Model-assisted complier average treatment effect estimates in randomized experiments with non-compliance and a binary outcome

Abstract

In randomized experiments, the actual treatments received by some experimental units may differ from their treatment assignments. This non-compliance issue often occurs in clinical trials, social experiments, and the applications of randomized experiments in many other fields. Under certain assumptions, the average treatment effect for the compliers is identifiable and equal to the ratio of the intention-to-treat effects of the potential outcomes to that of the potential treatment received. To improve the estimation efficiency, we propose three model-assisted estimators for the complier average treatment effect in randomized experiments with a binary outcome. We study their asymptotic properties, compare their efficiencies with that of the Wald estimator, and propose the Neyman-type conservative variance estimators to facilitate valid inferences. Moreover, we extend our methods and theory to estimate the multiplicative complier average treatment effect. Our analysis is randomization-based, allowing the working models to be misspecified. Finally, we conduct simulation studies to illustrate the advantages of the model-assisted methods and apply these analysis methods in a randomized experiment to evaluate the effect of academic services or incentives on academic performance.

Keywords: Causal inference; Instrumental variable; Logistic regression; Oaxaca–Blinder estimator; Regression adjustment.

1 Introduction

Randomized experiments are widely used to discover causality in social science, medical research, and many other fields. Under the Neyman-Rubin potential outcomes framework (Splawa-Neyman et al., 1990; Rubin, 1974), the average treatment effect can be identified and estimated without bias under random treatment assignment and the stable unit treatment value assumption (SUTVA) (Rubin, 1980; Imbens and Rubin, 2015).

However, in practice, some experimental units may not comply with their treatment assignments. For example, if someone is randomly assigned to take a new drug, he/she still has the right to refuse the drug and instead take the placebo. It is often difficult, or even impossible, to force experimental units to receive the assigned treatments. In this case, although the treatment assignment is randomized, the treatment received may not be. Non-compliance problems are common in randomized experiments in a variety of fields, such as clinical trials (Hirano et al., 2000), social experiments (Sherman and Berk, 1984), policy evaluations (Schochet et al., 2003), and educational studies (Susanne et al., 2005). Because the experimental units are assigned to only one of the treatment arms, we cannot observe their treatment received status under the alternative treatment arm. Thus, we do not know who the compliers are, and it is difficult to interpret the estimated treatment effect.

A highly successful application of the potential outcomes framework is to clarify the fundamental assumptions necessary to identify treatment effects in the non-compliance problems (Imbens and Angrist, 1994; Angrist and Imbens, 1995; Angrist et al., 1996; Imbens and Rubin, 1997). Angrist et al. (1996) proposed a set of identification assumptions. Under these assumptions, the instrumental variable estimand could be interpreted as the local average treatment effect (LATE) for the subpopulation of compliers, also called the complier average treatment effect (CATE). Moreover, they showed that the CATE is equal to the ratio of intention-to-treat (ITT) effects of the potential outcomes to that of the potential treatment received. Because the ITT effects can be consistently estimated by the difference in the sample means of the potential outcomes (or potential treatment received) under the treatment and control groups, we can consistently estimate the CATE using a plug-in method, often known as the Wald estimator (Wald, 1940).

Under a super-population framework, Imbens and Angrist (1994) showed that the Wald estimator is consistent and asymptotically normal. Although the super-population framework is convenient for theoretical analysis, it is unnatural in many problems (Manski and Pepper, 2018; Abadie et al., 2020; Guo and Basse, 2021). For example, when all of the states are recruited to an experiment for policy evaluation, it is not clear what the super-population refers to. In addition, if the experimental units are convenience sampled or carefully selected, they cannot be considered independent and identically distributed samples from a super-population. In these problems, the randomization-based inference is still meaningful, and the finite-population framework is more appropriate than the super-population framework. Our first contribution is to provide rigorous proof for the asymptotic normality of the Wald estimator under a finite-population and randomization-based inference framework. We assume that the potential outcomes and covariates are fixed quantities, the only source of randomness is the treatment assignment, and the treated units are sampled without replacement from the experimental units, and thus the treatment assignments are dependent.

In randomized experiments, baseline covariates are often collected for valid or more efficient inferences; however, the Wald estimator does not incorporate covariate information. To address this issue, the most popular method in econometrics is the two-stage least squares (2SLS), which 70 uses the simultaneous equations model (SEM) framework and allows for the inclusion of baseline covariates (Angrist and Pischke, 2008; Wooldridge, 2010). Moreover, under a fully parametric model specification, maximum likelihood and Bayesian inferential methods are also used to estimate the CATE (Imbens and Rubin, 1997; Hirano et al., 2000). However, these methods lack validity if the working models are misspecified. Semiparametric approaches have been proposed for robust estimation (Abadie, 2003; Tan, 2006; Clarke and Windmeijer, 2012; Ogburn et al., 2015; Wang et al., 2021). To further reduce the risk of model misspecification, Frölich (2007) proposed a nonparametric imputation-based CATE estimator, showed its asymptotic normality, and provided a semiparametric efficiency bound. Moreover, many researchers favour inverse probability weighting methods, some of which share the doubly robust properties (Tan, 2006; Frölich, 2007; Donald et al., 2014; Heiler, 2021; Sun and Tan, 2021). All of these studies assumed that the observed data, outcomes, covariates, treatment received, and treatment assignments, are independent and identically distributed, and sampled from a super-population. In this paper, we consider a finite-population and randomization-based inference framework, propose three model-assisted CATE estimators by incorporating the covariate information, study their asymptotic properties, and compare their efficiencies with that of the Wald estimator. In our theoretical analysis, we allow the working models to be arbitrarily misspecified.

In randomized experiments with perfect compliance, researchers have proposed regression adjustment methods with treatment assignment by covariate interactions to estimate the average treatment effect, and showed that the resulting estimator is generally more efficient than the simple difference-in-means estimator (Lin, 2013; Bloniarz et al., 2016; Fogarty, 2018; Yue et al., 2019; Liu and Yang, 2020; Li and Ding, 2020). Motivated by these ideas and considering non-compliance, we propose an indirect least squares (ILS) method that includes the treatment assignment by covariate interactions in the two linear (working) models. We show that the proposed estimator is consistent and asymptotically normal with an asymptotic variance no larger than that of the Wald estimator.

The ILS method uses linear regression, which ignores the binary nature of the potential outcomes and treatment received. For binary outcomes, logistic regression may fit the data better. Without considering non-compliance, Guo and Basse (2021) proposed a generalized Oaxaca–Blinder estimator and showed its consistency and asymptotic normality under the conditions of prediction unbiasedness, stability, and simple prediction models. We generalize the Oaxaca–Blinder estimator to solve the non-compliance problems and establish its asymptotic theory.

We find that, although the generalized Oaxaca–Blinder estimator is consistent and asymptotically normal, it may reduce the precision compared with the Wald estimator. To address this issue, we propose a calibrated Oaxaca–Blinder estimator, borrowing an idea from Cohen and Fogarty (2021). We show that it is consistent, asymptotically normal, and more efficient than or at least as efficient as the Wald estimator.

We also provide conservative variance estimators to construct asymptotically conservative confidence intervals for the CATE, and extend the proposed methods to estimate and infer the multiplicative complier average treatment effect (MCATE). Finally, we evaluate the finite-sample performance of the proposed estimators through simulation studies and a real data application.

The remainder of the paper proceeds as follows: Section 2 introduces the framework, notation, and identification assumptions for the CATE in completely randomized experiments with non-compliance; Section 3 reviews the Wald estimator and establishes its finite population asymptotic normality; Section 4 describes three model-assisted CATE estimators and discusses their asymptotic properties; Section 5 extends the proposed methods to estimate MCATE; Section 6 provides simulation studies, and Section 7 analyzes a randomized experiment to evaluate the effect of academic services or incentives on academic performance; Section 8 concludes the paper with discussions. The proofs are given in the Supplementary Material.

