Two-Price Equilibrium ††thanks: This work was partially supported by the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement No. 866132), by the Israel Science Foundation (grant number 317/17), and by the NSF-BSF (grant number 2020788).

Abstract

Walrasian equilibrium is a prominent market equilibrium notion, but rarely exists in markets with indivisible items. We introduce a new market equilibrium notion, called two-price equilibrium (2PE). A 2PE is a relaxation of Walrasian equilibrium, where instead of a single price per item, every item has two prices: one for the item’s owner and a (possibly) higher one for all other buyers. Thus, a 2PE is given by a tuple of an allocation S and two price vectors , where every buyer is maximally happy with her bundle , given prices for items in and prices for all other items. 2PE generalizes previous market equilibrium notions, such as conditional equilibrium, and is related to relaxed equilibrium notions like endowment equilibrium. We define the discrepancy of a 2PE — a measure of distance from Walrasian equilibrium — as the sum of differences over all items (normalized by social welfare). We show that the social welfare degrades gracefully with the discrepancy; namely, the social welfare of a 2PE with discrepancy is at least a fraction of the optimal welfare. We use this to establish welfare guarantees for markets with subadditive valuations over identical items. In particular, we show that every such market admits a 2PE with at least of the optimal welfare. This is in contrast to Walrasian equilibrium or conditional equilibrium which may not even exist. Our techniques provide new insights regarding valuation functions over identical items, which we also use to characterize instances that admit a WE.

1 Introduction

We consider a combinatorial market setting with items and buyers. Every buyer has a valuation function, , which maps every subset of items to a non-negative real number. A valuation profile is given by a vector . As standard, we assume that valuation functions are monotone and normalized, i.e., for every and for every .

An allocation is a partition of the items among the buyers; i.e., a vector of disjoint sets, where denotes the bundle allocated to buyer . The social welfare (SW) of an allocation S under valuation profile v is the sum of the buyers’ valuations for their bundles, that is, . The optimal (welfare-maximizing) allocation is denoted by .

Suppose every item has some price . Given a vector of prices , and an allocation S, the (quasi-linear) utility of buyer is .

Walrasian equilibrium (WE) is a classical and appealing market equilibrium notion that dates back to the 70’s (Walras [25]). In a WE, despite competition among buyers, every buyer is maximally happy with her bundle and the market clears. That is, a WE is given by a tuple ( satisfying: (i) Utility maximization: for every bundle , and (ii) Market clearance: all items are sold. Moreover, by the first welfare theorem (Bikhchandani and Mamer [3]), any allocation supported in a WE has optimal social welfare.

This appealing notion, however, comes with a serious downside, namely, it rarely exists in markets. In particular, it is known to exist for a strict subclass of submodular valuations, known as gross substitutes (Kelso and Crawford [20]), and in some precise technical sense, gross substitutes is a maximal class for WE existence (Gul and Stacchetti [15]).

As a result, different relaxations of WE have been introduced and studied. A notable one is the notion of conditional equilibrium (CE) (Fu et al. [14]), which is a tuple satisfying: (i) individual rationality: , (ii) outward stability: for every bundle and (iii) market clearance (all items are sold). That is, the difference between a WE and a CE is that it only requires that buyers do not wish to add items to their bundle, whereas a WE requires that buyers don’t wish to change their bundle with any other bundle. A CE is guaranteed to exist for every market with submodular valuations (or even a superclass of submodular, called XOS). In addition, the CE notion admits an approximate version of the first welfare theorem; namely, any allocation supported in a CE has social welfare of at least half of the optimal social welfare. However, the notion of CE has its limitations — it may not exist even in a market with two subadditive buyers (see Example 3.2).

Two-price equilibrium. We introduce a new notion of equilibrium that is based on the idea that an item may be assigned more than a single price. Indeed, item prices often have different prices based on different buyer characteristics, such as location, time, and history.

The new notion, termed two-price equilibrium (2PE), utilizes two prices per item. A 2PE is a relaxation of Walrasian equilibrium, and generalizes other WE relaxations (e.g., conditional equilibrium). Like WE, it is a tuple of allocation and prices that clears the market (every buyer is maximally happy and all items are sold). However, in contrast to WE, where every item has a single price, 2PE specifies two prices for each item: one price for the item’s owner and (a possibly higher) one for all other buyers. The utility maximization condition then states that every buyer is maximally happy with her bundle, given that she pays the low price for items in her possession, and the high price for all other items.

Formally, a 2PE is given by a tuple where are the high and low prices, respectively ( for every item ), and where (i) Utility maximization: for every bundle , and (ii) all items are sold. We note that Condition (i) of 2PE can be also written as for every bundle .

A 2PE for which for every item is a Walrasian equilibrium. Furthermore, one can show that is a conditional equilibrium iff is a 2PE (see Proposition 3.3). The 2PE notion is related to other relaxations of WE, such as the endowment equilibrium ([1], [9]), named after the endowment effect, discovered by Nobel laureate Richard Thaler ([18], [19], [21]), stating that buyers tend to inflate the value of items they own. Moreover, as we show in Section 3.1, 2PE is also related to Nash equilibria of simultaneous item auctions — a simple auction format that attracted much research in the last decade ([2], [6], [12], [11], [7], [4]).

Clearly, a 2PE is guaranteed to exist for every market instance. Moreover, every allocation can be supported in a 2PE. Indeed, for every allocation S, the tuple where and for every item is a 2PE. Thus, arbitrarily bad allocations can be supported in a 2PE. This is in stark contrast to Walrasian equilibrium or conditional equilibrium, where supported allocations have optimal welfare (for WE [3]) or at least half of the optimal welfare (for CE [14]). Moreover, 2PE’s in which the high and low prices of items admit a large difference seem to be far from the notion of Walrasian equilibrium.

To study 2PE’s that are “close” to WE, we define a new metric, called the discrepancy of a 2PE, defined as the sum of price differences over all items, , normalized by the social welfare. The discrepancy of a 2PE can be viewed as a measure of the distance between a given 2PE and a Walrasian equilibrium. Indeed, a 2PE with discrepancy 0 is a WE. Thus, every 2PE with discrepancy 0 has optimal welfare. We then ask whether there are instances that do not admit WE, or WE relaxations (such as CE), but do admit 2PE with low discrepancy and high welfare.

A particularly interesting class of valuations is the class of subadditive valuations — where for every sets . This is a natural class of valuations, known to be the frontier of “complement-free” valuations [22]. Markets with subadditive valuations may not admit any WE or CE, even in cases where all the items are identical. The following question arises:

Question: Do markets with subadditive valuations admit 2PE’s with low discrepancy and high welfare?

1.1 Our Results

We first show that the social welfare of a 2PE degrades gracefully with its discrepancy. Namely, the social welfare of a 2PE with discrepancy is at least a fraction of the optimal social welfare. Armed with this welfare guarantee, our goal is to show the existence of 2PE’s with low discrepancy. We establish such results for markets with subadditive valuations over identical items.

It should be noted that the problem of efficiently allocating identical items among multiple buyers has played a starring role in classical and algorithmic mechanism design. Identical item settings are of particular interest in our context, where a WE is guaranteed to exist for submodular valuations, but beyond submodular, even simple instances may not admit a WE, or even a relaxed equilibrium notion, such as conditional euilibrium.

We first establish a low discrepancy result for markets with two identical subadditive valuations over identical items.

Theorem 1: (see Theorem 7.1) Every market with 2 identical subadditive valuations over identical items admits a 2PE with discrepancy of at most 2, thus welfare of at least of the optimal welfare.

Moreover, we show an instance with 2 identical subadditive valuations, where the minimum discrepancy for any 2PE is (see Theorem 7.2).

For an arbitrary number of identical valuations over identical items we show the following:

Theorem 2: (see Theorem 7.3) Every market with (any number of) identical subadditive valuations over identical items admits a 2PE with discrepancy of at most , thus welfare of at least of the optimal welfare.

Our main result establishes a constant factor guarantee for markets with heterogeneous subadditve valuations over identical items.

Main Theorem: (see Theorem 8.1) Every market with (any number of) subadditive valuations over identical items admits a 2PE with discrepancy of at most , thus welfare of at least of the optimal welfare.

Furthermore, we find an interesting connection between 2PE and pure Nash equilibria (PNE) of simultaneous item auctions [5]. In these auctions every bidder submits a bid for every item, and items are sold simultaneously, each one in a separate auction given its own bids. For example, a simultaneous second price auction (S2PA) is one where every item is sold in a 2nd price auction.

