Improving Nonparametric Classification via Local Radial Regression with an Application to Stock Prediction

Abstract

For supervised classification problems, this paper considers estimating the query’s label probability through local regression using observed covariates. Well-known nonparametric kernel smoother and -nearest neighbor (-NN) estimator, which take label average over a ball around the query, are consistent but asymptotically biased particularly for a large radius of the ball. To eradicate such bias, local polynomial regression (LPoR) and multiscale -NN (MS--NN) learn the bias term by local regression around the query and extrapolate it to the query itself. However, their theoretical optimality has been shown for the limit of the infinite number of training samples. For correcting the asymptotic bias with fewer observations, this paper proposes a local radial regression (LRR) and its logistic regression variant called local radial logistic regression (LRLR), by combining the advantages of LPoR and MS--NN. The idea is quite simple: we fit the local regression to observed labels by taking only the radial distance as the explanatory variable and then extrapolate the estimated label probability to zero distance. The usefulness of the proposed method is shown theoretically and experimentally. We prove the convergence rate of the risk for LRR with reference to MS--NN, and our numerical experiments, including real-world datasets of daily stock indices, demonstrate that LRLR outperforms LPoR and MS--NN.

Keywords: Nonparametric classification, Bias correction, Stock prediction

1 Introduction

Predicting a query’s label from observed pairs of covariates and their labels is called supervised classification, and it has played an indispensable role in machine learning and statistics for long decades. For instance, medical diagnosis (Soni et al.,, 2011) predicts disease from a medical image, spam-mail filtering (Cristianini and Shawe-Taylor,, 2000) determines whether a mail is spam or not via texts in the mail, and so on; as is well known, there is a wide range of real-world applications.

For this supervised classification problem, many existing studies employ a simple two-step procedure: One first estimates the label probabilities by regression methods, and second applies a classifier so as to output some labels whose estimated probabilities are large enough (Devroye et al.,, 1996; Samworth,, 2012). The regression in the first step is compatible with arbitrary regression methods. To name a few, we may employ a logistic regression (Hastie et al.,, 2001; Bishop,, 2006), kernel smoother (Nadaraya,, 1964; Tsybakov,, 2009), -nearest neighbor (-NN) estimator (Fix and Hodges,, 1951; Cover and Hart,, 1967), and so forth including highly-expressive parametric approaches using neural networks (NN; Dreiseitl and Ohno-Machado,, 2002; Goodfellow et al.,, 2016). As they each have their own strengths, we need to choose one or aggregate some of them as circumstances dictate.

Amongst these regression approaches, an advantage of nonparametric methods such as kernel smoother and -NN is that they possess both theoretical tractability and high expressive power, i.e., they can approximate any form of representing the label probability for a query when is a Lipschitz function; is a binary response variable indicating the label if . Here and denote the conditional expectation and probability, respectively, given . The asymptotic higher-order biases of kernel smoother and -NN are keenly evaluated and the bias correction has also been developed. In theory, the bias-corrected estimators attain faster convergence than highly-expressive parametric models such as neural networks, when the specific form of the ground-truth function is unknown. See, e.g., Fan and Gijbels, (1996) for further applications of such bias-corrected estimators. More specifically, the asymptotic biases in the kernel smoother and -NN are corrected by local polynomial regression (LPoR; Fan and Gijbels,, 1996; Tsybakov,, 2009) and multiscale -NN (MS--NN; Okuno and Shimodaira,, 2020), respectively, where they are based on a similar idea: LPoR and MS--NN compute local regression (Loader,, 2006) around the query, fitting a parametric model of the asymptotic bias, and extrapolating it towards the query for the bias to be eradicated.

While LPoR and MS--NN are based on the similar idea, they are different in their response variable and explanatory variable (Table 1). Local regression function in LPoR models locally around the query ; is estimated by with at each , and it predicts the raw outcome by estimating its label probability from the difference of covariates between the -th sample and the query . On the other hand, in MS--NN predicts the -NN estimator at each from the radial distance , where denotes the index of -th nearest sample to the query; thus, are ordered distances, and is the average of the responses . Despite their theoretical optimality, they both rely on asymptotic theory, meaning that they consider the limit of the infinite number of observations for training. They do not perform as well as we expect in practical, real-world situations.

| Response var. | Explanatory var. | Regression func. | |

|---|---|---|---|

| Local Poly. Reg. (LPoR) | |||

| Multiscale -NN (MS--NN) | |||

| Proposed LRR |

In these circumstances, we provide the following contributions:

-

•

(Methodology) In Section 3, we propose a local radial regression (LRR) and its logistic regression variant called local radial logistic regression (LRLR), by combining the advantages of LPoR and MS--NN. LRR, which includes LRLR as a special case, predicts (i) the independent raw outcomes by estimating its label probability directly as well as LPoR, using (ii) the regression function of the radial distance as well as MS--NN. The proposed LRR is expected to be trained with fewer observations for the following reasons: (i’) predicting independent raw outcomes is easier than predicting mutually-dependent -NN estimators as we can ignore the covariance of the outcomes, and (ii’) training the regression function of -dimensional radial component is easier as it includes fewer parameters than that of the -dimensional raw covariate . For predicting at , we do not need the “full model” with all the variables in but the model with only suffices; thus, the proposed LRR is preferable according to the principle of simplicity, i.e., Occam’s Razor. Note that most of our argument applies to a real-valued response with , but we focus on the binary response in this paper.

-

•

(Theory) In Section 3.3, we prove the convergence rate of the point-wise -risk for the proposed LRR. The obtained rate is compatible with those of LPoR and MS--NN.

-

•

(Experiments) In Section 4, our numerical experiment shows that LRLR outperforms LPoR and MS--NN. In Section 5, we also apply LRLR to real-world datasets of daily stock indices called S&P 500, S&P/TSX, EURO STOXX 50, FTSE 100, DAX, CAC 40, TOPIX, and Hang Seng, by following Nakagawa et al., (2018). We classify whether month-end closing prices of target months are going up or down by LRLR, by comparing to the previous fluctuation patterns of stock indices. The predictive classification accuracy is improved from existing methods.

This paper is partially based on a short paper of ours (Cao et al.,, 2021), published in the proceedings of an annual domestic meeting of the Japanese Society for Artificial Intelligence (JSAI).

Organization of this paper:

Background of this study, including the descriptions of the existing kernel smoother, -nearest neighbor (-NN), local polynomial regression (LPoR), and multiscale -NN (MS--NN), is explained in Section 2. The proposed local radial regression (LRR), local radial logistic regression (LRLR), and related discussions are described in Section 3. Numerical experiments on synthetic datasets are conducted in Section 4, application to real-world datasets is shown in Section 5, and we conclude this paper in Section 6.

