Robustness and risk management via distributional dynamic programming

Abstract

In dynamic programming (DP) and reinforcement learning (RL), an agent learns to act optimally in terms of expected long-term return by sequentially interacting with its environment modeled by a Markov decision process (MDP). More generally in distributional reinforcement learning (DRL), the focus is on the whole distribution of the return, not just its expectation. Although DRL-based methods produced state-of-the-art performance in RL with function approximation, they involve additional quantities (compared to the non-distributional setting) that are still not well understood. As a first contribution, we introduce a new class of distributional operators, together with a practical DP algorithm for policy evaluation, that come with a robust MDP interpretation. Indeed, our approach reformulates through an augmented state space where each state is split into a worst-case substate and a best-case substate, whose values are maximized by safe and risky policies respectively. Finally, we derive distributional operators and DP algorithms solving a new control task: How to distinguish safe from risky optimal actions in order to break ties in the space of optimal policies?

Keywords: robust Markov decision process, distributional reinforcement learning, average value-at-risk, coherent risk measure, linear programming

1 Introduction

This paper is concerned with robust sequential decision making in an uncertain environment, modeled by a Markov decision process (MDP). In the classical setting, the decision maker is looking for a strategy (or “policy”) that is optimal in terms of a risk-neutral objective function. Typically, this objective is the expected value of some random cumulative return, accounting for both immediate and future rewards. The dynamic programming (DP) approach comes with practical algorithms to evaluate and optimize such objective functions, given the knowledge of the environment’s dynamics (see Puterman, 2014). DP is a popular framework for many applications ranging from computer programming to economics and inventory management: we refer to Bertsekas et al. (2000) for an overview. Reinforcement learning (RL) aims at solving the same problem as DP when the dynamical model is unknown: the learner only observes trajectories sampled from the MDP (see Sutton and Barto, 2018).

An inherent feature of standard dynamic programming procedures and most RL algorithms is their risk-neutrality, meaning that they do not differentiate between strategies with the same expected return but different levels of risk (for instance, different variances). As a vanilla example, getting with probability (w.p.) is safer than getting w.p. and w.p. , though both scenarios are equivalent in expectation. For this reason, standard DP and RL methods need to be adjusted to take risk into account, for instance by considering alternative objective functions such as mean minus variance in Mannor and Tsitsiklis (2011), conditional value-at-risk (“CVaR” in short) in Osogami (2012) and Chow et al. (2015), or Chernoff functionals in Moldovan and Abbeel (2012).

A more general approach, first proposed by Morimura et al. (2010) and Morimura et al. (2012), is to handle the whole distribution of the long-term return in a dynamic programming framework, not just its expectation or some risk measure. This approach is fittingly called distributional and is the main focus of our work. Recently, Bellemare et al. (2017) introduced the distributional reinforcement learning (DRL) framework and proposed the C51 algorithm, achieving state-of-the-art performance in playing video games on the Atari 2600 benchmark (Bellemare et al., 2013). Rowland et al. (2018) analyzed C51 with the Cramér distance and Bellemare et al. (2019) described another DRL algorithm that approximates distributions using the same metric. Many other DRL algorithms were proposed such as QR-DQN (Dabney et al., 2018b) and IQN (Dabney et al., 2018a) both based on quantile regression or ER-DQN in Rowland et al. (2019) based on expectile estimation. Most of these DRL approaches rely on summarizing distributions by atoms instead of the single state-action value function in classic RL or DP. Although there are empirical evidence of the regularizing effect of learning several atoms in a function approximation setup (Lyle et al., 2019), finding an intuitive explanation for these quantities is still an open problem to the best of our knowledge. Hence, it seems natural to ask the following question: “Is there any meaningful interpretation of these atoms?”. The answer provided by this paper is “Yes, a robust MDP interpretation!”.

The robust MDP framework is a seemingly unrelated way of dealing with uncertainties in sequential decision making, with the main idea being the optimization of a worst-case objective function subject to an uncertainty set over the true environment parameters (Iyengar, 2005, Nilim and El Ghaoui, 2005). In this work, we show that the usual notion of robustness in MDPs can be directly derived from the distributional Bellman operator combined with a carefully chosen projection to a family of distributions involving only two atoms: this is our main contribution. Additionally, we show that once all optimal policies have been identified and isolated from suboptimal ones (by solving classical DP), our methodology allows a further discrimination among the space of optimal policies, by distinguishing safe from risky optimal actions.

The rest of the paper is organized as follows. After providing the necessary technical background in Section 2, we introduce our framework for robust distributional dynamic programming in Section 3 and give an interpretation of the resulting value functions from the perspective of risk-measure theory in Section 4. Finally, in Section 5, we propose dynamic programming methods for tiebreaking in the space of optimal policies to favor safe or risky policies, and provide some numerical illustration to our results in Section 6. The paper is concluded with Section 7.

Notations.

Throughout the paper, we denote by the all-ones vector (the dimensionality will always be clear from the context). We let be the set of probability measures on with bounded support, and the set of probability mass functions on any countable set , whose cardinality is denoted by . The support of any discrete distribution is: . The cumulative distribution function (CDF) of a real-valued random variable is the mapping (), and we denote its generalized inverse distribution function (a.k.a. quantile function) by 111We will often express the expectation of with : Lemma 3 (in Appendix A) recalls the classic formula .. For any probability measure and measurable function , the pushforward measure is defined for any Borel set by . In this work, we will only encounter the affine case (with ) for which and if , or is the Dirac measure at if . Lastly, for two probability measures in , means that is absolutely continuous with respect to (i.e. ) and is the Radon-Nikodym derivative.

2 Background

This section presents basic technical background on Markov decision processes, robust MDPs, and distributional dynamic programming with -Wasserstein projections.

2.1 Markov decision process

In this article, we study one of the most fundamental models for sequential decision-making problems: discounted Markov decision processes (MDPs) with finite state and action spaces. Here we only describe the most essential elements of this framework and refer to the classic textbook of Puterman (2014) for details. A Markov decision process is described by the tuple with finite state space , finite action space , transition kernel , reward function and discount factor . An MDP describes a sequential process where in each round of interaction, the decision-making agent chooses an action while the environment occupies some state , then the next state is sampled from the distribution and the agent gets the reward . A stationary Markovian policy maps any state to a distribution over the actions . We denote by the set of stationary Markovian policies. The two major classes of problems in an MDP are the following.

The policy evaluation task:

the goal is to assess the quality of a policy in terms of expected return, through its state-action value function defined for all as follows,

where and . The Bellman equation verified by is

The corresponding value function is .