We show a correspondence between 2PEs of a market and PNE of S2PA for the corresponding market (see Proposition 3.5). Similar correspondences have been shown for WE and PNE of simultaneous first price auctions [17] and for conditional equilibria and PNE of S2PA under the no-overbidding assumption [14].

Combined with our welfare guarantees for 2PEs in markets with subadditive valuations over identical items, this correspondence implies that S2PA for such markets admit PNE (without no-overbidding) with a constant fraction of the optimal welfare. Note that S2PAs for such markets do not necessarily admit PNE with no-overbidding [2].

To obtain our results, we provide new tools for the analysis of valuation functions over identical items. Using these tools, we also establish a necessary and sufficient condition for the existence of WE given an arbitrary valuation profile over identical items (see Theorem 9.1).

Open Problems:

Our model and results constitute a first step in the analysis of 2PE, and leave some open problems for future work. Most immediately, it would be interesting to close the gaps between the upper and lower bounds on the discrepancy of the markets we study. In addition, it would be interesting to conduct a similar analysis for markets with heterogeneous items. Specifically, do markets with subadditive valuations over heterogeneous items admit a 2PE with constant discrepancy? (This is true for XOS valuations.) If the answer to this question is affirmative, then it implies that every S2PA admits a PNE with constant approximation to the optimal welfare. Finally, in Section 3.1 we show that every PNE of a S2PA has a corresponding 2PE with the same allocation (see Proposition 3.5). Feldman and Shabtai [11] establish bounds on the price of anarchy of S2PA under a “no underbidding” assumption for different valuation classes. It would be interesting to study whether a PNE satisfying no underbidding corresponds to a 2PE with bounded discrepancy.

1.2 Additional Related Work

Our work belongs to the line of research proposing relaxed market equilibrium notions that exist quite broadly and gives good welfare guarantees. Obvious examples include the conditional equilibrium notion of Fu et al. [14] discussed above and the combinatorial Walrasian equilibrium notion introduced by Feldman et al. [13]. Fu et al. [14] show that a market admits a conditional equilibrium if and only if a S2PA for the corresponding market admits a PNE with no overbidding. A related notion is local equilibrium, introduced by Lehmann [23], which generalizes conditional equilibrium by relaxing individual rationality and outward stability. The endowment equilibrium notion was proposed by Babaioff et al. [1] to capture the endowment effect discovered by [18]. Babaioff et al. [1] showed that every market with submodular valuations admits an endowment equilibrium with at least a half of the optimal welfare. Ezra et al. [9] introduced a general framework that captures a wide range of formulations for the endowment effect, and showed that stronger endowment effects can lead to existence of endowment equilibrium also in XOS markets. We show conditions under which one can transform an endowment equilibrium to a 2PE and vice versa. Ezra et al. [10] provide welfare guarantees via pricing for markets with identical items.

2 Preliminaries

Recall that we consider a combinatorial market setting with buyers and items, where every buyer has a valuation function that maps every subset of items into a real number (denoted by ). In this paper we consider mainly valuations over identical items, where , specifies the value of buyer for every number of items between 0 and (denoted by ). Such valuations are also called symmetric valuations. We consider the following symmetric valuation classes111The definitions of these valuation classes for heterogeneous items appear in Appendix A..

-

•

Unit demand: there exist a value , s.t. for every

-

•

Additive: there exist a value , s.t. for every

-

•

Submodular: for every

-

•

XOS: for any

-

•

Subadditive: for any s.t.

2.1 Walrasian Equilibrium and Relaxations

In this section we present the definitions of Walrasian equilibrium and conditional equilibrium (for general valuations). The definition of endowment equilibrium is deferred to Section 10.

Definition 2.1 (Walrasian equilibrium (WE) [25]).

A pair of an allocation and item prices , is a Walrasian equilibrium if:

-

1.

Utility maximization: Every buyer receives an allocation that maximizes her utility given the item prices, i.e., for every and bundle .

-

2.

Market clearance: All items are allocated.222More precisely, if an item is not allocated, then . One can easily verify that every such unallocated item can be allocated to an arbitrary buyer, and the resulting allocation, together with the original price vector, is also a Walrasian equilibrium. For simplicity of presentation, we assume throughout the paper that all items are allocated.

Definition 2.2 (Conditional equilibrium (CE) [14]).

A pair of an allocation and item prices , is a Conditional equilibrium if:

-

1.

Individual rationality: Every buyer has a non-negative utility, i.e., for every .

-

2.

Outward Stability: No buyer wishes to add items to her bundle, i.e., for every and bundle .

-

3.

Market clearance: All items are allocated.

An additional interesting relaxation of WE that attracted some attention recently is the notion of endowment equilibrium [1; 9], called after the endowment effect [18; 19; 21]. An endowment equilibrium is a Walrasian equilibrium with respect to endowed valuations, which inflate the value of items owned by the buyer. In Section 10 we discuss the relation between an endowment equilibrium and 2PE.

3 Two-Price Equilibrium (2PE)

In this section we introduce a new equilibrium notion termed Two Price Equilibrium (2PE). As we shall see, 2PE generalizes some market equilibrium notions considered in the literature.

A 2PE resembles a Walrasian equilibrium, but instead of one price per item, it has two prices per item: high and low. It requires that every buyer receives the bundle that maximizes her utility, given that she pays the low price on items in her bundle, and would have to pay the high price for items not in her bundle. The formal definition follow.

Definition 3.1 (Two Price Equilibrium (2PE)).

Given a valuation profile v, a triplet, , of an allocation S, and high and low price vectors , s.t. for every item , is called a two price equilibrium (2PE) if the following hold:

-

1.

Utility maximization: For every bundle and every buyer :

This is equivalent to

(1) -

2.

Market clearance: All items are allocated.

2PE generalizes both Walrasian equilibrium and conditional equilibrium. We next present a market that admits no Walrasian equilibrium nor conditional equilibrium, and yet, the optimal allocation can be supported in a 2PE.

Example 3.2.

Consider a market with 2 buyers and an item set . Suppose buyer 1 has the following subadditive valuations

and buyer 2 has a unit-demand valuation, where for every non-empty bundle. We claim that this market has no conditional equilibrium (CE). To see this, consider two cases. Case 1: all items are allocated to buyer 1. For this allocation to be supported by a CE, for every item . However, this violates individual rationality for buyer 1. Case 2: buyer 2 receives a non-empty bundle. To satisfy individual rationality, the sum of prices in buyer 2’s bundle cannot exceed . This, however, violates outward stability for buyer 1. We conclude that no CE exists for this market. The optimal allocation gives all items to buyer 1. One can verify that this allocation is supported by a 2PE with and for every item . Indeed, buyer 1 is maximally happy with the grand bundle, since dropping any item (or both) would give her a lower utility. Similarly, buyer 2 cannot increase her utility, since in order to obtain any item , she would need to pay , for a utility of 0.

Relation between 2PE and other market equilibrium notions.

Clearly, every 2PE in which for every item is a WE. That is, for every valuation profile v, is a WE if and only if is a 2PE for v.

The following proposition shows that CE is a special case of 2PE as well.

Proposition 3.3.

For every valuation profile v, is a CE if and only if is a 2PE.

Proof.

Assume that is a 2PE. We show that is a CE. Market clearance and individual rationality holds by the definition of 2PE. For outward stability, we show that no buyer can gain from adding items to . By utility maximization of 2PE, we have that for every buyer and every set , . Specifically, this inequality is true for every set , where . Thus, for every , , or which is precisely outward stability. It follows that is a CE

Now assume that is a CE. We show that is a 2PE. Market clearance holds by the definition of CE. By outward stability, for every buyer and every set ,

i.e.,

For every set , let . Then, by monotonicity . Thus, utility maximization follows, and is a 2PE. ∎

In Section 10 we show a strong connection between endowment equilibrium and 2PE; namely, we show how a 2PE can be transformed into an endowment equilibrium and vice versa.

3.1 Relation Between 2PE and Simultaneous Second Price Auctions

A simultaneous second price auction (S2PA) is a simple auction format, where, despite the complex valuations of the bidders, every bidder submits a bid on every item, and every item is sold separately in a 2nd price auction; i.e., every item is sold to the bider who submitted the highest bid for that item, and the winner pays the second highest bid for that item.

A bid profile in a S2PE is denoted by , where is the bid vector of bidder ; being bidder ’s bid on item , for . Let denotes the set of items won by buyer , and let denote the obtained allocation. Finally, let denote the price paid by the winner of item (i.e., the second highest bid on item ).

