Spectrally negative Lévy risk model under mixed

ratcheting-periodic dividend strategies

SUN FUYUNa AND SONG ZHANJIEa

aSchool of Mathematics, Tianjin University, Tianjin 300350, China

ABSTRACT In this paper, we consider the mixed ratcheting-periodic dividend strategies for spectrally negative Lévy risk model, in which dividend payments can both be made continuously without falling and discretely at the jump times of an independent Poisson process. The expected net present value(NPV) of dividends paid up to ruin and the Laplace transform of the ruin time are obtained by using Lévy fluctuation theory. All the results are expressed in terms of scale functions. Finally, numerical results for Brownian motion with drift are given. KEYWORDS Expected net present value(NPV) of dividends; Ratcheting dividend strategy; Periodic dividend strategy; Spectrally negative Lévy process; Scale function; Laplace transform. MATHEMATICS SUBJECT CLASSIFICATION 91B30, 97M30, 60J75.

Address correspondence to Fuyun Sun, School of Mathematics, Tianjin University, Tianjin 300350, China; E-mail: sunfy@tju.edu.cn

Introduction

In actuarial risk theory, the Lévy risk models with barrier dividend strategy have been studied extensively, see, e.g. Loeffen (2008); Kyprianou and Loeffen (2010); Kyprianou, Loeffen, and Pérez (2012); Yin and Wen (2013); Yin, Shen, and Wen (2013); Yin, Wen, and Zhao (2014), among others. In reality, the reduction in the dividend rate may have a negative psychological impact on shareholders, which may lead to a decrease in earnings. In order to avoid the above situation, a ratcheting dividend strategy in risk theory was considered by Albrecher, Bäuerle, and Bladt (2018), where the dividend rate can never decrease. They obtained the expected value of the aggregate discounted dividend payments until ruin under a ratcheting strategy for a Lévy risk model. After that there are some recent papers on ratcheting dividend strategy in different risk models Zhang and Liu (2020); Albrecher, Azcue, Muler (2020a,b); Song and Sun (2021).

However, for companies, the board should check the balance firstly on a periodic basis and then decide the dividend payments paid to the shareholders, turning out either continuous payment streams or one-off dividend payments at discrete time points. Hence the board of the company may choose a combined dividend strategy. Recently, mixed strategies have been studied by a lots of contributors in vary risk models, such as Avanzi, Tu, and Wong (2020b) studied hybrid continuous and periodic barrier strategies in the dual model, Liu, Chen, and Hu (2020) considered threshold and periodic dividend strategies in a dual model with diffusion, Avram, Pérez, and Yamazaki (2018) studied Parisian reflection below and classical reflection above in spectrally negative Lévy processes and other papers Zhang and Han (2017); Dong and Zhou (2019); Avanzi, Tu, and Wong (2016); Avanzi et al. (2017); Pérez and Yamazaki (2018), and so on. Motivated by the board’s reasonable behaves and these works, we consider in this paper the spectrally negative Lévy case with mixed ratcheting-periodic dividend strategy, which is a combination of continuous ratcheting dividend strategy and discrete periodic dividend strategy. The ratcheting dividend rate we considered during the lifetime can be increased once to a higher level from the original level, like in Albrecher, Bäuerle, and Bladt (2018). The periodic dividend strategy we considered can be portrayed as that the surplus process is pushed down to a preset barrier whenever it is above the barrier at the periodic dividend decision times.

The expected net present value(NPV) of dividends paid up to ruin and the Laplace transform of the ruin time have been extensively studied in the literature by using the resolvent measure, the Laplace transform of the occupation times and other fluctuation identities. We also obtained the numerical optimal barriers value under the special model, because the analysis solution of the optimal barriers is more complicated. For more studies on the expected NPV of dividends and the Laplace transform of the ruin time, see Yin and Yuen (2011); Shen, Yin, anf Yuen (2013); Dong, Yin, and Dai (2019); Avanzi, Lau, and Wong (2021); Avanzi, Tu, and Wong (2020a); Li et al. (2021), etc.It is worth mentioning that, ratcheting-periodic dividend strategy can reduce to the pure periodic barrier strategy(see e.g. Avram, Pérez, and Yamazaki (2018)) and to the pure ratcheting dividend strategy(see e.g. Albrecher, Bäuerle, and Bladt (2018)) under certain conditions.

