Dynamic growth-optimum portfolio choice

under risk control

Abstract

This paper studies a mean-risk portfolio choice problem for log-returns in a continuous-time, complete market. This is a growth-optimal problem with risk control. The risk of log-returns is measured by weighted Value-at-Risk (WVaR), which is a generalization of Value-at-Risk (VaR) and Expected Shortfall (ES). We characterize the optimal terminal wealth up to the concave envelope of a certain function, and obtain analytical expressions for the optimal wealth and portfolio policy when the risk is measured by VaR or ES. In addition, we find that the efficient frontier is a concave curve that connects the minimum-risk portfolio with the growth optimal portfolio, as opposed to the vertical line when WVaR is used on terminal wealth. Our results advocate the use of mean-WVaR criterion for log-returns instead of terminal wealth in dynamic portfolio choice.

Keywords: Mean-risk portfolio choice; growth-optimum; log-return; weighted Value-at-Risk; efficient frontier; quantile formulation

1 Introduction

The growth-optimal portfolio (GOP) is a portfolio which has a maximal expected growth rate (namely log-return) over any time horizon. As the GOP can be usually tracked to the work Kelly, (1956), it is also called the “Kelly criterion”. The GOP can also be obtained by maximizing log-utility which has a longer history. As the name implies, it can be used to maximize the expected growth rate of a portfolio. Indeed, it performs in some sense better than any other significantly different strategy as the time horizon increases.

Over the past half century, a lot of papers have investigated the GOP. In theory and practice, the GOP has widely applications in a large number of areas including portfolio theory, utility theory, game theory, information theory, asset pricing theory, insurance theory. For instance, to name a few of them in the recent studies in the literature, Aurell et al., (2000) study asset pricing problems in incomplete market; Rotar, (2004) considers optimal investment problems; Thorp, (2000) applies it to casino games.

We want to emphasize that the GOP ignores the relevant risk when maximizing the expected growth rate of a portfolio. It is the seminal work Markowitz, (1952) that takes the trade-off between the portfolio return and its risk into consideration when an investor chooses a portfolio. Markowitz, (1952) suggests to use variance to measure the risk. Since then, the mean-variance theory becomes one of the most dominant financial theories in the realm of portfolio choice. Besides variance, alternative risk measures have been proposed to measure the risk for portfolio choice. Research along this line includes Rockafellar and Uryasev, (2000), Campbell et al., (2001), Rockafellar and Uryasev, (2002), Alexander and Baptista, (2002), Alexander and Baptista, (2004), Jin et al., (2006), and Adam et al., (2008), where the authors study single-period mean-risk portfolio selection with various risk measures, such as semi-variance, value-at-risk (VaR), expected shortfall (ES), and spectral risk measures.

There also have numerous extensions of the mean-risk portfolio optimization from the single-period setting to the dynamic, continuous-time one (e.g. Zhou and Li,, 2000; Bielecki et al.,, 2005; Jin et al.,, 2005; Basak and Chabakauri,, 2010; He et al.,, 2015; Zhou et al.,, 2017; Gao et al.,, 2017; Dai et al.,, 2021; He and Jiang,, 2021). In particular, He et al., (2015) study a continuous-time mean-risk portfolio choice when risk is measured by the weighted Value-at-Risk (WVaR) but their results are rather pessimistic. The WVaR is a quantile-based risk measure that generalizes VaR and ES, two popular risk measures in quantitative risk management. They find that, when using WVaR (including VaR and ES) on terminal wealth to measure portfolio risk, the mean-risk model is prone to be ill-posed (i.e., the optimal value is infinite) and the investor tends to take infinite leverage on risky assets, leading to extremely risk-taking behaviors. Furthermore, the optimal risk is independent of the expected terminal target so the efficient frontier is a vertical line on the mean-WVaR plane. Their results suggest that the mean-WVaR model is an improper modeling of the trade-off between return and risk, when the WVaR is applied to the terminal wealth.

This paper proposes a continuous-time portfolio choice model with mean-WVaR criterion for portfolio log-returns, as opposed to the mean-WVaR criterion for terminal wealth in He et al., (2015). The motivation is two-fold. First, the mean-risk criterion for log-returns is consistent with Markowitz’s original idea to use mean and variance on portfolio returns. We consider a growth-optimal problem with risk control. Moreover, many single-period mean-risk models use risk measures on portfolio returns in the literature (e.g. Alexander and Baptista,, 2002, 2004, 2006; Jin et al.,, 2006; Adam et al.,, 2008). However, there is a discrepancy between single-period and dynamic portfolio choice models, as the latter typically considers mean-risk criterion for terminal wealth; an exception is Dai et al., (2021) who study continuous-time mean-variance portfolio choice for portfolio log-returns. We similarly adopt the mean-WVaR criterion for log-returns which naturally generalize the single-period return when returns are continuously compounded. Second, such a criterion conquers the ill-posedness of the model in He et al., (2015). As noted in He et al., (2015), the mean-WVaR criterion for terminal wealth is essentially a linear program for the quantile function of terminal wealth. This linearity, in turn, leads to the optimal terminal wealth’s quantile function being “corner points”, leading to extreme risk-taking behaviors. By contrast, our mean-WVaR criterion for log-returns is not linear in the quantile function of terminal wealth, and thus conquers the ill-posedness.

