Long Story Short: Omitted Variable Bias in Causal Machine Learning

Abstract.

We derive general bounds on the size of omitted variable bias for a broad class of common causal parameters, such as (weighted) average of potential outcomes, average treatment effects (including subgroup effects, such as the effect on the treated), average causal derivatives, and policy effects from shifts in covariate distribution—all for general, semiparametric and fully nonparametric regression models. Leveraging the Riesz-Frechet representation of the target parameter, we show that the bounds on the bias depend only on the additional variation that latent variables create both in the outcome regression and in the Riesz representer of the causal parameter of interest. We further show how simple plausibility judgments on the maximum explanatory power of latent variables are sufficient to place overall bounds on the size of the bias. Finally, to take the bounds to data, we develop flexible and efficient statistical inference methods on the learnable components of the bounds, which can make use of modern machine learning algorithms for estimation. These results allow empirical researchers to perform sensitivity analyses in a flexible class of machine-learned causal models using very simple, and interpretable, tools. We demonstrate the usefulness of the approach with two empirical examples.

Keywords: sensitivity analysis, short regression, long regression, omitted variable bias, omitted confounders, causal models, machine learning, confidence bounds.

This is an extended version of an earlier paper prepared for the NeurIPS-21 Workshop “Causal Inference & Machine Learning: Why now?”. We thank Elias Bareinboim, Ben Deaner, David Green, Judith Lok, Esfandiar Maasoumi, Steve Lehrer, Richard Nickl, Jack Porter, James Poterba, Eric Tchetgen Tchetgen, Ingrid Van Keilegom, and also participants of the Chambelain seminar, Canadian Economic Association the Institute for Nonparametric, and Uncertainty in Artificial Intelligence meetings, and seminars at Harvard-MIT, Wisconsin, Emory, and BU Causal Seminar for very helpful comments. We are grateful to Jack Porter for suggesting the long story short title.

1. Introduction

Causal inference with observational data usually relies on the assumption that the treatment assignment mechanism is “ignorable” (i.e, independent of potential outcomes) conditional on a set of observed variables; or, equivalently, that the set of observed covariates satisfy the “backdoor” (or, more generally, adjustment) criterion (Rosenbaum and Rubin, 1983a; Pearl, 2009; Angrist and Pischke, 2009; Shpitser et al., 2012; Imbens and Rubin, 2015). Investigators who rely on the conditional ignorability assumption for drawing causal inferences from non-experimental studies must, therefore, also be able to cogently argue that there are no unobserved confounders of the treatment-outcome relationship. Yet, claiming the absence of unmeasured confounders is not only fundamentally unverifiable from the data, but often an assumption that is very hard to defend in practice.

When the assumption of no unobserved confounders is called into question, researchers are advised to perform sensitivity analyses, consisting of a formal and systematic assessment of the robustness of their findings against plausible violations of unconfoundedness. The problem of sensitivity analysis has been studied across several disciplines, dating back to, at least, the classical work of Cornfield et al. (1959), and with more recent works from Rosenbaum and Rubin (1983b); Rosenbaum (1987); Robins (1999); Frank (2000); Rosenbaum (2002); Imbens (2003); Brumback et al. (2004); Altonji et al. (2005); Hosman et al. (2010); Imai et al. (2010); Vanderweele and Arah (2011); Blackwell (2013); Frank et al. (2013); Dorie et al. (2016); Oster (2017); VanderWeele and Ding (2017); Yadlowsky et al. (2018); Masten and Poirier (2018); Kallus and Zhou (2018); Kallus et al. (2019); Cinelli et al. (2019); Zhao et al. (2019); Franks et al. (2020); Cinelli and Hazlett (2020a, b); Bonvini and Kennedy (2021); Scharfstein et al. (2021); Jesson et al. (2021), among others. Most of this work, however, either focus exclusively on binary treatments, target a specific estimand of interest (e.g, a causal risk-ratio), or impose parametric assumptions on the observed data, or on the nature of unobserved confounding (see Section 6.1 for further discussion and comparisons, after we present our main results).

In this paper, we derive general, yet simple, sharp bounds on the size of the omitted variable bias for a broad class of causal parameters that can be identified as linear functionals of the conditional expectation function of the outcome. Such functionals encompass many of the traditional targets of investigation in causal inference studies, such as, for example, (weighted) average of potential outcomes, average treatment effects (including subgroup effects, such as the effect on the treated), (weighted) average derivatives, policy effects from shifts in covariate distribution, and others—all for general, nonparametric causal models. Our construction relies on the Riesz-Frechet representation of the target functional. Specifically, we show how the bound on the bias has a simple characterization, depending only on the additional variation that the latent variables create both in the outcome and in the Riesz representer (RR) for the parameter of interest. We can thus perform sensitivity analysis with respect to violations of conditional ignorability in a broad class of causal models and target estimands.

In many leading examples, the Riesz representer in fact corresponds to quantities that are well-known to empirical researchers. For instance, when estimating the average treatment effect in a partially linear model, the RR is the (scaled) residualized treatment, after “partialling out” for control covariates; for the average treatment effect in a general nonparametric model, with a binary treatment, the RR is given by the inverse probability of treatment weights. In such cases, we show how the bounds on the bias can be reparameterized in terms of familiar and interpretable quantities measuring the percentage gains in variance explained (or gains in precision), with the treatment and the outcome, due to confounders. Therefore, plausibility judgments on the maximum explanatory power of latent variables (in predicting the treatment and the outcome) are sufficient to place overall bounds on the bias, simplifying the task of sensitivity analysis even when using nonparametric or otherwise complex models. Similar interpretable quantities arise in other leading examples. We further help analysts place bounds on the size of the bias, by benchmarking the strength of unobserved confounders against the strength of key observed covariates.111We elaborate the benchmarking procedure in Appendix C, and illustrate its use in the empirical application.

Finally we provide flexible statistical inference for these bounds using debiased machine learning (DML) and auto-DML (Chernozhukov et al., 2018a, b, 2020, 2022c). DML methods can be seen as implementing the classical “one-step” semi-parametric correction (Levit, 1975; Hasminskii and Ibragimov, 1978; Pfanzagl and Wefelmeyer, 1985; Bickel et al., 1993) based on regression scores (Newey, 1994) and a Neyman orthogonal score that we obtain for the second moment of the RR, combined with cross-fitting, an efficient form of data-splitting. Our construction makes it possible to use modern machine learning methods for estimating the identifiable components of the bounds, including regression functions, Riesz representers, the norm of regression residuals, and the norm of RRs. Auto-DML further automates the process and estimates RRs using their variational or adversarial characterization, without needing to know their analytical form. We note targeted maximum likelihood estimation (TMLE) methods (Van der Laan and Rose, 2011) could also potentially be employed, though we do not do so here.222Existing results in TMLE can be applied to obtain the “short estimate,” but additional work is needed to extend TMLE to the other components of the bounds. We leave this to future work.

In what follows, Section 2 presents our method in the simpler context of partially linear models. The results in that section serve not only as an accessible introduction to the main ideas of our general framework, but are also important in their own right, since partially linear models are widely used in applied work. Section 3 develops the main results of the paper—sharp bounds on the omitted variable bias for continuous linear functionals of the conditional expectation function of the outcome, based on their Riesz representations, all for general, nonparametric causal models. Moreover, the section also provides theoretical details for many important leading examples. In Section 4 we construct high-quality inference methods for the bounds on the target parameters by leveraging recent advances in debiased machine learning with Riesz representers. Section 5 demonstrates the use of our tools to assess the robustness of causal claims in two empirical examples: (i) the impact of 401(k) eligibility on financial assets; and, (ii) the average price elasticity of gasoline demand. Section 6 concludes with a brief discussion of related work, and suggestions for possible extensions.

Notation. All random vectors are defined on the probability space with probability measure . We consider a random vector with distribution taking values in its support ; we use to denote the probability law of any subvector and denote its support. We use to denote the norm of a measurable function and also the norm of random variable . For a differentiable map , from to , abbreviates the partial derivatives , and means . We use to denote the transpose of a column vector ; we use to denote the from the orthogonal linear projection of a scalar random variable on a random vector . We use the conventional notation to denote the Radon-Nykodym derivative of measure with respect to .

