Modelling Cournot Games as Multi-agent Multi-armed Bandits

Abstract

We investigate the use of a multi-agent multi-armed bandit (MA-MAB) setting for modeling repeated Cournot oligopoly games, where the firms acting as agents choose from the set of arms representing production quantity (a discrete value). Agents interact with separate and independent bandit problems. In this formulation, each agent makes sequential choices among arms to maximize its own reward. Agents do not have any information about the environment; they can only see their own rewards after taking an action. However, the market demand is a stationary function of total industry output, and random entry or exit from the market is not allowed. Given these assumptions, we found that an -greedy approach offers a more viable learning mechanism than other traditional MAB approaches, as it does not require any additional knowledge of the system to operate. We also propose two novel approaches that take advantage of the ordered action space: -greedy+HL and -greedy+EL. These new approaches help firms to focus on more profitable actions by eliminating less profitable choices and hence are designed to optimize the exploration. We use computer simulations to study the emergence of various equilibria in the outcomes and do the empirical analysis of joint cumulative regrets.

Keywords Multi-armed Bandits Multi-agent Learning Cournot Games

1 Introduction

The Cournot oligopoly model Cournot (1838) is a well-known model in economic game theory. In this model, firms compete over production quantities, and the total quantity produced by the firms affects the market price. Cournot games are used to model many real-world problems such as energy systems Kirschen and Strbac (2018), transportation networks Bimpikis et al. (2019) and healthcare systems Chletsos and Saiti (2019). There are three main types of equilibria associated with this model: Walrasian equilibrium, Cournot/Nash equilibrium, and collusive equilibrium. Cournot games have been modeled in several ways in the literature with various assumptions on the firms’ cognitive capabilities and rationalities. Different learning mechanisms have been analyzed in order to understand the conditions required to arrive at a specific equilibrium.

Many learning mechanisms from the literature assume that the firms have some knowledge of the market and their competitors. In this paper, we model repeated Cournot games using MA-MAB setting, where firms learn independently and are autonomous. This setting provides a practical framework to model the Cournot game when there are assumptions of low cognitivity for the firms involved. Here, information on competitors is not available to the firms, and they cannot deduce the demand function. Moreover, firms do not even need to know their own cost function necessarily. However, we assume that the random entry and exit of the firms are not allowed. MAB framework facilitates the use of exploration-exploitation approaches. This MA-MAB setting is different from other MA-MAB settings studied in the literature.

Balancing the exploration-exploitation trade-off is an important part of learning in MAB settings. In our MA-MAB setting, as multiple agents learn simultaneously, where learning involves exploration, high uncertainty in the rewards can be seen from the perspective of a single agent having no knowledge of the environment. This uncertainty can vary based on agents’ exploration-exploitation strategies. However, it is guaranteed that the rewards are generated using the same mechanism every time, due to the assumption of static demand and the prevention of random entry or exit of firms from the market. We also assume that agents learn simultaneously using the same learning mechanism, and as they learn, their strategies converge. Because of this, we consider these bandits to be stochastic rather than non-stationary or non-stochastic.

In Lattimore and Szepesvári (2020), authors suggest that in real-world scenarios, it is unlikely to have truly stochastic bandit models; therefore only their usefulness matters. They encourage examining algorithms’ tolerance for deviations from the assumptions that the means of arms stay the same. We investigate three well-known algorithms: -greedy, UCB, and Thompson sampling. Literature mainly focuses on Bernoulli bandits, while we are dealing with normal bandits with unknown parameters. UCB-Normal Cowan et al. (2017) which is designed for such problems, fails to converge in our settings. Similarly, Thompson sampling proposed in Honda and Takemura (2014) depends on correctly setting priors to succeed. For both UCB and Thompson sampling, we found that the parameters controlling exploration need to be set cautiously to get any convergence in our setting; however, information about market is needed to set such parameters. Therefore, we think -greedy remains the most viable option.

In this work, we propose two novel approaches built on top of the -greedy algorithm that take advantage of the ordered action space to optimize exploration by reducing the action space. The first approach is similar to hierarchical learning; we call it -greedy+HL. It is based on partitioning the action space into few buckets and choosing the best bucket. The second method resorts to action/arm elimination to reduce the action space, and hence called as -greedy+EL; EL stands for elimination. In real-world scenarios, the exploration can be costly, and we think that the operating mechanism of our proposed approaches can significantly reduce the exploration cost. Therefore, these newly proposed approaches are more adaptable for real-world usage and applicable to other similar problems with ordered action spaces such as dynamic pricing.

We evaluate these approaches empirically by running different kinds of simulations. We study these approaches in terms of resulting equilibrium, scalability, and sensitivity to hyper-parameters. We investigate Cournot models with symmetric firms (same marginal cost) and extend our study to asymmetric firms (different marginal cost). We consider both deterministic and stochastic inverse demand functions. The stochastic demand function represents small fluctuations in the market demand as it is common in real-world scenarios. In experiments, we start with simulations same as that used in Waltman and Kaymak (2008); Xu (2020); these are the small-scale simulations as they contain total firms between . We further scale the models in terms of the number of firms and the size of the action space. In these evaluations, we compare joint quantity, joint profit, and joint cumulative regret obtained by -greedy and our proposed methods. In small-scale settings, with a limited number of firms and action choices, collusion in various degrees can be seen. In general, outcomes obtained by our proposed methods are more collusive than baseline -greedy, although full collusion usually does not emerge. Although the real-world scenarios are more complex than our simulations, the results still indicate the possibility of the emergence of collusive behavior, even without explicit instructions to collude. Joint cumulative regret obtained by -greedy+HL is the lowest, followed by that obtained by -greedy+EL. Moreover, our proposed approaches converge much faster than baseline -greedy method.

1.1 Related Work

Cournot oligopoly games, and their convergence to various equilibria, have been widely studied in past research. The literature establishes that the long-term outcome of a Cournot oligopoly model depends on the underlying learning mechanism, firms’ rationality, and the memory size of the firms. The learning of economic agents can be widely divided into two categories: individual learning and social learning Vriend (2000). In individual learning models, an agent learns exclusively from its own experience, whereas in social learning models, an agent also learns from the experience of other agents. Learning frameworks also reflect the rationality of agents. Several works have studied individual learning mechanisms Vriend (2000); Arifovic and Maschek (2006); Vallée and Yıldızoğlu (2009); Fudenberg et al. (1998); Riechmann (2006). Some works claim that while social learning leads to Walrasian equilibrium, individual learning scheme results in convergence of the Nash equilibrium Vriend (2000); Vega-Redondo (1997); Franke (1998); Dawid (2011); Bischi et al. (2015). In this work, we use MA-MAB setting Thompson (1933) as a learning framework. Firms make decisions based on the profit/reward they are getting, mostly unaware of the impact of other firms’ actions on the market price; this can be called as implicit individual learning.

There is also vast literature on multi-agent MAB problems. Some papers include models inspired by the cognitive radio problem where agents pulling the same arm cause collision resulting in zero or small rewards Anandkumar et al. (2011); Liu and Zhao (2010); Rosenski et al. (2016); Besson and Kaufmann (2018); Hanawal and Darak (2021); Wang et al. (2020). Other works study different kinds of MA-MAB models with various degrees of collaboration and communication among agents Sankararaman et al. (2019); Chawla et al. (2020); Vial et al. (2021); Agarwal et al. (2021). To our knowledge, MA-MAB setting has not been studied yet for Cournot games; however, some RL approaches have been applied.

Closely related to our work is the work by Waltman and Kaymak (2008) and Xu (2020) who have studied RL methods. Waltman and Kaymak analyze the results of Q-learning in a Cournot game with discrete action space and explain the emergence of collusive behavior. They focus on three types of firms; firms in our experiments are similar to the firms without memory as considered in their paper. Kimbrough and Lu (2003) also reported results on Q-learning behavior in a Cournot oligopoly game where they found a slight tendency towards collusive behavior in their simulation study. Xu incorporated memory and imitation with RL. Firms do not have any information about market demand, but they can observe quantities produced by the other firms and their profits. Unlike Waltman and Kaymak (2008), they use a continuous action space and parametric function approximation. They use three different environment settings, the first setting (Treatment 1 in their paper) resembles our models. They have used the same experimental setup as in Waltman and Kaymak (2008). Unlike our results, they observe convergence to Nash equilibrium for these settings. Both of these papers evaluate scalability up to a limited range, while our paper incorporates a more thorough investigation of scalability in terms of the number of firms and the size of action space. Huck et al. (2004) studied another trial-and-error method. In their work, firms do not have information about their rivals as well as the payoff function of the game. However, their method allows agents only to decrease or increase the production level. Therefore, there is a great deal of responsibility on firms to choose the starting quantity. They showed that full collusion can be achieved with their approach; however, they did not study the scalability of their approach.

There is a wide variety of work that uses RL for dynamic pricing problems. The market models considered in these works are diverse Den Boer (2015). Kephart and Tesauro (2000) use Q-learning in one of such settings, and Könönen (2006) use Q-learning with function approximation as well as policy gradient method. Misra et al. (2019) proposed a multi-armed bandit based algorithm for a multi-period dynamic pricing problem, where firms face ambiguity. Hansen et al. (2020); Trovo et al. (2015) studied the applicability of MAB algorithms on dynamic pricing problems and proposed variants of the UCB algorithm. Hansen et al. found that with static demand having low noise, it is possible to get collusive behavior in firms, but as the noise increases, the results become indistinguishable from Nash equilibrium. On contrary, we did not notice any significant changes in our outcomes due to increase in noise.

2 Preliminaries

2.1 Cournot Oligopoly Model

We consider a standard Cournot oligopoly model with firms which simultaneously produce identical/homogeneous products. Firm produces quantity with cost function . Let denote linear demand function with an inverse demand equation as

| (1) |

where and denote two parameters. Firms have constant marginal cost. Firm ’s total cost is, , where is the constant marginal cost. The profit of a firm is calculated as

| (2) |

2.2 Equilibria in Cournot Oligopoly Models

Following definitions are for models with symmetric firms.