The rest of the paper is organized as follows. In Section 2, we list and recall some preliminaries: spectrally negative Lévy risk processes in Subsection 2.1, some associated scale functions in Subsection 2.2, Lévy risk models with periodic barrier strategy in Subsection 2.3, and the definition of the ratcheting-periodic dividend strategy and the construction of the corresponding controlled surplus process in Subsection 2.4. The expressions of the expected NPV of dividends up to ruin and the Laplace transform of the ruin time are discussed in Sections 3 and 4, respectively. Section 5 shows the analysis with Brownian motion. A conclusion is given in Section 6.

Preliminaries

Spectrally negative Lévy processes

Let us consider a spectrally negative Lévy process , i.e. a Lévy process with only negative jumps. We assume that and the drift of this process is positive. For , we denote by the law of when it starts at . Accordingly, I shall write for the associated expectation operator. Throughout this work define the Laplace exponent , which is finite for at least all , by the Lévy-Khintchine formula(see e.g. Kuznetsov, Kyprianou,and Rivero (2013); Chan, Kyprianou, and Savov (2011); Kyprianou, Loeffen,and Pérez (2012)):

where , and is a measure on called the Lévy measure of that satisfies

It is well-known that has paths of bounded variation if and only if and ; in this case, can be written as , where

| (2.1) |

and is a driftless subordinator. Note that necessarily , since we have ruled out the case that has monotone paths; its Laplace exponent is given by

Throughout the paper, we assume that

Review of scale functions

Let , and , , , . In this paper, We also assume that (well defined in equation ) for ensuring both processes and have positive drift. To avoid confusion of the notations, we assume that denotes the Laplace exponent of process for the rest of the paper. Denote by the largest root of the equation , , . We now recall the definition of the -scale function . For each , there exists a continuous and increasing function , which is called the -scale function of the process . The -scale function and some related functions of the process are defined in such a way:

and for and ,

Noting that for , we then have , , and , respectively, for .

Define also

and its partial derivative with respect to :

In particular, for , and for ,

We give some more notations, which will be used later: for any measurable function ,

In particular, we let, for , and ,

which are taken from Pérez and Yamazaki (2018). Note that similar generalized scale functions are also introduced in Avram, Pérez, and Yamaziki (2018).

Define also for , and ,

Note in particular that for ,

| (2.2) |

The corresponding functions for the process will be denoted by , , , , , , , , and , respectively, and shall be the corresponding largest root of equation .

Lévy risk models with periodic barrier strategy

Firstly let be an increasing sequence of jump times of an independent Poisson process with rate . Whenever the observed surplus level at is larger than , the excess value will be paid off as dividend. We construct the Lévy risk model with periodic barrier strategy as follows. Specifically, we have:

where:

| (2.3) |

here and throughout, let . The process then jumps downward by so that . For , we have , and . The process can be constructed by repeating this procedure.

Suppose is the cumulative amount of periodic dividends until time . Then, we have:

| (2.4) |

with

where can be constructed inductively by and:

Similar to the construction method of process , we have the process , where denotes the corresponding cumulative periodic dividends until time .

For the processes and , define for a fixed the first passage times:

with the usual convention .

Mixed ratcheting-periodic dividend strategies

In this subsection, motivated by those works Albrecher, Bäuerle, and Bladt (2018), Liu, Chen, and Hu (2020) and Pérez and Yamazaki (2018), we propose a mixed dividend strategy, which contains a ratcheting dividend strategy and a periodic dividend strategy. With the mixed dividend strategy, we modify the process as follows. Whenever the observed surplus level at (well defined in subsection 2.3) is larger than , the excess value will be paid off as dividend. During the internal times , dividends are paid at a fixed constant rate until the first time when the surplus process hits a predetermined barrier and from this point the dividend rate will be ratcheted to () from a fixed constant and stays at this higher level until ruin. In order to give the mathematical descriptions of the modified surplus process , starting from , under the mixed ratcheting and periodic dividend strategies, we define an auxiliary process as follows:

where . Then the modified process is given by:

where

| (2.5) |

The process then jumps downward by so that . For , we have , and . The process can be constructed by repeating this procedure.

