title.1title.1\EdefEscapeHexTitleTitle\hyper@anchorstarttitle.1\hyper@anchorend

Semiparametric Conditional Factor Models: Estimation and Inference ††thanks: We thank Bin Chen, Xu Cheng, Robert Korajczyk (discussant), Yuan Liao, Hao Ma (discussant), Seth Pruitt (discussant), Andres Santos, Frank Schorfheide, Liangjun Su, Dacheng Xiu, Chu Zhang, and Linyan Zhu (discussant) as well as conference audiences and seminar participants at Nanyang Technological University, Peking University, Shanghai University of Finance and Economics, UC Riverside, University of Lausanne (Swiss Finance Institute), University of Pennsylvania, Xiamen University, 2021 YEAP, 2022 SFS Cavalcade, 2022 WFA, 2022 CICF, 2023 AFA, and Spring 2023 Rochester Conference in Econometrics for helpful discussions and comments.

Abstract

This paper introduces a simple and tractable sieve estimation of semiparametric conditional factor models with latent factors. We establish large--asymptotic properties of the estimators without requiring large . We also develop a simple bootstrap procedure for conducting inference about the conditional pricing errors as well as the shapes of the factor loading functions. These results enable us to estimate conditional factor structure of a large set of individual assets by utilizing arbitrary nonlinear functions of a number of characteristics without the need to pre-specify the factors, while allowing us to disentangle the characteristics’ role in capturing factor betas from alphas (i.e., undiversifiable risk from mispricing). We apply these methods to the cross-section of individual U.S. stock returns and find strong evidence of large nonzero pricing errors that combine to produce arbitrage portfolios with Sharpe ratios above 3. We also document a significant decline in apparent mispricing over time.

Keywords: Characteristics, managed portfolios, factor models, PCA, sieve estimation, conditional moments, nonparametric estimation, strong approximation

1 Introduction

Over the half-century that passed since publication of FamaMacBeth_RiskReturn_1973 financial economists have continued to grapple with their central question: whether asset returns are proportional, on average, to these assets’ exposures to systematic risk. The debate has centered on the role of asset characteristics that appear to be related to average returns, and whether this relationship represents “mispricing” or, instead, the characteristics’ role in capturing dynamically changing risk exposures. The challenge is that neither the nature of such systematic sources of risk nor the role of characteristics in capturing time-varying and asset-specific exposures to these sources of risk is known ex ante.

We consider the following semiparametric factor model

| (1) |

where is a vector of unobserved factors, is a vector of unknown factor loading functions, is an unknown intercept function, is the idiosyncratic component that cannot be explained by the common component, and and —an vector of covariates—are observed. Our main focus is on cross-sectional asset pricing, where are asset return realizations while are pre-specified asset characteristics (i.e. they are known at the beginning of period ).111Other potential applications include modelling the implied volatility of options (Parketal_FactorDynamics_2009) and describing consumer demand system (Lewbel_DemandSystems_1991), among others. In this case (1) describes a conditional factor model, in the sense that it captures time-variation in asset return exposures to the common factors (i.e., ) as well as the pricing errors (i.e., ), which are both functions of characteristics (i.e., ). As emphasized by Cochrane_Presidential_2011, this model is central to empirical asset pricing, since it potentially allows for distinguishing between “risk” and “mispricing” explanations of the role of characteristics in predicting asset returns.222While useful, it might not be sufficient to resolve the debate, since distinguishing between the different explanations requires understanding the economic nature of the latent factors - e.g., see Kozaketal_Interpreting_2018. Pooling the information in a multitude of stock characteristics and summarizing the common variation using a small number of factors would amount to “taming the zoo” of factors that proliferate in empirical asset pricing. The challenge to doing so is threefold: first, the identities of the common factors are unknown since the factors are latent; second, the functional forms of the and functions are also generally unknown; finally, the cross-sectional dimension is typically much larger than the sample time-series length , which renders standard tools of factor analysis inapplicable, especially when conditional covariances are time-varying.

We introduce a simple and tractable estimation method to recover both the latent factors and the functional parameters of the model, as well as develop formal inference procedures. First, we develop an easy-to-compute estimator for , and based on a sieve approximation to the nonparametric functions and . The estimators can be easily obtained by first running the regression of on sieves of for each and then applying principal component analysis (PCA) to the estimated coefficient matrix. Throughout the paper, we refer to the two-step procedure as the regressed-PCA. The first step of our procedure is a cross-sectional regression (FamaMacBeth_RiskReturn_1973). Thus, in asset pricing settings the regressed-PCA boils down to applying PCA to a relatively small set of characteristic-managed portfolios constructed via the Fama-MacBeth regressions. Second, we establish large sample properties of the estimators including consistency, rate of convergence, and asymptotic normality under mild conditions. In particular, we establish a strong approximation for the distribution of the estimator of the large dimensional coefficient matrix in the sieve approximation of and . These asymptotic results have several attractive properties: (i) they do not require large ; (ii) they allow to vary over time in a potentially non-stationary manner; (iii) they are applicable to unbalanced panels (which is useful since individual securities have varying life spans). Third, we provide two consistent estimators for the number of factors , which are also easy to compute. This enables us to conduct the regressed-PCA without specifying the number of factors a priori.

In asset pricing, testing the restriction that is equal to zero for a given set of factors is central for evaluating and comparing factor models. We show that linear specifications of and that are widely used in existing literature may adversely influence estimation of when the true underlying functional relationships are nonlinear. Therefore, along with the flexible nonparametric estimators we provide specification tests for the shape of and functions. We develop a simple bootstrap inference procedure for testing significance of pricing error as well as for linearity of and . First, we propose a weighted bootstrap procedure to approximate the distribution of the estimator of the large-dimensional coefficient matrix in the sieve approximation of and as well as construct a Wald-type test for examining the significance of . The main challenge to developing a valid bootstrap is that the asymptotic distribution usually involves a rotational transformation matrix, which could be different under the bootstrap distribution, invalidating the procedure. In order to solve this problem we enforce the same factor estimator in the bootstrap samples as in the actual data. Second, we develop a likelihood ratio-type test for examining the linearity of and . Specifically, we construct the test statistic by comparing estimators under the null hypothesis and the alternative hypothesis. The novelty of our construction is that we use the unrestricted factor estimator from the alternative to obtain the estimators of and under the null. This ensures the same rotational transformation matrix under the null and the alternative and thus the consistency of our test. Both of these tests also enjoy the aforementioned attractive features of our estimators: our Monte Carlo simulations show that the finite sample performance of our estimators and tests is satisfactory and encouraging for large , even when is small.

We apply our new methodology to analyze the cross section of individual stock returns in the US market. We use the same data set as in Kellyetal_Characteristics_2019, which is the closest study to ours in terms of its empirical aims, although both our econometric approach and empirical findings are quite different. First, in contrast to Kellyetal_Characteristics_2019; Kellyetal_IPCA_2017, our method does not attempt maximize the “fit” of the factor model to asset returns in time-series and cross-section simultaneously. Rather, we extract factors that capture the most time-series comovement in returns, as postulated by the arbitrage pricing theory (e.g., Ross_APT_1976), and then attribute average asset returns to their conditional loadings with these factors (or to pricing errors). Second, we allow for and functions to be non-linear. In fact, we are able to test–and reject–the validity of the linear specifications. Third, we are able to conduct rolling small sub-sample analyses to accommodate changing factor dynamics as our methods do not require large sample length . Finally, we are able to consistently estimate the number of latent factors.

Our empirical findings reveal that only one latent factor is detected by the formal tests when we consider linear dependence of and functions on characteristics, and two factors when we allow for nonlinearity–this is also in contrast to Kellyetal_Characteristics_2019, who advocate a five-factor model. Still, our tests reject the risk-based model, since the pricing errors associated with many characteristics are statistically different from zero. Their economic magnitudes are also substantial, as we are able to construct pure- portfolios with annualized Sharpe ratios typically above 3 (as is common in the literature, we refer to these as “arbitrage” portfolios, even though their returns are far from riskless). These Sharpe ratios tend to rise with the number of factors (we consider up to ten), indicating that adding factors does not improve the asset pricing properties of the model, even though it might help capture more time-series variation in returns. This result provides strong empirical evidence that the characteristics contain information about both risk exposures and mispricing. In addition, the nonlinear models often produce more reasonable estimated relationships between the risk exposures and characteristics than the linear model. For instance, the estimates from our nonlinear models show that firms with higher book-to-market ratios bear more systematic risk and hence have higher expected returns, whereas the estimates from the linear model often give the opposite result. Nevertheless, the additional flexibility provided by the nonparametric estimation of factor loadings does not result in an improved asset pricing performance of the factor models, yielding arbitrage portfolio Sharpe ratios that are as high or even higher than in the linear case, often exceeding 4. However, we also document the significant decline of pricing errors and arbitrage portfolio Sharpe ratios in the more recent years, in particular since 2000, potentially consistent with growth in quantitative investing that reduces mispricing by exploiting characteristic-related anomalies (e.g. as suggested by McLeanPontiff_DoesAcademic_2016 or Greenetal_Characteristics_2017). We also show that both in-sample and out-of-sample goodness of fits for all factor models declines from 1970 until roughly 2000 but increases thereafter, which is consistent with the findings in Campbell2001have and Campbell2022idiosyncratic on the time-variation in the amount of idiosyncratic volatility in the U.S. stock market.

Our paper relates to several strands of literature. Several studies estimate models similar to (1) under the assumption that are time-invariant, at least over subsamples. ConnorLinton_Semparametric_2007 and Connoretal_EfficientFFFactor_2012 develop estimation procedures based on kernel smoothing for the case with and being univariate functions. Fanetal_ProjectedPCA_2016 consider a sieve estimation which facilitates global inference, and propose a projected-PCA approach for the case with . Kimetal_Arbitrage_2019 extend the projected-PCA to allow for nonzero and use it to construct an arbitrage portfolio, while LiGeLinton_Dynamic_2020 develop a test of . Fanetal_StructuralDeep_2022 extend the projected-PCA by using deep neural networks to approximate and , and propose a local version of projected-PCA that relies on smooth behavior of over time. We contribute to this literature by introducing a robust sieve estimation that allows to vary over time and developing global inference for and . Despite some similarities, our regressed-PCA is genetically different from the projected-PCA. The regression in the former serves to extract from the common component for a consistent estimation, whereas the projection in the latter serves to remove the noise part of the factor loadings for a more efficient estimation. Therefore, the projected-PCA may fail to obtain consistent estimators when are time-varying. In contrast, our regressed-PCA is consistent even when are nonstationary over time.

Our study also contributes to the literature on time-varying factor models. Mottaetal_LocallyStationary_2011 and SuWang_TimeVarying_2017 consider the time-varying factor model with factor loadings being smooth functions of and propose local versions of PCA based on kernel smoothing.333There is a large literature on conditional models that considers time-varying factor loadings that are functions of aggregate variables rather than firm-specific characteristics, e.g. FersonHarvey_conditioning_1999 use a linear formulation while Roussanov_Composition_2014 considers nonparametric kernel-based specifications. Extending our method, Chen_UnifiedFramework_2022 provides an estimation of conditional factor models with heterogenous alpha and beta functions that allows for including aggregate variables in . PelgerXiong_State-varying_2019 assume that factor loadings are smooth functions of state variables and study a similar estimation procedure. GagliardiniMa_Extracting_2019 study a time-varying factor model with no arbitrage and extract local factors from conditional variance matrices. However, none of them are directly suitable for testing asset pricing models, since they all impose . Many empirical findings suggest that characteristics contain information about both pricing errors and risk exposures, which can be distinguished in our approach. There are numerous studies of conditional models with observed factors. For example, Gagliardinietal_Timevarying_2016 specify factor loadings as linear functions of both time-varying characteristics and state variables in a model with ; Gagliardinietal_EstimationConditionalFactor_2019 provide a comprehensive review.

