Pricing S&P 500 Index Options with Lévy Jumps

We analyze various jumps for Heston model, non-IID model and three Lévy jump models for S&P 500 index options. The Lévy jump for the S&P 500 index options is inevitable from empirical studies. We estimate parameters from in-sample pricing through SSE for the BS, SV, SVJ, non-IID and Lévy (GH, NIG, CGMY) models by the method of Bakshi et al. (1997), and utilize them for out-of-sample pricing and compare these models. The sensitivities of the call option pricing for the Lévy models with respect to parameters are presented. Empirically, we show that the NIG model, SV and SVJ models with estimated volatilities outperform other models for both in-sample and out-of-sample periods. Using the in-sample optimized parameters, we find that the NIG model has the least SSE and outperforms the rest models on one-day prediction.

Keywords— Lévy Process; S&P 500; Heston Model; SSE

1 Introduction

Option pricing puzzle has been discussed through plenty of different improvements base on models in Black and Scholes (1973) since 1970’s. The most well-known asset returns pricing models include the jump-diffusion model of Merton (1976) and Bates (1991); the stochastic volatility model of Heston (1993), Hull and White (1987) and Scott (1987); or both as the stochastic volatility jump-diffusion model of Bates (1996), Scott (1997) and Duffie et al. (2000). Stochastic interest rate is added in Merton et al. (1973) and the stochastic volatility and stochastic interest rate are both added in models of Amin and Ng (1993), Bakshi and Chen (1997), Scott (1997) and He and Zhu (2018).

Bakshi et al. (1997) exhibits empirical results of all those models above for the S&P 500 call option data by the square of sum of pricing errors (SSE) optimization. They find the misspecification of all models in different levels. The Black-Scholes (BS) model has the most pricing error and the stochastic volatility jump-diffusion (SVJ) model has the least bias. The SVJ model is the least and the stochastic volatility (SV) model is the second least misspecified models by comparing the SSE values. The stochastic interest (SI) model doesn’t improve the BS model significantly and the stochastic volatility, stochastic interest rate and random jump (SVSI-J) model does not enhance SVJ model too much as well. The stochastic volatility contributes the most in the calibration for the period used in Bakshi et al. (1997). However, the volatility is very difficult to verify in the market in fact, and contributions from the compensated Poisson jumps have inherent bias for the random jump process. Bakshi et al. (1997) builds up Heston call option formulas for all previous mentioned models, but the jump assumption is independent identical distributed (i.i.d) Poisson jump which has log-normal distributed jump sizes. There are other jumps like non-iid in Câmara and Li (2008) and Lévy jumps in Cont and Tankov (2003) which might have worth to explore.

Our paper inspects 27,363 entries as in-sample data and 34,468 entries as out-of-sample data of S&P 500 option prices. We work on the consistence of SV and SVJ models of Bakshi et al. (1997) and find these two models improve the performances of SSE value around 95 present less for both in-sample and out-of-sample comparing BS model. The SVJ models does not reduce bias a lot though the jump part is taken into account, where the jump part in Bakshi et al. (1997) is the i.i.d typed compound Poisson jump process. Besides these two models, the non-iid cases of Câmara and Li (2008) which relax the restricts of i.i.d jump distribution are considered but the SSE results improve slightly since the core dynamic does not change too much.

Constantinides et al. (2008) studies the S&P 500 index returns, where the underlying asset price is assumed to be the log-normal distribution in BS model without imposing parametric model. Their empirical results according to mispricing suggest that the option market is priced by a different probability distribution beyond what they estimated or modeled. They analyze the one month S&P 500 index options market from 1986 to 2006, which covers the stock market crash in October, 1987 with seven different samples of index return. Nevertheless the BS model fits the precrash option prices rationally well, the constant volatility setup is not reasonable. The precrash options cannot be priced correctly when the index return distribution is estimated from time series data even by using various statistical adjustments. Broadie et al. (2009) disclose the evidence of index option mispricing via option pricing models and stick out the statistical difficulties for option returns analysis. Empirical findings of S&P 500 put option returns suggest the puzzle that the large average out-of-money put returns is statistically consistent with the BS model, but the average returns, Sharpe ratios and CAPM alphas for deep OTM put returns are insignificant with the BS model statistically. Other evidences show that put returns are inconsistent with the Heston SV model as well.

To explore the jump role in the option pricing dynamics, we try to use Lévy jump processes to test the mis-specification. Lévy process is a kind of stochastic process which has independent, stationary increments and jumps. Lévy process is an analog of random walk which is the basic simulation of dynamics of market price over time. Lévy process can be fully represented by its corresponding characteristic function due to Lévy-Khinchin theorem. With the characteristic function of the Lévy process, the expectation integral of European call option pricing becomes easier to calculate than the according computation of density function of Lévy process. In recent research, Lee and Hannig (2010) present the signs of small and big jumps of Lévy processes with reasonable high belief by non-parametric tests. Testing of Dow Jones, S&P 500 index and individual stocks shows that indices and stocks indeed have different Lévy jump dynamics. The Lévy jump evidence is consistent with Li et al. (2006) which study the US market index by using a Bayesian Markov chain Monte Carlo method. Ornthanalai (2014) studies the contribution of infinitely active Lévy jumps in the equity risk premium, suggests that kind of Lévy jumps have dominant role beyond Brownian motions. Zaevski et al. (2014) obtain a general formula for the European option via infinitely divisible Lévy jumps produced by a tempered stable process, along with statistical test and forecasting. Li and Li (2015) disclose the explicit option pricing formula for underlying assets driven by the exponential Lévy process with gamma jumps. Cont and Voltchkova (2005) introduce the European option pricing as a solution of PIDE (Partial Integro-Differential Equation) for the underlying asset price as exponential Lévy process and the cases of one or two barriers. The PIDE from Lévy process model is very tough to solve explicitly, numerical methods in general include PDE2D scheme of Florescu et al. (2014) and fast Fourier transform (FFT) approximation. Duffie et al. (2000) discuss the analytic utility of Fourier transform in affine models and the main method is FFT estimation of Carr and Wu (2004), Lord et al. (2008) and Wong and Guan (2011). Kwok et al. (2012) and Hirsa (2016) elaborate the FFT algorithm which is applied in the calculation of option price with Lévy process. As an efficiently numerical method to solve PIDE relevant to Lévy process, the FFT method may evaluate the option price by interpolation inversely. Therefore we can check the sensitivities (Greeks) easily from the computation as a by-product.

To estimate the parameters of specific Lévy process, there are several statistical methods as maximum likelihood estimation (MLE), generalized method of moments (GMM) etc. Nevertheless there is a lack of the closed form of likelihood function of many Lévy processes. Even for known cases like generalized hyperbolic model, Barndorff-Nielsen and Blaesild (1981) and Blaesild and Sørensen (1992) point out some flaws of MLE method. The GMM method of Hansen (1982) builds up an estimator for fitting the empirical and theoretical moments to evaluate the parameters. Loretan and Phillips (1994) and Lux (2000) point out that there are some issues of consistency and asymptotic normality of GMM estimator for Lévy process. Geman et al. (2001) indicate that the financial assets price processes should include a jump component but it is unnecessary to have a diffusion component. The infinite arriving jump processes dynamics may represent the diffusion component contribution. As Cont and Tankov (2003) also mentioned, Lévy processes may cause high variability of realized volatility since heavy tailed increments, which means stochastic volatility effects are realized for free.

In this paper, we use the sum of squared weighted error method of Bakshi et al. (1997) and Christoffersen et al. (2009) uniformly and consistently to estimate parameters for SV, SVJ, non-iid and three special Lévy processes. Those three Lévy processes are general hyperbolic (GH) distribution model of Barndorff-Nielsen (1977), normal inverse Gaussian distribution (NIG) model of Barndorff-Nielsen (1997) and Carr-Geman-Madan-Yor distribution (CGMY) model of Carr et al. (2002). Previous studies on Lévy models use MLE method to estimate parameters of VG, NIG and CGMY models (see Ornthanalai (2014)), the different approach to estimate parameters makes it is hard to compare both BS and SV, SVJ models with Lévy models together. Under the same method with parameters estimated from in-sample S&P 500 index options, we evaluate and predict the SSE for both in-sample and out-of-sample periods for all models. By comparing BS, SV, SVJ models with different time period in Bakshi et al. (1997), we find the consistent results that the BS model is the least performed, and the SV and SVJ models with estimated volatility perform better than SV and SVJ models with implied volatility model. For both in-sample and out-of-sample, NIG model outperforms the GH and CGMY models consistently. The NIG model, SV and SVJ models with estimated volatility are the best among all the models for in-sample data. The SV and SVJ model with estimated volatility outperform the rest models for the out-of-sample data, and NIG follows next. For one-day prediction, using the in-sample estimated parameters, we find that NIG has the least SSE, and outperforms the rest models on March 1st, 2013 prediction.

The rest of paper is outlined as follows. Section 2 gives data description of S&P 500 index options. Section 3 introduces the methodology includes the Heston model, non-iid jumps model and Lévy jump models. Empirical analysis on S&P 500 index option is given in Section 4, including in-sample fitting, out-of-sample and one-day prediction. Section 5 concludes.

2 Data Description

Due to the most actively traded European style option contracts and data availability, as well as the continuation of the empirical analysis on option pricing models of Bakshi et al. (1997), we use S&P 500 call option prices for our option pricing analysis.

The Standard & Poor (S&P) 500 index is a market-capitalization-weighted index of the 500 largest U.S. publicly traded companies. The index is widely regarded as the best gauge of large-cap U.S. equities. It becomes the most popular subject in financial quantitative study since it is representative and data available.

The in-sample data are collected from the underlying S&P 500 index and its call option prices from September 4th, 2012 to February 28th, 2013, and the out-of-sample data are such data from March 1st, 2013 to August 30th, 2013.. The data are obtained from Wharton Research Data Services website (WRDS). The interest rate is using Treasury Bill Rates from treasury.gov on the corresponding period. We follow steps in Bakshi et al. (1997) to filter the data by several criteria:

First, the arbitrage restriction is applied:

| (1) |

where is the underlying S&P 500 index price, is the strike price, is time to maturity for the contract and is the dividend yield.

Second, the options with less than 6 days to expire are eliminated since they could cause liquidity-related biases.

Third, quotes prices of less than $ are excluded because these impacted by volatile bid and ask prices.

After the filtration, 27,363 S&P 500 index option prices are extracted from the in-sample 176,105 entries. Meanwhile, 34,468 observations are left from the out-of-sample 203,709 items.

Base on the moneyness ratio of and , we separate these observation as 5 groups: Deep out-of-the-money(DOTM) when is less than 0.94 and out-of-the-money(OTM) as ratio is between 0.94 and 0.97; At-the-money(ATM) when is between 0.97 and 1.03; In-the-money(ITM) if is between 1.03 and 1.06; and deep in-the-money(DITM) if the ratio is beyond 1.06.

Since the database counts the time as working days, which means one year only has 252 days. The options are classified as 3 categories depend on the time to maturity: short-term for less than 40 days, medium-term for 40-120 days, long-term for greater than 120 days444Bakshi, Cao and Chen (1997) use the sample period from June 1, 1988 to May 31, 1991 with same regions for the moneyness ratio. By the term expiration, they refer to an option contract is (i)short-term ( days), ours short term ( days); (ii)medium-term (60–180 days), ours medium-term (40–120 days); (iii) long-term ( days), ours long-term ( days).

Table LABEL:stat1 describes the statistics for these 27,363 in-sample observations.

Table 1 illustrates the in-sample properties of the S&P 500 index European-style option prices. Summary statistics are reported for the average bid-ask midpoint price (B-A mid-point price), the average effective bid-ask spread (Eff. B-A Spread), the average of implied volatility (Imp. Volatility) and the total number of observations for each category. For each moneyness category, the long term has the maximum effective bid-ask spread and the maximum of implied volatility. There are plenty of zeros for the long terms in ATM, ITM ans DITM categories, as well as for the medium term in ITM and DITM categories.

Table LABEL:stat2 describes the statistics for these 34,468 observations as out-of-sample.

Table LABEL:stat2 illustrates the out-of-sample properties of the S&P 500 index European-style option prices. Summary statistics are reported (similar to Table 1), where the short term total observations are 11,669 and 14,218 respectively for the in-sample and the out-of-sample periods, the medium term total observations are 8,611 and 11,148, the long term total observations are 7,083 and 9,102 respectively for two different periods. For the deep out-of-the-money, the middle term has the minimum average implied volatility for both in-sample and out-of-sample. Constantly, minimum average implied volatility happens at the short term for the other categories.

3 Methodology

The purpose of this section is to set our testing models for the jump-diffusion processes in our empirical studies of S&P 500 index options. Merton (1976) introduced the first jump processes in option pricing model, where the jump is a Poisson process with constant intensity independent of the continuous Brownian motion and i.i.d jumping size random variables independent from the Brownian motion and the Poisson jump process. We set the Black-Scholes model as a benchmark for the option pricing model, and first including the Heston model with stochastic volatility under the risk-neutral measure. Then we include the Non-iid jump model to vary the jumping size variables with different means and different variances. Following Câmara and Li (2008), it is convenient to follow a standard numerical analysis to estimate the option prices under a risk-neutral probability measure. This would naturally lead to consider more general jump processes as Lévy jump models, and to empirically test three typical Lévy jump processes (General hyperbolic distribution, Normal Inverse Gaussian distribution, and Carr-Geman-Madan-Yor class of distribution).

