moreover, condition numbers easily exceed (e.g., [6]; see also Section VI). In general, the mean condition number of a random matrix grows with [8], [9].

II-C Structure of optimal constrained estimators

We need some further definitions. Let and be full-rank. Suppose that a filter factorizes as for some . We call a prefilter of because the input first goes through , and then the prefiltered input goes through . Clearly, premultiplying by an invertible matrix also produces a prefilter of . The filter is said to be Wiener-structured if it has the form , i.e., the unique unconstrained LMMSE filter with the prefiltered input. Such filters are invariant to premultiplication of by any invertible matrix (this is easy to verify). Finally, the set is said to be Wiener-closed (with respect to ) if . Clearly, remains Wiener-closed if we premultiply by an invertible matrix.

For any full-rank (), the special case of (unconstrained as in (1)) is Wiener-closed. So are some other constraints of interest. We discuss a well-known example below in Section II-D and introduce another in Section II-E (with an additional requirement). Also, the optimal solution to (1) is always Wiener-structured, provided is a prefilter. In fact, given a Wiener-closed , a filter is optimal if and only if it is Wiener-structured, as shown below.

Proposition 1

Let be Wiener-closed with respect to (full-rank) and let have prefilter . Then is optimal for (2) if and only if it is Wiener-structured.

Proof:

Consider the prefiltered input . The covariance of is , which is positive definite because both and have full rank. The crosscovariance of and is . Because is Wiener-closed, it contains , which is the unique unconstrained optimal filter with input , i.e., has smaller mean square error than all other filters with prefilter . Hence, is optimal if and only if , which is Wiener-structured. ∎

Proposition 1, though elementary, exposes the intrinsic Wiener-structure (and hence invariance) of all optimal solutions with a Wiener-closed constraint set, thereby parameterizing them by equivalence classes of prefilters. The result also facilitates the design of candidate filters. To wit, once we select a prefilter , we can use the filter knowing that any optimal filter with a Wiener-closed constraint has this structure. This form of filters features prominently in the rest of the paper. Later, in Section III-A, we also exploit the invariance of Wiener-structured filters to invertible linear transformations of .

Assume that is Wiener-closed with respect to each feasible prefilter (i.e., each that is a prefilter for some ). Based on Proposition 1, (2) can be posed in an equivalent form involving only Wiener-structured filters:

| (3) | ||||

This equivalent form of the problem is useful because the decision-variable matrix here is smaller than in (2), and the constraint set here is smaller.

II-D Rank-constrained filters

An important special case of (2) is the following: Given a positive integer , let

| (4) |

(If , then .) Clearly, this is Wiener-closed for any full-rank . Moreover, we can derive a closed-form expression for an optimal solution, in terms of the singular-value decomposition (SVD), using the following notation. Let be the inverse square-root of . Write the SVD with singular values , listed in descending order by convention. Let , , and be the submatrices of , , and , respectively, consisting of the first columns. The following rank-constrained filter is optimal for (2) with in (4):

| (5) |

This solution is derived in [1], where it is called the low-rank Wiener (LRW) filter. Reduced-rank filters have been studied quite extensively; see, e.g., [2], [11], [12], and [13].

The LRW filter is Wiener-structured with prefilter , acting first on with , which whitens —the output has uncorrelated components with unit variance. The LRW filter then applies , which is equivalent to applying but keeping only the first components. Because is white, any of them have the same total power. However, the power lost in applying by keeping only singular values, an operation called truncation, is minimized by picking the first . This is the basic idea of principal component analysis.

A closely related cousin of the LRW filter is the cross-spectral Wiener (CSW) filter [2]. To define it, let be the th column of . The quantity is called the th cross-spectral power of and [2]. Next, suppose that we order the columns of not by the eigenvalues as before but by the cross-spectral powers instead. If we now redefine to be the first columns of according to this new ordering, then the expression in (5) gives the CSW filter. Because CSW is rank-constrained, and LRW is the unique optimal rank-constrained filter, generally CSW has worse mean square error in theory than LRW. More important, as shown next, neither LRW nor CSW is well-conditioned.

