On the Value of ML Models

Abstract

We argue that, when establishing and benchmarking Machine Learning (ML) models, the research community should favour evaluation metrics that better capture the value delivered by their model in practical applications. For a specific class of use cases—selective classification—we show that not only can it be simple enough to do, but that it has import consequences and provides insights what to look for in a “good” ML model.

1 Introduction

In business use cases and other practical applications, Machine Learning (ML) models are but components of larger processes, and the value we derive from such models thus depends on the profitability and performances of the workflow as a whole. However, when determining by which metrics models are to be benchmarked, we believe that the ML research community currently gives very little thoughts as to how value is generated in practice. While we acknowledge that researchers can’t be expected to account for the full diversity and/or complexity of real settings, we believe that value-estimating metrics can be designed to capture high-level commonalities among classes of use cases: benchmarks could (and should!) strive to reflect value. In this paper, we substantiate these claims for the ubiquitous practical case of selective classification.

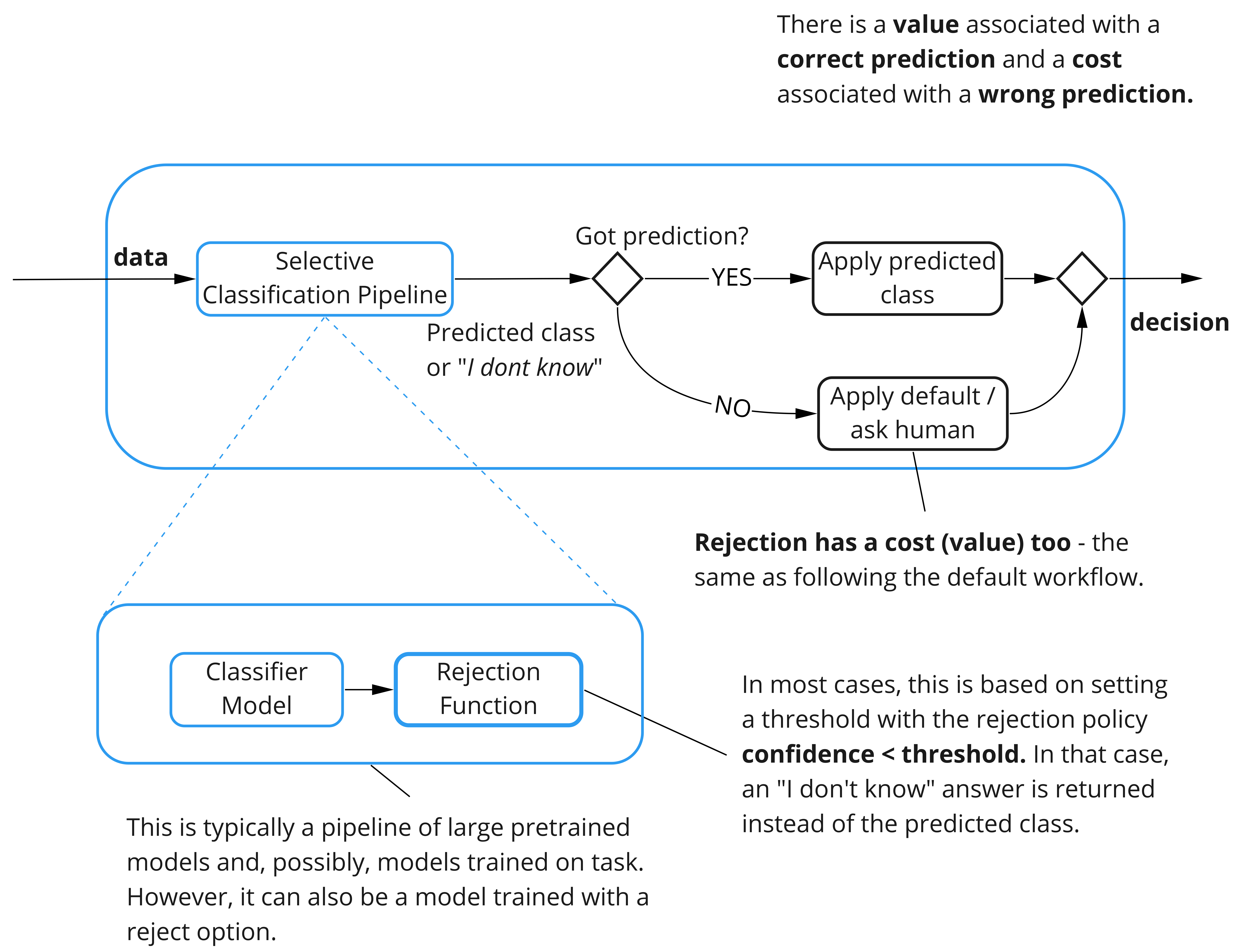

Indeed, in the overwhelming majority of enterprise workflows that we are aware of, ML models are deployed with a “default” (or “reject”) option: if the model is “confident enough” of a prediction, that prediction is acted on. Otherwise a default, safe path is taken (e.g., redirecting chat to a human agent, asking the driver to take the wheel). Figure 1 illustrates such workflows. Here we make these considerations concrete by introducing a special kind of “selective classifiers” [2, 6, 7, 8, 12], which we call abstaining classifiers. We then posit a simple form for the value derived from an abstaining classifier in an hypothetical workflow. Nontrivial consequences emerge from these basic assumptions, and we argue that these consequences would still play an important role in more realistic contexts: benchmarks not accounting from these phenomenons may paint a picture that has little to do with model value in real use cases.

There has been searches for “good general purpose metric to use when more specific criteria are not known” [4], and the literature has many examples where a mismatch between metrics and actual value may bring surprising, important consequences [5, 10, 13]. In fact it has long been known [3] that, given a concrete use case, the overall value of a process should be considered when selecting which model to use (and how to use it). Our stance and contributions are complementary: how should researchers benchmark general-purpose models for a broad spectrum of concrete use cases where they may bring value? Is such a feat possible at all?

Our results show that there is at least one class of practical concerns—processes with a “default” option—that can be distilled into a manageable, actionable metric, with nontrivial consequences backpropagating toward ML research. Among these consequences is the observation that “learning” does not imply a better accuracy nor a better calibration: given a calibrated model, its value can be increased without altering its prediction (and thus its accuracy) by learning a confidence distribution that is more discriminating. We hope that future work will show that this is not an isolated case, and that such value-related concerns will play a more important role in the mainstream ML research narrative.