Definition 1.

The Cournot (Nash) Equilibrium is obtained if each firm chooses the production level that maximizes its profit, given the production levels of its competitors. No firm wishes to unilaterally change its output level when the other firms produce the output levels assigned to them in the equilibrium. Firms individually maximize their profit; they do not maximize their joint profit. The resulting joint production level is

Definition 2.

Walrasian Equilibrium is obtained if firms are not aware of their influence on the market price, and therefore behave as price takers. They adopt Walrasian rule and produce Walrasian quantity. The Walrasian rule is based on the assumption that a firm acting as price taker decides next-period output maximizing its profit. The resulting quantity dynamics leads to a dynamic equation that allows the Walrasian equilibrium output as the unique steady state Radi (2017). The resulting joint production level is

Definition 3.

In Collusive Equilibrium, firms form a cartel and maximize the joint profit. They produce a smaller quantity than the quantity that maximizes their individual profit. Hence, they have an incentive to increase their production levels. The resulting joint production level is

2.3 Multi-agent Multi-armed Bandit Framework

We consider the firms in repeated Cournot game as the agents operating in a MA-MAB framework with their arms representing the different production choices. Agents do not have any knowledge of the environment; agents only have knowledge about their own payoffs/rewards after taking an action. The action space is discrete and ordered; every action represents a production level choice, and the action set consists of all the integer values in a specific range.

Let be the number of agents in our MA-MAB setting. As agents are independent and autonomous, they each face a separate stochastic MAB with arms. Each agent’s goal is to maximize their individual reward over a long (possibly infinite) time horizon . For a game played at time step , the reward is same as the profit, which is calculated using eq. 2. From eq. 2, we can see that reward depends on individual agent’s production as well as total industry output at time step . Since all the agents are learning simultaneously, these bandits are not perfectly stochastic MAB, and the means and variances associated with arms are unknown to the agents.

3 Methods

We have modeled the repeated Cournot oligopoly game as a MA-MAB setting. Each firm in the market faces separate stochastic MAB. We have also explained that these are not perfect stochastic MABs, and the means and variances associated with arms are unknown. We feel that this is important to investigate since, as stated in Lattimore and Szepesvári (2020), perfectly stochastic MABs cannot necessarily be expected in the real world.

We initially analyzed the applicability of three well-known multi-armed bandit algorithms: -greedy, UCB (Upper Confidence Bound), and Thompson sampling. Most of the literature deals with Bernoulli bandits; however, we are dealing with normal bandits with unknown means and variances associated with the arms. We found that the UCB-Normal algorithm Cowan et al. (2017) which is designed for such scenarios, fails to converge. Thompson sampling proposed in Honda and Takemura (2014) is also designed to handle such scenarios; however, the outcomes depend on priors. As it is required to set appropriate priors, we cannot use it for our models. We think that -greedy is the only one among these three algorithms which can work with our assumptions of the lack of knowledge. We propose two novel approaches specifically to deal with the ordered action space in the Cournot games. Both of these approaches use -greedy as a sub-routine.

3.1 -Greedy

-Greedy Sutton and Barto (1998) is a common method for balancing exploration and exploitation trade-offs. At each time step , an agent chooses random action with probability or otherwise chooses the action with the highest empirical mean. The empirical mean of an action is often referred to as that action’s -value and is denoted, . In our formulation, is the running average of rewards obtained by choosing an action.

A linear bound on the expected regret can be achieved with constant . For variant of the algorithm where decreases with time, Cesa-Bianchi and Fischer (1998) proved poly-logarithmic bounds. However, Vermorel and Mohri (2005) did not find any practical advantage to using these methods in their empirical study. Here, we are referring to regret as it is used conventionally in single agent stochastic MAB problems Kuleshov and Precup (2014); Lattimore and Szepesvári (2020).

3.2 -Greedy with Hierarchical Learning (-greedy+HL)

We propose a new approach similar to hierarchical learning. This approach makes use of the fact that the action set is ordered in Cournot games. Learning happens in multiple phases. In each phase, the -Greedy algorithm is applied to certain arms. In the initial phase, the whole action set is divided into equally-sized ranges (buckets). Each action range/bucket is then considered as a single arm. When such an arm is pulled, the action is chosen uniformly at random from the bucket associated with that arm. Each phase ends when the same arm/bucket is chosen during exploitation mode for some pre-specified number of time steps. At the end of each phase, the arm with the highest -value is selected, and the associated bucket is further split into smaller-sized buckets. These new smaller buckets are then considered as arms for the next phase of the learning. This continues until the bucket cannot be further divided. In this way, under-performing arms are eliminated, and the focus of learning shifts to high-performing arms. Firms can select the value of as per their choice. This learning process can also be visualized as the search for the best action in -ary tree.

3.3 -Greedy with Elimination of Arms (-greedy+EL)

With hierarchical learning, firms need to make partitions of their action space, which is a crucial but delicate task. To do it efficiently, firms may need some information about the environment. Wrong partitioning may lead to losing out on optimal actions, i.e., a seemingly optimal bucket may contain sub-optimal actions. For the circumstances where firms may not want to take the responsibility of partitioning the action space, we propose another novel approach that is based on eliminating, rather than partitioning, the actions.

This approach also relies on -greedy as an underlying mechanism, and similar to hierarchical learning, works in multiple phases. Unlike previous approach, the initial phase starts with considering each action as an arm. Each phase ends when the same action is chosen during exploitation mode for some pre-specified amount of time steps. At the end of each phase, an action with maximum -value is selected. Let be the size of the action space. If available, number of actions on either side of action on the ordered scale are kept in the action space, and other actions are eliminated. This continues until .

4 Experiments and Results

In experiments, we empirically evaluate all three methods discussed above, i.e., -greedy, -greedy+HL, and -greedy+EL. We utilize simulations similar to the ones used by Waltman and Kaymak (2008). We further explore the scalability of our methods by running simulations with models consisting of up to firms and up to actions. We run every simulation times; here, simulation means the entire training process that lasts for several time steps. For each simulation, we compute the final outcome as the average value over last time steps. We consider both deterministic and stochastic versions of inverse demand function, and also, models with both symmetric and asymmetric firms.

4.0.1 Evaluation Measures

We aim to investigate the resulting equilibrium that Cournot models achieve after applying the proposed approaches. We compare joint quantities and joint profits obtained with baseline -greedy as well as our proposed approaches. Moreover, we do an empirical analysis of the regrets. The environment evolves over time as agents learn. As a result, the optimal action to take changes from an individual agent’s perspective. Also, there is no way to foretell the convergence of other agents’ strategies to any specific action or policy. Therefore, we cannot calculate regret for individual agents the way it is calculated for typical stochastic MAB problems. However, we consider that the firms always strive for the maximum profit; this can only be achieved if firms form a cartel, i.e., full collusion. Therefore, despite agents being independent and autonomous, we calculate joint cumulative regret for the whole system. It is calculated by subtracting the joint cumulative profit that is actually obtained from the profit firms could have obtained by acting as a cartel. In graphs, the lines are plotted using mean values, and the fillers encompassing those lines are plotted using and percentiles.

4.0.2 Parameters

The exploration rate, , is one of the main hyper-parameters in -greedy approaches. In the reported experiments, we use the exploration rate for all three approaches. We also tried other exploration rates, and found that the final outcomes are robust to different exploration rates; however, an increase in joint cumulative regret can be seen with higher exploration rates. Moreover, decay in the exploration rate does not make any difference in outcomes or the convergence rate. We use the running average of rewards as the Q-values; therefore, the learning rate is not needed. Instead of learning for a pre-specified amount of steps, agents learn until they consistently pick a particular action in exploitation mode for the specific number of steps. For -greedy+HL and -greedy+EL, agents have to pick the same arm in exploitation mode for consecutive steps in each phase of the method. However, for baseline -greedy, agents have to pick the same arm in exploitation mode for consecutive steps. This difference is because there is no reduction in the size of the action space for baseline -greedy, and it takes more steps to get to the steady choice in multiple simulation runs. These choices apply to all types of simulations discussed below. For -greedy+HL, we use (number of partitions) to be . The outcomes in terms of equilibrium are robust to the choice of ; nonetheless, it can affect joint cumulative regret as the number of phases in the algorithm and total time steps depend on this parameter.

4.1 Small-scale Simulations

We first evaluate our approaches using the same simulations as those used by Waltman and Kaymak (2008). They used Cournot models with symmetric firms in their simulations. They used , as constants in an inverse demand function (eq. 1), along with constant marginal cost, . The action space is discrete, where agents can choose a production quantity between . They ran simulations with the total number of firms varying from to . The results of these simulations are shown in fig 1(a), 1(b), and 1(c) for joint quantities, joint profits, and joint cumulative regrets, respectively. From fig 1(a) and 1(b), we can see that with -greedy, the outcomes mostly converge somewhere between Nash and Walras equilibrium; however, for model with firms, output coincides with Nash equilibrium in fig 1(a). For both -greedy+HL and -greedy+EL, outcomes are collusive. However, with -greedy+HL those are closer to collusive equilibrium. We consider an outcome to be collusive when it is anywhere in between Nash and collusive equilibrium; therefore the degree of collusion may vary based on its closeness to collusive equilibrium. The outcomes seen in the graphs of joint quantities may not be perfectly reflected in the corresponding graphs of joint profits. This is a consistent outcome that can be seen throughout our experiments. We think that this is because we allow profits/rewards to be negative in our models. Firms lose the production costs regardless of the market price. Because of this, there is more variance in joint profits obtained through different simulations. As we take the average results of different simulations, it is reflected in the graphs.

