Lei and Pun

*Chi Seng Pun, 21 Nanyang Link, Singapore 637371.

Nonlocality, Nonlinearity, and Time Inconsistency in Stochastic Differential Games

Abstract

[Abstract]This paper studies the well-posedness of a class of nonlocal fully nonlinear parabolic systems, which nest the equilibrium Hamilton–Jacobi–Bellman (HJB) systems that characterize the time-consistent Nash equilibrium point of a stochastic differential game (SDG) with time-inconsistent (TIC) preferences. The nonlocality of the parabolic systems stems from the flow feature (controlled by an external temporal parameter) of the systems. This paper proves the existence and uniqueness results as well as the stability analysis for the solutions to such systems. We first obtain the results for the linear cases for an arbitrary time horizon and then extend them to the quasilinear and fully nonlinear cases under some suitable conditions. Two examples of TIC SDG are provided to illustrate financial applications with global solvability. Moreover, with the well-posedness results, we establish a general multidimensional Feynman–Kac formula in the presence of nonlocality (time inconsistency).

\jnlcitation\cnameand (\cyear2023), \ctitleNonlocality, Nonlinearity, and Time Inconsistency in Stochastic Differential Games, \cjournalMath. Finance, \cvol2023;00:1–47.

keywords:

Stochastic Differential Games; Time inconsistency; Existence and Uniqueness; Nonlocal Nonlinear Parabolic Systems; Feynman–Kac Formula; Mathematics of Behavioral Economics1 Introduction

The aim of this paper is to study the well-posedness of nonlocal fully nonlinear higher-order systems for the unknown of the form

| (1) |

where are -dimensional real-valued, is a positive integer, the nonlinearity could be nonlinear with respect to its all arguments, and both and are dynamical variables while should be considered as an external parameter. Here, is a multi-index with , and . To clarify, the system (1) consists of coupled -valued nonlocal fully nonlinear equations :

| (2) |

where the superscripts of represent the -th entry of the corresponding vector functions. The systems above characterize a series of systems indexed by , which are connected via their dependence on . The diagonal dependence, referring to that of are evaluated not only at but also at , directly results in nonlocality. When and , the system (1) or (2) is reduced to nonlocal fully nonlinear parabolic partial differential equations (PDEs) studied in 42.

The diagonal dependence is an inevitable consequence when we look for an equilibrium solution for a time-inconsistent (TIC) dynamic choice problem. The TIC problem was first seriously studied in 60 from an economic perspective, in which a consistent planning of control policies, characterized by a Nash equilibrium (NE), is considered as a suitable solution; see 51. With the popularity of behavioral economics, it has been recognized that the time inconsistency (also abbreviated as TIC) or dynamic inconsistency is prevalent when we consider behavioral factors in dynamic choice problems; see 61 for some empirical evidence, 38, 15 for non-exponential discounting, 29, 62 for (cumulative) prospect theory. However, a rigorous treatment in continuous-time settings was only available a decade ago; see 24 for a review. 1, 54 adopt a recursive approach, originally suggested in 60, to derive a time-consistent (TC) portfolio strategy for the mean-variance (MV) investor in continuous time. The MV analysis, pioneered by 49, is free of TIC in the static setting (single period) but the dynamic choice problem under the MV criterion is TIC due to the nonlinearity of the variance operator. Subsequently, 5, 3 establishes heuristic analytical frameworks for discrete- and continuous-time TIC stochastic control problems, which can successfully address the state-dependence issue (a type of TIC) of risk aversion in portfolio selection 6, but they leave behind many open problems, including the existence and uniqueness of the solution to their deduced Hamilton–Jacobi–Bellman (HJB) equation system.

Using a discretization approach, 73, 70 derive a so-called equilibrium HJB equation, which accords with the HJB system in 3, to characterize the equilibrium solutions to TIC stochastic control problems. The equilibrium HJB equation is a nonlocal PDE, whose nonlocality comes from the diagonal dependence, and is a special case of (1). 70 established the existence and uniqueness results for the equation in a quasilinear setting, which requires the linear dependence on the second-order derivative at local point and the removal of the second-order derivative at diagonal , such that the diffusion term of the state process was restricted to be uncontrolled. From the perspective of stochastic differential equations (SDEs), 68, 20, 64, 19, 66 made attempts to the TIC problem with a flow of forward-backward SDEs (FBSDEs) or backward stochastic Volterra integral equation (BSVIE) but their results are still subject to the same restriction as in the PDE theory or limitation to the first-order dependence. However, their work has converted the key open problem in 3 to another open problem in PDE or SDE theory. Recently, 42 has shown the existence and uniqueness of a nonlocal fully nonlinear parabolic PDE in a small-time setting.

Following 42, this paper extends the well-posedness results from a nonlocal fully nonlinear second-order PDE to a system of coupled nonlocal fully nonlinear higher-order PDEs, from small-time (in the sense of maximally defined regularity) to global settings, and from the conventional space of bounded functions to a weighted space with exponential growth functions. Similarly, the essential difficulty for constructing a desired contraction (to use fixed-point arguments) is the presence of the highest-order diagonal term . To see this, we discuss an intuitive attempt heuristically, from which we outline the distinct feature of our problem. To show the existence and uniqueness of (1), it is intuitive to consider a mapping from to that satisfies

| (3) |

Thanks to the classical theory of parabolic systems 58, 37, 14, the mapping is well-defined. By replacing the intractable diagonal term with a known vector-valued function , the well-posedness of the higher-order system (3) parameterized by promises the existence and uniqueness of the solution . Moreover, if , it is clear that the fixed point solves the original system (1). However, for the case of , since the input is of the same order of the output , it is not immediate to show the contraction. The curse has limited all aforementioned works to a restricted case of and except for 42 that extends the study to the case of and . This paper leverages on the techniques developed in 42 to further extend the study to with an arbitrary positive integer .

The mathematical extension achieved in this paper has two immediate implications, namely the establishments of mathematical foundation of TIC stochastic differential games (SDGs) and a general multidimensional Feynman–Kac formula under the framework of nonlocality.

-

1.

Some specific types of TIC SDGs are studied in 69, 40 for zero-sum games and 65 for nonzero-sum games but they still left behind the existence and uniqueness results. In this paper, we will show the relevance of the system (1) by introducing a general formulation of nonzero-sum TIC SDGs. Under some regularity assumptions as in 17, 18, 2, we yield the parabolic systems for the TIC SDGs as a special case of (1).

-

2.

The extended version of Feynman–Kac formula paves a new path for the SDE theory to study a flow of the multidimensional second-order FBSDEs (or 2FBSDEs), which is also called the multidimensional second-order BSVIEs (or 2BSVIEs), where both forward and backward SDEs are multidimensional. The 2BSDEs were first introduced in 7 to provide a probabilistic interpretation of a fully nonlinear parabolic PDE.

To clarify, our paper considers only the TIC caused by the initial-time-dependence in the control/game problems, and thus the parabolic systems of our interest (1) only involve the nonlocality with a two-time-variable structure. It is noteworthy that the initial-state-dependence and nonlinearity of conditional expectations also form the sources of TIC and there exist similar arguments to convert the control/game problem into a parabolic PDE systems with nonlocality in state; see 3, 39, 27, 28, 26, 25, 72. We do not attempt the initial-state-dependence in this paper as it poses technical challenges. Its key difference from our consideration is that the state variable is multidimensional and unrestricted, whereas the time variable is naturally bounded especially in a finite-time framework.

This paper contributes to the theories of PDE, SDE, and SDG, especially for the treatment of nonlocality in the multidimensional setting. Specifically,

- Section 2 (SDG aspect)

-

formulates TIC SDGs that incorporate with TIC behavioral factors, which facilitate developments of many studies in financial economics including robust stochastic controls and games under relative performance concerns. We heuristically derive the associate equilibrium HJB systems and reveal its relation with the TIC SDGs. Our focus is then placed on the well-posedness of such nonlocal systems as it serves as the prerequisite of using its solution to characterize the solution to the TIC SDGs. Noteworthy is that our study allows the diffusion of the state process to be controllable, which breaks through the existing bottleneck of time-inconsistent stochastic control problems.

- Section 3 (PDE aspect)

-

presents our main results of well-posedness of nonlocal higher-order systems in linear, quasilinear, and fully nonlinear settings individually. Our results generalize the existing studies while potential extensions are discussed. To our best knowledge, our well-posedness results in a larger function space that accommodate more complex research objects over a longer time horizon open the frontier of the existing literature on nonlocal PDEs/systems.

- Section 4 (SDG and PDE)

- Section 5 (SDE and PDE)

-

provides a nonlocal Feynman–Kac formula linking the solution to a flow of multidimensional 2FBSDEs to that of a nonlocal fully nonlinear parabolic system.

- Section 6

-

concludes.

