The integrated copula spectrum

Abstract

Frequency domain methods form a ubiquitous part of the statistical toolbox for time series analysis. In recent years, considerable interest has been given to the development of new spectral methodology and tools capturing dynamics in the entire joint distributions and thus avoiding the limitations of classical, -based spectral methods. Most of the spectral concepts proposed in that literature suffer from one major drawback, though: their estimation requires the choice of a smoothing parameter, which has a considerable impact on estimation quality and poses challenges for statistical inference. In this paper, associated with the concept of copula-based spectrum, we introduce the notion of copula spectral distribution function or integrated copula spectrum. This integrated copula spectrum retains the advantages of copula-based spectra but can be estimated without the need for smoothing parameters. We provide such estimators, along with a thorough theoretical analysis, based on a functional central limit theorem, of their asymptotic properties. We leverage these results to test various hypotheses that cannot be addressed by classical spectral methods, such as the lack of time-reversibility or asymmetry in tail dynamics.

keywords:

[class=MSC]keywords:

, and

1 Introduction

Spectral methods always have been central in the analysis of time series and remain (see von Sachs, (2020) for a recent review) a very active domain of methodological and applied statistical research. Their applications are without number, ranging from econometrics and finance (with classical monographs such as Granger and Hatanaka, (2015)) to geophysics (Likkason,, 2011), fluid mechanics (Lange et al.,, 2019), environmetrics, and climate change (Ghil et al.,, 2002).

Powerful as they are, classical spectral methods, however, suffer from the significant limitations inherited from their nature: being covariance-based, they fail to capture important distributional features such as dependence without correlation (as typically observed in financial returns), time-irreversibility, asymmetric dependence between high and low quantile values, or higher-order dynamics. This has motivated, in the past decades, a rich strand of literature replacing covariances with alternative measures of dependence related to joint distributions, copulas, and characteristic functions. Pioneering contributions in this direction were made by Hong, (1999), who proposes a generalized characteristic function-based concept of spectral density. In the specific problem of testing pairwise independence (rather than pairwise non-correlation), Hong, (2000) introduces a test statistic based on spectra derived from joint distribution functions and copulas at different lags. More recent contributions introduce the notions of Laplace, quantile-based, and copula spectral densities and spectral density kernels, involving various quantile-related spectral concepts, along with the corresponding sample-based (smoothed) periodograms. That strand of literature includes Li, (2008, 2012, 2013), Hagemann, (2013), Dette et al., (2015); Kley et al., 2016a and Lee and Rao, (2012). Extensions to locally stationary and multivariate time series are considered in Birr et al., (2017) and Baruník and Kley, (2019), respectively. An analysis of related concepts under long-range dependence can be found in Lim and Oh, (2021). The utility of quantile and copula spectra for model building and model assessment is demonstrated in Birr et al., (2019) and Li, (2021), while an application of quantile- and copula-based spectral techniques to the analysis of cryptocurrency returns can be found in Su et al., (2021). An extension of these concepts to the analysis of extreme events, which is related in spirit but different in many other respects, was considered by Davis et al., (2013). Finally, in the time domain, Linton and Whang, (2007), Davis and Mikosch, (2009), and Han et al., (2014) introduced the related concepts of quantilograms and extremograms.

Unfortunately, despite many attractive properties, spectral densities—whether traditional or generalized—in practice suffer from several drawbacks; among them, the need to choose a smoothing parameter to ensure consistent estimation and a lack of process convergence of the resulting estimators when indexed by frequencies. The latter makes it challenging to use them for inferential purposes such as testing for specific time series features.

In the classical world, this drawback has motivated the recourse to spectral distribution functions resulting from the integration of the spectral density over frequencies. In contrast to spectral densities, such integrated spectra can be estimated without the need for smoothing. Estimation of along with process convergence of the resulting estimators under increasingly general conditions was discussed in Grenander and Rosenblatt, (1957), Ibragimov, (1963), Brillinger, (1969), Dahlhaus, (1985), and Anderson, (1993) among others. Applications of this process convergence to various testing problems are provided in Priestley, (1987), Section 6.2.6 and Anderson, (1993). An extension to related processes indexed by more general classes of functions is considered in Dahlhaus, (1988); Mikosch and Norvaiša, (1997). Integrated versions of certain normalized periodograms were also studied in Klüppelberg and Mikosch, (1996) under various tail assumptions (including the infinite-variance case) on the underlying time series and extended to long-memory processes in Kokoszka and Mikosch, (1997).

The aim of the present paper is to combine the attractive features of copula–based spectra with the theoretical merits of spectral distributions. To this end, we define the copula spectral distribution function, which arises from integrating copula spectral densities over frequencies. We provide estimators which are based on partial sums of copula periodograms and do not require the choice of smoothing parameters.

The remaining paper is organized as follows. Copula spectral distribution functions are formally defined in Section 2 where their estimation is also discussed. Weak convergence (as stochastic processes) of the estimators from Section 2 is established in Section 3. Section 4 shows how this process convergence can be combined with sub–sampling to construct uniform confidence bands for integrated copula spectra and test various hypotheses about the underlying time series. Section 5 demonstrates the finite-sample properties of the methodology from Section 4 in an extensive simulation study. All proofs and additional simulation results are deferred to a series of Appendices.

2 Integrated copula spectra – definition and estimation

In what follows, let denote a strictly stationary real-valued time series. Denote by the marginal distribution function of and by the corresponding quantile function. As argued in Dette et al., (2015); Kley et al., 2016a , a natural way to capture the nonlinear dynamics of is the analysis of its copula spectral density

| (1) |

where ,

and denotes the copula of the random vector ; here denotes the indicator function of . To ensure the existence of , it suffices to assume that the are absolutely summable over for each pair , which we throughout implicitly assume. As shown in Dette et al., (2015); Kley et al., 2016a ; Birr et al., (2019), copula spectral densities enjoy many attractive properties; see also Li, (2013, 2021) for similar findings in the setting of Laplace spectra. They exist without any moment assumptions, are invariant under strictly increasing marginal transformations (hence are scale–free), and provide a complete characterization of the pairwise copulas—hence the pairwise dependencies—of the series at arbitrary lags. The last point is in stark contrast to classical spectral densities which are unable to capture many important properties of time series such as lack of time-reversibility, conditional heteroscedasticity, or asymmetry between upper- and lower-tail dynamics.

Yet, despite their flexibility, copula spectral densities are sharing with the traditional ones an important practical drawback: the choice of a smoothing parameter is required to obtain consistent estimators. Selecting this smoothing parameter is difficult in practice and poses substantial challenges for inference. Indeed, larger bandwidths lead to smaller variance but larger (asymptotic) bias and the exact amount of bias depends on unknown smoothness properties of the underlying copula spectral density. The need for local smoothing also leads to difficulties in obtaining results that hold uniformly in frequencies (more formally, no process convergence is possible). This poses a major roadblock for subsequent inference procedures. We note that those drawbacks are not limited to copula spectral densities but also appear in the estimation of classical, –based spectral densities.

Motivated by the above discussion, we propose to consider copula spectral distribution functions which are defined as

| (2) |

Copula spectral distributions inherit the virtues of copula spectral densities and are conveying the same information; at the same time, their estimation (as discussed below) does not involve the choice of smoothing parameters, and process convergence can be established in quantile levels and frequencies simultaneously (see Theorem 3.1 below).

Before proceeding to estimation, let us provide two examples of hypotheses about time series dynamics that can be conveniently formulated and tested through the use of spectral distribution functions.

Example 2.1.

Testing for time-reversibility. A strictly stationary process is called pairwise time-reversible at lag iff . A process is pairwise time-reversible if it is time-reversible for all lags . Determining if data can be modeled as a time-reversible process has important consequences for subsequent modeling: testing for time-reversibility therefore has attracted substantial interest in the literature—see Brillinger and Rosenblatt, (1967) for an early contribution, and chapter 8 in De Gooijer, (2017) for an overview. Copula spectral distribution functions provide a natural way of assessing time-reversibility since a process is pairwise time-reversible if and only if the imaginary part of the corresponding spectral distribution function is uniformly zero:

We will leverage this property of spectral distribution functions in Section 4.2 to construct a test that has power against the lack of (pairwise) time-reversibility at specified or unspecified lag.

Example 2.2.

Assessing symmetry of tail dynamics. It is well known that financial time series exhibit asymmetric dependence structures in left- and right-hand tails, respectively—see Jondeau and Rockinger, (2003), Li, (2021), among many others. Copula spectral distributions provide a natural model-free way to access this kind of asymmetry in tail dynamics. From a distributional perspective, asymmetry in tail dynamics corresponds to asymmetry in the lag- copula of for some lag : if

for small values of , then the tail behavior of is asymmetric. Copula spectral distributions provide a natural way of assessing this type of asymmetry since

for all is equivalent to

for all . A more formal discussion of the corresponding null hypothesis and testing procedure is provided in Section 4.3

We next discuss estimation. Recall the definition (Kley et al., 2016a, ) of the copula rank periodogram (in short, the CR periodogram):

| (3) |

with

| (4) |

As shown in Kley et al., 2016a , the vector is approximately multivariate complex normal with expected values and independent entries; see Proposition 3.4 in there for a formal statement. This motivates, for the copula spectral distribution function, the estimator

| (5) |

Observe that, in contrast to the copula spectral density estimators considered in Kley et al., 2016a , no smoothing parameter is required. In addition, as we shall show in Section 3, this estimator converges as a process in all three arguments when properly centered and scaled. This makes it a very attractive choice for testing various hypotheses about distributional dynamics of the underlying time series.

3 Asymptotic theory

This section is devoted to proving process convergence of the estimator after proper centering and scaling. We begin by stating the main technical conditions which are needed to establish this result.

Assumption 3.1.

-

(S)

The real-valued process is strictly stationary; the marginal distribution of is continuous.

-

(C)

There exist constants and such that, for arbitrary intervals of and arbitrary ,

(6) -

(D)

The partial derivatives of the function

(7) exist and are continuous for .

Remark 3.1 (Discussion of assumptions).

Assumption (C) places restrictions on the strength of time dependence in . This assumption also appears in the asymptotic analysis by Kley et al., 2016a of copula spectral densities. In particular, Kley et al., 2016a show that (6) is implied by several standard assumptions such as exponential - and -mixing. The same reference also shows that processes satisfying some geometric moment contraction properties defined in Wu and Shao, (2004) fulfill Assumption (C).

Condition (D) is needed to quantify the effect of estimating the marginal cdf by its empirical version . The derivatives of also appear in the covariance kernel of the limiting process.

