SNCP_supplement

Segmenting Time Series via Self-Normalization

Abstract

We propose a novel and unified framework for change-point estimation in multivariate time series. The proposed method is fully nonparametric, robust to temporal dependence and avoids the demanding consistent estimation of long-run variance. One salient and distinct feature of the proposed method is its versatility, where it allows change-point detection for a broad class of parameters (such as mean, variance, correlation and quantile) in a unified fashion. At the core of our method, we couple the self-normalization (SN) based tests with a novel nested local-window segmentation algorithm, which seems new in the growing literature of change-point analysis. Due to the presence of an inconsistent long-run variance estimator in the SN test, non-standard theoretical arguments are further developed to derive the consistency and convergence rate of the proposed SN-based change-point detection method. Extensive numerical experiments and relevant real data analysis are conducted to illustrate the effectiveness and broad applicability of our proposed method in comparison with state-of-the-art approaches in the literature.

Keywords: Binary segmentation; Change-point detection; Scanning; Studentization; Long-run variance; Temporal dependence

1 Introduction

Change-point detection has been identified as one of the major challenges for modern data applications (National Research Council,, 2013). There is a vast literature on change-point estimation and testing in statistics, in part due to its broad applications in bioinformatics, climate science, economics, finance, genetics, medical science, and signal processing among many other areas. See Csörgő and Horváth, (1997), Brodsky and Darkhovsky, (2013) and Tartakovsky et al., (2014) for book-length treatments of the subject. We also refer to Aue and Horváth, (2013), Casini and Perron, (2019) and Truong et al., (2020) for excellent reviews.

In this paper, we study the problem of time series segmentation, also known as (offline) change-point estimation, where the task is to partition a sequence of potentially non-homogeneous ordered observations into piecewise homogeneous segments. Many change-point problems arise within a time series context (e.g. climate, epidemiology, economics and financial data), where there is a natural temporal ordering in the observations. Although temporal dependence is the norm rather than the exception for time series, most literature in change-point analysis assume and require independence of observations over time for methodological and theoretical validity; see for example Olshen et al., (2004), Killick et al., (2012), Matteson and James, (2014), Fryzlewicz, (2014), and Baranowski et al., (2019) among others. One stream of literature addresses temporal dependence via the assumption of parametric models, see Davis et al., (2006) and Yau and Zhao, (2016) for change-point detection in AR process and Fryzlewicz and Subba-Rao, (2014) in ARCH process. However, parametric approaches generally require stronger conditions and potential violation of parametric assumptions can inevitably cast doubts on the estimation result.

Existing nonparametric approaches for change-point estimation in temporally dependent observations primarily focus on first or second-order moments, see Bai and Perron, (1998), Eichinger and Kirch, (2018) for change-point estimation in mean, Aue et al., (2009), Preuss et al., (2015) in (auto)-covariance, and Cho and Fryzlewicz, (2012), Casini and Perron, 2021a in spectral density function (thus second-order properties). However, for many applications, the key interest can go beyond mean or covariance. For example, detecting potential changes in extreme quantiles is critical for monitoring systemic risk (i.e. Value-at-Risk) in finance and for studying evolving behavior of severe weather systems such as hurricanes in climate science. Moreover, existing nonparametric methods are mostly designed for detecting only one specific type of change (e.g. mean or variance) and cannot be universally used for examining changes in different aspects of the data, which may limit its applications and cause inconvenience of implementation for practitioners. Additionally, existing nonparametric procedures typically involve certain tuning or smoothing parameters, such as the bandwidth parameter involved in the consistent estimation of the long-run variance, and how to choose these tuning parameters is important yet highly challenging in practice.

To fill in the gap in the literature, we propose a new multiple change-point estimation framework that is fully nonparametric, robust to temporal dependence, enjoys effortless tuning, and works universally for various parameters of interest for a multivariate time series where with a fixed dimension . Specifically, denote as the cumulative distribution function (CDF) of , the proposed procedure allows change-point detection for any such that , where is a functional that takes value in with This is a broad framework that covers important quantities such as mean, variance, quantile, (auto)-correlation and (auto)-covariance among others, see Künsch, (1989) and Shao, (2010).

As in the standard change-point literature, we assume the change happens in a piecewise constant fashion. Specifically, we assume is a piecewise stationary time series and there exist unknown number of change-points that partition into stationary segments. Define and , the th segment contains stationary observations that share common behavior characterized by (e.g. mean, variance, correlation, quantile), where we require for due to the structural break. Our primary interest is to recover the unknown number and locations of the change-points.

To achieve broad applicability and robustness against temporal dependence, our proposed multiple change-point estimation method is built upon self-normalization (SN, hereafter), a nascent inference technique for time series (Shao,, 2010, 2015). We note that since its first proposal in Shao, (2010), SN has been extended to retrospective change-point testing by Shao and Zhang, (2010), Hoga, (2018), Betken and Wendler, (2018), Zhang and Lavitas, (2018), and Dette et al., (2020), and to sequential change-point monitoring by Dette and Gösmann, (2020) and Chan et al., (2021). However, the primary focus of these papers is to construct SN-based change-point testing procedures (either retrospective or sequential) but not change-point estimation. Compared to change-point testing, change-point estimation is a much more challenging task both methodologically and theoretically: it further requires the estimation of the unknown number and locations of change-points, which involves substantially different techniques and analysis.

Indeed, the use of SN for time series segmentation (i.e. multiple change-point estimation) seems largely unexplored, with the exception of Jiang et al., (2020, 2022) for piecewise linear and quantile trend models designed for COVID-19 time series. One notable reason for the scarcity of SN-based time series segmentation algorithms is that, unlike the classical CUSUM-based change-point test, the SN-based change-point testing cannot be easily extended to multiple change-point estimation by combining with the standard binary segmentation algorithm (Vostrikova,, 1981). Such a combination simply fails due to the potential inflation of the self-normalizer under the presence of multiple change-points. We discuss this point in more details later in Section 3 and provide further illustration via both theory and numerical experiments in Section S.1 of the supplementary material.

To bypass this difficulty, we propose a novel nested local-window segmentation algorithm, which is then combined with an SN test to achieve multiple change-point estimation. We name the procedure SNCP. Through a series of carefully designed nested local-windows, the proposed procedure can isolate each true change-point adaptively and thus achieves respectable detection power and estimation accuracy. The statistical and computational efficiency of the nested local-window segmentation algorithm is further illustrated via extensive numerical comparison with popular segmentation algorithms such as SaRa in Niu and Zhang, (2012), WBS in Fryzlewicz, (2014) and SBS in Kovacs et al., (2020).

In addition to methodological advances, new theoretical arguments based on the partial influence functions (Pires and Branco,, 2002) are further developed to establish the consistency and convergence rate of the proposed change-point estimation procedure, which seems to be the first in the SN literature. The proof is non-standard and built on a subtle analysis of the behavior of SN-based test statistic around change-points. It differs from existing techniques in the change-point literature due to the presence of the self-normalizer (an inconsistent long-run variance estimator) and is of independent interest.

To our best knowledge, the proposed method (SNCP) is the first to address multiple change point estimation for a general parameter in the time series setting. One salient and distinct feature of SNCP is its versatility: it allows the user to examine potential change in virtually any parameter of interest in an effortless fashion. This is valuable as in practice, the ground truth is unknown and it is important to examine the behavior change of the data via different angles. In addition, due to its versatility and robustness to temporal dependence, SNCP can serve as a numerically credible and theoretically valid benchmark for almost all algorithms designed for multiple change-point estimation in a fixed-dimensional time series, which is of interest to both practical applications and academic research.

The rest of the paper is organized as follows. We first provide background of SN and introduce the SN-based detection method for single change-point estimation in Section 2. Building upon a novel nested local-window segmentation algorithm, Section 3 proposes a unified SN-based framework (SNCP) for multiple change-point estimation and further studies its theoretical properties. Extensive numerical experiments are conducted in Section 4 to demonstrate the promising performance of SNCP when compared with state-of-the-art methods for change-point estimation in mean, variance, quantile of univariate time series, and correlation and covariance matrix of multivariate time series. Section 5 concludes. Technical proofs and additional simulation and real data application results can be found in the supplement.

Some notations used throughout the paper are defined as follows. Let denote the space of functions on which are right continuous with left limits, endowed with the Skorokhod topology (Billingsley,, 1968). We use to denote weak convergence in or more generally in -valued function space , where . We use to denote convergence in distribution. We use to denote the norm of a vector and use to denote the spectral norm of a matrix.

2 Single Change-point Estimation

In this section, we provide some background on the SN test and propose an SN test based method for single change-point estimation, which serves as a building block for the proposed multiple change-point estimation procedure in Section 3. Model assumptions and consistency results are discussed in details to provide intuition and foundation for more involved results in Section 3. For ease of presentation, in the following we assume , in other words, the parameter of interest is univariate, and postpone the results for the multivariate case of to Section 3.3.

2.1 An SN-based estimation procedure

We start with single change-point estimation in a general parameter for a univariate time series , where denotes the CDF of and is a general functional. Under the no change-point scenario, is a stationary time series. Under the single change-point alternative, we follow the framework of Dette and Gösmann, (2020) and assume is generated by

| (1) |

where is a stationary time series with for . Thus we have . Denote and , we have and the change-point with . Note that the dependence between and is deliberately left unspecified, as the validity of the proposed method does not rely on the specification of the dependence (see Assumption 2.1(i) for more details).

To detect the existence and further estimate the location of the (potential) single change-point , we propose an SN-based testing approach. Specifically, we define

| (2) |

where

| (3) |

and for any , where is the empirical distribution of . In other words, denotes the nonparametric estimator of based on the subsample .