2 Background

In this section, we explain the background of this study. Problem setting is described in Section 2.1, and notation is shown in Section 2.2. Kernel smoother and -NN are described in Section 2.3, local polynomial regression and multiscale -NN correcting the asymptotic biases of the kernel smoother and -NN are shown in Section 2.4 and 2.5, respectively.

2.1 Problem Setting

Let be the sample size and be the dimensionality of the covariate. Our dataset consists of for , that are i.i.d. with a distribution . is called a covariate and is called a label (or more generally, outcome), where is also called label probability. The goal of supervised classification is to learn a classifier using the observation , so that predicts for . In particular, this paper considers a plug-in type classifier

| (1) |

equipped with the estimated label probability by regression function (see, e.g., Tsybakov, (2009), Samworth, (2012), and Okuno and Shimodaira, (2020)). A classifier using the ground-truth label probability is called Bayes-optimal classifier (Devroye et al.,, 1996). Herein, this paper discusses estimating the regression function , so as to approximate the ground-truth .

2.2 Notation

In the remainder of this paper, we employ the following symbols. Let be the set for any positive integer . for a vector . for , i.e., the maximal integer that is strictly smaller than ; for example, , , so this is slightly different from the typical definition of the floor function with . Given a query , indices of the observed covariates are rearranged to so that distances are ordered as . Then we define,

| (2) |

for . -dimensional ball of radius is defined as . denotes a pair of random variables following a distribution throughout this paper, and the conditional label probability with given is denoted by . denote sets of non-negative and positive real values, respectively.

2.3 Kernel Smoother and -NN

For estimating the label probability , a kernel smoother (KS; Nadaraya,, 1964; Tsybakov,, 2009) and -nearest neighbour estimator (-NN; Fix and Hodges,, 1951; Cover and Hart,, 1967) are defined by

| (3) | ||||

| (4) |

respectively, where and are hyper-parameters. is called bandwidth. Both of these two estimators take average of the observed labels , whose observed covariates are inside the balls and , respectively; these two estimators are compatible if . While the boxcar kernel in the kernel smoother (3) can be replaced with other types of kernel function (see Tsybakov, (2009)), this paper considers only the boxcar case for simplicity.

In theory, the convergence rate of the plug-in classifier (1) equipped with the kernel smoother is discussed in Hall and Kang, (2005), while the convergence rate for classifier using the -NN estimator is also proved in Chaudhuri and Dasgupta, (2014). These two plug-in classifiers attain the same optimal rate if the ground-truth function is Lipschitz but not differentiable. If the ground-truth function is highly-smooth (e.g., is twice-differentiable, so the target function class is more restricted), the theoretical efficiency limit for estimating is improved, and asymptotic higher-order biases become important in these estimators. See Appendix A for the summary. The following local polynomial regression and multiscale -NN correct these biases to attain the optimal rate, regardless of the smoothness.

2.4 Local Polynomial Regression

Local polynomial regression estimator (LPoR; Fan and Gijbels,, 1996; Tsybakov,, 2009) is defined by replacing the single real-valued parameter in (3) with a polynomial function of degree :

| (5) |

By specifying , i.e., for any , LPoR reduces to the kernel smoother (3).

Herein, assume that the ground-truth label probability is -times continuously differentiable for some . Intuitively speaking, the regression function of degree learns the asymptotic higher-order bias around the query , and eradicate the bias by extrapolating it to the query itself. See Appendix A for the summary. Further assuming that the -th derivatives of are no more differentiable, the plug-in classifier (1) equipped with the LPoR estimator using the polynomial of degree is proved to be minimax optimal (Samworth,, 2012), by specifying an appropriate bandwidth .

Besides the asymptotic optimality of LPoR, the polynomial function of the raw covariate includes parameters to be estimated: a larger number of observations is needed for training compared to the regression function of -dimensional radial distance . The regression function of the radial distance, used in the following multiscale -NN and our proposed LRR, includes only parameters.

2.5 Multiscale -NN

While LPoR corrects the asymptotic higher-order bias of the kernel smoother, multiscale -NN (MS--NN; Okuno and Shimodaira,, 2020) shown below is designed to eradicate the bias in -NN estimator :

| (6) |

with are user-specified parameters. By specifying the regression function and the parameters appropriately, extrapolating the trained towards yields an imaginary -NN whose asymptotic bias is eradicated. See Appendix A for the summary. The plug-in classifier (1) equipped with the MS--NN estimator attains the minimax optimal rate, same as the above LPoR. See Okuno and Shimodaira, (2020) Theorem 2 for details.

As for the local regression function , we may employ a logistic function

| (7) |

using a sigmoid function . is a parameter vector to be estimated. In our numerical experiments, we distinguish MS--NN (poly.) and MS--NN (logi.), where the former employs the polynomial function while the latter employs the logistic function (7).

In this MS--NN, the local regression function is trained as if the target variables (i.e., -NN estimators) were mutually independent. -NN estimators are in fact dependent as they share a part of the labels, i.e., and share : the loss function (6) should be weighted by the inverse matrix of the covariance matrix of outcomes, or independent outcomes should be considered as well as LPoR and our proposed LRR, to obtain a better estimator (see, e.g., Kariya and Kurata, (2004) Theorem 2.1 for the efficiency of general least squares predicting dependent outcomes).

3 Local Radial Regression

As explained in the previous sections, LPoR and MS--NN rely on the asymptotic theory, meaning that they consider the limit of the infinite number of observations for training. They do not perform as well as we expect in finite real-world situations, whereby they have substantial room for improvement. For computing bias-corrected estimator with fewer observations, we propose a local radial regression (LRR) and local radial logistic regression in Section 3.1. The relation to the existing LPoR and MS--NN is described in Section 3.2. The improved convergence rate is described in Section 3.3

3.1 Local Radial Regression (LRR) and Local Radial Logistic Regression (LRLR)

We propose a local radial regression (LRR) as

| (8) |

where denotes a user-specified weight function, denotes a user-specified parametric regression function such as the polynomial and denotes a loss function for some set such as the squared loss . LRR predicts the raw outcome directly as well as LPoR, while LRR uses the radial distance of the covariate as well as MS--NN. Therefore, the proposed LRR combines the advantages of LPoR and MS--NN.

Note that discussions on the weight function for local (non-radial) regression can be found in a range of existing studies. For example, the weighting for robust local regression has been well developed (see, e.g., Cleveland, (1979, 1981) and Cleveland and Devlin, (1988)). However, the weight function concerning the radial distance is slightly out of scope of the main interest in local regression studies; in our numerical experiments, we specify or .

Same as MS--NN, we may employ the logistic regression function (7) for ; training the logistic regression function by minimizing the logistic loss (i.e., negative log-likelihood for the binomial distribution) is considered as a special case of LRR. We call it local radial logistic regression (LRLR).

