Smooth test for equality of copulas

Abstract

A smooth test to simultaneously compare copulas, where is proposed. The observed populations can be paired, and the test statistic is constructed based on the differences between moment sequences, called copula coefficients. These coefficients characterize the copulas, even when the copula densities may not exist. The procedure employs a two-step data-driven procedure. In the initial step, the most significantly different coefficients are selected for all pairs of populations. The subsequent step utilizes these coefficients to identify populations that exhibit significant differences. To demonstrate the effectiveness of the method, we provide illustrations through numerical studies and application to two real datasets.

doi:

10.1214/154957804100000000keywords:

[class=MSC]keywords:

and t1corresponding author

1 Introduction and motivations

Copulas have been extensively studied in the statistical literature and their field of application covers a very wide variety of areas (see for instance the book of [14] and references therein). The problem of goodness-of-fit for copulas is, therefore, an important topic and can deserve many situations as in insurance to compare the dependence between portfolios (see for instance [31]), in finance to compare the dependence between indices (see for instance the book of [7]), in biology to compare the dependence between genes (see [16]), in medicine to compare diagnosis (see for instance [12]), or more recently in ecology to compare dependence between species (see [10]).

In the one-sample case, many testing methods have been proposed in the context of parametric families of copulas (see for instance the review paper of [9], or more recently [23], [6], and [5]).

In the two-sample case, an important reference is the work of [27]. They proposed a nonparametric test based on the integrated square difference between the empirical copulas. Their approach requires the continuity of partial derivatives of copulas which allows to obtain an approximation of the distribution under the null. Their test is convergent and is adapted to independent as well as paired populations, and an R package ’TwoCop’ is available (see [26]).

When , [24] proposed an innovative work to compare copulas. More recently [25] developed a second test statistic with a very original idea based on a generalized Szekely–Rizzo inequality. These tests are consistent and can also be used to test radial symmetry and exchangeability of copulas. However, [24, 25] restricted his study to the case of samples of the same size. More precisely both procedures consist of dividing the sample into sub-samples and testing the equality of the associated sub-copulas. Therefore, testing the equality of copulas from independent samples cannot be achieved by these works. Furthermore, in both cases the null distribution is intractable and the author needs a multiplier bootstrap method to implement these tests. Such bootstrap approach for copulas was initiated in [28]. Another extension of [27] is proposed in [4] when the populations are observed independently, but the proposed test statistic seems to work only for testing the simultaneous independence of the populations.

Recently, [22] studied a nonparametric copula estimator which showed very good numerical results. In this paper, we propose to address the problem of -copulas comparison with a new approach based on such estimators. We do not directly compare the empirical copulas, but we compare their projections on the basis of Legendre polynomials. We restrict our study to continuous variables whose populations can be paired. Then it makes possible to simultaneously compare the dependence structures of various populations, such as various portfolios in insurance, as well as to compare the same population followed over several periods, such as medical cohorts. Moreover, the procedure is valid for the case of several independent samples with different sample sizes, which is important for applications and a novelty compared to the works cited above, even if the works of [24, 25] could certainly be generalized in this direction.

Our method is a data-driven procedure derived from the Neyman’s smooth tests theory (see [21]). These smooth tests are omnibus tests and detect any departure from the null. In our case, we consider the orthogonal projections of the copula densities on the basis of Legendre polynomials and we compare their coefficients. For each pair of populations, a penalized rule is introduced to select automatically the coefficients that are the most significantly different. A second penalized rule selects the number of populations to be compared. Thus the procedure is a data-driven method with two selection steps. Under the null, due to the penalties, the rules select only one pair of populations and only one coefficient, leading to a chi-square asymptotic null distribution. Then the test is very simple and easy to implement. This is another major difference from the work of [24, 25] where the null distribution does not have an explicit form in general and where a multiplier bootstrap is used to calculate the p-values. We also prove that the test procedure detects any fixed alternative and gives us information on the reject decision. More precisely, the second penalized rule is calibrated to detect the populations that differ most significantly. Then in case of rejection, we can find the pairs of populations that contributed the most to the value of the test statistic. We can also proceed to a two-by-two test to search similar populations. In practice, we have developed an R package ’Kcop’ which is available on the Comprehensive R Archive Network (CRAN) to implement the -sample procedure.

A numerical study shows the good behaviour of the test. We apply this approach on two datasets related to biology and insurance. The first one is the very well-known Iris dataset. While this dataset is very famous there was no simultaneous comparison between the 4-dimensional dependence structures of the three species involved. We therefore propose to apply the smooth test to compare the dependence between sepals and petals, thus providing a new analysis. The second dataset is a large medical insurance database with possibly paired data and concerns claims from three years: 1997, 1998 and 1999. We apply the smooth test on several variables from this dataset illustrating the idea of risk pooling and price segmentation. All these results can be reproduced using the ’Kcop’ package.

The paper is organized as follows: in Section 2 we specify the null hypothesis considered in this paper and we set up the notation. Section 3 presents the method in the two-sample case. In Section 4 we extend the result to the () sample case and in Section 5 we proceed with the study of the convergence of the test under alternatives. Section 6 is devoted to the numerical study and Section 7 contains real-life illustrations. Section 8 discusses extensions and connections.

All proofs are located in Appendix A. The adaptation to the dependent case is straightforward and is summarized in Appendix B, where all results are rewritten in this context. A method for automating test parameters is available in Appendix C. Additionally, Appendices D to I contain supplementary materials, including various complements, additional simulations, and comparisons.

2 Notation and null hypotheses

Let be a -dimensional continuous random vector with joint cumulative distribution function (cdf) , and with unique copula defined by

where denotes the marginal cdf of . Writing

we have for all

with . The copula density (if it exists) defined by

coincides with the probability density function (pdf) of the vector . Write the set of orthogonal Legendre polynomials with first terms and , such that is of degree and satisfies (see Appendix D for more details):

where if and otherwise. The random variables are uniformly distributed and we have the following decomposition

| (1) |

where

as soon as exists and belongs to the space of all square-integrable functions with respect to the Lebesgue measure on , that is, if

| (2) |

Write and . We can observe that . Moreover, since by orthogonality we have , for all , we see that if only one element of is non null. When the copula density exists and is square integrable, we deduce from (1) that, for all ,

| (3) |

where , and stands for the set . The sequence will be referred to as the copula coefficients (as in [22]). Since is bounded, all copula coefficients exist. The following result, due to [29] or [17], shows that such a sequence characterizes the copula. Moreover, it shows that assumption (2) is unnecessary.

Proposition 1.

Let and be two sequence of copula coefficients associated to copulas and , respectively. Then

Thereby, the copula is determined by its sequence of copula coefficients, a property that holds even when condition (2) is not satisfied, and the copula density may not exist. Consequently, for any continuous random vectors, the comparison of their copulas coincides with the comparison of their copula coefficients. This equivalence holds true even when the random vectors lack a density or possess densities that are not square-integrable. We will use this characterization to construct the test statistic.

We consider continuous random vectors, namely

with joint cdf , and with associated copulas , respectively. Assume that we observe iid samples from , possibly paired, denoted by

The following assumption will be needed throughout the paper: we assume that for all , , and

| (4) |

Write . Hence, it will cause no confusion if we write when all , and for a series of univariate random variable the notation means that , for all .

We consider the problem of testing the equality

| (5) |

against there exist such that . From Proposition 1, testing the equality (5) remains to test the equality of all copula coefficients, that is

| (6) |

against there exist and such that , where stands for the copula coefficients associated to .

We will denote by the marginal cdf of the th component of and we write

For testing (6), we estimate the copula coefficients by

where , and denotes the empirical distribution function associated to . Such estimators have been extensively studied in [22] where it is shown their excellent behavior. Considering the null hypothesis as expressed in (6), our test procedure is based on the sequences of differences

with the convention that when only one component of is different from zero. This is due to the orthogonality of the Legendre polynomials, leading in such cases.

In order to select automatically the number of copula coefficients, for any vector , we will denote by

the norm and for any integer , we write

The set contains all non null positive integers with norm equal to and such that , for all . We will denote by the cardinality of and we introduce a lexicographic order on as follows:

This order will be used to compare successively the copula coefficients.

3 Two-sample case

We first consider the two-sample case when to detail the construction of the test statistics. We want to test

We restrict our attention to the iid case, the paired case with being briefly described in Appendix B. To compare the copulas associated with and , we introduce a series of statistics derived from the differences between their copula coefficients. Specifically, for , we define

| (7) |

and, for and ,

| (8) |

These statistics are embedded and we have for ,

It follows that

Each statistic contains information enabling the comparison of the copula coefficients and up to the norm and . Consequently, for a large value of , it will be possible to compare the coefficient of high orders using , while the parameter allows the exploration of all values of for the given order. To simplify notation, we write such a sequence of statistics as

By construction, for all integer , each statistic is a sum of elements. More precisely there exists a set , with , such that

| (9) |

It can be observed that if belongs to then . Moreover, we have the following relation: for all and

Notice that we need to compare all copula coefficients and then let tend to infinity to detect all possible alternatives. However, choosing a too large value for can lead to a dilution of the test’s power. Following [15], we suggest a data-driven procedure to automatically select the number of coefficients to test the hypothesis . For this purpose, we set

| (10) |

where and tend to , as , being a penalty term which penalizes the embedded statistics proportionally to the number of copula coefficients used. Roughly speaking, automatically selects the coefficients that exhibit the most significant differences.

Therefore, the data-driven test statistic that we use to compare and is . We consider the following rate for penalty term:

-

(A) , for i=1,2.

Our first result shows that under the null the least penalized statistic will be selected, that is, the first one.

Theorem 1.

If (A) holds, then, under , converges in probability towards 1 as .

It is worth noting that under the null, the asymptotic distribution of the statistic coincides with the asymptotic distribution of , with . In that case, we simply have

It follows that measures the discrepancy between and . This simply means that all other copula coefficients are not significant under the null and are therefore not selected. Asymptotically, the null distribution reduces to that of and is given below.

