Filtering time-dependent covariance matrices using time-independent eigenvalues

Abstract

We propose a data-driven, model-free, way to reduce the noise of covariance matrices of time-varying systems. If the true covariance matrix is time-invariant, non-linear shrinkage of the eigenvalues is known to yield the optimal estimator for large matrices. Such a method outputs eigenvalues that are highly dependent on the inputs, as common sense suggests. When the covariance matrix is time-dependent, we show that it is generally better to use the set of eigenvalues that encode the average influence of the future on present eigenvalues resulting in a set of time-independent average eigenvalues. This situation is widespread in nature, one example being financial markets, where non-linear shrinkage remains the gold-standard filtering method. Our approach outperforms non-linear shrinkage both for the Frobenius norm distance, which is the typical loss function used on covariance filtering, and for financial portfolio variance minimization, which makes our method generically relevant to many problems of multivariate inference. Further analysis of financial data suggests that the expected overlap between past eigenvectors and future ones is systematically overestimated by methods designed for constant covariances matrices. Our method takes a simple empirical average of the eigenvector overlap matrix, which is enough to outperform non-linear shrinkage.

Introduction

In multivariate systems, many statistical inference problems require estimating the covariance matrix or its inverse. In the simplest case, a system of interest has a constant covariance matrix and produces Gaussian features. Even in these favorable circumstances, a direct estimation of covariance matrices is very noisy when the number of data points is comparable with or smaller than the number of features, which is known as the curse of dimensionality, or high-dimensional setting. In time-evolving systems, when the underlying model is unknown, one faces the conundrum of using as few data points as possible so as to focus on the most recent information while still estimating the covariance matrix precisely enough. Thus, generically, covariance filtering requires removing two sources of systematic bias and noise: sampling noise and time evolution (which results in covariate shift).

Filtering sampling noise out of covariance matrices has a long history. There are two main approaches: either to coerce the matrix to follow a specified structure (i.e., to use an ansatz) [1, 2], or to use its decomposition into eigenvalues and eigenvectors (see [3] for a review) and filter them: for example, Random Matrix Theory provides tools to compute the noisy influence of sampling errors and reversely gives methods to denoise covariance matrices (e.g. [4, 5, 3]). Estimators that only modify the covariance matrix eigenvalues are known as Rotationally Invariant Estimators (RIE thereafter). According to recent literature, an optimal RIE should minimize the Frobenius distance between the filtered and true covariance matrix. If the true covariance matrix is known, the optimal RIE is named the Oracle estimator, and can be obtained analytically. Obviously, the Oracle estimator does not make sense for forecasting, as the true covariance is unknown. In this case, it yields the lowest Frobenius norm that an RIE can achieve. Remarkably, asymptotically optimal RIEs that converge to the Oracle estimator can be obtained without the knowledge of the true covariance matrix [6, 7, 8, 3, 9]; however, such estimators require that: i) the ground truth does not change, ii) the data matrix is very large, and iii) the data has at least finite fourth moments [3, 7]. In the following, we shall call this family of estimators NLS, which stands for non-linear shrinkage.

Yet, the most interesting complex systems are rarely time-invariant and often produce heavy-tailed features. Dissipative quantum systems, ecosystems, and many socio-economic systems are time-varying in essence [10]. Here, we propose a purely data-driven covariance filtering method that outperforms NLS as soon as the covariance matrix changes as a function of time. Remarkably, our method rests on an averaging procedure of Oracle eigenvalues in a long calibration dataset, which we call the Average Oracle. In other words, our method consists in replacing the eigenvalues of a time-dependent correlation matrix with time-invariant eigenvalues. Because the Average Oracle leads to appreciably better estimation of covariance matrices in systems with time-dependent correlation matrices, we expect its application domain to be vast. We apply it below to dynamic optimal resource allocation, which has interdisciplinary applications (financial portfolios, wind farm locations, marketing channels, and, more generally, optimization problems with a quadratic cost).

Covariance matrix filtering

At time , given time-series (features), one needs to predict their covariance matrix in the test interval from the information known in the train interval . Even in the assumption of a time-invariant world, the sample estimator is biased and noisy as soon the ratio is not negligible . Fortunately, one can improve the sample estimator by using a suitable filtering scheme, which yields a new estimator, denoted by . The idea is to bring as close as possible to , which is quantified by a distance, such as the Frobenius distance (squared element-wise difference) .

A special class of rotationally invariant estimators uses the decomposition of the covariance matrix into eigenvectors and eigenvalues. Indeed, the spectral decomposition theorem states that , where is the eigenvector matrix and is the diagonal matrix of eigenvalue monotonically ordered.

Let us focus on eigenvalue-based filtering (i.e., build an RIE) and thus use the empirical eigenvectors . Generically, if is an RIE, it can be written as

| (1) |

where is a diagonal matrix with well-chosen eigenvalues. For example, if one knows the future covariance matrix , the optimal eigenvalue matrix is the so-called Oracle and can be shown [8] to be

| (2) |

where the diag operator only keeps the diagonal of a matrix and sets the elements to zero elsewhere. These eigenvalues express the future empirical covariance matrix in the basis of the current one. They are optimal in the following sense: the related RIE

| (3) |

minimizes the (element-wise) Frobenius distance . Although the exact Oracle estimator cannot be used for practical purposes, since is in the future, asymptotical estimators that converge to the Oracle estimator are known [6, 11, 7, 3]. In other words, this optimal RIE exploits a way to express as a function of the past information only, provided that the hypotheses listed above hold, temporal independence being a crucial one.

