Preintegration is not smoothing when monotonicity fails

Abstract

Preintegration is a technique for high-dimensional integration over -dimensional Euclidean space, which is designed to reduce an integral whose integrand contains kinks or jumps to a -dimensional integral of a smooth function. The resulting smoothness allows efficient evaluation of the -dimensional integral by a Quasi-Monte Carlo or Sparse Grid method. The technique is similar to conditional sampling in statistical contexts, but the intention is different: in conditional sampling the aim is to reduce the variance, rather than to achieve smoothness. Preintegration involves an initial integration with respect to one well chosen real-valued variable. Griebel, Kuo, Sloan [Math. Comp. 82 (2013), 383–400] and Griewank, Kuo, Leövey, Sloan [J. Comput. Appl. Maths. 344 (2018), 259–274] showed that the resulting -dimensional integrand is indeed smooth under appropriate conditions, including a key assumption — the integrand of the smooth function underlying the kink or jump is strictly monotone with respect to the chosen special variable when all other variables are held fixed. The question addressed in this paper is whether this monotonicity property with respect to one well chosen variable is necessary. We show here that the answer is essentially yes, in the sense that without this property the resulting -dimensional integrand is generally not smooth, having square-root or other singularities.

1 Introduction

Preintegration is a method for numerical integration over , where may be large, in the presence of “kinks” (i.e., discontinuities in the gradients) or “jumps” (i.e., discontinuities in the function values). In this method one of the variables is integrated out in a “preintegration” step, with the aim of creating a smooth integrand over , smoothness being important if the intention is to approximate the -dimensional integral by a method that relies on some smoothness of the integrand, such as the Quasi-Monte Carlo (QMC) method [5] or Sparse Grid (SG) method [4].

Integrands with kinks and jumps arise in option pricing, because an option is normally considered worthless if the value falls below a predetermined strike price. In the case of a continuous payoff function this introduces a kink, while in the case of a binary or other digital option it introduces a jump. Integrands with jumps also arise in computations of cumulative probability distributions, see [6].

In this paper we consider the version of preintegration for functions with kinks or jumps presented in the recent papers [10, 11, 12], in which the emphasis was on a rigorous proof of smoothness of the preintegrated -dimensional integrand, in the sense of proving membership of a certain mixed derivative Sobolev space, under appropriate conditions.

A key assumption in [10, 11, 12] was that the smooth function (the function in (2) below) underlying the kink or jump is strictly monotone with respect to the special variable chosen for the preintegration step, when all other variables are held fixed. While a satisfactory analysis was obtained under that assumption, it was not clear from the analysis in [10, 11, 12] whether or not the monotonicity assumption is in some sense necessary. That is the question we address in the present paper. The short answer is that the monotonicity condition is necessary, in that in the absence of monotonicity the integrand typically has square-root or other singularities.

1.1 Related work

A similar method has already appeared as a practical tool in many other papers, often under the heading “conditional sampling”, see [8], Lemma 7.2 and preceding comments in [1], and a recent paper [15] by L’Ecuyer and colleagues. Also relevant are root-finding strategies for identifying where the payoff is positive, see a remark in [2] and [13, 17]. For other “smoothing” methods, see [3, 18].

The goal in conditional sampling is to decrease the variance of the integrand, motivated by the idea that if the Monte Carlo method is the chosen method for evaluating the integral then reducing the variance will certainly reduce the root mean square expected error. The reality of variance reduction in the preintegration context was explored analytically in Section 4 of [12]. But if cubature methods are used that depend on smoothness of the integrand, as with QMC and SG methods, then variance reduction is not the only consideration. In the present work the focus is on smoothness of the resulting integrand.

1.2 The problem

For the rest of the paper we will follow the setting of [12]. The problem addressed in [12] was the approximate evaluation of the -dimensional integral

| (1) |

with

where is a continuous and strictly positive probability density function on with some smoothness, and is a real-valued function of the form

| (2) |

or more generally

| (3) |

where and are somewhat smooth functions, is the indicator function which has the value if the argument is positive and otherwise, and is an arbitrary real number. When and we have and thus we have the familiar kink seen in option pricing through the occurrence of a strike price. When and are different (for example, when ) we have a structure that includes digital options.

The key assumption on the smooth function in [12] was that it has a positive partial derivative with respect to some well chosen variable (and so is an increasing function of ); that is, we assume that for the special choice of we have

| (4) |

In other words, is monotone increasing with respect to when all variables other than are held fixed.