II-E Well-conditioned filters

The LRW and CSW filters involve , the inverse of an matrix , which is (potentially) large and ill-conditioned. Indeed, the condition number of is , the square root of the condition number of . Therefore, we should expect that computing LRW or CSW is numerically problematic. So it turns out that simply constraining the rank is insufficient to guarantee a well-conditioned solution (though to do so was not the original goal of the LRW and CSW filters).

To circumvent this issue, we define a new constraint as follows. We say that a matrix is -well-conditioned (-WC) if it can be computed (from and ) without any inverse larger than . Define to be the set of all -WC filters, which is Wiener-closed for any -WC full-rank . Indeed, given any such , because the inverse in the expression is only . We call the problem with this new the well-conditioned LMMSE problem.

The LRW and CSW filters are no longer feasible here because they involve . Moreover, a closed-form expression for the optimal -WC solution is currently unknown to even exist. The best we can do here is to design approximately optimal solutions and analyze their performance. Two such filters follow next.

III Well-Conditioned Filter Designs

III-A JPC filter

Let be the vector with stacked above . Let be its covariance, which can be partitioned naturally as

| (6) |

Define the eigendecomposition with eigenvalues ordered from largest to smallest as usual. The matrices and (both ) depend jointly on , , and . Next, partition into (top rows) and (bottom rows). Given , write

| (7) |

where is , is , is , and is .

Next, define the resolution matrix , which produces the coordinates of the orthogonal projection onto the range of . Computing involves the inverse of only , which is and so is well-conditioned by definition. We use as the prefilter to define the following filter:

| (8) |

which we call the joint-principal-component (JPC) filter. JPC is well-conditioned—the matrix inverses are .

The invertible matrix premultiplying in can be eliminated, simplifying (8) to

| (9) |

So, though we started with to explain the approach, we do not need it to implement the filter. We can just substitute the simpler for as the prefilter even though the former is not an orthogonal-resolution matrix.

The JPC filter is well-conditioned, involving only an inverse. Moreover, it is Wiener-structured with prefilter . A similar filter was considered recently in [6] but not formally derived there and was evaluated only empirically, suggesting promising performance for JPC, even when fails badly because of ill-conditioning. Our results in Sections IV and VI corroborate this suggestion.

III-B Least-squares JPC (LSJPC) filter

We can simplify the JPC filter by the following observation. First define the Karhunen-Loève transform of by , so that . This means that and . Next, let be the top -subvector of , so that and . We now estimate from . However, we cannot use the LMMSE filter for this task because it involves . Instead, we use a least-squares estimate based on , giving the formula . Again, we recognize this to be the resolution of onto the range of . Using this estimate, we get the simple filter

| (10) |

called the least-squares JPC (LSJPC) filter. It is well-conditioned and is simpler than —it involves fewer multiplications. LSJPC is not Wiener-structured. Interestingly, LSJPC involves inverting only , suggesting better conditioning of relative to .

IV Asymptotic Optimality

Define the truncation-power loss as the power lost by truncation (made precise below), which is small by design. We now show that LRW, JPC, and LSJPC all converge to the unconstrained LMMSE filter as , with the same scaling law. Hence, these filters are “asymptotically just as good as” , even though JPC and LSJPC are well-conditioned while LRW is not.

Our analysis uses the Bachmann-Landau notation : Given a matrix depending on a parameter , means that for some and all sufficiently small , , where is some submultiplicative matrix norm [10] (e.g., nuclear norm). In this case, we say that with a scaling law of . Several algebraic rules help to simplify the calculations: If and are bounded (as ), then , , and . In our analysis, it suffices to treat only the singular values (or eigenvalues) from onward as vanishing.

IV-A LRW filter

For LRW, . Using and the Bachmann-Landau rules, , i.e., with scaling law . Here and below, a simple calculation shows that the mean square error also converges as .

IV-B JPC filter

For JPC and LSJPC, . Recall that unlike , the columns of are not orthonormal, i.e., ( identity) in general. So, we make the additional assumption that

| (11) |

This assumption is reasonable and natural. It holds whenever scales sublinearly with such that , which implies (11).

