Optimal Investment with Risk Controlled by

Weighted Entropic Risk Measures††thanks: Supported by the National Key R&D Program of China (NO. 2020YFA0712700) and NSFC (NO. 12071146).

Abstract

A risk measure that is consistent with the second-order stochastic dominance and additive for sums of independent random variables can be represented as a weighted entropic risk measure (WERM). The expected utility maximization problem with risk controlled by WERM and a related risk minimization problem are investigated in this paper. The latter is same to a problem of maximizing a weighted average of constant-absolute-risk-aversion (CARA) certainty equivalents. The solutions of all the optimization problems are explicitly characterized and an iterative method of the solutions is provided.

Keywords: expected utility maximization, risk management, weighted entropic risk measure, weighted CARA certainty equivalents, monotone additive risk measure

1 Introduction

An important feature in practical investments is managing market-risk exposure. In the existing literature, variance, value at risk (VaR), and conditional VaR (CVaR)111Known also as “expected shortfall” or “average VaR” in the literature. are the most popular three risk measures in studying the problem of portfolio optimization with risk constraints. Among others, Markowitz (1952) investigated the problem of mean-variance efficient portfolio selection, where variance is used as the risk measure; Basak and Shapiro (2001) and Basak et al. (2006) investigated the problem of expected utility maximization with VaR-based risk management; Rockafellar and Uryasev (2000) investigated the problem of portfolio optimization with CVaR-based risk management. Extensions of VaR and CVaR, including spectral risk measures and weighted VaR, have arisen and been applied to the problem of portfolio optimization with risk management; see Acerbi (2002), Acerbi and Simonetti (2002), Adam et al. (2008), Cahuich and Hernández-Hernández (2013), He et al. (2015), Ding and Xu (2015), and Wei (2018, 2021), for examples.

It is a natural requirement that a risk measure should have the following two properties.

-

•

Monotonicity: If first-order stochastically dominates , then .

-

•

Additivity: If and are independent, then .

The financial meaning of monotonicity is clear: the downside risk of a position is reduced if the payoff profile is increased. The financial meaning of additivity is also clear: the risk associated with a portfolio made of independent assets is exactly the sum of the risk associated with each individual asset. A risk measure satisfying monotonicity and additivity is called a monotone additive risk measure.

Variance, VaR, and CVaR are, however, not monotone additives risk measures (except for the trivial cases of VaR and CVaR with the extremal confidence levels ). Variance is additive but not monotone. VaR and CVaR are monotone but not additive.

Goovaerts et al (2004) and Mu et al (2021) showed that a monotone additive risk measure has a representation222The monotonicity of Goovaerts et al (2004) is stronger than that of Mu et al (2021). But their representations are same.

where is a probability measure on . Furthermore, Mu et al (2021) also showed that is consistent with the second-order stochastic dominance (SSD) if and only if the weighting measure is supported by . In that case,

It is well known that is the entropic risk measure with parameter ; see Föllmer and Schied (2016), for example. Therefore, an SSD-consistent monotone additive risk measure is a weighted average of entropic risk measures and hence is called a weighted entropic risk measure (WERM).

To the best of our knowledge, the literature to date contains no reports on the problem of expected utility maximization with risk controlled by WERMs. The present paper is aimed at filling that gap. As initiating work, we study the problem within a complete market.

The main contributions of the paper are as follows.

The feasibility problem of the constraints motives us to consider the problem of risk minimization, which is essentially same to the problem of maximizing a weighted average of CARA certainty equivalents. The existence and uniqueness of the optimal solution is established. The optimality condition for the optimal solution is given as

where is the stochastic discount factor (SDF)333Known also as the “pricing kernel” or “state price density” in the literature., is the Lagrangian multiplier, is given by

and is the so-called marginal risk density.

For the expected utility maximization problem with a WERM constraint, the existence and uniqueness of the optimal solution is also established. The optimality condition for the optimal solution is then

where is the utility function and and are the Lagrangian multipliers.

For the both optimization problems, an iterative method to the optimal solutions is provided.

The rest of this paper is organized as follows. Section 2 formulates the optimization problems. Section 3 investigates the risk minimization problem. Section 4 investigates the expected utility maximization problem with a WERM constraint. Section 5 provides numerical examples. Appendix A collects some properties of WERM. Appendix B presents some proofs.

2 Problem Formulation

2.1 Expected Utility

Consider a complete probability space and an arbitrage-free market. Assume that the market is complete and has a unique SDF , which is -measurable and satisfies and .