When is the mean functional, i.e., , the newly defined contrast-based test in (2) reduces to the CUSUM-based SN test statistic in Shao and Zhang, (2010) (cf. equation (4) therein). However, for a nonlinear functional , such as variance, correlation and quantile, is not equivalent to the CUSUM-based counterpart and is preferred due to its contrast nature. We refer to Zhang and Lavitas, (2018) for more discussion.

Built upon the test statistic defined in (2), the SN-based change-point detection procedure proceeds as follows. For a pre-specified threshold , we declare no change-point if . Given that exceeds the threshold, we estimate the single change-point location via

This SN-based procedure provides a general and unified change-point estimation framework, as it can be implemented for any functional with a nonparametric estimator based on the empirical distribution.

2.2 Assumptions and theoretical results

To establish the consistency of the SN-based estimation procedure under the general functional setting (1), the key is to track the asymptotic behavior of for . To achieve this, we operate under the framework of approximately linear functional, which covers important quantities such as mean, variance, covariance, correlation and quantile (Künsch,, 1989; Shao,, 2010).

Specifically, we assume the subsample estimator admits the following expansion on the stationary time series where

| (4) |

In other words, is approximately linear when the subsample is stationary. Note that and are indeed the influence functions of the functional (Hampel et al.,, 1986), which is the leading term for asymptotic behavior of , and are the remainder terms.

To further regulate the behavior of when the subsample is a mixture of two stationary segments, we utilize the concept of partial influence functions originated from the robust statistics literature (Pires and Branco,, 2002). Specifically, for , we assume

| (5) |

where denotes the proportion of each stationary segment in , denotes evaluated at the mixture distribution and is the remainder term. The terms and are related to the partial influence functions of the functional evaluated at the mixture distribution . See detailed discussion later.

Note that the expansion (5) generalizes (4) under the single change-point scenario. Specifically, define and for and respectively, (4) can be viewed as a special case of (5) where the mixture distribution is pure such that , and , respectively.

We now work out the explicit formulation of the expansion (5) under the framework of partial influence function (Pires and Branco,, 2002). Denote the mixture weight such that , and . Denote as the functional evaluated at the mixture . Definition 2.1 defines the partial influence function as in Pires and Branco, (2002).

Definition 2.1.

The partial influence functions of the functional with relation to and , respectively, are given by

provided the limits exist, where is the Dirac mass at .

To understand the partial influence functions, define , by Definition 2.1, we have

where is the Gâteaux derivative of in the direction . Similarly, , where is the Gâteaux derivative of in the direction .

To establish the expansion (5), note that , where denotes the empirical CDF based on the subsample . The key observation is that with . In other words, can be viewed as a mixture of two empirical CDFs and based on stationary segments with CDF and respectively. Thus, by the results in Pires and Branco, (2002), we have

where denotes the remainder term. The expansion (5) follows immediately by substituting the partial influence functions with the Gâteaux derivatives and .

We proceed by imposing the following Assumptions 2.1-2.3 on the approximately linear functional , which are further verified in Section S.4 of the supplement for the smooth function model (including mean, variance, (auto)-covariance, (auto)-correlation) and in Section S.5 of the supplement for quantile. We refer to Remark 1 in Section 3.2 for more detailed discussion on the verification of assumptions.

Assumption 2.1.

For some and , we have

where and are standard Brownian motions.

Assumption 2.2.

Assumption 2.1 regulates the behavior of the (partial) influence function and . Specifically, Assumption 2.1(i) requires the invariance principle to hold for each stationary segment. Note that the dependence of the two Brownian motions and are left unspecified as we do not require a specific dependence structure on and . Assumption 2.1(ii) are tailored to regulate estimated on a mixture of two stationary segments. Assumption 2.2 requires that the remainder term is asymptotically negligible and is a commonly used assumption in the SN literature (Shao,, 2010, 2015).

Assumption 2.3.

Denote , where is the mixture weight with and . There exist some constants such that for any mixture weight , we have

Assumption 2.3 regulates the smoothness of . Intuitively, it means that the functional can distinguish the mixture distribution from and . For mean functional, we have , thus we can set as is linear in .

Assumption 2.4.

as , and satisfies for some .

Assumption 2.4 quantifies the asymptotic order of the change size and the threshold . Under Assumptions 2.1-2.4, Theorem 2.1 gives the consistency results of the SN-based change-point estimation method for approximately linear functionals.

Theorem 2.1.

Theorem 2.1(i) indicates that the asymptotic distribution of for a general functional coincides with the asymptotic distribution of the CUSUM-based SN test for mean (see Theorem 3.1 in Shao and Zhang, (2010)). This implies that the same threshold can be used to control false positives (i.e. Type-I error) for change-point detection in various parameters and thus greatly simplifies the implementation of the proposed method. In practice, we recommend to set as the 90% or 95% quantile of , which can be obtained via simulation as is pivotal. See Shao and Zhang, (2010) for tabulated critical values of .

Theorem 2.1(ii) gives the convergence rate of the estimated change-point , providing a unified theoretical justification of the SN-based method for a broad class of functionals. Due to the presence of the self-normalizer , which is complex and further varies by , nonstandard technical arguments different from existing techniques in the change-point literature are developed to establish the consistency result. It involves a simultaneous analysis of the contrast statistic and the self-normalizer . In general, the localization error rate of SNCP is not optimal (at least for change in mean). However, a simple local refinement procedure can be performed to help achieve the optimal rate. We refer to the discussion following 3.1 in Section 3.2 for more details on this matter.

The traditional CUSUM based estimation procedure in the change-point literature typically admits the form , where theoretical results are derived under the assumption that is a consistent estimator of the long-run variance (LRV), leading to less involved technical analysis than the proposed SN-based estimation. However, in practice, the construction of a consistent involves a bandwidth tuning parameter that is difficult to select, especially under the presence of change-points. For example, in the mean case, using a data-driven bandwidth with the estimation-optimal bandwidth formula in Andrews, (1991) could lead to non-monotonic power under the change-point alternative and large size distortion under the null, see Crainiceanu and Vogelsang, (2007) and Shao and Zhang, (2010). Casini et al., (2021) and Casini and Perron, 2021b further provide a comprehensive theoretical analysis of such phenomenon based on Edgeworth expansion. Additionally, different construction of is required for different functional , which can be highly involved and non-trivial for parameters such as correlation and quantile, making the practical implementation challenging.

In contrast, thanks to the self-normalizer , the proposed SN-based procedure avoids the challenging estimation of LRV and provides a robust framework that works universally for a broad class of functionals under temporal dependence.

3 Multiple Change-point Estimation

In this section, we further extend the proposed SN-based test to multiple change-point estimation. As in standard change-point literature, we assume is a piecewise stationary time series and there exist unknown number of change-points that partition into stationary segments. Define and , the th segment contains stationary observations that share common behavior characterized by , for .

More specifically, we operate under the following data generating process for such that

| (6) |

where is a stationary time series with CDF and we require for due to the structural break. Our primary interest is to recover the unknown number and locations of the change-points.

To proceed, we first introduce some notations. For , we define

| (7) |

where , and

Note that is essentially the proposed SN test defined on subsample . Set and , reduces to the global SN test defined in (2) of Section 2.1.

The key observation is that, due to the presence of the self-normalizer , the global test statistic may experience severe power loss under multiple change-point scenarios. The intuition is as follows. Suppose is a true change-point and has other change-points besides . Intuitively, may observe significant inflation as and are based on contrast statistics and their values could significantly inflate due to the existence of other change-points besides . This can in turn cause to suffer severe deflation and thus a loss of power. Consequently, a naive combination of the standard binary segmentation (Vostrikova,, 1981) and the SN test cannot serve as a viable option for multiple change-point estimation (see both theoretical evidence and numerical illustration of this phenomenon in Section S.1 of the supplement).

3.1 The nested local-window segmentation algorithm

To bypass this issue, we combine the SN test with a novel nested local-window segmentation algorithm, where for each , instead of one global SN test , we compute a maximal SN test based on a collection of nested windows covering . Specifically, fix a small such as , define the window size . For each , we define its nested window set where

Note that for and , by definition, we have .

For each , based on its nested window set , we define a maximal SN test statistic such that

where we set Note that unlike the standard binary segmentation, the test statistic is calculated based on a set of nested local-window observations surrounding the time point instead of directly based on the global observations .

This mechanism is precisely designed to alleviate the inflation of the self-normalizer for the SN test under multiple change-point scenarios. With a sufficiently small window size , for any change-point , there exists some local-window which contains as the only change-point, thus the maximal statistic remains effective thanks to . In the literature, there exists pure local-window based segmentation algorithms, e.g. SaRa in Niu and Zhang, (2012) for change in mean, LRSM in Yau and Zhao, (2016) for change in AR models. The pure local-window approach only considers the smallest local-window when constructing change-point tests for given a window size . Such an approach is also employed in the literature of “piecewise smooth” change, see Wu and Zhao, (2007), Bibinger et al., (2017) and Casini and Perron, 2021a .

Compared to the pure local-window approach, the constructed nested window set makes our algorithm more adaptive as it helps retain more power when is far away from other change-points by utilizing larger windows that cover . We refer to Section S.1.2 of the supplement for more detailed discussion of this point and numerical evidence of the substantial advantage in detection power and estimation accuracy of the proposed nested local-window approach over the pure local-window approach. In addition, since the nested local-window algorithm examines a set of expanding windows instead of a single window, its performance is more robust to the choice of the bandwidth . This is confirmed by numerical experiments in Section S.2.1 of the supplement, where we conduct sensitivity analysis of and it is seen that performance of the nested local-window is robust and stable w.r.t. the choice of .

