Time-of-use Pricing for Energy Storage Investment

Abstract

Time-of-use (ToU) pricing is widely used by the electricity utility to shave peak load. Such a pricing scheme provides users with incentives to invest in behind-the-meter energy storage and to shift peak load towards low-price intervals. However, without considering the implication on energy storage investment, an improperly designed ToU pricing scheme may lead to significant welfare loss, especially when users over-invest the storage, which leads to new energy consumption peaks. In this paper, we will study how to design a social-optimum ToU pricing scheme by explicitly considering its impact on storage investment. We model the interactions between the utility and users as a two-stage optimization problem. To resolve the challenge of asymmetric information due to users’ private storage cost, we propose a ToU pricing scheme based on different storage types and the aggregate demand per type. Each user does not need to reveal his private cost information. We can further compute the optimal ToU pricing with only a linear complexity. Simulations based on real-world data show that the suboptimality gap of our proposed ToU pricing, compared with the social optimum achieved under complete information, is less than 5%.

Index Terms:

ToU pricing, energy storage, two-stage optimization, stochastic programming, storage investmentI Introduction

I-A Background and motivation

Time-of-use (ToU) pricing is a electricity tariff that is widely used by the electricity utility. It can help shave the system peak load and reduce the system overall cost [2]. In ToU pricing, the utility usually divides one day into two or three periods with different electricity prices. In a typical two-period ToU pricing [3], the utility defines a peak period (e.g., 4 PM to 9 PM) and an off-peak period (e.g., 10 PM to 3 PM). The price for the peak period is higher than that of the off-peak period. The ToU pricing can incentivize users to shift elastic loads from the peak period to the off-peak period to reduce their energy costs.

Besides changing the energy consumption pattern, users may further consider investing in energy storage to take advantage of the price difference in a ToU pricing [4]. Specially, during off-peak hours with a lower electricity price, users with storage can purchase more electricity (than the actual needed consumption) and charge it into storage for later use. During peak hours with a high electricity price, users can discharge the storage to partially fulfill their energy demands. In the ideal case, such operations of storage not only reduce users’ electricity bills but also help shave the system peak load and reduce the social cost. Note that although some part of user’s demand may be elastic, there always exists a substantial part of the demand that is inelastic, the latter of which can only be shifted by storage. The ToU pricing itself cannot shift users’ inelastic demand and reduce the system peak load unless with the help of users’ storage.

However, the increasing deployment of energy storage on the end-user side poses new challenges for the ToU pricing design. If the ToU pricing design does not consider the impact of storage, it may lead to new and even higher system peaks. To understand this, note that the storage investment decision depends on both the peak/off-peak price difference and the storage cost. A small price difference (compared with the storage cost) cannot incentivize sufficient storage investment from users. A higher price difference, however, may incentivize too much storage investment. Consider the extreme case where all the users invest in storage and shift the demand from the peak period to the off-peak period, such that the original peak period will have zero demand and the original off-peak period will become a new peak. Both the new peak and the large storage investment cost may increase the social cost. Although the utility may reduce the future price difference in the ToU pricing to flatten the new peak, the sunken cost of storage investment can not be recovered. This increases the social cost and leads to social welfare loss, which also harms users’ interests. Therefore, a proper design of the ToU pricing considering users’ storage investment and operation is critical to the performance of the electricity system.

The above discussions motivate us to answer the key question in this paper:

-

•

How to design a ToU pricing to induce proper users’ storage investment in order to achieve the social optimum?

The challenge for designing such ToU pricing is the private information of individual users’ storage costs, which makes it challenging to incentivize low-cost users to invest in storage while discouraging high-cost users from investing. To address the challenge, we define a set of storage types based on the possible storage costs on the market, and classify users based on such types. We propose a ToU pricing scheme based on each type’s storage cost and aggregate demand, instead of individual users’ private storage cost and demand. Such a ToU pricing scheme does not require users’ private information.

We compare our proposed pricing scheme (without individual users’ private information) against two other cases:

-

•

A ToU pricing scheme assuming knowledge of individual users’ private information.

-

•

The social-optimum benchmark where a social planner decides the storage investment for all users with complete system information.

I-B Main results and contributions

To the best of our knowledge, our paper is the first work that studies the ToU pricing design considering the impact of the end-users’ storage investment. Our results can guide users’ storage investment and operation to minimize the social cost.

To decide the optimal ToU pricing, we formulate a two-stage optimization problem between the utility and users over two timescales. In Stage I, before the investment horizon, the utility determines the peak and off-peak prices for the ToU pricing. In Stage II, at the beginning of the investment horizon, each user decides the optimal investment capacity of storage. Then, in each operational horizon (one day), each user determines the charging and discharging of the storage given the storage capacity and realized load profiles.

In our proposed ToU pricing, the utility only needs to know the storage cost of each storage type, and the aggregate demand of users in each type. It does not require knowledge of individual users’ private cost or demand information. We prove that the social cost under our proposed type-based ToU pricing is higher than that under individual-based ToU pricing, which is further higher than that under a social-optimum benchmark. However, extensive simulations based on real-world data show that our proposed type-based ToU pricing can induce a social cost very close to the social-optimum benchmark.

The main contributions of this paper are listed as follows.

-

•

Storage-aware ToU pricing: As far as we know, this is the first work that studies the ToU pricing design considering the impact of users’ storage investment decisions, with the purpose of achieving social optimum. Such a storage-aware ToU pricing can significantly improve the performance of the electricity system.

-

•

Pricing scheme without private information: The key challenge for designing the ToU pricing scheme is users’ private storage investment costs. We propose a simple yet effective pricing scheme for the utility based on the storage types, which does not require each user’s private information but only each type’s storage cost and aggregate demand. Such aggregation incurs no information loss if users demands’ are perfectly positively correlated.

-

•

Threshold-based algorithm: We formulate a two-stage optimization problem that is non-convex and challenging to solve. Despite such difficulty, we characterize a step-wise structure for the social cost with respect to the price, based on which we design an efficient algorithm to determine the optimal pricing by searching finite threshold points. The number of threshold points is linear in the numbers of demand outcomes and storage types.

-

•

Performance of the proposed pricing scheme: Extensive simulations based on real-world data validate the near-optimal performance of the proposed pricing scheme, where the suboptimality gap comparing with the social optimum is less than 5%. A surprising result is that an increased level of user demand uncertainty (within a certain range) can improve the performance of the pricing scheme by smoothing users’ storage investment decisions.

II Related works

There have been a series of active studies on the design of ToU pricing (e.g., [5, 6, 7]). Chen et al. [5] designed the optimal ToU pricing for households, which minimizes the system peak load and maximizes the utility’s profit. Kök et al. [6] designed the optimal ToU pricing considering the impact of renewable energy investment. Charwand et al. [7] proposed a robust midterm framework to optimize ToU pricing strategies. However, these studies did not consider the impact of end-users’ storage investment, which can significantly affect the system load and the ToU pricing strategy.

Some recent literature considered the optimal storage operation and investment under the ToU pricing (e.g., [8, 9, 10]). Nguyen et al.[8] optimized the operation of energy storage to minimize users’ energy costs under the ToU pricing. Carpinelli et al. [9] proposed a probabilistic method to size the energy storage under the ToU pricing. Kalathil et al. [10] studied the game-theoretic model for storage sharing under the ToU pricing. However, the ToU prices in these prior literature are exogenously given, without considering the impact of users’ proactive decisions in storage investment and operation on the system. To our best knowledge, there has been no literature studying the design of ToU pricing that directly takes into account the end-users’ storage investment decisions.

Multi-stage optimization models have been widely adopted in energy systems (e.g.,[11, 12, 13]). Chen et al. [11] formulated a two-stage model for the central storage sharing between a distribution company and customers. Wei et al. [12] optimized the energy pricing and dispatch for electricity retailers considering users’ demand response. Both [11] and [12] solved the two-stage optimization problem by constructing an equivalent single optimization problem, e.g., a mixed-integer linear programming problem, which requires all the users’ private information and is often solved with high computational complexity. Zhao et al. [13] proposed a distributed algorithm based on the information exchange between Stage I and Stage II, still assuming a truthful report of private information from Stage II. In our work, we design and solve the pricing scheme based on storage types’ information, which does not require any individual users’ private information. We also develop an efficient algorithm by searching a finite number of threshold points, which corresponds to low linear complexity in key system parameters.

III System Model

We consider one electricity utility serving a group of users. The utility sets a two-period ToU pricing for users, with a higher electricity price for the peak period and a lower price for the off-peak period.111Both two-period pricing and three-period pricing exist in practice, and both of them can incentivize the storage investment of end users. Our work focuses on the two-period pricing because it is simple and can always help us demonstrate the impact of ToU pricing on storage investment. We will consider the three-period pricing in the future work.

