Matrix completion and semidefinite matrices

Abstract

Positive semidefinite Hermitian matrices that are not fully specified can be completed provided their underlying graph is chordal. If the matrix is positive definite the completion can be uniquely characterized as the matrix that maximizes the determinant, or as the matrix whose inverse has zeroes in those places that were undetermined in the original matrix. This paper extends these uniqueness results to the case of semidefinite matrices. Because the determinant vanishes for singular matrices, and because the inverse does not exist, we introduce a generalized determinant and use generalized inverses to formulate equivalent characterizations in the semidefinite case. For a class of matrices that are singular but of maximal rank unique characterizations can be given, just as in the positive definite case.

AMS classification: 15A10; 15A15; 15A18; 15A83; 15B48

Keywords: positive definite; positive semidefinite; matrix completions

1 Introduction

The question of which partial Hermitian matrices can be completed to give a fully specified positive definite Hermitian matrix was solved in [1]. The solution provided in [1] was constructive but only gave one element of the completion with each step. While giving the correct solution, the practical implementation of this procedure was rather tedious. In [2] a faster procedure was proposed that delivered the same matrix in far fewer steps by focusing on whole blocks of the matrix at once.

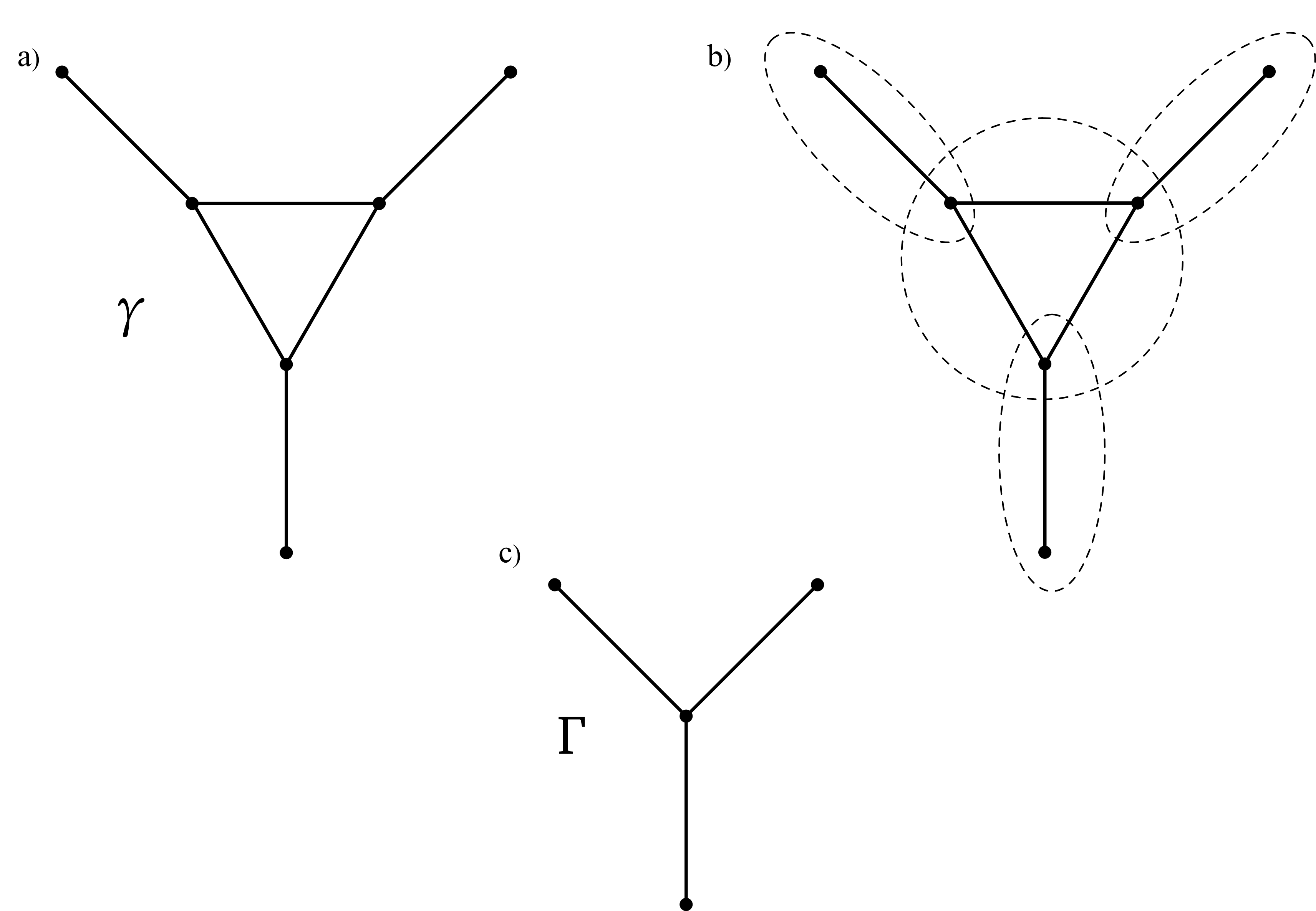

The starting point of both procedures is the graph that is constructed from the partial matrix. The vertices of are given by the rows (or columns) , , of the matrix . Two vertices and of are connected by an edge if the element

| (1) |

of the matrix is given. There is now one condition that the graph has to satisfy for the procedure to work: The graph has to be chordal. A graph is chordal if every loop of four or more elements has a chord, i.e. an edge that connects two nonconsecutive elements of the loop (for an introduction to graph theoretic notions see [3]). Given the graph we can now proceed by constructing another graph . The vertices of are given by the cliques of (a clique is a maximal set of vertices that are all connected to each other; again see [3]) and two vertices of are connected if the two corresponding cliques have a nonempty intersection (see figure 1).

The contribution of [2] is to show that the completion procedure can be reduced to edges of the graph . Any edge in is given by two cliques and that have a nonzero intersection . Let

| (2) |

be the submatrix of with rows and column indices in and let

| (3) |

be the submatrix of with rows and column indices in . We then have

| (4) |

We can combine these two matrices in one large matrix with row and column indices in ,

| (5) |

where the matrix remains to be specified. It was now shown in [2, Theorem 3.2.] that a partial positive semidefinite matrix can be completed to a positive semidefinite matrix by choosing

