Lin, Zhou, Ba and Zhang

\RUNTITLEDoubly Optimal No-Regret Online Learning with Bandit Feedback

\TITLEDoubly Optimal No-Regret Online Learning

in Strongly Monotone Games with Bandit Feedback

Tianyi Lin \AFFDepartment of Electrical Engineering and Computer Science, UC Berkeley, \EMAILdarren_lin@berkeley.edu \AUTHORZhengyuan Zhou \AFFStern School of Business, New York University, \EMAILzzhou@stern.nyu.edu \AUTHORWenjia Ba \AFFStanford Graduate School of Business, Stanford University, \EMAILwenjiaba@stanford.edu \AUTHORJiawei Zhang \AFFStern School of Business, New York University, \EMAILjzhang@stern.nyu.edu

We consider online no-regret learning in unknown games with bandit feedback, where each player can only observe its reward at each time – determined by all players’ current joint action – rather than its gradient. We focus on the class of smooth and strongly monotone games and study optimal no-regret learning therein. Leveraging self-concordant barrier functions, we first construct a new bandit learning algorithm and show that it achieves the single-agent optimal regret of under smooth and strongly concave reward functions ( is the problem dimension). We then show that if each player applies this no-regret learning algorithm in strongly monotone games, the joint action converges in the last iterate to the unique Nash equilibrium at a rate of . Prior to our work, the best-known convergence rate in the same class of games is (achieved by a different algorithm), thus leaving open the problem of optimal no-regret learning algorithms (since the known lower bound is ). Our results thus settle this open problem and contribute to the broad landscape of bandit game-theoretical learning by identifying the first doubly optimal bandit learning algorithm, in that it achieves (up to log factors) both optimal regret in the single-agent learning and optimal last-iterate convergence rate in the multi-agent learning. We also present results on several application studies – Cournot competition, Kelly auctions, and distributed regularized logistic regression – to demonstrate the efficacy of our algorithm.

no-regret learning; bandit feedback model; strongly monotone games; optimal regret; optimal last-iterate convergence rate; mirror descent

1 Introduction

In multi-agent online learning (Cesa-Bianchi and Lugosi 2006, Shoham and Leyton-Brown 2008, Busoniu et al. 2010), a set of players are repeatedly making decisions and accumulating rewards over time, where each player’s action impacts not only its own reward, but that of the others. However, the mechanism of this interaction – the underlying game that specifies how a player’s reward depends on the joint action of all – is unknown to players, and players may not even be aware that there is such a game. As such, from each player’s own perspective, it is simply engaged in an online decision-making process, where the environment consists of all other players who are simultaneously making such sequential decisions, which are of consequence to all players.

In the past two decades, the above problem has actively engaged researchers from two fields: machine learning (and online learning in particular), which aims to develop single-agent online learning algorithms that are no-regret in an arbitrarily time-varying and/or adversarial environment (Blum 1998, Shalev-Shwartz 2012, Arora et al. 2012, Hazan 2016); and game theory, which aims to develop (ideally distributed) algorithms (see Fudenberg and Levine (1998) and references therein) that efficiently compute a Nash equilibrium (a joint optimal outcome where no one can do better by deviating unilaterally) for games with special structures11endnote: 1Computing a Nash equilibrium is in general computationally intractable: the problem is indeed PPAD-complete (Daskalakis et al. 2009, Chen et al. 2009)). Although these two research threads initially developed separately, they have subsequently merged and formed the core of multi-agent/game-theoretical online learning, whose main research agenda can be phrased as follows: Will joint no-regret learning lead to a Nash equilibrium, thereby reaping both the transient benefits (conferred by low finite-time regret) and the long-run benefits (conferred by Nash equilibria)?

More specifically, through the online learning lens, the player’s reward function at – viewed as a function solely of its own action – is , and it needs to select an action before – or other feedback associated with it – is revealed. In this context, no-regret algorithms ensure that the difference between the cumulative performance of the best fixed action and that of the learning algorithm, a widely adopted metric known as regret (), grows sublinearly in . This problem has been extensively studied; in particular, when gradient feedback is available – can be observed after is selected – the minimax optimal regret is for concave and for strongly concave . Further, several algorithms have been developed that achieve these optimal regret bounds, including follow-the-regularized-leader (FTRL) (Kalai and Vempala 2005), online gradient descent (OGD) (Zinkevich 2003), multiplicative/exponential weights (MW) (Arora et al. 2012) and online mirror descent (OMD) (Shalev-Shwartz and Singer 2006). As these algorithms provide optimal regret bounds and hence naturally raise high expectations in terms of performance guarantees, a recent line of work has investigated when all players apply a no-regret learning algorithm, what the evolution of the joint action would be, and in particular, whether the joint action would converge in last iterate to a Nash equilibrium (if one exists).

These questions turn out to be difficult and had remained open until a few years ago, mainly because the traditional Nash-seeking algorithms in the economics literature are mostly either not no-regret or only exhibit convergence in time-average (ergodic convergence), or both. Despite the challenging landscape, in the past five years, affirmative answers have emerged from a fruitful line of work and new analysis tools developed therein, first on the qualitative last-iterate convergence (Balandat et al. 2016, Zhou et al. 2017a, b, 2018, Mertikopoulos et al. 2019, Mertikopoulos and Zhou 2019) in different classes of continuous games (such as the variationally stable games), and then on the quantitative last-iterate convergence rates in more specially structured games such as routing games (Krichene et al. 2015), co-coercive games (Lin et al. 2020), highly smooth games (Golowich et al. 2020a) and strongly monotone games (Zhou et al. 2021). These foundations have been inspirational to machine learning researchers in recent years, where zero-sum games have found applications, e.g., generative adversarial networks (GANs) (Goodfellow et al. 2014); indeed, there is the strand of literature on the quantitative last-iterate convergence rates in specially structured zero-sum games, including zero-sum games (Liang and Stokes 2019, Hsieh et al. 2019, Golowich et al. 2020b, Wei et al. 2021b), infinite-horizon discounted two-player zero-sum Markov games (Wei et al. 2021a) and zero-sum extensive-form games with perfect recalls (Lee et al. 2021). Among these works, Zhou et al. (2021) has recently shown that if each player applies a version of online gradient descent, then the expectation of squared Euclidean distance between the joint action in the last iterate and the unique Nash equilibrium in a strongly monotone game converges to 0 at an optimal rate of when the gradient feedback is not necessarily perfect.

Despite this remarkably pioneering line of work, which has elegantly bridged no-regret learning with convergence to Nash in continuous games and thus renewed the excitement of game-theoretical learning, a gap still exists and limits its practical usage in many real-world application problems. Specifically, in the multi-agent learning setting, a player is rarely able to observe gradient feedback. Instead, in most cases, only bandit feedback is available: each player observes only its own reward after choosing an action each time (rather than the gradient at the chosen action). For instance, in Cournot competition, each firm only observes the resulting market price, but not other firms production levels and hence can only recover its own profit (rather than its profit gradient); in Kelly auctions, each bidder can only observe the share of the resources it wins from the exchange, rather than other bidders’ bids, and hence can only compute its own gain; in pricing, each retailer only observes its own revenue, without the knowledge of other retailers’ revenue. This consideration of practical feasible algorithms then brings us to a more challenging and less explored desideratum: if each player applies a no-regret bandit learning algorithm, would the joint action still converge to the Nash equilibrium? At what rate and in what class of games?

1.1 Related Work

To appreciate the difficulty and the broad scope of this research agenda, we start by describing the existing related literature. First of all, we note that single-agent bandit learning algorithms – and their theoretical regret characterizations – are not as well-developed as their gradient counterparts. More specifically, Kleinberg (2004) and Flaxman et al. (2005) provided the first bandit learning algorithm (with continuous action) – known as FKM – that achieved the regret bound of for Lipschitz and concave reward functions. However, it was unclear whether is optimal. Subsequently, Saha and Tewari (2011) developed a barrier-based bandit learning algorithm and established a regret bound for smooth and concave reward functions, a result that has further been improved to (Dekel et al. 2015) via a variant on the algorithm and new analysis. More recently, progress has been made on developing bandit learning algorithms that achieve minimax-optimal regret. In particular, Bubeck et al. (2015) and Bubeck and Eldan (2016) provided the elegant non-constructive arguments showing that the minimax regret bound of (only considering the dependence on ) in one and high dimensions are achievable respectively, without providing any algorithm. Later, Bubeck et al. (2017) developed a kernel method based bandit learning algorithm which attains the regret bound of . Independently, Hazan and Li (2016) developed an ellipsoid method based bandit learning algorithm that also achieves the regret bound of .

For strongly concave reward functions, Agarwal et al. (2010) showed that the FKM algorithm achieves an improved regret bound of . For smooth and strongly concave reward functions, Hazan and Levy (2014) demonstrated that another variant of the barrier based bandit learning algorithm given in Saha and Tewari (2011) achieves the minimax-optimal regret of that matches the lower bound of derived in Shamir (2013) up to log factors. For an overview of the relevant theory and applications, we refer to the recent surveys (Bubeck and Cesa-Bianchi 2012, Lattimore and Szepesvári 2020) and references therein.

