DOPE: Doubly Optimistic and Pessimistic Exploration for Safe Reinforcement Learning

Abstract

Safe reinforcement learning is extremely challenging–not only must the agent explore an unknown environment, it must do so while ensuring no safety constraint violations. We formulate this safe reinforcement learning (RL) problem using the framework of a finite-horizon Constrained Markov Decision Process (CMDP) with an unknown transition probability function, where we model the safety requirements as constraints on the expected cumulative costs that must be satisfied during all episodes of learning. We propose a model-based safe RL algorithm that we call Doubly Optimistic and Pessimistic Exploration (DOPE), and show that it achieves an objective regret without violating the safety constraints during learning, where is the number of states, is the number of actions, and is the number of learning episodes. Our key idea is to combine a reward bonus for exploration (optimism) with a conservative constraint (pessimism), in addition to the standard optimistic model-based exploration. DOPE is not only able to improve the objective regret bound, but also shows a significant empirical performance improvement as compared to earlier optimism-pessimism approaches.

1 Introduction

Constrained Markov Decision Processes (CMDPs) impose restrictions that pertain to resource or safety constraints of the system. For example, the average radiated power in a wireless communication system must be restricted due to user health and battery lifetime considerations or the frequency of braking or accelerating in an autonomous vehicle must be kept bounded to ensure passenger comfort. Since these systems have complex dynamics, a constrained reinforcement learning (CRL) approach is attractive for determining an optimal control policy. But how do we ensure that safety or resource availability constraints are not violated while learning such an optimal control policy?

Our goal is to develop a framework for safe exploration without constraint violation (with high probability) for solving CMDP problems where the model is unknown. While there has been much work on RL for both the MDP and the CMDP setting, ensuring safe exploration in the CRL setting has received less attention. The problem is challenging, since we do not allow constraint violation either during learning or deployment, while ensuring a low regret in terms of the optimal objective. Our aim is to explore a model-based approach in an episodic setting under which the model (the transition kernel of the CMDP) is empirically determined as samples from the system are gathered.

| Algorithm | Model | Reward | Constraint | Objective | Constraint | Empirical |

|---|---|---|---|---|---|---|

| Optimism | Optimism | Pessimism | Regret | Regret | Perf. | |

| OptCMDP | ✓ | ✗ | ✗ | - | ||

| OptCMDP-B | ✗ | ✓ | ✗ | - | ||

| AlwaysSafe | ✓ | ✗ | Heuristic | Unknown | 0 | ✗ |

| OptPess-LP | ✗ | ✓ | ✓ | 0 | ✗ | |

| DOPE | ✓ | ✓ | ✓ | ✓ |

There has been much recent interest in model-based RL approaches to solving a constrained MDP, the most relevant of which we have summarized in Table 1. The setup is of a finite horizon episodic CMDP, with a state space of size an action space of size and a horizon of length Regret is measured over the first episodes of the algorithm. Both the attained objective and constraint satisfaction are computed in an expected sense for a given policy. Allowing constraint violations during learning means that the algorithm suffers both an objective regret and a constraint regret. Examples of algorithms following this method are OptCMDP, OptCMDP-Bonus [18]. The algorithms use different ways of incentivizing exploration to obtain samples to build up an empirical system model. OptCMDP uses the idea of optimism in the face of uncertainty from the model perspective and solves an extended linear program to find the best model (highest reward) under the samples gathered thus far. OptCMDP-Bonus uses a different approach of adding a bonus to the reward term to incentivize exploration of state-action pairs that have fewer samples, which we consider as a form of optimism from the reward perspective. While the objective regret of both these algorithms is the constraint regret too is of the same order, since constraints may be violated during learning.

An algorithm that begins with no knowledge of the model will have exploration steps during learning that might violate constraints in expectation. Hence, safe RL approaches assume the availability of an inexpert baseline policy that does not violate the constraints, but is insufficient to explore the entire state action space. So it cannot be simply applied until a high-accuracy model is obtained. A heuristic approach entitled AlwaysSafe [36] assumes a factored CMDP that allows the easy generation of a safe baseline policy. It then combines the optimism with respect to the model of OptCMDP with a heuristically chosen hardening of constraints. This guarantees no constraint violations, but does not have regret guarantee with respect to the objective. Its empirical performance is variable and its use is limited to factored CMDP problems.

The OptPessLP algorithm [28] formalizes the idea of coupling optimism and pessimism by starting with OptCMDPBonus that has an optimistic reward, and systematically applying decreasing levels of pessimism with respect to the constraint violations. The approach is successful in ensuring the twin goals of a objective regret, while ensuring no constraint violations. However, the authors do not present any empirical performance evaluation results. When we implemented OptPessLP, we found that the performance is singularly bad in that linear regret persists for a large number of samples, and the tapering off to regret behavior does not appear to happen quickly. The problem with this algorithm is that it is so pessimistic with regard to constraints that it heavily disincentivizes exploration and ends up choosing the base policy for long sequences.

The issue upon which algorithm performance depends is the choice of how to combine optimism and pessimism to obtain both order optimal and empirically good objective regret performance, while ensuring no constraint violations happen. Our insight is that optimism with respect to the model is a key enabler of exploration, and can be coupled with the addition of optimism with respect to the reward. This double dose of optimism—both with respect to model and reward—could ensure that pessimistic hardening of constraints does not excessively retard exploration. Following this insight, we develop DOPE, a doubly optimistic and pessimistic exploration approach. We are able to show that DOPE not only attains objective regret behavior with zero constraint regret with high probability, it also reduces the objective regret bound over OptPessLP by a factor of We conduct performance analysis simulations under representative CMDP problems and show that DOPE easily outperforms all the earlier approaches. Thus, the idea of double optimism is not only valuable from the order optimal algorithm design perspective, it also shows good empirical regret performance, indicating the feasibility of utilizing the methodology in real-world systems. The code for the experiments in this paper is located at: https://github.com/archanabura/DOPE-DoublyOptimisticPessimisticExploration

Related Work: Constrained RL: Constrained Markov Decision Processes (CMDP) has been an active area of research [2], with applications in domains such as power systems [39, 25], communication networks [3, 38], and robotics [17, 11]. In [9], the author proposed an actor-critic RL algorithm for learning the asymptotically optimal policy for an infinite horizon average cost CMDP when the model is unknown. This approach is also utilized in function approximation settings with asymptotic local convergence guarantees [8, 12, 40]. Policy gradient algorithms for CMDPs have also been developed [1, 44, 47, 35, 16, 27, 49]. However, none these works address the problem of safe exploration to provide guarantees on the constraint violations during learning.

Safe Multi-Armed Bandits: The problem of safe exploration in linear bandits with stage-wise safety constraint is studied in [4, 24, 31, 33]. Linear bandits with more general constraints have also been studied [34, 29]. These works do not consider the more challenging RL setting which involves an underlying dynamical system with unknown model.