3.2 Relation to LPoR and Multiscale -NN

In this section, we provide an intuitive explanation for the relations among LRR, LPoR, and MS--NN. Please see Section 3.3 for more rigorous theory on LRR. Here, for simplicity, we employ the squared loss , a fixed query , a constant bandwidth , , for and a weight function . Then, the local regression function trained in LPoR, MS--NN, and the proposed LRR are

respectively. The law of large numbers proves

| (9) | ||||

| (10) | ||||

| (11) |

as (whereby ) for some . Here and denotes the expectation with respect to and , respectively, by considering that is drawn independently from the same distribution of but conditioned as . The limit of is particularly obtained by Chaudhuri and Dasgupta, (2014) Lemma 9 proving that is asymptotically compatible with . These limits of the loss functions indicate what function each local regression is estimating.

Firstly, LPoR is compatible with LRR in some simple cases, regardless of whether we consider the asymptotic case or not: LPoR with reduces to LRR in this simple setting. This restriction on the regression function for LRR yields better empirical performance of LRR than general existing LPoR. Also see our numerical experiments in Section 4.

Regarding the MS--NN, its regression function approximates the label probability over the ball , while in the proposed LRR approximates the probability over the ball surface . These two estimators and are different but compatible in the limit . Despite their asymptotic compatibility, these two estimators are different in the finite real-world setting, where the function in LRLR is expected to be estimated more efficiently than in MS--NN due to the dependency issue described at the last of Section 2.5.

3.3 Convergence Rate Analysis

In this section, we show a convergence rate of the point-wise -risk for LRR, at a fixed query . We first describe the detailed settings and conditions, to prove the convergence rate in Theorem 1.

For simplicity of the proof, we employ a specific form of the weights and the loss function:

| (12) |

with a positive sequence . Herein,

denotes the number of positive weights (i.e., the number of observations used for local regression) and denotes its expectation. We assume that the sequence satisfies

| (13) |

for some , indicating that (for some ). Note that, while (13) is a slightly stronger condition than that of the bandwidth in standard nonparametric theories (; see, e.g., Tsybakov, (2009)), the optimal radius obtained by Theorem 1 still satisfies (13).

We employ a set of -th degree polynomials with even-degree terms

| (14) |

for . will be specified by under the assumptions that the distributions of the label and covariate are -Hölder (see Condition (C-2) for details). The settings (12) and (14) are compatible with the existing theories of MS--NN (Okuno and Shimodaira,, 2020).

For proving the convergence rate of LRR, we assume the following conditions (C-1)–(C-3) on the density function of the covariate and the label probability , with the fixed query and a fixed constant .

-

(C-1)

Over the ball , is lower-bounded by a positive constant .

-

(C-2)

Over the ball , and are -Hölder, i.e., there exist a polynomial of degree satisfying and such that

(15) (15) is analogous to Taylor expansion, and a similar expression can be obtained for .

-

(C-3)

There exist and such that

holds for

The above Conditions (C-1)–(C-3) are compatible with Okuno and Shimodaira, (2020). Therein, (C-1) and (C-2) are called strong density assumption (SDA) and ()-Hölder class of functions, respectively, with reference to Audibert and Tsybakov, (2007). (C-3) is a modification of the condition (C-3) in Okuno and Shimodaira, (2020) Section 4.3. As the LRR estimator is an intercept of the polynomial regression, a simple matrix algebra indicates that the LRR estimator is compatible with the weighted average of the outcomes for some weights defined in (35); then, the condition (C-3) is needed to prevent the weights from being diverged. We provide Example 1 satisfying the condition (C-3), with the proof shown in Appendix B.3.

Example 1.

Assuming that and distributes uniformly (at least over the ball ), (C-3) is satisfied with .

To ensure a proper estimation of LRR, we consider an event

with specified in (C-2) and (C-3), and we redefine the LRR estimator

| (16) |

with the negation . Then, the convergence rate of the risk is evaluated as follows.

Theorem 1.

See Appendix B.1 for the proof. The obtained upper-bound in Theorem 1 is compatible with LPoR with (Tsybakov,, 2009). Theorem 1 immediately proves the optimal rate of the LRR as follows.

Corollary 1.

with the optimal radius .

The obtained rate is optimal in estimating -Hölder functions (see, e.g., Tsybakov, (2009)), and this rate is compatible with the rates for LPoR and MS--NN:

for some , with the optimal bandwidth and (), and . See Tsybakov, (2009) and Okuno and Shimodaira, (2020) for details.

Note that, Corollary 1 proves the point-wise convergence at the fixed query in the sense of -risk (i.e., regression), while Okuno and Shimodaira, (2020) also provides the uniform convergence in the sense of misclassification error (i.e., classification) using the plug-in type classifier (1). See Audibert and Tsybakov, (2007) for a relation between the convergence rates of the -risk and the misclassification error.

4 Experiments on Synthetic Datasets

In this section, we conduct numerical experiments on synthetic datasets. We compare the plug-in classifier (1) of the proposed LRLR to those of logistic regression, -NN (which is also compatible with kernel smoother), LPoR, a logistic regression variant of LPoR (LPoLR), and MS--NN.

4.1 Experimental Setting

-

•

Datasets: Let be number of observations in training and test datasets, and let . For training sets, we randomly generate with , and with , and

(17) for . denotes Bernoulli distribution with mean and denotes the probability density function of univariate standard normal distribution. For test sets, we randomly generate with and for .

-

•

Evaluation: we take average of the concordance rates of each plug-in classifier to (i) randomly generated test labels and the (ii) optimal Bayes classifier , over times experiments.

-

•

Baselines: We compute -NN for each and MS--NN (logi.) with () for . We also compute LPoR and the logistic regression variant of LPoR (denoted by LPoLR, see Lee et al., (2006)) with bandwidth . Kernel smoother is not listed in the baselines, as it is compatible with -NN as explained in Section 2.3. In addition to those methods described in the previous sections, we include the random prediction: random predictor outputs and with probability and , respectively, regardless of the query . As a representative of parametric discrimination method, we used the logistic regression.

