Multivariate Realized Volatility Forecasting with Graph Neural Network

Abstract

The existing publications demonstrate that the limit order book data is useful in predicting short-term volatility in stock markets. Since stocks are not independent, changes on one stock can also impact other related stocks. In this paper, we are interested in forecasting short-term realized volatility in a multivariate approach based on limit order book data and relational data. To achieve this goal, we introduce Graph Transformer Network for Volatility Forecasting. The model allows to combine limit order book features and an unlimited number of temporal and cross-sectional relations from different sources. Through experiments based on about 500 stocks from S&P 500 index, we find a better performance for our model than for other benchmarks.

1 Introduction

††The authors would like to thank Mathieu Rosenbaum from Ecole Polytechnique for his valuable guidance and advice during this work. The authors also would like to express our gratitude to Kaggle users AlexiosLyon and Max2020 for their posts and discussions. The authors also appreciate the insightful discussions with Jianfei Zhang.Volatility is an important quantity in finance, it evaluates the price fluctuation and represents the risk level of an asset. It is one of the most important indicators used in risk management and equity derivatives pricing. Although the volatility is not observable, Andersen and Bollerslev (1998) show that realized volatility is a good estimator of volatility. Forecasting realized volatility has therefore attracted the attention of various researchers.

Brailsford and Faff (1996) propose using GARCH (Generalized AutoRegressive Conditional Heteroskedasticity) models to forecast realized volatilities based on daily prices. Gatheral and Oomen (2010) introduce several simple volatility estimators based on Limit Order Book (LOB) data, showing that the use of LOB data can lead to better predicting results. More recently, Rahimikia and Poon (2020b) and Zhang and Rosenbaum (2020) use machine learning techniques such as Recurrent Neural Network (RNN) to improve such predictions.

The aforementioned literatures adopt a univariate approach in this task, which means that the model only considers one outcome for one stock at the same time, instead of jointly considering the situations of all stocks, although the asset returns on the financial markets can be highly correlated (Campbell et al., 1993). Andersen et al. (2005) propose linear multivariate volatility forecasting methods based on daily price data to take into account this correlation, while Bucci (2020) further uses neural networks to forecast realized volatility covariance matrix non-linearly. Bollerslev et al. (2019) first propose a parametric multivariate model based on LOB data using covolatility and covariance matrices. More recently, a Kaggle multivariate realized volatility prediction competition111https://www.kaggle.com/c/optiver-realized-volatility-prediction was sponsored by Optiver to challenge data scientists to propose new multivariate forecasting methods.

Compared with the univariate approach, multivariate models can capture the relations among observations. Most recently, Graph Neural Networks (GNN) (Bruna et al., 2013) are proposed to integrate such relationship into the commonly used non-linear neural networks. This approach achieves significant success in multiple applications, such as traffic flow prediction (Li et al., 2017), recommender systems (Berg et al., 2017) and stock movement prediction (Sawhney et al., 2020; Chen and Robert, 2021). To the best of our knowledge, no graph-based structure for volatility forecasting has been proposed in the literatures.

Hence, to further improve the volatility forecasting performance, inspired by previous researches (Sec. 2), the Kaggle competition and our real-life use cases, we build a multivariate volatility forecasting model (Sec. 3) based on Graph Neural Network: Graph Transformer Network for Volatility Forecasting (GTN-VF). This model predicts the short-term volatilities from LOB data and both cross-sectional and temporal relationships from different sources (Sec. 4). With various experiments on about 500 stocks from the S&P 500 index, we demonstrate that GTN-VF outperforms other baseline models with a significant margin on different forecasting horizons (Sec. 5).

2 Related Work

2.1 Volatility Forecasting

As introduced in Section 1, there are two types of volatility forecasting models: univariate models and multivariate models.

In univariate approaches, researchers can design intuitive estimators (Zhou, 1996; Zhang, 2006), without considering relations among observations. More commonly, researchers adopt time-series methods to model the time dependence while ignoring the cross-sectional relations and calibrating one set of parameters for each asset. For example, Brailsford and Faff (1996) propose GARCH models, Sirignano and Cont (2019) use RNN models with Long Short-Term Memory (LSTM) and Ramos-Pérez et al. (2021) adopt a Transformer structure (Vaswani et al., 2017).

Multivariate models add cross-sectional relationships and achieve better results. For example, Kwan et al. (2005) introduce multivariate threshold GARCH model and Bollerslev et al. (2019) propose a multivariate statistical estimator based on co-volatility matrices. It is worth noting that all models above only use asset covariance as the source to build the relationship while ignoring the intrinsic relations between the companies that issue the stocks.

2.2 Graph Neural Network

A graph is composed of nodes and edges, where a node represents an instance in the network and an edge denotes the relationship between two instances. It is an intuitive structure to describe the relational information. Recently, many researches focus on generalizing neural networks on graph structure to capture non-linear interactions among the nodes.

Bruna et al. (2013) first generalize the Convolutional Neural Network (CNN) on graph-based data, while Kipf and Welling (2016) propose Graph Convolutional Network (GCN) and Defferrard et al. (2016) introduce ChebNet, both of which have reduced network complexity and better predictive accuracy.