The literature on the cross section of asset returns is vast; here we focus on multi-factor models motivated by the arbitrage pricing theory of Ross_APT_1976 and its generalizations (ChamberlainRothschild_FactorStuctures_1982; ConnorKorajczyk_Performance_1986; ConnorKorajczyk_RiskReturn_1988; Reisman/IAPT:1992). Empirical analysis that exploits the ability of stock characteristics to predict asset returns typically follows either the portfolio-sorting approach (FamaFrench_Commonrisk_1993; DanielTitman_Characteristics_1997; FamaFrench_FiveFactor_2015) or the characteristic-based approach (RosenbergMcKibben_ThePrediction_1973; Jacobs/Levy:88; Lewellen_Crosssection_2015; Greenetal_Characteristics_2017; Freybergeretal_Dissecting_2017; Kirby_FirmChar_2020; GiglioXiu_Asset_2019). The importance of nonlinearity is highlighted by several empirical studies (Connoretal_EfficientFFFactor_2012; Kirby_FirmChar_2020), and has also been addressed by machine learning methods in recent studies (Guetal_Autoencoder_2021; Chenetal_DeepLearning_2020).

The central issue with both of these approaches is that they are unable to distinguish between the two roles played by characteristics: capturing time-varying risk exposures and representing mispricing. We complement the literature by introducing a semiparametric time-varying characteristic-based factor model that provides a simple, tractable and robust method for estimation and inference. This new methodology enables us to estimate conditional (dynamic) behavior of a large set of individual assets from a number of characteristics exhibiting nonlinearity without the need to pre-specify factors, while allowing us to disentangle the risk and mispricing explanations, as least from the standpoint of arbitrage-based models.

The remainder of the paper is organized as follows. Section 2 introduces the estimation method—the regressed-PCA. Section 3 establishes large sample properties of the estimators, including consistency, rate of convergence, and asymptotic distribution. Section 4 introduces a weighted bootstrap and develops two tests. Section 5 provides two consistent estimators of the number of factors. Section 6 applies our new methodology to analyze the cross section of individual stock returns in the US market. Section 7 briefly concludes. Appendix A collects assumptions, while Appendix B provides proofs of the main results. The Online Appendix presents auxiliary results, simulation results, additional empirical results, and technical lemmas.

2 Estimation Method

In this section we introduce the approach to estimating a latent factor model that we term regressed principal component analysis or regressed-PCA.

We first illustrate the idea behind our regressed-PCA method by assuming that is null and is linear: and for some matrix . Let , , and . Then we may write (1) in a matrix form

| (2) |

The main challenge in applying standard PCA to estimating and is the presence of in the first term on the right-hand side of (2). In order to circumvent this problem, we first regress on . Thus, we obtain

| (3) |

Heuristically, variation in the common component over comes from two sources, and , and regressing on helps isolate them by extracting from the common component. Given the factor structure on the right-hand side of (3), we can apply the standard PCA to in order to obtain estimators of and .

The model in (2) can be alternatively viewed as a panel data model with time-varying slope coefficients , which exhibit a factor structure. Essentially, the regressed-PCA first estimates the time-varying slope coefficients by period-by-period cross-sectional regressions, and then exploits the factor structure by using PCA.

2.1 Regressed-PCA Estimation

Now we consider the general case with nonzero and show how to estimate and nonparametrically. To estimate and without falling prey to the curse of dimensionality when is multivariate, we assume and are separable. Specifically, we assume that there are and such that

| (4) |

where is the th entry of . We adopt the sieve method to estimate and . Let be a set of basis functions (e.g., B-spline, Fourier series, polynomials), which spans a dense linear space of the functional space for and . Then we may write

| (5) | ||||

| (6) |

Here, and are the sieve coefficients; and are “remaining functions” representing the approximation errors; denotes the sieve size. The basic assumption for the sieve method is that and as . Let , , which is a vector of the sieve coefficients, , and which is a matrix of the sieve coefficients. Let and . Then

| (7) |

Thus, and can be well approximated by and under the basic sieve assumption, and estimating and reduces to estimating and .

We now introduce the estimation of , and based on the above sieve approximation in (7) by adapting the regressed-PCA.Let , and . Using the sieve approximation in (7), we may write (1) in a matrix form

| (8) |

Under the basic sieve assumption, the term “” is negligible, so the main challenge in applying standard PCA to estimating , and is the presence of in the first two terms on the right-hand side of (8). To solve this problem we regress on to obtain

| (9) |

where . Thus, we estimate , and as follows. First, since , we can remove by subtracting from and estimate by applying the standard PCA to the demeaned . Second, for identification of (and thus ), we assume . Since where , we can estimate according to . Third, we can estimate according to .

The estimators of , , , and are formally defined as follows. Denote the estimators by , , , and . Let , where denotes a vector of ones. We use the following normalization: and being diagonal with diagonal entries in descending order. Let . Then the columns of are the eigenvectors corresponding to the first largest eigenvalues of the matrix , , and

| (10) |

Here, we assume that —the number of factors—is known, and conduct asymptotic analysis and develop inference method in Sections 3 and 4. In Section 5, we develop two consistent estimators of , so all the results carry over to the unknown case using a conditioning argument.

2.2 Key Properties

Our regressed-PCA estimation enjoys several desirable properties, and is also easy to implement. First of all, as elucidated in Section 3.1, it accommodates time-varying characteristics and does not require large . Thus, it allows us to examine the changing relationship between risk and return via both full-sample and sub-sample analyses.

Our estimation procedure is also applicable for unbalanced panels, which is especially pertinent to cross-sectional asset pricing applications. The key step of regressed-PCA is to obtain . We may write . In the case of an unbalanced panel, we may obtain by taking the two sums over ’s, for which both and are observed in time period . This is equivalent to replacing missing data with zeros and proceeding as balanced panels. The asymptotic results established in the following sections continue to hold as , where is the sample size in time period .

Our estimation procedure continues to work when pricing errors and risk exposures are not fully captured by . Let and error terms in the pricing errors and the risk exposures, which are not explained by (i.e.,, orthogonal to ). It follows that

where . Notice that we are not interested in estimating and . Thus, the asymptotic properties that we derive continue if we replace in (1) by .

Moreover, efficiency of estimation could potentially be improved by using generalized least squares in the first step estimation. The asymptotic results that we derive continue to hold if we replace and with the corresponding transformations and , where is the conditional covariance matrix of for each .

2.3 Comparing Methods

How does our regressed-PCA compare with existing methods that have been proposed in the literature?

First, the projected-PCA of Fanetal_ProjectedPCA_2016 applies the standard PCA to the projected data—. The regression in the regressed-PCA is designed to extract from the common component for a consistent estimation, whereas the projection in the projected-PCA is designed to remove the noise in the factor loadings for a more efficient estimation. Therefore, the projected-PCA may fail to provide consistent estimates when is time-varying. Indeed, as discussed by Fanetal_ProjectedPCASupp_2016 and further investigated by Fanetal_StructuralDeep_2022 and Chengetal_UniformPredictive_2020, one may need to impose certain smoothness conditions on how varies with to ensure the consistency of the projected-PCA. Our regressed-PCA does not require such conditions. Moreover, the projected-PCA may require that certain observations be dropped in order to obtain a balanced panel, while regressed-PCA is applicable to unbalanced panels.

Second, consider the least squares estimation approach (Parketal_FactorDynamics_2009), which is at the core of the instrumented PCA (IPCA) of Kellyetal_Characteristics_2019. The least squares estimation problem is nonconvex and thus cannot be solved explicitly; Parketal_FactorDynamics_2009 develop a numerical algorithm to find the estimators, while Kellyetal_Characteristics_2019 propose an alternating least squares procedure. However, both methods may require a good choice of initial values as convergence to the correct solution is not assured and their asymptotic properties are not well-understood. Lastly, while IPCA implicitly relies on a long time-series of returns, regressed-PCA does not require a large , which allows for sub-sample analyses as well as capturing potential time-variation in the coefficients ( and ).

Overall, in addition to the asymptotic properties that we derive, our estimators can always be explicitly solved for, and their computation is easy since it involves only least-squares regression and PCA.

2.4 Asset Pricing Interpretation

In a typical asset pricing application would be realized returns on asset at the end of period , while would represent an ’th attribute/characteristic of asset that is known a the beginning of period (or, alternatively, at the “end” of period ). The regressed-PCA first estimates the time-varying slope coefficients by period-by-period cross-sectional regressions of returns on (functions of) asset characteristics, and then exploits the factor structure by using PCA. The period-by-period cross-sectional regressions are known as Fama-MacBeth regressions (FamaMacBeth_RiskReturn_1973), which help transform the large unbalanced panel of noisy individual asset returns into a low-dimensional balanced panel of assets that are largely free of idiosyncratic noise, . In asset pricing applications, can be interpreted as the time realization of returns on a set of managed portfolios, sometimes referred to as “characteristic pure plays” or “cross-sectional factors” (e.g. as in Backetal_PurePlays_2015 or FamaFrench_CSTS_2020).

In particular, if the sieve basis () includes a constant term (e.g. as the first element in ), and is also standardized to have a zero mean in each cross-section, then intercept in Fama-MacBeth regressions (the first element in ) is a “level” return, which is the equal-weighted average excess return across all individual assets with weights that sum up to unity (sometimes referred to as a “naively diversified” or portfolio). As shown by Fama_76, the period-by-period slope coefficients corresponding to the time-varying characteristics are excess returns on zero-cost portfolios with weights on individual assets that set the weighted average value of the relevant characteristic to one and that of all the remaining characteristics bases to zero, as long as the right-hand side variables are suitably normalized (Kirby_FirmChar_2020 discusses other attractive properties of these portfolios). In our setting, the th entry of is a portfolio return (i.e. a weighted average of all test asset returns) with weights determined by the th row of , which is a standardized version of . If is diagonal, the portfolios are normalized by the second moment of .

3 Asymptotic Analysis

In this section we establish consistency of our estimators and provide their asymptotic distributions. We begin by defining some notation that is used throughout the paper. For a symmetric matrix , we denote its th largest eigenvalue by , and its smallest and largest eigenvalues by and . For a matrix , we denote its operator norm by , its Frobenius norm by , and its vectorization by . The Euclidian norm of a column vector is denoted . For matrices and , we use to denote their Kronecker product.

3.1 Consistency and Rate of Convergence

Prior to presenting formal theorems, we return to (2) to quickly illustrate why large is not required and are allowed to be nonstationary over in our asymptotic analysis. Assume and . Since the columns of and are the eigenvectors of and corresponding to the first largest eigenvalues, by the matrix perturbation theorem (see, for example, Yuetal_Useful_2014), to establish the consistency of to (up to a rotational transformation) it suffices to show

| (11) |

Since , (11) reduces to

| (12) |

When is fixed, (12) is equivalent to for each . Thus, we only need regularity conditions on and for each in order to apply the law of large numbers. This implies that can vary over in a non-stationary manner.

Let , which is a rotational transformation matrix that determines the convergence limit of , and . Let , which is for B-spline and Fourier series and for polynomials (see, for example, BelloniChernozhukovChetverikovKato_SeriesEstimator_2015). The first theoretical result of the paper is given as follows. We collect all assumptions with discussions in Appendix A.

Theorem 3.1.

We discuss two important findings. First, Theorem 3.1 implies that and can be consistently estimated by and , and , and can be consistently estimated by , and up to a rotational transformation under either large with fixed or large and large . In particular, the consistency of requires . This is because a large sieve approximation error of and may cause inconsistent estimation of . To quickly see this, let us look at the following simple linear models

| (13) | ||||

| (14) |

where and are vectors, is a scalar factor, and is independent of and . Let us further assume and , where is a scalar coefficient, and is independent of . Then (13) and (14) can be rewritten as

| (15) | ||||

| (16) |

where , , , and . Thus, if only is used for estimating (13) (i.e., the sieve approximation error of is large), then can consistently estimates up to a scalar; if only is used for estimating (14) (i.e., the sieve approximation error of is large), then can consistently estimate up to a scalar. In both cases, fails to consistently estimate the space spanned by , unless is proportional to in the former case and is not changing over in the latter case. The finding also suggests that misspefication of and may cause inconsistent estimation of , thus motivates us to develop a specification test for and in Section 4.2.

Second, Theorem 3.1 provides a fast convergence rate of , and . For example, when , and attains the optimal rate , which is the fastest rate that one can obtain when were known. Assume , which can be satisfied for sufficiently large under the restriction . Then attains the optimal rate , which is the fastest rate that one can obtain when and were known. This implies that the nonparametric specifications of and do not deteriorate the optimal rate for estimating as long as and are sufficiently smooth (i.e., is sufficiently large), or parametric specifications of and do not necessarily improve the estimation of . This implication is important in developing the specification test for and in Section 4.2. The fast convergence rate result also allows to derive the asymptotic distributions of the estimators.