3.1 Model Dynamics

In the last four decades, many modifications were made to relax the restrictions of the Black-Scholes (BS) model in Black and Scholes (1973). Heston (1993) model is a solid way by setting the volatility as a stochastic process as well. Heston (1993) assumes that the underlying stock price follows the geometric Brownian motion just as the process in the BS model, and the variance follows a stochastic CIR process in Cox et al. (1985). Then the Poisson jump model has the bi-variate system of Stochastic Differential Equations (SDEs) listing as (see Bakshi et al. (1997) and Rouah (2013)):

| (2) | ||||

| (3) |

where is the drifting term for the geometric Brownian motion, is the mean reversion speed for the variance, is the long-run mean, is the volatility of the variance, and are two Brownian motions with correlation coefficient , is the frequency of jump per year and is the percentage jump size which is log-normally distributed over time with unconditional mean such that with the continuous stochastic process part , is a Poisson jump counter with intensity . Hence, the parameters for the Heston model as are , and the parameters for the SVJ model as consists of those of Heston models.

If and , then the Heston model is reduced to the Black-Scholes model with . In the afterwards empirical study, we deal with the value in two choices: using the square of implied volatility given in the market database or estimate as a parameter. We implement every model by backing out, on each day, the implied volatility and structural parameters from the market option prices of that day. This is quite a common approach in literature (e.g., Bakshi et al. (1997)), to resolve internal consistency on parameters for models we test.

By the Esscher transform, under an risk-neutral measure , the new process SDEs are:

| (4) | ||||

| (5) |

where and are two Brownian motions under the risk-neutral measure with the correlation , and the market price of risk equation

If the stock pays a continuous dividend yield , we may replace in the equation (4) as . See Duffie et al. (2000), Cont and Tankov (2003) and Shreve (2004) for more details.

The close-form option pricing formula for Heston model SDEs is given by the solution of a difference between two expressions of probability, just as the close-form option pricing formula in the BS model. For a European call option with a strike price and time-to-maturity , the close-form option price subject to is given by

| (6) |

where the two probabilities and are represented by the respective characteristic functions ’s () for the stochastic-volatility jump-diffusion (SVJ) model (see Heston (1993), Bates (1996), Scott (1997), Bakshi et al. (1997) and Duffie et al. (2000)):

| (7) |

The stochastic volatility (SV) model can be obtained by setting , and the SVJ model is for the general nonzero . Bakshi et al. (1997) sets more general SVSI-J model along with five models on the Black-Scholes (BS) model, the stochastic volatility (SV), the stochastic interest-rate (SI or SVSI) and the stochastic volatility random jump (SVJ) to conduct a more comprehensive empirical study on the relative merits of competing option pricing models. They showed that the SI and SVSI-J models do not significantly improve the performance of the BS and SVJ models, based on the S&P 500 index call options from June 1988 to May 1991. Moreover their empirical findings indicate that the SVJ model has the least misspecified option pricings and the BS has the most. But the jumping process in the SVJ model is the compound Poisson jump with i.i.d jump size. Hence we first extend the SVJ model to the Non-iid jump model developed in Câmara and Li (2008).

3.2 Non-iid Jump Model

There is an important assumption of jumps diffusion model initially set up by Merton (1976) as we discussed before is that the underlying asset has the identically and independently distributed (i.i.d) jumps in the compound Poisson process. Câmara and Li (2008) derives the close-form of option pricing formula for the non-iid jumping sizes in the compound Poisson process. In order to compare with the SVJ and the SV models under the consistent parameters estimation, we analyze three types of the non-iid jumping sizes which are (i) with time-varying means, (ii) with time-varying variances and (iii) with auto-correlated jumps.

By building the non-iid jumps, Câmara and Li (2008) extend a fundamental formula base on the jump-diffusion pricing model in Merton (1976). We summarize their results in the following, in order to estimate and calculate the option prices numerically.

The jump-diffusion call option pricing without i.i.d assumption on jumps is given by:

| (8) |

where

(i) Corollary 1 (Jumps with time-varying means)

Let and . The specific parameters in formula (8) are computed as

(ii) Corollary 2 (Jumps with time-varying variances)

Let and . Then the parameters in formula (8) are given as:

(iii) Corollary 3 (Autocorrelated Jumps)

Let and . Then we have the parameters in formula (8) modified as:

The formula for the first case is similar to the classic Merton’s jump-diffusion pricing formula with modified parameters from the non-iid jump sizes in the jump-diffusion pricing model. Ordinarily, the call price formula here is a function of the stock price , strike price , time of maturity , interest rate , stock volatility , Poisson process intensity . The notation is covariances which are fixed, and () that means jumps affect the time-varying means only. There are some other parameters as is the total gross stock return factor, is the moving average for the price jump sizes means. The second non-iid case may occur on the variances of the price jumps only. The means are fixed as which is the average values for all ’s in the first case. The covariance , the moving average of jumps variances is the new average value which is different with the fixed value in (i). The third case of the non-iid jump model which is only on the autocorrelations of price jumps with nontrivial covariaces of jumps. Unlike the cases (i) and (ii), there is a new factor as the moving average of the autocorrelations. The moving average for the price jump sizes means in (i) and the moving average of jumps variances in (ii) are constants. See Câmara and Li (2008) for more details.

3.3 Lévy Jump Models

Lévy process enables flexible modelling of the distribution of returns at a given time horizon, especially when it comes to model the tails of the distribution. The distribution of asset returns in financial markets seems to carry a heavy tail which has positive excess kurtosis with a tail index, and the log-price of assets shows stylized empirical properties as the absence of autocorrelation in increments, heavy tails, finite variance, aggregational normality, jumps in price trajectoies which are natural properties Lévy processes endow, especially like the variance gamma, NIG, hyperbolic, CGMY Lévy processes carry the heavy tails. There are tremendous literature on Lévy processes in financial quantitative analysis (see Cont and Tankov (2003)).

In the BS model, the dynamics of asset price is described as an exponential of Brownian motion with drifting term, as the geometric Brownian motion,

where . For the exponential Lévy process, we have , where is a Lévy process. By the Ito formula and Lévy-Khinchin decomposition theory, we have the Martingale-drift decomposition of functions.

Cont and Tankov (2003) show that the geometric Lévy process is a semimartingale with a decomposition of a martingale process and continuous finite variation drifting term, where is a Lévy process with Lévy triplet () satisfying and is the martingale part

and the continuous finite variation drift part is

Therefore, is a martingale if and only if

With the Lévy jump model, the European option price can be evaluated by solving an Partial Integro-Differential Equation (PIDE) from the martingale property. Suppose the European option with maturity and payoff satisfies Lipschitz condition for some . Hence, the option price under the geometric Lévy process asset is given by

Then the risk-neutral dynamic of is obtained by (Cont and Tankov (2003))

where is the compensated jump measure of the Lévy process and is a martingale: verifies . Suppose If either the volatility strictly positive or there exists a such that then the option price of a European option with terminal payoff is a solution of the partial integro-differential equation (Backward PIDE for European option with Lévy process, see Cont and Tankov (2003)):

| (9) |

on with the terminal condition

By analyzing how to solve the PIDE (9), one realized that it is extremely difficult to get the closed-form option pricing formula since (i) it is a backwards partial differential equation with the boundary condition of maturity time, and (ii) the integral part in the equation is very tough to handle. Fortunately, we can use the Fourier transform to estimate the solution numerically. Fast Fourier transforms are used in modern applications in engineering, science, and mathematics widely. The Cooley-Turkey FFT algorithm which was introduced in Cooley and Tukey (1965) can reduce the multiplication of discrete Fourier transform to by using a divide. Strang (1994) described the FFT in 1994 as ”the most important numerical algorithm of our lifetime” and it is included in Top 10 Algorithms of 20th Century by the IEEE journal. For the details how to apply FFT method to estimate the solution, see Kwok et al. (2012), Kienitz and Wetterau (2012) or Hirsa (2016).

3.4 Three Typical Lévy Processes in Finance and Numerical Sensitivity Studies

Three typical Lévy processes are specified in order to evaluate the option pricing model explicitly, and the explicit density function and characteristic functions are listed in this subsection for later calibrations. Therefore the explicit formulas of FFT algorithm are determined. The sensitivities for the parameters through numerical solutions are also discussed.

1. General Hyperbolic (GH) Distribution

General Hyperbolic distribution is a class of Lebesgue continuous infinitely divisible distribution of 4 parameters. The Lebesgue density is defined in Barndorff-Nielsen (1977):

where the domain of parameters is specified by , , and are the modified third kind of Bessel functions with the order as subscripts. The characteristic function of this distribution law is given by When all data are on the same time scale, the sample from a GH model and estimating its parameters are relatively easy.

To analyze the sensitivities of the parameters in these three kinds of Lévy processes, we need to pick up some initial parameters (in related literature) to start the SSE procedure as in Bakshi et al. (1997). Here we fulfill the sensitivities investigation base on the optimal parameters of Schoutens (2003), which focus on the S&P 500 index call option prices study by minimizing the root-mean-square error for the price differences of market and models.

