Reinforcement Learning for Options on

Target Volatility Funds

Abstract

In this work we deal with the funding costs rising from hedging the risky securities underlying a target volatility strategy (TVS), a portfolio of risky assets and a risk-free one dynamically rebalanced in order to keep the realized volatility of the portfolio on a certain level. The uncertainty in the TVS risky portfolio composition along with the difference in hedging costs for each component requires to solve a control problem to evaluate the option prices. We derive an analytical solution of the problem in the Black and Scholes (BS) scenario. Then we use Reinforcement Learning (RL) techniques to determine the fund composition leading to the most conservative price under the local volatility (LV) model, for which an a priori solution is not available. We show how the performances of the RL agents are compatible with those obtained by applying path-wise the BS analytical strategy to the TVS dynamics, which therefore appears competitive also in the LV scenario.

JEL classification codes: C63, C45, G13.

AMS classification codes: 65C05, 68T07, 91G20.

Keywords: Reinforcement Learning, Hedging Costs, Target Volatility, Asset Allocation, Stochastic Optimal Control Problem.

The opinions here expressed are solely those of the authors and do not represent in any way those of their employers.

1 Introduction

In the recent years portfolio managers are exposed to very low interest rates and quickly changing market volatilities. An effective solution to control risks under such an environment is given by target volatility strategies (TVSs) (also known as constant volatility targeting) which are able to preserve the portfolio at a predetermined level of volatility. A TVS is a portfolio of risky assets (typically equities) and a risk-free asset dynamically re-balanced with the aim of maintaining the overall portfolio volatility level closed to some target value. The constant volatility approach can help investors to obtain desired risk exposures over the short and long term and it increases the risk-adjusted performance of the portfolio.

These products were initially offered in the Asian markets, see for instance the reports of [3] and [27], which highlight the pros and cons for investors, to be adopted in the following years in many other markets in North America and Europe as depicted in [20]. At the present day we can observe some new market indices based on the mechanism of the target volatility strategy such as Dow Jones Volatility Control Index, and S&P 500 Risk Control Index.

In the recent literature TVSs are tested to investigate their performances in term of realized returns, see for instance [16] and [21], and the soundness of the volatility targeting algorithm, as described in [17]. Moreover, in the present day, in the derivative market new structured financial products that see TVSs as underlying are becoming widely used by practitioners. Those derivative instruments are known as target volatility options (TVOs) and have gained great interest in the derivative pricing literature, see in particular [7], [12], [1] ad [8].

This paper is the first attempt, to the best of our knowledge, to analyze the funding costs coming from hedging the risky assets underlying the target volatility strategy. In particular, we consider the point of view of a bank selling a call option to a portfolio manager as protection on the capital invested in a TVS. The portfolio manager has the freedom of changing the relative weights of the risky assets during the life of the TVS. Since the risky assets have different hedging costs, the bank shall adjust the price of the protection to include them in the worst-case scenario, i.e. the most expensive strategy in term of the financing costs. Hence, the pricing problem becomes a continuous dynamical control problem over the risky portfolio composition. In our work we provide to the reader a formal description of the stochastic control problem and most importantly we derive an analytical solution assuming that the risky asset dynamics underlying the TVS follow a Black and Scholes (BS) model [2] and that the derivative contract is a European-style option.

Although from a theoretical point of view this solution represents a sub-optimal strategy when dealing with generic dynamics for the risky assets, we show that the BS solution provides a strong baseline as price to practitioners when testing it against numerical methods with different levels of sophistication for solving the control problem. More precisely we numerically study the problem in the general case of a local volatility dynamics [10, 5] by adopting a Reinforcement Learning approach, in particular an ad hoc vanilla direct policy algorithm and the more sophisticated proximal policy optimization technique developed in [24].

The paper is organized as follows. In Section 2 we introduce more in detail the manager-bank contract and provide the description of the TVS dynamics in presence of valuation adjustments such as the hedging costs. Then, in Section 3 we introduce the structured class of derivative contracts linked to TVSs, where we describe the arising dynamical control problem for pricing those options. Moreover in this section we derive the BS closed solution for European TVOs in two different ways: one applying the Gyöngy Lemma and the other by writing the Hamilton-Jacobi-Bellman equation. In Section 4 we illustrate how we have applied RL to solve the dynamic control problem, giving a description of the algorithm we have built. We conclude the paper with Section 5 where we present the numerical results obtained in this work for the Black and Scholes model and the local volatility one.

A part of this work has been developed during the Master thesis of one of us (SP), where we had the opportunity to collaborate with Marco Bianchetti and Diego Pierluigi Giovannini from Intesa Sanpaolo Milan, that we tank. Moreover we wish to thank the Italian computing centre Cineca, which approved our ISCRA C project and provided us with the high-computing resources of Marconi100 for the numerical simulations of this contribution.

2 Target Volatility Strategy

As mentioned before, this work aims to enrich the TVS pricing literature by studying the aspect related to the funding costs coming from hedging the risky assets underlying a target volatility portfolio. Thus we consider the following scenario: a bank selling a protection to a portfolio manager who has his capital invested in a TVS. In our case the fund manager has the freedom of changing the relative weights of the risky asset during the life of the TVS; once the allocation strategy is selected then the volatility targeting algorithm rebalances the risky component of the portfolio with the risk-free one in order to keep the overall portfolio volatility close to a target value. Clients investing in the fund pay a running fee for the service of the fund manager and their capital is protected.