The requirement is standard for sieve approximations (e.g. BelloniChernozhukovChetverikovKato_SeriesEstimator_2015). Note that if the functional forms of and are known and specified accordingly, then there is no sieve approximation error and we can dispense with the requirement that as the asymptotic properties continue to hold for a fixed .

3.2 Asymptotic Distribution

We focus on deriving the asymptotic distributions of and , since our main concern is inference for and . Let , where and . It is a variance-covariance matrix, which will appear in the asymptotic distributions of and . The second theoretical result is established as follows.

Theorem 3.2.

Theorem 3.2 establishes a strong approximation: can be well approximated by a normal random matrix , in the sense that their difference converges in probability to zero when , and . Therefore, behaves like a normal random matrix. Here, the dimensions of and grow with , so the classical central limit theorem does not apply. Instead, we use the Yurinskii’s coupling to establish the strong approximation that allows for weak dependence of over .

4 Bootstrap Inference

In this section we develop a weighted bootstrap approach to estimating the distribution of , as well as a specification test for linearity of and .

4.1 Weighted Bootstrap

It seems straightforward to estimate the distribution of by estimating its unknown components. However, it may be challenging to estimate , since we allow for weak dependence of over . In order to circumvent this challenge, we develop a weighted bootstrap, which may have an additional computational advantage.

Let be a sequence of independently and identically distributed positive random variables with and . For example, ’s can be drawn from the standard exponential distribution and . For each , we assign the same weight to all observations over to maintain the dependence of over . Let and , which is bootstrap version of . To define the bootstrap estimators of and , let and . The bootstrap estimators are given by

| (17) |

which mimic and following the formulas and . We propose to estimate the distribution of by the distribution of conditional on the data. The validity of the bootstrap for can be quickly seen when and .444In this case, , and . Thus, the distribution of can be estimated by the distribution of conditional on the data by the weighted bootstrap in BelloniChernozhukovChetverikovKato_SeriesEstimator_2015.

The bootstrap procedure can be easily adapted for unbalanced panels. The key step is to obtain . We may write . In the presence of unbalanced panels, we may obtain by taking the two sums over ’s, for which both and are observed in time period . This is equivalent to replacing missing data with zeros and proceeding as balanced panels. Prior to this, we need to generate once, where is the number of all observation unit ’s. The asymptotic results established below continue to hold as , where is the sample size in time period .

Let be the probability measure with respect to conditional on . The third theoretical result is established as follows.

Theorem 4.1.

Theorem 4.1 implies that the distribution of , which is equal to the distribution of , can be approximated by the distribution of conditional on the data, when , and . The result allows for the same weak dependence of over as Theorem 3.2.

A more natural bootstrap estimator for is given by , whose columns are the eigenvectors of corresponding to its first largest eigenvalues. We notice that conditional on the data may fail to estimate the distribution of . The key part of the proof is to show that and share a similar asymptotic expansion. Specifically, we show

and

where . Let and . Similarly, we can show

Thus, conditional on the data may fail to estimate the distribution of , since is not asymptotically negligible due to the relatively slow convergence rate of and . Since , it is important to use rather than in (17) to ensure that and share a common rotational transformation matrix and are centered around the same quantity , rendering the validity of the bootstrap.

Significance tests for and . We can immediately use Theorems 3.2 and 4.1 for several significance tests. We can test whether by comparing with the quantile of conditional on the data for . Similarly, we can test whether ’s are significant in for some given ’s and ’s, and whether ’s are jointly significant in for some given ’s and ’s, which is equivalent to whether certain rows of are jointly zero. However, due to the lack of identification, we are not able to test the significance of each component of ; due to the full rank requirement in Assumption A.2(i), we cannot use Theorems 3.2 and 4.1 to test whether .

4.2 Specification Test

In order to test for linearity of and , we develop a test by comparing their estimators under the null and the alternative. Specifically, we consider the following the hypothesis:

| (18) |

Estimators of and under are already given by and in (10). Let , , and . Estimators of and under are given by and , where and . Three remarks for and are as follows. First, we use the unrestricted estimator rather than a restricted one by imposing to ensure that and share a common rotational transformation matrix, which is important in justifying the validity of the test. Second, in we use , which is an unrestricted estimator of , rather than the restricted estimator under to avoid the full rank requirement of . Third, we note that using does not cause efficiency loss in estimating and , since has attained the optimal rate as discussed after Theorem 3.1. Our test statistic is

| (19) |

To obtain critical values, we adopt the bootstrap method. Let , , and , where . It is shown in the proof of Theorem 4.2 that under , . In view of this, we may estimate the null distribution of by the distribution of

| (20) |

conditional on the data, where and . For , let be the quantile of conditional on the data. Thus, we construct the test as follows: reject if .

Theorem 4.2.

The validity of the test does not require , as all above results. It also holds when but at a slower rate than , which is usually true in asset pricing.

5 Determining the Number of Factors

In this section we address the problem of estimating the number of factors . To solve the problem, we develop two estimators: one by maximizing the ratio of two adjacent eigenvalues (AhnHorenstein_EigenvalueRatio_2013), and another by counting the number of “large” eigenvalues (BaiNg_NumberofFactors_2002). To define the estimators, let denote the th largest eigenvalue of the matrix . The first estimator is given by

| (21) |

Here, is constrained to between and . This is not restrictive, since we assume that is fixed and . The second estimator is given by

| (22) |

where denotes the cardinality of and is a tuning parameter.

Theorem 5.1.

As the final theoretical result of the paper, Theorem 5.1 demonstrates that and are consistent estimators of . The consistency of requires , while the consistency of does not require . The latter relies on the choice of . In practice, is recommended when is large, and is recommended when is small.

6 Empirical Analysis

A central question in empirical asset pricing is why different assets earn different average returns. While asset pricing theory attributes cross-sectional differences in asset returns to risk exposures, there is substantial evidence suggesting a role for mispricing captured by dependence of returns on asset characteristics, which suggests potential market inefficiency. Much of the debate centers around multi-factor models that aim to link average returns to factor loadings following FamaFrench_Commonrisk_1993, who pursue a portfolio-sorting approach to constructing asset pricing factors. Since their seminal paper, hundreds of factors have been proposed, collectively dubbed a “factor zoo” by Cochrane_Presidential_2011 and further discussed by Harveyetal_FactorZoo_2016. While some of the factor models have an explicit justification based on economic theory, many implicitly rely on the idea that factors capture common variation in portfolio returns, thus appealing to arbitrage pricing theory and its extensions (Ross_APT_1976; ChamberlainRothschild_FactorStuctures_1982; ConnorKorajczyk_Performance_1986; ConnorKorajczyk_RiskReturn_1988). Since implementing the latter requires knowledge of the conditional covariance matrix of returns, which is infeasible to estimate when is larger than , most studies rely on stock characteristics to proxy for (imperfectly measured) factor exposures. However, this makes distinguishing between the two types of explanations virtually impossible, as exemplified by the “characteristics versus covariances” debate (DanielTitman_Characteristics_1997). Our method is perfectly suited for resolving this debate, since it allows characteristics to simultaneously appear in both pricing errors and conditional covariances with unobserved common factors, which they also help recover.

We consider the following semiparametric characteristic-based factor model

| (23) |

where is the excess return of asset (e.g., stock ) in time period , is a vector of characteristics in time period , is a vector of unobserved latent factors, the pricing error (i.e., ) and the risk exposures to factors (i.e., ) are nonparametric functions of characteristics (i.e., ). The model falls into the general framework of model (1), where we need to interpret as characteristics in time period . This model provides a unified approach for studying the cross section of asset returns that nests the characteristic-based model and the risk-based model. The modelling of the pricing error and the risk exposures not only provides a way to disentangle the versus explanations, but also allows us to estimate a model for a large set of individual stocks. In addition, we do not need to rely on ex ante knowledge to pre-specify the latent factors. Distinct from the models in ConnorLinton_Semparametric_2007, Connoretal_EfficientFFFactor_2012, Kellyetal_Characteristics_2019, and Kimetal_Arbitrage_2019, we allow for time-varying characteristics, nonzero pricing error, nonlinearity of and , and unknown number of factors. These are all crucial features of our approach, and not just for the sake of generality. For example, as illustrated in Section 3.1, failure to take into account the time-varying features of characteristics or mis-specifications in the functional forms of and may result in misleading estimation of factors.

6.1 Data and Methodology

We use the same dataset used in Kellyetal_Characteristics_2019, which is originally from Freybergeretal_Dissecting_2017. The data set contains monthly returns of individual stocks and associated characteristics with sample periods from July, 1962 to May, 2014. The data is in the form of an unbalanced panel, for which our methods are applicable. See the above two papers for the detailed descriptions of the data. For ease of comparison, we also use the same characteristics as those authors. By following the same procedure in Kellyetal_Characteristics_2019, we transform the values of the characteristics to relative ranking values with range . This can make the contributions of individual characteristic in pricing error and risk exposures comparable, and can further avoid the distorting effects from the outliers. To satisfy the large requirement, we select the sample period with at least individual stocks that have observations on both returns and the characteristics, which is different from the case with at least individual stocks in Kellyetal_Characteristics_2019. This yields a sample from September, 1968 to May, 2014.

To estimate the model, we implement the regressed-PCA by choosing the basis functions as and linear B-splines of . Using leads to linear specifications of and , while using linear B-splines of leads to nonlinear specifications of and , where and are continuous piecewise linear functions.555The one dimensional linear B-spline is defined on a set of consecutive equidistant knots: . For , on , on , and 0 elsewhere. For , on and 0 elsewhere. To estimate the number of factors , we use in (21). To implement the weighted bootstrap, we let ’s be i.i.d. random variables with the standard exponential distribution. To implement the tests of and linearity of and , we set the number of bootstrap draws to 499.

In order to evaluate the performance of the regressed-PCA, we compute several measures of fit. First, we calculate Fama-MacBeth cross sectional regression , which captures the variation in individual stock returns explained by “managed portfolios” constructed from the sieve functions of characteristics. Next, we report the panel regression which captures the variations of these managed portfolios explained by different sets of extracted factors. Then, we consider the following three types of measures that directly speak to the ability of the factor models to explain the cross-section of individual stock returns. The first one is total as used in Kellyetal_Characteristics_2019.The second one measures the cross-sectional average of time series across all stocks, which reflects the ability of the extracted factors to capture common variation in asset returns. The third measures the time series average of cross-sectional goodness of fit measures. As such, it corresponds to the of the Fama-MacBeth cross-sectional regression, and is the one of interest for evaluating the model’s ability to explain the cross-section of average returns. Fama-MacBeth regression slopes can be interpreted as returns on pure-play characteristic portfolios (corresponding to ) and factor-mimicking portfolios (for ) - i.e. portfolios that have unit loading on one characteristic/factor and zero on all the others). Thus, the Fama-MacBeth reflects how much ex post variation in returns these portfolios can explain, as pointed out by Fama_76 and emphasized by Lewellen_Crosssection_2015.

| (24) | ||||

| (25) | ||||

| (26) |

Second, we consider a version of these goodness-of-fit measures that zero in on the role of factors in explaining the time-series as well as the cross-section of stock returns, by excluding the conditional intercepts:

| (27) | ||||

| (28) | ||||

| (29) |

Third, we assess the out-of-sample prediction. For , we use the data through to implement the regressed-PCA and obtain estimators, say , , ; and then compute the out-of-sample prediction of as , where , that is, the average of factor estimators through . We can define three types of out-of-sample predictive ’s analogously by replacing , and with , and ,

| (30) | ||||

| (31) | ||||

| (32) |

Fourth, we assess out-of-sample fit by constructing factor returns based on expanding-window estimation. For , we use the data through to implement the regressed-PCA and obtain estimated and ; we then calculate the out-of-sample realized factor return at as

| (33) |

Even though the resulting factor returns are only known ex post at time , they represent returns on portfolios that are constructed ex ante, i.e. using weights based on estimates obtained at time . With this set of measures, we are able to access how much of the cross-sectional variation of individual stock returns can be explained by the pre-estimated . The associated ’s are defined as follows:

| (34) | ||||

| (35) | ||||

| (36) |

Finally, we construct an arbitrage portfolio based on a pure- strategy and evaluate its performance. By (9) and Theorem 3.1, it is easy to see that for each as . This allows us to construct an arbitrage portfolio based on an estimate of . For , we use the data through to implement the regressed-PCA and obtain an estimator of , say ; and then compute the portfolio weights by and the excess return of the portfolio by , where . We evaluate the annualized Sharpe ratio of this portfolio.