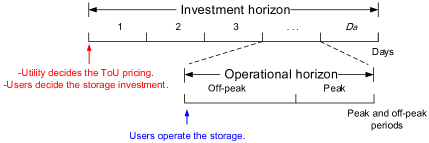

We illustrate two timescales of decision-making between the utility and users in Figure 1. Before an investment horizon of days (e.g., can correspond to many years), the utility announces the ToU pricing to users. Then, at the beginning of the investment horizon, users decide how much storage to invest in.222Note that, in order to show the impact of the utility’s ToU pricing on the users’ storage investment, we focus on a fixed investment horizon and assume that the utility’s ToU pricing shares the same time horizon as the investment horizon of users’ storage. The utility can make the ToU pricing decision sometime before the investment horizon but the ToU price should be effective over the whole investment horizon. The investment horizon is divided into operational horizons. Each operational horizon corresponds to one day, which is further divided into two periods : the peak period and the off-peak period . Each peak period and off-peak period can contain multiple hours. During each day, each user utilizes storage to minimize his energy cost through proper charging and discharging decisions. Next we will introduce the detailed models for users and utility.

III-A Users

We consider a group of users that face the ToU pricing from the utility. Based on ToU pricing, users can invest and operate the storage to shift the demand and reduce the electricity bill. Next, we introduce the model of users’ demands and storage costs.

III-A1 Demands

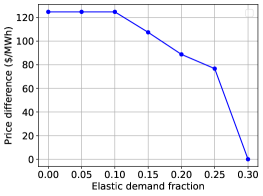

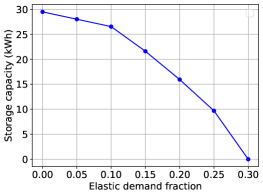

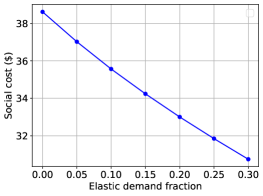

Users’ electricity bills only depend on the total demand at peak and off-peak periods. For each user, his peak and off-peak demands vary across days, so we model each user’s peak and off-peak demands for one day as random variables. We let denote the random demand of user in one day, where and denote his peak and off-peak demands, respectively. We denote the vector of all the users’ peak and off-peak demand as . We assume that the random variable has CDF with a range , . Across all the users, we assume a general joint CDF for the random vector , where users’ demands can be independent or dependent. To examine the impact of storage, we focus on the users’ inelastic demands [14] in the main text.333In Appendix.H, we generalize our model to incorporate the elastic demand, and provide additional simulation results about the impact of elastic demand. Our high-level finding is that additional elastic demand with a low shift cost will reduce users’ demand for storage but benefit the social welfare. Note that each user’s load depends on both his inelastic demand and storage operation. When a user charges the storage, his load is higher than the demand. When a user discharges, his load is smaller than his demand.

III-A2 Storage cost

Users can have heterogeneous storage costs, as they can choose different storage technologies, e.g., Lithium-ion storage or Lead-acid storage [16]. We denote the unit capacity investment cost of storage for user as .

The main cost of storage is the one-time investment cost. To facilitate the optimization problem formulation, we convert the one-time unit investment cost into a daily cost according to based on a scaling factor . To derive , we first calculate the present value of an annuity (a sequence of equal annual cash flows) with the annual interest rate , and then we divide the annuity equally to each day. This leads to the following formulation of the factor

| (1) |

where is the number of years over the total time horizon, and is the number of days (e.g., 365) in one year. For example, Tesla Powerwall’s price is 6500$ for 13.5 kWh with the warranty of 10 years [17]. Here, if we set the annual interest rate , we can calculate . Then, kWh.

III-B Electricity utility

The utility sets the ToU pricing for users and bears the energy supply cost of meeting users’ demand. We assume that the utility is regulated [14], which aims to maximize the social welfare, i.e., minimize the social cost. Next, we introduce the model of ToU pricing and supply cost for the utility.

III-B1 ToU pricing

The ToU pricing is announced once and is valid for the entire investment horizon. We assume that peak hours and off-peak hours are given as parameters, with hours for the peak period and hours for the off-peak period, where . For example, the peak period can be set from 4PM to 9PM and the off-peak period can be from 10PM to 3PM[3], hence and . Such division is based on the historical observations of the energy loads in the network. The utility decides the electricity price for the peak period and the price for the off-peak period for all users, with .

III-B2 Energy supply cost

We consider a quadratic supply cost, which is commonly used for thermal power plants [6].

Note that the power consumption here is the aggregated load in the system. The supply cost for power in hour is given by , where the coefficients , and are based on practical measurements given in the literature, such as in [18].

Our model focuses on the two-period ToU pricing in practice, which charges users based on their total demands in the peak period and off-peak period, respectively. The two-period pricing does not directly regulate users’ demand in each hour. To calculate the supply cost based on the total demand in the peak and off-peak periods, we adopt an approximation of constant load in each period. Specifically, we approximate the power of the peak period and off-peak period (with multiple hours) by the average power (in MWh per hour) in these periods, respectively. For example, for the peak period of 12 hours with total load 12 MWh, we use an average load of 1MWh per hour. The main purpose of such an approximation is to capture the load difference between the peak period and off-peak period for the two-period pricing structure.444Based on realistic data, we can show that such an assumption of two-period constant power can still provide a good approximation for the more elaborate model of 24-hour variable load in terms of the supply cost. The supply cost under the 2-period constant-load approximation has a small gap of 6.2% comparing with the supply cost computed based on the 24-hour variable load. This shows that the 2-period constant-power approximation is quite accurate in terms of predicting the total supply cost. We show more details about this approximation in Appendix.G. Then, for the peak period, if the total load is in the system, the average load is approximated by . The total peak period’s supply cost is given by

| (2) |

Similarly, the total supply cost for the load in the off-peak period is

| (3) |

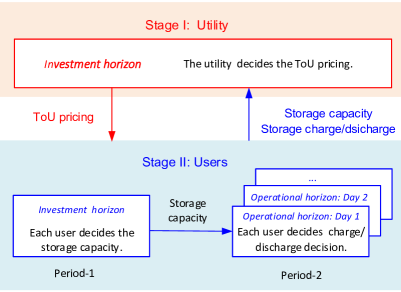

IV Two-stage optimization formulation

To decide the optimal ToU pricing, we formulate a two-stage optimization problem between the utility and users, as illustrated in Figure 2. Recall that we consider two timescales of decision-making: investment horizon and operational horizon. In Stage I, before the investment horizon, the utility decides the peak and off-peak prices of ToU pricing to minimize the social cost. In Stage II, at the beginning of the investment horizon (Period-1), each user decides the storage capacity to invest in. Then, for each operational horizon (Period-2), each user decides the storage charging and discharging decision. Each user aims to minimize his expected energy cost over the investment horizon.

We can model such a two-stage optimization problem as a dynamic game with incomplete information. The challenges of analyzing such a game are twofold. First, the social cost includes individual users’ storage investment costs, which can be users’ private information not known by the utility. Second, the utility’s optimization problem is non-convex even if the utility knows individual users’ private information.

To solve the private information problem, we will first define the storage types based on statistical information of storage costs. Then, we formulate a pricing problem for the utility based on the type information, which does not require users’ private information. To solve the two-stage optimization problem, later in Section V, we will first characterize the structure of the social cost for the utility based on backward induction and then propose an efficient algorithm by searching a finite set of threshold points.

IV-A Storage type

We consider a set of storage types, corresponding to different storage costs available in the market. The unit daily cost of storage capacity for type is . We rank the storage types in an increasing order of the storage costs, i.e., . Each user’s type is determined by the storage type that he can obtain. Multiple users can belong to the same type.

Similar to the individual user’s demand, we denote random daily aggregate peak and off-peak demand for a (user or storage) type as and , respectively. We let be the vector of the random daily demand for type , and let be the vector of all types’ peak and off-peak demand. We assume that the random variable has a CDF over the support of , where . Across all the types, we assume a joint CDF for the random vector .

We consider two different information structures for the utility. In the first case, the utility knows each individual user’s storage cost and demand distribution. In the second more realistic case, the utility only knows each type’s storage cost and aggregate demand distribution, without knowing each individual user’s information. Such aggregated information can be obtained through surveys, historical data of storage incentive programs[19], or market share of different storage products [20].

Under the two information structures, we propose the following two pricing schemes for the utility. The first one (PI) is based on each Individual user’s information and the second one (PT) is based on each Type’s information.

-

•

Pricing scheme based on individual’s information (PI): In Stage I, the utility decides the ToU pricing based on each individual user’s storage cost and joint demand distribution among users. In Stage II, each user decides the optimal storage capacity and operation based on the ToU pricing and individual user’s demand information.

-

•

Pricing scheme based on type’s information (PT): In Stage I, the utility decides the ToU pricing based on each type’s storage cost and joint demand distribution among types. In Stage II, each type decides the optimal storage capacity and operation based on the ToU pricing and the type’s demand information.