The fund manager usually buys from a bank an option on the TVS to ensure capital protection. For instance, the capital can be protected by buying a put option. In this case, we can write the net asset value (NAV) of the strategy as given by111Here we neglect discounting factors.

| (1) |

where is the price process of the strategy, and is the guaranteed capital. On the other hand, the fund manager can replicate the payoff by means of the put-call parity by investing the capital in a low-risk asset and buying a call on the strategy

| (2) |

In this way, the TVS is only defined in the two contracts client-fund and fund-bank. The fund manager is not implementing the strategy by trading in the market, and he is not subject to additional costs to access the market. On the other way, the bank is paying such costs since she is actively hedging the call option sold to the manager. The bank trading activity implemented to actively hedge the option requires funding the collateral procedures of the hedging instruments along with any lending/borrowing fee. We remark that the choices of the manager trading activity are stochastic processes since they will depend on the market evolution. Thus, neither the manager strategy nor the bank financing costs for hedging the option can be written in the fund-bank contract. For this reason, the price of a financial product sold by the bank is adjusted to include any valuation adjustment due to the trading activity.

Our aim is to find the most expensive investing strategy from the point of view of financing costs for the bank that the manager could choose in the market. In other words we want to determine the worst-case scenario for the bank. In this section we proceed by defining the price process of the TVS so that we can highlight the impact of valuation adjustments.

2.1 The strategy Price Process

We work on a filtered probability space satisfying the usual assumptions for a market model, where is the physical probability measure representing the actual distribution of supply and demand shocks on equities prices.

We consider a fund trading a basket of risky securities with price process with funded with a cash account accruing at . Any dividend paid by the securities is re-invested in the fund. Here, we assume that the TVS is implemented in continuous time, even if in the practice we can implement the strategy only on a discrete set of dates. We introduce the deflated gain process associated with the risky securities as given by

| (3) |

where we define the deflated price and cumulative dividend processes as

| (4) |

where represents the cumulative contractual-coupon process paid by the security, and represents the cumulative valuation adjustments. Since fund managers allocating TVS usually rely on equity assets, here we use the results of [11] who analyze the valuation adjustments for equity products. We can write

| (5) |

where we call cost of carry, which basically represents the hedging costs for the -th security.

Then, we introduce the strategy price process , and we define the deflated gain process as given by

| (6) |

where are the running fees earned by the fund manager for his activity. We assume that the strategy is self-financing, so that we can write

| (7) |

where is the quantity invested in the -th security222In all formulae we use dot notation for scalar product between vectors, i.e. , or between matrix and vector, i.e. or ..

Now, in order to prevent arbitrages, we assume the existence of a risk-neutral measure equivalent to under which the deflated gain processes of all traded securities are martingales. Under this assumption, we are able to derive the drift conditions on the security price processes, and in turn on the strategy price process.

| (8) |

where are martingale under . If we substitute this expression for the security dynamics into the definition of the strategy we can check that the price process of the strategy is accruing at a cash account rate compensated for the fund manager fees

| (9) |

with martingale under . Notice that, as expected from non-arbitrage considerations, the coupons paid by each security appear only in the drift of the security price process, but they do not impact the drift of the strategy.

Yet, the strategy priced by cannot be described in the contract between the parties, since Equation 7 depends via the security gain processes on the valuation adjustment , which is specific to the investor pricing the strategy. Thus, the TVS defined in the contract will be

| (10) |

leading to the following price process dynamics

| (11) |

with martingale under . In this case we observe that depends explicitly both on the valuation adjustments and on the allocation strategy. Indeed, if we substitute the valuation adjustments with their explicit expression (Equation 5), we get

| (12) |

where we can see the dependency on cost of carry and on the allocation strategy.

2.2 The Volatility Targeting Constraint

In a typical TVS, the fund manager selects a risky-asset portfolio with a specific time-dependent allocation strategy expressed by means of the vector of relative weights , along with a risk-free asset, which we can identify with the bank account . In the following, for sake of simplicity in exposition we consider only total-return securities, namely we set 8. Thus we can write Equation 10 as given by

| (13) |

where is a -dimensional vector of ones and is determined so that the strategy log-normal volatility is kept constant, namely

| (14) |

where is the target volatility value. In practice, this means that the fund manager will select a risky-portfolio choosing equities from the universe where he can trade and after that, his choices will be scaled by the automatic target volatility algorithm333We recall that the universe of assets where the manager can trade and the value of are written in the contract. .

To derive the expression for we need to assume a generic continuous semi-martingales dynamics under the risk-neutral measure for the underlying securities, so that we can write Equation 8 as

| (15) |

where is an adapted matrix process ensuring the existence of a solution for the stochastic differential equation (SDE) and is a -dimensional vector of Brownian motions under . Under these assumptions we can derive an expression for , and we get444In all formulae the norm for a vector is defined as .

| (16) |

Hence, putting this last result in the dynamics of we obtain

| (17) |

where we can see, as expected, that the strategy grows at the risk-free rate but for adjustments due to valuation adjustments and fees.

We highlight that, to derive the dynamics expressed in Equation 17, we have not made any assumptions on the risky allocation strategy; thus all this argument is valid for any constraints on the process .

3 Derivative Pricing

In this section, we analyze derivative contracts linked to the TVS described previously. In particular we will focus on European style options, and we will show that under appropriate assumptions it is possible to find a closed form solution for the optimal allocation strategy which maximizes the contract price.

In a general framework, a derivative contract on the TVS with maturity can be defined as

| (18) |

where is the discount factor with rate , inclusive of the derivative valuation adjustments, and is the cumulative coupon process paid by the derivative, and it depends on the allocation strategy since in turn the TVS depends on it via the valuation adjustments. We take the supremum over the strategies since we do not have any information on the future activity of the fund manager.

3.1 European Options

If the derivative contract depends only on the marginal distribution of at maturity (a European payoff), we are able to prove that exists an optimal strategy, and we are able to calculate it. We consider the following pricing problem

| (19) |

where is the payoff function of the derivative.