In a continuous-time, complete market framework, we solve the mean-WVaR portfolio choice for log-returns with the help of the so-called quantile formulation, developed in a series of papers (e.g. Schied,, 2004; Carlier and Dana,, 2006; Jin and Zhou,, 2008; He and Zhou,, 2011; Carlier and Dana,, 2011; Xia and Zhou,, 2016; Xu,, 2016). When risk is measured by a general WVaR risk measure, we characterize the optimal terminal wealth up to the concave envelope of a certain function through a detailed and involved analysis. When risk is measured by VaR or ES, two special cases of WVaR, we derive analytical expressions for the optimal terminal wealth and portfolio policy. The optimal terminal wealth turns out to be closely related to the growth optimal portfolio: the investor classifies market scenarios into different states, in which the terminal payoff can be constant, a multiple or fraction of the growth optimal portfolio. Furthermore, we obtain the efficient frontier, which is a concave curve that connects the minimum-risk (min-risk) portfolio with the growth optimal portfolio, as opposed to the vertical line in He et al., (2015). Our model allows for a meaningful characterization of the risk-return trade-off and may serve as a guideline for investors to set a reasonable investment target. Although He et al., (2015) provides a critique of using WVaR to measure risk, our results advocate that it is more appropriate to use WVaR, in particular, VaR and ES, on portfolio log-returns instead of terminal wealth for dynamic portfolio choice.

The rest of the paper is organized as follows. In Section 2, we propose a mean-WVaR portfolio choice problem for portfolio log-returns. We solve the problem in Section 3 by quantile optimization method. Section 4 presents optimal solutions and efficient frontiers when the risk is measured by VaR or ES. Some new financial insights and a comparation to the existing work are presented as well. Some concluding remarks are given in Section 5. Appendix A contains three useful lemmas. All remaining proofs are placed in Appendix B.

2 Mean-WVaR portfolio choice model

2.1 Financial market

Let be a given terminal time and be a filtered probability space, on which is defined a standard one-dimensional Brownian motion . It is assumed that augmented by all -null sets and that is complete.

We consider a Black-Scholes market in which there are a risk-free asset and a risky asset (called stock). The risk-free asset pays a constant interest rate and the stock price follows a geometric Brownian motion

where and , the appreciation rate and volatility of the stock, are positive constants. There exists a unique positive state price density (pricing kernel) process 111With additional assumptions on , our main results can be extended to a general complete market with stochastic investment opportunities. satisfying

| (2.1) |

where is the market price of risk in the economy. Therefore the market is complete.

Consider an economic agent with an initial endowment and faced an investment time horizon . The agent chooses a dynamic investment strategy , which represents the dollar amount invested in the stock at time . Assume the trading is continuous in a self-financing fashion and there are no transaction costs. The agent’s wealth process then follows a stochastic differential equation

| (2.2) |

The portfolio process is called an admissible portfolio if it is progressively measurable with , and the corresponding terminal wealth satisfies .

Let be the continuously compounded return (log-return) over the horizon , i.e.,

| (2.3) |

By convention, we define

2.2 Risk measure

We now introduce a risk measure that will be used in the portfolio choice model. In this paper, we focus on the weighted VaR (WVaR) risk measure proposed by He et al., (2015), which is a generalization of Value-at-Risk (VaR) and Expected Shortfall (ES), and encompasses many well-known risk measures that are widely used in finance and actuarial sciences, such as spectral risk measures and distortion risk measures; see Wei, (2018) for a review.

For any -measurable random variable , let denote its cumulative distribution function; and let denote its quantile function defined by

with the convention . The quantile function is non-decreasing, right-continuous with left limits (RCLL).

The WVaR risk measure for is defined as

| (2.4) |

where and is the set of all probability measures on .