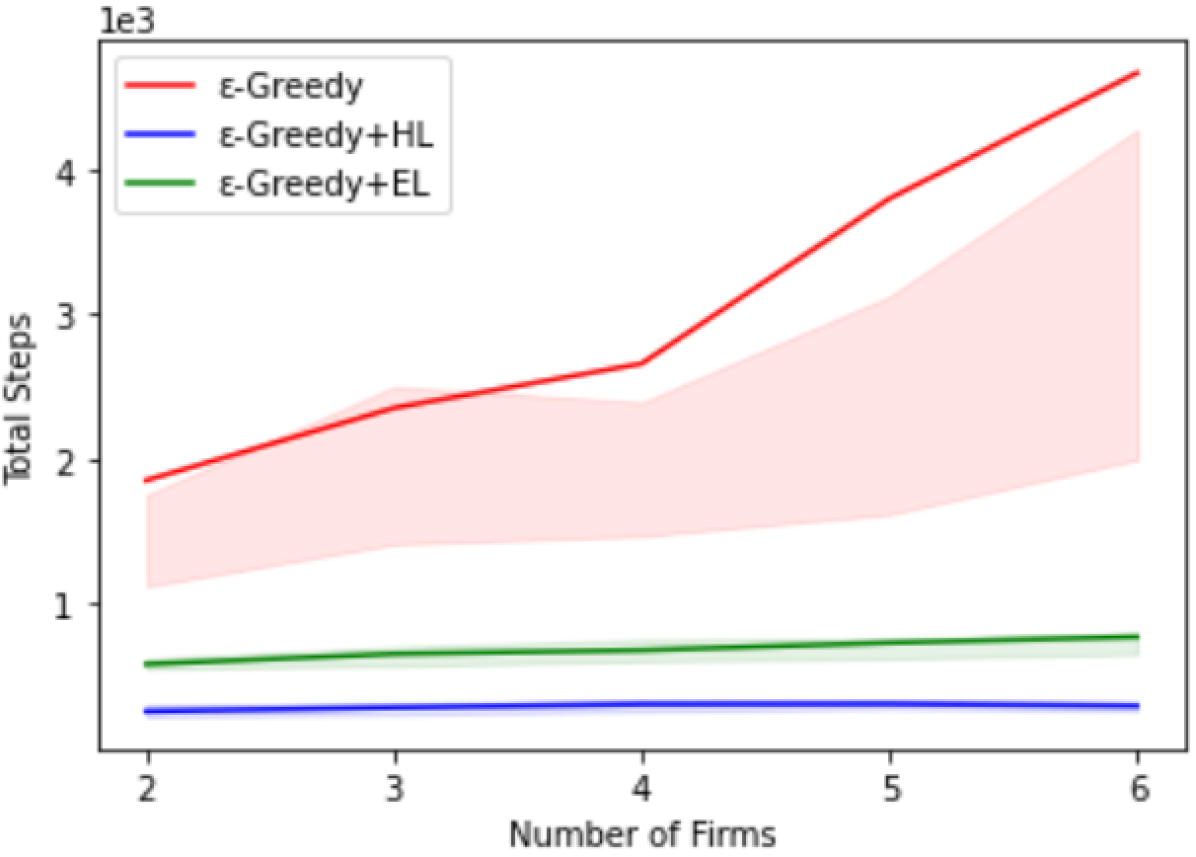

From fig 1(c), we can see that the -greedy+HL method obtains lowest regret, followed by -greedy+EL, and -greedy obtains very high regret in comparison to the other two methods. One of the reasons is that our proposed approaches take fewer steps to converge than -greedy. -greedy+HL on average takes only steps while -greedy+EL takes around steps. Graph comparing total time steps taken by these three approaches (shown in 4(a)) is very similar to joint cumulative regrets’ graph shown in fig 1(c). In addition to this, we think that the more collusive outcomes and rapid decrease in action space size causes -greedy+HL to have lower regret than -greedy+EL.

joint quantities

joint profits

joint cumu. regrets

simulations

(scaled actions)

(scaled agents)