In the following Lemma we show that Assumption (D) is satisfied for strictly stationary centered Gaussian processes with absolutely summable pairwise copula cumulants. The details of the proof are deferred to Section A.

Lemma 3.1.

Let be a stationary centered Gaussian process with auto–covariances where for and . Then the partial derivatives of the function exist and are continuous on the set .

In order to state our main result we need some additional notation. Define the copula spectral density of order as

with the copula cumulant function of order

for . We are now ready to state our main result—process convergence of the properly centered and scaled estimator . Applications of this result to inference will be discussed in the following sections.

Theorem 3.1.

Let Assumptions 3.1 hold. Then, for any , the process

| (8) |

converges weakly to the centered Gaussian process with covariance structure

| (9) |

that is, where denotes weak convergence, as , with respect to the uniform metric in the space . Moreover, the paths of the process are asymptotically uniformly equicontinuous with respect to any norm on .

Let us briefly compare this result with related results in the literature. Similarly to estimators of spectral distribution functions, we obtain process convergence in with a convergence rate. However, in contrast to the results in that literature, we have two additional parameters and we also obtain process convergence in these, which calls for completely different proofs.

Spectral distribution functions without marginal normalization are considered in Hong, (2000). The latter author establishes process convergence in and two parameters which play a similar role as our quantile levels assuming that the time series is a collection of i.i.d. data. This considerably simplifies the entire analysis and the proof technique used there does not extend to the case of general serial dependence. In addition, our analysis differs since we consider marginal normalization by estimating the marginal distribution function, something which is not covered by the results of Hong, (2000), even in the special case of i.i.d. observations.

Finally, we provide a comparison with corresponding results for the estimation of copula spectral densities as discussed in Kley et al., 2016a . There are several key differences in the form of the final result and the resulting theoretical analysis. First, observe that Theorem 3.1 provides process convergence of the integrated copula spectral densities in the quantile levels as well as the frequencies . This is in contrast to the copula spectral densities (1) considered in Kley et al., 2016a where only process convergence in the quantile levels is obtained. This is the case also for autocovariance-based spectral densities—due to the fact that the limiting processes, for distinct frequencies, are mutually independent, so that no tight element with the right finite-dimensional distributions exists in [see Remark 3.5 in Kley et al., 2016a ]. Second, we obtain an convergence rate, which is strictly faster than the rates obtained in Kley et al., 2016a for any permissible bandwidth choice. This is due to the need for local smoothing when estimating copula spectral densities, and similar phenomena also occur in the context of spectra and “classical” kernel density estimation. Third, as discussed in more detail in Remark 3.2, the limiting covariance in Theorem 3.1 has several terms that are due to empirical normalization of the margins. Such terms do not appear in the limiting process when estimating copula spectral densities because the effect of marginal standardization there is negligible relative to the convergence rate of the estimator with known margins. The fact that we need to account for such terms in our limit considerably complicates our asymptotic analysis compared to the developments in Kley et al., 2016a .

Remark 3.2 (A sketch of the proof).

The proof of Theorem 3.1 is long and technical; deferring details to the online supplement, we only outline here the main steps.

(a) A key ingredient is the weak convergence of the process

where denotes the (infeasible) oracle estimator where the empirical distribution function in is replaced by . We show that this process converges, in , to a centered Gaussian process with covariance structure

(b) Utilizing uniform asymptotic equicontinuity in probability of along with a Taylor expansion of the spectral distribution function , we obtain the stochastic representation

as , where the remainder is uniform in .

(c) The remaining part of the proof is devoted to establishing process convergence of the leading term in this representation. The sum captures the impact of estimating the marginal distribution function by its empirical counterpart. This expression also explains the additional terms in the covariance function of when compared to that of . Such additional terms also appear in the limiting distribution of empirical copula processes [see, for instance, Fermanian et al., (2004) or Segers, (2012)]. However, they do not appear in the estimation of copula spectra in Kley et al., 2016a because the convergence speed of the estimator there is strictly slower than .

4 Subsampling-based inference

Theorem 3.1 is a very powerful instrument allowing us to perform copula spectral analysis in a broad range of practical problems. Deriving valid procedures for inference, however, crucially depends on the limit process in Theorem 3.1—that is, on the covariance kernel defined in (3.1). This covariance kernel in turn depends on second-, third-, and fourth-order copula spectra and some partial derivatives of the function defined in (7). While for some testing problems (e.g., under the null hypothesis of serial independence: cf. Hong, (2000)) these quantities simplify substantially, they are quite difficult to estimate in general. In this section, we demonstrate how subsampling methods (Politis et al.,, 1999) yield feasible and asymptotically valid confidence bands and tests for time-reversibility [Example 2.1] and asymmetry of tail dynamics [Example 2.2].

A key quantity in all subsampling procedures described in this section is the estimator

| (10) |

of computed from the subsample , where

| (11) |

with

| (12) |

The block length is an integer between 1 and ; for our asymptotic results to hold, we will choose it such that and as .

4.1 Constructing uniform confidence bands

We now describe how asymptotically valid confidence bands can be obtained via subsampling. We will consider two types of confidence bands: (a) bands that are uniform in for fixed quantile levels and (b) bands that are uniform in all three arguments .

By Theorem 3.1 and the Continuous Mapping Theorem,

in , as . Further, for any continuous weight function that is bounded away from , we have

in distribution, as .

For the construction of an asymptotically valid -confidence band for , it is sensible to proceed as follows. We require

to satisfy

For a uniform-in- confidence band for fixed , choose and, for a uniform-in- confidence band, choose . The use of the weighting function improves the uniform confidence intervals by allowing the width to depend on ; cf. Neumann and Paparoditis, (2008). These confidence bands are (asymptotically) valid if and are the quantiles of the (limit) distributions of and , respectively. In practice, neither these distributions nor their limits are analytically tractable and we therefore propose the following subsampling-based intervals.

The -confidence band that is uniform in for fixed is defined by

| (13) |

where

with

| (14) | ||||

| (15) |

Note that is the empirical -quantile of

scaled by a factor . Intuitively, the proposed interval will be asymptotically valid, because the distributions of and converge to the same limit and the distribution of is well approximated by the empirical distribution .

The factor in (15) is an optional finite-population correction and can be replaced by any sequence converging to one. Such correction is recommended by Politis et al., (1999); our simulations in Section 5 below indicate that it is indeed quite advisable in this context. As for , a positive integer, it is typically chosen such that

which facilitates the evaluation of the estimates.

Similarly define the uniform-in- -confidence band as

| (16) |

where

with

where , the role of which will be made clear in the sequel, is a sequence of finite subsets of the interval .

Uniform confidence intervals and for the imaginary parts are defined in the same way, with real parts replaced by imaginary parts.

We now state a result that ensures correct asymptotic coverage for the subsampling-based confidence bands just defined.

Theorem 4.1.

Let the assumptions of Theorem 3.1 hold and assume moreover that is -mixing such that as . Assume that and as . Then, for the confidence band defined in (13),

as . Further, assuming that

| (17) |

for some , we have, for the confidence band defined in (16),

as . The same results hold for the bands for imaginary parts .

4.2 Testing for time-reversibility

An important feature that cannot be captured by second-order moments, hence escapes traditional spectral analysis, is time-(ir)reversibility. Time-irreversibility in time series is the rule rather than the exception (see e.g. Hallin et al., (1988)); it is ubiquitous in some applications such as financial econometrics. Yet, due to the fact that , most classical time-series models generate time-reversible processes while classical spectral analysis, being second-order-based, is unable to detect time-irreversibility. Copula-based spectral methods can.

Let the stochastic process satisfy Assumption 3.1; denote by its copula spectral density, by , , its marginal bivariate distributions. We say that the process is pairwise time-reversible if, for all , the distributions of and coincide, i.e., for all . The following characterization has been established by Dette et al., (2015).

Proposition 4.1.

The process is pairwise time-reversible if and only if

A test for (pairwise) time-reversibility thus is a test of the null hypothesis

| (18) |

with alternative

It follows from Proposition 4.1 that in (18) also can be written as

| (19) |

for arbitrarily small where for some . The function is essential to construct the critical region uniformly in (see the discussion in Section 4.1). Consider the test statistic (for testing against )

| (20) |

The next result is an immediate consequence of Theorem 3.1.

Proposition 4.2.

In actual calculations, needs to be discretized, and we compute it as

| (22) |

where denotes a sequence of discrete sets the exact choice of which will be discussed in more detail in Section 5. In our theoretical analysis, we will assume that there exists a sub-set such that

| (23) |

Asymptotic –values for this test can be determined based on subsampling: let

where

with defined in (10) denoting the subsampled version of on theblock of length . The validity of this subsampling procedure is discussed in the next theorem.

Theorem 4.2.

Remark 4.1.

We also considered the subsampled statistic

but this did not yield better results in simulations.

4.3 Assessing asymmetry in tail dynamics

Assessing asymmetry in tail dynamics is of critical importance for, e.g., risk management and investment strategy. Value at risk (VaR) and expected shortfall (ES) are popular risk measures in finance that are related to quantiles. According to Jondeau and Rockinger, (2003), investors suspect that the left tail of stock returns is heavier than the right one. And Li, (2021) pointed out asymmetry between lower quantiles and upper quantiles for the S&P500 index. As for copula-based modeling, asymmetry between upper and lower quantiles excludes families of (radially) symmetric copulas such as Gaussian and -copulas. Misspecified copulas lead to false conclusions and involve grave risks (Rosco and Joe, (2013); Mangold, (2017)). Hence, the investigation of tail behavior is important. Further discussions can be found in So and Chan, (2014) and Krupskii and Joe, (2019).

Denote by the lag– copula of for some lag . We are interested in the case where

for some : the copula then is called tail asymmetric at a level . This is not the case when for all and all , where : then we say that the copula is pairwise tail-symmetric at level . Note that tail symmetry boils down to radial symmetry when it holds that

for all , see e.g. Nelsen, (2006, p.36-p.38). We call a process pairwise tail-symmetric at level if the copula of is tail-symmetric at a level for all .

A test for (pairwise) tail symmetry of at given level is a test of the null hypothesis

| (24) |

against the alternative

The null hypothesis can be rewritten as

Hence, the following proposition holds true.

Proposition 4.3.

The process is pairwise tail-symmetric at level if and only if

In view of Proposition 4.3, we also consider the following hypothesis, which is slightly weaker than (24): for arbitrary small such that ,

| (25) |

where for some . For testing against , define

| (26) |

The next result then is an immediate consequence of Theorem 3.1.

Proposition 4.4.

