Lower bound for the expected supremum of fractional Brownian motion using coupling

Abstract.

We derive a new theoretical lower bound for the expected supremum of drifted fractional Brownian motion with Hurst index over (in)finite time horizon. Extensive simulation experiments indicate that our lower bound outperforms the Monte Carlo estimates based on very dense grids for . Additionally, we derive the Paley-Wiener-Zygmund representation of a Linear Fractional Brownian motion and give an explicit expression for the derivative of the expected supremum at in the sense of recent work by Bisewski, Dȩbicki & Rolski (2021).

Key words and phrases:

fractional Brownian motion; expected value of supremum; expected workload; lower bound2020 Mathematics Subject Classification:

60G22, 60G15, 68M201. Introduction

Let , where be fractional Brownian motion with Hurst index (or -fBm), that is, a centred Gaussian process with the covariance function

| (1) |

In this manuscript we consider the expected supremum of fractional Brownian motion with drift over time horizon , that is

Even though the quantity is so fundamental in the theory of extremes of fractional Brownian motion, its value is known explicitly only in two cases: and , when is a standard Brownian motion and a straight line with normally distributed slope, respectively. For general , the value of could, in principle, be approximated using Monte Carlo methods by simulation of an fBm on a dense grid, i.e.

where . However, this approach can lead to substantial errors. In [8, Theorem 3.1] it was proven that the absolute error behaves roughly (up to logarithmic terms) like , as . This becomes problematic, as , when additionally ; see also [16]. Similarly, the error is expected to be large, when is large, since in that case more and more points are needed to cover the interval . Surprisingly, even as one may also encounter problems because then for all , see [17, 4]. Since the estimation of is so challenging, many works are dedicated to finding its theoretical upper and lower bounds. The most up-to-date bounds for can be found in [8, 9], see also [23, 26] for older results. The most up-to-date bounds for can be found in [4].

In this work we present a new theoretical lower bound for for general , (including the case , ). Our approach is loosely based on recent work [5], where the authors consider a coupling between -fBms with different values of on the Mandelbrot & van Ness field [18]. The idea of considering such a coupling dates back at least to [20, 3], who introduced a so-called multi-fractional Brownian motion. In this manuscript, we consider a coupling provided by the family of Linear Fractional Stable motions with , see [21, Chapter 7.4] which we will call the linear fractional Brownian motion. Conceptually, our bound for is very simple — it is defined as the expected value of the -fBm at the time of maximum of the corresponding -fBm (i.e. Brownian motion). The difficult part is the actual calculation of this expected value. This is described in detail in Section 3. Our new lower bound, which we denote , is introduced in Corollary 2.

Our numerical experiments show that performs exceptionally well in the subdiffusive regime . In fact, the numerical simulations indicate that gives a better approximation to the ground truth that the Monte Carlo estimates with as many as gridpoints, i.e.

for all . We emphasize that is the theoretical lower bound for , which makes the result above even more surprising.

The manuscript is organized as follows. In Section 2 we define the Linear Fractional Brownian motion and establish its Paley-Wiener-Zygmund representation. We also recall the formula for the joint density of the supremum of drifted Brownian motion and its time and introduce a certain functional of the 3-dimensional Bessel bridge, which plays an important role in this manuscript. In Section 3 we show our main results; our lower bound is presented in Corollary 2. Additionally, in Corollary 4 we present an explicit formula for the derivative , which was given in terms of definite integral in [5]. The main results are compared to numerical simulations in Section 4, where the results are also discussed. The proofs of main results are given in Section 5. In Appendix A we recall the definition and properties of confluent hypergeometric functions. Finally, in Appendix B we enclosed various calculations needed in the proofs.

2. Preliminaries

2.1. Linear Fractional Brownian motion

In this section we introduce the definition of the Linear Fractional Brownian motion and establish its Paley-Wiener-Zygmund representation.