With the variable chosen to satisfy this condition, the preintegration step is to evaluate

| (5) |

where denotes all the components of other than . Once is known we can evaluate as the -dimensional integral

| (6) |

which can be done efficiently if is smooth. In the implementation of preintegration, note that if the integral (6) is to be evaluated by an -point cubature rule, then the preintegration step in (5) needs to be carried out for different values of .

The key is the preintegration step. Because of the monotonicity assumption (4), for each there is at most one value of the integration variable such that . We denote that value of , if it exists, by so that . Under the condition (4) it follows from the implicit function theorem that is smooth if is smooth. Then we can write the preintegration step as

| (7) |

which is a smooth function of if is smooth.

1.3 Informative examples

We now illustrate the success and failure of the preintegration process with some simple examples. In these examples we take and , and choose to be the standard normal probability density, . We also initially take , and comment on other choices at the end of the section.

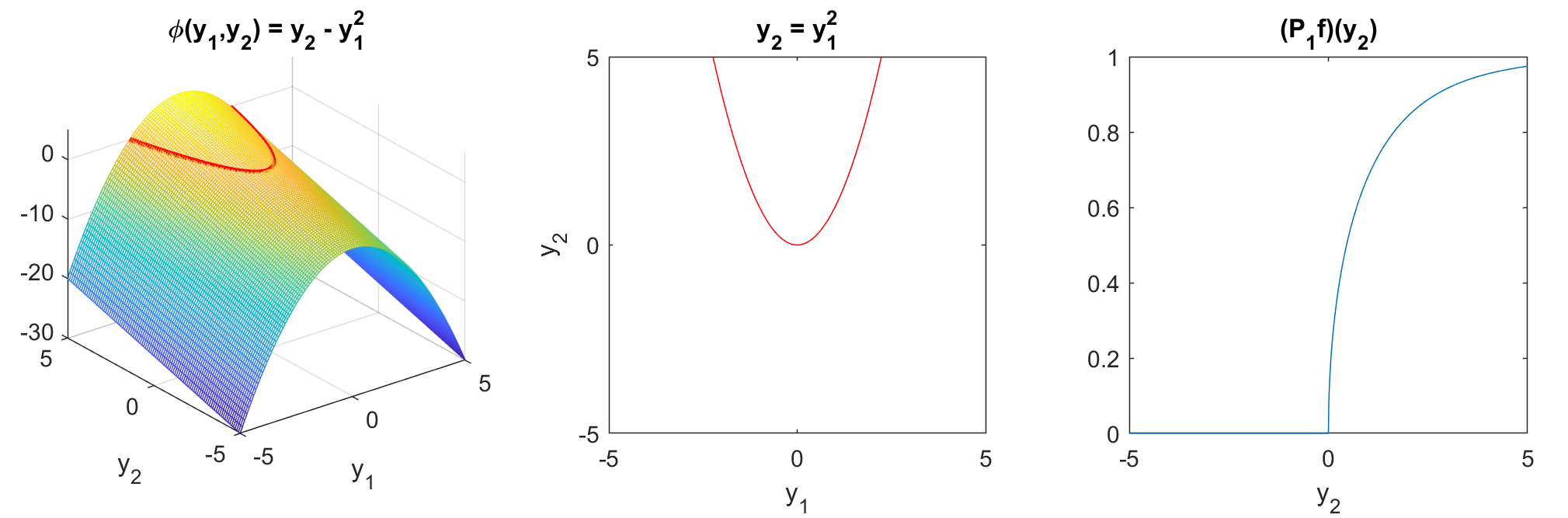

Example 1.

In this example we take

see Figure 1 (left). The zero set of this function is the parabolic curve , see Figure 1 (middle). The positivity set of (i.e., the set for which defined by (2) is non-zero) is the open region above the parabola.

If we take the special variable to be (i.e., if we take ) then the monotonicity condition (4) is satisfied, and the preintegration step is truly smoothing: specifically, we see that

where is the standard normal cumulative distribution. Thus is a smooth function for all , and is the integral of a smooth integrand over the real line,

If on the other hand we take the special variable to be (i.e., take ) then we have

The graph of , shown in Figure 1 (right), reveals that there is a singularity at . To see the nature of the singularity, note that since as , we can write

| (8) |

Thus in this simple example is not at all a smooth function of , having a square-root singularity, and hence an infinite one-sided derivative, at .

