Network Regression and Supervised Centrality Estimation

Abstract

The centrality in a network is a popular metric for agents’ network positions and is often used in regression models to model the network effect on an outcome variable of interest. In empirical studies, researchers often adopt a two-stage procedure to first estimate the centrality and then infer the network effect using the estimated centrality. Despite its prevalent adoption, this two-stage procedure lacks theoretical backing and can fail in both estimation and inference. We, therefore, propose a unified framework, under which we prove the shortcomings of the two-stage in centrality estimation and the undesirable consequences in the regression. We then propose a novel supervised network centrality estimation (SuperCENT) methodology that simultaneously yields superior estimations of the centrality and the network effect and provides valid and narrower confidence intervals than those from the two-stage. We showcase the superiority of SuperCENT in predicting the currency risk premium based on the global trade network.

keywords:

Cai: Department of Statistics and Data Science, The Wharton School, University of Pennsylvania, Philadelphia, PA 19104, USA (email: junhui@wharton.upenn.edu); Yang: Innovation and Information Management, Faculty of Business and Economics, The University of Hong Kong, Hong Kong, China (email: dyanghku@hku.hk); Zhu: Department of Finance, School of Economics and Management, Tsinghua University, Beijing, 100084, China (email: zhuwu@sem.tsinghua.edu.cn); Shen: Innovation and Information Management, Faculty of Business and Economics, The University of Hong Kong, Hong Kong, China (email: haipeng@hku.hk); Zhao: Department of Statistics and Data Science, The Wharton School, University of Pennsylvania, Philadelphia, PA 19104, USA (email: lzhao@wharton.upenn.edu).

1 Introduction

In economics, finance, operations, sociology, and many other disciplines, agents (individual persons, firms, industries, and countries, etc.) are usually connected through different relationships. The collection of the agents and their relationships is usually represented by a network. One extremely influential concept of networks is the agents’ positions, because they can induce a wide range of behaviors, including individuals’ decisions on education and human capital investment (Jackson et al.,, 2017), information sharing and advertisement (Banerjee et al.,, 2019, Breza and Chandrasekhar,, 2019), coalition for exchange or cooperation (Elliott and Golub,, 2019), firms’ investment decision-making (Allen et al.,, 2019), the identification of banks that are too-connected-to-fail (Gofman,, 2017), and stock returns (Ahern,, 2013, Richmond,, 2019).

An agent’s position or importance is usually captured by the so-called centrality, which measures how central the agent is in comparison to the others in a network. Since the position induces the agent’s behavior and thus shapes certain outcomes, the network centrality is often used as an intermediary to measure the network effects on the outcome of interest (Ahern,, 2013, Shao et al.,, 2018, Richmond,, 2019, Allen et al.,, 2019, Banerjee et al.,, 2019, Bovet and Makse,, 2019). There are many kinds of definitions of centrality (Jackson,, 2010, Kolaczyk,, 2010), among which we focus on the hub and authority centralities (Kleinberg,, 1999), of which the eigenvector centrality is a special case. See a brief overview of centralities and concrete examples on the implication of centralities in Section 2.

The value of network centralities is, therefore, two-fold: first, the centralities have natural implications on the importance of agents; second, the centralities are often used as regressors in a regression to model the network effects on some outcome of interest. In practice, the centralities are not directly observable while the network is. Hence, the two-fold value of centralities leads to two goals of this article:

-

(G1)

Estimate centralities from an observed network;

-

(G2)

Estimate and conduct inference of the network effects through the centralities.

In empirical studies including many of the above-cited, these two goals are usually achieved in sequential order, to which we refer as the two-stage procedure throughout this article. Stage 1 targets goal (G1) solely, which estimates centralities by performing the singular value decomposition (SVD) on the adjacency matrix that represents the network. Stage 2 aims at goal (G2) next, which estimates the network effects by regressing the outcome on the estimated centralities from Stage 1 and conducts inference using the naive confidence intervals from the regression, an ad-hoc inference, ignoring the centrality estimation error. The drawbacks of such two-stage procedure are that: Stage 1 only uses the information from the network to estimate centralities, without resorting to the auxiliary information from the regression on the centralities, which leads to an inaccurate estimation of the centralities due to large observational errors in the network (see more evidence in Section 2); Stage 2 is contingent on Stage 1 – regressing the outcome on the inaccurately estimated centralities further results in an inaccurate estimation of the regression coefficients, thereby invalidating the inference. Consequently, these two stages do not achieve the two goals at their best.

Motivated by the two goals and the shortcomings of the two-stage procedure, we first propose a unified framework that encapsulates two models for the corresponding two goals: one network generation model based on centralities for goal (G1) and one network regression model for the dependency of the outcome on the centralities for goal (G2). We further propose a novel supervised network centrality estimation (SuperCENT) methodology that accomplishes both (G1) and (G2) simultaneously, instead of sequentially. SuperCENT exploits information from the two models – the network regression model contains auxiliary information on the centrality in addition to the network, providing supervision to the centrality estimation. The supervision effect can improve the centrality estimation, which in turn benefits the network regression. In other words, the centrality estimation and the network regression complement and empower each other.

Under the unified framework, we derive the theoretical convergence rates of the centralities and the regression coefficients estimators via the two-stage and SuperCENT, as well as their asymptotic distributions, which can be used to construct confidence intervals. Comparing the two methods, SuperCENT universally dominates the two-stage theoretically and empirically in terms of centrality estimation (G1) as well as the estimation and inference of the network regression coefficients (G2). We summarize our contributions of this article in the following.

-

1.

To the best of our knowledge, we are the first to provide a unified framework to study properties of centrality estimation, centrality inference, and the subsequent network regression analysis when a noisy network is observed.

-

2.

We demonstrate that the common practice of two-stage can be problematic. For centrality estimation (G1), the two-stage centrality estimates using SVD in Stage 1 are inconsistent under large noise in the network. The same inconsistency phenomenon appears when we estimate the true underlying network. This finding of inconsistency extends the phase transition phenomenon of the singular vectors (Shabalin and Nobel,, 2013) and eigenvectors (Shen et al.,, 2016) to the network centrality problem. For the network regression (G2), the centrality coefficients estimates are biased and inconsistent given the inconsistent centrality estimates from Stage 1 and the ad-hoc inference can be either conservative or invalid depending on the network noise level.

-

3.

We show theoretically and empirically that the proposed SuperCENT dominates the two-stage universally. For (G1), SuperCENT yields superior estimations of both the centralities and true network over the two-stage. For (G2), SuperCENT can mitigate the coefficients estimation bias and thus boost the estimation accuracy under large network noise thanks to the superior centrality estimation. In addition, SuperCENT provides confidence intervals that are valid and narrower than the ad-hoc two-stage confidence intervals.

-

4.

Lastly, we apply SuperCENT and the two-stage to predict the currency risk premium, based on an economic theory on the relationship between a country’s currency risk premium and its importance within the global trade network. We show that a long-short trading strategy based on the SuperCENT centrality estimates yields a return three times as high as those by the two-stage procedure. Furthermore, SuperCENT can verify the economic theory via a rigorous statistical test while the two-stage fails.

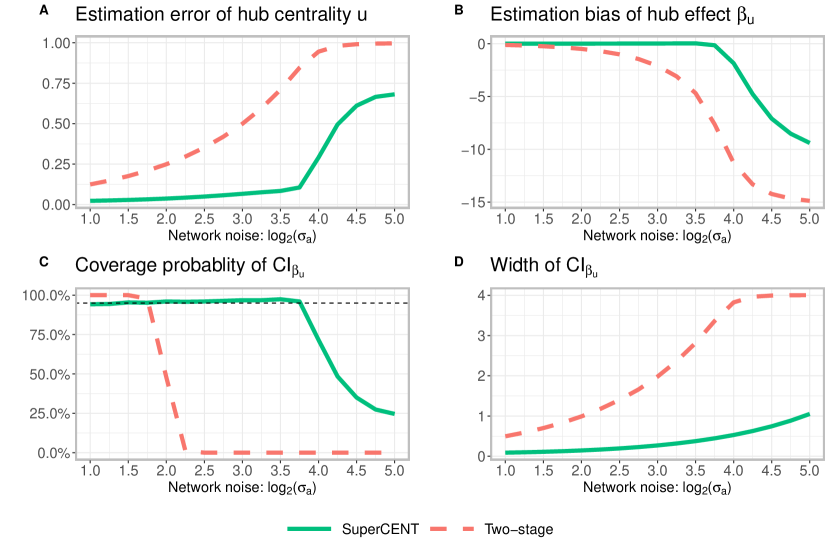

As a concrete manifestation of our contributions, we perform a toy experiment as follows. The network is constructed by perturbing a true network with noise of different level . The regression model includes both the hub and authority centralities, and , with their corresponding coefficients and , as well as other covariates111The detail of the network model is: , where the true hub centrality is , the true authority is , both of which are scaled to have norm , and contains i.i.d. normal random variables with mean zero and variance . For the regression model: where , the covariate matrix consists of a column of 1’s and two columns whose entries follow independently, and follows with . We vary the network noise level and each configuration is repeated 500 times. . Figure 1 shows the performance of the two-stage procedure and SuperCENT in terms of estimation of and as well as the coverage probability and the width of confidence interval (CI) for the hub centrality coefficient with varying network noise levels . Figure 1A shows the error of the hub centrality estimation. As the noise level increases, the two-stage estimate becomes increasingly inaccurate and eventually orthogonal to the truth, corroborating our inconsistency finding of the two-stage under large network noise. On the contrary, SuperCENT estimates very accurately until the network noise becomes very large. Even then, the accuracy of the SuperCENT estimate does not deteriorate to zero thanks to the auxiliary information from the regression. Figure 1B exhibits the estimation bias of : the two-stage estimate suffers from a severe attenuation bias while SuperCENT alleviates the bias. Figures 1C-D illustrate the coverage probability and the width of the confidence interval of . Depending on the noise level in the network model, the ad-hoc two-stage inference has different undesirable consequences: when the noise is small, the ad-hoc two-stage confidence interval is still valid but conservative; when the noise is large, the ad-hoc two-stage confidence interval is invalid and wider than necessary. In contrast, SuperCENT provides a valid and narrower confidence interval until the network noise becomes unreasonably large.