However, much remains unknown in understanding the convergence of these no-regret bandit learning algorithms to Nash equilibria. Bervoets et al. (2020) developed a specialized distributed reward-based algorithm that asymptotically converges to the unique Nash equilibrium in the class of strictly monotone games. However, the algorithm is not known to be no-regret and no rate is given. Héliou et al. (2020) considered a variant of the FKM algorithm and showed that it is no regret even under delays; further, provided the delays are not too large, the induced joint action would converge to the unique Nash equilibrium in the strictly monotone games (again without rates). At this writing, the most relevant and the-state-of-the-art result on this topic is presented in Bravo et al. (2018): if each player applies the FKM algorithm in strongly monotone games, then the last-iterate convergence to a unique Nash equilibrium is guaranteed at a rate of . Per Bravo et al. (2018), the analysis itself is unlikely to be improved to yield any tighter rate. However, a sizable gap still exists between this bound and the best known lower bound given in Shamir (2013), which established that in optimization problems with smooth and strongly concave objectives (which is a one-player Nash-seeking problem), no algorithm that uses only bandit feedback (i.e. zeroth-order oracle) can compute the unique optimal solution at a rate faster than . Consequently, it remains unknown as to whether other algorithms can improve the rate of as well as what the true optimal convergence rate is. In particular, since the lower bound of is established for the special case of optimization problems, it is plausible that in the multi-agent setting – where a natural potential function in optimization does not exist – the problem is inherently more difficult, and hence the convergence might be intrinsically slower. Further, note that the lower bound in Shamir (2013) is established against the class of all bandit learning algorithms, not necessarily no-regret; essentially, a priori, that could mean a larger lower bound when the algorithms are further restricted to be no-regret. As such, it has been a challenging open problem to close the gap.

1.2 Our Contributions

We tackle the problem of no-regret learning in strongly monotone games with bandit feedback and settle the above open problem by establishing that the convergence rate of – and hence minimax optimal (up to log factors) – is achievable. More specifically, we start by studying (in Section 2) single-agent learning with bandit feedback – in particular with smooth and strongly concave reward functions – and develop a mirror descent variant of the barrier-based family of bandit learning algorithms. We establish that the algorithm achieves the minimax optimal regret bound of where is the problem dimension. As such, our algorithm outperforms the FKM algorithm for the same setting in terms of regret22endnote: 2 Agarwal et al. (2010) also showed that the FKM algorithm achieves a regret bound of but for the special setting where the action set . In general, the regret bound is as mentioned before..

Extending to multi-agent learning in strongly monotone games, we show that if all players employ this optimal no-regret learning algorithm (see Algorithm 2), the joint action converges in the last iterate to the unique Nash equilibrium at a rate of . As such, we provide the first bandit learning algorithm (with continuous action) that is doubly optimal (up to log factors): it achieves optimal regret in single-agent settings under smooth and strongly concave reward functions and optimal convergence rate to Nash in multi-agent settings under smooth and strongly monotone games.

We also provide the numerical results on Cournot competition, Kelly auction, and two-player zero-sum game in Section 4, and that on distributed regularized logistic regression in the Appendix. These results demonstrate that our algorithm outperforms the multi-agent FKM algorithm.

2 Single-Agent Learning with Bandit Feedback

In this section, we provide a simple single-agent bandit learning algorithm that one player could employ to increase her individual reward in an online manner and prove that the algorithm achieves the near-optimal regret minimization property for bandit strongly concave optimization33endnote: 3This setting is the same as bandit convex optimization in the literature and we consider maximizing concave reward functions instead of minimizing convex loss functions..

In our setting, an adversary first chooses a sequence of -strongly concave reward functions , (formally, for all ), where is a closed, convex and compact set. At each round , a (possibly randomized44endnote: 4Randomization plays an important role in the online learning literature. For example, the follow-the-leader (FTL) algorithm does not attain any non-trivial regret guarantee for linear reward functions (in the worst case it can be if the reward functions are chosen in an adversarial manner). However, Hannan (1957) proposed a randomized variant of FTL, called follow-the-perturbed-leader (FTPL), which could attain an optimal regret of for linear reward functions over the simplex set.) decision maker has to choose a point and it will incur a reward of after committing to her decision. Her expected reward (where the expectation is taken with respect to her random choice) is and the corresponding notion of regret is defined by . In such bandit setting, it is worth mentioning that the feedback is limited to the value of reward function at the point that she has chosen, i.e., .

In what follows, we present the individual components used in our algorithm and then summarize the full scheme in Algorithm 1 and the regret minimization property in Theorem 2.10.

2.1 Self-Concordant Barrier Function

Most of the existing bandit learning algorithms are developed as the variants of online mirror descent framework (Cesa-Bianchi and Lugosi 2006) and the common choice of regularization is based on the self-concordant barrier function. Note that this is a key ingredient in regret-optimal bandit algorithms when the reward function is either linear (Abernethy et al. 2008) or smooth and strongly concave (Hazan and Levy 2014). For the sake of completeness, we provide a brief overview of self-concordant barrier functions and refer to Nesterov and Nemirovski (1994) for more details.

Definition 2.1

A function is a -self concordant barrier for a closed convex set , where is an interior of , if (i) is three times continuously differentiable; (ii) if , where is a boundary of ; (iii) for and , we have and where .

Resembling the existing bandit learning algorithms (Abernethy et al. 2008, Saha and Tewari 2011, Hazan and Levy 2014, Dekel et al. 2015), our algorithm requires a -self-concordant barrier function for the set . However, this does not weaken the applicability of our algorithm; indeed, it is well known that any convex and compact set in admits a non-degenerate -self-concordant barrier function with (Nesterov and Nemirovski 1994), and such barrier can be efficiently represented and evaluated for numerous choices of in real application problems. For example, the function is a -self-concordant barrier function for the set and there exist computationally tractable -self-concordant barrier functions for a -dimensional simplex. For a -dimensional ball, the function is a -self-concordant barrier function.

The above definition is only given for the sake of completeness and our analysis relies on some useful facts about self-concordant barrier functions. In particular, the Hessian of a self-concordant barrier function can induce a local norm for any given point ; that is, and for all . It is clear that the non-degeneracy of guarantees that both and are well defined.

The first important notion is the so-called Dikin ellipsoid: , which is defined at any . The following lemma summarizes some nontrivial facts (see Nesterov and Nemirovski (1994, Theorem 2.1.1) for a proof):

Lemma 2.2

Let be the Dikin ellipsoid at any , the following statements hold true:

-

1.

for every ;

-

2.

For , we have .

Remark 2.3

Further, we define the Minkowski function (Nesterov and Nemirovski 1994, Page 34) on (which is parametrized by a point ) as . Accordingly, the scaled version of is given by

A point is a “center” of satisfying that where is a -self-concordant barrier function for . The following lemma shows that is rather flat around the points that are far from the boundary (see Nesterov and Nemirovski (1994, Proposition 2.3.2 and 2.3.3)):

Lemma 2.4

Suppose that is a closed, convex and compact set, is a -self-concordant barrier function for and is a center. Then, we have . For any and , we have and .

Finally, we recall that the Newton decrement for a self-concordant function is defined as where and are a local norm and its dual respectively. This can be used to roughly measure how far a point is from a global optimum of . Formally, we summarize the results in the following lemma (see Nemirovski and Todd (2008) for a proof):

Lemma 2.5

For any self-concordant function and let , we have , where is the local norm given by .

2.2 Single-Shot Ellipsoidal Estimator

It was Flaxman et al. (2005) that introduced a single-shot spherical estimator in the literature and combined it with online mirror descent. In particular, let be a function, and where is a -dimensional unit sphere, a single-shot spherical estimator is defined by

| (1) |

This estimator is an unbiased prediction for the gradient of a smoothed version; that is, where where is a -dimensional unit ball. As , the bias caused by the difference between and vanishes while the variability of explodes. This manifestation of the bias-variance dilemma plays a key role in designing bandit learning algorithms and a single-shot spherical estimator is known to be suboptimal in terms of bias-variance trade-off and hence regret minimization. This gap is finally closed by using a more sophisticated single-shot ellipsoidal estimator based on the self-concordant barrier function for (Saha and Tewari 2011, Hazan and Levy 2014). Comparing to the spherical estimator in Eq. (1), they proposed to sample the direction w.r.t. an ellipsoid and give another unbiased gradient estimate of the scaled smooth version. In particular, a single-shot ellipsoidal estimator for an invertible matrix is defined by

| (2) |

The following lemma is a modification of Hazan and Levy (2014, Corollary 6 and Lemma 7).

Lemma 2.6

Suppose that is a concave function and is an invertible matrix, we define the smoothed version of with respect to by where is a -dimensional unit ball. Then, the following statements hold true:

-

1.

where is a -dimensional unit sphere.

-

2.

If is -strongly concave, we have is also -strongly concave.

-

3.

If is -Lipschitz continuous and we let be the largest eigenvalue of , we have .

Remark 2.7

We see from Lemma 2.6 that where is defined in Eq. (2) and . In our algorithm, we set using a self-concordant barrier function for and perform the shrinking sampling (Hazan and Levy 2014). This is the key to a better bias-variance trade-off than that achieved by the classical spherical estimators; see Algorithm 1 for the details.

2.3 Mirror Descent

Combining the idea of mirror descent55endnote: 5In reward maximization, we shall use mirror ascent instead of mirror descent since the player seeks to maximize her reward (as opposed to minimizing her loss). Nonetheless, we keep the original term “descent” throughout this paper because, despite the role reversal, it is the standard name associated with the method. (Nemirovski and Yudin 1983), our algorithm generates a new feasible point by taking a “mirror step” from a starting point along an “approximate gradient” direction . By abuse of notation, we let be a strictly convex distance-generating (or regularizer) function, i.e., with equality if and only if for all and all . We also assume that is continuously differentiable, i.e., is continuous. This leads to a Bregman divergence on via the relation

| (3) |

for all and , which might fail to be symmetric and/or satisfy the triangle inequality. Nevertheless, with equality if and only if , so the asymptotic convergence of to can be checked by showing that . We also assume that as , which is known as “Bregman reciprocity” (Chen and Teboulle 1993) as assumed in the literature. We continue with some basic relations connecting the Bregman divergence relative to a target point before and after a prox-map. The key ingredient is “three-point identity” which generalizes the law of cosines, and which is widely used in the literature (Beck and Teboulle 2003).