Note that for both pricing schemes PI and PT, after receiving the ToU pricing, each individual user will invest and operate the storage based on his own storage cost and demand in practice. In PT, when the utility designs the ToU pricing in Stage I, it considers each type’s information and predicts its storage investment decisions as an aggregate in Stage II. However, once the ToU pricing is announced, each individual user still makes his own storage investment decision based on his own information based on the ToU pricing. Therefore, compared with PT, the pricing scheme PI is more accurate in designing the ToU pricing. However, it requires each user’s private information, which can be difficult to implement in practice. In PT, the utility only needs to know each type’s aggregated demand and storage cost. In this sense, the pricing scheme PT is more flexible than PI and requires less information, which we refer to as “information loss”. As a result, the pricing scheme PT can only achieve a sub-optimal performance in designing the ToU pricing compared with PI.

The modeling and solution method are similar for the pricing schemes PI and PT, so we will focus on the discussion of PT. To derive the modeling and solution method of PI, we just treat each user as one type, by replacing each type ’s information and decisions variable in PT by each user ’s information and decision variable , respectively. In Sections VI and VII, we will also compare the performance of PI and PT with the social optimum.

IV-B Stage II: Type ’s cost minimization

In Stage II, each type needs to make decisions in two periods. In period-1, i.e., at the beginning of the investment horizon, each type decides the optimal storage capacity. In period-2, i.e., for each operational horizon (day), based on the invested capacity, each type decides the optimal storage charging and discharging decision for each demand realization.

The overall objective of each type is to minimize its energy cost (scaled into one day), which includes the electricity bill and the cost of storage investment (scaled into one day). We first introduce types’ storage investment cost and electricity bill, and then formulate types’ optimization problem.

IV-B1 Storage investment cost

At the beginning of the investment horizon, type decides the invested storage capacity . Recall the unit daily capacity cost of storage for type denoted by per day. Thus, type ’s daily storage cost is .

IV-B2 Electricity bill

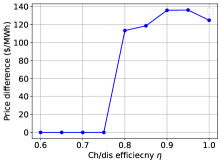

We will first discuss the electricity consumption of types with storage, and then calculate the electricity bill. For each realization of random demand , in the off-peak period, if type purchases amount of energy from the utility only for the purpose of charging the storage,555The payment in ToU pricing is based on the total energy consumption in peak and off-peak periods, which does not consider demand variation across hours. Thus, we use only to denote the total charge and discharge energy. We assume types’ charge and discharge of storage across hours can be regulated by the utility [19], so as to smooth the system load. the total electricity consumption from the utility will be . Here, the charge decisions is constrained by storage capacity, i.e., . As a result, in the peak period, the total consumption from the utility will be .666We do not consider the negative demand in the current model, i.e., we do not allow types to sell back energy from the storage to the utility [19]. All the energy charged into the storage during the off-peak period will be discharged to serve demand in the peak period.777In the main text, we consider the perfect charge and discharge efficiency, and no degradation cost of the storage. We generalize our model in Appendix.I, which further incorporates the imperfect charge and discharge efficiency as well as linear degradation cost (with respect to charge and discharge amount). Then, type ’s electricity bill is for a demand realization . Therefore, given the storage capacity , type minimizes the electricity bill in Period-2 for each demand realization as follows.

| (4) | ||||

| s.t. | (5) | |||

| (6) | ||||

Given the pricing , we denote type ’s optimal charging decision as for the demand realization .

Combining the storage investment cost and electricity bill, we formulate Problem PT-Stage-II for type , which minimizes its total energy cost (scaled to one day).

Problem PT-Stage-II: Type ’s Cost Minimization

| (7) | ||||

| s.t. | (8) | |||

| var: |

Problem PT-Stage-II is a two-period stochastic programming problem, which will be solved in Section V. Given the ToU pricing , we denote the optimal solution of type ’s storage capacity as .

IV-C Stage I: Utility’s pricing problem

Before the investment horizon, the utility decides the optimal ToU pricing and for all the types, which aims to minimize the social cost (scaled into one day).

The social cost includes the total storage investment cost and the supply cost for satisfying types’ demands. The storage investment cost over the investment horizon is , where is type ’s storage capacity in Stage II. The supply cost is based on all the types’ aggregated load profiles as well as the storage charging and discharging decisions over the operational horizon. For each demand realization , the supply cost is .

We formulate the utility’s optimization problem PT-Stage-I under the pricing scheme PT as follows.

Problem PT-Stage-I: Type-based Pricing for Social Cost Minimization

| (9) | ||||

| s.t. | (10) | |||

| var: |

where the invested capacity , and charging and discharging decision are type ’s decisions in Stage II.

In the next section, we solve the two-stage problem through backward induction. We first characterize the solution in Stage II, and then solve the utility’s pricing problem in Stage I.

V Solution method for utility’s pricing problem

The utility’s pricing problem is non-convex with the two-stage hierarchical structure and challenging to solve [21]. We adopt backward induction and characterize the solution structure to solve the problem. We will first characterize each type’s optimal solution (in Stage II) under an arbitrary fixed ToU pricing. Then, we incorporate types’ decisions into Stage I to characterize the properties of the social cost, and propose an algorithm to determine the optimal ToU pricing. We present the proofs of all mathematical results in Appendix.A-D.

For the solutions in both Stage II and Stage I, we will first consider a general distribution of type’s demand, and then focus on a discrete distribution of type’s demand. The discrete distribution is much more common in the decision-making of electricity planning based on the realistic data of load and renewable energy [22]. The discrete distribution can also make the computation tractable, as we will show that the utility only needs to search a set of threshold points, the size of which is linear in the number of demand outcomes and types. Furthermore, even given a continuous distribution, we can approximate it using the discrete distribution [23][24].

V-A Storage deployment solution of Stage II

We will first solve the Stage-II problem under a general distribution of type’s demand. Then, we focus on the solution under a discrete distribution of type’s demand.

V-A1 Storage deployment under a general demand distribution

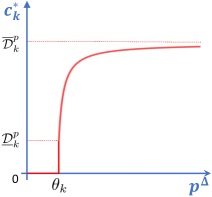

We define the price difference between peak and off-peak price as . We characterize the optimal storage capacity and charging/discharging decision of type in Stage II as a functions of in Proposition 1.

Proposition 1 (type ’s optimal solution with a general demand distribution).

Under a given , the optimal solution of Stage II is as follows.888Here we adopt the generalized inverse distribution function: , which can be applied to the case when the CDF is not strictly increasing, e.g., for discrete random variables.

-

•

Period-1 for :

-

–

If , .

-

–

If , .

-

–

If , can be any value in

-

–

-

•

Period-2 for at any demand realization : .

Proposition 1 shows that when the price difference is lower than the storage cost , the type will not invest in any storage. When the price difference is higher than the storage cost , the optimal storage capacity is increasing with the price difference , and is bounded by the type’s maximum peak demand. Figure 3(a) illustrates the optimal capacity as a function of , when the CDF of peak demand is strictly increasing and continuous.

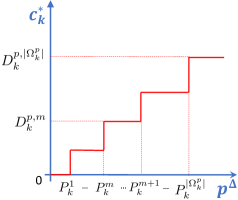

V-A2 Storage deployment under discrete demand distribution

We define the discrete random variable of type over a sample space , where . Each outcome , for , occurs with probability . We denote the sample space of the joint peak and off-peak demands across all the types as .

To characterize the solution of type , we first sort the outcomes of its peak demand in an increasing order, i.e., We characterize the type’s optimal solution in Proposition 2. For ease of exposition, we define , and if . We later also use for for simplicity.

Proposition 2 (Type ’s optimal solution with discrete demand distribution).

Given a fixed , the optimal solution of Stage II is as follows.

-

•

Period-1 for :

-

–

If , .

-

–

If , for :

-

*

, if there exists such that and .

-

*

can be any value in , if there exists such that .

Note that the optimal always exists.

-

*

-

–

-

•

Period-2 for : .

Proposition 2 shows that the optimal storage capacity is a step-wise function of the price difference . For type ’s step-wise function , we construct the set of thresholds points for as follows.

| (11) |

We let . Note that .

We illustrate such a step-wise property in Figure 3(b). The optimal storage capacity increases in a step-wise fashion as the price difference increases. When the price difference is higher than the threshold , the invested capacity is the maximum value of the peak demands in the sample space. Note that at each positive threshold-price point, the optimal invested capacity is not unique.

V-B Solution method of Stage I

According to the solution of Stage II, only the price difference will affect the types’ decisions. Thus, in Stage I, the utility only needs to decide the optimal price difference , while the specific peak price and off-peak price can be flexibly adjusted for regulating the utility’s profit.

V-B1 Pricing under a general demand distribution

It is highly challenging to solve the utility’s problem PT-Stage-I based on the general distribution of demands. Since we have closed-form solutions of Stage II and reduce two pricing variables of (peak and off-peak) into one variable of price difference , we can perform a heuristic exhaustive search by discretizing to find a close-optimal value of .