2 Nonzero-Sum Time-Inconsistent Stochastic Differential Games

In this section, we follow the frameworks of 17, 18, 2 to formulate general -player nonzero-sum TIC SDGs, where preferences and utility functions for each player are time-varying.

Let be a completed filtered probability space on which a -dimensional standard Brownian motion with the natural filtration augmented by all the -null sets in is well-defined. Let be the controlled -dimensional state process driven by the forward SDE (FSDE):

| (4) |

where is the set of -valued, -measurable, and square-integrable random variables and with is the aggregated control process that consists of all players’ controls characterized by , i.e. , with and . Here, are arbitrary positive integers. Hereafter, we follow the notations in 21 for the control policies that the left subscript and superscript denote the time bounds of truncated control policies, i.e. (they are suppressed when they are 0 and , respectively), while the right subscript indicates the control at specific time point. Denote by the aggregated controls except for such that consists of and for any , denoted by . Moreover, it is useful to introduce (or for short) the set of reachable states at time from the time-state with the strategy , which is defined by

where is the support of the distribution of of (4), the interior and the boundary of which in are denoted by and , respectively, and denotes the ball centered at with radius . We refer the readers to Section 3 of 23 for more details. Next, let be the adapted solution (see 48 Proposition 3.3 for the solvability) to the following backward SDE (BSDE):

| (5) |

where satisfies (4) and for , or , and is -valued. Equations (4) and (5) jointly form forward-backward SDEs (FBSDEs).

We presume that each Player () aims to choose her control to minimize the following cost functional:

| (6) |

With the similar arguments in 30, it turns out that under some mild conditions, the cost functional may be expressed as

Note that when , the problem is reduced to the TIC problem with recursive cost functional considered in 70, 72. Moreover, if both and are independent of the initial time , then it is further reduced to a TC problem with a recursive utility, considered in 31. Furthermore, when depends on neither nor , the cost functional reduces to the classical one; see 74.

A typical example of such initial-time-dependent cost functionals adopts non-exponential or hyperbolic discounting factors; see 38, 15. For illustration, we assume a Markovian framework and that all the coefficient and objective functions, , , and are deterministic, where . Moreover, we define the set of all admissible control processes on as follows:

Similarly, we define the admissible set for each player by replacing with . Under some mild conditions (see 48 Proposition 3.3), for any and , the controlled FBSDEs (4)-(5) admit a unique -adapted solution .

The -player game is formed, attributed to the common state processes and the recursion of the cost functionals on the aggregated . Each player wants to minimize her own cost functional, naturally resulting in a Nash equilibrium (NE) point. However, since the cost functions and in (6) are dependent on the initial time , we will observe TIC of the decision-making. In other words, the NE point found at time may not be the NE point when we evaluate again the SDG (4) with (6) at time . To deal with the TIC, we introduce the concept of time-consistent NE (TC-NE) point below, in line with the initiative of 60.

2.1 Time-Consistent Nash Equilibrium Point

Heuristically, we are treating the TIC SDGs as “games in subgames" while the similar concept is first proposed in 53 for robust TIC stochastic controls, where the problem is recast as a (two-player) nonzero-sum TIC SDG played by the agent and the nature. A TC-NE point of TIC SDG (4)-(5) with (6) finds the NE point over given that the players adopt the predetermined NE points over for a small time elapse and . In light of this search, the NE points identified backwardly are subgame perfect equilibrium (SPE). Note that the SPE concept is concerned about the (aggregated) controls across time and it implies the so-called time consistency of the NE points. We give the formal definition of TC-NE point as follows.

Definition 2.1 (Time-Consistent Nash Equilibrium (TC-NE) Point).

Let be a non-empty set of and for be the control set for the player . A continuous map is called a closed-loop TC-NE point of the nonzero-sum TIC SDG (4)-(5) with (6) if the following two conditions hold:

-

1.

For any , the state equation

admits a unique solution ;

-

2.

For any , let solves

then the following inequality holds:

(7) where

(8)

Furthermore, and for and are called the TC-NE state process and the TC-NE value functions, respectively.

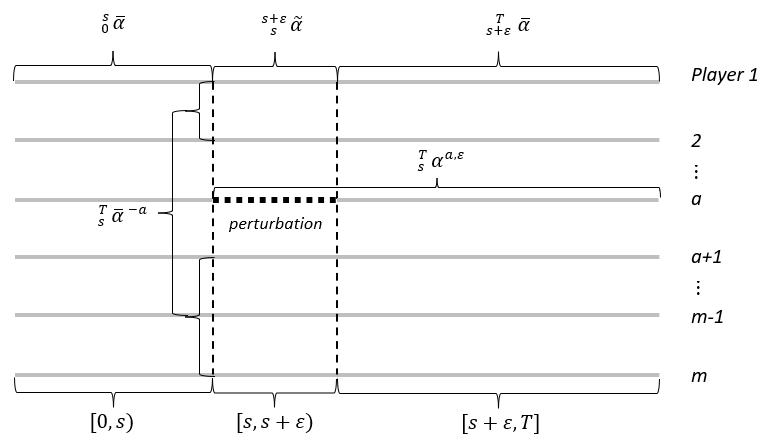

Remark 2.2.

For the local optimality condition (7) and the piecewise-defined strategy (8) in Definition 2.1, 23 conducts in-depth studies on the choice of reference points and perturbations in a small time period of the length . It summarizes a variety of similar but different concepts of closed-loop equilibrium strategies in the existing literature (see, for instance, 9, 10, 1, 4, 6, 8 where the perturbations of (8) are chosen from a set of all constant strategies; 11, 12, 3 where the perturbed strategies of (8) are constructed by pasting two feasible deterministic feedback strategies). One main result of 23 is to show the equilibrium strategy is independent of whether the alternative strategies are constant or deterministic strategies. In other words, can be taken as a deterministic feedback strategy , which would facilitate later analyses in Subsection 2.2. Another key contribution of 23 is to elaborate the set of and to show the advantage of replacing the whole set with the set of reachable states in (7). We assume that for all throughout our paper, except for Subsection 4.1.2 where we consider the power-utility model with . In addition to the closed-loop strategies, the existing literature also define so-called open-loop equilibrium policies (see, 27, 28, 72). In this paper, we handle TIC problem by the means of closed-loop strategies within a game-theoretical framework. When , the TC-NE point of the nonzero-sum TIC SDG is reduced to the SPE of the corresponding TIC control problem; see 70, 73, 72. When the TIC sources are eliminated, it is clear that the local optimality described by (7) agrees with the conventional dynamic optimality.

The inequality (7) implies that each player is locally optimal in minimizing the cost functional over in a proper sense and no player can do better by unilaterally changing their strategy. The basic idea is illustrated in Figure 1, which also clarifies the notations we used.

In the next subsection, we shall characterize the TC-NE point as well as the TC-NE value function with a differential equation approach. While a single equilibrium Hamilton–Jacobi–Bellman (HJB) equation is used to characterize the SPE of the TIC control problem in 3, 70, it can be imagined that a system of equilibrium HJB equations is needed for our case. Prior to its derivation, we first introduce some notations and make an assumption as with 17, 18, 2.

For , , where is the set of all symmetric matrices, we denote the Hamiltonian by a -valued function with and , and defined by

| (9) |

[Generalized minimax condition] There exist functions for with needed regularity such that

-

1.

for any , ;

-

2.

for any ,

This generalized minimax condition has implied the existence of the NE point at each in the sense that all are found simultaneously. It is desirable as we are discussing about a general setting and it is normally equivalent to model assumptions on and .

2.2 Heuristic Derivation of Equilibrium HJB System

In this subsection, we derive the system of equilibrium HJB equations, characterizing the TC-NE point in Definition 2.1, from which we reveal that it is a special case of our nonlocal parabolic system (1). Since the focus of our paper is on the well-posedness of (1) and the nested HJB system rather than the latter’s origination, a heuristic derivation in the similar fashion of 5, 3, 4 will be in place. For simplicity, we show only where the nonlocal terms come from and the linkage with the classical HJB equations. For a rigorous derivation, one can follow the discretization approach in 73, 70 or a rigorous argument in 23 to derive the nonlocal parabolic system but it is too lengthy and thus not adopted here.

In light of the methodology in 5, 3, 4, there are three main steps (Step 1-Step 3) to obtain the equilibrium HJB system of a multiplayer nonzero-sum TIC SDGs. For the sake of simplification of the heuristic derivation, we assume that and in (4)-(6), and adopt the deterministic feedback-type controls throughout this subsection. Next, let us consider

where is the conditional expectation under and (or for short) is the unique adapted solution to (4) on with and . The set of feasible feedback strategies is denoted by , which can be roughly understood as the class of deterministic functions that are regular enough to promise the well-posedness of the state process (4) and the cost functional (6). We refer the readers to Definition 2.2 of 3 and Definition 2.1 of 23 for more details.