Lemma 2.8

Let be a regularizer on . For all and all , we have .

Remark 2.9

In our algorithm, we set as a self-concordant barrier function for ; indeed, the function satisfies the aforementioned Bregman reciprocity for various constraint sets, e.g., a -dimensional simplex or a -dimensional ball; see Algorithm 1 for the details.

The key notion for Bregman divergence is the induced prox-mapping given by

| (4) |

which reflects the intuition behind mirror descent. Indeed, it starts with and steps along the vector to generate a feasible point . In our algorithm, we propose to use the specific prox-mapping as follows,

| (5) |

for all and all , where is a self-concordant barrier function for . We remark that the prox-mapping in Eq. (5) explicitly incorporates the problem structure information: the first term is squared Euclidean norm with the coefficient proportional to strong concavity parameter and the second term is a Bregman divergence with respect to a self-concordant barrier function . Such proximal mapping is crucial to establish the last-iterate convergence rate for our algorithm in the multi-agent setting; see Remark 3.11. In our algorithm, we employ the recursion in which is the chosen step-size and is a single-shot ellipsoidal estimator as mentioned before.

The use of a mirror descent framework with specific prox-mapping in Eq. (5) is the main difference between our algorithm and the one developed in Hazan and Levy (2014); indeed, their algorithm is developed based on the follow-the-regularized-leader (FTRL) framework with some different prox-mappings. Note that such seemingly minor modification is crucial to last-iterate convergence analysis when we extend our algorithm (cf. Algorithm 1) to the multi-agent setting; indeed, the multi-agent mirror descent can achieve the last-iterate convergence rate (Zhou et al. 2021) but we are not aware of such results for multi-agent FTRL. In Section 3, we will explain this point in more detail from a technical point of view.

2.4 Algorithm and Regret Bound

We consider the single-agent setting in which the adversary is limited to choosing smooth and strongly concave functions and is a closed, convex and compact set. With the components presented before, we summarize the scheme of our algorithm in Algorithm 1.

To facilitate the readers, we present the detailed scheme of Hazan and Levy (2014, Algorithm 1) using our notations such that we can see the difference. More specifically, their algorithm generates the estimators using the same strategy as ours (cf. Step 4 - Step 8) but performs the following FTRL update at each iteration:

Since , the iterates generated by Hazan and Levy (2014, Algorithm 1) are different from the ones generated by our algorithm and it remains unclear if the multi-agent variant of Hazan and Levy (2014, Algorithm 1) can achieve the last-iterate convergence rate.

The following theorem shows that Algorithm 1 can achieve the regret bound of , which has matched the lower bound established in Shamir (2013).

Theorem 2.10

Suppose that the adversary is limited to choosing smooth and -strongly concave functions . Each function is Lipschitz continuous and satisfies that for all . If is fixed and the player employs Algorithm 1 with the stepsize choice of , we have

Remark 2.11

Theorem 2.10 shows that Algorithm 1 is a near-regret-optimal bandit learning algorithm when the adversary is limited to choosing smooth and strongly concave functions. Note that the regret is better than the best-known one of FKM in the same setting (Agarwal et al. 2010), demonstrating another way where our result improves upon Bravo et al. (2018) which uses FKM. Moreover, the subproblem solving in Eq. (5) might become more difficult due to the use of a self-concordant barrier function; indeed, we do not have a closed-form solution even if the subproblem is unconstrained and convex. In contrast, the standard prox-mapping can admit a closed-form solution for the suitable regularizers, e.g., the quadratic regularizer for a box set and entropy regularizer for a simplex set. This sheds light on the trade-off between the computational efficiency of subproblem solving and regret minimization. This also highlights the practical advantage of multi-agent FKM over Algorithm 1 in terms of computational time for certain application problems; see Section 4 for the details.

Lemma 2.12

Suppose that the iterate is generated by Algorithm 1 and let each function satisfy that for all and , we have

where and the sequence is assumed to be non-increasing.

3 Multi-Agent Learning with Bandit Feedback

In this section, we consider multi-agent learning with bandit feedback and characterize the behavior of the system when each player employs the multi-agent variant of Algorithm 1. We first present some basic definitions and notations, discuss a few important examples of strongly monotone games and finally provide our multi-agent mirror descent self-concordant barrier bandit learning algorithm.

3.1 Basic Definition and Notation

We focus on games played by a set of players . At each round, each player selects an action from a convex and compact subset of a finite-dimensional vector space and their reward is determined by the profile of the action of all players; subsequently, each player receives the reward, and repeats this process. We denote as the Euclidean norm (in the corresponding vector space): other norms can be easily accommodated in our framework (and different ’s can have different norms), although we will not bother with these since we do not play with (and benefit from) complicated geometries.

Definition 3.1

A smooth and concave game is a tuple , where is a set of players, is a convex and compact set of finite-dimensional vector space representing the player’s action space, and is the player’s reward function satisfying that: (i) is continuous in and concave in for all fixed ; (ii) is continuously differentiable in and the individual reward gradient is Lipschitz continuous.

A commonly used solution concept for non-cooperative games is Nash equilibrium (NE). For smooth and concave games considered in this paper, we are interested in the pure-strategy Nash equilibria. Indeed, for finite games, the mixed strategy NE is a probability distribution over the pure strategy NE. Our setting assumes continuous and convex action sets, where each action already lives in a continuum, and pursuing pure-strategy Nash equilibria is sufficient.

Definition 3.2

An action profile is called a (pure-strategy) Nash equilibrium of a game if it is resilient to unilateral deviations; that is, for all and .

It is known that every smooth and concave game admits at least one Nash equilibrium when all action sets are compact (Debreu 1952) and Nash equilibria admit a variational characterization. We summarize this result in the following proposition.

Proposition 3.3

In a smooth and concave game , the profile is a Nash equilibrium if and only if for all and .

Proposition 3.3 shows that Nash equilibria of a smooth and concave game can be characterized as the solution set of variational inequality (VI), so the existence results follow from the standard results in the VI literature (Facchinei and Pang 2007). We omit the proof details and refer to Mertikopoulos and Zhou (2019, Proposition 2) for the reference.

3.2 Strongly Monotone Games

The study of (strongly) monotone games dates to Rosen (1965), with many subsequent developments; see, e.g., Facchinei and Pang (2007). Specifically, Rosen (1965) considered a class of games that satisfy the diagonal strict concavity (DSC) condition and prove that they admit a unique Nash equilibrium. Further work in this vein appeared in Sandholm (2015) and Sorin and Wan (2016), where games that satisfy DSC are referred to as “contractive” and “dissipative”. These conditions are equivalent to strict monotonicity in the context of convex analysis (Bauschke and Combettes 2011). To avoid confusion, we provide the formal definition of strongly monotone games.

Definition 3.4

A smooth and concave game is called -strongly monotone66endnote: 6In general, we assume that and for all . if we have for any .

The notion of (strong) monotonicity, which will play a crucial role in the subsequent analysis, is not necessarily theoretically artificial but encompasses a very rich class of games. We present four typical examples which satisfy the conditions in Definition 3.4 (see Appendix 8 for proof details and the selection of and in our examples).

Example 3.5 (Cournot Competition)

In the Cournot oligopoly model, there is a finite set of firms, each supplying the market with a quantity of some good (or service) up to the firm’s production capacity, given here by a positive scalar . This good is then priced as a decreasing function of the total supply to the market, as determined by each firm’s production; for concreteness, we focus on the standard linear model where and are positive constants. In this model, the reward of the firm (considered here as a player) is given by

where denotes the marginal production cost of the firm, i.e., as the income obtained by producing units of the good in question minus the corresponding production cost. Letting denote the space of possible production values for each firm, we can show that the game is -strongly monotone with and for all . Note that and are unknown to all the players and each player only knows its own and observes the market price, from which only the bandit feedback of its reward function can be recovered.

Example 3.6 (Strongly Concave Potential Game)

A game is called a potential game (Monderer and Shapley 1996, Sandholm 2001) if there exists a potential function such that

for all , all and all . If the potential function is -strongly concave, we can show from some basic results in the context of convex analysis (Bauschke and Combettes 2011) that the game is -strongly monotone with for all .

Example 3.7 (Kelly Auctions)

Consider a service provider with a number of splittable resources (representing, e.g., bandwidth, server time, ad space on a website, etc.). These resources can be leased to a set of bidders (players) who can place monetary bids for the utilization of each resource up to each player’s total budget , i.e., . A popular and widely used mechanism to allocate resources in this case is the Kelly mechanism (Kelly et al. 1998) whereby resources are allocated proportionally to each player’s bid, i.e., the player gets

units of the resource (in the above, denotes the available units of said resource and is the “entry barrier” for bidding on it). A simple model for the reward of the player is given by

where denotes the player’s marginal gain from acquiring a unit slice of resources. If we write for the entire space of possible bids of the player on the set of resources , we can show that the game is -strongly monotone with and for all . Although and are known to all bidders, each bidder’s reward gradient is not computable: other bidders’ bids are not observable and hence only is observable. Consequently, this is a strongly monotone game with only bandit feedback available.