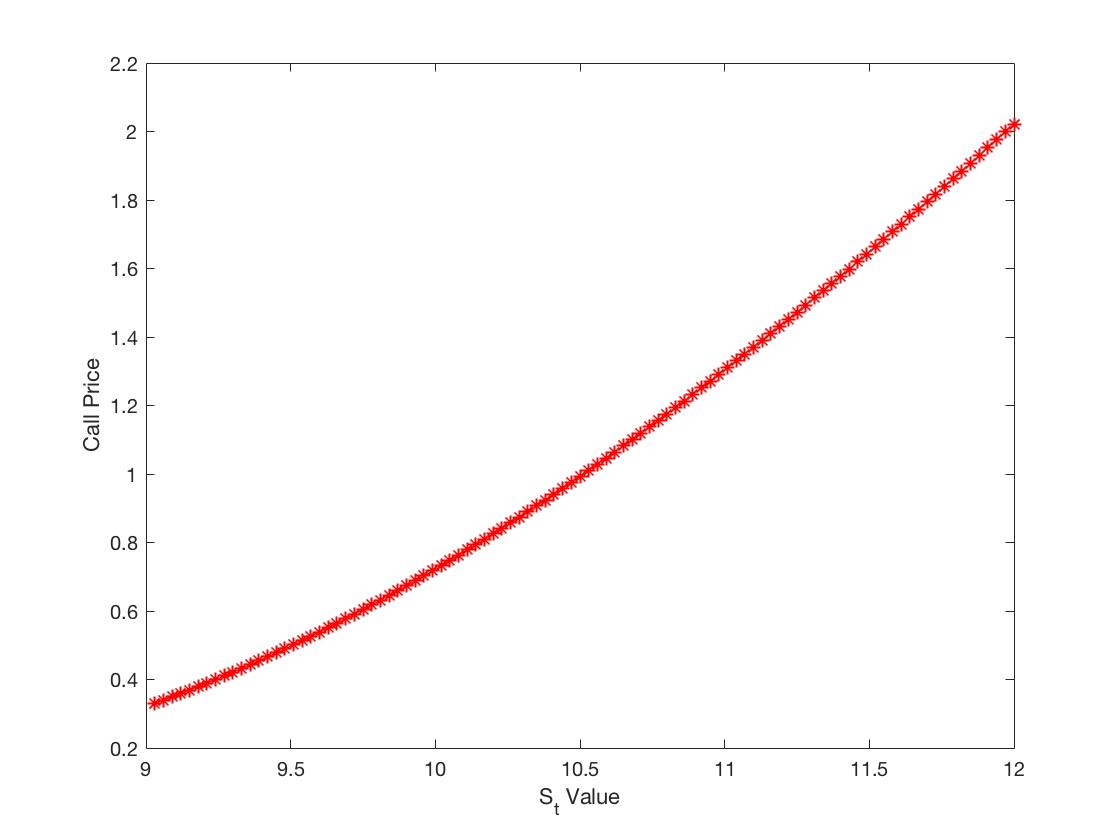

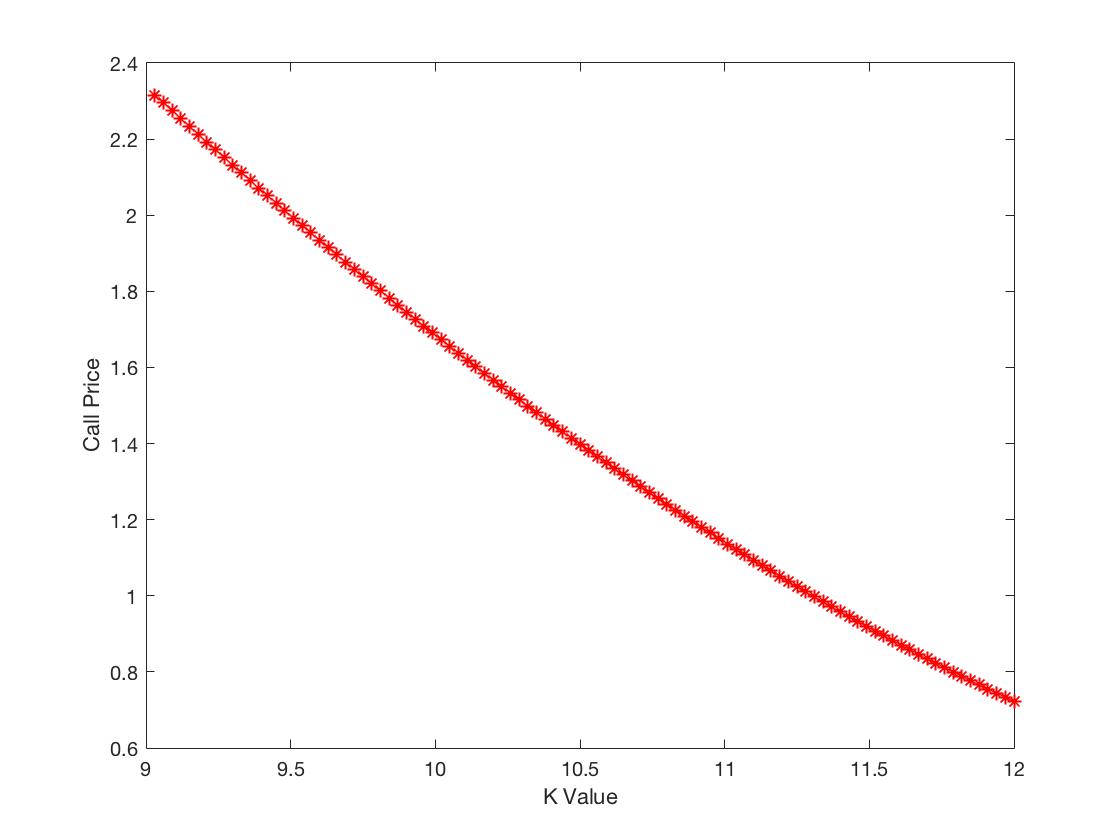

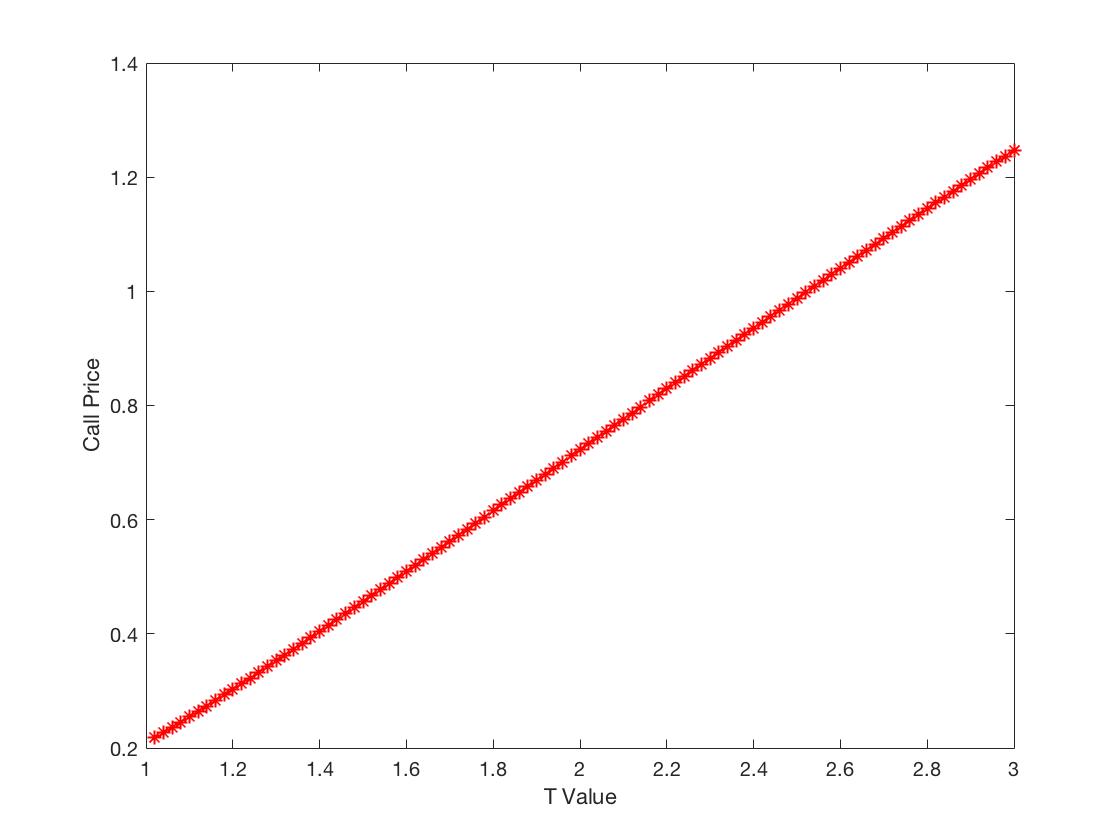

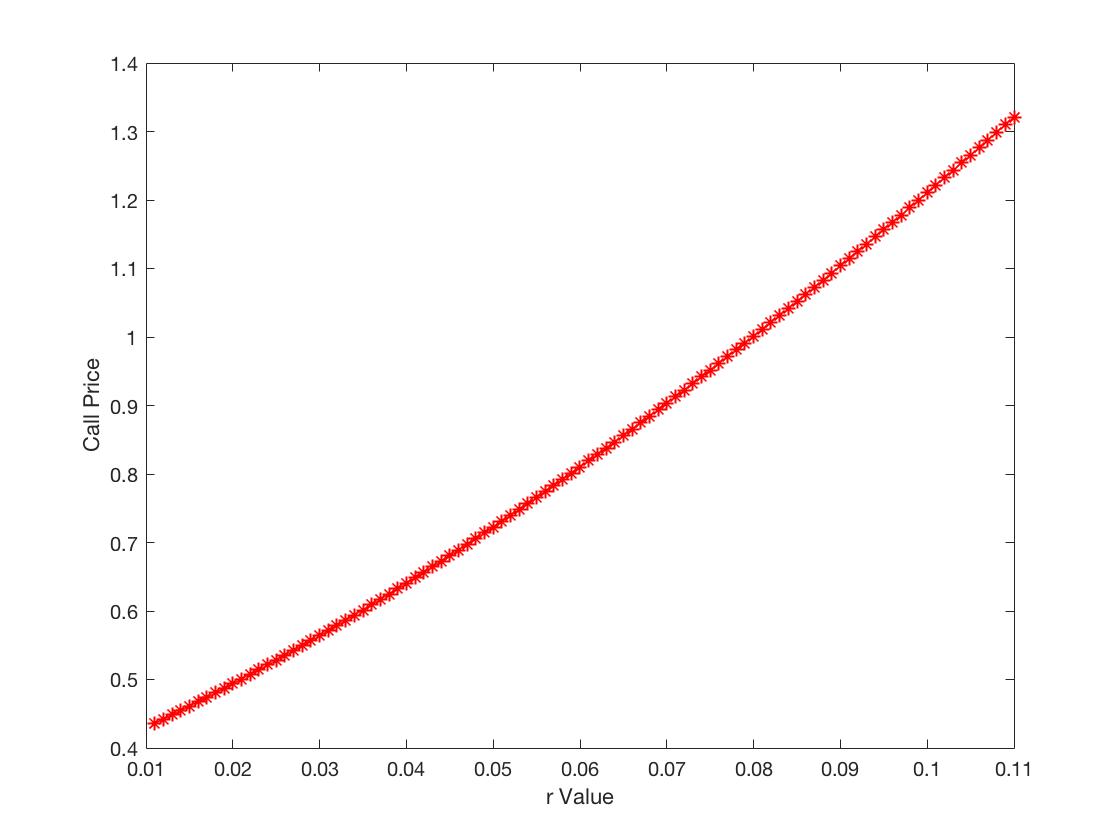

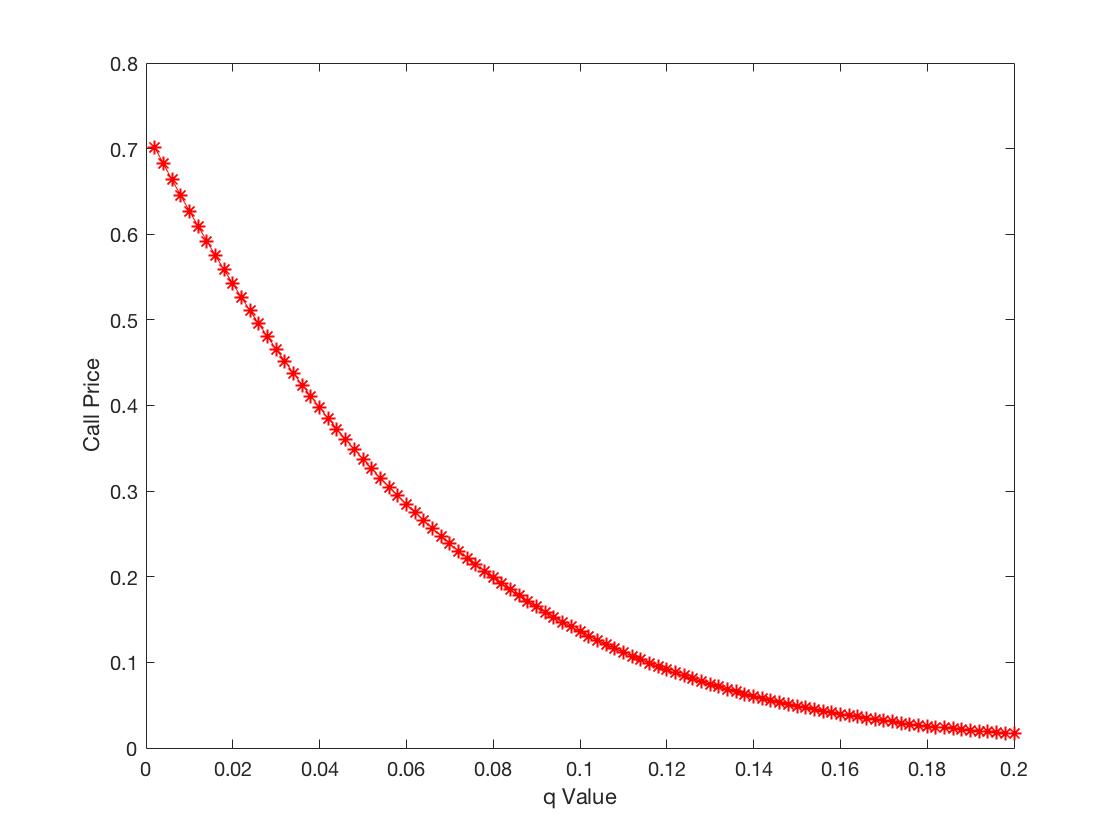

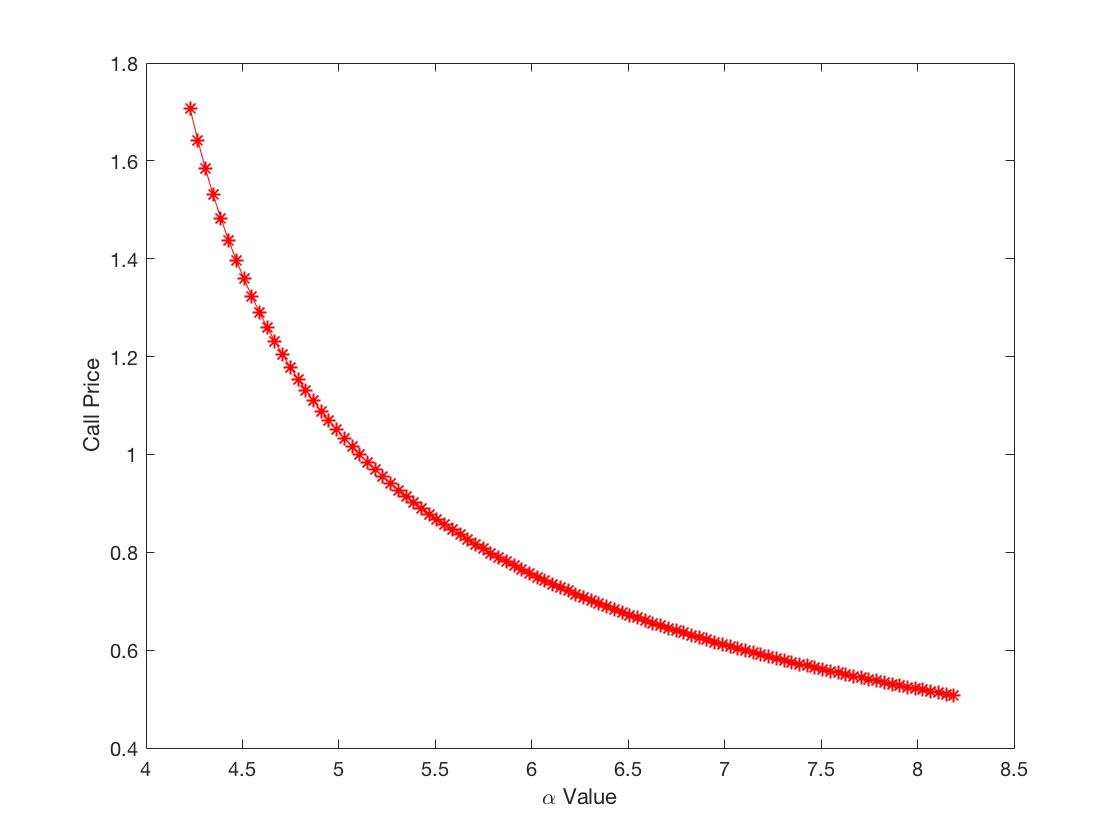

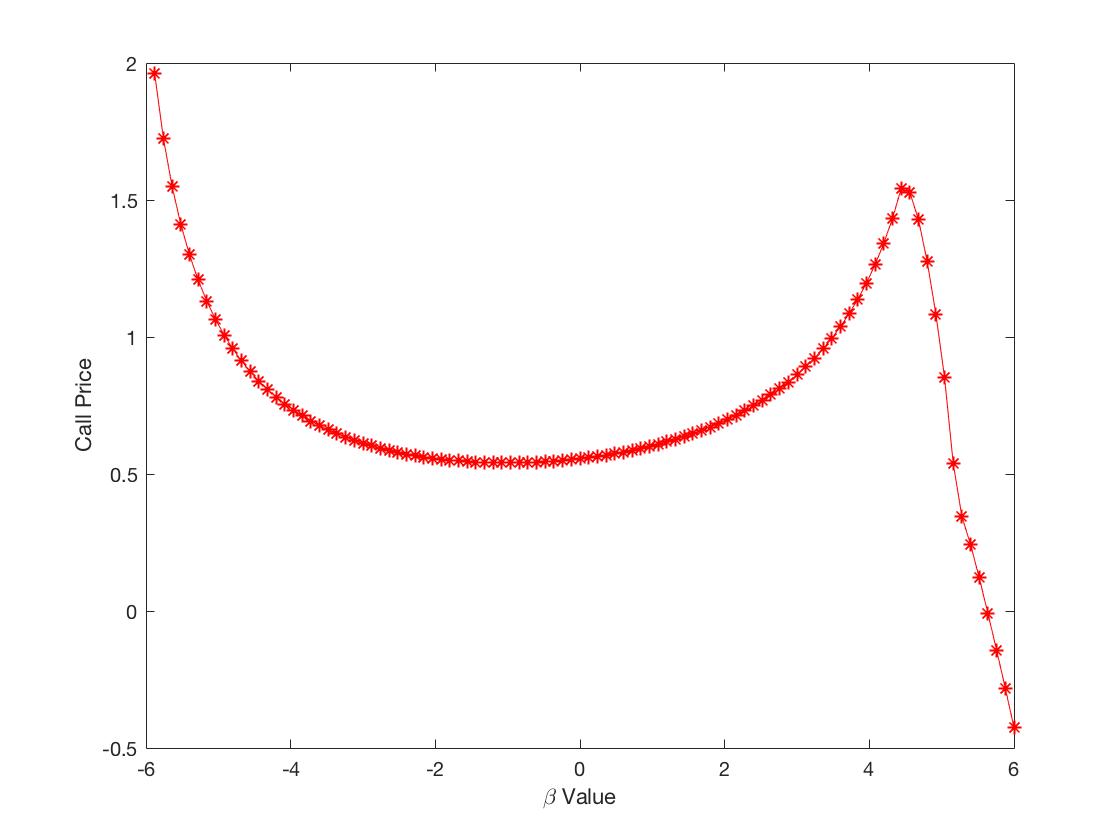

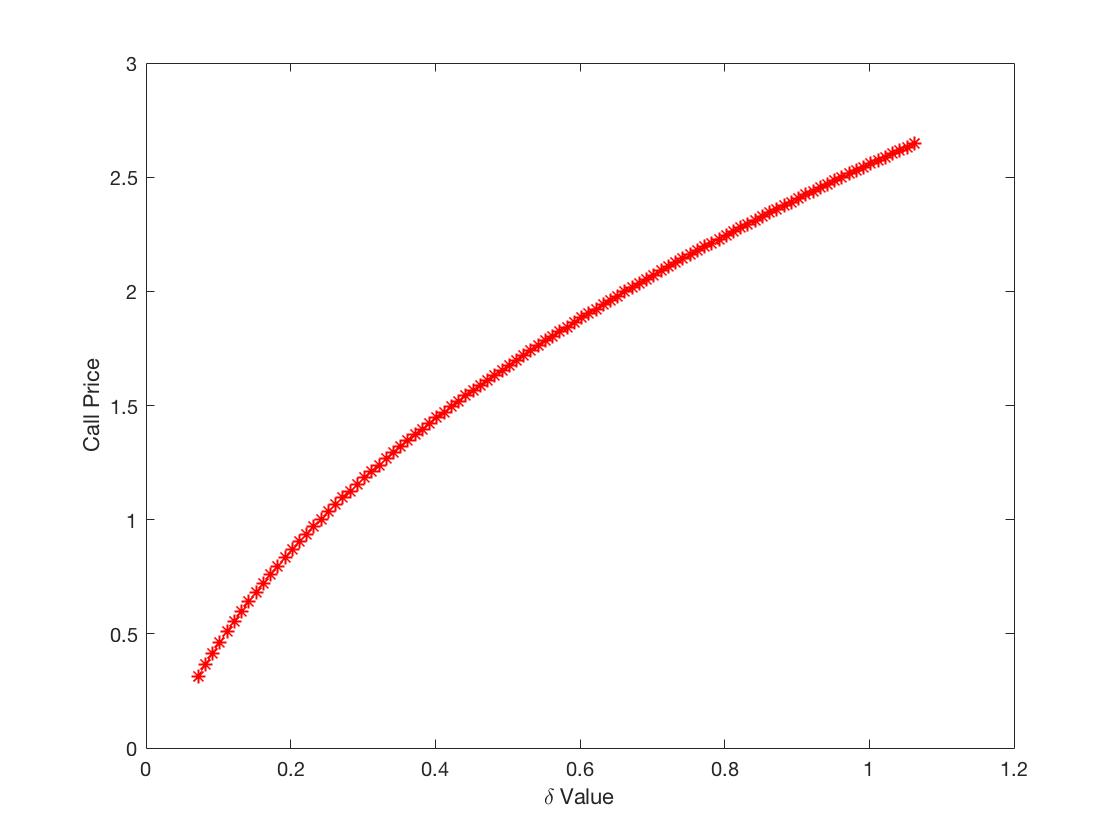

For the GH model, we set from Schoutens (2003) to understand the sensitivities of the option price with respect to various parameters. With this data, we compute call prices around the existing parameters by using FFT method with the given characteristic function. Visualizing the trends, we get nine figures listed in Figure (1a) to (1i).