Consider an agent that is an expected utility maximizer and whose utility function satisfies the next standing assumption.

Assumption 2.1.

is continuously differentiable, strictly increasing, and strictly concave and satisfies the Inada conditions:

Following Kramkov and Schachermayer (1999), we introduce the following assumption on the asymptotic behavior of the elasticity of .

Assumption 2.2.

.

Let denote all -measurable random variables and

For any initial capital , let denote all affordable terminal wealth:

The standard expected utility maximization problem is

| (2.1) |

and its optimal value is denoted by . To avoid unnecessary technical details, we make the following standing assumption.

Assumption 2.3.

for some .

2.2 Weighted Entropic Risk Measure

A monotone additive risk measure is a functional from a subspace to that satisfies the following two properties:

-

•

Monotonicity: If , then ;

-

•

Additivity: If and are independent, then .

Monotone additive risk measures, including WERMs as special cases, are axiomatically characterized by Goovaerts et al (2004) and Mu et al (2021); the axiomatic characterization of non-monotone additive risk measures can go back to Gerber and Goovaerts (1981). Goovaerts et al (2004) and Mu et al (2021) showed that a monotone additive risk measure can be represented as

Here is a probability measure on , and, for every and , is given by

| (2.2) |

In Goovaerts et al (2004), represents for all . In Mu et al (2021), represents that first-order stochastically dominates (FSD) . The monotonicity of Goovaerts et al (2004) is hence stronger than that of Mu et al (2021). But their representations are same.

Furthermore, Mu et al (2021) also showed that a monotone additive risk measure is SSD-consistent if and only if its has representation

| (2.3) |

where is a probability measure on . For each , is the well known entropic risk measure with parameter ; see Föllmer and Schied (2016). Therefore, the representation (2.3) is a weighted average of entropic risk measures according to a weighting measure . For this reason, an SSD-consistent monotone additive risk measure is also called a weighted entropic risk measure. Appendix A collects some properties of WERM.

We make the following assumption on the weighting measure .

Assumption 2.4.

There exists some such that .

Under Assumption 2.4 we have that

| (2.4) |

2.3 Optimization Problem

Given an initial capital , the problem that we consider is maximizing from the terminal wealth subject to the budget constraint and the risk constraint:

| (2.5) |

where is a constant. Before studying problem (2.5), we consider the feasibility problem of the constraints: is there a feasible solution, i.e., is there an that satisfies both the budget constraint and the risk constraint ? This motives us to consider the risk minimization problem as follows:

| (2.6) |

Let denote the minimal value of problem (2.6). The risk minimization problem will be investigated in the next section.

Remark 2.5.

The risk minimization problem is obviously same to the following problem

| (2.7) |

where

is a monotone utility that is additive for the sum of independent random variables. The utility is a weighted average of CARA certainty equivalents since each is the certainty equivalent of for CARA utility function . As pointed out by Mu et al (2021, Section 4.1), if a monotone preference over monetary gambles is not affected by independent background risks, then it can be represented by a weighted average of CARA certainty equivalents. Therefore, the next section itself is interesting if the optimization problem for such a preference is concerned.

3 Risk Minimization Problem

Recall that is the minimal value of problem (2.6). Obviously, is decreasing444Herein, “increasing” means “non-decreasing” and “decreasing” means “non-increasing.” and convex on . The following theorem establishes the existence and uniqueness of the solution of the risk minimization problem.

Proof. See Appendix B.1.

3.1 Optimality Condition

Problem (2.6) can be solved by using Lagrangian multipliers. We begin with the next lemma.

Lemma 3.2.

Proof. See Appendix B.2.

Obviously, is concave, increasing, and upper semi-continuous (and hence right-continuous) on . Let

It is easy to see that since if then

Therefore,

Remark 3.3.

Under Assumption 2.4, similarly to Theorem 3.1, we can show that problem (3.2) has a unique solution for each . Let

| (3.3) |

Then Lemma 3.2 implies that is decreasing on . Moreover, a combination of Theorem 3.1 and Lemma 3.2 implies that, for any , for some . Therefore, is continuous on ,

The monotonicity and continuity of make it easy to search for the desired Lagrangian multiplier for any given budget level by solving the equation .

The optimal solution is closely related to a transformation of , which is given by

| (3.4) |

We now give an economic interpretation of (3.4) by some heuristic calculations. Firstly, for any given state ,

The marginal risk of losing money in state is then

The marginal risk density of state is then

Therefore, is the marginal risk density of . Moreover, Theorem A.7 in the appendix shows that is something like the Gâteaux derivative of .