Safe Online Convex Optimization: Online convex optimization [20] has been studied with stochastic constraints [45, 10] and adversarial constraints [32, 46, 26]. These allow constraint violation during learning and characterize the cumulative amount of violation. A safe Frank-Wolf algorithm for convex optimization with unknown linear stochastic constraints has been studied in [41]. However, these too do not consider the RL setting with an unknown model.

Exploration in Constrained RL: There has been much work in this area with constraint violations during learning, including the work discussed in the introduction [18]. These include [37, 19, 23], which derive bounds either on the objective and constraint regret or on the sample complexity of learning an -optimal policy. Other works on safe RL include [43, 42], where a model-free approach is considered, and [5], that pertains to offline RL. These are complementary to our model-based approach. The problem of learning the optimal policy of a CMDP without violating the constraints was also studied in [48]. However, they assume that the model is known and only the cost functions are unknown, whereas we address more difficult problem with unknown model and cost functions.

Notations: For any integer , denotes the set . For any two real numbers , . For any given set , denotes the probability simplex over the set , and denotes the cardinality of the set .

2 Preliminaries and Problem Formulation

2.1 Constrained Markov Decision Process

We address the safe exploration problem using the framework of episodic Constrained Markov Decision Process (CMDP) [2]. We consider a CMDP, denoted as with , where is the state space, is the action space, is the episode length, is the objective cost function at time step , is the constraint cost function at time step , is the transition probability function with representing the probability of transitioning to state when action is taken at state at time . In the RL context, the transition matrix is also called the model of the CMDP. Finally, is a scalar that specifies the safety constraint in terms of the maximum permissible value for the expected cumulative constraint cost. We consider the setting where and are finite. Also, without loss of generality, we assume that costs and are bounded in .

A non-stationary randomized policy specifies the control action to be taken at each time step . In particular, denotes the probability of taking action when the state is at time step . For an arbitrary cost function , the value function of a policy corresponding to time step given a state is defined as

| (1) |

where . Since we are mainly interested in the value of a policy starting from , we simply denote as . For the rest of the paper, we will assume that the initial state is is fixed. So, we will simply denote as , when it is clear from the context. This standard assumption [18, 15] can be made without loss of generality.

The CMDP (planning) problem with a known model can then be stated as follows:

| (2) |

We say that a policy is a safe policy if , i.e., if the expected cumulative constraint cost corresponding to the policy is less than the maximum permissible value . The set of safe policies, denoted as , is defined as . Without loss of generality, we assume that the CMDP problem (2) is feasible, i.e., is non-empty. Let be the optimal safe policy, which is the solution of (2).

The CMDP (planning) problem is significantly different from the standard Markov Decision Process (MDP) (planning) problem [2]. Firstly, there may not exist an optimal deterministic policy for a CMDP, whereas the existence of a deterministic optimal policy is well known for a standard MDP. Secondly, there does not exist a Bellman optimality principle or Bellman equation for CMDP. So, the standard dynamic programming solution approaches which rely on the Bellman equation cannot be directly applied to solve the CMDP problem.

There are two standard approaches for solving the CMDP problem, namely the Lagrangian approach and the linear programming (LP) approach. Both approaches exploit the zero duality gap property of the CMDP problem [2] to find the optimal policy. In this work, we will use the LP approach, consistent with model optimism. Details of solving (2) using the LP approach are in Appendix A.

2.2 Reinforcement Learning with Safe Exploration

The goal of the reinforcement learning with safe exploration is to solve (2), but without the knowledge of the model a priori. Hence, the learning algorithm has to perform exploration by employing different policies to learn . However, we also want the exploration for learning to have a safety guarantee, i.e, the policies employed during learning should belong to the set of safe policies . Since itself is defined based on the unknown , the learning algorithm will not know a priori. This makes the safe exploration problem extremely challenging.

We consider a model-based RL algorithm that interacts with the environment in an episodic manner. Let be the policy employed by the algorithm in episode . At each time step in an episode , the algorithm observes state , selects action , and incurs the costs and . The next state is realized according to the probability vector . As stated before, for simplicity, we assume that the initial state is fixed for each episode , i.e., . We also assume that the maximum permissible cost for any exploration policy is known and it is specified as part of the learning problem.

The performance of the RL algorithm is measured using the metric of safe objective regret. The safe objective regret is defined exactly as the standard regret of an RL algorithm for exploration in MDPs [21, 14, 6], but with an additional constraint that the exploration polices should belong to the safe set . Formally, the safe objective regret after learning episodes is defined as

| (3) |

Since is unknown, clearly it is not possible to employ a safe policy without making any additional assumptions. We overcome this obvious limitation by assuming that the algorithm has access to a safe baseline policy such that . We formalize this assumption as follows.

Assumption 1 (Safe baseline policy).

The algorithm knows a safe baseline policy such that , where . The value is also known to the algorithm.

3 Algorithm and Performance Guarantee

DOPE builds on the optimism in the face of uncertainty (OFU) style exploration algorithms for RL [21, 14], using such optimism, both in terms of the model, as well as to provide a reward bonus for under-explored state-actions. However, a naive OFU-style algorithm may lead to selecting exploration policies that are not in the safe set . So we modify the selection of exploratory policy by incorporating pessimism in the face of uncertainty (PFU) on the constraints, making DOPE doubly optimistic and pessimistic in exploration.

DOPE operates in episodes, each of length . Define the filtration as the sigma algebra generated by the observations until the end of episode , i.e., . Let be the number of times the pair was observed at time step until the beginning of episode . Similarly, define . At the beginning of each episode , DOPE estimates the model as . Similar to OFU-style algorithms, we construct a confidence set around as , where

| (4) | ||||

| (5) |

where , and . Using the empirical Bernstein inequality, we can show that the true model is an element of for any with probability at least (see Appendix C).

Similarly, at the beginning of each episode , DOPE estimates the unknown objective and constraint costs as , . In keeping with OFU, we construct confidence sets and around and respectively, as

| (6) |

where , and . Using Hoeffding inequality, we can show that the true costs belong to and for any with probability at least (see Appendix C). We define to be the total confidence ball.

It is tempting to use the standard OFU approach for selecting the exploration polices since this approach is known to provide sharp regret guarantees for exploration problems in RL. The standard OFU approach will find the optimistic model and optimistic policy , where

| (7) |

The OFU problem (7) is feasible since the true model is an element of (with high probability). In particular, and are feasible solutions of (7). Moreover, (7) can be solved efficiently using an extended linear programming approach, as described in Appendix B. The policy ensures exploration while satisfying the constraint . However, this naive OFU approach overlooks the important issue that may not be a safe policy with respect to the true model . More precisely, it is possible to have even though . So, the standard OFU approach alone will not give a safe exploration strategy.