Let be a standard two-sided Brownian motion. For let

| (2) |

Note that in case we have , . Furthermore, for , with put

| (3) |

Finally, for any , we define the (standardized) Linear Fractional Brownian motion , where

| (4) |

Now, according to [25, Lemma 4.1] we have

| (5) |

where

| (6) |

We emphasize that is Gaussian field with well-known covariance structure, i.e. for each , the value of

| (7) |

is known, see [25, Theorem 4.1] (we do not write it here because the formula is quite involved and we don’t use it). While for each , the process is an -fBm (therefore its law is independent of the choice of the pair ), the covariance structure (7) of the entire field varies for different ; see [25]. In orther words, different choices of will provide different couplings between the fBms. The case corresponds to the fractional Brownian field introduced by Mandelbrot & van Ness in [18] (note that in this case we have ). We remark that the representation (4) was recently rediscovered in [14].

Following [5], we use the Paley-Wiener-Zygmund (PWZ) representation of processes and defined in (2)

| (8) |

Proposition 1.

is a continuous modification of .

Now let us define the counterpart of the process from Eq. (3), that is, for every define stochastic process , where

| (9) |

Corollary 1.

is a continuous modification of .

For completeness, we give a short proof of Proposition 1 below.

Proof of Proposition 1.

In [5, Proposition 2] it was shown that is a continuous modification of . Showing the sample path continuity of is analogous to showing sample path continuity of which was done in [5, Proposition 3]. Finally, due to [5, Lemma 2], for any we have

This shows that is a modification of and concludes the proof. ∎

2.2. Joint density of the supremum of drifted Brownian Motion and its time

In this section we recall the formulae for the joint density of the supremum of (drifted) Brownian motion over and its time due to [24]. This section relies heavily on [5, Section 2].

Let be a standard Brownian motion. For any and consider the supremum of drifted Brownian motion its time, i.e.

| (10) |

and its expectations

| (11) |

In the following, let be the joint density of , i.e.

| (12) |

When and then

| (13) |

for and . When , then the pair is well-defined with

| (14) |

for and .

Proposition 2.

It holds that

-

•

if and then

-

•

if then and ;

-

•

if then and .

Proof.

The fomula for can be obtained from the Laplace transform of , see formulas 1.1.1.3 and 2.1.1.3 in [7]. The formula for could similarly be obtained from the Laplace transform of . However, the numerical calculations indicate that the formulas for Laplace transforms 1.1.12.3, 2.1.12.3 in [7] are incorrect. Therefore, we provide our own derivation of in Appendix B. ∎

Finally, we introduce a certain functional of Brownian motion, which plays an important role in this manuscript. It is noted that its special case () appeared in [5, Eq. (11)]. In what follows let

| (15) |

Following [5], we recognize that the conditional distribution of the process given follows the law of the generalized 3-dimensional Bessel bridge from to . Therefore, can be thought of an expected value of a certain ‘Brownian area’, see [13] for a survey on Brownian areas. It turns out that the function can be explicitly calculated. In the following, is the Tricomi’s confluent hypergeometric function, see (33) in Appendix A.

Lemma 1.

If , and , then

3. Main results

Let be a standard, two-sided Brownian motion. Consider the PWZ representation of LFBM with parameter , that is , where

with defined in (9) and defined in (5). Then, according to Corollary 1, is a continuous modification of and therefore, for each fixed , is a fractional Brownian motion with Hurst index . It is noted that all processes live on the same probability space and are, in fact, defined pathwise for every realization of the driving Brownian motion.

For each , and define

| (17) |

which is the supremum of drifted Brownian motion with paremeter and its location. Now we define the expected expected values of these random variables

| (18) |

Recall that the random variables and their expectations above were already defined for in Eq. (10) and Eq. (11). Notice how and do not dependent on , because as vary, the joint law of the supremum of its location does not change. Now, for each define

| (19) |

which, in words, is the expected value of drifted fBm with parameter evaluated at time of the supremum of the driving Brownian motion. Clearly, this yields

and for every . We further maximize our lower bound by taking the supremum over all feasible pairs and define

| (20) |

It turns out that the value of can be found explicitly. Before showing the formula in Proposition 4 we define a useful functional

| (21) |

In the following is the incomplete Gamma function, see (41) in Appendix A.