We start by introducing the Markovian projection of the dynamics followed by . We name it , and we get by applying the Gyöngy Lemma [13]

| (20) |

where the local drift is defined as

| (21) |

and is a Brownian motion under the risk-neutral measure . Notice that the diffusion coefficient collapses to the target volatility value . Since European payoffs depend only on the marginal distribution at maturity, they can be calculated only by means of the Markovian projection , namely

| (22) |

Hence, we have our first result valid only if valuation adjustments can be neglected:

Proposition 3.1.

A European payoff on the TVS can be calculated by assuming any allocation in the underlying risky basket if all the underlying securities grow under the risk-neutral measure at the risk-free rate without any valuation adjustment, namely if we can write .

3.2 Stochastic Optimal Control Problem

In presence of valuation adjustments, we need to solve the full optimization problem. We discretize the optimal strategy as555We use the symbol for the indicator function of a subset .

| (23) |

according to a time grid with the pricing date and the maturity of the option. Therefore we can apply the dynamic programming principle to express the optimal at time as

| (24) |

where is the option value at time and is any Markovian state such that the drift and the diffusion coefficient of are a function of . We calculate for any given strategy by a suitable discretization of (17) starting from and .

Thus the derivative price is given by:

| (25) |

while the iteration starts from maturity date where the boundary condition is set equal to the payoff function:

| (26) |

3.3 Black and Scholes Model

In the time-dependent Black and Scholes model with deterministic rates, we can work with empty , since in this case the portfolio dynamics (17) is Markovian, leading to an optimal strategy which depends in principle only on . As a consequence, the local drift defined in Equation 21 can be written as

| (27) |

so that the optimization problem can be solved by looking only at the Markovian projection without simulating all the Brownian motions . Notice that we are indicating the dependency on time in parenthesis to highlight that in this formula all the quantities are deterministic functions of time.

A direct consequence is the following proposition, which is relevant for plain vanilla options on TVS.

Proposition 3.2.

When the underlying securities follow a Black and Scholes model with deterministic rates, the optimal strategy for a non-decreasing European payoff consists in minimizing the local drift function, independently of the current state

| (28) |

Analogously, the optimal strategy for a non-increasing European payoff consists in maximizing the local drift function:

| (29) |

The absence of stochastic elements in Equation 28 makes the optimal strategy known a priori with no simulation needed; in fact one can solve the optimization problem once for all just looking at the market data and for the securities. Once is known, then one can price the payoff by the following BS formula

| (30) |

where is the TVS forward curve defined by

| (31) |

while is the standard BS formula for a European option with forward curve , strike , time to maturity , volatility and discount factor .

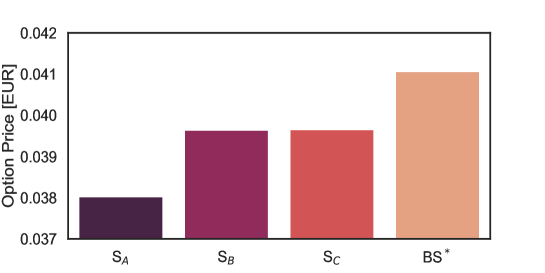

In Figure 1 we provide a comparison among the option price obtained with the optimal stragety (BS∗) of Equation 28 and those with other intutive strategies (SA, SB, SC). Here we consider the case of an at-the-money call option with spot , maturity , target volatility , and a nonnegative constraint on . The intuitive strategies are

-

•

SA: invest all in the asset with the maximum forward curve at maturity;

-

•

SB: for each market pillar before maturity invest all in the asset with minimum ;

-

•

SC: for each market pillar before maturity invest all in the asset with minimum .

As the reader can observe, our strategy outperforms any other intuitive one a practitioner might adopt.

3.3.1 Unconstrained Allocation Strategy: Closed Form Solution

In absence of constraints on the allocation strategy, we are able to derive a closed form solution to the BS problem (28).

Lemma 3.3.

Let be , be a full rank matrix and . Then the closed solution of the optimization problem (28) is

| (32) |

Proof.

Since the argument of the minimum (28) is zero-homogeneous, then we can rewrite the problem as

| (33) | ||||

By setting the Lagrangian function associated with the problem

| (34) |

we obtain the first order conditions

| (35) |

Then, by applying simple algebra, we obtain the analytical form for the free optimal strategy

| (36) |

We take the minus sign to get the minimum value of the TVS local drift while the plus sign for the maximum one (put payoff). ∎

3.3.2 Active Asset (or Bang Bang) Solution

A closed form solution to the minimization of the local drift correction (28) can also be derived in the common case that all costs of carry are nonnegative and the only constraint on portfolio weights is nonnegativity, which would mean a long-only strategy by the fund manager.

Lemma 3.4.

Let be a vector with nonnegative components, be a full rank matrix, and . Then

| (37) |

if is the index which realizes the min, then the infimimum is realized by a vector concentrated on the component: .

Proof.

Let us first consider the case in which . Since the argument of the infimum is zero-homogeneous, normalizing by we can restrict to the affine hyperspace , where the minimization (37) reduces to the maximization of its denominator: the required infimum will be the square root of the reciprocal of

Now we can note that is positive definite, hence , which implies

because . Since we trivially have equality for , this concludes the proof of the case .

Next, let us consider the case in which all components of are strictly positive, and define as the diagonal matrix with diagonal . Then we can rewrite the infimum as a function of :

which by the first part of the proof equals

Finally, let us consider the general case in which may have some components equal to zero. For an arbitrary let us define

One can easily note that as , tends to uniformly on the compact set , so that the minimum converges to the minimum on that set. Since we know by homogeneity that the minimum on equals the minimum on , we conclude

∎

3.4 Hamilton-Jacobi-Bellman Equation for Target Volatility Options

In this section, we want to provide to the reader a formal description of the dynamic problem associated with options on target volatility strategies by writing the Hamilton-Jacobi-Bellman (HJB) equation for the derivative price. We prove that from this equation one can recover the same closed formula (28) for the time-dependent BS model which was derived above from the Gyöngy Lemma.

