-Estimation based on quasi-processes from discrete samples of Lévy processes

Abstract

We consider -estimation problems, where the target value is determined using a minimizer of an expected functional of a Lévy process. With discrete observations from the Lévy process, we can produce a “quasi-path” by shuffling increments of the Lévy process; we call it a quasi-process. Under a suitable sampling scheme, a quasi-process can converge weakly to the true process according to the properties of the stationary and independent increments. Using this resampling technique, we can estimate objective functionals similar to those estimated using the Monte Carlo simulations, and it is available as a contrast function. The -estimator based on these quasi-processes can be consistent and asymptotically normal.

Keywords: -estimation; Lévy processes; resampling; quasi-process; discrete observations.

MSC2010: 62M20; 62G20, 62F40, 60G51

1 Introduction

On a stochastic basis, with a filtration , we consider a -Lévy process starting at of the form , where and are the Lévy process with the characteristic exponent

| (1.1) |

Let be a family of càdlàg functions on (or as ), be the Borel field on generated by the Skorokhod topology, which is metrizable with a suitable metric, called the Billingsley metric, and can be a Polish space; see Billingsley [1], Section 12 for details. Then is a measurable map . Throughout this study, we denote the distribution of on by and write

for a measurable function, .

Let be a subset of , and suppose the following is well-defined: for a real-valued function, , defined on ,

| (1.2) |

This study aims to statistically infer from the sampled data of .

This inference problem is often found in some applications in finance and insurance. For instance, consider a strategy of striking a perpetual American put option for a stock price such that we strike the right when for a certain threshold , and the strike time is given by a stopping time . To search for the optimal , say , it would be natural to consider

| (1.3) |

where is the interest rate, and is the strike price; see Gerber and Shiu [6]. Here, it is not easy to estimate the objective expectation from the observations of the stock price data because it depends on the entire path of , and it is implicit with respect to the general characteristics of .

There is another example from insurance risk theory. Assuming that process is a surplus for an insurance contract and considering the present value of a ruin-related ‘loss’ up to the time of ruin,

where and are the parameter that controls the ‘loss’; see Feng [3] and Feng and Shimizu [4]. Hereafter, given by (1.2) is an optimal parameter for minimizing the expected discounted ‘risk’ for surplus . For instance, consider a dividend strategy that pays ratio when the insurance surplus is over threshold . The total dividends up to the ruin is given by

| (1.4) |

In this quantity, the probability of paying the dividends is small when is large, although large dividends are paid, and vice versa. Therefore, the expectation can be optimized to a suitable level.

In these examples, we need to estimate the expected functionals (1.3) and (1.4) from observations of the Lévy process . However, it is often difficult to estimate these functionals because they include a random time, , which is often not observable in practice. If we observed many paths of the true process, we could estimate it using the Monte Carlo simulations, but this is impossible in practice.

Contrary to generating paths, we will produce “quasi-paths” from discrete observations of the Lévy process. This idea is similar to bootstrapping. Given discrete samples of , say with and , we approximate the path by a step function that jumps at with jump size ; see Section 2 for details. By shuffling the order of the increments, we can create different step functions, which can be regarded as different paths from the true distribution. Using these paths, we can estimate the expected functions of and construct an estimator of as an -estimator. Additionally, we can provide sufficient conditions to ensure that the -estimator can be consistent and asymptotically normal, which are the main results of this study.

The remainder of this paper is organized as follows. In Section 2, we define the quasi-processes from discrete observation of the Lévy process and the -esimator for (1.2). In Section 3, we show the weak convergence of quasi-processes to the true process based on the Skorokhod topology under the high-frequency sampling in the long term (HFLT), where the sampling interval, , goes to zero and the terminal of observation goes to infinity simultaneously: as the sample size increases. Additionally, we confirmed this phenomenon through simulations. Section 4 discusses the main results, weak consistency, and asymptotic normality of the -estimators. We provided some sufficient conditions for the results, and we confirmed that the conditions could be satisfied in some concrete examples in Section 5. In particular, we consider an example in which in (1.2) is dividends paid up to ruin, which is a widespread problem in insurance mathematics. We will make a further paper dealing with more examples in detail using our techniques; Shimizu and Shiraishi [12].