The above asymptotically optimal RIEs rest on neglecting any evolution of the covariance matrix. Although this makes sense for constant underlying covariance matrices, it likely discards relevant information for time-dependent matrices, and indeed Oracle eigenvalues do contain valuable information to filter as they encode the link between the past and the future in an RIE setting. With the aim of capturing the average transition from two consecutive time windows, our method rests on the averaging Eq. (2), rank-wise, over many randomly selected consecutive intervals taken from a long calibration window. The latter must be much larger than the one used to compute .

More precisely (see Fig. 1 for a graphical explanation), we need to define a long calibration window , with , and not necessarily linked to the actual test window size , as shown in appendix C. Then, we select random times . For a given , two consecutive intervals must defined: the first interval must be of size , while the length of the next one will be of size . It is worth mentioning that the next interval is in the future with respect but it is in the past with respect , i.e., with respect ; therefore, an Oracle-like scheme can be applied.

Each sub-sampling has an associated set of Oracle eigenvalues

| (4) |

With the eigenvectors of the sample covariance matrix computed in , and the sample covariance of . The Average Oracle eigenvalues are then defined as the average element-wise:

| (5) |

It is important to stress that the columns of the eigenvectors of (4) must always follow the same the eigenvalue ordering convention chosen.

The AO-filtered covariance matrix is given by

| (6) |

The empirical eigenvalues from the train interval are completely discarded and replaced by the AO ones. The fact that the Average Oracle is a better estimator for time-evolving covariance matrices most often implies that the most recent information contained in the sample eigenvalues is less relevant (and more noisy) than the AO ones that focus on the average transition. On the other hand, the train eigenvectors contain some dynamical information and are kept. Note also that our approach requires that the univariate variances are constant. If one deals with a system in which this is not the case, our method should be applied to the correlation matrix.

We thus propose to tackle the evolution of dependencies with a time-invariant eigenvalue cleaning scheme. This is a zeroth order approximation, as the fluctuations of the optimal eigenvalue matrix around sometimes most probably contain valuable additional information (as may do those of the eigenvectors). Nevertheless, this approximation is a powerful filtering tool and is easily computed from data without any modeling assumptions about the underlying system. In addition, our tests indicate that the filtering power does not decrease substantially as a function of time in the systems that we investigated.

The Role of the Temporal Evolution

To understand how the Oracle eigenvalues are related to the time-dependency of both the eigenvalues and eigenvectors of a covariance matrix, we decompose (2) as

| (7) |

where and are the eigenvalues shaped in column vectors, and represents the Hadamard element-wise square of the matrix . The matrix is in fact a rotation matrix from the eigenvector basis to the eigenvector basis and hence belongs in .

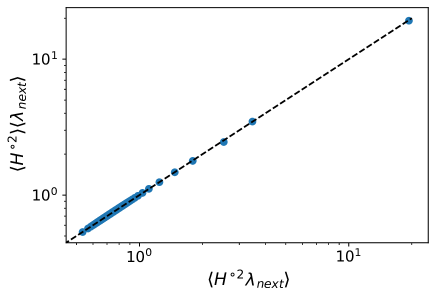

This decomposition of the Oracle estimator makes it possible to analyze the respective contributions of and to the Oracle estimator and, by linearity, to the Average Oracle. Indeed, according to Eq. 7, it is natural to test if the problem of overlap and test eigenvalues estimation can be separated, i.e., if

| (8) |

It is worth noticing that although the average element-wise of an element of the group is not an element of the group, the element-wise average of still has the same relevant property as the original elements, i.e., the row-wise or column-wise sum equal one.

We test Eq. (8) with financial data. It is worth stressing, as detailed in the appendix Ref sec:variance, that the variance of each time series varied tremendously in the last twenty years and hence we focus on correlation rather than covariance matrix. In practice, we standardize the time series on every subinterval considered (see the appendix A for a full description of data handling).

We find that Eq. (8) holds remarkably well (Fig. 2): and are linearly independent and thus both quantities can be assumed to contribute independently to the fluctuations of the Oracle eigenvalues. As a consequence, we are allowed to focus on the influence of eigenvalues and eigenvectors separately.

Overlap matrix stability

The element-wise square represents the projection of the eigenvector from on the eigenvector from . In the case of the perfect overlap, only one , all the others being zero. This never happens because of finite-sample size error and temporal evolution. The other extreme case is for all , which corresponds to the lowest overlap possible. Given these mathematical properties of the overlap matrix, Shannon entropy is an appropriate measure of the amount of overlap. For eigenvector , we write

| (9) |

with the standard Shannon entropy convention that and normalization by , in such a way that the highest overlap will be while the lowest .