Example 3.8 (Retailer Pricing Games)

We start with the single-retailer multi-product pricing setting. A retailer (with unlimited inventory) sells products over a horizon and makes pricing decisions at each period in order to maximize overall revenue across all products. Those products may be substitutes or complements to each other, and consequently, each product’s price not only affects its own demand, but also that of the other products. We focus on the standard linear model , where each component gives the demand for the product under the decision . Note that if the product is a complement to the product and if the product is a substitute to the product; further, and all prices are bounded (i.e. lie in some sets ). By definition, we have . The total revenue is , which is -strongly concave in if for all , where is not necessarily symmetrical. Note that the retailer observes the realized demand at the end of period , which only gives the bandit feedback. Interestingly, in this single-setting, without any additional assumptions, applying our algorithm yields regret bound, which appears to be novel.

We also consider the multi-retailer pricing setting, and for simplicity, we focus on the single product setting. Consider the set of retailers , each selling a different product that may either be a substitute or complement to products sold by other retailers. The retailer’s action is the price for its product, which is assumed to lie in some closed interval. For the retailer, the demand for its product depends on the joint price vector of all retailers (as similar products act as substitutes and hence influence this product’s demand): . Here, if the retailer’s product is a complement to the retailer’s product and if the retailer’s product is a substitute to the retailer’s product; further, and for all . The retailer’s reward function is its revenue . Th resulting game is -strongly monotone with for all if where the matrix is not necessarily symmetrical.

Note that in both cases, a sufficient condition for strong convexity and/or strong monotonicity is when the matrix is strictly diagonally dominant. This condition has a interpretable meaning: each product’s price impact on its own demand is larger than that of all other products combined. Unless products have very little differentiation, this assumption easily holds in practice.

There are also many other application problems that can be cast into the framework of strongly monotone games (Orda et al. 1993, Cesa-Bianchi and Lugosi 2006, Sandholm 2015, Sorin and Wan 2016, Mertikopoulos et al. 2017). Typical examples include strongly-convex-strongly-concave zero-sum two-player games, congestion games (Mertikopoulos and Zhou 2019), wireless network games (Weeraddana et al. 2012, Tan 2014, Zhou et al. 2021) and a wide range of online decision-making problems (Cesa-Bianchi and Lugosi 2006). With that being said, the notion of strong monotonicity has been widely used in the literature for characterizing real application problems. To make this argument more convincing, we consider one-player strongly monotone games which are simply the strongly convex optimization problems. Notably, the strongly convex optimization problems are well motivated and include many interesting application problems arising from ML and statistics; indeed, we often impose ridge regularization in the models, and the objective functions become strongly convex. A class of online decision-making problems with strongly convex loss functions is also well motivated and well studied in the literature (see, e.g., Hazan (2016)).

From an economic point of view, one appealing feature of strongly monotone games is that the last-iterate convergence can be achieved by some learning algorithms (Zhou et al. 2021), which is more natural than the time-average-iterate convergence (Fudenberg and Levine 1998, Cesa-Bianchi and Lugosi 2006). The finite-time convergence rate is derived in terms of the distance between and , where is the realized action and is the unique Nash equilibrium (under convex and compact action sets). In view of all this (and unless explicitly stated otherwise), we will focus on strongly monotone games throughout this paper.

3.3 Algorithm

In multi-agent learning with bandit feedback, at each round , every (randomized) decision maker selects an action . The reward is realized after all decision makers have chosen their actions. In addition to regret minimization, the convergence to Nash equilibria serves as an important criterion for measuring the performance of multi-agent learning algorithms. In multi-agent bandit learning, the feedback is limited to the value of the reward function at the point that each player has chosen, i.e., .

We propose a simple multi-agent bandit learning algorithm where each player chooses her action using Algorithm 1. In other words, it is a straightforward extension of Algorithm 1 from single-agent setting to multi-agent setting. Notably, our new algorithm differs from multi-agent FKM (cf. Bravo et al. (2018, Algorithm 1)) in two aspects: ellipsoidal SPSA estimator v.s. spherical SPSA estimator and self-concordant Bregman divergence v.s. standard Bregman divergence. We discuss these two crucial components before summarizing the scheme of our multi-agent bandit learning algorithm.

Single-shot ellipsoidal SPSA estimator.

Bravo et al. (2018) have recently extended the spherical estimator in Eq. (1) from single-agent setting to multi-agent setting; indeed, their approach posits that all the players use a simultaneous perturbation stochastic approximation (SPSA) approach (Spall 1997) to estimate their individual reward gradients based off a single reward function evaluation. More specifically, let be a reward function, and the query directions be drawn independently across players where is a -dimensional unit sphere, a single-shot spherical SPSA estimator is defined by

| (6) |

This estimator is an unbiased prediction for a partial gradient of a smoothed version of ; indeed, we have where where is a -dimensional unit ball. We can easily see the bias-variance dilemma here: as , becomes more accurate since , while the variability of grows unbounded since the second moment of grows as . By carefully choosing , Bravo et al. (2018) provided the best-known last-iterate convergence rate of which almost matches the lower bound established in Shamir (2013). However, a gap still remains and they believe it can be closed by using a more sophisticated single-shot estimator.

We now provide a single-shot ellipsoidal SPSA estimator by extending the estimator in Eq. (2) to multi-agent setting. More specifically, we let and define

| (7) |

The following lemma summarizes some results for the estimator in Eq. (7) and we provide the detailed proof in Appendix 9 for the sake of completeness.

Lemma 3.9

Suppose that is a concave function and is an invertible matrix for each , we define the smoothed version of with respect to by where is a -dimensional unit sphere, is a -dimensional unit ball and for all . Then, the following statements hold true:

-

1.

.

-

2.

If is -Lipschitz continuous and we let be the largest eigenvalue of , we have .

Mirror descent.

The standard prox-mapping in Eq. (4) has been used in Bravo et al. (2018) to construct their multi-agent bandit learning algorithm, which achieves the suboptimal regret minimization and last-iterate convergence. In contrast, our multi-agent bandit learning algorithm updates using the specific prox-mapping in Eq. (5) and the rule is given by

| (8) |

for all and all , where is a self-concordant barrier function for . In our algorithm, we employ the recursion in which is the chosen step-size and is a single-shot ellipsoidal SPSA estimator as mentioned before.

Remark 3.11

The use of mirror descent framework with specific prox-mapping in Eq. (8) is crucial to last-iterate convergence analysis in the next subsection. Roughly speaking, it allows us to directly bound the term and leads to a near-optimal last-iterate convergence rate. Moreover, we can see from the proof of Theorem 3.12 that the time-dependent coefficient of quadratic term in Eq. (8) plays a key role in bounding by . This is consistent with the fact that only multi-agent mirror descent is proven to achieve last-iterate convergence rate in strongly monotone games (Zhou et al. 2021) while no such results hold for multi-agent FTRL.

3.4 Finite-Time Last-Iterate Convergence Rate

We consider the multi-agent setting in a strongly monotone game in which each player’s reward function satisfies that for all and is a closed, convex and compact set. With the components presented before, we summarize the scheme of our algorithm in Algorithm 2.

The following theorem shows that Algorithm 2 can achieve the last-iterate convergence to a unique Nash equilibrium at a rate of . This has improved the rate of achieved by multi-agent FKM (Bravo et al. 2018) and matched the lower bound established in Shamir (2013).

Theorem 3.12

Suppose that is a unique Nash equilibrium of a smooth and -strongly monotone game. Each function satisfies that for all . If is fixed and each player employs Algorithm 2 with the stepsize choice of , we have

Remark 3.13

Theorem 3.12 shows that Algorithm 2 attains a near-optimal rate of last-iterate convergence in a smooth and strongly monotone game. It provides the first doubly optimal bandit learning algorithm, in that it achieves (up to log factors) both optimal regret in a single-agent setting and optimal last-iterate convergence rate in a multi-agent setting. In contrast, it remains unclear if the multi-agent FTRL (Hazan and Levy 2014) can achieve the last-iterate convergence rate.

Lemma 3.14

Suppose that the iterate is generated by Algorithm 2 and let each function satisfy that for all and , we have

where and the sequence is assumed to be non-increasing.

See the proofs of Lemma 3.14 and Theorem 3.12 in Appendix 10 and 11. We also provide the last-iterate convergence rate results under the imperfect bandit feedback in Appendix 12.

Remark 3.15

As we have mentioned before, one appealing feature of strongly monotone games is that the finite-time convergence rate can be derived in terms of (Zhou et al. 2021) (under convex and compact action sets). On the other hand, possibly converges to a limit cycle or repeatedly hit the boundary in monotone games (Daskalakis et al. 2018, Mertikopoulos et al. 2018) despite the time-average iterate converges. More recently, Cai et al. (2022) and Gorbunov et al. (2022) analyzed the optimistic gradient method (which is a no-regret learning algorithm) in monotone games (under convex and compact action sets) and proved that last-iterate convergence to Nash equilibria at an optimal rate of in terms of a gap function. However, there are no last-iterate convergence rates in terms of available for monotone games, and it seems impossible to attain such a rate without the quadratic growth of strong monotonicity. Moreover, analyzing the last-iterate convergence rate of no-regret bandit learning algorithms is completely out of reach of the existing techniques of Cai et al. (2022) and Gorbunov et al. (2022). Can we propose the no-regret bandit learning algorithms to handle monotone games and prove the last-iterate convergence rate in terms of a gap function? We leave the answers to future work.