Definition 2.3.

Given a feasible feedback strategy , we define by

| (10) |

i.e., its component for .

For any and , the process is a martingale and (10) satisfies

| (11) |

where is the controlled infinitesimal generator of the FSDE (4):

Similar to the classical dynamic programming principle in 74, we need to first derive a recursive relation between cost functionals/value functions evaluated at two different initial points and . Then, by sending the mesh size of the time interval partition to zero, a nonlocal system of parabolic type is derived, through which a closed-loop TC-NE point can be identified and the TC-NE value function can be obtained.

- Step 1: The Recursion for Cost functionals .

-

From the Markovian structure and Definition 2.3, we have , which yields . Taking conditional expectation at on both sides of the latter equation, we have

Moreover, by the tower rule of conditional expectations in the last term, we obtain the recursive equation for as follows:

(12) - Step 2: The Recursion for TC-NE Value functions .

-

Based on (12), we aim to derive a recursive equation for . We first define a perturbed feedback strategy such that for and for , where is an arbitrary element in that consists of the -th component of feasible controls in and can be viewed as a candidate equilibrium strategy. Note that is a function rather than a process in Definition 2.1 while they have similar roles. Noteworthy is that the perturbed strategy is constructed with two feedback strategies and rather than by pasting a constant strategy and a feedback one (as in (8)). However, Remark 2.2 illustrates that the slight difference does not affect our characterization of the equilibrium point and its associated HJB equations/systems. Then, Definition 2.1 implies that for ,

(13) (14) where represents and the function is defined by (10) with replaced by . Next, inspired by the discrete setting of TIC stochastic control problem in 5, 4, it is anticipated from (7) that

(15) However, for a continuous-time model, this statement is not always true since it is still possible that for sufficiently small and certain ; see 3, 23. Hence, the following analyses of (16) and (17) are rather heuristic, while they are included in our derivation of equilibrium HJB systems as they inspire us on how to investigate continuous-time TIC problems via the lens of discrete-time setting; see 3, 4 for the similar heuristic arguments. For a formal and rigorous proof, readers are suggested to refer to Theorem 3.3 of 23 and Section 4 of 70. Note that no matter whether the argument is formal or not, one always obtains the same HJB equations.

- Step 3: Equilibrium HJB System.

-

Letting in (17) gives a deterministic system:

with boundary conditions , where

for any . Note that the key difference between the operators and is that the former corresponds to a function while the latter corresponds to a point . By the generalized minimax condition in Assumption 9 and noting that , we know that the infimum above is achievable and the minimum is expressed by

(18) By the earlier discussion in Step 2, we must have to form a closed-loop TC-NE point. With the representation of , we can then solve for from (11) with replaced by , which is the equilibrium HJB system we look for, but we present only the system for the general case below to save space. It is noteworthy that even we can focus on solving hereafter, the derivation uses the definition of and thus we require to be first-order differentiable in .

- General Case.

-

Even if the running cost functional is non-zero and is a random variable, the heuristic derivation above is almost identical except for more tedious expressions, i.e., we can obtain a generalized HJB system:

(19) and the same expression of in (18). Plugging (18) into a modified version of (11) (with as a non-homogeneous term), we obtain

Similar to the notations and , for , we denote the nonlinearity by a -valued function with for . Then, we can simplify the system above as a nonlocal parabolic system for of the form

(20)

Remark 2.4.

Though the derivations above are heuristic, we can similarly develop the system-version results of 73, 70, 72, following their discretization approach or the argument in Theorem 3.3 of 23, and we will also end up with the equilibrium HJB equation/system (20) as well as a closed-loop TC-NE point (18) and the associated TC-NE value functions in the sense of Definition 2.1. The relationship between (19) and (20) is discussed in 25. While it is not the focus of this paper, we summarize the mathematical claims/conjectures about the connection between solutions to (20) and TIC SDGs in Section 2.3. Moreover, an interesting fact is that we only need to study the HJB system (20) in the set of reachable states rather than in ; see Section 2.3 of 23 and the example in Subsection 4.1.2.

From the derivations in this subsection, the inclusion of the nonlocal terms is rationalized: the characterizations of (or ) and are coupled. It is also easy to see that in the TC case (independent of the initial time point), i.e., , the HJB system (19) or equilibrium HJB system (20) reduce to the classicial ones (see 74). Proposition 3.2 below tells us that (20) is a special case of (1) with . Moreover, a closely related topic is robust TIC stochastic controls via the formulation of nonzero-sum TIC SDGs. From which, we can observe many solvable examples in finance and insurance; see 53, 21, 22, 71, 41. By carefully choosing cost functionals of nonzero-sum SDGs, we can model the relative performance concerns among multiple agents in decision-making and thus our theory can extend the related works of 13, 56, 55, 36 by introducing TIC or behavioral factors.

2.3 The Relation between the Equilibrium HJB System and TIC SDGs

The derivation of the equilibrium HJB system alone does not justify its mathematical connection with the stochastic control/game problem (4)-(6). We need to show two aspects of the connection, namely sufficiency and necessity, constituting two conjectures below:

- (Sufficiency/Verification theorem):

-

the solutions to (18) and (20) indeed give a TC-NE point and a TC-NE value function. Mathematically, we assume that solves (20) and that the infimum of (19) is attained for every in the sense of NE. Then, the minimizer of (under Assumption 9), given in (18), is a closed-loop TC-NE point and the function is the TC-NE value function as in Definition 2.1;

- (Necessity):

-

every TC-NE point must minimize the Hamiltonian associated to TIC problem (4)-(6) and the corresponding value function solves the HJB system (19). Mathematically, we assume that there exist a closed-loop TC-NE point and the corresponding value function and we define , where comes from being the adapted solution of the family of FBSDEs parameterized by :

Then, solves (19) and (20) while realizes the infimum of (19).

By the derivations in the previous subsection and using the similar arguments in 3, it is easy to establish the verification theorem for the Markovian setting while we omit the straightforward proof. It should be noted that the equilibrium HJB equation and the verification theorem for the non-Markovian setting are attempted in 26. The necessity issue is a difficult problem, while we refer the readers to the latest progress alone this line, such as 44, 26, 23, 19 and a comprehensive literature review of the field 24. Specifically, 26 proves the necessity for the scalar case (stochastic control problem) in a general non-Markovian setting. With a more mathematically rigorous definition of the SPE/TC solution (similar to Definition 2.1) and a discretization approach, 70, 72, 67, 66 show intuitively the desired mathematical connection between TIC stochastic control problem and the associated equilibrium HJB equation, given that the latter is well-posed. Even we consider TIC SDGs with higher dimensions, one could expect that the sufficiency and the necessity above are provable.

However, they are not the focus of this paper while the well-posedness of the equilibrium HJB system appears to be the core of the concerns above. It is noteworthy that the solvability of TIC SDGs has not been provided by the works on the sufficiency and necessity. The desired mathematical connection between the equilibrium HJB equations/systems and TIC stochastic controls/SDGs is meaningless if the equilibrium HJB equations/systems are not well-posed; see the assumptions in the two conjectures above. Moreover, though some works have proved the sufficiency and necessity, they uniformly assumed that the volatility of (4) is free of control such that the nonlocal second-order term in (20) vanishes; see 70, 26. Hence, our well-posedness results, which get rid of this bottleneck, benefit the studies on more general problems of TIC SDGs as well as the previous studies on TIC stochastic controls. While there may not be a specific order of studying the sufficiency, the necessity, and the well-posedness of the nonlocal parabolic system, this paper addresses the last one and based on which, the other two are relatively simple given the extensive related studies in the literature. By establishing the existence, uniqueness, stability, and regularities of solutions of (20), our PDE results directly imply the existence and uniqueness of TIC problems where both the drift and the volatility are controlled.

3 Well-posedness of Nonlocal Parabolic System

In this section, we present our main results about the well-posedness issues of the nonlocal higher-order systems (1). The overall idea is to first study the case with a linear operator, which will then be used to infer the well-posedness results for the system (1) with a general nonlinear operator, together with the linearization method. All the proofs are deferred to A.