The next theorem explicitly characterizes the solution of problem (3.2) in terms of the marginal risk density.

Theorem 3.4.

Proof. See Appendix B.3.

The optimality condition (3.5) is an explicit trade-off between the risk and the price by comparing the marginal risk density and the state price density .

Corollary 3.5.

In the next part of this subsection, we write the optimality condition (3.5) in another form. Let functions and be given by

| (3.6) |

It is easy to see that both and are continuous and strictly decreasing with

Proof. Recall that is strictly decreasing and . Then condition (3.5) reads

which is equivalent to

| (3.8) |

In view of (3.7), is determined by , which should be further jointly determined with . We now derive the equations for by plugging (3.7) into (3.6). By (3.7), the probability distribution function of satisfies that

Recalling the following formula, see Feller (1971, Section 13.2) for example,

we have that

| (3.9) |

since is strictly decreasing and hence

Therefore, we get the following system of integral equations for :

| (3.10) |

3.2 Iterative Method of the Optimal Solution

Now we provide an iterative method to solve problem (3.2). For any given , let

| (3.11) |

Obviously, both and are continuous and strictly decreasing. Moreover,

| (3.12) |

For any given , we consider a transform defined as follows.

Definition 3.7.

For any given , let

Obviously, (3.7) is equivalent to that is a fixed point of : .

Lemma 3.8.

The transform in Definition 3.7 is monotone: for any , we have that

Proof. It is easy and standard.

Now we consider a sequence given by

| (3.13) |

By Lemma 3.8 and a.s., we have that a.s. Successively continuing the above argument leads to a.s. for all . Then we know that

| (3.14) |

for some -valued random variable .

Theorem 3.9.

Proof. Assume that solves problem (3.2). Then a.s. by Lemma 3.8. Similarly, a.s. Successively continuing the above argument leads to a.s. for all . Therefore a.s. and hence .

Conversely, assume that . Now we show that solves problem (3.2). It suffices to show that . To this end, for all (including the case ), let

By (3.14) and the monotone convergence theorem,

By , there exists some such that

Then by the monotone convergence theorem once again,

Every (including ) is continuous and strictly decreasing on with

Then we have that555Obviously, on . Suppose on the contrary of (3.15) that for some and . Then , which contradicts .

| (3.15) |

Recall that, for all ,

By passing to the limit, we get that .

4 Expected Utility Maximization Problem

Now we go back to the expected utility maximization problem (2.5).

By Theorem 3.1, problem (2.5) has a feasible solution if and only if . Moreover, in the case when , problem (2.5) is solved by the risk minimizer, which has been characterized by Section 3. On the other hand, for every , let solve expected utility maximization problem (2.1) without risk constraint and let

| (4.1) |

Obviously, if , then solve problem (2.5) as well. Therefore, in the sequel, we always assume that .

We first establish the existence and uniqueness of the solution.

For any fixed , let denote the value of problem (2.5).

Theorem 4.1.

Proof. It is standard and similar to Wang and Xia (2021, Theorem 3.4), by combining some arguments in the proofs of Theorem 3.1.

4.1 Optimality Condition

Problem (2.5) can be solved by using Lagrangian multipliers. We begin with the following lemma, which can be proved in a similar way to Lemma 3.2.

Lemma 4.2.

Now we consider, for every , the problem

| (4.2) |

Remark 4.3.

Under Assumptions 2.1–2.4, similarly to Theorem 4.1, we can show that problem (4.2) has a unique solution for each . Let

| (4.3) |

Then Lemma 4.2 implies that is decreasing on . Moreover, a combination of Theorem 4.1 and Lemma 4.2 implies that, for any , for some . Therefore, is continuous on ,

This allows us to search for the desired Lagrangian multiplier for any given risk level by solving the equation .

Now we consider problem (4.2) for any fixed , which reads

| (4.4) |

The value of problem (4.4) is denoted by . It is easy to see that is increasing and concave on .

Similarly to Lemma 3.2, we have the next lemma.

Lemma 4.4.

From now on, we focus on studying the problem

| (4.6) |

where and . The value of problem (4.6) is denoted by .

It is easy to see that, for any given , is convex, decreasing, and lower semi-continuous (and hence right-continuous) on . Let

It is easy to see that since if then

Therefore,

Similarly to Remark 4.3, we have the next remark.

Remark 4.5.

The next theorem explicitly characterizes the solution of problem (4.6).

Theorem 4.6.