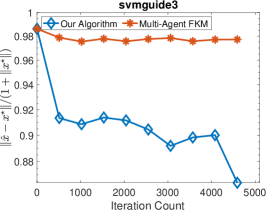

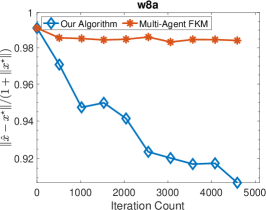

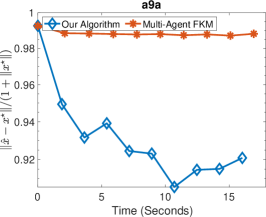

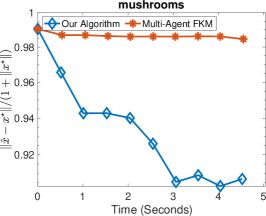

4 Numerical Experiments

In this section, we conduct the experiments using various tasks: Cournot competition, Kelly auction, strongly-convex-strongly-concave zero-sum game and strongly monotone potential game (appendix). The baseline approach is multi-agent FKM (cf. Bravo et al. (2018, Algorithm 1)) and the platform is MATLAB R2021b on a MacBook Pro with an Intel Core i9 2.4GHz and 16GB memory.

4.1 Cournot Competition

We fix for all and evaluate the algorithms by varying , and . For each , we draw independently from an uniform distribution on the interval . The game is -strongly monotone with and for all .

For both Algorithm 2 and multi-agent FKM, we consider the theoretically-correct choices of step sizes without fine-tuning. Indeed, we set for all and for Algorithm 2 due to the structure of Cournot competition. Since , we set . Also, we set which is chosen according to Theorem 3.12 that suggests . For all , we set in multi-agent FKM. We also set and according to a theoretically-correct choice from Bravo et al. (2018, Theorem 5.2). Moreover, it is well known that the Cournot competition in Example 3.5 is a strongly concave potential game and can be solved by minimizing a quadratic function as follows.

| (9) |

The evaluation metric is where is generated by the algorithms and is an approximate Nash equilibrium with high accuracy (we employ quadprog in Matlab for minimizing in Eq. (9)). This point is a benchmark for evaluating the quality of the solution obtained by the algorithms.

| Multi-Agent FKM | Our Algorithm | |

|---|---|---|

| (10, 10, 0.05) | 2.2e-01 4.4e-02 | 1.2e-01 9.2e-02 |

| (10, 10, 0.10) | 1.3e-01 3.9e-02 | 8.6e-02 5.8e-02 |

| (10, 20, 0.05) | 3.3e-01 6.5e-02 | 4.1e-01 8.4e-02 |

| (10, 20, 0.10) | 1.9e-01 3.5e-02 | 3.7e-01 1.2e-01 |

| (20, 10, 0.05) | 2.3e-01 3.4e-02 | 9.0e-02 5.1e-02 |

| (20, 10, 0.10) | 1.3e-01 1.8e-02 | 7.3e-02 4.1e-02 |

| (20, 20, 0.05) | 3.5e-01 3.0e-02 | 4.1e-01 5.9e-02 |

| (20, 20, 0.10) | 2.2e-01 3.9e-02 | 4.2e-01 8.1e-02 |

| (50, 10, 0.05) | 2.1e-01 2.4e-02 | 6.7e-02 2.4e-02 |

| (50, 10, 0.10) | 9.9e-02 2.1e-02 | 5.0e-02 6.0e-03 |

| (50, 20, 0.05) | 3.5e-01 2.4e-02 | 4.6e-01 5.1e-02 |

| (50, 20, 0.10) | 2.2e-01 1.5e-02 | 4.1e-01 5.8e-02 |

| (100, 10, 0.05) | 1.8e-01 1.5e-02 | 5.9e-02 2.3e-02 |

| (100, 10, 0.10) | 2.2e-02 2.0e-03 | 1.1e-01 1.1e-02 |

| (100, 20, 0.05) | 3.5e-01 2.0e-02 | 4.0e-01 3.3e-02 |

| (100, 20, 0.10) | 1.9e-01 1.6e-02 | 4.0e-01 3.3e-02 |

Experimental results.

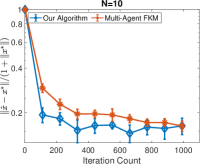

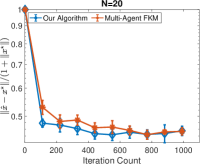

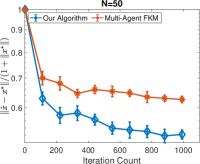

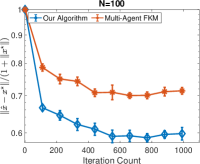

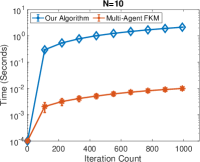

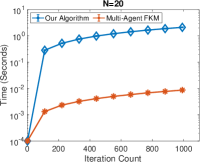

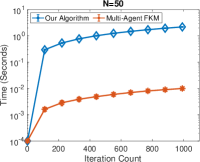

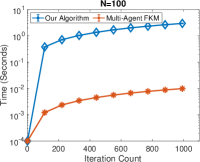

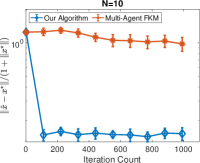

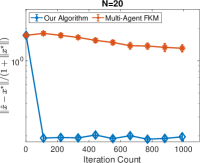

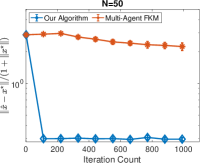

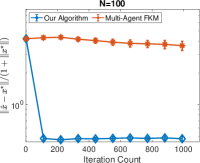

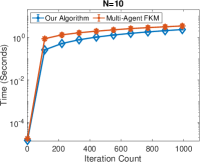

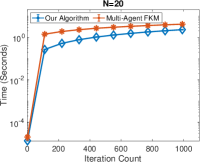

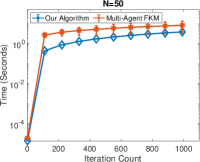

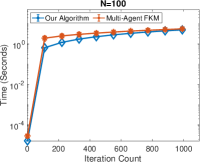

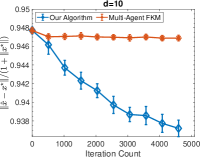

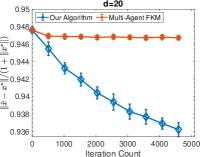

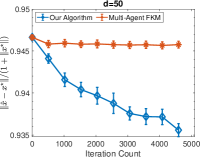

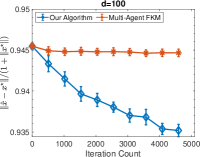

Fixing , we investigate the convergence behavior of both algorithms with a varying number of players, i.e., . Figure 1 indicates that our algorithm outperforms multi-agent FKM as it returns the iterates that are closer to a unique Nash equilibrium in fewer iteration counts. It also shows that the subproblem solving in our algorithm requires much more time; indeed, each subproblem in multi-agent FKM is simply the orthogonal projection onto a box constraint and thus admits a closed-form solution, while each subproblem in our algorithm is an unconstrained convex optimization problem that needs to be solved inexactly. This demonstrates the trade-off between the computational efficiency of subproblem solving and the last-iterate convergence rate. Nonetheless, our algorithm is acceptable in terms of total time and will approach a better solution. We also present the numerical results for all in Table 1.

4.2 Kelly Auction

We fix for all and evaluate the algorithms by varying , and . For each , we draw independently of a uniform distribution at the interval . For each , we draw independently from an uniform distribution on the interval and independently from an uniform distribution on the interval . The game is -strongly monotone with and for all .

For both Algorithm 2 and multi-agent FKM, we consider the theoretically-correct choices of step sizes without fine-tuning. Indeed, we set for all and for Algorithm 2 due to the structure of Cournot competition. Since , we set . Also, we set which is chosen according to Theorem 3.12 that suggests . For all , we set in multi-agent FKM. We also set and according to a theoretically-correct choice from Bravo et al. (2018, Theorem 5.2).

For both Algorithm 2 and multi-agent FKM, we consider the theoretically-correct choices of step sizes without fine-tuning. Indeed, we set for all and for Algorithm 2 due to the structure of Kelly auction. Since where is a vector of dimensional with all one, we set . Also, we set for and for , which is chosen according to Theorem 3.12 which suggests . For all , we set and in multi-agent FKM. We also set and according to a theoretically-correct choice from Bravo et al. (2018, Theorem 5.2). Moreover, it is well known that the Kelly auction in Example 3.7 has a variational characterization (Mertikopoulos and Zhou 2019, Proposition 2.1) and the equilibrium computation is equivalent to finding a point such that for all . The evaluation metric is where is generated by the algorithms and is an approximate Nash equilibrium with high accuracy (we obtain it by employing the optimistic gradient method (Hsieh et al. 2019) to find an approximate solution of the VI mentioned above). This point is a benchmark for evaluating the quality of the solution obtained by the algorithms.

| Multi-Agent FKM | Our Algorithm | |

|---|---|---|

| (10, 2, 0.50) | 8.3e-01 3.0e-01 | 1.7e-01 4.7e-02 |

| (10, 2, 1.00) | 1.0e+00 2.4e-01 | 1.4e-01 2.2e-02 |

| (10, 5, 0.50) | 8.4e-01 8.8e-02 | 1.9e-01 4.7e-02 |

| (10, 5, 1.00) | 9.5e-01 1.1e-01 | 1.6e-01 4.9e-02 |

| (20, 2, 0.50) | 1.4e+00 4.3e-01 | 2.2e-01 1.9e-02 |

| (20, 2, 1.00) | 1.6e+00 3.1e-01 | 1.9e-01 3.6e-02 |

| (20, 5, 0.50) | 1.3e+00 1.2e-01 | 2.1e-01 2.5e-02 |

| (20, 5, 1.00) | 1.4e+00 1.5e-01 | 2.0e-01 3.0e-02 |

| (50, 2, 0.50) | 2.5e+00 5.7e-01 | 3.2e-01 3.3e-02 |

| (50, 2, 1.00) | 2.7e+00 4.9e-01 | 3.5e-01 2.9e-02 |

| (50, 5, 0.50) | 2.1e+00 1.8e-01 | 2.4e-01 1.9e-02 |

| (50, 5, 1.00) | 2.2e+00 9.2e-02 | 2.3e-01 1.5e-02 |

| (100, 2, 0.50) | 3.6e+00 8.4e-01 | 4.9e-01 4.8e-02 |

| (100, 2, 1.00) | 4.1e+00 7.6e-01 | 5.3e-01 6.0e-02 |

| (100, 5, 0.50) | 3.2e+00 7.6e-02 | 4.2e-01 3.8e-02 |

| (100, 5, 1.00) | 3.3e+00 7.6e-02 | 4.3e-01 2.9e-02 |

Experimental results.