2 Framework, notation, and assumptions

Consider a completely randomized experiment with units, of which units are randomly assigned to the treatment group and the remaining units to the control group. We denote by the treatment assignment indicator. For unit , if it is assigned to the treatment group, and otherwise. The probability distribution of the treatment assignment indicator is . Throughout this paper, we assume that the SUTVA holds, which allows us to conveniently define the potential outcomes. Let denote the binary potential treatment received status. If unit is assigned to the treatment arm , , if it receives the active treatment and if it receives the control treatment. The observed treatment received is . According to the joint values of the potential treatment received , the experimental units can be divided into four strata: always takers with , never takers with , compliers with , and defiers with .

Let denote the binary potential outcomes if unit is assigned to the treatment arm , . The observed response value is . The average treatment effect of on , also called the ITT effect, is . Similarly, the ITT effect of on is .

Many studies have investigated the treatment effect of the treatment received on the response, i.e., the treatment effect of on instead of on . For example, if we want to evaluate the effect of a drug, we need to compare the outcomes between patients taking the drug and not taking the drug. The ITT effect considers all of the experimental units, including patients who always take the drug and those who never take the drug. Only for compliers does the treatment received status equal the treatment assigned status. Thus, we prefer to study the CATE, which is

where is the set of compliers, and is the total number of compliers.

As only one of the potential treatment received, or , can be observed, we do not know who the compliers are. Thus, to determine the CATE, we use the following identification assumptions proposed by Imbens and Angrist (1994) and Angrist et al. (1996).

Condition 1

(i) Exclusion restriction: for all units with ; (ii) Monotonicity: ; (iii) Strong instrument: , where is a positive constant independent of .

Remark 1

First, the exclusion restriction implies that the treatment assignment affects the potential outcome only through the treatment received . Thus, for always takers and never takers with , the treatment effect of on is 0. Second, the monotonicity assumption rules out the defiers. Third, the strong instrument assumption implies that the ITT effect of on is not equal to 0.

Under Condition 1, Angrist et al. (1996) showed that the CATE is equal to the ratio of the ITT effect of on to that of on , denoted by This identification formula has an intuitive explanation. The average treatment effect of on in the entire finite-population can be decomposed into the summation of the multiplication of the LATE and the proportion of its corresponding subpopulation. Under Condition 1, the LATE for always takers and never takers is 0, and the proportion of defiers is 0. Thus, the ITT effect of on is equal to the CATE multiplied by the proportion of compliers (the ITT effect of on ).

To proceed, we introduce the following notation. Let be a -dimensional vector of baseline covariates for unit . As the covariates are not affected by the treatment assignment, we have . For , the average values of the treatment received, response, and covariates in the finite-population, the treatment group, and the control group are

where indicates the finite-population mean, and the additional subscripts 1 and 0 indicate sample means in the treatment and control groups, respectively.

For each treatment arm , , let and be the finite-population variance of the potential outcomes and the unit-level treatment effect , respectively. Let and be the finite-population covariance between the potential outcomes and and between their unit-level treatment effects, respectively. We replace the uppercase with a lowercase to denote the sample analog.

3 Wald estimator

As the treatment assignment is completely randomized, the ITT effects and can be estimated without bias by the difference in the means of the observed outcomes under the treatment and control groups. The difference-in-means estimators are and . As , the Wald estimator for is to plug in the estimators for and . That is, .

Under the SEM framework, which is widely used in econometrics, the Wald estimator is equivalent to the 2SLS estimator without covariates (Angrist and Pischke, 2008). The 2SLS method by definition consists of two regression stages, i.e., fitting a linear regression of on and then fitting a linear regression of on the fitted values of :

where is the fitted value in the first regression. The 2SLS estimator is the estimator for the second-stage regression coefficient of , . The 2SLS has been investigated extensively in the econometric literature (Angrist and Pischke, 2008; Wooldridge, 2010), under a super-population framework. In what followings, we study its asymptotic properties under a finite-population and randomization-based inference framework using the finite-population central limit theorem (Li and Ding, 2017).

As , under mild conditions, has the same asymptotic distribution as , where is the difference-in-means estimator for the ITT effect of on the transformed potential outcomes : , . The asymptotic variance of is the limit of ,

As we cannot observe or estimate and simultaneously, the last term in is not estimable. We directly drop it and obtain a Neyman-type conservative variance estimator: where is the sample variance for the estimated outcome , . (A more rigorous notation for is . For ease of notation, we still use when it does not confuse.)

To establish the asymptotic normality of , the following regularity conditions are required by the finite-population central limit theorem (Li and Ding, 2017).

Condition 2

As , (i) the proportions of the treated and control units have limits between 0 and 1, i.e., and ; (ii) for , the finite-population means, and , the finite-population variances, , , , and , and the finite-population covariances, and , tend to finite limits, and the limit of is positive.

Remark 2

One crucial condition for the finite-population central limit theorem is . As and are binary potential outcomes, they are bounded and clearly satisfy this condition.

Theorem 1

Theorem 1 provides a normal approximation for the distribution of . The variance estimator is generally conservative. It is consistent if and only if the unit-level treatment effect of is constant, i.e., for some constant . Based on Theorem 1, an asymptotically conservative confidence interval for is , where is the significance level and is the upper quantile of a standard normal distribution. The asymptotic coverage rate of the above confidence interval is greater than or equal to .

4 Model-assisted CATE estimators

Although the Wald estimator exhibits good asymptotic properties, it does not use covariate information. If these baseline covariates can predict the potential outcomes, covariate adjustment tends to reduce the variance of the estimated treatment effect (Lin, 2013; Bloniarz et al., 2016; Fogarty, 2018; Yue et al., 2019; Liu and Yang, 2020; Li and Ding, 2020). In this section, we propose three model-assisted CATE estimators and study their asymptotic properties under the finite-population and randomization-based inference framework. The working models used to obtain these estimators can be arbitrarily misspecified.

4.1 Indirect Least Squares estimator with interactions

In econometrics, the ILS and 2SLS are two widely used methods to estimate the CATE under the SEM framework (Hayashi, 2000; Angrist and Pischke, 2008; Wooldridge, 2010). The ILS regresses the observed potential outcomes and on the treatment assigned status and covariates :

The ILS estimator estimates the ratio of two regression coefficients of , (Angrist and Pischke, 2008). The 2SLS method, using information from the covariates, performs the following two regressions:

where is the fitted value in the first regression. The 2SLS estimator estimates the second stage regression coefficient of , , where is the residual from a regression of on . The 2SLS estimator with a single instrument is identical to the ILS estimator (Angrist and Pischke, 2008).

Considering a randomization-based inference without imposing the linear modelling assumptions on the potential outcomes, neither regression in the ILS estimator can ensure efficiency gains relative to the estimator without adjusting the covariates (Freedman, 2008). For example, in the second regression, the OLS estimator for may have a larger asymptotic variance than that of the unadjusted difference-in-means estimator for estimating . Thus, the ILS estimator may not always be more efficient than the Wald estimator . To address this issue, we can add the treatment assignment by covariate interactions in both ILS regressions, utilizing the idea of Lin (2013). Intuitively, if we can estimate and more accurately, we can improve the efficiency of the CATE estimator.

Adding interactions is equivalent to regressing and on in the treatment and control groups separately. The OLS estimators for the slopes are

The OLS estimators for and are

Then, we can obtain the ILS estimator with interactions: .

To study the asymptotic properties of , we first define the projection coefficients:

Then, we decompose the potential outcomes and into two parts, i.e., projection on the space spanned by the linear combination of the covariates and projection error:

The above equations are only used to define the projection errors and , and all quantities in these equations are fixed.

Similar to the Wald estimator, we define the transformed potential outcomes :

As shown in the following Theorem 2, the asymptotic variance of is the limit of ,

Similar to the estimation, we drop the last term to derive a conservative variance estimator. Specifically, we define

by plugging in the unknown quantities , , and . Then, we use the sample variance of to estimate , denoted by where the factor adjusts for the degrees of freedom to achieve a better finite-sample performance. Then, a conservative estimator for is

To establish the asymptotic normality of , we need the following regularity condition:

Condition 3

As , (i) for each covariate , ; (ii) for , the finite-population covariances, , , and , tend to finite limits with and its limit being strictly positive definite, and the limit of is positive.