In Table I, we consider linear specifications of and by letting . In Table II, we consider continuous piecewise linear specifications with 18 characteristics with one internal knot by letting be linear B-splines of , where we split into two equal-length intervals. In Table III, we further consider continuous piecewise linear specifications with 12 characteristics with two internal knots by letting be linear B-splines of , where we split [-0.5; 0.5] into three equal length intervals. In the nonlinear specifications we use characteristics that are shown to be statistically significant under the linear model, as detailed in Appendix E.

6.2 Empirical Results

The main findings are summarized as follows. First, the eigenvalue-based estimators described in Section 5 select one factor in the linear case and two factors in the nonlinear cases, which is in contrast to the arguments of Kellyetal_Characteristics_2019 that five factors are needed. Second, the out-of-sample based on our estimated one or two factor model with nonzero is 0.54% in the linear specification, 0.59% and 0.57% in the two nonlinear specifications, all of which are comparable to 0.60% in Kellyetal_Characteristics_2019 linear specifications with five factors. Similarly, the out-sample-sample fits are close to Kellyetal_Characteristics_2019. With six factors, the total based on our method is 15.42%, 15.89% and 16.31% under three model specifications, which is close to 17.80% in Kellyetal_Characteristics_2019. We notice that the total in-sample ’s from this estimated single factor models is smaller than Kellyetal_Characteristics_2019’s. This is not surprising, since the objective of their IPCA estimation is (essentially) maximizing total (in-sample) . Third, by increasing the number of factors, we can improve the in-sample fit, since all three in-sample ’s increase with . However, increasing the number of factors does not necessarily improve the out-of-sample prediction of the model, since factor betas simply soaks up the variation that is otherwise captured by .666Formally, this is because , which does not depend on , where is the average of the coefficient estimates from the first-step Fama-MacBetch regressions (also see (9)). Fourth, compared to the linear specification, the nonlinear specifications improve in-sample fit significantly and out-of-sample prediction slightly. Both the improved fit and robustness show the advantage of nonlinear model estimation based on linear B-splines (we provide additional empirical results in Appendix E).

We further use our tests to examine whether factor models explain the cross-section of average stock returns (i.e. ) as well as whether and functions are linear in characteristics. First, we find strong evidence to reject the null hypothesis of in our estimated factor models whether we consider the one- or two-factor models that are selected by our formal procedure, or indeed any number of factors between one and ten (we report the p-values here concisely in Table I-III to save space, suffice it to say that in all cases the pricing errors are significant at level). This result is in contrast to Kellyetal_Characteristics_2019 who find that increasing the number of factors can turn rejection to failure to reject, settling on a five-factor model. The difference stems from the nature of factors that we extract: our factors are designed to capture common time-series variation of stock returns, in the spirit of the APT, while the IPCA procedure of Kellyetal_Characteristics_2019 is designed to fit the cross-section of stock returns as well as their common time-variation, potentially giving up on the latter in order to improve the former. Indeed, our factors do a better job of capturing common time variation in stock returns, as exhibited both by the measures above and, more importantly, by the Sharpe ratios of the arbitrage portfolios that exploit the non-zero alphas. In particular, we find a high annualized Sharpe ratio for the pure- strategy in all of the cases that we consider. The Sharpe ratio increases from 3.18 to 3.82 as we increase from to in the linear specification, and are in the same range (sometimes exceeding ) in the nonlinear specifications that utilize B-splines while reducing the number of characteristics used (when we use fewer characteristics, the Sharpe ratio tends to fall with the number of factors in some of the specifications). Since alphas always decline when additional factors are introduced, the rise in Sharpe ratios as the number of factors grows is clear evidence of the important role of the factors in hedging out common variation in stock returns, which reduces the volatility of the arbitrage portfolio at a rate that exceeds the decline in alphas.

We also report the Sharpe ratios for each out-of-sample realized factor , as defined in (33), and out-of-sample mean-variance efficient (MVE) portfolio of this group of factors. The out-of-sample MVE portfolio of the factors is defined as at time , where is the solution to

| (37) |

Here and , which are based on the estimates from regressed-PCA available at time . Importantly, this construction of the MVE portfolio is robust to the time-variation in the rotation matrices that arises when factors are extracted using PCA period by period, so that the factor realizations are not orthogonal ex post.

The MVE portfolio Sharpe ratio is not monotonically increasing in the number of factors since some factors have essentially zero (or negative) out-of-sample Sharpe ratios, and the factors are not necessarily exactly orthogonal out-of-sample, adding to the portfolio volatility. In fact, in the linear specification where only one factor is estimated to be optimal, the out-of-sample MVE portfolio Sharpe ratio varies around that of the first factor, . At the same time, when we consider nonlinear models the MVE portfolio Sharpe ratio increases with the number of factors , from about when up to above when , which is comparable to the arbitrage portfolio. This result underscores the importance of allowing for a flexible nonlinear relationship between characteristics and risk exposures, which is one of the key advantages of our methodology.

Before proceeding to the detailed investigation of characteristics and nonlinearity, we need to pin down the signs of the extracted factors. Under the normalization and being diagonal with diagonal entries in descending order, the signs of the extracted factors are undetermined. We let the sample means of the extracted factors to be positive so that the unconditional risk premium on each factor is positive. Further, to interpret the latent factors, we also report the factor projection regressions and correlation matrix among the extracted factors and six Fama-French factors in Appendix E. in particular, compared to the linear case, the factors extracted using our nonlinear specifications have much higher correlations with the market excess return, size, and profitability factors of FamaFrench_FiveFactor_2015.