Our paper contributes to several lines of inquiry in the network and econometrics literature on network modeling, network regression with centralities, covariate-assisted network modeling, network effect modeling, and measurement error. First, the proposed unified framework unites the literature on the noisy network and network regression with centralities. Most existing network literature focuses on only one of the two aspects in our unified framework. On one hand, in the presence of noisy network generation, there are many empirical studies (Lakhina et al.,, 2003, Banerjee et al.,, 2013, Breza et al.,, 2020, Zhu and Yang,, 2020) and many that try to estimate or recover the true network without involving centrality (Butts,, 2003, Handcock and Gile,, 2010, Chandrasekhar and Lewis,, 2011, Le et al.,, 2018, Newman,, 2018, Rohe,, 2019). On the other hand, many researchers focus on the network regression model with centralities while ignoring the noise of the centrality estimation inherited from the noise of the network (Ahern,, 2013, Hochberg et al.,, 2007, Shao et al.,, 2018, Richmond,, 2019, Allen et al.,, 2019, Liu,, 2019, Banerjee et al.,, 2019, Bovet and Makse,, 2019, Fogli and Veldkamp,, 2021).

Our unified framework is also connected to the line of research related to network with covariates supervision (Newman and Clauset,, 2016, Zhang et al.,, 2016, Li et al.,, 2016, Graham,, 2017, Binkiewicz et al.,, 2017, Yan et al.,, 2019, Ma et al.,, 2020, Chen et al.,, 2021). One major difference is that SuperCENT uses both the covariates and the response to supervise, instead of only the covariates. And they focus mostly on network formation or community detection.

In econometrics, there has been a significant effort to model the network effect on an outcome of interest through regression. See De Paula, (2017) for a review on the econometrics of network models. One popular approach follows the pioneer work of Manski, (1993), the “reflection model” (Lee,, 2007, Bramoullé et al.,, 2009, Lee et al.,, 2010, Hsieh and Lee,, 2016, Zhu et al.,, 2017). This approach handles the network effect through the observed adjacency matrix itself, not through centralities like ours. There is also a recent surge of literature in network recovery based on the reflection model (De Paula et al.,, 2019, Battaglini et al.,, 2021). Literature on this approach mainly focuses on the issue of identifiability, while our work attends to both the estimation and inference of the network effect. Nevertheless, it is possible to incorporate our model into the reflection model by assuming a low-rank structure on the true underlying network. Another popular approach assumes that the outcome depends on individual fixed effects, which are only estimable by imposing constraints or penalties, and the role of the network is cast through the Laplacian matrix, such that connected nodes share similar individual fixed effects (Jochmans and Weidner,, 2019, Li et al.,, 2019, Le and Li,, 2020). This approach emphasizes the network homophily, while ours concentrates on nodes’ position or importance in the network using centralities.

Lastly, our methodology further contributes to the measurement error literature. Most literature concerns a regression setup where the covariates are observed with errors, which leads to bias in the coefficient estimation (Garber and Klepper,, 1980, Griliches,, 1986, Pischke,, 2007, Wooldridge,, 2015, Abel,, 2017). We extend it to the network regression problem. Specifically, the two-stage procedure resembles the measurement error problem where the estimated centralities that are used as covariates in the regression of Stage 2 contain estimation error. Nevertheless, the derivation of the two-stage bias is not a trivial extension of the classical results because it involves the asymptotic joint distributions of the two-stage centrality estimators. Furthermore, SuperCENT corrects the bias problem in the regression coefficient estimation induced by the estimation errors and provides valid inference for the regression coefficients.

The rest of this article is organized as follows. Section 2 reviews the concept and properties of networks, network centralities, noisy networks, and provides concrete examples of network centralities and their effects on the outcome variables. Section 3 formally introduces the unified framework and makes connections with the existing work. Details of the proposed SuperCENT methodology are provided in Section 4. Theoretical properties are studied in Section 5 and the simulation study is demonstrated in Section 6. Section 7 presents the case study of the global trade network centralities and their relationships with risk premiums. Section 8 concludes with a summary and future work. Some concrete mathematical expressions, a special case of an undirected network with the eigenvector centrality, more simulation results, additional information of the case study, and the proofs are delegated to the supplementary materials. A new R package called SuperCENT implements the methods (https://jh-cai.com/SuperCENT).

2 Network and network centrality

In this section, we provide background knowledge and a literature review on networks and network centralities. We review how network centralities are used in various fields, particularly via the above-mentioned two-stage procedure, and point out the challenge in centralities estimation due to observational errors in networks. Sophisticated readers may skip this section.

In a network, the nodes are agents involved in a network of relationships and the edges represent the relationships between the nodes. The edges can be directed or undirected depending on whether the relationships are reciprocal. For a directed network composed of nodes and a set of weighted directed edges , it can be represented by an asymmetric adjacency matrix where is the weighted edge from node to .

A full description of the network depends on all the nodes and edges, whose information is too much to be thoroughly understood in empirical analysis. To feasibly analyze the network, researchers usually resort to dimension reduction or low-rank approximation to extract the characteristics and structural properties. Centralities are common low-rank summaries of the network information. Depending on goals and domain knowledge, researchers have used multiple versions of centralities. We refer readers to Chapter 2 of Jackson, (2010), Chapter 4 of Kolaczyk, (2010) or Chapter 1 of Graham and De Paula, (2020) for a comprehensive introduction to centralities.

In this article, we focus on the hub and authority centralities for directed networks (Kleinberg,, 1999, Benzi et al.,, 2013), which can be reduced to eigenvector centrality for undirected networks. For directed networks, there is a distinction between the giver and the recipient, such as the citee-citor in citation networks or webpage networks, the exporter-importer in trade networks, and the investor-investee in investment networks. The concept of “hubs and authorities” originated from web searching. Intuitively, the hub centrality of a web page depends on the total level of authority centrality of the web pages it links to, while the authority centrality of a web page depends on the total level of hub centrality of the web pages it receives links from. Similar intuition can be applied to citation networks where the hub centrality of a paper reveals the quality of a survey paper while an authoritative paper is one that is cited a lot by well-respected survey papers.

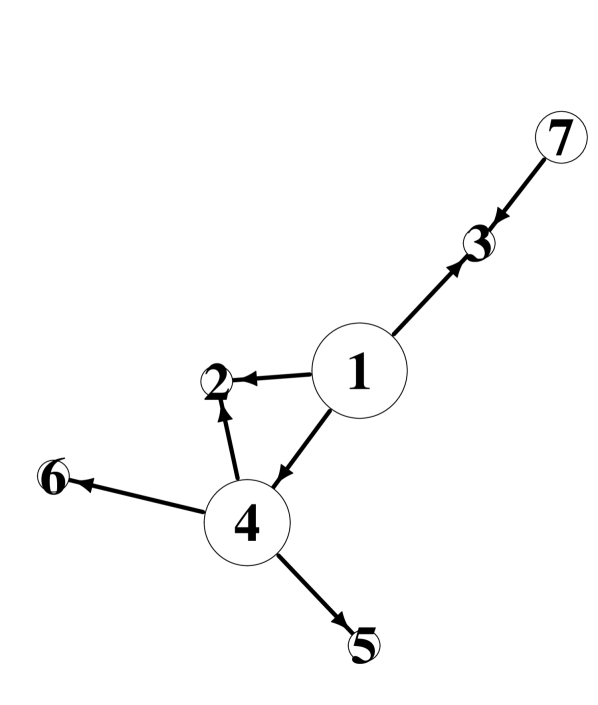

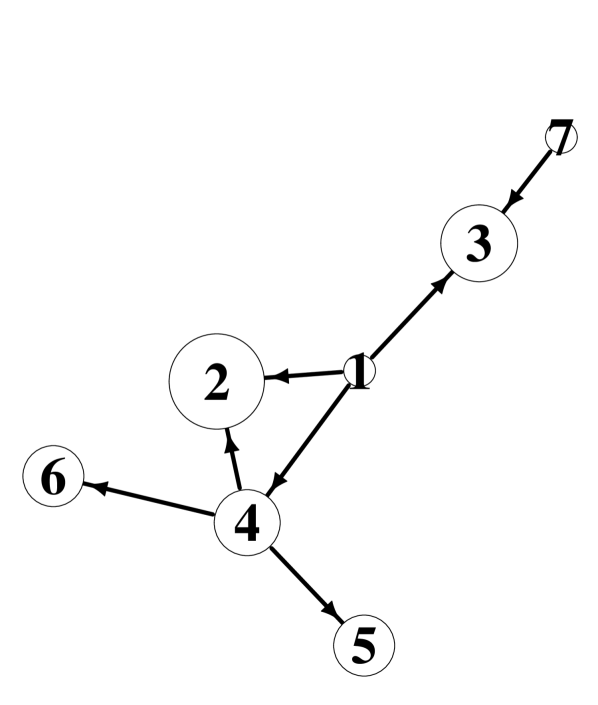

Let us use a toy example to further illuminate the intuition behind the hub and authority centralities. Consider a citation network where each paper is a node and an edge from Paper A to Paper B indicates Paper A cites Paper B. Figure 2(a) shows an example of the adjacency matrix of such network. Figures 2(b) and 2(c) show the same network with different node sizes: the node sizes in Figure 2(b) are proportional to the hub centralities while those in Figure 2(c) are proportional to the authority centralities.