Without loss of generality, we set . Note that is not a dividend decision time, therefore even if . Then we have

| (2.6) |

with

where can be constructed inductively by and

For the process , define for a fixed the first passage times:

with the usual convention .

Analyzing these processes , , , , and , we can obtain the following lemma.

Lemma 1.

| (2.7) | |||

| (2.8) | |||

| (2.9) |

The expected net present value of dividends

In this section, we present the expression of the expected NPV of dividends up to ruin via scale functions. In our assumption, the inter-dividend-decision times , are i.i.d. and exponentially distributed with mean . Define the expected NPV of dividends paid up to ruin by

where is the ruin time of the process well defined in , with . Note that .

According to our understanding and experience of the barrier dividend strategy, is different in the intervals , and as both and are the ratcheting-periodic barriers. Then for easy identification, we denote by for , for and for , which will be given in Theorems 4–6.

Before stating Theorems 4–6, we first present two technical lemmas, which will be used to the proofs later. By directly applying Corollaries and in the works of Pérez and Yamazaki (2018), we obtain the first Lemma 2:

Lemma 2.

For , and , we have

| (3.1) |

and

| (3.2) |

Using the Theorems , and in Pérez and Yamazaki (2018), we obtain the following Lemma 3.

Lemma 3.

For and , we have

| (3.3) | |||

| (3.4) | |||

| (3.5) |

Theorem 4.

For , the expected NPV of dividends paid up to ruin is given by

| (3.6) |

Proof. When the initial value , dividends caused by ratcheting strategy are paid at rate until ruin. That means the whole modified risk model under mixed dividend strategy can be considered as the process (see also equation (2.9) in Lemma 1). But the total dividend amount of risk model includes the dividend amount generated by ratcheting strategy. Then we have

| (3.7) |

Substituting equations and in Lemma 2 into , we have . This ends the proof.

Theorem 5.

For , the expected NPV of dividends paid up to ruin is given by

| (3.8) |

where

Proof Consider this case , we discuss it in two ways. When the modified process does not reach before ruin, we can take it as process (see also equation in Lemma 1), where the dividends generated by the ratcheting strategy until ruin . On the other hand, the modified process reaches before ruin. In this case, the surplus can be described by equations and . Then for this case we apply the strong Markov property at that point (up through ) in time, from which the process starting at dynamics change to the process starting at , which means ratcheting dividend rate changes to from . We thus have

| (3.9) |

By virtue of in Lemma 1, we get the first two terms of equation

| (3.10) |

The last equation is derived from - in Lemma 3. Applying equations and Lemma 2 to equation , we have .

Let in equation , we then have the constant . The proof is end.

Theorem 6.

For , the expected NPV of dividends paid up to ruin is given by

| (3.11) |

where

Proof Consider this case , we discuss it in two ways. When the modified process does not reach before ruin, we can take it as process (see also equation in Lamma 1), where the dividends generated by the ratcheting strategy until ruin . On the other hand, the modified process reaches before ruin. Similar to the case of , in this case we also apply the strong Markov property at that point (up through ) in time, from which the process or starting at dynamics change to the process with mixed ratcheting-periodic dividend strategy starting at , which is the situation we discussed in the previous theorem. We thus have

| (3.12) |

By virtue of and in Lemma 3, we get the equation .

From equations , we have and =1. Letting in equation and substituting these equations, we obtain the constant . The proof is end.

Let denote the expected NPV of dividends only under the periodic barrier strategy for spectrally negative Lévy processes. By taking and in Theorems 4-6, we have the following Corollary.

Corollary 7.

For , and , we have

Corollary 7 was used in Noba et al. (2018) to show the optimality of a periodic barrier strategy under the assumption that the Lévy measure has a completely monotone density.