In full generality we assume that the time evolution of the Markovian factors governing the problem dynamics is given by a stochastic multidimensional process in , , that is the unique strong solution to the following It SDE

| (38) |

which is driven by a -dimensional Wiener process with independent components, . We point out to the reader that with this notation we are including general dynamics models like those with stochastic drift and stochastic diffusive coefficients. Let be the dynamics of the securities a generic function of the Markovian factors, namely

| (39) |

In this framework, the TVS price process dynamics is given by the SDE

| (40) |

where the expression of and can be recovered by applying the It formula to Equation 39.

Given and , we can write the HJB equation for as follows

| (41) | |||

where is the trace operator of , the gradient of w.r.t. , the Hessian matrix of w.r.t. and is the vector defined by:

| (42) |

We take out from the maximum operator all the elements that do not depend on the risky allocation strategy

| (43) | |||

Equation 43 is the Hamilton-Jacobi-Bellman equation describing the TVS dynamic problem for a generic dynamics of the risky securities underlying the portfolio.

If we assume a time-dependent BS dynamics for the risky equities (, and deterministic), then and all the derivatives w.r.t. are zero. Therefore the reduced HJB equation is

| (44) |

if the payoff is non-decreasing in by homogeneity of the SDE we get that is non-decreasing; thus the solution is given by

| (45) |

which is the same result expressed in Equation 28. On the other hand, if the payoff is non-increasing in then the solution will be the .

Conversely, if we deal with a dynamic model for which the derivative contract depends on then the volatility versor term, namely the second one, in the operator of Equation 43 is no longer zero and thus one must solve the entire control problem numerically.

In this work we tackle the non-trivial case of a local volatility (LV) model for the -dynamics, such that . We have chosen the LV model since it is well known in financial literature and among practitioners.

4 Reinforcement Learning

As we have discussed in the previous sections, one must resort to numerical approaches to solve the stochastic control problem related to the TVS in the case of general payoffs or risky securities dynamics. The standard approach could be to use classical techniques based on backwards recursion (24)-(25) such as American Monte Carlo [19]. However, their performances degrade exponentially as the dimension of the problem increases, making prohibitively costly finding the solution to the problem. In our contribution, we adopt a novel technique which is free from the curse of dimensionality and is gaining popularity in many scientific branches for solving stochastic optimal control problems: Reinforcement Learning (RL) [26].

Reinforcement Learning is a branch of Machine Learning which allows an artificial agent to interact with an environment through actions and observations in order to maximize some notion of cumulative reward. In RL the agent is not told which actions to take but instead it must discover by trial and error which are the behaviours yielding the highest reward. This is obtained by updating the agent policy which is a mapping from the environment states to the set of actions. Thus RL is independent of pre-collected data as opposed to other Machine Learning techniques. Because of its nature, RL has been successful in quantitative finance for solving control problems; among the most important RL applications in this field, we refer to [4] as the pioneers in studying self-taught reinforcement trading problems, while to [18] and [14] for hedging derivatives with RL under market frictions.

In our work we adopt two learning strategies to compare their performances in terms of overall reward: an ad hoc direct policy algorithm and the state of the art proximal policy optimization (PPO) developed in [24] and [23].

The first method is a specific algorithm developed by us to fit the problem aim to find the optimal option price; this technique can take place as a direct policy optimization method in the wide taxonomy of Reinforcement Learning algorithms. We will go into details in Section 4.1.

On the other hand, the PPO is a high-level actor-critic algorithm well-suited for continuous control problems. It collects a small batch of experiences interacting with the environment to update its decision-making policy. From those interactions with the environment, PPO is able to compute the expected reward and the value function. We will not provide a complete description of this sophisticated learning strategy; for more details, we refer to the authors’ papers. In our work, we adopt the PPO implementation found in OpenAI Baselines [6].

In the following sections, we describe the way we have formalized the TVS problem in the Reinforcement Learning framework.

4.1 Direct Policy Approach

We consider an episode of length that takes place on a discrete time-grid of fixing times expressed in year fractions with and maturity of the option. At a given episodic time the RL agent interacts with the environment: it receives a representation of the environment called state and on the basis of that it selects an action sampling from the current policy . Here with we refer to the set of parameters through which we parameterize the agent policy at the -th algorithm iteration. In our case the agent can choose the composition of the risky asset portfolio, so that the policy is the allocation strategy introduced in Equation 13:

| (46) |

Since the value function of the problem depends on the Markovian state , the portfolio level and time , our natural choice for the observation state is the following block

| (47) |

In this way, the state contains all the information needed by the agent to take an optimal action, leading to the maximum plain vanilla TVO price.

In this algorithm, we parameterize the agent policy with a feed forward neural network (FFNN), such that coincide with the hidden weights, with the inputs, and with the output. In this way, we are dealing with a deterministic policy, where its functional form is given by the neural network. The parameters update is performed as follows: the agent collects a finite batch of experiences interacting with the environment in a set of episodes , then the loss function is evaluated as

| (48) |

where the expectation indicates the empirical average on the batch. Then the parameters are updated by plugging the policy into a stochastic gradient ascent algorithm. The choice of Equation 48 is justified by the fact that, when the algorithm will find the optimal set , then will be a good proxy of the optimal option price.

Once the training phase is ended and the agent has selected the optimal policy, we can run a Monte Carlo (MC) simulation with never seen scenarios to price the optimal target volatility option and test if the algorithm does not overfit the data.