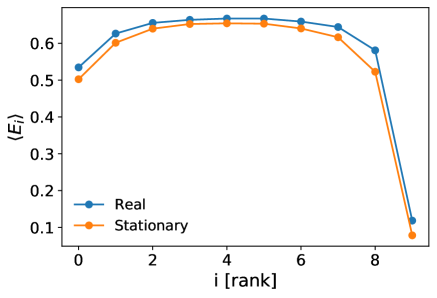

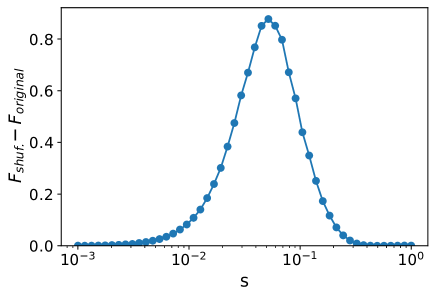

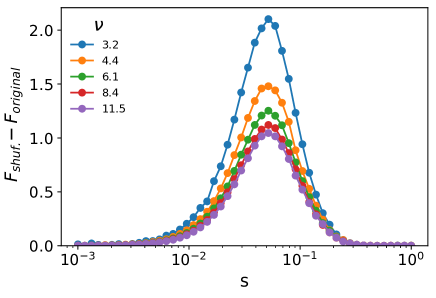

By using Eq. (9), we can test on real data if the average overlap in a time-invariant world, due only to sampling size error, is compatible with the measured overlap of the real world. We carried out such an experiment in the following way. We randomly select random time-windows , with days and perform an independent random selection of stocks for each time-window. We then measure the entropy of the overlap for each eigenvector ranked from the smallest eigenvalue to the largest one. The entropy is then averaged element-wise over these independent realizations, which yields a measure of real-world overlap, influenced both by sampling error and time evolution.

To show that the real-life overlap is systematically lower than the one expected for a time-invariant world, we design a local data shuffling procedure to remove any effect of temporal evolution, and we measure the rank-wise average overlap again. First we take the union of the intervals , then we shuffle the temporal ordering of the observations, then we split the shuffled data again into , , but after the shuffling both intervals will contain a mixture a past and future events; therefore, any quantity has the same expectation in both intervals.

Figure 3 displays the average entropy for both cases. One sees that data shuffling leads to smaller entropy, hence, larger apparent overlap. This means that in a fictional time-invariant world, the overlap is mechanically larger, which in turn implies that this assumption leads to a bias in the eigenvectors’ stability in the real world. While for the overestimation of the overlap for the time-invariant cases is clear, for we must look at the difference between the two estimators. One notes that the overestimation of the time-invariant case is systematic even for large .

Eigenvalues stability

In Eq. 2, the other part of Oracle the estimator is the expectation of . A reasonable assumption in a time-invariant world, if , is that .

Another possibility is that, because of very fast temporal evolution, the eigenvalues fluctuate so much that their average computed over many time-windows within a much larger calibration time-window is a better predictor of than the closest past .

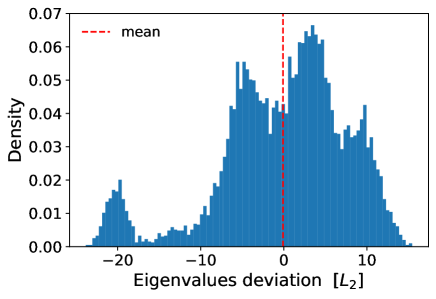

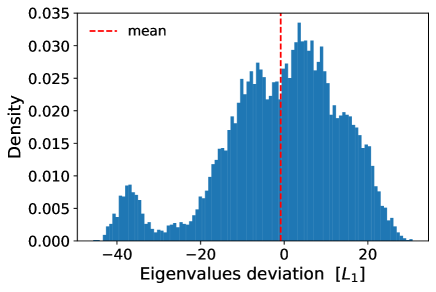

In order to test these two hypotheses, we computed the average over randomly chosen time-windows of days in the the calibration window . We then we tested the deviation and in the test window with randomly chosen time-windows. We carried out such a comparison with and norms.

Specifically, the norm is defined as

| (10) |

and the norm is defined as

| (11) |

where can be the or .

In Fig. 4, we show the distribution of the eigenvalue deviation as - and -. Each point of the distribution is a random selection of the time window on the validation period. The average of both distributions is close to zero, supporting the idea that the most recent eigenvalues are approximately as good as the average historical ones. More precisely the distribution average is slightly negative: for the , with a 95-percentile bootstrap p-value of and with a 95-percentile bootstrap p-value of zero (computed with bootstrap re-sampling). However, such a difference is marginal, and the average approach does not bring any significant improvement.

Matrix distance between filtered and realized covariance

We expect our method to be useful for any system with time-dependent dependencies as a zeroth order correction. Here, we test AO vs. NLS with financial data as they are abundant, have dynamic dependencies, and are heavy-tailed [12]. We also use synthetic data to assess the respective influence of covariance temporal evolution and heavy tails on the performance of both AO and NLS in appendix D.

In some systems with time-dependent covariances, such as financial markets, the order of magnitude of univariate variances strongly depends on time. In order to remove this source of time-dependence, we focus on the eigenvalue correction of the correlation matrix and compute where the eigenvalues and eigenvectors are those of correlation matrices. The elements of a filtered covariance matrix are obtained by multiplying the filtered correlation matrix by the respective univariate standard deviations

| (12) |

In the following, we use about 24 years of daily data for assets from the US stock market. The Average Oracle eigenvalues are calibrated in the 1995 to 2005 period from subintervals; for the sake of computation speed, we take random assets in each subinterval. Because we randomize asset selection, the resulting Average Oracle eigenvalues can be applied to any selection of assets (and to other markets). One could also choose to compute for a fixed set of assets. For a full description of the data handling, see the appendix A.