4.2 Large-scale Simulations

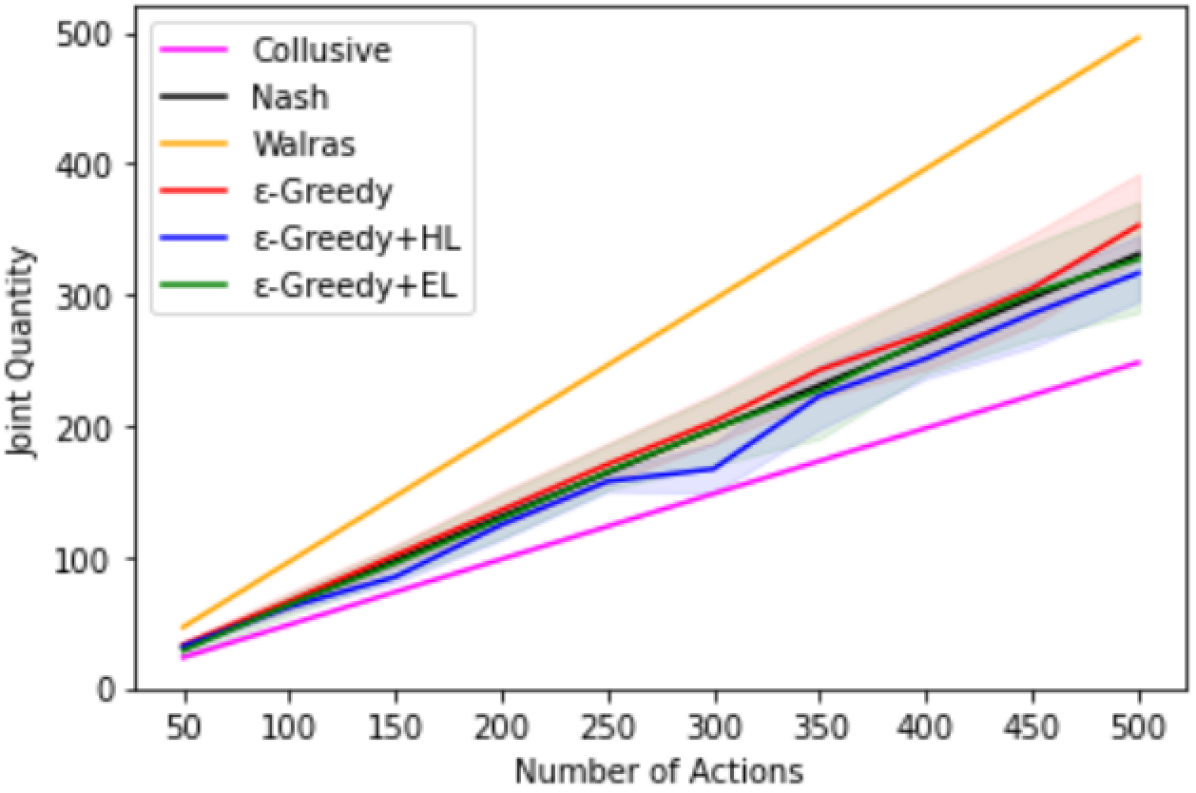

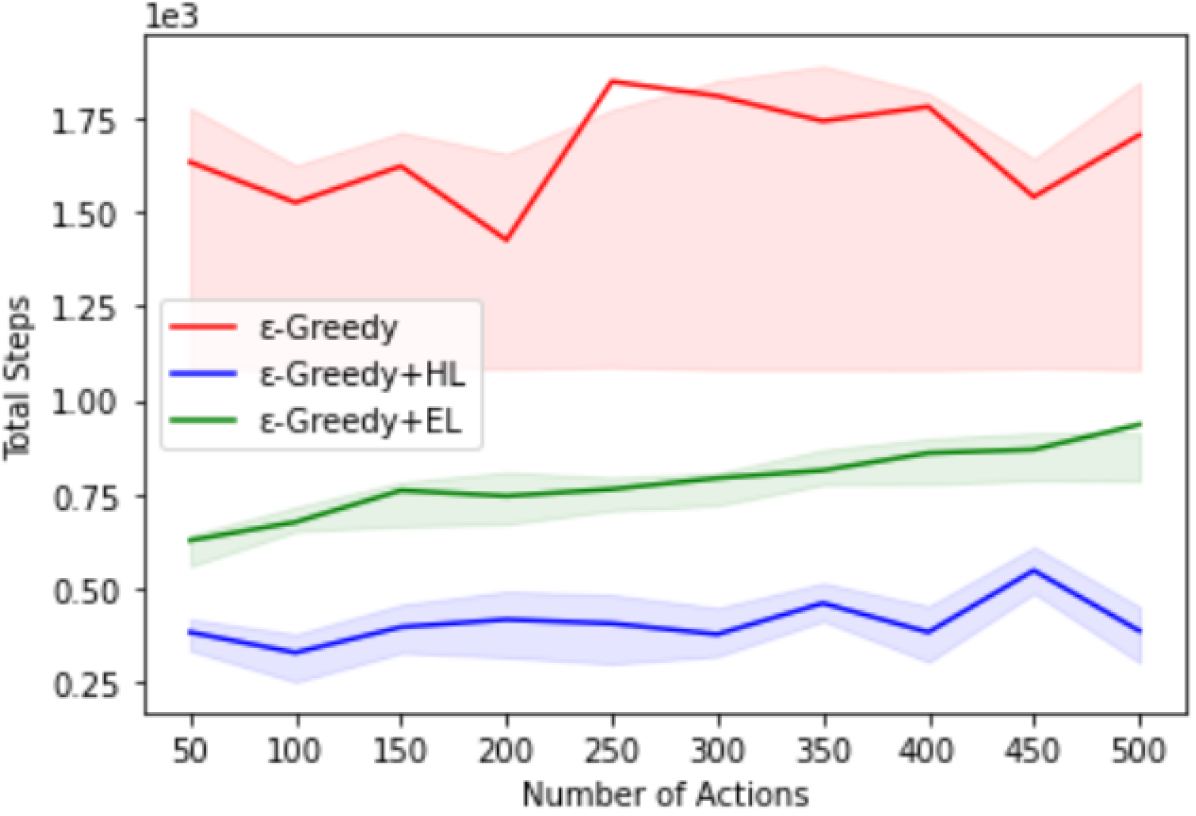

4.2.1 Scaling action space:

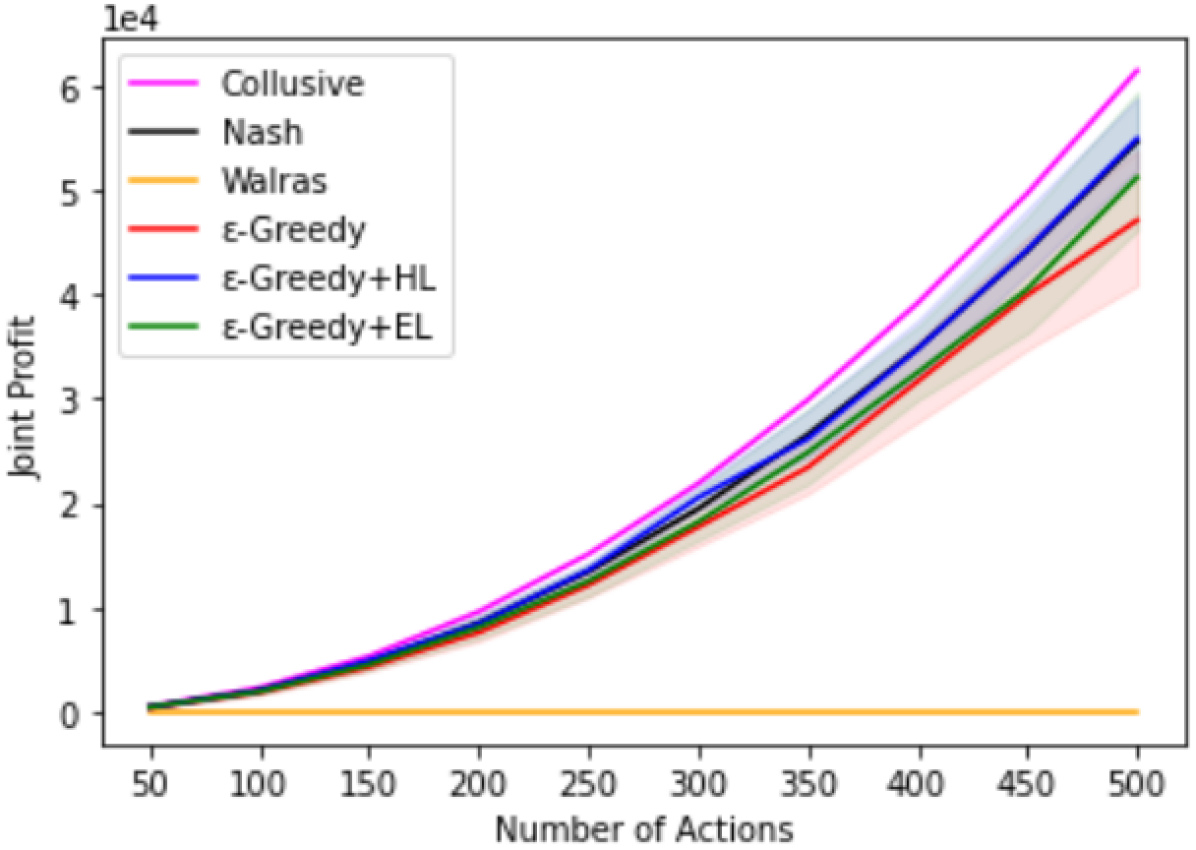

Firms with high production capacities can exist in the market. With high production capacity, more actions, i.e., production level choices, are available to the firms. Here, we use the Cournot duopoly model consisting of symmetric firms. However, the size of action space, , varies from to . Available actions in the specific model are in the range . For the meaningful exploration of action space, the market demand also varies according to the size of the action space, such that the value of parameter in the demand function is equal to the size of action space, . From fig 2(a), we can see that most of the outcomes converge to Nash equilibrium. However, for -greedy+HL outcomes are somewhat collusive, and for -greedy, those are bit off from Nash equilibrium and lies between Nash and Walras equilibrium.

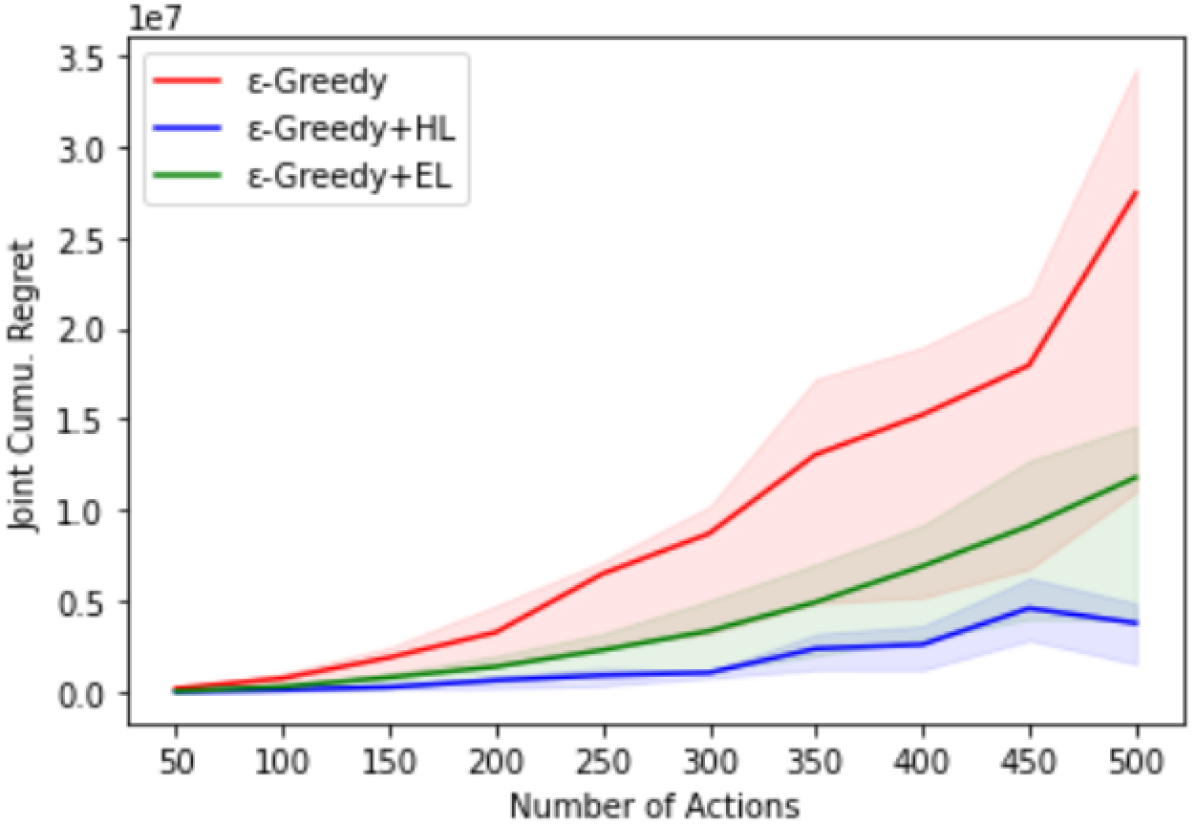

For the reasons discussed in previous section, joint profits shown in fig 2(b) are slightly different from their counterpart joint quantities in fig 2(a). As shown in fig 2(c), the regret with -greedy is larger than that for -greedy+EL, which is, in turn, larger than the regret for -greedy+HL. In fig 2(c), joint cumulative regret increases with the size of action space for all three approaches, but this pattern is not seen with the total steps required to converge (from 4(b)); for all approaches, total steps required to converge do not differ much with varying action space size; nonetheless, they are directly proportional to joint regrets.