While the SDG and the Feynman–Kac formula are usually formulated in a backward setting, we first show the equivalence between the solvabilities of the nonlocal backward (terminal-value) problems,

| (21) |

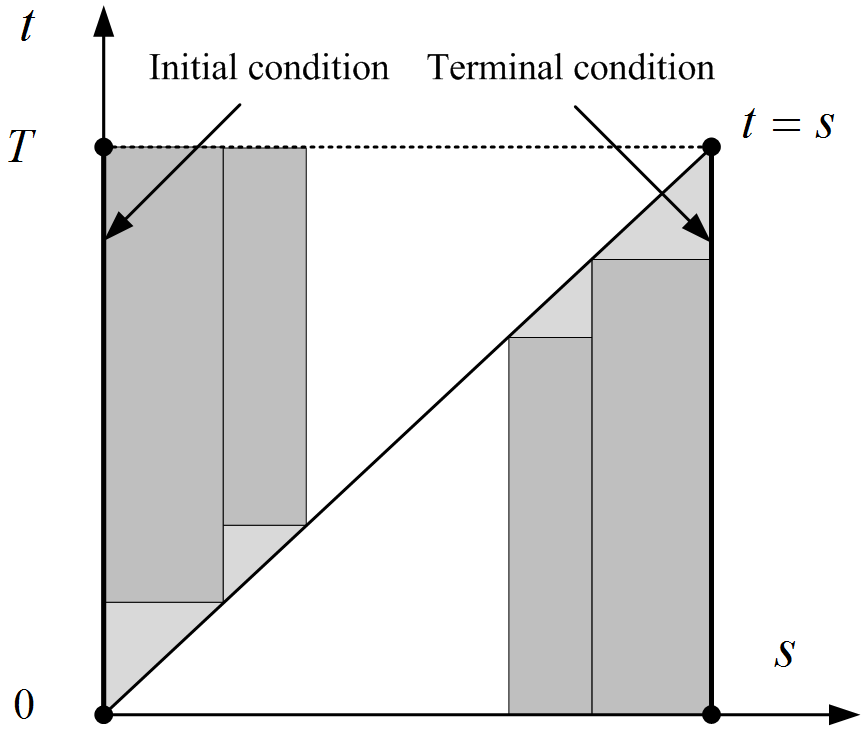

and the nonlocal forward (initial-value) problems (1). There are a few noteworthy differences between the two systems: first, for the backward problem (21), if we move the to the right-hand side, we will have a negative sign , compared to the forward problem (1); second, the ordering between and are the opposite of one another. The symmetry between (1) and (21) is shown in Figure 2. Notation-wise, we use the time region for forward problems to distinguish from for backward problems.

Given Proposition 3.1, we only study the forward problem (1) in this section as it can simplify the notations. To this end, we introduce some norms and the induced Banach spaces for the problems of our interest. The solvability of (1) will be first investigated in the usual space of bounded and continuous functions in Subsection 3.1-3.3. Subsequently, in order to meet practical needs for more financial applications, it is necessary to extend the well-posedness results in an exponentially weighted space of growth functions in Subsection 3.4.

3.1 Norms and Banach Spaces

For a -dimensional real-valued array , . Given , we denote by the set of all the continuous and bounded -valued functions in endowed with the supremum norm . Wherever no confusion arises, we write instead of . Then, we revisit the definition of “parabolic" Hölder spaces, which is commonly adopted in the studies of local parabolic equations, including 14, 42. Let be the Banach space of the functions such that is continuous in , its derivatives of the form for exist, and it has a finite norm defined by

where is always a positive integer, is a non-integer positive number and is the floor function, represents the -dimensional array, the entries of which are the j-th-order mixed partial derivatives of in , i.e. . Moreover, for and ,

The defined norms depend on but indeed for different they are equivalent. Hence, we suppress the dependence on will be not noted unless otherwise specified. Moreover, wherever no confusion arises, we do not distinguish between and for functions independent of .

Now, we are ready to define the norms and Banach spaces for nonlocal systems of unknown vector-valued functions . For any and such that , we introduce the following norms:

where . Then, these norms induce the following spaces, respectively,

where is the set of all continuous and bounded -valued functions defined in . It is easy to see that both and are Banach spaces. The definitions above leverage not only the order relation between and but also the sufficient regularities in all arguments.

3.2 Nonlocal Linear Higher Order Parabolic Systems

Let be a family of nonlocal, linear, and strongly elliptic operator of order , whose -th entry, , , takes the form

| (22) |

where the nonlocality stems from the presence of and the strong ellipticity condition implies that there exists some such that

| (23) | |||||

| (24) |

uniformly for any , , and . Next we consider a nonlocal linear system:

| (25) |

where all coefficients and belong to . Moreover, the inhomogeneous term and the initial condition .

Suppose that is differentiable with respect to , then by differentiating (25) with respect to , the derivative satisfies

| (26) |

By taking advantage of the integral representations:

it is clear that , denoted by , satisfies the following system of equations:

| (27) |

Lemma 3.2.

Theorem 3.3.

Next, thanks to the equivalence between (25) and (27), we will establish the global well-posedness of nonlocal linear systems. Moreover, we will derive a Schauder-type estimate of solutions of (25). It not only justifies the stability of the solutions to (25) with respect to the data , but also establishes a foundation for the further analysis of nonlocal fully nonlinear systems (1) in the next section.

Theorem 3.4.

3.3 Nonlocal Fully Nonlinear Higher Order Parabolic Systems

After studying the solvability of nonlocal linear system, we will adopt the method of linearization to prove the well-posedness of nonlocal fully nonlinear system of the form (1).

To take advantage of the results of nonlocal linear systems in Section 3.2, we require certain regularity assumptions on and . Generally speaking, we require the initial condition . The nonlinearity is a vector-valued function defined in , where and is a open ball centered at with a positive radius . Denoting by the open set (ball) in consisting of all the functions such that the range of is contained in the open ball, then the nonlinearity can be regarded as a mapping from . We require satisfies that

-

(i)

(Ellipticity condition) for any and , there exists a such that

(30) (31) hold uniformly with respect to .;

-

(ii)

(Hölder continuity) there exists a positive constant such that

(32) -

(iii)

(Lipschitz continuity) there exists a such that for any , ,

(33)

where denotes the derivative of with respect to its argument while denotes the derivative of with respect to its argument and the generic notation represents itself and some of its first- and second-order derivatives, whose variables to be differentiated are indicated by “" in Tables 1 and 2. Hereafter, we also adopt the similar notations for second-order derivatives of : denotes the derivative of with respect to its argument and denotes the derivative of with respect to its argument . In fact, for a simple check, the assumptions above over and are satisfied if is thrice continuously differentiable with respect to its corresponding arguments.

3.3.1 Small-time Well-posedness of Nonlocal Fully Nonlinear Nonlinear Systems

Before we present our main result, we stress that the standard linearization methods are not applicable for the nonlocal case. In the setting of local parabolic systems, 14 introduced a so-called “quasi-linearization method" and studied local existence for fully nonlinear parabolic problems by transforming fully nonlinear systems into quasi-linear systems. Noteworthily, 32, 63 utilized a variant of this method to investigate fully nonlinear PDEs or systems. The linearization method, which we propose to prove for Theorem 3.5 below, is substantially inspired by 34, 47. Although there are some previous works on how to linearize nonlinear equations or systems, it is still difficult to extend the existing methods from a local setting to a nonlocal setting. In fact, even for a nonlocal linear system (25), the literature is lack of its mathematical analysis, not to mention the nonlinear case and the conversion from nonlinearity to linearity.

Theorem 3.5 below is our main innovative result, which shows the (small-time) well-posedness of nonlocal fully nonlinear systems (1).

Theorem 3.5.

It should be noted that in the small-time setting, we only require the conditions of (30)-(33) of in an open ball while the range of is contained in with a smaller ball . For a pair that satisfies their coupled assumptions, Theorem 3.5 provides the local/maximally-defined (see Remark 3.6) well-posedness of (1). The (relaxed) local assumptions on facilitates a larger class of (1). From the proof of Theorem 3.5 (see (88)) and the example provided below, we find that the local solution always exists if since is an open set in . Hence, to check if (1) exists a local solution, it is more convenient to check if the conditions (30)-(33) of can be satisfied in a small open ball centered at the range of , instead of in . For the global solvability (well-posedness), we will discuss it in Subsection 3.3.2.

Remark 3.6 (Maximally defined solutions).

We have proven the local well-posedness of (1) in and thus the diagonal condition can be determined for . After which, the nonlocal fully nonlinear system (1) is reduced to a classical local fully nonlinear systems parameterized by . Then we take as initial time and as initial datum, we can extend the solution to a larger time interval up to the maximal interval. It is analogous to the process of identifying the global solution of nonlocal linear systems in the proof of Theorem 3.3. The procedure could be repeated up to a maximally defined solution , belonging to for any . The time region is maximal in the sense that if , then there does not exist any solution of (1) belonging to ; see Figure 3. An example of can be proposed similarly as in the local case; see 43 pp. 203. It is noteworthy that the problem of existence at large for arbitrary initial data is a difficult task even in the classical fully nonlinear case. The difficulty is caused by the fact that a priori estimate in a very high norm is needed to establish the existence at large. To this end, there will be severe restrictions on the nonlinearities. More details are discussed in 35, 43.

Remark 3.7 (Stability analysis).