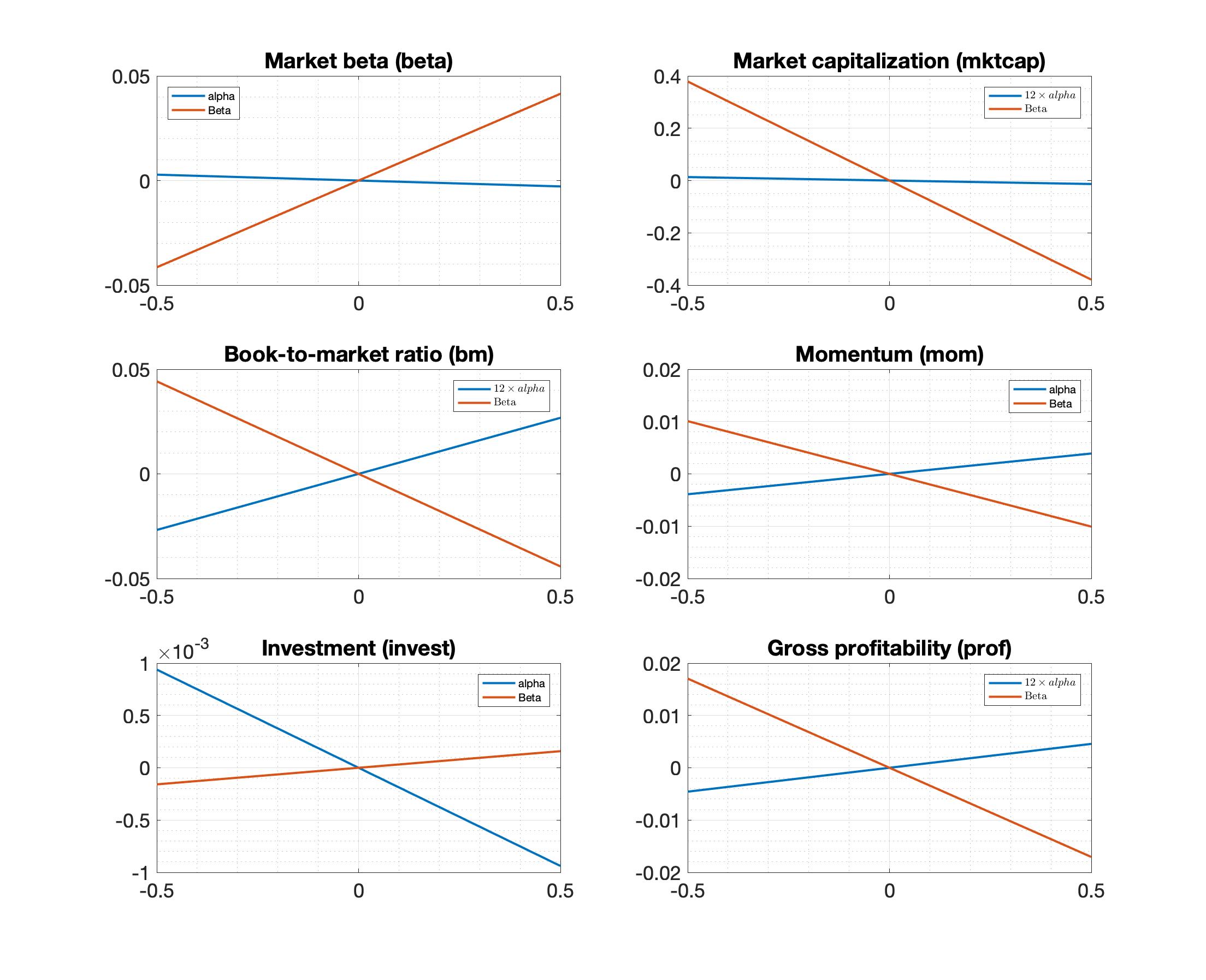

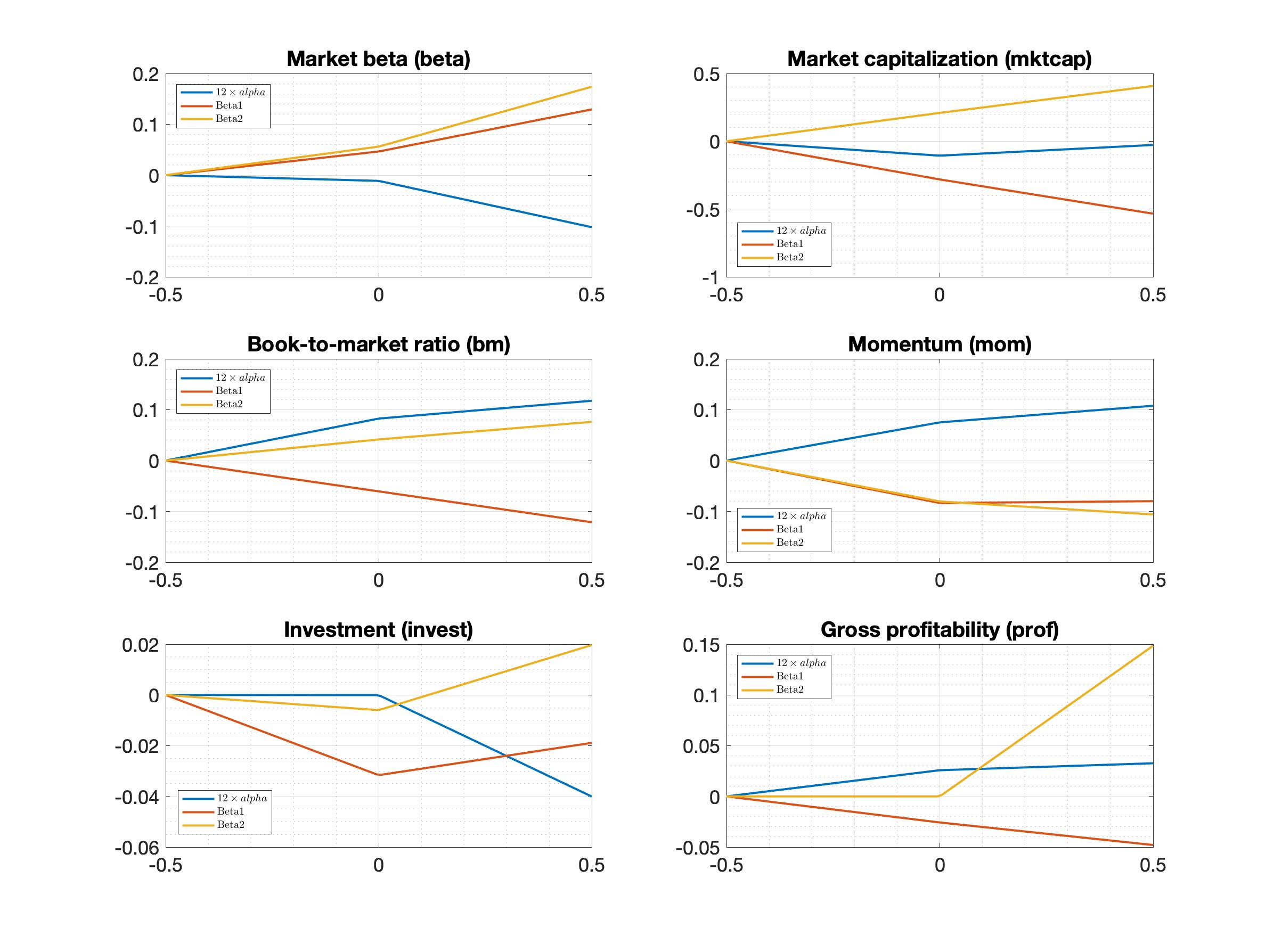

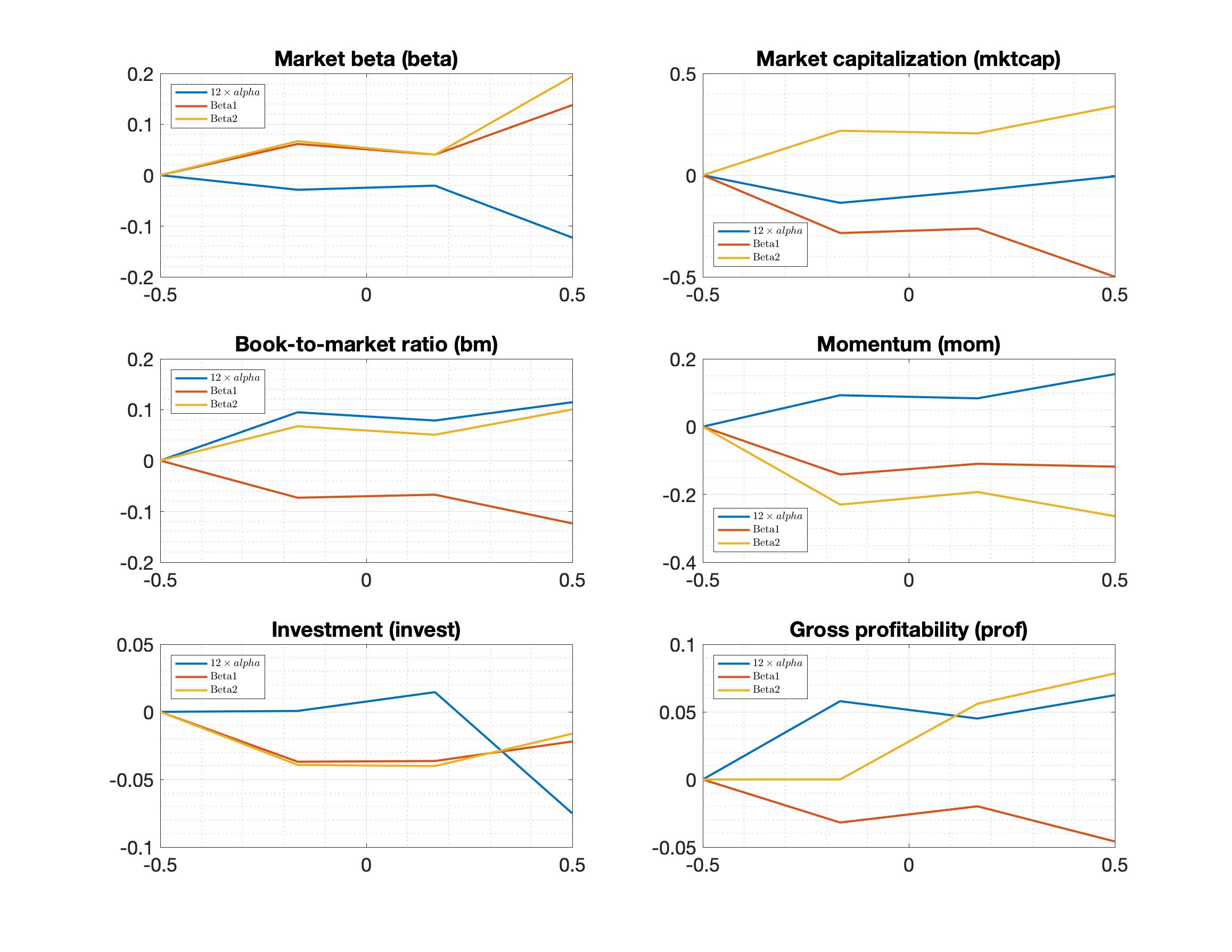

Empirical studies show that stocks with smaller market capitalization, higher book-to-market ratio (FamaFrench_Commonrisk_1993), or higher past returns (JegadeeshTitman_Returnstobuying_1993) tend to have higher returns, often referred to as “size”, “value”, and “momentum” anomalies in equity market. The presumed “rational” explanation for these anomalies is that smaller or value firms or firms with better past performance have larger exposures to priced systematic risky factors. In order to test this hypothesis, we plot pricing errors and the risk exposures as functions of six key characteristics. Figure 1 reports the results for the linear specification, and we find a downward sloping factor loading (on the one common factor) as a function of book-to-market ratio, which rejects a (conditional) one-factor-model explanation of value. Figure 2-3 report the results for the nonlinear specifications with 18 characteristics with one knot and 12 characteristics with two knots, separately, while we find the associated nonlinear and upward sloping exposure to the second extracted factor, which is more consistent with the risk-based view. Similarly, we find opposite curve slopes from the linear and nonlinear specifications for investment and profitability, where the results from the nonlinear specifications are more consistent with the findings in FamaFrench_FiveFactor_2015: firms with low investment and high profitability bear greater exposures to systematic risks. As detailed in Appendix E, most of the characteristics contain relevant information about and/or . Overall, estimates from the nonlinear specifications are more consistent with the risk view than those from the linear specification. All the conclusions are robust to different choices of linear B-splines.

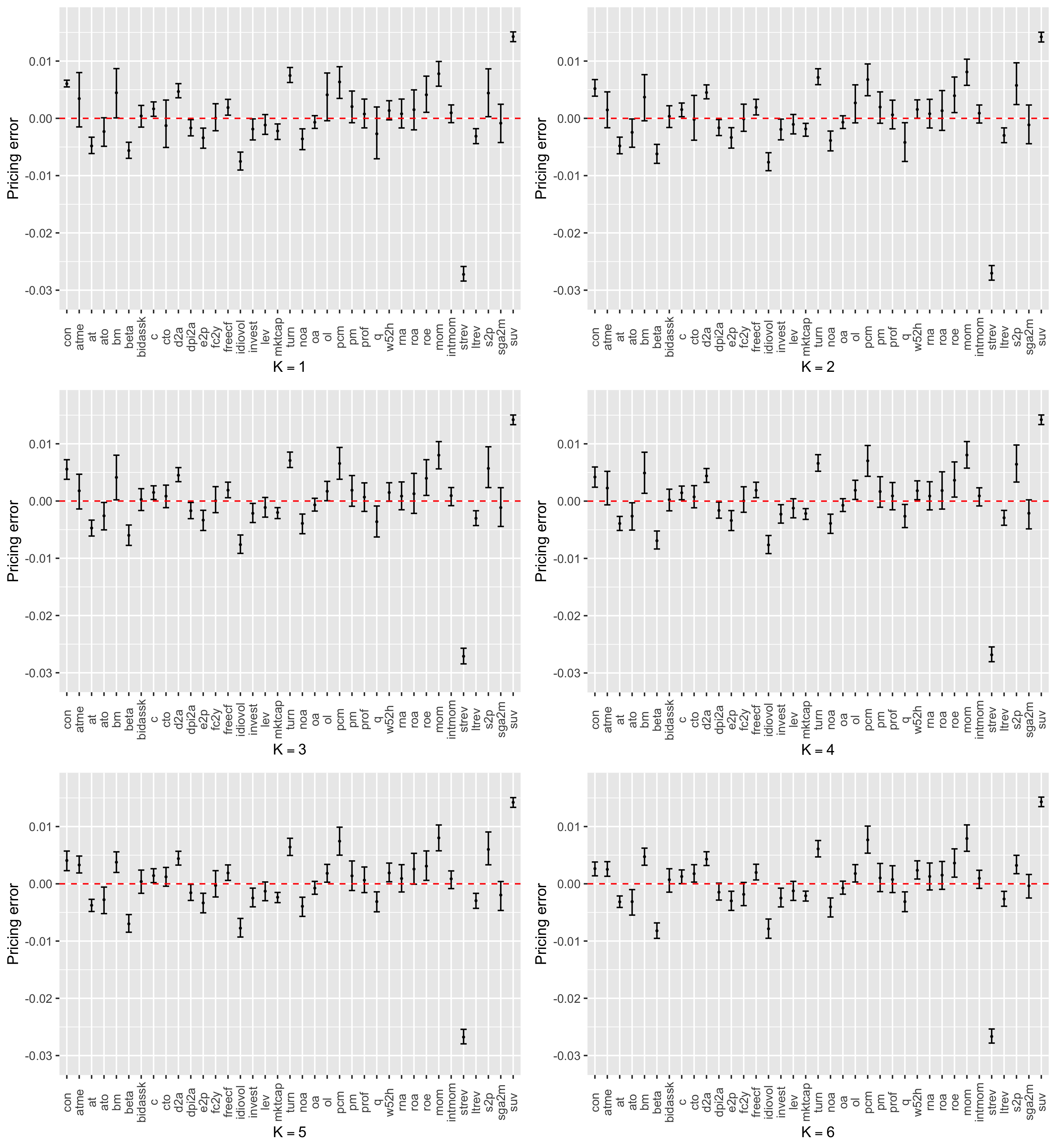

We also examine the estimated contribution of each individual characteristic to the conditional pricing error as we vary the number of factors. In Figure 4, we report the estimates and their associated confidence intervals for the coefficients in the linear specification. We find that increasing the number of factors does not affect the estimates and confidence intervals significantly. This implies that the estimation of is not sensitive to the number of factors, in stark contrast to the estimates of Kellyetal_Characteristics_2019.