The WVaR is a law-invariant comonotonic additive risk measure, and it covers many law-invariant coherent risk measures; see He et al., (2015) for a more detailed discussion. If is the Dirac measure at , i.e., , for all , then the corresponding WVaR measure becomes the VaR at , in other words,

If admits a density , then the corresponding WVaR measure becomes the ES, i.e.,

In the original paper of He et al., (2015), WVaR is applied to measure the risk of a portfolio’s terminal wealth. In this paper, we propose to apply WVaR to the portfolio’s log-return instead of its terminal wealth. Let be the terminal wealth of a portfolio and be the log-return of . Due to the monotonicity of logarithm functions, the quantile function of is

Therefore, the WVaR of can be expressed as

| (2.5) |

However, the extension from terminal wealth to log-return is not straightforward as the integral in (2.5) may not be well-defined since may take the value of 0 with positive probability. Let

be the set of quantile functions of all non-negative random variables, which include all terminal wealth of admissible portfolios. For any and , the integral is not well-defined if for some such that . Define

We set

| (2.6) |

Intuitively, if the terminal wealth of a portfolio is (so that the log-return is ) in some states, and the weighting measure assigns non-zero weighs to these states, then the WVaR of the log-return is assumed to be . In particular, if .222It is straightforward to verify , given that is log-normally distributed.

2.3 Portfolio choice model

We assume the agent chooses a dynamic portfolio strategy in the period to maximize the expected log-return while minimizing the risk of the portfolio’s log-return. The risk is evaluated by a WVaR risk measure on the portfolio’s log-return . Specifically, we consider the following dynamic portfolio choice problem

| (2.7) | ||||

| subject to | ||||

where is a “risk-tolerance” parameter that reflects the investor’s tradeoff between return and risk. This is a stochastic control problem, but not standard (namely, unlike those in Yong and Zhou, (1999)) due to the existence of the nonlinear probability measure .

In view of the standard martingale method, e.g., Karatzas and Shreve, (1998), we can first solve the following static optimization problem333This formulation implies that the optimal log-return is independent of .

| (2.8) | ||||

| subject to | ||||

where is given by (2.1). Then apply backward stochastic control theory to derive the corresponding optimal portfolio strategy .

The optimization problem (2.8) nests two special cases.

- Case .

-

In this case the investor minimizes the risk without any consideration of the expected log-return, and solves the following minimum-risk problem

(2.9) subject to The resulting portfolio is termed the min-risk portfolio.

- Case .

-

In this case the investor maximizes the expected log-return without any consideration of the risk. This is the so-called growth-optimal problem

(2.10) subject to

3 Quantile formulation and optimal solution

In this section, we solve the optimization problem (2.8) for .

If , then . If is the the uniform measure on , then and the growth optimal portfolio (2.11) is optimal to (2.8). To exclude these trivial cases, we make the following assumption on from now on.

Assumption 3.1.

and is not the uniform measure on .

The objective in (2.8) is based on the quantile function of the log-return; thus, the standard convex duality method is not readily applicable. To overcome this difficulty, we employ the quantile formulation, developed in a series of papers including Schied, (2004), Carlier and Dana, (2006), Jin and Zhou, (2008), He and Zhou, (2011), Carlier and Dana, (2011), Xia and Zhou, (2016), and Xu, (2016), to change the decision variable in (2.8) from the terminal wealth to its quantile function. This allows us to recover the hidden convexity of the problem and solve it completely.

We first show that the budget constraint in (2.8) must hold with equality and the objective function is improved with a higher level of initial wealth.

Lemma 3.1.

If is an optimal solution to the problem (2.8), then .

All the proofs of our results are put in Appendix B.

Denote by and the distribution and quantile functions of , respectively. With slight abuse of notation, we suppress the subscript when there is no need to emphasize the dependence on . Since is log-normally distributed, both and are functions. The following lemma can be found in Jin and Zhou, (2008).

Lemma 3.2 (Jin and Zhou, (2008)).

We have for any lower bounded random variable whose quantile function is . Furthermore, if , then the inequality becomes equality if and only if

From Lemmas 3.1 and 3.2, we know that if is optimal to (2.8), then where is the quantile function of . Let be the log-return of . We have

and

Therefore, we can consider the following quantile formulation of (2.8)

| (3.1) | ||||

| subject to |

where the decision variable is the quantile function of the terminal wealth. Once we obtain the optimal solution to (3.1), then the optimal solution to (2.8) is given by

Define

| (3.2) |

Because is log-normally distributed, is a function with , and , on . Let be the inverse function of and define

Then is a function with , , and , on . It is easy to see if and only if , and if and only if , where

In terms of new notation, we have

and

Consequently, solving (2.8) reduces to solving the following quantile optimization problem (after dropping constant terms)

| (3.3) | ||||

| subject to |

This is a concave optimization problem, so it can be tackled by the Lagrange method.

Define the Lagrangian

where is a Lagrange multiplier to fit the budget constraint in (3.3). Define

and its left-continuous version

We additionally set .