2 Theory: Estimating the Value of a Model in a Simple Use Case

This section formalizes how we estimate the value of a classifier that is part of a process with a “default” option. We posit rather simple assumptions, and investigate some of their consequences. Questions as to whether those assumptions hold in real use cases are briefly treated in Appendix A.

Abstaining classifiers. Traditionally, a classifier uses the input data to assign a confidence to each class , with the understanding that is the predicted class with associated confidence . We define an abstaining classifier as a function mapping the input data to a single class , where the special class indicates that the classifier abstains from making a call111 does not provide any “score”: confidence may be used internally, but it is not exposed through ’s “API”.. Many strategies, including end-to-end training, can be used to obtain an abstaining classifier, but by far the most common approach in applications is to apply a threshold to a provided traditional classifier so that the model returns the traditional predicted class if its confidence exceeds the threshold, and abstains otherwise

| (1) |

Value. There is a benefit (resp. cost) for a correct (resp. wrong) prediction, as well as a cost for following the default path, and these quantities depend on the use case. We make this concrete for a specific use case by prescribing the value—measured in dollars or other forms of utility—that a customer gets out of an abstaining classifier’s prediction. Specifically, is a triple whose entries respectively characterize the value of a correct prediction, of an abstention, and of an incorrect prediction. Furthermore, we assume that these values combine linearly so that, given a dataset composed of pairs of inputs and labels , we may count the numbers of correct predictions, of abstentions, and of incorrect predictions of any abstaining classifier , from which we can establish the total value brought by in the use case for the dataset

| (2) |

For the sake of our argument, we posit that Eq. 2 is exactly true. In fact, we further posit that it is the upper bound to the value that any model making the same predictions as —although perhaps returning extra information such as confidences—could possibly achieve in this use case. Of course, this is probably never “exactly true”, and Appendix A discusses some reasons why. Nonetheless, we believe that our simple assumptions capture important properties of the class of use cases with a “default” option, and that their consequences should be treated seriously.

Dimensionless formulation. In the interesting222Indeed, we would never consider abstention if , and we would always abstain if . case where , applying to Eq. (2) the change of variables

| (3) |

gives the dimensionless average value per sample

| (4) |

We can understand Eq. (4) as an empirical average where each correct prediction grants a value of , an abstention grants no value, and a wrong prediction incurs a cost (negative value) determined by the penalty333You may use ”rong” as a mnemonic device. parameter , which fully captures the relevant information from the use case .