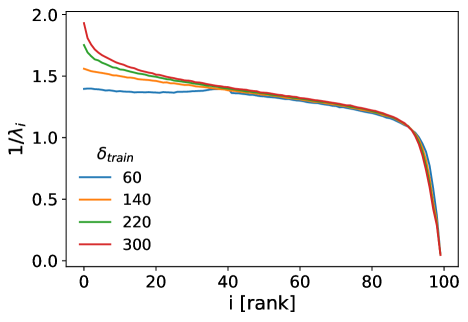

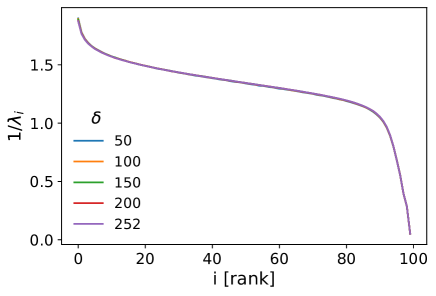

The resulting AO eigenvalues are reported in Fig. 5. Note that we plot the inverse of the average eigenvalues in order to emphasize the dependence on of small eigenvalues, as many inference problems use the inverse covariance matrix (see below), and also to reduce the influence of the largest eigenvalues on the clarity of the figure.

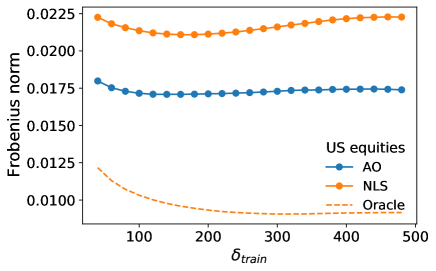

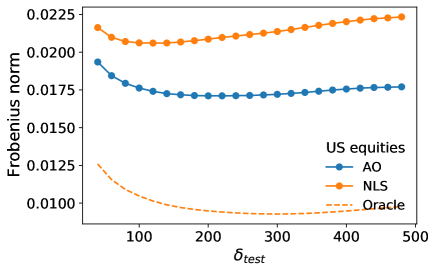

The first way to compare the performance of both NLS and AO is to compute the average Frobenius norm in the out-of-sample period (). We carried out extensive simulations with various , selecting 100 random selections of assets for each . While depends on and , it does not seem to depend on (see appendix C) which we fix henceforth to 252 (one year of daily data). We compared the Average Oracle approach with an efficient and provably good numerical implementation of NLS [11, 13] based on cross-validation within the train window.

The average Frobenius norm in the out-of-sample period for NLS and AO is reported in the left plot of Fig. 6. AO clearly does better than NLS, even if the latter is designed to minimize this norm in the time-invariant case. For the sake of completeness, we also added the unrealistic case where the Oracle eigenvalues are computed from the future as in Eq. (2), which shows how much the AO could still be improved with a predictive model of eigenvalues. Note that the advantage of AO over NLS increases with (appendix F). We also check in appendix E that the same results hold for the Kullback-Leibler distance.

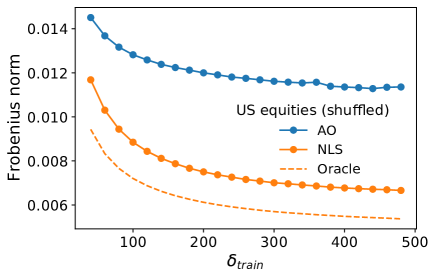

The superior performance of the Average Oracle is mainly due to the time evolution of the true correlation matrix. Indeed, when we shuffle the data in the train and test interval as described in Sec. Overlap matrix stability, the advantage of using AO disappears. In particular, in Fig. 6 (right plot), we show that NLS clearly outperforms the Average Oracle on the Frobenius distance on shuffled data. Thus, the advantage of the Average Oracle is precisely that it captures some part of the average dynamics that is discarded by the assumption of a constant true covariance matrix (see also appendix D).

Application to portfolio optimization

Portfolio optimization is a canonical application of covariance matrices in a resource allocation context. The simplest case only uses the covariance matrix and aims at minimizing the realized variance of the value of a portfolio of assets from the knowledge of data in the train interval. Mathematically, a portfolio is defined by the fraction of wealth invested into each available asset . In other words, the performance of a portfolio with weights is the weighted sum of the performance of all the assets, i.e., , where is the price return of asset , and its variance is . Practically, the weights are computed from the train window data, and the covariance is that of the test window, thus the realized portfolio volatility is given by

| (13) |

The optimization problem usually adds the normalization constraint . This defines the Global Minimum Variance Portfolio problem (GMV). Intuitively, minimizing requires a small distance between and , hence the importance of the Frobenius norm (see Fig. 6), which is the usual criterion in the covariance matrix filtering literature [3], which however, does not lead to the optimal portfolio weights [14] in finite sample size cases.

The weights that minimize the portfolio variance given a covariance estimator can be computed analytically

| (14) |

One immediately notices that portfolio optimization also requires that the inverse of the covariance matrix (the precision matrix) be also well filtered as the optimal weights are much influenced by the smallest eigenvalues of .