The control task:

find an optimal policy that simultaneously maximizes the values across all states,

where satisfies the Bellman optimality equation

Moreover , where the maximizing actions include the support of any optimal policy, in any state:

Equivalently, (resp. ) can be seen as the unique fixed point of the Bellman operator (resp. Bellman optimality operator), which is a -contraction222A function mapping a metric space to itself is called a -contraction if it is Lipschitz continuous with Lipschitz constant . in supremum norm333The supremum norm of any function is . (Bertsekas and Tsitsiklis, 1996). The dynamic programming (DP) approach consists in recursively applying these contractive operators until convergence to their fixed points (see Bellman, 1966). In Section 2.3, we recall how the same idea can be extended to entire probability distributions, not just expected values.

2.2 Robust MDPs

Sometimes, there may be uncertainty in the transition probabilities, for instance when they are estimated from noisy observations, or when the state transitions can be influenced by an external adversary. The robust MDP framework models this situation with an uncertainty set consisting of a family of candidate transition kernels . The worst-case value function of a policy with respect to this set is defined for each state as

| (1) |

where denotes the value function in the MDP with kernel . Then, given an initial state , the goal is to find a robust optimal policy satisfying

This setting has been extensively studied in the literature under various assumptions for the uncertainty set. In Iyengar (2005) and Nilim and El Ghaoui (2005), the uncertainty set is a Cartesian product over state-action pairs:

In other words, each component can be chosen independently among the set in the infimum in Eq. (1). This is the -rectangularity assumption, under which there exists a robust optimal policy that is stationary, Markovian and deterministic, that can be computed by robust dynamic programming. Similarly, the -rectangularity assumption is considered in Wiesemann et al. (2013):

Under this weaker assumption, there is a stationary Markovian robust optimal policy, but (unfortunately) it may not be deterministic. More general assumptions have also been studied. Factor matrix uncertainty sets along with the so-called “-rectangularity” structure are investigated in Goyal and Grand-Clement (2018). This alternative hypothesis is proved to generalize the -rectangulariy condition, and to produce as well a deterministic robust optimal policy. In Mannor et al. (2016), the authors consider a generalization of -rectangularity, called -rectangularity. In section 4, we show that our distributional approach reformulates as a robust MDP outside of any of the aforementioned rectangulariy assumptions. Further in section 5, our setting leads to a deterministic robust optimal policy. But first, we need to recall the definition of the distributional Bellman operator, which is the main tool to handle distributions in MDPs.

2.3 The distributional Bellman operator

The distributional Bellman operator (DBO) was introduced in Morimura et al. (2010) and Morimura et al. (2012) for CDFs, in Bellemare et al. (2017) with random variables; here we recall its formulation based on pushforward measures from Rowland et al. (2018). On a high level, the DBO takes as input a distribution function that models the collection of return distributions indexed by state-action pairs, and returns another distribution function corresponding to the distribution of returns after being pushed through the transition dynamics. The more formal definition is the following:

Definition 1

(Distributional Bellman operator). Let . The distributional Bellman operator is defined for any distribution function by

In particular, the DBO is mixture-linear: for all and ,

It was proved in Bellemare et al. (2017) that is a -contraction in the maximal -Wasserstein metric444We recall that the -Wasserstein distance () between two probability distributions on with CDFs is defined as , and for as .

at any order . Akin to the “non-distributional” case, we know from Banach’s fixed point theorem that iterating the distributional Bellman operation, namely (starting from an arbitrary initial ), defines a sequence that converges exponentially fast to the unique fixed point . This equality is called the distributional Bellman equation. The fixed point is the collection of the probability laws of the returns:

| (2) |

Nevertheless, it may be hard in practice to compute , as it requires to deal with general distributions. In the example below, we focus on a basic family of probability distributions: the atomic distributions, over which the DBO is stable.

Example 1

(“Atomic fission”). Let be an atomic distribution function with

where , , . Then for any ,

which is still an atomic distribution, but with up to times more particles.

Motivated by Example 1, several distributional RL algorithms are based on atomic distributions: they apply —which multiplies the number of particles by a factor up to —followed by a projection to bring the number of particles back to a fixed budget .

Projected operators. In Dabney et al. (2018b), every distribution with CDF is projected to a discrete distribution with uniform probabilities over evenly spread quantiles:

This specific choice comes from minimizing the -Wasserstein distance between and such average of Dirac measures. Notice that in the monoatomic case , this approach summarizes an entire distribution by a single scalar: the median . Interestingly, this suggests that these projected operators are not an appropriate generalization of the classical Bellman operators that involve the expectation of the return instead of the median.

This issue can be addressed by using the -Wasserstein distance for projection:

Indeed, this -error is a quadratic function in , whose minimum is attained at the mean value (by Lemma 3). Thus, combining the distributional Bellman operators with a 2-Wasserstein projection correctly recovers the classical DP operators in the special monoatomic case . More formally, it is easy to check that averaging after applying the DBO to a collection of Dirac measures, is nothing but the usual policy evaluation update:

This simple observation motivated -projections in Achab (2020) (see chapter VII therein), who derived multiatomic variants of the Temporal-Difference and Q-learning algorithms. As shall be seen in the next section, this choice leads to a natural extension of non-distributional DP with closed-form updates even for more than one atom.

3 Risk-sensitive distributional dynamic programming with 2-Wasserstein projections

We now turn to describing our main contribution: a framework for risk-sensitive dynamic programming using -projected distributional Bellman operators, arising as a special case of the distributional DP framework described in the previous section using projections onto the set of diatomic distributions with fixed non-uniform weights. As we will show, projection to this set corresponds to calculating the well-studied coherent risk measure of average value-at-risk or “AVaR”555AVaR and CVaR are two different names for the same quantity (Chun et al., 2012). (see Rockafellar et al., 2000, Rockafellar and Uryasev, 2002 and Acerbi and Tasche, 2002). We start with the formal definitions below.

Definition 2

(Average value-at-risk). Let and with CDF . The left and right AVaRs of at respective levels and are defined as:

Definition 3

(Diatomic distribution function). Given and some bidimensional function , we call “diatomic distribution function” and denote the following collection of diatomic distributions:

In other words, we associate a mixture of two Dirac masses to each state-action pair . As a comparison, this doubles the space complexity of the usual DP framework that uses a single action-value function in place of . Although we focus on distributions made of two atoms, most of the techniques used in this paper easily extend to any number of atoms.

In order to respect our diatomic constraint, we apply successively the distributional Bellman operator and a projection onto the space of diatomic distribution functions. More precisely, every time the operator is applied to some , we use the -Wasserstein-projection to approximate by another collection of distributions in the same family . The following lemmas give a tractable method for evaluating the resulting operator.