Proposition 3.

It holds that

| (22) |

Finally, we can show that

We emphasize the the values of functions and are known explicitly, see Proposition 3 and Proposition 2 respectively. Additionally, we write down the formulas for in two special cases below.

-

•

if , then ;

-

•

if , then .

Interestingly, we can further improve the lower bound derived in Proposition 4 simply by using self-similarity of fractional Brownian motion, i.e. for any we have

which also holds for and , i.e. . Therefore, we present our final result in the corollary below. In the following, let

| (25) |

Corollary 2.

For any , , and it holds that

In particular,

-

(i)

if , then ;

-

(ii)

if , then .

It is noted that . In general, the solution to the optimization problem (25) can be found numerically because the explicit formula for is known, cf. Proposition 4.

3.1. Secondary results

Before ending this section, we would to present two immediate corollaries, which are implied by our main results. First result describes the asymptotic behavior of , as while the second result pertains the evaluation of the derivative of the expected supremum at .

Behavior of , as .

Using the formula for from Corollary 2(i), it is easy to obtain the following result.

Corollary 3.

It holds that

The asymptotic lower bound in Corollary 3 is over 5 times larger than the corresponding bound derived in [8, Theorem 2.1(i)], where it was shown that for all . Moreover, together with [9, Corollary 2], our result implies that

for all small enough. Determining whether the limit , as exists and finding its value remains an interesting open question.

Derivative of the expected supremum

Using the formula for in Proposition 3 and recent findings in [5], we are able to explicitly evaluate the derivative of the expected supremum at . The proof of [5, Theorem 1] implies that

Therefore, using the formula for from Proposition 4, we find that . In the following let .

Corollary 4.

It holds that

It is noted that the continuous extension of the function to and to agrees with Corollaries 1(i) and 1(ii) from [5], respectively.

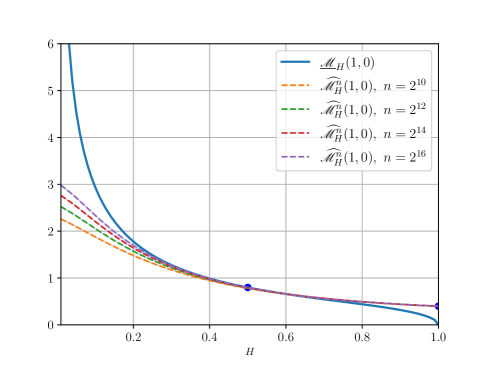

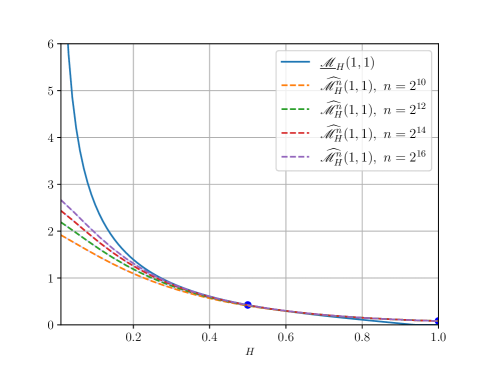

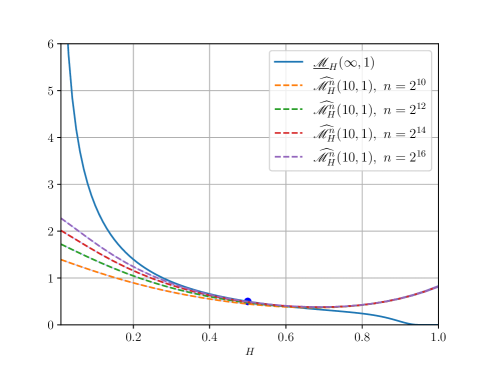

4. Numerical experiments

In this section we compare our theoretical lower bound with Monte Carlo simulations.