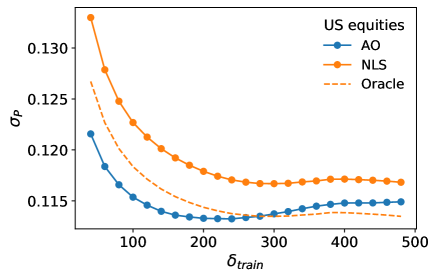

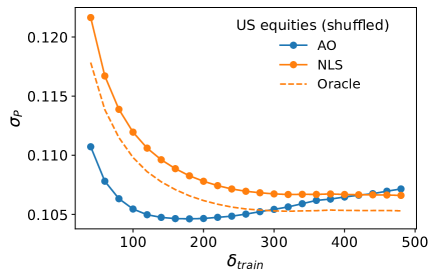

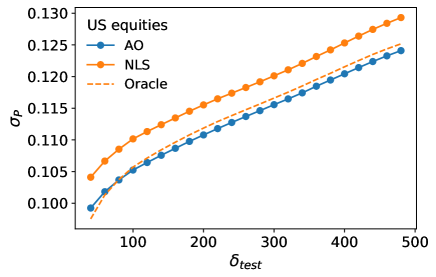

Figure Ref. 7 shows that the realized volatility of GMV portfolios is smaller when using the Average Oracle than when using NLS, as expected from the Frobenius norm. However, quite remarkably, AO is also better than the Oracle eigenvalues when . We use the same shuffling procedure of the previous section to check the importance of correlation time evolution. The Average Oracle still outperforms the Oracle and NLS for small enough . i.e., in the high-dimensional case. These two results are all the more remarkable since the Oracle (and thus NLS) was shown to be optimal also for portfolio optimization (theorem 4.1 in Ref. [7]). Let us remark here that reality differs from the assumptions of this theorem in three key ways: the realized covariance matrix is only relevant for a finite number of time steps in the future, this matrix evolves as a function of time, and the calibration data matrix is in the finite-size regime. This implies that in real-life conditions, minimizing the Frobenius norm (or maximizing the Sharpe ratio with calibration data only) is not optimal for portfolio optimization [14].

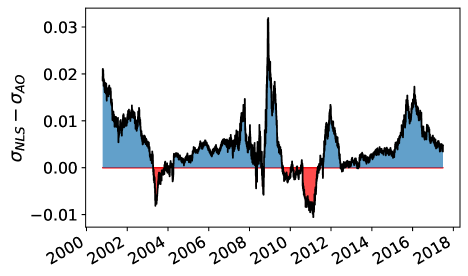

The Average Oracle outperforms NLS most of the time: plotting the average realized volatility as a function of time (Fig. 8), one sees that there are only a few periods during which AO loses to NLS, that there seems to be no difference between the AO calibration period (until 2005) and the testing period (from 2006), and finally that the advantage of AO does not decrease as time goes on.

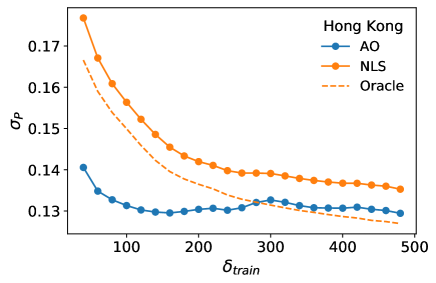

As a final test, we applied the Average Oracle calibrated with US data to Hong-Kong equity data and found qualitatively similar data (see appendix H). This strongly suggests that the AO captures a systematic time-varying effect found in two different systems with time-varying correlations.

Interestingly, the Average Oracle and the method (CV) we use to compute the NLS [11] share a common ingredient: CV is a -fold cross-validation scheme that computes Oracle eigenvalues from splits of into sub-intervals and averages them. Equivalently to our case, the two intervals and will refer to the train and test split of the -fold approach. It is important to point out that restricting the Oracle procedure to the interval implies that at least in of the intervals will have some data points in the past with respect to , leading to an overestimation of the overlap matrix . Differently, our method uses 20 years of data and respects causality (time ordering) between and time windows. The reason why AO outperforms NLS is causality; hence, time ordering needs to be preserved in systems with time-evolving correlations. Note finally that NLS can be computed with other numerical methods which yield similar performance.

We note that NLS can also be applied to z-scores of asset price returns instead of on the returns themselves. In this case, we find that NLS leads to smaller GMV portfolio variance on average, still larger than AO, but with a significantly larger Frobenius distance. This means that the Average Oracle provides a hands-off approach to covariance cleaning and does not require complex computations. Once calibrated, the AO is much faster than NLS.

Discussion

By outperforming the optimal estimators for time-invariant covariance matrices, our method shows the need for (and the possibility of) further improvement. Indeed, real systems are rarely time-invariant, and thus one needs to account for the evolution of the real covariance matrix. In such circumstances, we have shown that a simple zeroth-order eigenvalues filtering method that only retains an average dependence between past and future already outperforms known optimal solutions for constant covariance matrices.

The Average Oracle is a first step towards accounting for temporal evolution when filtering covariance matrices, as it is a zeroth-order correction. Beyond time-invariant eigenvalues, AO can also include exponentially weighted moving averages, as in [15, 16], which results in a slight improvement, as shown by preliminary results. Any additional knowledge about the underlying system may help design higher-order corrections to our method. This knowledge may not come from the covariance matrix itself but from possibly higher-order dependence measures, such as triads, which are much better at predicting the instability of the sign of correlation coefficients (see Ref. [17]).

The fact that the average influence of the future on the correlation matrix eigenvalues is more informative than the empirical eigenvalues themselves suggests ways to extend analytical results. Similarly, it is natural to quantify how much exploitable information lies in the difference between the empirical and Oracle eigenvalues, i.e., how to mix the Average Oracle eigenvalues with the empirical ones from the training period.

Financial literature proposes complex dynamical models of correlation [9, 18, 19, 20] that also contains a mechanism to account for the evolution of both eigenvalues and eigenvectors. They are generally computationally much more demanding than AO and rely on strong modeling assumptions. A full comparison between portfolios produced by the naive, model-free, and fast AO and sophisticated DCC-based methods will be reported in future work.