-

•

Parametric regression function: LPoR employs the polynomial function of degree . Logistic regression, MS--NN (logi.), LPoLR, and LRLR employ the polynomial of degree with the sigmoid function. In particular, MS--NN (logi.) in this section optimizes the regression function by minimizing the logistic loss defined with , but not the squared loss used in (6)

4.2 Results

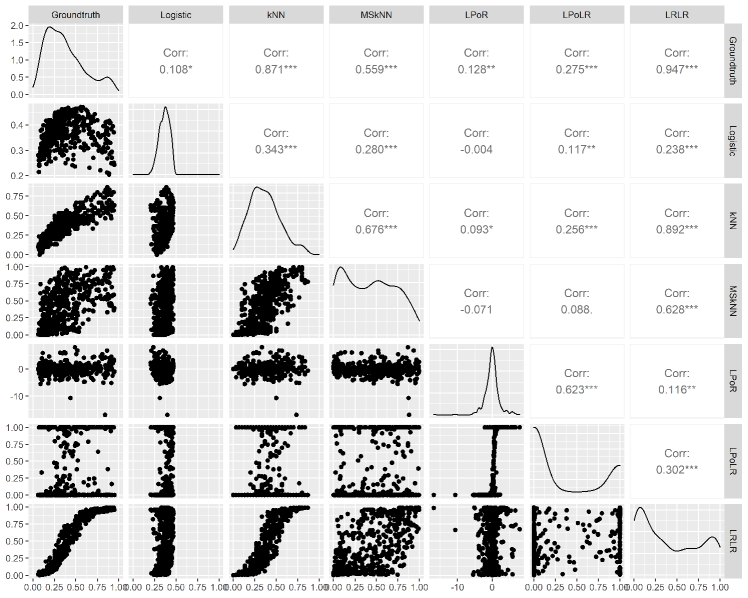

Experimental results are shown in Table 2. For both (i) and (ii), the proposed LRLR outperforms the remaining existing methods. In particular, LRLR with constant weight function shows the best score, and subsequently, LRLR with the decreasing weight is almost the second best. This classification problem is particularly difficult for extrapolation-based approaches and logistic regression, as the ground-truth function is bi-modal.

The scatter plot matrix of estimators in an instance of the above experiment is also shown in Figure 1: we can see the detailed correlation between each pair of regression methods. For instance, we can examine the high correlation coefficient between -NN and MS--NN (logi.). The logistic regression does not perform well as its expressive power is limited to approximate the bi-modal ground-truth function (17). LPoR is hard to compute stably, as its regression function is not restricted to take value within and it uses raw -dimensional covariates; LPoR and LPoLR tend to be unstable. LRLR is stably computed, and the correlation coefficient to the ground-truth is the highest among all the methods.

Further experiments with more realistic settings (including the selection of parameters by cross-validation) are shown in the following Section 5.

| Method | (i) Test Labels | (ii) Optimal Bayes Clas. | |

|---|---|---|---|

| Random | |||

| Logistic | |||

| -NN | () | ||

| () | |||

| () | |||

| () | |||

| () | |||

| MS--NN (logi.) | |||

| LPoR | () | ||

| LPoLR | () | ||

| () | |||

| LRLR | () | ||

5 Application to Predictive Month-End Closing Price Classification

In this section, we conduct experiments on real-world datasets, that predict the rise or fall of eight major world stock indices over a period from 1989 to 2021. Experiments in this section basically follow Nakagawa et al., (2018), which conducts similar experiments with the stock indices before 2018.

5.1 Overview

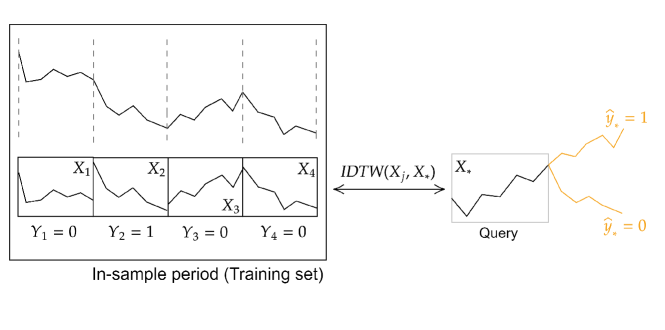

In our experiments, we consider classifying the month-end closing prices of eight major world stock indices, S&P500 (U.S.), S&P/TSX (Canada), FTSE100 (U.K.), DAX (German), CAC40 (France), Euro Stoxx 50 (EU), TOPIX (Japan), and Hang Seng Index (Hong Kong), obtained from Jan. 1989 to Oct. 2021. The covariate denotes the concatenation of daily closing prices in a month indexed by , and the response denotes whether the closing price at the last day in the month rises or falls from the month . Here denotes the number of days the market is open, which varies from month to month. Given an observed covariate of a query month, we predictively classify whether the month-end closing price rises or not. See Section 5.2 for more details, and also see Figure 2 for illustration of this classification problem.

An interesting point of these datasets is that each observed covariate has the individual dimensionality , so we cannot compute simple distances (e.g., Euclidean distance) between and with different dimensionalities . To measure their discrepancy, we employ the dynamic time warping (DTW; Bellman and Kalaba, (1959) and Müller, (2007) Section 4); denotes the Euclidean distance between the best-aligned vectors, which may be computed by the dynamic programming algorithm. For comparing daily stock prices, we first rescale and so that their first elements become one: and . We then apply DTW to the rescaled vectors; this method is called indexing DTW (IDTW; Nakagawa et al.,, 2018), denoted as . We replace the radial distance (2) by

| (18) |

satisfying , yielding IDTW variants of -NN, multiscale -NN and LRLR. The simple logistic regression, LPoR, and LPoLR cannot be computed for these datasets, as their regression functions require covariates of the same dimensionality .

5.2 Experimental Setting

-

•

Datasets: Daily closing price data of major world stock indices S&P 500 ( days), S&P/TSX ( days), EURO STOXX 50 ( days), FTSE 100 ( days), DAX ( days), CAC 40 ( days), TOPIX ( days) and Hang Seng ( days) are obtained from Bloomberg terminal ***Bloomberg terminal is a computer software provide by Bloomberg L.P. (https://about.bloomberg.co.jp/). We retrieve the datasets in November, 2021.. Ticker codes for these indices are SPX, SPTSX, SX5E, UKX, DAX, CAC, TPX, and HSI, respectively in this order, and the data period of all indices was from Jan. 1989 to Oct. 2021.

For each index, the dataset is divided by month, with the first month being Jan. 1989 and the 394th month being Oct. 2021: in each month indexed by , the daily closing prices of length are concatenated to form an observed covariate vector . For each index, the mean value of with its standard deviation is for S&P 500, for S&P/TSX, for EURO STOXX 50, for FTSE 100, for DAX, for CAC 40, for TOPIX and for Hang Seng. For each month, we let the label be 1 if the next month-end closing price increases from the current month and 0 otherwise.

-

•

Prediction: We consider predicting the next month-end prices of months from Jan. 2005 to Oct. 2021 as the test set, by leveraging the most recent months from each test month as the training set. For instance, let the query be the daily closing prices in Jan. 2010: we predict whether the month-end closing price of Feb. 2010 rises or falls by leveraging the most recent months, i.e., those from Jan. 1994 to Dec. 2009. Note that the prediction always employs the most recent months but not the fixed months. The above query, representing the prices in Jan. 2010, is also used as a training sample for predicting the prices of the subsequent months.