Before we study the global well-posedness, we provide an example to understand the assumptions on and in Theorem 3.5. Without loss of generality, we assume that and the coefficients of (4) and (6) are

Then, it is clear that the optimun of the Hamiltonian is attained by . Moreover, according to (18), the equilibrium control is given by

Consequently, with a variable substitution, the (backward) equilibrium HJB equation can be reformulated forwardly as:

| (34) |

where . Finally, by our local well-posedness results (Theorem 3.5), there exists such that (34) is solvable in , if there exists a constant such that

-

1.

-

2.

-

3.

where is the nonlinearity of (34) and represents the remaining terms of excluding . In general, it is not necessary to identify the properties of nonlinearity in a large ball . According to the proof of Theorem 3.5, the local solution of (1) can arbitrarily approach to the initial data by choosing a small enough ; see (88). Consequently, if the domain, where nonlinearity satisfies these requirements in Theorem 3.5, contains an open ball centered at (i.e. ), then there exists a local solution for the nonlocal systems. It is clear that is locally Lipschitz and Hölder continuous. Moreover, for a large enough and , the three inequalities above hold such that (34) is solvable at least in a small time interval.

3.3.2 On the Global Well-posedness of Nonlocal Nonlinear Systems

In this subsection, we show that (1) is well-posed globally, i.e. , if a very sharp a priori estimate is available. Moreover, we introduce a class of nonlocal nonlinear system called nonlocal quasilinear system of the form (36) and we establish its global solvability under a growth condition.

In contrast with the nonlocal linear systems (25), where the (small-time) solution can be extended arbitrarily many times to a global solution over for any , it is possible for the nonlinear case (1) that the extension procedure is terminated at some . The dissatisfying result is caused mainly by the fact in the proof of Theorem 3.5 that in order to obtain a -contraction from to defined by , we need to strike a balance between and such that . In the extension procedure in view of Remark 3.6, it is possible that the solution blows up near . In this case, both and tend to infinity under the norm . From this perspective, it becomes clear that the inequality has restricted to be infinitely small. Consequently, the extension procedure is forced to stop to generate a maximally defined solution over instead of a global solution over the whole interval .

In fact, it has been an unavoidable problem in the study of differential equations. To extend the maximally defined solution from to , the key step is to show that the mapping is uniformly continuous in some sense such that an analytic continuation argument works. Next, inspired by 46, 52, we show that it is possible to have if a very sharp a priori estimate is available.

Theorem 3.8.

Generally speaking, in the proof of Theorem 3.5, the in the depends on since the -contraction operator via defined in a closed set of . Hence, the prior estimate of for all is not enough for the existence in the large. Instead, we need an estimate on the modulus of continuity of . Similar sufficient conditions to obtain a priori estimates like (35) for the classical PDEs/systems can be found in 35, 43. However, it is not straightforward to express such conditions in terms of coefficients and data of the local and nonlocal fully nonlinear system.

Next, we show that the desired sharp a priori estimate is available for a class of nonlocal nonlinear systems, namely nonlocal quasilinear systems, of the form:

| (36) |

Compared with (1), (36) is free of the highest order nonlocal term and is linear in the highest order local term . It is clear that (36) is a special case of (1). The nonlocal quasilinear systems are relevant from both theoretical and practical viewpoints, since they cover the equilibrium HJB systems of TIC SDG problems, where the diffusion of (4) is uncontrolled, i.e., . By leveraging Theorem 3.5 and Theorem 3.8 of nonlocal fully nonlinear systems (1), we aim to show that (36) is solvable globally under some technical conditions in the theorem below. In fact, our results have been the best in the existing literature on nonlocal PDEs/systems in terms of the global well-posedness issues.

Theorem 3.9.

Suppose that all coefficient functions of (36) belong to and satisfy (23), , and the nonlinearity has enough regularities required in (32) and (33), satisfies a linear growth condition: , and has its bounded first order partial derivatives with respect to and . Then, the nonlocal quasilinear system (36) admits a unique solution in .

As closing remarks of this section, we review our studies on nonlocal linear (25), quasilinear (36), and fully nonlinear systems (1) in parallel. Our analyses are based on the Banach fixed point arguments to first establish their small-time solvability and then extend the results to a longer time horizon, while the later extension faces different situations for different systems. In the case of nonlocal linear systems (25), a contractive mapping can be constructed by choosing a suitably small such that with a constant depending only on the data of (25). Hence, there is no issue as discussed at the beginning of Section 3.3.2 and thus the global well-posedness of (25) can be obtained without extra conditions. In contrast, the nonlocal nonlinear systems, including the quasilinear (36) and the fully nonlinear (1) systems, need to balance and such that . Through mathematical analyses, the for the quasilinear system (36) is quantified by while the fully nonlinear one is quantified by . This observation explains the different levels of difficulty when we establish their global existence; see Theorems 3.8 and 3.9. It is an important and promising research direction to rewrite the condition (35) in terms of the model coefficients of the original problem (1).

3.4 Well-posedness in a Weighted Space

In this subsection, we extend the main results in the previous subsections to a weighted space, which allows its elements (functions) as well as their partial derivatives grow exponentially in the spatial variable . Throughout this subsection, we consider the exponential weights, defined by for any , being any symmetric positive-definite matrix with eigenvalues in and . First of all, we introduce the following weighted norms

| (37) |

| (38) |

| (39) |

Next, before defining weighted spaces, we illustrate the following equivalence property.

By Lemma 3.10, the norms defined in (37)-(39) can be all denoted by an unified notation . Similar to Subsection 3.1, we can then define weighted norms and and weighted spaces , and . Although the norms defined in (37)-(39) are equivalent, it is useful to distinguish them since they have their own advantages. The first one (37) presents an intuitive understanding of functions with an exponential growth in the spatial argument, while the other two weighted norms (38) and (39) are convenient in showing some related conclusions in Theorem 3.12 below.

Next, we introduce a class of nonlinearities that extend the nonlinearity in Subsection 3.3 for the study of well-posedness in the weighted spaces.

Definition 3.11.

A pair of is appropriate if there exist , such that for any ,

-

(a)

while at belongs to ;

-

(b)

both and at belong to ;

-

(c)

-

(d)

, ;

-

(e)

and

where .

The conditions (a)-(e) in Definition 3.11 allow us to utilize the methodologies in Section 3.2-3.3, including the linearization method and the fixed-point argument, to study nonlocal fully nonlinear systems in a weighted space. The first three conditions (a)-(c) guarantee that the mapping , defined by , is well-defined. Moreover, with (d) and (e), we can prove that it is contractive.

Now, we are ready to show the extension of the well-posedness results for nonlocal systems in a weighted space.

Theorem 3.12.

All well-posedness results for nonlocal systems in Subsections 3.2-3.3 can be extended to the setting with weighted spaces defined in this subsection. Specifically, we have

- 1.

- 2.

-

3.

Assume further that for some finite constant across all , then either the pair of is not appropriate or . Consequently, the nonlocal quasilinear system (36) is globally solvable.

In this refined framework, although we allow the nonhomogeneous term and the initial data to increase exponentially in the spatial variable (more specifically, and ), it is still required that all coefficients of defined in (22) belong to . This also induces the condition (b) of Definition 3.11 that requires that and at belong to ordinary normed spaces instead of the weighted ones. Nevertheless, these conditions are necessary for our analyses, including the linearization method adopted in the later analysis of solvability of nonlocal nonlinear systems in the weighted spaces, and satisfied by our first financial example in Section 4.

Remark 3.13.

[Potential relaxations] Echoing our discussion at the end of Section 2.3, we establish the first analytical framework for such emerging type of nonlocal PDEs/systems with a two-time-variable structure. Hence, we have to require some additional conditions and regularities for the nonlocal setting to support our proofs. From this perspective, one may work towards lifting the restrictions so as to embrace a larger class of nonlocal systems. It should be noticed that the main restrictions originate from the limitations on coefficients of the nonlocal linear operator defined in (22). Here, we list some promising future extensions. We first note that this paper adopts a concept of strongly ellipticity conditions (23)-(24), (30)-(31), and (c) in Definition 3.11. Following 14, 37, 16, the conditions can be substituted so as to contain a larger class of parabolic systems (in the sense of Petrowski-type). Moreover, we may substantially improve the results by modifying the underlying norms and spaces to obtain a more general PDE theory which allows degenerate coefficients.

4 Well-posedness of Equilibrium HJB Systems and Examples

The previous two sections have established the linkage between the TIC SDGs and equilibrium HJB systems and the well-posedness of nonlocal parabolic systems that nest the equilibrium HJB systems. This section intends to summarize our results in the context of TIC SDGs and provide two examples (in finance), the induced nonlocal fully nonlinear systems of which are globally solvable under some technical conditions in Propositions 4.2 and 4.4.

Let us denote defined in (20), where , and . Then we have the following theorem, which follows directly Proposition 3.1 and Theorems 3.5 and 3.9.