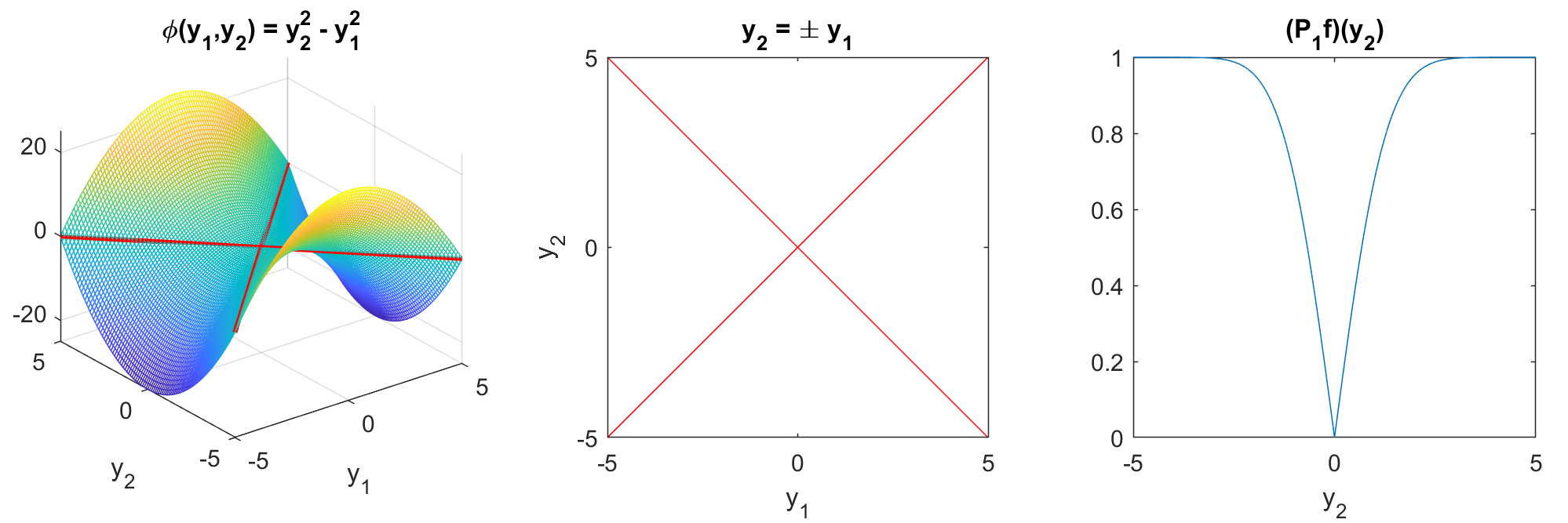

Example 2.

In this example we take

see Figure 2 (left). The zero set of is now the hyperbola , see Figure 2 (middle), and the positivity set is the union of the open regions above and below the upper and lower branches respectively. Taking , we see that monotonicity again fails, and that specifically

the graph of which is shown in Figure 2 (right). Again we see square-root singularities, this time two of them.