In our experiments we use the circulant embedding method (also called Davies-Harte method [10]) for the simulation of fBm; see also [11] for various methods of simulation. Experiments were perfomed in Python and the code of the Davies-Harte method was adapted from [15, Section 12.4.2]. The method relies on the simulation of fBm on an equidistant grid of points, that is . The resulting estimator has the expected value

where . Clearly, , i.e. on average, the Monte Carlo estimator underestimates the ground truth, as the supremum is taken over a finite subset of . Nonetheless, as we should observe that .

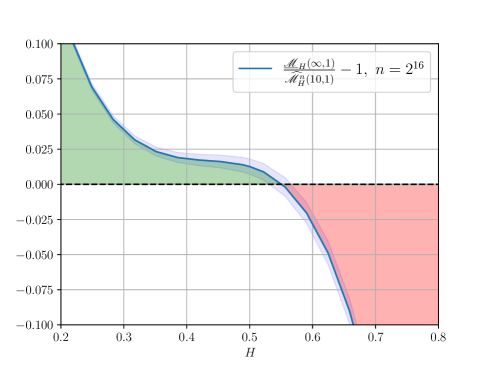

In our experiments, we consider three different cases (i) , , (ii) , , and finally (iii) , . In each case the theoretical lower bound is compared with the corresponding simulation results for based on independent runs of Davies-Harte algorithm; in case (ii) we took because it is not possible to simulate the process over the infinite time horizon.

The results corresponding to cases (i)–(iii) are displayed in Figures 1–3. Each curve is surrounded by its confidence interval depicted as a shaded blue area. The results are presented in two different scales. We interpret the results on the figures on the left and on the right separately, in the following two paragraphs.

In the figures on the left, we compare the bound with the simulation results on the ‘high-level’ for all . The blue dots at and correspond to the known values of and respectively; the value at in Figure 3 is not shown because . As expected, the value of is increasing, as is increasing. The simulation results seem to roughly agree with the ground truth at and , while the lower bound, agrees with the ground truth at by the definition, i.e. . On the ‘high-level’, we can conclude that the lower bound

-

-

is close to the simulation results for all ,

-

-

perfoms much better than the simulation results as , and

-

-

performs worse when (in fact, the bound seems to converge to there).

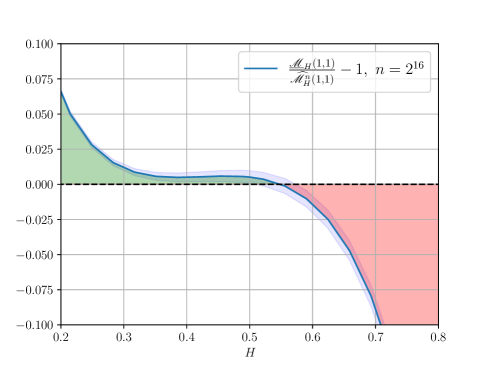

In the figures on the right, we compare the bound with the simulation results in the region . We plotted the relative error between the theoretical lower bound and the simulation results based on gridpoints, that is

It is noted that if relative error is positive, then the theoretical lower bound yields a better approximation to the ground truth than the Monte Carlo method, which is indicated by the green area below the curve on the plot. In this sense, we see that the theoretical lower bound outperforms the Monte Carlo simulations for in all three cases (i)–(iii). We remark that the value of the relative error at equals approximately in Figure 1 and in Figure 2, which roughly agrees with [6, Corollary 4.3], which states that

see also [2, Theorem 2] in case .

5. Proofs

In the following, let

| (26) |

Lemma 2.

If and then

Proof of Lemma 2.

For breviety we write and put . See that according to the PWZ representation of in Eq. (8), we have

| (27) |

where in the second line we simply substituted . Furthermore, notice that for any , the PWZ representation of from Eq. (8) can be rewritten as

Since Brownian motion is centred and it has independent increments, therefore is independent of and the expected value of each term in the second and third line above is equal to . This yields

After substituting we find that the above equals

Now, let be the time-reverse of process , that is and let be its time of the supremum over . Notice that we must have . After substituting for , we find that

Finally, we notice that , that is is has the law of drifted Brownian motion with drift . Comparing the above with Eq. (27) for concludes the proof. ∎

In light of the result in Lemma 2 the function can be expressed using , which justifies our notation , cf. (21). Before proving Proposition 3, we need to establish a certain continuity property of the argmax functional of Brownian motion. In what follows, let

be the argmax functional of drifted Brownian motion, see also the definition (17).