Note that the nested window-based SN statistic can be viewed as a discretized version of the SN test statistic , which is related to the scan statistics (Chan and Walther,, 2013) and multiscale statistics (Frick et al.,, 2014). However, is computationally impractical, thus we instead approximate by computed on the nested window set .

Based on the maximal test statistic and a prespecified threshold , the SN-based multiple change-point estimation (SNCP) proceeds as follows. Starting with the full sample , we calculate Given that , SNCP declares no change-point. Otherwise, SNCP sets and we recursively perform SNCP on the subsample and until no change-point is declared.

Denote and , which is the nested window set of on the subsample . Define the subsample maximal SN test statistic as . Algorithm 1 gives the formal description of SNCP.

Comparison with popular segmentation algorithms in the literature: We remark that it is possible to combine the proposed SN test statistic with other segmentation algorithms designed for multiple change-point estimation, such as wild binary segmentation (WBS) (Fryzlewicz,, 2014) or its variants including narrowest-over-threshold (NOT) (Baranowski et al.,, 2019) and seeded binary segmentation (SBS) (Kovacs et al.,, 2020). WBS and NOT use randomly generated intervals for searching multiple change-points, whereas SBS employs deterministic intervals. However, theoretical guarantees for such procedures can be challenging to establish as the above-mentioned segmentation algorithms are mainly used for change-point estimation in a sequence of independent data. Nevertheless, in Section S.2.2 of the supplement, we provide an extensive numerical comparison between the proposed nested local-window segmentation algorithm (SNCP) and the combinations of the SN test with WBS, NOT and SBS, where the performance of SNCP is seen to be very competitive in terms of both statistical accuracy and computational efficiency.

3.2 Assumptions and theoretical results

In this section, we study the theoretical properties of the proposed SNCP for multiple change-point estimation. We operate under the classical infill framework where we assume for as Define and , we further assume that , where is the window size parameter used in SNCP, which imposes an implicit upper bound for such that This is a common assumption in the literature for change-point testing and estimation under temporal dependence, see Andrews, (1993), Bai and Perron, (2003), Davis et al., (2006) and Yau and Zhao, (2016). In practice, we set to be a small constant such as , which can be based on prior information about the minimum spacing between consecutive change-points.

In Section S.2.1 of the supplement, we conduct an extensive sensitivity analysis of SNCP w.r.t. the window size and the threshold , and the result indicates SNCP is rather robust to the choices of as long as , the violation of which could lead to unsatisfactory segmentation results. This suggests that the assumption is necessary both theoretically and empirically, and hence the proposed SNCP may not be suitable for time series with frequent change-points where is vanishing with ; see Fryzlewicz, (2020) for a recent contribution to detecting frequent change-points.

Denote the true parameter for the th segment by and denote the change size by for For ease of presentation, we assume that for , where is a fixed constant. Thus, the overall change size is controlled by

We assume the following expansions for the empirical functional , which is a natural extension of the expansions (4) and (5) from the single change-point setting in Section 2.2 to the multiple change-point setting. Specifically, for computed exclusively on the th stationary segments with , we assume

| (8) |

where is the influence function of the functional for the th segment and denotes the remainder term. For computed based on a mixture of stationary segments, we further assume

| (9) |

where with denotes the true change-points between and such that and , and

denotes the proportion of each stationary segment in , denotes evaluated at the mixture distribution and denotes the remainder term.

Similar to the single change-point scenario, the expansion (8) of with can be viewed as a special case of (3.2) where the mixture distribution is pure and is defined as and . We proceed by making the following assumptions.

Assumption 3.1.

For some , ,

where , are standard Brownian motions.

Assumption 3.2.

Assumptions 3.1 and 3.2 are natural extensions of Assumptions 2.1 and 2.2 to the multiple change-point setting and can also be verified for smooth function models and quantile under mild conditions. We refer to Sections S.4 and S.5 of the supplement for more details.

Assumption 3.3.

For , can be expressed almost linearly such that .

Assumption 3.3 imposes a relatively strong technical condition on the functional such that . Assumption 3.3 holds trivially for mean change and is typically satisfied when is the only quantity that changes, which is a common assumption in testing-based change-point estimation literature. For example, Assumption 3.3 holds for variance, (auto)-covariance change with constant mean (Aue et al.,, 2009; Cho and Fryzlewicz,, 2012) and (auto)-correlation change with constant mean and variance (Wied et al.,, 2012). Numerical experiments conducted in Section 4.4 and Sections S.2.6-S.2.9 of the supplement indicate that SNCP is robust and continues to perform well when Assumption 3.3 can not be easily verified.

An alternative Assumption 3.3∗ is provided in Section S.4.2.3 of the supplement, which is a natural extension of Assumption 2.3 to the multiple change-point setting and further includes Assumption 3.3 as a special case. We defer Assumption 3.3∗ to the supplement as it is a more involved technical assumption.

Remark 1 (Verification of assumptions): Assumptions 3.1-3.3 are high-level assumptions made on a general functional to facilitate presentation. In Sections S.4 and S.5 of the supplement, under mild conditions, we provide verification of Assumptions 3.1-3.3 for commonly used functionals including the smooth function model and quantile. In general, the assumptions can be verified for mean change, variance and (auto)-covariance change with constant mean or with concurrent small-scale mean change, (auto)-correlation change with constant mean and variance or with concurrent small-scale mean and variance change, and quantile change with density functions that are smooth and bounded. In particular, the verification of Assumption 3.2 for quantile is highly nontrivial and of independent interest. It essentially provides a uniform Bahadur representation for quantiles in subsamples. Our result allows for change-points and temporal dependence, and thus generalizes the ones in Wu, (2005) and Dette and Gösmann, (2020).

For , define the scaled limit of by and define , where is a standard Brownian motion. Theorem 3.1 gives the consistency result of SNCP for multiple change-point estimation.

Theorem 3.1.

Theorem 3.1(i) characterizes the asymptotic behavior of SNCP under no change-point and thus provides a natural choice of threshold . In practice, we set as a high quantile, e.g. 90% or 95% quantile of to control the Type-I error of SNCP. For a given window size , is a pivotal distribution and its critical values can be obtained via simulation. Theorem 3.1(ii) indicates that SNCP can correctly identify the number of change-points with an increasing threshold of a proper order. Note that the localization error rate of SNCP is the same as the single change-point scenario in Theorem 2.1.

Theorem 3.1(ii) assumes all changes have the same order and requires to achieve consistency. In fact, this can be relaxed to allow multiscale changes and we then require , where and denotes the maximum and minimum change size. This multiscale condition matches the one required by Lavielle and Moulines, (2000) for multiple change-point estimation in mean under temporal dependence (cf. Theorem 3 therein).

Remark 2 (Localization error rate and local refinement): Set the change size with and , Theorem 3.1(ii) implies that . Under the fixed change size (), it implies that the convergence rate of SNCP is at best , which is slower than the optimal rate for change-point estimation in mean under temporal dependence, see Bai, (1994) and Lavielle and Moulines, (2000).111For multiple change-point estimation of univariate mean in a sequence of independent sub-Gaussian observations, this is further shown as the minimax optimal localization rate, see Wang et al., (2020), Verzelen et al., (2020) and references therein. We note that the derived rate is technically difficult to be further improved due to the complex nature of the self-normalizer . On the other hand, the derived rate applies to a general functional, which seems not well studied in the literature. Nevertheless, in Section S.8 of the supplement, we further propose a simple and intuitive local refinement procedure, which provably improves the localization error rate of SNCP to for the mean functional. The key observation is that by Theorem 3.1, SNCP can asymptotically isolate each single change-point and thus a simple CUSUM statistic can be used within a well-designed local interval around each estimated change-point by SNCP to achieve further refinement. We refer to Sections S.8.1-S.8.2 for more detailed theoretical and numerical results of the procedure.

3.3 Extension to vector-valued functionals

In this section, we discuss the extension of SNCP to a vector-valued functional, where with A natural example is change-point detection in mean or covariance matrix of multivariate time series, see for example Aue et al., (2009). Additionally, for a univariate time series, we may be interested in detecting any structural break among multiple parameters of interest, such as examining mean and variance together or examining multiple quantile levels simultaneously.

Note that the dimension of the underlying time series may or may not equal to that of (i.e. ). For change-point estimation in mean of multivariate time series, we have and the dimension of is . However, for change-point estimation in covariance matrix () or multiple parameters (e.g. and ), the dimension of can be smaller than . We examine the performance of SNCP for all three cases via numerical experiments in Section 4.

To accommodate the vector-valued functional, we modify the SN test statistic in (7) such that

| (11) |

where with being the empirical distribution of and

With a pre-specified threshold , SNCP proceeds as in Algorithm 1 where the only difference is that we replace with as defined in (11).

Limiting distribution under no change-point scenario: We first derive the limiting null distribution of , which is pivotal and thus provides natural choices of the threshold . We assume the subsample estimator for the parameter of interest admits the following expansion

where denotes the true value of , denotes the influence function of and is the remainder term. We further impose the following mild assumptions.

Assumption 3.4.

For some positive definite matrix , we have

where is a -dimensional Brownian motion with independent entries.

Assumption 3.4 is a standard functional central limit theorem (FCLT) result commonly assumed in the SN literature under the no change-point scenario, and can be verified under mild moment and weak dependence conditions, see for example, Shao, (2010) (Assumption 2.1), Shao and Zhang, (2010) (Assumption 3.1) and Dette and Gösmann, (2020) (Assumption 3.1).