-aware vs calibrated. We say of an abstaining classifier that it is -aware if it can depend—explicitly, through training or otherwise—on the penalty parameter . For example, given a standard classifier and defining444 is an hyperparameter, hence why we optimize using a different (e.g., validation) dataset .

| (5a) | |||

| then is penalty-aware. In fact, according to our last assumption in introduction, it is the best value you can get out of . Interestingly, the case gives : in that limit, the model never abstains and corresponds to the traditional classification accuracy. | |||

Conversely, while the threshold in Eq. (5a) depends on the classifier , fully specifies the threshold to be used for all calibrated classifiers, i.e., whose confidence score matches the probability for the associated prediction to be correct. Indeed, if the standard classifier is calibrated with respect to the dataset , then we have

| (5b) |

Here is the Probability Density Function (PDF) for the confidence score given by for an input randomly sampled from . Since is calibrated, is the PDF for its correct classifications at confidence .

If has been obtained by “calibrating” so that, for any sample, their predicted classes match and the former’s confidence is provided by applying a monotonously increasing function to the latter’s, then Eqs. (5a) and (5b) can be related with . More importantly, both approaches result in the same dimensionless value: calibration (limited to a rescaling ) does not improve an abstaining classifier whose threshold is fixed by Eq. (5a).

VOC curves. In analogy with the Receiver Operating Characteristic (ROC) curve often used to characterize binary classifiers, we now introduce the Value Operating Characteristic (VOC) curve to characterize abstaining classifiers and, using Eq. (1), standard classifiers. The VOC curve of a abstaining classifier is simply the plot of the dimensionless value per sample as a function of the penalty for a given test dataset .

Unless a model doesn’t make a single wrong classification on the provided dataset , there exist values of for which is zero or negative. When this happen, is useless in the sense that we may as well enforce the policy “always abstain” to achieve a dimensionless value of zero. The quantity is the upper bound of the regime where that model has any use for that dataset.

But perhaps the most important property of VOC curves is that, in the limit of an infinite dataset , if an abstaining model’s VOC curve is everywhere above (or tying with) another model’s VOC curve in the interval , then the former model is guaranteed to provide more (or as much) value as the latter for any use case: it is just “better”. It is because of this universality over use cases that we advocate for VOC curves to become an important benchmarking component for all classification problems.

Improving standard classifiers. VOC curves compare models in terms of their value: here we consider how we may alter a standard classifier to “improve” its VOC curve. Since calibration cannot affect the VOC curve, we restrict our study to calibrated classifiers without loss of generality. Inspecting the left part of Eq. (5b), we notice that fully specifies . We thus consider perturbations of and investigate how they affect the VOC.

If some mass is taken from near some to be “pushed up” to higher confidence, this will always result in a better classifier (i.e., improves the value for some ranges of , and doesn’t make it worse for any others). Conversely, pushing mass down makes it worse (i.e., degrades value for some , and cannot make it better for any ). However, since we consider a calibrated model, this is trivially related to a change in model accuracy . What is slightly less trivial is that we can push a fraction greater or equal to of the mass around by pushing up a fraction greater or equal to , with equality corresponding to the case where accuracy is kept constant.

To make the arguments from the previous paragraph crisper, we introduce the discrimination metric : it is independent from both accuracy555To understand why, consider the new distribution . and calibration666From our assumption that is already calibrated. concerns. It can be understood as the average of two quantities: how far the confidence of good predictions is from , i.e., , and how far the confidence of bad predictions is from , i.e., . Ceteris paribus, a classifier with a higher discrimination is preferable to one with a lower one. Higher discrimination does not guarantee a better classifier, but neither does a better accuracy.

Learning beyond accuracy and calibration. Finally, we introduce, as a thought experiment and/or as an actual ML model, a family of discriminators so that if is the top class predicted with confidence by for the input , then is the revised confidence of the discriminator. With a minor abuse of notation, we can combine the two models to obtain the abstaining classifier

| (6) |

By design, can only affect whether the model abstains or not, and thus cannot affect the accuracy (i.e., the total proportion of correct predictions in the limit ). In fact, when paired with an already calibrated standard classifier , any improvement in the VOC of over the one of cannot be “blamed” on accuracy nor calibration, but should instead relate to discrimination.