Using (11) and the Bachmann-Landau rules, we have

| (12) | ||||

| (13) |

Using these and the Bachmann-Landau rules again,

| (14) |

So, with scaling law , just like .

IV-C LSJPC filter

Again using (11) and the Bachmann-Landau rules,

| (15) |

and so

| (16) |

So, with scaling law , just like and .

The analysis above suggests further simplifications to JPC and LSJPC. For example, approximating by , . Also, approximating by , (no matrix inverse); it could not get any simpler.

V Weighted Trace and Determinant

Our objective function so far, the mean square error, can also be expressed as the trace of the error-covariance matrix as . An immediate generalization of this objective function is the weighted trace, , where is invertible, leading to a problem like (2) but with objective function [11]. Clearly, the regular mean square error is a special case of with . In fact, as shown below, the weighted-trace case is equivalent—its solution can be obtained from the regular case.

Rewriting , the new objective is simply the previous objective with covariance of , , and crosscovariance of and , , except that the decision variable is premultiplied by . Therefore, the optimal solution can be obtained as a special case of the regular (unweighted) constrained LMMSE problem. Indeed, the rank-constrained optimal filter for the weighted-trace case is easy to write down based on (5). Similarly, we can apply JPC and LSJPC to the weighted-trace case with the same asymptotic analyses.

Another objective function of interest is the determinant of the error covariance: . The associated rank-constrained optimal filter is also studied in [11], where it is shown that minimizing is equivalent to minimizing with . So the minimizer of can be obtained as a special case of the minimizer of , and hence also of the unweighted mean square error. Accordingly, JPC and LSJPC can also be applied to the determinant case as a special case of the weighted-trace modification described above.

VI Quantitative Performance with Real Data

VI-A Overview of VIX data

To illustrate the performance of JPC and LSJPC relative to LMMSE, we provide empirical results using real data. We also show that LRW suffers from the same ill-conditioning as LMMSE. We do not consider CSW here as its ill-conditioned behavior is already reflected in LMMSE and LRW.

Our empirical data consists of historical Cboe Volatility Index (VIX) daily closing values [14]. VIX is a quantitative indicator of the equity market’s expectation for the strength of future changes of the S&P 500 index (in the United States). The historical VIX data is freely available and suits our purposes because of its abundance. We obtained our data from [15]. The VIX sequence has been shown to be empirically wide-sense stationary [14].

For our estimation problem, we take to be the finite sequence of VIX daily closing values over consecutive days and to be the sequence of VIX values over the immediate prior consecutive days. So, our estimation problem is to predict consecutive VIX values from the most recent prior values, with time measured in days. To estimate covariances, we use samples consisting of vectors of VIX values for consecutive days (corresponding to samples of ). These vector-valued samples start at every available day from the earliest date until the date before the days ending with the most recent date available. Owing to stationarity, we treat these samples to be drawn from a common -variate distribution and with constant mean. The samples are correlated because of the relatively long-range correlation of VIX data.

VI-B Data processing

Our VIX dataset corresponds to consecutive trading days, starting on 2-January-1990 and ending on 17-June-2021. In our experiments, we vary from to , and we fix . Therefore, the number of data samples is . We reserve 20% of the samples for test and evaluation, while the other 80% are for computing the covariance matrix of (training); i.e., we conduct out-of-sample test experiments. The test-and-evaluation data vectors are sampled uniformly from the available data samples.

For example, for , there are vector samples; samples are for covariance estimation and are for the prediction experiments. Despite the correlation of the samples, these large numbers allow for relatively accurate estimation of the covariance and quantitative performance. We subtracted the empirical average value (approximately ) from the VIX values before computing predictions.

Because of the abundance of data, it suffices to compute the empirical covariance matrix of using the standard estimation formula. To elaborate, let be the data-vector samples (with average subtracted). Then, is computed using . We extract and from as submatrices (see (6)).