-

•

Evaluation by accuracy: All classifiers are evaluated by accuracy, i.e., the concordance rate between predicted labels and test labels.

-

•

Evaluation by cumulative return for virtual trading: Let be the month index for the test set; corresponds to Jan. 2005. For month , buy the stock index if the predicted label for the month (indicating whether the month-end price of the month would rise or fall) is , and sell it otherwise. The return for -th month from the virtual trading is

where denotes the stock index price at month-end of month . The cumulative return up to month is used as a score (Shen et al.,, 2015). A higher return is better.

-

•

Parametric regression function: MS--NN (poly.) employs the polynomial function of degree : . MS--NN (logi.) and LRLR employ polynomial function of degree with the sigmoid function : . In particular, MS--NN (logi.) optimizes the regression function by minimizing a variant of the squared loss function , using the logit function .

-

•

Hyper-parameter tuning: In order to determine hyper-parameters in -NN and MS--NN (poly., logi.), we perform a walk forward testing (Katz and McCormick,, 2000). Specifically, for month in the test set period, the parameter that yields the maximum accuracy on months to is chosen, while months are used for the actual training. We select parameter in -NN from . As to MS--NN (poly., logi.), instead of choosing , let , , and only one parameter be selected from . are specified by such that is an arithmetic sequence.