Theorem 2.

To normalize the test, we consider the following estimator

with

where

Proposition 2.

Under ,

We then deduce the limit distribution under the null.

Corollary 1.

Assume that (A) holds. Under , converges in law towards a chi-squared distribution as .

4 -sample case

We restrict our attention to the iid case here. The paired case is treated in Appendix B.

Our aim is to generalize the two-sample case by considering a series of embedded statistics. Each new statistic will include a new pair of populations to be compared. We will use the first rule (10) to select a potentially different copula coefficient between each pair. A second rule will then be considered to select a possibly different pair between all populations. To select the pairs of populations we introduce the following set of indices:

Clearly, contains elements which represent all the pairs of populations that we want to compare and that can be ordered as follows: we write if , or and , and we denote by the associated rank of in . This can be seen as a natural order (left to right and top to bottom) of the elements of the upper triangle of a matrix as represented below:

We see at once that and more generally, for we have

We construct an embedded series of statistics as follows:

or equivalently,

where is given by (10) and is defined as in (9), replacing the pair index by . We have . The first statistic compares the first two populations 1 and 2. The second statistic compares the populations 1 and 2, and, in addition, the populations 1 and 3. And more generally, the statistic compares pairs of populations. For each , there exists a unique pair such that . To choose automatically the appropriate number of pairs we introduce the following penalization procedure, mimicking the Schwarz criterion procedure [30]:

| (12) |

where is a penalty term. The choice of is discussed in Remark 1. We will need the following assumption:

-

(A’)

The following result shows that, under the null, the penalty will choose the first element of asymptotically. This means that all other pairs are not significantly different under the null and do not contribute to the statistic.

Theorem 3.

Assume that (A) and (A’) hold. Then under , converges in probability towards 1 as .

Corollary 2.

Assume that (A) and (A’) hold. Then under , converges in law towards a distribution as .

Then the final data-driven test statistic is given by

Remark 1.

In the classical smooth test approach (see [18]), the standard penalty in the univariate case is , a choice closely linked to the Schwarz criteria [30] as detailed in [15]. Here, we extend this approach to the multivariate case with the following generalization:

| (13) |

Proposition 5 demonstrates that this choice is sufficient for detecting alternatives. In practical applications, the introduction of the factor serves to stabilize the empirical level, bringing it closer to the asymptotic one. Details on the automatic selection of can be found in Appendix C, offering a straightforward calibration of the test.

It’s worth noting that in [13], a comparison between this Schwarz penalty and the Akaike penalty was conducted. The latter proposes a constant value for or , providing an alternative approach to calibrating the test.

Finally, in the paired case where , we opt for .

5 Alternative hypotheses

We consider the following series of alternative hypotheses: for

The hypothesis asserts that for a given , the populations indexed by and with are the first to exhibit a difference, as per the order defined on ). If , it means that the two first copulas and have at least one different copula coefficient. We will need the following assumption:

-

(B) .

Proposition 3.

Assume that (A)-(A’)-(B) hold. Then under , converges in probability towards , as , and converges to , that is, , for all .

Thus a value of equal to indicates that the first pairs of populations are equal and that a difference appears from the th pair (following the order on ).

6 Numerical study of the test

We choose the penalty , as indicated in Remark 1. In our proofs, we set for simplicity. However, in practice, we enhance this tuning factor empirically using the data-driven procedure outlined in Appendix C.

Concerning the value of , conditions (A) and (A’) are asymptotic conditions and from our experience setting or is enough to have a very fast procedure which detects alternatives where copulas differ by a coefficient with a norm less than or equal to . This parameter can be modified in the package ’Kcop’. In our simulation, we fixed . The nominal level is equal to .

6.1 Simulation design

We consider the following copula families: Gaussian, Student, Gumbel, Frank, Clayton, and Joe Copulas (briefly denoted by Gaus, Stud, Gumb, Fran, Clay and Joe). For the explicit forms and properties of these copulas, we refer the reader to [20]. For each copula , the sample is generated with a given Kendall’s parameter, and we denote it briefly by . When is close to zero the variables are close to the independence. Conversely, if is close to 1 the dependence becomes linear.

In our simulation, we compute empirical levels and empirical powers as the percentage of rejections under the null and alternative hypotheses based on replicates. We consider the following scenarios:

-

•

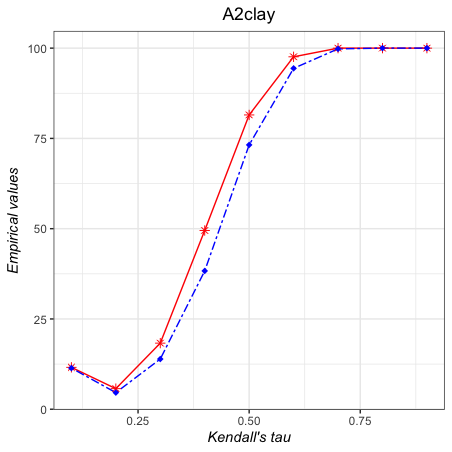

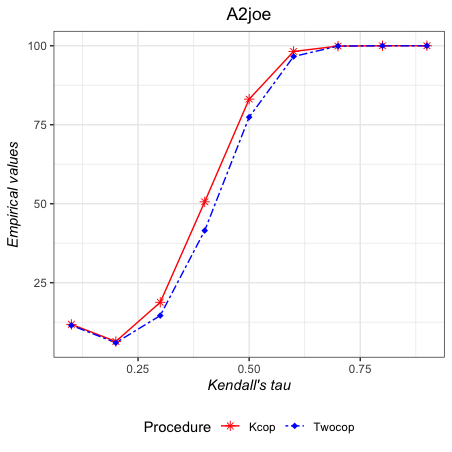

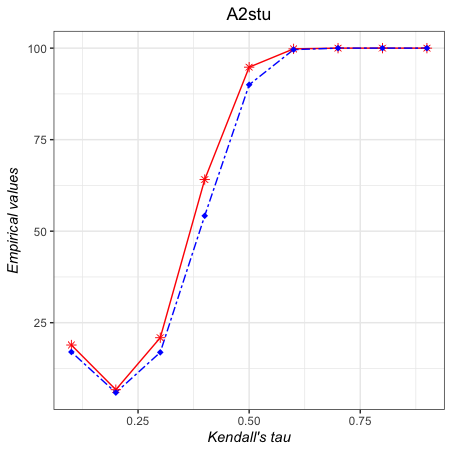

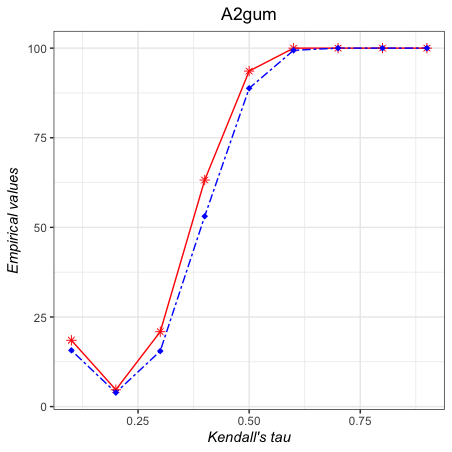

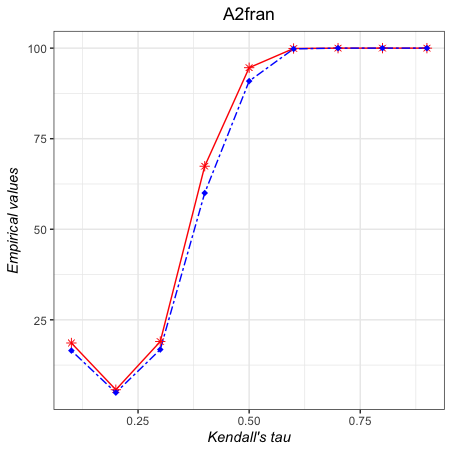

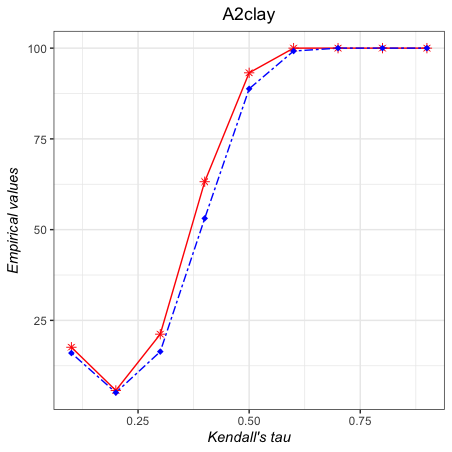

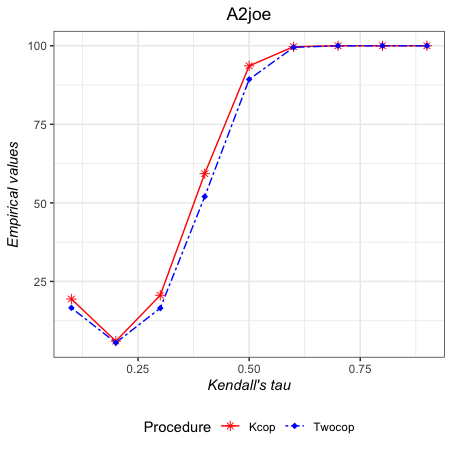

We first consider the two-sample case where we compare our test procedure to that proposed in [27] which is the competitor we found for dependent as well as independent bivariate observations. Both methods give very similar results.

-

•

Then, we consider two cases: a -sample case and a -sample case. In both situations, alternatives are constructed by modifying .

- •

-

•

A -population case is studied where we change copulas, keeping the same .

-

•

Finally an additional simulation study is proposed in Appendix H. We compared three Student copulas with and with or .