| (6) |

where denotes the Moore-Penrose inverse of (see [4] and [5] for details on the Moore-Penrose inverse). Note that the matrix does not need to be positive definite for the construction to work. It it sufficient for the matrix to be positive semidefinite.

If the matrix is positive definite the choice of in equation (6) can be uniquely characterized in two ways. First, it is the choice that maximizes the determinant of the completed matrix. It is also the choice for which the inverse of has zeroes in those places where sits in .

We see that the treatment of positive definite and positive semidefinite matrices differs. For positive definite matrices the completion in equation (6) has properties that uniquely determine it. For the semidefinite case we are just left with the existence result. Since the determinant of a singular matrix vanishes and since the inverse of a singular matrix does not exist it is not clear if we can hope to improve this situation.

In this paper we now make two contributions. The first contribution is a new proof that the from equation (6) gives a positive semidefinite completion of . We then extend the uniqueness results to the semidefinite case. To do this we need to introduce a generalized determinant that gives the determinant of the nonsingular part of the matrix. This determinant lacks many of the nice properties that the usual determinant has. If we restrict our attention to a special class of matrices, though, we can prove three results that hold for positive definite matrices: Fischer’s inequality, the Schur determinant lemma, and Banachiewicz’s form of the inverse. These three results will then be used to uniquely characterize the completion in equation (6) for semidefinite matrices.

We start by introducing the class of matrices for which our results are valid.

2 Partitioned matrices of maximal rank

Let the Hermitian matrix be partitioned as follows:

| (7) |

with , , , . Let be the decomposition of in accordance with the partition of in equation (7) so that is a map from to , and is a map from to . Let us further assume that is positive semidefinite. Let be an element of the nullspace of , i.e. let . For we then have

| (8) |

Since is positive semidefinite this implies (see [5]) that we already have

| (9) |

or

| (10) |

In a similar fashion we can establish that the nullspace of is contained in the null space of :

| (11) |

The relations for the nullspaces are equivalent to these relations for the ranges of and :

| (12) | ||||

| (13) |

Because of these properties is said to have the column inclusion property[5]. It follows from equations (10) and (11) that

| (14) |

This implies that the rank of is less than or equal to the sum of the ranks of and :

| (15) | ||||

| (16) | ||||

| (17) | ||||

| (18) |

We have equality if and only if . In the following, matrices for which this equality holds will be of particular interest to us which is why we make the following definition:

Definition 1.