A S2PA is not a truthful auction, and its performance is often measured in equilibrium. A bid profile is said to be a pure Nash equilibrium in a S2PA if the following holds.

Definition 3.4.

A bid profile in a S2PA is a pure Nash equilibrium (PNE) if for any and for any , .

The following proposition shows that a pure Nash equilibrium of S2PA corresponds to a 2PE of the corresponding market.

Proposition 3.5.

Consider a valuation profile v. The triplet is a 2PE for v if and only if there exists a bid profile, , which is a PNE of the S2PA for (under some tie breaking rule), such that , and for every item , and .

Proof.

Assume that is a S2PA PNE for . We show that is a 2PE. Notice that for every , . Since is a PNE, for every buyer , for every bid . Let and substitute and , then:

By subtracting from both sides and rearranging, we get:

which is precisely the utility maximization condition of 2PE. Moreover, all items are allocated in , and therefore the market clearance condition is also satisfied. Hence, the triplet is a 2PE.

Now assume that is a 2PE. We need to show that there exists a bid profile, , which is a S2PA PNE for (under some tie breaking rule), such that , and . Let be a bid profile, such that for every buyer and every item :

As , if tie breaking is done according to , then . We show that is a PNE. Let be some bid vector of buyer , and let . Then,

where the inequality follows from the fact that is a 2PE. ∎

4 Discrepancy Factor of 2PE

The main difference between a two-price equilibrium and a Walrasian equilibrium is the use of two prices per item (high price and low price ) rather than a single price. This makes the notion of 2PE similar in spirit to WE. Namely, prices are still almost anonymous (in contrast to other approaches where prices are buyer-dependent, see, e.g., [16]), and every buyer is maximally happy with her bundle. The closer the two prices and are together, the better the 2PE resembles a WE. Indeed, in the extreme case, where for every item , the two notions coincide.

Consequently, a natural measure of distances of a 2PE from WE is the sum of price differences over all items. We further normalize the sum of price differences by the social welfare of the allocation, so that the discrepancy is independent of the units used (e.g., USD vs. Euros)333Formally, suppose is a 2PE with respect to valuation profile , and let be a valuation profile such that for every buyer and bundle and some constant . Clearly, is a 2PE w.r.t. , which has the same discrepancy as that of ..

This motivate us to define the discrepancy of a 2PE as follows.

Definition 4.1 (Discrepancy).

The discrepancy of a 2PE under valuation profile is

| (2) |

Low discrepancy is a desired property; a 2PE with low discrepancy is closer in spirit to WE in both fairness and simplicity. As we shall soon show, low discrepancy also implies high efficiency.

The 2PE notion is appealing from an existence perspective; indeed, every allocation S can be supported in a 2PE by setting , for every item . However, from a welfare maximization perspective, no guarantee can be given. This is in stark contrast to WE (where, by the 1st welfare theorem, every allocation supported in a WE has optimal welfare), and to weaker equilibrium notions, such as conditional equilibrium (where every allocation supported in a CE gives at least half of the optimal welfare [14]). In contrast, an allocation supported in a 2PE may have an arbitrarily low welfare.

The following proposition shows that the social welfare of a 2PE degrades gracefully with its discrepancy.

Proposition 4.2.

(low discrepancy implies high welfare) Let be a 2PE for valuation with discrepancy . Then, .

Proof.

Let be an optimal allocation. Let and . Since is a 2PE we have that for every buyer and bundle :

Summing the above inequality over all and substituting with gives

It follows that

Substitutes and rearrange to get the desired bound ∎

We also define the discrepancy of a given allocation as the discrepancy of the smallest-discrepancy 2PE supporting .

Definition 4.3.

Given valuation profile v, the discrepancy of an allocation is defined as

For all reasons mentioned above, it is desirable to identify allocations with low discrepancy.

Clearly, if is supported by a WE, then . Indeed, every allocation supported by a WE has optimal welfare.

It is also known that every allocation supported by a conditional equilibrium has at least a half of the optimal welfare [14]. The following proposition shows that the discrepancy of every such allocation is at most 1. Together with Proposition 4.2, it gives an alternative proof to the welfare guarantee of a conditional equilibrium.

Proposition 4.4.

Let be an allocation that is supported by a conditional equilibrium. Then, . Moreover, this is tight.

Proof.

let be a CE then:

where the inequality follows by individual rationality of CE.

Next, we show an example in which the above bound is tight. Let , and suppose buyers 1, 2 have unit-demand valuations where and . Consider the allocation and . One can easily verify that is a CE for . Now observe that is a 2PE for , and . ∎

It is shown in [5] that for any XOS valuation profile, the optimal allocation is supported by a S2PA PNE with no-overbidding. By [14], every S2PA PNE with no-overbidding can be transformed into a CE that preserves the same allocation. It then follows by Proposition 4.4 that the discrepancy of the optimal allocation in every XOS valuation profile is at most 1. In Appendix B we show that for any general valuation profile, every welfare-maximizing allocation has a discrepancy of at most .

Notably, there exist markets that admit neither Walrasian equilibrium, nor conditional equilibrium, and yet, the optimal allocation is supported by a 2PE with small discrepancy. For example, the market in Example 3.2 admits no Walrasian equilibrium, nor conditional equilibrium, and yet, the optimal allocation, , is supported in a 2PE with discrepancy .

5 Geometric Properties of Valuations over Identical Items

In this section we introduce new geometric properties of valuations over identical items, which prove useful in establishing upper bounds on the discrepancy of 2PE in such markets. Hereafter, we refer to a valuation over identical items as a symmetric valuation.

Definition 5.1 (max-forward-slope ()).

Given a symmetric valuation , and some , and , the -max-forward-slope is defined as

| (3) |

We say that realizes , if is the minimum index s.t. . In addition, we use to denote , and refer to as the -max-forward-slope.

The sorted vector of the max-forward slopes is defined by . That is, for every .

Definition 5.2 (min-backward-slope ()).

Given a symmetric valuation , and some , and , the -min-backward-slope is defined as

| (4) |

We say that realizes , if is the minimum index s.t. . In addition, we use to denote , and refer to as the -min-backward-slope.

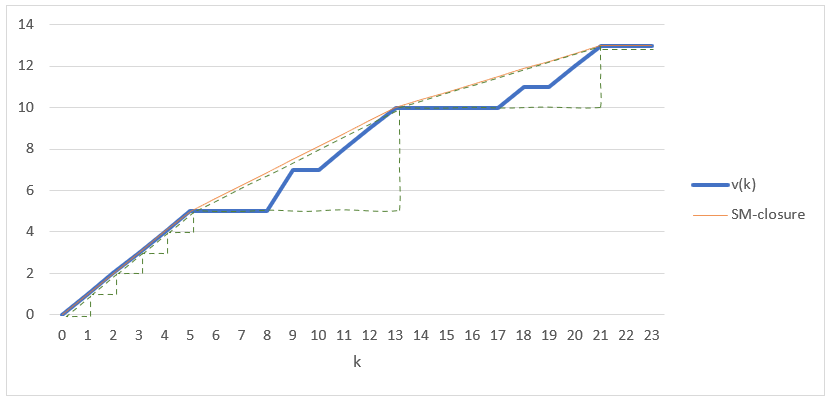

Submodular closure: Given a symmetric valuation , the minimal submodular valuation that (point-wise) upper bounds it is called the submodular closure (SM-closure) of . The SM-closure of a function is known to be unique (see, e.g., Ezra et al. [10]); see Figure 1 for an illustration.

Given a symmetric valuation function , we define the following: Let be the SM-closure of , and let be the set of indices for which , i.e., the set of points in which the and intersect. We refer to as the set of intersection indices. For , let be the right triangle between two adjacent intersecting indices, and , with vertices , and (see Figure 1). Let be the slope of the triangle . If , then is a degenerated triangle (a line), with slope . Let be the set of all right triangles of . For every , and every , we say that .

In what follows we present some useful lemmas and theorems regarding symmetric valuation functions. The complete proofs, as well as additional observations, appear in Appendix C.

The following lemma gives a lower bound on as a function of the max-forward-slopes of up to .

Lemma 5.3.

For every symmetric subadditive valuation function , and , .

The flat function of a symmetric valuation is defined as

The following observation specifies the max-forward-slope of the flat function.

Observation 5.4.

Let be a symmetric function and let be its flat function. Then, .

Proof.

For ,

where the second equality follows from Definition 5.1 and the last two equalities follow from the definition of . Hence, ∎

We now show that given a valuation and its corresponding flat function , the sorted-max-forward-slope of is at most the max-forward-slope of .