Let denote the expected NPV of dividends only under the ratcheting dividend strategy(single-rise) for spectrally negative Lévy processes. By taking in Theorems 4-6, we have the following result, which coincides with the result in Theorem of Albrecher, Bäuerle, and Bladt (2018).

Corollary 8.

For and , we have

Proof It is obvious that . Next we aim to calculate this limit.

Note that for , and ,

According to the definition of , we have

as . Then

as .

From above equations and equations , , , we have

and

This ends the proof.

Remark 3.1.

By taking in equation and taking in equation , we obtain

This shows that for any spectrally negative Lévy processes , with respect to the initial value , , even if has paths of unbounded variation. The continuity property may be a necessary condition for existing of the optimal mixed strategy, if the mixed optimal strategy exists under some certain assumptions.

Laplace transform of the ruin time

In this section, we consider the distribution of the ruin time , under a ratcheting-periodic strategy. For a fixed , define

as the expected NPV of a payment of at the ruin time, and the Laplace transform of the probability density function of . We discuss how to calculate as follows for three cases , and , respectively.

Theorem 9.

For , , and , we have

Proof Consider the first case , according to the Lemma 1, it is easy to obtain that

| (4.1) |

where the last equation is obtained from equation in Lemma 2.

For the case , according to the law of total probability and the strong Markov property, we have

| (4.2) | ||||

| (4.3) |

where is obtained by equation when and the last equation is obtained by using Lemma 3.

Similarly, for the last case , we have

| (4.4) | ||||

| (4.5) |

where is obtained by in equation . This proof is end.

Remark 4.1.

Noting that by taking in equations -, we obtain that for , as .

Let , , denote the Laplace transform of the ruin time for the spectrally negative Lévy processes with the ratcheting dividend strategy(single-rise). By taking in Theorems 9, we derive the expression of Laplace transform , which can reduce the results in Section of Albrecher, Bäuerle, and Bladt (2018).

Corollary 10.

For and , we have

Numerical illustrations

In this subsection, we give some graphs, under the special cases of the Brownian motion with drift, to show the effects of some parameters on the expected NPV of dividends up to ruin and the Laplace transform of the ruin time.

Let where is the initial surplus, is a constant drift, and denotes a standard Brownian motion. The Brownian risk model has also been considered by Albrecher, Bäuerle, and Bladt (2018). It is worth mentioning that the expected gain per unit time should be positive( i.e. ). In the diffusion case the scale functions of and are given by

where

Note that, in this case . For , by the define of and , we have

By some algebraic manipulations, for , we have

Analysis with the expected NPV of dividends up to ruin

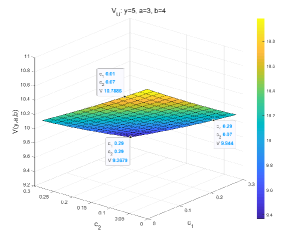

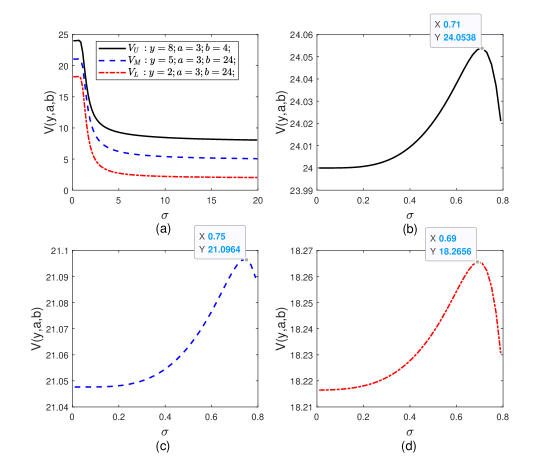

In this section, we reveal the impact of various parameters on the expected discounted cumulative dividend function. In order to investigate that, in the following analysis, unless otherwise specified, the basic parameter settings are as follows: , , , , , .