Let be a positive semidefinite Hermitian matrix that is partitioned as in equation (7). We say that is of maximal rank if and only if 111We should be precise and say that is of maximal rank with respect to the partition in equation (7). For the sake of readability we will refrain from doing so and rely on the reader to infer the partition from the context..

When is of maximal rank, it vanishes on

| (19) |

and is positive definite when restricted to the sum of the ranges of and :

| (20) |

In section 4 we will use this property to extend results that are valid for positive definite matrices to partitioned matrices of maximal rank. We need one more notion before we can formulate these results.

3 The generalized determinant

A Hermitian matrix defines a nonsingular map from its range to its range . If the nullspace is nonzero, i.e. if is singular, the determinant of vanishes. The determinant thus contains no information about the nonsingular map that is restricted to . To recover this information we introduce a generalized determinant :

Definition 2.

Let be Hermitian. Let be restricted to the range of :

| (21) |

For we then set

| (22) |

For we set .

We note a number of properties of the generalized determinant:

Lemma 3.1.

Let be Hermitian of rank . Let , be the eigenvalues of . Let us assume that they are ordered in such a way that , for . We then have:

-

1.

If is of full rank (i.e. if ) we have

(23) -

2.

For we have

(24) -

3.

We have

(25) -

4.

For we have

(26)

Proof.

All of these identities follow from the fact that for a unitary and a diagonal that contains the eigenvalues of on the diagonal. ∎

We note that the generalized determinant lacks many of the properties the usual determinant has. In particular, it is not a continuous function of , and the generalized determinant of the product of two matrices is not the product of the two generalized determinants.

4 The extensions

With the preparations in section 2, and the definition of the generalized determinant in the last section, we now want to extent three results to singular matrices: Fischer’s inequality, the determinant equality for the Schur complement, and Banachiewicz’s form of the inverse of a matrix.

4.1 Fischer’s inequality

Fischer’s inequality states that for a Hermitian positive semidefinite as in equation (7) we have (see e.g. [7]):

| (27) |

Furthermore, if is positive definite, we have equality if and only if . If is singular, the determinant of vanishes and the inequality is no longer much of a constraint. We can also no longer infer that vanishes in the case of equality.

We can do better when is of maximal rank. In this case vanishes on and is positive definite on

| (28) |

We now look at the restriction of and all its submatrices to this space and use the Fischer’s inequality there. Note that because is positive semidefinite it has the column (and row) inclusion property and we have

| (29) |

and

| (30) |

thus vanishes on the complement of and maps into . The restriction of to thus keeps the nontrivial part of . The same is true for and its restriction to . As in definition 2, we denote the restriction of to its range by . We obtain

| (31) | ||||

| (32) | ||||

| (33) |

Because we are looking at the restriction of to and because is positive definite on , we also get that , when restricted to , vanishes if and only if equality holds above. Since vanishes on , this is the case if and only if

| (34) |

We thus have the following result:

Proposition 4.1.

Let a Hermitian be positive semidefinite and partitioned as in equation (7). If is of maximal rank then

| (35) |

with equality if and only if .

Let us note that we arrived at this result in two steps. Because is positive semidefinite we know that restricted to is zero. That the restriction of to the range is also zero follows from Fischer’s equality for the positive definite matrix that is restricted to .

4.2 Schur complement

The Schur complement arises naturally when using Gaussian elimination to solve a linear equation. Let be as in equation (7) and let us assume we want to solve

| (36) | ||||

| (37) |

Assuming that is invertible we can solve for in the first equation of (37) to obtain

| (38) |

The second equation of (37) then gives

| (39) |

The expression in the parentheses is called the Schur complement of in and is denoted by :

| (40) |

For a positive semidefinite matrix we may generalize the definition to

| (41) |

where is the Moore-Penrose inverse of (again, see [4] and [5]). Note that the choice of generalized inverse does not matter here since . Emilie Haynsworth introduced the name and showed that the Schur complement possesses many interesting properties [6] (see [7] for a detailed exposition). In [8] Issai Schur showed that for a positive definite the determinant of satisfies

| (42) |

We now want to show that this equality also holds for the generalized determinant. Again, we focus our attention on where is positive definite. Using the notation from the previous section we obtain:

| (43) | ||||

| (44) | ||||

| (45) |

We need to convince ourselves that the last determinant is equal to . To check this, we need to show that

| (46) | ||||

| (47) |

We already know that . To show equality let . This thus satisfies equation (39) that was obtained through Gaussian elimination. We define according to equation (38):

| (48) |

It then follows that

| (49) |

Since is of maximal rank this implies that . In particular, we have . We thus obtain our second result:

Proposition 4.2.