2. Warm-Up: Omitted Variable Bias in Partially Linear Models

To fix ideas, we begin our discussion in the context of partially linear models (PLM). These results not only provide the key intuitions and the building blocks for the general case of nonseparable, nonparametric models of Section 3, but they are also important in their own right, as these models are widely used in applied work.

2.1. Problem set-up

Consider the partially linear regression model of the form

| (1) |

Here denotes a real-valued outcome, a real-valued treatment, an observed vector of covariates, and an unobserved vector of covariates. We refer to as the “long” list of regressors, and to equation (1) as the “long” regression. For now, we assume the error term obeys and thus .333We can also consider, more generally, the case where the error term is centered and simply obeys . In this case, we lose the interpretation of as the CEF of the outcome, and it can be interpreted as the projection of the CEF on the space of functions that are partially linear in .

Under the traditional assumption of conditional ignorability, we have that the regression coefficient identifies the average treatment effect of a unit increase of on the outcome , that is,

where denotes the potential outcome of when the treatment is experimentally set to . The problem, however, is that is not observed, and thus both the long regression, and the regression coefficient cannot be computed from the available data.

Since the latent variables are not measured, an alternative route to obtain an approximate estimate of is to consider the regression of on the “short” list of observed regressors , as in,

| (2) |

Following convention, we call equation (2) the “short” regression. Here, again, we assume the error term obeys and we thus have .444As before, one can also consider the case where simply obeys the orthogonality condition . Here the partial linearity in both regression models simply reflects a practical view of applied work: if a researcher was already willing to estimate a partial linear model without the confounder , they would likely be just as willing to estimate a partially linear model had been observed. We can then use the “short” regression parameter as a proxy for .

Evidently, in general is not equal to , and this naturally leads to the question of how far our “proxy” can deviate from the true inferential target . Our goal is, thus, to analyze the difference between the short and long parameters—the omitted variable bias (OVB):

and perform inference on this bias under various hypotheses on the strength of the latent confounders .

2.2. OVB as the covariance of approximation errors

Recall that, using a Frisch-Waugh-Lovell partialling out argument, one can express the long and short regression parameters, and , as the linear projection coefficients of on the residuals and , respectively. That is,

| (3) |

where here we define

For reasons that will become clear in the next section, we can refer to and as the “long” and “short” Riesz representers (RR).

Now let and denote the long and short regression functions, respectively. Using the orthogonality conditions in (1) and (2), we can further express and as

| (4) |

Our first characterization of the OVB is thus as follows, where we use the shorthand notation: , , , and .

Theorem 1 (OVB Bounds in PLM).

Assume that and are square integrable with:

Then the OVB for the partially linear model of equations (1) - (2) is given by

that is, it is the covariance between the regression error and the RR error. Furthermore, the squared bias can be bounded as

where

The bound is the product of additional variations that omitted confounders generate in the regression function and in the RR. This bound is sharp for the adversarial confounding that maximizes to over choices of and , holding and fixed.

Note that the bound is the maximum amount of squared bias generated by confounding; the actual bias is amortized by the correlation , which we call the “degree of adversity.” For a given value of , adversarial confounding would select this correlation to maximize the bias, by setting , while amicable confounding would minimize the bias, and set . In principle could be set to various values less than 1 (for example, ) when confounding is assumed to be “natural” rather than adversarial.555For instance, suppose that nature draws . This yields an expected value for of 1/3. Remark 8 on the Appendix shows, however, that there does not seem to exist a natural way to set the level of natural confounding. Here we focus on the maximal degree of adversity, but empirical researchers are free to consider other choices (perhaps motivated by empirical benchmarking; as, for example, in Appendix C).

2.3. Further characterization of the bias

Sensitivity analysis requires making plausibility judgments on the values of the sensitivity parameters. Therefore, it is important that such parameters be well-understood, and easily interpretable in applied settings. Here we show how the bias of Theorem 1 can be further interpreted in terms of conventional s.

Recall that, when the CEF is not linear, a natural measure of the strength of relationship between some variable and another variable is the nonparametric (also known as Pearson’s correlation ratio (Pearson, 1905; Doksum and Samarov, 1995)):

Further, the nonparametric partial of a variable with another variable given variables and measures the additional gain in the explanatory power that provides, beyond what is already is explained by and :

We are now ready to rewrite the bound of Theorem 1.

Corollary 1 (Interpreting OVB Bounds in Terms of ).

The bound is the product of the term , which is directly identifiable from the observed distribution of , and the term , which is not identifiable, and needs to be restricted through hypotheses that limit strength of confounding. The factors and measure the strength of confounding that the omitted variables generate in the outcome and treatment regressions:

-

•

in the first factor measures the proportion of residual variation of the outcome explained by latent confounders; and,

-

•

in the second factor measures the proportion of residual variation of the treatment explained by latent confounders.

Note how this result greatly simplifies the complexity of plausibility judgments. No matter how complicated and are, to place bounds on the size of the bias, researchers need only to reason about the maximum explanatory power that unobserved confounders have in explaining treatment and outcome variation.

In addition, the corollary also emphasizes a universal OVB formula that holds for general models, and any target parameter that can be expressed as a linear functional of the CEF, which we derive in Section 3. In particular, is determined by —the proportion of residual variation of the long RR generated by latent confounders. In the partially linear model, it turns out that is simply given by . Similar simplification shows up in many cases, as we will see in Section 3.

Finally, the above results hold for population data. In practice, both and need to be estimated from finite samples. This can be readily done using debiased machine learning, as we discuss in Section 4. This enables efficient statistical inference on the bounds for under any hypothetical strength of the sensitivity parameters and . These results allow researchers to perform sharp sensitivity analyses in a flexible class of machine-learned causal models using very simple, and interpretable, tools.

2.4. Preview of empirical example.

As a preview of how these bounds can be used in practice, we briefly consider a real example: the robustness of the estimated impact of 401(k) eligibility on financial assets against the presence of unobserved confounders, such as firm characteristics (Poterba et al., 1994, 1995; Chernozhukov et al., 2018a). This example is discussed in detail in Section 5. Here the short regression coefficient is estimated to be , suggesting that 401(k) availability leads to an extra $9,051 in financial assets. But how robust is this result to presence of omitted confounders?

Confounding scenarios.

Suppose that latent variables can explain at most 4% of the residual variation of the outcome, and of the residual variation of the treatment; that is, we have that and . In Section 5 we explain why this may be a conservative scenario. Given the estimate for , these values for the partial of with and translate into an estimated bound on the absolute value of the bias of:

In other words, such confounding would lead us to consider a bias of at most $4,153 in our original estimate of $9,051. This implies the following estimated bounds for the target parameter (under maximal confounding with ):

That is, even under such violation of conditional ignorability, our estimate of the effect of 401(k) availability on financial assets is still large, and it could be anywhere in the stated bounds.

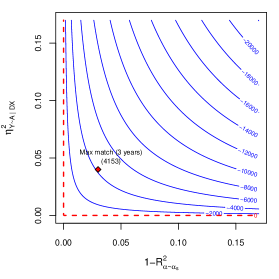

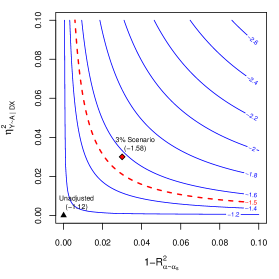

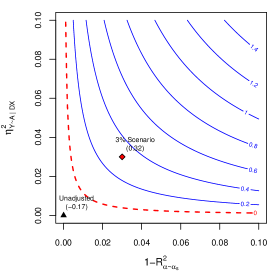

Sensitivity contours.

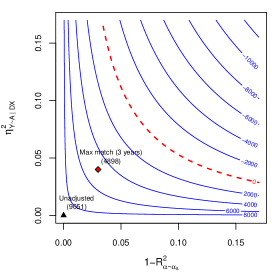

A useful tool for visualizing the whole sensitivity range of the target parameter, under different assumptions regarding the strength of confounding, is a bivariate contour plot showing the collection of curves in the space of nonparametric partial values () along which the bounds are constant. Figure 1 illustrates such curves for the 401(k) example, both for the estimated bound on the absolute value of the bias (Fig 1(a)), and for the estimated lower bound of the target parameter itself, i.e, (Fig 1(b)). In Fig 1(b), the black triangle in the lower corner shows the original estimate of $9,051. The red diamond shows the lower bound implied by the particular confounding scenario described above, $4,898. But now notice that, with the contour plot, we can readily assess the sensitivity of our estimate to any confounding scenario. In this particular example, for instance, even substantially stronger confounders that explain, say, 10% percent of the residual variation of the treatment and 5% of the residual variation of the outcome (or vice-versa) would not be sufficiently strong to bring down the estimate of the lower bound beyond the critical threshold of zero (although the estimate would be substantially reduced).