However, the aforementioned models are required to load all the graph data into the memory at the same time, making training larger relation networks impossible. Gilmer et al. (2017) state that Graph Neural Networks are essentially message passing algorithms. It means that the model makes decision not only based on one node’s observation, but also the information passed from all other related nodes defined in the format of a graph. Based on this generalization, Hamilton et al. (2017) propose GraphSAGE which allows batch training on graph data.

Shi et al. (2020) further show that using a Transformer-like operator to aggregate node features and the neighbor nodes’ features gives a better performance than a simple average such as GraphSAGE or an attention mechanism such as Graph Attention Network (Veličković et al., 2017).

To close the gap in the researches, we propose GTN-VF, which adopts the state-of-the-art Graph Neural Networks to model the relationships. In addition, GTN-VF allows to integrate an unlimited number of relational information, including both widely used covariance and other external relations such as sector and supply chain, which were rarely used in previous researches.

3 Problem Formulation

We formulate this multivariate volatility forecasting problem as a regression task. The goal is to predict the realized volatility vector over the next seconds at a given time with all previously available data.

We first define the return of stock at time as

| (1) |

where is the last trade price of at .

We then use to denote the realized volatility for stock between and , it is defined as:

| (2) |

Previous researches (Malec, 2016; Rahimikia and Poon, 2020a, b) usually calibrate one model for each stock. This prediction model for stock can be written as:

| (3) |

where denotes the limit order book data related to stock between and , and . is a parameter denoting the backward window used to build features for , while represents the model parameters.

However, as stated in Section 1, the realized volatilities of the stocks are related through their LOBs. We want to consider this effect in our model and we write our prediction model as:

| (4) |

where is the relationship of stock with all other stocks . It means that our model jointly considers all the features from all other stocks when predicting realized volatility for stock and its relationship with other stocks, instead of only taking its own features into account.

In additional to the relationship among stocks, we can also consider the relationship among the timestamps we predict. For example, at time , we can check whether the behaviors of the stocks are similar to their behaviors at previous timestamps. We use to denote this temporal relationship. Our prediction model is finally written as:

| (5) |

4 Graph Transformer Network for Realized Volatility Forecasting

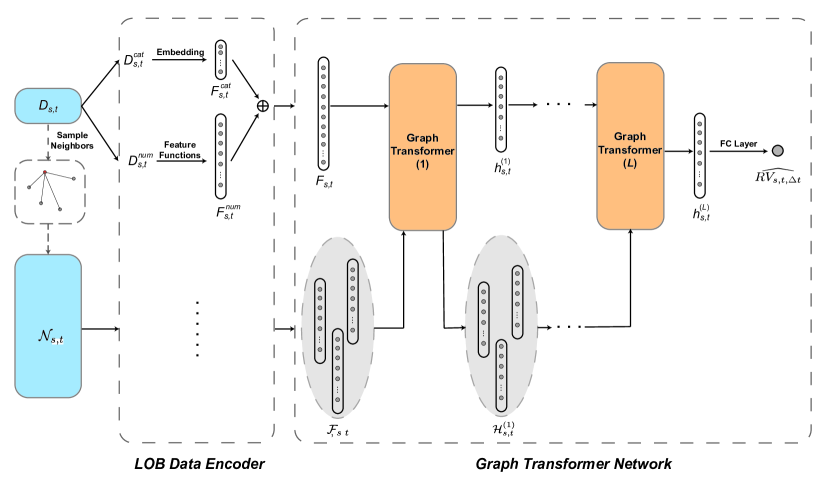

Our model consists of two main components: a LOB data encoder and a Graph Transformer Network. The LOB data encoder transforms numerical LOB data into multiple features. It also transforms categorical information, such as the stock ticker, into a fixed-dimension embedding. It finally concatenates the numerical features and the embedding for categorical features as the node feature.

The Graph Transformer Network then takes all the node features and the pre-defined relationship information as input. After training, it will give each node a new meaningful embedding which contains information from both LOB data and relational data. With a fully connected layer, we can get the final prediction of realized volatility for this node.

An illustration of the whole structure is shown in Figure 1.

4.1 LOB data encoder

We first divide our LOB data into two parts: numerical data and categorical data . For numerical data, we can define different functions to aggregate them into numerical values. Suppose that we have such functions , we get features and we put them into a single vector where

| (6) |

is therefore a vector of size .

Following Kercheval and Zhang (2015); Bissoondoyal-Bheenick et al. (2019); Mäkinen et al. (2019), we define a similar set of numerical features. We also add some other features which are suitable for our dataset. We show the detailed list of features we use in our experiments in Appendix A.

For other categorical features, such as stock ticker, we simply adopt an embedding layer to transform them into a fixed-dimension vector . This vector is of size where is the embedding dimension we can choose.

We then concatenate these two vectors into one vector , where . This operation is written as

| (7) |

where denotes the concatenation operation.

4.2 Graph Transformer Network

As stated in Section 2.2, Graph Transformer operator shows a better performance compared with other structures, we use it to build our network in this study.

We first build a graph with nodes where is the number of timestamps and is the number of stocks. Each node represents the situation of stock at time . Its initial node feature is (Equation 7) encoded by LOB data encoder. From the relationship and , we can find all other nodes connected with . We use to denote all the connected nodes. For each stock at time , the model takes both its own LOB features and the LOB features from other related pairs of into account. It then forecasts the realized volatility based on both self node features and neighbor node features, instead of the traditional approach which considers only self node features.