6.2 Simulation results in the two-sample case

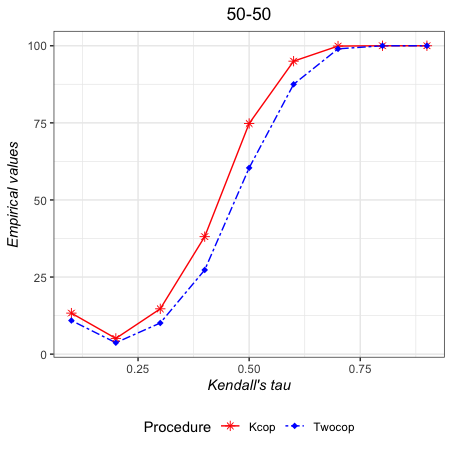

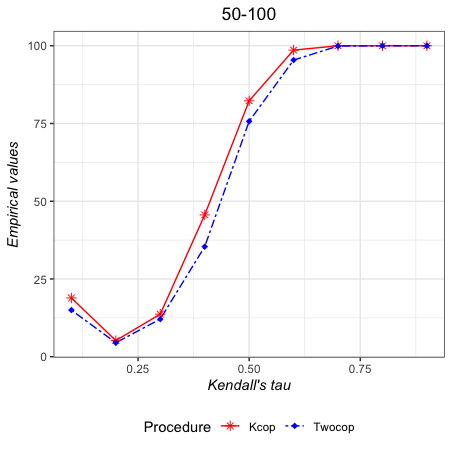

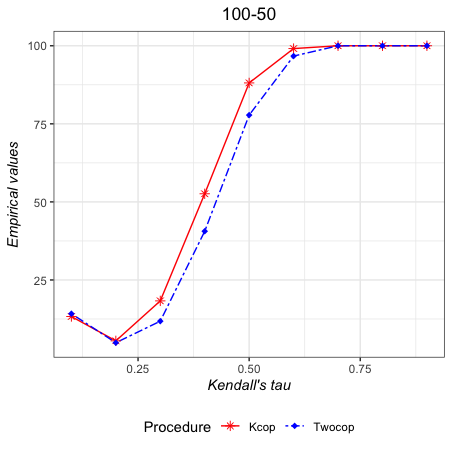

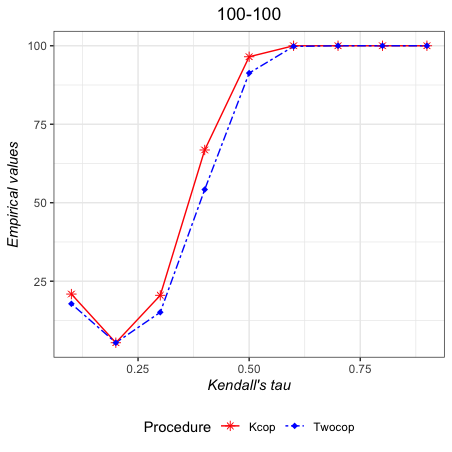

In this case () we consider the procedure of [27] as a competitor. Let us recall that this approach is based on the Cramer-von-Mises statistic between the two empirical copulas and an approximate p-value is obtained through the multiplier technique with replications. They also proposed a R package denoted by Twocop. By extension, we call our R package Kcop.

Here we fix the dimension . The following groups of scenarios are considered:

-

1.

: it includes six alternatives of size which are:

-

•

: and

-

•

: and where is a degree of freedom

-

•

: and

-

•

: and

-

•

: and

-

•

: and

-

•

-

2.

with and

-

3.

with and

-

4.

with and

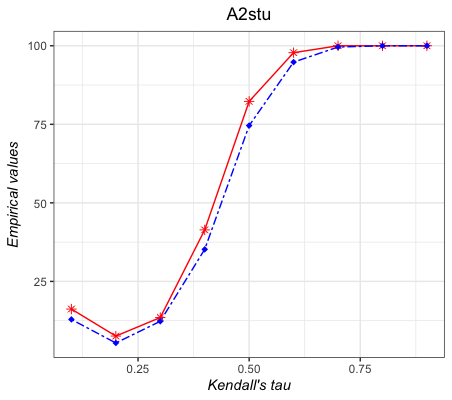

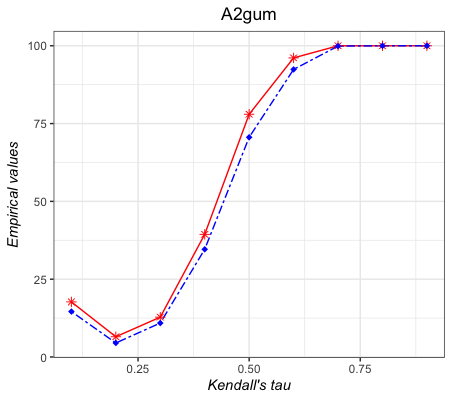

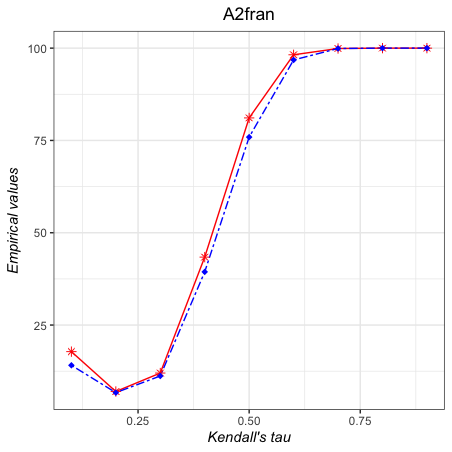

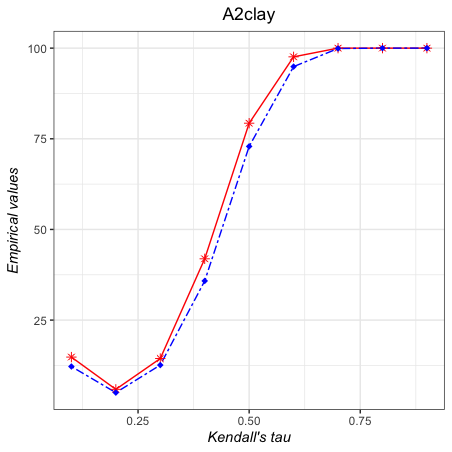

Recall that this methodology to evaluate the finite sample performance was proposed in [27]. We follow their designs with the same sample sizes . Such scenarios coincide with the null hypothesis when .