5.3 Results

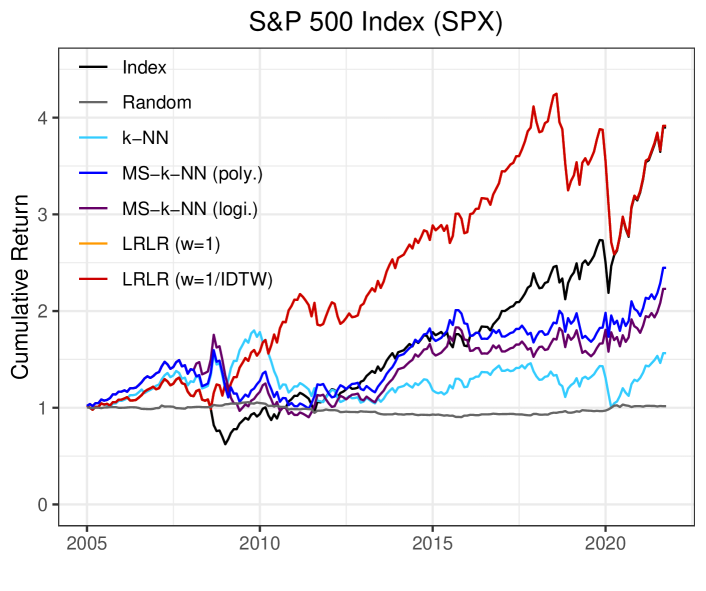

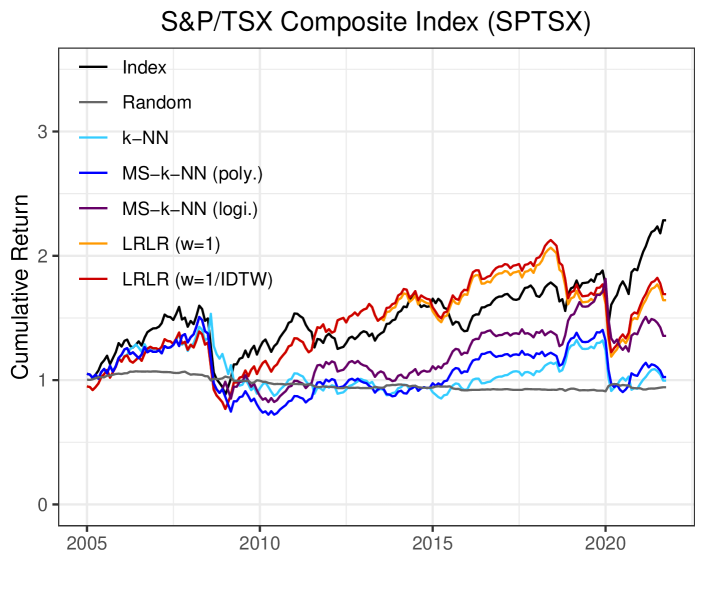

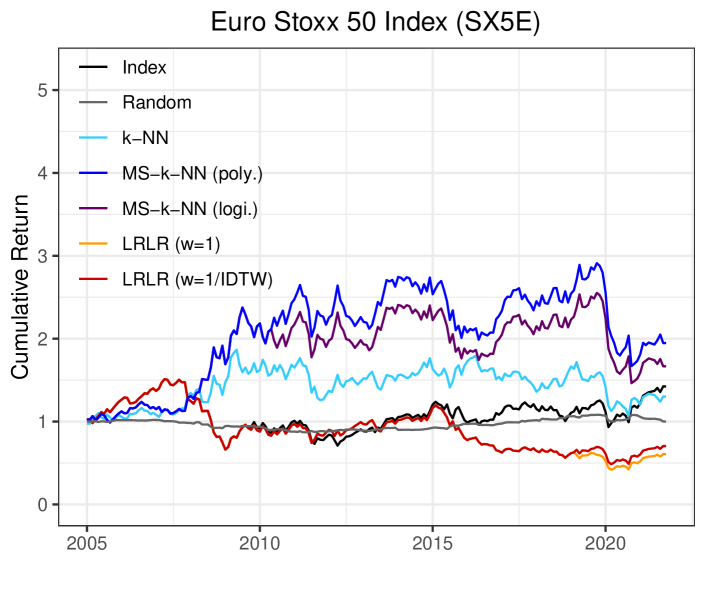

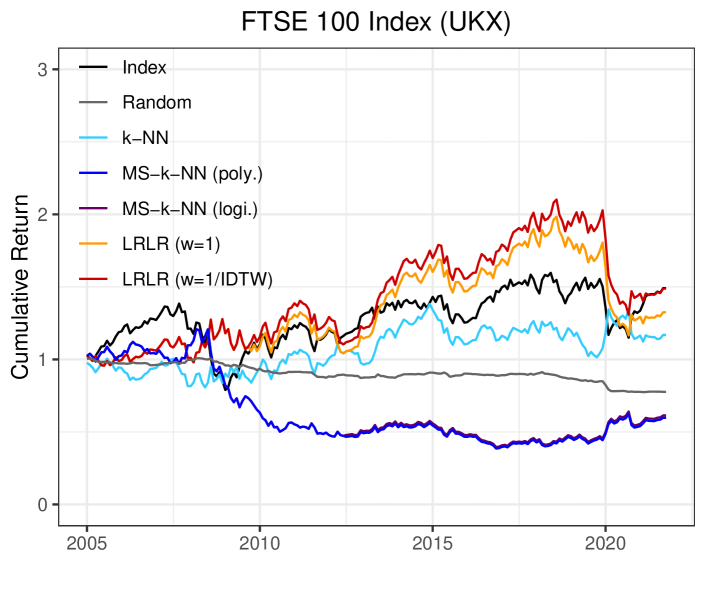

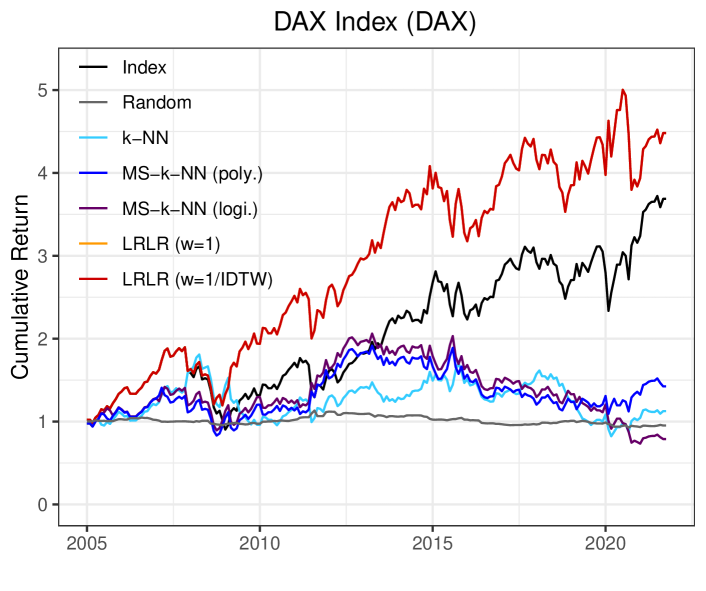

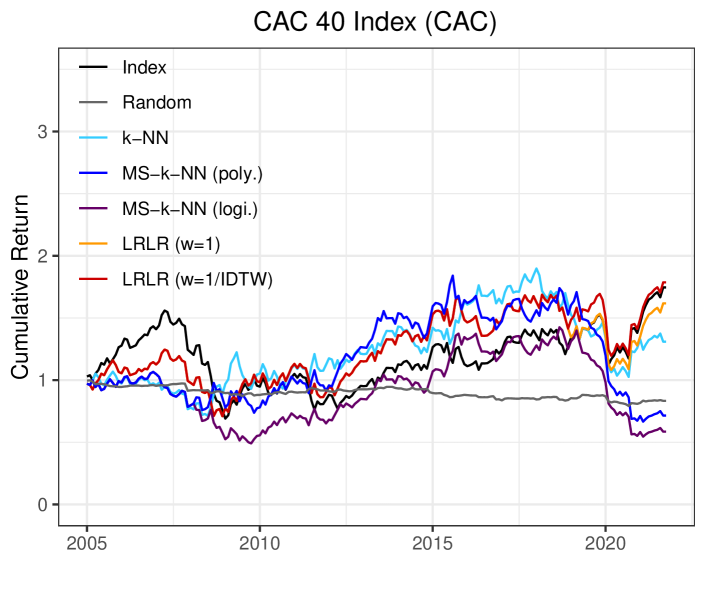

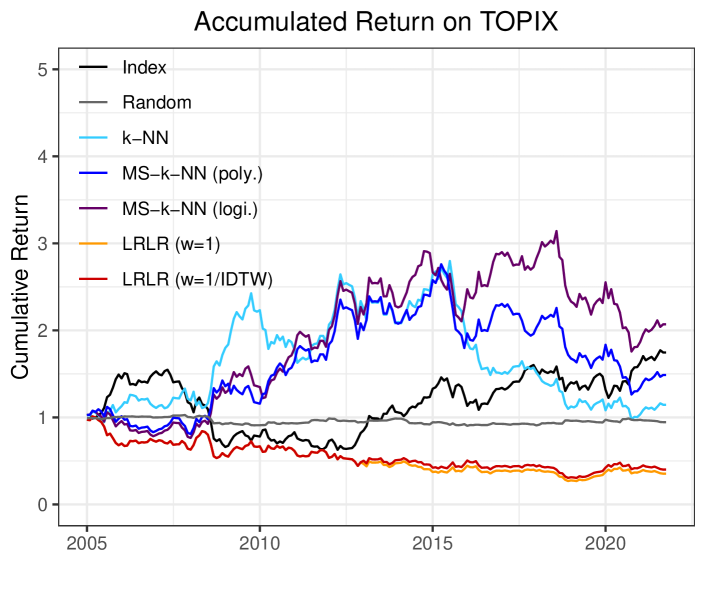

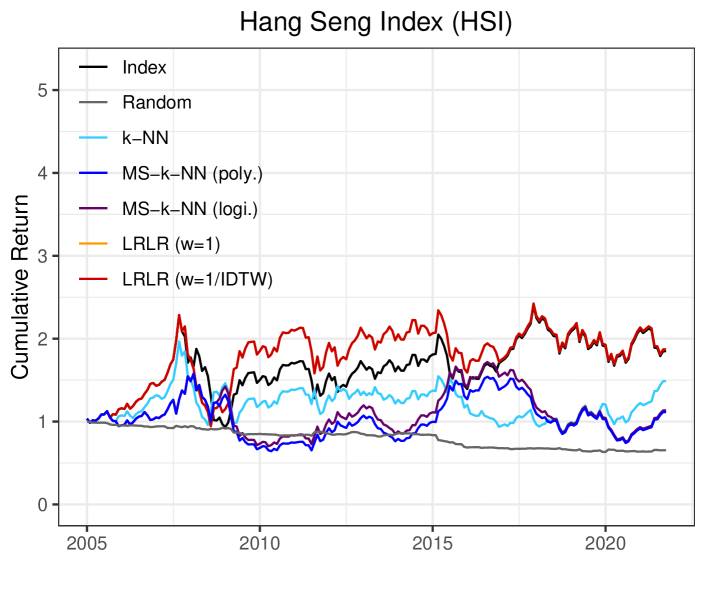

The accuracy and the cumulative return for virtual trading are shown in Table 3 and Figure 3, respectively. Note that for random prediction, the accuracy and cumulative return are both the average of corresponding results obtained by 30 experiments.

As to accuracy, both LRLR with and outperform random prediction, -NN, MS--NN (poly.) and MS--NN (logi.) on S&P 500, S&P/TSX, FTSE 100, DAX, CAC 40 and Hang Seng Index, while both of them demonstrate lower performance than some baselines on EURO STOXX 50 and TOPIX. On all stock indices, LRLR with achieves higher or the same performance than . This result shows that is superior to for LRLR in terms of accuracy.

According to the cumulative return displayed in Figure 3, LRLR with always performs better or the same as LRLR with , while it also outperforms random prediction, -NN, MS--NN (poly.) and MS--NN (logi.) on S&P 500, S&P/TSX, FTSE 100, DAX, CAC 40 and Hang Seng Indices. These are consistent with the results obtained from the comparison of accuracy.