Some readers may notice that, in Eq. (6), the discriminator basically acts as a binary classifier assessing whether correctly classifies or not. From this perspective, using the traditional binary classifier lingo, amounts to the number of “true positives”, amounts to the number of “false positives”, and amounts to the conflated sum of the number of “true negative” and “false negative”. The fact that these last two quantities are conflated is a feature of our approach, not a bug: when a model appears in a workflow as a selective classifier, it doesn’t matter if the model “would have been right/wrong” had it not abstained.

3 Implications and Considerations

The assumptions we posit in Sec. 2 may apply to a different extent in different use cases: Appendix A lists a few caveats to consider. However, notwithstanding those caveats, we believe that it is important for the ML community, both research and enterprise, to consider the notion of “value”. For the sake of simplicity, and to better ground our discussion, the rest of this section continues with those same assumptions. However, the reader is encouraged to think of broader implications.

Limits of existing correctness and calibration metrics. Accuracy is most useful as a metric when there are no incentives to abstain, because the cost of being wrong is the same for abstaining (i.e., is zero or close to zero). When abstaining is a valid option (i.e., ), a classifier may have greater accuracy (e.g., ) than a second classifier (e.g., ), yet the latter may have a higher value than the former. Similar comments could be formulated for other “correctness” metrics (e.g., precision and recall).

Expected Calibration Error (ECE) and similar measures of calibration [11] are also limited: they may not provide much information as to the model’s discriminating power (e.g., a model whose confidence is a constant corresponding to its accuracy has zero ECE, yet those confidences are not very useful), and improving the ECE by itself may not lead to a more valuable model. In fact, if we are already fixing with Eq. (5a), there is no way to achieve additional value through any form of calibration performing a monotonically increasing rescaling of the confidence.

Interestingly, having access to a model, regardless of its “correctness” and calibration, is almost always better than not having a model at all. Indeed, as long as ranking the predictions in terms of confidence would end up with a sufficient density of correct predictions on the top, then we may use Eq. (5a) to fix a non-trivial threshold .