Assumption 3.5.

The remainder term is asymptotically negligible such that

Proposition 3.1.

The proof of Proposition 3.1 is straightforward and follows the same argument as the proof of Theorem 2.1 in Shao, (2010) and the continuous mapping theorem, hence omitted. For a given dimension and window size , the limiting distribution is pivotal and its critical values can be obtained via simulation. Table 1 tabulates the critical values of for and . Note that for , coincides with the univariate limiting distribution derived in Theorem 3.1(i).

Consistency of SNCP: To ease presentation and facilitate understanding, we first establish the consistency of SNCP for change-point estimation in mean of multivariate time series. We then provide further discussions on how to extend the consistency result to a general vector-valued functionals.

Specifically, we operate under the following data generating process for such that

where is a -dimensional stationary time series with , denote the (potential) change-points, and denotes the mean of the th segment. We assume that, for , where is a nonzero vector. Thus, the overall change size is controlled by

Same as in Section 3.2, we use the infill framework where we assume for as Define and , we again require that , where is the window size parameter used in SNCP.

Theorem 3.2.

Suppose satisfies the invariance principle such that , where is a positive definite matrix.

Under the no change-point scenario, we have .

Under the multiple change-point scenario, suppose Assumption 2.4 hold and suppose , we have

for any sequence such that and as .

Compared to the univariate result in Theorem 3.1(ii), it can be seen that the same localization rate is obtained in Theorem 3.2(ii) for the multivariate mean case. However, compared to the univariate proof, the technical argument needed for Theorem 3.2 is substantially different, which is indeed much more challenging as it requires the analysis of a random matrix and its inverse, since the self-normalizer is a random matrix in due to the vector nature of the functional .

It is easy to see that the result of Theorem 3.2 can be directly used to establish consistency of SNCP for change-point estimation in covariance matrix of (assuming constant mean ), as the problem can be transformed into multivariate mean change-point estimation for the -dimensional time series , see for example Aue et al., (2009).

Remark 3 (Extension to general vector-valued functionals): To further extend the consistency result in Theorem 3.2 to a general vector-valued functional , we need an additional assumption on the (approximate) linearity of , similar to Assumption 3.3 of the univariate case. Combined with Assumption 3.4 (FCLT) and 3.5 (asymptotic negligibility of reminder terms), the same argument used for the multivariate mean in Theorem 3.2 can then be applied to establish consistency of SNCP for the general functional . We omit the details to conserve space.

4 Simulation Studies

In this section, we conduct extensive numerical experiments to demonstrate the promising performance of SNCP for a wide range of change-point detection problems under temporal dependence. Under the unified framework of SNCP, we consider change-point estimation for four different settings: mean, covariance matrix, multi-parameter and correlation. In the supplement, we further consider change-point estimation for variance, autocorrelation and quantile.

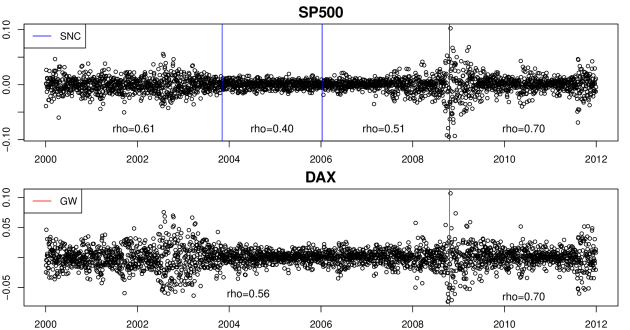

For comparison, we further implement several state-of-the-art nonparametric change-point detection methods in the literature that are explicitly designed to accommodate temporal dependence. Specifically, (A) For mean change, we compare with the classical CUSUM with binary segmentation (Csörgő and Horváth,, 1997) (hereafter CUSUM) and Bai and Perron, (2003) (hereafter BP), which are designed for detecting mean change in time series and uses a model selection approach to simultaneously detect all change-points. (B) For covariance matrix change, we compare with the CUSUM method in Aue et al., (2009) (hereafter AHHR). (C) For correlation change, we compare with Galeano and Wied, (2017) (hereafter GW), which is essentially a combination of binary segmentation and the correlation change test proposed in Wied et al., (2012). (D) For variance change and autocorrelation change, we compare with Cho and Fryzlewicz, (2012) (hereafter MSML) and Korkas and Fryzlewicz, (2017) (hereafter KF). Both methods are designed for detecting second-order structural change in time series based on wavelet representation. (E) For multi-parameter change and quantile change, to our best knowledge, there is no existing nonparametric method that works under temporal dependence. For illustration, we compare with the energy statistics based segmentation in Matteson and James, (2014) (hereafter ECP) for multi-parameter change and with the multiscale quantile segmentation in Vanegas et al., (2021) (hereafter MQS) for quantile change. Both ECP and MQS require temporal independence. All methods are implemented using the recommended setting in the corresponding R packages or papers. We refer to Section S.2.12 of the supplement for implementation details of these methods.

Implementation details of SNCP: Throughout Sections 4, we set the window size of SNCP to be . We denote SNCP for mean as SNM, for covariance matrix as SNCM, for multi-parameter as SNMP, for correlation as SNC, for variance as SNV, for autocorrelation as SNA, and for quantile as SNQ. In addition, SNM90 denotes SNM using 90% quantile (i.e. critical value at ) of the limiting null distribution as the threshold , and similarly for other types of change and levels of critical value. For the power analysis in Sections 4 and real data applications in Section S.3, the threshold for SNCP is set at 90% quantile of (i.e. ), which can be found in Table 1 for

We remark that the performance of SNCP is robust w.r.t. the window size and the quantile level as the limiting distribution , and thus the threshold , adapt to the effect of and . We refer to Section S.2.1 of the supplement for a detailed sensitivity analysis.

| 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 | |

|---|---|---|---|---|---|---|---|---|---|---|

| 90% | 141.9 | 208.2 | 275.0 | 344.4 | 415.9 | 492.5 | 568.4 | 651.4 | 740.3 | 823.5 |

| 95% | 165.5 | 237.5 | 309.1 | 387.5 | 464.5 | 541.7 | 624.1 | 713.3 | 808.6 | 898.9 |

Error measures of change-point estimation: To assess the accuracy of change-point estimation, we use the Hausdorff distance and adjusted Rand index (ARI). The Hausdorff distance is defined as follows. Denote the set of true (relative) change-points as and the set of estimated (relative) change-points as , we define where measures the over-segmentation error of and measures the under-segmentation error of . The Hausdorff distance is . The ARI is originally proposed in Morey and Agresti, (1984) as a measure of similarity between two different partitions of the same observations for evaluating the accuracy of clustering. Under the change-point setting, we calculate the ARI between partitions of the time series given by and . Ranging from 0 to 1, a higher ARI indicates more coherence between the two partitions by and and thus more accurate change-point estimation.

4.1 No change

We first investigate the performance of SNCP under the null, where the time series is stationary with no change-point. We report the performance of SNM and SNV observed in extensive numerical experiments. The performance of SNCP for other functionals is similar and thus omitted.

We simulate a stationary univariate time series from an AR(1) process where is i.i.d. standard normal . We set 222 is deliberately set as power of 2 as MSML in Cho and Fryzlewicz, (2012) can only handle such sample size. and vary to examine robustness of SNCP against false positives (i.e. Type-I error) under different direction and strength of temporal dependence. Section S.2.3 of the supplement further provides the simulation results for . For each combination of (), we repeat the simulation 1000 times.

The numerical result is summarized in Table 2, where we report the proportion of , and among 1000 experiments. In general, the observation is as follows. SNCP gives satisfactory performance under moderate temporal dependence with for all sample sizes and its performance further improves as the sample size increases.

BP performs well under but exhibits severe over-rejection under positive temporal dependence for and the performance does not improve as increases. KF and MSML perform well under but produce high proportion of false positives under negative temporal dependence for and the performance does not improve as increases. Overall, SNCP provides reasonably accurate size under different direction and strength of temporal dependence and achieves the target size as the sample size increases.

| SNM90 | 0.99 | 0.01 | 0.00 | 0.96 | 0.04 | 0.00 | 0.93 | 0.06 | 0.00 | 0.87 | 0.12 | 0.01 | 0.60 | 0.30 | 0.10 |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| BP | 1.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.99 | 0.01 | 0.00 | 0.35 | 0.12 | 0.53 | 0.00 | 0.00 | 1.00 |

| SNV90 | 0.80 | 0.18 | 0.02 | 0.90 | 0.09 | 0.01 | 0.90 | 0.09 | 0.01 | 0.86 | 0.12 | 0.01 | 0.73 | 0.22 | 0.05 |

| KF | 0.18 | 0.20 | 0.63 | 0.76 | 0.14 | 0.10 | 0.96 | 0.03 | 0.01 | 0.95 | 0.04 | 0.01 | 0.94 | 0.04 | 0.02 |

| MSML | 0.48 | 0.33 | 0.19 | 0.84 | 0.15 | 0.01 | 0.92 | 0.08 | 0.00 | 0.92 | 0.08 | 0.00 | 0.90 | 0.09 | 0.00 |

| SNM90 | 0.94 | 0.06 | 0.00 | 0.89 | 0.10 | 0.00 | 0.89 | 0.10 | 0.01 | 0.88 | 0.11 | 0.01 | 0.84 | 0.14 | 0.02 |

| BP | 1.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 1.00 | 0.00 | 0.00 | 0.49 | 0.13 | 0.38 | 0.00 | 0.00 | 1.00 |

| SNV90 | 0.88 | 0.12 | 0.00 | 0.90 | 0.10 | 0.01 | 0.91 | 0.08 | 0.00 | 0.90 | 0.09 | 0.01 | 0.85 | 0.13 | 0.02 |

| KF | 0.02 | 0.01 | 0.97 | 0.54 | 0.17 | 0.29 | 0.90 | 0.06 | 0.04 | 0.92 | 0.05 | 0.04 | 0.88 | 0.06 | 0.06 |

| MSML | 0.38 | 0.27 | 0.36 | 0.80 | 0.18 | 0.02 | 0.92 | 0.08 | 0.00 | 0.92 | 0.08 | 0.00 | 0.90 | 0.10 | 0.00 |

4.2 Change in mean

For mean change, we first simulate a stationary -dimensional time series from a VAR(1) process with where is i.i.d. standard -variate normal , and denotes the -dimensional identity matrix. We then generate time series with piecewise constant mean based on .