In practice, a discretisation

| (27) |

of is required, where the sequence is such that

| (28) |

The -value of the resulting test for (pairwise) tail symmetry is

where

with defined in (10). The next theorem establishes the properties of the testing procedure based on .

Theorem 4.3.

5 Simulations

This section illustrates the finite-sample performance of the methods proposed in Sections 4.1–4.3. We consider a range M0-M15 of fifteen models, which we describe in detail in the Appendix. These models include linear and nonlinear ones, Gaussian and non-Gaussian ones, models with serial independence, weak serial dependence, and stronger serial dependence. Table 1 lists the main features of these models. The R package quantspec (Kley,, 2016) was used for all simulations.

| model | time | tail | short | ||

| -reversibility | symmetry | description | |||

| M0 | i.i.d. Gaussian | ||||

| M1 | ✓ | ✓ | QAR(1) (Koenker and Xiao,, 2006) | ||

| M2 | AR(2) (Li,, 2012) | ||||

| M3 | ✓ | ARCH(1) (Lee and Rao,, 2012). | |||

| M4 | ✓ | GARCH(1,1) (Birr et al.,, 2019) | |||

| M5 | ✓ | ✓ | EGARCH(1,1,1) (Birr et al.,, 2019) | ||

| M6a–c | AR(1) with Gaussian innovation | ||||

| M7a–c | ✓ | AR(1) with Cauchy innovation | |||

| M8a–g | ✓ |

|

|||

| M9a–g | ✓ |

|

|||

| M10a–g | ✓ | the modified models M8a–g | |||

| M11a–g | ✓ | the modified models M9a–g | |||

| M12a–c | ✓ |

|

|||

| M13a–c | ✓ |

|

|||

| M14 | ✓ |

|

|||

| M15 | ✓ |

|

5.1 Confidence bands

In this subsection, models M0-M7 from Table 1 are used to study the empirical coverage111Throughout, with a slight abuse of language, we write “coverage probability” instead of “coverage frequency” in order to avoid confusion with . of the confidence bands described in Section 4.1. We consider and, for each (choosing powers of 2 for allows for quick computation of the CR periodograms), ; as a rule of thumb, we selected

| (29) |

yielding for , respectively. As for the Fourier frequencies in (15), we put .

We simulated independent series for each configuration. For each of them, we computed the confidence band as explained in Section 4.1. To obtain their empirical coverage, we compare them with the actual value of the integrated copula spectral density. The latter can be computed precisely for M0; else, it was obtained from simulated CR periodograms.

The finite-population correction in (15) was applied; without it, the results (not shown here) are significantly worse: the correction, thus, is essential in numerical applications.

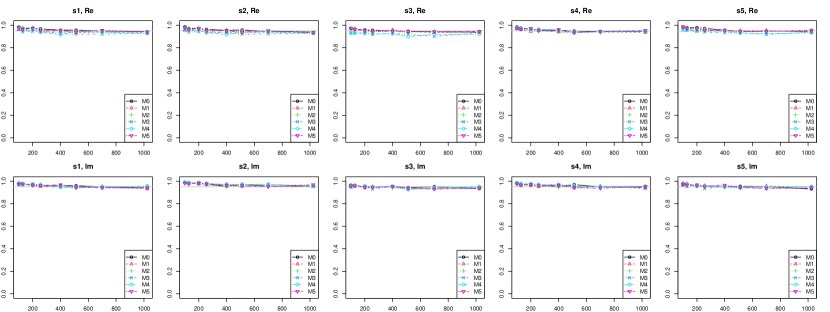

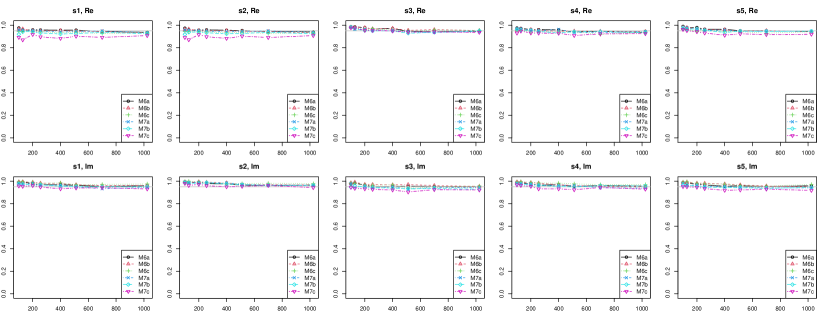

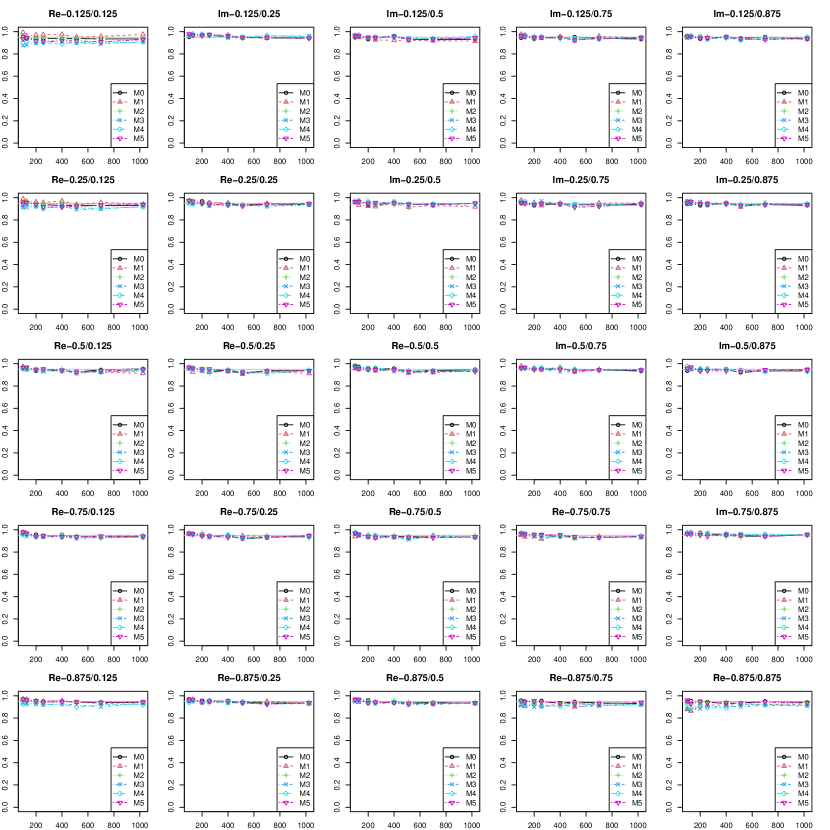

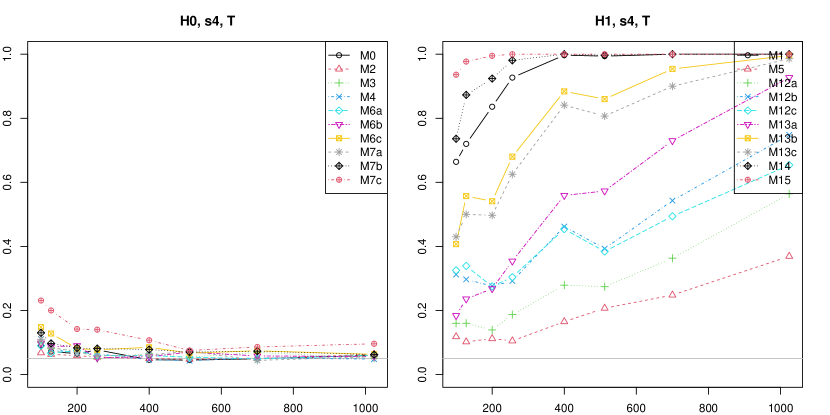

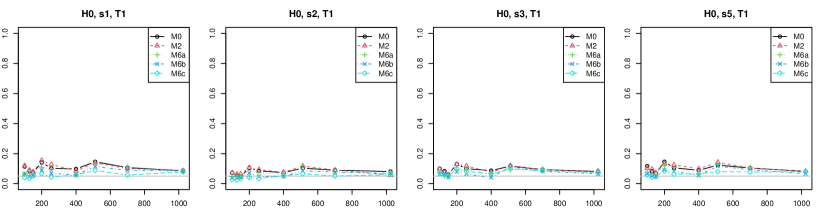

We throughout used . We simulated pointwise in coverage for all in . For the uniform procedures, maxima with respect to all 15 quantile levels were used [see Appendix .4 for a detailed description of how coverage is computed]. For pointwise coverage, we only display results for .

Figure 1 reports, for models M0-M7 and the -uniform procedure with finite-population correction (15), the coverage probabilities as functions of the sample size. For weighting, we have used the weights defined in the Appendix. All results are very close to the nominal 0.95 level; the equal weights function yields the best results. Figures 2 (for models M0-M5) and 3 (for models M6-M7) report the coverage probabilities of the -uniform, -pointwise procedure, still with finite-population correction. Here and in subsequent tables reporting -pointwise results, we have followed the convention to show the results for real parts on and below the diagonal and the results for imaginary parts above the diagonal. Overall, the method (with finite-population correction) works well. As expected, large sample sizes are required to obtain reasonable coverage probability for extreme quantiles, for example, . Especially, the construction of confidence bands for extreme quantiles in models M3, M4, and M7c is challenging. For , the results for imaginary parts are better than for real parts.