V-B2 Pricing under discrete demand distribution

Based on the step-wise structure of the types’ decisions in Stage II as shown in Proposition 2, we further analyze the structure of the social cost as a function of the price difference . We then propose an efficient algorithm to achieve the social optimum.

First, we show a step-wise structure of the social cost with respect to the price difference in Theorem 1, which is due to the step-wise solution structure in Stage II.

Theorem 1 (Step-wise structure of social cost).

Under types’ optimal decisions in Stage II, the social cost is step-wise in the price difference , with the threshold set .

Based on Theorem 1, we propose Algorithm 1 that searches all the threshold prices to find the social optimum. Specifically, the utility first calculates the set of threshold prices from each type , which can be executed in a distributed fashion at the type side based on equation (11) (Steps 2-5). Then, the utility searches all the threshold prices from the threshold-price set to obtain the optimal one (Steps 6-18). Note that there can be multiple solutions for at each threshold price. To eliminate the ambiguity, we choose a sufficiently small parameter . The utility will search over for each . Among those search steps 6-18, given the announced price difference (Step 8), each type computes and report the optimal storage deployment decisions in a distributed fashion (Steps 9-12). Finally, the utility computes the optimal that minimizes the social cost (Step 19).

When we consider types and outcomes in the sample space of the joint demand distribution across types, the utility needs to search at most threshold prices to find the optimal value. Therefore, the computational complexity is . Note that Algorithm 1 is for the pricing scheme PT. The algorithm for PI is similar by replacing each type’s information and decisions with each user.

VI Performance analysis of the pricing scheme

To examine the performance of the pricing schemes PT and PI, we first formulate a benchmark problem SO, where a social planner centrally decides and controls the optimal storage investment and operation decisions for each user. Then, we present theoretical comparisons among PI, PT, and SO. Finally, we characterize the upper bound for the ratio between the social cost under PT and the social optimum under SO, when the storage costs approach zero or are sufficiently high.

VI-A Benchmark: Social optimum

For the benchmark problem SO, we consider two periods as in Section IV. In Period-1, i.e., before the investment horizon, the social planner decides the optimal invested storage capacity for each user. In Period-2, i.e., for each operational horizon, the social planner decides the optimal charging and discharging decisions for each user.

Benchmark SO: Social Optimum by Social Planner

| (12) | ||||

| s.t. | (13) | |||

For each demand realization of , we have

| (14) | ||||

| s.t. | (15) | |||

| (16) | ||||

| var: |

It is challenging to solve Benchmark SO based on the general demand distribution. Fortunately, based on the discrete demand distribution, Benchmark SO is a quadratic programming problem whose optimal solution can be efficiently solved[25]. For the continuous demand distribution, we can adopt discrete approximations for computation [23][24].

We will compare social costs under the pricing schemes PI and PT with that of the benchmark SO. We denote the social costs induced by PT, PI, and SO as , , and , respectively. Although in the pricing scheme PT, the utility decides the pricing based on types’ information, the actual social cost is calculated based on each individual user’s storage decision in response to the announced ToU pricing. We show the comparison of social costs in Proposition 3.

Proposition 3 (Social costs comparison).

The social costs of the three schemes satisfy

Proof: The optimal storage investment and operation decision induced in the pricing scheme PI is a feasible solution to Benchmark SO. Thus, we must have .

Note that the social cost is always calculated based on the individual users’ information. In the pricing scheme PI, the utility designs the ToU pricing based on individual users’ information. Thus, the social cost is optimal under the ToU pricing. Thus, we always have . Overall, we obtain .∎

The gap between PT and PI is due to the information loss during the aggregation of user’s demands of each type. The gap between the pricing scheme PI and the benchmark SO is because the ToU pricing may not achieve the social optimum. Next, we show some theoretical results for the gaps between PT, PI, and SO.

VI-B Gap analysis among PT, PI, and SO.

VI-B1 Comparison between PT and PI

The difference between PT and PI is affected by the correlation of users’ demand in each type. In each type, if users’ peak demands have perfect positive correlations, the pricing scheme PT will be equivalent to PI, since no information is lost in the aggregation. In Appendix.F, we will further present numerical results when users’ peak demands are negatively correlated or weakly positively correlated, which shows that a stronger positive correlation will reduce the gap between the pricing schemes PT and PI.

VI-B2 Comparison between PI and SO

In our simulation results in Section VII, we find that the pricing schemes PT and PI often achieve social costs very close to the benchmark SO. One reason behind such results is that PI and PT can lead to a similar storage investment structure among storage types, as in the benchmark SO.

To illustrate the insights, we first present the storage investment structure of different storage types under the benchmark SO in Proposition 4.

Proposition 4 (Investment structure of SO).

In the benchmark SO with for each user , we denote the number of users who invest in storage at the optimal solution as . These users belong to storage types. Then, the storage costs of those users must be the lowest costs in the system. Users can also be classified into three classes.

-

•

for any user with , the optimal capacity satisfies ;

-

•

for any user with , ;

-

•

for users with , .

We denote the users with the storage cost as the boundary users, who are the highest-cost users that invest in positive storage capacity. The boundary users’ optimal investment capacity can be any value between . Next, we present the storage investment structure of storage types for the pricing scheme PI in Proposition 5.

Proposition 5 (Investment structure of PI).

In PI, we denote the number of users who invest in storage at the optimal solution as . These users belong to storage types. Then, the storage costs of those users must be the lowest costs in the system. Further, users can be classified into two classes.

-

•

for any user with , the optimal capacity satisfies ;

-

•

for any user with , .

The pricing scheme PT induces the same structure as PI. Comparing Propositions 4 and 5, we can see that the pricing scheme PI (or PT) can induce a structure of storage investment for users very similar to the benchmark SO. In both cases, the low-cost users will invest in a capacity within their peak-demand range, while the high-cost users will invest in no storage.

However, there are two differences between PI (or PT) and SO. First, compared with SO (Proposition 4), there is no so-called boundary users in PT or PI (Proposition 5) due to the limitation of ToU pricing in inducing social optimum. Second, when demands vary across days, the invested capacity can be different between PT, PI and SO, even though they all follow similar structures. In the special case when the peak demand is fixed across days, i.e., for each user , each user’s storage investment in PI (or PT) will be the same as SO, except the possible boundary users [1]. In this case, in PI (or PT), each user will either invest in zero capacity or the amount of peak demand (all-or-nothing).999For the deterministic demand, we design a contract in the conference paper [1] for users to minimize the social cost considering the boundary-user impact. Later in Section VII, we will present simulation results that show the impact of the demand variance on the performance of PI and PT.

VI-C Performance bound

As the pricing scheme PT is the easiest to implement, we are interested in characterizing its relative performance to the benchmark. We define as the ratio between the social costs under the pricing scheme PT and under the social-optimum benchmark SO. We characterize upper bounds of for two special cases: (i) the storage costs approach zero and (ii) the storage costs are sufficiently high. Later in Section VII, we will show more simulation results for the ratio under different storage costs using realistic data.

Proposition 6 considers the case where users’ storage costs approach zero.

Proposition 6 (Zero storage cost).

When each user’s storage cost approaches zero, is upper-bounded as follows.

The upper bound is tight.

Proposition 6 shows that the worst upper-bound of the ratio is 2, when , i.e., the number of peak hours equal to the number of off-peak hours. If the gap between and is large, the upper-bound is close to 1 and the scheme PT is close to the social optimum. We can construct an extreme example where only one type has positive peak demand in each demand realization, such that can reach the upper bound. We show the example in detail in Appendix.D.

Then, when each user’s storage cost is sufficiently high, the ratio will be 1 since no users will invest in any storage in both the pricing scheme PT and the benchmark SO.

Proposition 7 (High storage cost).

When each user’s storage cost is higher than a certain threshold, will be 1.

Later in Section VII, we will show more simulation results of under different storage costs using realistic data.

VII Numerical Study

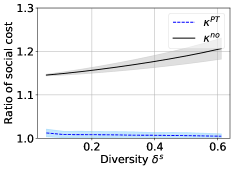

We use the realistic data of users’ demand in Austin and New York, US [26] to perform the simulation. We will first show the importance of designing the ToU pricing considering the storage impact. Then, we show that the pricing scheme PT achieves good performance with the ratio always lower than 1.05. Finally, we investigate the impact of demand variance on the performance of PT and PI, where a higher demand variance may improve the performance.