Lemma 1

(From -projection to AVaR). Let and . Then, there exists a unique couple minimizing the -Wasserstein approximation error between and any diatomic proxy. In addition, this best diatomic approximation is given by the left and right AVaRs of , at levels and respectively:

Proof For any with , first notice that the CDF and the quantile function of the diatomic distribution are given by:

By definition of the -Wasserstein distance, we have:

where the first term (which only depends on ) rewrites:

which is minimized for .

Similarly, the second term is minimal if and only if , which concludes the proof.

The -projection in Lemma 1 appears as a natural and canonical choice:

it is simply an orthogonal projection in the space of quantile functions.

In the following, we will apply it entrywise, i.e. by computing the left and right AVaRs for each of the distributions contained in .

Key observation: discrete AVaR.

Although the AVaR may not be easy to compute for general distributions, luckily our approach only requires it for discrete distributions. Indeed,

| (3) |

is simply a weighted average of Dirac masses. Plus, the AVaR of a discrete distribution comes with a closed-form expression provided below.

Lemma 2

(AVaR of a discrete distribution). Let and be a discrete distribution:

with , , and sorted values .

-

(i)

Closed-form expression: the left and right AVaRs of at respective levels and are

with the empty sum convention .

-

(ii)

Dual representation: denoting and ,

where the infimum and supremum both range over weights such that

Proof (i) Closed-form expression. First denote for each , and . Then, the CDF and quantile function of the discrete distribution are:

which are both step functions. Hence, the right AVaR of at level simply writes:

Observing that the length of the intersection of two intervals and is equal to

concludes the proof.

(ii) Dual representation. If , then .

For , if , then obviously

.

All these different cases coincide with the expression provided in (i) for the left AVaR.

We conclude the proof by observing that and that both the infimum and the supremum in (ii) are attained at the same .

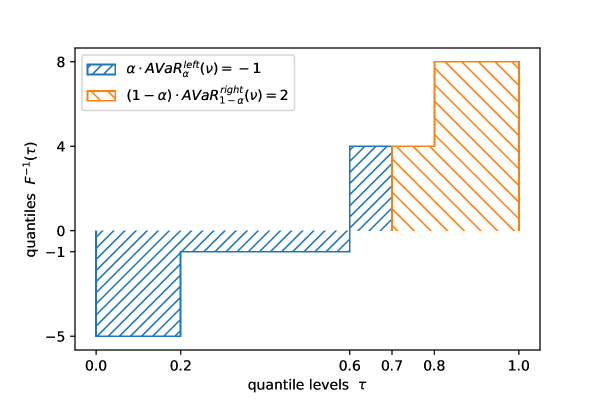

Figure 3 depicts an application of Lemma 2: the left (resp. right) AVaR is obtained by computing the signed area delimited by the staircase curve of the quantile function on the segment (resp. ). The reason why we have the closed-form formula in Lemma 2-(i) is because this area is just the sum of the areas of rectangles.

3.1 Diatomic policy evaluation

Using Lemma 1, our distributional DP method can be formulated with operators that map functions to in the same space. We introduce below the diatomic Bellman operator for the policy evaluation task.

Definition 4

(Diatomic Bellman operator). Let . Given a stationary Markovian policy , the diatomic Bellman operator is defined for all by: such that for each pair ,

We point out that the update rule in Definition 4 can be expressed explicitly as a function of by combining Eq. (3) with Lemma 2-(i). More precisely, one shall set and the sorted values with the corresponding probabilities (). A detailed description of this practical sorting procedure is provided in Algorithm 1.

| SPE Algorithm 1 | Safe/Risky SVI Algorithm 2 | Classic value iteration |

|---|---|---|

Next is a list of some important properties that are satisfied by our new operator . In particular, the property (iii) and its proof show that is not affine, which is in contrast with the classical Bellman operators that are affine.

Proposition 1

(Properties of ). Let , and denote by the two inequalities and . The following properties are verified.

-

(i)

Monotonicity: if , then .

-

(ii)

Distributivity: for any , .

-

(iii)

Concavity/convexity: for , .

-

(iv)

-Contraction in sup norm: .

-

(v)

Fixed point: there exists a unique fixed point , with .

-

(vi)

Averaging property: .

-

(vii)

Relative order: .

Proof (i) Monotonicity. means that for all , and . The monotonicity property follows from combining Eq. (3) with the dual representation Lemma 2-(ii).

(ii) Distributivity. Fix a pair and . The quantile function of is obtained by shifting that of by . The result follows by linearity of the Lebesgue integral.

(iii) Concavity/convexity. Denoting , it holds from Lemma 2-(ii) that

is a concave piecewise linear function of . For the same reason, is a convex piecewise linear function of .

(iv) Contraction. Given that is a -contraction in (Lemma 3 in Bellemare et al., 2017), it is enough to prove that the -projection is a non-expansion in . Let with respective CDFs . Then,

where we used a triangular inequality in the last step.

(v) Fixed point. Consequence of (iii) combined with Banach’s fixed point theorem and the completeness of .

(vi) Average. By Lemma 3: for any distribution with CDF ,

It follows for that solves the classical Bellman equation.

(vii) Relative order. As quantile functions are always non-decreasing,

from which the proof follows for and (and from Lemma 3, the expected value of is equal to ).

In brief, our approach comes with two state-action value functions and , instead of just . Indeed from Proposition 1-(v), we know that our -projected operator has a unique fixed point . Plus, properties such as (vi) and (vii) indicate that this method extends the expected case. Still, so far we have not yet provided any meaningful interpretation of and . The next section shows that these quantities are related to some notion of robustness induced by the policy . By analogy with the AVaR, we call the left Bellman average value-at-risk (left BAVaR) and the right Bellman average value-at-risk (right BAVaR), for a given risk level .

4 Robustness and risk-awareness

The purpose of this section is to interpret the left BAVaR and the right BAVaR from the double perspective of robustness and risk-measure theory.

-

•

Our first interpretation bridges the gap with the robust MDP framework: and are respectively “worst-case” and “best-case” -functions, in a latent augmented MDP with twice more states. To the best of our knowledge, this constitutes the first formal link between the distributional Bellman operator and robust MDPs.

-

•

Our second point states that and are both coherent risk measures.

4.1 Robust MDP with double state space

The purpose of this first interpretation is to unveil the link existing between our distributional approach and robust MDPs, in the special case of -coherent policies.

Definition 5

(-coherent policy). For , we define the set of -coherent policies that satisfy the following condition:

All deterministic policies belong to , as well as the safe/risky policies that are derived in section 5. For such -coherent policies, the BAVaR factorizes to a robust MDP formulation.

Augmented state space.