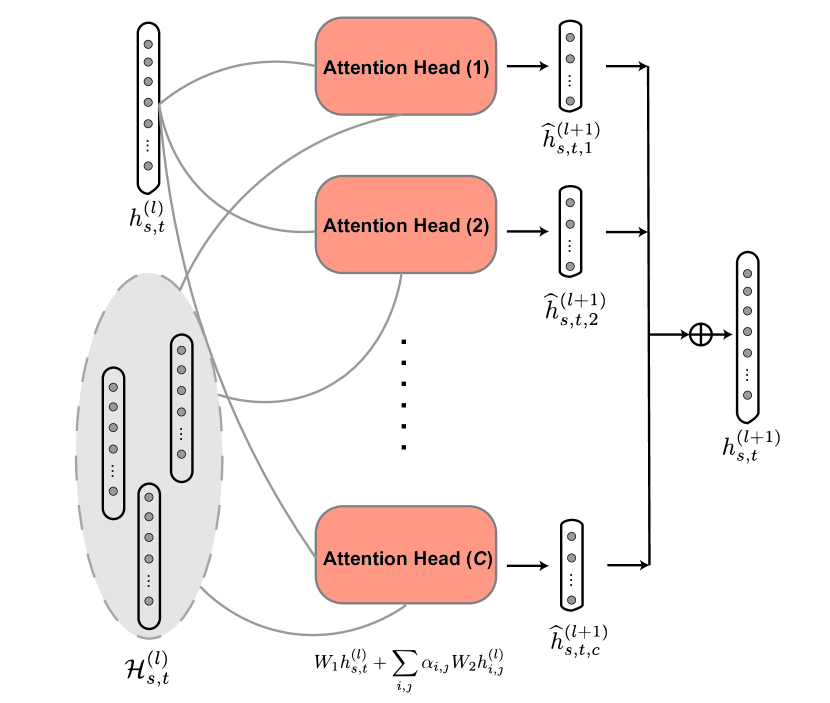

The Graph Transformer operator for the -th layer with heads is written as:

| (8) |

| (9) |

Equation 8 first calculates the output vector for one single head , in which is the -th layer hidden node embedding for , are trainable parameters. are attention coefficients associated with for head . It is calculated via dot product attention (Bahdanau et al., 2014) by

| (10) |

where and are both trainable parameters of size .

We then use Equation 9 to aggregate the output from all heads into a final output vector for the -th layer. It is then used as the input for the -th layer. In this equation, denotes the concatenation operation and is an activation function such as ReLU (Glorot et al., 2011). We show the structure of this operator in Figure 2.

We can then accumulate multiple layers of this structure to better retreive information. Suppose that our Graph Transformer Network (GTN) has layers in total, for each node, its initial node features will be transformed into a node embedding . We then use a fully-connected layer to get the final predictions of realized volatility from the node embeddings. This operation is written as

| (11) |

where are trainable parameters in the fully connected layer.

We then use Root Mean Square Percentage Error (RMSPE) as our loss function to evaluate the model and propagate back into the model. It is define as

| (12) |

where is the total number of nodes in the graph and is a small constant to avoid overflow.

We use RMSPE instead of the standard Mean Square Error (MSE) because the volatilities of different stocks are intrinsically different. For example, more liquid stocks are usually more volatile than less liquid stocks (Domowitz et al., 2001). The RMSPE loss function helps normalize the difference among stocks to make sure that the model has a similar effect on all stocks.

5 Experiments

5.1 LOB data

We use NYSE daily TAQ data222https://www.nyse.com/market-data/historical/daily-taq as our limit order book data. The data contains all the quotes (only first limit, i.e., best bid and best ask) and trades happening in the US stock exchanges. We select the entries concerning all the stocks included in the S&P 500 index333https://www.spglobal.com/spdji/en/indices/equity/sp-500/#overview as our universe. Compared with other researches (5 stocks in Mäkinen et al. (2019), 23 stocks in Rahimikia and Poon (2020b)), this large selection of around 500 stocks also covers some less liquid stocks. We will show that it is more difficult to have a good prediction on less liquid stocks in Section 5.5.1.

Data Sampling

Following Barndorff-Nielsen et al. (2009); Rahimikia and Poon (2020a), we first sample the data with a fixed frequency . Since we focus on short-term volatility forecasting in this paper, we use a one second sampling frequency instead of 5 minutes used by Rahimikia and Poon (2020a) to forecast daily volatility. Our sampling strategy is as follows:

-

•

For quote data, we snapshot the best ask price (), best bid price (), best ask size () and best bid size () for each stock at the end of each second.

-

•

For trade data, we aggregate all the trades for each stock during each second. We record the number of trades (), the total number of shares traded () and the volume weighted average price ()444 where is the price for trade and is the number of shares traded. is the total number of trades recorded during second . of all trades.