Theorem 2

Theorem 2 provides a normal approximation for the distribution of under complete randomization. The variance estimator is generally conservative. It is consistent if and only if the unit-level treatment effect of is constant, i.e., for some constant . Based on Theorem 2, an asymptotically conservative confidence interval for is , whose asymptotic coverage rate is greater than or equal to . Comparing the asymptotic variances and variance estimators of and , we have the following result:

Theorem 3

Theorem 3 shows that both the asymptotic variance and variance estimator of are no greater than those of . Thus, the ILS estimator with interactions improves or at least does not degrade the estimation and inference efficiencies. The improvement in asymptotic efficiency mainly depends on the of the projection of on , which measures the variance of the potential outcomes that is explained by the covariates. In particular, if , i.e., does not affect , has no asymptotic efficiency gain compared with . For another special case with , although has no asymptotic efficiency improvement, it can produce a shorter confidence interval because of the variance estimator, if at least one of and is not equal to 0.

4.2 Logistic Oaxaca–Blinder estimator

The ILS estimator uses a linear regression model to fit the data. However, for a binary outcome, it is natural to consider a logistic regression model to improve the efficiency further. To motivate the method, we discuss an imputation-based interpretation of the OLS estimator (Imbens and Rubin, 2015; Guo and Basse, 2021). We can derive by the following imputation procedure: we fit a linear regression model of on using the data in the treatment group. Thereafter, for any unit in the control group, we impute the unobserved potential outcome , denoted by , by the fitted model and obtain . Similarly, we can obtain for unit in the treatment group. As shown by Imbens and Rubin (2015) and Guo and Basse (2021), . In econometrics, this double-imputation procedure is known as the Oaxaca–Blinder method (Blinder, 1973; Oaxaca, 1973; Kline, 2011).

We can use nonlinear models, such as logistic regression, Poisson regression, or smoothing splines, to impute the unobserved potential outcomes if they fit the data better than the linear model and obtain a generalized Oaxaca–Blinder estimator (Guo and Basse, 2021). We extend this idea to the non-compliance case. In this paper, and are binary, and thus we consider using the logistic regression models to fit the data and impute the unobserved potential outcomes.

For , to fill in the unobserved potential outcome for units assigned to the treatment arm , we use data from the treatment arm and fit logistic regression models:

where , and is the predicted probability of . Then, we fill in the unobserved values of and using

and obtain the estimator for : . Similarly, we can obtain . Then, the logistic Oaxaca–Blinder estimator for is .

Remark 3

When is rank-deficient, or the 1’s and 0’s among the observed outcomes in the treatment or control group can be perfectly separated by a hyperplane, the logistic regression coefficient estimators, or , may not be unique or even exist. In this case, variable selection or regularization is necessary to obtain these estimators.

To investigate the asymptotic properties of , we define and as the solutions of the following finite-population logistic regression problems: for , ,

Throughout the paper, we assume that and exist and are unique. The predicted probabilities are and the residuals are , , , where , and all depend on . For ease of notation, we omit this dependence when it does not confuse.

We define the transformed potential outcomes as follows:

As shown in Theorem 4, the asymptotic variance of is the limit of ,

Similar to the estimation, we can obtain a conservative variance estimator: , where is the sample variance of the estimated outcomes

We require the following condition to derive the asymptotic normality of :

Condition 4

(i) For all large , , and , is positive semi-definite for some constant independent of , where is a identity matrix; (ii) the fourth moments of the covariates are uniformly bounded, i.e., for and some constant ; (iii) as , for , the finite-population variances, , , , and , and the finite-population covariances, and , tend to finite limits, and the limit of is positive.

Theorem 4

Theorem 4 provides a normal approximation for the distribution of . Again, the variance estimator is generally conservative, and is consistent if and only if the unit-level treatment effect is constant. Based on Theorem 4, we can obtain an asymptotically conservative confidence interval for : . However, and cannot always improve the asymptotic efficiency compared with the difference-in-means estimators and . We refer to Cohen and Fogarty (2021) for a counterexample. Thus, may degrade the efficiency in some extreme cases compared with .

4.3 Calibrated Oaxaca–Blinder estimator

Although the logistic regression model might be more appropriate to predict binary potential outcomes than the linear regression model, cannot ensure efficiency gains. To solve this non-inferiority problem, we propose a calibrated Oaxaca–Blinder estimator, borrowing techniques from Cohen and Fogarty (2021).

The basic idea is to take the logistic regression fitted values and as new covariates , and regress and on in the treatment and control groups separately. The coefficient estimators are

We obtain the estimators for and :

where . Then, the calibrated Oaxaca–Blinder estimator for is .

Remark 4

In practice, if some of the potential outcomes are sparse (the proportion of elements 1 is close to zero), the logistic regression model might overfit the data such that the fitted probabilities are numerically 0 or 1. Over-fitting makes the fitted model lack robustness. Any slight disturbance significantly affects the prediction result and may destabilize the calibrated linear regressions. When faced with this issue, we should carefully use the calibrated Oaxaca–Blinder estimator, or more robustly, not perform the calibration step.

To study the asymptotic properties of , we decompose the potential outcomes and into projections on the space spanned by the linear combination of the covariates and projection errors:

where is the finite-population projection coefficient,

and is the projection error.

We define the transformed potential outcomes as follows:

The asymptotic variance of is the limit of ,

Similar to the estimation, let be the estimated value of :

and let be the sample variance of under treatment arm . Then, can be conservatively estimated by

Condition 5

As , for , the finite-population covariances, , , and , tend to finite limits with and its limit being strictly positive definite, and the limit of is positive.

Theorem 5

Theorem 5 provides a normal approximation for the distribution of , which can be used to construct an asymptotically conservative confidence interval for : . Moreover, both the asymptotic variance and the variance estimator of are no greater than those of and , as indicated by the following Theorem:

Theorem 6

Under the conditions of Theorems 1, 2, 4, and 5, the difference between the asymptotic variances of and is the limit of the difference between the variance estimators and converges in probability to the limit of where and ; and the asymptotic variance and variance estimator of are less than or equal to those of (the conclusion for the variance estimator holds in probability).

Theorem 6 shows that generally outperforms and . If but (or ), has the same asymptotic distribution as , while its variance estimator is generally smaller than that of , resulting in a narrower confidence interval. If , has no asymptotic efficiency improvement and has the same confidence interval length as . The relative asymptotic efficiency of and depends on which models, logistic regression or linear regression, fit the data better.

5 Extension to multiplicative complier average treatment effect

The CATE is a natural choice to evaluate the complier treatment effect. When is binary, another interesting and well-studied estimand is the MCATE (Didelez et al., 2010; Clarke and Windmeijer, 2012; Ogburn et al., 2015; Wang et al., 2021), defined as the treatment relative risk:

The MCATE is well-defined when we assume that almost surely. Let and . Abadie (2002) showed that under Condition 1, MCATE can be identified as

where is the ITT effect of on , and is the ITT effect of on . We consider and as new binary potential outcomes, and use the methods introduced in Sections 3 and 4 to estimate and separately. Then, we take a ratio (plug-in) to estimate : . All of the theoretical results on the CATE estimation can be easily extended to the MCATE estimation. The detailed asymptotic results are presented in the Supplementary Material.

Remark 5

is the product of two binary potential outcomes, which may make close to 0. In this case, all of the MCATE estimators may be unstable. In practice, we should be cautious when is the target estimand.

6 Simulation

In this section, we evaluate the finite-sample performance of the Wald estimator and three model-assisted estimators through a simulation study. We consider both the CATE and MCATE. The treatment received and potential outcomes are generated by the following models:

where follows a two-dimensional normal distribution with mean zero and covariance , which entries and .