Theorem 5.5.

For every symmetric valuation , for every , .

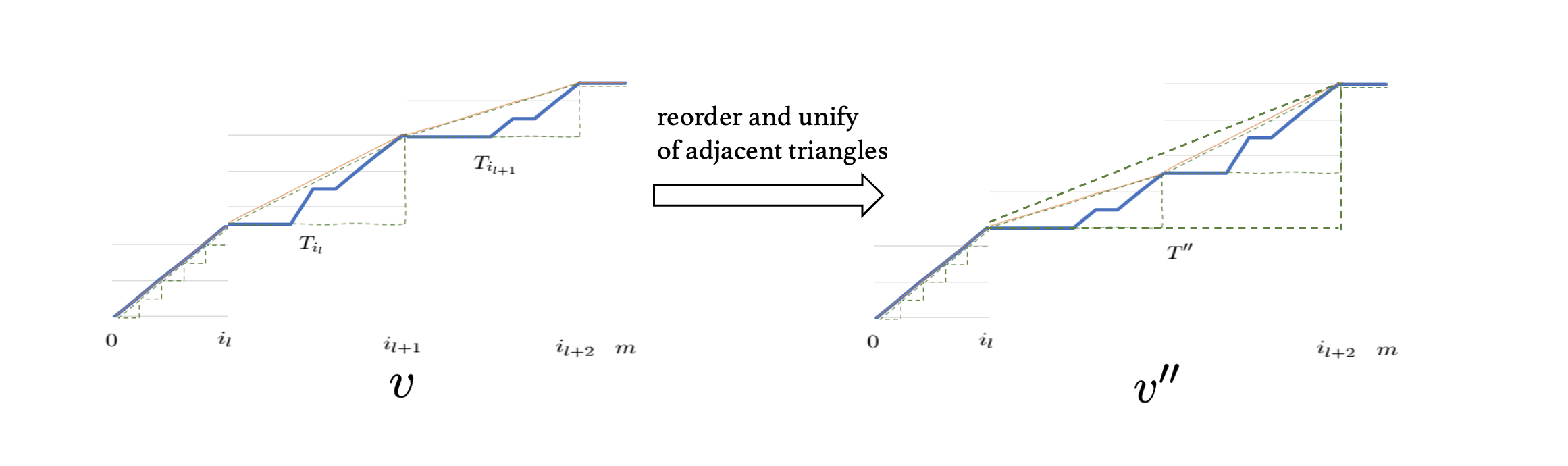

To prove Theorem 5.5, we introduce the ”reorder and unify of adjacent triangles” operation in Lemma C.9. The idea is to repeatedly switch two adjacent triangles in , until the obtained valuation comprises of a single triangle.

Definition 5.6.

Given a symmetric valuation , a constant and an integer , we say that is bad if ; otherwise, we say that is good.

The following lemma establishes an upper bound on the number of bad numbers in .

Lemma 5.7.

For every symmetric valuation , for every , there are at most bad integers in .

Proof.

Fix and let be ’s corresponding flat function. By observation 5.4, for every , . Let be a integer w.r.t. , i.e., . Rearranging we get that . Since is monotonically increasing, there are exactly integers in which are bad. By Theorem 5.5, for every , , and therefore there are at most integers which are bad w.r.t. .

∎

6 Properties of 2PEs with Identical Items

In this section we present some properties of 2PEs in markets with identical items. We first define 2PE with uniform prices:

Definition 6.1 (2PE with uniform prices (U-2PE)).

A triplet is a 2PE with uniform prices (U-2PE) for valuation profile v, if it is a 2PE for v and for every buyer , every items , and . Let and denote these prices, respectively.

The following proposition shows that for studying the discrepancy in markets with identical items it is without loss of generality to restrict attention to U-2PEs.

Proposition 6.2.

If is a 2PE for some symmetric valuation profile v, then there exists a U-2PE s.t. .

The proof of Proposition 6.2 follows by an iterative invocation of the following lemma for every buyer .

Lemma 6.3.

Let be a 2PE for some symmetric valuation profile v. Let be some buyer. Let and for every item and and for every item . Then:

-

•

is a 2PE.

-

•

is a 2PE.

-

•

Proof.

As is a 2PE, for every buyer and every set . As and for every item , we have that,

| (5) |

For a given set , let and let be the set of the items with the lowest in . Let . Notice that and therefore, . Hence, , where the first equality follows from the fact that and that for every . The last inequality follows from Inequality (1), and the last equality follows from the definition of and the fact that the function is symmetrical. That is, Inequality (5) holds for buyer and every set , and hence is a 2PE for v. Finally, follows directly from the definition of and the definition of .

To show that is a 2PE, it remains to show that (6) holds for every buyer . Let be the set of the items with the lowest in , where , and let . Notice that and therefore, . Hence, for every buyer we have, , where the first equality follows from the definition of , the first inequality follows from Inequality (1), the third equality is due to the definition of and the fact that the function is symmetrical, and the last equality is derived form the fact that for every item . We showed that, for every buyer and every set , and hence is a 2PE for v. Finally, follows directly from the definition of and the definition of . ∎

The complete proofs of the following propositions appear in Appendix D.

The following proposition gives necessary and sufficient conditions for the utility maximization property of a U-2PE.

Proposition 6.4.

Consider a symmetric valuation profile v and a triplet , s.t. for every item , and for every buyer and every items , and . Then, the following conditions are necessary and sufficient for utility maximization of a U-2PE:

-

1.

, for every .

-

2.

, for every .

-

3.

, for every and every s.t. .

Given Proposition 6.4, we can now specify simple sufficient conditions for U-2PE in market with identical items.

Proposition 6.5.

Consider a symmetric valuation profile v and let be a triplet satisfying the following conditions for every buyer :

-

1.

For every items , and . Let and denote these prices, respectively.

-

2.

.

-

3.

.

-

4.

.

-

5.

All items are allocated.

Then, is a U-2PE for v.

7 Discrepancy in Markets with Identical Subadditive Buyers

In this section we establish the existence of 2PEs with small discrepancy for markets with identical items and identical subadditive buyers.

We first show that every market with identical items and 2 identical subadditive buyers admits a 2PE with discrepancy of at most .

Theorem 7.1.

Every market with 2 identical subadditive symmetric valuations admits a U-2PE with discrepancy of at most 2.

Proof.

Consider a valuation and an allocation . Let and . For every , let and for every , let . As for every , and , for every , the triplet satisfies all the conditions in Proposition 6.5 and hence it is a U-2PE.

It holds that

| (7) |

Our goal is to show that there exists a pair (,), s.t , and . Therefore, it suffices to prove that there exists at least one good pair, (,), i.e., that both and are good elements. Indeed, for such a pair,

| (8) |

where the first inequality follows from the fact that both and are good elements and the last inequality is due to subadditivity. Notice that there are exactly pairs that satisfy and . According to Lemma 5.7, there are at most integers which are bad, i.e. with . Similarly, there are at most integers which are bad, i.e. with . Overall there are at most bad elements, and since this number is strictly less than , which is the number of pairs, there exists at least one good pair that satisfies , , and , which concludes the proof.

∎

We next establish a lower bound on the discrepancy of a 2PE for 2 identical subadditive buyers.

Theorem 7.2.

There exists a market with identical items and 2 identical subadditive buyers that admits no 2PE with discrepancy smaller than .

Proof.

Consider a setting with identical items and two identical buyers with valuation function as follows:

There are possible allocations, in which the first buyer gets items and the second gets items, where . We claim that the minimum discrepancy is achieved at and with discrepancy of slightly above . This is proved using a computer program [24].

∎

We now extend the result of Theorem 7.1 to markets with an arbitrary number of identical subadditive buyers.

Theorem 7.3.

Every market with identical subadditive symmetric valuations admits a U-2PE, , with discrepancy of at most .

To prove Theorem 7.3, we present an algorithm that computes some allocation , and show in Lemma 7.4 that the obtained allocation is supported in a 2PE with discrepancy of at most .

Line 13 in the algorithm refers to a good pair. For two buyers and integers , we say that a pair is good w.r.t. , and if (i) (ii) , (iii) , and (iiii) .