An example of sampled quote and trade data is shown in Table 1.

| Date | Symbol | seconds | ||||

|---|---|---|---|---|---|---|

| 1/3/2017 | A | 0 | 45.92 | 1 | 46.09 | 1 |

| 1/3/2017 | A | 1 | 45.92 | 3 | 46 | 2 |

| 1/3/2017 | A | 2 | 45.92 | 2 | 46 | 2 |

| 1/3/2017 | A | 5 | 45.92 | 2 | 46 | 1 |

| 1/3/2017 | A | 6 | 45.94 | 1 | 46.05 | 3 |

| Date | Symbol | seconds | |||

|---|---|---|---|---|---|

| 1/3/2017 | A | 0 | 8 | 1500 | 45.802 |

| 1/3/2017 | A | 1 | 7 | 24959 | 45.94963 |

| 1/3/2017 | A | 2 | 1 | 300 | 45.96 |

| 1/3/2017 | A | 3 | 1 | 100 | 45.9544 |

| 1/3/2017 | A | 5 | 7 | 916 | 45.97817 |

Data Bucket

As introduced in Section 3, our goal is to forecast the realized volatility seconds after a given timestamp based on the features built from a backward window of seconds.

Hence, we need to build buckets which have the length of seconds between and . In each bucket, we only use the returns between and to calculate our target , we use both returns and other information from LOBs between and to build a set of features with LOB data encoder.

In our experiments on US stocks, we create 6 buckets for each stock each day. We select 10:00, 11:00, 12:00, 13:00, 14:00 and 15:00 EST as 6 different . For the sake of simplicity, we use . We use three different of 600 seconds, 1200 seconds and 1800 seconds to show that our model is robust to this choice and is capable of forecasting volatility on different horizons. This choice also ensures that there is no overlap between buckets to avoid information leakage. The detailed experiment results are shown in Section 5.4.

Data Split

We split our LOB data into 3 parts: train, validation and test. We ensure that the validation set and the test set are no earlier than the training set to avoid backward looking. We also remove the buckets where there are no quotes or trades during . Detailed statistics of our dataset are shown in Table 2.

| train | val | test | |

| start | Jan-17 | Jan-20 | Jan-21 |

| end | Dec-19 | Dec-20 | Oct-21 |

| # time | 4,464 | 1,505 | 1,236 |

| # stock | 494 | 494 | 494 |

| # bucket | 2,141,108 | 743,068 | 607,770 |

| proportion | 61% | 21% | 18% |

5.2 Graph Building

As stated in Section 3, we consider both temporal () and cross-sectional () relationships among buckets. In this subsection, we first introduce a method to construct relations without using other data than our LOB data. We also introduce other relations we constructed with external data, for example, stock sector and supply chain data.

5.2.1 Temporal Relationship

To construct the temporal relationship among the nodes, we only use LOB data.

As introduced in Equation 6, for each , we can calculate features. Suppose that is the -th feature for stock at time . For each time , we let

| (13) |

where represents the feature of all stocks at time .

Given a time , we calculate the RMSPE (Equation 12) of between and all other . We then choose the -smallest RMSPE to form pairs of times, represented by . Then for each such pair , we connect the two nodes where is the same and the time is and respectively. This can be written as:

| (14) |

After this operation, we get single-directed edges in the graph for . We then repeat the same process for all , and get edges in total.

In our study, we use two features to get edges in the graph, namely, the average quote WAP555Weighted Average Price, defined as for the first 100 seconds and the average quote WAP for the last 100 seconds in the bucket.

5.2.2 Cross-sectional Relationship

Unlike times, there are intrinsic relations among stocks since each stock represents a company in the real life. Hence, in addition to building relationship based on LOB features, we can also build the cross-sectional graph with external data.

Feature Correlation

We then build the edges for with

| (16) |

with denoting the stock pairs which are among the -smallest feature RMSPE for stock .

We repeat the same process for all stocks and we use the same features as in 5.2.1 to build another edges.

Stock Sector

In finance, each company is classified into a specific sector with Global Industry Classification Standard666https://www.msci.com/our-solutions/indexes/gics (GICS). It is shown that the performances of stocks in the same sector are often correlated (Vardharaj and Fabozzi, 2007). Hence, we simply connect the times of a pair of stocks if they belong to the same sector. This is written as:

| (17) |

where is the ensemble of all the stocks in the sector .

There are four granularities in GICS sector data: Sector, Industry Group, Industry, Sub-Industry. We can therefore construct four different types of edges with this GICS sector data. In our experiments, we use the Industry granularity as it gives a good performance with a reasonable number of edges. The detail of this choice is discussed in Section 5.5.3.

Supply Chain

Supply chain describes the supplier-customer relation between companies and it is proved to be useful in multiple financial tasks such as risk management (Yang et al., 2020) and performance prediction (Chen and Robert, 2021). We use the supply chain data from Factset777https://www.factset.com/marketplace/catalog/product/factset-supply-chain-relationships to build this graph. We connect two companies if they have a supplier-customer relationship in the training period. This is described as:

| (18) |

where is the ensemble of all the supplier-customer relations among the stocks.

We show a detailed statistics of each type of relationship we built in Table 3. In addition to using these relations separately, we can also join these relations by simply putting all the edges together in the same graph. We will show that combining the edges can help improve the result in Section 5.4.

| Type | Relation | # edges |

|---|---|---|

| Temporal | Feature Corr | 8.36M |

| Cross-sectional | Feature Corr | 8.21M |

| Sector | 47.86M | |

| Supply Chain | 22.22M | |

| Total | 76.33M | |

5.3 Baseline Models

In order to prove the effectiveness of our model structure, we also include the performance of some other widely used models as our benchmarks.