To understand the hub centrality, note that Papers 1 and 4 are the major citors: they both cite three papers with Paper 2 being the common one. Except for the common one, Paper 4 cites Papers 5 and 6, which are only cited by Paper 4, and Paper 1 cites Papers 4 and 3, among which Paper 3 is cited twice. Therefore, compared with Paper 4, Paper 1 cites the same number of papers with one being cited more than the others. This makes the hub centrality of Paper 1 larger than that of Paper 4. One can think of Paper 1 as a better survey paper than Paper 4. Paper 7 cites only one paper, which makes its hub centrality smaller than Papers 1 and 4. The rest of the papers have small hub centrality since they do not cite other papers. As for the authority centrality, attention should be given to citees. Papers 2 and 3 both have two citations, but Paper 2 is cited by Papers 1 and 4 while Paper 3 is cited by Papers 1 and 7. Observe that Paper 4 as a hub is more influential than Paper 7. So the authority centrality for Paper 2 is the highest, followed by Paper 3. For the same reason, Paper 4 has higher authority centrality than Papers 5 and 6, since Paper 4 is cited by Paper 1 while Papers 5 and 6 are cited by Paper 4.

One can obtain the hub and authority centralities using an iterative method. Let denote the hub centrality and denote the authority centrality for node . Kleinberg, (1999) proposes to initiate each and with certain nonzero value and then iteratively update as follows:

| (1) |

This iterative algorithm is shown to converge under some regularity conditions with proper normalization; and the hub and authority centralities are the final and after convergence. This iterative algorithm is also well known as the power method to compute the leading left and right singular vectors of (Van Loan and Golub,, 1996). Due to the equivalence between singular value decomposition (SVD) and eigen-decomposition, the hub centrality is the leading left singular vector of and the leading eigen-vector of while the authority centrality is the leading right singular vector of and the leading eigen-vector of .

The hub and authority centralities and their variants are widely used in many fields to study how network positions affect a particular outcome of interest. In practice, as mentioned in Section 1, one needs to estimate the centralities and then use them as regressors in the subsequent regression to estimate the network effects. To achieve these two goals, the naive two-stage procedure has been widely used in the empirical studies although it lacks statistical justifications. In the following, we showcase some concrete examples on how centralities and the two-stage procedure are used in portfolio management, finance, and social media.

In portfolio management, recent research shows that, for a trade network of firms or industries or countries, a strategy that shorts portfolios of nodes with high centralities and longs those with low centralities yields significant excess return, where they use the two-stage procedure to provide empirical evidence (Hochberg et al.,, 2007, Ahern,, 2013, Richmond,, 2019). An accurate centrality estimate, therefore, can significantly boost the investment return. As a matter of fact, our case study in Section 7 shows that such a long-short strategy based on the centrality estimated using SuperCENT yields return three times as high as the existing method. In finance, financial institutions such as banks are usually linked through debt or equity, and thus an adversarial shock to one institution can be propagated to others via the debt or equity network (See Elliott et al., (2014), Glasserman and Young, (2016), Vohra et al., (2020) and references therein). When a central institution is subject to a severe adversarial shock, the shock will propagate and the impact will be significantly amplified, resulting in a systemic risk for the whole economy. Thus, identifying the central institutions in the network is the key for policymakers to impose additional supervision to mitigate concerns of systemic risk. To support their claims, many of the above-cited use the two-stage procedure for empirical evidence by regressing risk metrics on the estimated centrality of the financial institutions in a certain network. In social media such as Twitter or Facebook, networks often serve a role in information transmission or sharing. Individuals in the center of the social network, i.e., the “influencers”, can significantly expedite information dissemination (Shao et al.,, 2018, Bovet and Makse,, 2019). Identifying these central individuals can have a wide range of implications from marketing to information censorship.

One challenge of measuring centralities is that we often observe networks with observational error due to the cost of data collection (Lakhina et al.,, 2003, Banerjee et al.,, 2013, De Paula,, 2017, Breza et al.,, 2020, Zhu and Yang,, 2020). For example, to measure the social connections between people, researchers usually use the friendship on Facebook or Twitter to measure the tie, which is obviously not a perfect measure of the social connection strength. In particular, Banerjee et al., (2013) uses the self-reported friendship in villages of India to measure the social tie between villagers, which is subject to self-reporting and subjective bias. Zhu and Yang, (2020) uses the patent citations to measure the knowledge flow between companies, which neglects the communication among workers or executives. The measurement noise of the links could significantly worsen the estimation of the centrality; see Borgatti et al., (2006), Frantz et al., (2009), Wang et al., (2012), Martin and Niemeyer, (2019) and the references therein. The inaccurate centrality estimation will further affect the subsequent analysis.

3 A unified framework

3.1 Set-up and notation

We observe a sample of observations where is the response and is the vector of covariates for the -th observation as in the multivariate regression setting. The data can be represented in matrix form. Let denote the column vector of outcome and denote the design matrix with rows and columns. We consider the fixed design by treating fixed. In addition, we observe a weighted and directed network representing connections between the observations. Here, are the nodes corresponding to observations and is the set of directed edges. The directed network can be represented by an asymmetric adjacency matrix where if with edge weight and otherwise.

We adopt the following notation conventions. Given a matrix , define its Frobenius norm: , its operator norm: , and the vectorization operator that converts into a column vector of dimension as:

denotes the projection matrix that projects onto the column space of .

3.2 A unified framework

The hub and authority centralities are widely used in many fields as shown in Section 2, thanks to their natural implication on network positions. However, literature that investigates their statistical properties is scarce. The most direct model for them is based on the low-rank decomposition of the network as follows: the adjacency matrix for the observed directed network is generated by some underlying true hub and authority centralities corrupted with noise,

| (2) |

where the true authority and hub centralities are the parameters to be estimated, is the true network, and is the noise.

Such a low-rank mean plus noise model has been commonly adopted for matrix estimation or matrix denoise (Shabalin and Nobel,, 2013, Yang et al.,, 2016) and matrix completion (Candes and Plan,, 2010, Negahban and Wainwright,, 2011). Since the hub and authority centralities are the leading left and right singular vectors of respectively, it is natural to consider the noiseless rank-one structure for the network . This framework can be extended to general rank , although the implications of the non-leading singular vectors as centralities are unclear.

Note that and are only identifiable up to a scalar. Typically, in SVD, people assume and have unit length. However, in our framework of network analysis, we assume , in view of the fact that the network can grow and consequently the centralities should roughly be on the same scale no matter how large the network is. Furthermore, we assume the noise matrix has entries with zero mean, i.e., for .

Under Model (2), with an extra assumption that all entries of are i.i.d. with variance , Shabalin and Nobel, (2013) has shown that the angle between the leading left singular vector of and that of , i.e., the estimated hub centrality and the true hub centrality , can converge to a nonzero quantity or even asymptotically orthogonal as goes to infinity, if the signal-to-noise ratio is not large enough. This implies that the naive estimation of the centralities by implementing SVD on the observed network will fail in the presence of large noise.

Fortunately, when the naive estimation is inconsistent, it is still possible to obtain a consistent estimation of the centralities by including additional information from other sources. As we discussed in Sections 1 and 2, the positions of agents (nodes) impact the agents’ behaviors and thus shape their outcomes. Since the centralities measure the positions of nodes, researchers often study the relationship between the centralities and a certain response variable of interest so as to investigate the network effect. And this relationship contains an additional source of information for the centralities.

To explore such a relationship, the common practice is to regress the response variable on the estimated hub and authority centralities, which are obtained through the SVD of the observed network , not the true network . But the generative model is actually prescribed as follows: for the -th observation, the outcome depends on the true hub and authority centralities along with the covariates :

| (3) |

where is the vector of regression coefficients and are the coefficients of the hub and authority centralities respectively. The nuance of using the estimated versus the true centralities has consequences which we will explicate later. At this stage, no extra assumptions are imposed on the distribution of the regression error, except that we assume and . We further assume and is invertible.

Putting (2) and the matrix version of (3) together, we propose the following unified framework that encapsulates the two models:

| (4a) | ||||

| (4b) | ||||

With the unified framework (4) and the observed data , our original two goals of centrality estimation and network regression analysis can be specified as the following three: (i) estimate the true centralities and the true network ; (ii) estimate the regression coefficients of the predictors and the centralities ; (iii) construct valid confidence intervals for the centralities as well as the regression coefficients that account for the randomness in the observed network.

The unified framework unites our estimation goals and provides a theoretical framework to study the behaviors of the two-stage procedure. Furthermore, unifying the two models motivates our supervised network centrality estimation (SuperCENT) methodology, which we will describe formally in the next section. We name it the “supervised centrality estimation” because in the regression (4b) can be thought of as the supervisors that offer additional supervision to the centrality estimation. It is expected that if the centralities indeed have strong predictive power (that is, the centrality regression coefficients are large compared with the regression noise level ), the estimation of the centralities will be better when combining (4a) and (4b) together instead of only considering (4a). With the improved estimation of the centralities via the supervising effect, SuperCENT can further improve the estimation and inference in the regression model. A similar idea of supervision has also been implemented in matrix decomposition (Li et al.,, 2016), albeit the absence of response prediction.

Remark 1.

The unified framework (4) can be extended to a general case with rank , that is,

| (4ea) | ||||

| (4eb) | ||||

where and are orthonormal matrices of size and is a diagonal matrix with the singular values as the diagonal entries. Such a natural extension may contribute to the existing literature on regression with network information, because most existing papers consider the centralities as the predictors, which are the leading singular vectors. But potentially, the few leading singular vectors can offer additional predictive power as well.

4 Methodology

Given the unified framework (4), we first elaborate on the widely used two-stage procedure which first estimates the centralities and then estimates and provides inference for the centrality effects in the regression in Section 4.1. We then describe the SuperCENT methodology that simultaneously solves the centrality estimation and network regression in Section 4.2. Section 4.3 is devoted to the prediction problem where new nodes are included together with covariates and a corresponding new network. Section 4.4 describes strategies for tuning parameter selection in SuperCENT.

4.1 A naive two-stage procedure

As mentioned in Sections 1 and 2, given the unified framework (4) and the observed data , a natural and naive procedure is the two-stage estimator, which can serve as a benchmark. To make notations consistent, we now formally introduce the estimator.