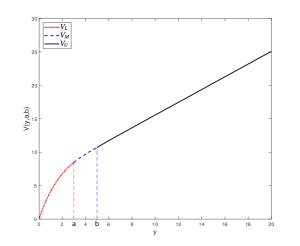

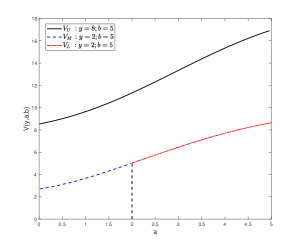

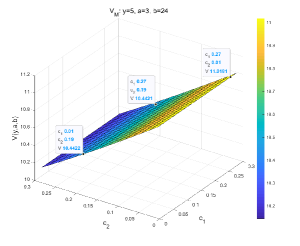

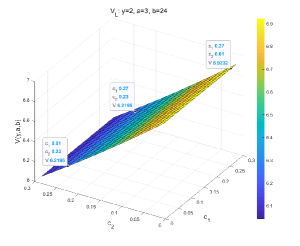

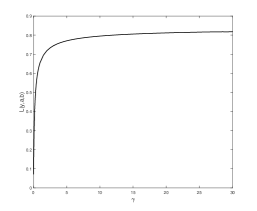

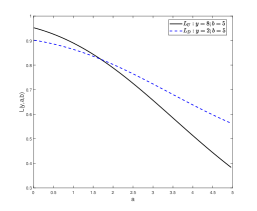

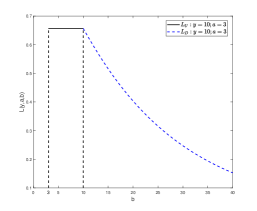

For finding the influence, in Figures 1-4, we show the curves of as functions of , , , , and , respectively. First, for fixed ratcheting-periodic barriers and , we find from Figure 1(a) that the expected NPV of dividends paid up to ruin increases as the initial value increases, which is an intuitive conclusion. When the initial surplus increases, the surplus process is more likely to be above the ratcheting-periodic barriers, and is more likely to survive longer, and then there may be more dividend payments paid off. Meanwhile, we see that is continuous obviously in , which coincides with Remark 3.1. Figure 1(b) shows a result that be not intuitively understood: For fixed and , increases with respect to the periodic dividend barrier , which is also a very important discovery. We can explain this phenomenon as follows: As increases, the ruin time may be delayed, which result that the potential dividend at later times increases. From that we also find the optimal periodic value . This implies that under certain circumstances, in order to maximize , we should let the periodic dividend barrier be equal to the ratcheting dividend barrier(i.e. ). In fact, Song and Sun (2021) have been studied this situation in a dual risk model. In view of , we want to find the optimal ratcheting value , which is corresponding to the maximum value of for fixed the values of other parameters except parameter . Then we plot curves for as a function of the ratcheting barrier in Figure 2.

From Figure , we see that the value of is a constant when the initial value is greater than . This is consistent with Theorem 4: the value of has nothing to do with . Figure 2 also shows that: is increasing in the ratcheting dividend barrier when is lower than and converges to a nonzero constant when tends to infinity. Then the optimal periodic dividend barrier . However it is unrealistic to set for nondecreasing dividend rate, so in the light of the result of Figure 2, we can find the approximate value of optimal ratcheting barrier within an acceptable error range.

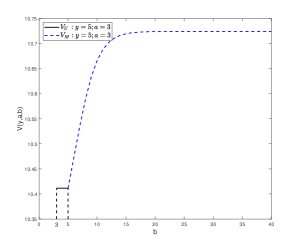

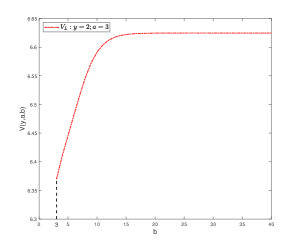

As can be seen in Figure 3, for three different cases, all of are decreasing functions of and , respectively. Meanwhile, we find from the remarked values of that the influence of and on is relatively smaller. For this result, we think the optimal barriers and do not make sense. Conversely, we can choose the value of and depending on the market condition and the insurance company’s own needs.