While LRLR outperforms existing methods for most indices, their scores are degraded for EURO STOXX (EU) and TOPIX (Japan): EURO STOXX is distinct from other indices as it combines indices for a number of countries in the EU, and the Japanese market is often considered to be different from the international market. See Fama and French, (2012).

| S&P 500 | S&P/TSX | EURO S. 50 | FTSE 100 | DAX | CAC 40 | TOPIX | Hang Seng | |

|---|---|---|---|---|---|---|---|---|

| random | ||||||||

| -NN | ||||||||

| MS--NN (poly.) | 0.525 | |||||||

| MS--NN (logi.) | 0.535 | |||||||

| LRLR () | 0.649 | 0.609 | 0.574 | |||||

| LRLR () | 0.649 | 0.619 | 0.584 | 0.609 | 0.554 | 0.574 |

6 Conclusion

We proposed a local radial regression (LRR) and its logistic regression variant called a local radial logistic regression (LRLR). LRR/LRLR combines the existing local polynomial regression (LPoR) and multiscale -nearest neighbor (MS--NN). We proved the convergence rate of the risk for LRR. In our numerical experiments, LRLR outperforms these existing bias-correction approaches LPoR and MS--NN. We applied LRLR to real-world datasets of eight major world stock indices, and classified whether month-end closing prices rise or fall: predictive classification accuracy is improved, compared to existing methods.

Acknowledgement

AO is supported by JSPS KAKENHI (21K17718). HS is supported by JSPS KAKENHI (20H04148). HS and AO are supported by JST CREST (JPMJCR21N3). We would like to thank Takuma Tanaka for helpful discussions.

Appendix A Bias Correction via LPoR and MS--NN

This section briefly summarizes the asymptotic higher-order bias of the kernel smoother (KS) and -NN, and their bias correction via LPoR and MS--NN. See Tsybakov, (2009), Samworth, (2012) and Okuno and Shimodaira, (2020) for more rigorous descriptions.

Here, assume that the function is -times continuously differentiable for some , i.e., has a Taylor expansion

for some polynomial of degree satisfying . Also assume so that the kernel smoother (3) and the -NN estimator (4) are compatible, and

Then, the law of large numbers proves

see, e.g., eq. (31) in Okuno and Shimodaira, (2020) Supplement F.2 with , for the evaluation of the bias term . Both LPoR and MS--NN eradicate the bias term in the above formula: approximates and approximates . Namely, the regression functions in LPoR and MS--NN are trained to predict not only the target ground-truth label probability but also the bias term : substituting into and into eradicates the bias as

As is the leading term, LPoR and MS--NN attain the faster convergence rate than the rate of kernel smoother and -NN.

Appendix B Proofs

Proof of Theorem 1 is provided in Appendix B.1 with supporting propositions shown in Appendix B.2. Proof of Example 1 is shown in Appendix B.3.

B.1 Proof of Theorem 1

For the proof, we consider a decomposition of the risk:

| (19) |

with

Herein, we evaluate the terms in the decomposition (19), by the following three steps.

Step 1: Derivation of the probability density .

To evaluate the terms in (19), we first derive the conditional probability density . However, this conditional probability is not simply obtained by Bayes’ theorem as both denominator and numerator of the fraction are (i.e., cannot be defined). Thus we employ another derivation

| (20) |

see, e.g., Theorem 3 in Evans and Garzepy, (1992) p.38 proving that (20) is compatible with the conditional probability. Using this derivation, we obtain an expression

| (21) | ||||

Step 2: Explicit forms of .

As the estimators are intercepts of polynomial regressions, their explicit forms can be obtained by a simple matrix algebra. Using a vector , an identity matrix , a projection matrix for a matrix

| (34) | ||||

| and | (35) |

we have

| (36) |

by following the same calculation as Appendix E in Okuno and Shimodaira, (2020). Here are interpreted as weights, and and are expressed as the weighted averages of ’s and ’s, respectively. The weights satisfy but are not restricted to non-negative, so there is a concern if some of the weights may diverge. Thus we need the condition (C-3) in Section 3.3. Note that in Okuno and Shimodaira, (2020) correspond to the above defined , respectively.

For the remaining case,

| (37) |

Step 3: Evaluation of the terms in the decomposition (19).

-

•

Evaluation of the first term. Firstly, we consider the case that is satisfied. With vectors

the expression (21) gives

(38) Considering the equations

(39) where the latter equation is proved by , we have

The inequality () is proved by

(40) and for .

If is not satisfied, . Therefore, we have

(41) -

•

Evaluation of the second term. Here, we consider the case that is satisfied. For the quantity

to be evaluated, we have the conditional expectation

(42) and the conditional variance

(43) where the inequality () follows from the simple fact that the variance of any random variable taking value in is bounded by (). Therefore,

for some , where the last inequality is obtained by Proposition 6 in Appendix B.2. As holds for the remaining case , we have

(44)

B.2 Supporting Propositions

Throughout this section,

denotes an integral of the function over a ball with , denotes a derivative operator equipped with a multiple index satisfying , and denotes Gamma function. denotes the volume of a set , i.e., . denotes a binomial coefficient.

With these symbols, the following Propositions hold.

Proposition 1.

Let with , and let be a -Hölder function over the ball . Namely, in the expansion (15) of degree for , the residual satisfies . Using constants

we have

| (45) |

where

Proof of Proposition 1.

For this proof, we employ Corollary 2 in Okuno and Shimodaira, (2020):

| (46) |

Although (46) replaces the upper-bound evaluation of the error term (; proved at the last line of Proof of Proposition 6 in Okuno and Shimodaira, (2020)) by the exact term , following the proof therein immediately proves (46). Using the inequality

| (47) |

the expression (46) gives

| (48) |

The last term in (48) is evaluated as

with the volume of the -dimensional hypersphere and . By arranging the terms as

(48) divided by reduces to the assertion

∎

Proposition 2.

Let . Assume that the functions are -Hölder and define constants in the same way as in Proposition 1. Then, we have

for some constants and .

Proof of Proposition 2.

Proposition 3.

There exists such that .

Proof.

as is lower-bounded by and for some . ∎

Proposition 4.

There exists such that .

Proof.

Proposition 5.

There exist such that .

Proof.

Let . Applying the inequalities in Proposition 4 and Condition (C-3) to the rightmost side of

proves the assertion. ∎

Proposition 6.

There exist and such that for .

B.3 Proof of Example 1

As , we regard as a vector of length for notation simplicity. then reduces to

and holds. Therefore, it suffices to show the exponential concentration of and , and

Moments of .

Under the condition with fixed , the radii can be regarded as copies of a random variable following a conditional distribution .