In view of (4a), the first stage is to perform SVD on the observed adjacency matrix and take its leading left and right singular vectors and rescale them to have length , denoted as and , as the estimates for the centralities and respectively. The superscript ts stands for the two-stage procedure. In view of (4b), given the estimates and , the second stage performs the ordinary least square (OLS) regression of on and , treating as given covariates. To be specific, the two-stage procedure solves the following two optimization problems sequentially,

| (4fa) | ||||

| (4fb) | ||||

Algorithm 1 outlines the two-stage procedure.

-

1.

;

;

.

Remark 2.

Besides the estimation of the unknown parameters, valid inference is necessary to evaluate the network effect. In numerous empirical studies, researchers usually construct confidence intervals of the regression coefficients from the second stage regression by assuming that and are fixed and noiseless. This assumption simplifies the inferential statement because it follows that where . However, the observed network is one realization from as in Model (4a), which makes its singular vectors random. If one proceeds with inference ignoring the randomness, then the inference loses its justifications and the ensuing validity due to violation of the assumption. We refer to such “ad-hoc” confidence interval as the “two-stage-adhoc” method. To correct for the randomness of the estimated singular vectors and make valid inferences, the asymptotic distribution of the estimator is derived rigorously in Section 5. Remarks 5 and 7 further discuss the theoretical property of the two-stage-adhoc method. The toy experiment in Figure 1 and simulation results in Section 6 show that the two-stage-adhoc method is either conservative with low network noise level or invalid with high network noise level.

4.2 SuperCENT methodology

From the two-stage procedure, we observe that the second step of estimation and inference in the regression model depends on the first step of centrality estimation. The more accurate the centrality estimates are, the better we are able to make inference in the regression model. On the other hand, the centralities are incorporated in the regression model as regressors, have supervising effect on centrality estimation and can boost the estimation accuracy.

Motivated by the above intuition, we propose to optimize the following objective function to obtain the SuperCENT estimates,

| (4g) |

The above objective function combines the residual sum of squares (4fb) and the rank-one approximation error of the observed network (4fa). The connection between the two terms is the centralities. The tradeoff between the two terms can be tuned through a proper selection of the hyper-parameter . This idea is somewhat similar to the supervised SVD method in Li et al., (2016), but both the supervising mechanism and the optimization objective function of the SuperCENT are different.

To solve (4g), we can use a block gradient descent algorithm by updating iteratively until convergence, where . Such an iterative algorithm requires an initialization, which can be the first stage of the two-stage procedure, i.e., from the SVD of . The complete algorithm with a given tuning parameter is shown in Algorithm 2. We use to denote the estimations in the -th iteration. The derivation of Algorithm 2 and the algorithm for a symmetric network with the eigenvector centrality, a special case of Model (4), are deferred to the supplement. We will discuss the methods to choose in Section 4.4, including cross-validation and others.

-

1.

;

-

2.

;

-

3.

;

-

4.

;

-

5.

Normalize such that ;

-

6.

;

-

7.

Normalize such that ;

-

8.

;

Note that although and with length are only identifiable up to the sign, and are uniquely identifiable. One procedure to determine the sign of all the parameters is as follows: first, find the entry that has the largest magnitude in and , and make that entry positive so that the sign of either the hub centrality or the authority centrality can be fixed; then adjust the sign of the other centrality since the product is identifiable, and finally determine the signs of accordingly.

4.3 Prediction

Once the model is fitted with training data, it can be used for prediction. Suppose there are new observations, they have not only the new covariates and the new network among themselves , but also new edges connecting them with the training observations. The original network is augmented to as follows

| (4h) |

where is of size .

Given the augmented network and new covariates , the task is to make prediction for . To make use of the regression equation , it is necessary to estimate and . Similarly as (4a), we assume where and . Therefore, we obtain the model

| (4i) |

In view of (4i), to obtain estimates of and , one can either perform SVD of or SVD of and reserve only the relevant components of the singular vectors. The latter approach is more accurate and is formally described in Algorithm 3.

-

1.

are the left and right singular vectors of ;

and ;

and ;

Rescale and .

Remark 3.

(Sign and scaling issue) Since and are only identifiable up to sign, we determine their signs as Step 2 of Algorithm 3 such that the angles between the training proportions and the SuperCENT estimates are less than 90 degrees, i.e., and . In addition, and need to be scaled to match with and . Recall that for identifiability, and are of norm , and and are of the corresponding scale. In the prediction process, we need to scale and accordingly so that is on par with . Step 3 of Algorithm 3 is designed for this purpose.

4.4 Selection of the tuning parameter

The tuning parameter can be selected using the -fold cross-validation. Given the prediction procedure in Section 4.3, the cross-validation procedure can be easily carried out as follows. For each fold of validation data, we first fit the model using the remaining folds with the corresponding induced subnetwork and obtain the estimates for the regression coefficients by implementing Algorithm 2; we then obtain the estimates of the centralities for the validation data by applying Algorithm 3; we last obtain the total prediction error for the validation data by combining the outcomes from the first two steps. The best tuning parameter is set to be the minimizer of the total cross-validation error that sums over all folds. Algorithm 4 outlines this procedure in more detail.

Another strategy for selecting the tuning parameter is through generalized cross-validation (GCV), which can save computational time. Denote , then the GCV criterion is

| (4j) |

The explicit form of can be derived from the proof of the theorems. The performance of GCV is left for future investigation.

As a third strategy, Remark 12 in the next section offers an alternative way to choose the tuning parameter based on the theoretical analysis of SuperCENT, which is less time-consuming than cross-validation. However, we recommend using the cross-validation strategy for the best performance based on the simulation results.

-

0.

Split the covariates and response into training and

SuperCENT

SVD and re-scale by Algorithm 3;

;

5 Theoretical properties

We investigate the statistical properties of the two-stage procedure in Section 5.1 and SuperCENT in Section 5.2. The two main theorems provide the asymptotic distributions of the estimators under appropriate conditions, which can be used for inference. The corollaries state the convergence rates and the bias of the relevant quantities.

We first introduce some notations and assumptions. Recall that denotes the projection matrix, such as , and . Define , , which are the centralities projected onto the orthogonal space of . Denote and .

Assumption 1.

Under the unified framework (4), the noise of the network independently follows , and the noise of the outcome regression independently follows .

Assumption 2.

The fixed design matrix with and is invertible. The dimension is not diverging.

Assumption 3.

The scaled network noise-to-signal ratio .

In Assumption 1, the independence is assumed for simplicity. If the network noise or the regression noise are dependent with known covariance, the theorems and corollaries still hold with slight modifications; if they are dependent with unknown covariance, extra assumptions on the covariance structure need to be made and new methodologies and theories should be developed. Assumption 3 is required for the consistency of the SVD of the observed noisy network of model (4a), which can be seen from Corollary 1 below.

5.1 Theoretical properties for the two-stage procedure

Under the three aforementioned assumptions, the two-stage procedure in Algorithm 1 is consistent, and the asymptotic distribution of its estimators is given in Theorem 1. The convergence rates of the estimators are given in Corollaries 1 and 2. When Assumption 3 is violated, the two-stage procedure is no longer consistent – the centralities estimation is inconsistent in Stage 1, which leads to bias in the regression coefficients estimation in Stage 2 resembling the measurement error problem as shown in Corollary 3, consequently to the detriment of the inference.

Recall that the two-stage estimates from Algorithm 1 are denoted as , , and . Let be the estimate of .

Theorem 1.

Recall the two-stage procedure first estimates the centralities and and then plugs the estimated centralities into the regression model. Therefore, the asymptotic distributions for , and only depend on the noise from the network model, not the regression noise . This can also be seen in the definition of , where the three top left blocks are zeros.

Remark 4.

(Covariance of ) One important fact to emphasize is that the covariance of is not where , which is the classical results of regression when are considered fixed. This makes sense, as in our model, the observed network contains noise, which makes the estimated centralities from the first stage random quantities and invalidates the traditional covariance result. As a matter of fact, the bottom right three blocks of are not zero, which highlights this phenomenon. Corollary 2 further illustrates this fact and its consequences on the inference.

In what follows, we present the convergence rates of the estimated centralities , , and the network in Corollary 1, and the convergence rates of the regression coefficients and the prediction error in Corollary 2. In Corollary 3, we show the bias of and when the two-stage is inconsistent.

The convergence rates of the centralities depend on the selection of the loss function. Ideally, since the scales of the centralities are not fully determined, one prefers the loss function , which equals the squared sine of the angle between and , . However, the exact form of this loss function is not clean mathematically. Instead, we use the scaled Euclidean distance , which has a cleaner expression and is connected to the squared sine through . These two losses are approximately equivalent when the estimator is consistent and the loss goes to zero.

Corollary 1.

According to Corollary 1, the rate for in (4x) is and the rate for in (4y) is . They have the same order as , which suggests that the noise-to-signal ratio is the critical quantity that determines the consistency of the two-stage procedure.

Note that, for the two-stage procedure to be consistent, one needs as , which depends on the three parameters and their relationships. We first discuss two consistent scenarios: 1) the signal strength and the noise level are of constant order while diverges; 2) the noise level stays constant, but the signal strength can decrease when more nodes are collected for the network (because the network edge density might decay with more nodes), in which case as long as , still goes to zero. For real data, it is possible that the observed network gets noisier with more nodes and the signal strength decays . In this case, it is highly likely that the two-stage procedure will be inconsistent, for example, with a fast diverging noise level; then SuperCENT can improve the performance and remain consistent as discussed below in Section 5.2.

Corollary 2.

(Rate of ) Under the unified framework (4) and Assumptions 1, 2 and 3, the two-stage estimators satisfy

| (4aa) | |||||

| (4ab) | |||||

| (4ad) | |||||

| (4ae) | |||||

| (4ap) | |||||

Remark 5.