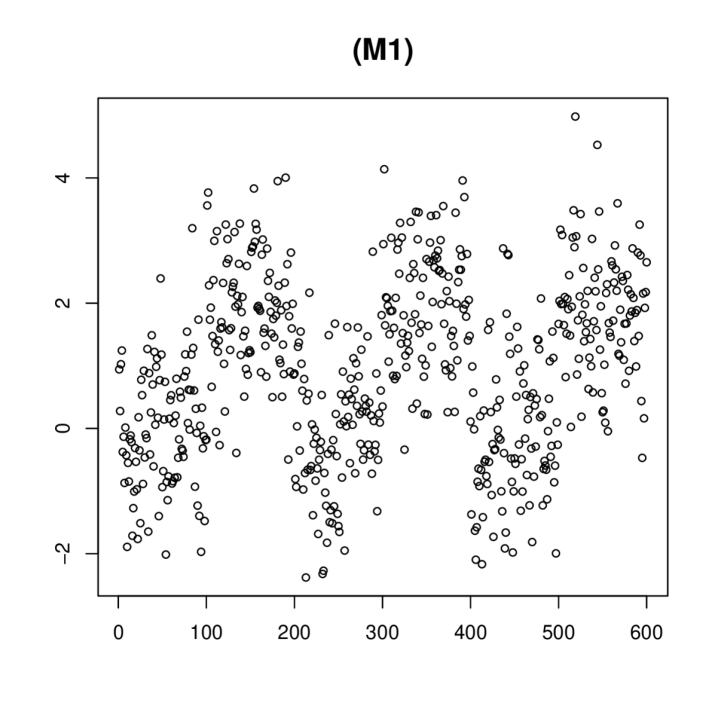

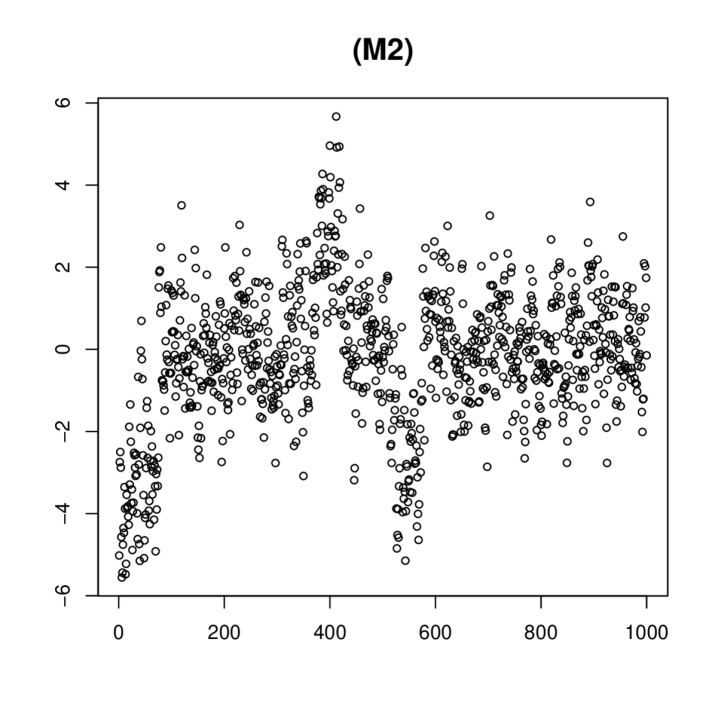

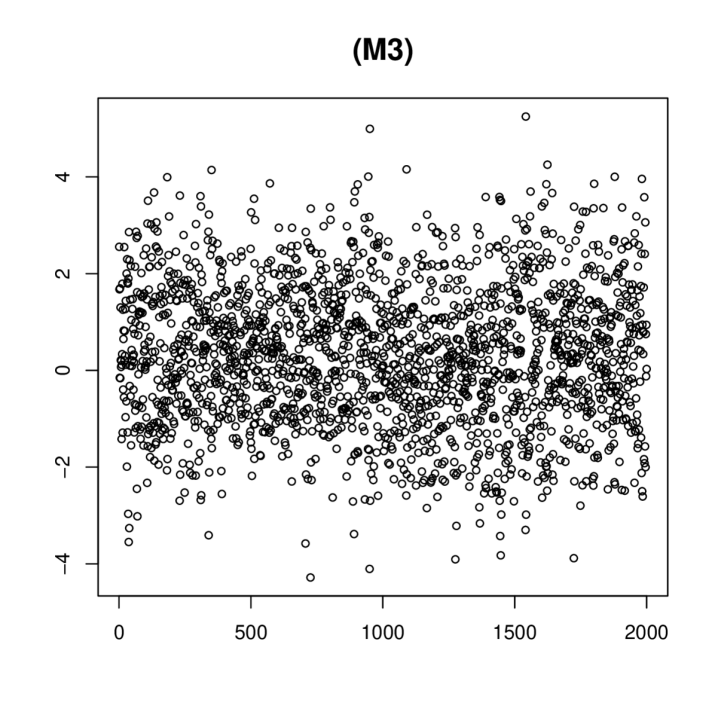

(M1) has evenly spaced change-points with moderate temporal dependence, (M2) features abrupt changes where shortest segments have only 50 or 75 time points with change-points mainly located at the first half of the time series, and (M3) has longer segments with small-scale changes. Typical realizations of (M1)-(M3) for can be found in Figure S.2 of the supplementary material.

Note that the change size in (M1)-(M3) is normalized by to keep the signal-to-noise ratio (SNR) the same across time series of different dimensions. This enables us to isolate and examine the effect of dimension on estimation. Intuitively, a larger makes the estimation more difficult as the quality of finite sample approximation by FCLT worsens for higher dimension.

We set the dimension . Note that BP only works for (i.e. univariate time series) and thus is not included in the comparison for . The estimation results for and are summarized in Table 3, where we report the distribution of , average ARI, over- and under-segmentation errors , and Hausdorff distance among 1000 experiments. The estimation result for can be found in Table S.14 of the supplement.

Univariate time series : For (M1), all methods perform well overall, though CUSUM tends to greatly over-estimate the number of change-points , as reflected by the distribution of . For (M2), SNM tends to slightly under-estimate (missing a short segment) while BP and CUSUM severely over-estimate and provide much less accurate estimation with noticeably larger Hausdorff distance and smaller ARI. For (M3), which corresponds to strong negative dependence, BP experiences severe power loss and have large under-segmentation error . In summary, BP and CUSUM are prone to produce false positives under positive dependence, and BP may lose power under strong negative dependence. SNM is robust but may experience power loss when detecting short segment changes.

Multivariate time series : For (M1) and (M3), the estimation accuracy of SNM is remarkably robust to the increasing dimension, where the ARI and achieved by SNM only worsen slightly from to . This also holds true for (see Table S.14 of the supplement). For (M2), with abrupt changes and strong positive temporal dependence, SNM is less robust to the increasing dimension and gives more false positives for , however, its performance is still decent as measured by ARI and . On the contrary, for all three models (M1)-(M3), the performance of CUSUM worsens significantly from to (and even more so for ).

| Method | Model | ARI | time | ||||||||||

| SNM | 0 | 0 | 9 | 974 | 17 | 0 | 0 | 0.960 | 0.87 | 0.90 | 1.01 | 1.75 | |

| BP | 0 | 0 | 0 | 847 | 142 | 11 | 0 | 0.974 | 1.48 | 0.50 | 1.48 | 9.10 | |

| CUSUM | 0 | 0 | 0 | 438 | 414 | 119 | 29 | 0.944 | 4.43 | 0.53 | 4.43 | 0.05 | |

| SNM | 0 | 11 | 196 | 749 | 43 | 1 | 0 | 0.970 | 1.33 | 1.77 | 2.67 | 3.55 | |

| BP | 0 | 0 | 0 | 425 | 226 | 203 | 146 | 0.863 | 11.68 | 0.19 | 11.68 | 34.04 | |

| CUSUM | 2 | 0 | 15 | 365 | 341 | 190 | 87 | 0.821 | 10.63 | 2.86 | 10.76 | 0.06 | |

| SNM | 0 | 0 | 1 | 986 | 13 | 0 | 0 | 0.969 | 1.11 | 0.80 | 1.14 | 10.59 | |

| BP | 0 | 371 | 6 | 623 | 0 | 0 | 0 | 0.616 | 0.33 | 19.03 | 19.03 | 179.75 | |

| CUSUM | 0 | 0 | 0 | 947 | 53 | 0 | 0 | 0.965 | 1.32 | 0.88 | 1.32 | 0.09 | |

| Method | Model | ARI | time | ||||||||||

| SNM | 0 | 0 | 13 | 946 | 41 | 0 | 0 | 0.953 | 1.16 | 1.12 | 1.37 | 12.48 | |

| CUSUM | 167 | 0 | 0 | 230 | 336 | 189 | 78 | 0.783 | 5.18 | 11.41 | 15.71 | 0.04 | |

| SNM | 0 | 11 | 175 | 628 | 166 | 18 | 2 | 0.937 | 4.59 | 1.93 | 5.68 | 22.88 | |

| CUSUM | 63 | 5 | 5 | 98 | 161 | 213 | 455 | 0.626 | 18.02 | 5.77 | 20.88 | 0.07 | |

| SNM | 0 | 0 | 4 | 993 | 3 | 0 | 0 | 0.968 | 0.93 | 0.96 | 1.03 | 60.00 | |

| CUSUM | 0 | 70 | 0 | 928 | 2 | 0 | 0 | 0.896 | 1.02 | 4.50 | 4.52 | 0.07 | |

4.3 Change in covariance matrix

For covariance matrix change, we adopt the simulation settings in Aue et al., (2009) and detect change in covariance matrices of a four-dimensional time series with . Thus, the number of parameters in the covariance matrix is . Denote as an exchangeable covariance matrix with unit variance and equal covariance , we consider