Lemma 3.

It holds that

-

(i)

a.s. for any , and

-

(ii)

a.s. for any .

Proof.

Let . It is easy to see that the trajectories converge uniformly to , as , hence the argmax functionals also converge, see e.g. [22, Lemma 2.9], which concludes the proof of item (i). Furthermore, since is almost surely finite, then there must exist some (random) such that for all , which implies item (ii). ∎

Proof of Proposition 3.

Let and observe that

therefore , which agrees with Proposition 2 (note that the error function is a special case of the incomplete Gamma function, cf. (45)).

Till this end, let . For breviety denote and let . Till this end, consider the case . Recall that from (27) we have

Now, we have

We now recognize that the above equals to , with defined in Eq. (15). Using Lemma 1 we obtain

where

The joint density of the pair is well-known, see (13) in Section 2.2 therefore both functions and can be written as definite integrals and calculated. In fact, we have

| (28) |

The derivation of Eq. (28) is purely calculational and is provided in Appendix B. This ends the proof in case , .

In order to derive the formula for in the remaining two cases (i.e. , and , ), we could redo the calculations in Eq. (28) with appropriate density functions for the pair , see (14) and (13). However, it is not necessary, as it suffices to show that the function is continuous at and .

Let , . Using the fact that , as , it can be seen that

Showing that would therefore conclude the proof in this case. By the definition, we have . Since is continuous at , therefore it suffices to show

| (29) |

as . Using Proposition 1 and Lemma 3(i) we obtain

Moreover, for any and all we have

which has finite expectation. Therefore, by Lebesgue dominated convergence we can conclude that the limit (29) holds, which ends the proof in this case.

Let , . It is easy to see that

Analogously to the proof of the previous case, it suffices to show

| (30) |

as . Using Proposition 1 and Lemma 3(ii) we find that

Moreover, since the mapping is nondecreasing, it holds that

and the right-hand-side above has a finite expectation. Using Lebesgue dominated convergence we conclude that the limit (30) holds, which ends the proof. ∎

Proof of Proposition 4.

From the definition of in (19),

In light of Lemma 2, for we have

| (31) |

We will now show that Eq. (31) holds also in case , . Using Proposition 1 and Lemma 3(ii) we find that

Now we have the bound , which is integrable, hence we can conclude that

Furthermore, from Proposition 3 and Proposition 2 it is clear that and as , respectively. Hence,

which concludes the proof that Eq (31) holds for all admissible pairs .

Appendix A Special functions

All of definitions, formulae and relations from this section can be found in [1].

Confluent hypergeometric functions

For any and we define Kummer’s (confluent hypergeometric) function

| (32) |

where is the rising factorial, i.e.

Similarly, for any and we define Tricomi’s (confluent hypergeometric) function, i.e.

| (33) |

When , then Kummer’s function can be represented as an integral

| (34) |

and similarly, for , Tricomi’s function can be represented as an integral

| (35) |

Moreover, the following Kummer’s transformations hold

| (36) | ||||

| (37) |

and the following recurrence relations hold:

| (38) | ||||

| (39) |

In this manuscript, we often use the following integral equality. Let and , then

| (40) |

which can be verified using [12, 7.613-1].

Incomplete Gamma function

For any , we define the upper and lower incomplete Gamma functions respectively

| (41) |

so that , where the standard Gamma function . Using integration by parts we obtain the following useful recurrence relation

| (42) |

Notice that as , the above is reduced to the well-known recurrence relation for the Gamma function, that is . Finally, we note that can be expressed in terms of the confluent hypergeometric function:

| (43) |

Error function

For we define the error function and complementary error function respectively:

| (44) |

The error function can be expressed in terms of the incomplete Gamma function, and as such, in light of (43), also in terms of the hypergeometric function:

| (45) |

Appendix B Calculations

Derivation of the formula for in Proposition 2.