VII-A Simulation setup

VII-A1 Load profile

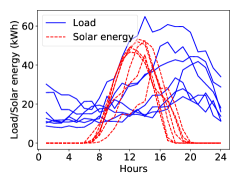

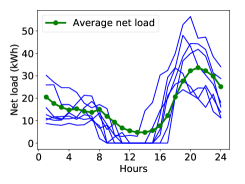

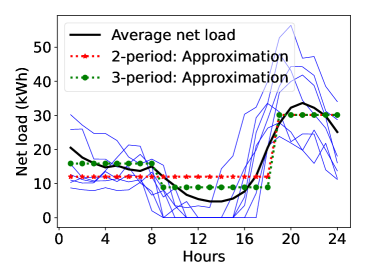

Based on the Pecan Street load dataset [26], we consider hourly load and solar energy generations of 16 (households) users in one year (with valid data for 361 days) from Austin (USA). In Figure 4(a), we show the aggregate energy profile with seven randomly picked days in one year, where the blue curves and red curves represent the aggregate loads and solar energy generations, respectively. In Figure 4(b), we show the aggregate net load (load minus solar energy)101010We let users curtail the surplus renewable energy in simulations. of seven randomly-picked days (blue curves). We also show the mean value of the entire year data in the green curve. We construct users’ demand distribution based on their net load data of the entire year, e.g., 361 joint demand outcomes with a probability 1/361 for each.

VII-A2 Peak and off-peak periods of ToU pricing

Based on the average net load of all users in Figure 4(b), we empirically set the peak period from 18:00 to 00:00 (7 hours), and the off-peak period from 01:00 to 17:00 (17 hours).

VII-A3 Storage cost

We consider 4 storage types with the corresponding (daily) investment costs of . The mean value of the storage costs is . The coefficient indicates the level of storage-cost diversity among types.111111Storage costs can be very diverse. According to [27], the compressed-air energy storage (CAES) has cheap capital costs about 53-84$/kWh, with the lifespan of 20-100 years. The Lithium battery’s cost is high. Typically, Tesla Powerwall’s price is 6500$ for 13.5 kWh, with the warranty of 10 years [17].

VII-B Social welfare loss due to an improperly designed ToU pricing scheme

We show that a properly designed ToU pricing scheme can incentivize users’ storage investment and reduce the social cost, while an improper one may fail to incentivize users’ storage investment and even lead to a much higher social cost compared with no storage in the system.

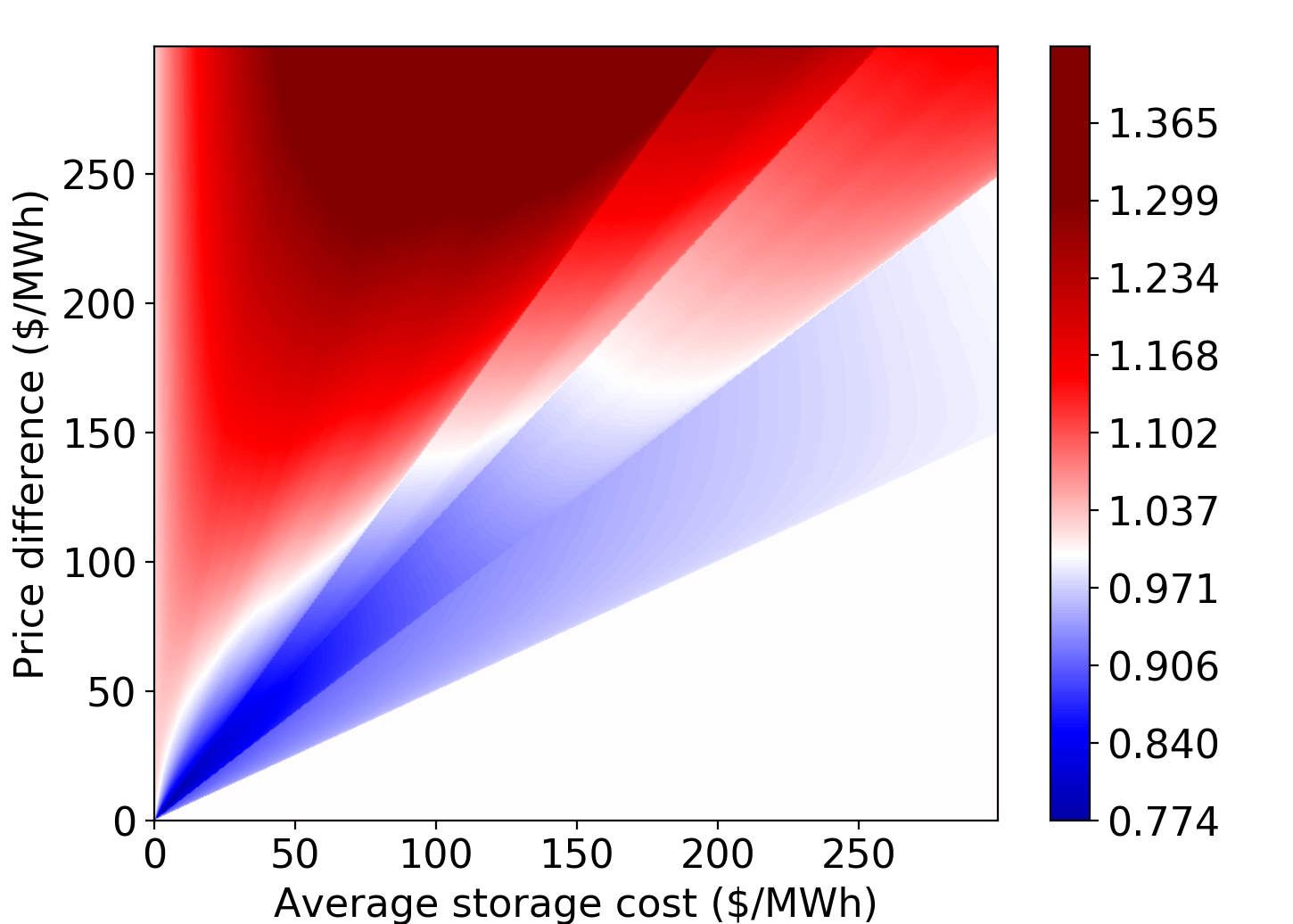

We examine a ratio between the social cost under various ToU pricing (affecting users’ storage investment decisions) and the social cost under no storage in the system. In Figure 5, we show the ratio in different colors under different price differences and different average storage costs.

We can see that the figure can be divided into 3 parts: (a) white region in the bottom right; (b) red region in the upper left; (c) blue region in the middle. In the white region (a), the price difference is low compared with the storage cost. Thus, users will not be incentivized to invest in any storage in the ToU pricing and the ratio is 1. In the red region (b), the price difference is high compared with the storage cost. This leads to the over-investment of storage in the system and the ratio is higher than 1 (sometimes even higher than 1.35). This shows that an improperly designed high price difference can lead to the over-investment of storage and a much higher social cost, compared with no storage in the system. In the blue region (c), the price difference is not too high or too low, so it can incentivize proper storage investment to reduce the social cost, which drives the ratio below 1 (sometimes even lower than 0.78). Note that between the red region () and blue region (), there is a transition of small white space (), where the social cost under the positive amount of storage investment is equal to the no-storage case.

In summary, in the ToU pricing, a price difference that is too low can not incentivize storage investment, while a price difference that is too high will incentivize too much investment. They can both lead to a high social cost compared with a properly designed price difference in the ToU pricing.

VII-C Performance of the pricing scheme PT

We will first show the optimal ToU pricing in the scheme PT. Then, we show that the pricing scheme PT can achieve a good performance with an empirical close to 1. Furthermore, we find that the performance is robust across different data sets, different average storage costs , and different storage cost diversities , where is always less than 1.05.

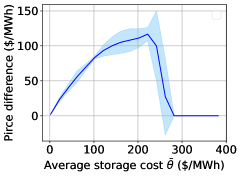

VII-C1 Optimal price difference

In Figure 6(a), we show the optimal price difference as the average storage increases. We report the overall results for 50 random groupings of 16 users into 4 types using Austin data. We show the mean value of optimal price difference as well as the one-standard-deviation range (in shades).

In Figure 6(a), we can see that the optimal price difference first increases (when $/MWh) and then decreases (when $/MWh) as the average storage cost increases. The reason is that, when the storage cost is close to zero, the optimal price difference should also be close to zero, otherwise it will cause the over-investment of storage. As the storage cost increases, the price difference will also increase to incentivize the storage investment. However, if the storage cost is too high, the storage investment is no longer beneficial to the social welfare, so the optimal price difference will decrease to prevent users’ storage investment.

VII-C2 Good performance of PT

We will first show the social costs in the pricing scheme PT, the social-optimum benchmark, and no-storage case, respectively. Then, in order to more clearly show the good performance of PT, we examine the ratios between the social cost in PT and the social cost in the social-optimum benchmark.

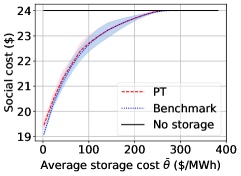

In Figure 6(b), considering 50 random groupings of 16 users into 4 types using Austin data, we show the mean values of social costs under the no-storage case (black curve), under the pricing scheme PT (red curve), and under the social-optimum benchmark (blue curve). We also show the one-standard-deviation range (in shades). We can see that the social costs under the pricing scheme PT (red curve) and under the social-optimum benchmark (blue curve) both increase with the average storage cost . These two costs are very close. When the storage cost is too high ($/MWh), no storage will be invested under both PT and the social-optimum benchmark, which will be the same as the no-storage case.