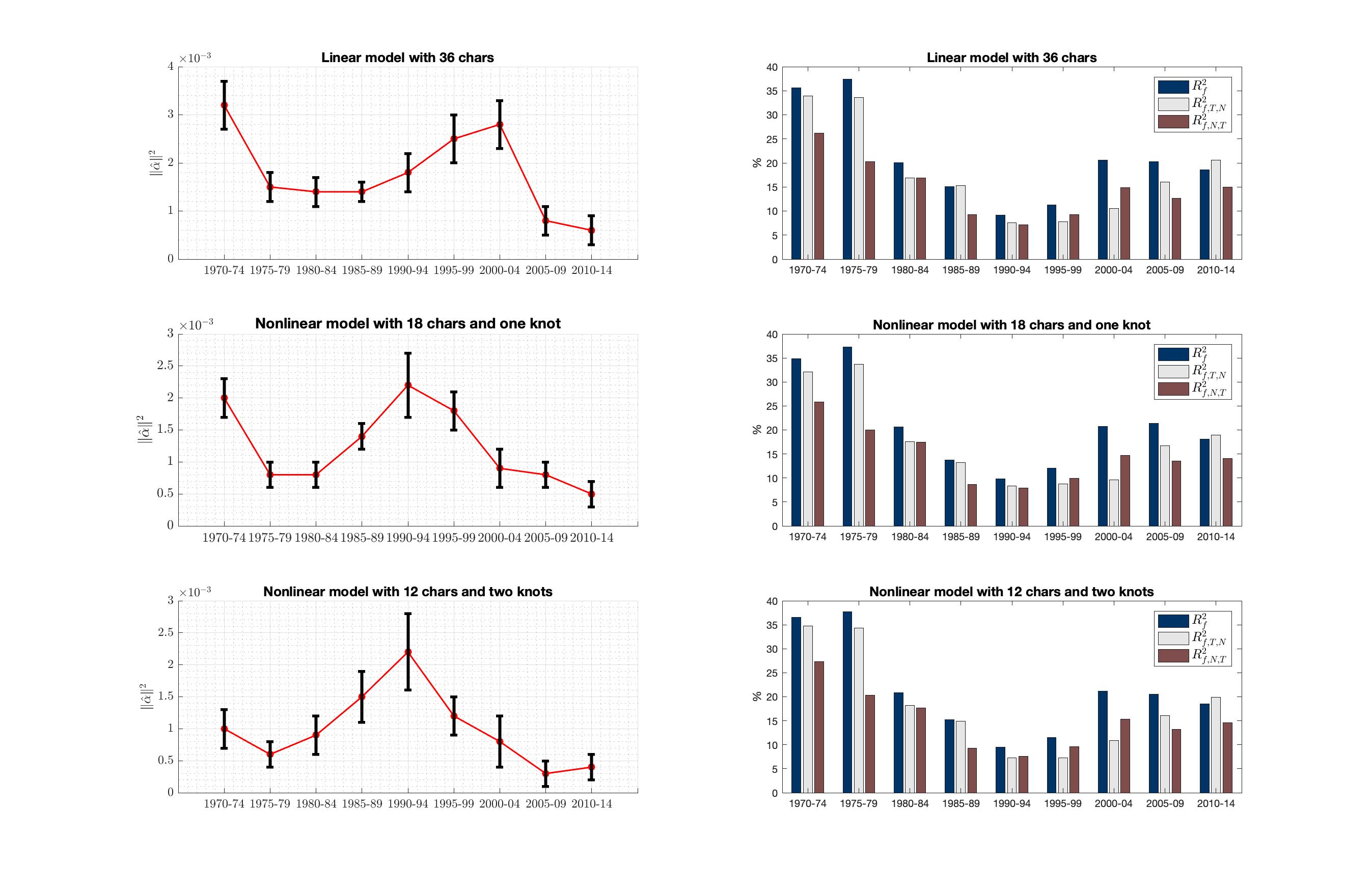

We further estimate the model with ten factors over different subsample periods by dividing the entire sample (starting in January 1970 and ending in May 2014) into five-year intervals. Since our method does not requite a large , we are able to reliably estimate the factor model over such short subsamples. We report the key results from this subsample analysis in Figure 5. As shown in the panels on the left side of the figure, the mispricing errors under nonlinear models are significantly smaller than under the linear model, which is consistent with the findings of strong nonlinearity for model specification. In the linear case, the average squared pricing errors are the highest in the beginning of the sample, in 1970-1974, dropping subsequently, rising over the equity market “boom” period of the 1990s and peaking in the early 2000s, then falling sharply. In the nonlinear cases, the pattern looks a bit different, but in both of the nonlinear specifications the pricing errors spike around 1990-1994, falling afterwards to roughly the same level towards the end of the sample as in the linear case.

The share of both time-series and cross-sectional variation in returns that is attributable to the common factors, as evidenced by the measures reported in the right-side panels of Figure 5, is similar across the different model specifications. More importantly, in Figure 5, we document that all the reported measures decline starting in 1970, reach their trough in the mid-1990s, and then continue to rise until the end of our sample in 2014. This observation is consistent with the findings in Campbell2001have and Campbell2022idiosyncratic: Campbell2001have document that there has been a noticeable increase in firm-level volatility from 1962 to 1997; extending this analysis until the year 2021, Campbell2022idiosyncratic find that the idiosyncratic volatility declined after spiking in 1999-2000.

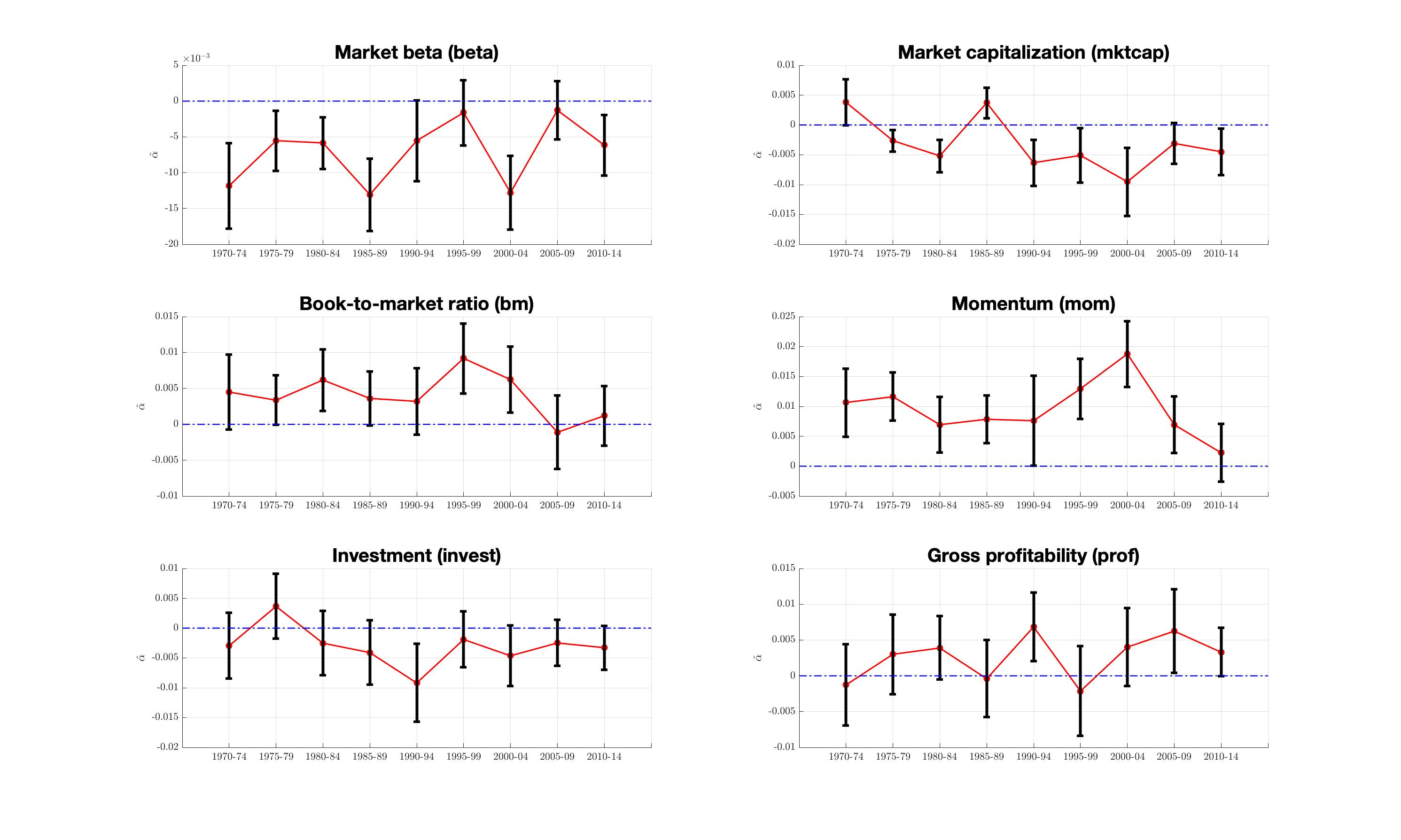

We plot the estimated coefficients with which the characteristics enter the alpha function in different subsample periods with ten factors for six important characteristics under the linear model with 36 characteristics in Figure 6. From the figure, we can conclude that the coefficients for “market capitalization”, “book-to-market ratio” and “momentum” are significantly different from zero in almost all of the subsample periods. The signs of associated coefficients are consistent with the traditional views in FamaFrench_Commonrisk_1993 and FamaFrench_FiveFactor_2015. In parallel with the results in Figure 5, the magnitude of respective coefficients is significantly larger during 1995-2004 compared to other subsample periods, indicating that there is more substantial mispricing associated with these characteristics during that time period. At the same time, the “investment” and “profitability” characteristics are not statistically significantly associated with alpha across different sample periods, suggesting that they capture exposure to common sources of risk.

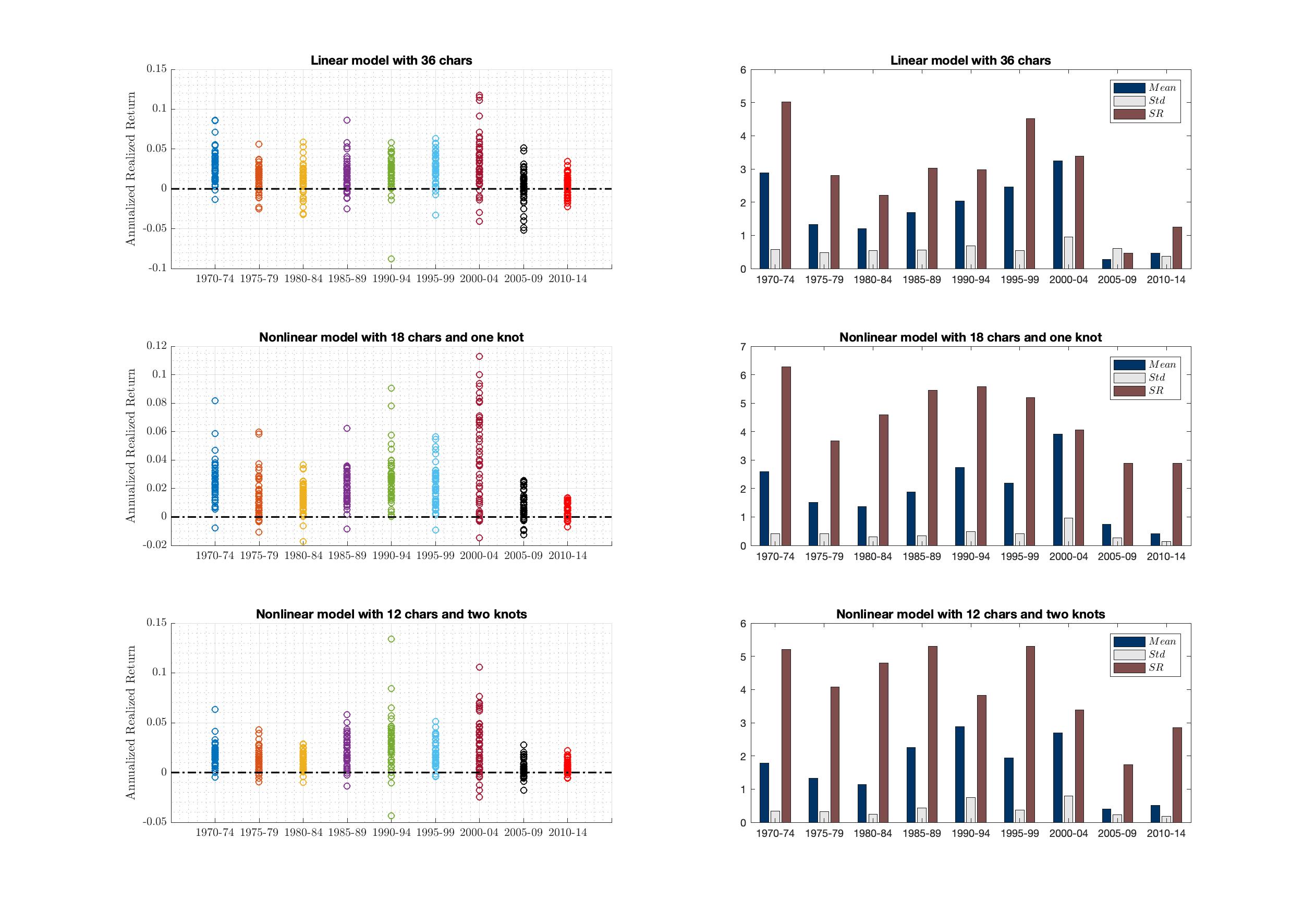

In order to examine the performance of arbitrage portfolios constructed using different subsample periods, in Figure 7, we plot the out-of-sample average annualized excess returns and associated Sharpe ratios of arbitrage portfolios using expanding window estimation starting from the second year in each subsample period. Consistent with the findings in Figure 5, we observe the significant decline of mispricing errors since 2000. From the right panel of Figure 7, we conclude that the decline of arbitrage portfolio Sharpe ratios is due to the decrease of portfolio’s average returns rather than increase in standard deviations.