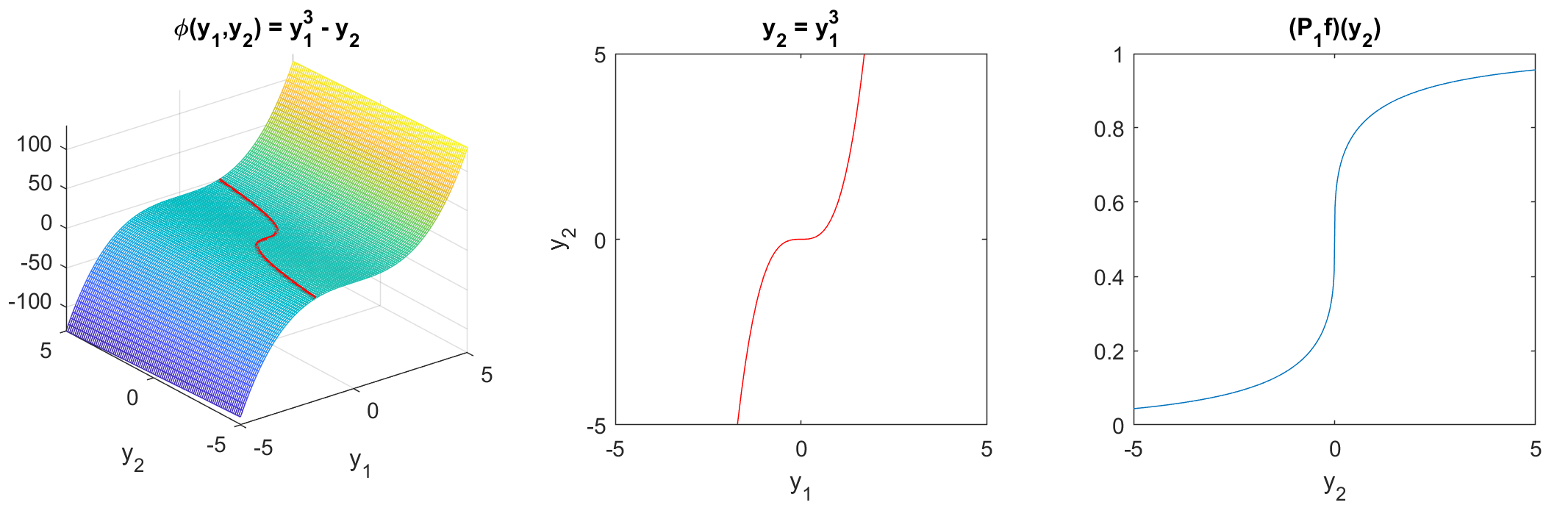

Example 3.

Here we take

see Figure 3 (left). The level set is now the pair of lines , see Figure 3 (middle), and the positivity set is the open region above and below the crossed lines. This time is given by

revealing in Figure 3 (right) a different kind of singularity (a simple discontinuity in the first derivative), but one still unfavorable for numerical integration.

Example 3 is rather special, in that the preintegration is performed on a line that touches a saddle at its critical point (the “flat” point” of the saddle). Example 4 below illustrates another situation, one that is in some ways similar to Example 1, but one perhaps less likely to be seen in practice.

Example 4.

In each of the above examples we took . Other choices for are generally not interesting, as they do not affect the nature of the singularity. An exception is the choice , which yields a kink rather than a jump because

and so leads to a weaker singularity. For example, for with as in Example 1, we obtain instead of (8)

With the recognition that kinks lead to less severe singularities than jumps, but located at the same places, from now on we shall for simplicity consider only the case .

1.4 Outline of this paper

In Section 2 we study theoretically the smoothness of the preintegrated function, assuming that the original -variate function is , with smooth but not monotone. We prove that the behavior seen in the above informative examples is typical. Section 3 contains a numerical experiment for a high-dimensional integrand that allows both monotone and non-monotone choices for the preintegrated variable. Section 4 gives brief conclusions.

2 Smoothness theorems in dimensions

In the general -dimensional setting we take , and use the general form (3) with arbitrary . Thus now we consider

| (9) |

A natural setting in which can take any value is in the computation of the (complementary) cumulative probability distribution of a random variable , as in [6]. In the case of option pricing varying corresponds to varying the strike price.

For simplicity in this section we shall take the special preintegration variable to be , so fixing . The question is then, assuming that in (9) has smoothness at least , whether or not given by

is a smooth function of .

To gain a first insight into the role of the parameter in (9), it is useful to observe that for the examples in Section 1.3 a variation in can change the position and even the nature of the singularity in , but does not necessarily eliminate the singularity. For a general and as in Example 1, we easily find that (8) is replaced by

so that the graph of is simply translated with the singularity now occurring at instead of . The situation is the same for as in Example 4.

For as in Example 2, the choice recovers Example 3, while for we find

thus in this case has square-root singularities at . For the case (which we leave to the reader) has no singularity.

In [12] it was proved that has the same smoothness as , provided that

| (10) |

together with some other technical conditions, see [12, Theorems 2 and 3].

Here we are interested in the situation when is not monotone increasing with respect to for all . In that case (unless is always monotone decreasing) there is at least one point, say , at which . At such a point the gradient of is either zero or orthogonal to the axis. If in (9) has the value then there is generically a singularity of some kind in at the point . If then there is in general no singularity in at the point , but if is not constant then the risk of encountering a near-singularity is high.

The following theorem states a general result for the existence and the nature of the singularities induced in in the common situation in which the second derivative of with respect to is non-zero at , the point at which the first derivative with respect to is zero.

Theorem 1.

Proof.

Since is not zero, and has no component in the direction of the axis, it follows that can be written as , where is a non-zero vector in orthogonal to the axis. Note that as changes in a neighborhood of , the function is increasing in the direction , and also in the direction of an arbitrary unit vector in that has a positive inner product with . Our aim now is to explore the nature of on the line through that is parallel to any such unit vector .