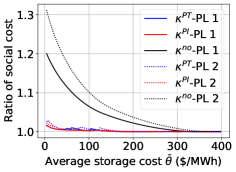

Then, to further show the good performance of PT, we examine the ratios between the social costs. Similar to the definition of ratio , we define as the ratio between the social costs under PI and under the benchmark SO, and as the ratio between the social costs under no storage in the system and under the benchmark SO.

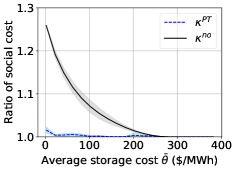

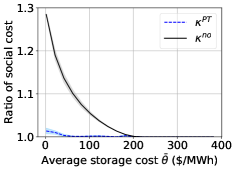

In Figure 7(a), we randomly group 16 users into 4 types. We show the ratios (black curves), (blue curves), and (red curves), which vary as the average storage cost increases. The solid curves correspond to the actual penetration level of solar energy as in the data set. The dotted curves correspond to the setting when we double the solar energy amount comparing with the actual data, which can represent the future situation when the renewable energy penetration level is high. While Figure 7(a) reports the results for one grouping, Figure 7(b) reports the overall results for 50 random groupings of 16 users into 4 types,121212 To facilitate the computation with multiple random grouping results, we adopt a scenario-reduction method that reduces the original 361 outcomes (days) to 100 outcomes [28]. where both the mean ratios (black curve) and (blue curve) as well as the one-standard-deviation range (in shades) are shown.131313In Figures 7(b)-(d), we focus on the case of double solar energy amount. Figure 7(b) shows the results using the Austin data, while Figure 7(c) shows similar results using the New York data. In Figures 5(a)-(c), we fix and vary the average storage cost . Instead, in Figure 5(d), we vary the storage cost diversity while fixing /(MWh).

We have the following observations based on Figure 7.

Observation 1: The pricing scheme PT can achieve a good performance with an empirical ratio lower than 1.05.

To see this, note that the ratio in one-standard-deviation range (blue curves with shades) is lower than 1.05 in all subfigures. Such good performance is also robust across different average storage costs (in Figure 7(b)), different data sets (in Figure 7(b) and Figure 7(c)), and different storage cost diversities (in Figure 7(d)). Furthermore, PT performs as well as PI (comparing the blue and red curves in Figure 7(a)).

Observation 2: Compared with the case of no storage investment in the system, the PT scheme can incentivize proper storage investment and significantly reduce the social cost.

Indeed, in all subfigures the ratio (black curves) is much higher than 1, while the ratio (blue curves) is close to 1. Furthermore, our pricing scheme can reduce the social cost more significantly compared with no storage, if the solar energy penetration level is high (comparing the dotted and solid curves in Figure 7(a)). The reason is that more solar energy further reduces the load in daytime hours, which makes the system peak load more significant. Thus, a larger storage capacity can shift load and reduce the social cost.

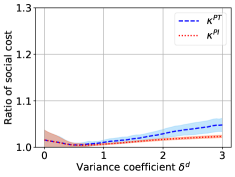

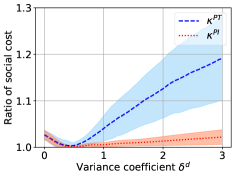

VII-D Impact of demand variance on the performance of PT

Intuitively a higher demand uncertainty may cause a larger gap of storage investment between the ToU pricing and the social optimum, which can reduce ToU pricing’s performance. However, counter-intuitively, we find that the ratios and are not monotonic in the demand variance, where both ratios first decrease and then increase in the demand variance.

To see this, we will first describe how we adjust the variance of each user’s peak demand under one demand distribution. Then, we generate different demand distributions based on realistic data and synthetic data so as to examine the average results among different distributions. Finally, we report the mean value of ratios and with respect to the demand variance among different distributions.

VII-D1 Demand variance adjustment

Under a given distribution of demand, we adjust the original peak load of each user and each outcome to . Here, is the mean of user ’s peak demand. We adjust the variance of the off-peak demand in the same way. Note that we control the variance of demand through the parameter . When , the demand is deterministic at the mean. When , the load is just the same as the original one in the data set. The case means that we increase each outcome’s demand variance comparing with the original data, while the case means that we reduce the variance.

We set up different distributions based on both realistic data and synthetic data. Realistic data is the data used as in Section VII.B and synthetic data for users’ demand is generated uniformly within a range so as to capture the generality. We present the details in Appendix.E.

VII-D2 Results

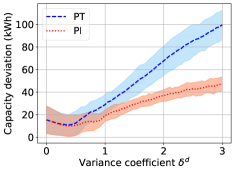

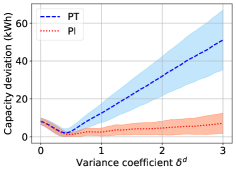

In Figure 8, we show the average ratios (blue curves) and (red curves) as well as the one-standard-deviation range (among different distributions) as the variance coefficient increases. Figure 8(a) is based on realistic data, while Figure 8(b) is based on synthetic data. In Figure 9, we show the absolute value of how much the total invested storage capacities under PT (blue curve) and PI (red curve) deviate from the total capacity under the benchmark SO, respectively, as increases. Similarly, we show the mean value and one-standard-deviation range, where Figure 9(a) is based on realistic data and Figure 9(b) is based on synthetic data. We have the following observation.

Observation 3: A larger demand uncertainty may decrease the ratios and , i.e., improving the relative performance of PT and PI comparing with the social optimum.

As shown in Figure 8, the ratios and are non-monotonic in the demand variance. In both Figures 8(a) and 8(b), when is high (e.g., ), both the ratios and increase in . This might seem intuitive as a higher uncertainty in demand leads to a higher gap of the invested storage capacity between ToU pricing PT (PI) and the benchmark SO, as shown in Figure 9 (e.g., ). This leads to a higher gap of social costs. However, when is low (e.g., ), an increased can reduce and as shown in Figure 8. This is due to the smoothed boundary-user impact, which we explain below.

Recall the discussions in Propositions 4 and 5 that there are boundary users in the benchmark SO but no such users in PT (or PI). Thus, in PT, under a deterministic peak demand of (), any user can only invest in either or 0 amount of energy storage (Proposition 5). However, in the benchmark SO, the boundary users may be required to invest in a storage amount between (Proposition 4). This can lead to a large gap between PT and SO. In contrast, when the demand is random, the boundary-user effect may diminish. For example, under a random demand over the support of with a mean value , a user can invest in 0, or any capacity in the range of depending on the PT pricing. This gives users more investment choices compared with all-or-nothing investment in the deterministic or near-deterministic case. As a result, the gap between the investment capacities under PT (PI) and SO also decreases. Figure 9 illustrates such a decreasing gap, where the capacity deviation of PT and PI from the benchmark decreases as increases in .

VIII Conclusion

This paper designs an optimal ToU pricing explicitly considering the impact of users’ storage investment. We formulate a two-stage optimization problem between the utility and users to minimize the social cost. Since the utility may not know individual users’ private information, we propose a pricing scheme for the utility based on the storage type information. We design an efficient algorithm for the utility to determine the optimal price difference of ToU pricing, which only involves searching over a finite set of threshold prices. Simulations based on realistic data demonstrate the good performance of our proposed pricing scheme. We also find that when the demand variance is low, an increased variance range may improve the performance of the ToU pricing by smoothing the all-or-nothing storage investment.

References

- [1] D. Zhao, H. Wang, J. Huang, and X. Lin, “Contract-based time-of-use pricing for energy storage investment,” in Proc. of IEEE SmartGridComm, 2020, pp. 1–6.

- [2] Y. Hung and G. Michailidis, “Modeling and optimization of time-of-use electricity pricing systems,” IEEE Trans.on Smart Grid, vol. 10, no. 4, pp. 4116–4127, 2019.

- [3] “Time of use plans,” accessed on 2020.5.20. [Online]. Available: https://www.sce.com/residential/rates

- [4] A. J. Pimm, T. T. Cockerill, and P. G. Taylor, “Time-of-use and time-of-export tariffs for home batteries: Effects on low voltage distribution networks,” Journal of Energy Storage, vol. 18, pp. 447–458, 2018.

- [5] S. Chen, H. Alan Love, and C. Liu, “Optimal opt-in residential time-of-use contract based on principal-agent theory,” IEEE Transactions on Power Systems, vol. 31, no. 6, pp. 4415–4426, 2016.

- [6] A. G. Kök, K. Shang, and Ş. Yücel, “Impact of electricity pricing policies on renewable energy investments and carbon emissions,” Management Science, vol. 64, no. 1, pp. 131–148, 2018.

- [7] M. Charwand and M. Gitizadeh, “Optimal tou tariff design using robust intuitionistic fuzzy divergence based thresholding,” Energy, vol. 147, pp. 655–662, 2018.