The derivation in cases , and , is straightforward using Eq. (14) and Eq. (13) respectively. Till this end assume that and . We have

see e.g. 2.1.12.4 in [7]. We now have

where we substituted and put . Now, we have

| (46) |

where

Using the fact that and applying substitution , we obtain

In the following, let

where the first integral can be calculated using substitution . Then

Now, applying substitution and formula [19, 4.3.20] we obtain

Further, using integration by parts we obtain

In the following let

which can be easily calculated using substitution . Then

and therefore

| (47) |

In the following, let

where the first integral was calculated using integration by parts. Using the identity we find that

We will now find the value of the integral . See that After applying substitution we obtain

After integration by parts we find that

therefore

After simple algebraic manipulations this yields

| (48) |

Finally, after plugging in the expressions for , and calculated in (47) and (48) into Eq. (46) we obtain

which concludes the proof. ∎

Continuation of the proof of Lemma 1.

First we show that

| (49) |

where , which generalizes [5, Proposition 1] in case . From (49) we have

where , and . We now apply substitution , then , which gives us

which after substitution yields (49). from [5, Eq. (54)] we find that for any :

Therefore,

| (50) |

where we put and

Using (35) we find that

Integration by parts yields

and after applying (35) we find that

The integral is computed analogously to and it equals

Now, after simple algebraic manipulations we obtain

where

Applying the relation (38) to the last term above we obtain

Applying the relation (39) to the first and third terms above we obtain

where in the last equality we applied the Kummer’s transformation (37). This concludes the proof. ∎

Lemma 4.

If and , then

Proof.

Using (36) we find that therefore, using (35) we have

After substitution we obtain

where

Now, can be easily found from the definition of the Beta function, while can be found using (34), hence

The integral is now computed using the error function representation from (45) and the result in (40), i.e.

Finally, using (43) we obtain

which ends the proof. ∎

Proof of Eq. (28).

Recall that , and . We will first show that

| (51) |

The joint density of the pair is well-known, see (13) in Section 2.2. We have , where

hence

where in the last line we substituted . It can be seen that the definite integral with respect to equals to because for every we have

We have established that Eq. (51) holds and therefore it is left to calculate the integral

Consider the innermost integral. After substituting we find that

Using Lemma 4 we obtain

| (52) |

where

It is left to calculate each of the integrals above. Using substitution and putting we can find that

Let us define:

Slightly abusing notation, for breviety we write and . We then have

and the quantities , can be expressed as

Before we calculate the values of we introduce two useful functions, for :

The values of these functions were found by applying relation (43) and finding the value of the integral using (40). Now, integration by parts yields

where in the last line we used the recurrence relation for the incomplete Gamma function in Eq. (42). Now, notice that for any :

Therefore, integration by parts yields

Finally, this gives us

Using analogous methods, we find that

Through straightforward algebraic manipulations and applying simple recurrence relation (42), we finally obtain

which concludes the proof. ∎

Acknowledgements

The author would like to thank Prof. Krzysztof Dȩbicki and Prof. Tomasz Rolski for helpful discussions. Krzysztof Bisewski’s research was funded by SNSF Grant 200021-196888.

References

- [1] Milton Abramowitz, Irene A Stegun, and Robert H Romer. Handbook of mathematical functions with formulas, graphs, and mathematical tables, 1988.

- [2] Søren Asmussen, Peter Glynn, and Jim Pitman. Discretization error in simulation of one-dimensional reflecting Brownian motion. Ann. Appl. Probab., 5(4):875–896, 1995.

- [3] Albert Benassi, Daniel Roux, and Stéphane Jaffard. Elliptic gaussian random processes. Revista matemática iberoamericana, 13(1):19–90, 1997.

- [4] Krzysztof Bisewski, Krzysztof Dȩbicki, and Michel Mandjes. Bounds for expected supremum of fractional Brownian motion with drift. J. Appl. Probab., 58(2):411–427, 2021.

- [5] Krzysztof Bisewski, Krzysztof Dȩbicki, and Tomasz Rolski. Derivatives of sup-functionals fo fractional brownian motion evaluated at H=1/2. arXiv preprint arXiv:2110.08788, 2021.