We then have

and we can consider the following optimization problem

| (3.4) |

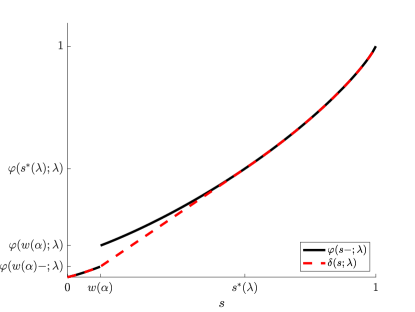

Inspired by Rogers, (2009), Xu, (2016), and Wei, (2018), we introduce , the convex envelope function of on , given by

| (3.5) |

The convex envelope is the largest convex function dominated by , and is affine on the set

The following proposition presents the optimal solution to (3.4).

Proposition 3.1.

We want to find a Lagrange multiplier such that satisfies the budget constraint in (3.3). Clearly,

and consequently

We are ready to state the optimal solution to (3.3).

Proposition 3.2.

The optimal solution to (3.3) is given by

Finally, the optimal solution to (2.8) is given by

In particular, we can obtain the min-risk portfolio by setting :

which solves (2.9).

We summarize the main results of the paper in the following proposition.

4 Examples with explicit solution

In this section, we present two examples to illustrate our general results. In particular, we consider the optimization problem (2.8) when the WVaR risk measure is given by either VaR or ES, two popular risk measures.

4.1 Mean-VaR efficient portfolio

In this subsection, we specialize our setting to the mean-VaR optimization problem. In particular, we consider the optimization problem (2.8) when the WVaR risk measure is given by the VaR at a confidence level , namely

In other words, is given by the Dirac measure at .

Proposition 4.1.

When is given by the Dirac measure at , we have the following assertions.

- Case .

-

-

1.

The minimum-VaR (min-VaR) terminal wealth is

where

-

2.

The optimal log-return is

-

3.

The expected optimal log-return is

-

4.

The VaR of the optimal log-return is

-

1.

- Case .

-

- 1.

-

2.

The optimal log-return is

-

3.

The VaR of the optimal log-return is

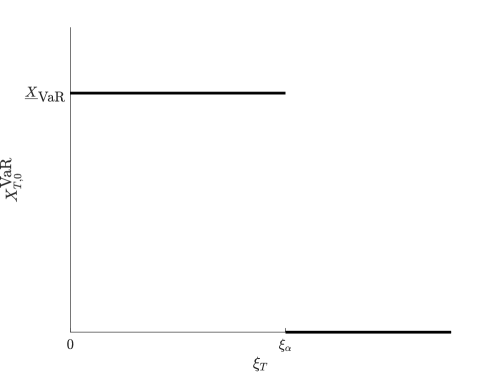

Figure 1 depicts the optimal terminal payoff of the min-VaR portfolio (), which resembles a digital option. Essentially, the investor invests all the money in a digital option that pays in the good states of the market () and 0 otherwise. The probability of winning the option depends solely on the confidence level of VaR and is given by .

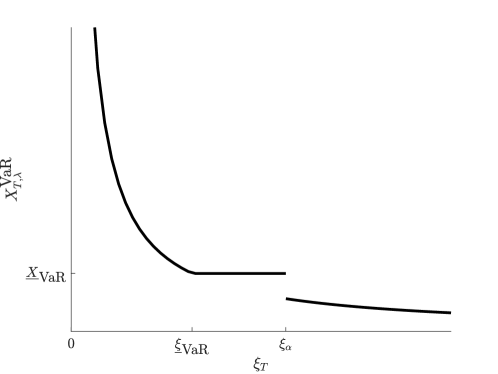

Figure 2 displays the optimal terminal payoff of the mean-VaR efficient portfolio (). The investor classifies market scenarios into three subsets: in the good states () and in the bad states (), the terminal payoff is a fraction () of the growth optimal portfolio; in the intermediate states (), the investor receives a constant payoff . Moreover, the terminal wealth has a jump discontinuity at and the corresponding log-returns are always finite (but can be extremely large or small).

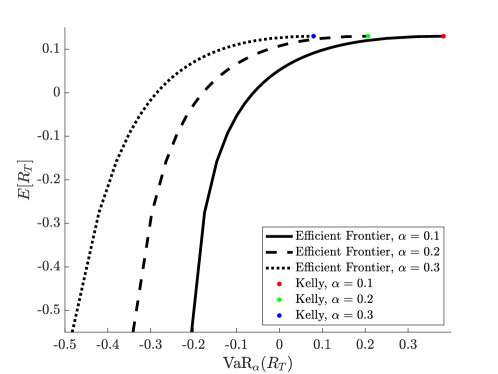

Figure 3 plots the mean-VaR efficient frontiers for different confidence levels . The efficient frontier is a concave curve that connects the growth optimal portfolio (colored dots) with the min-VaR portfolio (not shown in the graph). The growth optimal portfolio has the highest expected log-return but also the highest VaR. By contrast, the min-VaR portfolio has the smallest expected log-return (negative infinity) but also the lowest VaR. Figure 3 also displays a sensitivity analysis of the efficient frontier with respect to , the confidence level of VaR. As increases, the efficient frontier shifts to the left: for a given level of the expected log-return, the VaR of the corresponding efficient portfolio decreases as increases.