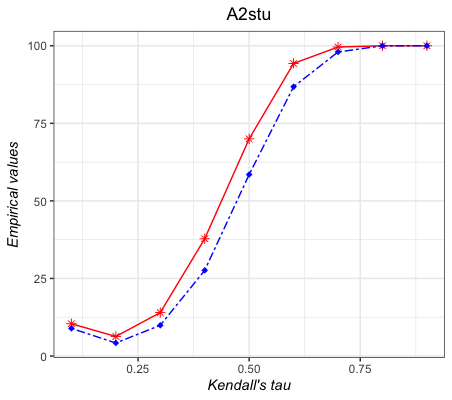

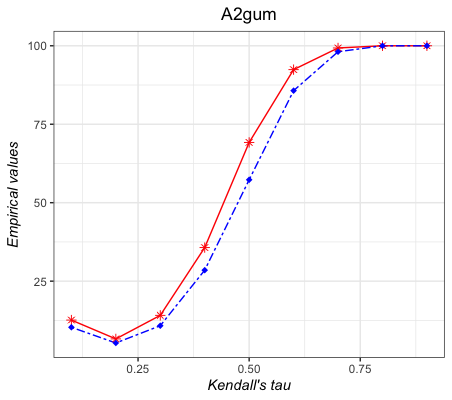

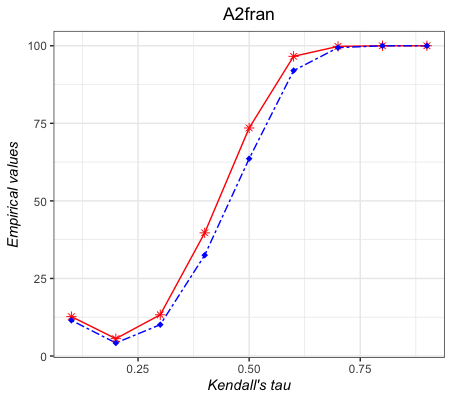

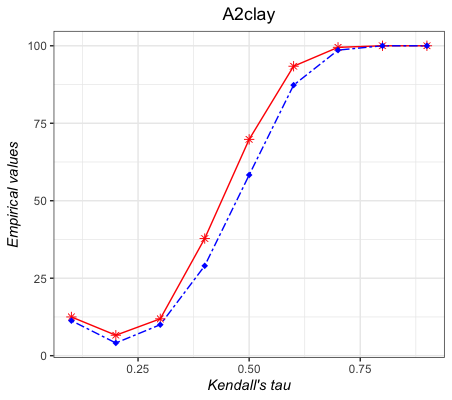

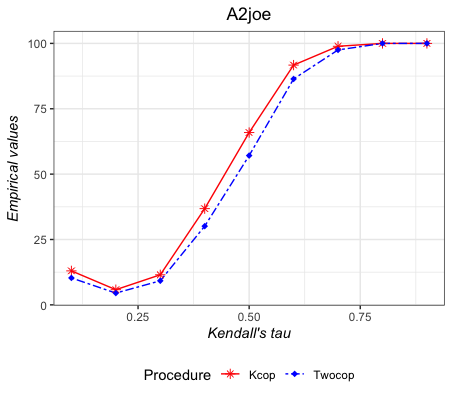

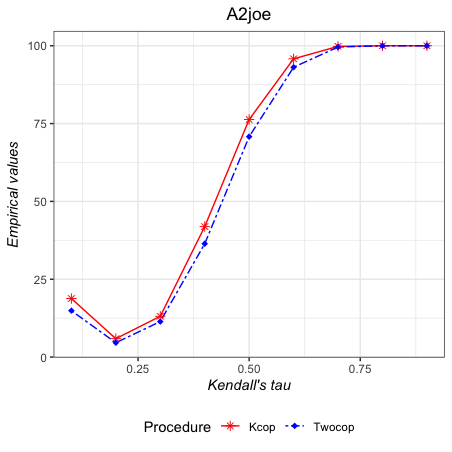

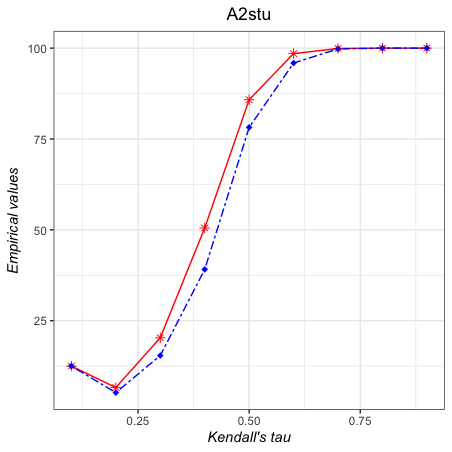

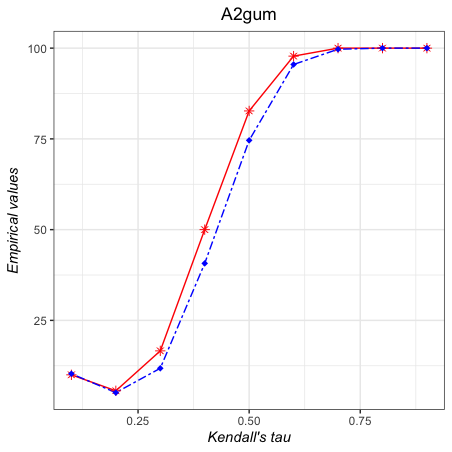

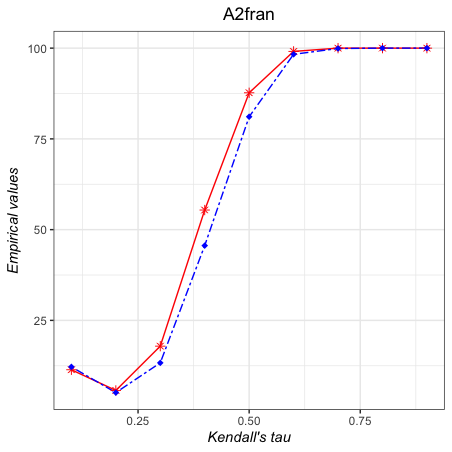

The results are very similar for all scenarios and we present the alternatives in this section, reserving the remaining results for Appendix F. Figures 1-2 illustrate that both methods (Twocop and Kcop) exhibit highly comparable performance. As expected, the more different the Kendall tau, the greater the power. In our simulation, the tau associated with is fixed and equal to 0.2. The tau associated with varies and the power is maximal (100%) when it is greater than or equal to 0.7. Conversely, the power is minimal (approaching 5%) when the tau is set at 0.2, corresponding to the null hypothesis.

6.3 Five-sample case

In this case () we fix and we consider the same size for all samples, that is . We fixed a theoretical level .

Null hypotheses: under the null hypothesis we consider the same copulas (Gaussian, Student with degree of freedom = 17, Gumbel, Frank, Clayton, Joe) with three levels of dependence: (low dependence), (middle dependence) and (high dependence).

Alternatives with different tau: we consider the following alternatives hypotheses with in the same copula family but with different as follows

-

•

Alt1: and

-

•

Alt2: and , and

-

•

Alt3: and , and

Alt1 contains only one different population. Concerning Alt2 and Alt3, they differ solely in their Kendall’s tau, allowing us to highlight its effect.

Table 1 presents empirical levels (in ) with respect to sample sizes when and , respectively. In each case, one can observe that the empirical level is close to the theoretical 5% as soon as is greater than 200. For or , two phenomena emerge: the empirical level appears larger than the theoretical level when is small and smaller than the theoretical level when is large. Hence, with fewer observations, the procedure more readily identifies identical copulas when their dependence structure is stronger. This leads to the following recommendations: for a small size () if the estimation of is close to 0.1, it is advisable to adopt a more conservative approach (choosing a larger theoretical level, e.g., around 0.09). Conversely, if the estimation of is close to 0.9, it is preferable to be anticonservative (choosing a lower theoretical level around 0.02). This implies a slight reduction in power in the first case, while power increases in the second case. A tuning procedure could be considered, incorporating a data-driven criterion based on the estimation of .

| Models | ||||||

| Gaussian | Student | Gumbel | Frank | Clayton | Joe | |

| Kendall tau | ||||||

| 50 | 11.4 | 10.5 | 10.0 | 11.1 | 10.3 | 11.4 |

| 100 | 10.0 | 8.4 | 8.1 | 7.6 | 8.1 | 9.1 |

| 200 | 7.6 | 8.0 | 6.2 | 6.3 | 5.8 | 7.4 |

| 300 | 6.9 | 7.3 | 6.6 | 7.5 | 6.5 | 6.3 |

| 400 | 6.4 | 5.7 | 7.1 | 4.7 | 5.7 | 7.4 |

| 500 | 5.1 | 4.8 | 4.9 | 7.0 | 5.9 | 5.5 |

| 600 | 5.6 | 6.5 | 4.4 | 5.1 | 5.1 | 6.0 |

| 700 | 5.0 | 5.3 | 6.1 | 5.5 | 4.4 | 6.5 |

| 800 | 5.1 | 6.8 | 4.8 | 5.5 | 5.4 | 6.0 |

| 900 | 5.6 | 6.2 | 6.3 | 5.7 | 6.5 | 6.8 |

| 1000 | 5.9 | 5.5 | 6.0 | 5.3 | 5.2 | 5.0 |

| Kendall tau | ||||||

| 50 | 5.4 | 4.0 | 4.0 | 4.1 | 5.0 | 3.2 |

| 100 | 6.0 | 3.7 | 5.0 | 5.4 | 5.1 | 2.8 |

| 200 | 4.9 | 5.0 | 5.6 | 5.5 | 6.0 | 4.8 |

| 300 | 5.7 | 3.9 | 4.6 | 4.9 | 5.6 | 4.0 |

| 400 | 4.7 | 3.9 | 4.9 | 5.1 | 4.6 | 4.6 |

| 500 | 4.4 | 3.6 | 3.6 | 5.5 | 4.4 | 4.5 |

| 600 | 4.8 | 5.0 | 3.2 | 4.2 | 4.7 | 5.5 |

| 700 | 5.4 | 5.5 | 5.0 | 6.0 | 5.0 | 4.6 |

| 800 | 4.9 | 4.6 | 4.6 | 3.7 | 4.5 | 4.4 |

| 900 | 4.6 | 5.0 | 4.2 | 6.1 | 4.2 | 4.0 |

| 1000 | 4.2 | 4.6 | 4.1 | 4.9 | 5.8 | 3.5 |

| Kendall tau | ||||||

| 50 | 1.0 | 0.6 | 0.6 | 0.7 | 3.0 | 0.4 |

| 100 | 2.6 | 1.9 | 2.2 | 2.9 | 4.5 | 1.4 |

| 200 | 4.1 | 3.1 | 3.5 | 3.9 | 5.3 | 3.0 |

| 300 | 4.0 | 3.3 | 4.5 | 3.4 | 5.4 | 2.1 |

| 400 | 3.5 | 3.4 | 4.3 | 4.2 | 5.5 | 3.9 |

| 500 | 4.9 | 3.9 | 3.4 | 3.8 | 4.0 | 3.6 |

| 600 | 4.6 | 3.9 | 4.1 | 4.5 | 5.1 | 4.8 |

| 700 | 4.0 | 5.4 | 4.0 | 4.4 | 5.8 | 3.7 |

| 800 | 4.5 | 4.6 | 5.0 | 5.0 | 4.8 | 4.1 |

| 900 | 4.4 | 4.1 | 3.8 | 5.1 | 4.8 | 4.2 |

| 1000 | 3.7 | 5.4 | 3.8 | 5.6 | 5.4 | 4.1 |

Concerning the empirical power, Tables 2-4 contain all results under the alternatives. We omit some large sample size results where empirical powers are equal to 100%. It is important to note that, even for a sample size equal to , the program runs very fast. It can be seen for alternatives Alt2 and Alt3 that the empirical powers are extremely high even for small sample sizes. The first series of alternatives yields lower empirical powers since only one copula differs with a slight change in .

| Alternatives | ||||||

| Gaussian | Student | Gumbel | Frank | Clayton | Joe | |

| 39.9 | 35.7 | 35.6 | 36.6 | 35.9 | 35.5 | |

| 64.1 | 61.8 | 60.3 | 64.0 | 61.1 | 60.7 | |

| 91.5 | 88.4 | 87.5 | 91.1 | 89.9 | 87.7 | |

| 97.9 | 98.0 | 97.7 | 98.2 | 97.3 | 97.2 | |

| 99.8 | 99.7 | 99.6 | 99.8 | 99.7 | 99.8 | |

| 100 | 100 | 100 | 100 | 100 | 99.9 | |

| 100 | 100 | 100 | 100 | 100 | 100 | |

| Alternatives | ||||||

| Gaussian | Student | Gumbel | Frank | Clayton | Joe | |

| 97.8 | 97.6 | 96.3 | 98.6 | 97.4 | 95.6 | |

| 100 | 100 | 99.9 | 100 | 100 | 100 | |

| 100 | 100 | 100 | 100 | 100 | 100 | |

| Alternatives | ||||||

| Gaussian | Student | Gumbel | Frank | Clayton | Joe | |

| 100 | 100 | 100 | 100 | 100 | 100 | |

6.4 Ten-sample case

Analogously to the previous -sample case, we consider null hypotheses with Gaussian, Student, Gumbel, Frank, Clayton, and Joe copulas. We fixed . We consider the following alternatives where only one copula differs from the others.