VI-C Performance

For the remainder of the evaluation, we need to define the normalized root-mean-square (RMS) error as a performance metric. The RMS error, a standard performance metric for prediction, is simply the square root of the mean square error. Empirically, we first compute the squared Euclidean norm of the difference between the true and predicted vectors (of length ). Then we average the squared norm of the errors over all the data samples reserved for test and evaluation (described earlier). None of these samples were used in empirically computing . We then take the square root of this average to get the RMS error value. The normalized RMS error is then calculated by dividing the RMS error value by the RMS value of the -vectors being estimated (including the nonzero mean). This RMS value is empirically computed by taking the squared norm of each sample of plus its empirical mean, averaging these values, and then taking the square root of the average. Using the earlier notation, the normalized RMS error of a filter (LMMSE, LRW, JPC, or LSJPC) is

where is the -subvector of corresponding to , is the -subvector corresponding to , and is the average -vector. (Of course, we can dispense with the factor .) As intended, the normalization provides performance-metric values that are directly comparable as we vary the parameters in our experiment. Good performance values are significantly smaller than .

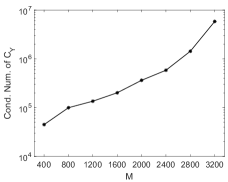

Figure 1a shows the condition number of as increases. As we can see, the condition number increases by over two orders of magnitude as varies from to . As shown later, above about , computing the inverse of is unreliable, which corresponds to a condition number of roughly .

a. b.

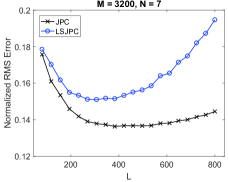

Figure 1b shows the normalized RMS error as a function of for . As we increase , the truncation-power loss for each filter decreases, and the filter becomes more like . At the same time, the ill-conditioning increases, and the filter increasingly exhibits numerical unreliability. Thus, there is an optimal intermediate value of (see Figure 1b).

Practically, a suitable value of can be found using a simple line-search procedure [10] together with the formula for the mean square error of any filter . Fortunately, with respect to the normalized RMS error, the performance is relatively insensitive close to the minimizer. For JPC in Figure 1b, we can vary by even without significantly changing the normalized RMS error. This approximately corresponds to a 50% variation in , which is a very wide margin. LSJPC is slightly more sensitive—we can vary by about without significantly affecting the performance, still a very wide margin. This means that the performance is relatively robust to our choice of (within certain generous bounds), a desirable feature of JPC and LSJPC. The insensitivity increases as decreases. Unsurprisingly, JPC slightly outperforms LSJPC (by less than 10% at their optimal points), likely because of the additional approximations involved in LSJPC. But recall that LSJPC involves fewer computations than JPC, so this tradeoff is favorable in many cases.

a. b.

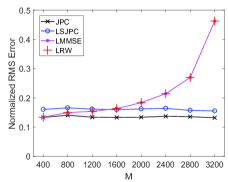

Figure 2a shows the normalized RMS error as a function of for JPC, LSJPC, LMMSE, and LRW (indistinguishable from LMMSE). For JPC and LSJPC, we used approximate best values. Because is small in this case and , ; i.e., the truncation to in has no effect on its performance, which should be close to that of LMMSE except for the impact of computing twice (in LRW) instead of (in LMMSE). We include LMMSE and LRW here to illustrate their performance deterioration as increases: While JPC and LSJPC have stable performance as increase, the performance of LMMSE and LRW deteriorates significantly. Moreover, LRW and LMMSE are indistinguishable in performance, reflecting the common cause of the deterioration: the unreliability of computing and , respectively.

For small , the performance of JPC and LSJPC are comparable to LMMSE and LRW. However, while the performance of JPC and LSJPC continues to decrease with (albeit only slightly), the same is untrue for LMMSE and LRW. Above about , LMMSE and LRW are worse than both JPC and LSJPC, indicating the unreliability of computing the inverses and . This behavior can be expected of CSW too, which unlike LRW is suboptimal. At , the normalized RMS errors of LMMSE and LRW are approximately three times those of JPC and LSJPC, and are increasing steeply. This illustrates the effectiveness of JPC and LSJPC in addressing the ill-conditioning in LMMSE estimation for large .

Note that we could have simply started with a small and applied LMMSE or LRW, but we would not have known this beforehand. A distinct advantage of JPC and LSJPC is that they have stable performance without knowing how large we can set for LMMSE or LRW to perform well without ill-conditioning.