As the optimal terminal wealth is known, we can solve for the optimal time- wealth and portfolio policy.

Corollary 4.1.

We have the following assertions.

- Case .

-

-

1.

The min-VaR efficient wealth at time is

-

2.

The optimal portfolio policy at time is

-

1.

- Case .

-

-

1.

The mean-VaR efficient wealth at time is

-

2.

The optimal portfolio policy at time is

-

1.

Here and hereafter

and is the standard normal distribution function, and is the standard normal probability density function.

4.2 Mean-ES efficient portfolio

In this subsection, we specialize our setting to the mean-ES optimization problem. In particular, we consider the optimization problem (2.8) when the WVaR risk measure is given by the ES at a confidence level , namely

In other words, admits a density , for all .

Proposition 4.2.

When admits a density with , we have the following assertions.

- Case .

-

- 1.

-

2.

The optimal log-return is

-

3.

The ES of the optimal log-return is

where

- Case .

-

- 1.

-

2.

The optimal log-return is

-

3.

The ES of the optimal log-return is

where

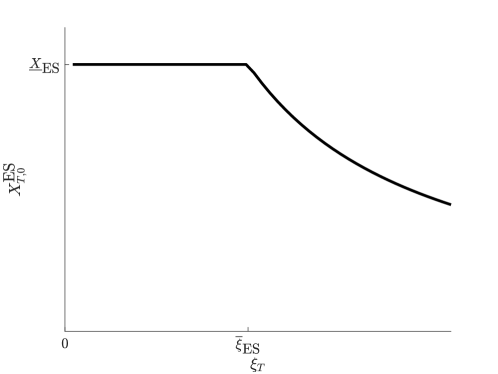

Figure 4 depicts the optimal terminal payoff of the min-ES portfolio (). The investor classifies market scenarios into two subsets: in the good states (), the investor receives a constant payoff ; in the bad states (), the payoff is a multiple () of the growth optimal portfolio.

Figure 5 displays the optimal terminal payoff of the mean-ES efficient portfolio (). The investor classifies market scenarios into three subsets: in the good states (), the terminal payoff is a fraction () of the growth optimal portfolio; in the intermediate states (), the investor receives a constant payoff ; in the bad states (), the terminal payoff is a multiple () of the growth optimal portfolio. In contrast to the mean-VaR efficient portfolio, the terminal payoff of the mean-ES efficient portfolio is continuous in the state price density.

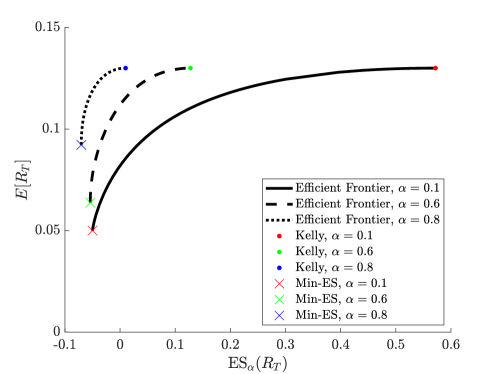

Figure 6 shows the mean-ES efficient frontiers for different confidence levels . The efficient frontier is a concave curve that connects the growth optimal portfolio (colored dots) with the min-ES portfolio (colored crosses). The growth optimal portfolio has the highest expected log-return but also the highest ES. By contrast, the min-ES portfolio has the smallest expected log-return but also the lowest ES. In contrast to the min-VaR portfolio, the risk of the min-ES portfolio is finite and thus the mean-ES efficient frontier is a finite curve. Figure 6 also displays a sensitivity analysis of the efficient frontier with respect to , the confidence level of ES. As increases, the efficient frontier shifts to the left: for a given level of the expected log-return, the ES of the corresponding efficient portfolio decreases as increases. In particular, the minimum ES that the investor can achieve is decreasing in .

The following corollary presents the optimal time- wealth and portfolio policy. The proof is similar to that of Corollary 4.1 and thus we omit it.

Corollary 4.2.

We have the following assertions.

- Case .

-

-

1.

The min-ES efficient wealth at time is

-

2.

The efficient portfolio policy at time is

-

1.

- Case .

-

-

1.

The mean-ES efficient wealth at time is

-

2.

The efficient portfolio policy at time is

-

1.