-

•

Alt4: and

Empirical levels seem to tend fast to 0.5 and are relegated in Appendix I. Table 5 shows empirical powers under alternatives Alt4. We only treat the cases where and , as beyond these values, all empirical powers are equal to . Remarkably, even for such small sample sizes, we observe very good behavior of the test even with small sample sizes.

| Alternatives | ||||||

| Gaussian | Student | Gumbel | Frank | Clayton | Joe | |

| 98.0 | 96.7 | 96.2 | 97.9 | 97.1 | 97.3 | |

| 100 | 100 | 100 | 100 | 100 | 100 | |

6.5 Alternatives with the same Kendall’s tau

We consider a last alternative hypothesis with which are the six copulas defined in the null hypothesis models above all with the same and with a dimension up to 5 as follows

-

•

Alt5: ; , , , , , , and the dimension .

Empirical powers are presented in Table 6. It can be seen that the power increases with the dimension when the sample size is less than : it is then easier to detect differences between the dependence structures of the vectors. When , the empirical power is stable and equal to in all scenarios.

| Dimension | ||||

| 1.2 | 3.1 | 14.8 | 20.0 | |

| 2.0 | 27.3 | 73.6 | 79.1 | |

| 19.8 | 89.9 | 99.8 | 100 | |

| 60.3 | 100.0 | 100.0 | 100 | |

| 90.9 | 100.0 | 100.0 | 100 | |

| 98.3 | 100.0 | 100.0 | 100 |

6.6 Testing the equality of all the bivariate sub-copulas of copulas

The purpose of this section is to compare the performance of our test with that obtained by [24]. We follow the same design (see Tables 3 in [24]) and we adopt the same notation. More precisely, we simulated data , where is a -dimensional copula and we examine the equality of all the bivariate sub-copulas of , that is

We denote by ) the model where is generated by the -variate normal copula and by the model where is generated by the Student copula with degrees of freedom, where the correlation matrix is such that and for all

We compare our procedure () to the following quadratic functional procedures proposed in [24]:

-

•

Cramér-von Mises () statistic,

-

•

Two characteristic function statistics, denoted as (,), correspond to the weights functions of normal and double-exponential distributions, respectively

-

•

Diagonal statistics (Dia).

We refer the reader to [24] for more detail and to code for the program.

The results are provided in Tables 10 and 11. There is no overarching conclusion that allows determining a superior method. The various statistics seem to yield fairly similar results, except in the case of , where the emprical powers associated with our test statistic appear to be generally superior.

Approaches 4.7 5.2 6.2 6.1 6.0 4.7 3.9 4.7 4.7 4.0 4.1 3.9 4.8 4.6 6.0 4.4 4.6 5.2 5.3 5.0 3.3 4.8 5.7 4.8 4.0 2.9 4.1 3.3 3.8 4.0 3.0 4.4 3.9 3.7 6.0 4.0 5.1 4.3 4.5 6.0 3.4 4.1 5.7 4.9 5.0 2.3 3.0 3.5 3.3 6.0 1.7 4.9 3.5 3.0 6.0 4.4 4.5 6.2 6.1 6.0

Approaches 16.8 15.5 21.3 19.8 22.5 21.8 28.5 26.4 44.2 48.1 48.1 35.0 78.0 75.4 81.2 40.0 51.3 48.9 62.2 58.1 84.1 81.7 90.1 87.7 88.6 92.2 90.7 60.0 84.0 12.0 12.7 17.8 16.1 20.3 21.1 25.2 23.6 40.7 47.7 47.3 45.7 76.7 76.6 79.4 73.0 47.3 48.2 63.0 56.8 85.8 84.7 91.5 88.6 90.1 93.2 92.4 89.0 100.0 99.8 99.9 97.0 9.8 12.0 16.1 14.1 19.6 20.6 27.1 25.0 34.6 41.7 43.9 42.3 74.4 75.5 78.8 77.6 43.4 45.8 57.2 53.5 81.5 80.3 88.9 86.4 86.3 91.7 91.0 90.5 99.8 99.8 99.0

7 Real datasets applications

7.1 Biology data

We analyze Fisher’s well-known Iris dataset. The data consists of fifty observations of four measures: Sepal Length (), Sepal Width (), Petal Length (), and Petal Width (), for each of three Species: Setosa, Virginica, and Versicolor. We then have populations, and the dimension is . The lengths and widths for the three species are represented in Appendix E. In [8] the authors show that multivariate normal distributions seem to fit the data well for all three Iris species. Looking at their mean parameters the 4-dimensional joint distributions seem different but that does not tell us about their dependence structures.

We propose to test the equality of the dependence structure between the four variables in the three-sample case, that is:

We consider the data as possibly dependent, with the same sample size . We then apply the test for paired data. We obtain a p-value close to zero () and a very large test statistic . We reject the equality of the dependence structure here. The selected rank is equal to 2. It means that the most significant difference is obtained when considering the statistics associated with population 1 versus 2 (Setosa and Virginica) and population 1 versus 3 (Setosa and Versicolor).

In case of rejection, we can proceed to an “ANOVA” type procedure, applying a series of two-sample tests. Table 9 contains the associated p-values and we conclude with the equality of the dependence structure between Versicolor and Virginica.

| Setosa | Virginica | Versicolor | |

| Setosa | 1 | 0.0021 | |

| Virginica | 0.0021 | 1 | 0.68 |

| Versicolor | 0.68 | 1 |

7.2 Insurance data

Insurance is an area in which understanding the dependence structure among multiple portfolios is crucial for pricing, especially for risk pooling or price segmentation. To illustrate, we examine the Society of Actuaries Group Medical Insurance Large Claims Database, which contains claims information for each claimant from seven insurers over the period to . Each row in the database presents a summary of claims for an individual claimant in fields (columns). The first five columns provide general information about the claimant, the next twelve quantify various types of medical charges and expenses, and the last ten columns summarize details related to the diagnosis. For a detailed and thorough description of the data available online, refer to [11], accessible on the web page of the Society of Actuaries. In this context, we focus on dimensional variables , where = paid hospital charges, = paid physician charges, = paid other charges, for all claimants insured by a Preferred Provider Organization plan providing exposure for members. This consideration becomes pertinent for risk pooling if the objective is to group together similar charge scenarios or for price segmentation to provide similar guarantees for the charges. We employ a procedure with three scenarios to study the dependence structure of as follows:

Three-sample test, paired case. In this case, we consider the same claimants (paired situation) present over the three periods . At the end of the data processing, we obtained three samples of size observations. We analyse the dependence structure of the charges X between the three years, that is, we test . The test concluded with the non-rejection of the equality of the three dependence structures, as evidenced by a p-value = 0.788, a test statistic of and a selected rank equal to . Hence, the dependence structure of paid for insured over the three years seems to be similar. It can be an argument for keeping the same distribution of risks on the different charges and .

Three-sample test, independent case. Here, we narrow our focus to female claimants. The three populations consist of individuals classified by their relationship with the subscriber, which can be “Employee” ( observations), “Spouse” ( observations), or “Dependent” ( observations), all for the year .

Our objective is to test the equality of the dependence structure among the charges . In this context, we assume independence among the populations. Through our testing procedure, we obtain a p-value close to zero. Consequently, we reject the null hypothesis of equal dependence structure for these charges.

Subsequently, applying an ANOVA procedure reveals that the two-by-two equalities are rejected for “Dependent” vs “Employee” and “Employee” vs “Spouse”, with a p-value close to zero in each case. The p-value for “Dependent” vs “Spouse” is close to one.

Therefore, the status of being a “Dependent” or “Spouse” implies a similar dependence structure for the charges, distinct from the status of being an “Employee”. In the context of risk pooling, differentiating charges between these two groups becomes relevant.

Ten-sample test, independent case. Here, we analyze data from the year where the relationship to the subscriber is “Employee”. We categorize the charges based on age ranges of three years, creating groups as follows: , , .

The null hypothesis is : the dependence structures of these 10-sample groups are identical. Applying our test procedure, we obtain a p-value close to and a test statistic of . Thus, we reject the null hypothesis of equal dependence structure by age at a significant level of .

There is evidence to suggest that the dependence structure of changes over age. We further apply an ANOVA procedure, and the results are presented in Appendix G, Table 12, where a two-by-two comparison is proposed. Notably, there are no significant differences between two successive years. Additionally, Group 6 exhibits a similar dependence structure to the other groups, except for Group 3. The disparity increases with the gap between the years, especially between the first age categories and the last ones.

Observing the age range, we identify two clusters: Group 1, , Group 5 and Group 6, , Group 10. In terms of price segmentation, this allows the formation of two groups with similar dependencies.

8 Other similar tests

Some extensions of the K-sample test to various null hypotheses have been studied in [24, 2, 25]. Following his approach we indicate how to adapt the previous test procedure to answer the following hypotheses:

Clearly, coincides with the radial symmetry, that is and have the same joint distribution, while means that copulas are pairwise exchangeable. The exchangeable symmetry is represented by . These three hypotheses have been elegantly grouped together and tested in [24, 25]. We can also adapt our procedure to such hypotheses very naturally by considering the density representation given by (3). For instance, in the two-sample case, testing remains to compare the coefficients to the coefficients for all in . Asymptotically, under the test statistic coincides with the comparison of to and the selected test statistic is

which has an asymptotic centred normal distribution under with variance similar to that studied in Proposition 1 of the paper.

In the same way, consists in comparing to for all . Under the null hypothesis, the test statistic coincides simply with the comparison of the first coefficients (the least penalized) and , asymptotically. Then the selected statistic under the null is

which has asymptotically a centered normal null distribution.

Finally, the same reasoning applies to where the test statistic is asymptotically the same as the previous one.