Fixing , we investigate the convergence behavior of both algorithms with a varying number of players, i.e., . Figure 2 indicates that our algorithm outperforms multi-agent FKM as it returns iterates that are closer to a unique Nash equilibrium in fewer iteration counts. It also shows that the subproblem solving in our algorithm requires slightly less time than that in multi-agent FKM. This is because each constraint set in the Kelly auction is a simplex set and the subproblems in our algorithm and multi-agent FKM both need to be solved inexactly. More specifically, applying Euclidean projection is crucial to derive the last-iterate convergence rate of multi-agent FKM (see Bravo et al. (2018, Theorem 5.2)). This in fact necessaries the inexact subproblem solving in multi-agent FKM since such projection onto a simplex set does not have a closed-form solution. We exclude multi-agent FKM with entropy regularizers from our experiments, since it remains unknown whether this approach can achieve the last iterate convergence rate in terms of the distance to a unique Nash equilibrium. Compared to the numerical results in Figure 1, the quality of the solutions obtained by both algorithms is poorer. Indeed, the simplex set is more complicated than the box set assumed in the Cournot competition. Thus, the theoretically correct choices are somehow too conservative from a practical viewpoint. While multi-agent FKM gets stuck after a few iterations, our algorithm approaches Nash equilibrium slowly but steadily. We also present the numerical results for all in Table 2.

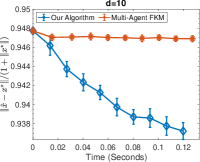

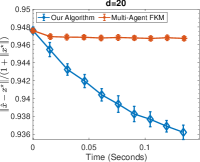

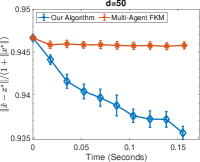

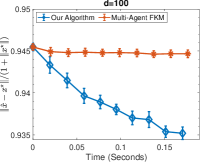

4.3 Strongly-Convex-Strongly-Concave Zero-Sum Game

We consider the strongly-convex-strongly-concave zero-sum game as follows,

| (10) |

which is the saddle point reformulation of the -regularized linear regression problem in the form of ; see Du and Hu (2019) and Mokhtari et al. (2020). The squared -norm prevents overfitting issue and balances goodness-of-fit and generalization.

We evaluate the algorithms by varying , and . Following the setup of Mokhtari et al. (2020), we generate the rows of from a Gaussian distribution and from a uniform distribution on the interval . We also set . Then, it is clear that the problem in Eq. (10) is a two-player zero-sum game where the decision variables of the first and second players are and . In other words, , , , and the corresponding model for the reward of the first and second players is given by

The game is -strongly monotone for and for all .

For both Algorithm 2 and multi-agent FKM, we consider the theoretically-correct choices of step sizes without fine-tuning. Indeed, we set for all and for Algorithm 2 due to the structure of a game as argued before. Since , we set . We also set which is chosen according to Theorem 3.12 that suggests . Moreover, for all , we set and in multi-agent FKM since . We also set and according to a theoretically-correct choice from Bravo et al. (2018, Theorem 5.2). The evaluation metric is where is generated by the algorithms and is a unique Nash equilibrium (we obtain it by solving a linear equation). This point will be a benchmark for evaluating the quality of the solution obtained by the algorithms.

| Multi-Agent FKM | Our Algorithm | |

|---|---|---|

| (1000, 50, 1.00) | 9.5e-01 8.7e-04 | 9.3e-01 1.7e-03 |

| (1000, 50, 2.00) | 9.5e-01 9.9e-04 | 9.4e-01 1.9e-03 |

| (1000, 100, 1.00) | 9.4e-01 7.1e-04 | 9.3e-01 9.5e-04 |

| (1000, 100, 2.00) | 9.4e-01 1.2e-03 | 9.3e-01 2.4e-03 |

| (1000, 200, 1.00) | 9.4e-01 7.2e-04 | 9.3e-01 1.3e-03 |

| (1000, 200, 2.00) | 9.4e-01 5.4e-04 | 9.3e-01 1.9e-03 |

| (1000, 500, 1.00) | 9.3e-01 1.8e-03 | 9.2e-01 2.8e-03 |

| (1000, 500, 2.00) | 9.3e-01 2.4e-03 | 9.2e-01 6.1e-03 |

| (5000, 50, 1.00) | 9.8e-01 1.9e-04 | 9.7e-01 3.4e-04 |

| (5000, 50, 2.00) | 9.8e-01 1.2e-04 | 9.7e-01 4.3e-04 |

| (5000, 100, 1.00) | 9.8e-01 1.9e-04 | 9.7e-01 4.1e-04 |

| (5000, 100, 2.00) | 9.8e-01 1.7e-04 | 9.7e-01 4.7e-04 |

| (5000, 200, 1.00) | 9.8e-01 1.9e-04 | 9.7e-01 4.2e-04 |

| (5000, 200, 2.00) | 9.8e-01 3.0e-04 | 9.7e-01 4.2e-04 |

| (5000, 500, 1.00) | 9.7e-01 2.4e-04 | 9.7e-01 5.5e-04 |

| (5000, 500, 2.00) | 9.7e-01 1.2e-04 | 9.7e-01 3.2e-04 |

Experimental results.

Fixing , we investigate the convergence behavior of both algorithms with a varying dimension of decision variable, i.e., . Figure 3 indicates that our algorithm slightly outperforms multi-agent FKM as it returns the iterates that are closer to a unique Nash equilibrium in fewer iteration counts and less time. Compared to the numerical results on other tasks with synthetic data, the quality of the solutions obtained by both Algorithm 2 and multi-agent FKM are much lower, which is possibly caused by very small modules of strong monotonicity, i.e., . We also present the numerical results for all in Table 3.

5 Concluding Remarks and Future Directions

In a multi-agent online environment with bandit feedback, the most sensible choice for a player who is oblivious to the presence of others (or who are conservative), is to deploy an optimal no-regret learning algorithm. With this in mind, we investigate the long-run behavior of individual optimal regularized no-regret learning policies. We show that, in strongly monotone games, the joint actions of all players converge to a (necessarily) unique Nash equilibrium, and the rate of convergence matches the lower bound established in Shamir (2013) up to log factors.

We conduct the experiments using Cournot competition, Kelly auction, strongly-convex-strongly-concave zero-sum game and strongly monotone potential game (appendix), the results demonstrate the superiority of our algorithm in practice. Our work thus settles an open problem and contributes to the broad landscape of bandit game-theoretical learning by identifying the first doubly optimal bandit learning algorithm, in that it achieves (up to log factors) both optimal regret in the single-agent learning and optimal last-iterate convergence rate in the multi-agent learning. Future works include the design of a fully decentralized bandit learning algorithm where the players’ updates need not be synchronous, the extension to the non-strongly monotone games, and the applications of our algorithms to online decision-making problems in practice.

References

- Abernethy et al. (2008) Abernethy, J., E. Hazan, A. Rakhlin. 2008. Competing in the dark: An efficient algorithm for bandit linear optimization. COLT. 263–273.

- Agarwal et al. (2010) Agarwal, A., O. Dekel, L. Xiao. 2010. Optimal algorithms for online convex optimization with multi-point bandit feedback. COLT. 28–40.

- Arora et al. (2012) Arora, S., E. Hazan, S. Kale. 2012. The multiplicative weights update method: A meta-algorithm and applications. Theory of Computing 8(1) 121–164.

- Aybat et al. (2017) Aybat, N. S., Z. Wang, T. Lin, S. Ma. 2017. Distributed linearized alternating direction method of multipliers for composite convex consensus optimization. IEEE Transactions on Automatic Control 63(1) 5–20.

- Balandat et al. (2016) Balandat, M., W. Krichene, C. Tomlin, A. Bayen. 2016. Minimizing regret on reflexive Banach spaces and Nash equilibria in continuous zero-sum games. NIPS. 154–162.

- Bauschke and Combettes (2011) Bauschke, H. H., P. L. Combettes. 2011. Convex Analysis and Monotone Operator Theory in Hilbert Spaces, vol. 408. Springer.

- Beck and Teboulle (2003) Beck, A., M. Teboulle. 2003. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters 31(3) 167–175.

- Bervoets et al. (2020) Bervoets, S., M. Bravo, M. Faure. 2020. Learning with minimal information in continuous games. Theoretical Economics 15(4) 1471–1508.

- Blum (1998) Blum, A. 1998. Online algorithms in machine learning. Online Algorithms. Springer, 306–325.