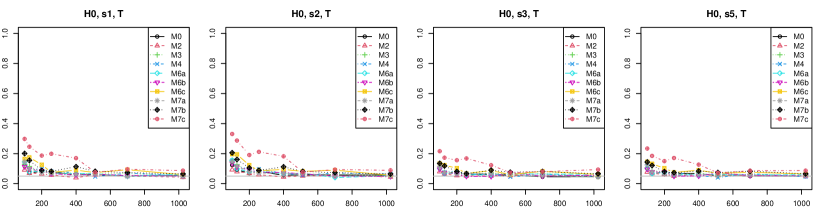

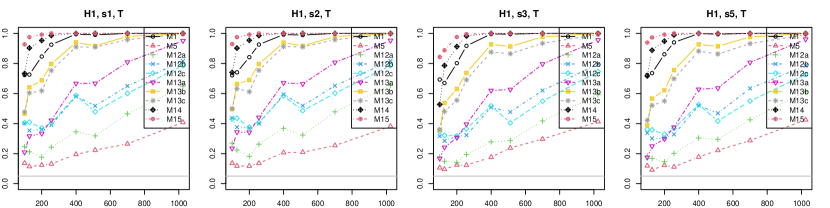

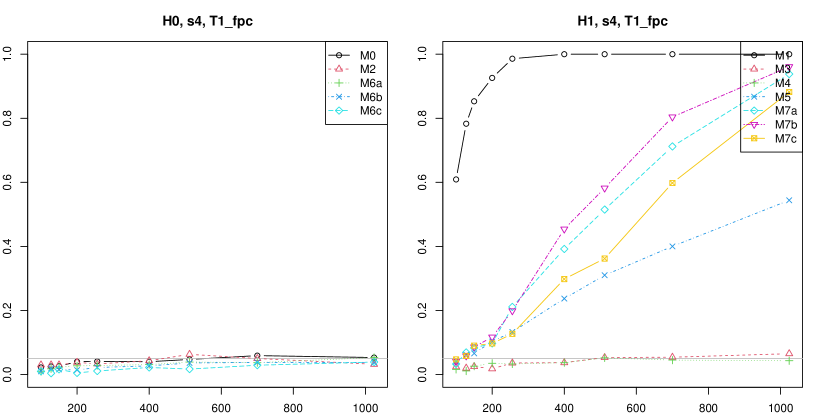

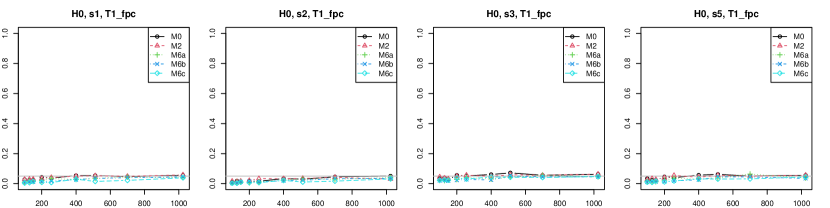

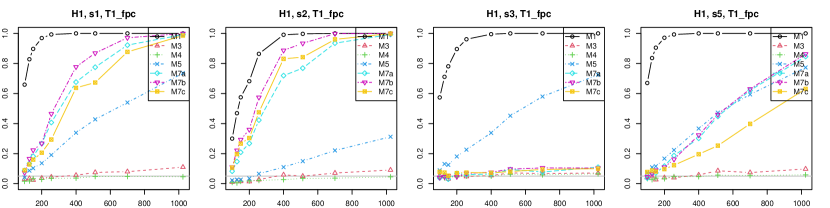

5.2 Time-reversibility

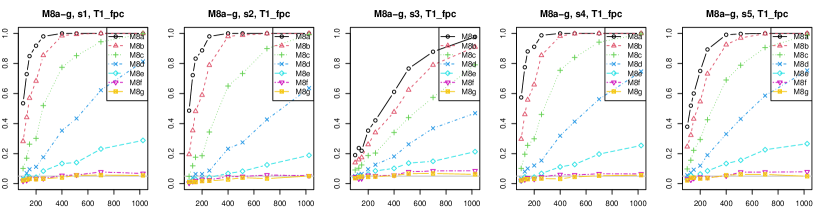

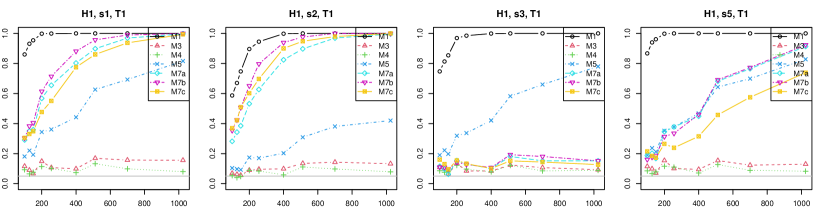

In this subsection, we evaluate, based on models M0-M7 and M8-M11, the finite-sample performance of the tests for time-reversibility introduced in Section 4.2 and compare it to that of their main competitors. The simulation procedure is essentially the same as in Section 5.1: for each value of the sample size in , a subsampling block size is chosen via the rule of thumb (29). The maxima in the test statistic (22) are taken over the frequency range and the quantiles , with the weight functions defined in the Appendix. The significance level throughout is .

For each case, replications were generated. For each replication, two tests were performed, based on (no finite-population correction) and (finite-population correction), respectively. The resulting rejection frequencies with weight function (empirical sizes for M0, M2, M6, empirical powers for M1, M3, M4, M5, and M7) are shown in Figure 4 for and Figure 5 for , respectively.

The test based on suffers of size distortion (over–rejection) while the size control, for the test based on , is good. The finite-population correction, thus, is highly recommended. We can see that the power of our tests is high for large sample sizes except for M3-M5. Results for other weight functions are provided in the online supplement.

Next, we compare our tests with the few existing ones, namely, the tests proposed by Ramsey and Rothman, (1996), Chen et al., (2000), Paparoditis and Politis, (2002), and Beare and Seo, (2014), based on the test statistics

| (30) |

respectively, where . The critical values of these tests are calculated via local bootstrap (see Sections 3.2 and 3.3 in Beare and Seo, (2014)). The intuition behind and is that time-reversibility of the process implies the symmetry of about the origin, while is motivated by the fact that under time-reversibility if has finite third moments. These facts, however, are just necessary conditions for time-reversibility. As for , it is based on a property of Markov processes, which are time-reversible at lag one if and only if the copula of is.