We propose now to compare the performance of our test to the one developed in [24] for testing the equality of all the bivariate sub-copulas of copulas. We follow the design given in [24](see Table 3). We adopt the same notation and the same design. More precisely, we simulated data , where is a -dimensional copula and we examine the equality of all the bivariate sub-copulas of , that is

We denote by ) the model where is generated by the -variate normal copula and by the model where is generated by the Student copula with degrees of freedom where the correlation matrix is such that and for all

We compare our procedure () to the following quadratic functional procedures proposed in [24]:

-

•

Cramér-von Mises () statistic,

-

•

Two characteristic function statistics, denoted as (,), correspond to the weights functions of normal and double-exponential distributions, respectively,

-

•

Diagonal statistics (Dia)

We refer the reader to [24] for more details on these procedures and to code on their program.

Approaches 4.7 5.2 6.2 6.1 6.0 4.7 3.9 4.7 4.7 4.0 4.1 3.9 4.8 4.6 6.0 4.4 4.6 5.2 5.3 5.0 3.3 4.8 5.7 4.8 4.0 2.9 4.1 3.3 3.8 4.0 3.0 4.4 3.9 3.7 6.0 4.0 5.1 4.3 4.5 6.0 3.4 4.1 5.7 4.9 5.0 2.3 3.0 3.5 3.3 6.0 1.7 4.9 3.5 3.0 6.0 4.4 4.5 6.2 6.1 6.0

Approaches 16.8 15.5 21.3 19.8 22.5 21.8 28.5 26.4 44.2 48.1 48.1 35.0 78.0 75.4 81.2 40.0 51.3 48.9 62.2 58.1 84.1 81.7 90.1 87.7 88.6 92.2 90.7 60.0 84.0 12.0 12.7 17.8 16.1 20.3 21.1 25.2 23.6 40.7 47.7 47.3 45.7 76.7 76.6 79.4 73.0 47.3 48.2 63.0 56.8 85.8 84.7 91.5 88.6 90.1 93.2 92.4 89.0 100.0 99.8 99.9 97.0 9.8 12.0 16.1 14.1 19.6 20.6 27.1 25.0 34.6 41.7 43.9 42.3 74.4 75.5 78.8 77.6 43.4 45.8 57.2 53.5 81.5 80.3 88.9 86.4 86.3 91.7 91.0 90.5 99.8 99.8 99.0

9 Conclusion

In this paper, we introduced characteristic sequences, referred to as copula coefficients, for testing the equality of copulas. We developed a data-driven procedure in the two-sample case, accommodating both independent and paired populations. The extension to the -sample case involves a second data-driven method, resulting in a two-step automatic comparison method. Our approach is applicable to all continuous random vectors, even in cases where the copula density does not exist.

Our method differs from the two-sample test proposed by [27] and complements the -sample test developed by [24, 25], enabling the comparison of separate samples. The simulation study demonstrates the effectiveness of our approach, even for more than two populations. The test is user-friendly and performs efficiently. We have limited our simulations to the case of ten samples, but larger dimensions are conceivable with this method. For future exploration, studying high dimensions within limited computation time may require dimension reduction by selecting a limited number of copula coefficients and vector components, which extends beyond the scope of this paper.

Comparing our method to existing approaches in the two-sample case, it appears as efficient as the competitor proposed by [27]. In the -sample case with , numerical results suggest performance at least as good as those obtained by [24, 25]. In both cases of comparison, we used the previous models proposed by the authors. An R package of our procedure, named ”Kcop,” is available on CRAN.

Following the seminal work of [24] we can adapt our procedure to test radial symmetry or exchangeability with a very similar statistic. This idea is already nicely developed in [24, 2, 25] with a general approach.

Eventually, our approach can be extended in various directions. Two potential directions include:

-

•

Copula coefficients can be used to obtain a simplified and unified expression for some measures of association. Let us recall that for any continuous -dimensional random variable with copula , one of the well-known popular multivariate versions of Spearman’s rho can be expressed as (see [20]):

and where . Then Spearman’s rho coincides with the first copula coefficients, that is

For instance, for , we have

and we deduce a novel estimator of the multivariate Spearman’s rho as follows:

This estimator opens up possibilities for constructing tests comparing Spearman’s rho. However, this requires the calculation of the asymptotic distributions of copula coefficients as proposed in [32].

-

•

Secondly, since the copula coefficients characterize the dependence structure, we could use such coefficients for testing independence between random vectors in the same spirit as the penalized smooth tests proposed here.

Acknowledgements

The authors would like to express their gratitude for the thorough reading, thoughtful comments, and numerous helpful suggestions provided by two anonymous referees and an Associate Editor. Their contributions greatly contributed to the improvement of this paper. The authors would like to extend special thanks to the Associate Editor for his helpful remarks, which led to Proposition 6. The second author would also like to acknowledge the support received from the Research Chair DIALog under the aegis of the Risk Foundation, an initiative by CNP Assurances.

References

- [1] {bbook}[author] \bauthor\bsnmAbramowitz, \bfnmMilton\binitsM. and \bauthor\bsnmStegun, \bfnmIrene A\binitsI. A. (\byear1964). \btitleHandbook of mathematical functions with formulas, graphs, and mathematical tables \bvolume55. \bpublisherUS Government printing office. \endbibitem

- [2] {barticle}[author] \bauthor\bsnmBahraoui, \bfnmTarik\binitsT. and \bauthor\bsnmQuessy, \bfnmJean-François\binitsJ.-F. (\byear2017). \btitleTests of radial symmetry for multivariate copulas based on the copula characteristic function. \bjournalElectronic Journal of Statistics \bvolume11 \bpages2066 – 2096. \bdoi10.1214/17-EJS1280 \endbibitem

- [3] {barticle}[author] \bauthor\bsnmBhuchongkul, \bfnmSubha\binitsS. (\byear1964). \btitleA class of nonparametric tests for independence in bivariate populations. \bjournalThe Annals of Mathematical Statistics \bpages138–149. \endbibitem

- [4] {barticle}[author] \bauthor\bsnmBouzebda, \bfnmS.\binitsS., \bauthor\bsnmKeziou, \bfnmA.\binitsA. and \bauthor\bsnmZari, \bfnmT.\binitsT. (\byear2011). \btitleK-Sample Problem Using Strong Approximations of Empirical Copula Processes. \bjournalMathematical Methods of Statistics \bvolume20 \bpages14–2. \endbibitem

- [5] {barticle}[author] \bauthor\bsnmCan, \bfnmSami Umut\binitsS. U., \bauthor\bsnmEinmahl, \bfnmJohn H. J.\binitsJ. H. J. and \bauthor\bsnmLaeven, \bfnmRoger J. A.\binitsR. J. A. (\byear2020). \btitleGoodness-of-fit testing for copulas: A distribution-free approach. \bjournalBernoulli \bvolume26 \bpages3163 – 3190. \bdoi10.3150/20-BEJ1219 \endbibitem

- [6] {barticle}[author] \bauthor\bsnmCan, \bfnmSami Umut\binitsS. U., \bauthor\bsnmEinmahl, \bfnmJohn H. J.\binitsJ. H. J., \bauthor\bsnmKhmaladze, \bfnmEstate V.\binitsE. V. and \bauthor\bsnmLaeven, \bfnmRoger J. A.\binitsR. J. A. (\byear2015). \btitleAsymptotically distribution-free goodness-of-fit testing for tail copulas. \bjournalThe Annals of Statistics \bvolume43 \bpages878 – 902. \bdoi10.1214/14-AOS1304 \endbibitem

- [7] {bbook}[author] \bauthor\bsnmCherubini, \bfnmUmberto\binitsU., \bauthor\bsnmLuciano, \bfnmElisa\binitsE. and \bauthor\bsnmVecchiato, \bfnmWalter\binitsW. (\byear2004). \btitleCopula methods in finance. \bpublisherJohn Wiley & Sons. \endbibitem

- [8] {barticle}[author] \bauthor\bsnmDhar, \bfnmSubhra Sankar\binitsS. S., \bauthor\bsnmChakraborty, \bfnmBiman\binitsB. and \bauthor\bsnmChaudhuri, \bfnmProbal\binitsP. (\byear2014). \btitleComparison of multivariate distributions using quantile–quantile plots and related tests. \bjournalBernoulli \bvolume20 \bpages1484 – 1506. \bdoi10.3150/13-BEJ530 \endbibitem

- [9] {barticle}[author] \bauthor\bsnmGenest, \bfnmChristian\binitsC., \bauthor\bsnmRemillard, \bfnmBruno\binitsB. and \bauthor\bsnmBeaudoin, \bfnmDavid\binitsD. (\byear2009). \btitleGoodness-of-fit tests for copulas: A review and a power study. \bjournalInsurance: Mathematics and Economics \bvolume44 \bpages199-213. \endbibitem

- [10] {barticle}[author] \bauthor\bsnmGhosh, \bfnmS.\binitsS., \bauthor\bsnmSheppard, \bfnmL. W.\binitsL. W., \bauthor\bsnmHolder, \bfnmM. T.\binitsM. T., \bauthor\bsnmLoecke, \bfnmT. D.\binitsT. D., \bauthor\bsnmReid, \bfnmP. C.\binitsP. C., \bauthor\bsnmBever, \bfnmJ. D.\binitsJ. D. and \bauthor\bsnmReuman, \bfnmD. C.\binitsD. C. (\byear2020). \btitleCopulas and their potential for ecology. \bjournalAdvances in Ecological Research \bvolume62 \bpages409–468. \endbibitem

- [11] {bbook}[author] \bauthor\bsnmGrazier, \bfnmK. L.\binitsK. L. and \bauthor\bsnmG’Sell, \bfnmW.\binitsW. (\byear2004). \btitleGroup Medical Insurance Claims Database Collection and Analysis. Report for public release. \bpublisherSociety of Actuaries. \endbibitem