Here, is a two-dimensional stationary VAR(1) process with the transition matrix and denotes the factor loading matrix. (C1) and (C2) generate covariance changes in the dynamic factor model, which is widely used in the time series literature. We refer to Section S.2.10 of the supplement for additional simulation settings with covariance changes in VAR models. The estimation result is reported in Table 4. For monotonic changes (C2), both methods perform well though AHHR tends to over-estimate the number of change-points, while for non-monotonic changes (C1), AHHR seems to over-estimate and experience power loss at the same time and is outperformed by SNCM. For (C0), both methods give decent performance under moderate temporal dependence with SNCM achieving the target size more accurately.

| Method | Model | ARI | time | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SNCM | 0 | 1 | 19 | 951 | 29 | 0 | 0 | 0.923 | 2.13 | 2.46 | 2.78 | 56.44 | |

| AHHR | 0 | 221 | 0 | 687 | 82 | 10 | 0 | 0.721 | 2.45 | 12.37 | 13.50 | 0.44 | |

| SNCM | 0 | 0 | 59 | 902 | 39 | 0 | 0 | 0.898 | 2.53 | 3.95 | 4.37 | 55.17 | |

| AHHR | 0 | 0 | 1 | 792 | 168 | 32 | 7 | 0.896 | 4.97 | 2.34 | 5.00 | 0.56 | |

| Method | Model | ||||||||||||

| SNCM | 916 | 80 | 4 | ||||||||||

| AHHR | 932 | 59 | 9 | ||||||||||

4.4 Change in multi-parameter

As discussed before, one notable advantage of SNCP is its universal applicability, where it treats change-point detection for a broad class of parameters in a unified fashion. To conserve space, we refer to Sections S.2.5, S.2.6, S.2.7 and S.2.8 of the supplement for extensive numerical evidence of the favorable performance of SNCP for change-point detection in variance, auto-correlation, correlation and quantile.

In this section, we further consider change-point estimation for multi-parameter of a univariate time series, where we aim to detect any structural break among multiple parameters of interest. This can be useful for practical scenarios where one does not know the exact nature of the change but wishes to detect any change among a group of parameters of interest. For example, if one is interested in central tendency of the time series, SNMP can be used to simultaneously detect change in mean and median, while if the user suspects there is change in the dispersion/volatility of the data, SNMP can be used to detect change jointly in variance and high quantiles.

In some sense, this is related to change-point detection in distribution (e.g. ECP, Matteson and James,, 2014), where the focus is to detect any change in the marginal distribution of a univariate time series. In theory, algorithms that target distributional change can capture all potential changes in the data. However, it only informs users the existence of a change but is unable to narrow down the specific type of change (e.g. is the detected change in central tendency or in volatility?). This can be less informative in real data analysis when the practitioner is particularly concerned about one certain behavior change of the data and may also lead to potential power loss compared to methods that target a specific type of change. In addition, existing methods on distributional change typically require the temporal independence assumption, such as ECP in Matteson and James, (2014).

We consider two simulation settings with , and compare the performance of SNMP and ECP.

For (MP1), follows an AR(1) process with where and is i.i.d. , denotes the CDF of , and denotes a mixture of a truncated normal and a generalized Pareto distribution such that for and for Thus, for (MP1), the change originates from upper quantiles. We refer to Section S.2.8 of the supplement for the detailed definition of and its motivation from financial applications. For (MP2), is i.i.d. , thus we have temporal independence and the change is solely driven by variance.

The estimation result is summarized in Table 5. We compare the performance of SNCP based on individual parameters and their multi-parameter combination. For clarity, we specify the multi-parameter set that SNMP targets. For example, SNQ90V denotes the SNMP that targets 90% quantile and variance simultaneously. For (MP1), SNQ90 and SNQ95 perform well as the change originates from upper quantiles, and further improvement can be achieved by combining them into multi-parameter SNQ90,95. Similarly, including variance in the multi-parameter set further improves the estimation accuracy. ECP provides decent performance but tends to over-estimate due to the temporal dependence of the time series. For (MP2), since the change is solely driven by variance, SNV gives the best performance, while quantile based detection, such as SNQ90 experiences power loss. However, the multi-parameter detection based on SNQ10,90 and SNQ10,20,80,90 provide much improved performance over SNQ90, though similar to ECP, they do experience certain power loss compared to SNV. Moreover, SNMP performs competently compared to SNV once variance is included in the multi-parameter set.

This numerical study clearly demonstrates the versatility of SNCP, where it can be effortlessly tailored to target various types of parameter change and their multi-parameter combination. Moreover, compared to detection based on an individual parameter, multi-parameter detection tends to enhance power and improve estimation accuracy when the underlying change affects several parameters in the considered multi-parameter set. We further illustrate this point in more details via real data analysis in Section S.3.2.

| Method | Model | ARI | time | ||||||||||

| SNQ90 | 0 | 10 | 132 | 805 | 50 | 3 | 0 | 0.839 | 3.25 | 7.26 | 7.85 | 17.74 | |

| SNQ95 | 0 | 5 | 100 | 820 | 73 | 2 | 0 | 0.868 | 3.16 | 5.70 | 6.62 | 17.20 | |

| SNV | 0 | 2 | 110 | 832 | 54 | 2 | 0 | 0.869 | 2.45 | 5.47 | 6.06 | 12.20 | |

| SNQ90,95 | 0 | 3 | 82 | 850 | 62 | 3 | 0 | 0.878 | 3.01 | 4.88 | 5.67 | 39.56 | |

| SNQ90V | 0 | 0 | 56 | 869 | 70 | 5 | 0 | 0.891 | 3.04 | 3.95 | 4.77 | 30.96 | |

| SNQ95V | 0 | 2 | 64 | 861 | 68 | 5 | 0 | 0.889 | 2.92 | 4.30 | 5.14 | 30.81 | |

| SNQ90,95V | 0 | 2 | 48 | 882 | 66 | 2 | 0 | 0.894 | 2.95 | 3.79 | 4.58 | 49.72 | |

| ECP | 0 | 0 | 0 | 730 | 144 | 92 | 34 | 0.850 | 6.33 | 3.68 | 6.41 | 10.58 | |

| SNV | 0 | 0 | 14 | 956 | 28 | 2 | 0 | 0.928 | 2.15 | 2.13 | 2.60 | 12.28 | |

| SNQ90 | 0 | 71 | 282 | 596 | 48 | 3 | 0 | 0.705 | 4.10 | 15.72 | 16.33 | 17.50 | |

| SNQ10,90 | 0 | 13 | 165 | 788 | 32 | 2 | 0 | 0.826 | 3.00 | 8.36 | 8.84 | 39.62 | |

| SNQ90V | 0 | 0 | 32 | 929 | 39 | 0 | 0 | 0.913 | 2.42 | 2.95 | 3.45 | 30.92 | |

| SNQ10,90V | 0 | 1 | 50 | 917 | 32 | 0 | 0 | 0.903 | 2.37 | 3.67 | 4.06 | 49.74 | |

| SNQ10,20,80,90 | 0 | 5 | 118 | 816 | 60 | 1 | 0 | 0.849 | 3.41 | 6.51 | 7.27 | 68.96 | |

| ECP | 0 | 49 | 46 | 807 | 79 | 15 | 4 | 0.833 | 3.43 | 6.78 | 7.58 | 9.96 | |

For each estimated change-point by SNMP, one may want to identify which features actually changed. One informal strategy is to further conduct a subsequent SN-test. Specifically, for each estimated change-point, based on a well-designed local interval, we can further conduct a single change-point SN test via (2) for each feature and determine if it is changed at this very change-point. Though this procedure is obviously subject to multiple testing issues, it can shed some light on which feature actually changed. We refer to Section S.8.1 for more details of this informal procedure.

5 Conclusion

In this paper, we present a novel and unified framework for time series segmentation in multivariate time series with rigorous theoretical guarantees. Our proposed method is motivated by the recent success of the SN method (Shao,, 2015) and advances the methodological and theoretical frontier of statistics literature on change-point estimation by adapting the general framework of approximately linear functional in Künsch, (1989). Our method is broadly applicable to the estimation of piecewise stationary models defined in a general functional. In terms of statistical theory, the consistency and convergence rate of change-point estimation are established under the multiple change-points setting for the first time in the literature of SN-based change-point analysis.