-

•

Naïve Guess: We simply use the realized volatility between and to predict the target. It is written as .

-

•

HAR-RV: Heterogeneous AutoRegressive model of Realized Volatility. A simple but effective realized volatility prediction model proposed by Corsi (2009).

-

•

LightGBM: A gradient boosting decision tree model introduced by Ke et al. (2017). It is proven to be highly effective on tabular data.

-

•

MLP: Multi-Layer Perception network (Rumelhart et al., 1985). We build a fully connected neural network with three layers, which have 128, 64, 32 hidden units respectively.

-

•

TabNet: A neural network proposed by Arık and Pfister (2020) which specializes in dealing with tabular data.

-

•

Vanilla GTN-VF: Our Graph Transformer Network for Volatility Forecasting trained without any relationship information.

In addition, we show the model performance with different relations individually to demonstrate how different types of relational data help improve the result compared with Vanilla GTN-VF and other benchmarks.

5.4 Experiment Results

| Model | val | test | val | test | val | test |

| Naïve Guess | 0.2911 | 0.2834 | 0.2650 | 0.2628 | 0.2296 | 0.2364 |

| HAR-RV | 0.2684 | 0.2612 | 0.2149 | 0.2061 | 0.1968 | 0.1939 |

| LightGBM | 0.2583 | 0.2492 | 0.2414 | 0.2035 | 0.2349 | 0.1963 |

| MLP | 0.2431 | 0.2514 | 0.2200 | 0.2308 | 0.2270 | 0.1999 |

| TabNet | 0.2517 | 0.2478 | 0.2212 | 0.1996 | 0.2204 | 0.2019 |

| Vanilla GTN-VF | 0.2457 | 0.2498 | 0.2229 | 0.2251 | 0.2092 | 0.2160 |

| GTN-VF Cross FC | 0.2414 | 0.2382 | 0.2162 | 0.2196 | 0.2066 | 0.2046 |

| GTN-VF Temp FC | 0.2326 | 0.2358 | 0.1974 | 0.1921 | 0.1896 | 0.1853 |

| GTN-VF Cross Sector | 0.2406 | 0.2422 | 0.2067 | 0.2248 | 0.2071 | 0.2091 |

| GTN-VF Cross Supply Chain | 0.2430 | 0.2411 | 0.2105 | 0.2244 | 0.2057 | 0.2000 |

| GTN-VF Cross FC + Temp FC | 0.2326 | 0.2306 | 0.1936 | 0.1917 | 0.1848 | 0.1802 |

| GTN-VF | 0.2314 | 0.2287 | 0.1916 | 0.1892 | 0.1809 | 0.1798 |

In our short-term realized volatility forecasting task, we use a 3-layer () Graph Transformer Network with 8 heads (). All three layers have 128 channels (). We embed our categorical features into a 32-dimension vector ().

The detailed results of our experiments are shown in Table 4. We can see that our full GTN-VF model with all four types of relational information outperforms all baseline models and each type of relational information individually on all prediction horizons. The improvement is significant. In average, we gain 6% in RMSPE compared with Naïve Guess and 2% compared with the best baseline model TabNet on test set. It proves that our GTN model structure and relation building methods are effective.

In terms of individual relationship, all relations are useful since they all show improvement compared with the vanilla model. The temporal feature correlation shows the most predicting power, contributing 1.2% RMSPE gain while the Sector relation only contributes 0.7% improvement when the window is set to 600 seconds although it has the largest number of edges. This can be explained by the ’noise’ included in this type of information since we need to connect every two stocks in the same sector although not all of them have significant connection. However, feature correlation only selects the two most related stocks or times, making it more discriminational when building edges. This suggests that if we have the constraint on the number of edges in the graph, quality is more important than quantity. On the other hand, these relations are complementary to each other, adding more relations on top of existing relations can help improve the prediction if we have enough computing power.

It is also worth noting that when we forecast the realized volatility with a longer forward looking and backward looking window, the result is better. This is simple because the same volatility jump causes more volatility changes in shorter forecasting horizon (Ma et al., 2019).

5.5 Ablation Studies

5.5.1 Prediction accuracy and stock liquidity

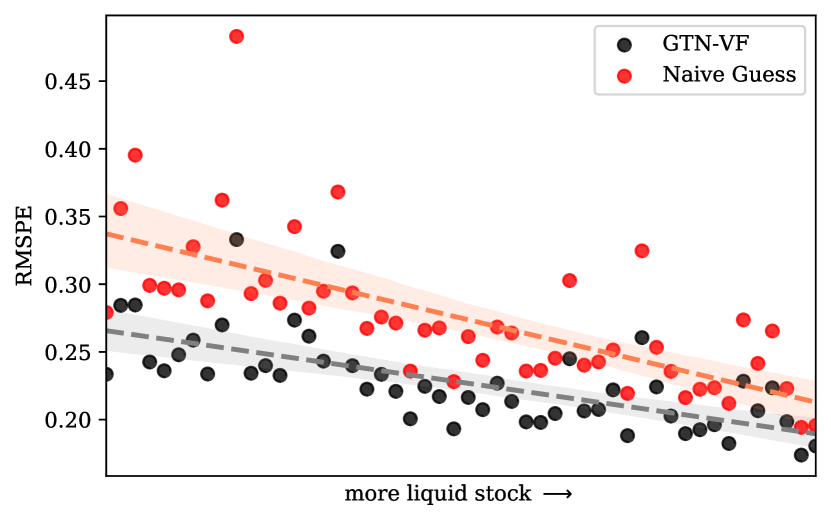

In general, it is more difficult to have a good prediction on less liquid stocks because there are fewer market participants for them. One sudden change in quote or trade can cause significant volatility jump, which is difficult to foresee. We analyze the result to understand where the improvement comes from.