In the beginning, the algorithm allocates “whole triangles” to buyers, each time allocating to the buyer with the highest max-forward slope, breaking ties in favor of buyers with smaller bundles. As buyer valuations are identical, this ensures that a triangle in is allocated to all buyers before the next triangle in is allocated to any buyer. If the number of remaining items, , is less than the number of items in the selected buyer’s triangle, i.e., there are not enough elements to allocate the whole triangle that was chosen, the algorithm allocates the remaining items to two buyers, s.t. the pair of the max-forward slopes is a 2-good pair. Note that the naive idea of allocating all the items to the selected buyer is potentially bad, because we have no control over the max-forward slope within the triangle.

The following lemma shows that every allocation that is obtained as an output of Algorithm 1 can be supported in a U2PE with the desired discrepancy.

Lemma 7.4.

Let be an allocation returned by Algorithm 1, and let be a an allocation satisfying . There exist and s.t. is a U2PE with discrepancy of at most .

Proof.

First note that if Algorithm 1 ends without going through step 10, then the of each buyer is located at the beginning of a triangle. Let be the last buyer that has been chosen in step 5 and let be the slope of buyer before entering step 7. Note that if , then at the last time that buyer was chosen in step 5, she had max forward slope of at least . Therefore, By Corollary C.8 and lemma 5.3, the SW is at least . Moreover, by step 4 and Lemma C.6, for every , . Let for every and for every item . It is easy to see that satisfies all the conditions of Proposition 6.5, and hence it is a U2PE. The discrepancy is,

Note that if the of each buyer in Algorithm 1’s output is located at the beginning of a triangle, then for every , and also . One can easily verify that for , is a WE for the SM-closure valuation profile and according to Theorem 9.1, it is also a WE for v.

Now assume Algorithm 1 goes through step 10 before ending. Let be the value of and the value of when the algorithm enters step 10. We denote current triangle of buyer as the triangle with as its left most point and previous triangle of buyer as the triangle with as its right most point. Let us denote as buyer current triangle. We consider two cases. The first one is when there is another buyer, , with the same current triangle, . Then by Lemma C.6, buyer is chosen at step 12. Let be the slope of buyer when she is chosen. Since both buyers current triangle is identical we have that . By Claim C.7 and step 13, and . By step 4 and Lemma C.6, the slopes of all buyers current triangles are at most . Thus, we can set and for every item . Once again, it is easy to see that satisfies all the conditions of Claim 6.5, and hence it is a U2PE. Next, we bound the SW. Let be a buyer with previous triangle . By step 4 and Lemma C.6, the minimum max-forward-slope up to is . By Lemma 5.3 we have that . Now, let be a buyer with current triangle , then by Lemma C.6, where is buyer previous triangle slope. We can now bound the SW by . Concluding,

The second case is when buyer is the only buyer with as its current triangle (i.e., all other buyers previous triangle is ). By Claim C.7 and step 13, and . Since for every we have that we can set for every item . Note that for every . Namely, before the last step of the algorithm every buyer except from has items and . Thus,

where the last inequality is due to the fact that . Since for every we have that we can set for every item and for every item and get that . As for the SW, since the minimum max-forward-slope before entering step 10 is at least , from Lemma 5.3 we have that . Combining it all together,

∎

It now remains to show that there always exists a good pair in line 13 of Algorithm 1. This is established in the following lemma, which concludes the proof of Theorem 7.3.

Lemma 7.5.

Proof.

Let , , and be the respective values of , , and when the algorithm enters step 13. It holds that and are located at the beginning of a triangle, with slopes and , respectively. Hence, we need to show that there exists a pair s.t.: , , , and .

Let be buyer ’s current triangle. We know that its length is and that . We would like to ”truncate” after points and consider the max-forward-slopes of the truncated triangle. Let be the following monotone set function:

Notice that consists of one triangle, , with length and slope . Geometrically, is identical to in its first points, but the point of is higher than the point of , since every point in is located strictly below the hypotenuse. Hence, for every ,

Consider now buyer . Let be the following monotone set function:

Similar to the arguments of buyer , , for every .

Therefore, it suffices to show that there exists a pair s.t.: , , , and . Notice that there are exactly pairs that satisfy and . According to Lemma 5.7, there are at most element in which are bad, i.e. with max-forward-slope which is strictly more than . Similarly, there are at most element in which are bad, i.e. with max-forward-slope which is strictly higher than . Overall there are at most bad elements in and , and since this number is strictly less than , which is the number of pairs, there exists at least one good pair that satisfies , , , and . ∎

8 Discrepancy in Markets with Heterogeneous Subadditive Buyers

In this section we show that for every market with identical items and any number of subadditive buyers, there exists a 2PE with discrepancy of at most 6.

Theorem 8.1.

Every market with subadditive symmetric valuations admits a U2PE, , with discrepancy of at most .

To prove Theorem 8.1, we present an algorithm that computes some allocation , and show in Lemma 8.2 that the obtained allocation is supported in a 2PE with discrepancy of at most .

Line 11 in the algorithm refers to a good pair. For two buyers and integers , we say that a pair is good w.r.t. , and if (i) : (ii) , (iii) , and (iiii) .

Similar to Algorithm 1, the algorithm start by allocating “whole triangles” to buyers, each time allocating to the buyer with the highest max-forward slope. When there are not enough elements to allocate the whole triangle that was chosen, the algorithm allocates the remaining items to two buyers s.t. the pair of the max forward slopes is a 3-good pair.

Given the output of Algorithm 2, let be an allocation that satisfies and let for every and for every item . It is easy to see that satisfies all the conditions of Proposition 6.5, and hence it is a U2PE.

The following lemma shows that has the desired discrepancy.

Lemma 8.2.

The discrepancy of is at most .

Proof.

First note that if Algorithm 2 ends without going through step 9, then the of each buyer is located at the beginning of a triangle. Let be the last buyer that has been chosen in step 4 and let be the slope of buyer before entering step 6. By step 4 and Lemma C.6, for every , and therefore for every . Note that if , then at the last time that buyer was chosen in step 4, she had max forward slope of at least . Therefore, By Corollary C.8 and lemma 5.3, the SW is at least . Therefore,

Note that if the of each buyer in Algorithm 2’s output is located at the beginning of a triangle, then for every , and also . One can easily verify that for , is a WE for the SM-closure valuation profile and according to Theorem 9.1, it is also a WE for v.

We now assume that Algorithm 2 goes through step 9 before ending. Let be the value of and the value of when the algorithm enters step 9. We denote current triangle of buyer as the triangle with as its left most point and previous triangle of buyer as the triangle with as its right most point. At this stage, the algorithm allocated items, i.e. . By step 4 and Lemma C.6, the slope of all buyers previous triangle is at least , and the slope of all buyers current triangle is at most .

Consider the stage in which Algorithm 2 enters step 9 and let be the slope of buyer when she is chosen. Since is located at the beginning of a triangle, by Lemma C.5, the slope of the current triangle of buyer equals to the max-forward-slope at that point, . Notice that by step 10, for every buyer , . By Claim C.7 and step 11, and . Therefore, after the algorithm ends, for every and every , , and for every , . Hence,

| (9) |

By Corollary C.8 and lemma 5.3, the SW of the items that were allocated up to step 9 is at least . At step 11 we add at least items to buyer and since are located somewhere in buyer ’s current triangle, with slope , the added SW of the items is, by lemma 5.3, is at least . Hence,

| (10) |

where the last inequality is due to the fact that .

To conclude the proof of Theorem 8.1 it remains to establish the existence of a good pair that satisfies the condition in line 11 of Algorithm 2.

Lemma 8.3.

Proof.

Let , , and be the respective values of , , and when the algorithm enters step 11. It holds that and are located at the beginning of a triangle, with slopes and , respectively. Hence, we need to show that there exists a pair s.t.: , , , , and .

Let be buyer ’s current triangle. We know that its length is and that . We would like to ”truncate” after points and consider the max-forward-slopes of the truncated triangle. Let be the following monotone set function:

Notice that consists of one triangle, , with length and slope . Geometrically, is identical to in its first points, but the point of is higher than the point of , since every point in is located strictly below the hypotenuse. Hence, for every ,

Consider now buyer ’s current triangle. It is followed by other triangles, each with slope at most (see Lemma C.6). Let be the following monotone set function:

Notice that consists of one triangle with length of and slope . Similar to the arguments of buyer , , for every .

Therefore, it suffices to show that there exists a pair s.t.: , , , , and . Notice that can get the values and can get the values . Hence, there are exactly pairs that satisfy , , and . According to Lemma 5.7, there are at most elements in which are bad, i.e. with max-forward-slope which is strictly more than . Similarly, there are at most elements in which are bad, i.e. with max-forward-slope which is strictly higher than . Overall there are at most bad elements in and , and since this number is strictly less than , which is the number of pairs, there exists at least one good pair that satisfies , , , , and . ∎

9 WE in Markets with Identical Items

In markets with identical items, one can restrict attention to WE in which all prices are equal. Indeed, if there are at least two buyers who are allocated, then it is clear. Otherwise, simply replace all prices by their average (see Lemma 6.3). A WE with a single price and allocation S is denoted by .