Let a Hermitian be positive semidefinite and partitioned as in equation (7). If is of maximal rank then

| (50) |

4.3 The inverse

The last result concerns the inverse of . When is positive definite its inverse can be written as

| (51) |

This is a remarkable formula because to find the inverse of we just need to invert and . This formula was first established by Banachiewicz [9] (see also [10, p.112]). We now want to adapt this formula to our situation where might be singular but is of maximal rank.

Again, we start by looking at the restriction of to its range . is positive definite and we can express its inverse in the form of equation (51). In the last section we established that the ranges and nullspaces of and coincide so that by replacing the inverses in equation (51) with Moore-Penrose inverses we obtain the unique Moore-Penrose inverse of .

Proposition 4.3.

Let a Hermitian be positive semidefinite and partitioned as in equation (7). If is of maximal rank then its Moore-Penrose inverse is given by

| (52) |

This result can also be deduced from [11, Theorem 4.6].

5 Matrix completion

Let be a Hermitian matrix in that is partitioned as follows:

| (53) |

As in the introduction we use the notation from [5] to denote submatrices of . For let

| (54) |

be the submatrix of with row and column indices in . For we let

| (55) |

be the submatrix with row indices in and column indices in . Now let and be such that

| (56) |

and

| (57) |

For we then have

| (58) |

and for the matrix in the upper right corner we have

| (59) |

We now want to know under what conditions we can choose so that the matrix is positive semidefinite. Before we state the result we note this helpful theorem:

Theorem 5.1.

Let be Hermitian and partitioned as in equation (7). Then these two statements are equivalent:

-

1.

is positive semidefinite.

-

2.

and are positive semidefinite, and .

A proof of this result can be found in [12]. We now have:

Theorem 5.2.

Let be partitioned as in (53) and let and be positive semidefinite. Setting

| (60) | ||||

| (61) |

turns into a positive semidefinite matrix.

Proof.

We apply theorem 5.1 to the positive semidefinite matrices and to obtain:

| (62) | ||||

| (63) | ||||

| (64) | ||||

| (65) | ||||

| (66) |

The Schur complement is given by

| (67) |

If we choose

| (68) |

and also recognize the expressions for and we find

| (69) |

Because of equations (63) and (64) we have

| (70) |

Equations (65) and (66) then ensure that

| (71) |

Since we also have we can use the theorem 5.1 one more time, this time in the other direction, to obtain

| (72) |

This completes the proof. ∎

This result appeared already in [2]. We have provided a different proof that makes use of theorem 5.1.

It turns out that the choice of in theorem 5.2 gives unique properties. It is in these characterizations of that we go beyond the results in [2] because we include the case in which is singular. The first result characterizes as the unique extension of that maximizes the determinant of . If is nonsingular we can just talk about the regular determinant of . If is singular we have to use the generalized determinant that we introduced in section 3.

Theorem 5.3.

Let be partitioned as in (53) and let and be positive semidefinite and of maximal rank. The choice

| (73) |

is the unique choice for for which is positive semidefinite, of maximal rank, and for which the (generalized) determinant is maximal.

Proof.

We have shown in the last theorem that is positive semidefinite if we set . is also of maximal rank. In general we have

| (74) |

For a positive semidefinite matrix rank is additive over the Schur complement (see [11]) so that we actually have equality:

| (75) | ||||

| (76) | ||||

| (77) |

To establish the last equality we have used the assumption that both and are of maximal rank. Thus turns into a matrix of maximal rank. We now want to show that it is the only such choice that also maximizes the determinant.