We first split the stocks into 50 buckets according to their average daily turnover, which represents the liquidity of a stock. We calculate the RMSPE in each bucket for both Naïve Guess and GTN-VF. The result is illustrated in Figure 3.

First, we notice that more liquid stocks have smaller RMSPE for both models, which is intuitive. The prediction for the most liquid stocks is 5% better than the least liquid stocks in terms of RMSPE, which is a large margin in realized volatility forecasting. We can also see that our graph based model has more improvement on the less liquid stocks (around 8% for more liquid stocks and 2% for less liquid stocks), although it is more effective than Naïve Guess on all scenarios.

5.5.2 Prediction accuracy and node connection

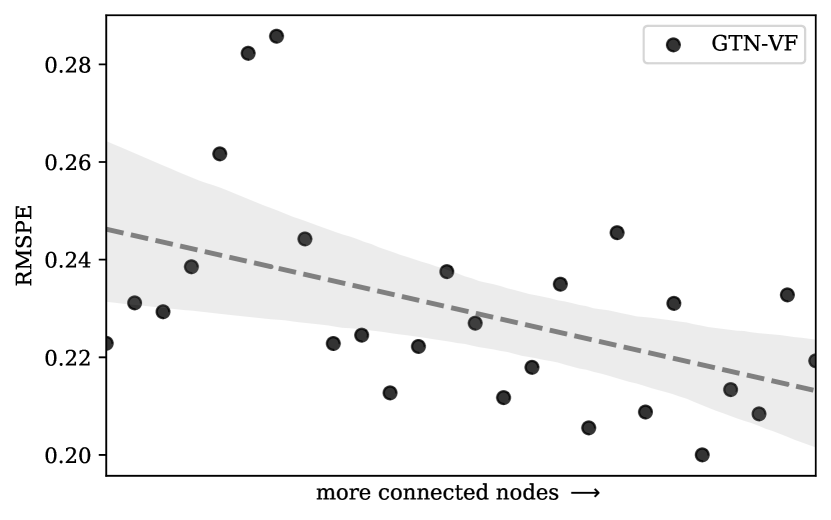

We also investigate how our model performs on different nodes. We use the same approach in Section 5.5.1 by splitting nodes into buckets according to the number of edges connected to each node. We can see from Figure 4 that more connected nodes usually have better RMSPE result, with a 2% difference between the most connected and the least connected. This can be explained by the fact that mode connected nodes make decision based on more information from their neighbor, while the nodes with fewer or no connections can only rely on the information from themselves. This phenomenon proves again the effectiveness of our graph based method.

5.5.3 Sector Relationship

As introduced in Section 5.2.2, there are four granularities in the GICS sector data. We run different experiments to evaluate the performance of each type of sector relationship. The result is shown in Table 5.

| Granularity | # edges | test RMSPE |

|---|---|---|

| Sector | 178.7M | N.A. |

| IndustryGroup | 83.39M | 0.2578 |

| Industry | 47.86M | 0.2422 |

| SubIndustry | 19.88M | 0.2441 |

We observe that Industry shows the best performance with a modest number of edges. If we add more edges, such as IndustryGroup, the RMSPE decreases since the relations among stocks are less meaningful. For the Sector granularity, we are not even able to obtain a result since the number of edges exceeds the memory limit. Hence, in our final model combining multiple sources of relations, we choose Industry as our sector relationship.

6 Conclusion

We forecast the short-term realized volatility in a multivariate approach. We design a graph based neural network: Graph Transformer Network for Volatility Forecasting which incorporates both features from LOB data and relationship among stocks from different sources. Through extensive experiments on around 500 stocks, we prove the that our method outperforms other baseline models, both univariate and multivariate. In addition, the model structure allows to combine an unlimited number of relations, the study of the effectiveness of other relational data is open for future researches.

Acknowledgments

The authors gratefully acknowledge the financial support of the Chaire Machine Learning & Systematic Methods in Finance.

References

- Andersen and Bollerslev (1998) Torben G Andersen and Tim Bollerslev. 1998. Answering the skeptics: Yes, standard volatility models do provide accurate forecasts. International economic review pages 885–905.

- Andersen et al. (2005) Torben G Andersen, Tim Bollerslev, Peter Christoffersen, and Francis X Diebold. 2005. Volatility forecasting.

- Arık and Pfister (2020) Sercan O Arık and Tomas Pfister. 2020. Tabnet: Attentive interpretable tabular learning. arXiv .

- Bahdanau et al. (2014) Dzmitry Bahdanau, Kyunghyun Cho, and Yoshua Bengio. 2014. Neural machine translation by jointly learning to align and translate. arXiv preprint arXiv:1409.0473 .