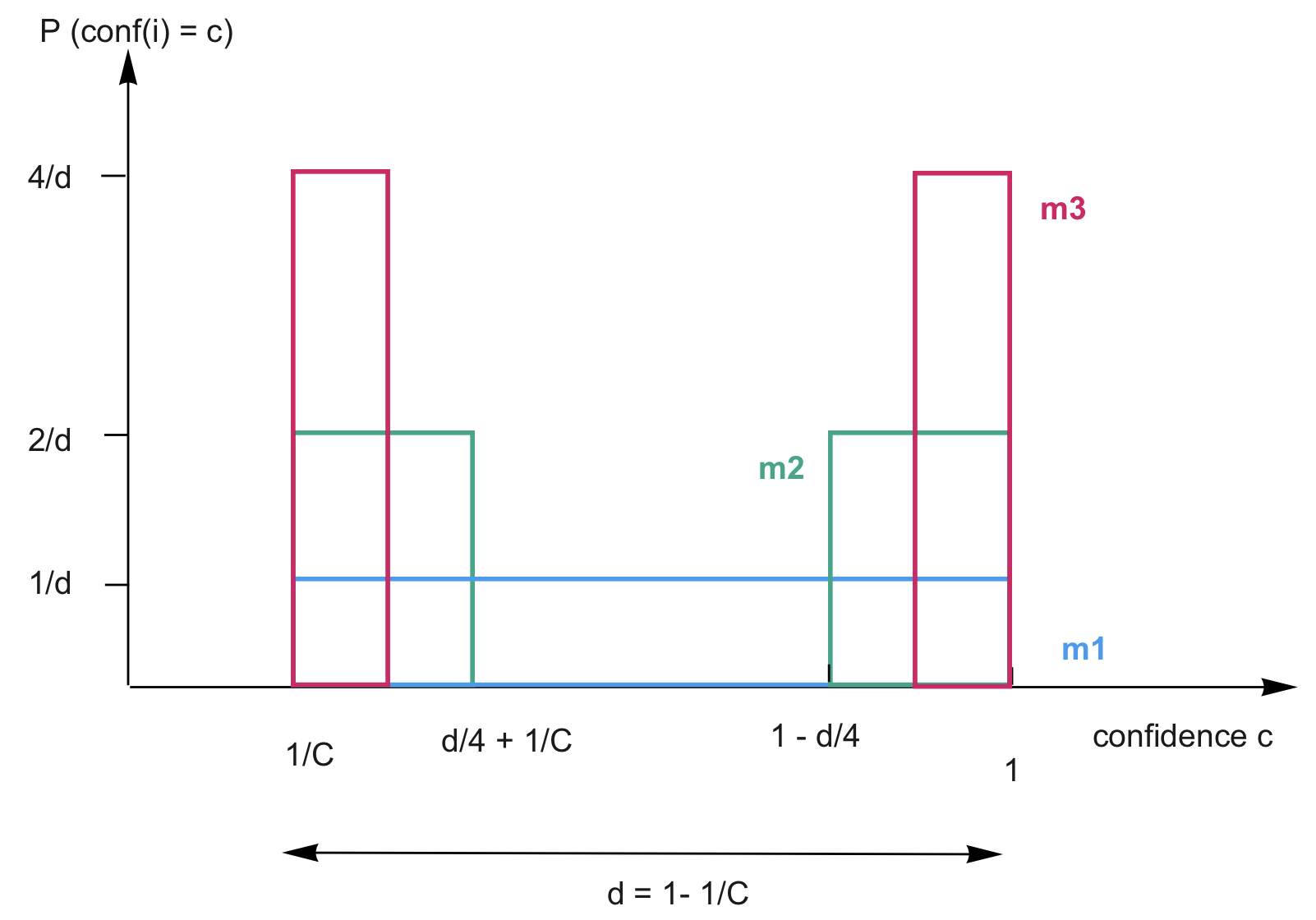

The importance of confidence and confidence distributions. We argue that the confidence measures of classifiers play a key role in the value of a model (i.e., they are not “just” a way to select the predicted class), and that studying (empirical) confidence distributions—the probability distribution or proportion of items with a given confidence—reveals useful information on the quality of a model.

To see this, consider the three confidence distributions in Fig 2, representing a model that predicts one among C classes (so that the minimal confidence for each prediction is 1/C). Assuming that they are perfectly calibrated, the three models have the same accuracy and, by hypothesis, the same calibration. However, the red classifier model will always have equal of better value, no matter the cost.

What makes more valuable is that it pushes confidence mass towards the edges, which is both good (many calibrated high confidence predictions, on which the model is truly pretty sure about) and bad (many calibrated low confidence predictions, on which the model is truly unsure about), so that the overall distribution of confidence results in a better model. This type of “shove away from the center” is discussed at the end of Sec. 2. One way to summarize those discussions is that if , and were snapshots taken at increasing epochs in a training algorithm, we could safely say that the model is learning, and that what it learns is valuable. Confidence is not only a mean to an end, it is an end of its own.

To some extent research on unknown unknowns focuses on this [9]. However, (i) the problem of unknown knowns may, depending on , be as important, and (ii) the typical definition of unknown unknown (“high confidence errors”) depends on knowing what “high confidence” means, which depends on the threshold and cost. This means that we are back to value functions even when we want to explore the unknown unknowns and unknown knowns space.

Active Learning and Uncertainty Sampling. A question that comes from the above discussion is whether uncertainty sampling [1] is a proper active learning strategy in all cases, or if there are cases where the opposite—“certainty sampling”—would be more valuable. Indeed, for calibrated distributions, we may be more interested to know what is happening above (or not too far below) the threshold .

A natural quantity of interest is the VOC’s Area Under the Curve (VOC AUC) . Ceteris paribus, we likely prefer a model whose VOC AUC is higher than another one. However, it would probably be more informative to report the VOC AUC for different ranges of values of , e.g., and . How many such ranges are desirable and at which values of should we break them are questions that would need to be answered empirically.

References

- [1] Charu C Aggarwal, Xiangnan Kong, Quanquan Gu, Jiawei Han, and S Yu Philip. Active learning: A survey. In Data Classification: Algorithms and Applications, pages 571–605. CRC Press, 2014.

- [2] Peter L Bartlett and Marten H Wegkamp. Classification with a reject option using a hinge loss. Journal of Machine Learning Research, 9(8), 2008.

- [3] Paul Boothe and Debra Glassman. Comparing exchange rate forecasting models: Accuracy versus profitability. International Journal of forecasting, 3(1):65–79, 1987.