(Comments on (4aa)-(4ab) for ) For the variance of , the first term (4aa) is the typical expression for traditional regression with deterministic predictors. The additional term (4aa) is caused by the randomness of . Note that the second term (4aa) is non-negative and is zero if , or . Furthermore, the first term in (4ab) is of order while the second term is of order . So if and are of constant order and , the second term is of smaller order than the first term.

The above Theorem and Corollaries assume Assumptions 1-3. When Assumption 3 is violated, i.e., , the two-stage cannot estimate and consistently, and consequently and are biased.

Corollary 3.

Remark 6.

(Conditions for the bias of and ) Corollary 3 assumes either , namely the true regression model only involves two centrality predictors, both of which have measurement errors, or , namely the true regression model involves predictors without measurement error and two centrality predictors with measurement errors, but the noiseless predictors and two centrality predictors are uncorrelated. These assumptions are adopted so that the expression of the bias has intuitive explanations to be followed momentarily. In general, when the noiseless ones and the two centralities are correlated, the bias persists as long as the signal-to-noise of the network is small when , although the expressions are less comprehensive.

Remark 7.

(Special cases for the bias of and ) There are a few special cases for Corollary 3. (i) When , and . That implies that when and are consistent estimators of and respectively, the existence of the estimation error of the centralities does not affect the bias-ness of the second stage regression. This has correspondence to the errors-in-variables literature: when the relative amount of measurement error is small compared to the total variance of the observed variable, the OLS estimate is unbiased. In other words, can be viewed as the reliability, attenuation factor, or the signal-to-total variance ratio. (ii) When , but the two true centralities are uncorrelated, , we have and . The OLS estimate is biased towards zero, and the degree of bias depends on . (iii) When and , if , then , which is equivalent to . This implies that has attenuation bias. As for , we obtain that , which implies that is biased away from zero. (iv) When and have similar size, the directions of the biases depends on the , , and . For , the asymptotic bias is . Since the denominator is always larger than because and , the direction of the bias depends on the sign of : when , ; when , . Similar conclusions can be drawn for .

Remark 8.

(Review of inference property in the framework of classical measurement error with one predictor) Consider the simplest classical population model with measurement error . For simplicity and clarity, we exclude and from the model. We only observe with measurement error instead of the true . It can be shown that the OLS estimate that regresses on satisfies that , where is our scaled noise-to-signal ratio and is the attenuation factor.

Furthermore, with the OLS estimate, the residual sum of squares has limit . Hence, the traditional estimate of , , over-estimates , the larger the and , the larger the over-estimation. It can also be shown that the standard error of OLS converges to . Combined, the -ratio goes to , which is smaller than . So the traditional inference ignoring the measurement error is conservative. Please refer to Pischke, (2007) and Wooldridge, (2015) for more details on measurement error.

Remark 9.

(CI for from the ad-hoc two-stage method) Remark 8 has a few implications on the confidence interval (CI) for under the unified framework (4) when the two-stage estimator is consistent (). On one hand, when all of the quantities in (4aa)-(4aa) (including ) are known, one should use both terms to make valid inference. If one uses (4aa) alone while assuming noiseless to construct the CI, i.e. the “two-stage-adhoc” method, the inference is invalid unless , or . But the degree of invalidity is typically small because when . On the other hand, when the quantities are unknown and need to be estimated and plugged into these two terms, the stories are different. Note that from the classical measurement error literature, from the two-stage over-estimates and the inference based on the first estimated term (4aa) alone is already conservative. As a consequence, the inference based on the two estimated terms would be even more conservative with unnecessarily large width.

In the simulation study, we consider three relevant methods: two-stage-oracle uses both terms with the true parameters, two-stage uses both terms with the estimated parameters, and the two-stage-adhoc uses only the first term with the estimated parameters. The results are consistent with the above discussion.

To further add to Remark 4 on the covariance of , due to the randomness of , the covariance of in Corollary 2 involves three terms, where (4ap) is the term involving and would be the traditional covariance of if and were indeed fixed, the two additional terms (4ap)-(4ap) are the extra covariance caused by the randomness of and .

5.2 Theoretical properties for SuperCENT

This section states the theoretical properties of our proposed SuperCENT method. Intuitively, we expect SuperCENT to be superior to the two-stage procedure when the signal-to-noise ratio of the regression model is large (so that the supervision information from the regression model is strong enough), especially when the observed network is noisy. Theorem 2 shows the asymptotic distribution of the SuperCENT estimators under the same set of conditions as the two-stage and Corollaries 4 and 5 provide their convergence rates. Comparing SuperCENT with the two-stage, we further explicate the discrepancy between SuperCENT and the two-stage and the conditions such that SuperCENT outperforms the two-stage, particularly when the two-stage is inconsistent. Note that the SuperCENT estimates from Algorithm 2 with a given tuning parameter are denoted as , , , and . Let be the estimate of .

Theorem 2.

Corollaries 4 and 5 provide the convergence rates of the SuperCENT estimators. To explicate the difference between the two-stage and SuperCENT, let

| (4bb) |

Corollary 4.

Remark 10.

(The role of ) Let us consider the estimation of . Similar messages can be obtained for and . Comparing the rate of and in (4bd) and (4x), , where is defined in (4bb). As one can see, is the crucial quantity that measures the discrepancy between the two-stage and SuperCENT estimators for . When , SuperCENT outperforms two-stage and vice versa. The positiveness requires . On one hand, this inequality can be satisfied when is not too small and is satisfied when takes the optimal value given in the remark below. It implies that when the tuning parameter is properly selected, SuperCENT performs better than the two-stage. On the other hand, this inequality is more likely to hold when the signal of the regression is large, or the noise of the regression is small, or the signal of the network is small, or the noise of the network is large. This exactly corresponds to our intuition: when the signal-to-noise ratio in the regression model is high, we gain information from the regression model to assist centrality estimation; and the advantage is more pronounced when the signal-to-noise ratio in the network is low, which is exactly when the two-stage behaves poorly.

Remark 11.

(Optimal ) SuperCENT achieves the best performance with the following value

| (4bi) |

SuperCENT with this also obtains the most improvement over the two-stage procedure. It can be directly derived by minimizing (4bd), (4bf), or (4bh). Plugging the optimal value into the SuperCENT objective function (4g) leads to

| (4bj) |

which is times log likelihood when the errors and are normally distributed. Nevertheless, the objective function is just the scaled residual sum of squares of the regression and the scaled rank-one approximation error of the observed network, which does not require the normality assumption.

Remark 12.

( and ) The benefit of the optimal value is twofold: 1) to benchmark the cross-validation procedure in Algorithm 4; 2) to avoid the time-consuming cross-validation by supplying a candidate for the tuning parameter . We can obtain a crude estimate of by plugging in the two-stage estimates of and . To be specific, after we obtain and from the two-stage procedure by Algorithm 1, we estimate and . We then plug in and obtain . We refer to the SuperCENT with given as , whose empirical performance is given in the simulation study. Furthermore, can be used as a guide to lay out the cross-validation grid points in Algorithm 4, to obtain and .

Remark 13.

(Comparison of the estimation of when two-stage is inconsistent) For the two-stage procedure, is consistent if and only if , which implies the network signal-to-noise ratio has to be large enough for the two-stage to be consistent. When , the two-stage procedure is inconsistent. Can the SuperCENT estimates remain consistent under this regime?

The answer is positive. Plugging in the optimal , the rate of in (4bd) becomes

| (4bk) |

which is obviously smaller than , the rate of in (4x). We want the above rate converges to 0 when . Given (4bk), the convergence of boils down to the signal-to-noise ratio of and in the network regression model, i.e., and . One sufficient condition for convergence is then and , meaning the signal for has to be stronger than both the signal for and the noise to guarantee convergence of .

If we want to guarantee the convergence of under this regime, one sufficient condition is and . This conflicts with the requirement of the convergence of . Fortunately, the rates of both and are smaller than those of and , so SuperCENT always improves the estimation: when or , one of and will be consistent. We will demonstrate this phenomenon in the simulation.

Lastly, for the estimation of with , the rate of in (4bh) becomes

which is much smaller than , the rate of in (4y). Better yet, to ensure is consistent, we only require either or . This means that, as long as one of SuperCENT or is consistent, SuperCENT is consistent as well, while two-stage is only consistent when both and are consistent.

When the two-stage estimator is consistent, the supervision effect of SuperCENT only takes place for the estimation of and the in-sample prediction, but not for , as shown in Corollary 5.

Corollary 5.

Remark 14.

(Comparison of the estimation of ) When and the two-stage is consistent, from the perspective of regression coefficient estimation, SuperCENT and the two-stage are similar. However, when and the two-stage regression coefficient estimation is biased as shown in Corollary 3. While for SuperCENT, if the conditions in Remark 13 hold, the SuperCENT coefficient estimates are still consistent and satisfy Corollary 5.

6 Simulation

In this section, we investigate the empirical performances, including the estimation accuracy and inference property of the two-stage and SuperCENT estimators under various simulation setups. We describe our simulation setup and overview the simulation results in Section 6.1 and show the simulation results for the inconsistent regime of the two-stage procedure in Section 6.2. The simulation results for the consistent regime of the two-stage procedure is deferred to the supplement.

6.1 Simulation setup and results overview

We generate the network as where and are vectors of the hub and authority centralities and all the entries of follow independently. The elements of are first generated from i.i.d. and where are generated from i.i.d. . and are then re-scaled to have norm . For the regression model, , we set , the coefficients for the covariates , the covariate matrix consists of a column of 1’s and columns whose entries follow independently, and .

Since only the signal-to-noise of the network and the signal-to-noise of the regression matter to the properties of our estimator and inference, we fix , and to study the effect of , and . To study the effect of the signal-to-noise of the regression, we vary and so that and . Now that the signal-to-noise of the network is solely controlled by , we vary to differentiate the regimes when the two-stage estimator is consistent with small and inconsistent with large . Specifically, for the consistent regime of the two-stage, i.e., when the network noise-to-signal ratio , we vary to keep . For the inconsistent regime of the two-stage, i.e., , we vary so that .