- Barndorff-Nielsen et al. (2009) Ole E Barndorff-Nielsen, P Reinhard Hansen, Asger Lunde, and Neil Shephard. 2009. Realized kernels in practice: Trades and quotes.

- Berg et al. (2017) Rianne van den Berg, Thomas N Kipf, and Max Welling. 2017. Graph convolutional matrix completion. arXiv preprint arXiv:1706.02263 .

- Bissoondoyal-Bheenick et al. (2019) Emawtee Bissoondoyal-Bheenick, Robert Brooks, and Hung Xuan Do. 2019. Asymmetric relationship between order imbalance and realized volatility: Evidence from the australian market. International Review of Economics & Finance 62:309–320.

- Bollerslev et al. (2019) Tim Bollerslev, Nour Meddahi, and Serge Nyawa. 2019. High-dimensional multivariate realized volatility estimation. Journal of Econometrics 212(1):116–136.

- Brailsford and Faff (1996) Timothy J Brailsford and Robert W Faff. 1996. An evaluation of volatility forecasting techniques. Journal of Banking & Finance 20(3):419–438.

- Bruna et al. (2013) Joan Bruna, Wojciech Zaremba, Arthur Szlam, and Yann LeCun. 2013. Spectral networks and locally connected networks on graphs. arXiv preprint arXiv:1312.6203 .

- Bucci (2020) Andrea Bucci. 2020. Cholesky–ann models for predicting multivariate realized volatility. Journal of Forecasting 39(6):865–876.

- Campbell et al. (1993) John Y Campbell, Sanford J Grossman, and Jiang Wang. 1993. Trading volume and serial correlation in stock returns. The Quarterly Journal of Economics 108(4):905–939.

- Chen and Robert (2021) Qinkai Chen and Christian-Yann Robert. 2021. Graph-based learning for stock movement prediction with textual and relational data. arXiv preprint arXiv:2107.10941 .

- Corsi (2009) Fulvio Corsi. 2009. A simple approximate long-memory model of realized volatility. Journal of Financial Econometrics 7(2):174–196.

- Defferrard et al. (2016) Michaël Defferrard, Xavier Bresson, and Pierre Vandergheynst. 2016. Convolutional neural networks on graphs with fast localized spectral filtering. Advances in neural information processing systems 29:3844–3852.

- Domowitz et al. (2001) Ian Domowitz, Jack Glen, and Ananth Madhavan. 2001. Liquidity, volatility and equity trading costs across countries and over time. International Finance 4(2):221–255.

- Gatheral and Oomen (2010) Jim Gatheral and Roel CA Oomen. 2010. Zero-intelligence realized variance estimation. Finance and Stochastics 14(2):249–283.

- Gilmer et al. (2017) Justin Gilmer, Samuel S Schoenholz, Patrick F Riley, Oriol Vinyals, and George E Dahl. 2017. Neural message passing for quantum chemistry. In International conference on machine learning. PMLR, pages 1263–1272.

- Gini (1921) Corrado Gini. 1921. Measurement of inequality of incomes. The economic journal 31(121):124–126.

- Glorot et al. (2011) Xavier Glorot, Antoine Bordes, and Yoshua Bengio. 2011. Deep sparse rectifier neural networks. In Proceedings of the fourteenth international conference on artificial intelligence and statistics. JMLR Workshop and Conference Proceedings, pages 315–323.

- Hamilton et al. (2017) William L Hamilton, Rex Ying, and Jure Leskovec. 2017. Inductive representation learning on large graphs. In Proceedings of the 31st International Conference on Neural Information Processing Systems. pages 1025–1035.

- Ke et al. (2017) Guolin Ke, Qi Meng, Thomas Finley, Taifeng Wang, Wei Chen, Weidong Ma, Qiwei Ye, and Tie-Yan Liu. 2017. Lightgbm: A highly efficient gradient boosting decision tree. Advances in neural information processing systems 30:3146–3154.

- Kercheval and Zhang (2015) Alec N Kercheval and Yuan Zhang. 2015. Modelling high-frequency limit order book dynamics with support vector machines. Quantitative Finance 15(8):1315–1329.

- Kipf and Welling (2016) Thomas N Kipf and Max Welling. 2016. Semi-supervised classification with graph convolutional networks. arXiv preprint arXiv:1609.02907 .

- Kwan et al. (2005) CK Kwan, WK Li, and K Ng. 2005. A multivariate threshold garch model with time-varying correlations. Econometric reviews 24.

- Li et al. (2017) Yaguang Li, Rose Yu, Cyrus Shahabi, and Yan Liu. 2017. Diffusion convolutional recurrent neural network: Data-driven traffic forecasting. arXiv preprint arXiv:1707.01926 .

- Ma et al. (2019) Feng Ma, Yin Liao, Yaojie Zhang, and Yang Cao. 2019. Harnessing jump component for crude oil volatility forecasting in the presence of extreme shocks. Journal of Empirical Finance 52:40–55.

- Mäkinen et al. (2019) Ymir Mäkinen, Juho Kanniainen, Moncef Gabbouj, and Alexandros Iosifidis. 2019. Forecasting jump arrivals in stock prices: new attention-based network architecture using limit order book data. Quantitative Finance 19(12):2033–2050.

- Malec (2016) Peter Malec. 2016. A semiparametric intraday garch model .