Let be an -coherent policy. We want to show that and can respectively be interpreted as worst-case and best-case value functions in an augmented MDP, where each state is split into two distinct substates and . We denote the augmented state space by:

| (4) |

which has double size . We consider a decision-maker that only observes his current state in the original state space, not the latent substate (either or ) in the augmented one. For that reason, it is natural to extend the reward function and the policy to the augmented state space without distinguishing the substates: for any transition , and corresponding substates , ,

| (5) |

Refined dynamics.

In the augmented MDP, we constrain the transition probabilities to be consistent with the transition kernel of the original MDP: this characterizes the following dichotomous uncertainty set.

Definition 6

(Dichotomous uncertainty set). Given the original transition kernel and , the dichotomous uncertainty set is the set of transition kernels (in the augmented MDP with double state space ) verifying: for all ,

The inequality constraint in Definition 6 ensures that, starting from substate , the next substates with the same mode are visited in priority compared to those with different mode . All together, these constraints also imply the symmetric inequality: . Interestingly, our new uncertainty set does not fulfil any of the rectangularity assumptions that have been considered in the literature (see subsection 2.2). In Definition 6, we highlight that . Still, the two sets are symmetric: is obtained from by permuting the roles of and for each . We are now ready to state our main result.

Theorem 1

(Robust MDP interpretation). Let and be an -coherent policy. Let be the value function of in the augmented MDP (see Eq. (5)) with transition kernel . Then, and are respectively worst-case and best-case value functions:

where the infimum and supremum are attained at the same kernel(s) .

Proof Fix and denote by the CDF of . Using the dual representation of the left AVaR in Lemma 2-(ii),

where the infimum ranges over functions such that for all ,

-

•

,

-

•

,

-

•

.

Under the additional assumption , any (resp. ) with is equal to (resp. ), which simplifies the expression to:

| (6) |

Symmetrically for the right AVaR,

| (7) |

Hence,

and

From equations (6) and (7), the infimum and the supremum are clearly attained at the same verifying because . Denoting by the non-distributional Bellman operator in the augmented MDP with kernel , we just proved that

where is characterized by .

To conclude the proof, it remains to prove by induction that for any , the following properties hold for all :

-

(a)

averaging property:

-

(b)

monotonicity:

The result then follows from taking the limit .

Base case . The monotonicity property (b) trivially holds, while (a) derives from Proposition 1-(vi).

Induction step: assume that the induction hypothesis is true for some .

(a) Averaging property. Let us prove that the averaging property is true for :

(b) Monotonicity. We have,

Theorem 1 shows that and merge into a value function in a state-augmented MDP such that contains worst-case values. Similar results can be found in the risk-sensitive MDP literature. In Chow et al. (2015), risk-sensitive MDPs with CVaR objective are linked to robust MDPs where the state space is augmented with a continuous state causing computational issues. The relation between CVaR and robustness has been also investigated in Osogami (2012) at the price of augmenting the state space with the time step variable. In contrast in Theorem 1, we only double the number of states, which makes our approach more tractable.

Characterization of .

A careful look at the proof of Theorem 1, combined with Lemma 2, reveals the exact expression of the kernel attaining both the and the :

where is defined in Definition 9 (in Appendix B) for a generic permutation . Here, is a permutation that sorts the particles

in non-decreasing order:

Example 2

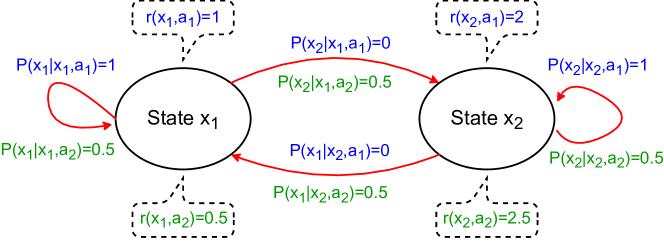

In the MDP in Figure 1 (with ), for the deterministic policy and level ,

and can be chosen arbitrarily as long as .

Bridging the BAVaR-AVaR gap.

In general, the BAVaRs are not equal to the AVaRs of the distributional return. A consequence of Theorem 1 is that the BAVaRs are more concentrated than the AVaRs around their common mean, namely the value function.

Corollary 1

(BAVaR vs. AVaR). Consider and for a given level , an -coherent policy and a state . Then for any action ,

Proof From Föllmer and Schied (2008), the left AVaR at level of the distribution admits the dual expression:

| (8) |

On the other side, from Theorem 1, also writes as an infimum of expected values. However, the distributions need to satisfy more constraints than in Eq. (8), due to the geometry of the uncertainty set . Indeed, with evident notations,

where the fixed point distributions in the augmented MDP verify:

Hence, satisfies the constraints in Eq. (8):

which implies .

The other half of the proof is similar, with replaced by , and by .

We recall that the whole approach developed in this paper relies on the successive applications of the distributional Bellman operator (DBO) followed by the -projection. Similarly, one could derive -step operators obtained by applying times the DBO (instead of just once) before projecting. Obviously, by taking arbitrarily large, one can make the gap between the resulting “-step BAVaRs” and the true AVaRs arbitrarily small.

4.2 The BAVaR coherent risk measure

We now expose our second interpretation stating that the negative left BAVaR and the right BAVaR are coherent risk measures. This claim is good news: indeed, a risk measure is termed coherent if it satisfies a set of properties that are desirable in a wide range of applications including financial ones (Artzner et al., 1999).

Corollary 2

(Coherent risk measure). Let , and .

-

(i)

The quantity , seen as a function of the reward function , is a coherent risk measure.

-

(ii)

The quantity , seen as a function of the negated reward function , is a coherent risk measure.

Proof (ii) Right BAVaR. Let us prove that is a coherent risk measure. Here, is seen a function of the opposite reward function . For clarity, we denote it by for a given reward function . We need to prove each of the following four properties (see Artzner et al., 1999).

-

(a)

Translation invariance:

-

(b)

Sub-additivity: for all reward functions ,

-

(c)

Positive homogeneity:

-

(d)

Monotonicity:

All four properties easily follow from Theorem 1, by writing as a supremum of value functions.

(i) Left BAVaR. The proof is similar to (ii), except that we parametrize

by the reward function, namely .

This result bridges the gap between our distributional point of view in section 3 and the concept of coherent risk measure. The fixed point object now appears as an appealing objective for risk-aware purpose in MDPs. Equipped with Theorem 1, we follow in the next section the robust MDP paradigm: maximize the worst-case value function to obtain a safe policy.

5 Safe or risky control

We now turn to describing a dynamic programming framework for risk-aware control problems derived from our distributional MDP perspective introduced in the previous sections. By leveraging the robustness insights developed earlier, it makes sense to either

-

•

look for a safe policy that maximizes and minimizes ,

-

•

or rather for a risky policy that minimizes and maximizes .