The potential outcomes and covariates are generated once and then kept fixed. We set , , and . The proportions of compliers, always takers, and never takers are approximately 0.5, 0.36, and 0.14, respectively. We perform completely randomized experiments 1000 times to compare the performance of , , , and , in terms of bias, standard deviation (SD), root mean square error (RMSE), empirical coverage probability (CP), and mean confidence interval length (CI length) of the confidence intervals (CI).

| Bias | SD | RMSE | RMSE | CP | CI | Length | |||

|---|---|---|---|---|---|---|---|---|---|

| ratio | length | ratio | |||||||

| 0 | 0.3 | 0.000 | 0.102 | 0.102 | 1.000 | 0.955 | 0.407 | 1.000 | |

| 0 | 0.3 | 0.001 | 0.066 | 0.066 | 0.643 | 0.965 | 0.274 | 0.673 | |

| 0 | 0.3 | 0.001 | 0.057 | 0.057 | 0.557 | 0.962 | 0.239 | 0.586 | |

| 0 | 0.3 | 0.001 | 0.057 | 0.057 | 0.561 | 0.962 | 0.238 | 0.585 | |

| 0 | 0.4 | 0.000 | 0.098 | 0.098 | 1.000 | 0.960 | 0.381 | 1.000 | |

| 0 | 0.4 | -0.000 | 0.063 | 0.063 | 0.645 | 0.956 | 0.257 | 0.675 | |

| 0 | 0.4 | 0.000 | 0.054 | 0.054 | 0.546 | 0.966 | 0.225 | 0.591 | |

| 0 | 0.4 | -0.000 | 0.054 | 0.054 | 0.547 | 0.966 | 0.224 | 0.588 | |

| 0 | 0.5 | 0.000 | 0.095 | 0.095 | 1.000 | 0.964 | 0.375 | 1.000 | |

| 0 | 0.5 | -0.001 | 0.059 | 0.059 | 0.629 | 0.971 | 0.253 | 0.674 | |

| 0 | 0.5 | -0.001 | 0.052 | 0.052 | 0.553 | 0.967 | 0.221 | 0.590 | |

| 0 | 0.5 | -0.001 | 0.052 | 0.052 | 0.553 | 0.961 | 0.220 | 0.588 | |

| 1 | 0.3 | 0.000 | 0.098 | 0.098 | 1.000 | 0.963 | 0.405 | 1.000 | |

| 1 | 0.3 | -0.001 | 0.060 | 0.060 | 0.610 | 0.967 | 0.259 | 0.640 | |

| 1 | 0.3 | -0.000 | 0.047 | 0.047 | 0.476 | 0.971 | 0.210 | 0.520 | |

| 1 | 0.3 | -0.000 | 0.047 | 0.047 | 0.481 | 0.968 | 0.210 | 0.518 | |

| 1 | 0.4 | 0.001 | 0.093 | 0.093 | 1.000 | 0.965 | 0.379 | 1.000 | |

| 1 | 0.4 | -0.002 | 0.054 | 0.055 | 0.585 | 0.980 | 0.243 | 0.641 | |

| 1 | 0.4 | 0.000 | 0.043 | 0.043 | 0.459 | 0.976 | 0.198 | 0.523 | |

| 1 | 0.4 | 0.000 | 0.043 | 0.043 | 0.462 | 0.975 | 0.198 | 0.521 | |

| 1 | 0.5 | -0.001 | 0.092 | 0.092 | 1.000 | 0.960 | 0.373 | 1.000 | |

| 1 | 0.5 | -0.002 | 0.055 | 0.055 | 0.594 | 0.983 | 0.239 | 0.640 | |

| 1 | 0.5 | -0.002 | 0.043 | 0.043 | 0.463 | 0.978 | 0.195 | 0.522 | |

| 1 | 0.5 | -0.002 | 0.043 | 0.043 | 0.466 | 0.979 | 0.194 | 0.520 |

Note: SD, standard deviation; RMSE, root of mean squared error; RMSE ratio, relative to the Wald estimator; CP, empirical coverage probability of the confidence intervals; CI length, mean confidence interval length of the confidence intervals; Length ratio, relative to the Wald estimator.

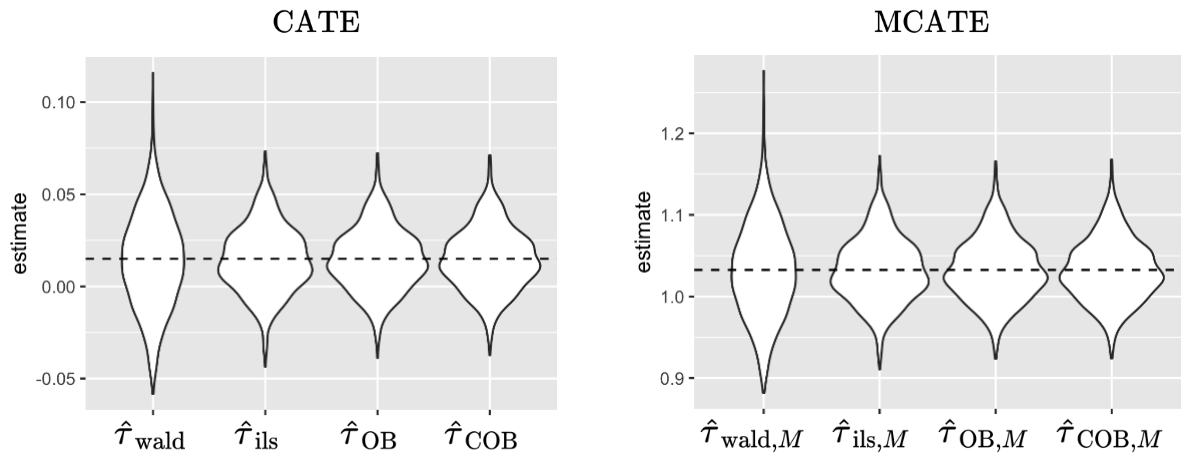

The results for CATE are shown in Figure 1 and Table 1 for , and the results for and the MCATE are presented in the Supplementary Material. From these results, we observe that, first, the biases of all of the methods are negligible in accordance with their asymptotic unbiasedness. Second, compared with , reduces the RMSE and CI length by and , respectively. The logistic regression based estimator further reduces the RMSE and CI length by and , respectively. The calibrated estimator performs similarly to . Furthermore, the empirical coverage probabilities of the confidence intervals produced by , , and are higher than in all of the cases, because of the conservative variance estimators.

7 Real data Analysis

In this section, we apply the proposed methods to analyze a real data set from the Student Achievement and Retention Project (STAR), a randomized trial to evaluate the effect of academic services or incentives on academic performance among first-year college students (Angrist et al., 2009). This trial was conducted at one of the satellite campuses of a large Canadian university. All of the first-year students entering in September 2005 were randomly assigned to the treatment or control group. The students in the treatment group were offered academic support services, financial incentives, or a combination of services and incentives, and they were required to sign up for consent; otherwise, they were ineligible for services and incentives. denotes whether the student was assigned to the treatment group, and denotes whether the student signed up for consent. The monotonicity assumption seems reasonable because the students assigned to the control group were unlikely to sign up for consent. There were students in total, and the cross-tabulation of the treatment assigned and received is shown in Table 2.

| Sign up () | No sign up () | |

|---|---|---|

| Treatment () | 409 | 157 |

| Control () | 0 | 895 |

The outcome of interest is whether the students were in good standing after one year. To evaluate the effect of services or incentives on college achievement, we estimate both the CATE and MCATE using the following 11 covariates to perform regression adjustment (linear or logistic): gender, age, high school GPA, whether mother tongue is English, whether lives at home, whether at first-choice school, whether plans to work while in school, whether rarely or never puts off studying for tests, whether wants more than a BA, whether intends to finish in 4 years, and parents’ education.

The point estimates and CIs are presented in Tables 3. The results show that the support of services or incentives has no significant effect on students’ good standing after one year. This conclusion is the same as that drawn by Angrist et al. (2009). Moreover, compared with , all of the model-assisted methods, , , and , reduce the variance by, , , for the CATE, and , , for the MCATE, respectively, and thus produce shorter confidence intervals.

| Effect | Method | Point estimator | CI | Variance reduction |

|---|---|---|---|---|

| CATE | 0.050 | [-0.022,0.123] | 0 | |

| 0.044 | [-0.025,0.113] | 0.106 | ||

| 0.044 | [-0.025,0.112] | 0.109 | ||

| 0.044 | [-0.024,0.112] | 0.123 | ||

| MCATE | 1.108 | [0.942,1.273] | 0 | |

| 1.093 | [0.940,1.246] | 0.142 | ||

| 1.091 | [0.938,1.244] | 0.146 | ||

| 1.091 | [0.939,1.242] | 0.160 |

Note: CI, confidence interval; Variance reduction, relative to the Wald estimator.