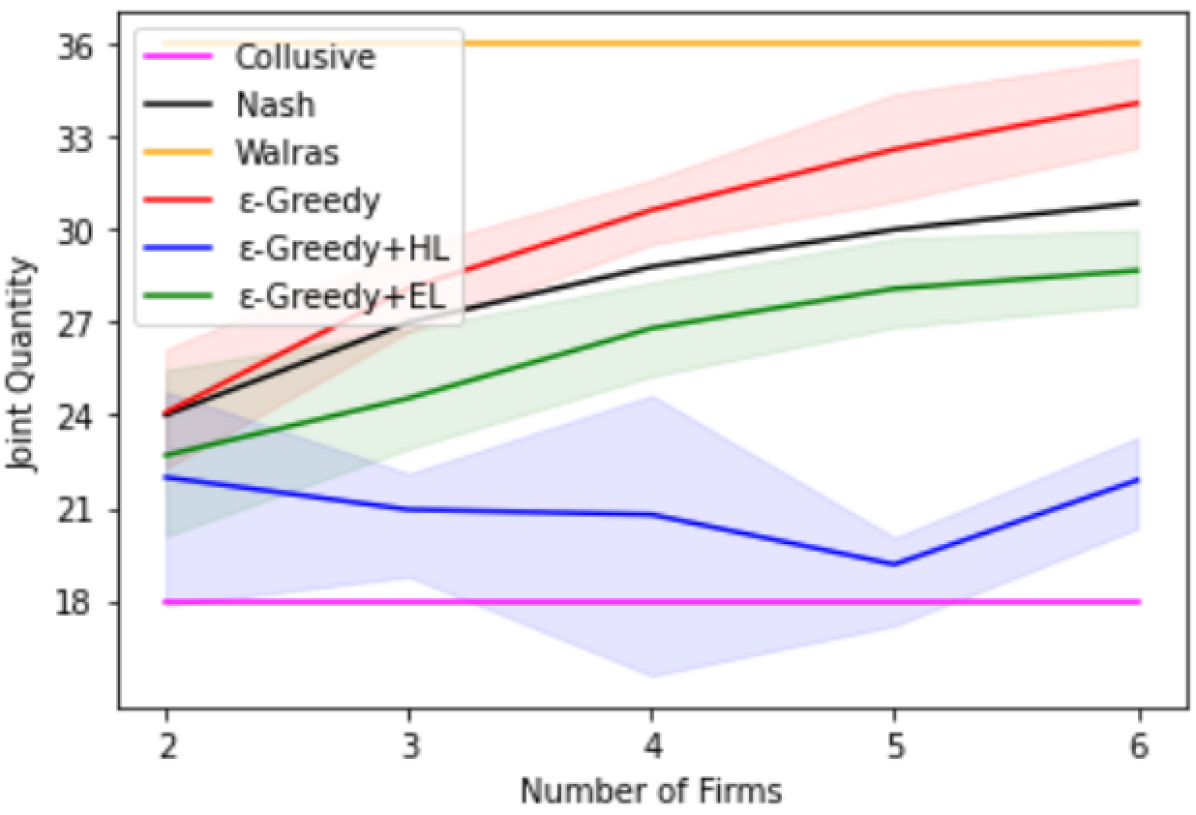

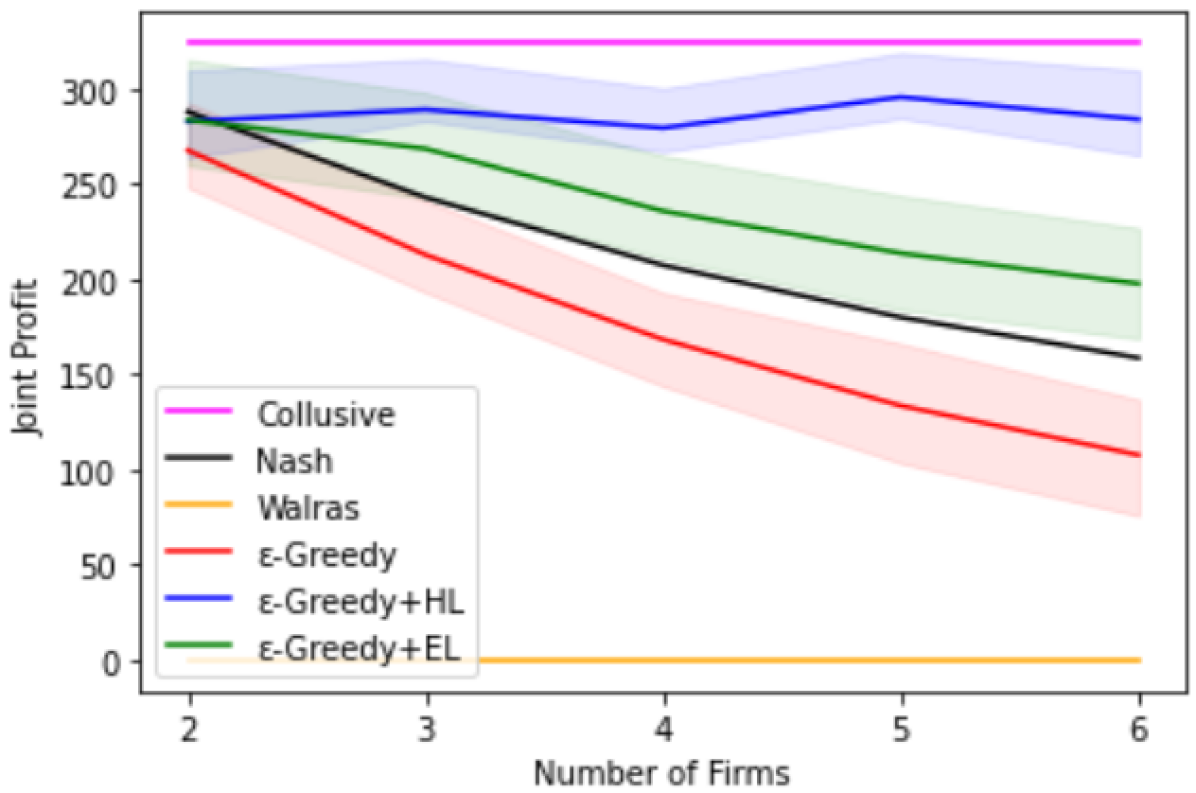

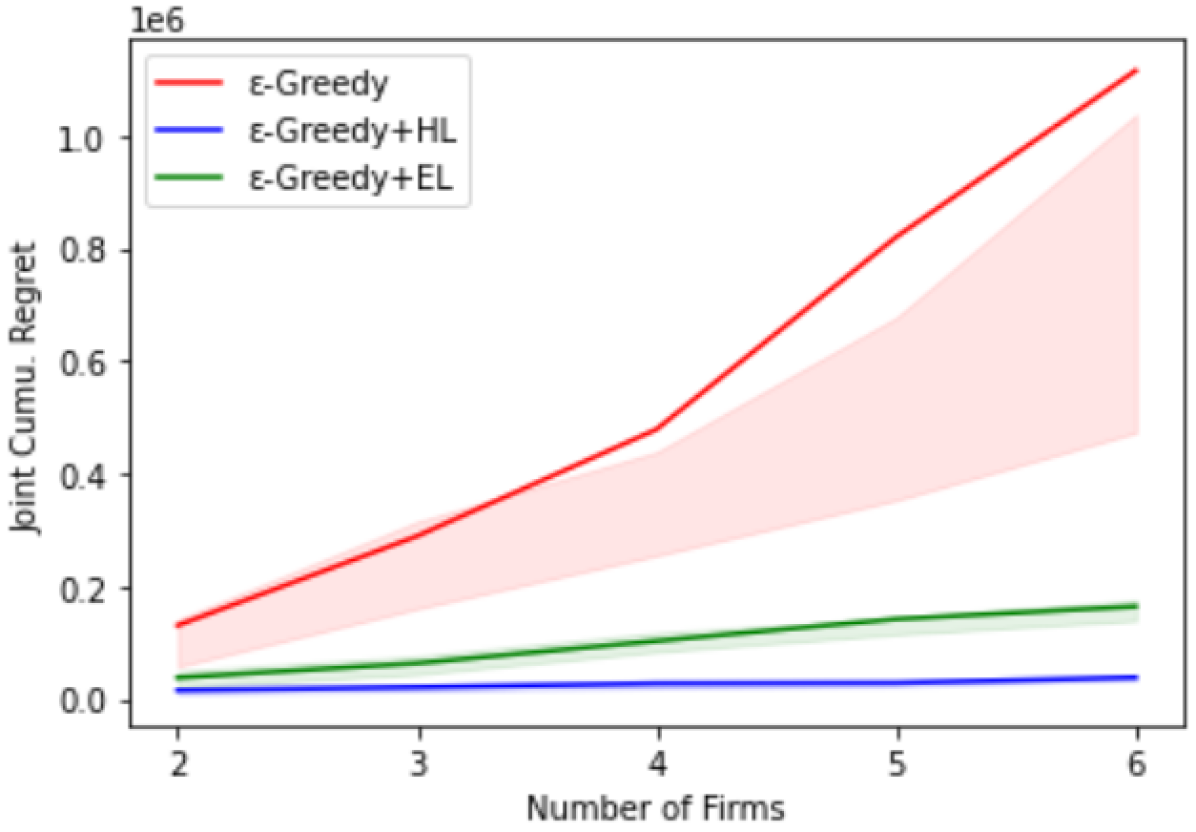

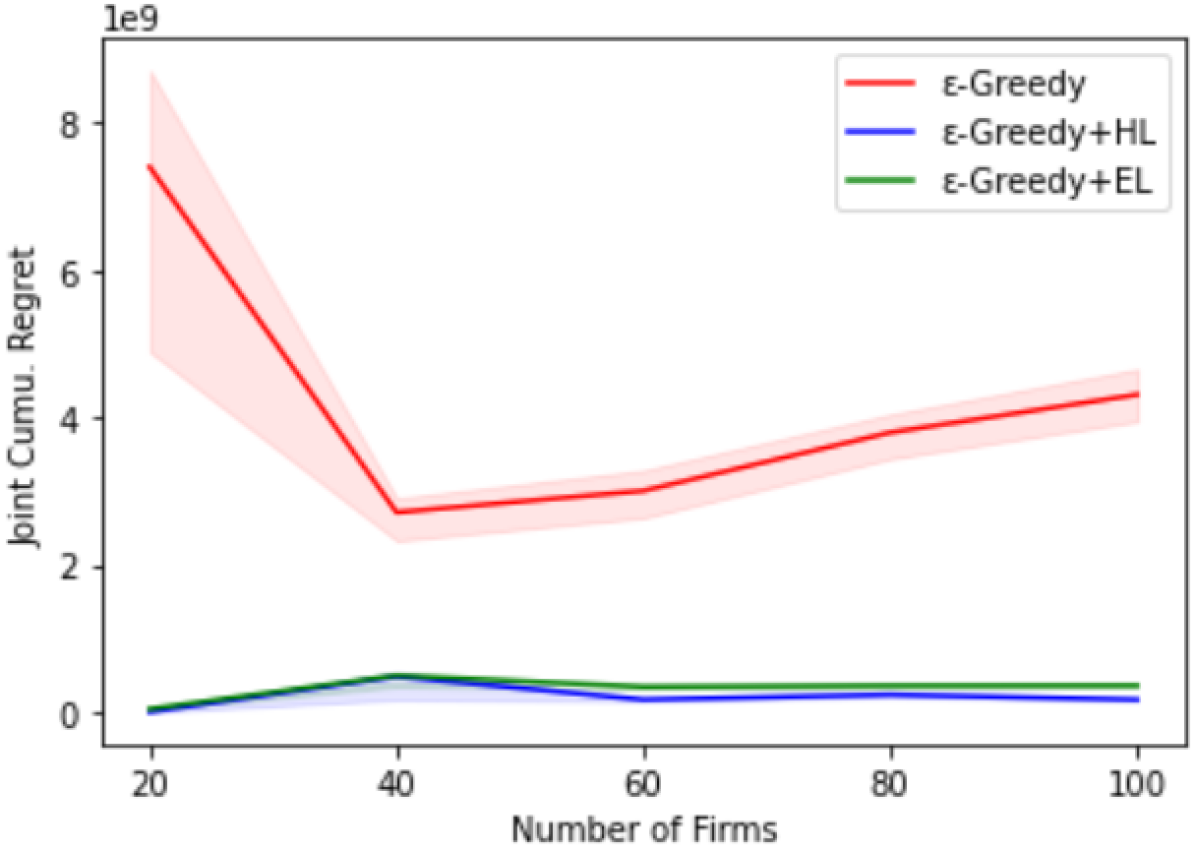

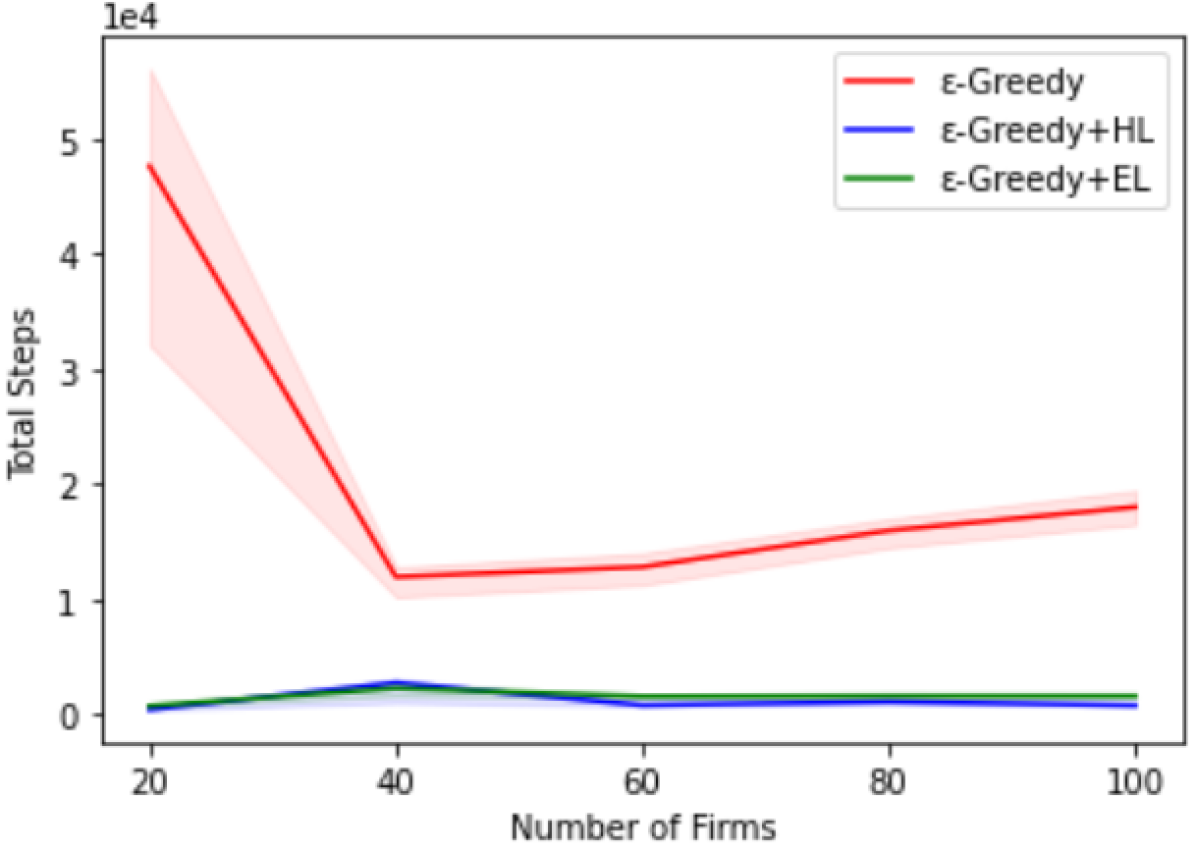

4.2.2 Scaling number of firms:

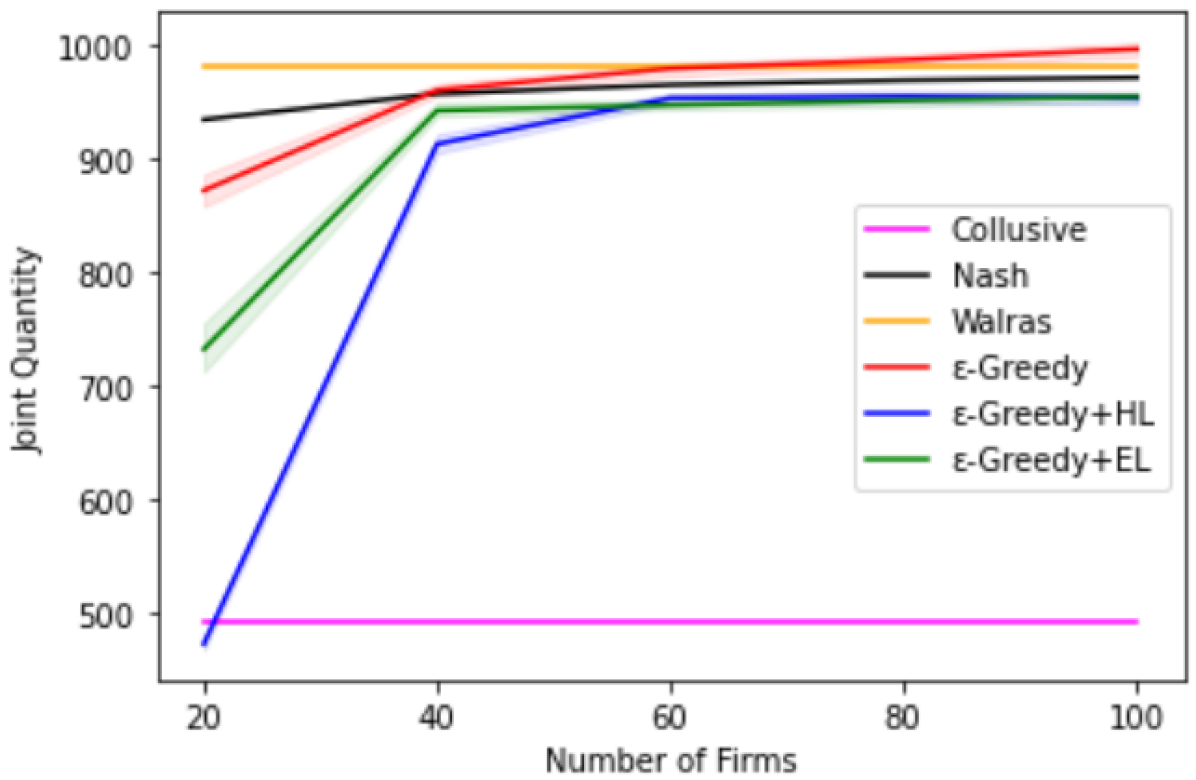

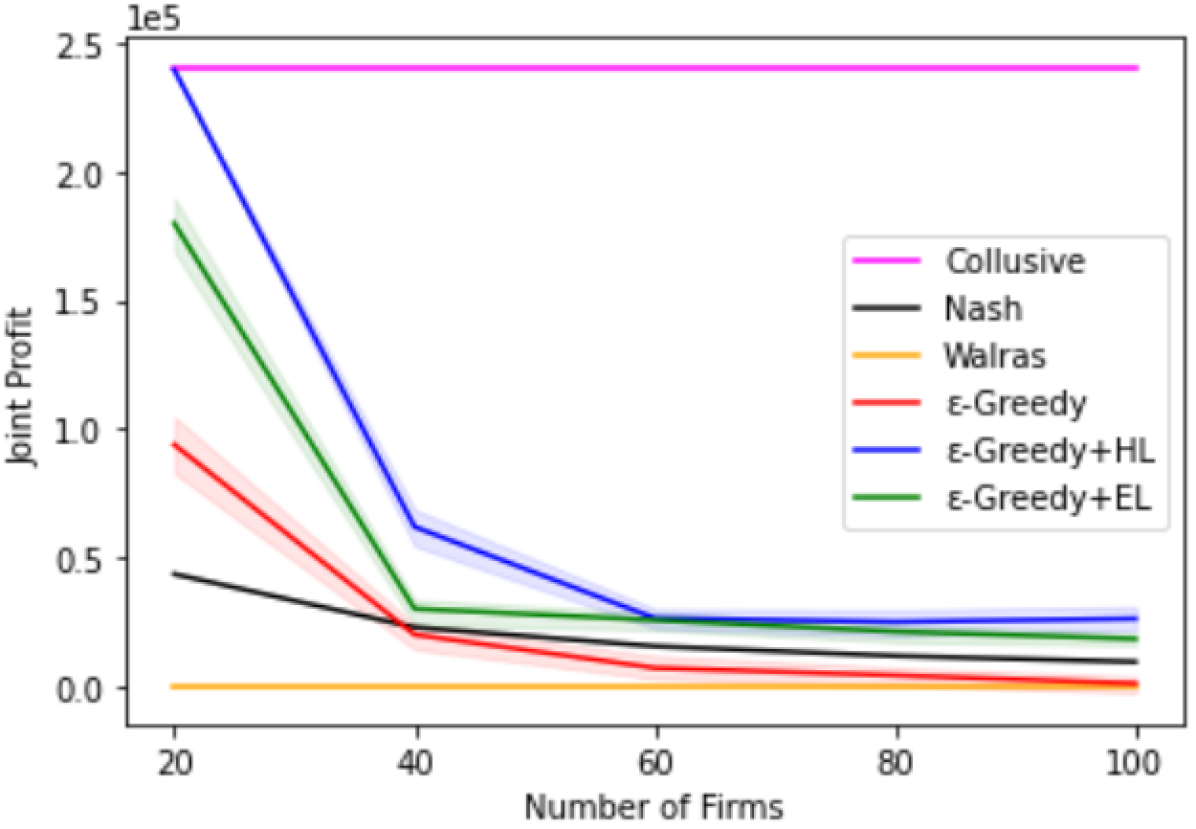

Cournot models with a large number of firms have been rarely explored in the literature. We simulate models consisting of , , , , and total number of firms. Here, we consider the demand function with and , along with . The action choices range from to . The results for joint quantity, joint profit, and joint cumulative regret are shown in figures 3(a), 3(b), and 3(c), respectively. With increasing number of firms, Nash equilibrium approaches Walrasian equilibrium. In fig 3(a), for -greedy we can see that the outcome is collusive for model with firms; with firms, it coincides with Nash equilibrium; for models with and firms, it seems to coincide with Walras equilibrium and interestingly, outcomes seems to be slightly more than Walras equilibrium for model with firms. Therefore, we can say that -greedy performs very poorly for models with large number of firms and begins to break down when the total number of firms is greater than . Surprisingly, if we compare its performance in terms of joint profits, it is better in the sense that it does not fall below Walras equilibrium for model with firms. This is unlike the results for previous sections where joint profits tend to be worse than their counterparts in joint quantities (if we assume that collusive Nash Walras).

-greedy+HL and -greedy+EL both obtain collusive results in these simulations. For models with comparatively smaller number of firms ( and ), -greedy+HL seems to be more collusive; however, outcomes of both approaches are similar for larger models. Unlike previous results, -greedy+HL and -greedy+EL methods obtain nearly the same regrets. Not surprisingly, we found that both -greedy+HL and -greedy+EL run for almost equal time steps (shown in 4(c)). Overall, the graph for total time steps is very similar to fig 3(c) showing joint cumulative regrets. Interestingly, even though the model with firms converge to collusive outcomes, the regret obtained by -greedy in this case is higher than other larger models. As the demand and size of action space stay the same across all models with varying number of firms, agents in smaller models have more viable action choices that give positive payoffs/rewards. It causes a delay in converging to the final outcome and hence more exploration, which in turn causes more regret. From both types of large-scale simulations, we can see that having more viable action choices leads to more regret.

4.2.3 Stochastic demand function

