Quantum portfolio value forecasting

Abstract

We present an algorithm which efficiently estimates the intrinsic long-term value of a portfolio of assets on a quantum computer. The method relies on quantum amplitude estimation to estimate the mean of a novel implementation of the Gordon-Shapiro formula. The choice of loading and readout algorithms makes it possible to price a five-asset portfolio on present day quantum computers, a feat which has not been realised using quantum computing to date. We compare results from two available trapped ion quantum computers. Our results are consistent with classical benchmarks, but result in smaller statistical errors for the same computational cost.

Introduction.- Monte Carlo methods are a hallmark of modern computing. These algorithms are essential for modelling random processes, as well as numerical integration and various optimization algorithms. They are ubiquitous in finance, where they are used to estimate risk and uncertainty. They are applied in fields which are intrinsically uncertain, such as option pricing, stock management, and default risk estimation Wilmott (2013). As such, Monte Carlo simulations also typically represent the largest computational cost to financial institutions. Using these methods one can estimate risk up to an arbitrary precision, at the cost of a large number of runs. Financial institutions such as banks need to estimate risk with very high accuracies in order to minimize losses, and it is not uncommon for them to run simulations which take upwards of 24 hours in the best case.

In parallel to the above, quantum computing is known to accelerate many computational tasks. Some of these can be proven to not be achievable through any classical means (such as the square-root speed-up when searching in unstructured databases Grover (1996)). In fact, quantum computing has already found many applications in finance – for a detailed review, see Ref. Orús et al. (2019). In this context, Montanaro Montanaro (2015); An et al. (2021) was the first to suggest using quantum amplitude estimation to accelerate Monte Carlo methods. He showed that quantum computers can run Monte Carlo simulations to the same accuracy as classical computers, but reducing quadratically the number of samples, thus resulting in overall faster calculations. Variations of this method have been successfully applied to toy academic models in finance in Refs. Rebentrost et al. (2018); Woerner and Egger (2019); Ramos-Calderer et al. (2021); Stamatopoulos et al. (2019).

In this paper, we develop a quantum method to estimate the intrinsic long-term value of a portfolio of assets, and implement it with real-life data. This is a core open problem in finance, which relies on an accurate forecasting of risk and market predictions. Accurate intrinsic long-term value estimation is crucial to portfolio optimization applications, which has been heavily investigated in the context of quantum computing Mugel et al. ; Mugel et al. (2021, 2020); Rosenberg et al. (2016); Elsokkary et al. (2017); Grant et al. (2020); Cohen et al. (2020); Palmer et al. (2021). Moreover, we implement the method in two different quantum computing architectures based on trapped ions: one provided by IonQ 111See https://ionq.com/., and one described in Ref. Pogorelov et al. (2021) (AQTION project). The results provide a use case of both quantum platforms when applied to a real financial problem. We choose to work with trapped ions because they provide a natural all-to-all connectivity among the qubits. Importantly, this property makes it simpler to implement the quantum circuit required in this work, in turn avoiding errors in, e.g., arbitrary 2-qubit gates between non-neighbouring qubits.

Mathematical model.- In general, an asset’s intrinsic long-term value is the present value of all future cash flows Williams (1938). If a portfolio’s value is growing, its intrinsic value is given by the Gordon-Shapiro model D’Amico and De Blasis (2020). It is possible to price assets based on their dividend yield at all times in the future. In practice, this can cause issues, as the intrinsic price diverges in certain parameter regimes as time goes to infinity. In this paper, we consider a truncated Gordon-Shapiro model, which only considers the assets’ growth over the first two years, followed by a period at maturity. For more in-depth information, see Refs. Williams (1938); D’Amico and De Blasis (2020).

Typically, the Gordon-Shapiro model prices assets based on the dividend yield. These do not always provide an accurate estimation of the assets’ value, particularly for immature companies, or companies that have a culture of distributing little or no dividends. Thus, we prefer to evaluate asset value based on the asset’s earnings per share. Our modified Gordon-Shapiro model is therefore given by:

| (1) |

where is the total value of the portfolio, indicates the asset’s index, the total number of assets, is the weight of asset (normalized to the total amount of investment), and is the single asset intrinsic value. This last quantity is given in the model by:

| (2) |

In the equation above, and are the earnings per share (EPS) of asset respectively for the first and second year. The first-year, second-year, and long-term discount rates are given by , , and , respectively. The EPS long-term growth rate of asset is given by .

In the following, we will assume that the short-term variables , , and , as well as the growth rates can be forecasted to reasonable accuracy, and that the long-term variables and are harder to accurately predict, so that we include small relative stochastic shifts and . In general, all variables from Eq. (2) could be described as stochastic variables themselves. In our implementation, however, we are motivated to approximate the short-term variables by their mean values as these only contribute weakly to Eq. (2).