As we do not observe all of the potential outcomes, we cannot know the true gains of the model-assisted methods. For this purpose, we impute all of the missing potential outcomes using fitted logistic regression models under the monotonicity constraint. For these synthetic data, the true values of the CATE, MCATE, and the proportion of compliers are 0.015, 1.032, and 0.872, respectively. We perform completely randomized experiments 1000 times to evaluate the performance of different methods. The results are shown in Figure 2 and Table 4.

The conclusions are similar to those in the simulation section. First, the biases of all the methods are negligible. Second, compared with , , , and decrease RMSE by and CI length by , and thus they improve efficiency. Among these methods, the model-assisted method based on logistic regression perform better than that based on linear regression, and the calibrated logistic regression method performs the best. Finally, the empirical coverage probabilities of confidence intervals are all higher than because of conservative variance estimators.

| Effect | Method | Bias | SD | RMSE | RMSE | CP | CI length | Length |

|---|---|---|---|---|---|---|---|---|

| ratio | ratio | |||||||

| CATE | -0.001 | 0.026 | 0.026 | 1.000 | 0.982 | 0.120 | 1.000 | |

| -0.000 | 0.018 | 0.018 | 0.690 | 0.989 | 0.094 | 0.786 | ||

| -0.000 | 0.017 | 0.017 | 0.654 | 0.989 | 0.090 | 0.753 | ||

| -0.000 | 0.017 | 0.017 | 0.652 | 0.989 | 0.090 | 0.747 | ||

| MCATE | -0.001 | 0.057 | 0.057 | 1.000 | 0.976 | 0.266 | 1.000 | |

| 0.000 | 0.040 | 0.040 | 0.691 | 0.987 | 0.209 | 0.787 | ||

| -0.000 | 0.038 | 0.038 | 0.664 | 0.991 | 0.203 | 0.763 | ||

| -0.001 | 0.038 | 0.038 | 0.663 | 0.992 | 0.201 | 0.755 |

Note: SD, standard deviation; RMSE, root of mean squared error; RMSE ratio, relative to the Wald estimator; CP, empirical coverage probability of the confidence intervals; CI length, mean confidence interval length of the confidence intervals; Length ratio, relative to the Wald estimator.

8 Discussion

In this paper, we study how to efficiently estimate the CATE and MCATE in a completely randomized experiment with non-compliance and a binary outcome.

Under the finite-population framework and mild conditions, we proved that the Wald estimator is consistent and asymptotically normal, and the variance estimator is generally conservative.

To improve the estimation efficiency, we proposed three model-assisted methods, the ILS estimator with interactions, logistic Oaxaca–Blinder estimator, and calibrated Oaxaca–Blinder estimator, and established their asymptotic theories. Our analysis is purely randomization-based, allowing the working model to be misspecified. We showed that the ILS estimator with interactions is no worse than the Wald estimator; the logistic Oaxaca–Blinder estimator cannot ensure efficiency gains relative to the Wald estimator; the calibrated Oaxaca–Blinder estimator is generally more efficient than the Wald estimator and the logistic Oaxaca–Blinder estimator. The efficiencies of the calibrated Oaxaca–Blinder estimator and the ILS estimator with interactions are not ordered unambiguously, depending on which models, linear or logistic, fit the data better. In addition, we proposed conservative variance estimators to facilitate inferences.

This paper focuses on estimating the CATE and MCATE in completely randomized experiments with non-compliance and binary outcomes. Other causal estimands, such as the complier odds ratio, are also interesting and worthy of further investigation. The identification of the complier odds ratio is more complex than the CATE and MCATE, and is left to future research. Moreover, regression adjustment methods have been widely used to improve the estimation efficiency in more complicated randomized experiments, such as stratified randomized experiments, paired randomized experiments, and cluster randomized experiments (Liu and Yang, 2020; Fogarty, 2018; Su and Ding, 2021). It would also be interesting to extend the proposed methods to estimate the treatment effect in these experiments when non-compliance problems occur.

References

- Abadie (2002) Abadie, A. (2002) Bootstrap tests for distributional treatment effects in instrumental variable models. Journal of the American Statistical Association, 97, 284–292.

- Abadie (2003) — (2003) Semiparametric instrumental variable estimation of treatment response models. Journal of Econometrics, 113, 231–263.

- Abadie et al. (2020) Abadie, A., Athey, S., Imbens, G. W. and Wooldridge, J. M. (2020) Sampling-based versus design-based uncertainty in regression analysis. Econometrica, 88, 265–296.

- Angrist et al. (2009) Angrist, J., Lang, D. and Oreopoulos, P. (2009) Incentives and services for college achievement: Evidence from a randomized trial. American Economic Journal: Applied Economics, 1, 136–163.

- Angrist and Imbens (1995) Angrist, J. D. and Imbens, G. W. (1995) Two-stage least squares estimation of average causal effects in models with variable treatment intensity. Journal of the American Statistical Association, 90, 431–442.

- Angrist et al. (1996) Angrist, J. D., Imbens, G. W. and Rubin, D. B. (1996) Identification of causal effects using instrumental variables. Journal of the American Statistical Association, 91, 444–455.

- Angrist and Pischke (2008) Angrist, J. D. and Pischke, J.-S. (2008) Mostly Harmless Econometrics: An Empiricist’s Companion. Princeton University Press.

- Blinder (1973) Blinder, A. S. (1973) Wage discrimination: Reduced form and structural estimates. The Journal of Human Resources, 8, 436–455.

- Bloniarz et al. (2016) Bloniarz, A., Liu, H., Zhang, C. H., Sekhon, J. and Yu, B. (2016) Lasso adjustments of treatment effect estimates in randomized experiments. Proceedings of the National Academy of Sciences of the United States of America, 113, 7383–7390.

- Clarke and Windmeijer (2012) Clarke, P. S. and Windmeijer, F. (2012) Instrumental variable estimators for binary outcomes. Journal of the American Statistical Association, 107, 1638–1652.

- Cohen and Fogarty (2021) Cohen, P. L. and Fogarty, C. B. (2021) No-harm calibration for generalized oaxaca-blinder estimators. arXiv:2012.09246v2.

- Didelez et al. (2010) Didelez, V., Meng, S. and Sheehan, N. A. (2010) Assumptions of IV methods for observational epidemiology. Statistical Science, 25, 22–40.

- Donald et al. (2014) Donald, S. G., Hsu, Y.-C. and Lieli, R. P. (2014) Testing the unconfoundedness assumption via inverse probability weighted estimators of (L)ATT. Journal of Business & Economic Statistics, 32, 395–415.

- Fogarty (2018) Fogarty, C. B. (2018) Regression-assisted inference for the average treatment effect in paired experiments. Biometrika, 105, 994–1000.

- Freedman (2008) Freedman, D. A. (2008) On regression adjustments to experimental data. Advances in Applied Mathematics, 40, 180–193.

- Frölich (2007) Frölich, M. (2007) Nonparametric IV estimation of local average treatment effects with covariates. Journal of Econometrics, 139, 35–75.

- Guo and Basse (2021) Guo, K. and Basse, G. (2021) The generalized oaxaca-blinder estimator. Journal of the American Statistical Association, in press.

- Hayashi (2000) Hayashi, F. (2000) Econometrics. Princeton University Press.

- Heiler (2021) Heiler, P. (2021) Efficient covariate balancing for the local average treatment effect. Journal of Business & Economic Statistics, in press.

- Hirano et al. (2000) Hirano, K., Imbens, G., Rubin, D. B. and Zhou, X. (2000) Assessing the effect of an influenza vaccine in an encouragement design. Biostatistics, 1, 69–88.