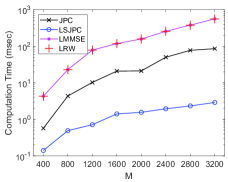

Finally, Figure 2b shows the computation times for the four filters. Unsurprisingly, JPC and LSJPC take less time than LMMSE and LRW. We can see the tradeoff mentioned earlier between JPC and LSJPC when considering the performance and computation times.

VII Conclusion

We have shown that all optimal filters with a Wiener-closed constraint set have an inherent structure: They are parameterized by their equivalence classes of prefilters. The LRW filter, while constrained in its rank, is not well-conditioned, nor is CSW. We introduced two well-conditioned filters, JPC and LSJPC, and showed that both are asymptotically equivalent to the unconstrained LMMSE filter as the truncation-power loss goes to zero. Our results also apply to minimizing weighted trace and determinant of the error covariance. We tested JPC and LSJPC on real data, with promising results.

References

- [1] L. L. Scharf, Statistical Signal Processing: Detection, Estimation, and Time Series Analysis. Reading, MA: Addison-Wesley, 1991.

- [2] J. S. Goldstein and I. S. Reed, “Reduced-rank adaptive filtering,” IEEE Trans. Sig. Proc., vol. 45, no. 2, pp. 492–496, Feb. 1997.

- [3] S. J. Shellhammer and R. A. Iltis, “Numerically well conditioned implementations of the PDA and PMA filters,” in IEEE Int. Symp. Circ. & Sys., Portland, OR, May 8–11, 1989.

- [4] G. Yu Kulikov and M. V. Kulikova, “Numerical robustness of extended Kalman filtering based state estimation in ill-conditioned continuous-discrete nonlinear stochastic chemical systems,” Int. J. Robust & Nonlin. Contr., vol. 29, no. 5, pp. 1377-1395, 2019.

- [5] J. Ghafuri, H. Du, and S. Jassim, “Sensitivity and stability of pretrained CNN filters,” in Proc. SPIE 11734, Mult. Image Expl. & Learning 2021, 117340B, April 12, 2021.

- [6] M. Ghorbani and E. K. P. Chong, “Stock price prediction using principal components,” PLOS One, vol. 15, no. 3, e0230124, Mar. 20, 2020.

- [7] D. A. Belsley, E. Kuh, and R. E. Welsch, Regression Diagnostics: Identifying Influential Data and Sources of Collinearity. Hoboken, NJ: John Wiley & Sons, 1980.

- [8] S. Smale, “On the efficiency of algorithms of analysis,” Bull. Amer. Soc., vol. 13, pp. 87–121, 1985.

- [9] A. Edelman, “Eigenvalues and condition numbers of random matrices,” SIAM J. Matrix Analysis, vol. 9, no. 4, Oct. 1988.

- [10] E. K. P. Chong and S. H. Żak, An Introduction to Optimization, Fourth Edition. New York, NY: John Wiley and Sons, 2013,

- [11] Y. Hua, M. Nikpour, and P. Stoica, “Optimal reduced-rank estimation and filtering,” IEEE Trans. Sig. Proc., vol. 49, no. 3, pp. 457–469, 2001.

- [12] G. K. Dietl, “Reduced-rank matrix Wiener filters in Krylov subspaces,” in Linear Estimation and Detection in Krylov Subspaces, Ch. 4, part of Foundations in Signal Processing, Communications and Networking series, vol. 1., Berlin, Heidelberg: Springer, 2007.

- [13] L. L. Scharf, E. K. P. Chong, M. D. Zoltowski, J. S. Goldstein, and I. S. Reed, “Subspace expansion and the equivalence of conjugate direction and multistage Wiener filters,” IEEE Trans. Sig. Proc., vol. 56, no. 10, pp. 5013–5019, Oct. 2008.

- [14] A. Saha, B. G. Malkiel, and A. Rinaudo, “Has the VIX index been manipulated?” J. Asset Manag. vol. 20, pp. 1–14, 2019.

- [15] VIX Historical Price Data, Cboe Global Markets, Inc., data available freely for download at https://www.cboe.com/tradable_products/vix/vix_historical_data/, downloaded on 17-June-2021.