Before proceeding to the next section, we shall make some notations used throughout the paper.

Notation

-

•

means that there exists a universal constant, , such that .

-

•

For a -th order tensor , denote by

-

•

For and ,

-

•

For any , we denote by the Skorokhod metric:

where is a family of monotonically increasing functions on and is the identity .

-

•

For and a measure on , we denote using the family of functions such that

Moreover, we write for .

-

•

For function , means that is of class w.r.t. and w.r.t. . In particular, represents a set of continuous functions. Moreover, means that and are bounded up to all possible derivatives.

2 Contrast functions via “quasi-processes”

We observed the Lévy process, , starting from equidistantly in time: the observations consist of , where

Let be a vector of increments with , and let

be a family of all the permutations of . Because ’s are i.i.d. for each , is exchangeable; that is, it follows for any permutation that

has the same distribution as .

Definition 2.1.

For given and , a stochastic process given by

is said to be a quasi-process of for a permutation .

The path of the quasi-process belongs to : a right continuous step function that has a jump at with amplitude .

For a given number , let be IID samples withdrawn uniformly from : for a given ,

| (2.1) |

where is the delta measure concentrated on . In particular, as we fix a sequence of permutation sets , we simply write

Definition 2.2.

Given a vector of increments, , and a number , we denote the minimum contrast estimator of in (1.2) as

| (2.2) |

where for each .

In some special cases where is a function of the Lévy measure of the form

for some , can be estimated as

with some under some regularities; Comte and Genon-Catalot [5]; Jacod [7]; Shimizu [11]; Kato and Kuris [8]. In this case, the quasi-process does not make sense because the estimator is exchangeable with respect to increments . Our method is advantageous when function depends on the entire path of . For instance, when we consider an example in (1.4), we may need many data such that in the past. Using quasi-processes , we can select many “quasi-samples” such that , which gives us a better approximation of .

3 Weak convergence for quasi-processes

3.1 Theoretical results

Here, we consider a high-frequency sampling in the long term:

(HFLT) , and as .

Theorem 3.1.

Under the sampling scheme (HFLT), it holds for any sequence of permutations that

Proof.

Note that the process generally has the following decomposition:

where , , and are the Wiener process and is the pure-jump Lévy process independent of , with the characteristic exponent

Hereafter, we fix permutation arbitrarily, and let for simplicity of notation

where , and so does . Because the limit process is a Lévy process, which is stochastically continuous, the claim of the statement is equivalent to the following conditions (a) and (b) hold true:

-

(a)

Any finite dimensional distribution of converges weakly to the corresponding finite dimensional distribution of : for any time points , it holds that as because the probability that the Lévy process jumps at a fixed time points is zero;

-

(b)

The tightness of in : ;

see Billingsley [1], Section 13 for details.

For (a), we show the case where for simplicity of discussion, and for any , we show that

| (3.1) |

which leads to by the continuous mapping theorem. Here, when is sufficiently large, we assume that and for without loss of generality. Hereafter, the components of are independent and stationary; it suffices for (3.1) to show that

| (3.2) |

separately. Moreover, for

and are identically distributed, it suffices to show the first convergence in (3.2) for any initial value . Hence, we show only the first one.

Fixing any , we can assume that there exists some such that and , as . For ,

because based on the property of independent and stationary increments of . Hence, we obtain from the stochastic continuity of the Lévy processes: as and Slutsky’s lemma; van der Vaart [13], Theorem 2.7, (iv).

For the proof of (b): the tightness of , we use the following lemma obtained from Theorem 16.8 by Billingsley [1] and its corollary.

Lemma 3.1.