Proof. See Appendix B.4.

The optimality condition (4.8) is an explicit trade-off among the utility, the price, and risk by comparing the marginal utility , state price density , and the marginal risk density .

Corollary 4.7.

Let functions be given by

| (4.9) |

where function is defined by (3.6). Then the optimality condition (4.8) reads

| (4.10) |

In view of (4.10), is determined by , which should be further jointly determined with . Now we derive the equations for . The distribution function satisfies that

| (4.11) |

Therefore, similarly to (3.9), we get the following system of integral equations for .

| (4.12) |

4.2 Iterative Method of the Optimal Solution

Now we provide an iterative method to solve problem (4.6).

Recall that satisfies the Inada condition and function is given by (3.11). For any given , by (3.12), equation

| (4.13) |

has a unique solution . Obviously, a.s. We consider a transform defined as follows.

Definition 4.8.

For any given , let be determined by (4.13). Then .

Obviously, (4.10) is equivalent to .

5 Numerical Example

5.1 Entropic Risk Measure

In this subsection we consider a simple but illustrative case when is an entropic risk measure:

where parameter . In this case,

Risk Minimization

Let be determined by

Then, by Corollary 3.5 and Lemma 3.6,

solves the risk minimization problem (2.6). Moreover,

implying that

So we get the closed-form solution for the risk minimization problem in the case when is an entropic risk measure.

Example 5.1 (Log-Normally Distributed SDF).

Assume that the SDF is log-normally distributed: , where and are constants. Let

In this case, we have that

We can search for the desired by solving the equation . Then the risk minimizer

Moreover, , where

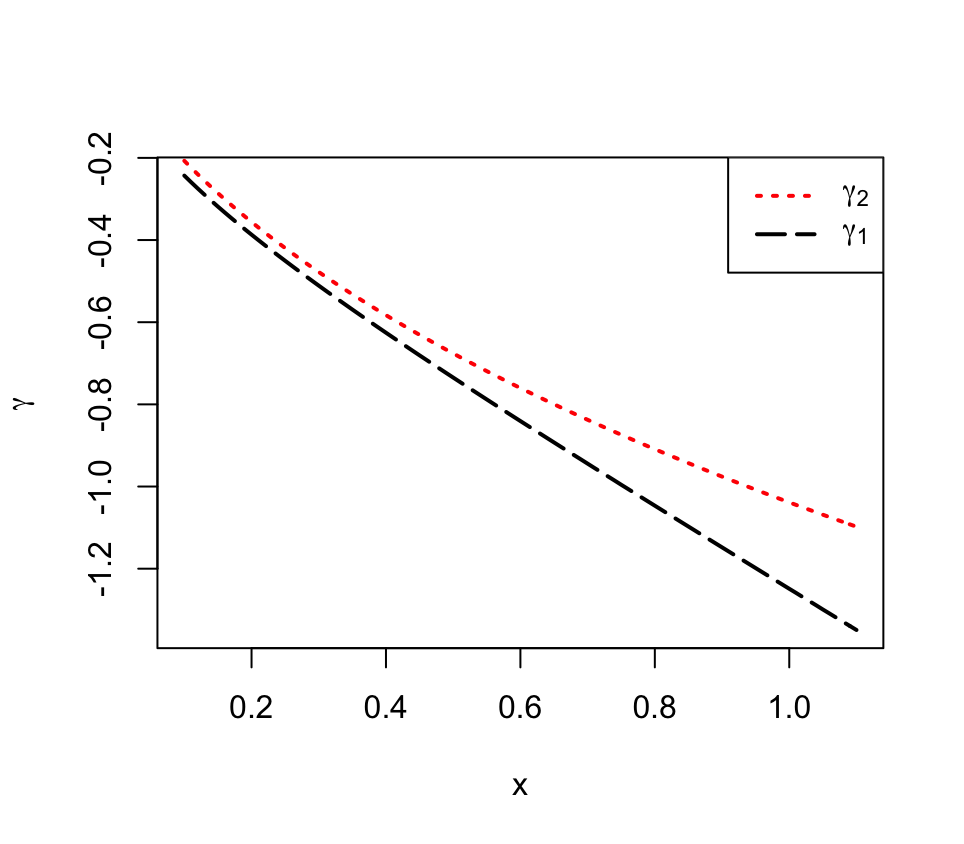

Figure 1 displays when and . (In this case, .) Particularly, .

Expected Utility Maximization

Recall that is the solution of expected utility maximization problem (2.1) without risk constraint. It is well known that and hence that

where is the solution of equation

Example 5.2.