- [6] Krzysztof Bisewski and Jevgenijs Ivanovs. Zooming-in on a lévy process: failure to observe threshold exceedance over a dense grid. Electronic Journal of Probability, 25:1–33, 2020.

- [7] Andrei N. Borodin and Paavo Salminen. Handbook of Brownian motion—facts and formulae. Probability and its Applications. Birkhäuser Verlag, Basel, second edition, 2002.

- [8] Konstantin Borovkov, Yuliya Mishura, Alexander Novikov, and Mikhail Zhitlukhin. Bounds for expected maxima of Gaussian processes and their discrete approximations. Stochastics, 89(1):21–37, 2017.

- [9] Konstantin Borovkov, Yuliya Mishura, Alexander Novikov, and Mikhail Zhitlukhin. New and refined bounds for expected maxima of fractional Brownian motion. Statist. Probab. Lett., 137:142–147, 2018.

- [10] Robert B Davies and DS Harte. Tests for hurst effect. Biometrika, 74(1):95–101, 1987.

- [11] Ton Dieker. Simulation of fractional brownian motion. Master’s thesis, Department of Mathematical Sciences, University of Twente, 2004.

- [12] Izrail S. Gradshteyn and Iosif M. Ryzhik. Table of integrals, series, and products. Elsevier/Academic Press, Amsterdam, eighth edition, 2015. Translated from the Russian, Translation edited and with a preface by Daniel Zwillinger and Victor Moll, Revised from the seventh edition [MR2360010].

- [13] Svante Janson. Brownian excursion area, wright’s constants in graph enumeration, and other brownian areas. Probability Surveys, 4:80–145, 2007.

- [14] Nino E Kordzakhia, Yury A Kutoyants, Alexander A Novikov, and Lin-Yee Hin. On limit distributions of estimators in irregular statistical models and a new representation of fractional brownian motion. Statistics & Probability Letters, 139:141–151, 2018.

- [15] Dirk P Kroese and Zdravko I Botev. Spatial process simulation. In Stochastic geometry, spatial statistics and random fields, pages 369–404. Springer, 2015.

- [16] Vitalii Makogin. Simulation paradoxes related to a fractional Brownian motion with small Hurst index. Mod. Stoch. Theory Appl., 3(2):181–190, 2016.

- [17] Artagan Malsagov and Michel Mandjes. Approximations for reflected fractional Brownian motion. Phys. Rev. E, 100(3):032120, 7, 2019.

- [18] Benoit B. Mandelbrot and John W. Van Ness. Fractional Brownian motions, fractional noises and applications. SIAM Rev., 10:422–437, 1968.

- [19] Edward W. Ng and Murray Geller. A table of integrals of the error functions. J. Res. Nat. Bur. Standards Sect. B, 73B:1–20, 1969.

- [20] Romain-François Peltier and Jacques Lévy Véhel. Multifractional Brownian motion: definition and preliminary results. PhD thesis, INRIA, 1995.

- [21] Gennady Samorodnitsky and Murad S. Taqqu. Stable non-Gaussian random processes. Stochastic Modeling. Chapman & Hall, New York, 1994. Stochastic models with infinite variance.

- [22] Emilio Seijo and Bodhisattva Sen. A continuous mapping theorem for the smallest argmax functional. Electron. J. Stat., 5:421–439, 2011.

- [23] Qi-Man Shao. Bounds and estimators of a basic constant in extreme value theory of Gaussian processes. Statist. Sinica, 6(1):245–257, 1996.

- [24] Lawrence A. Shepp. The joint density of the maximum and its location for a Wiener process with drift. J. Appl. Probab., 16(2):423–427, 1979.

- [25] Stilian A. Stoev and Murad S. Taqqu. How rich is the class of multifractional Brownian motions? Stochastic Process. Appl., 116(2):200–221, 2006.

- [26] Ceren Vardar-Acar and Hatice Bulut. Bounds on the expected value of maximum loss of fractional brownian motion. Statistics & Probability Letters, 104:117–122, 2015.