- Bottou (2010) Bottou, L. 2010. Large-scale machine learning with stochastic gradient descent. Proceedings of COMPSTAT’2010. Springer, 177–186.

- Boyd et al. (2011) Boyd, S., N. Parikh, E. Chu, B. Peleato, J. Eckstein. 2011. Distributed optimization and statistical learning via the alternating direction method of multipliers. Foundations and Trends® in Machine Learning 3(1) 1–122.

- Bravo et al. (2018) Bravo, M., D. Leslie, P. Mertikopoulos. 2018. Bandit learning in concave N-person games. NIPS. 5666–5676.

- Bubeck and Cesa-Bianchi (2012) Bubeck, S., N. Cesa-Bianchi. 2012. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Machine Learning 5(1) 1–122.

- Bubeck et al. (2015) Bubeck, S., O. Dekel, T. Koren, Y. Peres. 2015. Bandit convex optimization: sqrtt regret in one dimension. COLT. PMLR, 266–278.

- Bubeck and Eldan (2016) Bubeck, S., R. Eldan. 2016. Multi-scale exploration of convex functions and bandit convex optimization. COLT. PMLR, 583–589.

- Bubeck et al. (2017) Bubeck, S., Y. T. Lee, R. Eldan. 2017. Kernel-based methods for bandit convex optimization. SOTC. 72–85.

- Busoniu et al. (2010) Busoniu, L., R. Babuska, B. De Schutter. 2010. Multi-agent reinforcement learning: An overview. Innovations in Multi-Agent Systems and Applications-1. Springer, 183–221.

- Cai et al. (2022) Cai, Y., A. Oikonomou, W. Zheng. 2022. Tight last-iterate convergence of the extragradient method for constrained monotone variational inequalities. ArXiv Preprint: 2204.09228 .

- Cesa-Bianchi and Lugosi (2006) Cesa-Bianchi, N., G. Lugosi. 2006. Prediction, Learning, and Games. Cambridge University Press.

- Chen and Teboulle (1993) Chen, G., M. Teboulle. 1993. Convergence analysis of a proximal-like minimization algorithm using Bregman functions. SIAM Journal on Optimization 3(3) 538–543.

- Chen et al. (2009) Chen, X., X. Deng, S-H. Teng. 2009. Settling the complexity of computing two-player Nash equilibria. Journal of the ACM (JACM) 56(3) 1–57.

- Daskalakis et al. (2009) Daskalakis, C., P. W. Goldberg, C. H. Papadimitriou. 2009. The complexity of computing a Nash equilibrium. SIAM Journal on Computing 39(1) 195–259.

- Daskalakis et al. (2018) Daskalakis, C., A. Ilyas, V. Syrgkanis, H. Zeng. 2018. Training GANs with optimism. ICLR. 1–30. URL https://openreview.net/forum?id=SJJySbbAZ.

- Debreu (1952) Debreu, G. 1952. A social equilibrium existence theorem. Proceedings of the National Academy of Sciences 38(10) 886–893.

- Dekel et al. (2015) Dekel, O., R. Eldan, T. Koren. 2015. Bandit smooth convex optimization: Improving the bias-variance tradeoff. NIPS. 2926–2934.

- Du and Hu (2019) Du, S. S., W. Hu. 2019. Linear convergence of the primal-dual gradient method for convex-concave saddle point problems without strong convexity. AISTATS. PMLR, 196–205.

- Facchinei and Pang (2007) Facchinei, F., J-S. Pang. 2007. Finite-Dimensional Variational Inequalities and Complementarity Problems. Springer Science & Business Media.

- Flaxman et al. (2005) Flaxman, A. D., A. T. Kalai, H. B. McMahan. 2005. Online convex optimization in the bandit setting: gradient descent without a gradient. SODA. 385–394.

- Fudenberg and Levine (1998) Fudenberg, D., D. K. Levine. 1998. The Theory of Learning in Games, vol. 2. MIT Press.

- Golowich et al. (2020a) Golowich, N., S. Pattathil, C. Daskalakis. 2020a. Tight last-iterate convergence rates for no-regret learning in multi-player games. NeurIPS, vol. 33. 20766–20778.

- Golowich et al. (2020b) Golowich, N., S. Pattathil, C. Daskalakis, A. Ozdaglar. 2020b. Last iterate is slower than averaged iterate in smooth convex-concave saddle point problems. COLT. PMLR, 1758–1784.

- Goodfellow et al. (2014) Goodfellow, I. J., J. Pouget-Abadie, M. Mirza, B. Xu, D. Warde-Farley, S. Ozair, A. Courville, Y. Bengio. 2014. Generative adversarial nets. NeurIPS. 2672–2680.

- Gopal and Yang (2013) Gopal, S., Y. Yang. 2013. Distributed training of large-scale logistic models. ICML. PMLR, 289–297.

- Gorbunov et al. (2022) Gorbunov, E., A. Taylor, G. Gidel. 2022. Last-iterate convergence of optimistic gradient method for monotone variational inequalities. ArXiv Preprint: 2205.08446 .

- Hannan (1957) Hannan, J. 1957. Approximation to Bayes risk in repeated play. Contributions to the Theory of Games 21(39) 97–139.

- Hazan (2016) Hazan, E. 2016. Introduction to online convex optimization. Foundations and Trends® in Optimization 2(3-4) 157–325.

- Hazan and Levy (2014) Hazan, E., K. Y. Levy. 2014. Bandit convex optimization: Towards tight bounds. NIPS. 784–792.

- Hazan and Li (2016) Hazan, E., Y. Li. 2016. An optimal algorithm for bandit convex optimization. ArXiv Preprint: 1603.04350 .

- Héliou et al. (2020) Héliou, A., P. Mertikopoulos, Z. Zhou. 2020. Gradient-free online learning in continuous games with delayed rewards. ICML. PMLR, 4172–4181.

- Hsieh et al. (2019) Hsieh, Y-G., F. Iutzeler, J. Malick, P. Mertikopoulos. 2019. On the convergence of single-call stochastic extra-gradient methods. NeurIPS. 6938–6948.

- Kalai and Vempala (2005) Kalai, A., S. Vempala. 2005. Efficient algorithms for online decision problems. Journal of Computer and System Sciences 71(3) 291–307.

- Kelly et al. (1998) Kelly, F. P., A. K. Maulloo, D. K. H. Tan. 1998. Rate control for communication networks: Shadow prices, proportional fairness and stability. Journal of the Operational Research society 49(3) 237–252.

- Kleinberg (2004) Kleinberg, R. 2004. Nearly tight bounds for the continuum-armed bandit problem. NIPS. 697–704.

- Krichene et al. (2015) Krichene, S., W. Krichene, R. Dong, A. Bayen. 2015. Convergence of heterogeneous distributed learning in stochastic routing games. Allerton. IEEE, 480–487.

- Lattimore and Szepesvári (2020) Lattimore, T., C. Szepesvári. 2020. Bandit Algorithms. Cambridge University Press.

- Lee et al. (2021) Lee, C-W., C. Kroer, H. Luo. 2021. Last-iterate convergence in extensive-form games. NeurIPS. 14293–14305.

- Liang and Stokes (2019) Liang, T., J. Stokes. 2019. Interaction matters: A note on non-asymptotic local convergence of generative adversarial networks. AISTATS. PMLR, 907–915.

- Lin et al. (2020) Lin, T., Z. Zhou, P. Mertikopoulos, M. I. Jordan. 2020. Finite-time last-iterate convergence for multi-agent learning in games. ICML. PMLR, 6161–6171.

- Liu et al. (2015) Liu, J., S. J. Wright, C. Ré, V. Bittorf, S. Sridhar. 2015. An asynchronous parallel stochastic coordinate descent algorithm. The Journal of Machine Learning Research 16 285–322.

- Mahajan et al. (2017) Mahajan, D., S. S. Keerthi, S. Sundararajan. 2017. A distributed block coordinate descent method for training l1-regularized linear classifiers. The Journal of Machine Learning Research 18(1) 3167–3201.

- Mertikopoulos et al. (2017) Mertikopoulos, P., E. V. Belmega, R. Negrel, L. Sanguinetti. 2017. Distributed stochastic optimization via matrix exponential learning. IEEE Transactions on Signal Processing 65(9) 2277–2290.

- Mertikopoulos et al. (2019) Mertikopoulos, P., B. Lecouat, H. Zenati, C-S. Foo, V. Chandrasekhar, G. Piliouras. 2019. Optimistic mirror descent in saddle-point problems: Going the extra(-gradient) mile. ICLR. 1–23. URL https://openreview.net/forum?id=Bkg8jjC9KQ.

- Mertikopoulos et al. (2018) Mertikopoulos, P., C. Papadimitriou, G. Piliouras. 2018. Cycles in adversarial regularized learning. SODA. SIAM, 2703–2717.

- Mertikopoulos and Zhou (2019) Mertikopoulos, P., Z. Zhou. 2019. Learning in games with continuous action sets and unknown payoff functions. Mathematical Programming 173(1) 465–507.

- Mokhtari et al. (2020) Mokhtari, A., A. Ozdaglar, S. Pattathil. 2020. A unified analysis of extra-gradient and optimistic gradient methods for saddle point problems: Proximal point approach. AISTATS. PMLR, 1497–1507.

- Monderer and Shapley (1996) Monderer, D., L. S. Shapley. 1996. Potential games. Games and Economic Behavior 14(1) 124–143.

- Nemirovski and Todd (2008) Nemirovski, A. S., M. J. Todd. 2008. Interior-point methods for optimization. Acta Numerica 17 191–234.