Assume that . In this case, and . Therefore, and . So we have . Figure 1 displays when and . Particularly, .

Let and be fixed. Now we assume that solves the expected utility maximization problem (2.5). By Theorem 4.6 and Lemma 4.2,

Therefore,

and

In the above, the Lagrangian multipliers and are determined by

Once and have been determined by (5.1)–(5.2), then by (4.10),

So we also get the closed-form solution for the expected utility maximization problem (2.5) in the case when is an entropic risk measure.

Example 5.3.

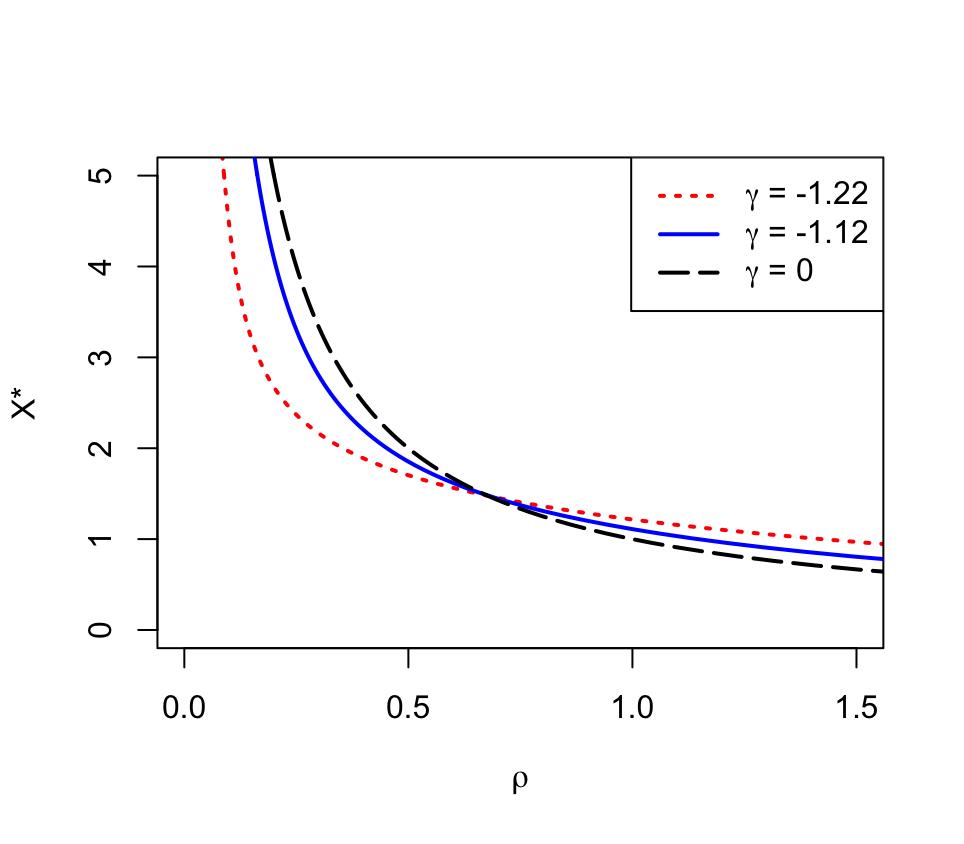

Assume that , , and . When the budget level , recall that and . In Figure 2, the expected utility maximizers are displayed as functions of for risk levels and , as well as for (corresponding to the case without risk constraint). The lower the risk level , i.e., the less the risk tolerance, the less risky is the terminal payoff in the sense of He, Kouwenberg, and Zhou (2017, Definition 3.9 and Proposition 3.11): the optimal terminal payoffs for two risk levels, as decreasing functions of the SDF , have the single-crossing property.

5.2 Weighted Entropic Risk Measure

For the optimization problems with risk controlled by a general WERM, the closed-form solutions are not available. We can find the numerical solutions by the iterative methods in Sections 3.2 and 4.2 and provide some numerical results for a specific model where the stochastic discount factor , the utility function , and the weighting measure are given as follows.

-

•

is log-normally distributed: , where and .

-

•

, .

-

•

and is the probability measure of the uniform distribution on . In this case,

(5.3)

We begin with the risk minimization problem.