In order to ensure that the exploration policy employed at any episode is safe, we add a pessimistic penalty to the empirical constraint cost to get the pessimistic constraint cost function as

| (8) |

where Since is , pairs that are less observed have a higher penalty, disincentivizing their exploration. However. such a pessimistic penalty may prevent the exploration that is necessary to learn the optimal policy. To overcome this issue, we also modify the empirical objective cost function by subtracting a term to incentivize exploration, to obtain an optimistic objective cost function

| (9) |

Since is , pairs that are less observed will have a lowered cost to incentivize their exploration.

We select the policy for episode by solving the Doubly Optimistic-Pessimistic (DOP) problem:

| (10) |

Notice that DOPE is doubly optimistic by considering both the optimistic objective cost function in (9) and the optimistic model from the confidence set in (10), while being pessimistic on the constraint in (10). Later, in Lemma 18 in the appendix, we prove that is indeed an optimistic solution. This is in contrast with [28], where the optimism is solely limited to the objective cost. We will show that our approach carefully balances double optimism and pessimism, yielding a regret minimizing learning algorithm with episodic safe exploration guarantees.

We note that the DOP problem (10) may not be feasible, especially in the first few episodes of learning. This is because, and may be large during the initial phase of learning so that there may not be a policy and a model that can satisfy the constraint . We overcome this issue by employing a safe baseline policy (as defined in Assumption 1) in the first episodes, a value provided by Proposition 4. Since is safe by definition, DOPE ensures safety during the first episodes. We will later show that the DOP problem (10) will have a feasible solution after the first episodes (see Proposition 4). For any episode , DOPE employs policy , which is the solution of (10). We will also show that from (10) (once it becomes feasible) will indeed be a safe policy (see Proposition 5). We present DOPE formally in Algorithm 1.

We now present our main result, which shows that the DOPE algorithm achieves regret without violating the safety constraints during learning, with high probability.

Theorem 3.

Fix any . Consider the DOPE algorithm with as specified in Proposition 4. Let be the sequence of policies generated by the DOPE algorithm. Then, with probability at least , for all . Moreover, with probability at least , the regret of the DOPE algorithm satisfies

4 Analysis

We now provide the technical analysis of DOPE, concluding with the proof outline of Theorem 3.

4.1 Preliminaries

For an arbitrary policy and transition probability function , define and as

| (11) |

4.2 Feasibility of the OP Problem

Even though is a feasible solution to the original CMDP problem (2), it may not be a feasible for the DOP problem (10) in the initial phase of learning. To see this, note that and since under the good event, and , we will have if . So, is a feasible solution for (10) if . This sufficient condition may not be satisfied for initial episodes. However, since and are decreasing in , if becomes a feasible solution for (10) at episode , then it will remain feasible for all episodes . Also, since and decrease with , one can expect that (10) becomes feasible after some number of episodes. We use these intuitions, along with some technical lemmas to show the following result.

Proposition 4.

Under the DOPE algorithm, with a probability greater that , is a feasible solution for the DOP problem (10) for all , where .

4.3 Safety Exploration Guarantee

We show that the DOPE algorithm provides a safe exploration guarantee, i.e., for all with high probability, where is the exploration policy employed by DOPE in episode . This is achieved by the carefully designed pessimistic constraint of the DOP problem (10).

For any , since , and it is safe by Assumption 1. For , (10) is feasible according to Proposition 4. Since is the solution of (10), we have . This implies that . We have that under the good event, and hence, the above equation implies that , i.e., satisfies a tighter constraint with respect to the model . However, it is not obvious that the policy will be safe with respect to the true model because may be larger than due to the change from to .

We, however, show that cannot be larger than by more than , i.e., . This will then yield that , which is the true safety constraint. The key idea is in the design of the pessimistic cost function such that its pessimistic effect will balance the change in the value function (from to ) due to the optimistic selection of the model . We formally state the safety guarantee of DOPE below.

Proposition 5.

Let be the sequence of policies generated by the DOPE algorithm. Then is safe , i.e., , for all , with a probability greater than .

4.4 Regret Analysis

The regret analysis for most OFU style RL algorithms follows the standard approach of decomposing the regret into two terms as , where denotes the regret in episode . The first term is the difference between value functions of the selected policy with respect to the true model and optimistic model . Bounding this term is the key technical analysis part of most of the OFU algorithms for the unconstrained MDP [21, 13] and also the CMDP [18]. In the standard OFU style analysis for the unconstrained problem, since for all , it can be easily observed that is a feasible solution for the OFU problem (7) for all . Moreover, since is the optimal solution in episode, we get . So, the second term will be non-positive, and hence can be dropped from the regret analysis. However, in our setting, the second term can be positive since may not be a feasible solution of the DOP problem (10) due to the pessimistic constraint. This necessitates a different approach for bounding the regret. Existing work [28] only considers optimism in the objective cost, and hence their proof closely follows that of OptCMDP-Bonus algorithm in [18] with pessimistic constraints. In analyzing the regret of DOPE, we need to handle the optimism in objective cost as well as the model in regret terms, along with the pessimistic constraints. This make the analysis particularly challenging. The full proof is detailed in the appendix.

5 Experiments

We now evaluate DOPE via experiments. We have two relevant metrics, namely, (i) objective regret, defined in (3) that measures the optimality gap of the algorithm, and (ii) constraint regret, defined as where is the output of the algorithm in question at episode This measures the safety gap of the algorithm. Our candidate algorithms are (i) OptCMDP, (ii) AlwaysSafe, (iii) OptPessLP and (iv) DOPE, all described in the introduction. OptCMDP is expected to show constraint violations, while the other three should show zero constraint regret. We consider two environments here, with a third environment presented in the appendix. AlwaysSafe can directly be used only with a factored CMDP, and only applies to the first environment presented. We simulate both variants of this algorithm, referred to as AlwaysSafe and AlwaysSafe , respectively [36].

Factored CMDP: We first consider a CMDP where the safety relavant features of the model can be separated, as shown in [36]. This CMDP has states arranged in a circle, and actions in each state, to move right or stay put, respectively. The transitions move the agent to its right state with probability , if action is taken. If action is taken, it remains in the same state with probability . Action does not incur any objective cost or constraint cost. Action incurs an objective cost equals to the state number, and a constraint cost of . We choose episode length , and constraint as . The structure of this CMDP allows AlwaysSafe to extract a safe baseline policy from it.

Media Streaming CMDP: Our second environment represents media streaming to a device from a wireless base station, which provides high and low service rates at different costs. These service rates have independent Bernoulli distributions, with parameters , and , where corresponds to the fast service. Packets received at the device are stored in a media buffer and played out according to a Bernoulli process with parameter We denote the number of incoming packets into the buffer as , and the number of packets leaving the buffer The media buffer length is the state and evolves as where is the maximum buffer length. The action space is , where action corresponds to using the fast service. The objective cost is while the constraint cost is , i.e., we desire to minimize the outage cost, while limiting the usage of fast service. We consider episode length , and constraint .