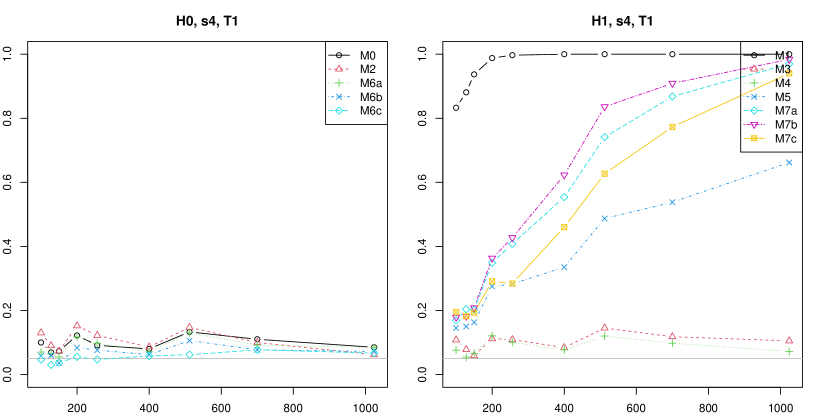

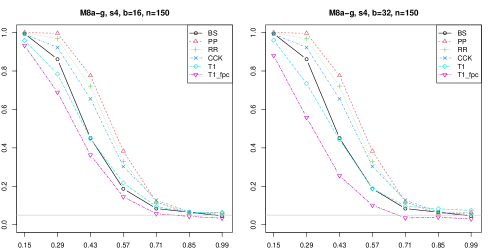

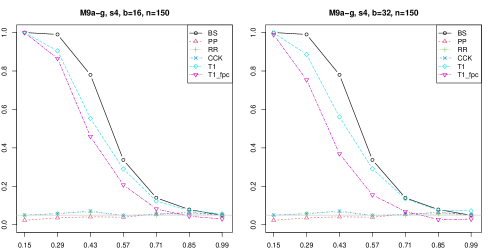

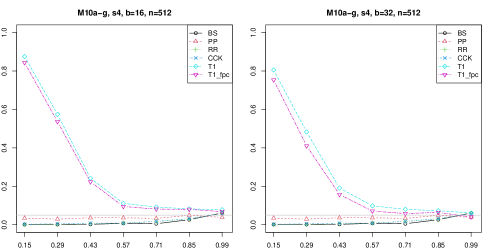

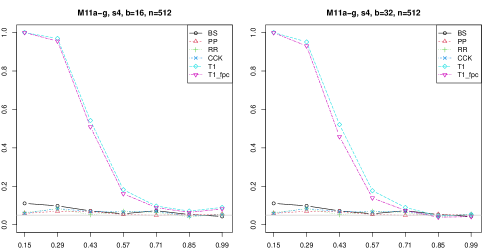

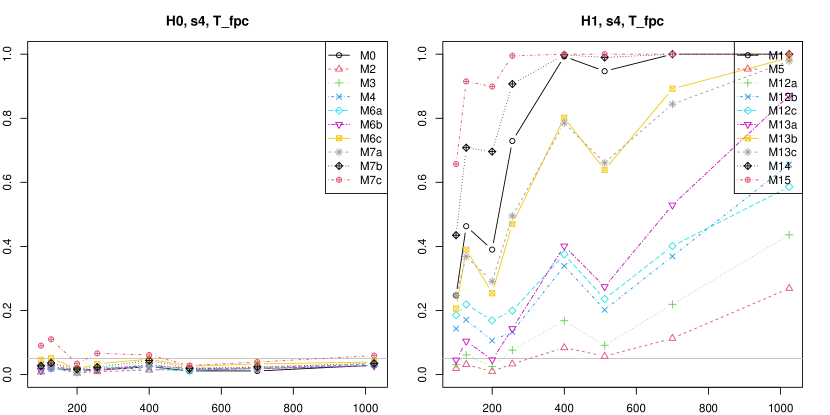

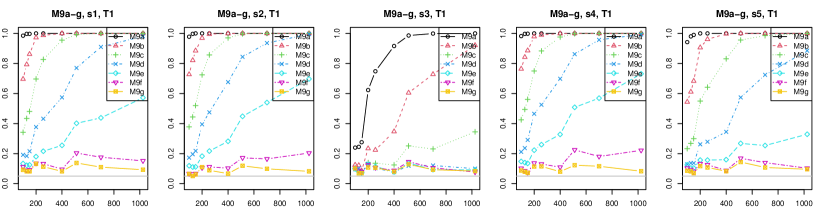

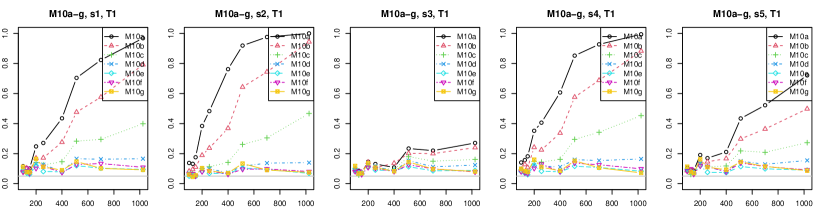

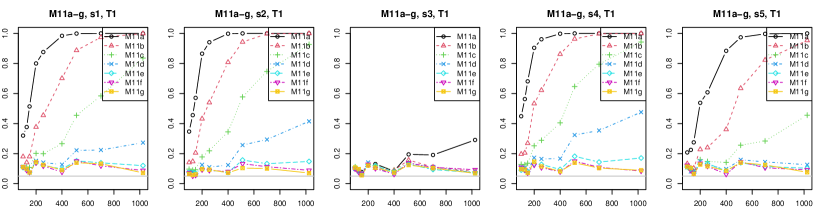

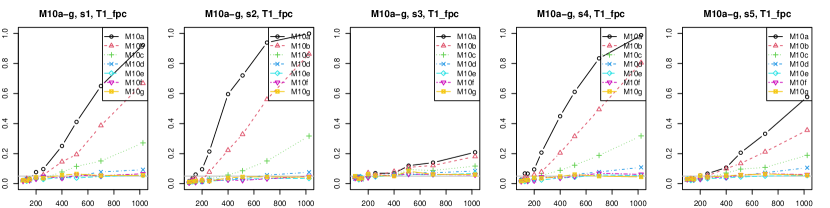

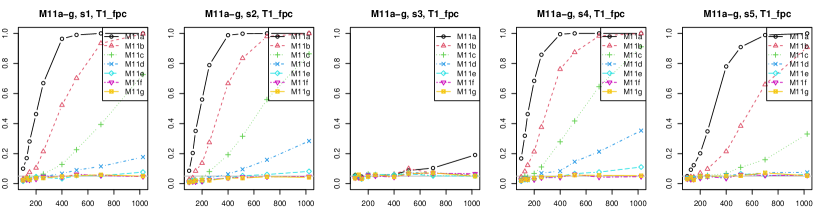

Our comparison is based on simulations of models M8-M9 with sample size (Figure 6), of models M10-M11 with sample size (Figure 7), with subsampling block sizes and and weight function . Other settings and simulations have been performed, and yield similar results. Empirical power plots are provided in Figures 6 and 7, with increasing degree of time-reversibility (measured by the parameters and , respectively, with value one corresponding to the null hypothesis of time-reversibility) on the horizontal axis. Model M9 is such that, among the competitors (30), only can detect time-irreversibility; models M10 and M11 are such that none of these competitors can detect time-irreversibility. Our tests were implemented with and without finite population correction.

Figure 6 shows the expected result that the power of all tests increases with the degree of time-irreversibility for M8; the same holds true for M9, but only for our tests and the test based on , while , , and (which are best under M8) are totally powerless. Our tests behave quite well in all cases, although outperformed by the test based on . Figure 7, however,

establishes that in models M10 and M11 with moderate degree of time-irreversibility, our tests very efficiently do reject time-reversibility while all their competitors, including the -based one, fall short from detecting anything. The finite population correction and the choice of the subsampling block size apparently have little impact, irrespective of the model and the sample size. Additional simulations can be found in the online Supplement.

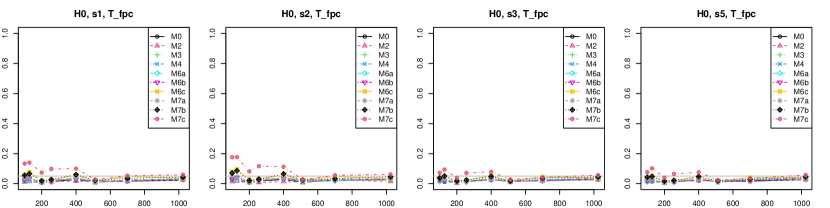

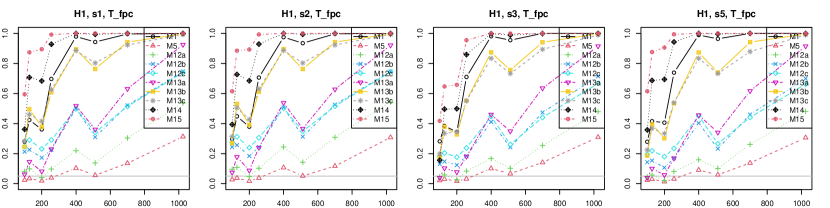

5.3 Asymmetry in tail dynamics

In order to study the empirical size and power of the test for quantile symmetry introduced in Section 4.3, we simulated observations from models M0–M7c and M12a–M15. For each sample size , a subsampling block size is chosen via the rule of thumb (29). As in Section 5.2, the maxima in statistic (27) were taken over the frequency range and the quantiles , with weight functions . Significance level throughout is .

For each case, replications were generated. For each replication, two tests were performed, based on the test statistics (as defined in (27); no finite-population correction) and (with finite-population correction), respectively.

The resulting rejection frequencies (empirical sizes for M0, M2, M3, M4, M6a-c, and M7a- c, empirical powers for M1, M5, M12a-c, M13a-c, M14, and M15) are displayed in Figure 8 for and Figure 9 for .

The test based on (Figure 8) exhibits significant size distortions for small sample sizes—particularly so under models M7b–c and M6c. The test based on the corrected statistic provides much better results in that respect, although overrejection is still present under M7b–c. The finite population correction, thus, is still recommended. As for empirical powers, they all increase with the sample size; detecting tail asymmetry in M5 and, to a lesser extent, in M12a remains difficult. Simulation results for additional weight functions are provided in the online Supplement.

Additional details on simulations

.4 Computation of coverage frequencies

The coverage probability of the procedure that is uniform with respect to and pointwise with respect to for a real part is defined by the empirical probability (with respect to the iterations) of the event, for fixed and ,

where is the true spectrum derived by the direct calculation for (M0) and the true spectrum simulated by quantspec for the other cases. In case of the simulated spectra, they are available at the Fourier frequencies , with and we round down to the next available such frequency , where .

The coverage probability of the procedure that is uniform with respect to for a real part is defined by the empirical probability (with respect to the iterations) of the event

The coverage probabilities of the procedure that is uniform with respect to and pointwise with respect to and of the procedure that is uniform with respect to for imaginary parts are defined in the same way.

.5 Weight functions

The weight functions are defined as

.6 Detailed definitions of the models used in simulations

Models M0–M15 are defined, for and , as

| (M0) | ||||

| (M1) | ||||

| (M2) | ||||

| (M3) | ||||

| (M4) | ||||

| (M5) | ||||

| (M6) | ||||

| (M7) | ||||

| (M8) | ||||

| (M9) | ||||

| (M10) | ||||

| (M11) | ||||

| (M12) | ||||

| (M13) | ||||

| (M14) | ||||

| (M15) |

In (M1), denotes a sequence of i.i.d. standard uniform random variables, and denotes the cdf of . This model is from the class of QAR(1) processes, which was introduced by Koenker and Xiao, (2006). In (M2), denotes a sequence of standard normal white noise. This AR(2) process was previously considered by Li, (2012). (M3) is ARCH(1) process previously considered by Lee and Rao, (2012). (M4) and (M5) are GARCH(1,1) and EGARCH(1,1,1) models, respectively, previously considered by Birr et al., (2019). (M6) is AR(1) model with a Gaussian innovation. The AR coefficient of this model is defined as for in order. In (M7), denotes a sequence of i.i.d. standard Cauchy distribution. This is AR(1) model with a Cauchy innovation. The ordinary spectral density of (M7) does not exist. In (M8) and (M9), denotes a sequence of i.i.d. standard uniform distribution. The conditional distribution function is defined, for whose joint distribution follows , as for . The function is the asymmetric Gumbel copula, which is defined as

where and . The function is the zero total circulation copula, which is defined, for , as

where

and the generalized inverse is calculated via a grid of 1000 points equispaced over . Let and take values for , respectively. These models were considered by Beare and Seo, (2014) in their simulation. When and , both models reduce to the product copula. Therefore, (M8) with and (M9) with are time-reversible. The models (M10) and (M11) are designed that any time-reversibility tests based on a first-order Markov process cannot detect time-irreversibility. In (M12), the function is the Gumbel copula, which is defined as

where with Kendall’s tau for . In (M13), the function is the Clayton copula, which is defined as

where with Kendall’s tau for . The parameters and are defined as for , respectively. These models are considered by Li and Genton, (2013) in their simulation. In (M14), the function is the copula 3 of Nelsen, (1993, Figure 1), which is defined as

where

In (M15), the function is the copula 6 of Nelsen, (1993, Figure 1), which is defined as

where

The models M12j–M15 are not radially symmetric.

[Acknowledgments] The first three authors contributed equally to the paper and are listed alphabetically. The authors are grateful to Brendan K. Beare and Juwon Seo for kindly sharing their Matlab codes for Section 5.2.

This work has been supported in part by the Collaborative Research Center “Statistical modeling of nonlinear dynamic processes” (SFB 823, Teilprojekt A1,C1) of the German Research Foundation (DFG). Yuichi Goto was supported by JSPS Grant-in-Aid for Research Activity Start-up under Grant Number JP21K20338. Stanislav Volgushev was partially supported by a discovery grant from NSERC of Canada,

References

- Anderson, (1993) Anderson, T. W. (1993). Goodness of fit tests for spectral distributions. The Annals of Statistics, pages 830–847.

- Baruník and Kley, (2019) Baruník, J. and Kley, T. (2019). Quantile coherency: A general measure for dependence between cyclical economic variables. The Econometrics Journal, 22(2):131–152.

- Beare and Seo, (2014) Beare, B. K. and Seo, J. (2014). Time irreversible copula-based markov models. Econometric Theory, pages 923–960.

- Birr et al., (2019) Birr, S., Kley, T., and Volgushev, S. (2019). Model assessment for time series dynamics using copula spectral densities: a graphical tool. arXiv:1804.01440.

- Birr et al., (2017) Birr, S., Volgushev, S., Kley, T., Dette, H., and Hallin, M. (2017). Quantile spectral analysis for locally stationary time series. Journal of the Royal Statistical Society: Series B, 79(5):1619–1643.

- Brillinger and Rosenblatt, (1967) Brillinger, D. and Rosenblatt, M. (1967). Computation and interpretation of kth order spectra. In Harris, B., editor, Spectral Analysis of Time Series, pages 189–232. John Wiley, New York.

- Brillinger, (1969) Brillinger, D. R. (1969). Asymptotic properties of spectral estimates of second order. Biometrika, 56(2):375–390.

- Brillinger, (1975) Brillinger, D. R. (1975). Time series: Data Analysis and Theory. Holt, Rinehart and Winston, Inc.

- Chen et al., (2000) Chen, Y.-T., Chou, R. Y., and Kuan, C.-M. (2000). Testing time reversibility without moment restrictions. J. Econometrics, 95(1):199–218.

- Dahlhaus, (1985) Dahlhaus, R. (1985). Asymptotic normality of spectral estimates. Journal of Multivariate Analysis, 16(3):412–431.

- Dahlhaus, (1988) Dahlhaus, R. (1988). Empirical spectral processes and their applications to time series analysis. Stochastic Processes and their Applications, 30(1):69–83.