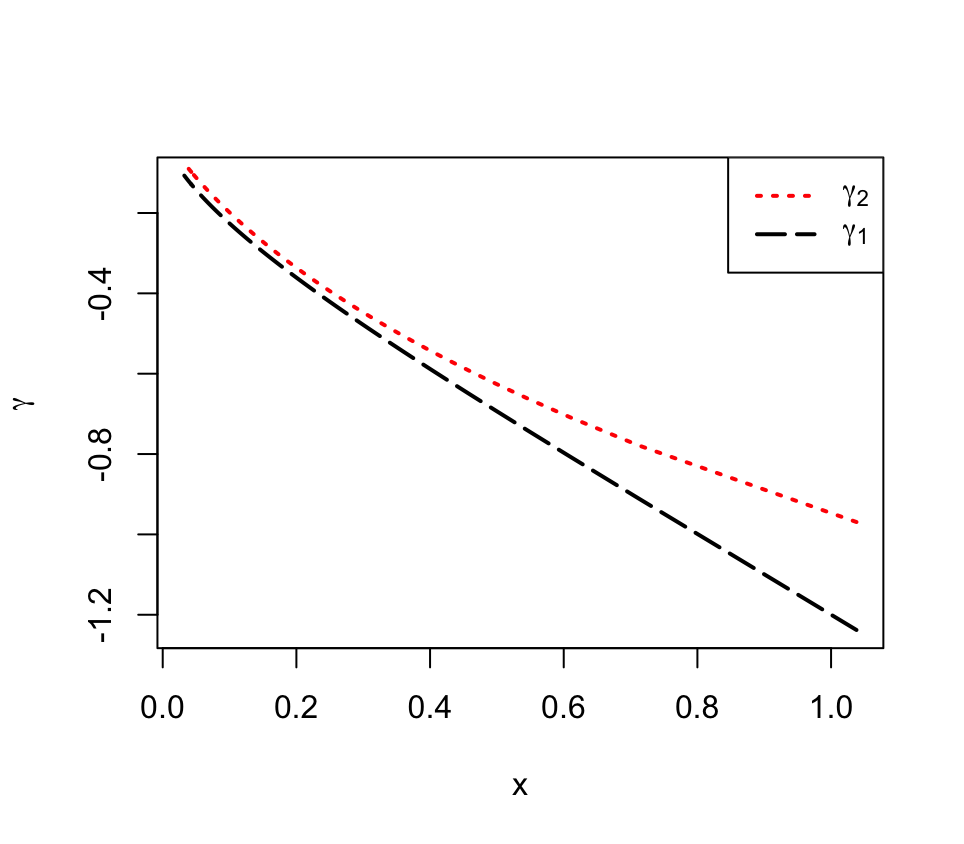

First, for some given , compute the optimal solution of problem (3.2) according to the iterative method in Section 3.2 and get the value of according to (3.3). Obviously, . By varying , we plot v.s. , as done in Figure 3. (By (4.1) and Example 5.2, .)

Second, for any given budget level , say , search for such that and then apply the iterative method to find the optimal solution of problem (2.6) and get the value of . For the specific model above, we get that and .

Now we provide some numerical results for the expected utility maximization problem.

First, for some given and , we can compute the optimal solution of problem (4.6) according to the iterative method is Section 4.2 and get the value of according to (4.7). Therefore, for the given , we can search for such that .

Second, for given , we know that is the solution of problem (4.2), i.e., . Then we can compute according to (4.3).