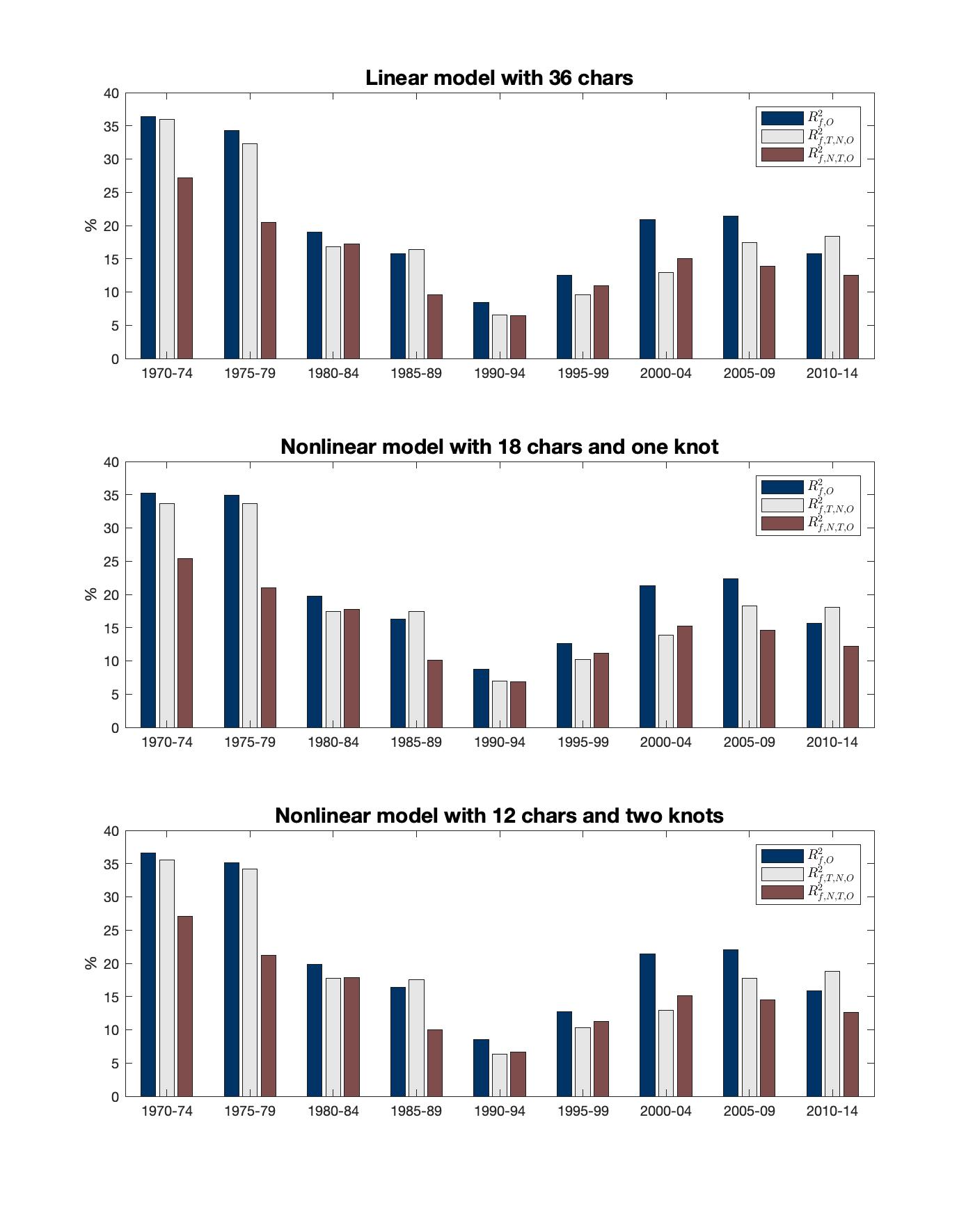

Finally, we assess the out-of-sample fit of the conditional factor model with ten factors in different sample periods; and report the associated results in Figure 8. Overall, the estimated factors are able to explain substantial proportion of cross-sectional variation of individual stock returns out-of-sample, as well as the common time-series variation in returns, but measures of fit vary over time. Similar to Figure 5 discussed above, the findings are consistent with the observation that firm-level volatility increases from 1970 until about 1999 and then decreases, as in Campbell2001have and Campbell2022idiosyncratic. Similarly, the ability of the factor models to explain the cross-section of average stock returns deteriorates between 1980 and mid-1990s, and improves thereafter.

7 Conclusion

In this paper we developed a simple and tractable sieve estimation of conditional factor models with time-varying covariances and latent factors, as well as a weighted-bootstrap procedure for conducting inference on the intercept and factor loading functions. We established large sample properties of the estimators and validity of the tests for large , even when is small. These results enable us to estimate conditional (dynamic) behavior of a large set of individual assets from a number of characteristics exhibiting nonlinearity without the need to pre-specify factors, while allowing us to disentangle the from betas. We applied these methods to explain the cross-sectional differences of individual stock returns in the US market. We found strong evidence of conditional factor structure as well as nonlinearity in conditional and beta functions. Importantly, although only one or two factors are selected by the formal tests, even when a large number of common factors is considered, conditional pricing errors remain large, resulting in arbitrage portfolios with high Sharpe ratios (typically above 3). We also document the significant decline of pricing errors since 2000.

| Unrestricted () | ||||||||||||||||

| Mean | Std | |||||||||||||||

| 26.55 | 2.54 | 1.37 | 0.36 | 2.07 | 0.59 | 0.11 | 6.23 | 3.79 | 5.65 | 1.72 | 0.54 | 3.18 | 0.61 | 0.61 | ||

| 2 | 36.42 | 4.52 | 2.43 | 1.76 | 4.08 | 1.75 | 1.37 | 13.59 | 10.63 | 11.28 | 1.74 | 0.52 | 3.36 | -0.12 | 0.55 | |

| 3 | 45.03 | 5.70 | 3.70 | 2.70 | 5.24 | 2.95 | 2.31 | 14.09 | 11.10 | 11.67 | 1.77 | 0.50 | 3.56 | -0.34 | 0.46 | |

| 4 | 52.55 | 11.69 | 8.55 | 9.27 | 11.28 | 7.92 | 8.69 | 14.74 | 12.15 | 12.11 | 1.77 | 0.47 | 3.74 | 0.02 | 0.44 | |

| 5 | 58.65 | 11.90 | 8.73 | 9.48 | 11.49 | 7.99 | 8.90 | 15.17 | 12.90 | 12.42 | 1.70 | 0.44 | 3.84 | 0.42 | 0.53 | |

| 6 | 64.20 | 13.90 | 10.30 | 11.80 | 13.53 | 9.79 | 11.24 | 15.38 | 13.19 | 12.63 | 1.68 | 0.44 | 3.78 | 0.23 | 0.57 | |

| 7 | 69.15 | 15.59 | 12.23 | 13.76 | 15.23 | 11.71 | 13.23 | 15.62 | 13.32 | 12.87 | 1.63 | 0.44 | 3.73 | 0.60 | 0.68 | |

| 8 | 72.84 | 15.93 | 12.59 | 13.98 | 15.56 | 12.00 | 13.44 | 15.90 | 13.58 | 13.12 | 1.61 | 0.42 | 3.79 | 0.24 | 0.72 | |

| 9 | 76.26 | 16.08 | 12.67 | 14.19 | 15.72 | 12.15 | 13.64 | 16.13 | 13.83 | 13.33 | 1.61 | 0.42 | 3.80 | -0.06 | 0.69 | |

| 10 | 79.15 | 16.23 | 12.82 | 14.35 | 15.87 | 12.34 | 13.80 | 16.29 | 14.06 | 13.47 | 1.60 | 0.42 | 3.82 | 0.11 | 0.67 | |

| 1-10 | 0.54 | 0.64 | 0.21 | |||||||||||||

-

†

: the number of factor specified (∗ denotes the estimated one by our methods); Fama-MacBeth cross sectional regression : ; measures the variations of managed portfolios captured by different numbers of factors from PCA; , , : various in-sample ’s (), see (24)-(26); , , : various in-sample ’s () without , see (27)-(29); , , : various out-sample predictive ’s (), see (30)-(32); , , : various out-sample fits ’s (), see (34)-(36); Mean: out-of-sample annualized means of the pure-alpha arbitrage strategy(); Std: out-of-sample annualized standard deviations of the pure-alpha arbitrage strategy(); : out-of-sample annualized Sharpe ratios of the pure-alpha arbitrage strategy; : out-of-sample annualized Sharpe ratios of the realized -th out-of-sample factor; : out-of-sample annualized Sharpe ratios of the MVE portfolio of out-of-sample factors; and are the p-values of alpha test () and model specification test (joint linearity of and ), separately.

| Unrestricted () | ||||||||||||||||

| Mean | Std | |||||||||||||||

| 1 | 41.61 | 5.94 | 3.47 | 3.60 | 5.52 | 2.99 | 3.11 | 11.27 | 7.81 | 8.93 | 2.46 | 0.69 | 3.54 | 0.51 | 0.51 | |

| 59.05 | 9.56 | 6.17 | 6.91 | 9.18 | 5.67 | 6.33 | 14.04 | 11.31 | 11.29 | 2.39 | 0.57 | 4.22 | 0.18 | 0.53 | ||

| 3 | 64.47 | 10.42 | 6.78 | 7.96 | 10.03 | 6.27 | 7.38 | 14.64 | 11.93 | 11.95 | 2.36 | 0.57 | 4.17 | 0.45 | 0.64 | |

| 4 | 68.99 | 13.83 | 10.26 | 11.52 | 13.40 | 9.80 | 10.90 | 15.44 | 12.98 | 12.54 | 2.19 | 0.53 | 4.12 | 0.85 | 1.04 | |

| 5 | 72.33 | 14.32 | 10.73 | 11.98 | 13.91 | 10.29 | 11.38 | 15.78 | 13.43 | 12.89 | 2.19 | 0.51 | 4.26 | -0.03 | 0.93 | |

| 6 | 75.35 | 14.71 | 10.97 | 12.40 | 14.29 | 10.55 | 11.86 | 16.20 | 14.16 | 13.18 | 1.95 | 0.49 | 3.96 | 1.23 | 1.62 | |

| 7 | 77.63 | 15.28 | 11.78 | 12.99 | 14.84 | 11.27 | 12.42 | 16.45 | 14.34 | 13.37 | 1.90 | 0.48 | 3.93 | 0.45 | 1.66 | |

| 8 | 80.83 | 15.44 | 11.98 | 13.16 | 15.10 | 11.59 | 12.73 | 16.59 | 14.50 | 13.52 | 1.73 | 0.47 | 3.66 | 1.11 | 1.99 | |

| 9 | 82.88 | 15.84 | 12.33 | 13.49 | 15.48 | 11.87 | 13.05 | 16.86 | 14.69 | 13.81 | 1.31 | 0.40 | 3.26 | 1.81 | 2.80 | |

| 10 | 85.61 | 16.39 | 12.89 | 13.93 | 15.71 | 11.80 | 13.14 | 16.98 | 14.72 | 13.86 | 0.88 | 0.28 | 3.14 | 1.72 | 3.33 | |

| 1-10 | 0.59 | 0.64 | 0.28 | |||||||||||||

-

†

: the number of factor specified (∗ denotes the estimated one by our methods); Fama-MacBeth cross sectional regression : ; measures the variations of managed portfolios captured by different numbers of factors from PCA; , , : various in-sample ’s (), see (24)-(26); , , : various in-sample ’s () without , see (27)-(29); , , : various out-sample predictive ’s (), see (30)-(32); , , : various out-sample fits ’s (), see (34)-(36); Mean: out-of-sample annualized means of the pure-alpha arbitrage strategy(); Std: out-of-sample annualized standard deviations of the pure-alpha arbitrage strategy(); : out-of-sample annualized Sharpe ratios of the pure-alpha arbitrage strategy; : out-of-sample annualized Sharpe ratios of the realized -th out-of-sample factor; : out-of-sample annualized Sharpe ratios of the MVE portfolio of out-of-sample factors; and are the p-values of alpha test () and model specification test (joint linearity of and ), separately.