As mentioned in the preliminaries, the stochastic demand function (eq. 3) is obtained by multiplying the inverse demand function (eq. 1) with noise. This noise is derived from a normal distribution. We evaluate two types of models with stochastic demand. In the first one, noise is derived from a normal distribution having mean, , and standard deviation, . For the second type of model, we increase to . We found no significant difference between the outcomes for both the cases, and the results are very similar to the ones obtained by having deterministic demand. We examined the results for both small-scale and large-scale simulations. For both types of simulations, there is no difference between outcomes in terms of joint quantity and joint profit; this is true for all three approaches. For small-scale simulations, with -greedy, the outcomes obtained for models with stochastic demand are worse than those obtained with deterministic demand in terms of joint cumulative regrets; in most of the cases, more stochasticity leads to worse outcome. However, this difference lessened in the results obtained by -greedy+HL and -greedy+EL, which are almost same for all types of models. It shows that our proposed approaches can handle stochasticity in the demand function. Surprisingly, for large-scale simulations, in some cases, joint cumulative regret obtained for models with static demand is slightly more than that obtained for models with stochastic demand. Here, stochasticity might have helped to find better actions.

4.2.4 Asymmetric firms

We also study Cournot models with asymmetric firms, i.e., firms with different marginal costs. In simulations, we use Cournot duopoly models with two firms having different marginal costs. These costs vary in different simulations. We used the same model parameters as those used in small-scale simulations. We have and as constants in an inverse demand function (eq. 1), but the constant marginal cost is different for two firms. Let and be the marginal costs for two firms, then lies in range and in range . Overall, the results (shown in 1) are similar to those with symmetric firms. -greedy mostly converges to outcomes worse than Nash equilibrium. However, for -greedy+HL and -greedy+EL, most of the outcomes are collusive; more collusive with -greedy+HL than with -greedy+EL.

| Nash Equilibrium | -greedy | -greedy + HL | -greedy + EL | ||

|---|---|---|---|---|---|

| (1, 2) | Q | [13.3, 12.3] | [13.8±4.3, 12.4±3.9] | [11.3±2.9, 10.8±2.7] | [11.4±3.9, 12.7±4.7] |

| P | [177.8, 152.2] | [170.6±49.0, 143.2±49.3] | [181.6±35.0, 164.2±27.7] | [163.9±38.2, 164.5±30.3] | |

| (1, 3) | Q | [13.7, 11.7] | [13.7±5.2, 12.3±5.5] | [11.8±3.7, 10.0±3.0] | [12.8±3.1, 10.5±4.1] |

| P | [186.7, 136.1] | [166.8±69.5, 122.3±66.5] | [196.9±45.3, 142.4±43.0] | [189.2±29.4, 138.3±36.0] | |

| (1, 4) | Q | [14.0, 11.0] | [13.5±4.6, 12.1±5.2] | [11.9±3.2, 9.7±2.4] | [12.8±3.6, 10.1±3.2] |

| P | [196.0, 121.0] | [177.2±62.1, 117.6±58.8] | [199.6±39.1, 129.6±43.5] | [196.7±23.1, 125.3±31.8] | |

| (1, 5) | Q | [14.3, 10.3] | [13.5±4.6, 11.3±4.8] | [12.6±2.4, 8.4±3.1] | [12.4±2.7, 10.0±2.1] |

| P | [205.5, 106.8] | [180.9±59.6, 107.1±56.4] | [216.0±47.5, 109.5±34.4] | [194.6±24.5, 122.9±31.9] | |