For simplicity of presentation, and without loss of generality, we assume from now on that the unit vector points in the direction of the positive axis. This allows us to write , temporarily ignoring all components other than the first two. In this -dimensional setting we know that

Since is continuous and positive at , it follows that is positive on the rectangle for sufficiently small . Since is increasing with respect to on this rectangle, it follows that for each there is at most one value of such that , and further, that for sufficiently small there is exactly one value of such that . For that unique value we write , hence by construction we have , and .

From the implicit function theorem (or by implicit differentiation of with respect to ) we obtain

| (12) |

in which the denominator is non-zero in a neighborhood of . From this it follows that

Differentiating (12) using the product rule and the chain rule and then setting (so that several terms vanish), we obtain

which by assumption is non-zero. Below we assume that , from which it follows that is positive; the case is similar. Taylor’s theorem with remainder gives

| (13) |

where as , thus is a convex function in a neighborhood of .

Given in a neighborhood of , our task now is to evaluate the contribution to the integral

from a neighborhood of . Thus we need to find the set of values in a neighborhood of for which . Because of (2), the set is either empty, or is the open interval with extreme points given by the solutions of , i.e.,

implying

There is no solution for , while for the solutions are

with . Thus the contribution to from the neighborhood of is zero for , and for is

Thus there is a singularity in of exactly the same character as that in Examples 1 and 2. ∎

Remark 1.

- •

- •

-

•

For as in Example 3, we have the same derivative expressions as in Example 2. Thus (11) holds, e.g., again with , but now , and we effectively recover Example 2 with square-root singularities for at . However, if we consider instead the point and , as in Figure 3, then we have so the non-vanishing gradient condition in (11) fails and Theorem 1 does not apply at this point . In this case we actually observe an absolute-value singularity for at rather than a square-root singularity.

-

•

For as in Example 4, we have , , and . It is impossible to satisfy both the first and second conditions in (11) so Theorem 1 does not apply anywhere. In particular, at the point and , as in Figure 4, we have , and in consequence (given that the third derivative does not vanish) has a cube-root singularity at rather than a square-root singularity.

From Theorem 1 one might suspect, because in the theorem has the particular value , that singularities of this kind are rare. However, in the following theorem we show that values of at which singularities occur in are generally not isolated. This is essentially because points at which are themselves generally not isolated.

Theorem 2.

Let , and assume that is such that

| (14) |

with not parallel to . Then for any in some open interval containing there exists a point in a neighborhood of at which

| (15) |

Moreover, if we assume also that , then the preintegrated quantity has a square-root singularity at along any line in through that is not orthogonal to .

Proof.

It is convenient to define , which by assumption is a real-valued function that satisfies

We need to show that for in some open interval containing there exists in a neighborhood of at which

Clearly, we can confine our search for to the zero level set of , that is, to the solutions of

Since is continuous and non-zero in a neighborhood of , the zero level set of is a manifold of dimension near , whose tangent hyperplane at is orthogonal to , see, e.g., [16, Chapter 5]. On this hyperplane there is a search direction starting from for which has a maximal rate of increase, namely the direction of the orthogonal projection of onto the tangent hyperplane, noting that this is a non-zero vector because is not parallel to . Setting out from the point in the direction of positive gradient, the value of is strictly increasing in a sufficiently small neighborhood of , while in the direction of negative gradient it is strictly decreasing. Thus searching on the manifold for a such that will be successful in one of these directions for in a sufficiently small open interval containing .

Under the additional assumption that , all the conditions of Theorem 1 are satisfied with replaced by , noting that because the second derivative is also non-zero in a sufficiently small neighborhood of . This completes the proof. ∎

Remark 2.

We now show that for as in Examples 1–4 the singularities in , with as in (9), are not isolated and furthermore, we give the exact regions in which the singularities exist.

-

•

For as in Example 1 we may choose , as in Remark 1. Indeed, the gradient of the first derivative with respect to is , which is not parallel to for all . It follows that (14) holds, e.g., at . Hence Theorem 2 implies that for in some interval around there is in a neighborhood of such that and (15) holds. In particular, there is still a square-root singularity in at . We confirm that this is indeed the case by taking and by observing that, as is easily verified, has a square-root singularity at for all real numbers . This singularity in is similar to the singularity depicted in Figure 1, but translated by .