4.3 Comparison with He et al., (2015)

He et al., (2015) consider a continuous-time mean-risk portfolio choice problem in which the risk is measured by WVaR. They assume the decision-maker minimizes the risk of terminal wealth, while maintaining the expected terminal wealth above a prescribed target. They find that the model can lead to extreme risk-taking behaviors. When bankruptcy is allowed, the optimal terminal wealth is binary, i.e., the investor invests a small amount of money in an extremely risky digital option and saves the rest of the money in the risk-free asset. When bankruptcy is prohibited, the terminal wealth can be three-valued and the optimal strategy is to invest a small amount of money in an extremely risky digital option and put the rest in an asset with moderate risk. These strategies are not commonly seen in practice and are not appropriate for many investors. Furthermore, the optimal value (the risk) is independent of the expected terminal wealth target. Therefore the efficient frontier is a vertical line in the mean-risk plane and there is no explicit trade-off between risk and return. They conclude that using the WVaR on terminal wealth is not an appropriate model of risk for portfolio choice.

In contrast to He et al., (2015), our model uses the expected target and risk measure on log-returns instead of terminal wealth. When the risk is evaluated by the VaR or ES, two popular risk measures, we find that the investor classifies market scenarios into different states, in which the terminal payoff is a multiple or fraction of the growth optimal portfolio, or constant. Furthermore, the efficient frontier is a concave curve that connects the min-risk portfolio with the growth optimal portfolio. Our model allows for an explicit characterization of the risk-return trade-off and may serve as a guideline for investors to set reasonable investment targets. Our results demonstrate that it is more appropriate to use the WVaR, in particular, the VaR and ES, on the log-return instead of the terminal wealth for portfolio choice.

5 Conclusion

We have proposed and solved a dynamic mean-WVaR portfolio choice problem with risk measured to log-returns, as opposed to terminal wealth in He et al., (2015). Our model conquers the ill-posedness of the mean-WVaR criterion for terminal wealth in He et al., (2015), and allows for an explicit and meaningful characterization of the trade-off between return and risk. We have demonstrated that our proposed mean-WVaR criterion for log-returns is more appropriate and tractable than the mean-WVaR criterion for terminal wealth in serving as a guideline for dynamic portfolio choice.

Appendix A Useful Lemmas

The following function

| (A.1) |

is increasing, continuous and convex on and on , respectively. It has an upward jump at .

Lemma A.1.

If is defined by (A.1) with . Then its convex envelope is given by

Proof.

When , we have

It is straightforward to verify is convex. For any convex function dominated by , it is clearly dominated on by as . Because and , for any , we have

Therefore, is the largest convex function dominated by on , and thus is the convex envelope of . The left panel of Figure (7) gives a graphical illustration. ∎

Lemma A.2.

If is defined by (A.1) with . Then its convex envelope is given by

where is the unique number in such that

Proof.

Let

which is continuous in . For , by integration by parts we have

thanks to the convexity of on , so is a strictly decreasing function of . Meanwhile,

and

Therefore, there exists a unique such that .

Thanks to the convexity of on and on , it is easy to verify that is a continuous convex function dominated by on . For any convex function dominated by , it is clearly dominated on by as . By the same argument as in the proof of Lemma A.1, we have that is dominated by on too. Therefore, is the largest convex function dominated by , and thus the convex envelope of . The right panel of Figure (7) gives a graphical illustration. ∎

The following function

| (A.2) |

is increasing, and convex on and on , respectively. It is continuous on .

Lemma A.3.

If is defined by (A.2) with . Then its convex envelope is given by

where is the unique number in such that

Proof.

When , we have

Let

For , by integration by parts we have

again thanks to the convexity of on , so is a strictly decreasing function of . Moreover, thanks to the strictly convexity of ,

and

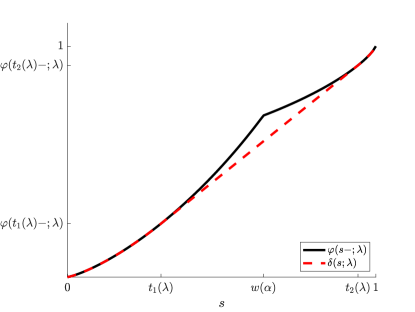

Therefore, there exists a unique such that . By the same argument as in the proof of Lemma A.1, we can show that is the convex envelope of . The left panel of Figure (8) gives a graphical illustration. ∎

Lemma A.4.

If is defined by (A.2) with . Then its convex envelope is given by

where are the unique pair such that

| (A.3) |

Proof.

Again by the same argument as in the proof of Lemma A.1, we can show that is the convex envelope of . The right panel of Figure (8) gives a graphical illustration. It is only left to show the existence and uniqueness of the pair that satisfies (A.3).