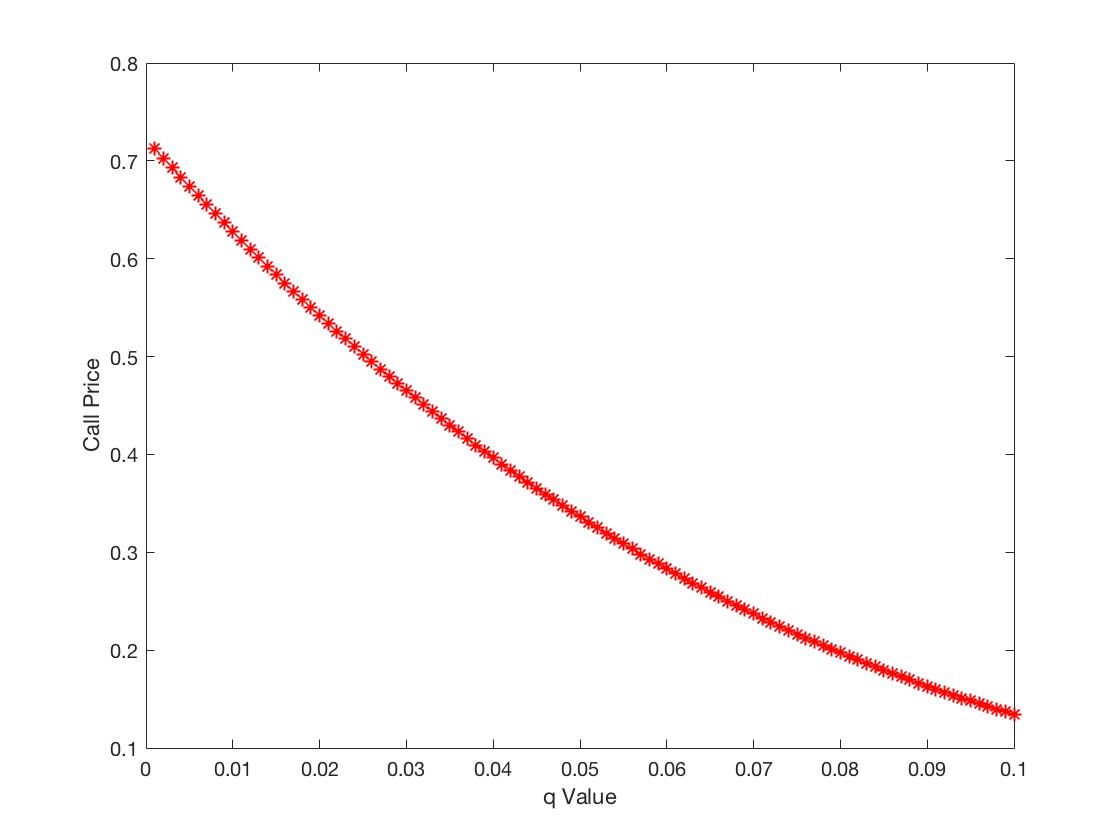

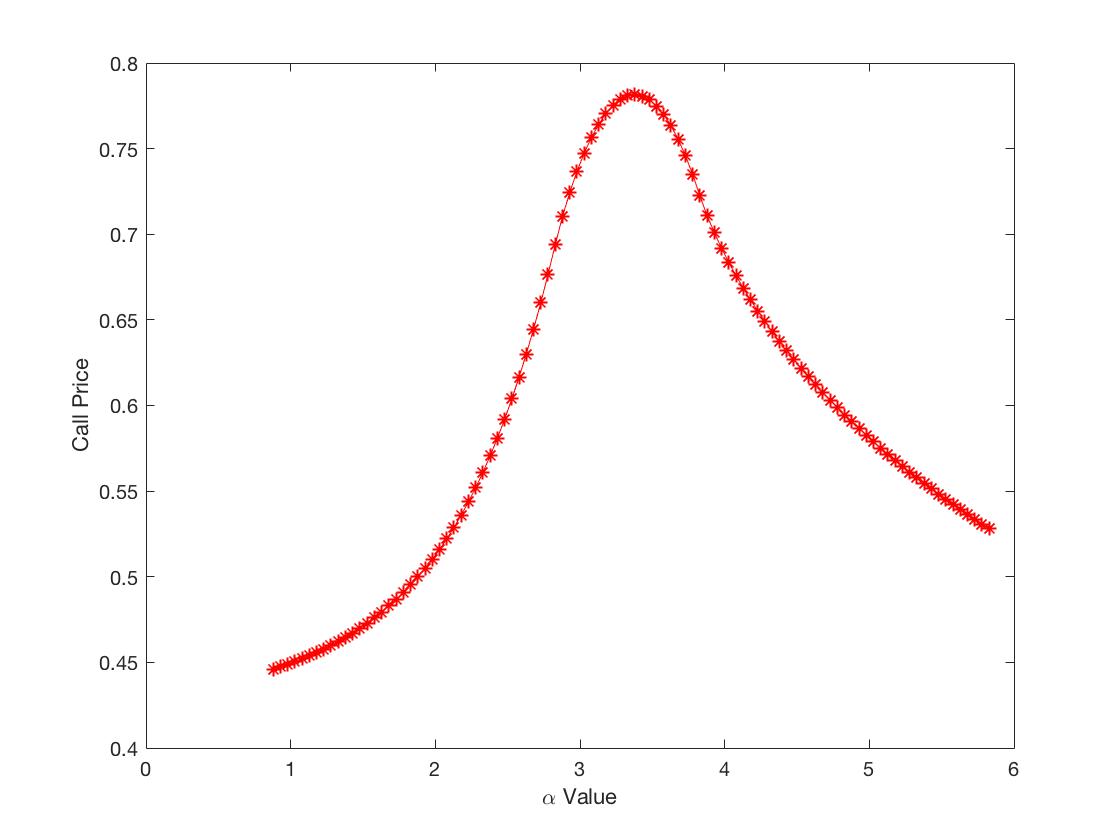

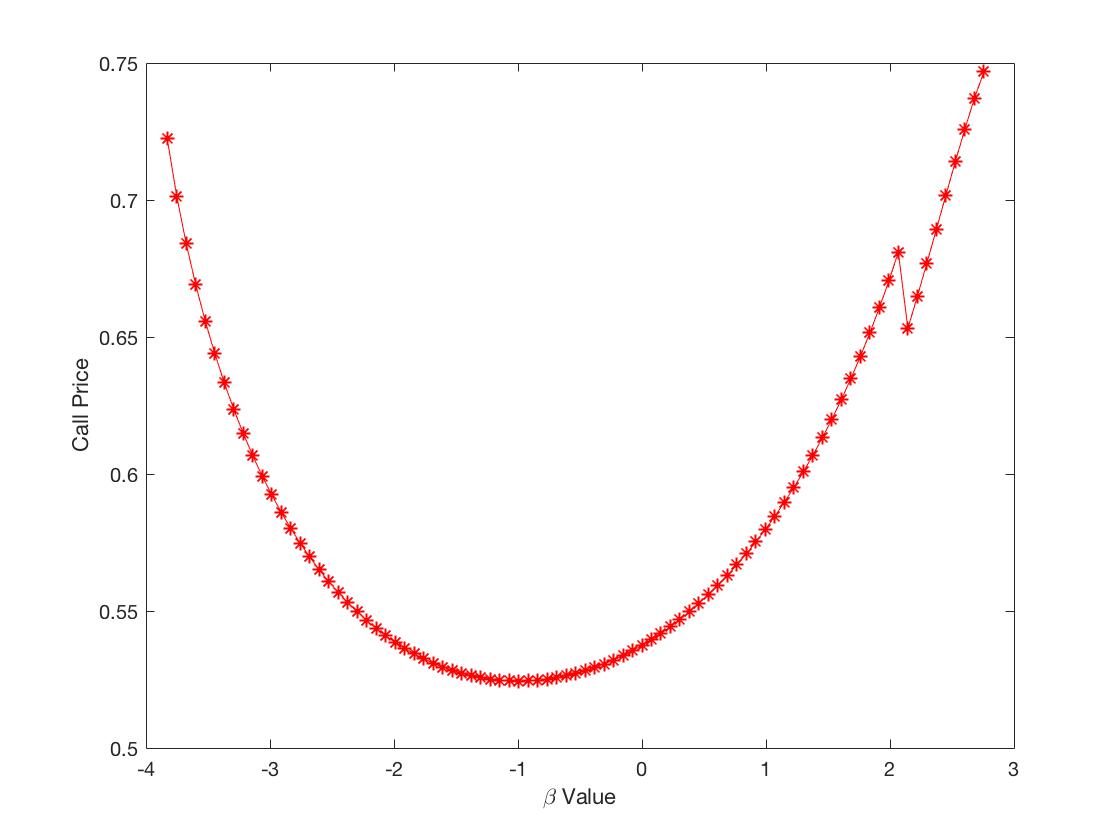

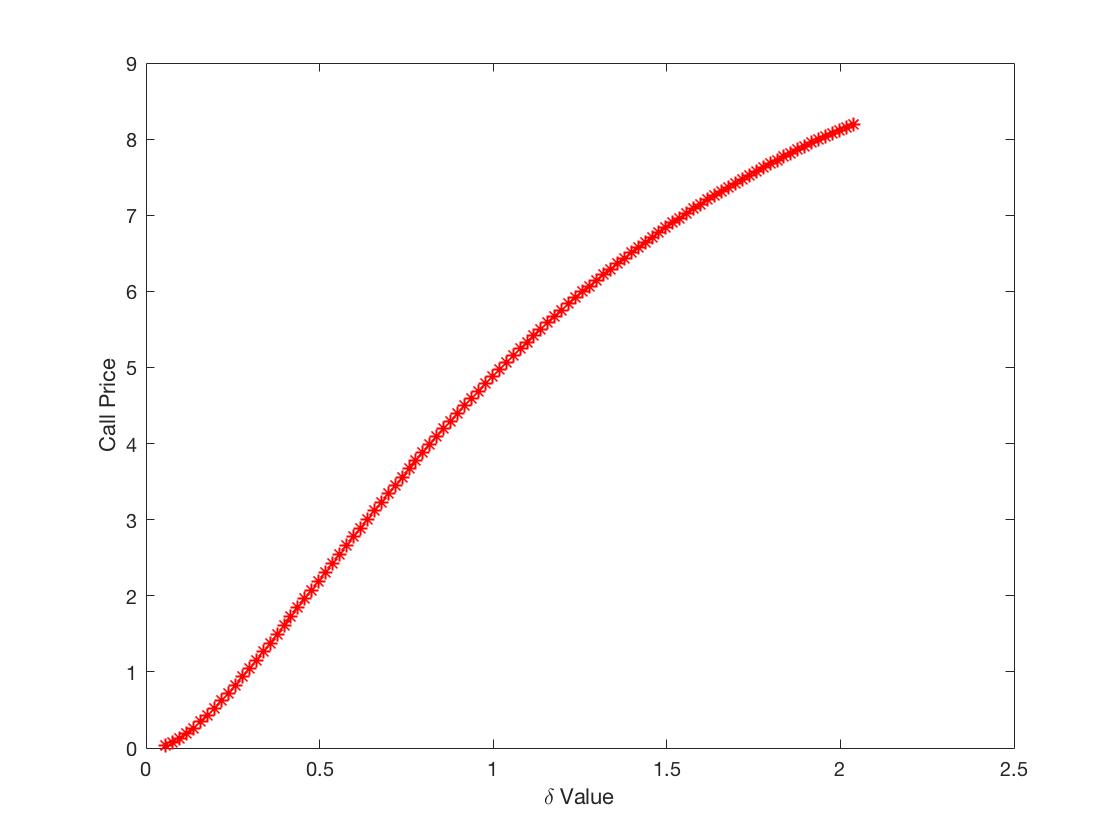

Figure 1 illustrates the call option prices under the GH model for the underlying asset increases with respect to the underlying asset price , the time to maturity , the risk-free rate and the parameter , decreases with respect to the strike price K and the dividend rate . The call option price presents a hump shape with respect to the parameter , a concave up shape with respect to the parameter , a concave up increasing and then concave down increasing to near flat shape with respect to the parameter for the GH model.

2. Normal Inverse Gaussian (NIG) Distribution

Setting , we get the Normal Inverse Gaussian (NIG) distribution from the hyperbolic model in Barndorff-Nielsen (1997). The characteristic function of the NIG distribution is given by