3. Main Results: Omitted Variable Bias in Nonparametric Causal Models

In this section we derive the main partial identification theorems of the paper, and construct sharp bounds on the size of the omitted variable bias for a broad class of causal parameters that can be identified as linear functionals of the conditional expectation function of the outcome, all for general nonparametric causal models. Although more abstract, the presentation of this section largely parallels the special case of partially linear models given in Section 2.

3.1. Problem set-up

Consider the following modern nonparametric structural equation model (SEM) as an example:

where is an outcome variable, is a treatment variable, is a vector-valued observed confounder variable, is a vector-valued latent confounder variable, are vector-valued structural disturbances that are mutually independent, and denotes assignment. This model has an associated Directed Acyclic Graph (DAG) (Pearl, 2009) as shown in Figure 2.

The SEM above induces the potential outcome under the intervention that sets experimentally to ,

Additionally, the independence of the structural disturbances implies the following conditional exogeneity (or, ignorability) condition:

| (7) |

which states that the realized treatment is independent of the potential outcomes, conditionally on and .

More generally, we can work with any framework that implies potential outcomes , and such that the conditional exogeneity (7) holds (Imbens and Rubin, 2015). In fact there are many structural causal models that imply potential outcomes and that satisfy the conditional exogeneity assumption (7); (see e.g. Pearl (2009) and Figure 3 for concrete examples). The causal interpretation of our results rely only on the existence of potential outcomes and conditional exogeneity. Under this set-up and when is in the support of given , , we then have the following (well-known) identification result

that is, the conditional average potential outcome coincides with the “long” regression function of on , , and . Therefore, we can identify various causal parameters—functionals of the average potential outcome—from the regression function. Important examples include: (i) the average treatment effect (ATE)

for the case of a binary treatment ; and, (ii) the average causal derivative (ACD)

for the case of a continuous treatment .

In fact, our framework is considerably more general, in that it covers any target parameter of the following general form.

Assumption 1 (Target “Long” Parameter).

The target parameter is a continuous linear functional of the long regression:

| (8) |

where the mapping is linear in , and the mapping is continuous in with respect to the norm.

This formulation covers the two working examples above with for the ATE and for the ACD, and the continuity condition holds under the regularity condition provided in the remark below. We discuss many other examples of this form later in Section 3.4.

Remark 1 (Regularity Conditions for ATE and ACD).

As regularity conditions for the ATE we assume and the weak overlap condition:

As regularity conditions for the ACD we assume , that the conditional density is continuously differentiable on its support , the regression function is continuously differentiable on , and we have that vanishes whenever is on the boundary of . The above needs to hold for all values and in the support of . We also impose the bounded information assumption:

These conditions imply that Assumption 1 holds, by Lemma 3 given in Section 3.4. ∎

The key problem is that we do not observe , and therefore we can only identify the “short” conditional expectation of given and , i.e.

which, by the tower property, is given by the conditional expectation of the long regression given the observed variables and . With the short regression in hand, we can compute proxies (or approximations) for . In particular, for the ATE, the short parameter consists of

and for the ACD,

In this general framework, the proxy parameter can also be expressed as the same linear functional applied to the short regression, .

Assumption 2 (Proxy “Short” Parameter).

The proxy parameter is defined by replacing the long regression with the short regression in the definition of the target parameter:

We require , i.e., the score depends only on when evaluated at .

Indeed, in the two working examples this assumption is satisfied, since for the ATE and for the ACD. Section 3.4 verifies this assumption for other examples.

Our goal is to provide bounds on the omitted variable bias (OVB), ie., the difference between the “short” and “long” functionals,

under assumptions that limit the strength of confounding, and perform statistical inference on its size.

3.2. Omitted variable bias for linear functionals of the CEF

The key to bounding the bias is the following lemma that characterizes the target parameters and their proxies as inner products of regressions with terms called Riesz representers (RR).

Lemma 1 (Riesz Representation).

There exist unique square integrable random variables and , the long and short Riesz representers, such that

for all square-integrable ’s and . Furthermore, is the projection of in the sense that

In the case of the ATE with a binary treatment, the representers are just the classical inverse probability of treatment (Horvitz-Thompson) weights:

This readily follows from change of measure arguments. While it may not be immediately obvious that , one can easily show that by applying Bayes’ rule.

In the case of the ACD with a continuous treatment, using integration by parts we can readily verify that the representers are logarithmic derivatives of the conditional densities:

We give more involved examples in the next section.

Sometimes it is useful to impose restrictions on the regression functions, such as partial linearity or additivity. The next lemma describes the RR property for the long and short target parameters in this case.

Lemma 2 (Riesz Representation for Restricted Regression Classes).

Furthermore, if is known to belong to a closed linear subspace of , and is known to belong to a closed linear subspace , then there exist unique long RR in and unique short RR in that continue to have the representation property

for all and . Moreover, they are given by the orthogonal projections of and on and , respectively. Since projections reduce the norm, we have and . Furthermore, the best linear projection of on is given by , namely,

In what follows we use the notation and without bars, with the understanding that if such restrictions have been made, then we work with and .

To illustrate, suppose that the regression functions are partially linear, as in Section 2

then for either the ATE or the ACD we have that the RR are given by

That is, the representer is given by the (scaled) residualized treatment, which we previously derived using the classical Frisch-Waugh-Lovell theorem, without invoking Riesz representation per se.666Similarly to footnote 4, we note Lemma 2 can be seen as a pragmatic result: if a researcher was already willing to impose, say, a partial linearity assumption in the absence of latent variables , it is likely she would also impose this assumption had she measured . Thus, from a pragmatic point of view, the conditions of Lemma 2 do not impose any additional assumptions the researcher was not already willing to defend.

Using these lemmas, we immediately obtain the following characterization of the OVB and sharp bounds on its maximal size.

Theorem 2 (OVB and Sharp Bounds).

Consider the long and short parameters and as given by Assumptions 1 and 2. We then have that the OVB is

that is, it is the covariance between the regression error and the RR error. Therefore, the squared bias can be bounded as

where

The bound is the product of additional variations that omitted confounders generate in the regression function and in the RR. This bound is sharp for the adversarial confounding that maximizes to over choices of and , holding and fixed.

This is the main conceptual result of the paper, and it is new. It covers a rich variety of causal estimands of interest, as long as they can be written as linear functionals of the long regression. We analyze further examples of this class of estimands in Section 3.4.

Finally, we note the following interesting fact.

Remark 2 (Tighter Bounds under Restrictions).

When we work with restricted parameter spaces, the restricted RRs obey

since the orthogonal projection on a closed subspace reduces the norm. This means that the bounds become tighter in this case. Therefore, by default, when restrictions have been made, we work with restricted RRs. ∎

3.3. Characterization of the OVB bounds

In the same spirit of Section 2, we can further derive useful characterizations of the bounds.

Corollary 2 (Interpreting Bounds).

This generalizes the result of Corollary 1 to fully nonlinear models, and general target parameters defined as linear functionals of the long regression. As before, the bound is the product of the term , which is directly identifiable from the observed distribution of , and the term , which is not identifiable, and needs to be restricted through hypotheses that limit strength of confounding.

Thus, again, the terms and generally measure the strength of confounding that the omitted variables generate in the outcome regression and in the treatment:

-

•

in in the first factor measures the proportion of residual variance in the outcome explained by confounders;

-

•

in the second factor measures the proportion of residual variation of the long RR generated by latent confounders.

Likewise, we have the same useful interpretation of as the nonparametric partial of with , given and , namely, . The interpretation of can be further specialized for different cases, as follows.

Remark 3 (Interpretation of for ATE with a Binary Treatment).