| (2, 2) | Q | [12.7, 12.7] | [12.5±5.1, 12.9±4.8] | [10.9±2.6, 10.9±2.8] | [11.7±3.4, 11.8±3.8] |

| P | [160.4, 160.4] | [149.4±63.6, 154.0±60.1] | [170.2±44.6, 167.8±35.1] | [162.7±30.2, 160.7±27.7] | |

| (2, 3) | Q | [13.0, 12.0] | [13.1±5.1, 13.2±5.7] | [11.6±3.0, 9.6±2.2] | [12.8±2.7, 11.1±3.3] |

| P | [169.0, 144.0] | [148.6±67.1, 133.2±67.5] | [186.9±43.8, 142.8±36.2] | [173.9±26.4, 141.3±35.0] | |

| (2, 4) | Q | [13.3, 11.3] | [13.6±5.0, 11.2±4.9] | [11.9±3.3, 10.0±3.6] | [12.3±3.4, 10.7±2.1] |

| P | [177.8, 128.5] | [167.5±67.2, 115.8±60.1] | [185.9±44.3, 131.8±31.7] | [175.9±36.0, 133.6±33.0] | |

| (2, 5) | Q | [13.7, 10.7] | [13.3±4.7, 12.1±4.7] | [12.7±3.9, 7.9±3.2] | [12.6±2.6, 9.6±2.7] |

| P | [186.7, 113.7] | [160.1±62.2, 106.5±64.1] | [211.8±49.8, 103.0±32.4] | [186.1±30.4, 118.2±27.0] | |

| (3, 2) | Q | [12.0, 13.0] | [12.9±6.1, 13.0±4.7] | [9.8±3.4, 12.2±2.6] | [11.6±2.6, 11.9±2.3] |

| P | [144.0, 169.0] | [130.5±66.7, 153.7±66.3] | [141.8±40.2, 186.9±36.0] | [147.4±30.3, 164.9±25.5] | |

| (3, 3) | Q | [12.3, 12.3] | [13.5±6.1, 12.3±4.4] | [9.7±3.5, 11.3±2.4] | [11.5±2.8, 11.6±2.1] |

| P | [152.2, 152.2] | [135.9±68.0, 135.4±61.6] | [145.5±29.9, 172.0±31.9] | [153.1±29.3, 154.1±28.4] | |

| (3, 4) | Q | [12.7, 11.7] | [12.9±4.5, 11.9±5.1] | [11.6±2.3, 8.9±2.1] | [11.4±2.4, 11.4±2.3] |

| P | [160.4, 136.1] | [149.6±62.4, 121.3±64.0] | [179.9±29.2, 130.1±27.2] | [152.6±23.9, 142.8±31.9] | |

| (3, 5) | Q | [13.0, 11.0] | [13.3±5.4, 11.3±3.5] | [11.5±2.9, 9.0±3.0] | [12.2±2.2, 10.2±2.8] |

| P | [169.0, 121.0] | [149.8±58.4, 115.6±54.7] | [180.8±23.0, 121.1±21.3] | [168.5±27.9, 120.5±23.6] | |

5 Conclusion and Future Work

We have investigated the modeling of Cournot games in MA-MAB setting, especially when the firms have no knowledge of the market. Using MA-MAB setting allows for the implementation of approaches based on exploration-exploration paradigm. To deal with ordered action sets, we proposed two novel approaches, which are extensions of -greedy algorithm. Given the assumption of static demand, proposed methods optimize the exploration by reducing the action space. -greedy+HL performs best in terms of joint cumulative regret but comes with the additional responsibility of deciding the number of partitions in action space. With -greedy+EL, there is no such burden, but it may cause more regret than -greedy+HL. Our proposed approaches converge much faster than baseline -greedy method. -greedy rarely produces collusive outcomes, but mostly obtains Nash quantity or any state between Nash and Walrasian outcome. Our proposed approaches mostly obtain somewhat collusive outcomes for all kinds of simulations, although full collusion usually does not emerge. We think that these results are supportive of the concern over online algorithms being collusive without any external intervention Klein (2020). In future, we would like to work with Cournot models having non-stationary demand functions, and random entry or exit allowed to the firms.