- Rahimikia and Poon (2020a) Eghbal Rahimikia and Ser-Huang Poon. 2020a. Big data approach to realised volatility forecasting using har model augmented with limit order book and news. Available at SSRN 3684040 .

- Rahimikia and Poon (2020b) Eghbal Rahimikia and Ser-Huang Poon. 2020b. Machine learning for realised volatility forecasting. Available at SSRN 3707796 .

- Ramos-Pérez et al. (2021) Eduardo Ramos-Pérez, Pablo J Alonso-González, and José Javier Núñez-Velázquez. 2021. Multi-transformer: A new neural network-based architecture for forecasting s&p volatility. Mathematics 9(15):1794.

- Rumelhart et al. (1985) David E Rumelhart, Geoffrey E Hinton, and Ronald J Williams. 1985. Learning internal representations by error propagation. Technical report, California Univ San Diego La Jolla Inst for Cognitive Science.

- Sawhney et al. (2020) Ramit Sawhney, Shivam Agarwal, Arnav Wadhwa, and Rajiv Shah. 2020. Deep attentive learning for stock movement prediction from social media text and company correlations. In Proceedings of the 2020 Conference on Empirical Methods in Natural Language Processing (EMNLP). pages 8415–8426.

- Shi et al. (2020) Yunsheng Shi, Zhengjie Huang, Shikun Feng, Hui Zhong, Wenjin Wang, and Yu Sun. 2020. Masked label prediction: Unified message passing model for semi-supervised classification. arXiv preprint arXiv:2009.03509 .

- Sirignano and Cont (2019) Justin Sirignano and Rama Cont. 2019. Universal features of price formation in financial markets: perspectives from deep learning. Quantitative Finance 19(9):1449–1459.

- Vardharaj and Fabozzi (2007) Raman Vardharaj and Frank J Fabozzi. 2007. Sector, style, region: Explaining stock allocation performance. Financial Analysts Journal 63(3):59–70.

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Lukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. arXiv preprint arXiv:1706.03762 .

- Veličković et al. (2017) Petar Veličković, Guillem Cucurull, Arantxa Casanova, Adriana Romero, Pietro Lio, and Yoshua Bengio. 2017. Graph attention networks. arXiv preprint arXiv:1710.10903 .

- Yang et al. (2020) Shuo Yang, Zhiqiang Zhang, Jun Zhou, Yang Wang, Wang Sun, Xingyu Zhong, Yanming Fang, Quan Yu, and Yuan Qi. 2020. Financial risk analysis for smes with graph-based supply chain mining. In IJCAI. pages 4661–4667.

- Zhang and Rosenbaum (2020) Jianfei Zhang and Mathieu Rosenbaum. 2020. Universal volatility formation : perspective from rough volatility and deep learning. Technical report, Ecole Polytechnique.

- Zhang (2006) Lan Zhang. 2006. Efficient estimation of stochastic volatility using noisy observations: A multi-scale approach. Bernoulli 12(6):1019–1043.

- Zhou (1996) Bin Zhou. 1996. High-frequency data and volatility in foreign-exchange rates. Journal of Business & Economic Statistics 14(1):45–52.

Appendix A List of node features

We introduce the features we use in our experiments.

In each bucket, we have lines as training data. We first calculate an indicator for each line, we then aggregate these indicators in the same bucket with an aggregation function (aggregator). In such way, we have one value per indicator per aggregator as one feature for the bucket. The full list of indicators and aggregators are listed in Table 6.

For some important indicators, we also calculate their progressive features. It means that instead of applying an aggregator on all the lines, we apply it on the lines between 0 and , , , , , . In such way, we have 6 features per indicator per aggregator for an progressive feature. This is shown in the column Progressive in Table 6.

We define our aggregation functions as follows. We use to denote the -th line in the bucket and represents the total number of lines.

| Type | Notation | Description | Aggregators | Progressive | Count |

| Quote | WAP | mean, std, gini | N | 5 | |

| mean of first 100, mean of last 100 | |||||

| Ask Price | % difference | N | 1 | ||

| Bid Price | % difference | N | 1 | ||

| Price Relative Spread | mean, std, gini | N | 3 | ||

| WAP bid difference | mean, std, gini | N | 3 | ||

| Return | realized volatility | Y | 6 | ||

| Squared Return | std, gini | N | 2 | ||

| Size Relative Spread | mean, std, gini | N | 3 | ||

| Ask Size | % difference | N | 1 | ||

| Bid Size | % difference | N | 1 | ||

| Normalized Ask Size | mean, std, gini | N | 3 | ||

| Total Size | sum, max | N | 2 | ||

| Size Imbalance | sum, max | N | 2 | ||

| Trade | Price | % greater than mean, % less than mean | N | 5 | |

| median diviation, energy, IQR | |||||

| Return | realized volatility | Y | 6 | ||

| % greater than 0, % less than 0 | N | 2 | |||

| Squared Return | std, gini | N | 2 | ||

| Size | sum | Y | 6 | ||

| max, median diviation, energy, IQR | N | 4 | |||

| Seconds | count | Y | 6 | ||

| Order Count | sum | Y | 6 | ||

| max | N | 1 | |||

| Amount | sum, max | N | 2 | ||

| Total | 73 | ||||