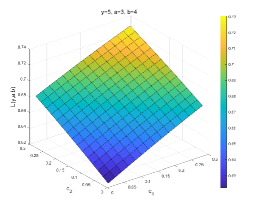

Next, we describe the overall trend of as the market volatility changes in Figure 4(a). On one hand, we find that is not a monotone function of and converges to a nonzero constant as . This shows that even when the market volatility is very high, can remain at a relatively stable value. On the other hand, for making a more precise conclusion, we plot as functions of in Figure 4(b-d). From that we see for every fixed , , and , that is a concave function of , which means that first increases and then decreases in . From the remarked values in Figure 4(b-d)(i.e. the corresponding optimal value ), the value under these three cases is different. This indicates that depends on other parameters. Therefore, we can control other controllable parameters to make close to , so as to obtain the maximum value of . Finally, as the process becomes deterministic, but , which interprets that no turbulent market is not optimal and a smaller market volatility can increase .

Analysis with the Laplace transform of the ruin time

In this subsection, we focus on the Laplace transform of the ruin time. Also set the same basic parameter settings with previous subsection 5.1. In Figure 5, we characterize the effects of the main parameters , , , , and on the Laplace transform of the ruin time .

First, we show in Figure 5(a) that the curve of as a function of the inter-dividend-decision times parameter when , , and , in which we denote by . We find that is a monotonically increasing and convex function as . There are two factors that bring about this phenomenon. On one hand, smaller means that more dividend decision times per unit time, which will lead to ruin earlier. On the other hand, when is larger, dividend payments may become small, which will lead to the ruin time delayed.

Next, in Figure 5(b-c), we plot function with respect to barriers and under two different cases and . From Figure 5(b), we know that both and decrease as increases. We see also from Figure 5(c) that is a non-increasing function as . We can explain these phenomena as follows. Larger or means that small potential dividends will be paid off, therefore ruin postpones. In the end, we plot as a function of in Figure 5(d). As can be seen from Figure 5(d), one can observe that is a decreasing function of both and . When or is larger, more potential dividends will be paid off, thus the ruin time will be prolonged.

Conclusions

In this paper, we studied dividend problems and ruin problems for spectrally negative Lévy risk model with ratcheting-periodic dividend strategy. Dividend payments can both be made discretely at the jump times of an independent Poisson process and continuously without falling. The precise expressions of the expected NPV of dividends paid up to ruin and the Laplace transform of the ruin time are derived by using Lévy fluctuation theory and are written concisely in terms of scale functions.

Finally, we describe the two functions, the expected NPV of dividends and the Laplace transform of the ruin time, under Brownian risk model, a special spectral negative Lévy process. The optimal dividend value and the minimum Laplace transform value and the corresponding optimal barriers in the fixed settings are obtained. The two results are consistent as follows: and . If we fixed the two barriers , , and other parameters, the optimal and should be . This indicates that if we do not consider the factor the investors are unwilling to see a decline in the dividend rate, the optimal mixed dividend strategy is pure periodic dividend strategy.

References

Albrecher, H., Azcue, P., Muler, N. 2020a. Optimal ratcheting of dividends in a Brownian risk model. arXiv:2012.10632.

Albrecher, H., Azcue, P., Muler, N. 2020b. Optimal ratcheting of dividends in insurance. SIAM J. Control Optim. 58, 1822–1845.

Albrecher, H., Bäuerle, N., Bladt, M. 2018. Dividends: From refracting to ratcheting. Insur. Math. Econ. 83, 47–58.

Avanzi, B., Lau, H., Wong, B. 2020a. Optimal periodic dividend strategies for spectrally positive Lévy risk processes with fixed transaction costs. Insur. Math. Econ. 93, 315–332.

Avanzi, B., Lau, H., Wong, B. 2021. On the optimality of joint periodic and extraordinary dividend strategies. Eur. J. Oper. Res. 295, 1189–1210.

Avanzi, B., Pérez, J.L., Wong, B., Yamazakid, K. 2017. On optimal joint reflective and refractive dividend strategies in spectrally positive Lévy models. Insur. Math. Econ. 72, 148–162.