Experiment Setup: OptCMDP and OptPessLP algorithms have not been implemented earlier. For accurate comparison, we simulate all the algorithms true to their original formulations of cost functions and confidence intervals. Our experiments are carried out for random runs, and averaged to obtain the regret plots. For DOPE, we choose to be as specified in Proposition 4. Full details on the algorithm parameters and experiment settings are provided in Appendix E.

Baseline Policies: Both OptPessLP and DOPE require baseline policies. We select the baseline policies as the optimal solutions of the given CMDP with a constraint . We choose the same baseline policies for both the algorithms. This choice is to showcase the efficacy of DOPE, despite starting with a conservative baseline policy.

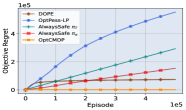

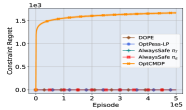

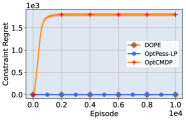

Results for Factored CMDP: Fig. 1(a) shows the objective regret of the algorithms in this environment. OptCMDP has a good objective regret performance as expected, but shows constraint violations. AlwasySafe fails to achieve regret in the episodes shown for both variants, although the variant has smaller regret as compared to the variant. OptPessLP takes a long time to attain behavior, which means that is chooses the baseline policy for an extended period, and shows high empirical regret. This suggests that reward optimism of OptPessLP is insufficient to balance the pessimism in the constraint. DOPE not only achieves the desired regret, but also does so in fewer episodes compared to the other two algorithms. Furthermore, it has low empirical regret. Fig. 1(b) shows that the constraint violation regret is zero for all the episodes of learning for all the safe algorithms, while OptCMDP shows a large constraint violation regret.

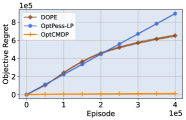

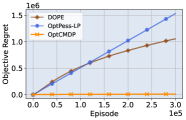

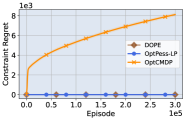

Results for Media Streaming CMDP: Fig.2(a) compares the objective regret across algorithms. The value of DOPE over OptPessLP is more apparent here. After a linear growth phase, the objective regret of DOPE changes to a square-root scaling. OptPessLP has not explored sufficiently at this point, and hence suffers high linear regret. Finally, OptCMDP also has square-root regret scaling, but is fastest, since it is not constrained by safe exploration. Fig.2(b) compares the regret in constraint violation for these algorithms. As expected, DOPE and OptPessLP do not violate the constraint, while the OptCMDP algorithm significantly violates the constraints during learning.

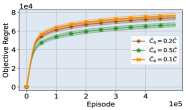

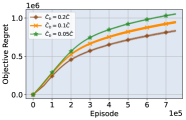

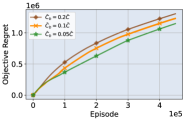

Effect of Baseline Policy: We compare the objective regret of DOPE under different baseline policies in Fig.1(c) and Fig.2(c). We see that less conservative (but safe) baselines result in lower regret, but the difference is not excessive, implying that the exact baseline policy chosen is not crucial.

Summary: DOPE has two valuable properties: Faster rate of shift to behavior, since the linear regret phase where it applies the baseline policy is relatively short, and regret with respect to optimal, which together mean that the empirical regret is lower than other approaches.

Limitations: Our goal is to find an RL algorithm with no constraint violation with high probability in the tabular setting. Since safe exploration is a basic problem, we follow the usual approach in the literature of first establishing the fundamental theory results for the tabular setting [21, 14, 6]. We also note that most of the existing work on exploration in safe RL is in the tabular setting [18, 37, 28]. In our future work, we plan to employ the DOPE approach in a function approximation setting.

6 Conclusion

We considered the safe exploration problem in reinforcement learning, wherein a safety constraint must be satisfied during learning and evaluation. Earlier approaches to constrained RL have proposed optimism on the model, optimism on reward, and pessimism on constraints as means of modulating exploration, but none have shown order optimal regret, no safety violation, and good empirical performance simultaneously. We started with the conjecture that double optimism combined with pessimism is the key to attaining the ideal balance for fast and safe exploration, and design DOPE that carefully combines these elements. We showed that DOPE not only attains order-optimal regret without violating safety constraints, but also reduces the best known regret bound by a factor of Furthermore, it has significantly better empirical performance than existing approaches. We thus make a case for adoption of the approach for real world use cases and extension to large scale RL problems using function approximation.

7 Acknowledgement

This work was supported in part by the grants NSF-CAREER-EPCN 2045783, NSF ECCS 2038963, and ARO W911NF-19-1-0367. Any opinions, findings, and conclusions or recommendations expressed in this material are those of the authors and do not necessarily reflect the views of the sponsoring agencies.

References

- [1] Joshua Achiam, David Held, Aviv Tamar, and Pieter Abbeel. Constrained Policy Optimization. In International Conference on Machine Learning, pages 22–31. PMLR, 2017.

- [2] Eitan Altman. Constrained Markov decision processes, volume 7. CRC Press, 1999.

- [3] Eitan Altman. Applications of Markov decision processes in communication networks. In Handbook of Markov decision processes, pages 489–536. Springer, 2002.

- [4] Sanae Amani, Mahnoosh Alizadeh, and Christos Thrampoulidis. Linear stochastic bandits under safety constraints. Advances in Neural Information Processing Systems, 32:9256–9266, 2019.

- [5] Sanae Amani and Lin F. Yang. Doubly pessimistic algorithms for strictly safe off-policy optimization. In 2022 56th Annual Conference on Information Sciences and Systems (CISS), pages 113–118, 2022.

- [6] Mohammad Gheshlaghi Azar, Ian Osband, and Rémi Munos. Minimax regret bounds for reinforcement learning. In International Conference on Machine Learning, pages 263–272. PMLR, 2017.

- [7] Dimitri P Bertsekas et al. Dynamic programming and optimal control: Vol. 1. Athena scientific Belmont, 2000.

- [8] Shalabh Bhatnagar and K Lakshmanan. An online actor–critic algorithm with function approximation for constrained Markov decision processes. Journal of Optimization Theory and Applications, 153(3):688–708, 2012.

- [9] Vivek S Borkar. An actor-critic algorithm for constrained Markov decision processes. Systems & control letters, 54(3):207–213, 2005.

- [10] Sapana Chaudhary and Dileep Kalathil. Safe online convex optimization with unknown linear safety constraints. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 36, pages 6175–6182, 2022.

- [11] Yin-Lam Chow, Marco Pavone, Brian M Sadler, and Stefano Carpin. Trading safety versus performance: Rapid deployment of robotic swarms with robust performance constraints. Journal of Dynamic Systems, Measurement, and Control, 137(3):031005, 2015.

- [12] Yinlam Chow, Mohammad Ghavamzadeh, Lucas Janson, and Marco Pavone. Risk-constrained reinforcement learning with percentile risk criteria. The Journal of Machine Learning Research, 18(1):6070–6120, 2017.