Following the above, the long-term variables can be expressed as:

| (3) | |||||

| (4) |

where is the mean of , is the cost of capital for a risk-free asset, and is a fixed risk premium. In Eq. (3), we used the share’s growth rate to estimate the mean EPS in the second year. Moreover, and are stochastic variables following a probability distribution.

Including the above in Eq. (1), we see that the intrinsic value is itself a stochastic quantity that follows a probability distribution. In the following, we find it useful to discretise its value over states, each with value and probability . Our goal is to compute the mean intrinsic value:

| (5) |

where is the discretization index. The aim of our quantum algorithm is, precisely, to estimate such expectation value as efficiently and accurately as possible.

Quantum algorithm.- We discuss here briefly the main features of our quantum implementation, and leave the more in-depth technical details for the Supplementary Material. Let us start by saying that we encode all the possible discretised intrinsic values with probability in quantum states, and then implement an algorithm which allows us to efficiently estimate the mean intrinsic value provided in Eq. (5) by using “quantum-enhanced” Monte Carlo. The main steps involved are:

-

1.

State preparation: encode the distribution of the stochastic variables into a quantum state.

-

2.

Manipulation and readout: manipulate the quantum state in such a way that we can efficiently estimate the mean of the probability distribution with the smallest possible error.

Concerning state preparation, the first step requires the definition of a Grover-like loading operator , as required for quantum amplitude estimation. On the one hand, the operator encodes a known probability distribution to qubits:

| (6) |

where is the total number of states and . We discuss the choice of this operator in the Supplementary Material. On the other hand, is designed in such a way that it allows the encoding of a function in an ancilla qubit, in such a way that this enconding gets entangled with the probability distribution as follows:

| (7) |

with . Importantly, this implies

| (8) |

so that the expectation value of measuring in the ancilla qubit is, in fact, the mean value of . This is exactly how we are going to compute the mean intrinsic value of Eq. (5).

| Index | SXXP | SPX | NKY | MXEF | EPRA |

|---|---|---|---|---|---|

| Holdings | 2.75 | 19.5 | 0.04 | 0.89 | 0.59 |

In general, choosing such that we can effectively attach requires a significant overhead in circuit depth or ancilla qubits Häner et al. (2018); Mitarai et al. (2019). Instead, we use the algorithm described in Ref. Woerner and Egger (2019), which proposes an efficient way of implementing via controlled-Y rotations, provided is a polynomial function in the stochastic variables. The latter is achieved using the Taylor expansion of , for which we assume here just linear order given that . We furthermore rescale from to as , for implementation purposes. The details of the Taylor expansion and rescaling can be found in the Supplementary Material.

As for the readout, we have constructed a controlled rotation which maps the expectation value of the intrinsic price to the amplitude of an ancilla qubit as in Eq. (7). This can be done efficiently using, e.g., the quantum implementation of the reversible classical circuit for the function. Then, we estimate this amplitude efficiently using Quantum Amplitude Amplification (QAA) Brassard et al. (2002); Montanaro (2015). Usually this is done using approaches based on phase estimation Kitaev (1995). However, here we prefer the Maximum Likelihood Estimation (MLE) method from Ref. Suzuki et al. (2020), which has low circuit depth, does not rely on expensive controlled rotations, and maintains the quadratic speedup. This method is described in the Supplementary Material.

Results.- As a proof of concept, we study a portfolio of five assets, with each one of them being an index. We invest 1000 euros in each asset, with a full value of 5000 euros, bought at market value on 2021-04-25. The corresponding number of shares being held is shown in Table 1. Forecasted EPS, growth rates, and discount rates for each asset were purchased from a market data provider. All the input data used is summarised in the Supplementary Material.

| Market | Classical | IonQ | AQTION |

|---|---|---|---|

| Bearish | |||

| Regular | |||

| Bullish |

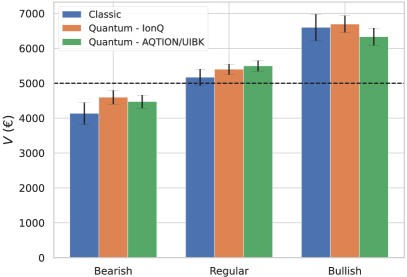

The forecasted intrinsic values of the portfolio are presented in Fig. 1. Technical details on the algorithm and the error calculation are in the Supplementary Material. We compare the results obtained using “quantum-enhanced” Monte Carlo to those obtained using classical Monte Carlo for an equal amount of samples. Our circuits are run on two quantum hardware platforms based on trapped ions: IonQ and AQTION quantum processing units (QPUs). In order to evaluate the resilience of our model, we compare the results from three different market trends: bearish or receding, regular or stable, and bullish or rising. These behaviours are obtained by tuning the volatility and EPS long-term growth (). We assume bearish and bullish markets to be more volatile than the stable ones (see the size of the error bars in Fig. 1), and set for bearish market, for stable markets, and for bullish markets.