For the ATE example, we have that

| (10) |

where and That is, measures the relative gain in predictive power due to in the treatment model, as measured by the average precision (i.e, the inverse of the variance). Therefore, the interpretation of for the ATE with a binary treatment is similar in spirit to the interpretation for the case of the partially linear model.777This connection could be further enhanced by considering the latent normal confounder model where where and latent are independent standard Gaussian, that are independent of . Then is parameterized in terms of in the latent regression: , analogously to the partially linear case. This connection is useful for empirical work; also see comments on benchmarking below. ∎

And an analogous interpretation applies for average causal derivatives.

Remark 4 (Interpretation of for Average Causal Derivatives).

For the ACD example,

| (11) |

which can be interpreted as the relative gain in information that the confounder provides about the location of . If is homoscedastic Gaussian, conditional on both and , we have

so that simplifies to the term found for the partially linear model. ∎

Beyond making direct plausibility judgments on the strength of confounding using the above quantities, analysts can also leverage judgments of relative importance of variables to bound the size of the bias. For instance, if one has reasons to believe that would not generate as much gains in explanatory power as certain key observed covariates , this can be used to formally place bounds on the maximal strength of confounding due to . This allows one to assess, for instance, whether confounders as strong or stronger then observed covariates would be sufficient to overturn an empirical result. We elaborate the benchmarking procedure formally in Appendix C and illustrate its use in the empirical application. These results extend previous benchmarking ideas for linear regression models (e.g, Oster, 2017; Cinelli and Hazlett, 2020a) to the general case.

3.4. Theoretical details for leading examples

We now provide theoretical details for a wide variety of interesting and important causal estimands. Recall that we use to denote the “long” set of regressors and to denote the “short” list of regressors.

Let us start with examples for the binary treatment case, with the understanding that finitely discrete treatments can be analyzed similarly.

Example 1 (Weighted Average Potential Outcome).

Let be the indicator of the receipt of the treatment. Define the long parameter as

where is a bounded nonnegative weighting function and is a fixed value in . We define the short parameter as

We assume and the weak overlap condition

The long parameter is a weighted average potential outcome (PO) when we set the treatment to , under the standard conditional exogeneity assumption (7). The short parameter is a statistical approximation based on the short regression. In this example, setting

-

•

gives the average PO in the entire population;

-

•

the average PO for group ;

-

•

the average PO for the treated.

Above we can consider as small regions shrinking in volume with the sample size, to make the averages local, as in Chernozhukov et al. (2018b), but for simplicity we take them as fixed in this paper.

Example 2 (Weighted Average Treatment Effects).

In the setting of the previous example, define the long parameter

and the short parameter as

We further assume and the weak overlap condition

The long parameter is a weighted average treatment effect under the standard conditional exogeneity assumption. In this example, setting

-

•

gives ATE in the entire population;

-

•

the ATE for group ;

-

•

the ATE for the treated;

-

•

the average value of policy (APV) ,

where the policy assigns a fraction of the subpopulation with observed covariate value to receive the treatment.

In what follows does not need to be binary. We next consider a weighted average effect of changing observed covariates according to a transport map , where is deterministic measurable map from to . For example, the policy

adds a unit to the treatment , that is . This has a causal interpretation if the policy induces the equivariant change in the regression function, namely the counterfactual outcome under the policy obeys , and the counterfactual covariates are given by .

Example 3 (Average Policy Effect from Transporting ).

For a bounded weighting function , the long parameter is given by

The short form of this parameter is

As the regularity conditions we require that the support of is included in the support of , and require the weak overlap condition

We now turn to examples with continuous treatments taking values in . Consider the average causal effect of the policy that shifts the distribution of covariates via the map weighted by , keeping the long regression function invariant. The following long parameter is an approximation to times this average causal effect for small values of . This example is a differential version of the previous example.

Example 4 (Weighted Average Incremental Effects).

Consider the long parameter taking the form of the average directional derivative:

where is a bounded weighting function and is a bounded direction function. The short form of this parameter is

As regularity conditions, we suppose that . Further for each in the support of , and each in , the support of given , the derivative maps and , for , are continuously differentiable; the set is bounded, and its boundary is piecewise-smooth; and vanishes for each in this boundary. Moreover, we assume the weak overlap:

Another example is that of a policy that shifts the entire distribution of observed covariates, independently of . The following long parameter corresponds to the average causal contrast of two policies that set the distribution of observed covariates to and , independently of . Note that this example is different from the transport example, since here the dependence between and is eliminated under the interventions.

Example 5 (Policy Effect from Changing Distribution of ).

Define the long parameter as

where is a bounded weight function, and the short parameter as

As the regularity conditions we require that the supports of and are contained in the support of , and that the measure is absolutely continuous with respect to the measure on . We further assume that and the weak overlap:

The following result establishes the validity of the OVB formulas and bounds for all examples.

Theorem 3 (OVB Validity in Examples 1-5 ).

Under the conditions stated in Examples 1,2,3,5, Assumptions 1 and 2 are satisfied. Under conditions stated in Example 4, Assumptions 1 and 2 are satisfied for the Hahn-Banach extension of the mapping to the entire , given by . The m-scores and the corresponding short m-scores in Examples 1-5 are given by:

| (1) ; (2) ; (3) ; (4) ; (5) ; | (1) ; (2) ; (3) ; (4) ; (5) . |

The long RR and corresponding short RR are given by:

| (1) (2) (3) ; (4) ; (5) | (1) (2) (3) (4) ; (5) |

where above we used the notations: , In Examples 1-2, when the weight function only depends on , namely , we have the simplifications

4. Statistical Inference on the Bounds

The bounds for the target parameter take the form

The components , are set through hypotheses on the explanatory power of omitted variables. The correlation (degree of confounding) can be set to 1 under adversarial confounding.888Or other values less than 1, as motivated by empirical benchmarking. The unknown components of the bounds are and . We can estimate these components via debiased machine learning (DML), which is a form of the classical “one-step” semi-parametric correction (Levit, 1975; Hasminskii and Ibragimov, 1978; Pfanzagl and Wefelmeyer, 1985; Bickel et al., 1993; Chernozhukov et al., 2022a) based on regression scores (Newey, 1994) and a Neyman orthogonal score we give for the second moment of the RR, combined with cross-fitting, an efficient form of data-splitting.

For debiased machine learning of , we exploit the representation

as in Chernozhukov et al. (2022c, 2021). This representation is Neyman orthogonal with respect to perturbations of , which is a key property required for DML. Another component to be estimated is

which is also Neyman-orthogonal with respect to . The final component to be estimated is . For this we explore the following formulation:

where the latter parameterization is Neyman-orthogonal. Specifically Neyman orthogonality refers to the property:

where is the Gateaux (pathwise derivative) operator over directions .

Application of DML theory in Chernozhukov et al. (2018a) and the delta-method gives the statistical properties of the estimated bounds under the condition that machine learning of and is of sufficiently high quality, with learning rate faster than .

The estimation relies on the following generic algorithm.

Definition 1 (DML()).

Input the Neyman-orthogonal score , where . Then (1), given a sample , randomly partition the sample into folds of approximately equal size. Denote by the complement of . (2) For each , estimate from observations in . (3) Estimate as a root of: Output and the estimated scores for each and each .

Therefore the estimators are defined as

for the scores

We say that an estimator of is asymptotically linear and Gaussian with the centered influence function if

The application of the results in Chernozhukov et al. (2018a) for linear score functions yields the following result.

Lemma 3 (DML for Bound Components).

Suppose that each of ’s listed above and the machine learners of in obey Assumptions 3.1 and 3.2 in Chernozhukov et al. (2018a), in particular the rate of learning in the norm needs to be . Then the estimators are asymptotically linear and Gaussian with influence functions:

The covariance of the scores can be estimated by the empirical analogues using the covariance of the estimated scores.

The resulting plug-in estimator for the bounds is then:

Theorem 4 (DML Confidence Bounds for Bounds).

Under the conditions of Lemma 3, the plug-in estimator is also asymptotically linear and Gaussian with the influence function:

Therefore, the confidence bound

has the one-sided covering property, namely

The same results continue to hold if are replaced by the empirical analogue

Remark 5 (Confidence Bounds).

The above interval has the following set-wise covering property for the region : the region is covered with probability no less than , by the union bound. However, as argued by Imbens and Manski (2004), the goal is often to cover a true value with a prescribed probability, which is a two-sided point-wise covering property. The above confidence interval does cover any such with probability no less than , when the width of the bound is bounded away from zero. This follows by the argument of Imbens and Manski (2004). If we want to have the two-sided pointwise covering property to be uniform in , then we can use the further adjustment of Stoye (2009) to guarantee that. For simplicity though, we focus on the one-sided covering property stated in the theorem, because in applications the relevant hypotheses are often one-sided.∎

The following remark discusses learning the regression function and the Riesz representer .