- Nemirovski and Yudin (1983) Nemirovski, A. S., D. B. Yudin. 1983. Problem Complexity and Method Efficiency in Optimization. Wiley-Interscience.

- Nesterov (2018) Nesterov, Y. 2018. Lectures on Convex Optimization, vol. 137. Springer.

- Nesterov and Nemirovski (1994) Nesterov, Y., A. Nemirovski. 1994. Interior-Point Polynomial Algorithms in Convex Programming. SIAM.

- Orda et al. (1993) Orda, A., R. Rom, N. Shimkin. 1993. Competitive routing in multiuser communication networks. IEEE/ACM Transactions on Networking 1(5) 510–521.

- Rosen (1965) Rosen, J. B. 1965. Existence and uniqueness of equilibrium points for concave n-person games. Econometrica: Journal of the Econometric Society 520–534.

- Saha and Tewari (2011) Saha, A., A. Tewari. 2011. Improved regret guarantees for online smooth convex optimization with bandit feedback. AISTATS. 636–642.

- Sandholm (2001) Sandholm, W. H. 2001. Potential games with continuous player sets. Journal of Economic Theory 97(1) 81–108.

- Sandholm (2015) Sandholm, W. H. 2015. Population games and deterministic evolutionary dynamics. Handbook of Game Theory with Economic Applications, vol. 4. Elsevier, 703–778.

- Shalev-Shwartz (2012) Shalev-Shwartz, S. 2012. Online learning and online convex optimization. Foundations and Trends in Machine Learning 4(2) 107–194.

- Shalev-Shwartz and Singer (2006) Shalev-Shwartz, S., Y. Singer. 2006. Convex repeated games and Fenchel duality. NeurIPS. 1265–1272.

- Shamir (2013) Shamir, O. 2013. On the complexity of bandit and derivative-free stochastic convex optimization. COLT. PMLR, 3–24.

- Shoham and Leyton-Brown (2008) Shoham, Y., K. Leyton-Brown. 2008. Multiagent Systems: Algorithmic, Game-Theoretic, and Logical Foundations. Cambridge University Press.

- Sorin and Wan (2016) Sorin, S., C. Wan. 2016. Finite composite games: Equilibria and dynamics. Journal of Dynamics and Games 3(1) 101–120.

- Spall (1997) Spall, J. C. 1997. A one-measurement form of simultaneous perturbation stochastic approximation. Automatica 33(1) 109–112.

- Tan (2014) Tan, C. W. 2014. Wireless network optimization by Perron-Frobenius theory. CISS. IEEE, 1–6.

- Weeraddana et al. (2012) Weeraddana, P. C., M. Codreanu, M. Latva-aho, A. Ephremides, C. Fischione. 2012. Weighted Sum-Rate Maximization in Wireless Networks: A Review. Now Foundations and Trends.

- Wei et al. (2021a) Wei, C-Y., C-W. Lee, M. Zhang, H. Luo. 2021a. Last-iterate convergence of decentralized optimistic gradient descent/ascent in infinite-horizon competitive Markov games. COLT. PMLR, 4259–4299.

- Wei et al. (2021b) Wei, C-Y., C-W. Lee, M. Zhang, H. Luo. 2021b. Linear last-iterate convergence in constrained saddle-point optimization. ICLR. 1–39. URL https://openreview.net/forum?id=dx11_7vm5_r.

- Zhang and Kwok (2014) Zhang, R., J. Kwok. 2014. Asynchronous distributed ADMM for consensus optimization. ICML. PMLR, 1701–1709.

- Zhou et al. (2018) Zhou, Z., P. Mertikopoulos, S. Athey, N. Bambos, P. Glynn, Y. Ye. 2018. Learning in games with lossy feedback. NIPS. 1–11.

- Zhou et al. (2017a) Zhou, Z., P. Mertikopoulos, N. Bambos, P. Glynn, C. Tomlin. 2017a. Countering feedback delays in multi-agent learning. NIPS. 6172–6182.

- Zhou et al. (2017b) Zhou, Z., P. Mertikopoulos, A. L. Moustakas, N. Bambos, P. Glynn. 2017b. Mirror descent learning in continuous games. CDC. IEEE, 5776–5783.

- Zhou et al. (2021) Zhou, Z., P. Mertikopoulos, A. L. Moustakas, N. Bambos, P. Glynn. 2021. Robust power management via learning and game design. Operations Research 69(1) 331–345.

- Zinkevich (2003) Zinkevich, M. 2003. Online convex programming and generalized infinitesimal gradient ascent. ICML. 928–936.

Auxiliary Results and Missing Proofs

6 Proof of Lemma 2.12

By the definition of in Eq. (5), the iterate satisfies that

Using Lemma 2.8 with and , we have

By the definition, we have . Putting these pieces together yields that

| (11) |

Then we bound the term by Lemma 2.5. Indeed, we let the function be defined as

Since is the sum of a self-concordant barrier function and a quadratic function, we have is also a self-concordant function and have

| (12) |

By definition of , we have . Then, Eq. (12) implies that

| (13) |

To apply Lemma 2.5, we need to guarantee that . Indeed, by the definition of and using , we have

Since and for all , we have . Combining it with yields that . By Lemma 2.5, we have

This together with the Hölder’s inequality yields that

Using again, we have . Plugging this inequality into Eq. (11) yields the desired inequality.

7 Proof of Theorem 2.10

We are in a position to prove Theorem 2.10 regarding the regret bound of Algorithm 1. For simplicity, we assume that for some . Fixing a point , we have

where . Since is positive definite, and , we have

| (15) |

By Lemma 2.6 and Eq. (15), we have

| (16) |

Since is concave and , we have

| (17) |

By the definition of , we have

By Lemma 2.6 and Eq. (15) again, we have

| (18) |

It remains to bound the second term. Since , Lemma 2.12 implies that

Taking the expectation of both sides conditioned on and dividing both sides by , we have

By the definition of and using Lemma 2.6, we have

and

Since is -strongly concave, Lemma 2.6 implies that is also -strongly concave and we have . Putting these pieces together yields that

Rearranging the above inequality and take the expectation of both sides, we have

Therefore, we have

| II | (19) | ||||

Since , we have and . Then, we consider the following two cases:

- •

- •

Combining the above two cases with the fact that is arbitrarily chosen, we have

This completes the proof.

8 Proofs for Example 3.5, 3.7 and 3.8

We show that Cournot competition and Kelly auction in Example 3.5 and 3.7 are -strongly monotone games (cf. Definition 3.4) for some and for all .

Cournot competition.

Kelly auction.

Example 3.7 satisfies Definition 3.4 with and for all . Indeed, each players’ reward function is given by

Define for all , it suffices to prove that

The following proposition is a restatement of Rosen (1965, Theorem 6) and plays an important role in the subsequent analysis.

Proposition 8.1

Given a continuous game , where each is twice continuously differentiable. For each , define the -weighted Hessian matrix as follows:

If is negative-definite for every , we have

where the equality holds true if and only if .

As a consequence of Proposition 8.1, we have for all if for all . Thus, it suffices to show that

| (22) |

where for each and all .

We define the so-called social welfare function as follows,

| (23) |

By the definition, we have

For the simplicity, we just write , and . Then, we have

| (24) |

We are now ready to prove Eq. (22). Indeed, since the is concave for all , we have

-

•

The social welfare function is concave in .

-

•

Each reward function is concave in and convex in .

Since is concave in , we have for all . Since is convex in , we have for all and all (simply note that is the Hessian of with the variable omitted). Putting all these pieces together with Eq. (24) yields that

| (25) |

Note that is a block diagonal matrix with being the diagonal elements. Since is the sum of functions where the one only depends on , we have

Since for all , we have

| (26) |

Plugging Eq. (26) into Eq. (25), we have

Therefore, we conclude the desired result as mentioned before.

Retailer Pricing Games.

For the single-retailer multi-product pricing setting, we have

Recall that (not necessarily symmetrical) and we let , we have

Since the transpose of a scalar is itself, we have for all . Then, we have

If for all , we can easily verify that

which implies that the total revenue function is -strongly concave in .

For the multi-retailer pricing with a single product (for simplicity), we can show that the game satisfies Definition 3.4 with and for all if . Indeed, each players’ reward function is given by

Taking the derivative of with respect to yields that . As a consequence of Proposition 8.1, we have for all if for all . Thus, it suffices to show that

| (27) |

where for each and all . Through some simple calculations, we have for all where . Therefore, we conclude the desired result in Eq. (27) from the condition assumed in Example 3.8.

9 Proof of Lemma 3.9

By the definition, we have

Since all of are invertible, we can define the auxiliary functions by

| (28) |

and have

For simplicity, we let . By applying the same argument as used in (Bravo et al. 2018, Lemma C.1) with the independence of sampling directions , we have

where, in the last equality, we use the identity

which, in turn, follows from the Stoke’s theorem. Since , the above argument indeed implies that with . Using Eq. (28) and , we have

with where for all .

Moreover, we have is -Lipschitz continuous. Thus, we have

This completes the proof.

10 Proof of Lemma 3.14

Since Algorithm 2 is developed in which each player chooses her decision using Algorithm 1, Lemma 2.12 implies that

where and is a nonincreasing sequence satisfying that . Since in the multi-agent setting, the above inequality holds true for all if . Multiplying it by , summing over , and then using , we obtain the desired inequality.

11 Proof of Theorem 3.12

We are in a position to prove Theorem 3.12 regarding the last-iterate convergence rate of Algorithm 2 for the case when the bandit feedback is available. For simplicity, we assume that for some . Since , Lemma 3.14 implies that

Taking the expectation of both sides conditioned on , we have