- [12] {barticle}[author] \bauthor\bsnmHoyer, \bfnmA.\binitsA. and \bauthor\bsnmKuss, \bfnmO.\binitsO. (\byear2018). \btitleMeta-analysis for the comparison of two diagnostic tests - A new approach based on copulas. \bjournalStatistics in Medicine \bvolume37 \bpages739–748. \endbibitem

- [13] {barticle}[author] \bauthor\bsnmInglot, \bfnmT.\binitsT. and \bauthor\bsnmLedwina, \bfnmT.\binitsT. (\byear2006). \btitleTowards data driven selection of a penalty function for data driven Neyman tests. \bjournalLinear Algebra and its Applications \bvolume417 \bpages124–133. \endbibitem

- [14] {bbook}[author] \bauthor\bsnmJoe, \bfnmHarry\binitsH. (\byear2014). \btitleDependence modeling with copulas. \bpublisherCRC press. \endbibitem

- [15] {barticle}[author] \bauthor\bsnmKallenberg, \bfnmWilbert C. M.\binitsW. C. M. and \bauthor\bsnmLedwina, \bfnmTeresa\binitsT. (\byear1995). \btitleConsistency and Monte Carlo Simulation of a Data Driven Version of Smooth Goodness-of-Fit Tests. \bjournalThe Annals of Statistics \bvolume23 \bpages1594 – 1608. \bdoi10.1214/aos/1176324315 \endbibitem

- [16] {barticle}[author] \bauthor\bsnmKim, \bfnmJong-Min\binitsJ.-M., \bauthor\bsnmJung, \bfnmYoon-Sung\binitsY.-S., \bauthor\bsnmSungur, \bfnmEngin A\binitsE. A., \bauthor\bsnmHan, \bfnmKap-Hoon\binitsK.-H., \bauthor\bsnmPark, \bfnmChangyi\binitsC. and \bauthor\bsnmSohn, \bfnmInsuk\binitsI. (\byear2008). \btitleA copula method for modeling directional dependence of genes. \bjournalBMC bioinformatics \bvolume9 \bpages225. \endbibitem

- [17] {barticle}[author] \bauthor\bsnmKleiber, \bfnmChristian\binitsC. and \bauthor\bsnmStoyanov, \bfnmJordan\binitsJ. (\byear2013). \btitleMultivariate distributions and the moment problem. \bjournalJournal of Multivariate Analysis \bvolume113 \bpages7–18. \endbibitem

- [18] {barticle}[author] \bauthor\bsnmLedwina, \bfnmTeresa\binitsT. (\byear1994). \btitleData-driven version of Neyman’s smooth test of fit. \bjournalJournal of the American Statistical Association \bvolume89 \bpages1000–1005. \endbibitem

- [19] {barticle}[author] \bauthor\bsnmMassart, \bfnmPascal\binitsP. (\byear1990). \btitleThe tight constant in the Dvoretzky-Kiefer-Wolfowitz inequality. \bjournalThe annals of Probability \bpages1269–1283. \endbibitem

- [20] {bbook}[author] \bauthor\bsnmNelsen, \bfnmRoger B\binitsR. B. (\byear2007). \btitleAn introduction to copulas. \bpublisherSpringer Science & Business Media. \endbibitem

- [21] {barticle}[author] \bauthor\bsnmNeyman, \bfnmJerzy\binitsJ. (\byear1937). \btitle”Smooth test” for goodness of fit. \bjournalScandinavian Actuarial Journal \bvolume1937 \bpages149–199. \endbibitem

- [22] {barticle}[author] \bauthor\bsnmNgounou-Bakam, \bfnmY. I.\binitsY. I. and \bauthor\bsnmPommeret, \bfnmD.\binitsD. (\byear2023). \btitleNonparametric estimation of copulas and copula densities by orthogonal projections. \bjournalTo appear in Econometrics and Statistics. \endbibitem

- [23] {barticle}[author] \bauthor\bsnmOmelka, \bfnmMarek\binitsM., \bauthor\bsnmGijbels, \bfnmIrène\binitsI. and \bauthor\bsnmVeraverbeke, \bfnmNoël\binitsN. (\byear2009). \btitleImproved kernel estimation of copulas: Weak convergence and goodness-of-fit testing. \bjournalThe Annals of Statistics \bvolume37 \bpages3023 – 3058. \bdoi10.1214/08-AOS666 \endbibitem

- [24] {barticle}[author] \bauthor\bsnmQuessy, \bfnmJean-François\binitsJ.-F. (\byear2016). \btitleA general framework for testing homogeneity hypotheses about copulas. \bjournalElectronic Journal of Statistics \bvolume10 \bpages1064 – 1097. \endbibitem

- [25] {barticle}[author] \bauthor\bsnmQuessy, \bfnmJean-François\binitsJ.-F. (\byear2021). \btitleA Szekely–Rizzo inequality for testing general copula homogeneity hypotheses. \bjournalJournal of Multivariate Analysis \bvolume186. \endbibitem

- [26] {bmanual}[author] \bauthor\bsnmRemillard, \bfnmBruno\binitsB. and \bauthor\bsnmPlante, \bfnmJean-Francois\binitsJ.-F. (\byear2012). \btitleTwoCop: Nonparametric test of equality between two copulas \bnoteR package version 1.0. \endbibitem

- [27] {barticle}[author] \bauthor\bsnmRémillard, \bfnmBruno\binitsB. and \bauthor\bsnmScaillet, \bfnmOlivier\binitsO. (\byear2009). \btitleTesting for equality between two copulas. \bjournalJournal of Multivariate Analysis \bvolume100 \bpages377-386. \endbibitem

- [28] {barticle}[author] \bauthor\bsnmScaillet, \bfnmOlivier\binitsO. (\byear2005). \btitleA Kolmogorov-Smirnov type test for positive quadrant dependence. \bjournalCanadian Journal of Statistics \bvolume33 \bpages415–427. \endbibitem

- [29] {barticle}[author] \bauthor\bsnmSchmüdgen, \bfnmKonrad\binitsK. (\byear2020). \btitleTen Lectures on the Moment Problem. \bjournalarXiv:2008.12698. \bdoi10.48550/ARXIV.2008.12698 \endbibitem

- [30] {barticle}[author] \bauthor\bsnmSchwarz, \bfnmG.\binitsG. (\byear1978). \btitleEstimating the dimension of a model. \bjournalThe Annals of Statistics \bvolume6 \bpages461–464. \endbibitem

- [31] {barticle}[author] \bauthor\bsnmShi, \bfnmPeng\binitsP., \bauthor\bsnmFeng, \bfnmXiaoping\binitsX. and \bauthor\bsnmBoucher, \bfnmJean-Philippe\binitsJ.-P. (\byear2016). \btitleMultilevel modeling of insurance claims using copulas. \bjournalThe Annals of Applied Statistics \bvolume10 \bpages834 – 863. \bdoi10.1214/16-AOAS914 \endbibitem

- [32] {barticle}[author] \bauthor\bsnmSinha, \bfnmBimal Kumar\binitsB. K. and \bauthor\bsnmWieand, \bfnmHS\binitsH. (\byear1977). \btitleMultivariate nonparametric tests for independence. \bjournalJournal of Multivariate Analysis \bvolume7 \bpages572–583. \endbibitem

Appendix A Proofs

We detail the proof in the independent case. The dependent case with is similar and will be indicated briefly in Appendix B. Throughout the proofs, we used the equality and the following inequalities are satisfied by Legendre polynomials (see [1]):

| (15) | |||||

| (16) |

where and are constant.

Proof of Proposition 1

From Corollary 6.7 of [29], if is a Radon measure on for which all moments are finite and if there exists such that

| (17) |

then is said determinate, that is: if is a Radon measure with the same moments then . Since is bounded on , all its moments are finite and (17) is satisfied for all . It follows that its distribution is determinate.

Proof of Theorem 1

We want to show that as tends to infinity. We have

| (18) |

with satisfying (9) and where . The last inequality comes from the fact that if a sum of positive terms, say is greater than a constant , then necessarily there exists a term such that . The important point here is that , which corresponds to the number of elements of the form in the difference . For simplification of notation, we write instead of .

Under the null and we decompose as follows

| (19) | |||||

| (20) |

that we combine with the standard inequality for positive random variables: , to get

| (21) | ||||

| (22) |

We now study the first quantity , the quantity being similar. Writing

we obtain

| (23) |

where

Then we have

| (24) |

We first study the quantity involving in (24). Write

| (25) |

Applying the mean value theorem to we obtain

From (15) and (16) there exists a constant such that

| (26) |

When belongs to we necessarily have . Moreover . It follows that

| (27) |

since for all , converges in law to a Kolmogorov distribution and by (A).

Coming back to (23), we now study the quantity involving . First note that . Moreover, . Then, by Markov inequality we have

and from (15) there exists a constant such that

It follows that

| (28) |

We now combine (27) and (28) with (24) to conclude that , as .

In the same manner we can show that , which completes the proof.

Proof of Theorem 2

Let . We have and we can decompose under the null as follows:

| (29) | |||||

| (30) |

where, under the null

By Taylor expansion, using the fact that the Legendre polynomials satisfy and , we obtain

By symmetry, the second term can be expressed as:

and finally

This expression is very similar to the expansion used in [32] (see his proof of Theorem 1) and [3] (see his equation (3.4)). We imitate their approach here. Therefore, we will show that and have a limiting normal distribution and the rest of the terms are all . Using the expression of the empirical cdf we can rewrite

where are iid random variables. By symmetry we get

Clearly . Since and , we also have and similarly . Moreover, and have finite variances. Applying the Central Limit Theorem to the independent iid series and we obtain

with

where is given by (4), and where, for ,

We now proceed to check that , are for . The asymptotic negligibility of and follows directly from those of and in [3]. The arguments are exactly similar to those of [3] (see his proof of Theorem 1) and we therefore omit the details.