The following theorem establishes necessary and sufficient conditions for the existence of a WE in markets with identical items.

Theorem 9.1.

Let be a symmetric valuation profile. Let be the SM-closure of for every , and let . is a WE for valuation profile if and only if is a WE for valuation profile and for every .

Proof of Theorem 9.1.

’Only if’ direction: Assume that is a WE for and for every . Let , where , for every . Since is a WE, is a 2PE and as all prices are equal, it is also a U-2PE for . By condition (2) of Proposition 6.4, we have that . Consider condition (3) of Proposition 6.4 and let , and , . We get that, for every and every . That is, . Since for every , by Lemma C.5 we have that and . Therefore . That is, conditions (1)-(5) of Proposition 6.5 are satisfied. Hence, is a U-2PE for , and is a WE for .

’If’ direction: Assume that is a WE for v. Similar to the ’Only if’ direction, we can show that by conditions (2) and (3) of Proposition 6.4, . Let be a triangle and let be some buyer with bundle , s.t. , and assume toward a contradiction that . By Claim C.7, and ; namely, and , a contradiction. Therefore, for every . By Lemma C.5, and . Thus, , i.e. conditions (1)-(5) of Proposition 6.5 are satisfied. Hence, is a U-2PE for , and is a WE for and for every . ∎

10 Endowment Equilibrium

In this section we present the notion of endowment equilibrium [1; 9], and show its relation to 2PE. Discovered by Nobel laureate Richard Thaler, the endowment effect states that buyers tend to inflate the value of items they already own.

This motivates the introduction of an endowed valuation, , which assigns some real value to every bundle , given an endowment of . The inflated value of items in the endowed set is captured by a gain function , which maps every bundle to some real value. Specifically, the endowed valuation, given an endowment of , is assumed to take the form

For every buyer and every bundle , denotes the gain function of with respect to endowment . Let denote the gain functions of buyer , and let denote the set of gain functions of all buyers.

An endowment equilibrium is then a Walrasian equilibrium with respect to the endowed valuations. A formal definition follows.

Definition 10.1 (Endowment equilibrium (EE) [1], [9]).

A pair of an allocation and item prices , is called an endowment equilibrium with respect to if it is a WE with respect to the endowed valuations , i.e:

-

1.

Utility maximization: Every buyer receives an allocation that maximizes her utility given the item prices, i.e., for every and bundle .

-

2.

Market clearance: All items are allocated.

10.1 Relation between endowment equilibrium and 2PE

In this section we show how to transform an EE into a 2PE and vice versa. That is, we show how high the endowment effect should be in order to compensate for a given price difference of a 2PE, and how low a price vector needs to be to make all buyers happy with their bundles in the absence of the corresponding endowment effects.

Proposition 10.2.

Consider a valuation profile v. Given a 2PE , let for every item . Then, for every endowed valuation profile s.t. for every and , is an EE with respect to .

Proof.

Let be an endowed valuation profile with corresponding gain functions . Let denote buyer ’s utility under the 2PE ; that is,

Let denote buyer ’s utility in under endowed valuations ; i.e.,

By rearranging we get

and

Therefore, if and only if . As is a 2PE, for every . Hence, if , then is an EE as desired. ∎

Proposition 10.3.

Consider a valuation profile v and gain functions . Let be an EE with respect to . Then, for every low price vector s.t.

| (11) |

for every , is a 2PE for v. In particular, is a 2PE for v.

Proof.

Let be some price vector satisfying equation (11) for every . Let and be as in the proof of proposition 10.2. By rearrangement we get

Therefore, is a 2PE if . As is an EE w.r.t. , for every . Hence, it suffices to require that for every .

We next show that in those cases where the right-hand side of the last inequality is negative, then is a 2PE.

To see this, note first that for every buyer and every set

where the inequality follows from monotonicity. Second, since is an EE, for every buyer and every set , , i.e., . Therefore, , and we get , as desired. ∎

10.2 A Weaker Gain Function for XOS Valuations

Ezra et al. [9] define a partial order over gain functions: Fix a valuation function and two gain functions, and . Given an endowed set , we write that if for all , . We write if for every , and we say that is weaker than .

The Identity (ID) gain function is defined as [1]. The Absolute Loss (AL) gain function is defined as [9]. Ezra et al. [9] show that every market with XOS buyers admits an EE with respect to the AL gain function.

In this Section we introduce a new gain function for markets with XOS buyers, which we call Supporting Prices (SP). We show that for such markets, the SP gain function is weaker than AL, but stronger than ID.

Let us first recall the definition of supporting prices.

Definition 10.4 (Supporting Prices [8]).

Given a valuation and a set , the prices are supporting prices w.r.t. and if and for every , .

Let be an XOS valuation function, and let be the supporting prices with respect to the function and the set . The SP gain function is given by , for every set .

Proposition 10.5.

For any XOS valuation, the Supporting Prices gain function is weaker than the AL gain function and stronger than the ID gain function, i.e., .

Proof.

We first show that . For every and ,

where the inequality follows from the definition of supporting prices.

We now show that . For every and ,

where the inequality follows from the definition of supporting prices. On the other hand,

Therefore, for every and every , i.e., . ∎

We next show that every market with XOS buyers admits an endowment equilibrium with SP gain functions.

Claim 10.6.

Consider an XOS valuation profile v. Then,

-

1.

There exists a 2PE, , where for every , .

-

2.

is an EE with SP gain functions.

Proof.

Christodoulou et al. [5] showed that in a market with XOS buyers, there always exists a S2PA PNE bid profile, where are the supporting prices w.r.t. and if , and otherwise. According to Proposition 3.5, the triplet is a 2PE, where for every , .

By Proposition 10.2, if for every buyer and every , then is an EE. Notice that, , where the first equality follows from the definition of the SP gain function, the second equality is given and the third equality is due to the fact that for every . Therefore, is an EE. ∎

References

- Babaioff et al. [2018] Moshe Babaioff, Shahar Dobzinski, and Sigal Oren. Combinatorial auctions with endowment effect. In Proceedings of the 2018 ACM Conference on Economics and Computation, pages 73–90, 2018.

- Bhawalkar and Roughgarden [2011] Kshipra Bhawalkar and Tim Roughgarden. Welfare guarantees for combinatorial auctions with item bidding. In Dana Randall, editor, Proceedings of the Twenty-Second Annual ACM-SIAM Symposium on Discrete Algorithms, SODA 2011, San Francisco, California, USA, January 23-25, 2011, pages 700–709. SIAM, 2011.

- Bikhchandani and Mamer [1997] Sushil Bikhchandani and John W. Mamer. Competitive equilibrium in an exchange economy with indivisibilities. Journal of Economic Theory, 74(2):385–413, 1997.

- Cai and Papadimitriou [2014] Yang Cai and Christos H. Papadimitriou. Simultaneous bayesian auctions and computational complexity. In Moshe Babaioff, Vincent Conitzer, and David A. Easley, editors, ACM Conference on Economics and Computation, EC ’14, Stanford , CA, USA, June 8-12, 2014, pages 895–910. ACM, 2014.

- Christodoulou et al. [2008] George Christodoulou, Annamária Kovács, and Michael Schapira. Bayesian combinatorial auctions. In Luca Aceto, Ivan Damgård, Leslie Ann Goldberg, Magnús M. Halldórsson, Anna Ingólfsdóttir, and Igor Walukiewicz, editors, Automata, Languages and Programming, 35th International Colloquium, ICALP 2008, Reykjavik, Iceland, July 7-11, 2008, Proceedings, Part I: Tack A: Algorithms, Automata, Complexity, and Games, volume 5125 of Lecture Notes in Computer Science, pages 820–832. Springer, 2008.

- Christodoulou et al. [2016a] George Christodoulou, Annamária Kovács, and Michael Schapira. Bayesian combinatorial auctions. J. ACM, 63(2):11:1–11:19, 2016a.

- Christodoulou et al. [2016b] George Christodoulou, Annamária Kovács, Alkmini Sgouritsa, and Bo Tang. Tight bounds for the price of anarchy of simultaneous first-price auctions. ACM Trans. Economics and Comput., 4(2):9:1–9:33, 2016b.