- [13] Christoph Dann and Emma Brunskill. Sample complexity of episodic fixed-horizon reinforcement learning. Advances in Neural Information Processing Systems, 28:2818–2826, 2015.

- [14] Christoph Dann, Tor Lattimore, and Emma Brunskill. Unifying pac and regret: Uniform pac bounds for episodic reinforcement learning. arXiv preprint arXiv:1703.07710, 2017.

- [15] Dongsheng Ding, Xiaohan Wei, Zhuoran Yang, Zhaoran Wang, and Mihailo Jovanovic. Provably efficient safe exploration via primal-dual policy optimization. In International Conference on Artificial Intelligence and Statistics, pages 3304–3312. PMLR, 2021.

- [16] Dongsheng Ding, Kaiqing Zhang, Tamer Basar, and Mihailo Jovanovic. Natural policy gradient primal-dual method for constrained Markov decision processes. Advances in Neural Information Processing Systems, 33:8378–8390, 2020.

- [17] Xu Chu Ding, Alessandro Pinto, and Amit Surana. Strategic planning under uncertainties via constrained Markov decision processes. In 2013 IEEE International Conference on Robotics and Automation, pages 4568–4575. IEEE, 2013.

- [18] Yonathan Efroni, Shie Mannor, and Matteo Pirotta. Exploration-exploitation in constrained MDPs. arXiv preprint arXiv:2003.02189, 2020.

- [19] Aria HasanzadeZonuzy, Archana Bura, Dileep Kalathil, and Srinivas Shakkottai. Learning with safety constraints: Sample complexity of reinforcement learning for constrained MDPs. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 7667–7674, 2021.

- [20] Elad Hazan. Introduction to online convex optimization. Foundations and Trends in Optimization, 2(3-4):157–325, 2016.

- [21] Thomas Jaksch, Ronald Ortner, and Peter Auer. Near-optimal regret bounds for reinforcement learning. Journal of Machine Learning Research, 11(4), 2010.

- [22] Chi Jin, Tiancheng Jin, Haipeng Luo, Suvrit Sra, and Tiancheng Yu. Learning adversarial Markov decision processes with bandit feedback and unknown transition. In Proceedings of the 37th International Conference on Machine Learning, volume 119, pages 4860–4869. PMLR, 13–18 Jul 2020.

- [23] Krishna C Kalagarla, Rahul Jain, and Pierluigi Nuzzo. A sample-efficient algorithm for episodic finite-horizon MDP with constraints. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 8030–8037, 2021.

- [24] Kia Khezeli and Eilyan Bitar. Safe linear stochastic bandits. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 34, pages 10202–10209, 2020.

- [25] Hepeng Li, Zhiqiang Wan, and Haibo He. Constrained EV charging scheduling based on safe deep reinforcement learning. IEEE Transactions on Smart Grid, 11(3):2427–2439, 2019.

- [26] Nikolaos Liakopoulos, Apostolos Destounis, Georgios Paschos, Thrasyvoulos Spyropoulos, and Panayotis Mertikopoulos. Cautious regret minimization: Online optimization with long-term budget constraints. In International Conference on Machine Learning, pages 3944–3952. PMLR, 2019.

- [27] Tao Liu, Ruida Zhou, Dileep Kalathil, PR Kumar, and Chao Tian. Fast global convergence of policy optimization for constrained mdps. arXiv preprint arXiv:2111.00552, 2021.

- [28] Tao Liu, Ruida Zhou, Dileep Kalathil, PR Kumar, and Chao Tian. Learning Policies with Zero or Bounded Constraint Violation for Constrained MDPs. In Thirty-fifth Conference on Neural Information Processing Systems, 2021.

- [29] Xin Liu, Bin Li, Pengyi Shi, and Lei Ying. An efficient pessimistic-optimistic algorithm for stochastic linear bandits with general constraints. arXiv preprint arXiv:2102.05295, 2021.

- [30] Andreas Maurer and Massimiliano Pontil. Empirical Bernstein bounds and sample-variance penalization. In COLT 2009 - The 22nd Conference on Learning Theory, Montreal, Quebec, Canada, June 18-21, 2009, 2009.

- [31] Ahmadreza Moradipari, Christos Thrampoulidis, and Mahnoosh Alizadeh. Stage-wise conservative linear bandits. Advances in Neural Information Processing Systems, 33, 2020.

- [32] Michael J Neely and Hao Yu. Online convex optimization with time-varying constraints. arXiv preprint arXiv:1702.04783, 2017.

- [33] Aldo Pacchiano, Mohammad Ghavamzadeh, Peter Bartlett, and Heinrich Jiang. Stochastic bandits with linear constraints. In International Conference on Artificial Intelligence and Statistics, pages 2827–2835. PMLR, 2021.

- [34] Advait Parulekar, Soumya Basu, Aditya Gopalan, Karthikeyan Shanmugam, and Sanjay Shakkottai. Stochastic linear bandits with protected subspace. arXiv preprint arXiv:2011.01016, 2020.

- [35] Santiago Paternain, Luiz Chamon, Miguel Calvo-Fullana, and Alejandro Ribeiro. Constrained reinforcement learning has zero duality gap. Advances in Neural Information Processing Systems, 32:7555–7565, 2019.

- [36] Thiago D Simão, Nils Jansen, and Matthijs TJ Spaan. Alwayssafe: Reinforcement learning without safety constraint violations during training. In Proceedings of the 20th International Conference on Autonomous Agents and MultiAgent Systems. International Foundation for Autonomous Agents and Multiagent Systems, 2021.

- [37] Rahul Singh, Abhishek Gupta, and Ness B Shroff. Learning in Markov decision processes under constraints. arXiv preprint arXiv:2002.12435, 2020.

- [38] Rahul Singh and PR Kumar. Throughput optimal decentralized scheduling of multihop networks with end-to-end deadline constraints: Unreliable links. IEEE Transactions on Automatic Control, 64(1):127–142, 2018.

- [39] Rahul Singh, PR Kumar, and Le Xie. Decentralized control via dynamic stochastic prices: The independent system operator problem. IEEE Transactions on Automatic Control, 63(10):3206–3220, 2018.

- [40] Chen Tessler, Daniel J Mankowitz, and Shie Mannor. Reward constrained policy optimization. In International Conference on Learning Representations, 2018.

- [41] Ilnura Usmanova, Andreas Krause, and Maryam Kamgarpour. Safe convex learning under uncertain constraints. In The 22nd International Conference on Artificial Intelligence and Statistics, pages 2106–2114. PMLR, 2019.

- [42] Honghao Wei, Xin Liu, and Lei Ying. A provably-efficient model-free algorithm for infinite-horizon average-reward constrained Markov decision processes. In AAAI Conference on Artificial Intelligence, 2022.