While there is a degree of symmetry to these tasks, it is easy to see that there are fundamental differences between them: while risky control aims to solve a relatively straightforward maximization problem, the safe control objective has a more intricate “max-min” nature. In what follows, we study both objectives under a specific simplifying assumption on the underlying MDP that allows an effective and (relatively) symmetric treatment of both cases.

5.1 Breaking the optimality ties

We provide the dynamic programming toolbox for solving these two control tasks for a very special type of MDP, that we call balanced MDP, where the expected returns of all policies are equal.

Assumption 1

(Balanced MDP). A Markov decision process is said “balanced” if for every state . In other words, all policies are optimal in terms of their expected return:

Under such assumption, there is a clear trade-off between and . Indeed from Proposition 1-(vi), their average has to remain constant:

Hence, maximizing one of these two quantities necessarily means minimizing the other one. Of course, any MDP can be reduced to a balanced MDP by 1) first, identifying the set of optimal actions in each state (classic control problem) and 2) then, filtering the action space to only allow optimal actions.

5.2 Safe and risky operators

In balanced MDPs, we necessarily have

In other words, is completely characterized by (and vice-versa): hence, we can restrict our attention to to define our risk-aware operators more concisely.

Definition 7

(Safe & risky Bellman operators). Consider a balanced MDP and let .

-

(i)

The safe Bellman operator is defined for all by: such that for any ,

where .

-

(ii)

The risky Bellman operator is defined for all by: such that for any ,

where .

As for the policy evaluation operator, these two control operators can be easily implemented through a sorting step: see Algorithm 2. Moreover, they satisfy the properties listed below.

Proposition 2

(Properties of and ). Assume a balanced MDP, let , . The following properties hold.

-

(i)

Concavity of the risky operator: if and , then for any ,

-

(ii)

-Contraction in sup norm: .

-

(iii)

Fixed point: there exists a unique fixed point .

-

(iv)

Safe optimality: for all ,

where .

-

(v)

Risky optimality: for all ,

where .

Proof (i) Concavity. The assumption is equivalent to with . Then, given and using the dual representation of the left AVaR from Lemma 2-(ii),

where the infimum is necessarily attained for . We deduce that is a concave piecewise linear function for .

(ii) Contraction. Let us consider the safe case: . Given a pair , by the dual representation of the left AVaR in Lemma 2-(ii),

where the infimum ranges over functions such that for all ,

-

•

,

-

•

,

-

•

.

Hence, by successive applications of the triangular inequality,

The risky case is analogous.

(iii) Fixed point. Consequence of (i) combined with Banach’s fixed point theorem and the completeness of .

(iv) Safe optimality. Fix a policy . Let us prove by induction that for any : for all ,

-

(a)

relative order:

-

(b)

monotonicity:

Taking the limit will then conclude the proof.

Base case .

(b) Monotonicity. As , then the infimum below is necessarily attained for :

| (9) |

where the second infimum ranges over functions such that for all ,

-

•

,

-

•

,

-

•

.

(a) Relative order. From the first infimum in Eq. (9) for , and using that ,

where the last inequality is obtained by choosing the “risk-neutral” weight functions defined for all by

Induction step: assume that the induction hypothesis is true for some .

(a) Relative order. Let us prove that the inequality holds for :

(b) Monotonicity. We have,

(v) Risky optimality.

The proof is similar to the safe case (iii).

Basically, Proposition 2 says that the safe and risky Bellman operators enjoy properties that are similar to the ones verified by the classical Bellman optimality operators. In particular, their fixed points and allow to identify the safest and riskiest actions and policies.

5.3 Safest and riskiest policies

From Proposition 2, it is natural to define the set of the safest/riskiest policies as follows:

The following corollary claims that these sets are non-empty and simply characterized by the fixed points: this is an immediate consequence of Proposition 2-(iii).

Corollary 3

(Safest & riskiest actions). Consider a balanced MDP and .

-

(i)

Safest policies: if and only if in each state ,

-

(ii)

Riskiest policies: if and only if in each state ,

Thereby in a balanced MDP, the safest (resp. riskiest) actions/policies can be identified by computing the fixed point of the safe (resp. risky) Bellman operator. This is analogous to the set of optimal actions in the classic control problem. From Corollary 3, there always exist safe and risky policies that are deterministic. Plus, notice that all these safest and riskiest policies are -coherent (), which means they come with the robust MDP interpretation of Theorem 1.