- Dobzinski et al. [2010] Shahar Dobzinski, Noam Nisan, and Michael Schapira. Approximation algorithms for combinatorial auctions with complement-free bidders. Mathematics of Operations Research, 35(1):1–13, 2010.

- Ezra et al. [2019] Tomer Ezra, Michal Feldman, and Ophir Friedler. A general framework for endowment effects in combinatorial markets. arXiv preprint arXiv:1903.11360, 2019.

- Ezra et al. [2020] Tomer Ezra, Michal Feldman, Tim Roughgarden, and Warut Suksompong. Pricing multi-unit markets. ACM Transactions on Economics and Computation (TEAC), 7(4):1–29, 2020.

- Feldman and Shabtai [2020] Michal Feldman and Galia Shabtai. Simultaneous 2nd price item auctions with no-underbidding. arXiv preprint arXiv:2003.11857, 2020.

- Feldman et al. [2013a] Michal Feldman, Hu Fu, Nick Gravin, and Brendan Lucier. Simultaneous auctions are (almost) efficient. In Dan Boneh, Tim Roughgarden, and Joan Feigenbaum, editors, Symposium on Theory of Computing Conference, STOC’13, Palo Alto, CA, USA, June 1-4, 2013, pages 201–210. ACM, 2013a.

- Feldman et al. [2013b] Michal Feldman, Nick Gravin, and Brendan Lucier. Combinatorial walrasian equilibrium, 2013b.

- Fu et al. [2012] Hu Fu, Robert Kleinberg, and Ron Lavi. Conditional equilibrium outcomes via ascending price processes with applications to combinatorial auctions with item bidding. In Boi Faltings, Kevin Leyton-Brown, and Panos Ipeirotis, editors, Proceedings of the 13th ACM Conference on Electronic Commerce, EC 2012, Valencia, Spain, June 4-8, 2012, page 586. ACM, 2012.

- Gul and Stacchetti [1999] Faruk Gul and Ennio Stacchetti. Walrasian equilibrium with gross substitutes. Journal of Economic theory, 87(1):95–124, 1999.

- Hartline and Roughgarden [2009] Jason D. Hartline and Tim Roughgarden. Simple versus optimal mechanisms. In Proceedings of the 10th ACM Conference on Electronic Commerce, EC ’09, page 225–234, New York, NY, USA, 2009. Association for Computing Machinery. ISBN 9781605584584. doi: 10.1145/1566374.1566407.

- Hassidim et al. [2011] Avinatan Hassidim, Haim Kaplan, Yishay Mansour, and Noam Nisan. Non-price equilibria in markets of discrete goods. In Yoav Shoham, Yan Chen, and Tim Roughgarden, editors, Proceedings 12th ACM Conference on Electronic Commerce (EC-2011), San Jose, CA, USA, June 5-9, 2011, pages 295–296. ACM, 2011.

- Kahneman et al. [1990] Daniel Kahneman, Jack L. Knetsch, and Richard H. Thaler. Experimental tests of the endowment effect and the coase theorem. Journal of Political Economy, 98(6):1325–1348, 1990.

- Kahneman et al. [1991] Daniel Kahneman, Jack L. Knetsch, and Richard H. Thaler. Anomalies: The endowment effect, loss aversion, and status quo bias. Journal of Economic Perspectives, 5(1):193–206, March 1991.

- Kelso and Crawford [1982] Alexander S Kelso and Vincent P Crawford. Job matching, coalition formation, and gross substitutes. Econometrica: Journal of the Econometric Society, pages 1483–1504, 1982.

- Knetsch et al. [2001] Jack Knetsch, Fang-Fang Tang, and Richard Thaler. The endowment effect and repeated market trials: Is the vickrey auction demand revealing? Experimental Economics, 4(3):257–269, 2001.

- Lehmann et al. [2006] Benny Lehmann, Daniel Lehmann, and Noam Nisan. Combinatorial auctions with decreasing marginal utilities. Games and Economic Behavior, 55(2):270–296, 2006.

- Lehmann [2018] Daniel Lehmann. Local equilibria. CoRR, abs/1807.00304, 2018.

- [24] Galia Shabtai Michal Feldman and Aner Wolfenfeld. 2pe: Script to calculate minimum discrepancy. URL https://github.com/anerwolf/2PE.

- Walras [1874] Léon Walras. Eléments d’economie politique pure. ed. Lausanne:[sn], 1877, 1874.

Appendix A Valuation classes

Definitions for the valuation classes over heterogeneous items:

-

•

Unit demand: there exist values , s.t.

-

•

Additive: there exist values , s.t.

-

•

Submodular: for any it holds that

-

•

XOS: there exist vectors s.t. for any it holds that

-

•

Subadditive: for any it holds that

Appendix B An upper bound on the discrepancy of the optimal allocation

In this section we show that for any valuation profile, every welfare-maximizing allocation can be supported in a 2PE with a discrepancy of at most . The proof of Proposition B.1 is similar to the proof of Proposition 7.1 in [9].

Proposition B.1.

Consider valuation profile v. Let be an optimal allocation and where is the buyer who gets item in . Then, is a 2PE and .

Proof.

We first show that is a 2PE. Let be some bundle. Then,

where the first and second inequality follows by monotonicity, the third inequality follows since equality holds whenever , and strict inequality holds otherwise. The last inequality is due to optimality. Thus is a 2PE. Next, we bound the discrepancy of the optimal allocation,

∎

Appendix C Missing proofs and lemmas for section 5

The following lemma shows that for every submodular valuation , the -max-forward-slope and -min-backward-slope are realized at , hence they do not depend on the horizon .

Lemma C.1.

For every submodular symmetric valuation

-

1.

, for every and every .

-

2.

, for every and every .

Proof.

For every , it holds that

where the inequality follows from submodularity. By rearranging we get that

It follows that realizes for every , .

Similarly, for every , it holds that

where the inequality follows from submodularity. By rearranging we get that

It follows that realizes for every , . ∎

The following lemma shows that the the max-forward-slope and min-backward-slope of the SM-closure always equal to the slope of the corresponding triangle.

Lemma C.2.

For every

-

1.

For every

-

2.

For every

Proof.

By Lemma C.1, for every , . Since the valuation is linear in the range , the max-forward-slope does not change inside the triangle range, and it equals to:

for every .

Similarly, by Lemma C.1, for every . Since the valuation is linear in the range , the min-backward-slope does not change inside the triangle range, and it equals to:

for every . ∎

The following lemma shows that the max-forward-slope of the valuation at equals to the slope of the corresponding triangle, and that the max-forward-slope of any is realized at .

Lemma C.3.

For every triangle ,

-

1.

.

-

2.

is realized at .

-

3.

For every , is realized at .

Proof.

As is the first point after in which , we have that for every point , . Moreover, since is linear in the triangle, the -max-forward-slope of , is realized at . That is,

where the last equality follows from the definition of .

As submodular functions are convex, the slope of the triangles is non decreasing, and therefore the slope of all the following triangles after are at most . Since for every , the -max-forward-slope of at point cannot increase beyond for , i.e., . For the same argument, we conclude that , for every . That is, is realized at for , and at for . ∎

The following lemma shows that the min-backward-slope of the valuation at equals to the slope of triangle , and that the min-backward-slope of any is realized at .

Lemma C.4.

For every triangle ,

-

1.

.

-

2.

is realized at .

-

3.

For every , is realized at .

Proof.

Since is the SM-Closure of , for every , . Since is linear in we have that the -min-backward-slope is realized at . That is:

where the last equality follows from the definition of .

As submodular functions are convex, the slope of the triangles is non decreasing, and therefore the slope of all the triangle that come before are at least . Thus, the -min-backward-slope cannot decrease beyond for , i.e., . For the same argument, we conclude that , for every . That is, is realized at for , and at for . ∎

The following lemma shows that at the intersecting indices, both the max-forward-slope and min-backward-slope of and , equal to the slope of the corresponding triangle.

Lemma C.5.

For every ,

-

1.

.

-

2.

.

The following lemma shows that the slopes of the triangles are monotonically decreasing.

Lemma C.6.

.

We next show that the max-forward-slope (respectively, min-backward-slope) of the left-most (resp., right-most) point of a triangle is the minimal max-forward-slope (resp., maximal min-backward-slope) among all triangle points.

Claim C.7.

For every triangle , for every ,

-

1.

-

2.

Proof.

From Claim C.7, Lemma C.5 and Lemma C.6, we conclude that the minimum value of the max-forward-slope up to a point , equals to the slope of the last triangle that precedes , i.e.,

Corollary C.8.