We see that, when the market is stable or bullish, the portfolio’s intrinsic value exceeds the portfolio’s market value. This implies that this portfolio is a sound investment, i.e: the rewards from buying this portfolio justify the risks. In this example, this is not the case when the market behaves bearishly, as the market overestimates the portfolio’s value. Additionally, the error bars in Fig. 1 (exact values in Table 2) show the confidence interval of the intrinsic price. These are larger in the classical case than the quantum case. This is because, by virtue of Chebyshev’s inequality 222Let be a random variable with a finite expected value and finite non-zero variance . Then, for any real number , one has that Cheby., the computational cost of classically calculating the intrinsic value within distance of its actual value becomes prohibitively large for small . This inequality does not hold in the quantum case, and the quantum implementation is more efficient by a quadratic factor.

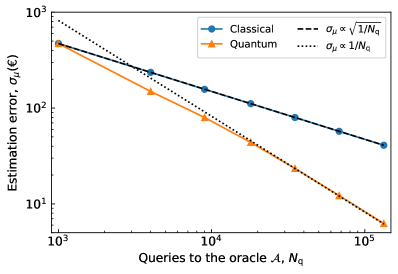

The estimation error 333Importantly, error here means the statistical error due to the intrinsic uncertainty in the sampling, either classical or quantum. It does not refer to the experimental error in the calculation, such as quantum gate errors. This experimental error is considered in the supplementary material. on the mean intrinsic price can in theory be arbitrarily reduced by increasing the circuit depth in the quantum case, or increasing the number of samples in the classical case. In Fig. 2 we plot the estimation error versus number of calls to the operator , as computed by a simulator of the quantum hardware in the “regular” scenario. In our algorithm, denotes the (classical) number of samples or (quantum) circuit depth and, therefore, it is proportional to the computational cost. The specific method we use to estimate the error in the forecast intrinsic price of the portfolio is explained in the Supplementary Material. The results in Fig. 2 clearly confirm a quadratic quantum speedup: whereas in classical Monte Carlo simulations the estimation error drops as , with quantum methods we can achieve , as shown in the figure. Or in financial words: for the same computational cost, we estimate the intrinsic portfolio value with a quadratically-lower risk.

Conclusions.- In this paper we have presented a method for efficiently estimating the intrinsic long-term price of a portfolio of assets using quantum computation. This method relies on Quantum Amplitude Estimation to evaluate the mean of a modified Gordon-Shapiro model. We demonstrate the effectiveness of our algorithms by estimating the intrinsic long-term value of a portfolio of 5 assets on present day quantum computers, namely, those provided by IonQ and AQTION, both of them based on trapped ions. Our quantum model outputs results which are consistent with the classical Monte Carlo benchmark, but with quadratically smaller statistical error for the same computational cost.

In order to price such a large portfolio on present-day quantum computers, we had to make a number of assumptions about the nature of the stochastic variables. We anticipate that, in the near future, quantum computers will become available with a higher quantum volume. This will allow to represent more stochastic variables also in a more accurate way, in turn allowing for even more accurate calculations of portfolio prices. Another interesting direction for future work would involve finding implementations of operator that can optimally implement functions such as . This would allow us to price our portfolio without linearising Eq. (1), leading to an overall improvement of the result’s accuracy.

Acknowledgments: We gratefully acknowledge funding from the EU H2020-FETFLAG-2018-03 under Grant Agreement No. 820495. We also acknowledge support by the Austrian Science Fund (FWF), through the SFB BeyondC (FWF Project No. F7109), as well as from Automatiq (FFG Project No. 872766), ELQO (FFG Project No. 884471), and the IQI GmbH. Moreover, we thank Christophe Jurczak, Pedro Luis Uriarte, Pedro Muñoz-Baroja, Joseba Sagastigordia, Creative Destruction Lab, BIC-Gipuzkoa, DIPC, Ikerbasque, Basque Government and Diputación de Gipuzkoa for constant support, as well as Denise Ruffner for her special implication that guaranteed the success of this project. We also acknowledge the hard work and constant feedback from AQTION, IonQ, and Multiverse Computing fantastic teams.

References

- Wilmott (2013) P. Wilmott, The Wiley Finance Series, Paul Wilmott Introduces Quantitative Finance (2013).

- Grover (1996) L. K. Grover, Proceedings of the Twenty-Eighth Annual ACM Symposium on Theory of Computing STOC ’96, 212 (1996).