Theorem 4.1.

The regularity requirements of and in Theorem 4.1 characterize the “needed regularity" of in Assumption 9. By the implied existence of the NE point at each time point from Assumption 9, it is clear that the Hamiltonian satisfies (30), (32), and (33). We only need to check if and jointly satisfy the condition (31). Especially for a nonlocal quasilinear system (i.e. a TIC SDG with controls on drift only), it is easy to see that conditions (30)-(31) hold. Hence, with smooth enough coefficients in (4)-(6), the corresponding equilibrium HJB system satisfies the requirements in Theorem 4.1. Finally, based on the conjectures in Section 2.3, we may conclude that the associated TIC SDG admits a TC-NE point and the TC-NE value function for . Analogously, Theorem 3.12 supports that all results in Theorem 4.1 still hold in a weighted space.

4.1 Financial Examples

In this subsection, we provide two examples of TIC SDGs among players on for an arbitrary positive integer and an arbitrary large time , the first one of which studies how the investors (players) choose their own optimal investment strategies to increase their own exponential utility and the second one of which studies the optimal investment and consumption strategy pairs of investors that optimize their own power utility. These two examples showcase two different uses of our well-posedness results in Subsection 3.4. The first example satisfies all the conditions in our refined (weighted-norm) framework and thus the corresponding TIC problem is globally solvable over the whole time horizon . The second example is, however, not covered by our framework due to its degeneracy property, but this interesting and relevant example is still considered here while it shows the necessity of extending our analytic framework from the non-degenerate setting to a degenerate one; see also the discussion in Remark 3.13. Though the second example is beyond our general framework, we make another problem-specific attempt in the similar spirit of the proof of Theorem 3.8. Specifically, with some suitable ansatzs of solutions, both examples admit explicit expressions of (18) and (20) while the latter can be further reduced to ordinary differential equation (ODE) systems. We can then show the global solvability of these ODE systems and thus we obtain the global solvability of the two listed examples.

We first introduce the general setup for the two examples. Suppose that the players have similar interests, e.g., a risk investment fund managed by investors (managers). To maintain and increase their own utility, each investor needs to study their own optimal investment and consumption strategy. Consider a market model in which there are one bond with the riskless interest rate and some risky assets while the -th investor has estimated the appreciation rate of his/her return on investment (ROI) by and its volatility by . Further assume that the investors’ ROIs are uncorrelated, the yield rate vector of the investors is characterized by

where is a diagonal matrix with main diagonal elements of , , and . Denoted by the dollar amounts managed by the -th investor and the aggregated wealth process (from this perspective, we are similarly considering a problem by a fund of funds), we can obtain the following FSDE for :

| (41) |

where and with the consumption rate of the -th investor valued in , is valued in , and will be specified for our examples. For any fixed , the admissible set of investment-consumption strategy pairs is then defined as the set of progressively measurable processes such that and for and that the FSDE (41) has a strong solution with , -a.s., for .

Next, to characterize the investors’ preferences, let be the adapted solution to the following BSDE:

| (42) |

where the generator and terminal condition are both deterministic -valued functions, and they will be specified in the study of different utility problems. Then, we define the recursive utility functional of the -th investor for as follows:

Consequently, the problem of maximizing for is a TIC SDG since and both depend on the initial time point . Note that in Section 2, we illustrate with an SDG with minimization while it is equivalent to considering maximization. It is noteworthy that the -th functional is a Uzawa-type differential utility being not only recursive (in the sense that it depends on itself) but also dependent on other investors’ utility functionals . It is sensible because enormous experiments in behavioral economics/finance show that people’s assessment on their wellbeing is relative rather than absolute. Moreover, the controlled FBSDEs of the investors are coupled together through and in the BSDE and in the FSDE. Furthermore, compared to the existing literature on the well-posedness results, we allow the diffusion of the wealth process to be controlled.

4.1.1 TIC Merton Problem with Exponential Utility and Zero Consumption

In the first example, we assume that

| (43) |

where and are - and -valued continuous and positive functions, respectively. Next, we will show that this example can be analyzed within our framework in Subsection 3.4. Specifically, in order to show the well-posedness of solutions to the TIC SDG (41)-(43), the main steps are listed as follows:

- 1.

-

2.

prove the global well-posedness of solutions of in the case of such that the mapping from to the solution is well-defined;

-

3.

show that admits a unique analytic continuation at such that the problem (i.e. ) has global existence and uniqueness of solutions as well.

These three steps not only show the global well-posedness of solutions of nonlocal HJB system and the TIC SDG but also give explicit representations for equilibrium strategies (18) and equilibrium value functions of (20). We cannot directly analyze as its nonlinearity is not regular enough and thus we parametrize the problem such that the nonlinearity of with satisfies the regularity conditions in our framework.

First of all, it is more convenient to consider a transformed state for the dynamics of (41) before our analyses. By Corollary 5.6 of 74, it is clear that

Consequently, without loss of generality, let us consider a modified version of (41) with the following form:

| (44) |

where and .

Step 1: A family of parameterized problems . Next, let us consider a family of problems (BSDEs) parameterized by an external parameter ,

| (45) |

where denotes the Kronecker product, denotes the Hadamard product, , , and , , , and are all -valued continuous functions that will be specified later. It is clear that (45) reduces to (43) when and . Our later specification will also parametrize and with and when . Thus in this case, (45) is actually parameterized by a single parameter .

It is noteworthy that there are multiple embedding schemes while any of them can work out the well-posedness of solutions of the problem (41)-(43) as long as the mapping from to the solution of is well-defined and is at least Cauchy-continuous at the point that reduces the parametrized problem to . Moreover, the fact about whether the problem is well-posed is free of the choice of the embedding scheme. We will show that the embedding (45) with (50) facilitate Step 2 and Step 3. The relationship between parameterized data and solutions was discussed in the earlier stability analysis of nonlocal systems; see Remark 3.7.

Step 2. The well-definedness of with . According to the definitions of formulated by controlled FBSDEs (44)-(45), the Hamiltonian system of the players has the form: for ,

Maximizing the above with respect to with fixed , , and yields

where and . Thus, eventually, the equilibrium strategy will be given by

| (46) |

with ( is suppressed) being the solution to an equilibrium HJB system of the form:

| (47) |

It is equivalent to solving the following forward problem:

| (48) |

Next, let us consider the partial derivatives of the nonlinearity of (48) with respect to its arguments in order to verify its regularities. The nonlinearity of (48) is denoted by . After a rather lenghty but staightforward calculation, we can obtain all partial derivatives in Table 1 and 2, which are all listed in Appendix B. Consequently, for the initial condition , one can verify that the pair of is appropriate in the sense of Definition 3.11 for some suitable and ; see (50). Hence, our well-posedness results in Subsection 3.4 promise that there exist and a unique solution satisfying (48) in . Equivalently, the backward problem (47) is solvable as well in .

In order to find an explicit solution to (47) and show its global solvability in the whole time horizon , we consider the following ansatz:

| (49) |

for some suitable , and . Then we have and . Furthermore, let us assume that

| (50) |

where is a given continuously differentiable and positive function. Under the assumptions of (50), we have for . Subsequently, by simple calculation, and solve the following ODE systems, respectively,

| (51) |

where and . Moreover, . By the classical theory of ODE systems, systems (51) admit a unique solution for since () are both bounded. Furthermore, the ansatz solution (49) of (47) can be represented by

| (52) |

where is the fundamental matrix of the -th ODE system of (51), the associated inverse matrix, and

| (53) |

in which is identity matrix. Note that (53) converges absolutely for every and uniformly on every compact interval in . In particular for , if the matrix satisfies the Lappo–Danilevskii condition (see Remark 4.3), then .

Note that of (52) does not blow-up at for any such that we can update a new terminal condition at . Furthermore, thanks to (50), the uniformly elliptic conditions, the locally Lipschitz and Hölder continuity still hold within a small open ball centered at the range of the updated data. Consequently, one can repeat indefinitely the solving procedure up to a global solution for (47) over . With our well-posedness results of nonlocal systems in Subsection 3.4, we show that the mapping from the parameter into the solution of (47), i.e. , is well-defined.

Step 3. Analytic continuation of at . For the original problem , i.e. , our well-posedness results of nonlocal systems are not feasible even in a small time interval since the locally Lipschitz and Hölder continuity conditions are violated for some derivatives of the nonlinearity . However, for any fixed , we have shown that the mapping is well-defined and has an explicit formula (52). From which, we can easily see that the mapping is at least uniformly continuous in and thus we can extend it at uniquely. Consequently, we can obtain the unique solution for in , . Furthermore, the closed-loop TC-NE point and the corresponding TC-NE value function of the TIC SDG (41)-(43) have the following explicit representations:

| (54) |

Indeed, by directly making an ansatz for the solution of (i.e. (44)-(43)), we can still obtain the same explicit solution (54). However, as we stressed before, our well-posedness results do not cover the problem since (50) and (51) induce when . Hence, it is necessary to embed into a family of problem ().