A sequence of -valued random elements is uniformly tight when the following conditions (i)–(iii) hold true:

-

(i)

For any ,

-

(ii)

For any ,

-

(iii)

For each , there exists some and such that, for any , and some discrete -stopping time with ,

First, we show (i) for any , for some and large enough because as . Further, we suppose that and as , as in the proof of (a).

For any , it follows that

Through infinite divisibility of and and their stochastic continuity, we have

Hence, we observe that

by the tightness of the random variables and .

Second, we show (ii). Fixing in the proof of (i), for any and , it follows that

Note that is a compound Poisson process with intensity , and it is almost finite for each . Therefore, the following holds:

Finally, we show (iii). Fix any and consider the stopping time as . For any sufficiently small , there exist some numbers and such that for any ,

and, as in the above argument, we assume that and as without loss of generality.

We note that for any and the above ,

Because

and

we have

For the above , there exists a with such that

for any . Moreover, it follows from the stochastic continuity of the Lévy process that, for any , there exist and such that

for any , and

for any ; therefore, it also holds that

for any and . As a consequence, it follows for any and that

. ∎

3.2 Numerical experiments

Let us numerically confirm the weak convergence of the quasi-processes when .

Consider a jump-diffusion process of the form

| (3.3) |

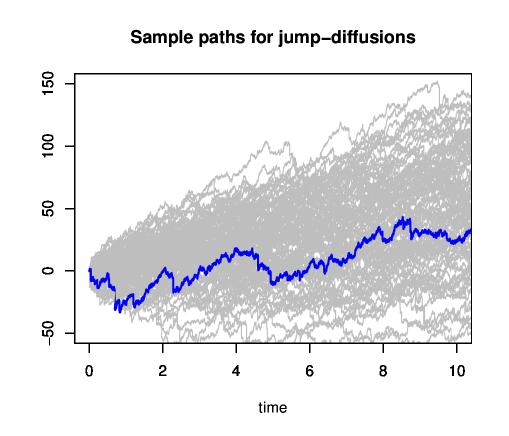

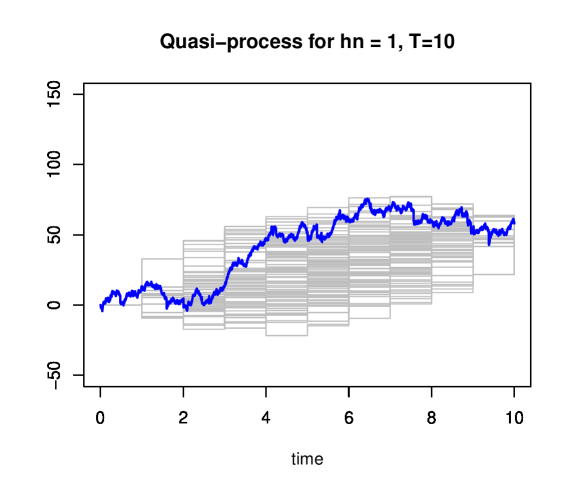

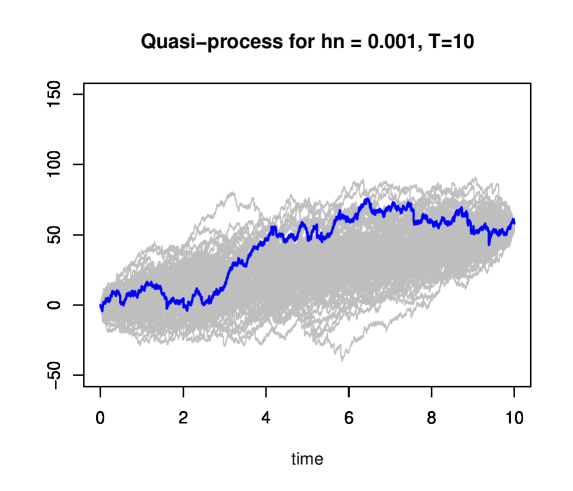

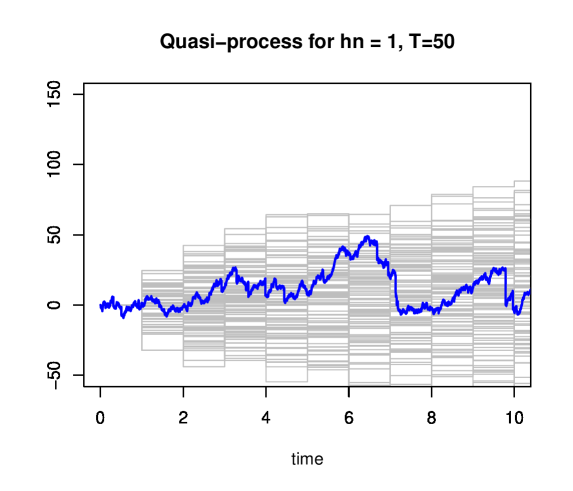

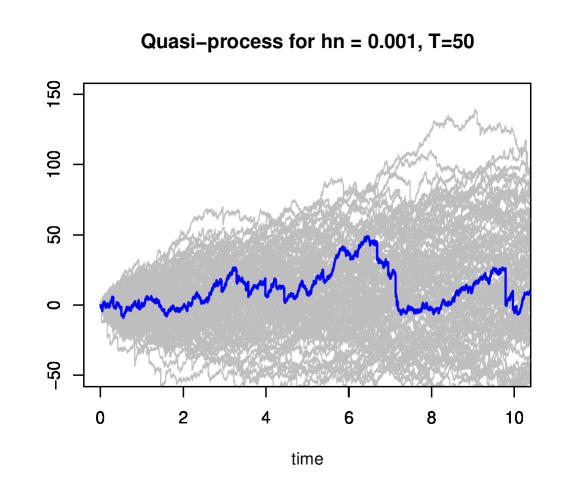

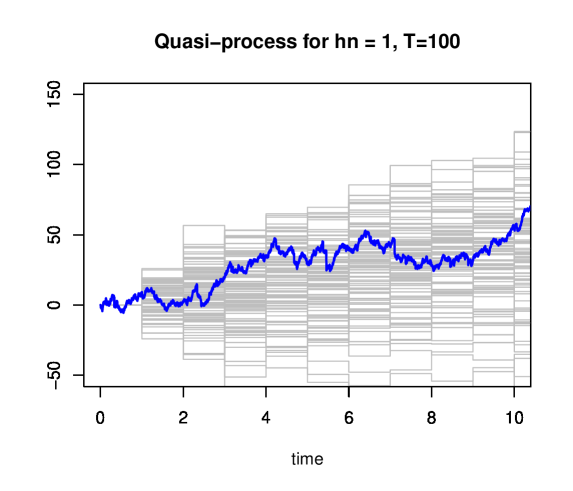

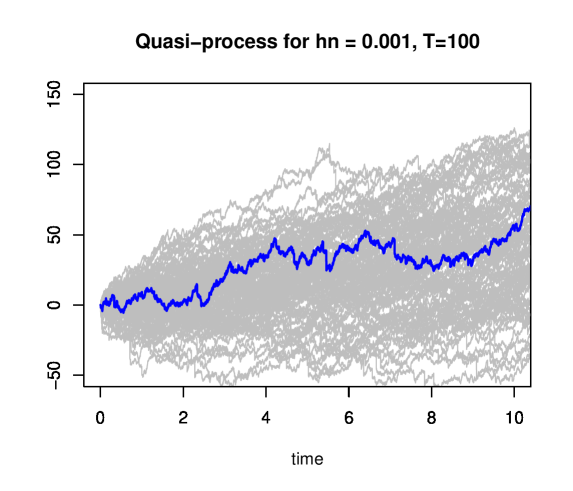

where is a Wiener process, is a Poisson process with intensity , and ’s are i.i.d. exponential variables with mean . As shown in Figure 1, we simulate 100 paths of the process with parameters . Assuming that we observe the blue path, the other scenarios are shown in gray. From this perspective, we can image the distribution of the proecss.