- Davis and Mikosch, (2009) Davis, R. A. and Mikosch, T. (2009). The extremogram: A correlogram for extreme events. Bernoulli, 15(4):977–1009.

- Davis et al., (2013) Davis, R. A., Mikosch, T., and Zhao, Y. (2013). Measures of serial extremal dependence and their estimation. Stochastic Processes and their Applications, 123:2575–2602.

- De Gooijer, (2017) De Gooijer, J. G. (2017). Elements of nonlinear time series analysis and forecasting, volume 37. Springer.

- Dette et al., (2015) Dette, H., Hallin, M., Kley, T., Volgushev, S., et al. (2015). Of copulas, quantiles, ranks and spectra: An -approach to spectral analysis. Bernoulli, 21(2):781–831.

- Fermanian et al., (2004) Fermanian, J.-D., Radulovic, D., Wegkamp, M., et al. (2004). Weak convergence of empirical copula processes. Bernoulli, 10(5):847–860.

- Gaenssler et al., (2007) Gaenssler, P., Molnár, P., and Rost, D. (2007). On continuity and strict increase of the cdf for the sup-functional of a gaussian process with applications to statistics. Results in Mathematics, 51(1-2):51–60.

- Ghil et al., (2002) Ghil, M., Allen, M., Dettinger, M., Ide, K., Kondrashov, D., Mann, M., Robertson, A., Saunders, A., Tian, Y., Varadi, F., and Yiou, P. (2002). Advanced spectral methods for climate time series. Rev. Geophys., 2002:1003–1043.

- Granger and Hatanaka, (2015) Granger, C. W. J. and Hatanaka, M. (2015). Spectral Analysis of Economic Time Series. Princeton University Press.

- Grenander and Rosenblatt, (1957) Grenander, U. and Rosenblatt, M. (1957). Statistical analysis of stationary time series. John Wiley & Sons, New York.

- Hagemann, (2013) Hagemann, A. (2013). Robust spectral analysis (arxiv:1111.1965v2). ArXiv e-prints.

- Hallin et al., (1988) Hallin, M., Lefevre, C., and Puri, M. L. (1988). On time-reversibility and the uniqueness of moving average representations for non-gaussian stationary time series. Biometrika, 75(1):170–171.

- Han et al., (2014) Han, H., Linton, O., Oka, T., and Whang, Y.-J. (2014). The cross-quantilogram: measuring quantile dependence and testing directional preeictability between time series. available at: http://papers.ssrn.com/sol3/papers.cfm?abstract_id=2338468.

- Hong, (1999) Hong, Y. (1999). Hypothesis testing in time series via the empirical characteristic function: a generalized spectral density approach. Journal of the American Statistical Association, 94(448):1201–1220.

- Hong, (2000) Hong, Y. (2000). Generalized spectral tests for serial dependence. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 62(3):557–574.

- Ibragimov, (1963) Ibragimov, I. A. (1963). On estimation of the spectral function of a stationary gaussian process. Theory of Probability & Its Applications, 8(4):366–401.

- Jondeau and Rockinger, (2003) Jondeau, E. and Rockinger, M. (2003). Testing for differences in the tails of stock-market returns. J. Empir. Finance, 10(5):559–581.

- Kley, (2014) Kley, T. (2014). Quantile-Based Spectral Analysis: Asymptotic Theory and Computation. PhD thesis, Ruhr-Universität Bochum.

- Kley, (2016) Kley, T. (2016). Quantile-based spectral analysis in an object-oriented framework and a reference implementation in R: The quantspec package. Journal of Statistical Software, 70(3):1–27.

- (30) Kley, T., Volgushev, S., Dette, H., Hallin, M., et al. (2016a). Quantile spectral processes: Asymptotic analysis and inference. Bernoulli, 22(3):1770–1807.

- (31) Kley, T., Volgushev, S., Dette, H., Hallin, M., et al. (2016b). Supplement to ”quantile spectral processes: Asymptotic analysis and inference”. Bernoulli, 22(3):1770–1807.

- Klüppelberg and Mikosch, (1996) Klüppelberg, C. and Mikosch, T. (1996). The integrated periodogram for stable processes. The Annals of Statistics, 24(5):1855–1879.

- Koenker and Xiao, (2006) Koenker, R. and Xiao, Z. (2006). Quantile autoregression. Journal of the American Statistical Association, 101(475):980–990.

- Kokoszka and Mikosch, (1997) Kokoszka, P. and Mikosch, T. (1997). The integrated periodogram for long-memory processes with finite or infinite variance. Stochastic processes and their applications, 66(1):55–78.

- Krupskii and Joe, (2019) Krupskii, P. and Joe, H. (2019). Nonparametric estimation of multivariate tail probabilities and tail dependence coefficients. J. Multivar. Anal., 172:147–161.

- Lange et al., (2019) Lange, H., Brunton, S., and Kutz, N. (2019). Spectral Methods for Time Series Prediction with Application to Fluid Flows. In APS Division of Fluid Dynamics Meeting Abstracts, APS Meeting Abstracts, page Q41.008.

- Lee and Rao, (2012) Lee, J. and Rao, S. S. (2012). The probabilistic spectral density. Personal Communication.

- Li and Genton, (2013) Li, B. and Genton, M. G. (2013). Nonparametric identification of copula structures. J. Amer. Statist. Assoc., 108(502):666–675.

- Li, (2008) Li, T.-H. (2008). Laplace periodogram for time series analysis. Journal of the American Statistical Association, 103(482):757–768.

- Li, (2012) Li, T.-H. (2012). Quantile periodograms. Journal of the American Statistical Association, 107(498):765–776.

- Li, (2013) Li, T.-H. (2013). Time Series with Mixed Spectra: Theory and Methods. CRC Press, Boca Raton.

- Li, (2021) Li, T.-H. (2021). Quantile-frequency analysis and spectral measures for diagnostic checks of time series with nonlinear dynamics. J. R. Stat. Soc. Ser. C Appl. Stat., 70(2):270–290.

- Likkason, (2011) Likkason, O. (2011). Spectral Analysis of Geophysical Data.

- Lim and Oh, (2021) Lim, Y. and Oh, H.-S. (2021). Quantile spectral analysis of long-memory processes. Empirical Economics, pages 1–22.

- Linton and Whang, (2007) Linton, O. and Whang, Y.-J. (2007). The quantilogram: with an application to evaluating directional predictability. Journal of Econometrics, 141:250–282.

- Mangold, (2017) Mangold, B. (2017). New concepts of symmetry for copulas. Technical report, FAU Discussion Papers in Economics.

- Mikosch and Norvaiša, (1997) Mikosch, T. and Norvaiša, R. (1997). Uniform convergence of the empirical spectral distribution function. Stochastic processes and their applications, 70(1):85–114.

- Nelsen, (1993) Nelsen, R. B. (1993). Some concepts of bivariate symmetry. J. Nonpara. Statist., 3(1):95–101.

- Nelsen, (2006) Nelsen, R. B. (2006). An introduction to copulas. Springer Science & Business Media.

- Neumann and Paparoditis, (2008) Neumann, M. H. and Paparoditis, E. (2008). Simultaneous confidence bands in spectral density estimation. Biometrika, 95(2):381–397.

- Paparoditis and Politis, (2002) Paparoditis, E. and Politis, D. N. (2002). The local bootstrap for markov processes. J. Stat. Plan. Inf., 108(1-2):301–328.

- Politis et al., (1999) Politis, D. N., Romano, J. P., and Wolf, M. (1999). Subsampling. Springer.

- Priestley, (1987) Priestley, M. B. (1987). Spectral analysis and time series. Academic press.

- Ramsey and Rothman, (1996) Ramsey, J. B. and Rothman, P. (1996). Time irreversibility and business cycle asymmetry. J. Money Credit Bank., 28(1):1–21.

- Rosco and Joe, (2013) Rosco, J. and Joe, H. (2013). Measures of tail asymmetry for bivariate copulas. Stat. Pap., 54(3):709–726.

- Rudin et al., (1964) Rudin, W. et al. (1964). Principles of mathematical analysis, volume 3. McGraw-Hill New York.

- Segers, (2012) Segers, J. (2012). Asymptotics of empirical copula processes under non-restrictive smoothness assumptions. Bernoulli, 18(3):764–782.

- Sklar, (1959) Sklar, M. (1959). Fonctions de répartition à n dimensions et leurs marges. Publ. Inst. Statist. Univ. Paris, 8:229–231.

- So and Chan, (2014) So, M. K. and Chan, R. K. (2014). Bayesian analysis of tail asymmetry based on a threshold extreme value model. Comput. Stat. Data Anal., 71:568–587.

- Su et al., (2021) Su, X., Zhan, W., and Li, Y. (2021). Quantile dependence between investor attention and cryptocurrency returns: evidence from time and frequency domain analyses. Applied Economics.

- Van der Vaart, (2000) Van der Vaart, A. W. (2000). Asymptotic statistics, volume 3. Cambridge university press.

- van der Vaart and Wellner, (1996) van der Vaart, A. W. and Wellner, J. A. (1996). Weak Convergence and Empirical Processes. Springer.

- Vervaat, (1972) Vervaat, W. (1972). Functional central limit theorems for processes with positive drift and their inverses. Probability Theory and Related Fields, 23(4):245–253.

- von Sachs, (2020) von Sachs, R. (2020). Nonparametric spectral analysis of multivariate time series. Annual Review of Statistics and Its Application, 7(1):361–386.

- Wu and Shao, (2004) Wu, W. B. and Shao, X. (2004). Limit theorems for iterated random functions. Journal of Applied Probability, 41(2):425–436.

Online Supplement

Appendix A Proofs

A.1 Proof of Lemma 3.1

Proof.

Throughout the proof, let and denote the cumulative distribution functions of

and , respectively.

We first provide a bound on . Observe the following representation:

where

Now, from a Taylor expansion, we find

where is a value between and . In particular, for any . A straightforward calculation shows that there exists a function , independent of such that for all

for all and such that

Summarizing, we have shown that for any and any

Since by assumption , we can have for at most a finite set of . Thus,

| (31) |

Next note that, employing Leibniz’s integral rule, we have

Observe that

and, by adding a square,

Thus, altogether,

Next, let and observe that . The function is continuous and differentiable on . Thus, by the mean value theorem, for any with there exists with such that

Since

and, hence,

we obtain

Therefore,

where we have used that, by assumption, . Combining this with (31) we can apply Theorem 7.17 in Rudin et al., (1964) to conclude that the partial derivatives

exist and are continuous on . ∎

A.2 Proof of Theorem 3.1

We begin by deriving an alternative representation for the copula-based spectral distribution function defined in (2) and introduce some additional notation.