- [43] Honghao Wei, Xin Liu, and Lei Ying. Triple-q: A model-free algorithm for constrained reinforcement learning with sublinear regret and zero constraint violation. In International Conference on Artificial Intelligence and Statistics, pages 3274–3307. PMLR, 2022.

- [44] Tsung-Yen Yang, Justinian Rosca, Karthik Narasimhan, and Peter J Ramadge. Projection-based constrained policy optimization. In International Conference on Learning Representations, 2019.

- [45] Hao Yu, Michael J Neely, and Xiaohan Wei. Online convex optimization with stochastic constraints. In Proceedings of the 31st International Conference on Neural Information Processing Systems, pages 1427–1437, 2017.

- [46] Jianjun Yuan and Andrew Lamperski. Online convex optimization for cumulative constraints. In Proceedings of the 32nd International Conference on Neural Information Processing Systems, pages 6140–6149, 2018.

- [47] Yiming Zhang, Quan Vuong, and Keith Ross. First order constrained optimization in policy space. Advances in Neural Information Processing Systems, 33, 2020.

- [48] Liyuan Zheng and Lillian Ratliff. Constrained upper confidence reinforcement learning. In Learning for Dynamics and Control, pages 620–629. PMLR, 2020.

- [49] Ruida Zhou, Tao Liu, Dileep Kalathil, PR Kumar, and Chao Tian. Anchor-changing regularized natural policy gradient for multi-objective reinforcement learning. arXiv preprint arXiv:2206.05357, 2022.

- [50] Alexander Zimin and Gergely Neu. Online learning in episodic Markovian decision processes by relative entropy policy search. In Neural Information Processing Systems 26, 2013.

Societal Impact and Ethics Statement

Reinforcement learning has much potential for application to a variety of cyber-physical systems, such as the power grid, robotics and other systems where guarantees on the operating region of the system must be met. Our work provides a theoretical basis for the design of controllers that can be applied in such scenarios. The approaches presented in the paper were tested on simulated environments, and did not involve any human interaction. We do not see any ethical concerns with our research approach.

A note of caution with our approach is that the policy generated is only as good as the training environment, and many examples exist wherein the policy generated is optimal according to its training, but violates basic truths known to human operators and could fail quite badly. Indeed, our approach does not provide sample-path guarantees, and the system could well move into deleterious states for a small fraction of the time, which might be completely unacceptable and trigger hard fail safes, such as breakers in a power system. Understanding the right application environments with excellent domain knowledge is hence needed before any practical success can be claimed.

Checklist

-

1.

For all authors…

- (a)

-

(b)

Did you describe the limitations of your work? [Yes] In Section 5.

-

(c)

Did you discuss any potential negative societal impacts of your work? [Yes] Societal Impact and Ethics Statement.

-

(d)

Have you read the ethics review guidelines and ensured that your paper conforms to them? [Yes] Described in Societal Impact and Ethics Statement.

- 2.

-

3.

If you ran experiments…

-

(a)

Did you include the code, data, and instructions needed to reproduce the main experimental results? [Yes] Supplemental material

- (b)

-

(c)

Did you report error bars (e.g., with respect to the random seed after running experiments multiple times)? [Yes] Figures contain error bars.

-

(d)

Did you include the total amount of compute and the type of resources used (e.g., type of GPUs, internal cluster, or cloud provider)? [Yes] Appendix E

-

(a)

-

4.

If you are using existing assets (e.g., code, data, models) or curating/releasing new assets…

-

(a)

If your work uses existing assets, did you cite the creators? [N/A]

-

(b)

Did you mention the license of the assets? [N/A]

-

(c)

Did you include any new assets either in the supplemental material or as a URL? [Yes] Code is released as supplemtental material.

-

(d)

Did you discuss whether and how consent was obtained from people whose data you’re using/curating? [N/A]

-

(e)

Did you discuss whether the data you are using/curating contains personally identifiable information or offensive content? [N/A]

-

(a)

-

5.

If you used crowdsourcing or conducted research with human subjects… [N/A]

Appendix A Linear Programming Method for Solving the CMDP Problem

Here we give a brief description on solving the CMDP problem (2) using the linear programming method when the model is known. The details can be found in [18, Section 2].

The first step is to reformulate (2) using occupancy measure [2, 50]. For a given policy and an initial state , the state-action occupation measure for the MDP with model is defined as

| (12) |

Given the occupancy measure, the policy that generated it can easily be computed as

| (13) |

The occupancy measure of any policy for an MDP with model should satisfy the following conditions. We omit the explicit dependence on and from the notation of for simplicity.

| (14) | ||||

| (15) |

From the above conditions, it is easy to show that . So, occupancy measures are indeed probability measures. Since the set of occupancy measures for a model , denoted as , is defined by a set of affine constraints, it is straight forward to show that is convex. We state this fact formally below.

Proposition 6.

The set of occupancy measures for an MDP with model , denoted as , is convex.

Recall that the value of a policy for an arbitrary cost function with a given initial state is defined as . It can then be expressed using the occupancy measure as

where with element is given by and with element is given by . The CMDP problem (2) can then be written as

| (16) |

Appendix B Extended Linear Programming Method for Solving OFU and DOP problems

The OFU problem (7) and the DOP problem (10) may appear much more challenging than the CMDP problem (2) because they involve a minimization over all models in , which is non-trivial. However, finding the optimistic model (and the corresponding optimistic policy) from a given confidence set is a standard step in OFU style algorithms for exploration in RL [21, 18]. In the case of standard (unconstrained) MDP, this problem is solved using a approach called extended value iteration [21]. In the case of constrained MDP, (7) (and similarly (10) ) can be solved by an approach called extended linear programming. The details are given in [18]. We give a brief description below for completeness. Note that the description below mainly focus on solving (7). Solving (10) is identical, just by replacing the constraint cost function with pessimist constraint cost function , , and is mentioned at the end of this subsection.

Define the state-action-state occupancy measure as . The extended LP formulation corresponding to (7) is then given as follows:

| (18a) | ||||

| s.t. | (18b) | |||

| (18c) | ||||

| (18d) | ||||

| (18e) | ||||

| (18f) | ||||

| (18g) | ||||

The last two conditions ((18f) and (18g)) distinguish the extended LP formulation from the LP formulation for CMDP. These constraints are based on the Bernstein confidence sets around the empirical model .

From the solutions of the extended LP, we can obtain the solution of (7) as

| (19) |

Appendix C Useful Technical Results

Here we reproduce the supporting technical results that are required for analyzing our DOPE algorithm. We begin by stating the following concentration inequality, known as empirical Bernstein inequality [30, Theorem 4].

Lemma 7 (Empirical Bernstein Inequality).

Let be i.i.d random vector with values in , and let . Then, with probability at least , it holds that

where is the sample variance.

We can get the following result using empirical Bernstein inequality and union bound. This result is widely used in the literature now, for example see [22, Proof of Lemma 2],

Lemma 8.

With probability at least , for all , , we have

Lemma 9.

Let be the event defined as in (20). Then, .