For future research, it may be desirable to relax the piecewise constant assumption and allow the parameter to vary smoothly within each segment; see Wu and Zhou, (2019) for such a formulation in nonparametric trend models and Casini and Perron, 2021a in locally stationary time series.

Supplementary Material

The supplementary material is organized as follows. Section S.1 illustrates the failure of combining the proposed SN-based test with the classical binary segmentation or a pure local-window based segmentation algorithm. Section S.2 contains additional simulation results. Section S.3 illustrates the effectiveness and practical significance of SNCP via meaningful real data applications in climate science and finance. Section S.4 provides detailed verification for technical assumptions of SNCP for the smooth function model, which includes a wide class of parameters such as mean, variance, (auto)-covariance and (auto)-correlation. Section S.5 further provides detailed verification for technical assumptions of SNCP for quantiles. Section S.6 contains the consistency proof of SNCP for a general univariate functional. In Section S.7, we further provide the proof for the consistency of SNCP for detecting changes in multivariate mean. Section S.8 proposes a simple local refinement procedure for SNCP, which improves the localization error rate of SNCP to the optimal rate for the mean functional.

There are 12 subsections in Section S.2. In particular, Section S.2.1 conducts sensitivity analysis w.r.t. to the choice of the window size and the critical value level for SNCP; Section S.2.2 provides extensive numerical comparison between the proposed nested local-window segmentation algorithm and other popular state-of-the-art segmentation algorithms (WBS, SBS, NOT and fused-LASSO) for detecting changes in univariate and multivariate mean; Section S.2.3 contains additional results for no change; Section S.2.4 presents additional numerical comparison between SNCP and the conventional CUSUM for the multivariate mean case; Section S.2.5, S.2.6, S.2.7, S.2.8 and S.2.9 conduct numerical comparison between SNCP and other popular change-point detection methods for variance, auto-correlation, correlation, and quantile changes, respectively; Section S.2.10 contains additional results for changes in covariance matrix; Section S.2.11 provides additional simulation results for changes in multi-dimensional parameters; Section S.2.12 contains the implementation details of comparison methods and typical realizations of DGP used in simulation.

In terms of notation, throughout the supplement, we let with dimension be a set of random vector defined in a probability space . For a corresponding set of constants , we say if for any , there exists a finite and a finite such that for all ,

where denotes the norm, i.e. we say if both and are bounded (from above) in probability. In addition, we let be a generic constant that may vary from line to line.

S.1 Failure of SN with binary segmentation and the pure local-window based segmentation

S.1.1 Theoretical evidence

In this section, we provide theoretical evidence to demonstrate that a simple combination of the proposed SN test statistic and the classical binary segmentation can suffer severe power loss and inconsistency under the multiple change-point scenario.

For simplicity, we focus on the univariate mean case with two change-points. Suppose is generated by:

where is a constant, is a stationary time series, and , with denotes the two change-points.

In the following, we explicitly derive the asymptotic limit of the SN test statistic based on the entire sample and show that the asymptotic order of is (see Section 2 of the main text for detailed definition of ). Note that the binary segmentation algorithm uses to detect the existence of potential change-points and thus indicates the power loss and asymptotic inconsistency of the binary segmentation algorithm.

Denote . By simple calculation, the contrast statistic takes the form

Similarly, we can derive the explicit form of the self-normalizer . For ,

For ,

For ,

Thus, by the FCLT that , we have that

and

where , and

In other words, the asymptotic limit of the SN test statistic is a deterministic constant . This interesting phenomenon is caused by the existence of the two change-points, which inflates the self-normalizer and thus deflates the SN test statistic .

Together, this implies that . Hence the probability of detecting change-points is less than 1 even when , indicating the power loss and asymptotic inconsistency for a simple combination of the SN test and binary segmentation.

As explained in the main text, unlike the classical binary segmentation, which evaluates the SN test based on the whole sample, the proposed nested local-window segmentation bypasses this power loss issue due to inflated self-normalizer by evaluating the SN test statistic on a set of carefully designed nested local-windows.

Another popular segmentation algorithm in the change-point literature is the pure local-window based approach, see for example, Niu and Zhang, (2012), Yau and Zhao, (2016) and Niu et al., (2016). Compared to the proposed nested local-window segmentation algorithm in our paper, the pure local-window approach only considers one single local-window around each time point in the data.

Specifically, denote the window size as , following the notation in Section 3 of the main text, for each , the pure local-window approach computes the SN-based test for time point via

In other words, the pure local-window approach only computes the SN-based statistic on the smallest local-window . The change-point estimator is then obtained by comparing the so-called local-window maximizer (see Niu and Zhang, (2012) for detailed definition) of with a properly chosen threshold. Following the same argument as the one for Theorem 3.1 in the main text, we can easily show that

Thus, we can use the 90% or 95% quantile of the limiting distribution as the threshold for the pure local-window approach, which controls the asymptotic false positive detection rate.

In comparison, the proposed nested local-window segmentation algorithm computes the SN-based test for each time point via

based on a series of expanding nested local-windows surrounding indexed by Note that is the smallest local-window in . As discussed in the main text, such a strategy is expected to achieve higher power than the pure local-window approach, especially for the case where the change-point is far away from other change-points by utilizing larger nested windows that cover other than . We further verify this claim in Section S.1.2 via numerical study.

S.1.2 Numerical evidence

In this section, we demonstrate the power loss of the simple combination between the SN test and the classical binary segmentation or the pure local-window approach via a small simulation example. To illustrate, we simulate from

where is a stationary AR(1) process such that where is i.i.d. . Note that the main difference between (M4) and (M5) is that the mean change in (M4) is non-monotonic while the mean change in (M5) is monotonic.

We apply the proposed nested local-window based SNM for change-point detection in mean. We further apply the simple combination between the SN test and the classical binary segmentation (SNBS) or the pure local-window approach (SNLocal). The estimation result is summarized in Table S.6. As can be seen clearly, SNLocal has severe power loss compared to SNM in both (M4) and (M5), indicating the advantage of the proposed nested local-window segmentation over the pure local-window approach. In addition, under the non-monotonic change in (M4), SNBS almost completely loses power while its performance is comparable to SNM under monotonic change in (M5). In summary, this result suggests the necessity of the proposed nested local-window segmentation algorithm in SNCP for change-point detection.

| Method | Model | ARI | time | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| SNM | 0 | 19 | 237 | 688 | 51 | 5 | 0 | 0.825 | 3.57 | 9.03 | 10.20 | 11.54 | |

| SNBS | 0 | 981 | 19 | 0 | 0 | 0 | 0 | 0.009 | 0.14 | 49.66 | 49.66 | 0.61 | |

| SNLocal | 0 | 563 | 329 | 94 | 12 | 2 | 0 | 0.250 | 3.25 | 39.10 | 39.52 | 0.10 | |

| SNM | 0 | 11 | 268 | 669 | 49 | 3 | 0 | 0.824 | 3.60 | 9.09 | 10.23 | 11.35 | |

| SNBS | 0 | 2 | 56 | 722 | 215 | 5 | 0 | 0.800 | 7.24 | 6.33 | 8.38 | 1.02 | |

| SNLocal | 0 | 528 | 369 | 85 | 17 | 1 | 0 | 0.273 | 3.14 | 38.17 | 38.56 | 0.10 | |

S.2 Additional Simulation Results

S.2.1 Sensitivity analysis

In this section, we conduct sensitivity analysis of SNCP w.r.t. the window size and the critical value level . Specifically, we vary and vary the critical value level , and study how influences the performance of SNCP. For clarity of presentation, in the following, we use the quantile level to refer to the critical value level .

Recall that the window size reflects one’s belief of minimum (relative) spacing between two consecutive change-point and the quantile value level balances one’s tolerance of type-I and type-II errors. For consistency of SNCP, we require , which is the minimum spacing between change-points.

We consider two simulation settings (SA1) and (SA2) for change in mean. Specifically, we first simulate a stationary unit-variance univariate time series from a unit-variance AR(1) process with where is i.i.d. standard normal . We then generate univariate time series with piecewise constant mean based on

Note that for both (SA1) and (SA2), all change-points are evenly located with the minimum spacing

For (SA1), the noise is i.i.d. Gaussian random variables as . We further vary to generate two scenarios with low and high signal-to-noise ratios (SNR). For (SA2), the noise is a stationary AR(1) process with moderate temporal dependence We set to generate scenarios with low and high SNR. Note that compared to (SA1), in (SA2) is multiplied by a factor of to compensate the long-run variance (LRV) of , which is . Thus, (SA1) and (SA2) have the same level of SNR.

The estimation results under (SA1) and (SA2) are summarized in Table S.7 and Table S.8. The general findings are as follows. We focus on the result of (SA1) as the result of (SA2) is similar.

Robustness w.r.t. the window size : The performance of SNCP is reasonably robust across all window sizes , as evidenced by the stable values of ARI and Hausdorff distance achieved across different . This is especially true for the high SNR scenario.

On the other hand, SNCP fails to detect changes with the window size , which exceeds the minimum spacing . This is consistent with the discussion in Section 3.1 of the main text. As for , even the smallest local-window centered around any true change-point contains at least two change-points, this significantly lowers the power of SN-tests due to inflated self-normalizer. The drastic contrast between the performance of SNCP with and is partially due to the fact that in (SA1), all change-points are evenly spaced with the same spacing , thus the assumption is violated all at once for all change-points.

Note that though SNCP with may not always deliver the best performance among all window sizes, it does offer one of the best performance under both low and high SNR scenarios. Thus, we recommend setting as it guards against the violation of to the best extent.