4.2 Proximal Policy Optimization Approach

As for the direct policy approach, we model the pricing problem considering an episode that takes place on the time-grid with and . Again we choose as observation state the block defined in Equation 47 and the agent policy coincides with the risky allocation strategy (Equation 46). An important difference from the previous method is that: once the agent has selected the action sampled from the current policy, it receives at the next time a reward generated by the environment.

In our work, we have defined two different reward functions with the purpose to analyze which could help the agent to learn more efficiently the optimal policy . Our first definition is

| (49) |

Therefore, during the whole episode, the agent receives a nil reward except at maturity when the reward coincides with the option intrinsic value. This choice may seem too daring because the agent receives a real feedback of its actions only at the end of the whole episode, increasing the probability to obtain a slow learning. However, if the agent has learnt , the average cumulative reward per episode will coincide with the optimal TVO price.

The second reward function we have defined is

| (50) |

where is an hyper-parameter of the PPO, while is a proxy of the residual option price defined by

| (51) |

with the BS optimal strategy (28) calculated in the state . In this form the agent actions are hidden inside the term used to compute the TVS forward curve defined by Equation 31. In this case, the reward function does not suffer of nil values for : the RL agent always gets a feedback from the environment for its choices. The hyper-parameter plays the role of a discount factor in the sense that, as approaches to zero, the RL agent will tend to maximize immediate rewards while neglecting possible larger rewards in the future. If we take the cumulative reward per episode and set the PPO parameters666We refer to [23] for a more detailed description for the generalized advantage estimation parameter . we obtain

| (52) |

which is equal to the intrinsic value of the option. This result does not depend on the definition of , but we conjecture that the closer is to the value function, the easier the agent is in learning.

Thus one can train the agent choosing the optimal value for , and then run, as test phase, a Monte Carlo simulation with and the optimized fixed, where, if the agent has learnt , the average of ) along different episodes will match the optimal undiscounted price of the derivative contract on the TVS.

In the OpenAI Baselines implementation of the PPO, the agent policy is parameterized again by a neural network; as for the previous method we have chosen an FFNN. In particular with PPO we deal with a stochastic policy whose functional form is a multivariate diagonal Gaussian distribution where the mean is the output vector of the FFNN and the log-standard deviation is an external parameter

| (53) |

As one can observe, is state-independent, but it is reduced as the number of the PPO update iterations increases. The idea is that the log-standard deviation will be higher at the beginning of the training phase in order to guarantee a good exploration of the action space while it will be lower at the end to avoid too much noise in the proximity of the optimal policy.

The fact that the PPO implementation exploits a stochastic policy ensures us a better exploration of the action space than with the previous approach. Moreover, the algorithm tries to learn an approximator of the on-policy value function as control variate for the training phase. This approximator is an FFNN with the same architecture as the one for the policy.

5 Numerical Investigations

Here we present the numerical results obtained with our proposed methods. We focus our analysis on a European call option on a TVS with the following product details

Moreover without loss of generality we consider the case of a completely free allocation strategy . The extension to the constrained case is easy.

It is our aim to investigate the control problem under non-trivial dynamics like the local volatility one where the volatility of the risky asset is also a function of the state. By looking at the HJB equation (43), we expect that the volatility versor will play a role in finding the optimal solution, giving rise to a non-trivial strategy.

Although in Section 3.3 we have proved that under the Black and Scholes model the Equation 28 solves the control problem, we want to take advantage of this a priori solution as a benchmark to gather evidence on the robustness of our Reinforcement Learning approach and to check if our analytical result is correct. Moreover, we use the BS model as numerical laboratory to perform fine-tuning tests for the RL algorithms hyper-parameters and analyze how they impact the final results and performances.

We recall that in both the algorithms we parameterize the agent policy with an FFNN; thus this is completely characterized by the following hyper-parameters: number of hidden layers, number of neurons per hidden layer, activation function per hidden layer. This is due to the fact that in this Reinforcement Learning problem the number of the input neurons is equal to the state space dimension (47), while the number of the output ones coincides with the action space dimension (46). It is well known in the literature that neural networks give better performances in the training phase if the input data are well normalized [25, 22]. Thus we choose as state the following normalized block

| (54) |

where is the forward curve vector of the risky assets from to . In Equation 54 we have chosen as Markovian state the martingale term of the securities dynamics. In this way we have that in the input block the variables have the same order of magnitude.

5.1 Black and Scholes: Hyper-Parameters Fine Tuning

We use the BS environment as toy model to understand which parameters of the RL algorithm play key roles in the training and testing phase. Our first approach has been the direct policy one since it represents a natural way to tackle the problem: since our goal is to find the allocation strategy that maximizes the option price, we update the FFNN weights following the gradient direction of the loss function defined in Equation 48.

We try to investigate the following hyper-parameters: the FFNN architecture, in particular which feature between the depth and the width of the network is more important, the activation function and the learning rate of the optimizer. Moreover, we compare the performances of two well-known optimizers in Machine Learning literature: Nadam [9] and RMSprop [15]. Since we deal with a free allocation strategy that can assume negative values, we have chosen among the wide variety of activation functions the tanh and the elu. In this way, we can analyze the performance of a saturating activation function and a non-saturating one. Firstly we have performed a grid search on the learning rate starting value and we have found a good choice in terms of speed of learning and avoiding over-fitting.