Finally, let us summarize our results in the following proposition.

Proposition 4.2.

Remark 4.3.

The matrix satisfies the Lappo-Danilevskii condition, which means that it commutes with its integral, i.e. . Let us list four cases in which the condition holds, (1) ; (2) ; (3) is a diagonal matrix; (4) and commute for all , , and .

4.1.2 TIC Merton Investment-Consumption Problem with Power Utility

In our second example, we assume that

| (55) |

where and are both -valued functions and is -valued continuous and positive function. In this case, each player () needs to choose an investment and consumption strategy pair valued in to optimize their own power utility. With a specific model, we can obtain explicit expressions of (18) and (20) while the latter can be further reduced to an ordinary differential equation (ODE) system with an ansatz. In the similar spirit of the proof of Theorem 3.8, we can show the global solvability of the ODE system and thus we obtain the global well-posedness of (20). However, although our results are applicable to the state process with controlled drift and volatility, which is the case of this example, they do not cover this example due to its degeneracy property. Moreover, since the power utility function is defined over , we also need the constraint that the solution of (41) is almost surely nonnegative, i.e. . Such a constraint is not necessary for our first example since the domain of exponential utility function is .

According to the definitions of formulated by controlled FBSDEs (41)-(42) with (55), the Hamiltonian system of the players has the form: for ,

where and represent the -entry of matrices and , respectively. Maximizing the above with respect to and with fixed , , , and yields

Thus, eventually, the equilibrium strategy will be given by

| (56) |

for with being the solution to an equilibrium HJB system:

| (57) |

The HJB equations system of (57) are coupled with each other via the equilibrium strategy and the recursive dependence on in the generators of (55), i.e. the terms of of (57). By substituting (56) into the Hamiltonian, (57) becomes

| (58) |

It is clear that the first order derivative of the nonlinearity of (58) with respect to at would be degenerate. Consequently, our well-posedness results are not applicable to analyze its solvability. Thus, this second example is more of an inspiration and serves as an indication of the validity of the general (degenerate) case. To facilitate our analysis of (57), we need a more explicit form of and thus inspired by its terminal condition, we consider the following ansatz:

| (59) |

for some suitable , . Then we have and by simple calculation, satisfies the following system of ODEs:

Denoting by , the ODE system above becomes

| (60) |

where

.

According to the classical theory of system of ODEs, the fundamental matrix makes it possible to write every solution of the inhomogeneous system (60) in the form of Cauchy’s formula

| (61) |

where is the inverse matrix of , and

| (62) |

in which is identity matrix. Note that (62) converges absolutely for every and uniformly on every compact interval in . Taking gives us that

By introducing , we have

| (63) |

which is a nonlinear integral system for the unknown function . Once the diagonal value can be determined uniquely, there exists a unique solution from the integral equation (61) of . By (56) and (59), the equilibrium investment-consumption strategy and equilibrium value functions can be represented with in (63) as follows:

| (64) |

The preliminary analyses above provide us the analytical form of the TC-NE value function, while the key is to make use of the ansatz (59) to transform the nonlocal PDE system (57) into a classical (local) ODE system (60) (and equivalently, an conventional integral system (63)). We can then again use the contraction mapping arguments to establish the local well-posedness of (63). Moreover, to prove its solvability in an arbitrary large time interval, we shall show the boundedness of the solution of (63) such that the extension procedure can be completed. The following proposition supplements the mathematical details of the above.

Proposition 4.4.

Suppose that , , and are continuously differentiable, then there exists such that the TIC SDG problem (41)-(42) with (55) admits a closed-loop TC-NE point given by (56) and the corresponding TC-NE value function over . Moreover, if is a diagonal matrix and and satisfy (124)-(125), then , which implies that the TIC SDG problem (41)-(42) with (55) is globally solvable.

Remark 4.5.

For the condition (125), 73, 70 have investigated the case where for and . As they showed, the continuous differentiability of in can guarantee (125) for this special case. Moreover, in contrast to Proposition 4.2 that provides the existence and uniqueness of solutions of equilibrium HJB system (47), Proposition 4.4 only promises the existence of solutions for the TIC SDG problem (41)-(42) with (55). Since the equilibrium HJB system (58) cannot be covered by the current framework, we merely constructed one solution for the power utility model via the ansatz (59).

Our TIC SDG examples and results generalize the ones in the existing literature. Specifically, in the case of , the TIC SDG is reduced to the TIC stochastic control problem in 70 with recursive utility functional and in 73 with non-recursive one. Noteworthy is that the well-posedness results in 73, 70 do not allow the diffusion to be controlled. Moreover, when , , , and are all independent of , the problem is reduced to the TC case with recursive utility functional studied in 31. Based on these restrictions, if is constant and , the examples are further reduced to the classical Merton problem in 50.

5 Feynman–Kac Formula for Nonlocal Parabolic Systems

In this section, we provide a nonlocal version of the Feynman–Kac formula, which establishes a closed link between the solutions to a flow of FBSDEs in the multidimensional case and nonlocal second-order parabolic systems. All the proofs are deferred to A.

Before we present the formula, we reveal more properties of the solution to (1). Like the classical theory of parabolic systems, the stronger conditions imposed to the nonlinearity and the given data suggest the higher regularity of the corresponding solutions of nonlocal higher-order systems.

Lemma 5.1.

Let and be both non-negative integers satisfying . Suppose that is smooth and regular enough and , then there exist and a unique in satisfying (1) with for all .

Next, to connect parabolic systems with the theory of FBSDEs, we consider a second-order backward nonlocal fully nonlinear system with of the form:

| (65) |

where has enough regularities and is suitable in the sense that is a subset of the time interval for the maximally defined solution of (65). The following theorem reveals the relationship between the solutions to a nonlocal fully nonlinear second-order system and to a flow of 2FBSDEs (67).

Theorem 5.2.

Suppose that has enough regularities, , and . Then, (65) admits a unique solution that is first-order continuously differentiable in and third-order continuously differentiable with respect to in . Moreover, for any , let

where and the operator is defined by

then the family of random fields is an adapted solution of the following flow of 2FBSDEs:

| (67) | ||||

where is defined by

| (68) |

with the definition of

We make three important observations about the stochastic system (67): (I) When the generator is independent of diagonal terms, i.e. , , and , the flow of FBSDEs (67) is reduced to a family of 2FBSDEs parameterized by , which is exactly the 2FBSDEs in 33 and equivalent to the ones in 7 for any fixed ; (II) (67) is more general than the systems in 68, 64, 20, 42 since it allows for a nonlinearity of by increasing the dimensions and/or introducing an additional SDE of as well as diagonal terms in almost arbitrary way; (III) Theorem 5.2 shows how to solve the flow of multidimensional 2FBSDEs (67) from the perspective of nonlocal systems. Inspired by 7, 59, the opposite implication of solutions (from 2FBSDEs to PDE) is likely valid by establishing the well-posedness of (67) in the theoretical framework of SDEs. However, it is beyond the scope of this paper, while we will prove the existence and uniqueness of (67) in our future works.

6 Conclusions

We provided the conditions on the nonlocal higher-order systems, under which the global well-posedness of the linear, quasilinear, fully nonlinear systems can be proved. The results are significant for a general class of nonzero-sum TIC SDGs that we formulated and discussed in Section 2. Moreover, we present a nonlocal multidimensional version of a Feynman–Kac formula. It provides new insights into the studies of a flow of 2FBSDEs or 2BSVIEs.

We presented two immediate applications (SDG and SDE) drawing upon our main results from the PDE perspective. In fact, the study of systems of differential equations is crucial for developing other mathematical tools (in PDE), such as quasilinearization among many others, in a new environment (here, with nonlocality). The quasilinearization is a common technique in the classical (fully nonlinear) PDE problems. Specifically, under suitable regularity assumptions, we can differentiate the fully nonlinear equation of an unknown function with respect to each state variable and yield an induced quasilinear system for . Before taking advantage of the mathematical results of quasilinear systems, it is crucial to verify the equivalence between the original fully nonlinear equation for and the induced quasilinear system for . The verification, however, requires the existence and uniqueness of (nonlocal) linear systems. Hence, our study for nonlocal linear systems can serve as a prerequisite for one to develop quasilinearization methods for nonlocal differential equations.

Acknowledgements

The authors are thankful to two anonymous reviewers for constructive comments that helped improve the paper. Chi Seng Pun gratefully acknowledges Ministry of Education (MOE), AcRF Tier 2 grant (Reference No: MOE-T2EP20220-0013) for the funding of this research. Data sharing is not applicable to this paper as no dataset was generated or analyzed during this study.