References

- [1] Michele Tumminello, Fabrizio Lillo, and Rosario N Mantegna. Hierarchically nested factor model from multivariate data. EPL (Europhysics Letters), 78(3):30006, 2007.

- [2] Christian Bongiorno and Damien Challet. Reactive global minimum variance portfolios with k-bahc covariance cleaning. The European Journal of Finance, pages 1–17, 2021.

- [3] Joël Bun, Jean-Philippe Bouchaud, and Marc Potters. Cleaning large correlation matrices: tools from random matrix theory. Physics Reports, 666:1–109, 2017.

- [4] Laurent Laloux, Pierre Cizeau, Jean-Philippe Bouchaud, and Marc Potters. Noise dressing of financial correlation matrices. Physical Review Letters, 83(7):1467, 1999.

- [5] Vasiliki Plerou, Parameswaran Gopikrishnan, Bernd Rosenow, Luís A Nunes Amaral, and H Eugene Stanley. Universal and nonuniversal properties of cross correlations in financial time series. Physical Review Letters, 83(7):1471, 1999.

- [6] Olivier Ledoit, Michael Wolf, et al. Nonlinear shrinkage estimation of large-dimensional covariance matrices. The Annals of Statistics, 40(2):1024–1060, 2012.

- [7] Olivier Ledoit and Michael Wolf. Nonlinear shrinkage of the covariance matrix for portfolio selection: Markowitz meets goldilocks. The Review of Financial Studies, 30(12):4349–4388, 2017.

- [8] Joël Bun, Romain Allez, Jean-Philippe Bouchaud, and Marc Potters. Rotational invariant estimator for general noisy matrices. IEEE Transactions on Information Theory, 62(12):7475–7490, 2016.

- [9] Robert F. Engle, Olivier Ledoit, and Michael Wolf. Large dynamic covariance matrices. Journal of Business & Economic Statistics, 37(2):363–375, 2019.

- [10] TT Chen, B Zheng, Y Li, and XF Jiang. Temporal correlation functions of dynamic systems in non-stationary states. New Journal of Physics, 20(7):073005, 2018.

- [11] Daniel Bartz. Cross-validation based nonlinear shrinkage. arXiv preprint arXiv:1611.00798, 2016.

- [12] Parameswaran Gopikrishnan, Vasiliki Plerou, Luis A Nunes Amaral, Martin Meyer, and H Eugene Stanley. Scaling of the distribution of fluctuations of financial market indices. Physical Review E, 60(5):5305, 1999.

- [13] Joël Bun, Jean-Philippe Bouchaud, and Marc Potters. Overlaps between eigenvectors of correlated random matrices. Physical Review E, 98(5):052145, 2018.

- [14] Christian Bongiorno and Damien Challet. Non-linear shrinkage of the price return covariance matrix is far from optimal for portfolio optimisation. Finance Research Letters, page 103383, 2022.

- [15] Marc Potters, Jean-Philippe Bouchaud, and Laurent Laloux. Financial applications of random matrix theory: Old laces and new pieces. Acta Physica Polonica B, 36:2767, 2005.

- [16] Vincent WC Tan and Stefan Zohren. Large non-stationary noisy covariance matrices: A cross-validation approach. arXiv preprint arXiv:2012.05757, 2020.

- [17] Christian Bongiorno and Damien Challet. Non-parametric sign prediction of high-dimensional correlation matrix coefficients. EPL (Europhysics Letters), 133(4):48001, 2021.

- [18] Cavit Pakel, Neil Shephard, Kevin Sheppard, and Robert F Engle. Fitting vast dimensional time-varying covariance models. Journal of Business & Economic Statistics, 39(3):652–668, 2021.

- [19] Gianluca De Nard, Olivier Ledoit, and Michael Wolf. Factor models for portfolio selection in large dimensions: The good, the better and the ugly. Journal of Financial Econometrics, 19(2):236–257, 2021.

- [20] Guilherme V Moura, André AP Santos, and Esther Ruiz. Comparing high-dimensional conditional covariance matrices: Implications for portfolio selection. Journal of Banking & Finance, 118:105882, 2020.

- [21] Vasiliki Plerou, Parameswaran Gopikrishnan, Luis A Nunes Amaral, Martin Meyer, and H Eugene Stanley. Scaling of the distribution of price fluctuations of individual companies. Physical Review E, 60(6):6519, 1999.

- [22] Michele Tumminello, Fabrizio Lillo, and Rosario N Mantegna. Kullback-leibler distance as a measure of the information filtered from multivariate data. Physical Review E, 76(3):031123, 2007.

Acknowledgements

This publication stems from a partnership between CentraleSupélec and BNP Paribas and used HPC resources from the “Mésocentre” computing center of CentraleSupélec and École Normale Supérieure Paris-Saclay supported by CNRS and Région Île-de-France.

Code: a notebook is available at

https://gitlab-research.centralesupelec.fr/2019bongiornc/average-oracle-cleaning.

Appendix A Data

We use about 25 years of daily data for about US equities from which we compute returns adjusted for splits, reverse splits and dividends. When computing Oracle eigenvalues, we applied two asset selection filters.

We applied two asset selection filters. First, for a given time subinterval and its corresponding subinterval, we only keep the assets that have less than of zero or missing values in the train window in order to avoid undefined standard deviation during the shuffling procedure. Some assets do not have data for the whole period. Other causes for missing data or zero values are technical issues or trading stops. We did not apply the same filter to the test window so as to avoid using future information in our analysis.