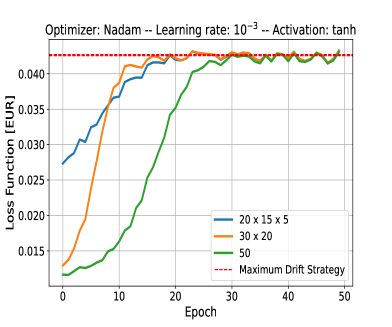

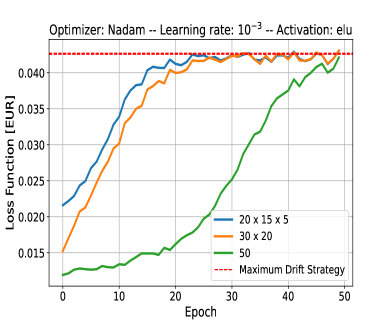

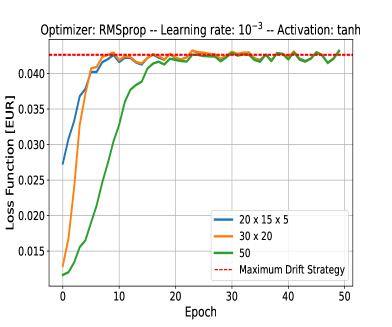

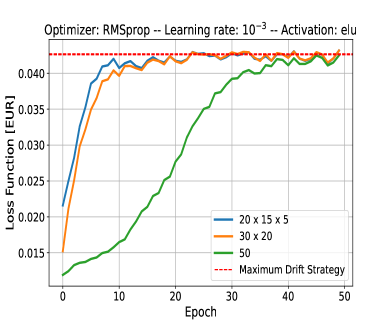

In Figures 3 and 2 we present the learning curves of our fine-tuning tests for the RMSProp and the Nadam respectively. The three lines of each plot display the learning curves for different FFNN architectures: a one hidden layer network with 50 neurons, a 2 hidden layers with 30 and 20 neurons respectively, and a deeper one with three layers with 20, 15, and 5 neurons. Each learning curve is compared with the optimal option price (red dotted line) that we have computed with the closed form solution we have derived for the BS model in Section 3.3. We can see that all the learning curves converge to our expected price, providing a numerical demonstration of our theoretical result. More deeply, from the plots we observe that the RMSprop optimizer outperforms the Nadam. Moreover, the tanh activation function seems to be more preferable than the non-vanishing elu. However, more importantly, we have evidence that a deeper architecture of the neural network outperforms the shallow one. All the learning curves we have presented are the best-in-sample results, in terms of performance, of four runs with different random starting guesses for the hidden weights . This procedure is necessary since the objective function is not convex.

We take the network with tanh from RMSprop as the best optimized network, and we run a Monte Carlo simulation with never-seen scenarios to check if the agent overfits the new data.

| Method | TVO price [EUR] |

|---|---|

| Analytical Solution | |

| Direct policy RL |

We report the results in Table 1: the RL price is compatible with the closed formula price. Thus the RL agent did not overfit the data during the training phase.

We will take advantage of those fine-tuning results to tackle the local volatility problem.

5.2 Local Volatility Dynamics

In this section, we study the TVS control problem assuming a local volatility model for the dynamics of the risky assets. Thus in this case we have a diffusive term in Equation 15 that is a deterministic function both of time and state, i.e. the spot price, . This additional dependency of volatility makes the problem of finding the optimal strategy non-trivial; in fact if we consider the whole securities smiles then the second-order term in the HJB equation (43) is not zero and thus a closed formula for is not available anymore. Because of that, one must resort to numerical techniques to recover the problem solution. Unlike the BS model where the strategy depends only on time, in LV dynamics there is no unnecessary information provided by the state block in Equation 47 to take the optimal action. Here we consider the same market data (, and ) as in the Black and Scholes environment to study how the optimal solution changes with the dynamics model.

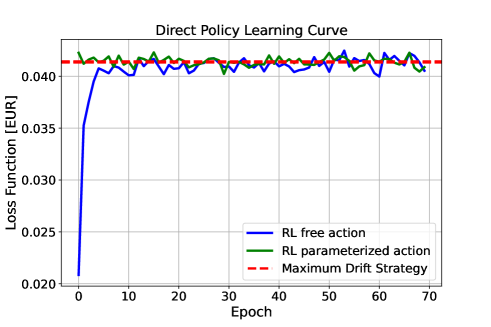

Our first way to tackle the problem is to exploit the results obtained in the BS case. Thus we train by direct policy algorithm a deep neural network with tanh activation function and a RMSprop optimizer. We report in Figure 4 the corresponding learning curve (blue line). From this, we observe that the network has learnt some good policy since the curve grows as the number of training epochs increases until it saturates at a certain value. To try to measure the performance of the policy selected by the agent, we can build a näif strategy called “baseline”. By looking at the Markovian projection in (20)-(21) and the first term in the HJB (43), a natural choice for the baseline is to maximize the TVS local drift. In other words this coincides by applying the path-wise the Black and Scholes solution of Equation 28; since here we deal with a free allocation strategy, we can simply use our analytical result (36). In the same Figure 4 we report the 99% confidence interval of the MC price obtained with the maximum drift baseline as two red-dashed lines. As we can see, the optimized loss function is compatible with the baseline price. Following the theoretical result of the HJB equation, we can assert that the agent has learnt a sub-optimal policy. Since we LV model differs from the BS one for a corrective term in the HJB (43), we expect that the optimal solution in the LV framework will be in a close region of the maximum drift strategy. Thus we train another agent with the direct policy learning by parameterizing its action with the baseline strategy and choosing a smaller learning rate of . With this parameterization, at each observational time the risky allocation strategy is obtained by summing the network output with the Equation 36. Even in this case, the corresponding learning curve (green line in Figure 4) is stuck in the maximum drift strategy. The first possible reason for this behaviour is that the learning strategy of the direct policy approach is too simple for the learning task. The second interpretation is that the volatility versor in the HJB does not affect significantly the optimum location since it is a second-order term and it is lost in the MC error.

Because of that, we change the learning strategy by adopting a more sophisticated one: the PPO algorithm. The big advantage of PPO is that, in addition to the policy, a guess of the value function in Equation 43 is also computed by a parameterization through an FFNN. As for the direct policy approach, we use the BS environment to fine-tune the PPO hyper-parameters. Again we experienced that deeper FFNNs outperform shallow ones and tanh is the most preferable. We report for completeness the values of the other PPO hyper-parameters, for the description of which we refer to [24]: learning rate , , , , and mini-batch size of 2048 episodes.