For each setting, we compare several two-stage-based and SuperCENT-based procedures in terms of estimation accuracy and inference property as follows.

Estimation accuracy

For the estimation accuracy, we compare the following procedures:

-

1.

Two-stage: the two-stage procedure as in Algorithm 1;

- 2.

-

3.

: SuperCENT with estimated tuning parameter based on Remark 12, where and are estimated from the two-stage procedure. This way, is implementable for real data;

-

4.

: SuperCENT with tuning parameter chosen by 10-fold cross-validation as in Algorithm 4.

In the SuperCENT Algorithm 2, the tolerance parameter for the stopping criterion is set to be . The following five performance metrics are used to compare these four procedures: the first two are from the perspective of network and centralities, and the last three are from the network regression.

-

1.

The loss for estimating and , and ;

-

2.

The loss for estimating , ;

-

3.

The normalized squared error loss for estimating and , and ;

-

4.

The estimation bias for regression coefficients and .

Inference property

For the inference property, let denote the -quantile of the standard normal distribution and we consider the following procedures to construct the confidence intervals (CIs) for the regression coefficient, and :

-

1.

Two-stage-adhoc: , where is the two-stage estimate of and is the standard error from OLS, assuming are fixed predictors;

- 2.

- 3.

- 4.

- 5.

For these five methods, we compare the empirical coverage probability (CP) and the average width of the confidence intervals. The experiments are repeated 500 times. In parallel, the same five procedures can be used to study the inference regarding the true network . The only difference is that the inference is made for each entry of , which we denote as ; and the CP and the average width reported are the average over all the entries .

To give an overview of the simulation results, Table 1 summarizes the comparison of the two-stage method and SuperCENT in the consistent and the inconsistent regimes of the two-stage from the perspectives of both estimation and inference. SuperCENT universally outperforms the two-stage in terms of centrality estimation, regression coefficients estimation, and inference. In what follows, we focus on the inconsistent regime of the two-stage and defer the consistent regime of the two-stage to the supplement.

| : two-stage consistent | : two-stage inconsistent | |||

| Two-stage | SuperCENT | Two-stage | SuperCENT | |

| Estimation | ||||

| ✓ | Improved | ✗ | ✓ | |

| ✓ | Slightly Improved | ✗ | ✗ (Slightly Improved) | |

| ✓ | Improved | ✗ | ✓ | |

| ✓ | ✓ | ✗ (Biased) | ✓ | |

| ✓ | ✓ | ✗ (Biased) | ✗ (Biased) | |

| Inference | ||||

| ✓ (Conservative) | ✓ (Shorter) | ✗ | ✓ | |

| ✓ | ✓ | ✗ | ✗ | |

| ✓ | ✓ (Shorter) | ✗ | ✓ | |

6.2 Simulation results for the inconsistent regime of the two-stage procedure

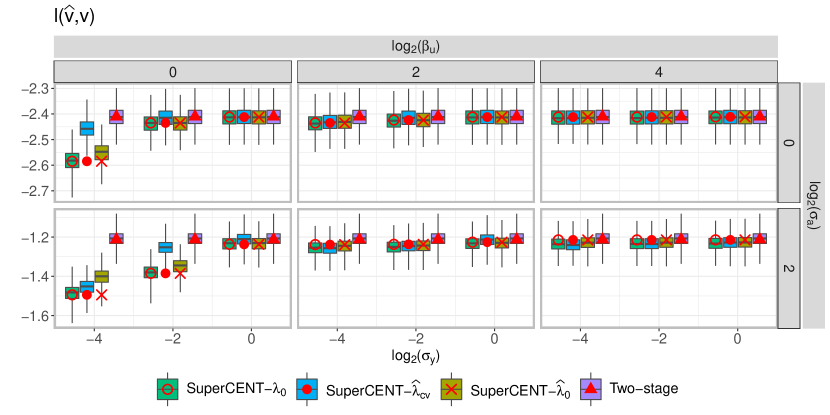

In the inconsistent regime of two-stage where , the two-stage procedure cannot consistently estimate and , i.e., and are inconsistent. Recall that we fix and vary , , and , so that the scaled noise-to-signal of the network , and the signal-to-noise of the regression and . In such a range, we expect the two-stage to be inaccurate for the estimation of and SuperCENT to be much more accurate for , as mentioned in Remark 13. In addition, the two-stage estimates of are biased as shown in Corollary 3 while SuperCENT estimates remain consistent as in Remark 14. As to the inference property, the two-stage-based confidence intervals are expected to be under-covered and wider than necessary while SuperCENT confidence intervals are valid and narrower.

Estimation accuracy

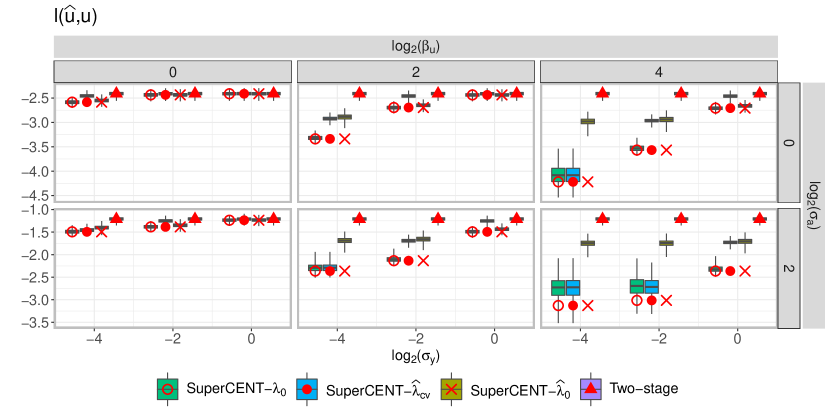

Figure 4 shows the boxplot of the logarithm of across different , and with and . The rows correspond to and the columns correspond to . For each panel, the x-axis is and the y-axis is . The super-imposed red symbols show the theoretical rates of in Corollary 1 and that of in Corollary 4. The two-stage estimator performs the same no matter how large and are, and it has a smaller error with smaller . The performance of SuperCENT is better with smaller or larger . As expected, the three SuperCENT-based methods estimate much more accurately than the two-stage procedure. In particular, the supervision effect of is more pronounced when the noise of the outcome regression, , is small, or when the signal of the outcome regression, , is large, or when the network noise-to-signal, is large. This validates Remarks 10 and 13 on the theoretical comparison of the estimators. Comparing the three SuperCENT-based methods, the benchmark is always the best, and are sometimes worse than , but still better than the two-stage. is typically comparable to or worse than , because fails to locate the optimal due to inaccurate estimate of and from the two-stage procedure.

For the estimation of shown in Figure 4, the improvement of SuperCENT over two-stage is not as large as that of the estimation of when , because and . But the improvement is still quite significant when . It is worth noting that the supervised effect to shrinks as increases, leading to a different trend comparing Figures 4 and 4. This phenomena aligns with Remark 13 where we discuss the estimation of and when the two-stage is inconsistent. Specifically, the roles of and are not exchangeable, because here we have by fixing and varying . On the other hand, when we should expect the improvement in estimating to increase.

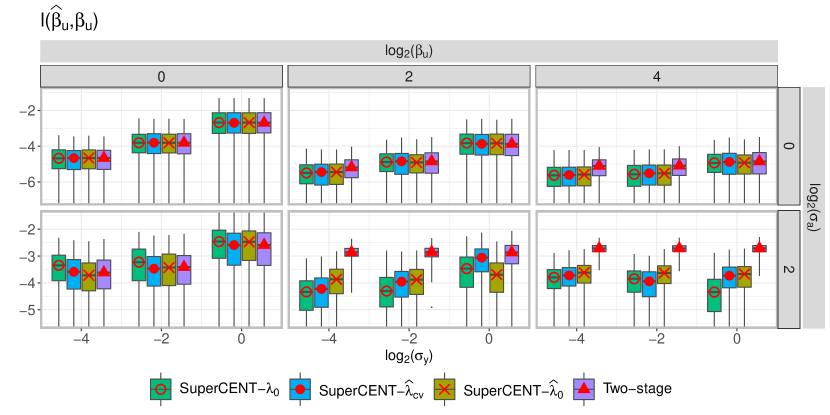

The conclusion for the estimation of is similar to that of as shown in Figure 5. With the improvement from estimating and , estimates more accurately across all the settings. As claimed in Remark 13, the convergence of in this regime only requires or . Therefore, with , , converges and . Comparing Figures 4, 4 and 5 altogether, when , SuperCENT improves the estimation of both and significantly; when , SuperCENT improves the estimation of a lot; therefore, SuperCENT improves the estimation of a lot for all the ranges of .

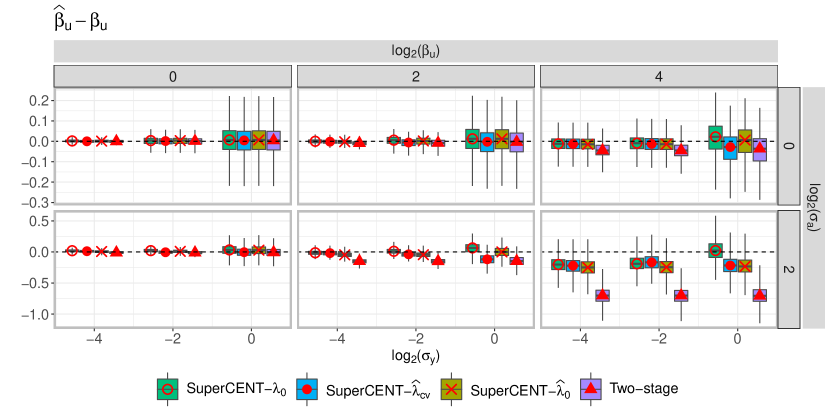

The attention is next turned to the regression coefficient . Based on Corollary 3 on the issues of measurement error, the two-stage coefficient estimates tend to have bias under the inconsistent regime for the two-stage and the directions of the bias depend on the size of , , , and the correlation between and . Figure 7 shows the estimation bias . With large or large , the two-stage estimates suffer from sever attenuation bias, while SuperCENT can alleviate the bias. The attenuation bias by the two-stage can be explained by Remark 7 as follows. In this regime where , and are correlated with , and , then . Hence, has an attenuation bias and the bias becomes larger as increases. On the other hand, this also implies that the two-stage estimation of is biased away from zero and the bias is also larger as increases as shown in the supplement. The improvement of SuperCENT over the two-stage is relatively small and sometimes negligible for .