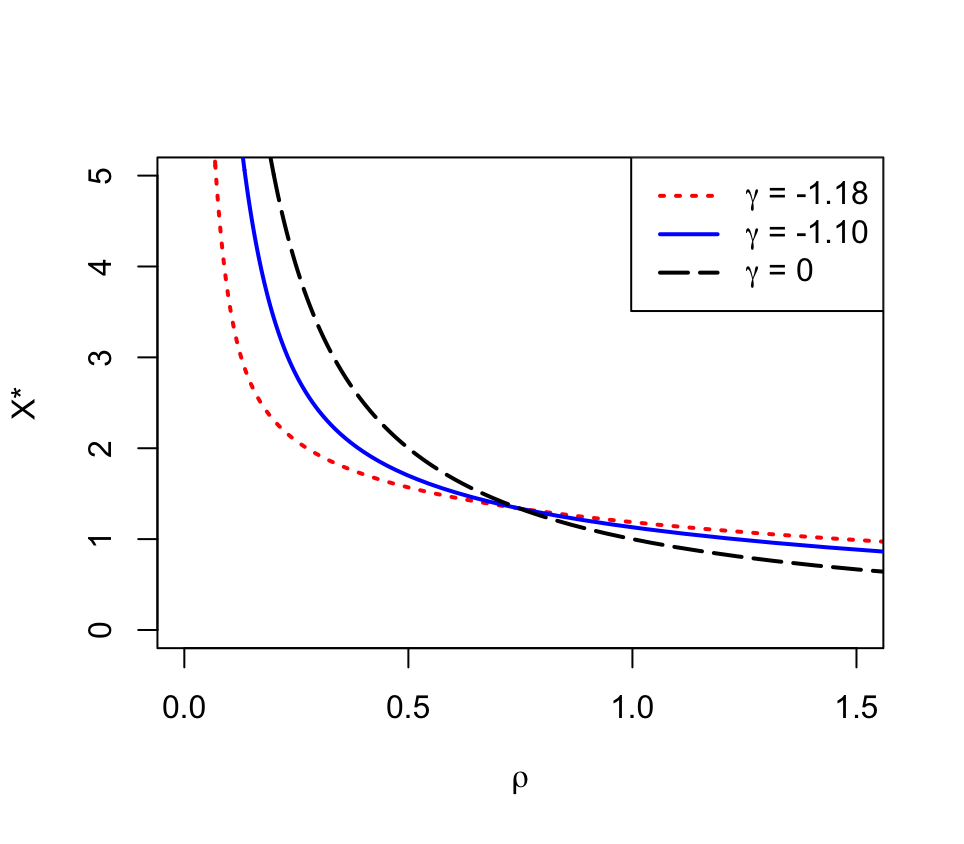

Third, search for such that and then apply the iterative method to find for and , which gives the optimal solution of problem (2.5). For the specific model above, budget level , and risk levels , , and , the optimal solutions are displayed in Figure 4, where corresponding to the case without risk constraint. Similarly to Figure 2, the optimal terminal payoffs for two risk levels, as decreasing functions of the SDF , also have the single-crossing property.

Appendix

Appendix A Some Properties of Weighted Entropic Risk Measures

Recall that is defined by (2.2) for all and . A weighted entropic risk measure is given by

where the weighting measure is a probability measure on .

Definition A.1.

For any , we say that is not constant if for all .

Lemma A.2.

Let and , . If is not constant and both and are finite, then

Proof. For every , we can find some such that

Then , i.e.,

By assumption, . Then the strict convexity of function implies that

Therefore,

Theorem A.3.

Assume . Let , . If is not constant and both and are finite, then

Proof. It is an abvious consequence of Lemma A.2.

The next lemma is obvious.

Lemma A.4.

If , then for all . If is not constant, then for all .

Lemma A.5.

Let and a sequence converge to some in probability. Then the sequence is bounded and non-positive.

Proof. It suffices to show that the sequence is lower bounded since for and . Suppose on the contrary that there exists some subsequence, which is still denoted by , such that , i.e., . In this case, we have that in probability, i.e., in probability. This contradicts with the assumption that in probability. Therefore, is lower bounded.

Theorem A.6.

Let satisfy Assumption 2.4 and a sequence converge to some in probability. Then .

Proof. The bounded convergence theorem implies that

Lemma A.4 implies that

Then by the bounded convergence theorem,

Proof. By the mean value theorem, there exists some measurable functions

and

such that, for all ,

and

Then for all ,

Obviously, function is strictly positive and continuous on and hence there exists some such that

Then by the dominated convergence theorem, we have that

Theorem A.8.

Let satisfy Assumption 2.4. If , then

Proof. Assume that . We first show that

| (A.1) |

Assume that . For any , let . Then is convex on and hence

where the last equality follows from Theorem A.7. If , for any , let

Obviously, for all . Moreover,

and

yielding . Then by (A.1), we have that

Noting that a.s., and , we have that

Then applying Fatou lemma yields that

Here , . Moreover, Theorem A.6 implies that

Therefore, we have that

Obviously, a.s. Then by Theorem A.6 once again, we get that

Appendix B Proofs

B.1 Proof of Theorem 3.1

Let . Then there exists a sequence such that as . By Komolós lemma [see Kramkov and Schachermayer (1999, Lemma 3.1) for example], there exits a sequence such that for all and converges in probability to some -valued random variable , where denotes the convex hull. Then by Fatou lemma,

Therefore, . Then by (2.4), Theorem A.6 and the convexity of ,

Therefore, solves problem (2.6).

B.2 Proof of Lemma 3.2

The “if” part is an implication of Luenberger (1969, Theorem 1 on p. 220). Now we show the “only if” part. Assume that solves problem (2.6). Then by Luenberger (1969, Theorem 1 on p. 217), there exists some such that

| (B.1) |

It is easy to see that the optimization problem in (B.1) has no solution if . Therefore, and hence .