Avanzi, B., Tu, V., Wong, B. 2016. On the interface between optimal periodic and continuous dividend strategies in the presence of transaction costs. ASTIN Bull. 46, 708–745.

Avanzi, B., Tu, V., Wong, B. 2020b. Optimality of hybrid continuous and periodic barrier strategies in the dual model. Appl. Math. Optim. 82, 105–133.

Avram, F., Pérez, J.L., Yamazaki, K. 2018. Spectrally negative Lévy processes with Parisian reflection below and classical reflection above. Stoch. Process. Their Appl. 128, 255–290.

Chan, T., Kyprianou, A.E., Savov, M. 2011. Smoothness of scale functions for spectrally negative Lévy processes. Probab. Theory Relat. Field 150, 691–708.

Dong, H., Yin, C., Dai, H. 2019. Spectrally negative Lévy risk model under Erlangized barrier strategy. J. Comput. Appl. Math. 351, 101–116.

Dong, H., Zhou, X. 2019. On a spectrally negative Lévy risk process with periodic dividends and capital injections. Stat. Probab. Lett. 155, 108589.

Kuznetsov, A., Kyprianou, A.E., Rivero, V. 2013. The theory of scale functions for spectrally negative Lévy processes. Springer Berlin Heidelberg, Berlin, Heidelberg. pp. 97–186.

Kyprianou, A.E., Loeffen, R. 2010. Refracted Lévy processes. Annales de l’Institut Henri Poincaré, Probabilités et Statistiques 46, 24–44.

Kyprianou, A.E., Loeffen, R., Pérez, J.L. 2012. Optimal control with absolutely continuous strategies for spectrally negative Lévy processes. J. Appl. Probab. 49, 150–166.

Li, P., Meng, Q., Yuen, K.C., Zhou, M. 2021. Optimal dividend and risk control policies in the presence of a fixed transaction cost. J. Comput. Appl. Math. 388, 113271.

Liu, Z., Chen, P., Hu, Y. 2020. On the dual risk model with diffusion under a mixed dividend strategy. Appl. Math. Comput. 376, 125115.

Loeffen, R. 2008. On optimality of the barrier strategy in de Finetti’s dividend problem for spectrally negative Lévy processes. Ann. Appl. Probab. 18, 1669–1680.

Noba, K., Pérez, J.L., Yamazaki, K., Yano, K. 2018. On optimal periodic dividend strategies for Lévy risk processes. Insur. Math. Econ. 80, 29–44.

Pérez, J.L., Yamazaki, K. 2018. Mixed periodic-classical barrier strategies for Lévy risk processes. Risks 6, 33.

Shen, Y., Yin, C., Yuen, K.C. 2013. Alternative approach to the optimality of the threshold strategy for spectrally negative Lévy processes. Acta Math. Appl. Sin.-Engl. Ser. 29, 705–716.

Song, Z., Sun, F. 2021. The dual risk model under a mixed ratcheting and periodic dividend strategy. Commun. Stat. Theory Methods, 1–15.

Yin, C., Shen, Y., Wen, Y. 2013. Exit problems for jump processes with applications to dividend problems. J. Comput. Appl. Math. 245, 30–52.

Yin, C., Wen, Y. 2013. Optimal dividend problem with a terminal value for spectrally positive Lévy processes. Insur. Math. Econ. 53, 769–773.

Yin, C., Wen, Y., Zhao, Y. 2014. On the optimal dividend problem for a spectrally positive Lévy process. ASTIN Bull. 44, 635–651.

Yin, C., Yuen, K.C. 2011. Optimality of the threshold dividend strategy for the compound Poisson model. Stat. Probab. Lett. 81, 1841 C1846.

Zhang, A., Liu, Z. 2020. A Lévy risk model with ratcheting dividend strategy and historic high-related stopping. Math. Probl. Eng. 2020, 6282869.

Zhang, Z., Han, X. 2017. The compound Poisson risk model under a mixed dividend strategy. Appl. Math. Comput. 315, 1–12.