References

- Cournot [1838] Antoine Augustin Cournot. Recherches sur les Principes Mathématiques de la Théorie des Richesses. L. Hachette, 1838.

- Kirschen and Strbac [2018] Daniel S Kirschen and Goran Strbac. Fundamentals of power system economics. John Wiley & Sons, 2018.

- Bimpikis et al. [2019] Kostas Bimpikis, Shayan Ehsani, and Rahmi Ilkılıç. Cournot competition in networked markets. Management Science, 65(6):2467–2481, 2019.

- Chletsos and Saiti [2019] Michael Chletsos and Anna Saiti. Hospitals as suppliers of healthcare services. In Strategic Management and Economics in Health Care, pages 179–205. Springer, 2019.

- Lattimore and Szepesvári [2020] Tor Lattimore and Csaba Szepesvári. Bandit algorithms. Cambridge University Press, 2020.

- Cowan et al. [2017] Wesley Cowan, Junya Honda, and Michael N Katehakis. Normal bandits of unknown means and variances. J. Mach. Learn. Res., 18:154–1, 2017.

- Honda and Takemura [2014] Junya Honda and Akimichi Takemura. Optimality of thompson sampling for gaussian bandits depends on priors. In Artificial Intelligence and Statistics, pages 375–383. PMLR, 2014.

- Waltman and Kaymak [2008] Ludo Waltman and Uzay Kaymak. Q-learning agents in a Cournot oligopoly model. Journal of Economic Dynamics and Control, 32(10):3275–3293, 2008.

- Xu [2020] Junyi Xu. Reinforcement learning in a Cournot oligopoly model. Computational Economics, pages 1–24, 2020.

- Vriend [2000] Nicolaas J Vriend. An illustration of the essential difference between individual and social learning, and its consequences for computational analyses. Journal of economic dynamics and control, 24(1):1–19, 2000.

- Arifovic and Maschek [2006] Jasmina Arifovic and Michael K Maschek. Revisiting individual evolutionary learning in the cobweb model–an illustration of the virtual spite-effect. Computational economics, 28(4):333–354, 2006.

- Vallée and Yıldızoğlu [2009] Thomas Vallée and Murat Yıldızoğlu. Convergence in the finite Cournot oligopoly with social and individual learning. Journal of Economic Behavior & Organization, 72(2):670–690, 2009.

- Fudenberg et al. [1998] Drew Fudenberg, Fudenberg Drew, David K Levine, and David K Levine. The theory of learning in games, volume 2. MIT press, 1998.

- Riechmann [2006] Thomas Riechmann. Cournot or Walras? long-run results in oligopoly games. Journal of Institutional and Theoretical Economics (JITE)/Zeitschrift für die gesamte Staatswissenschaft, pages 702–720, 2006.

- Vega-Redondo [1997] Fernando Vega-Redondo. The evolution of Walrasian behavior. Econometrica: Journal of the Econometric Society, pages 375–384, 1997.

- Franke [1998] Reiner Franke. Coevolution and stable adjustments in the cobweb model. Journal of Evolutionary Economics, 8(4):383–406, 1998.

- Dawid [2011] Herbert Dawid. Adaptive learning by genetic algorithms: Analytical results and applications to economic models. Springer Science & Business Media, 2011.

- Bischi et al. [2015] Gian Italo Bischi, Fabio Lamantia, and Davide Radi. An evolutionary Cournot model with limited market knowledge. Journal of Economic Behavior & Organization, 116:219–238, 2015.

- Thompson [1933] William R Thompson. On the likelihood that one unknown probability exceeds another in view of the evidence of two samples. Biometrika, 25(3/4):285–294, 1933.

- Anandkumar et al. [2011] Animashree Anandkumar, Nithin Michael, Ao Kevin Tang, and Ananthram Swami. Distributed algorithms for learning and cognitive medium access with logarithmic regret. IEEE Journal on Selected Areas in Communications, 29(4):731–745, 2011.

- Liu and Zhao [2010] Keqin Liu and Qing Zhao. Distributed learning in multi-armed bandit with multiple players. IEEE Transactions on Signal Processing, 58(11):5667–5681, 2010.

- Rosenski et al. [2016] Jonathan Rosenski, Ohad Shamir, and Liran Szlak. Multi-player bandits–a musical chairs approach. In International Conference on Machine Learning, pages 155–163. PMLR, 2016.

- Besson and Kaufmann [2018] Lilian Besson and Emilie Kaufmann. Multi-player bandits revisited. In Algorithmic Learning Theory, pages 56–92. PMLR, 2018.

- Hanawal and Darak [2021] Manjesh Kumar Hanawal and Sumit Darak. Multi-player bandits: A trekking approach. IEEE Transactions on Automatic Control, 2021.

- Wang et al. [2020] Po-An Wang, Alexandre Proutiere, Kaito Ariu, Yassir Jedra, and Alessio Russo. Optimal algorithms for multiplayer multi-armed bandits. In International Conference on Artificial Intelligence and Statistics, pages 4120–4129. PMLR, 2020.

- Sankararaman et al. [2019] Abishek Sankararaman, Ayalvadi Ganesh, and Sanjay Shakkottai. Social learning in multi agent multi armed bandits. Proceedings of the ACM on Measurement and Analysis of Computing Systems, 3(3):1–35, 2019.

- Chawla et al. [2020] Ronshee Chawla, Abishek Sankararaman, Ayalvadi Ganesh, and Sanjay Shakkottai. The gossiping insert-eliminate algorithm for multi-agent bandits. In International Conference on Artificial Intelligence and Statistics, pages 3471–3481. PMLR, 2020.

- Vial et al. [2021] Daniel Vial, Sanjay Shakkottai, and R Srikant. Robust multi-agent multi-armed bandits. In Proceedings of the Twenty-second International Symposium on Theory, Algorithmic Foundations, and Protocol Design for Mobile Networks and Mobile Computing, pages 161–170, 2021.

- Agarwal et al. [2021] Mridul Agarwal, Vaneet Aggarwal, and Kamyar Azizzadenesheli. Multi-agent multi-armed bandits with limited communication. arXiv preprint arXiv:2102.08462, 2021.

- Kimbrough and Lu [2003] Steven O Kimbrough and Ming Lu. A note on Q-learning in the Cournot game. In Proceedings of the Second Workshop on e-Business, 2003.

- Huck et al. [2004] Steffen Huck, Hans-Theo Normann, and Jörg Oechssler. Through trial and error to collusion. International Economic Review, 45(1):205–224, 2004.

- Den Boer [2015] Arnoud V Den Boer. Dynamic pricing and learning: historical origins, current research, and new directions. Surveys in operations research and management science, 20(1):1–18, 2015.

- Kephart and Tesauro [2000] Jeffrey O Kephart and Gerald J Tesauro. Pseudo-convergent Q-learning by competitive pricebots. In Proc. 17th Int’l Conf. Machine Learning. Citeseer, 2000.

- Könönen [2006] Ville Könönen. Dynamic pricing based on asymmetric multiagent reinforcement learning. International journal of intelligent systems, 21(1):73–98, 2006.

- Misra et al. [2019] Kanishka Misra, Eric M Schwartz, and Jacob Abernethy. Dynamic online pricing with incomplete information using multiarmed bandit experiments. Marketing Science, 38(2):226–252, 2019.

- Hansen et al. [2020] Karsten Hansen, Kanishka Misra, and Mallesh Pai. Algorithmic collusion: Supra-competitive prices via independent algorithms. CEPR Discussion Paper No. DP14372, 2020.

- Trovo et al. [2015] Francesco Trovo, Stefano Paladino, Marcello Restelli, and Nicola Gatti. Multi-armed bandit for pricing. In 12th European Workshop on Reinforcement Learning, pages 1–9, 2015.

- Karlin and Carr [1962] Samuel Karlin and Charles R Carr. Prices and optimal inventory policy. Studies in Applied Probability and Management Science, 4:159–172, 1962.

- Petruzzi and Dada [1999] Nicholas C Petruzzi and Maqbool Dada. Pricing and the newsvendor problem: A review with extensions. Operations research, 47(2):183–194, 1999.

- Huang et al. [2013] Jian Huang, Mingming Leng, and Mahmut Parlar. Demand functions in decision modeling: A comprehensive survey and research directions. Decision Sciences, 44(3):557–609, 2013.

- Radi [2017] Davide Radi. Walrasian versus cournot behavior in an oligopoly of boundedly rational firms. Journal of Evolutionary Economics, 27(5):933–961, 2017.

- Sutton and Barto [1998] RS Sutton and AG Barto. Reinforcement learning: An introduction. cambridge, ma: Mit press. 1998.

- Cesa-Bianchi and Fischer [1998] Nicolo Cesa-Bianchi and Paul Fischer. Finite-time regret bounds for the multiarmed bandit problem. In ICML, volume 98, pages 100–108. Citeseer, 1998.

- Vermorel and Mohri [2005] Joannes Vermorel and Mehryar Mohri. Multi-armed bandit algorithms and empirical evaluation. In European conference on machine learning, pages 437–448. Springer, 2005.

- Kuleshov and Precup [2014] Volodymyr Kuleshov and Doina Precup. Algorithms for multi-armed bandit problems. arXiv preprint arXiv:1402.6028, 2014.

- Klein [2020] Timo Klein. (M)isunderstanding algorithmic collusion. Competition Policy International (CPI), 2020.