- Imbens and Angrist (1994) Imbens, G. W. and Angrist, J. D. (1994) Identification and estimation of local average treatment effects. Econometrica, 62, 467–475.

- Imbens and Rubin (1997) Imbens, G. W. and Rubin, D. B. (1997) Bayesian inference for causal effects in randomized experiments with noncompliance. The Annals of Statistics, 25, 305–327.

- Imbens and Rubin (2015) — (2015) Causal Inference for Statistics, Social, and Biomedical Sciences: An Introduction. New York: Cambridge University Press.

- Kline (2011) Kline, P. M. (2011) Oaxaca-blinder as a reweighting estimator. American Economic Review, 101, 532–537.

- Li and Ding (2017) Li, X. and Ding, P. (2017) General forms of finite population central limit theorems with applications to causal inference. Journal of the American Statistical Association, 112, 1759–1769.

- Li and Ding (2020) — (2020) Rerandomization and regression adjustment. Journal of the Royal Statistical Society, Series B, 82, 241–268.

- Lin (2013) Lin, W. (2013) Agnostic notes on regression adjustments to experimental data: Reexamining Freedman’s critique. The Annals of Applied Statistics, 7, 295–318.

- Liu and Yang (2020) Liu, H. and Yang, Y. (2020) Regression-adjusted average treatment effect estimators in stratified randomized experiments. Biometrika, 107, 935–948.

- Manski and Pepper (2018) Manski, C. F. and Pepper, J. V. (2018) How do right-to-carry laws affect crime rates? Coping with ambiguity using bounded-variation assumptions. The Review of Economics and Statistics, 100, 232–244.

- Oaxaca (1973) Oaxaca, R. L. (1973) Male-female wage differentials in urban labor markets. International Economic Review, 14, 693–709.

- Ogburn et al. (2015) Ogburn, E. L., Rotnitzky, A. and Robins, J. M. (2015) Doubly robust estimation of the local average treatment effect curve. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 77, 373–396.

- Rubin (1974) Rubin, D. B. (1974) Estimating causal effects of treatments in randomized and nonrandomized studies. Journal of Educational Psychology, 66, 688–701.

- Rubin (1980) — (1980) Randomization analysis of experimental data: the fisher randomization test comment. Journal of the American Statistical Association, 75, 591–593.

- Schochet et al. (2003) Schochet, P. Z., McConnell, S. M. and Burghardt, J. A. (2003) National job corps study: Findings using administrative earnings records data. Final report. Mathematica Policy Research, Incorporated.

- Sherman and Berk (1984) Sherman, L. W. and Berk, R. A. (1984) The specific deterrent effects of arrest for domestic assault. American Sociological Review, 49, 261–272.

- Splawa-Neyman et al. (1990) Splawa-Neyman, J., Dabrowska, D. M. and Speed, T. P. (1990) On the application of probability theory to agricultural experiments. Essay on Principles. Section 9. Statistical Science, 5, 465–472.

- Su and Ding (2021) Su, F. and Ding, P. (2021) Model-assisted analyses of cluster-randomized experiments. arXiv:2104.04647.

- Sun and Tan (2021) Sun, B. and Tan, Z. (2021) High-dimensional model-assisted inference for local average treatment effects with instrumental variables. Journal of Business & Economic Statistics, in press.

- Susanne et al. (2005) Susanne, J.-B., Dynarski, M., Moore, M., Deke, J., Mansfield, W. and Pistorino, C. (2005) When schools stay open late: The national evaluation of the 21st century community learning centers program: Final report. U.S. Department of Education, Institute of Education Sciences, National Center for Education Evaluation and Regional Assistance.

- Tan (2006) Tan, Z. (2006) Regression and weighting methods for causal inference using instrumental variables. Journal of the American Statistical Association, 101, 1607–1618.

- Wald (1940) Wald, A. (1940) The fitting of straight lines if both variables are subject to error. The Annals of Mathematical Statistics, 11, 284–300.

- Wang et al. (2021) Wang, L., Zhang, Y., Richardson, T. S. and Robins, J. M. (2021) Estimation of local treatment effects under the binary instrumental variable model. Biometrika, in press.

- Wooldridge (2010) Wooldridge, J. M. (2010) Econometric Analysis of Cross Section and Panel Data, 2nd ed. The MIT Press, Cambridge, Massachusetts, London, England.

- Yue et al. (2019) Yue, L., Li, G., Lian, H. and Wan, X. (2019) Regression adjustment for treatment effect with multicollinearity in high dimensions. Computational Statistics & Data Analysis, 134, 17–35.

Supplementary Material

Appendix A Theoretical results for MCATE estimators

Let us denote the Wald, ILS with interactions, logistic Oaxaca–Blinder, and calibrated Oaxaca–Blinder point and variance estimators for MCATE by , , , and , respectively. Let and denote convergence in distribution and in probability, respectively.

Similar to the study of the asymptotic properties of the CATE estimators, we define the following transformed potential outcomes: for ,

where , , , , , , and are defined similarly to , , , , , , and .

Let us denote

To study the asymptotic properties of the MCATE estimators, we need the following condition. Recall that, for and ,

Condition S.1

As , for ,

(1) the proportions of the treated and control units have limits between 0 and 1, i.e., and ;

(2) the finite-population means, and , the finite-population variances, , , , and , and the finite-population covariances, and , tend to finite limits, and the limit of is positive;

(3) for each covariate , ;

(4) the finite-population covariances, , , and , tend to finite limits with and its limit being strictly positive definite, and the limit of is positive;

(5) for all large and , is positive semidefinite for some constant independent of , and the fourth moments of the covariates are uniformly bounded;

(6) the finite-population variances, , , , and , and the finite-population covariances, and , tend to finite limits, and the limit of is positive;

(7) the finite-population covariances, , , and , tend to finite limits with and its limit being strictly positive definite, and the limit of is positive.

Theorem S.1

Suppose that Condition 1 holds.

(1) Under Condition S.1 (1)–(2), and . Furthermore, converges in probability to

(2) Under Condition S.1 (1)–(4), and . Furthermore, converges in probability to

(3) Under Condition S.1 (1), (2), (5), (6), and . Furthermore, converges in probability to

(4) Under Condition S.1 (1), (2), (5), (7), and . Furthermore, converges in probability to

Theorem S.1 provides normal approximations for the distributions of the proposed MCATE estimators. The variance estimators are generally conservative and they are consistent if and only if the unit-level treatment effects on the transformed potential outcomes are constant.

Theorem S.2

(1) The difference between the asymptotic variances of and is

and the difference between the variance estimators and converges in probability to

where and ;

(2) The difference between the asymptotic variances of and is

and the difference between the variance estimators and converges in probability to

where and ;

(3) The asymptotic variance of and its variance estimator are less than or equal to those of .

Theorem S.2 shows that, and generally improve the efficiency compared with , and generally improves the efficiency compared with . The relative efficiency of and depends on which models, linear or logistic, fit the data better.

Appendix B Proof of main results

B.1 Proof of Theorem 1

Proof 1

Our proof relies on the finite-population central limit theorem (CLT) developed by Li and Ding (2017); see the following Lemma 1.

In completely randomized experiments, let be the potential outcome with observed value , and be the ITT effect of on . The difference-in-means estimator for is , and the variance of is . Let , and and be the sample variance and covariance under treatment arm , . Let be another potential outcome.

Lemma 1

As , for , if (i) has positive limiting value between 0 and 1, i.e., and ; (ii) ; (iii) and have limiting values and the limit of is positive, then , , , and . Furthermore, if , then .

Under Conditions 1 and 2 and by Lemma 1, we have , , and . Thus, using Slutsky’s theorem, we have and has the same asymptotic distribution as , where is the difference-in-means estimator for the ITT effect of on the transformed potential outcomes : , .

It is easy to check that . Moreover, . As and are binary, is bounded. Thus, the regularity condition on the maximum squared distance holds. Under Condition 2, the finite-population variances of , and ,

have limiting values. Applying the finite-population CLT (Lemma 1) to , we have , where

Therefore, , where .