In addition, we require that no pair of assets in our subset have a correlation coefficient larger than in the train window to avoid duplicated assets (for example, different asset classes of the same company).

Appendix B Dealing with large fluctuations of univariate variance

When the variance of individual time series is not constant, one should apply the AO method on the correlation matrix, i.e., compute the AO eigenvalues on data standardized in and separately, and use them to replace the eigenvalues of the correlation matrix computed in . As this is clearly the case with financial data, all the results reported here that use financial data use this kind of standardization. The filtered covariance matrix is then defined as the filtered correlation matrix suitably multiplied by the individual standard deviation (see Eq. (12)).

Appendix C Dependence of the Average Oracle eigenvalues on the next subinterval length

We checked that the Oracle eigenvalues can be considered independent from the window length . In Fig. 9, we show that the AO eigenvalues for different fixing days: the estimator is only weakly sensitive to the test window length. This observation supports the idea that the AO procedure can extract the underlying time-invariant part of the eigenvalue dynamic. Note that by reducing the test window, the estimation becomes noisier and thus requires more train and test windows (denoted by ) to yield average eigenvalues with the same level of precision.

Appendix D Influence of overlaps in synthetic data with time-evolving covariance matrices

The empirical findings about overlaps in the main text suggest a simple model with a fixed set of true eigenvalues and a dynamical set of eigenvectors . To mimic the real heterogeneity of the eigenvalues, we choose a geometric progression of the eigenvalues, whereas the initial eigenvector basis is chosen randomly from the group. At each time-step, the eigenvectors are rotated with rotation matrix , which yields

| (15) |

In order to control the amount of rotation, we decompose the rotation matrix as elementary plane rotation according to the canonical basis, which corresponds to the decomposition of the rotation matrix in Euler angles

| (16) |

The limit corresponds to constant eigenvectors and constant covariance. In order to test different levels of time dependence, we sampled independently from a normal distribution with expected value and standard deviation .

To simulate the data, we used a factor model

| (17) |

where

| (18) |

and are sampled from independent standardized normal or Student t-distributions.

According to this definition,

| (19) |

since is the identity and are deterministic.

D.1 Simulations

Because the eigenvalues are kept fixed in this model, Eq. (8) stipulates that it is enough to compute the average in order to obtain the Average Oracle. To this end, we generate 1,000 simulations for each parameter in the following way. For each simulation, we produce a data matrix of elements and records which represents the full historical dataset. The last records will be kept as the test window, while the first will be the calibration window. The small choice was necessary due to the non-negligible computational effort to apply the Euler angles rotations.

We first compute the average overlap matrix from random consecutive time intervals of length drawn from the calibration window; this is done in two ways, as described in the main text: first by keeping the original time order of the data, and then by building a shuffled data set, which yields the time-dependent and time-independent average overlap matrices. Finally, we compute the train eigenvectors from the last records of the calibration window.

Then, the two AO estimators corresponding to are obtained with

| (20) |

and the RIE estimator as

| (21) |

We included the true eigenvalues in the estimator to reduce the amount of noise in the benchmark and to focus on the effect of the eigenvector rotation. Finally, we compute the Frobenius distance between the estimators and from the test window.

In Fig. 10, we show that for no difference between the two estimators is detected, as such a case corresponds to the limit of a constant world. Similarly, for very large, we do not observe any significant difference between the two estimators, as the temporal evolution is so fast that it destroys any relationship between past and future, and both estimators converge to the identity. Finally, for intermediate values of , the time-dependent estimator outperforms the time-independent one. It is worth reporting that for the case of Student t-distributed variables, the discrepancy between the two estimators increases when the degree of freedom of the t-distribution decreases. This is particularly relevant for financial applications, where the returns are characterized by heavy tails with on average [21].

Appendix E Kullback–Leibler Divergence

For the sake of completeness, we include a comparison between the covariance estimators and realized covariance matrix by using the Kullback–Leibler (KL) divergence and compare our results with those for the Frobenius distance.

The KL divergence of the two distributions and measures the amount of information lost if is used to approximate . It is defined as

| (22) |

which is the expectation according to distribution of the log difference . Some authors proposed the KL divergence as an alternative metric to the Frobenius distance when comparing correlation or covariance matrices [22].

In case of two multivariate central normal distribution data with respective covariance matrices and , eq. (22) reduces to

| (23) |

Unfortunately, there is no closed analytical expression for the KL divergence for multivariate t-distributions

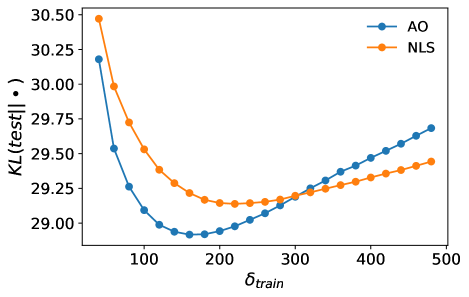

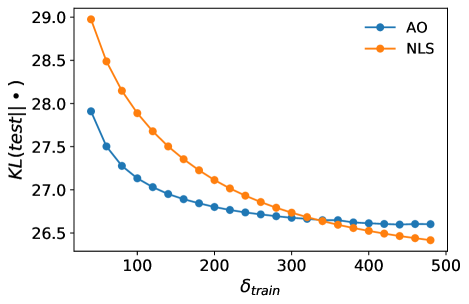

The average KL divergence in base over the validation window is reported in Fig. 11. It is important to remark that Eq. (23) is not defined if one of the two covariance matrices has at least one null eigenvalue. While the RIE is always positive-defined, it is possible that the test covariance matrix is not. Those cases were not considered in our analysis.