- [8] T. A. Nguyen and R. H. Byrne, “Maximizing the cost-savings for time-of-use and net-metering customers using behind-the-meter energy storage systems,” in NAPS, 2017, pp. 1–6.

- [9] G. Carpinelli, F. Mottola, and D. Proto, “Probabilistic sizing of battery energy storage when time-of-use pricing is applied,” Electric Power Systems Research, vol. 141, no. 1, pp. 73–83, 2016.

- [10] D. Kalathil, C. Wu, K. Poolla, and P. Varaiya, “The sharing economy for the electricity storage,” IEEE Transactions on Smart Grid, vol. 10, no. 1, pp. 556–567, 2019.

- [11] H. Chen, Y. Yu, Z. Hu, H. Luo, C. Tan, and R. Rajagopal, “Energy storage sharing strategy in distribution networks using bi-level optimization approach,” in IEEE PES General Meeting, July 2017, pp. 1–5.

- [12] W. Wei, F. Liu, and S. Mei, “Energy pricing and dispatch for smart grid retailers under demand response and market price uncertainty,” IEEE Transactions on Smart Grid, vol. 6, no. 3, pp. 1364–1374, May 2015.

- [13] D. Zhao, H. Wang, J. Huang, and X. Lin, “Virtual energy storage sharing and capacity allocation,” IEEE Transactions on Smart Grid, vol. 11, no. 2, pp. 1112–1123, 2020.

- [14] D. S. Kirschen and G. Strbac, Fundamentals of power system economics. John Wiley & Sons, 2018.

- [15] H. Wang and J. Huang, “Joint investment and operation of microgrid,” IEEE Trans. on Smart Grid, vol. 8, no. 2, pp. 833–845, March 2017.

- [16] M. Fisher, J. Apt, and J. F. Whitacre, “Can flow batteries scale in the behind-the-meter commercial and industrial market? a techno-economic comparison of storage technologies in California,” Journal of Power Sources, vol. 420, no. 1, pp. 1–8, 2019.

- [17] “Tesla powerwall,” accessed on 2021.3.12. [Online]. Available: https://electrek.co/2020/10/01/tesla-tsla-increases-powerwall-price-demand/

- [18] L. Wu, “A tighter piecewise linear approximation of quadratic cost curves for unit commitment problems,” IEEE Transactions on Power Systems, vol. 26, no. 4, pp. 2581–2583, Nov 2011.

- [19] “Discover the self-generation incentive program,” accessed on 2019.12.2. [Online]. Available: https://www.selfgenca.com/home/resources

- [20] “Energy storage market - growth, trends, and forecast (2020 - 2025),” accessed on 2019.12.8. [Online]. Available: https://www.mordorintelligence.com/industry-reports/energy-storage-market

- [21] B. Colson, P. Marcotte, and G. Savard, “An overview of bilevel optimization,” Annals of operations research, vol. 153, no. 1, pp. 235–256, 2007.

- [22] T. Dai, “Optimum bidding of renewable energy system owners in electricity markets,” in Optimization in Renewable Energy Systems. Elsevier, 2017, pp. 117–158.

- [23] J. Kennan, “A note on discrete approximations of continuous distributions,” University of Wisconsin-Madison, 2006.

- [24] J. Kazempour, P. Pinson, and B. F. Hobbs, “A stochastic market design with revenue adequacy and cost recovery by scenario: Benefits and costs,” IEEE Transactions on Power Systems, vol. 33, no. 4, pp. 3531–3545, 2018.

- [25] A. Altman and J. Gondzio, “Regularized symmetric indefinite systems in interior point methods for linear and quadratic optimization,” Optimization Methods and Software, vol. 11, no. 1-4, pp. 275–302, 1999.

- [26] “Dataport from pecan street,” acessed on 2020.5.20. [Online]. Available: https://dataport.cloud

- [27] P. Ralon, M. Taylor, A. Ilas, H. Diaz-Bone, and K. Kairies, “Electricity storage and renewables: Costs and markets to 2030,” International Renewable Energy Agency: Abu Dhabi, United Arab Emirates, 2017.

- [28] H. Heitsch and W. Römisch, “Scenario reduction algorithms in stochastic programming,” Computational optimization and applications, vol. 24, no. 2, pp. 187–206, 2003.

![[Uncaptioned image]](/html/2112.06358/assets/figure/DongweiZhao.jpg) |

Dongwei Zhao (M’21) received the B.S. degree from Zhejiang University, Hangzhou, in 2015, and the Ph.D. degree from The Chinese University of Hong Kong, Hong Kong, in 2021. He is currently a postdoctoral associate in MIT Energy Initiative, Massachusetts Institute of Technology. His main research interests are in the optimization and game theory of power and energy systems. More information at https://sites.google.com/view/joris-zhao |

![[Uncaptioned image]](/html/2112.06358/assets/figure/HaoWang.png) |

Hao Wang (M’16) received the Ph.D. degree from the Chinese University of Hong Kong, Hong Kong, in 2016. He was a Postdoctoral Research Fellow with Stanford University and a Washington Research Foundation Innovation Fellow with the University of Washington. He is currently a Lecturer with the Department of Data Science and Artificial Intelligence, Faculty of Information Technology, Monash University, Australia. His research interests are in optimization, machine learning, and data analytics for power and energy systems. More information at https://research.monash.edu/en/persons/hao-wang. |

![[Uncaptioned image]](/html/2112.06358/assets/figure/JianweiHuang.jpeg) |

Jianwei Huang (F’16) received the Ph.D. degree in ECE from Northwestern University in 2005, and worked as a Postdoc Research Associate in Princeton University during 2005-2007. From 2007 until 2018, he was on the faculty of Department of Information Engineering, The Chinese University of Hong Kong. Since 2019, he has been on the faculty at The Chinese University of Hong Kong, Shenzhen, where he is currently a Presidential Chair Professor and an Associate Dean of the School of Science and Engineering. He also serves as a Vice President of Shenzhen Institute of Artificial Intelligence and Robotics for Society. His research interests are in the area of network optimization, network economics, and network science, with applications in communication networks, energy networks, data markets, crowd intelligence, and related fields. He has published more than 300 papers in leading venues, with a Google Scholar citation of 14000+ and an H-index of 59. He has co-authored 10 Best Paper Awards, including the 2011 IEEE Marconi Prize Paper Award in Wireless Communications. He has co-authored seven books, including the textbook on ”Wireless Network Pricing.” He is an IEEE Fellow, and was an IEEE ComSoc Distinguished Lecturer and a Clarivate Web of Science Highly Cited Researcher. He is the Editor-in-Chief of IEEE Transactions on Network Science and Engineering, and was the Associate Editor-in-Chief of IEEE Open Journal of the Communications Society. |

![[Uncaptioned image]](/html/2112.06358/assets/figure/XiaojunLin.jpg) |

Xiaojun Lin (S’02 M’05 SM’12 F’17) received his B.S. from Zhongshan University, Guangzhou, China, in 1994, and his M.S. and Ph.D. degrees from Purdue University, West Lafayette, IN, in 2000 and 2005, respectively. He is currently a Professor of Electrical and Computer Engineering at Purdue University. Dr. Lin’s research interests are in the analysis, control and optimization of large and complex networked systems, including both communication networks and power grid. He received the NSF CAREER award in 2007. He received 2005 best paper of the year award from Journal of Communications and Networks, IEEE INFOCOM 2008 best paper award, and ACM MobiHoc 2021 best paper award. He was the Workshop co-chair for IEEE GLOBECOM 2007, the Panel co-chair for WICON 2008, the TPC co-chair for ACM MobiHoc 2009, the Mini-Conference co-chair for IEEE INFOCOM 2012, and the General co-chair for ACM e-Energy 2019. He has served as an Area Editor for (Elsevier) Computer Networks Journal, an Associate Editor for IEEE/ACM Transactions on Networking, and a Guest Editor for (Elsevier) Ad Hoc Networks journal. |

IX Appendix

IX-A Proof of Proposition 1 and Proposition 2

We consider a general demand distribution for type ’s peak demand with the CDF function .

We first analyze the optimal storage operation decision in Period-2 given the storage capacity , and then characterize the optimal storage capacity in Period-1.

First, in Period-2, given the storage capacity , we have for any realization since .

Then, we incorporate in Period-2 into Period-1, and the objective is equivalent to

We will analyze the optimum of function . We take the derivative of with respect to , and have

Note that , which shows the convexity of the function . Therefore, we will have the optimal solution as follows and prove Proposition 1.

-

•

If , .

-

•

If , .

-

•

If , can be any value in .