-

•

For as in Example 3 we can consider as in Remark 1. The gradient of the first derivative with respect to is , which is not parallel to for all with . Thus (14) holds, e.g., at . Theorem 2 implies that for in some interval around there is a point in a neighborhood of such that , (15) holds, and has a square-root singularity at . Indeed, for any real number , taking gives , and it can easily be verified that has two square-root singularities at . In this case the behavior of is similar to Figure 2, with the location of the singularities now depending on .

- •

- •

3 A high-dimensional example

Motivated by applications in computational finance, for a high-dimensional example we consider the problem of approximating the fair price for a digital Asian option, a problem that can be formulated as an integral as in (1) with a discontinuous integrand of the form (9). When monotonicity holds, it was shown in [12] that preintegration not only has theoretical smoothing benefits, but also that when followed by a QMC rule to compute the -dimensional integral the computational experience can be excellent. On the other hand that paper provided no insight as to what happens, either theoretically or numerically, when monotonicity fails. In this section, in contrast, we will deliberately apply preintegration using a chosen variable for which the monotonicity condition fails. We will demonstrate the resulting lack of smoothness, using the theoretical results from the previous section, and show that the performance of the subsequent QMC rule can degrade when the preintegration variable lacks the monotonicity property.

For a given strike price , the payoff for a digital Asian call option is given by

where is the average price of the underlying stock over the time period. Under the Black–Scholes model the time-discretised average is given by

| (16) |

where is a vector of i.i.d. standard normal random variables, is the initial stock price, is the final time, is the risk-free interest rate, is the volatility and is the number of timesteps, which is also the dimension of the problem. Note that in (16) we have already made a change of variables to write the problem in terms of standard normal random variables, by factorising the covariance matrix of the Brownian motion increments as , where the entries of the covariance matrix are . Then in (16), denotes the th row of this matrix factor.

The fair price of the option is then given by the discounted expected payoff

| (17) |

Letting , this example clearly fits into the framework (9) where is the average stock price (16), is the strike price and each is a standard normal density.

There are three popular methods for factorising the covariance matrix: the standard construction (which uses the Cholesky factorisation), Brownian bridge, and principal components or PCA, see, e.g., [7] for further details. In the first two cases all components of the matrix are positive, in which case it is easily seen by studying the derivative of (16) with respect to for some ,

that is monotone increasing with respect to no matter which is chosen.

In contrast, for the PCA construction, which we consider below, the situation is very different, in that there is only one choice of for which is monotone with respect to . This is because with PCA the factorisation of employs its eigendecomposition, with the th column of being a (scaled) eigenvector corresponding to the th eigenvalue labeled in decreasing order. Since the covariance matrix is positive definite the eigenvector corresponding to the largest eigenvalue has all components positive, thus for monotonicity of is achieved. On the other hand, every eigenvector other than the first is orthogonal to the first, and therefore must have components of both signs. Given that

it follows that for there is at least one term in the sum over in (16) that approaches as and at least one other term that approaches as . Given that all terms in the sum over in (16) are positive, it follows that for the PCA case and , must approach as , so is definitely not monotone. Moreover, with respect to each variable the function is strictly convex, since

For definiteness, in the following discussion we denote by the preintegration variable for which monotonicity fails, and denote the other variables by . We now use the results from the previous section to determine the smoothness, or rather the lack thereof, of when . To do this we will use Theorem 1 and Theorem 2, where with a slight abuse of notation we replace by as our special preintegration variable.

First, note that we have already established that is not monotone with respect to , and since is strictly convex with respect to , for a given there exists a unique such that . Since is strictly increasing with respect to , it follows that . Furthermore, since , Theorem 1 implies that for the preintegrated function has a square-root singularity along any line not orthogonal to , with defined analogously to in Theorem 1.

Furthermore, Theorem 2 implies that this singularity is not isolated. To apply Theorem 2 we note that we have already established the first two conditions in (14) (recall again that we now take as the preintegration variable). We also have , which implies . Moreover, we know that and are not parallel, since the former has a positive second component while the latter has a zero second component.