B.2 Proof of Theorem 2

Proof 2

First, we present a lemma on the asymptotic properties of the OLS-adjusted estimator (or ). Let us denote as the OLS-adjusted estimator for ,

where

We define the population regression (projection) coefficient vector and decompose the potential outcomes as . Let .

Lemma 2

As , for , if (i) has positive limiting value between 0 and 1; (ii) and , ; (iii) , , , and have limiting values with and its limit being strictly positive definite, and the limit of is positive, then we have , and . Furthermore, , where is the sample variance of under treatment arm .

The proof of Lemma 2 can be found in Li and Ding (2017), so we omit. Lemma 2 implies that for . As , we have .

Next, we prove the asymptotic normality of . By definition, , where

Clearly, is the slope of the population regression (or projection) of on . Let be the OLS-adjusted estimator for (); that is,

Under Conditions 2 and 3, , , , and have finite limiting values. Thus, . Moreover, Conditions 2 and 3 imply that

have finite limits. Similarly, and have finite limits. As the limit of

is positive, applying Lemma 2 to , we have . Moreover, , .

As and , by Slutsky’s theorem, we have . Moreover,

B.3 Proof of Theorem 3

Proof 3

According to Theorems 1 and 2, the asymptotic variances of and are, respectively,

Note that, for ,

where . Thus,

Similarly,

Let and , then

As we have

Therefore, the difference between the asymptotic variances of and is the limit of times

Furthermore, since

and , , then, the difference between the variance estimators and converges in probability to

B.4 Proof of Theorem 4

Proof 4

First, we introduce a useful result on the asymptotic linear expansion of the imputed potential outcomes, obtained by Guo and Basse (2021).

Lemma 3 is a direct result of Theorems 2 and 3 of Guo and Basse (2021) applied to and , respectively, so we omit the proof. Next, we prove the theorem.

According to Lemma 3, we have

According to the definite of , we have (by first-order condition of the optimization problem). Then, by Lemma 1, under Condition 4,

Therefore, . Similarly, . Then, .

Recall that

Then,

where is the difference-in-means estimator for the ITT effect of on with . First, since and are binary and the predicted probabilities and are bounded, then, is bounded. Thus, . Second, under Condition 4, the finite-population variances, , , and , tend to finite limits. Then, applying the finite-population CLT (Lemma 1) to the transformed potential outcomes , we have , where

Since follows the same asymptotic distribution as , then, , where

B.5 Proof of Theorem 5

Proof 5

For , we define as the prediction equation from the population-level linear regression of on with an intercept, and as the prediction equation from the sample-level linear regression of on with an intercept under treatment arm . Similarly, we define and . We use and to impute the unobserved potential outcomes, and let

Then, the calibrated Oaxaca–Blinder estimators for and have the following form and .

Applying an intermediate result in the proof of Theorem 1 of Cohen and Fogarty (2021) to the calibrated Oaxaca–Blinder estimators and separately, we have the following lemma:

Next, we prove the asymptotic normality. Since

then

where is the difference-in-means estimator for the ITT effect of on with . To derive the asymptotic normality of , we only need to check that the conditions required by the finite-population CLT hold. First, as and are binary, and the covariates are bounded, then and are bounded. Thus, is bounded, which implies . Second, the finite-population variances of , , and are

Under Conditions 2 and 5, the above variances tent to finite limits. Then, applying Lemma 1 to , we have , where

As , by Slutsky’s theorem, we have , where .

Finally, we derive the probability limit of the variance estimator. By definition and Lemma 4,

Similarly, and . Thus,

Therefore,

B.6 Proof of Theorem 6

Proof 6

According to Theorem 5, the asymptotic variance of is

Note that, for ,

where . Thus, similar to the proof of Theorem 3, we have

Let and , then

As

we have

Therefore, the difference between the asymptotic variances of and is the limit of times

Moreover, since

and , the difference between the variance estimators and converges in probability to

Next, we compare the asymptotic variances and variance estimators of and . During the proof of Theorems 4 and 5, we have shown that differs by from the following difference in means:

and differs by from the following difference in means:

Unpacking the notation, we have,

Both equations are, up to an difference, of the form

with the only difference being that in we take and , whereas in we take and . Since the term contributes nothing to the asymptotic variances of and , we neglect it in the remainder of the proof.

By the argument presented in Section 4.1 of Lin (2013), the variance is minimized when is taken to be the population OLS linear regression intercepts and slopes. This is exactly the case for , whereas presents a feasible, but not necessarily optimal solution to the OLS problem. Consequently, the asymptotic variance of does not exceed that of .

B.7 Proof of Theorems S.1 and S.2

Appendix C Additional simulation results

In this section, we present the simulation results for estimating CATE () and MCATE; see Figures S.1-S.3 and Tables S.1-S.3. The conclusions for the CATE estimators are similar to those in the main text. For MCATE, when , , , and also perform better than , while the improvement of over is not as significant as the cases of CATE estimation, and performs better than . When , the MCATE estimators have some large values (looks like outliers; especially for the Wald estimator) in certain cases, mainly because of the estimations of are close to zero in some of the randomization realizations. Moreover, does not work as well as , but the calibrated estimator still works the best.

| Bias | SD | RMSE | RMSE | CP | CI | Length | |||

|---|---|---|---|---|---|---|---|---|---|

| ratio | length | ratio | |||||||

| 0 | 0.3 | -0.001 | 0.153 | 0.153 | 1.000 | 0.971 | 0.636 | 1.000 | |

| 0 | 0.3 | -0.004 | 0.105 | 0.105 | 0.687 | 0.966 | 0.439 | 0.691 | |

| 0 | 0.3 | -0.003 | 0.092 | 0.092 | 0.602 | 0.957 | 0.376 | 0.591 | |

| 0 | 0.3 | -0.002 | 0.093 | 0.093 | 0.611 | 0.951 | 0.376 | 0.590 | |

| 0 | 0.4 | 0.001 | 0.149 | 0.149 | 1.000 | 0.954 | 0.594 | 1.000 | |

| 0 | 0.4 | 0.001 | 0.099 | 0.099 | 0.664 | 0.967 | 0.412 | 0.694 | |

| 0 | 0.4 | -0.000 | 0.087 | 0.087 | 0.585 | 0.962 | 0.355 | 0.598 | |

| 0 | 0.4 | -0.000 | 0.089 | 0.089 | 0.595 | 0.953 | 0.355 | 0.598 | |

| 0 | 0.5 | -0.002 | 0.142 | 0.142 | 1.000 | 0.960 | 0.583 | 1.000 | |

| 0 | 0.5 | -0.000 | 0.097 | 0.097 | 0.683 | 0.967 | 0.404 | 0.693 | |

| 0 | 0.5 | 0.000 | 0.084 | 0.084 | 0.590 | 0.970 | 0.349 | 0.599 | |

| 0 | 0.5 | -0.000 | 0.084 | 0.084 | 0.595 | 0.965 | 0.349 | 0.599 | |

| 1 | 0.3 | 0.008 | 0.178 | 0.178 | 1.000 | 0.964 | 0.729 | 1.000 | |

| 1 | 0.3 | -0.000 | 0.117 | 0.117 | 0.660 | 0.962 | 0.487 | 0.668 | |

| 1 | 0.3 | -0.001 | 0.100 | 0.100 | 0.563 | 0.960 | 0.415 | 0.569 | |

| 1 | 0.3 | -0.000 | 0.100 | 0.100 | 0.565 | 0.964 | 0.414 | 0.568 | |

| 1 | 0.4 | 0.010 | 0.165 | 0.165 | 1.000 | 0.962 | 0.676 | 1.000 | |

| 1 | 0.4 | -0.000 | 0.104 | 0.104 | 0.629 | 0.972 | 0.455 | 0.672 | |

| 1 | 0.4 | -0.001 | 0.086 | 0.086 | 0.520 | 0.968 | 0.390 | 0.577 | |

| 1 | 0.4 | -0.001 | 0.087 | 0.087 | 0.525 | 0.968 | 0.389 | 0.575 | |

| 1 | 0.5 | 0.007 | 0.164 | 0.165 | 1.000 | 0.969 | 0.663 | 1.000 | |

| 1 | 0.5 | -0.002 | 0.104 | 0.104 | 0.631 | 0.963 | 0.445 | 0.672 | |

| 1 | 0.5 | -0.001 | 0.089 | 0.089 | 0.539 | 0.967 | 0.383 | 0.578 | |

| 1 | 0.5 | -0.001 | 0.089 | 0.089 | 0.542 | 0.961 | 0.382 | 0.576 |

Note: SD, standard deviation; RMSE, root of mean squared error; RMSE ratio, relative to the Wald estimator; CP, empirical coverage probability of the confidence intervals; CI length, mean confidence interval length of the confidence intervals; Length ratio, relative to the Wald estimator.