Robustness w.r.t. the quantile level : The choice of the quantile level is less essential for SNCP and it is more about the trade-off between type-I and type-II error in finite sample. As can be seen in Table S.7, for low SNR, given the same window size , the quantile level provides better performance due to higher power, while for high SNR, the difference between and is minimal. Of course, setting will incur higher type-I error when there is no change-point.

Finally, comparing the estimation results in Table S.7 (SA1) and Table S.8 (SA2), it can be seen that given the same SNR, the robustness of SNCP w.r.t. the window size and the quantile level remain the same with or without temporal dependence.

| Model | ARI | time | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 90, 0.05 | 0 | 2 | 89 | 899 | 10 | 0 | 0 | 0.930 | 1.07 | 2.09 | 2.14 | 3.34 | |

| 95, 0.05 | 0 | 19 | 180 | 796 | 5 | 0 | 0 | 0.916 | 1.02 | 3.31 | 3.33 | 3.34 | |

| 90, 0.08 | 0 | 26 | 169 | 805 | 0 | 0 | 0 | 0.913 | 1.00 | 3.30 | 3.30 | 1.20 | |

| 95, 0.08 | 8 | 75 | 282 | 635 | 0 | 0 | 0 | 0.886 | 0.95 | 5.38 | 5.38 | 1.20 | |

| 90, 0.10 | 0 | 1 | 46 | 953 | 0 | 0 | 0 | 0.931 | 1.04 | 1.59 | 1.59 | 0.71 | |

| 95, 0.10 | 0 | 16 | 102 | 882 | 0 | 0 | 0 | 0.921 | 1.02 | 2.44 | 2.44 | 0.71 | |

| 90, 0.12 | 0 | 6 | 148 | 846 | 0 | 0 | 0 | 0.930 | 0.77 | 2.37 | 2.37 | 0.47 | |

| 95, 0.12 | 1 | 15 | 173 | 811 | 0 | 0 | 0 | 0.924 | 0.76 | 2.80 | 2.80 | 0.47 | |

| 90, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.002 | 0.00 | 49.95 | 49.95 | 0.27 | |

| 95, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.001 | 0.00 | 50.01 | 50.01 | 0.27 | |

| Method | Model | ARI | time | ||||||||||

| 90, 0.05 | 0 | 0 | 3 | 980 | 17 | 0 | 0 | 0.963 | 0.68 | 0.63 | 0.72 | 3.76 | |

| 95, 0.05 | 0 | 0 | 7 | 982 | 11 | 0 | 0 | 0.963 | 0.65 | 0.68 | 0.73 | 3.76 | |

| 90, 0.08 | 0 | 0 | 13 | 987 | 0 | 0 | 0 | 0.961 | 0.60 | 0.75 | 0.75 | 1.34 | |

| 95, 0.08 | 0 | 0 | 39 | 961 | 0 | 0 | 0 | 0.958 | 0.59 | 1.06 | 1.06 | 1.34 | |

| 90, 0.10 | 0 | 0 | 1 | 999 | 0 | 0 | 0 | 0.959 | 0.65 | 0.66 | 0.66 | 0.80 | |

| 95, 0.10 | 0 | 0 | 5 | 995 | 0 | 0 | 0 | 0.958 | 0.64 | 0.70 | 0.70 | 0.80 | |

| 90, 0.12 | 0 | 0 | 38 | 962 | 0 | 0 | 0 | 0.956 | 0.59 | 0.99 | 0.99 | 0.53 | |

| 95, 0.12 | 0 | 0 | 39 | 961 | 0 | 0 | 0 | 0.956 | 0.59 | 1.00 | 1.00 | 0.53 | |

| 90, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.000 | 0.00 | 50.01 | 50.01 | 0.31 | |

| 95, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.000 | 0.00 | 50.00 | 50.00 | 0.31 | |

| Model | ARI | time | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 90, 0.05 | 0 | 1 | 89 | 882 | 27 | 1 | 0 | 0.933 | 1.12 | 2.06 | 2.18 | 3.12 | |

| 95, 0.05 | 0 | 26 | 175 | 788 | 11 | 0 | 0 | 0.918 | 1.01 | 3.32 | 3.38 | 3.12 | |

| 90, 0.08 | 0 | 33 | 195 | 772 | 0 | 0 | 0 | 0.911 | 0.97 | 3.65 | 3.65 | 1.10 | |

| 95, 0.08 | 16 | 85 | 302 | 597 | 0 | 0 | 0 | 0.880 | 0.92 | 5.92 | 5.92 | 1.10 | |

| 90, 0.10 | 0 | 4 | 58 | 938 | 0 | 0 | 0 | 0.931 | 1.02 | 1.75 | 1.75 | 0.66 | |

| 95, 0.10 | 0 | 24 | 120 | 856 | 0 | 0 | 0 | 0.919 | 0.99 | 2.74 | 2.74 | 0.66 | |

| 90, 0.12 | 0 | 4 | 130 | 866 | 0 | 0 | 0 | 0.933 | 0.77 | 2.17 | 2.17 | 0.44 | |

| 95, 0.12 | 1 | 14 | 159 | 826 | 0 | 0 | 0 | 0.926 | 0.76 | 2.69 | 2.69 | 0.44 | |

| 90, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.002 | 0.00 | 49.98 | 49.98 | 0.25 | |

| 95, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.001 | 0.00 | 50.01 | 50.01 | 0.25 | |

| Model | ARI | time | |||||||||||

| 90, 0.05 | 0 | 0 | 4 | 964 | 31 | 1 | 0 | 0.965 | 0.72 | 0.60 | 0.77 | 2.88 | |

| 95, 0.05 | 0 | 0 | 11 | 968 | 21 | 0 | 0 | 0.965 | 0.66 | 0.68 | 0.79 | 2.88 | |

| 90, 0.08 | 0 | 0 | 16 | 984 | 0 | 0 | 0 | 0.963 | 0.58 | 0.77 | 0.77 | 1.03 | |

| 95, 0.08 | 0 | 2 | 48 | 950 | 0 | 0 | 0 | 0.958 | 0.57 | 1.17 | 1.17 | 1.03 | |

| 90, 0.10 | 0 | 0 | 2 | 998 | 0 | 0 | 0 | 0.961 | 0.62 | 0.65 | 0.65 | 0.61 | |

| 95, 0.10 | 0 | 0 | 8 | 992 | 0 | 0 | 0 | 0.961 | 0.62 | 0.72 | 0.72 | 0.61 | |

| 90, 0.12 | 0 | 0 | 34 | 966 | 0 | 0 | 0 | 0.958 | 0.59 | 0.95 | 0.95 | 0.41 | |

| 95, 0.12 | 0 | 0 | 34 | 966 | 0 | 0 | 0 | 0.958 | 0.59 | 0.95 | 0.95 | 0.41 | |

| 90, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.000 | 0.00 | 50.01 | 50.01 | 0.24 | |

| 95, 0.15 | 1000 | 0 | 0 | 0 | 0 | 0 | 0 | 0.000 | 0.00 | 50.00 | 50.00 | 0.24 | |

S.2.2 Comparison with state-of-the-art segmentation algorithms

In this subsection, we further demonstrate the promising performance of the proposed nested local-window segmentation algorithm (i.e. SCNP) by comparing it with state-of-the-art segmentation algorithms in the change-point literature. In particular, we consider the wild binary segmentation (WBS) in Fryzlewicz, (2014), the narrowest over threshold (NOT) in Baranowski et al., (2019) and their variants including seeded binary segmentation (SBS) and seeded NOT (SNOT) in Kovacs et al., (2020). We also compare with the change-point estimators by least squares with total variation penalty (i.e. the fused LASSO penalty) in Harchaoui and Lévy-Leduc, (2010), which is denoted by LASSO.

WBS, NOT, SBS and SNOT are generic segmentation algorithms that can be combined with a specific change-point test statistic to achieve multiple change-point detection and are robust to non-monotonic changes. Thus, we combine the SN-based test statistic proposed in the main text (equation (7)) with WBS, NOT, SBS and SNOT to construct multiple change-point detection procedures SN-WBS, SN-NOT, SN-SBS and SN-SNOT, respectively.

For SN-WBS and SN-NOT, we set the number of random intervals used in the algorithm at . Furthermore, we consider two versions of SN-WBS and SN-NOT, where we set the minimal length of the random intervals to be (default value in WBS and NOT) or (same as the minimum nested local window in SNCP with ), and denote the corresponding procedures by the superscript 1 or 2, respectively.

For SN-SBS and SN-SNOT, following Kovacs et al., (2020), we set the decay rate for the seeded intervals to be or , and denote the corresponding procedures by the superscript 1 or 2, respectively. Note that for SN-SBS and SN-SNOT, the minimal length of the seeded intervals is only set at with , instead of , to avoid overwhelming number of short seeded intervals that are not suitable for the use of self-normalization.

S.2.2.1 Univariate mean change

For simulation comparison, we first consider the change in univariate mean setting, specifically models (M1), (M2) and (M3) with , as in Section 4.2 of the main text.

The estimation result is summarized in Table S.9. As can be seen, for all three models (M1)-(M3), the proposed SNM gives comparable (or more favorable in (M2)) performance as SN-WBS, SN-NOT, SN-SBS and SN-SNOT and outperforms LASSO. Furthermore, SNM is computationally more efficient than SN-WBS and SN-NOT, and comparable with SN-SBS, SN-SNOT and LASSO. This further confirms the value of the proposed nested local-window segmentation algorithm. Moreover, in unreported simulation experiments, similar findings are confirmed universally under other simulation settings such as change in variance, covariance, auto-correlation and quantile.