6 Numerical illustrations

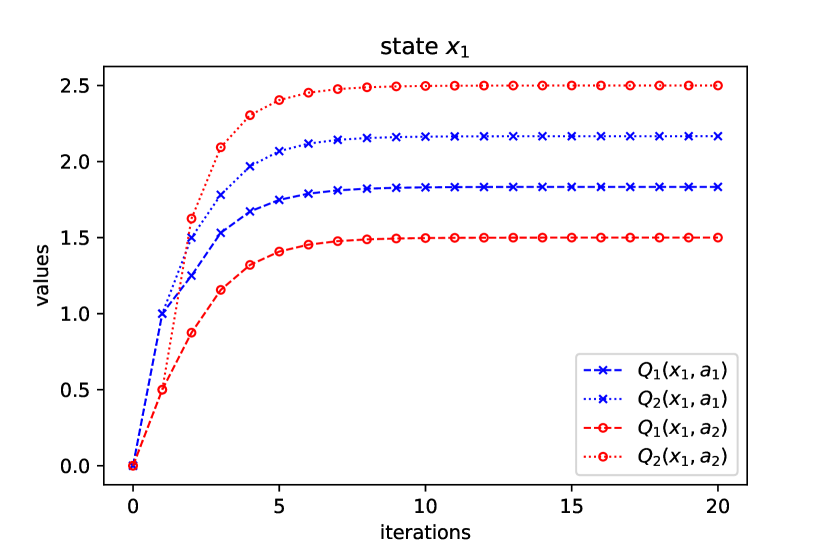

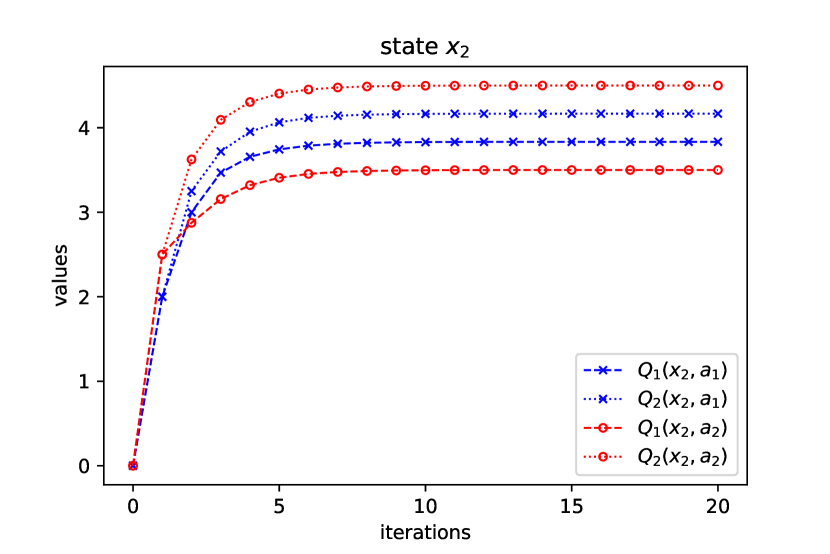

In this section, we test our Algorithms 1 and 2 in a practical example, for the risk level . We run our experiments in the two-states two-actions MDP from Figure 1 combined with the discount factor , which constitutes a balanced MDP. Indeed, the Q-function

solves the Bellman optimality equation

6.1 Evaluation of a policy

Consider the policy picking uniformly at random the two actions in any of the two states:

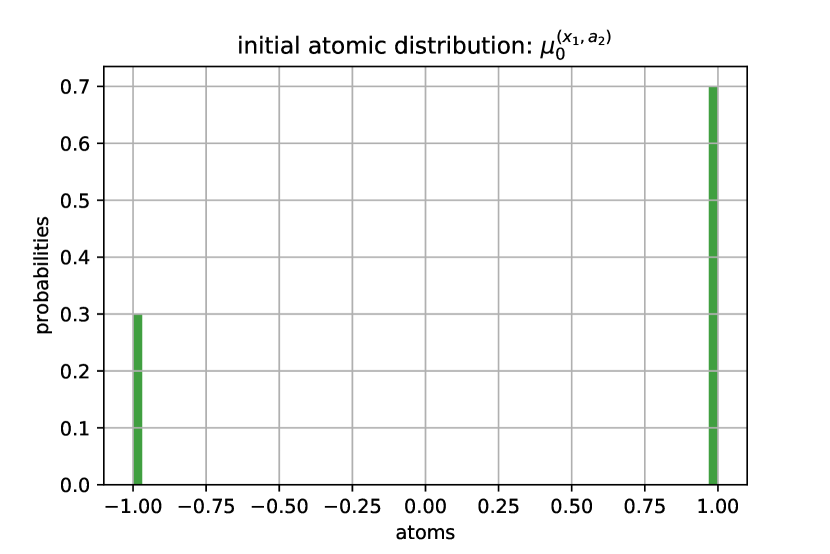

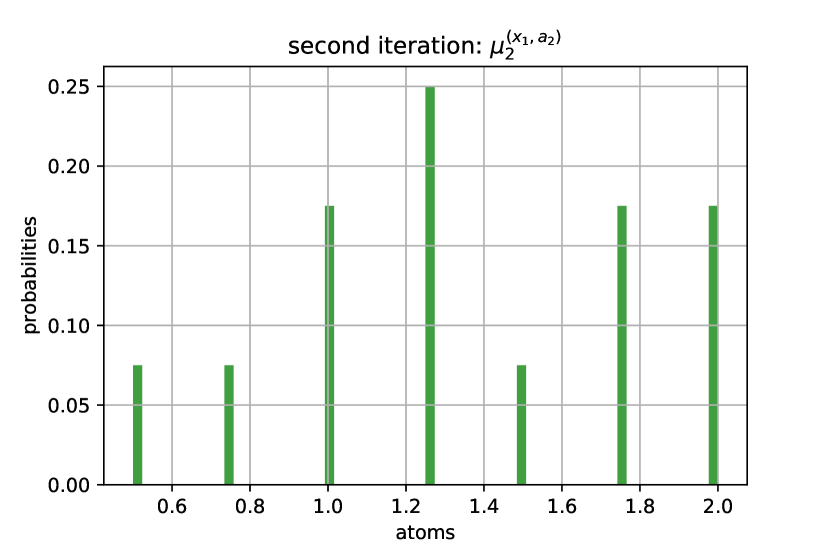

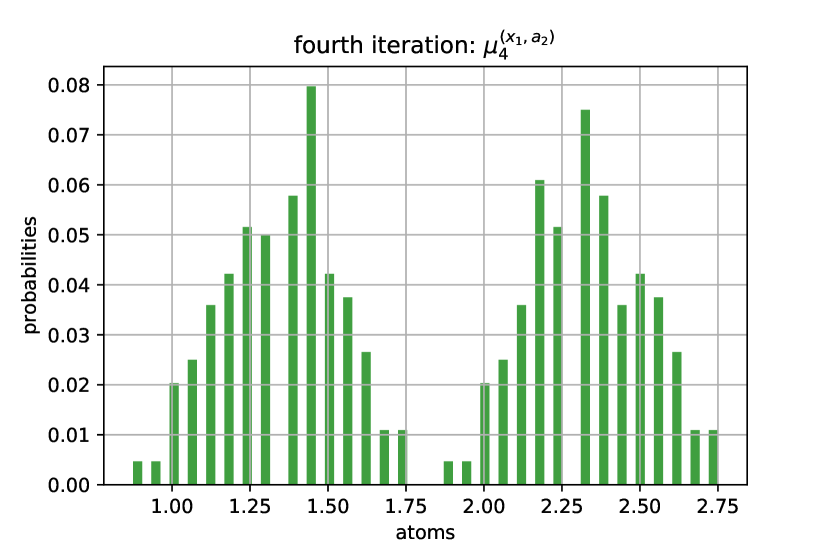

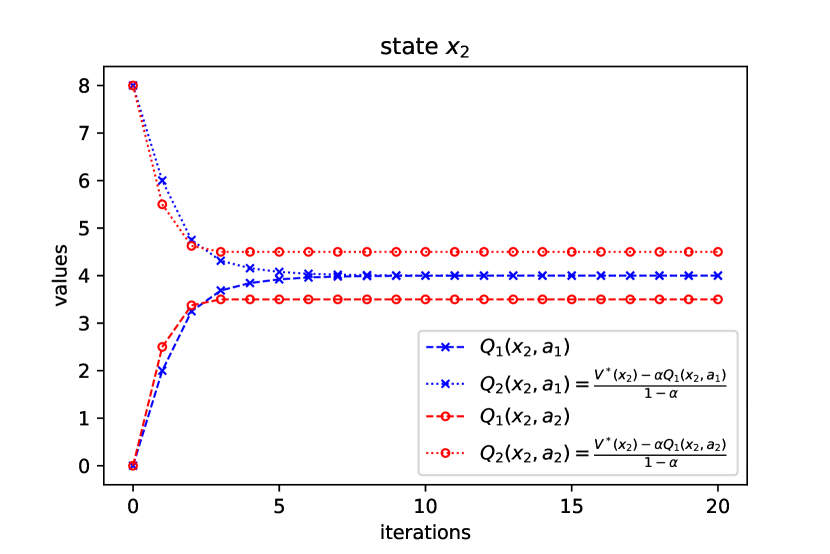

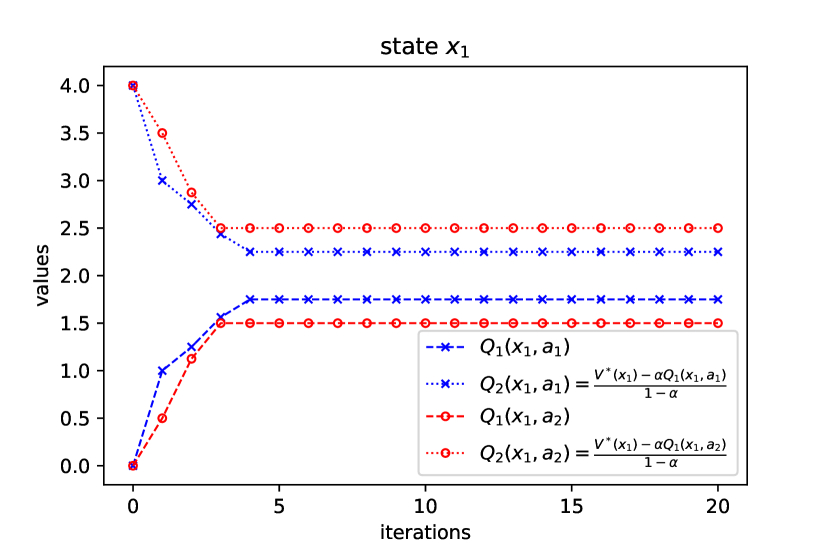

For the policy evaluation task, we run iterations of the SPE algorithm, starting from and initialized (arbitrarily) at zero. Figure 4 displays the plots across iterations, showing quick convergence to the fixed point .

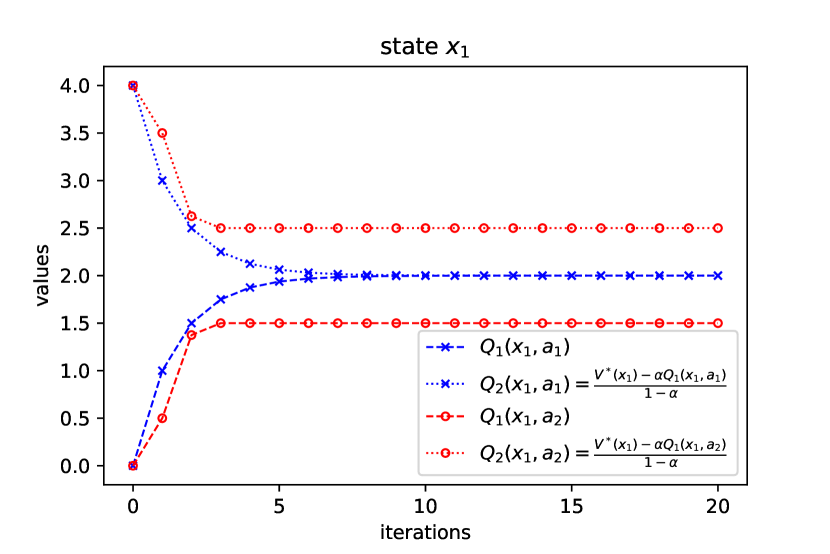

6.2 Finding safe and risky policies

For the safe (resp. risky) control task, we run iterations of the Safe SVI (resp. Risky SVI) algorithm, starting from initialized at zero. In both cases, we see quick convergence to the fixed points. In Figure 5, the safe fixed point satisfies , which confirms that the corresponding policy is the safest one that always takes the action , thus producing a deterministic discounted return. In Figure 6, the risky fixed point satisfies and , where is the policy from Example 2 that always takes the riskiest action . Hence, our two control algorithms work as expected: they quickly converge to the desired fixed points, from which the safe or risky (deterministic) policies can be extracted.

7 Conclusion

In this paper, we showed that the distributional perspective in MDPs can be leveraged to define new robust control tasks in the exact tabular setting. Our approach allows to distinguish safe from risky policies among the space of optimal policies. In other words, we first require the classic control problem to be solved, so that all suboptimal actions can be identified and removed from the action space, before we can apply our method. This strong “balanced MDP” requirement constitutes the main limitation of our work. Future lines of research include relaxing this assumption (e.g. in the safe case, by just requiring the condition ) or finding a natural class of MDPs with such structure. Future work could as well investigate risk-seeking algorithms (based on the linear programming formulation provided in Appendix B) in a reinforcement learning setting with an agent only observing empirical transitions.

Appendix A. A technical prerequisite

We recall the classic quantile representation of the expected value, that is used several times throughout the paper.

Lemma 3

(Expectation by quantiles). Let be a real-valued random variable with CDF and quantile function . Then,

Proof As any CDF is non-decreasing and right continuous (see, e.g., Billingsley, 2013), we have for all :

Then, denoting by a uniformly distributed random variable over ,

which shows that the random variable has the same distribution as . Hence,

Appendix B. A linear programming formulation of risky control

Here, we show that the risky control task in a balanced MDP can be written as a linear program (LP). From Lemma 2, we can get a closed-form expression of the left AVaR appearing in the fixed point equation of the risky Bellman operator. Given , we need to sort the particles

As , we restrict our attention to the following constrained permutations and transition kernels.

Definition 8

(Constrained permutations). Let us denote by the set of permutations that verify for all .

It can be shown by induction on that the cardinality of the set is

We refer to Achab et al. (2019) (and references therein) for a related analysis of constrained permutations in a statistical learning context. With a slight abuse of notation, we denote for all ,

Definition 9

(Permutation kernels). For any constrained permutation , we define the transition kernel as follows: for all ,

Primal & dual LPs. For an initial state distribution over , we define the primal problem as:

| (10) |

Lemma 4

Proof

(i) Primal LP. This follows from the properties of the risky Bellman operator (Proposition 2) combined with Lemma 2 in Nilim and El Ghaoui (2005).

(ii) Dual LP. The Lagrangian function of the LP (10) is:

| (12) |

The result follows by setting the gradients of with respect to and to zero.

(iii) Strong duality.

It can be proved by Slater’s condition, see Boyd et al. (2004).