Observe that from definitions (3) and (4) we can derive the following representation of the copula rank periodogram:

| (32) |

Since for , we have, for ,

| (33) |

where can be chosen arbitrarily. Using property (33) in (A.2), after rearranging sums, we obtain

| (34) |

with arbitrary ,

and . Next, using (34) in the definition of the estimator of the spectral distribution function (2) and rearranging sums yields

Define the weights

| (35) |

and the rank-based copula cumulant function of order

| (36) |

Then, we obtain

| (37) |

as an alternative representation of the estimator of the copula spectral distribution function. Similarly, the copula spectral distribution function has the alternative representation

In the subsequent analysis, we sometimes will consider versions of and , where the terms corresponding to lag are removed, that is,

and as defined in (7). Also, in the analysis of the asymptotic properties, instead of the process

we often prove intermediate results for the process

where is defined exactly as but with the actual distributions function replacing the

empirical one . More precisely, in order to prove the weak convergence of the process for , we derive, according to Lemma 2.2.2 in van der Vaart and Wellner, (1996), the stochastic equicontinuity for the process . The impact of replacing the true distribution functions by the empirical versions in is then seen in the derivation of the covariance structure of the limiting process.

We are now ready to start with the main proof. We first prove several intermediate results for the process

indexed by , where

with and

As for , we have

where is defined in (35),

| (38) |

with , , where can be chosen arbitrarily since for .

Finally, as for the rank-based versions, we define

and

where the terms corresponding to lag have been removed.

A.2.1 Proof of Theorem 3.1 – Main arguments

The proof of Theorem 3.1 is rather technical and consists of a series of lemmas and intermediate results. To facilitate the reading we give an overview of the most important arguments of the proof.

For all , consider the stochastic process

| (39) |

indexed by . Observe that since is assumed to be continuous, the ranks of are almost surely the same as the ranks of , i.e., without loss of generality, we can assume the marginals to be uniformly distributed. In what follows, let denote the empirical distribution function of . With , we have, by Lemma B.1 (the proof of which is deferred to Section B.3),

| (40) |

Furthermore, by Lemma B.2 (which is also proved in Section B.3),

and, therefore, we have the decomposition

| (41) |

where, by Assumption (D),

as , by Lemma A.5 in Kley et al., 2016a ,

Moreover, noting that converges to a tight Gaussian limit with continuous sample paths [see the proof of Lemma A.5 in Kley et al., 2016b ], we obtain under the given assumptions by Vervaat’s Lemma [see Vervaat, (1972)],

| (42) |

where .

As a second step, to prove the weak convergence of , it suffices, by Lemmas 1.5.4 and 1.5.7 in van der Vaart and Wellner, (1996), to show that the finite-dimensional distributions converge in distribution and to prove stochastic equicontinuity. That is, we need to establish

-

(i)

the convergence of the finite-dimensional distributions of the process (8), i.e.

(44) for any and and

-

(ii)

stochastic equicontinuity, i.e., for all ,

(45)

We start by proving the stochastic equicontinuity (45). In regard of equation (A.2.1), our proof consists of three steps:

-

•

establish the stochastic equicontinuity of ;

-

•

establish the stochastic equicontinuity of ;

-

•

show that

(46)

The assertion in the second step has been established in Kley et al., 2016a and the third step follows from the first one (see Section B.1.1). For simplicity of notation, introduce and . The main part in the proof of the stochastic equicontinuity of

is the establishment of a uniform bound on the increments of the process . The derivation of this bound relies on two intermediate bounds. First, we need a general bound on the moments of which is obtained in Lemma B.4. Second, we provide in Lemma B.5 a sharper bound on the same increments when and are “close.”

We now turn to the proof of the weak convergence of the finite-dimensional distributions (44). From (46), we have

and hence, it suffices to show the convergence of the finite-dimensional distributions of the process

indexed by . By Lemma P4.5 of Brillinger, (1975), it suffices to prove that for any , and any , the cumulants of the vector

converge to the corresponding cumulants of the vector

To this end, we proceed again in three steps:

-

•

show that the first-order moments of vanish;

-

•

show that the second-order moments yield the asymptotic covariance structure (3.1);

-

•

show that the moments of order greater than two vanish.

The first assertion is proved in Lemma B.3; detailed proofs of the second and third ones can be found in Section B.2.

A.2.2 Proof of (45) – stochastic equicontinuity

Assertion (46) mainly follows by the stochastic equicontinuity of which will be proved in the rest of this section. Details of the proof of (46) can be found in Section B.1.1.

We now prove the stochastic equicontinuity of . By Lemma B.3, it suffices to consider the process

| (47) |

and we need to prove that ,for all ,

This will be achieved by applying Lemma A.1 from Kley et al., 2016a to the process (A.2.2). Therefore, we will prove in Section B.1.2 that the assumptions for that lemma are fulfilled with the metric

for a that will be specified in the proof of (48). More precisely, for all in with , we have

| (48) |

where denotes the Orlicz norm .

In particular, (48) holds for , i.e. . Denoting by the packing number of [cf. van der Vaart and Wellner, (1996), page 98], we have . Therefore, by Lemma A.1 in Kley et al., 2016a , for all and all , there exists a random variable and a constant such that, for and ,

with

where the set contains at most points. In particular, by Markov’s inequality [cf. van der Vaart and Wellner, (1996), page 96],

A.2.3 Proof of (44) – convergence of the finite-dimensional distributions

In view of (A.2.1) and (46), it suffices to prove that the finite-dimensional distributions of

converge, i.e. that

for any and , where the process is defined in Theorem 3.1. For this purpose, we apply Lemma P4.5 of Brillinger, (1975), that is we prove that for any , and any in , the cumulants of the vector

converge to the corresponding cumulants of the vector

It can easily be shown that . Hence, it is equivalent to show the convergence of the cumulants of the vector

A.3 Proof of Theorem 4.1

We only prove the second part; the proof of the first part indeed is similar but simpler, and we only focus on confidence bands for the real part of . Define

Observe that

| (51) |

where

| (52) | ||||

By Corollary 1.3 and Remark 4.1 in Gaenssler et al., (2007), the distribution function of the random variable

is continuous and strictly increasing on . Let us show that converges in distribution to . Defining

note that converges in distribution to by Theorem 3.1 and the continuity of the map

By Slutzky, it suffices to show that . Note that, for any bounded function on and any , we have, by the triangle inequality,

which yields

Define

and apply the above inequality with and to obtain

By a simple calculation and Theorem 3.1, the paths of are uniformly asymptotically equicontinuous, whence the right-hand side of the last display is . Indeed, for any fixed and , we have

Since the left-hand side above does not depend on we can take the limit on both sides to obtain

where the last equality follows from uniform asymptotic equicontinuity. Since was arbitrary this implies . Thus, by continuity of the distribution of , we have, for all ,

| (53) |

Denote by the bounded Lipschitz metric on the space of distribution functions on : the following result will be established later in the proof

| (54) |

From (54) and the continuity of , we obtain the following two convergences (note that both suprema are measurable since their value does not change if is replaced by and the latter is taken over a countable set):

| (55) |

and

| (56) |

Here (56) follows from (55) by continuity of . Indeed, any continuous distribution function is also uniformly continuous, and we have, for any ,

Letting , we obtain, from the uniform continuity of ,

To establish (55), note that, by Problem 23.1 in Van der Vaart, (2000), (55) is equivalent to for every , which can be established by a standard approximation of indicator functions through Lipschitz continuous functions.

Then, the assertion of the theorem follows from (51), (53), the continuity of , (55), and (56). The coverage probability in (51) indeed is bounded from above by

| (57) |

where the first equality follows from the fact that is monotone increasing; for the second equality, letting and , note that and since

and, in view of Lemma 21.1 (ii), (iii) in Van der Vaart, (2000),

Finally, as is continuous, it follows from the Continuous Mapping Theorem and Slutzky’s lemma, that

this completes the proof of (57). Now, the same coverage probability in (51) is bounded from below by

since is non-decreasing222Indeed, by contraposition, implies , so yields and since the continuity of implies that . Theorem 4.1 follows from combining this with (57).

Proof of (54) The proof of (54) follows along similar arguments as in Section 7.3 of Politis et al., (1999). Similar to the notation there, let and

Denoting by the cdf of (recall that was defined in (52)), let be the empirical cdf of (recall that denotes the empirical cdf of ). A close look at the proof of Proposition 7.3.1 from Politis et al., (1999) reveals that this result continues to hold if in there is replaced by as in our setting.333Note that we have an additional dependence on the full sample size which is not present in Politis et al., (1999). It follows that

By the reverse triangle inequality and some elementary computations, we have

Let

denote the set of bounded Lipschitz functions from to : we have

Thus, we have shown that . Note that (53) also entails . Together with and the triangle inequality, this yields (54).

A.4 Proof of Theorem 4.2

We begin with Part 1 of the theorem. Let us show that, under the null,

More precisely, by employing Theorem 3.1 and the Continuous Mapping Theorem, it holds that, under the null,

Further,

where and . Uniform asymptotic equicontinuity of (which follows from Theorem 3.1 after a simple computation) implies that

Proposition 7.3.1 in Politis et al., (1999) then implies that as , where is the cdf of and

Next note that the function is continuous; this can be established similarly to the continuity of in the proof of Theorem 3.1. Now we obtain, as in the proof of (55), that

which in turn yields

Consequently, it holds that, for ,

in view of the continuity of which, by the Continuous Mapping Theorem and Slutzky’s Lemma, implies . This establishes Part 1 of the theorem.

We now turn to Part 2 of the same theorem. Note that it suffices to show that , since then for all . Next, since all copulas are continuous and since Assumption 3.1(C) implies uniform convergence of the series defining in (1), we have that is continuous as a function of . Now recall the definition in (2): . Thus, is continuous. Now, by assumption there exists such that . The continuity of together with (17) implies that there exist such that

| (58) |

where .

Let

and

We have, under , that

| (59) |

Denoting by the cdf of and defining

we have, by the subsampling arguments used in the proof of Part 1, that

Finally, letting , we have

Let us show that this implies . From (59) we have that ; i. e., for every , there exists and such that for all . Hence,

Here we used the fact that , which in turn implies that since is a cdf. Since is arbitrary, it follows that , which completes the proof of Part 2.