The results for the KL divergence reported for the time-ordered data are compatible with those for the Frobenius norm: the AO estimator outperforms NLS, with an optimal calibration window around days. For the shuffled case, we observe an important difference from the Frobenius norm results since AO outperforms NLS for small training windows days. The behavior of both curves, in this case, is monotonically decreasing, which is expected since, in a world with constant covariance matrices, more data always yields a better estimation. We suspect that such difference might be due to a higher sensitivity of the KL divergence to overfitting in the train window; thus, a small should affect more NLS than AO. The fact that NLS outperforms AO for large in the shuffled case is to be expected, as NLS is optimal in the asymptotic regime of and large for time-independent covariance matrices.

Appendix F Optimal Test Window Length of the Estimators

In this section, we explored how the performance changes as the length of the test window varies.

In the upper panel of Fig. 12 we show the Frobenius norm between the estimators and the test covariance. For very small time horizons, all estimators reach a high distance with the test covariance. This is probably due to the high sample size error on the test covariance if it is computed over a short time window. In addition, we observe that the Frobenius norm of the NLS estimator has a minimum at around days, a further increase of decreasing its performance. On the other hand, the AO estimator is much more stable for large . This supports the intuition that AO can really extract the time-invariant part of the system evolution.

Looking at the volatility of the GMV portfolio, we observe that the global minimum is reached for all estimators at the smallest then it increases approximately linearly with . The latter is not in contradiction with the results of the Frobenius norm since the global optimal minimum of the volatility changes as increases. In simple words, with a single portfolio held for two years, it is impossible to reach the same low volatility of a portfolio updated weekly.

Appendix G System size dependence

In this section, we explored how the performance changes as the system size varies.

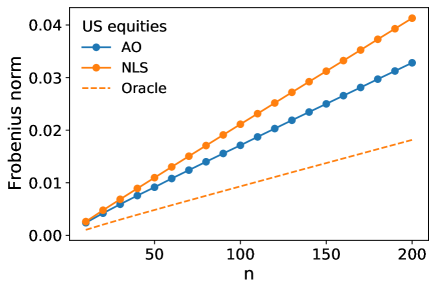

In the upper panel of Fig. 13 we show the Frobenius norm distance for the three estimators. As increases, the distance between the three estimators and the test covariance matrix increases. This is expected since the eigenvalue correction is only applied to degrees of freedom, whereas the Frobenius norm increases as . It is worth remarking that the AO estimator outperforms the NLS for all the values of

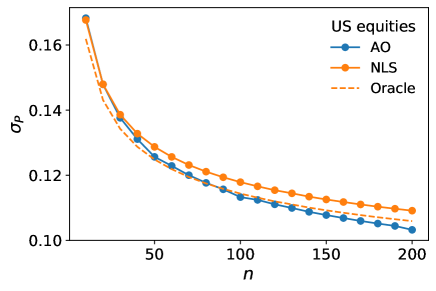

In the lower panel of Fig. 13 we show the GMV portfolio volatility as a function of . As in the previous case, changing the number of stocks changes the optimal minimum reachable on the test window: the larger , the more possibilities one has to obtain a low-volatility portfolio. In addition, we observe that the relative discrepancy between the AO and NLS estimator increases with .

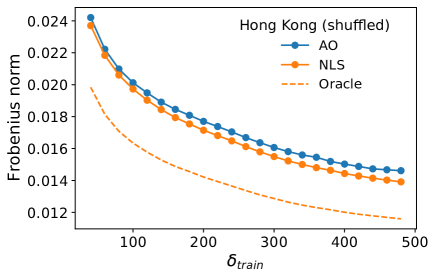

Appendix H Hong Kong Stock Exchange

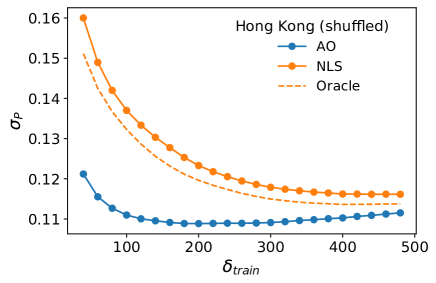

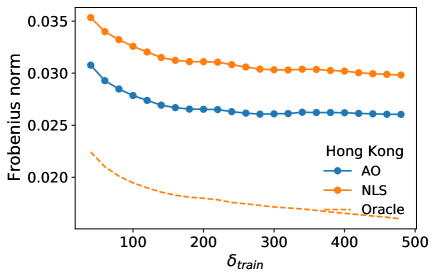

We took the AO eigenvalues calibrated with US equities data and used them to filter covariance matrices from the Hong Kong stock exchange data from the [2004-01-01,2017-06-23] period. In Fig. 14 we show the Frobenius distance between the covariance estimator and the out-of-sample covariance matrix. As for US equities, the AO provides a better estimator of the out-of-sample covariance matrix for the regular time series while being worse for shuffled data.

In Fig. 15, we show the realized variance of global minimum portfolios. As for the US equities, the AO yields lower variance than the Oracle for short calibration windows; AO also beats NLS for all the calibration window lengths that we tested, both for the regular and shuffled cases.