Finally, by Luenberger (1969, Theorem 1 and the last paragraph on p. 222), we have .

B.3 Proof of Theorem 3.4

B.4 Proof of Theorem 4.6

It is divided into a series of lemmas.

Proof. Assume on the contrary that . For any , let . The concavity of and imply that

On the other hand,

and

by Theorem A.7. Then we have that

as . This contradicts the optimality of . Therefore, and hence a.s.

Proof. Let . Suppose on the contrary that . Then for some , where

For every , we can find a random variable a.s. such that

Let . Then

implying that

Observing that , we can let (and ) be small enough such that

By the concavity of and Theorem A.8, we have that

which contradicts the optimality of .

Proof. Let . Suppose on the contrary that . Then for some , where

By Lemma B.1, a.s. For every , we can find a random variable a.s. such that a.s. on and

Let . Then

implying that

Observing that , we can let be small enough such that

By the concavity of and Theorem A.8, we have that

which contradicts the optimality of .

Lemma B.4.

References

-

Acerbi, C. (2002): “Spectral measures of risk: A coherent representation of subjective risk aversion,” Journal of Banking and Finance 26, 1505–1518.

-

Acerbi, C., and P. Simonetti (2002): “Portfolio optimization with spectral measures of risk,” Unpublished manuscript.

-

Adam, A., M. Houkari and J.-P. Laurent (2008): “Spectral risk measures and portfolio selection,” Journal of Banking and Finance 32, 1870–1882.

-

Basak, S., and A. Shapiro (2001): “Value-at-risk-based risk management: Optimal policies and asset prices,” Review of Financial Studies 14, 371–405.

-

Basak, S., A. Shapiro, and L. Teplá (2006): “Risk management with benchmarking,” Management Science 52, 542–557.

-

Cahuich, L. D., and D. Hernández-Hernández (2013): “Quantile Portfolio Optimization under Risk Measure Constraints,” Appl. Math. Optim. 68, 157–179.

-

Ding, P., and Z. Q. Xu (2015): “Rank-Dependent Utility Maximization under Risk Exposure Constraint,” working paper.

-

Feller, W. (1971): An Introduction to Probability Theory and its Applications, Vol. 2, (2nd Edition). New York: John Wiley & Sons

-

Föllmer, H. and A. Schied (2016): Stochastic Finance: An Introduction in Discrete Time (4th Edition). Berlin: Walter de Gruyter.

-

Gerber, H. U. and Goovaerts, M. J. (1981): “On the representation of additive principles of premium calculation,” Scand. Actuarial J. 4, 221–227.

-

Goovaerts, M. J., Kaas, R., Laeven, R. J. A., Tang, Q. (2004): “A comonotonic image of independence for additive risk measures,” Insurance: Mathematics and Economics 35, 581–594.

-

He, X. D., H. Jin, and X. Y. Zhou (2015): “Dynamic Portfolio Choice When Risk is Measured by Weighted VaR,” Mathematics of Operations Research 40: 773–796.

-

He, X. D., R. Kouwenberg, and X. Y. Zhou (2017): “Rank-Dependent Utility and Risk Taking in Complete Markets,” SIAM Journal on Financial Mathematics 8, 214–239.

-

Kramkov, D. and W. Schachermayer (1999): “The Asymptotic Elasticity of Utility Functions and Optimal Investment in Incomplete Markets,” Ann. Appl. Prob. 9, 904–950.

-

Luenberger, D. (1969): Optimization by Vector Space Methods. New York: John Wiley & Sons

-

Markowitz, H. (1952): “Portfolio Selection,” J. Finance 7, 77–91.

-

Mu, X., L. Pomatto, P. Strack, and O. Tamuz (2021): “Monotone Additive Statistics,” arXiv: 2102.00618.

-

Rockafellar, R. T., and S. Uryasev (2000): “Optimization of conditional value-at-risk,” Journal of Risk 2, 21–42.

-

Wang, X. and J. Xia (2021): “Expected Utility Maximization with Stochastic Dominance Constraints in Complete Markets,” SIAM Journal on Financial Mathematics 12, 1054–1111.

-

Wei, P. (2018): “Risk Management with Weighted VaR,” Math. Finance 28, 1020–1060.

-

Wei, P. (2021): “Risk management with expected shortfall,” Math Finan Econ, forthcoming.