Remark 6 (Machine Learning of and ).

Estimation of the short regression is standard and a variety of modern methods can be used (neural networks, random forests, penalized regressions). Estimation of the short RR can proceed in one of the following ways. First, we can use analytical formulas for (see e.g., Chernozhukov et al. (2018a); Semenova and Chernozhukov (2021), and references therein, for practical details). Second, we can use a variational characterization of :

where is the parameter space for , as proposed in Chernozhukov et al. (2021, 2022c). This avoids inverting propensity scores or conditional densities, as usually required when using analytical formulas. This approach is motivated by the first-order-conditions of the variational characterization:

which is the definition of the RR. Neural network (RieszNet) and random forest (ForestRiesz) implementations of this approach are given in Chernozhukov et al. (2022b), and the Lasso implementation in Chernozhukov et al. (2022c). Third, we may use a minimax (adversarial) characterization of , as in Chernozhukov et al. (2018b, 2020):

where is the parameter space for . The Dantzig selector implementation of this approach is given in Chernozhukov et al. (2018b). The neural network implementation of this approach is given in Chernozhukov et al. (2020).∎

5. Empirical Examples

We now re-analyze two empirical examples: (i) the causal effect of 401(k) eligibility on net financial assets (Poterba et al., 1994, 1995; Chernozhukov et al., 2018a); and, (ii) the price elasticity of gasoline demand (Blundell et al., 2012, 2017; Chetverikov and Wilhelm, 2017). Our goal is to complement previous studies with a sensitivity analysis, utilizing the methods developed in the present paper. More specifically we want to determine whether prior conclusions, reached under the assumption of conditional ignorability, are robust to potential uncontrolled confounding. As a preview of the results, we find that the conclusions of the first example are robust to plausible scenarios of latent confounding, whereas in the second example this is not the case.

5.1. The effect of 401(k) eligibility on financial assets

A 401(k) plan is an employed sponsored tax-deferred savings option that allows individuals to deduct contributions from their taxable income, and accrue tax-free interest on investments within the plan. Introduced in the early 1980s as an incentive to increase individual savings for retirement, an important question in the savings literature is precisely to quantify the causal impact of 401(k) eligibility on net financial assets. Indeed, a naive comparison of net financial assets between those individuals with and without 401(k) eligibility suggests a positive and large impact: using data from the 1991 Survey of Income and Program Participation (SIPP), this difference amounts to $19,559.

The problem of this naive comparison, however, is that 401(k) plans can be obtained only by those individuals that work for a firm that offers such savings option—and employment decisions are far from randomized. As an attempt to overcome this lack of random assignment, Poterba et al. (1994), Poterba et al. (1995), and more recently Chernozhukov et al. (2018a), leveraged the 1991 SIPP data to adjust for potential confounding factors between 401(k) eligibility and the financial assets of an individual. Their main argument is that eligibility for enrolling in a 401(k) plan can be taken as exogenous after conditioning on a few observed variables, most importantly, income. As explained in Poterba et al. (1994), at least around the time 401(k) plans initially became available, people were unlikely to make employment decisions based on whether an employer offered a 401(k) plan; instead, their main focus were on salary and other aspects of the job. Thus, whether one is eligible for a 401(k) plan could be taken as ignorable once we condition on income and other covariates related to job choice.

It is useful to think about causal diagrams (Pearl, 2009) that represent this identification strategy. One possible model is shown Figure 4(a). Here our outcome variable, , consists of net financial assets999Defined as the sum of IRA balances, 401(k) balances, checking accounts, U.S. saving bonds, other interest-earning accounts in banks and other financial institutions, other interest-earning assets (such as bonds held personally), stocks, and mutual funds less non-mortgage debt.; the treatment variable, , is an indicator for being eligible to enroll in a 401(k) plan; finally, the vector of observed covariates, , consists of: (i) age; (ii) income; (iii) family size; (iv) years of education; (iv) a binary variable indicating marital status; (v) a “two-earner” status indicator; (vi) an IRA participation indicator; and, (vii) a home ownership indicator. We consider that the decision to work for a firm that offers a 401(k) plan depends both on the observed covariates , but also on latent firm characteristics, denoted by ; moreover, , and are jointly affected by a set of latent factors . Most importantly, note the assumption of absence of direct arrows, both from and , to . Under such assumption, conditional ignorability holds adjusting for only. The story represented by the DAG of Figure 4(a) is one way of rationalizing the identification strategy used in earlier papers.

The first two columns of Table 1 shows the estimates for the average treatment effect of 401(k) eligibility on net financial assets under this conditional ignorability assumption. For these estimates, we follow the same strategy used in Chernozhukov et al. (2018a), and we estimate the causal effect using DML with Random Forests, considering both a partially linear model (PLM), and a fully nonparametric model (NPM). As we can see, after flexibly taking into account observed confounding factors, although the estimates of the effect of 401(k) eligibility on net financial assets are substantially attenuated, they are still large, positive and statistically significant (more precisely, $9K for the PLM and $8K for the NPM).

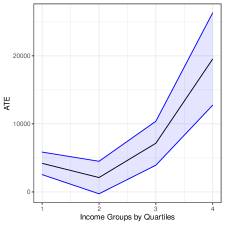

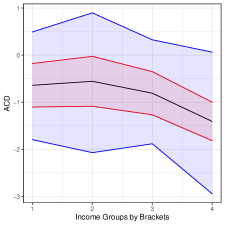

With the nonparametric model, we further explore heterogeneous treatment effects, by analyzing the ATE within income quartile groups. The results are shown in Figure 5(a). We see that the ATE varies substantially across groups, with effects ranging from approximately $5,000 (first quartile) to almost $20,000 (last quartile).

| Short Results | Robustness Values | |||||

|---|---|---|---|---|---|---|

| Model | Short Estimate | Std. Error | ||||

| Partially Linear | 9,051 | 1,313 | 7.4% | 5.5% | ||

| Fully Nonparametric | 8,076 | 1,164 | 6.2% | 4.7% | ||

Omitted confounder analysis

It is now useful to consider scenarios in which conditional ignorability fails. Figure 4(b) presents one such scenario, where a violation of conditional ignorability is credible.101010We note that Figure 4(b) is just one example, and our sensitivity analysis results hold for any model in which conditional ignorability holds given observed variables and latent confounders. Employers often offer a benefit in which they “match” a proportion of an employee’s contribution to their 401(k) up to 5% of the employee’s salaries. The model in Figure 4(b) allows this “matched amount,” denoted by , to be determined by unobserved firm characteristics , observed worker characteristics , and by 401(k) eligibility . In this model, adjustment for alone is not sufficient for control of confounding. Instead, we now need to condition both on observed covariates and latent confounders for ignorability to hold.111111Note that in this case the average treatment effect is still defined as . The relevant counterfactuals are obtained by setting for all descendants of , that is , where

How strong would the omitted firm characteristics have to be in order to overturn our previous conclusions? How would our estimates have changed under certain posited strengths of the explanatory power of firm characteristics? And how plausible are the strengths revealed to be problematic? In what follows, we use our sensitivity analysis results to address these questions.

Minimal sensitivity reporting.

In reporting empirical results, the following definitions will be useful.

Definition 2 (Robustness Values).

For example, measures the minimal equal strength of both confounding factors such that the estimated bound for the ATE would include zero; and measures the the minimal equal strength of both confounding factors such that the estimated confidence bound for the ATE would include zero, at the 5% significance level.

In Table 1 we report the robustness values of the short estimate, both for the PLM and the fully nonparametric model. Starting with the PLM, the of 7.4% means that unobserved confounders that explain less than 7.4% of the residual variation, both of the treatment, and of the outcome, are not sufficiently strong to explain away the observed effect. If we further account for sampling uncertainty (at the 5% significance level), we obtain an of 5.5%, meaning that if latent firm characteristics explain less than 5.5% of the residual variation, both of 401(k) eligibility and net financial assets, this would not be sufficient to bring down the lower limit of the confidence bound for the ATE to zero. Moving to the fully nonparametric model, we obtain similar, but somewhat lower values of and . The RV thus provides a quick and meaningful reference point that summarizes the robustness of the short estimate against unobserved confounding—any postulated confounding that does not meet this minimal criterion of strength cannot overturn the results of the original study.