References

- Acerbi and Tasche (2002) Carlo Acerbi and Dirk Tasche. On the coherence of expected shortfall. Journal of Banking & Finance, 26(7):1487–1503, 2002.

- Achab (2020) Mastane Achab. Ranking and risk-aware reinforcement learning. PhD thesis, Institut polytechnique de Paris, 2020.

- Achab et al. (2019) Mastane Achab, Anna Korba, and Stephan Clémençon. Dimensionality reduction and (bucket) ranking: a mass transportation approach. In Algorithmic Learning Theory, pages 64–93. PMLR, 2019.

- Artzner et al. (1999) Philippe Artzner, Freddy Delbaen, Jean-Marc Eber, and David Heath. Coherent measures of risk. Mathematical finance, 9(3):203–228, 1999.

- Bellemare et al. (2013) Marc G Bellemare, Yavar Naddaf, Joel Veness, and Michael Bowling. The arcade learning environment: An evaluation platform for general agents. Journal of Artificial Intelligence Research, 47:253–279, 2013.

- Bellemare et al. (2017) Marc G Bellemare, Will Dabney, and Rémi Munos. A distributional perspective on reinforcement learning. In International Conference on Machine Learning, pages 449–458. PMLR, 2017.

- Bellemare et al. (2019) Marc G Bellemare, Nicolas Le Roux, Pablo Samuel Castro, and Subhodeep Moitra. Distributional reinforcement learning with linear function approximation. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 2203–2211. PMLR, 2019.

- Bellman (1966) Richard Bellman. Dynamic programming. Science, 153(3731):34–37, 1966.

- Bertsekas and Tsitsiklis (1996) Dimitri P Bertsekas and John N Tsitsiklis. Neuro-dynamic programming, volume 5. Athena Scientific Belmont, MA, 1996.

- Bertsekas et al. (2000) Dimitri P Bertsekas et al. Dynamic programming and optimal control: Vol. 1. Athena scientific Belmont, 2000.

- Billingsley (2013) Patrick Billingsley. Convergence of probability measures. John Wiley & Sons, 2013.

- Boyd et al. (2004) Stephen Boyd, Stephen P Boyd, and Lieven Vandenberghe. Convex optimization. Cambridge university press, 2004.

- Chow et al. (2015) Yinlam Chow, Aviv Tamar, Shie Mannor, and Marco Pavone. Risk-sensitive and robust decision-making: a cvar optimization approach. arXiv preprint arXiv:1506.02188, 2015.

- Chun et al. (2012) So Yeon Chun, Alexander Shapiro, and Stan Uryasev. Conditional value-at-risk and average value-at-risk: Estimation and asymptotics. Operations Research, 60(4):739–756, 2012.

- Dabney et al. (2018a) Will Dabney, Georg Ostrovski, David Silver, and Rémi Munos. Implicit quantile networks for distributional reinforcement learning. arXiv preprint arXiv:1806.06923, 2018a.

- Dabney et al. (2018b) Will Dabney, Mark Rowland, Marc Bellemare, and Rémi Munos. Distributional reinforcement learning with quantile regression. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 32, 2018b.

- Föllmer and Schied (2008) Hans Föllmer and Alexander Schied. Convex and coherent risk measures. Encyclopedia of Quantitative Finance, pages 355–363, 2008.

- Goyal and Grand-Clement (2018) Vineet Goyal and Julien Grand-Clement. Robust markov decision process: Beyond rectangularity. arXiv preprint arXiv:1811.00215, 2018.

- Iyengar (2005) Garud N Iyengar. Robust dynamic programming. Mathematics of Operations Research, 30(2):257–280, 2005.

- Lyle et al. (2019) Clare Lyle, Marc G Bellemare, and Pablo Samuel Castro. A comparative analysis of expected and distributional reinforcement learning. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 33, pages 4504–4511, 2019.

- Mannor and Tsitsiklis (2011) Shie Mannor and John Tsitsiklis. Mean-variance optimization in markov decision processes. arXiv preprint arXiv:1104.5601, 2011.

- Mannor et al. (2016) Shie Mannor, Ofir Mebel, and Huan Xu. Robust mdps with k-rectangular uncertainty. Mathematics of Operations Research, 41(4):1484–1509, 2016.

- Moldovan and Abbeel (2012) Teodor Mihai Moldovan and Pieter Abbeel. Risk aversion in markov decision processes via near optimal chernoff bounds. In NIPS, pages 3140–3148, 2012.

- Morimura et al. (2010) Tetsuro Morimura, Masashi Sugiyama, Hisashi Kashima, Hirotaka Hachiya, and Toshiyuki Tanaka. Nonparametric return distribution approximation for reinforcement learning. In ICML, 2010.

- Morimura et al. (2012) Tetsuro Morimura, Masashi Sugiyama, Hisashi Kashima, Hirotaka Hachiya, and Toshiyuki Tanaka. Parametric return density estimation for reinforcement learning. arXiv preprint arXiv:1203.3497, 2012.

- Nilim and El Ghaoui (2005) Arnab Nilim and Laurent El Ghaoui. Robust control of markov decision processes with uncertain transition matrices. Operations Research, 53(5):780–798, 2005.

- Osogami (2012) Takayuki Osogami. Robustness and risk-sensitivity in markov decision processes. Advances in Neural Information Processing Systems, 25:233–241, 2012.

- Puterman (2014) Martin L Puterman. Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons, 2014.

- Rockafellar and Uryasev (2002) R Tyrrell Rockafellar and Stanislav Uryasev. Conditional value-at-risk for general loss distributions. Journal of banking & finance, 26(7):1443–1471, 2002.

- Rockafellar et al. (2000) R Tyrrell Rockafellar, Stanislav Uryasev, et al. Optimization of conditional value-at-risk. Journal of risk, 2:21–42, 2000.

- Rowland et al. (2018) Mark Rowland, Marc G Bellemare, Will Dabney, Rémi Munos, and Yee Whye Teh. An analysis of categorical distributional reinforcement learning. arXiv preprint arXiv:1802.08163, 2018.

- Rowland et al. (2019) Mark Rowland, Robert Dadashi, Saurabh Kumar, Rémi Munos, Marc G Bellemare, and Will Dabney. Statistics and samples in distributional reinforcement learning. arXiv preprint arXiv:1902.08102, 2019.

- Sutton and Barto (2018) Richard S Sutton and Andrew G Barto. Reinforcement learning: An introduction. MIT press, 2018.

- Wiesemann et al. (2013) Wolfram Wiesemann, Daniel Kuhn, and Berç Rustem. Robust markov decision processes. Mathematics of Operations Research, 38(1):153–183, 2013.