A.5 Proof of Theorem 4.3

First, we show that the proposed test based on hs asymptotic size . By the uniform asymptotic equicontinuity of and Theorem 3.1, a simple calculation shows that under the null ,

Proposition 7.3.1 of Politis et al., (1999) entails , where

is the empirical distribution function of and is the distribution function of . The continuity of follows from the same arguments as used for the continuity of in the proof of Theorem 4.1. This, combined with the arguments used in the proof of (55), yields

Therefore, it holds that, under the null ,

where the last line follows from the fact that the continuity of implies that

This shows that the proposed test has asymptotic level and completes the proof of the first part of Theorem 4.3.

Next, we show that the test is consistent against fixed alternatives. To this end, let us show that for all follows from the fact that . By assumption, there exists some such that

From (17) and the continuity of with respect to , there exists such that

| (60) |

where by continuity of on a compact set. Defining

with

observe that, under the alternative ,

| (61) |

By similar arguments as in the proof of the first part, it follows that

| (62) |

where the cdf of . By (60), (61) and (62), it holds that

where the first inequality follows by the same arguments as in the proof of Theorem 4.2 and the last line is a consequence of (62). Since and since

we obtain the desired result that that as .

Appendix B Technical details

B.1 Details for the proof of (45)

B.1.1 Proof of (46)

Observe that, for any and with , we have

It follows from Lemma A.5 in the online appendix of Kley et al., 2016a that

since , this implies . As for we have

which vanishes asymptotically for by the stochastic equicontinuity

of the process proved in Section A.2.2.

B.1.2 Proof of (48) – convergence of higher order cumulants

Let , . In this case, the Orlicz norm coincides with the -norm so that

| (63) |

In order to bound for , observe that can be written as

where , and

with

for and . Furthermore, by Lemma A.4 in Kley et al., 2016a , there exist constants and , independent of and , such that

for any Borel sets with .

Lemma B.4 in Section B.3 below yields

for sufficiently small and . Observing that for sufficiently small, for any , we obtain

| (64) |

Similarly, for ,

| (65) |

where and

with

for and .

Similar arguments imply

and hence,

| (66) |

Furthermore, if then for all so that

It follows that, for all with sufficiently small and for all such that ,

Observing that if and only if

we have

for all with . This establishes (48).

B.2 Details for the proof of (44)

All results in this section rely on the assumption

-

(CS)

Assume that assumption (S) holds and that, for given , a constant exists such that the summability condition

holds for arbitrary intervals and all .

This condition is a consequence of Assumption (C), but is slightly weaker and, therefore, mentioned seperately.

B.2.1 Proof of (A.2.3)

Note that

where

First consider . We have

By Theorem 2.3.2 in Brillinger, (1975), as for any ,

and, from Theorem 1.3 in the online appendix of Kley et al., 2016a , we know that under Assumption (CS) with and , for all and ,

| (67) |

where and

Observe that

Hence, the functions impose linear restrictions on the summation indices and we obtain

Similar arguments as in the proof of Lemma B.3 in Section B.3 below yield

and, as

because ,

| (68) |

B.2.2 Proof of (50) – convergence of the second-order cumulants

Observe that

Let for some finite sets . Then, by Theorem 2.3.1 (ii) and (iv) in Brillinger, (1975), with , we have

where we have used the convention that .

Hence, since by Assumption (D),

| (69) | ||||

for some constant . Put

Then, by Theorem 2.3.2 in Brillinger, (1975),

| (70) |

where the summation is over all indecomposable partitions of the table

| ⋮ | ⋮ |

| ⋮ | |

However, all indecomposable partitions of the above table are obtained by adding in the various possible ways the elements to the indecomposable partitions of the table

| ⋮ | ⋮ |

Therefore, and since for all , the first-order cumulants in (B.2.2) are zero. Furthermore, the maximum number of sets in an indecomposable decomposition of the above table is . Hence, neglecting, for notational convenience, the indices of , by (B.2.1) we obtain, with the convention ,

| (71) |

where

That is, after substituting (71) into (69), the functions impose linear restrictions on the summation indices, whence

with

Note that there are linear constraints on if and linear constraints if , i.e. there are linear constraints. This follows similarly as in the proof of Lemma A.2 in Kley et al., 2016a . More precisely, if we define for every a vector with

we can rewrite the condition as . Note that two at most of the vectors have non-zero entries being one and the other at each position . Hence, the linear restrictions corresponding to are linearly dependent if and only if . However, in the case of indecomposable partitions, if and only if .

B.3 Auxiliary results

Lemma B.1.

Under the assumptions of Theorem 3.1,

Proof.

Let and , where

is the generalized inverse of the empirical distribution function . Then, from (38), we have

By the representation (A.2) of , we obtain

where

Observing that

since if and only if for any distribution function and that, similarly,

we have

and

Furthermore,

Hence, the second indicator is never greater than the first one, whence, for any ,

where and the above -bound is a consequence of Lemma 8.6 of Kley et al., 2016b .

This concludes the proof. ∎

Lemma B.2.

Under the assumptions of Theorem 3.1,

| (72) | ||||

| (73) |

Proof.

The result follows if we show that

As the indicator is of bounded variation, we have

Furthermore, since is assumed to be continuous, the ranks of are almost surely the same as the ranks of , i.e. we can, without loss of generality, assume the marginals to be uniformly distributed and, letting in (36), write

Next, as in equation (A.4) in Kley et al., 2016a , for any ,

| (74) |

where and

| (75) |

whence, for any ,

∎

Lemma B.3.

Under Assumption (CS) with and ,

Proof.

First, for , ,

By Lemma 1.4 (or the remark thereafter) in the online appendix of Kley et al., 2016a , we have, for ,

with . Therefore,

Assumption (CS) implies that has bounded and uniformly continuous derivatives of order , that is is of finite total variation on the interval . Moreover, the indicator function is also of finite total variation. Then, their product is of finite total variation , and we obtain

Hence,

which concludes the proof. ∎

Lemma B.4.

Let be the finite realization of a strictly stationary process with , and for and let

where

with

and the weight function bounded, real-valued and even, with support .

For any Borel set , define

Assume that, for , there exist a constant and a function , both independent of and , such that

for any Borel sets with . Then, for , there exists a constant (depending on , , and only) such that

for all with .

Proof.

First note that, for ,

Repeating the arguments of the proof of Lemma A.2 in Kley et al., 2016a yields the representation

| (76) |

where the summation runs over all partitions of such that each set contains at least two elements, and

for any set , where and

with the sets , , , and the signs defined by

Then, we obtain, similarly as in the proof of Lemma A.2 in Kley, (2014),

where summation runs over all indecomposable partitions of the scheme

| ⋮ | ⋮ |

and

Furthermore, by assumption, the function has support and hence, there is at most one such that . Denote this integer by . Therefore,

and, with similar arguments,

where we have used the fact that

and the fact that the number of summands that are equal to one is less than since

lies in the support of for at most values of .

Lemma B.5.

Under the assumptions of Theorem 8, let be a sequence of non-negative real numbers. Assume that there exists such that . Then, as ,

Proof.

Note that

where

To bound , use (65) to obtain

From Lemmas A.6 and A.4 in Kley et al., 2016a , we know that, for any ,

and that, for and some constants and that do not depend on ,

for , i.e.

Observing that the sum

contains at most non-zero summands, we have, for any ,

and

Hence,

| (78) |

for sufficiently large.

Note that is equivalent to defined in (36) with .

Furthermore,

where is the integer such that . With this notation, for ,

Hence, for ,

where we have used the fact that and for . Similarly, for ,

as and for .

Summing up,

| (79) |

Next, note that, letting , we have

| (80) |

In a first step, let us show that, for any , there exists a constant such that

| (81) |

For this, for and fixed , let

where

By Theorem 2.2.4 in Nelsen, (2006) and since ; , we have

As, for and ,

we have, since ,

Analogously,

By bounding and , we have bounded the error made by evaluating the copulas on the points of the grid

whereas the copulas in are already evaluated on the grid and, thus, do not have to be treated separately.

The cardinality of the set

is of the order . Hence, by Lemma 2.2.2 in van der Vaart and Wellner, (1996) using and the upper bounds on and ,

where is some adequate constant.

Lemma B.6.

For any there exist constants and such that

Proof.

First note that

where the terms and can be handled similarly. Concentrating on the first one, let us prove that for any there exist and depending only on such that

where the sum runs over all partitions of .

Next, for any set with of a partition , we have by Theorems 2.3.1 and 2.3.2 of Brillinger, (1975)

where the sum runs over all indecomposable partitions of the table

| ⋮ | ⋮ |

| . |

Note that in there are at most cumulants of order one for which we have

where denotes the Lebesgue measure. Moreover, we will never encounter the case of the first-order cumulants and , for some , both appear in the product since the partition then would be decomposable.

The other cumulants in are at least of second-order and, as can be seen from the definition of a cumulant and the triangle inequality,

Furthermore, if we let and define

by Assumtion (C), we have

Hence, for all cumulants of order greater than two, we have the bound

Thus, for one partition we obtain

Since and ,

since for ,

and since ,

Thus, if we let and

we have

Next,

In order to estimate the cardinality of the set , consider first the case . We have

where (since there are possibilities to fix one element of and at most possible values for the remaining , )

For the case ,

where

| (84) |

In order to prove this, start by considering the set of one partition which contains either or or both. By indecomposability of the partition there exists at least one other or in such that or are not contained in . Hence, there are possible values for and at most possible values for any other so that either or exclusively is contained in since is fixed. Next, observe that by indecomposability of the partition, all sets hook [for a precise definition see page 20 in Brillinger, (1975)] and thus there exists a such that is contained in and in or vice versa. Again by indecomposability we find another or exclusively in for which we have at most choices so that . Continuing this argumentation until the maximum over all sets have been taken into consideration, we see that is at most of the order , since the indecomposable partitions yielding the highest order are those where each set is of size and contains or and or .

Therefore, (84) follows and

Observe that for some constant ,

because

-

(1)

if , then ;

-

(2)

if , setting (so that is such that for any ), then and

Hence, in total, for an indecomposable decomposition , we have

and therefore, for one set of elements,

Thus, for any partition with of ,

and, if we let and , we obtain

that is,

Analogously,

and hence

which completes the proof. ∎

Appendix C Additional simulation results

C.1 Additional simulation results for the test for time-reversibility

We show additional simulation results for the test for time-reversibility introduced in Section 4.2. We set the sample size and the block size, for a given , to , the range of maximum for frequency as , and the range of maxima for quantiles as . The weight functions defined in the Appendix and the significance level as are employed.

The simulation procedure is as follows: generate time series and calculate the -values based on and , which is defined as . Then, iterate times and compute empirical size or power. In the figures, is chosen by the rule of thumb defined by (29).