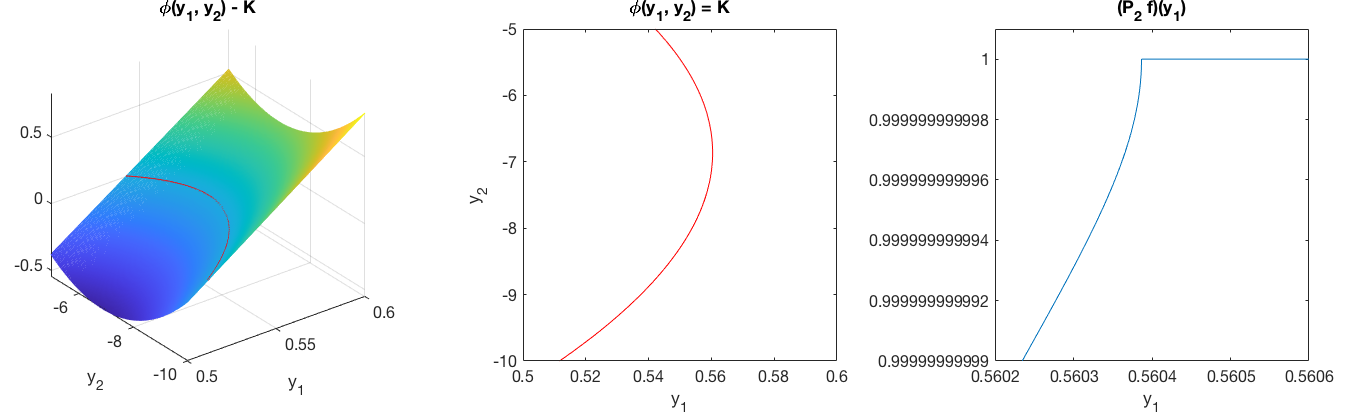

To visualise this singularity, in Figure 5 we provide an illustration of the option in two dimensions. (Note that we consider here for visualisation purposes only; we have shown already that the singularity exists for any choice of . Later we present numerical results for .) Figure 5 gives a contour plot of (left), the zero level set of (middle) and then the graph of (right). As expected, we can clearly see that has a singularity that is of square-root nature.

To perform the preintegration step in practice, note that since is strictly convex with respect to for each there is a single turning point for which and is a global minimum. It follows that there are at most two distinct points, , such that

Preintegration with respect to then simplifies to

In practice, for each the turning point and the points of discontinuity and are computed numerically, e.g., by Newton’s method.

We now look at how this lack of smoothness affects the performance of using a numerical preintegration method to approximate the fair price for the digital Asian option in dimensions. Explicitly, we approximate the integral in (17) by applying a -dimensional QMC rule to . As a comparison, we also present results for approximating the integral in (17) by applying the same QMC rule to . Recall that is monotone in dimension and furthermore, it was shown in [12] that is smooth.

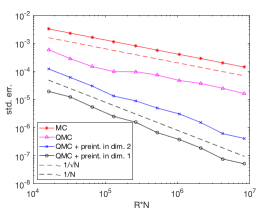

For the QMC rule we use a randomly shifted lattice rule based on the generating vector lattice-32001-1024-1048576.3600 from [14] using points with random shifts. The parameters for the option are , , , timesteps, and . We also performed a standard Monte Carlo approximation using points and a plain (without preintegration) QMC approximation using the same generating vector.

In Figure 6, we plot the convergence of the standard error, which we estimate by the sample standard error over the different random shifts, in terms of the total number of function evaluations . We can clearly see that preintegration with respect to produces less accurate results compared to preintegration with respect to , with errors that are up to an order of magnitude larger for the higher values of . We also note that to achieve a given error, say , the number of points needs to be increased tenfold. Furthermore, we observe that the empirical convergence rate for preintegration with respect to is , which is sightly worse than the rate of for preintegration with respect to . Hence, when the monotonicity condition fails, not only does the theory for QMC fail due to the presence of a singularity, but we also observe worse results in practice and somewhat slower convergence.

We also plot the error of standard Monte Carlo and QMC approximations, which behave as expected and are both significantly outperformed by the two preintegration methods.

4 Conclusion

If the monotonicity property (10) fails and is defined by (9) then we have seen that generically there is a singularity in for some values of , and under known conditions this is true even for values of in an interval.

It should also be noted that implementation of preintegration is more difficult if monotonicity fails, since instead of a single integral from to , as in (7), there will in general be additional finite or infinite intervals to integrate over, all of whose end points must be discovered by the user for each required value of .

To explore the consequences of a lack of monotonicity empirically, we carried out in Section 3 a -dimensional calculation of pricing a digital Asian option, first by preintegrating with respect to a variable known to lack the monotonicity property, and then with a variable where the property holds, with the result that both accuracy and rate of convergence were observed to be degraded when monotonicity fails.