| Bias | SD | RMSE | RMSE | CP | CI | Length | |||

|---|---|---|---|---|---|---|---|---|---|

| ratio | length | ratio | |||||||

| 0 | 0.3 | 0.020 | 0.287 | 0.287 | 1.000 | 0.967 | 1.212 | 1.000 | |

| 0 | 0.3 | 0.003 | 0.198 | 0.198 | 0.689 | 0.969 | 0.824 | 0.680 | |

| 0 | 0.3 | 0.036 | 0.228 | 0.231 | 0.805 | 0.970 | 0.917 | 0.757 | |

| 0 | 0.3 | 0.016 | 0.194 | 0.195 | 0.678 | 0.975 | 0.781 | 0.645 | |

| 0 | 0.4 | 0.027 | 0.282 | 0.284 | 1.000 | 0.957 | 1.152 | 1.000 | |

| 0 | 0.4 | 0.014 | 0.188 | 0.189 | 0.665 | 0.974 | 0.790 | 0.685 | |

| 0 | 0.4 | 0.024 | 0.210 | 0.212 | 0.746 | 0.971 | 0.873 | 0.758 | |

| 0 | 0.4 | 0.019 | 0.181 | 0.182 | 0.643 | 0.966 | 0.739 | 0.642 | |

| 0 | 0.5 | 0.023 | 0.274 | 0.275 | 1.000 | 0.963 | 1.132 | 1.000 | |

| 0 | 0.5 | 0.012 | 0.185 | 0.186 | 0.675 | 0.965 | 0.775 | 0.685 | |

| 0 | 0.5 | 0.022 | 0.198 | 0.200 | 0.726 | 0.969 | 0.862 | 0.762 | |

| 0 | 0.5 | 0.018 | 0.174 | 0.175 | 0.636 | 0.969 | 0.722 | 0.638 | |

| 1 | 0.3 | 0.066 | 0.419 | 0.425 | 1.000 | 0.955 | 1.685 | 1.000 | |

| 1 | 0.3 | 0.019 | 0.245 | 0.246 | 0.579 | 0.968 | 1.029 | 0.611 | |

| 1 | 0.3 | 0.036 | 0.291 | 0.293 | 0.690 | 0.964 | 1.193 | 0.708 | |

| 1 | 0.3 | 0.024 | 0.254 | 0.255 | 0.602 | 0.954 | 1.012 | 0.601 | |

| 1 | 0.4 | 0.060 | 0.379 | 0.383 | 1.000 | 0.946 | 1.536 | 1.000 | |

| 1 | 0.4 | 0.015 | 0.217 | 0.218 | 0.568 | 0.976 | 0.960 | 0.625 | |

| 1 | 0.4 | 0.026 | 0.267 | 0.268 | 0.700 | 0.965 | 1.098 | 0.715 | |

| 1 | 0.4 | 0.024 | 0.225 | 0.226 | 0.589 | 0.968 | 0.948 | 0.617 | |

| 1 | 0.5 | 0.067 | 0.407 | 0.412 | 1.000 | 0.959 | 1.556 | 1.000 | |

| 1 | 0.5 | 0.016 | 0.227 | 0.228 | 0.552 | 0.968 | 0.963 | 0.619 | |

| 1 | 0.5 | 0.025 | 0.250 | 0.251 | 0.609 | 0.968 | 1.075 | 0.691 | |

| 1 | 0.5 | 0.017 | 0.221 | 0.222 | 0.538 | 0.968 | 0.935 | 0.601 |

Note: SD, standard deviation; RMSE, root of mean squared error; RMSE ratio, relative to the Wald estimator; CP, empirical coverage probability of the confidence intervals; CI length, mean confidence interval length of the confidence intervals; Length ratio, relative to the Wald estimator.

| Bias | SD | RMSE | RMSE | CP | CI | Length | |||

|---|---|---|---|---|---|---|---|---|---|

| ratio | length | ratio | |||||||

| 0 | 0.3 | 0.013 | 0.211 | 0.212 | 1.000 | 0.964 | 0.843 | 1.000 | |

| 0 | 0.3 | 0.007 | 0.134 | 0.134 | 0.635 | 0.966 | 0.563 | 0.668 | |

| 0 | 0.3 | 0.016 | 0.143 | 0.144 | 0.680 | 0.975 | 0.616 | 0.731 | |

| 0 | 0.3 | 0.011 | 0.132 | 0.133 | 0.628 | 0.966 | 0.548 | 0.650 | |

| 0 | 0.4 | 0.014 | 0.205 | 0.205 | 1.000 | 0.961 | 0.796 | 1.000 | |

| 0 | 0.4 | 0.005 | 0.130 | 0.130 | 0.632 | 0.960 | 0.532 | 0.668 | |

| 0 | 0.4 | 0.005 | 0.135 | 0.135 | 0.660 | 0.964 | 0.580 | 0.728 | |

| 0 | 0.4 | 0.009 | 0.123 | 0.124 | 0.603 | 0.967 | 0.514 | 0.646 | |

| 0 | 0.5 | 0.015 | 0.197 | 0.198 | 1.000 | 0.960 | 0.789 | 1.000 | |

| 0 | 0.5 | 0.003 | 0.123 | 0.123 | 0.622 | 0.970 | 0.524 | 0.664 | |

| 0 | 0.5 | 0.007 | 0.134 | 0.135 | 0.680 | 0.971 | 0.577 | 0.731 | |

| 0 | 0.5 | 0.007 | 0.120 | 0.120 | 0.606 | 0.972 | 0.505 | 0.639 | |

| 1 | 0.3 | 0.011 | 0.198 | 0.198 | 1.000 | 0.962 | 0.813 | 1.000 | |

| 1 | 0.3 | 0.002 | 0.119 | 0.119 | 0.600 | 0.971 | 0.514 | 0.632 | |

| 1 | 0.3 | 0.008 | 0.131 | 0.131 | 0.662 | 0.986 | 0.586 | 0.721 | |

| 1 | 0.3 | 0.002 | 0.113 | 0.113 | 0.572 | 0.968 | 0.490 | 0.603 | |

| 1 | 0.4 | 0.013 | 0.190 | 0.190 | 1.000 | 0.957 | 0.770 | 1.000 | |

| 1 | 0.4 | 0.000 | 0.109 | 0.109 | 0.572 | 0.981 | 0.486 | 0.632 | |

| 1 | 0.4 | 0.001 | 0.120 | 0.120 | 0.628 | 0.979 | 0.546 | 0.710 | |

| 1 | 0.4 | 0.002 | 0.105 | 0.105 | 0.549 | 0.974 | 0.463 | 0.601 | |

| 1 | 0.5 | 0.011 | 0.188 | 0.189 | 1.000 | 0.957 | 0.761 | 1.000 | |

| 1 | 0.5 | -0.000 | 0.109 | 0.109 | 0.575 | 0.977 | 0.482 | 0.633 | |

| 1 | 0.5 | 0.003 | 0.117 | 0.117 | 0.620 | 0.980 | 0.536 | 0.704 | |

| 1 | 0.5 | 0.002 | 0.101 | 0.101 | 0.535 | 0.975 | 0.456 | 0.600 |

Note: SD, standard deviation; RMSE, root of mean squared error; RMSE ratio, relative to the Wald estimator; CP, empirical coverage probability of the confidence intervals; CI length, mean confidence interval length of the confidence intervals; Length ratio, relative to the Wald estimator.