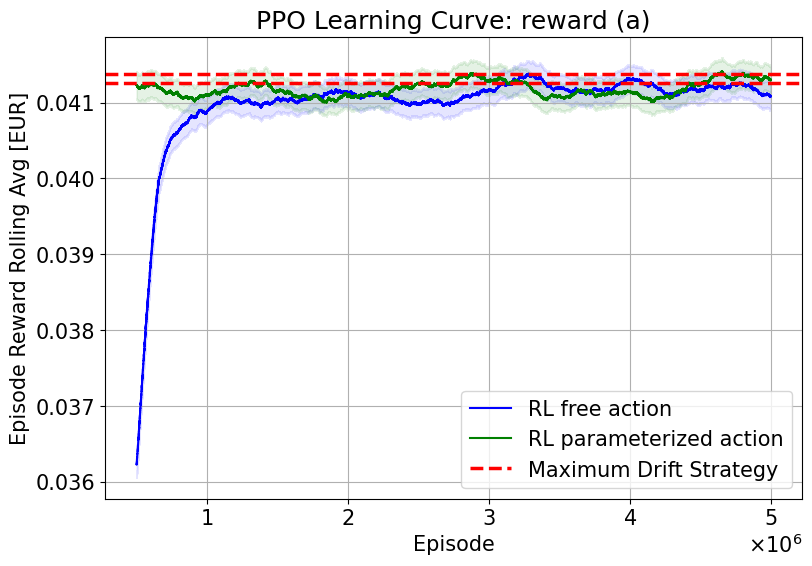

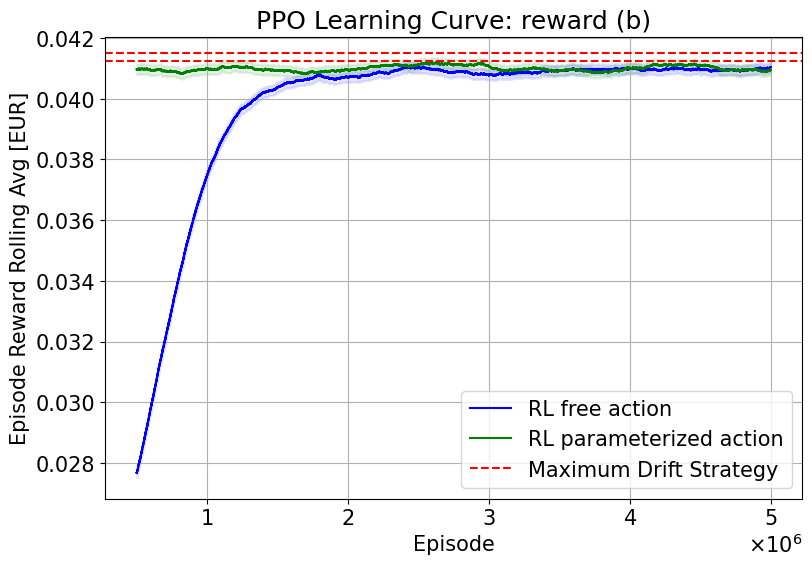

We have trained a 5 layer FFNN with 8 neurons each with the PPO algorithm in two different environments: one environment generates the reward according to Equation 49, while the other exploits the reward function (50) where we set as discount factor to make the agent prefer immediate rewards. Again, for both environments, we train two different agents: one whose action is given by Equation 46, while the other implements the action parameterization with the baseline.

We report in Figure 5 the results of the learning curves. In all the PPO cases, the trained agents seem to be stuck in the sub-optimal maximum drift strategy policy. For the case of the immediate reward function (Figure 5 on the right), we have that the learning curves converge to a saturation value that is not compatible with the baseline price; this is due to the fact that with we introduce a bias in the problem. Because of that, we need to run a test MC simulation with freezed agents and to obtain a result to compare with the baseline price. We report the results in Table 2. The Reinforcement Learning agents we have trained with PPO give all prices compatible with the baseline one.

| Method | TVO price [EUR] |

|---|---|

| Baseline | |

| RL free (a) | |

| RL parameterized (a) | |

| RL free (b) | |

| RL parameterized (b) |

6 Conclusion and Further Developments

In this paper, we described a non-trivial control problem related to derivative contracts on target volatility strategies. In particular, we have considered a bank selling a call option to a fund manager as protection on the capital invested on the TVS. We showed how the presence of different funding costs coming from hedging the risky assets underlying the TVS, obliges the bank to solve a stochastic optimal control problem to price the protection. This is due to the fact that the bank strategy is not self-financing. This kind of control problem is hard to solve because here the control process affects both drift and diffusive coefficients of the controlled process. Despite its complexity, our first contribution is the derivation of a closed form solution of the control problem in a Black and Scholes framework, which could represent a useful tool for practitioners since it outperforms intuitive trading strategies. We have derived this solution in two different ways: first by applying the Gyöngy Lemma and then by writing the Hamilton-Jacobi-Bellman equation. We numerically studied the problem in the more general local volatility model where the solution is not available and thus an numerical investigation is needed. We tackled the problem by means of the novel Reinforcement Learning techniques, by both the direct policy learning and the proximal policy optimization one. We used the BS model, where the solution is a priori known, as benchmark to perform a series of fine-tuning of the RL algorithm hyper-parameters, such as the artificial neural network architecture. We have tested in the LV model the two RL approaches and from our simulations we have evidence that nor the simple direct policy learning strategy nor the sophisticated PPO are able to outperform our analytical solution applied path-wise. Thus our analytical result for the Black and Scholes model seems to be a good proxy solution also for the local volatility one.