For every , let be the largest intersecting index that is smaller than . It holds that .

Proof of Lemma 5.3.

Consider the SM-closure, . Notice that the valuation at any intersecting index equals to the sum of previous triangle increases, i.e. .

Lemma C.9.

Let be some valuation and its SM-closure. Let be a valuation s.t. for every and every , while in the range , is composed of the triangles and of the function in the opposite order (see Figure 2). Then,

-

1.

and .

-

2.

is monotone.

-

3.

has only one right triangle, , in the range , with slope , where .

-

4.

is realized at .

-

5.

For every , .

Proof.

It is easy to see that and , by the definition on . Moreover, as is monotone, every slice of is also monotone. Therefore, changing the order of some slices of keeps the monotonicity property, which leads to the conclusion that is monotone.

Consider the range . From Lemma C.2, , where the inequality follows from Lemma C.1 and the fact that is submodular. As in this range is composed of the same triangles but in the opposite order, intersect with its SM-closure in only two points: the first point, , and the last point, . Therefore, has only one right triangle, , in the range and it is easy to see that the slope satisfies . Moreover, according to Lemma C.3 (2), is realized at .

Now lets look at triangle . According to Lemma C.3 (3), the max-forward-slope of every in is realized at and by definition is determined only by the triangle points that comes after it. In , is part of a larger triangle, , but as it is located at the end of , there is no change in the max-forward-slope of ’s points when moving from to . The above is not true for triangle , which is located at the beginning of in . Hence, the max-forward-slope of every in is influenced by the points in that come after it, including the points of . However, the max-forward-slope of every can only increase when moving from to , as the max-forward-slope is a maximum over a larger set. Moreover, according to Lemma C.3, the slope of all points and stays the same.

Therefore, for every . ∎

Proof of Theorem 5.5.

We prove this theorem by induction. We will denote as the valuation and as its flat function. The base case is , where is some valuation. In this case, for every . Therefore, for every .

Assume that for every for any valuation . We need to show that for every for any valuation .

Consider a valuation , it’s SM-closure . Let be two consecutive intersecting indices in and let be their corresponding two adjacent triangles.

By Lemma C.2, , where the inequality follows from Lemma C.1 and the fact that is submodular. That is, the list of triangle slopes is non-increasing, . For ease of presentation, we refer to the last intersecting index, which is as , and to the intersecting index from the end, i.e., , as .

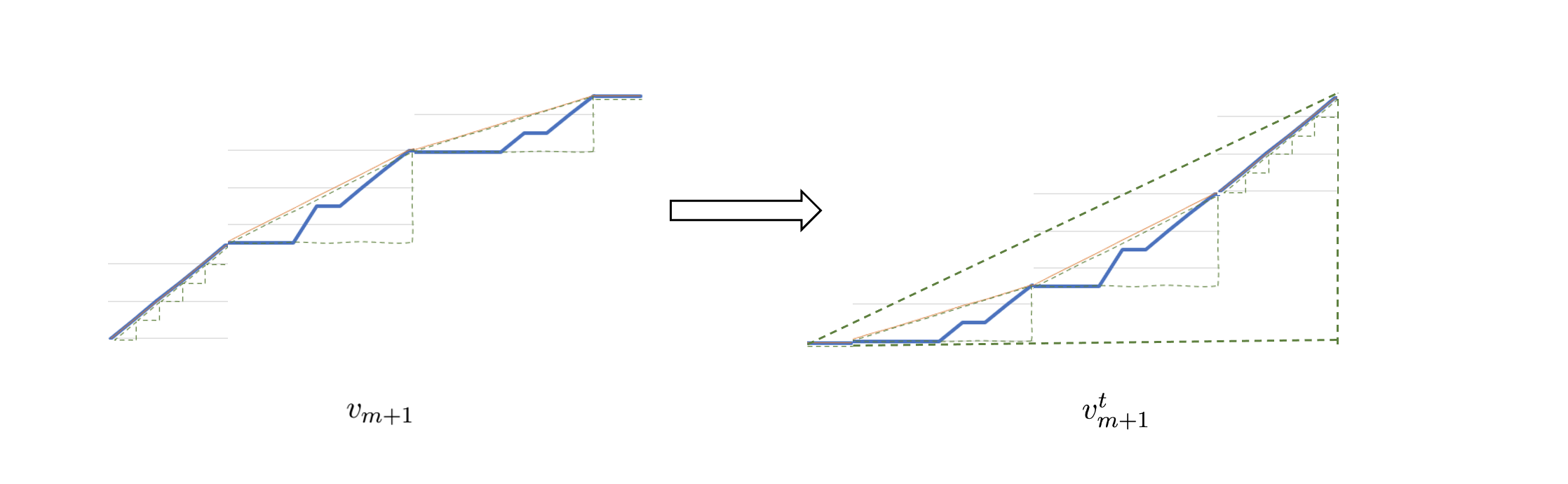

We now want to create a new function from the function by reorder and unify of the last two triangles as described in Lemma C.9. There is no change in the other points , i.e. for every . Let be the new triangle created after the reorder of unify of triangles and , with slope . According to Lemma C.9, is monotone, , , and for every . Note that has triangles, i.e. one triangle less than . We can now create a new function from the function by reorder and unify of the last two triangles of . Similar to the previous arguments, is monotone and has triangles, i.e. one triangle less than and for every . We can repeat this process till the last function, , has only one triangle (see Figure 3).

Using Lemma C.9 (1), we get that and , and therefore the flat function, , which corresponds to the function , and the flat function, , which corresponds to the function are the same, i.e., . Moreover, since for every , it is sufficient to show is that for every .

First notice that according to Lemma C.9 (4), is realized at point . Therefore,

| (14) |

where the last equality follows from Observation 5.4.

Let be the following monotone set function:

and let be its corresponding flat function. By the definition of , we have that for every ,

| (15) |

and for every ,

| (16) |

As for every and , we have that,

| (17) |

By the induction assumption, we know that for every , and together with Equations (14), (15), (16) and (17), we get that for every .

∎

Appendix D Missing proofs for section 6

Proof of Proposition 6.4.

Let , , , . For identical items, Inequality (1) can be written as

for every and every , such that and . Alternatively,

| (18) |

Necessity: Assume that Inequality (18) holds. Substituting and in Inequality (18), we get for every . Together with the assumption that for every item , condition (1) follow. Substituting and for every in Inequality (18), we get

which is equivalent to

for every , which is precisely condition (2. Condition (3) is obtained by applying in Inequality (18). That is,

| (19) |

for every and every .

Sufficiency: Assume that conditions (1), (2) and (3) of the proposition hold. Fix buyer , and some . One can easily verify that, since for every , the right hand side of Inequality (18) attains its highest value when , and . Therefore, it suffices to satisfy Inequality (18) for this case. If , then , for every , and if then , . Therefore, it remains to show that:

| (20) |

for every and every , s.t. , and for every , . One can easily verify that the above Inequality holds whenever conditions (2) and (3) of the proposition hold.

∎

Proof of Proposition 6.5.

From condition (5) we get market clearance. From condition (4), for every and , we have:

for every , and therefore,

for every and . That is, condition (3) of Proposition 6.4 holds and together with conditions (1), (2) and (3) of the current proposition, all the conditions of Proposition 6.4 hold. Therefore, utility maximization holds and hence is a U-2PE. ∎

Appendix E A simpler lower bound

Theorem E.1.

There exists a market with identical items and 2 subadditive buyers that admits no 2PE with discrepancy smaller than .

Proof.

Consider a setting with two buyers with the following identical subadditive valuation over 27 identical items:

To find the minimum possible discrepancy of any 2PE for this setting, we need to consider all 14 possible allocations (up to symmetry). Table 1 gives the values of the max-forward-slope and min-backward-slope of each allocation for each buyer. One can now use Proposition 6.5 to calculate the maximum and minimum and the corresponding minimum discrepancy for every allocation. One can verify that the minimum discrepancy over all allocations is achieved for , with discrepancy .

| 0 | 27 | |||||||||

| 1 | 26 | |||||||||

| 2 | 25 | |||||||||

| 3 | 24 | |||||||||

| 4 | 23 | |||||||||

| 5 | 22 | |||||||||

| 6 | 21 | |||||||||

| 7 | 20 | |||||||||

| 8 | 19 | |||||||||

| 9 | 18 | |||||||||

| 10 | 17 | |||||||||

| 11 | 16 | |||||||||

| 12 | 15 | |||||||||

| 13 | 14 |

∎