Define the events , and , and define

| (21) |

The following is a standard result, and can be obtained by Hoeffding’s inequality, and using a union bound argument on all and all possible values of , for all .

Lemma 10.

.

We now define the event as follows

| (22) |

where is the occupancy measure corresponding to the policy chosen in episode . We have the following result from [14, Corollary E.4.]

We now define the good event . Using union bound, we can show that . Since our analysis is based on this good event, we formally state it as a lemma.

Lemma 12.

We will also use the following results for analyzing the performance of our DOPE algorithm.

Lemma 13 (Lemma 36, [18]).

Under the event ,

Lemma 14 (Lemma 37, [18]).

Under the event ,

Lemma 15 (Lemma 8,[22]).

Under the event , for all , and for all , there exists constants such that .

Lemma 16 (Value difference lemma).

Consider two MDPs and . For any policy , state , and time step , the following relation holds.

Appendix D Proof of the Main Results

All the results we prove in this section are conditioned on the good event defined in Section C. So, the results hold true with a probability greater than according to Lemma 12. We will omit stating this conditioning under in each statement to avoid repetition.

D.1 Proofs of Proposition 4

Lemma 17.

Let and be as defined in (11). Also, let be the sequence of policies generated by DOPE algorithm. Then, for any , each of the following relations hold with a probability greater than .

Proof.

| (25) |

Here, we get inequality by the definition of (c.f. (5)). To get , note that by Cauchy-Schwarz inequality and . We get using Lemma 13 and Lemma 14.

The other part can also be obtained similarly from Lemma 13. ∎

We now give the proof of Proposition 4.

Proof of Proposition 4.

First note that even though is a feasible solution for the original CMDP problem (2), it may not feasible for the DOP problem (10). To see this, note that since and , and , we will have if . So, is a feasible solution for (10) if, . This is a sufficient condition for the feasibility of . This condition may not be satisfied in the initial episodes.

However, since and are decreasing in , if becomes a feasible solution for (10) at episode , then it will remain to be a feasible solution for all episodes .

Suppose for all . Also, suppose the above condition is not satisfied in the algorithm until episode . Then, for all . So, we should get

where the last inequality is from Lemma 17. However, this inequality is violated for . So, is a feasible solution for (10) for any episode provided that for all . ∎

The above result, however, only shows that becomes a feasible policy after some finite number of episodes. A natural question is, is the only feasible policy? In such a case, the DOPE algorithm may not provide enough exploration to learn the optimal policy.

We alleviate the concerns about the above possible issue by showing that for all , there exists a feasible solution for the OP problem (10) such that for every with . Informally, this implies that will visit all state-action pairs that will be visited by the optimal policy . This result can be derived as a corollary for Proposition 4.

D.2 Proof of Proposition 5

Proof.

For any episode , we have , and it is safe by Assumption 1. For , (10) is feasible according to Proposition 4. Since is the solution of (10), we have . We will now show that , conditioned on the good event .

By the value difference lemma (Lemma 16), we have

| (26) |

Here, we get by Holder’s inequality inequality. To get , we make use of two observations. First, note that because the expected cumulative cost cannot be grater than since by assumption. Second, under the good event , .

D.3 Proof of Theorem 3

We first prove an important lemma.

Lemma 18 (Optimism).

Let be the optimal solution corresponding to the DOP problem (10). Then,

Proof.

We will first consider a more general version of the DOP problem (10) as

| (27) |

where we change in (10) to above, with , for . Note that (27) reduces to (10) for and hence it is indeed a general version.

Using the occupancy measures and , define a new occupancy measure for an .

Note that is a valid occupancy measure since the set of occupancy measure is convex (c.f. Proposition 6). Let be the policy corresponding to the occupancy measure , which can be obtained according to (13) so that .

Claim 1: is a feasible solution for (27) when satisfies the sufficient condition

| (28) |

Proof of Claim 1: Since value function is a linear function of the occupancy measure, we have

where inequality is due to the good event that is within the confidence interval, , for any and inequality is due to the fact that , and .

For to be a feasible solution for (27), it must be true that . Hence, it is sufficient to get an such that

This yields a sufficient condition (28). Note that is non-negative because for , as shown in the proof of Proposition 4. This concludes the proof of Claim 1.

Claim 2: if satisfies the sufficient condition

| (29) |

Proof of Claim 2: Selecting an that satisfies the condition (28), is a feasible solution of (27). Since is the optimal solution of (27), we have . So, it is sufficient to find a such that . Using the linearity of the value function w.r.t. occupancy measure, this is equivalent to .

Since for any under the good event, it is sufficient if we find a such that . This will yield the condition Now, we choose that satisfies the condition (28) as, . Using this in the previous inequality for , we get the sufficient condition . Since and , we get the sufficient condition (29). This concludes the proof of Claim 2.

Now, let . So, and . Hence, by Claim 2, we have . Hence, we have the desired result. ∎

We now present the proof of Theorem 3.

Proof of Theorem 3.

The regret for the DOPE algorithm after episodes can be written as,

| (30) |

We will bound the first term in (30) as

| (31) |

where we get the first inequality because , and the second inequality follows from the bound on in Proposition 4.

The second term in (30) can be bounded as

| (32) |

where is due to the fact that from Lemma 18, is due to the fact that conditioned on the good event set (see Lemma 10), follows from the definition of , and follows from Lemma 17.

We will now bound the first term in (32) as

| (33) |

Now, for the first term in (33),

| (34) |

In order to now bound the second term in (33), we proceed in similar lines to the proof of Lemma from [18].

Consider,

| (35) |

where the last inequality is obtained from Lemma 15. We will bound the term in (35) as

| (36) |

where the first inequality is from bounding by . This is obtained by noting that , since , from the definition. The second inequality is from Lemma 17.

We now bound the term in (35) as follows.

| (37) |

Here, is obtained by Jensen’s inequality, is by cauchy schwartz inequality, is from the property of the occupancy measure, i.e., , is obtained from Lemma 14. To get , we use the result from Lemma 19 that , and hence obtain, . We prove from Lemma of [18]. The step is to get is more involved and we prove it separately in Lemma 20, following a similar result from Lemma of [18]. The inequality holds from the fact that .

Using the above obtained bounds on and in (35), we get

Let . Then, the above bound takes the form , where , and .

Now, using the fact that, if , then (Lemma from [18]), we can obtain the bound

| (38) |

Using the above bound in (32), we obtain,

| (39) |

The left hand side of the above inequality is non-negative, since , from lemma 18, and , since is the optimal policy on . This equation is again of the form , where . Using the same result we used to get (38), we deduce that , and hence,

and hence, from (32), .

Moreover, from proposition (5), we have that for all , with probability . ∎

Lemma 19 (Bonus optimism).

For any , conditioned on good event, we have that , and, for any , it holds that .

Proof.

Consider

where the last inequality is due to the fact that .