Let

In view of the strict monotonicity of and and positivity of , we have

Define

Then by monotonicity, for ,

and it is not hard to verify that

| (A.4) |

Let

For , thanks to (A.4) and using integration by parts, we have

by virtue of for and is convex on , so is a strictly decreasing function of . Moreover, thanks to the strictly convexity of and on , respectively, and the fact that , we have

and

Therefore, there exists a unique that solves . Let . Then, and solve (A.3). ∎

Appendix B Proofs

Proof of Lemma 3.1.

This is indeed contained in the proof of Theorem 7, Xu, (2014). We give it here to make the paper self-contained. Suppose is optimal to (2.8) and . Define

which satisfies the budget constraint. Clearly . Let and be the corresponding log-returns of and , respectively. Then

and consequently

contradicting the optimality of to (2.8). ∎

Proof of Proposition 3.1.

We handle the two cases and separately.

- Case .

-

Define

It suffices to consider the following optimization problem

as if .

Because is the convex envelope of , , , and . For any , we have

From Fubini’s theorem, we have

and consequently

where is given by point-wise optimization. We then show that

which is equivalent to

or by Fubini’s theorem,

namely,

(B.1) Because is constant on any sub-interval of , the above identity (B.1) holds.

Finally, we need to verify . If , then

if , then

Because , for . We claim for . Otherwise, we have

Since , we have . It follows from the convexity of that for and for . This means is not affine around . But , so should be affine in the neighborhood of , leading to a contradiction.

We need to additionally show if . In fact, . If , then and is affine for sufficiently close to , which contradicts the fact for .

- Case .

-

In view of (2.6), we need to solve the following optimization problem

Let

We then have and , for all . According to (3.5), we know that , for all . There are two subcases.

-

•

If , then and

Similar to the case , we can show, for any ,

We then have

where

is given by point-wise optimization. We can similarly show

by verifying

We now verify by showing . Similar to the case , we can show for . Because , we can prove in a similar fashion.

-

•

If , then , and

Similar to the case and , we can show, for any ,

where

is given by point-wise optimization. We can similarly show

Finally, it is easy to verify for and thus .

-

•

The proof is complete. ∎

Proof of Proposition 3.2.

Proof of Proposition 4.1.

First, we have

Next, let be the convex envelope of , and , the right derivative of with respect to .

- Case .

- Case .

The rest of the claim is straightforward to verify. ∎

Proof of Corollary 4.1.

Conditional on , is normally distributed with mean and variance .

For , we have

Applying Ito’s lemma to , we have

Comparing the coefficient of the term with (2.2), we arrive at the expression for .

For , we have

Applying Ito’s lemma to and comparing the coefficient of the term with (2.2), we have

Noting that

we arrive at the expression for . ∎

References

- Adam et al., (2008) Adam, A., Houkari, M., and Laurent, J.-P. (2008). Spectral risk measures and portfolio selection. Journal of Banking & Finance, 32(9):1870–1882.

- Alexander and Baptista, (2002) Alexander, G. J. and Baptista, A. M. (2002). Economic implications of using a mean-VaR model for portfolio selection: A comparison with mean-variance analysis. Journal of Economic Dynamics and Control, 26(7):1159–1193.

- Alexander and Baptista, (2004) Alexander, G. J. and Baptista, A. M. (2004). A comparison of VaR and CVaR constraints on portfolio selection with the mean-variance model. Management Science, 50(9):1261–1273.

- Alexander and Baptista, (2006) Alexander, G. J. and Baptista, A. M. (2006). Does the basle capital accord reduce bank fragility? an assessment of the value-at-risk approach. Journal of Monetary Economics, 53(7):1631–1660.

- Aurell et al., (2000) Aurell, E., Baviera, R., Hammarlid, O., Serva, M. and Vulpiani, A. (2000). A general methodology to price and hedge derivatives in incomplete markets, International Journal of Theoretical and Applied Finance, 3(1): 1–24.

- Basak and Chabakauri, (2010) Basak, S. and Chabakauri, G. (2010). Dynamic mean-variance asset allocation. Review of Financial Studies, 23(8):2970–3016.

- Bielecki et al., (2005) Bielecki, T. R., Jin, H., Pliska, S. R., and Zhou, X. Y. (2005). Continuous-time mean-variance portfolio selection with bankruptcy prohibition. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 15(2):213–244.

- Campbell et al., (2001) Campbell, R., Huisman, R., and Koedijk, K. (2001). Optimal portfolio selection in a value-at-risk framework. Journal of Banking & Finance, 25(9):1789–1804.

- Carlier and Dana, (2006) Carlier, G. and Dana, R.-A. (2006). Law invariant concave utility functions and optimization problems with monotonicity and comonotonicity constraints. Statistics & Decisions, 24(1/2006):127–152.