- Orús et al. (2019) R. Orús, S. Mugel, and E. Lizaso, Reviews in Physics 4, 100028 (2019), arXiv:1807.03890 .

- Montanaro (2015) A. Montanaro, Proceedings of the Royal Society A: Mathematical, Physical and Engineering Science 471, 20150301 (2015).

- An et al. (2021) D. An, N. Linden, J.-P. Liu, A. Montanaro, C. Shao, and J. Wang, Quantum 5, 481 (2021).

- Rebentrost et al. (2018) P. Rebentrost, B. Gupt, and T. R. Bromley, Physical Review A 98, 022321 (2018).

- Woerner and Egger (2019) S. Woerner and D. J. Egger, npj Quantum Information 5, 15 (2019), arXiv:1806.06893 .

- Ramos-Calderer et al. (2021) S. Ramos-Calderer, A. Pérez-Salinas, D. García-Martín, C. Bravo-Prieto, J. Cortada, J. Planagumà, and J. I. Latorre, Physical Review A 103, 032414 (2021), arXiv:1912.01618 .

- Stamatopoulos et al. (2019) N. Stamatopoulos, D. J. Egger, Y. Sun, C. Zoufal, R. Iten, N. Shen, and S. Woerner, Quantum 4, 1 (2019), arXiv:1905.02666 .

- (10) S. Mugel, C. Kuchkovsky, E. Sanchez, S. Fernandez-Lorenzo, J. Luis-Hita, E. Lizaso, and R. Orús, Physical Review Research (in press), arXiv:2007.00017 .

- Mugel et al. (2021) S. Mugel, M. Abad, M. Bermejo, J. Sánchez, E. Lizaso, and R. Orús, Scientific Reports 11, 19587 (2021).

- Mugel et al. (2020) S. Mugel, E. Lizaso, and R. Orús, (2020), arXiv:2010.01312 [q-fin.GN] .

- Rosenberg et al. (2016) G. Rosenberg, P. Haghnegahdar, P. Goddard, P. Carr, K. Wu, and M. López De Prado, IEEE Journal of Selected Topics in Signal Processing 10, 1053 (2016).

- Elsokkary et al. (2017) N. Elsokkary, F. S. Khan, D. L. Torre, T. S. Humble, and J. Gottlieb, 2017 IEEE High Performance Extreme Computing Conference (HPEC ’ 17) 2, 1 (2017).

- Grant et al. (2020) E. Grant, T. Humble, and B. Stump, (2020), arXiv:2007.03005 .

- Cohen et al. (2020) J. Cohen, A. Khan, and C. Alexander, (2020), arXiv:2007.01430 .

- Palmer et al. (2021) S. Palmer, S. Sahin, R. Hernandez, S. Mugel, and R. Orús, (2021), arXiv:2106.06735 [q-fin.PM] .

- Note (1) See https://ionq.com/.

- Pogorelov et al. (2021) I. Pogorelov, T. Feldker, C. D. Marciniak, L. Postler, G. Jacob, O. Krieglsteiner, V. Podlesnic, M. Meth, V. Negnevitsky, M. Stadler, B. Höfer, C. Wächter, K. Lakhmanskiy, R. Blatt, P. Schindler, and T. Monz, PRX Quantum 2, 020343 (2021).

- Williams (1938) J. B. Williams, The theory of investment value, (1938).

- D’Amico and De Blasis (2020) G. D’Amico and R. De Blasis, (2020), 10.1002/9781119779421.ch3, arXiv:2001.00465 .

- Häner et al. (2018) T. Häner, M. Roettelery, and K. M. Svorez, arXiv (2018), arXiv:1805.12445 .

- Mitarai et al. (2019) K. Mitarai, M. Kitagawa, and K. Fujii, Physical Review A 99, 012301 (2019), arXiv:1805.11250 .

- Brassard et al. (2002) G. Brassard, P. Høyer, M. Mosca, and A. Tapp, (2002), 10.1090/conm/305/05215, arXiv:quant-ph/0005055 [quant-ph] .

- Kitaev (1995) A. Y. Kitaev, (1995), arXiv:quant-ph/9511026 .

- Suzuki et al. (2020) Y. Suzuki, S. Uno, R. Raymond, T. Tanaka, T. Onodera, and N. Yamamoto, Quantum Information Processing 19, 3 (2020), arXiv:1904.10246 .

- Note (2) Let be a random variable with a finite expected value and finite non-zero variance . Then, for any real number , one has that Cheby.

- Note (3) Importantly, error here means the statistical error due to the intrinsic uncertainty in the sampling, either classical or quantum. It does not refer to the experimental error in the calculation, such as quantum gate errors. This experimental error is considered in the supplementary material.