Similarly, by value difference lemma 16, we have,

where the last inequality is obtained just earlier. ∎

Lemma 20.

We prove inequality in bounding term , i.e., we prove that,

Proof.

Let us start with,

Summing this relation for , we get,

Hence, we obtain,

∎

Appendix E Detailed Description of Experiment Environments and Algorithm Implementation

E.1 Experiment Environments

Factored CMDP environment: The factored CMDP is represented in Fig. 3. The state space is , and the action space is , where action corresponds to moving one step to the right and corresponds to staying put. Objective cost is , and . The constraint cost is, , and . The probability transition matrix under action is,, and under action , it is .

Media Streaming Environment: Here, we model the media streaming control from a wireless base station. The base station provides two types of service to a device, a fast service and a slow service. The packets received are stored in a media buffer at the device. The goal is to minimize the cost of having an empty buffer (which may result in stalling of the video), while keeping the utilization of fast service below certain level.

We denote by , the number of incoming packets into the buffer, and by , the number of packets leaving the buffer. The state of the environment, denoted as in step, is the media buffer length. It evolves as, . We consider as the maximum buffer length in our experiment. The action space is , i.e., the action is to use either fast server or slow server . We assume that the service rates of the servers have independent Bernoulli distributions, with parameters , and , where corresponds to the fast service. The media playback at the device is also Bernoulli with parameter . Hence, is a random variable with mean either or depending on the action taken, and is a random variable with mean . These components constitute the unknown transition dynamics of our environment.

The objective cost is . i.e., it has a value of , when the buffer hits zero, and is zero everywhere else. Our constraint cost is , i.e., there is a constraint cost of when the fast service is used, and is zero otherwise. We then constrain the expected number of times the fast service is used to , in a horizon of length .

Inventory Control Environment: We consider a single product inventory control problem [7]. Our environment evolves according to a finite horizon CMDP, with horizon length , where each time step represents a day of the week. In this problem, our goal is to maximize the expected total revenue over a week, while keeping the expected total costs in that week below a certain level. We do not backlog the demands.

The storage has a maximum capacity , which means it can store a maximum of items. We denote by , the state of the environment, as the amount of inventory available at day. The action is the amount of inventory the agent purchases such that the inventory does not overflow. Thus, the action space for the state . The exogenous demand is represented by , which is a random variable representing the stochastic demand for the inventory on the day. We assume to be in with distribution . If the demand is higher than the inventory and supply, the excess demand will not be met. The state evolution then follows as .

We define the rewards and costs as follows. The revenue is generated as, , when , and is otherwise. The reward obtained in state is then the expected revenue over all next states , . The cost associated with the inventory has two components. Firstly, there is a purchase cost when the inventory is brought in, which is a fixed cost of units, plus a variable cost of , which increases with the amount of purchase. Secondly, we also have a non decreasing holding cost , for storing the inventory. Hence, the cost in is . We normalize the rewards and costs to be in the range . Our goal is to maximize the expected total revenue over a week , while keeping the expected total costs in that week below a threshold .

E.2 Details of the Implementation

We now describe the algorithms described in the introduction.

AlwaysSafe: AlwaysSafe [36] shows empirical results that only depict the expected cost of various policies deduced from their linear programs versus the optimal expected cost. We note that this comparison is not a reasonable measure of regret, since cumulative regret can be linear even though the expected costs are close.

We consider a factored CMDP environment described previously. For implementing this algorithm, in each episode, we solve the LP4 linear program described in [36], based on the observations. For solving LP4, one also needs an abstract CMDP as described in Section of [36]. We follow their description to construct such a model for the factored CMDP. The confidence intervals for AlwaysSafe algorithm are same as the ones for OptCMDP algorithm from [18] and of DOPE. We notice that the regret of Always safe algorithms indeed grow at a linear rate.

OptPessLP: We implement Algorithm from [28]. We choose the baseline policy by solving the corresponding CMDP with a more conservative constraint. For the factored CMDP and Media Control environment, we choose the constraint as , and solve the MDP to obtain and the corresponding cost . Similarly, for the inventory control environment, we choose the constraint as . These choices of are the same for both OptPessLP and DOPE, for a fair comparison. We play when the condition in Equation from [28] is met, otherwise we choose the maximizing policy from their linear program. We choose the confidence intervals as specified in their work, without any scaling. Despite the results suggested by theory, we notice that its empirical performance is very poor in every environment we consider.

OptCMDP: We implement Algorithm from [18]. This algorithm solves the linear program that minimizes the objective cost with optimism in the model. Since this algorithm does not consider zero-violation setting, we expect to see constraint violation of the same order as the regret. We use the confidence intervals as specified in their work, without any scaling.

DOPE: We implement Algorithm from our work. The choice of baseline policy is exactly the same as that for OptPessLP for each environment. is played until episodes, as provided by Proposition 4. Then, the algorithm solves the linear program given by Equation (10) to obtain in episode .

The details for the linear program formulations are given in Appendices A and B. DOPE, AlwaysSafe and OptCMDP algorithms use the Extended LP formulations, while OptPessLP uses the regular LP formulation.

For each environment, each of these algorithms are run for random seeds, and are averaged to obtain the regret plots in the figures.

E.3 Experiment Results for Inventory Control Environment

We show the performance of our DOPE algorithm in Inventory Control Environment. As before, we compare it against the OptCMDP Algorithm 1 in [18], and and OptPess-LP algorithm from [29]. Also, we choose the optimal policy from a conservative constrained problem (with a stricter constraint) as the baseline policy. We use .

Fig. 4(a) compares the objective regret for the inventory control environment incurred by each algorithm with respect to the number of episodes. As we see in this figure, in the initial episodes, the objective regret of DOPE grows linearly with number of episodes. Later, the growth rate of regret changes to square root of number of episodes. We see that this change of behavior happens after episodes specified by Proposition 4. Hence, the linear growth rate indeed corresponds to the duration of time in which the base policy is employed. In conclusion, the regret for DOPE algorithm depicted in Figures 4(a) matches the result of Theorem 3. Next, the OptPess-LP algorithm performs quite badly in terms of objective regret, as it fails to achieve regret performance within the chosen number of episodes. It thus shows the same issue of excessive pessimism observed in the other environments. Finally, we observe that the objective regret of OptCMDP is lower than DOPE. This behavior can be attributed to the fact that in order to perform safe exploration, DOPE includes a pessimistic penalty in the constraint (8).

Fig. 4(b) compares the regret in constraint violation for DOPE, OptPess-LP and OptCMDP algorithms for the inventory control setting. Here, we see that DOPE and OptPess-LP do not violate the constraint, while OptCMDP incurs a regret that grows sublinearly. This figure shows that DOPE does indeed perform safe exploration as proved, while OptCMDP violates the constraints during learning.

Finally, Fig. (4(c)) compares the optimality regret for various baseline policies. Again, the takeaway here is that a good baseline policy is helpful, although the variation across different baseline policies is not very large.