Some quai-paths based on observations from the blue line on are shown in Figures 2 – 4, where the graphs on are extracted from the paths on with , and . In each figure, the left shows the quasi-paths for , and the right shows the ones for smaller (e.g., 0.1, 0.05, and 0.005). In the simulation, we randomly select randomly from as a subset of with , that is, 100 sample paths were generated.

We can observe that the larger the and the smaller the , the distribution of the quasi-paths (gray) seems to be similar to the distribution of the true paths in Figure 1 (compare Figure 1 and the bottom in Figure 4), which is a visual confirmation of the weak convergence of the quasi-paths.

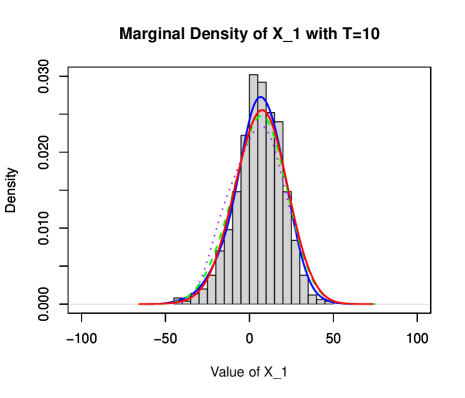

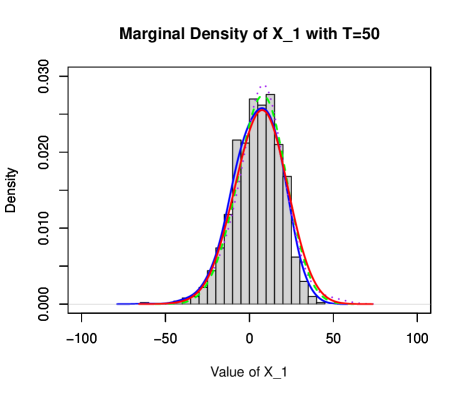

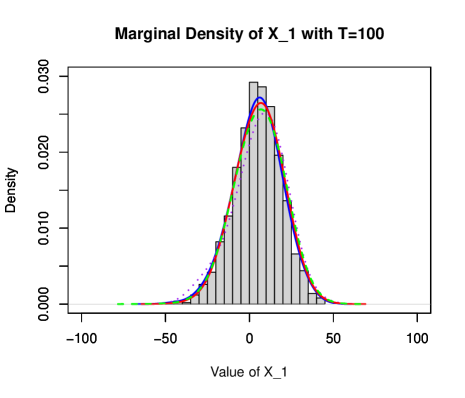

Next, let us we compare the marginal distribution of and that of the quasi-process, , under the same parameter values as in the previous experiments. Figures 5 – 7 show histograms of 1000 values of from the true distribution and its estimated density (blue solid curve) with and . At the same time, estimated densities of with (purple dotted curve), (green dashed curve), and (red solid curve). From those, we can observe the convergence of the marginal distribution when and .

4 Main results for -estimation

4.1 Consistency results

Let be independent copies of process defined on the same probability space , and denote its empirical measure as

| (4.1) |

In the sequel, we assume that, in the empirical measure in (2.1), the permutation samples are taken such that as . Moreover, when is a family of measurable functions , we assume that is given by (2.2) for a given .

Theorem 4.1.

Suppose that is open bounded subset of with smooth boundary, and that

| (4.2) |

Moreover, for , suppose that there exists such that for any ,

| (4.3) |

Then is weakly consistent to :

Proof.

It follows for any sequence of permutations that

| (4.4) |

and the last second term goes to zero because, under condition (4.2), class is -Glivenko-Cantelli:

| (4.5) |

To show the convergence of the first term in the last right-hand side of (4.4), we show that

| (4.6) |

for any sequence of .