References

- Basak and Chabakauri 2010 Basak, S. and G. Chabakauri, 2010: Dynamic mean-variance asset allocation. Review of Financial Studies, 23, no. 8, 2970–3016, doi:10.1093/rfs/hhq028.

- Bensoussan and Frehse 2000 Bensoussan, A. and J. Frehse, 2000: Stochastic games for N players. Journal of Optimization Theory and Applications, 105, no. 3, 543–565, doi:10.1023/a:1004637022496.

- Björk et al. 2017 Björk, T., M. Khapko, and A. Murgoci, 2017: On time-inconsistent stochastic control in continuous time. Finance and Stochastics, 21, no. 2, 331–360, doi:10.1007/s00780-017-0327-5.

- Björk and Murgoci 2010 Björk, T. and A. Murgoci, 2010: A general theory of Markovian time inconsistent stochastic control problems. SSRN, doi:10.2139/ssrn.1694759.

- Björk and Murgoci 2014 — 2014: A theory of Markovian time-inconsistent stochastic control in discrete time. Finance and Stochastics, 18, no. 3, 545–592, doi:10.1007/s00780-014-0234-y.

- Björk et al. 2014 Björk, T., A. Murgoci, and X. Y. Zhou, 2014: Mean-variance portfolio optimization with state-dependent risk aversion. Mathematical Finance, 24, no. 1, 1–24, doi:10.1111/j.1467-9965.2011.00515.x.

- Cheridito et al. 2007 Cheridito, P., H. M. Soner, N. Touzi, and N. Victoir, 2007: Second-order backward stochastic differential equations and fully nonlinear parabolic PDEs. Communications on Pure and Applied Mathematics, 60, no. 7, 1081–1110, doi:10.1002/cpa.20168.

- Dai et al. 2021 Dai, M., H. Jin, S. Kou, and Y. Xu, 2021: A dynamic mean-variance analysis for log returns. Management Science, 67, no. 2, 1093–1108, doi:10.1287/mnsc.2019.3493.

- Ekeland and Lazrak 2006 Ekeland, I. and A. Lazrak, 2006: Being serious about non-commitment: subgame perfect equilibrium in continuous time.

- Ekeland and Lazrak 2010 — 2010: The golden rule when preferences are time inconsistent. Mathematics and Financial Economics, 4, no. 1, 29–55, doi:10.1007/s11579-010-0034-x.

- Ekeland et al. 2012 Ekeland, I., O. Mbodji, and T. A. Pirvu, 2012: Time-consistent portfolio management. SIAM Journal on Financial Mathematics, 3, no. 1, 1–32, doi:10.1137/100810034.

- Ekeland and Pirvu 2008 Ekeland, I. and T. A. Pirvu, 2008: Investment and consumption without commitment. Mathematics and Financial Economics, 2, no. 1, 57–86, doi:10.1007/s11579-008-0014-6.

- Espinosa and Touzi 2015 Espinosa, G.-E. and N. Touzi, 2015: Optimal investment under relative performance concerns. Mathematical Finance, 25, no. 2, 221–257, doi:10.1111/mafi.12034.

- Ėǐdel’man 1969 Ėǐdel’man, S. D., 1969: Parabolic Systems. North-Holland and Pub. Co.Wolters-Noordhoff, Amsterdam, Groningen.

- Frederick et al. 2002 Frederick, S., G. Loewenstein, and T. O’donoghue, 2002: Time discounting and time preference: A critical review. Journal of Economic Literature, 40, no. 2, 351–401, doi:10.1257/jel.40.2.351.

- Friedman 1964 Friedman, A., 1964: Partial Differential Equations of Parabolic Type. 1stnd ed., Prentice-Hall, Englewood Cliffs, N.J.

- Friedman 1972 — 1972: Stochastic differential games. Journal of Differential Equations, 11, no. 1, 79–108, doi:10.1016/0022-0396(72)90082-4.

- Friedman 1976 — 1976: Stochastic Differential Equations and Applications, volume 2 of Probability and Mathematical Statistics. Academic Press.

- Hamaguchi 2021a Hamaguchi, Y., 2021a: Extended backward stochastic Volterra integral equations and their applications to time-inconsistent stochastic recursive control problems. Mathematical Control & Related Fields, 11, no. 2, 197–242, doi:10.3934/mcrf.2020043.

- Hamaguchi 2021b — 2021b: Small-time solvability of a flow of forward-backward stochastic differential equations. Applied Mathematics & Optimization, 84, no. 1, 567–588.

- Han et al. 2021 Han, B., C. S. Pun, and H. Y. Wong, 2021: Robust state-dependent mean-variance portfolio selection: A closed-loop approach. Finance and Stochastics, 25, no. 3, 529–561, doi:10.1007/s00780-021-00457-4.

- Han et al. 2022 — 2022: Robust time-inconsistent stochastic linear-quadratic control with drift disturbance. Applied Mathematics & Optimization, 86, no. 1, doi:10.1007/s00245-022-09871-2.

- He and Jiang 2021 He, X. D. and Z. L. Jiang, 2021: On the equilibrium strategies for time-inconsistent problems in continuous time. SIAM Journal on Control and Optimization, 59, no. 5, 3860–3886, doi:10.1137/20m1382106.

- He and Zhou 2022 He, X. D. and X. Y. Zhou, 2022: Who are I: Time inconsistency and intrapersonal conflict and reconciliation. Stochastic Analysis, Filtering, and Stochastic Optimization, G. Yin and T. Zariphopoulou, Eds., Springer, Cham, 177–208, a Commemorative Volume to Honor Mark H. A. Davis’s Contributions.

- Hernández and Possamaï 2021 Hernández, C. and D. Possamaï, 2021: A unified approach to well-posedness of type-I backward stochastic Volterra integral equations. Electronic Journal of Probability, 26, doi:10.1214/21-ejp653.

- Hernández and Possamaï 2023 — 2023: Me, myself and I: A general theory of non-Markovian time-inconsistent stochastic control for sophisticated agents. The Annals of Applied Probability, 33, no. 2, 1396–1458, doi:10.1214/22-aap1845.

- Hu et al. 2012 Hu, Y., H. Jin, and X. Y. Zhou, 2012: Time-inconsistent stochastic linear–quadratic control. SIAM Journal on Control and Optimization, 50, no. 3, 1548–1572, doi:10.1137/110853960.

- Hu et al. 2017 — 2017: Time-inconsistent stochastic linear-quadratic control: Characterization and uniqueness of equilibrium. SIAM Journal on Control and Optimization, 55, no. 2, 1261–1279, doi:10.1137/15m1019040.

- Kahneman and Tversky 1979 Kahneman, D. and A. Tversky, 1979: Prospect theory: An analysis of decision under risk. Econometrica, 47, no. 2, 263, doi:10.2307/1914185.

- Karoui et al. 1997 Karoui, N. E., S. Peng, and M.-C. Quenez, 1997: Backward stochastic differential equations in finance. Mathematical Finance, 7, no. 1, 1–71, doi:10.1111/1467-9965.00022.

- Karoui et al. 2001 Karoui, N. E., S. Peng, and M. C. Quenez, 2001: A dynamic maximum principle for the optimization of recursive utilities under constraints. The Annals of Applied Probability, 11, no. 3, 664–693.

- Khudyaev 1963 Khudyaev, S., 1963: The first boundary-value problem for non-linear parabolic equations. Doklady Akademii Nauk, Russian Academy of Sciences, volume 149, 535–538.

- Kong et al. 2015 Kong, T., W. Zhao, and T. Zhou, 2015: Probabilistic high order numerical schemes for fully nonlinear parabolic PDEs. Communications in Computational Physics, 18, no. 5, 1482–1503, doi:10.4208/cicp.240515.280815a.

- Kruzhkov et al. 1975 Kruzhkov, S. N., A. Castro, and M. L. Morales, 1975: Schauder-type estimates and existence theorems for the solution of basic problems for linear and nonlinear parabolic equations. Doklady Akademii Nauk, Russian Academy of Sciences, volume 220, 277–280.

- Krylov 1987 Krylov, N. V., 1987: Nonlinear Elliptic and Parabolic Equations of the Second Order, volume 7 of Mathematics and its Applications. 1nd ed., Springer Netherlands.

- Lacker and Zariphopoulou 2019 Lacker, D. and T. Zariphopoulou, 2019: Mean field and -agent games for optimal investment under relative performance criteria. Mathematical Finance, 29, no. 4, 1003–1038, doi:10.1111/mafi.12206.

- Ladyenskaja et al. 1968 Ladyenskaja, O. A., V. A. Solonnikov, and N. N. Ural’ceva, 1968: Linear and Quasi-linear Equations of Parabolic Type. 1stnd ed., American Mathematical Society.