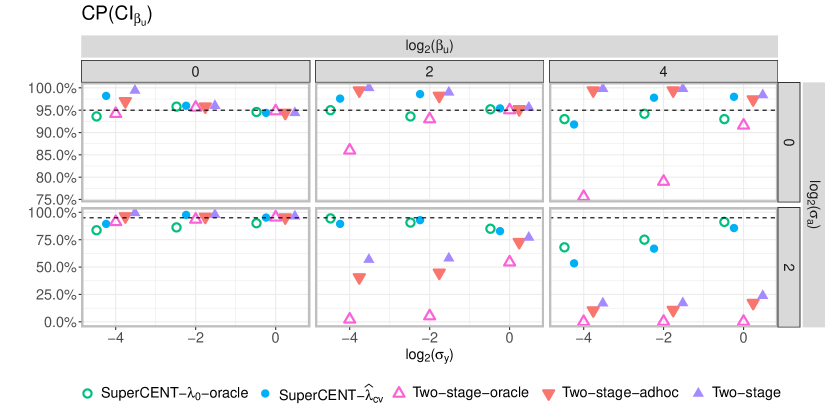

Inference property

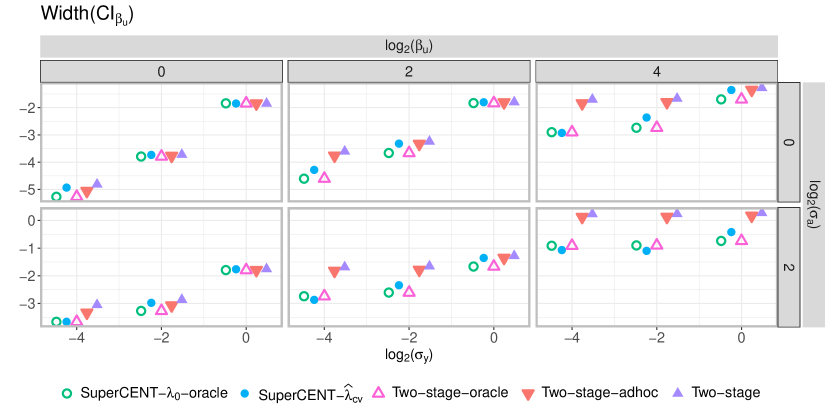

We now switch gears to the inference property. The bias in the estimation of by the two-stage further affects its confidence interval. Figures 9 and 9 show the empirical coverage and the average width of the 95% confidence interval for respectively. For the empirical coverage, when is small (leftmost column), all the methods are close to the nominal level. When increases and remains small (top right two panels), all the methods remain valid except for two-stage-oracle, but different methods remain valid for different reasons. The two SuperCENT-based methods remain valid because there is no estimation bias and the estimation of the standard error is accurate. Two-stage and two-stage-adhoc remain valid mainly because they over-estimate , and this conservative-ness covers up the issue of bias. Two-stage-oracle uses the true and the issue of bias uncovers itself, consequently invalidating the inference. When increases and gets large as well (bottom right two panels), the over-estimation of can no longer conceal the issue of bias and all two-stage related methods are not valid anymore. Again, the SuperCENT can mitigate the bias and the coverage probability is closer to the nominal level.

As for the width of , Figure 9 shows that the confidence intervals by the SuperCENT-based methods have better coverage and are narrower than those by the two-stage methods. The improvement in the width is more significant with larger .

For the confidence interval of the authority centrality coefficient, , the improvement of SuperCENT over two-stage is relatively small in terms of both the coverage probability and width as shown in the supplement, a similar phenomena as of the estimation accuracy of .

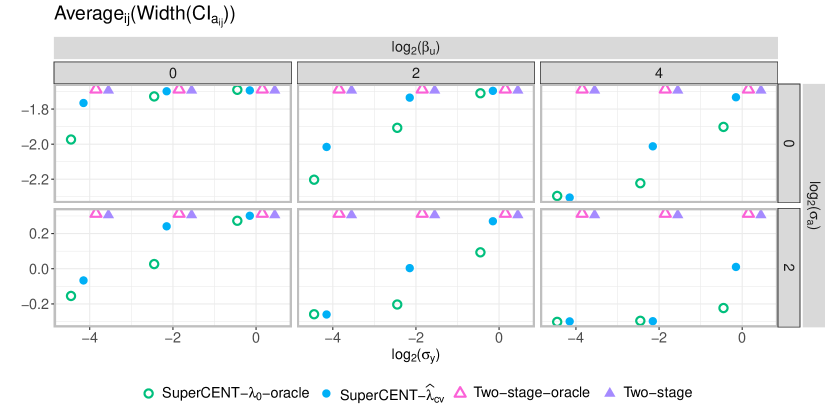

Finally, we investigate the average coverage and the average width of confidence intervals for all the entries of respectively. The average coverage probability of all the methods, , achieves the nominal level of 95% as shown in the supplement. The coverage tends to be slightly below the nominal coverage as increases, because the estimation becomes worse and the theorem only holds up to . is the closest to the nominal coverage in all the settings compared to the others. Figure 10 shows the of the average width of the CIs, . -oracle provides the shortest width among the four methods, followed by . The widths of the confidence intervals of both SuperCENT-based methods are shorter than those of the two-stage methods. Again, the improvement of SuperCENT over the two-stage increases as and increase or decreases.

7 Case study: global trade network and currency risk premium

We consider a real case study with a triplet of , where is the country-level trade network, is the currency risk premium, and is GDP share, whose detailed information and construction will be given shortly. In this case study, we demonstrate that SuperCENT can provide more accurate estimation of the centrality, which is closely related to currency risk premium, and hence has a profound and lucrative implication on portfolio management. We further show that the SuperCENT method outperforms the two-stage methods in the inference of regression coefficients, providing less biased estimates and narrower CIs, and thus strengthens a related economic theory.

In the literature of international finance, economists have been studying currency risk premium extensively and are puzzled by its driving forces. The currency risk premium is formally defined as the excess return from holding foreign currency compared to holding the US dollar. Specifically, for an investor going long in a country/region , the log risk premium “rx” at time is

| (4bx) |

where is log interest rate of country/region , is the log interest rate of the U.S. and is the appreciation of U.S. dollar.

In this case study, we investigate how the global trade network drives the currency risk premium and build a regression model that regresses the currency risk premium on the centrality from the international trade network. Such a predictive relationship is motivated by Richmond, (2019), which developed a general equilibrium with international trade between countries and showed that countries’ positions in the trade network can explain the difference in currency premiums across countries. Specifically, he showed an economic theory that countries that are central in the trade network exhibit lower currency risk premiums. This has two implications: (i) the regression coefficients for the centralities should be negative; (ii) international investors can obtain profit through taking a long-short strategy for foreign exchange – take a long position in currencies of countries with low centralities and a short position in currencies of countries with high centralities. Therefore, if the centralities can be estimated accurately, one can yield a significant investment return based on the strategy.

To verify the economic theory and construct a profitable portfolio, we first need to compute the currency risk premium and construct the global trade network following Richmond, (2019), because these data are not directly available. We then apply the developed methodologies and theories to compare the two-stage and SuperCENT. We focus on the period between 1999 and 2013222Euro was first adopted in 1999. Exchange rate for Malaysia (MYS) is not available from 1999 to 2004. The bilateral trade data is only available till 2013..