Main confounding scenario.

We now proceed to construct a particular confounding scenario, based on the contextual details of the problem. We start with the assumption that explains as much variation in net financial assets as the total variation of the maximal matched amount of income (5%) over the period of three years (roughly the period over which the effect is measured)121212This strategy of bounding the strength of confounding in is based on a suggestion by James Poterba. . In the worst case scenario, this would lead to an additional of total variation explained, resulting in a partial of outcome with omitted firm characteristics of .131313 This amounts to a relative increase of approximately 10% in the baseline of the outcome regression of 28%. Following similar reasoning, and more conservatively, we posit that omitted firm characteristics can explain an additional of the variation in 401(k) eligibility, corresponding to a relative increase in the baseline of the treatment regression of 11.4%. For the partially linear model, this results in (and also ).141414. We adopt the same scenario for the nonparametric model. Since both and are below the robustness value of 5.5% (or 4.7%) , we immediately conclude that such confounding scenario is not capable of bringing the lower limit of the confidence bound of the ATE to zero.

| Model | Short Estimate | |Bias| Bound | ATE Bounds | Confidence Bounds |

|---|---|---|---|---|

| Partially Linear | 9,051 (1,313) | 4,153 (307) | [4,898; 13,204] | [2,715 ; 15,458] |

| Fully Nonparametric | 8,076 (1,164) | 4,459 (325) | [3,618; 12,535] | [1,654; 14,547] |

Note: ; ; . Significance level of 5%. Standard errors in parenthesis.

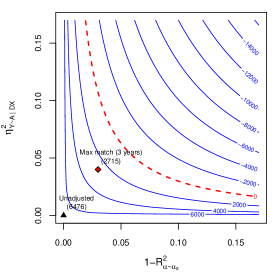

Next we determine the exact bias, bounds, and confidence bounds on the ATE implied by the posited scenario, as shown in Table 2. Starting with the partially linear model, we see that the confounding scenario would create an estimated absolute bias of at most . Accounting for statistical uncertainty, we obtain a lower limit for the confidence bound of . The results for the fully nonparametric model are qualitatively similar, with point estimates and bounds for the ATE shifted down by roughly one thousand dollars. Confidence bounds for group-wise ATEs can also be computed, and are shown in Figure 5(b). Note how the bounds are still largely positive, with only a small excursion into the negative side in the case of the second quartile group. These results suggest that the main qualitative findings reported in earlier studies are robust to the violation of unconfoundedness specified by the confounding scenario above.

Benchmarking against observed covariates.

Another approach to construct confounding scenarios is to use observed covariates to “benchmark” the plausible strength of unobserved covariates. Here we consider the variables (i) income, (ii) whether a worker has an individual retirement account, and (iii) whether the worker’s family has a two-earner status. These observed covariates were chosen because of their financial nature, and they may be acting similarly to the effect of omitted firm characteristics via match amount. As shown in Appendix C, apart from income, all these covariates have limited estimated explanatory power, and result in weaker confounding scenarios than the one we have previously considered. We conclude that, for latent confounders to completely eliminate the observed effect, they would need to generate higher gains in explanatory power than the gains generated by key observed covariates.

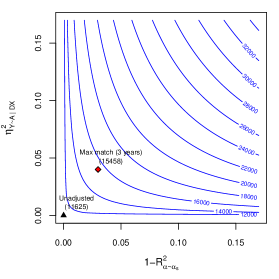

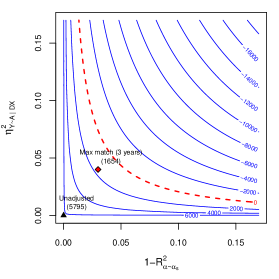

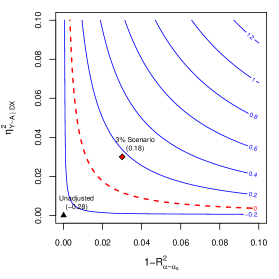

Sensitivity contour plots.

Contour plots for the absolute value of the bias, as well as for the estimated lower bound of the ATE, were already given in Figure 1 of Section 2.4. Here we provide analogous plots for the lower limit and upper limit of the confidence bounds for the ATE. These plots allow investigators to quickly and easily assess the robustness of their findings against any postulated confounding scenario.

Starting with the partially linear model, the results are shown in Figure 6. As before, the horizontal axis describes the fraction of residual variation of the treatment explained by unobserved confounders, whereas the vertical axis describes the share of residual variation of the outcome explained by unobserved confounders. The contour lines show the lower limit (Figure 6(a)) and upper limit (Figure 6(b)) of the confidence bounds for the ATE (see Theorem 4), with a given pair of hypothesized values of partial (and the conservative assumption of adversarial confounding, ). Note of Table 1 is the point where the 45-degree line crosses the critical contour of zero (red dashed line), offering a convenient and interpretable summary of the critical contour.

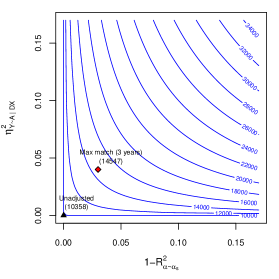

We can further place reference points on the contour plots, indicating plausible bounds on the strength of confounding, under alternative assumptions about the maximum explanatory power of omitted variables. The red diamond point on the plot—Max match (3 years)—shows the bounds on the partial as previously discussed, resulting in confidence bounds for the ATE of $2,715 to $15,458, in accordance with Table 2. Note here we consider adversarial confounding, by setting . Setting to a value similar to what is observed for income results in a much weaker scenario (see Appendix C for details). Contour plots for the nonparametric model are very similar, and are provided in Figure 7.

5.2. Average price elasticity of gasoline demand

An important part of estimating the welfare consequences of price changes is to identify the price elasticity of demand. Here we re-analyze the data on gasoline demand from the 2001 National Household Travel Survey (NHTS) (Blundell et al., 2012, 2017; Chetverikov and Wilhelm, 2017). This is a household level survey conducted by telephone and complemented by travel diaries and odometer readings (see Blundell et al. (2012) and ORNL (2004) for details). Important variables in the survey include household income, gasoline price, and annual gasoline consumption (as inferred by odometer readings and fuel efficiency of vehicles). Income data corresponds to the median of the income bracket of the household, with income brackets equally spaced apart in the logarithmic scale. The survey also contains covariates related to population density, urbanization, demographics and US Census region indicators.151515The data is available on the npiv STATA package (Chetverikov et al., 2018). The full data contains observations. After applying the same filters suggested by Blundell et al. (2017) and Chetverikov et al. (2018), the final data contains observations.

| Short Results | Robustness Values | ||||||

|---|---|---|---|---|---|---|---|

| Model | Short Estimate | Std. Error | |||||

| Partially linear | -0.701 | 0.257 | 0.054 | 0.026 | 0.047 | 0.019 | |

| Non-parametric | -0.761 | 0.360 | 0.047 | 0.010 | 0.049 | 0.011 | |

Note: ; Significance level of 5%. Standard errors in parenthesis.

Under the assumption of conditional ignorability, we estimate the average causal derivative of log price on log demand, adjusting for the observed covariates.161616This can be interpreted as the average price elasticity of demand. We approximate the derivative numerically using a finite difference (e.g, ). We consider both a partially linear model, and a fully non-parametric model171717For the partially linear specification we use DML with a cross-validated generic machine learning regression to residualize the outcome and the treatment. For the fully non-parametric specification, we use a generic machine learning approach to estimate both the regression function and the Riesz Representer. In both cases, the regression estimator uses fold cross-validation to select the best among: (i) lasso models with feature expansions; (ii) random forests; and, (iii) local polynomial forests. The Riesz representer is estimated based on the loss outlined in Remark 6. We again use -fold cross-validation to choose the best model among a penalized linear Riesz representation with expanded features and a combination of and penalty (Chernozhukov et al., 2021, 2022c), and a random forest representation (ForestRiesz) (Chernozhukov et al., 2022b). In both analyses, in order to reduce the variance that stems from sample splitting for cross-validation and for cross-fitting, we repeat the experiment for random partitions of the data and average the final estimate, incorporating variation across experiments into the standard error, as described in Chernozhukov et al. (2018a). Moreover, since samples are highly correlated within states, we perform grouped cross-validation, where samples of the same state are always in the same fold and we stratify the folds by the census region variable.. The results are shown in the first column of Table 3. In both models, we obtain estimates similar to the ones obtained in prior literature, with an estimated price elasticity of approximately .