Note the set admits a version of Sobolev inequality for embedding for , that is, for every , it holds that

see Evans [2], Sec.5.6, Theorem 5. We used this inequality to obtain

4.2 Asymptotic normality

For class , we denote the bracketing number of by , which is the minimum number of -brackets, including , that is a family of measurable functions satisfying with , covering .

Theorem 4.2.

Considering the same assumptions as in Theorem 4.1, with matrix invertible. Moreover, suppose that there exist a constant and a sequence with and such that, for and any ,

| (4.10) |

as . Then the -estimator is asymptotically normal:

with .

Remark 4.1.

Note that in Theorem 4.2 is not necessarily unique because, if some satisfies (4.10), then also satisfies (4.10). Because we can freely control , we can attain the -consistency for various . If satisfies (4.10) and it holds for with ,

Then this is optimal. In addition, the example in Section 5.1; see Remark 5.1, indicates that several can be found and the optimal rate of convergence is attained by choosing suitably.

Proof.

We shall use the notation (4.1). Because any function in is Lipschitz with respect to , it follows from, for example, argument as in Example 19.7 in van der Vaart [13], p.271, that the bracketing number of is finite. For every ,

which implies that class is -Donsker, and therefore,

Therefore it follows from the decomposition (4.4) that

Under assumption (4.10), it follows the same argument as in (4.7)-(4.9) that

Consequently, it holds that

Considering and the definition of , we have

and

Here, we assume that is Lipschitz continuous with respect to . The bracketing number satisfies ; see Example 19.7 in van der Vaart [13]. Then, using the same argument as in the proof of Corollary 5.53 in van der Vaart [13] with replaced by our , we established that is bounded in probability.

Similarly, we have

which yields

| (4.11) |

Hence, is approximately a minimum contrast estimator for the contrast function . Hereafter, we can obtain

using the same argument as in the proof of Theorem 5.23 in van der Vaart [13] with the condition (4.11): replace with ; with ; with in the proof.

In particular, because ’s are IIDs, we conclude by the central limit theorem that

∎

5 Examples

5.1 Default-related discounted losses

Here, we consider concrete examples for and investigate sufficient conditions that ensure the conditions in Theorems 4.1 and 4.2.

Suppose the Lévy process with (1.1) represents a ‘loss’ process of a company, and we define the time of default as

for constants and . is interpreted as the time of default (resp. ruin) with default levels in the context of finance (resp. insurance). In this section, we consider a discounted loss up to default. For ,

| (5.1) |

where and are a bounded function with parameter to be controlled. Then, is the expected discounted loss up to default

| (5.2) |

see Feng and Shimizu [4] for details on this quantity.

In the sequel, we consider the Skorokhod space , where is the Skorokhod metric given in Section 1.

Lemma 5.1.

Let . The functional defined on is continuous with respect to ; that is, for any and , there exists a such that

Proof.

Note that the functional

in is continuous in the sense of the Skorokhod metric , and it follows for each and , there exists a constant such that when ,

which implies that

Because by the definition of , when is sufficiently small, we have

which is equivalent to . ∎

Lemma 5.2.

Let be an integer and . For bounded function with parameter , suppose that the derivatives up to th order with respect to are uniformly bounded

| (5.3) |

for constant . Moreover, suppose the Lipschitz continuity:

| (5.4) |

Then the functional (5.1) satisfies that

Proof.

In this proof, we arbitrarily fix and simply write .

For any and any increasing surjection

where is the identity map of . In the last inequality, we use that is Lipschitz continuous with the Lipschitz constant . Consider the infimum with respect to on both sides to obtain

This inequality with Lemma 5.1 implies that is continuous on .

Because under this assumption, the same argument is valid for . ∎

Lemma 5.3.

Suppose we use the same assumptions as in Lemma 5.2, and that there exist constants and as well as sequence with such that

| (5.5) |

For each , where -term is independent of . Then it follows for each and any that

Proof.

We can check the condition (5.5) by taking the sampling interval suitably, as in the following Lemma:

Lemma 5.4.