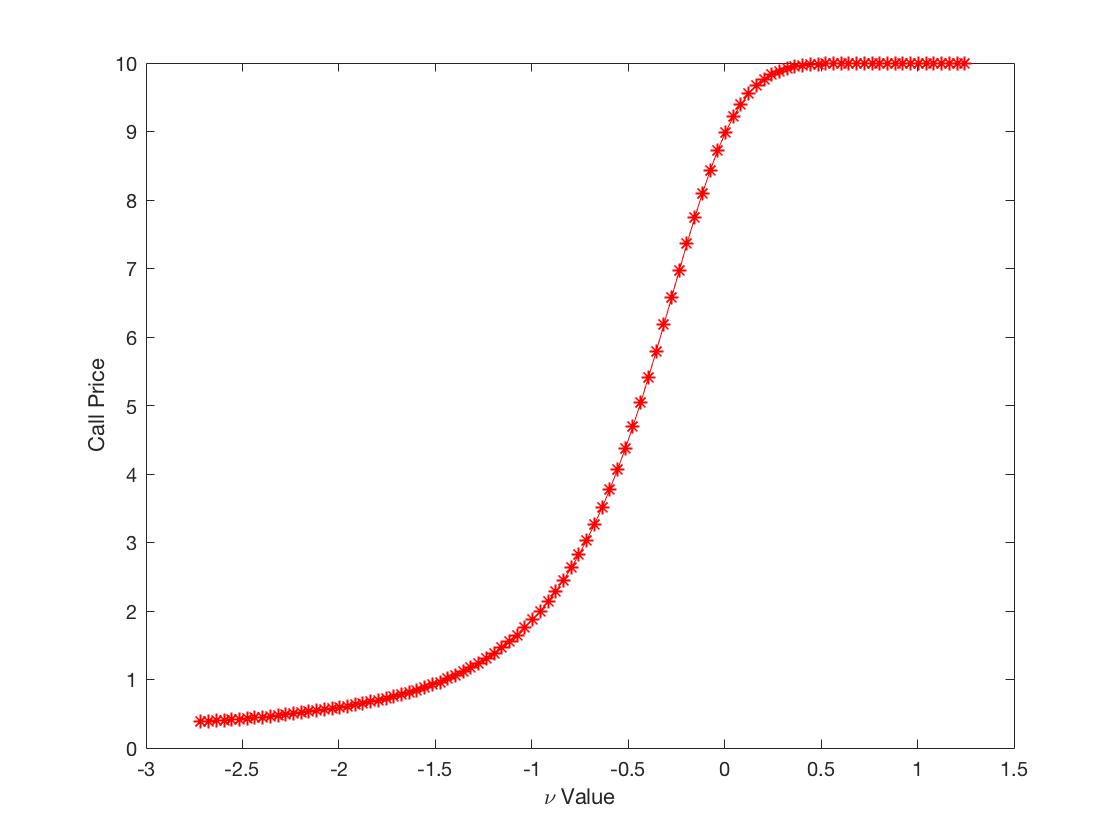

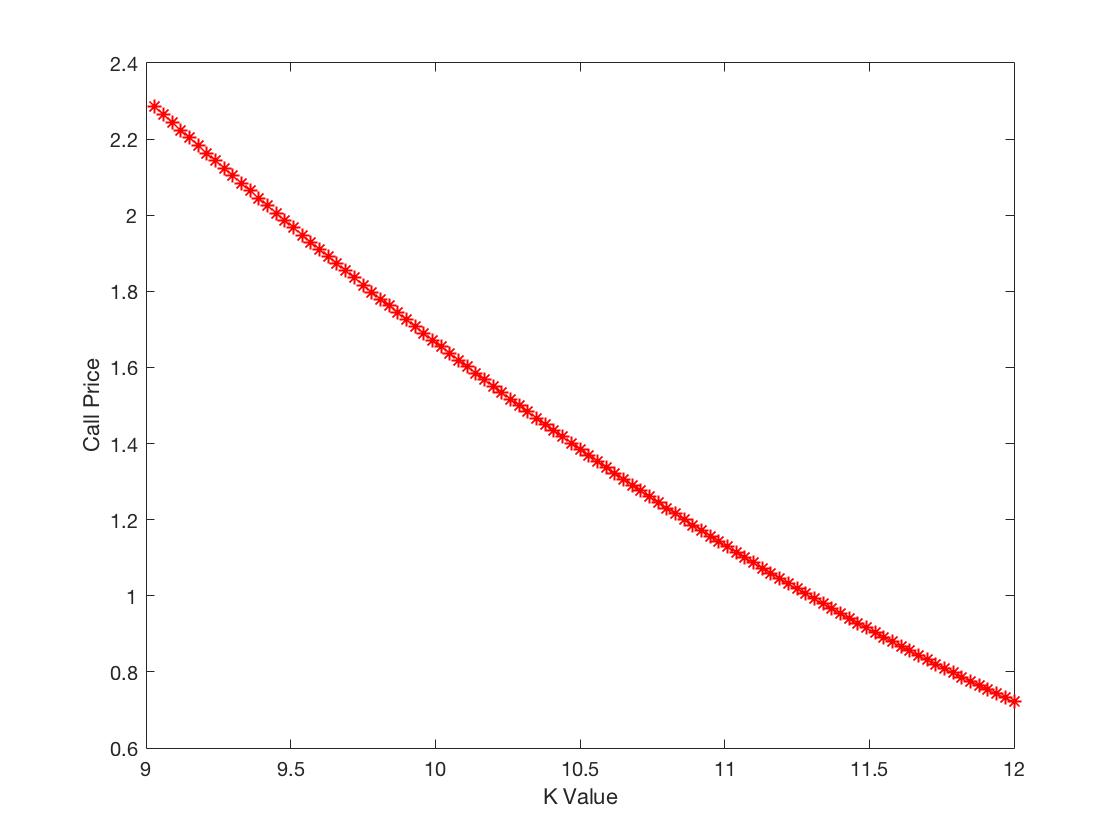

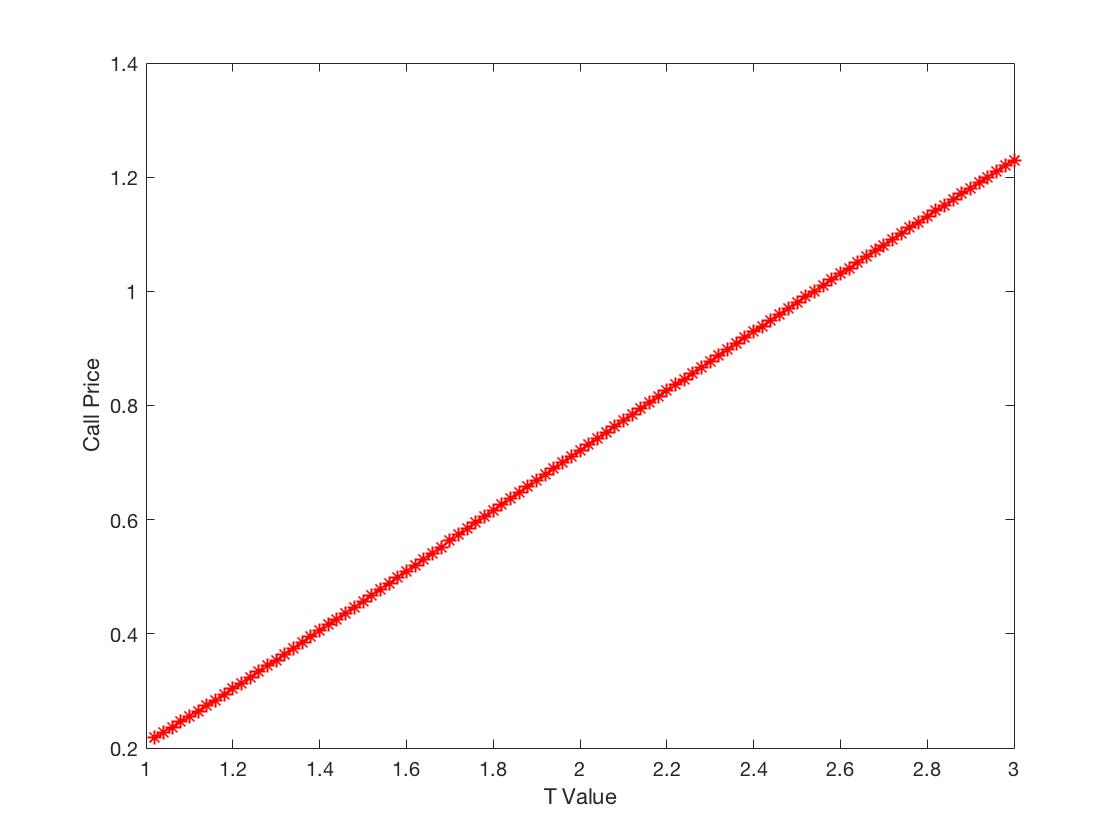

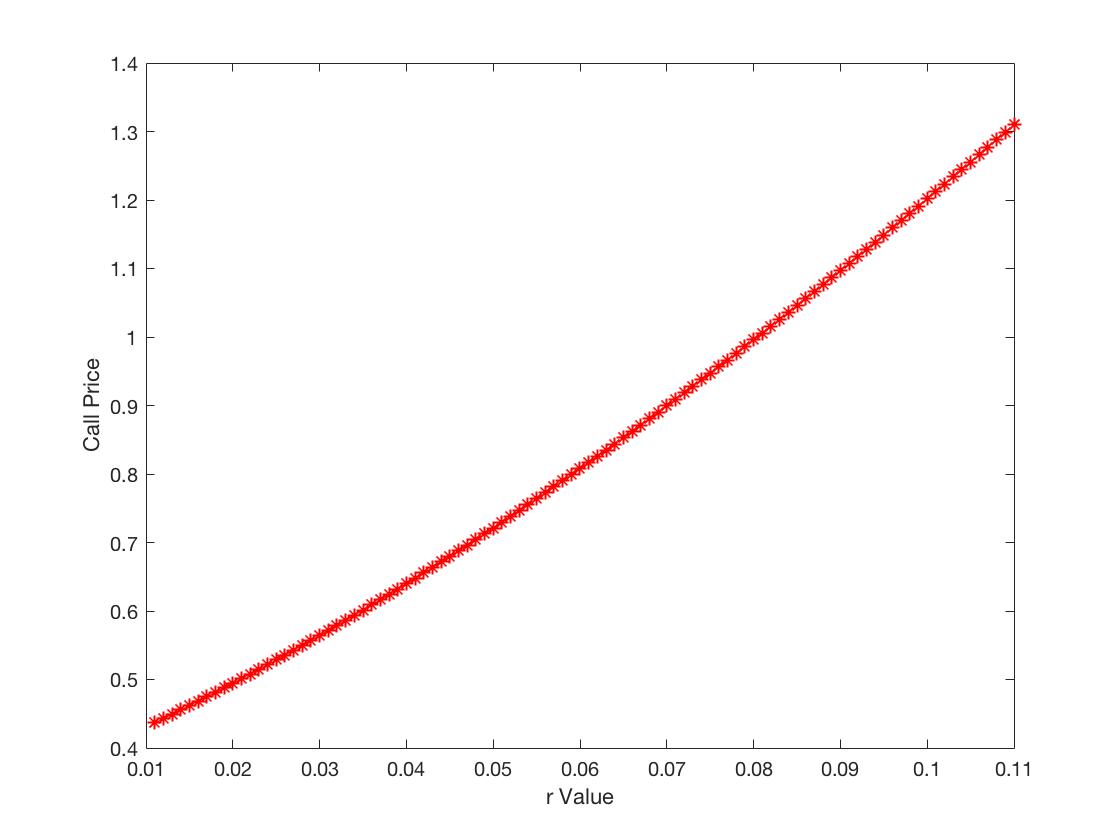

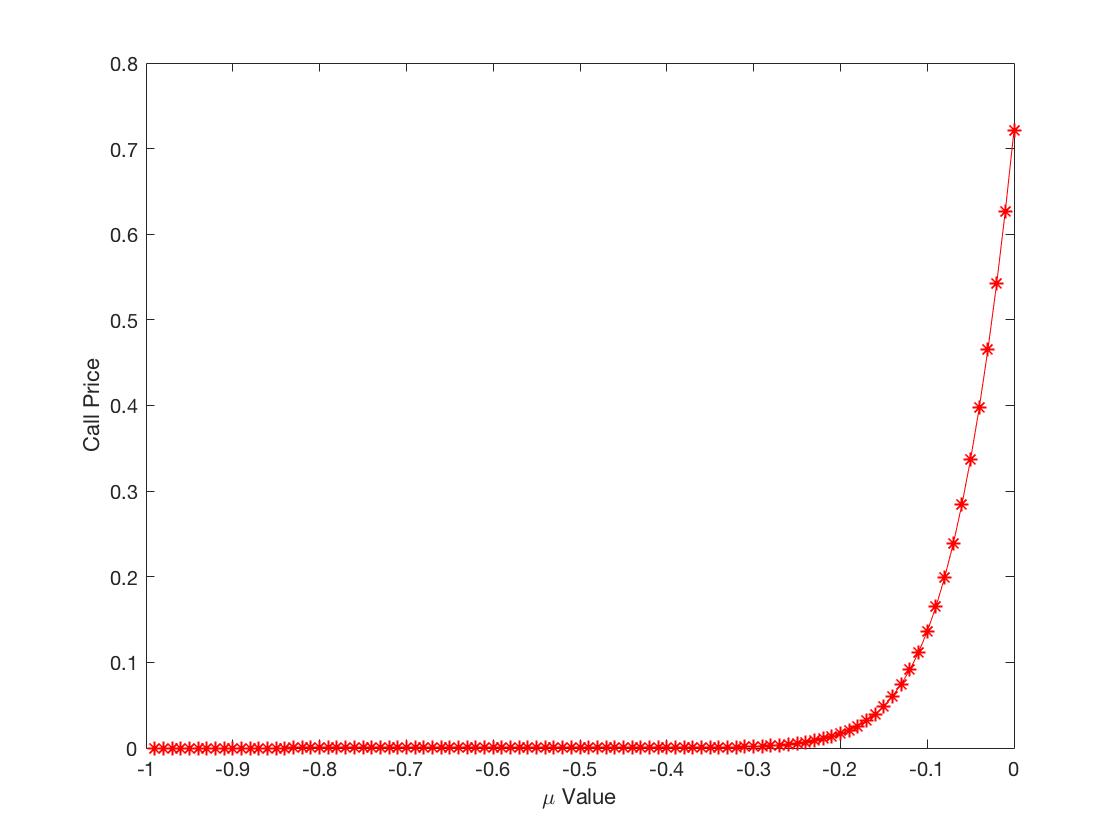

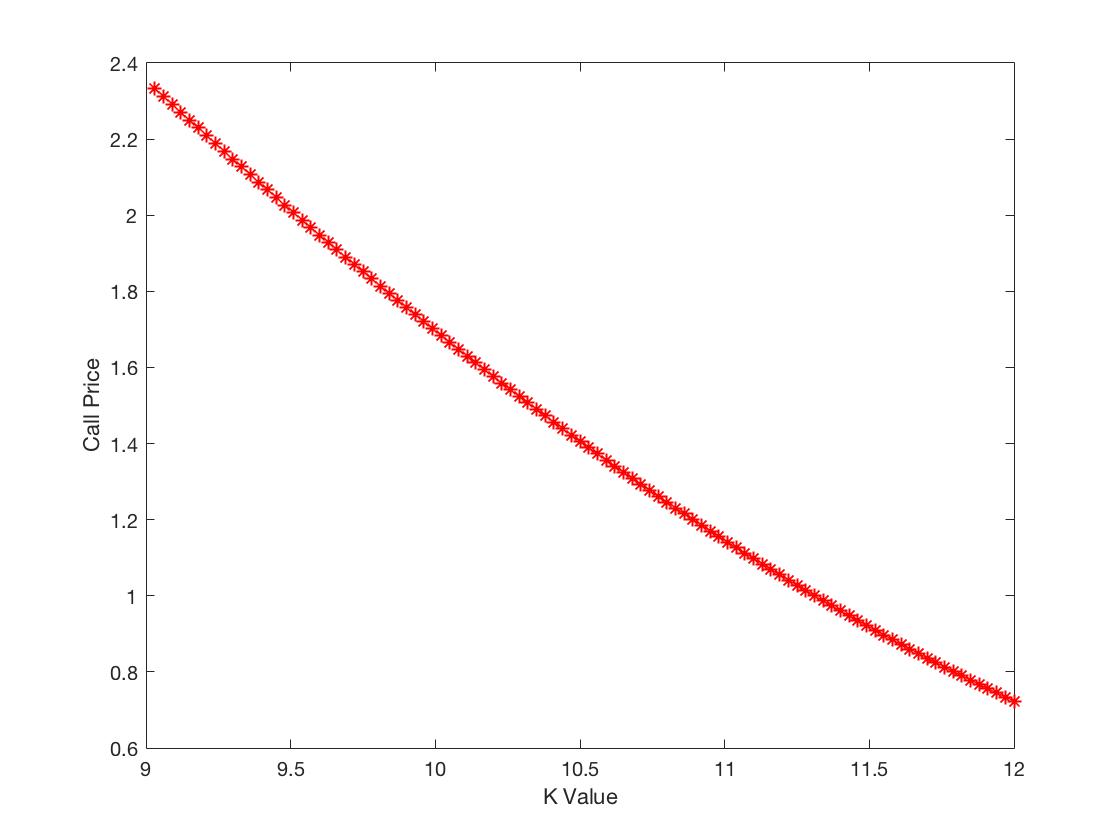

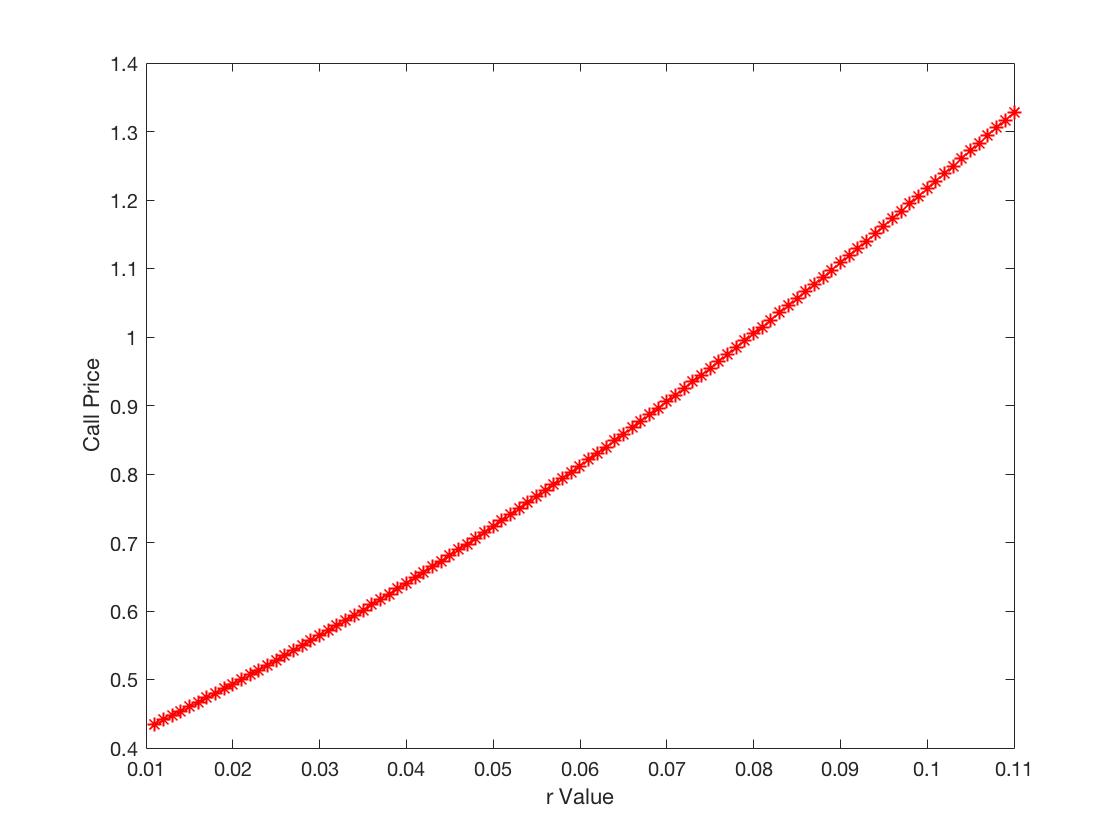

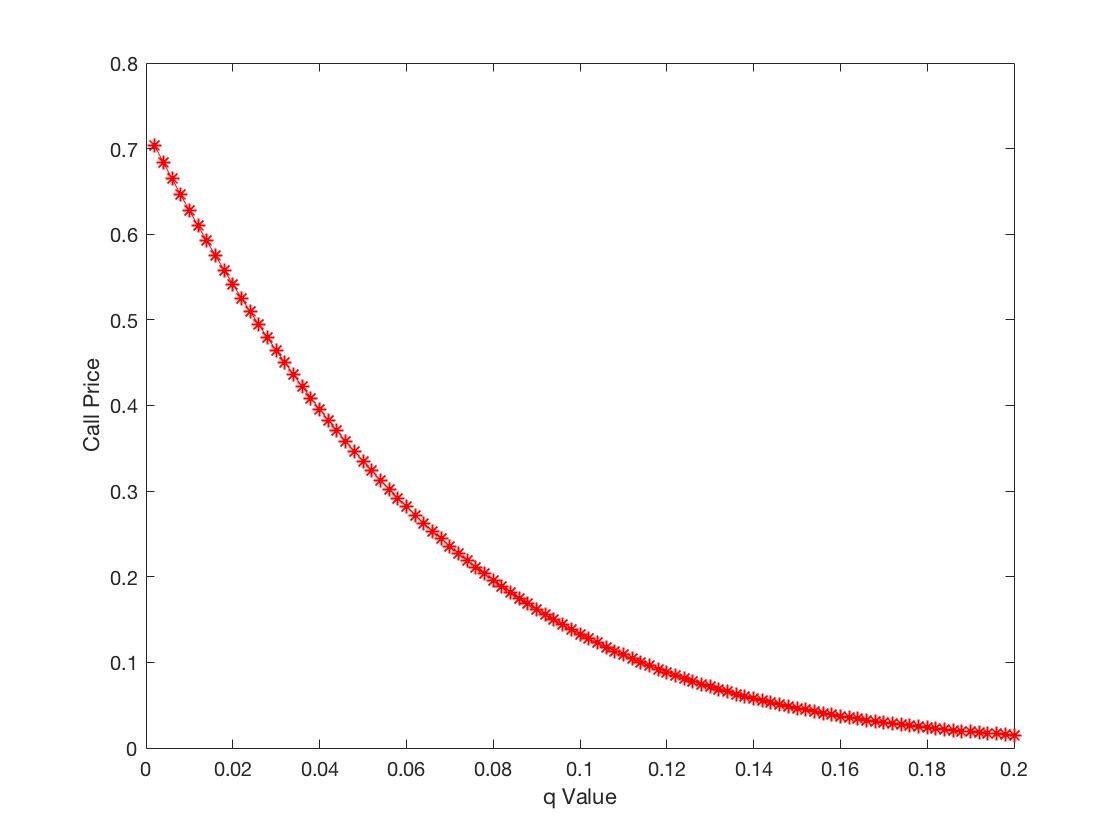

For the NIG model, we set from Schoutens (2003) to understand the sensitivities of the option price with respect to various parameters. We set as the initial value for NIG model since it is the drifting term of process. Therefore, we obtain Figure (LABEL:fig:NIGpara) by FFT method estimation for existing characteristic function of the NIG model.

For the NIG model, Figure 2 shows that the option price is increasing with respect to and , is decreasing with respect to , and . And there is no trend about , where it exhibits the concave