Omitted confounder analysis.

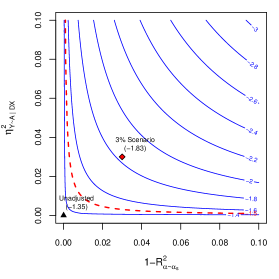

Despite having a large number of control variables, there are several reasons why one should worry about the assumption of no unobserved confounders in this setting. For instance, as was argued in Blundell et al. (2017), prices vary at the local market level, and unobserved factors that affect consumer preferences could act as unobserved confounders. Another potential source of endogeneity is the fact that we only observe the median of the income bracket of each household, and not the actual income. Since these brackets correspond to large income intervals, the remnant variation in the true income could be another major source of unobserved confounding. This is exacerbated in the larger income brackets, which correspond to larger intervals (and explains the reason why these larger income brackets were not included in prior work).181818Prior work has also analyzed this data via instrumental variable (IV) approaches (Blundell et al., 2017; Chetverikov and Wilhelm, 2017), using the distance to the closest major oil platform as an instrument. They find that IV estimates are close to the ones based on unconfoundedness (Chetverikov and Wilhelm, 2017). Further, note that the above threats to conditional ignorability are also credible threats to the validity of this proposed instrument. Extensions of our sensitivity results to IV is left to future work. We thus applied our sensitivity analysis tools to assess the sensitivity of the previous estimates to unobserved confounding.

The second part of Table 3 reports the robustness values for price elasticity, such that the sensitivity bounds would contain a target value . Here we consider (very elastic) and (perfectly inelastic). We find that, at the 5% confidence level, these robustness values are at around 2% (PLM) and 1% (NPM). These results show that, unless researchers are able to rule out confounding that explains at about 2% of the residual variation of gasoline price and gasoline consumption, the evidence provided by the data is not strong enough to distinguish between extremes such as a “very elastic,” or a “perfectly inelastic” demand function. To put this number in context, our coarse measure of income (median of the income bracket) explains around 15% of the residual variation of gasoline price and 7% of the residual variation of gasoline demand. It is thus not implausible that remnant variation in the true income could overturn these results.

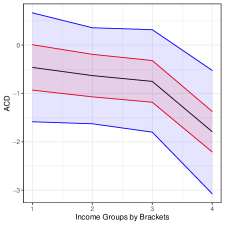

Finally, we explore how price elasticity varies with income under a specific confounding scenario. We consider three overlapping income groups defined as observations with income within in log-scale around the income points , and , as well as a fourth high income group of all units with income above on the log scale (). To illustrate, we consider a confounding scenario of approximately 3% for both sensitivity parameters, and repeat our non-parametric and partially linear estimation and sensitivity analysis for each sub-group. Point-estimates, bounds and confidence bounds are reported in Figure 8. Note that, under this scenario, the evidence for effect heterogeneity is substantially weakened, especially when using a fully non-parametric model. Sensitivity contour plots for the gasoline demand example, both for the partially linear model and the fully non-parametric model, are provided in Figures 9 and 10.

6. Discussion

In this paper we provide sharp bounds on the size of omitted variable bias for continuous linear functionals of the conditional expectation function of the outcome—all for general, non-parametric, causal models. In particular, we allow for arbitrary (e.g., binary or continuous) treatment and outcome variables, and we show that the bounds on the bias depends only on the additional gains in variation that latent variables create both in the outcome regression, via the parameter , and in the Riesz representer of the target functional, via the parameter . Moreover, since , plausibility judgments on alone are sufficient to bound the target parameter of interest. We also provide theoretical details of important leading examples. In particular we derive novel bounds for the important special cases of average treatment effects in partially linear models, and in nonparametric models with a binary treatment. Finally, we leverage the Riesz representation of our bounds to offer flexible statistical inference through (debiased) machine learning, with rigorous coverage guarantees. Therefore, we provide a concise and complete solution to the problem of bounding the size of OVB, as well performing statistical inference on these bounds, for a rich and important class of causal parameters.

We now provide a brief discussion of the related literature on sensitivity analysis, as well as suggestions for possible extensions and future work. We focus the discussion on recent methods, and on how they differ from our proposal. We refer readers to Liu et al. (2013), Richardson et al. (2014), Cinelli and Hazlett (2020a), and Scharfstein et al. (2021) for further details.

6.1. Related literature

In contrast to our approach, many of the earlier works on sensitivity analyses demand from users a rather extensive specification, or parameterization, of the nature of unobserved confounders. This could range from positing the marginal (or conditional) distribution of these latent variables, along with specifying how such confounders would enter the outcome or treatment equations (e.g, entering linearly). Among such proposals, with varying degrees of requirements and parametric assumptions, we can find, e.g, Rosenbaum and Rubin (1983b), Imbens (2003), Vanderweele and Arah (2011), Dorie et al. (2016), Altonji et al. (2005), and Veitch and Zaveri (2020).

Another branch of the sensitivity literature requires users to specify instead a “tilting,” “selection,” or “bias” function, directly parameterizing the difference between the conditional distribution of the outcome under treatment (control) between treated and control units; or, when the target parameter is the ATE, just parameterizing the difference in conditional means. Earlier work on this area goes back to Robins (1999), Brumback et al. (2004), and Blackwell (2013), with more recent works from Franks et al. (2020) and Scharfstein et al. (2021), the latter with a special focus on binary treatments, and flexible semi-parametric estimation procedures. Our proposal differs from this literature in that we do not model the bias directly, instead we impose constraints on the maximum explanatory power of confounders.

Continuing with binary treatments, many sensitivity proposals focus on this special case. They differ mainly on how to parameterize departures from random assignment. For instance, Masten and Poirier (2018) places bounds on the difference between the treatment assignment distribution, conditioning and not conditioning on potential outcomes, whereas Rosenbaum (1987, 2002) and more recently Tan (2006); Yadlowsky et al. (2018); Kallus and Zhou (2018); Kallus et al. (2019); Zhao et al. (2019); Jesson et al. (2021) place bounds on the odds of such distributions. Bonvini and Kennedy (2021), on the other hand, propose a contamination model approach, placing restriction on the proportion of confounded units. Our approach is different from all these approaches in at least two main ways. First, we do not restrict our analyses to the binary treatment case. Second, even in the important case of a binary treatment, we parameterize violations of ignorability via the gains in precision, due to omitted variables, when predicting treatment assignment. Our sensitivity parameters and bounds are thus different from these approaches (we provide a numerical example in Appendix C.1, which demonstrates practical and theoretical value of the new parameterization).

Other sensitivity results, while allowing for general confounders, treatments and outcomes, restrict their attention to specific target parameters. For example, Ding and VanderWeele (2016) derive general bounds for the risk-ratio, with sensitivity parameters also in terms of risk-ratios. Our approach is thus different both in terms of target parameters (continuous linear functionals of the CEF), and in terms of sensitivity parameters ( based sensitivity parameters). Cinelli and Hazlett (2020a) derive bounds for linear regression coefficients. Their result is a special case of ours when the target functional is the coefficient of a linear projection. Their approach does not cover nonlinear regression and the causal parameters that we study here (e.g, it does not cover the ATE in the nonparametric model with a binary treatment). Finally, Detommaso et al. (2021) provide an alternative expression for omitted variable bias of average causal derivatives, but they do not provide the sharp interpretable bounds, nor statistical inference for the bounds.

6.2. Possible extensions and future work

While throughout the paper we focus on bounding biases due to unmeasured confounding, we note that the same strategy we employ here can potentially be extended to bound biases due to misspecification errors, sampling selection, missing data, generalization of experimental results, imperfect instruments, among many other problems faced by empirical economists.

Consider, for example, the case of biased survey sampling. Suppose the target parameter is the population mean , and we may believe that the sampling selection process is only ignorable when conditioning on observed covariates and unobserved covariates . We then have that the long parameter is and the short parameter is . One can thus extend our results to bound survey biases using similar tools for bounding average potential outcomes provided in Section 3.