- Carlier and Dana, (2011) Carlier, G. and Dana, R.-A. (2011). Optimal demand for contingent claims when agents have law invariant utilities. Mathematical Finance, 21(2):169–201.

- Dai et al., (2021) Dai, M., Jin, H., Kou, S., and Xu, Y. (2021). A dynamic mean-variance analysis for log returns. Management Science, 67(2):1093–1108.

- Gao et al., (2017) Gao, J., Zhou, K., Li, D., and Cao, X. (2017). Dynamic mean-LPM and mean-CVaR portfolio optimization in continuous-time. SIAM Journal on Control and Optimization, 55(3):1377–1397.

- He and Jiang, (2021) He, X. D. and Jiang, Z. (2021). Mean-variance portfolio selection with dynamic targets for expected terminal wealth. Mathematics of Operations Research.

- He et al., (2015) He, X. D., Jin, H., and Zhou, X. Y. (2015). Dynamic portfolio choice when risk is measured by Weighted VaR. Mathematics of Operations Research, 40(3):773–796.

- He and Zhou, (2011) He, X. D. and Zhou, X. Y. (2011). Portfolio choice via quantiles. Mathematical Finance, 21(2):203–231.

- Jin et al., (2006) Jin, H., Markowitz, H., and Zhou, X. Y. (2006). A note on semivariance. Mathematical Finance, 16(1):53–61.

- Jin et al., (2005) Jin, H., Yan, J.-A., and Zhou, X. Y. (2005). Continuous-time mean–risk portfolio selection. In Annales de l’Institut Henri Poincare (B) Probability and Statistics, volume 41, pages 559–580. Elsevier.

- Jin and Zhou, (2008) Jin, H. and Zhou, X. Y. (2008). Behavioral portfolio selection in continuous time. Mathematical Finance, 18(3):385–426.

- Kelly, (1956) Kelly, J. L. (1956). A new interpretation of information rate, Bell System Techn. Journal, 35:917–926.

- Karatzas and Shreve, (1998) Karatzas, I. and Shreve, S. E. (1998). Methods of Mathematical Finance, volume 39. Springer Science & Business Media.

- Markowitz, (1952) Markowitz, H. (1952). Portfolio selection. Journal of Finance, 7(1):77–91.

- Rockafellar and Uryasev, (2000) Rockafellar, R. T. and Uryasev, S. (2000). Optimization of conditional value-at-risk. Journal of Risk, 2:21–42.

- Rockafellar and Uryasev, (2002) Rockafellar, R. T. and Uryasev, S. (2002). Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26(7):1443–1471.

- Rogers, (2009) Rogers, L. (2009). Optimal and robust contracts for a risk-constrained principal. Mathematics and Financial Economics, 2(3):151–171.

- Rotar, (2004) Rotar, V. (2004). On optimal investment in the long run: Rank dependent expected utility as a bridge between the maximum-expected-log and maximum-expected-utility criteria, Working Paper, San Diego State University.

- Schied, (2004) Schied, A. (2004). On the Neyman–Pearson problem for law-invariant risk measures and robust utility functionals. Annals of Applied Probability, 14(3):1398–1423.

- Thorp, (2000) Thorp, E. O. (2000). The Kelly criterion in blackjack, sports betting and the stock market, in O. Vancura, J. A. Cornelius and W. R. Eadington (eds.), Finding the Edge: Mathematical Analysis of Casino Games, (University of Nevada, Reno, NV), pp. 163–213.

- Wei, (2018) Wei, P. (2018). Risk management with weighted VaR. Mathematical Finance, 28(4):1020–1060.

- Xia and Zhou, (2016) Xia, J. and Zhou, X. Y. (2016). Arrow–Debreu equilibria for rank-dependent utilities. Mathematical Finance, 26(3):558–588.

- Xu, (2016) Xu, Z. Q. (2016). A note on the quantile formulation. Mathematical Finance, 26(3):589–601.

- Xu, (2014) Xu, Z. Q. (2014). A new characterization of comonotonicity and its application in behavioral finance. Journal of Mathematical Analysis and Applications, 418:612–625.

- Yong and Zhou, (1999) Yong, J. and Zhou, X. Y. (1999). . Stochastic controls: Hamiltonian systems and HJB equations, Springer-Verlag, New York.

- Zhou et al., (2017) Zhou, K., Gao, J., Li, D., and Cui, X. (2017). Dynamic mean–VaR portfolio selection in continuous time. Quantitative Finance, 17(10):1631–1643.

- Zhou and Li, (2000) Zhou, X. Y. and Li, D. (2000). Continuous-time mean-variance portfolio selection: A stochastic LQ framework. Applied Mathematics and Optimization, 42(1):19–33.