Let us now assume that is positive semidefinite and of maximal rank so that we can make use of propositions 4.1 and 4.2. Because of proposition 4.2 we have

| (78) |

Because of proposition 4.1 we have

| (79) |

with equality if and only if

| (80) |

It follows that this is the unique choice that maximizes the determinant of . ∎

For a nonsingular matrix we can use the determinant to find the inverse of (see [5]):

| (81) |

Since was chosen such that the determinant is maximal the derivative in equation (81) vanishes for indices and that denote elements of itself. It follows that has zeroes in those places where the matrix sits in . It turns out that this uniquely determines even if is only positive semidefinite and we have to talk about the Moore-Penrose inverse of instead.

Theorem 5.4.

Let be partitioned as in (53) and let and be positive semidefinite and of maximal rank. The choice

| (82) |

is the unique choice for for which is of maximal rank and for which has zeroes in those places where sits in .

Proof.

Because is of maximal rank we can use proposition 4.3 to express the Moore-Penrose inverse of in terms of and . If is to have zeroes where is in then we must have

| (83) |

which can only be the case if . ∎

For completeness we give the Moore-Penrose inverse for :

| (84) |

with

| (85) |

6 Conclusion

The problem of how to complete partial Hermitian matrices arises frequently in practical applications (see [13] for an example from finance). This problem was solved in [1] for partial matrices whose corresponding graph is chordal. The procedure provided in [1] was improved upon in [2] by giving a way to calculate whole blocks of the completion at once. For positive definite matrices the resulting completion is singled out by two uniqueness results. It is the unique matrix that maximizes the determinant, and it is the unique matrix whose inverse has zeroes in those places that were unspecified in the original matrix. In this paper we have extended these uniqueness results to include semidefinite matrices. To make this extension possible we needed to introduce a generalized determinant that gives the determinant of the nontrivial part of a Hermitian matrix. We also needed to focus on matrices whose rank is determined solely by the rank of its diagonal matrices. For these matrices the same uniqueness results hold that hold for positive definite matrices.

Acknowledgement

I would like to thank Patrick Büchel for his support during the creation of this work as well as Horst Köhler and Thomas Streuer for their initial push to look into maximal determinant completions of matrices, and for their support during the creation of this work.

References

- [1] R. Grone, C. R. Johnson, E. Sa, H. Wolkowicz, Positive definite completions of partial Hermitian matrices, Linear Algebra Appl. 58 (1984) 109–124. https://doi.org/10.1016/0024-3795(84)90207-6.

- [2] R. L. Smith, The positive definite completion problem revisited, Linear Algebra Appl. 429 (2008) 1442–1452. https://dx.doi.org/10.1016/j.laa.2008.04.020

- [3] M.C. Golumbic, W. Rheinboldt, Algorithmic Graph Theory and Perfect Graphs, 1st edition, Elsevier Inc, Academic Press, 1980.

- [4] R. Penrose, A generalized inverse for matrices, Math Proc Cambridge 51 (1955) 406–413. https://doi.org/10.1017/s0305004100030401.

- [5] R. A. Horn, C. R. Johnson, Matrix Analysis, 2nd ed., Cambridge University Press, 2012.

- [6] E. V. Haynsworth, Determination of the inertia of a partitioned Hermitian matrix, Linear Algebra Appl. 1 (1968) 73–81.

- [7] R. A. Horn, Basic Properties of the Schur Complement. In Fuzhen Zhang (Ed.), The Schur complement and its application (17–46), Springer, 2005.

- [8] J. Schur, Über Potenzreihen, die im Innern des Einheitskreises beschränkt sind, Journal für die reine und angewandte Mathematik 147 (1917) 205 – 232.

- [9] T. Banachiewicz, Zur Berechnung der Determinanten, wie auch der Inversen, und zur darauf basierten Auflösung der Systeme linearer Gleichungen, Acta Astronom. Sér. C 3 (1937) 41–67.

- [10] R. Frazer, W. Duncan, A. Collar, Elementary Matrices And Some Applications To Dynamics And Differential Equations, Cambridge University Press, 1938.

- [11] D. Ouellette, Schur complements and statistics Linear Algebra Appl. 36 (1981) 187–295. https://dx.doi.org/10.1016/0024-3795(81)90232-9.

- [12] A. Albert, Conditions for Positive and Nonnegative Definiteness in Terms of Pseudoinverses, SIAM Journal on Applied Mathematics 17 (1969) 434–440. https://dx.doi.org/10.1137/0117041

- [13] O. Dreyer, H. Köhler, T. Streuer, Completing correlation matrices, arXiv:2111.12640