Proof of Proposition 2

Let us define

where

We focus on , the case being similar. We have

| (31) |

According to Slusky’s Lemma and (31), the proof is completed by showing that

We have

From (15), there exists a constant such that, for all and for all ,

which implies that

It remains to prove that . We have , where

Since , we get

where and are given by (25). We next show that . We have

To deal with , we note that

Since the random vectors are iid, the weak law of large numbers and the continuous mapping theorem show that

For , we can write

and since has continuous uniform distribution it follows that

where

Observe that for all ,

with , that is, if we change the th variable of while keeping all the others fixed, then the value of the function does not change by more than . Then, by McDiarmid’s inequality, we get

It implies that , and we conclude that and similarly that . It follows that which completes the proof.

Proof of Theorem 3

Let us prove that vanishes as . By definition of we have:

Since the previous sum contains positive elements, there is at least one element greater than . It follows that

First, we can remark that is finite and then there is a finite number of terms in . It follows that we simply have to show that the probability vanishes as for any values of . Since have:

| (32) | |||||

Comparing (32) and (18) we can see that the study is now similar in spirit to the two-sample case and we can simply mimic the proof of Theorem 1 to conclude.

Proof of Proposition 3

We give the proof for the case , the particular case being similar. For simplification of notation, we now write instead of . We first show that tends to 1. Under , we have for all :

| (33) |

When , under , since , there exists such that . We have

| , | (34) |

and we can decompose as follows

| (35) |

We first decompose the quantities and . We only detail the calculus for , since the case of is similar. We have

We can reuse (26) to get:

for some constants and . Since (see for instance [19]) we have . As is an empirical estimator we also have , which yields

| (36) |

We now consider the quantity in (35). The inequality implies that

| (37) |

Finally, under , we combine (36) and (37) with (35) to get

.

If we prove that as tends to infinity

then (34) tends to 1, from assumption (B).

Mimicking the proof of Theorem 1 we can prove that

which gives the result.

Our next goal is to determine the limit of for . It is sufficient to prove that as tends to infinity. We have

From what has already been proved, under

For the second quantity we obtain

which is due to the fact that the statistics are embedded. Let be such that . Since , we have

Under , as in the proof of Theorem 1 we can see that the probability tends to zero as tends to infinity. It follows that

and since the statistics are embedded we have for all which implies that

| (38) |

since by (35) , and finally

Appendix B Paired case

We briefly describe the adaptation in the case of dependent samples, rewriting the previous definitions and the main results. In what follows we write .

B.1 Two-sample paired case

The constructions (7) and (8) become

and, for and ,

where and tend to as . A classical choice for is , where can be simply equal to 1, or obtained by the tuning procedure described in Appendix C.

Finally, the associated data-driven test statistic to compare and is

We consider the following rate for the penalty:

-

(A”) .

Theorem 4.

If (A”) holds, then, under , converges in Probability towards 1 as .

Asymptotically, the null distribution will reduce to that of , with and

Theorem 5.

Let . Then Under ,

where

To normalize the test, we consider the following estimator

where

Proposition 4.

Under ,

We then obtain the following result.

Corollary 3.

Assume that (A”) holds. Under , converges in law towards a chi-squared distribution as .

B.2 K-sample paired case

Theorem 6.

Assume that (A”)-(A”’) hold. Under , converges in probability towards 1 as .

Corollary 4.

Assume that (A”)-(A”’) hold. Under , converges in law towards a distribution.

Then the final data-driven test statistic is given by

B.3 Alternative hypotheses in the paired case

We need the following assumption:

-

(B’) .

Proposition 5.

Assume that (A”)-(A”’)-(B’) hold. Under , converges in probability towards as , and converges to , that is, for all .

Proposition 6.

Assume that (A”) and (A”’) hold. Then under , converges in probability towards 1 as and converges in law towards a distribution.

Proposition 7.

Assume that (A”)-(A”’)-(B’) hold. Then under , converges in probability towards and converges in probability towards , as . Moreover converges to .

Appendix C Tuning the test statistic

As evoked in Remark 1, we can choose the penalty

by using the following data-driven procedure.

Data-driven tuning procedure:

-

•

Assume we observe populations, namely

-

•

Split randomly each population into sub-populations, say , for , .

-

•

Clearly, for , the sub-populations have the same copula, that is, the null hypothesis is satisfied.

-

•

We can repeat times such a procedure to get samples under the null.

-

•

We then approximate numerically the value of the factor such that the selection rule retains the first component, that is , for all the -sample tests. From Theorem 3 this is the asymptotic expected value under the null.

More precisely we fix

In our simulation, we fixed arbitrarily , which seems to give a very correct empirical level. Note that the use of this factor only slightly modified the empirical results.

Appendix D Legendre polynomials

The Legendre polynomials used in this paper are defined on by

They satisfy

where if and otherwise.

Appendix E Representations of sepals and petals distributions

Appendix F Simulation results in the two-sample case (complements)

Appendix G Insurance data: the two-by-two comparison

| Groups | |||||||||

| 0.794 | |||||||||

| 0.265 | 0.193 | ||||||||

| 0.827 | 0.952 | 0.175 | |||||||

| 0.397 | 0.588 | 0.051 | 0.519 | ||||||

| 0.066 | 0.138 | 0.003 | 0.10 | 0.325 | |||||

| 0.002 | 0.009 | 0.000 | 0.005 | 0.028 | 0.209 | ||||

| 0.001 | 0.005 | 0.000 | 0.002 | 0.017 | 0.152 | 0.883 | |||

| 0.030 | 0.069 | 0.001 | 0.046 | 0.179 | 0.700 | 0.389 | 0.304 | ||

| 0.008 | 0.020 | 0.000 | 0.013 | 0.056 | 0.289 | 0.925 | 0.816 | 0.483 |

Appendix H 3-sample with Student copulas

We consider three Student copulas , with df=5 and Kendall’s tau , respectively. The first alternative is a very smooth deviation = coinciding with three closely related populations. The second alternative is formed of only two populations but with a slightly larger difference . Table 13 contains empirical powers for . It appears to be easier to detect the second alternative, which involves two more distinct groups, rather than three groups with a smooth variation. This finding may suggest the possibility of a forward test-based clustering procedure, wherein each population is successively tested before being joined to a cluster. This perspective could be explored further.

| 56.4 | 73.2 | 96.6 | |

| 17.6 | 29.8 | 39.5 |

Appendix I Empirical levels for the ten-sample case

| Models | ||||||

| Gaussian | Student | Gumbel | Frank | Clayton | Joe | |

| Kendall tau | ||||||

| 50 | 11.5 | 12.1 | 10.6 | 10.9 | 11.0 | 10.8 |

| 100 | 9.9 | 9.3 | 9.3 | 9.6 | 8.3 | 8.3 |

| 200 | 7.8 | 6.2 | 7.9 | 6.2 | 7.5 | 7.8 |

| 300 | 6.9 | 7.5 | 7.0 | 7.0 | 5.7 | 6.8 |

| 400 | 6.4 | 5.1 | 6.7 | 5.7 | 5.3 | 6.0 |

| 500 | 5.2 | 6.0 | 5.9 | 6.2 | 7.1 | 5.7 |

| 600 | 5.6 | 7.4 | 5.2 | 6.4 | 5.7 | 5.6 |

| 700 | 5.1 | 6.3 | 5.4 | 6.0 | 5.2 | 7.2 |

| 800 | 5.1 | 5.6 | 6.2 | 5.8 | 6.3 | 5.8 |

| 900 | 5.8 | 3.4 | 5.6 | 6.2 | 5.3 | 6.6 |

| 1000 | 6.0 | 5.9 | 5.1 | 4.2 | 6.4 | 5.1 |

| Kendall tau | ||||||

| 50 | 5.4 | 4.0 | 3.6 | 3.2 | 4.4 | 3.7 |

| 100 | 6.0 | 4.2 | 4.0 | 5.4 | 5.6 | 3.6 |

| 200 | 4.9 | 4.5 | 5.2 | 5.1 | 5.3 | 4.3 |

| 300 | 5.7 | 5.5 | 5.5 | 4.7 | 5.4 | 4.0 |

| 400 | 4.7 | 5.0 | 5.4 | 4.6 | 5.3 | 3.2 |

| 500 | 4.4 | 4.9 | 4.1 | 5.5 | 5.5 | 4.8 |

| 600 | 4.8 | 6.5 | 5.1 | 6.1 | 4.8 | 6.2 |

| 700 | 5.4 | 5.2 | 6.1 | 4.6 | 4.8 | 3.9 |

| 800 | 4.9 | 6.3 | 4.5 | 6.1 | 4.9 | 4.8 |

| 900 | 4.6 | 4.0 | 4.8 | 5.2 | 4.9 | 4.2 |

| 1000 | 4.2 | 5.5 | 4.5 | 4.1 | 4.8 | 3.6 |

| Kendall tau | ||||||

| 50 | 1.0 | 0.6 | 0.6 | 0.8 | 3.1 | 0.0 |

| 100 | 2.6 | 2.5 | 1.8 | 2.0 | 4.8 | 0.7 |

| 200 | 4.1 | 4.0 | 4.3 | 4.0 | 5.1 | 2.3 |

| 300 | 4.0 | 4.5 | 3.6 | 4.0 | 5.7 | 4.3 |

| 400 | 3.5 | 4.1 | 4.9 | 3.7 | 5.0 | 3.3 |

| 500 | 4.9 | 3.9 | 3.6 | 4.8 | 3.9 | 4.4 |

| 600 | 4.6 | 5.2 | 5.7 | 4.9 | 4.9 | 4.8 |

| 700 | 4.0 | 5.0 | 5.5 | 4.9 | 4.6 | 4.0 |

| 800 | 4.5 | 6.5 | 3.2 | 3.7 | 4.3 | 3.5 |

| 900 | 4.4 | 4.6 | 4.0 | 5.9 | 5.8 | 4.5 |

| 1000 | 3.7 | 5.5 | 4.7 | 4.3 | 5.2 | 4.7 |