- [4] Rich Caruana and Alexandru Niculescu-Mizil. Data mining in metric space: An empirical analysis of supervised learning performance criteria. In Proceedings of the Tenth ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, KDD ’04, page 69–78, New York, NY, USA, 2004. Association for Computing Machinery.

- [5] Filip Chybalski. Forecast value added (fva) analysis as a means to improve the efficiency of a forecasting process. Operations Research and Decisions, 27(1):5–19, 2017.

- [6] Giorgio Fumera, Fabio Roli, and Giorgio Giacinto. Reject option with multiple thresholds. Pattern recognition, 33(12):2099–2101, 2000.

- [7] Yonatan Geifman and Ran El-Yaniv. Selective classification for deep neural networks. In Proceedings of the 31st International Conference on Neural Information Processing Systems, NIPS’17, page 4885–4894, Red Hook, NY, USA, 2017. Curran Associates Inc.

- [8] Heinrich Jiang, Been Kim, Melody Y Guan, and Maya Gupta. To trust or not to trust a classifier. arXiv preprint arXiv:1805.11783, 2018.

- [9] Anthony Liu, Santiago Guerra, Isaac Fung, Gabriel Matute, Ece Kamar, and Walter Lasecki. Towards hybrid human-ai workflows for unknown unknown detection. In TheWebConf’20, pages 2432–2442, 2020.

- [10] Lydia T. Liu, Sarah Dean, Esther Rolf, Max Simchowitz, and Moritz Hardt. Delayed impact of fair machine learning. In Jennifer Dy and Andreas Krause, editors, Proceedings of the 35th International Conference on Machine Learning, volume 80 of Proceedings of Machine Learning Research, pages 3150–3158. PMLR, 10–15 Jul 2018.

- [11] Matthias Minderer, Josip Djolonga, Rob Romijnders, Frances Hubis, Xiaohua Zhai, Neil Houlsby, Dustin Tran, and Mario Lucic. Revisiting the calibration of modern neural networks. CoRR, abs/2106.07998, 2021.

- [12] Hussein Mozannar and David Sontag. Consistent estimators for learning to defer to an expert. In Hal Daumé III and Aarti Singh, editors, Proceedings of the 37th International Conference on Machine Learning, volume 119 of Proceedings of Machine Learning Research, pages 7076–7087. PMLR, 13–18 Jul 2020.

- [13] Fabian Wunderlich and Daniel Memmert. Are betting returns a useful measure of accuracy in (sports) forecasting? International Journal of Forecasting, 36(2):713–722, 2020.

Appendix A Some Caveats of our Definition of “Value”

This Appendix is an non-exhaustive list of possibles ways that the assumptions posited in introductions may not exactly correspond to the reality of the use case.

We posited that the per-sample value was solely dependent on the “true label” and on the prediction of the form (i.e., either a class or for “abstain”).

-

•

Value of confidence. Value could be derived from the prediction’s score in a manner more intricate than whether the prediction should be used or not. For example, a low-ish scored prediction could be used to automatically pre-fill a box in a, but then adding a special flab prompting the user to confirm the value.

-

•

Class-dependent value. The value of “correct” and “wrong” predictions could instead be some matrix whose element is the value of predicting if the correct answer is (i.e., the kind of information captured by a confusion matrix). The value of abstaining could similarly depend on the correct label .

-

•

Ranking/alternatives. If the default behaviour is that the user must select the correct category in a drop-down menu of 1000 elements, providing a top-10 containing the correct entry at a position different than the first may be more desirable.

-

•

Nonlinearity. Equation (2) presumes that value scales linearly with count, but nonlinear scaling is also possible. Indeed, different externalities that were not accounted for in the calculation of the cost may begin to matter when proportion of “wrong” prediction dominates: loss of customer trust, need to hire new staff, supply-chain failure, etc. Such concerns could induce a “dip” in the VOC curve at low .

Please note that our argumentation in the main text is made in view of the caveats listed here: we are aware of these failings, yet we believe our main message to hold true. In particular, focusing too much on the above caveats has caveats of its own.

-

•

“Value”, in a form or another, should play a central role in model benchmarking (and it currently doesn’t).

-

•

For classification problems, our formulation in terms of captures important concerns that are currently neither properly handled by the research community nor the enterprise.

-

•

Classification problems are only one example among many.