up shape connecting with a deep down. For the parameter , the behavior is undetermined since the NIG is a special case of the GH model. The option price is increasing concave down way for the parameter , and concave up way for the parameter .

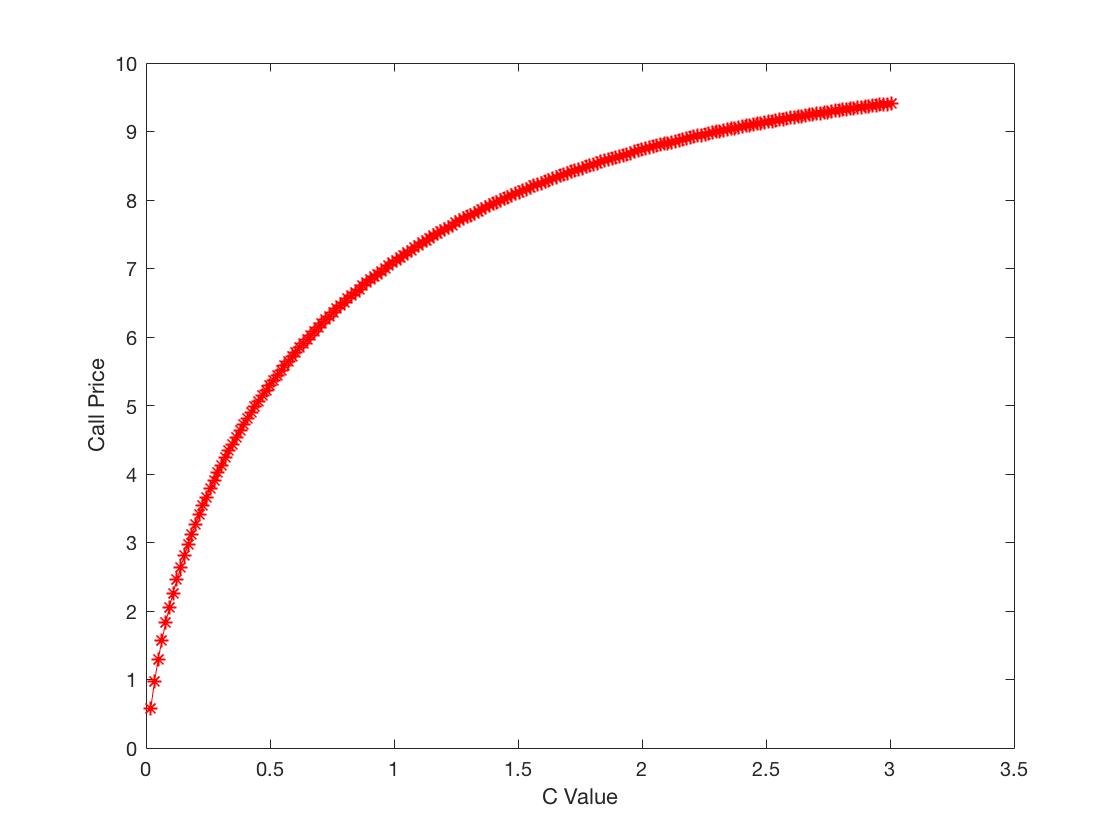

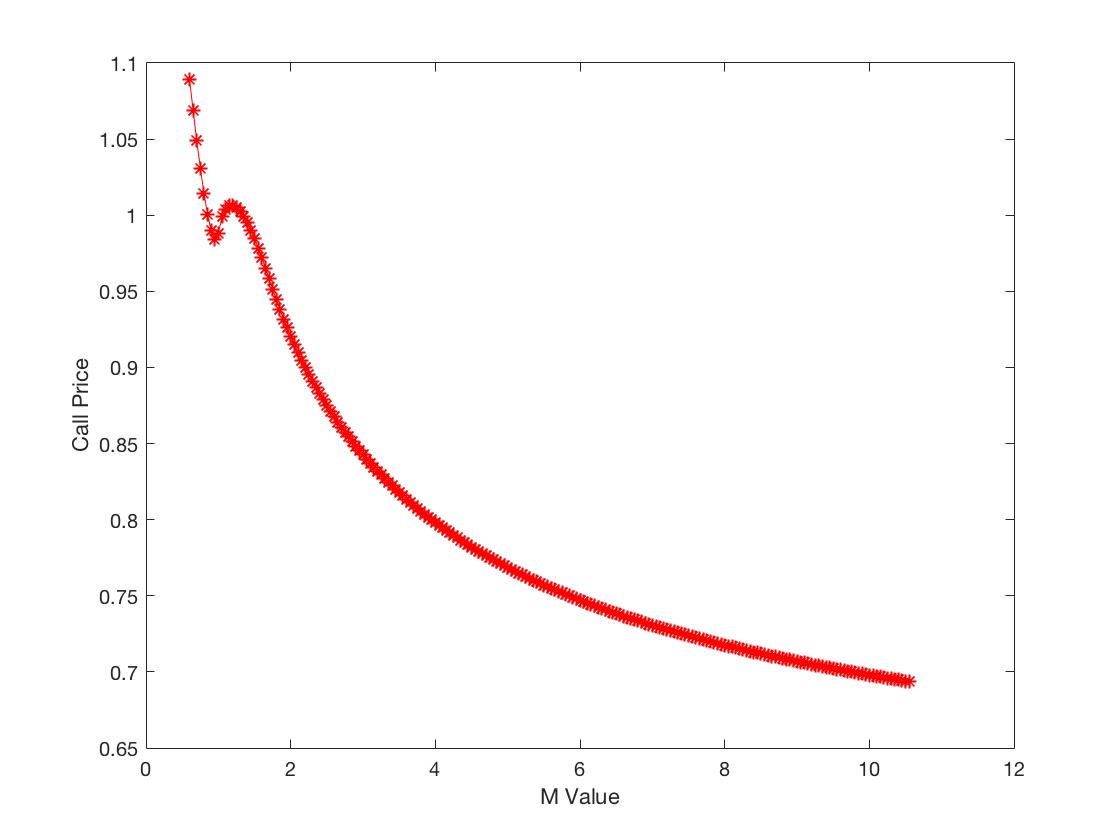

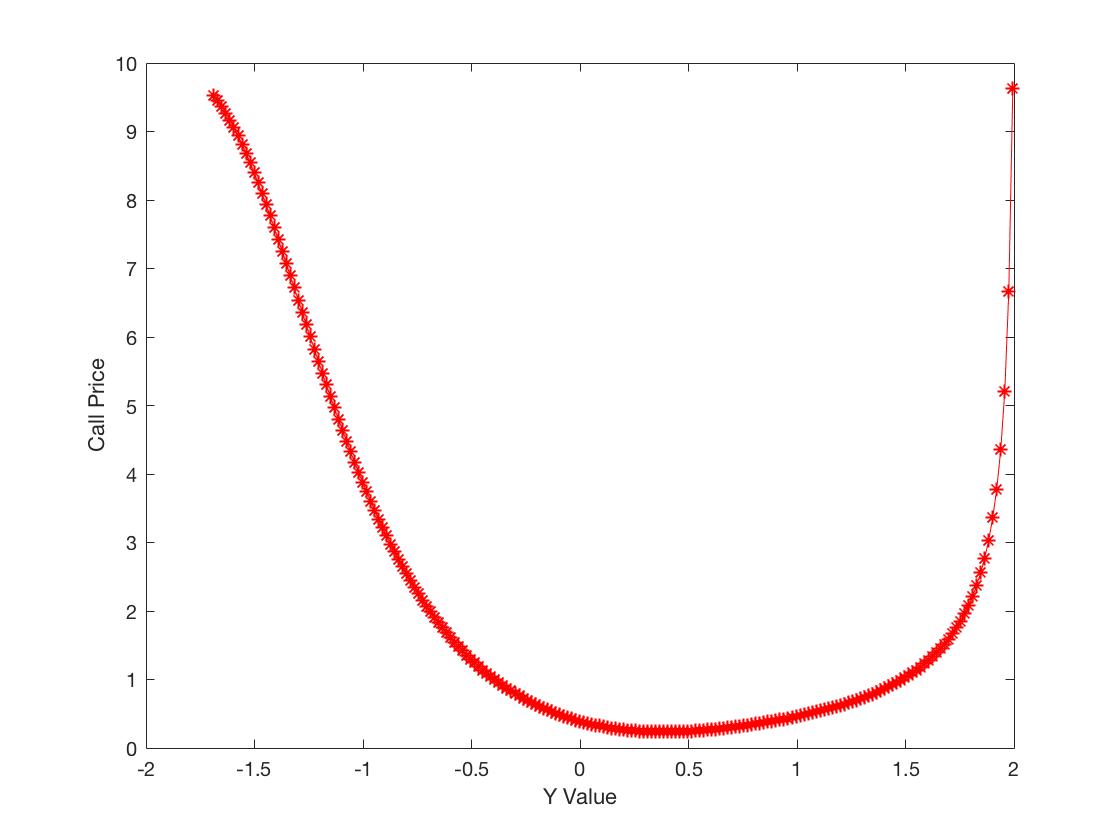

3. The Carr-Geman-Madan-Yor (CGMY) Class of Distribution

The CGMY distribution class is defined by Carr et al. (2002) with the Lévy density

The characteristic function of the CGMY distribution is

The CGMY model is also the class of tempered stable processes with time changed Brownian motion, it has a better model freedom than those with Brownian subordination. The main impact on option prices is due to large jumps, and the CGMY model shows its flexibility among those tempered stable processes.