There is an additional problem of preintegrating with respect to a variable for which the monotonicity fails, namely that because of the proven lack of smoothness, the resulting preintegrated function no longer belongs to the space of -variate functions of dominating mixed smoothness of order one, and as a consequence there is at present no theoretical support for our use of QMC integration for this -dimensional integral.

The practical significance of this paper is that effective use of preintegration is greatly enhanced by the preliminary identification of a special variable for which the monotonicity property is known to hold. The paper does not offer guidance on the choice of variable if there is more than one such variable; in such cases it may be natural to choose the variable for which preintegration leads to the greatest reduction in variance.

Acknowledgements

The authors acknowledge the support of the Australian Research Council under the Discovery Project DP210100831.

References

- [1] N. Achtsis, R. Cools, and D. Nuyens, Conditional sampling for barrier option pricing under the LT method, SIAM J. Financial Math. 4 (2013), 327–352.

- [2] N. Achtsis, R. Cools, and D. Nuyens, Conditional sampling for barrier option pricing under the Heston model, in: J. Dick, F.Y. Kuo, G.W. Peters, I.H. Sloan (eds.), Monte Carlo and Quasi-Monte Carlo Methods 2012, pp. 253–269, Springer-Verlag, Berlin/Heidelberg (2013).

- [3] C. Bayer, M. Siebenmorgen, and R. Tempone, Smoothing the payoff for efficient computation of Basket option prices, Quant. Finance 18 (2018), 491–505.

- [4] H. Bungartz and M. Griebel, Sparse grids, Acta Numer. 13 (2004), 147–269.

- [5] J. Dick, F. Y. Kuo, and I. H. Sloan, High dimensional integration – the quasi-Monte Carlo way, Acta Numer. 22 (2013), 133–288.

- [6] A. D. Gilbert, F. Y. Kuo, and I. H. Sloan, Approximating distribution functions and densities using quasi-Monte Carlo methods after smoothing by preintegration, arXiv:2112.10308, (2021).

- [7] P. Glasserman, Monte Carlo Methods in Financial Engineering, Springer-Verlag, Berlin-Heidelberg, (2003).

- [8] P. Glasserman and J. Staum, Conditioning on one-step survival for barrier option simulations, Oper. Res., 49 (2001), 923–937.

- [9] M. Griebel, F. Y. Kuo, and I. H. Sloan, The smoothing effect of the ANOVA decomposition, J. Complexity 26 (2010), 523–551.

- [10] M. Griebel, F. Y. Kuo, and I. H. Sloan, The smoothing effect of integration in and the ANOVA decomposition, Math. Comp. 82 (2013), 383–400.

- [11] M. Griebel, F. Y. Kuo, and I. H. Sloan, Note on “the smoothing effect of integration in and the ANOVA decomposition”, Math. Comp. 86 (2017), 1847–1854.

- [12] A. Griewank, F. Y. Kuo, H. Leövey, and I. H. Sloan. High dimensional integration of kinks and jumps – smoothing by preintegration, J. Comput. Appl. Math. 344 (2018), 259–274.

- [13] M. Holtz, Sparse Grid Quadrature in High Dimensions with Applications in Finance and Insurance (PhD thesis), Springer-Verlag, Berlin, 2011.

- [14] F. Y. Kuo, https://web.maths.unsw.edu.au/fkuo/lattice/index.html, (2007), accessed December 13, 2021.

- [15] P. L’Ecuyer, F. Puchhammer, and A. Ben Abdellah. Monte Carlo and Quasi-Monte Carlo Density Estimation via Conditioning, arXiv:1906.04607, (2021).

- [16] J. .M. Lee, Introduction to Smooth Manifolds, Springer, New York, (2000).

- [17] D. Nuyens and B. J. Waterhouse, A global adaptive quasi-Monte Carlo algorithm for functions of low truncation dimension applied to problems from finance, in: L. Plaskota and H. Woźniakowski (eds.), Monte Carlo and Quasi-Monte Carlo Methods 2010, pp. 589–607, Springer-Verlag, Berlin/Heidelberg (2012).

- [18] C. Weng, X. Wang, and Z. He, Efficient computation of option prices and greeks by quasi-Monte Carlo method with smoothing and dimension reduction, SIAM J. Sci. Comput. 39 (2017), B298–B322.