| Unrestricted () | ||||||||||||||||

| Mean | Std | |||||||||||||||

| 1 | 42.78 | 5.57 | 2.98 | 3.32 | 5.19 | 2.54 | 2.83 | 11.08 | 7.57 | 8.77 | 3.29 | 0.99 | 3.33 | 0.54 | 0.54 | |

| 61.36 | 9.56 | 5.97 | 6.87 | 9.18 | 5.51 | 6.26 | 13.85 | 11.12 | 10.99 | 3.01 | 0.80 | 3.78 | 0.47 | 0.70 | ||

| 3 | 67.77 | 10.59 | 6.65 | 7.88 | 10.20 | 6.15 | 7.29 | 14.66 | 12.25 | 11.83 | 2.94 | 0.80 | 3.69 | 0.51 | 0.78 | |

| 4 | 72.86 | 13.62 | 10.09 | 11.35 | 13.17 | 9.64 | 10.67 | 15.39 | 13.53 | 12.53 | 2.97 | 0.78 | 3.81 | -0.18 | 0.59 | |

| 5 | 76.92 | 14.14 | 10.43 | 12.01 | 13.73 | 10.01 | 11.48 | 15.82 | 13.94 | 12.90 | 2.98 | 0.76 | 3.91 | -0.04 | 0.56 | |

| 6 | 80.63 | 14.94 | 11.45 | 12.75 | 14.42 | 10.51 | 12.05 | 16.16 | 14.20 | 13.22 | 1.51 | 0.41 | 3.73 | 2.47 | 2.55 | |

| 7 | 84.29 | 15.17 | 11.59 | 12.94 | 14.76 | 10.77 | 12.447 | 16.57 | 14.59 | 13.57 | 1.01 | 0.33 | 3.09 | 1.87 | 3.20 | |

| 8 | 87.42 | 15.45 | 11.87 | 13.23 | 15.26 | 11.47 | 12.98 | 16.94 | 14.83 | 13.88 | 0.73 | 0.22 | 3.36 | 1.25 | 3.29 | |

| 9 | 89.11 | 16.33 | 12.68 | 13.94 | 16.16 | 12.31 | 13.72 | 17.12 | 15.00 | 14.09 | 0.71 | 0.20 | 3.62 | 0.28 | 3.24 | |

| 10 | 90.72 | 16.54 | 12.91 | 14.17 | 16.38 | 12.54 | 13.95 | 17.30 | 15.19 | 14.29 | 0.69 | 0.18 | 3.90 | 0.23 | 3.19 | |

| 1-10 | 0.57 | 0.57 | 0.27 | |||||||||||||

-

†

: the number of factor specified (∗ denotes the estimated one by our methods); Fama-MacBeth cross sectional regression : ; measures the variations of managed portfolios captured by different numbers of factors from PCA; , , : various in-sample ’s (), see (24)-(26); , , : various in-sample ’s () without , see (27)-(29); , , : various out-sample predictive ’s (), see (30)-(32); , , : various out-sample fits ’s (), see (34)-(36); Mean: out-of-sample annualized means of the pure-alpha arbitrage strategy(); Std: out-of-sample annualized standard deviations of the pure-alpha arbitrage strategy(); : out-of-sample annualized Sharpe ratios of the pure-alpha arbitrage strategy; : out-of-sample annualized Sharpe ratios of the realized -th out-of-sample factor; : out-of-sample annualized Sharpe ratios of the MVE portfolio of out-of-sample factors; and are the p-values of alpha test () and model specification test (joint linearity of and ), separately.

Appendix Appendix A Assumptions

Assumption A.1 (Basis functions).

(i) There are positive constants and such that: with probability approaching one (as ),

where ; (ii) .

Since is a matrix with much smaller than , Assumption A.1(i) can follow from the law of large numbers for finite and its uniform variant for ; see Proposition C.1 for a set of sufficient conditions. The conditions can be easily verified for B-spline, Fourier series, and polynomials basis functions. In particular, we allow to be nonstationary over . When is not changing over , Assumption A.1 reduces to Assumptions 3.3 of Fanetal_ProjectedPCA_2016.

Assumption A.2 (Factor loading functions and factors).

There are positive constants and such that: (i) ; (ii) ; (iii) ; (iv) and for some constant .

Assumption A.2(i) is similar to the pervasive condition on the factor loadings in StockWatson_PCA_2002. Similar assumptions also are imposed in Assumption B of Bai_Inferential_2003 and Assumption 4.1(ii) of Fanetal_ProjectedPCA_2016. For simplicity of presentation, we assume that ’s are nonrandom. Since the dimension of is , Assumption A.2(i) requires . Since the rank of is , Assumption A.2(iii) requires , which implies . These two requirements are not restrictive, since we assume is fixed. Assumption A.2(iv) is standard in the sieve literature. It can be easily satisfied by using B-spline or polynomials basis functions under certain smoothness of and ; see, for example, Lorentz_Approximation_1986 and Chen_Handbook_2007.

Assumption A.3 (Data generating process).

(i) is independent of ; (ii) for all and ; (iii) there is such that

Assumption A.3(iii) requires to be weakly dependent over both and , and is commonly imposed for high-dimensional factor analysis; see, for example, StockWatson_PCA_2002, Bai_Inferential_2003, and Fanetal_ProjectedPCA_2016. When is not changing over , Assumption A.3 reduces to Assumptions 3.4 (i) and (iii) of Fanetal_ProjectedPCA_2016.

Assumption A.4 (Intercept function).

and for some .

Assumption A.4 is needed for the identification of . Similar assumption is imposed in Connoretal_EfficientFFFactor_2012 and Assumption 3.1(i) of Kimetal_Arbitrage_2019.

Assumption A.5 (Rate of convergence).

(i) ; (ii) , where ; (iii) are independent across ; (iv) there is such that

and

Assumptions A.1-A.4 allow us to establish a preliminary rate of the estimators in Theorem C.1. Assumption A.5 is an additional assumption that we need to establish a fast rate in Theorem 3.1. Assumption A.5(i) strengthens Assumption A.1(ii). Assumption A.5(ii) requires that the second moment matrix is bounded and nonsingular for all and , which is widely used in the sieve literature; see, for example, Newey_SeriesEstimator_1997 and Huang_Series_1998. Assumption A.5(iii) is commonly imposed in the sieve literature, which is used to justify the asymptotic convergence of . Assumption A.5(iv) allows for weak dependence of over both and . The second condition is similar to the second condition in Assumption A.3(iii); both are satisfied if is bounded.

Assumption A.6 (Asymptotic distribution).

(i) has distinct eigenvalues; (ii) are independent across ; (iii) there is such that

Assumption A.6 is needed in Theorem 3.2. The distinct eigenvalue condition in Assumption A.6(i) is necessary to establish the asymptotic normality, as known in the literature; see, for example, Bai_Inferential_2003 and ChenFang_ImprovedInference_2017. Assumption A.6(ii) imposes independence of across for simplicity.777This assumption allows us to use the Yurinskii’s coupling. In fact, we may relax this assumption and alternatively use LiLiao_NonparametricTimeSeries_2019’s coupling, so that the dependence across can be allowed. However, it is challenging to develop an inference procedure allowing the dependence over both and . Therefore, we stick with this assumption. Assumption A.6(iii) allows for weak dependence of over .

Assumption A.7 (Bootstrap).

(i) is a sequence of independently and identically distributed positive random variables with and , and is independent of ; (ii) there are positive constants and such that: with probability approaching one (as ),

where ; (iii) .

Assumption A.7 is needed in Theorem 4.1. Assumption A.7(i) defines the bootstrap weight for each . Since is a matrix with much smaller than , Assumption A.7(ii) can follow from the law of large numbers for finite and its uniform variant for , similar to Assumption A.1(i). Assumption A.7(iii) requires nonsingularity of the variance-covariance matrix .

Assumption A.8 (Specification test).

(i) There are positive constants and such that: with probability approaching one (as ),

(ii) ; (iii) ; (iv) with probability approaching one (as ),

(v) and .

Assumption A.8 is needed in Theorem 4.2. Assumptions A.8(i)-(iv) are analogous to Assumptions A.1(i), A.5(i), (ii) and A.7(ii), respectively. When is included as a part of , which is true in the case of polynomial basis functions, the former are implied by the latter ones. In this case, Assumptions A.8(i)-(iv) thus are redundant.

Assumption A.9 (Determination of ).

(i) ; ii) there is such that

Assumption A.9 is needed in Theorem 5.1(i). Assumption A.9(i) requires that the covariance matrix is bounded and nonsingular for all . In particular, allows for weak dependence of across . When are independent across , the condition is satisfied when and . Assumption A.9(ii) allows for weak dependence of over both and ; see Proposition C.2 for a set of sufficient conditions.

Appendix Appendix B Proofs of Main Results

Proof of Theorem 3.1: Let us begin by defining some notation. For and , let . Let and . Then (9) can be written as

| (38) |

where denote a vector of ones. Recall . Post-multiplying (38) by to remove , we thus obtain

| (39) |

Let be a diagonal matrix of the first largest eigenvalues of . By the definitions of and , and . Thus, and . We may substitute (39) to to obtain

| (40) |

where , , , and . By the definition of ,

| (41) |

where is well defined with probability approaching one by (C.1) and Lemma F.2(ii), and we have used and . Noting , we may substitute (38) to to obtain

| (42) |

where is well defined with probability approaching one by (C.1) and Lemma F.2(ii), and we have used . Theorem C.1 provides a preliminary rate of , and by using rough bounds based on (40)-(42). To improve the rate of , we need to treat in as (40) a whole to establish its rate. By the Cauchy-Schwartz inequality and the fact that and , (40) implies

| (43) |

where the equality follows by , Lemmas F.1(i)-(iv), F.2(i) and F.6(ii) and the fact that . Given the rate of in (Appendix B), the rate of immediately follows from the same argument in (C.1). To improve the rate of , we need to plug in the expansion of to (Appendix B), and treat , , and as a whole to establish their rates. By the fact that and , combining (40) and (42) implies

| (44) |

where the equality follows by , Assumptions A.2(ii) and A.4, Lemmas F.1(i)-(iii), F.2, F.3(i), F.6 and F.7(i) and the fact that . Thus, the third result of the theorem follows from (Appendix B). The proofs of the last two results of the theorem are similar to the proofs of the last two results of Theorem C.1.∎

Proof of Theorem 3.2: Let us first look at (Appendix B). The asymptotic distribution can be obtained by choosing large and assuming not too large such that the terms with and are negligible relative to the term with . Thus, the asymptotic distribution is determined by the term with . Specifically, by the fact that and , (40) implies

| (45) |

where the equality follows by , Lemmas F.1(i)-(iii), F.2(i) and F.6(ii) and the fact that . Let . Since , . By the fact that , combining (Appendix B) and Lemma F.13 implies

| (46) |

Note that is a matrix from the last columns of . Thus, the second result of the theorem follows from (46) and Lemma F.14. We now look at (Appendix B). By the fact that , it implies

| (47) |

where the equality follows by Lemma F.3(i). Given the rate of in Theorem 3.1 and the rate of in Lemma F.4(ii), we may replace all except those in with to obtain

| (48) |

by noting that and . Similarly, given the rate of in Lemma F.15, we may replace all except those in with to obtain

| (49) |

Let . Given the rate of in Lemma F.13, we may replace with to obtain

| (50) |

by noting that . The arguments in (Appendix B)-(Appendix B) are similar to those for the first result in Lemma F.13. Note that is a vector from the first column of . Thus, the first result of the theorem follows from (Appendix B), Lemma F.14 and the second result of the theorem. ∎

Proof of Theorem 4.1: Let us begin by defining some notation. For and , let . Let and . Then we have

| (51) |

where denotes a vector of ones. Recall . Post-multiplying (51) by to remove , we thus obtain

| (52) |

Recall that us a diagonal matrix of the first largest eigenvalues of as defined in the proof of Theorem 3.1, and as showed in the proof of Theorem 3.1. By the definitions of , . We may substitute (52) to it to obtain

| (53) |

where in the first equality we have used and , in the second equality we have substituted (39) into the equation, and , , , , and . We can conduct the same exercise as in (Appendix B) to obtain

| (54) |

where the equality follows by , Lemmas F.18 and F.2(i). Let . Since , . By the fact that , combining (Appendix B) and Lemma F.19 implies

| (55) |

Let . Note that . By the fact that , we now may combine (46) and (55) to obtain

| (56) |

Note that is a matrix from the last columns of . Thus, the second result of the theorem follows from (56) and Lemmas F.5 and F.20. We now show the first result of the theorem. By the definition of ,

| (57) |

where is well defined with probability approaching one by (C.1) and Lemma F.2(ii), and we have used and . Let . By a similar argument as in (Appendix B)-(Appendix B), we have

| (58) |