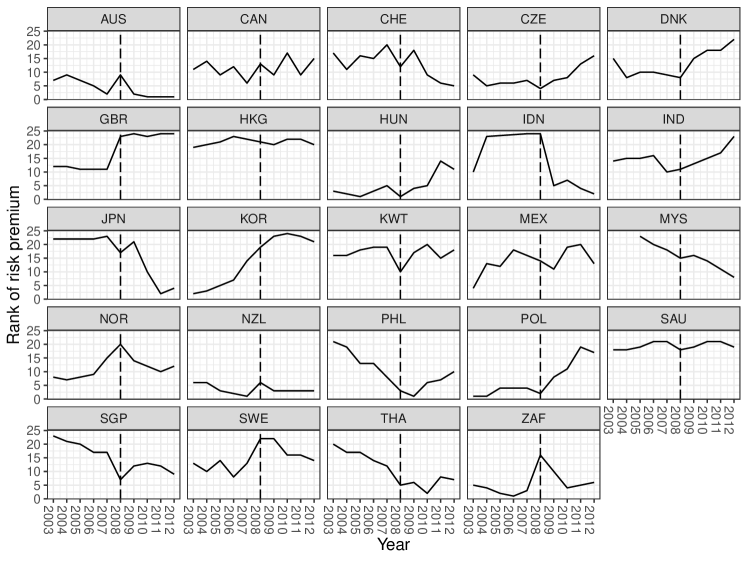

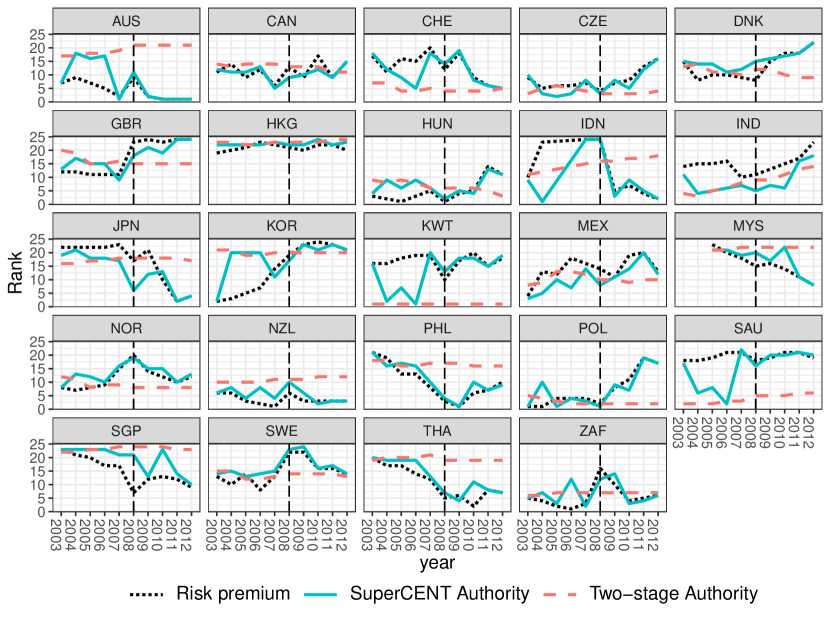

To compute the currency risk premium, we obtain the interest rates and the exchange rates from DataStream. The currency risk premium can be calculated by plugging the interest rates and exchange rates into the definition of risk premium (4bx). Only 25 countries/regions have exchange rates available during the period of interest. We further exclude the region of Europe as it is not comparable to the others in the trade network, resulting in 24 countries/regions in the end333The list of country acronyms is provided in the supplement.. We use a 5-year moving average of the currency risk premium. Specifically, when considering year , all the relevant quantities are the averages from year to year . Figure 11 shows the time series plot of the rank of the 5-year moving average of risk premium from 2003 to 2012444We leave the last available year 2013 for the validation purpose. for the 24 countries/regions. In each year, we rank the 24 countries/regions from 1 to 24 from the largest risk premium to the smallest, i.e., in descending order of the risk premium.

Richmond, (2019) defined the trade linkage as the trade amount normalized by the pair-wise total GDP, which represents the relative trade (export/import) intensity between two countries. Specifically, the trade linkage between two countries is computed as

| (4by) |

where is the dollar value of goods and commodities exported from country to country at time , and is the GDP of country at time in U.S. dollar. The bilateral trade data come from the correlates of war project (COW) (Barbieri et al.,, 2009) and the International Monetary Fund (IMF) Direction of Trade Statistics555https://data.imf.org/?sk=9D6028D4-F14A-464C-A2F2-59B2CD424B85. Current U.S. dollar GDP (using 2015 as the base year) data are from the World Bank’s World Development Indicators666https://databank.worldbank.org/source/world-development-indicators. Same as the currency risk premium, we also use the 5-year moving average in the following analysis. In the supplement, we show a circular plot to visualize the average trade volume from 2003 to 2012.

As neither the two-stage nor SuperCENT is applicable for panel data, we will repeat the analysis for each year from 2003 to 2012. Besides the network and the response variable, we also include the predictor of GDP share, which is defined as the percentage of country/region GDP among the world GDP, where the world GDP is the total GDP of all available countries in the sample for that year. In summary, the models are, for each ,

| (4bz) | |||||

| (4ca) |

In Sections 5 and 6, we have demonstrated that the two-stage procedure is problematic under large network noise. In this case study, the observational error of the network comes from two sources: GDPs and the trade volumes, because each entry of the observed network is defined as (4by), i.e., the trade tie between country and country normalized by their GDPs. GDPs and the trade volumes are often measured with errors. For the GDP, its accounting has been a challenge in macroeconomics (Landefeld et al.,, 2008). For the trade volume, the measurement errors are mostly due to (i) underground or illegal import and export; (ii) not including service trade; (iii) trade cost like transportation or taxes (Lipsey,, 2009). Consequently, the observed trade network can be very noisy and the two-stage method can perform badly.

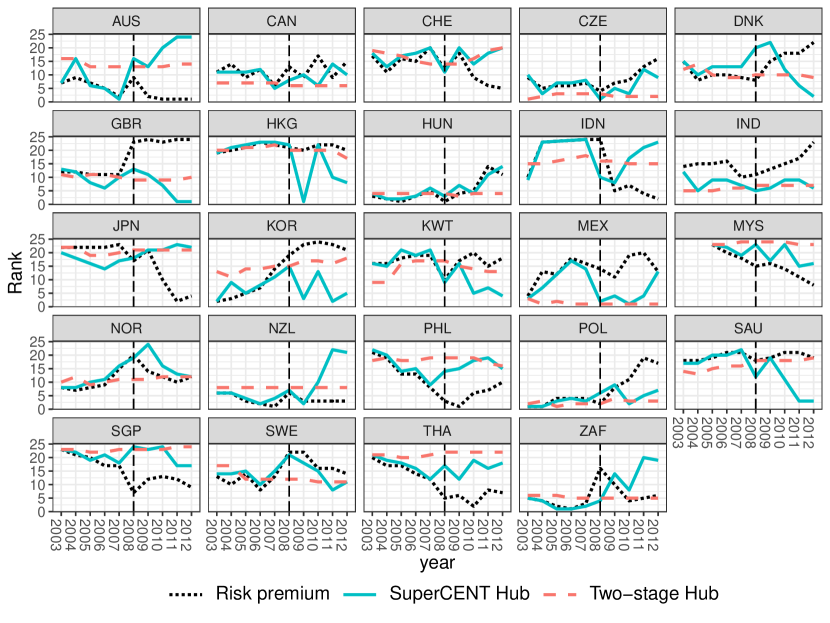

On the other hand, SuperCENT can significantly improve over the two-stage when the network noise is large. In what follows, we focus on using -fold cross-validation. We will refer to SuperCENT for simplicity and use the superscript for the estimates. Figure 12 shows the time series plots of the ranking of the hub centrality estimated by two-stage and SuperCENT for the 24 countries/regions, together with the ranking of the currency risk premium. Figure 13 is for the authority centrality. We rank the centrality in ascending order and the risk premium in descending order. Based on the negative relationship between centralities and risk premium established in Richmond, (2019), the closer the trends of rankings between centralities and risk premium are, the better the centralities capture the time variation in the risk premium. In general, the centrality estimated by the two-stage procedure is relatively more stable over time compared to SuperCENT, since SuperCENT incorporates information of both the GDP share and currency risk premium, which is more volatile than the trade network itself. Asian trade hubs such as Hong Kong (HKG) and Singapore (SGP) are the most central; while countries like South Africa (ZAF) and New Zealand (NZL) are peripheral. Comparing with the ranking of risk premium, the time variation is not reflected in the centrality estimated by the two-stage procedure, while it can be captured by SuperCENT. In 2008, the year of the financial crisis, the SuperCENT centralities fluctuate together with risk premium while the two-stage centralities almost remained unchanged.

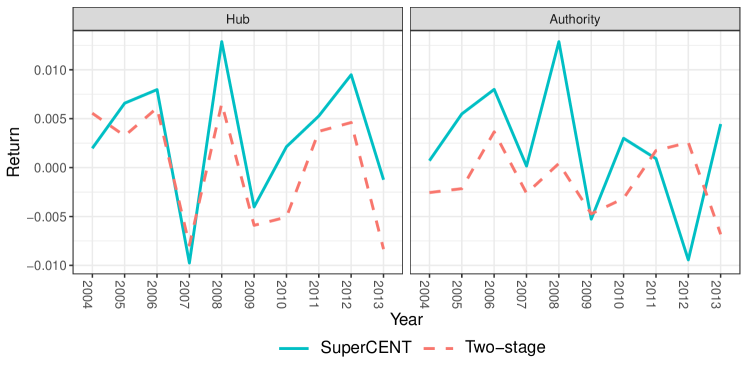

To emphasize the importance of an accurate centrality estimation for portfolio management, we examine whether a long-short strategy based on our estimated centrality can significantly boost investment performance. Specifically, Richmond, (2019) showed in theory that a country with low centrality exhibits a higher expected currency premium than the ones with high centralities. We have shown in theory and simulations that the two-stage centrality estimation can be off from or even orthogonal to the truth when the signal-to-noise ratio of the network is low. Thus, if we can estimate the centralities more accurately than the two-stage procedure, we expect to obtain a higher return through longing countries with low centralities and shorting countries with high centralities.

To illustrate this insight, for each method, we take a long position on the currencies with the lowest 3 centralities (bottom 10%) and a short position on the currencies with the highest 3 centralities (top 10%). That is, we obtain a long-short return based on the estimated centrality of the period between year and . Figure 14 shows the year return based on this strategy. The return based on the centrality estimated by SuperCENT is much higher than that of the two-stage procedure. Table 2 shows the 10-year average return based on this strategy with the top and bottom 3, 4, and 5 currencies, respectively. The 10-year average return based on the SuperCENT centralities increased more than twice from that of the two-stage procedure. Thus, an accurate estimate of the centrality can significantly boost the average portfolio return.

We further demonstrate the superiority of SuperCENT in inference. Again since our method is not directly applicable to longitudinal data, we take the 10-year average of trade volume and GDP to construct a 10-year trade network and GDP share. Similarly, we take the 10-year average of risk premium as the response.

To better understand the behavior of the two-stage and SuperCENT estimators, it is crucial to know which regime the trade network belongs to. However, the true noise-to-signal ratio of the trade network is unknown, so we estimate it using SuperCENT: , which falls in the inconsistent regime of the two-stage. Note that for the simulation study, when , two-stage already shows inconsistency.

To further comprehend the behavior of SuperCENT and gauge how much improvement SuperCENT can potentially achieve in the inconsistent regime, we estimate the signal-to-noise ratio of the regression: and . Compared with the simulation settings in the inconsistent regime where , and , we should expect SuperCENT to improve enormously over two-stage for both the estimation and inference of , thanks to a large and under a relatively large .