Considering that follows uniform distribution, the conditional probability density is proportional to the area of the ball surface; we have and thus we obtain

Namely, is of order , and this ensures the following concentration of .

Concentration of and .

As , Hoeffding inequality proves

for and . With sufficiently small and , we have

indicating that,

| (49) |

for some . Therefore, by specifying such that

we have

Combined with the concentration inequality of shown in Proposition 4, we have

for some , as and (13). By specifying sufficiently small , we can take arbitrarily small ; with and , the assertion is proved by

References

- Audibert and Tsybakov, (2007) Audibert, J.-Y. and Tsybakov, A. B. (2007). Fast learning rates for plug-in classifiers. Ann. Statist., 35(2):608–633.

- Bellman and Kalaba, (1959) Bellman, R. and Kalaba, R. (1959). On Adaptive Control Processes. IRE Transactions on Automatic Control, 4(2):1–9.

- Bishop, (2006) Bishop, C. M. (2006). Pattern Recognition and Machine Learning. Springer.

- Cao et al., (2021) Cao, R., Tanaka, T., Okuno, A., and Shimodaira, H. (2021). A Study on Regression and Loss Functions for Multiscale -Nearest Neighbour. Proceedings of the Annual Conference of JSAI, JSAI2021:1G4GS2c01–1G4GS2c01. In Japanese.

- Chaudhuri and Dasgupta, (2014) Chaudhuri, K. and Dasgupta, S. (2014). Rates of Convergence for Nearest Neighbor Classification. In Advances in Neural Information Processing Systems, volume 27, pages 3437–3445. Curran Associates, Inc.

- Cleveland, (1979) Cleveland, W. S. (1979). Robust locally weighted regression and smoothing scatterplots. Journal of the American Statistical Association, 74(368):829–836.

- Cleveland, (1981) Cleveland, W. S. (1981). LOWESS: A program for smoothing scatterplots by robust locally weighted regression. American Statistician, 35(1):54.

- Cleveland and Devlin, (1988) Cleveland, W. S. and Devlin, S. J. (1988). Locally weighted regression: An approach to regression analysis by local fitting. Journal of the American Statistical Association, 83(403):596–610.

- Cover and Hart, (1967) Cover, T. and Hart, P. (1967). Nearest Neighbor Pattern Classification. IEEE Transactions on Information Theory, 13(1):21–27.

- Cristianini and Shawe-Taylor, (2000) Cristianini, N. and Shawe-Taylor, J. (2000). An Introduction to Support Vector Machines and Other Kernel-based Learning Methods. Cambridge University Press.

- Devroye et al., (1996) Devroye, L., Györfi, L., and Lugosi, G. (1996). A Probabilistic Theory of Pattern Recognition, volume 31. Springer, New York.

- Dreiseitl and Ohno-Machado, (2002) Dreiseitl, S. and Ohno-Machado, L. (2002). Logistic regression and artificial neural network classification models: a methodology review. Journal of Biomedical Informatics, 35(5-6):352–359.

- Evans and Garzepy, (1992) Evans, L. C. and Garzepy, R. F. (1992). Measure theory and fine properties of functions. Routledge, 1st edition.

- Fama and French, (2012) Fama, E. F. and French, K. R. (2012). Size, value, and momentum in international stock returns. Journal of Financial Economics, 105(3):457–472.

- Fan and Gijbels, (1996) Fan, J. and Gijbels, I. (1996). Local Polynomial Modelling and Its Applications. Routledge.

- Fix and Hodges, (1951) Fix, E. and Hodges, J. L. (1951). Discriminatory analysis-Nonparametric discrimination: Consistency properties. Technical report, USAF School of Aviation Medicine. Technical Report 4, Project no. 21-29-004.

- Goodfellow et al., (2016) Goodfellow, I., Bengio, Y., and Courville, A. (2016). Deep Learning. MIT Press. http://www.deeplearningbook.org.

- Hall and Kang, (2005) Hall, P. and Kang, K.-H. (2005). Bandwidth choice for nonparametric classification. Ann. Statist., 33(1):284–306.

- Hastie et al., (2001) Hastie, T., Tibshirani, R., and Friedman, J. (2001). The Elements of Statistical Learning. Springer Series in Statistics. Springer New York Inc., New York, NY, USA.

- Kariya and Kurata, (2004) Kariya, T. and Kurata, H. (2004). Generalized Least Squares. Wiley Series in Probability and Statistics. Wiley, Chichester, West Sussex, England; Hoboken, NJ.

- Katz and McCormick, (2000) Katz, J. O. and McCormick, D. L. (2000). The encyclopedia of trading strategies. McGraw-Hill Professional.

- Lee et al., (2006) Lee, Y. K., Lee, E. R., and Park, B. U. (2006). Conditional quantile estimation by local logistic regression. Journal of Nonparametric Statistics, 18(4-6):357–373.

- Loader, (2006) Loader, C. (2006). Local regression and likelihood. Springer Science & Business Media.

- Müller, (2007) Müller, M. (2007). Information Retrieval for Music and Motion. Springer Berlin Heidelberg, Berlin, Heidelberg.

- Nadaraya, (1964) Nadaraya, E. A. (1964). On estimating regression. Theory of Probability & Its Applications, 9(1):141–142.

- Nakagawa et al., (2018) Nakagawa, K., Imamura, M., and Yoshida, K. (2018). Stock price prediction with fluctuation patterns using indexing dynamic time warping and -nearest neighbors. In New Frontiers in Artificial Intelligence, pages 97–111, Cham. Springer International Publishing.

- Okuno and Shimodaira, (2020) Okuno, A. and Shimodaira, H. (2020). Extrapolation towards imaginary 0-nearest neighbour and its improved convergence rate. In Advances in Neural Information Processing Systems, volume 33, pages 21889–21899. Curran Associates, Inc.

- Samworth, (2012) Samworth, R. J. (2012). Optimal weighted nearest neighbour classifiers. Ann. Statist., 40(5):2733–2763.

- Shen et al., (2015) Shen, W., Wang, J., Jiang, Y.-G., and Zha, H. (2015). Portfolio choices with orthogonal bandit learning. In Proceedings of the Twenty-Fourth International Joint Conference on Artificial Intelligence, pages 974–980.

- Soni et al., (2011) Soni, J., Ansari, U., Sharma, D., and Soni, S. (2011). Predictive data mining for medical diagnosis: An overview of heart disease prediction. International Journal of Computer Applications, 17(8):43–48.

- Tsybakov, (2009) Tsybakov, A. B. (2009). Introduction to Nonparametric Estimation. Springer Series in Statistics. Springer New York.

- Vershynin, (2018) Vershynin, R. (2018). High-dimensional probability: An introduction with applications in data, volume 47. Cambridge University Press.