We can obtain Proposition 2 based on Proposition 1. When we consider the discrete distribution of the peak demand, the CDF function is step-wise. Note that if , the solution takes the value according to the definition of generalized diverse function in Proposition 1. In fact, the optimal investment can be any value within due to the step-wise structure of . ∎

IX-B Proof of Theorem 1

This conclusion is due to that the utility makes decision based on the optimal storage capacity and storage charge/discharge from Stage II. The solution is step-wise in the price difference . The solution is determined by as in Proposition 2, which shows that is also step-wise in the price difference .

The utility’s social cost includes the storage investment cost and energy supply cost. The storage investment cost is determined by all the users’ storage capacity, and the supply cost is determined by the aggregated charge/discharge amount of all users. Therefore, the social cost is also step-wise in the price difference , which has the threshold price set . ∎

IX-C Proof of Proposition 4 and Proposition 5

Proposition 5 can be directly proved by the solution structure in Proposition 2 and Proposition 1. Note that if the price difference is higher than the storage cost of a user, i.e., , the invested capacity is between the lower support and upper support of the peak demand random variable. If the price difference is lower than the storage cost, i.e., , the invested capacity is zero. For the case , we assume that users will also not invest in storage.

We next prove Proposition 4 by the following steps. In Step 1, we show that considering any two users with different storage costs, if the high-cost user invests in a positive capacity, then the low-cost user must also invest in positive capacity. Step 2: We show that if user invests in positive capacity, the capacity cannot be beyond the upper support of the peak demand variable, i.e., . Step 3: Among all users who invest in storage with storage types, for any user with , we show that the optimal capacity is within the lower support and upper support of the peak demand , i.e., . We show the steps in detail as follows.

Step 1: We assume that user invests in capacity and user invests in capacity , where . In this case we can always reduce by a sufficiently small value and increase by corresponding , such that . In this case, the storage investment cost will be reduced while the aggregate charge/discharge amount can remain unchanged. This contradicts the social optimum. Therefore, if users invest in positive capacity, they are with the lowest storage costs.

Step 2: We assume that user invests in capacity . Note that the charge/discharge decision . Thus, we can always reduce to , which will reduce the investment cost without affecting charge/discharge decision. This contradicts the social optimum. Therefore, for any user , we have .

Step 3: Among all users who invest in storage with storage types, for any user with , we assume that . We can always increase by a sufficiently small value such that , while reduce by such that for user with storage cost . In this case, the storage investment cost will be reduced while the aggregate charge/discharge amount can remain unchanged. This contradicts the social optimum. Therefore, for any user with , we have .

We have Proposition 4 proved based on the three steps above. ∎

IX-D Proof of Proposition 6

We will first characterize the upper bound in subsection 1) in this part and then show the upper bound is tight in subsection 2).

IX-D1 Characterize the upper bound

We construct the upper bound based on two sub-optimal solutions of the ToU pricing.

-

•

Low price difference that leads to no storage invested in the system. We denote the social cost as in this case.

-

•

High price difference that incentivizes all the users to invest in storage capacity at the maximum peak demand in the sample space (due to zero storage cost). Then, for each demand realization, the peak demand is totally shifted to the off-peak period. We denote the social cost as in this case.

Thus, we have . We will first derive the social costs , and , respectively, and then we analyze the upper bound for and . We denote the original aggregate peak demand and off-peak demand (with no storage in the system) as and , which are random variables.

First, we have the social costs and as follows.

Then, we characterize the social cost . For the benchmark problem, since the storage cost approaches zero, the storage investment cost can be neglected. Also, the social planner can invest in enough storage capacity to shift the demand. The benchmark problem SO can be reformulated as follows.

| s.t. | |||

We only need to derive the optimal aggregate charge/ discharge decision for each realization of joint random demand. Such a problem is convex, and we can have the solution as follows.

Recall that we assume , which means that the average power in peak period is higher than the average power in off-peak period. We further calculate the social optimum as follows.

| (17) |

Next, we characterize the upper bound for and . We first consider the ratio .

We focus on each demand realization, and have

| (18) | ||||

| (19) | ||||

| (20) | ||||

| (21) |

We define the function , where . We take the first order derivative and have

which shows that always increases over . Note that when , . Thus, we always have

| (22) |

Considering the expectation overall the random variables, we always have

Similarly, for the ratio , we can have

Overall, we will have

IX-D2 Tightness of the upper bound

We construct a special example to show the tightness of the upper bound. We make the following assumptions.

-

•

A1: We consider zero off-peak demand.

-

•

A2: Users’ peak demands in each type have perfect positive correlations such that the pricing scheme PT is equivalent to the pricing scheme PI.

-

•

A3: We assume types for the users, whose joint peak demand distribution across types are constructed as follows.

-

–

We assume outcomes of joint peak demand with equal probability .

-

–

For Outcome , type has peak demand and other types have peak demand .

Outcome 1:

Outcome 2:

Outcome 3:

…

Outcome :

-

–

-

•

A4: We assume that the hourly supply cost only has the quadratic term, i.e., . Thus, the supply cost function for peak demand is and the supply cost function for off-peak demand is .

We next characterize the ratio . First, we calculate the social cost in the benchmark according to (17).

Second, we characterize the optimal ToU pricing that minimizes the social cost. According to Proposition 5, any ToU pricing will always incentive some low-cost types to invest in storage and other high-cost types not to invest in storage. Furthermore, in the constructed example, each user only has peak demand or in his sample space, so each user will either invest in 0 or capacity under the ToU pricing based on Proposition 2. Therefore, we assume that the optimal ToU pricing will incentivize types to invest in storage with capacity , and types not to invest in storage, i.e., based on Proposition 2. We will choose the optimal to get the optimal ToU pricing. In each outcomes, we have

-

•

Type will totally shift the peak demand to off-peak period in each outcome. .

-

•

Type will not shift any demand.

Thus, for any Outcome , , the aggregate peak demand is , and the off-peak demand is in the system. For any Outcome , , the aggregate peak demand is , and the off-peak demand is in the system. Therefore, we can calculate the social cost under such conditions as follows.

Then, we choose the optimal that minimizes to get the optimal ToU pricing. If , we have and . If , we have and . Therefore, the ratio , which shows the upper bound is tight in the worst case. Overall, we have Proposition 6 proved. ∎

IX-E Setup of different demand distributions in Section VII.C

We set up different distributions based on realistic data and synthetic data, respectively.

-

•

Setting 1 with realistic data: We randomly classify 16 users from Austin data set into 4 types. This simulates different demand distributions for types and different storage costs for users based on realistic data.

-

•

Setting 2 with synthetic data: We consider 16 users of 4 types, and each type has 4 users. We set the off-peak demand to zero and vary the joint peak demands across users (with 7 outcomes). For the discrete joint distribution of peak demands across 16 users, we assume 7 outcomes with equal probability. To construct one joint distribution, we uniformly generating peak demand from for each user at each outcome . Based on this, we randomly construct 500 joint peak demand distributions across users.

IX-F Impact of demand correlation within types on the performance of PT

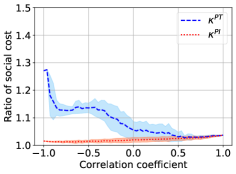

As we discussed in Section VI, the correlation of users’ demand within each type will determine the difference between PT and PI. Next, we show that the positive correlation between users’ demand in each type will cause a lower gap between PT and PI. In the realistic data, most users’ demands are positively correlated, which helps the pricing scheme PT to achieve good performance.

IX-F1 Setup

We consider 8 users of 4 types, and each type has 2 users. We set the off-peak demand to zero and vary the peak demand. We assume the following discrete joint distribution of peak demands across 8 users, which has 7 outcomes with equal probability. In each type, we fix one user’s peak demand distribution, and adjust the other user’s demand by choosing different permutations across different outcomes. For example, in each type, we fix User 1’s peak demand over 7 joint outcomes as

The peak demand distributions of User 1 and User 2 are positively correlated with coefficient 1 if User 2’s peak demand over 7 outcomes is The peak demand distributions are negatively correlated with coefficient -1 if User 2’s peak demand is We choose the same distributions of User 1 and User 2 for all 4 types. We randomly generate 5000 permutations for User 2’s peak demand with . For each permutation, we calculate the ratios and as well as the correlation coefficient of two users. We then report the mean value of the ratios among different permutation results.

IX-F2 Results

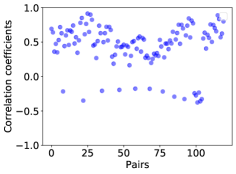

In Figure 10(a), we show the average ratios (in blue curve) and (in red curve) as well as the one-standard-deviation range as the correlation coefficient increases. In Figure 10(b), we show the correlation coefficient of the peak demand distribution between every two users from the 16 users of the Austin data set.

We have the following observations based on Figure 10.

Observation 4: A positive correlation leads to a smaller gap between the pricing PT and PI.

As shown in Figure 10(a), a positive correlation leads to a smaller gap between the pricing schemes PT and PI. When the correlation coefficient is 1, the pricing schemes of PT and PI are equivalent.

Observation 5: Most users’ demands are positively correlated in practice, which can improve the performance of the pricing scheme PT.