Suppose that for some . Hereafter, the condition (5.5) holds with for any .

Proof.

Recall that

Hereafter, it follows that

where , which is the number of pairs with in is equal to . Here, we claim that the number of such that is

Generally, it follows from the Vandermonde’s formula that

for each . Therefore, we have

and that

Taking () and , we observe that

Hence, when we take , it holds that

∎

5.2 Dividends up to ruin

In the dividends problem, we can consider a case where in (5.2) is of the form

where is a constant and is an increasing function in . Assuming that a surplus of an insurance company is given, the functional

is interpreted as the aggregate dividends paid up to ruin or maturity depending on the parameter , where the dividend is paid when the surplus is over the threshold , and the maturity depends on the threshold. That is, when the threshold level is high (the dividends are hard to pay), the maturity for dividends will be longer, but the maturity will be shorter when the threshold level is low (the dividends are easy to pay). Because the ruin level is , the threshold should be set over , and we assume that for constant .

For technical reasons, we replace the indicator function with with bounded derivatives such that

for a ‘small’ constant . That is, we can replace the following indicators as:

Hereafter, the functional can be approximated by

This approximation is valid because it follows by the bounded convergence theorem that

Moreover, because the derivatives of are uniformly bounded, it follows that for fixed and ,

satisfies conditions (5.3) and (5.4) in Lemma 5.2. Hereafter, Theorem 4.2 is applicable for with the Lévy process . Further examples will be discussed in a different paper; Shimizu and Shiraishi [12].

Acknowledgments

The first author was partially supported by JSPS KAKENHI Grant Numbers JP21K03358 and JST CREST JPMJCR14D7, Japan. The second author was supported by JSPS KAKENHI Grant Number JP16K00036.

References

- [1] Billingsley, P. (1999). Convergence of probability measures. 2nd ed. John Wiley & Sons, New York.

- [2] Evans, L. C. (2010). Partial differential equations, 2nd ed., American Mathematical Society, Providence, RI.

- [3] Feng, R. (2011). An operator-based approach to the analysis of ruin-related quantities in jump diffusion risk models. Insurance: Mathematics and Economics, 48 (2), 304–313.

- [4] Feng, R. and Shimizu, Y. (2013). On a generalization from ruin to default in a Lévy insurance risk model. Methodol. Comput. Appl. Probab., 15, (4), 773–802.

- [5] Comte, F. and Genon-Catalot, V. (2011). Estimation for Lévy processes from high frequency data within a long term interval. The Annals of Statistics, 39, (2), 803–837.

- [6] Gerber, H. U. and Shiu, E. S. W. (1997). From ruin theory to pricing reset guarantees and perpetual put options, Insurance: Math. and Econom., 24, 3–14.

- [7] Jacod, J. (2007). Asymptotic properties of power variations of Lévy processes. ESAIM Probab. Statist. 11, 173–196.

- [8] Kato, K. and Kurisu, D. (2020). Bootstrap confidence bands for spectral estimation of L évy densities under high-frequency observations. Stoch. Proc. Appl., 130, (3), 1159–1205.

- [9] Kuratowski, K. (1966). Topology I. Academic Press, New York.

- [10] Mammen, E. (1992). When Does Bootstrap Work?: Asymptotic Results and Simulations, Springer-Verlag, New York.

- [11] Shimizu, Y. (2009). Functional estimation for Lévy measures of semimartingales with Poissonian jumps. J. Multivariate Anal., 100, (6), 1073–1092.

- [12] Shimizu, Y. and Shiraishi, H. (2022). Semiparametric Estimation of Optimal Dividend Barrier for Spectrally Negative Lévy Process, preprint.

- [13] van der Vaart, A. W. (1998). Asymptotic Statistics. Cambridge University Press, Cambridge.

- [14] van der Vaart, A. W. and Wellner, J. A. (1996). Weak Convergence and Empirical Processes: With Applications to Statistics. Springer, New York.