Our results can also be potentially extended to nonlinear functionals, such as those arising in instrumental variable (IV) methods. For instance, consider a variant of the IV problem (Imbens and Angrist, 1994), where the instrumental variable is valid only when conditioning both on observed covariates , and latent variables . In this case, the IV estimand is given by the ratio of two average treatment effects,

Both the numerator and denominator can be bounded using the methods for the ATE proposed in this paper.

Another interesting direction for future work is to consider causal estimands that are functionals of the long quantile regression, or causal estimands that are values of a policy in dynamic stochastic programming. When the degree of confounding is small, it seems possible to use the results in Chernozhukov et al. (2022a) to derive approximate bounds on the bias that can be estimated using debiased ML approaches. A final suggestion for future studies is to investigate the use of shape restrictions on the long regression that can potentially sharpen the bounds.

Data Availability, Conflict of Interests, and Funding

Data availability.

All data is is publicly available in our GitHub repository: https://github.com/carloscinelli/dml.sensemakr.

Conflict of interest.

There are no relevant financial or nonfinancial competing interests to report.

Funding.

This research received no external funding.

References

- Altonji et al. (2005) Joseph G Altonji, Todd E Elder, and Christopher R Taber. Selection on observed and unobserved variables: Assessing the effectiveness of catholic schools. Journal of political economy, 113(1):151–184, 2005.

- Angrist and Pischke (2009) Joshua D. Angrist and Jorn-Steffan Pischke. Mostly Harmless Econometrics: An Empiricist’s Companion. Princeton University Press, 2009.

- Bickel et al. (1993) Peter J Bickel, Chris AJ Klaassen, Ya’acov Ritov, and Jon A Wellner. Efficient and Adaptive Estimation for Semiparametric Models, volume 4. Johns Hopkins University Press, 1993.

- Blackwell (2013) Matthew Blackwell. A selection bias approach to sensitivity analysis for causal effects. Political Analysis, 22(2):169–182, 2013.

- Blundell et al. (2012) Richard Blundell, Joel L Horowitz, and Matthias Parey. Measuring the price responsiveness of gasoline demand: Economic shape restrictions and nonparametric demand estimation. Quantitative Economics, 3(1):29–51, 2012.

- Blundell et al. (2017) Richard Blundell, Joel Horowitz, and Matthias Parey. Nonparametric estimation of a nonseparable demand function under the slutsky inequality restriction. Review of Economics and Statistics, 99(2):291–304, 2017.

- Bonvini and Kennedy (2021) Matteo Bonvini and Edward H Kennedy. Sensitivity analysis via the proportion of unmeasured confounding. Journal of the American Statistical Association, pages 1–11, 2021.

- Brumback et al. (2004) Babette A Brumback, Miguel A Hernán, Sebastien JPA Haneuse, and James M Robins. Sensitivity analyses for unmeasured confounding assuming a marginal structural model for repeated measures. Statistics in medicine, 23(5):749–767, 2004.

- Chernozhukov et al. (2018a) Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters. The Econometrics Journal, 2018a. ArXiv 2016; arXiv:1608.00060.

- Chernozhukov et al. (2018b) Victor Chernozhukov, Whitney Newey, and Rahul Singh. De-biased machine learning of global and local parameters using regularized riesz representers. arXiv preprint arXiv:1802.08667, 2018b.

- Chernozhukov et al. (2020) Victor Chernozhukov, Whitney Newey, Rahul Singh, and Vasilis Syrgkanis. Adversarial estimation of riesz representers. arXiv preprint arXiv:2101.00009, 2020.

- Chernozhukov et al. (2021) Victor Chernozhukov, Whitney K Newey, Victor Quintas-Martinez, and Vasilis Syrgkanis. Automatic debiased machine learning via neural nets for generalized linear regression. arXiv preprint arXiv:2104.14737, 2021.

- Chernozhukov et al. (2022a) Victor Chernozhukov, Juan Carlos Escanciano, Hidehiko Ichimura, Whitney K Newey, and James M Robins. Locally robust semiparametric estimation. Econometrica, 2022a.

- Chernozhukov et al. (2022b) Victor Chernozhukov, Whitney K. Newey, Victor Quintas-Martinez, and Vasilis Syrgkanis. Riesznet and forestriesz: Automatic debiased machine learning with neural nets and random forests. International Conference on Machine Learning, 2022b.

- Chernozhukov et al. (2022c) Victor Chernozhukov, Whitney K Newey, and Rahul Singh. Automatic debiased machine learning of causal and structural effects. Econometrica, 2022c.

- Chetverikov and Wilhelm (2017) Denis Chetverikov and Daniel Wilhelm. Nonparametric instrumental variable estimation under monotonicity. Econometrica, 85(4):1303–1320, 2017. doi: https://doi.org/10.3982/ECTA13639.

- Chetverikov et al. (2018) Denis Chetverikov, Dongwoo Kim, and Daniel Wilhelm. Nonparametric instrumental-variable estimation. The Stata Journal, 18(4):937–950, 2018.

- Cinelli and Hazlett (2020a) Carlos Cinelli and Chad Hazlett. Making sense of sensitivity: Extending omitted variable bias. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 82(1):39–67, 2020a.

- Cinelli and Hazlett (2020b) Carlos Cinelli and Chad Hazlett. An omitted variable bias framework for sensitivity analysis of instrumental variables. Work. Pap, 2020b.

- Cinelli et al. (2019) Carlos Cinelli, Daniel Kumor, Bryant Chen, Judea Pearl, and Elias Bareinboim. Sensitivity analysis of linear structural causal models. International Conference on Machine Learning, 2019.

- Cornfield et al. (1959) Jerome Cornfield, William Haenszel, E Cuyler Hammond, Abraham M Lilienfeld, Michael B Shimkin, and Ernst L Wynder. Smoking and lung cancer: recent evidence and a discussion of some questions. Journal of the National Cancer institute, 22(1):173–203, 1959.

- Detommaso et al. (2021) Gianluca Detommaso, Michael Brückner, Philip Schulz, and Victor Chernozhukov. Causal bias quantification for continuous treatment, 2021.

- Ding and VanderWeele (2016) Peng Ding and Tyler J VanderWeele. Sensitivity analysis without assumptions. Epidemiology (Cambridge, Mass.), 27(3):368, 2016.

- Doksum and Samarov (1995) Kjell Doksum and Alexander Samarov. Nonparametric estimation of global functionals and a measure of the explanatory power of covariates in regression. The Annals of Statistics, pages 1443–1473, 1995.

- Dorie et al. (2016) Vincent Dorie, Masataka Harada, Nicole Bohme Carnegie, and Jennifer Hill. A flexible, interpretable framework for assessing sensitivity to unmeasured confounding. Statistics in medicine, 35(20):3453–3470, 2016.

- Frank (2000) Kenneth A Frank. Impact of a confounding variable on a regression coefficient. Sociological Methods & Research, 29(2):147–194, 2000.

- Frank et al. (2013) Kenneth A Frank, Spiro J Maroulis, Minh Q Duong, and Benjamin M Kelcey. What would it take to change an inference? Using Rubin’s causal model to interpret the robustness of causal inferences. Educational Evaluation and Policy Analysis, 35(4):437–460, 2013.

- Franks et al. (2020) AlexanderM Franks, Alexander D’Amour, and Avi Feller. Flexible sensitivity analysis for observational studies without observable implications. Journal of the American Statistical Association, 115(532):1730–1746, 2020.

- Hasminskii and Ibragimov (1978) Rafail Z Hasminskii and Ildar A Ibragimov. On the nonparametric estimation of functionals. In Proceedings of the 2nd Prague Symposium on Asymptotic Statistics, pages 41–51, 1978.

- Hosman et al. (2010) Carrie A Hosman, Ben B Hansen, and Paul W Holland. The sensitivity of linear regression coefficients’ confidence limits to the omission of a confounder. The Annals of Applied Statistics, pages 849–870, 2010.

- Imai et al. (2010) Kosuke Imai, Luke Keele, Teppei Yamamoto, et al. Identification, inference and sensitivity analysis for causal mediation effects. Statistical science, 25(1):51–71, 2010.

- Imbens (2003) Guido W Imbens. Sensitivity to exogeneity assumptions in program evaluation. American Economic Review, 93(2):126–132, 2003.