This result seems to be a local optimum from the HJB equation of the problem, since in the LV model the volatility versor term should influence the RL agent actions. Thus natural development of this work could be to solve the HJB numerically in low dimension in order to check why such sophisticated algorithms are not able to find the global optimum of the problem, or to understand which are the key elements of the problem, such as market data or the payoff function, that can give rise to a solution far from the intuitive one.

References

- [1] S. Albeverio, S. Victoria and K. Wallbaum “The volatility target effect in investment-linked products with embedded American-type derivatives” In Investment Management and Financial Innovations 16, 2019, pp. 18–28

- [2] F. Black and M. Scholes “The Pricing of Options and Corporate Liabilities” In Journal of Political Economy 81 University of Chicago Press, 1973 DOI: 10.2307/1831029

- [3] L. Chew “Target Volatility Asset Allocation Strategy”, 2011

- [4] Y. Deng, F. Bao, Y. Kong, Z. Ren and Q. Dai “Deep Direct Reinforcement Learning for Financial Signal Representation and Trading” In IEEE Transactions on Neural Networks and Learning Systems 28.3, 2017, pp. 653–664 DOI: 10.1109/TNNLS.2016.2522401

- [5] E. Derman and I. Kani “Riding on a Smile” In Risk 7, 1994, pp. 32–39

- [6] P. Dhariwal, C. Hesse, O. Klimov, A. Nichol, M. Plappert, A. Radford, J. Schulman, S. Sidor, Y. Wu and P. Zhokhov “OpenAI Baselines” In GitHub repository GitHub, https://github.com/openai/baselines, 2017

- [7] G. Di Graziano and L. Torricelli “Target Volatility Option Pricing” In International Journal of Theoretical and Applied Finance 15.1, 2012

- [8] L. Di Persio, L. Prezioso and K. Wallbaum “Closed-End Formula for options linked to Target Volatility Strategies”, 2019 URL: https://ideas.repec.org/p/arx/papers/1902.08821.html

- [9] T. Dozat “Incorporating nesterov momentum into adam” In International Conference on Learning Representations, 2016

- [10] B. Dupire “Pricing with a Smile” In Risk Magazine, 1994, pp. 18–20

- [11] S. Gabrielli, A. Pallavicini and S. Scoleri “Funding Adjustments in Equity Linear Products” In Risk, 2020

- [12] M. Grasselli and J.. Romo “Stochastic Skew and Target Volatility Options” In Journal of Futures Markets 36.2, 2016, pp. 174–193

- [13] I. Gyöngy “Mimicking the one-dimensional marginal distributions of processes having an ito differential” In Probability Theory and Related Fields 71.4 Springer ScienceBusiness Media LLC, 1986, pp. 501–516 DOI: 10.1007/bf00699039

- [14] I. Halperin “QLBS: Q-Learner in the Black-Scholes(-Merton) Worlds” In The Journal of Derivatives 28 Pageant Media US, 2020, pp. 99–122 DOI: 10.3905/jod.2020.1.108

- [15] G. Hinton, N. Srivastava and K. Swersky “Neural networks for machine learning lecture 6a overview of mini-batch gradient descent” In Cited on 14.8, 2012, pp. 2

- [16] A. Hocquard, S. Ng and N. Papageorgiou “A constant volatility framework for managing tail risk” In The Journal of Portfolio Management 39.2, 2013, pp. 28–40

- [17] Y. Kim and D. Enke “A dynamic target volatility strategy for asset allocation using artificial neural networks” In The Engineering Economist 63.4, 2019, pp. 273–290

- [18] P.. Kolm and G. Ritter “Dynamic Replication and Hedging: A Reinforcement Learning Approach” In The Journal of Financial Data Science 1.1 Institutional Investor Journals Umbrella, 2019, pp. 159–171 DOI: 10.3905/jfds.2019.1.1.159

- [19] F. Longstaff and E. Schwartz “Valuing American Options by Simulation: A Simple Least-Squares Approach” In Review of Financial Studies 14, 2001, pp. 113–47 DOI: 10.1093/rfs/14.1.113

- [20] S. Morrison and L. Tadrowski “Guarantees and Target Volatility Funds”, 2013

- [21] R. Perchet, R.. De Carvalho, T. Heckel and P. Moulin “Predicting the Success of Volatility Targeting Strategies: Application to Equities and Other Asset Classes” In The Journal of Alternative Investements 18.3, 2016

- [22] M. Puheim and L. Madarász “Normalization of inputs and outputs of neural network based robotic arm controller in role of inverse kinematic model” In 2014 IEEE 12th International Symposium on Applied Machine Intelligence and Informatics (SAMI), 2014, pp. 85–89 DOI: 10.1109/SAMI.2014.6822439

- [23] J. Schulman, P. Moritz, S. Levine, M: I. Jordan and P. Abbeel “High-Dimensional Continuous Control Using Generalized Advantage Estimation” In 4th International Conference on Learning Representations, ICLR 2016, San Juan, Puerto Rico, May 2-4, 2016, Conference Track Proceedings, 2016

- [24] J. Schulman, P. Wolski, P. Dhariwal, A. Radford and O. Klimov “Proximal Policy Optimization Algorithms”, 2017 arXiv:1707.06347 [cs.LG]

- [25] J. Sola and J. Sevilla “Importance of input data normalization for the application of neural networks to complex industrial problems” In IEEE Transactions on Nuclear Science 44.3, 1997, pp. 1464–1468 DOI: 10.1109/23.589532

- [26] R.. Sutton and A.. Barto “Reinforcement Learning: An Introduction” The MIT Press, 2018

- [27] Y. Xue “Target Volatility Fund: An Effective Risk Management Tool for VA?”, 2012