For the CGMY model, we set from Schoutens (2003). The FFT method for estimating call option prices gives Figures (LABEL:fig:CGMYpara) about parameter sensitivities.

For the CGMY model over our data range, the option price is increasing with respect to , and increasing concave down way in , is decreasing with respect to , and decreasing concave up way in and . And the tendency about is increasing with a small hump and then starts to decrease. The option price has the U-shape with respect to the parameter Y in the CGMY model.

4 Empirical Analysis on S&P 500 Index Option

In this section, we use the sum of squared pricing error (SSE) method to calibrate the model parameters by optimizing the least squared summation as Bakshi et al. (1997) did for those five models. We focus on the BS, SV, Non-iid, Lévy processes (GH, NIG, CGMY) models to compare the relative performance on these variations. First we shall use the data to examine the direction and the extent of biases associated with the BS, to back out a BS implied volatility from each option price in the sample.

The sum of squared dollar pricing errors (SSE) is obtained by following. Collect option prices on S&P 500 option taken from the same period. For each , setting and be the time-to-maturity and the strike prices of the -th option respectively. Let be the observed market option price and the model price determined by equation (6) for BS, SV and equation (8) for non-iid and equation (9) for the three typical Lévy jump models. The difference between and is a function of and parameters. Define . Then SSE is defined by

| (10) |

where is the Black-Scholes sensitivity of the option price with respect to the market implied volatility :

and is the standard normal density (see Lewis (2000) or Christoffersen et al. (2009)). Note that our is normalized by the Vega refer to Christoffersen et al. (2009), where Bakshi et al. (1997) simply use the squared dollar pricing errors without the term.

Considering the S&P 500 index option during September 2012 to August 2013, the previous half year’s data, from September 4th 2012 to February 28th 2013, is treated as in-sample and the latter period, from March 1st 2013 to August 30th 2013, as out-of-sample. For the spot volatility which is conditional on no jump from the BS model, the structural parameters and the jump-related parameters as well as parameters of three typical Lévy models are required to be estimated. One may apply econometric tools to obtain these required estimations. However, in order to be consistent with the empirical results along Bakshi et al. (1997), we follow their method to reduce data requirement dramatically (comparing to other methods) and also improve the performance significantly.

4.1 In-sample Pricing Fit

1. Comparison of BS model and Heston Model

For the in-sample data, we need to find the optimal parameters in the close-form Heston option price formula (6) firstly to fix those continuous model parameters (no jumps). We minimize (10) by applying an implied parameter procedure to implement candidate models to best estimate each model parameters.

The parameters are estimated by function in Matlab to find the group of parameters which make the SSE value in (10) to be the minimum. The is an important gradient-based algorithm of Matlab to find a constrained minimum for a multivariable function for nonlinear optimization starts at an initial estimate. Based on previous results in Bakshi et al. (1997) and Rouah (2013), we can have a rough idea to restrict each parameter in its searching region. In our experiments, the searching initial and range of parameters are listing below. The parameter starts at 2 in the range , the parameter starts with in the range , with initial parameter 1.3 lies in , the prarmeter starts at 0.8 in the range . Similarly we have that starts at 0.05 in , starts at -0.1 in and starts at 0.1 in . The volatility starts at 0.5 in from earlier empirical estimates Bakshi et al. (1997), Rouah (2013) etc.

For the in-sample data, there are total option prices for S&P 500 index. We handle two panels of different upper bound as 100 and 500 for the integral in the equation (7) due to different computational consumption. The parameters are listed in Table 3.

The results tell us the two panels have the same order of magnitude of SSE values although the panel B has smaller numbers. We prefer to use results of integral upper bound as 100 in panel A to compare with Lévy processes calibration later since it has lower computational consumption. For different time periods, we can see those parameters varying dramatically as our Table 3 for the S&P 500 index option on September 4, 2012– Feburary 28, 2013 and Table III for the S&P 500 index option on June 1988–May 1991 of Bakshi et al. (1997).

For every panel, we deal with the diffusion volatility in two cases. One case is to use the implied volatility given by the market noted as . Another case is to estimate that parameter as a fixed value in the optimal searching.

The structural parameters of SV and SVJ are estimated by minimizing the sum of squared pricing errors between the market price and the model-determined price for options in each day in the sample period. The SSE in (10) with weighted BSVega is estimated in Panel A with the upper bound 100 and Panel B with the upper bound 500. For each model in each panel, there are two ways to choose the volatility parameter, first column is estimated by using the implied volatility and the second column by estimating the volatility parameter. The results show that the two panels have the same order of magnitude of SSE values although Panel B has smaller numbers. Panel A (upbound=100) Panel B (upbound=500) SV SVJ SV SVJ 20.0000 12.8826 19.9994 13.2477 20.0000 10.329 20.0000 11.493 0.0112 0.0125 0.0109 0.0131 0.0336 0.0112 0.0319 0.0108 0.7329 0.1399 0.7244 0.1551 2.2288 0.3169 2.1773 0.2422 0.1954 0.7938 0.1921 0.6891 0.0054 0.5992 -0.0025 0.7659 0.0089 0.0090 0.0076 0.0077 0.5207 0.0530 0.00001 0.00001 0.0001 -0.0001 -0.0592 -0.3245 0.0002 0.0009 1.9679 0.00009 SSE 5.1238 4.1293 5.1045 4.0942 3.7231 3.5773 3.7668 3.5591

Table 3 illustrates that the SSE results, are equal to 5.1238 for using the implied volatility in the first case, and equal to 4.1293 for the second case of estimating volatility value of SV model in panel A. We see that the second case of estimating volatility value gets the lower consequence in both panel A and B. And the SSE value drops a bit from 5.1238 of SV model to 5.1045 of SVJ model for the first volatility case in panel A due to the jump, and from 4.1293 of SV model to 4.0942 of SVJ mode for the second estimating volatility parameter. Generally, SVJ model has the lower SSE values except the findings in panel B, which has 3.7231 of SV model improved to 3.7668 of SVJ model in the first volatility case of panel B, from 3.5773 of SV model to 3.5591 of SVJ model for the second estimating volatility parameter. This is a clue for the idea that the Poison jumps part in Heston model contributes less misspecification on option prices.

The comparison with the BS model is listed in Table 4.

Define averages of error (AE) between the Heston model price and the market price as and averages of relative error (ARE) as . The AE and ARE values are remarkably dropping from BS model to Heston model for all cases.

For both implied volatility and estimating volatility parameter cases, the SSE, AE and ARE are improved from the BS model to the Heston model, and from the SV model to the SVJ model for both cases in each corresponding panel, except in Panel B the AE and ARE of the SV model for the implied volatility case are smaller than those of SVJ and the ARE of the SV model for the estimating volatility case is smaller than that of the SVJ model.

Panel A (upbound=100)

Panel B (upbound=500)

BS

SV

SVJ

SV

SVJ

estimate

estimate

estimate

estimate

SSE

96.3520

5.1238

4.1293

5.1045

4.0942

3.7231

3.5773

3.7668

3.5591

AE

15.8135

1.9272

1.8763

1.8982

1.8305

1.6279

1.6004

1.6529

1.5676

ARE

4.4620

0.6035

0.5400

0.5770

0.5082

0.4692

0.4123

0.5139

0.4183

The Heston model has the sum of squared error dramatically less than BS model by comparing the consequence in Table 4 for both implied volatility and estimating volatility cases. Table 4 shows that the SSE values are 96.3520 of the BS model and 5.1238 for the SV model with implied volatility case and 4.1293 for estimating volatility case. Define averages of error (AE) between the Heston model price and the market price as and averages of relative error (ARE) as . The AE and ARE values are remarkably dropping from the BS model to the Heston model for all cases. Table 4 also shows that for in-sample data, the SSE, AE and ARE values decreases slightly as 1%, 2% and 6% respectively when jump is considered for the first panel. All the SSE, AE and ARE are improved from the BS model to the Heston model, and from the SV model to the SVJ model for both cases in each corresponding panel, except in panel B the AE and ARE of the SV model for the implied volatility case are smaller than those of the SVJ model, and the ARE of the SV model for the estimating volatility case is smaller than that of the SVJ model.

2. Comparison of the BS model and the Non-iid model

With the models of three cases of non-iid price jumps distribution, we may compare with classic BS model together.

For the case with jumps, the parameters are using market implied volatility or , and , , consistently of Panel A in the Heston model calibrations. The half-year in-sample non-iid cases empirical comparisons against the BS model are showing in Table 5.

For the first case in the model next to the BS model, take , , , , and the others are zeroes for the varying mean in the jumping size; the jumping variance keeps unchanged.

For the second case of non-iid models with varying variance in the jumping size, take , the mean in the jumping size is fixed,

and the variance of the jumping size varies , , , and the others are zeroes.

For the third case of autocorrelated non-iid models, as using the parameters from the Heston model, , , , , . AE means the average of errors, ARE means the average of relative errors. The percentages in the parenthesis are improvements according to BS model prices.

BS

Cor 1

Cor 2

Cor 3 (n=50)

(n=15)

= 0.009

= 0.009

= 0.009

= 0.009

SSE

96.3520

96.3076

93.1146

96.3075

93.1146

96.3076

93.1145

96.3076

93.1146

(0.044%)

(3.358%)

(0.044%)

(3.358%)

(0.044%)

(3.358%)

(0.044%)

(3.358%)

AE

15.8135

15.8093

15.4337

15.8093

15.4337

15.8093

15.4337

15.8093

15.4337

(0.004%)

(2.380%)

(0.004%)

(2.380%)

(0.004%)

(2.380%)

(0.004%)

(2.380%)

ARE

4.4620

4.4606

4.3081

4.4606

4.3081

4.4606

4.3081

4.4606

4.3081

(0.031%)

(3.449%)

(0.031%)

(3.449%)

(0.031%)

(3.449%)

(0.031%)

(3.449%)

Table 5 illustrates four models that the BS model against the three non-iid models with mean-varying, variance-varying and auto-correlated non-iid cases. For the auto-correlated non-iid case, we set two estimations for and . For the first case in the model next to the BS model, take , , , , and the others are zeroes for the varying mean in the jumping size; the jumping variance keeps unchanged. We get the results as and for implied volatility and estimated volatility cases respectively for in-sample.

For the second case of non-iid models with varying variance in the jumping size, take , the mean in the jumping size is fixed, and the variance of the jumping size varies , , , and the others are zeroes. The results are for implied volatility and for estimated volatility case for in-sample.

For the third case of autocorrelated non-iid models, as using the parameters from the Heston model, , , , , . The calculation results are for implied volatility and for estimated volatility for in-sample.

By checking results in Table 5, we can see that besides the SSE values, the AE and ARE values of three non-iid cases are very close to the BS model results as , and respectively. With the autocorrelation 0.95 between two consecutive jumps and decreases for 5 percent for every next period, we choose , then the farthest autocorrelation is . The almost same outcomes are obtained as the previous case when . The improvement percentages are around 3% for the three non-iid cases in Table 5 when is fixed as , and less than 0.1% for using market implied volatility.

Meanwhile, we want to know the sensitivities for parameters and . Furthermore, the influence of combined movements in both is tested. We check one day data for simplicity.

For one day data, we analysis 3 cases of the non-iid model: First is to set increase from , to then stay, and the parameter is always unchanged; Second is to set fixed as , decrease from , to , then stay at ; Third case is to let increase from , to then stays, and simultaneously decreases from , to , then stays in . Choosing the first day of the in-samples data then the results are listed in Table 6.

AE means Average Error, ARE means Average Relative Error. The percentages in the parenthesis are improvements according to BS model prices.

For the first day of in-sample data, we analysis 3 cases of the non-iid model: First is to set increase from , to then stay, and the parameter is always unchanged; Second is to set fixed as , decrease from , to , then stay in ; Third case is to let increase from , to then stays, and simultaneously decreases from , to , then stays in .

BS

Cor 1

Case 1

Case 2

Case 3

Cor 2

Case 1

Case 2

Case 3

SSE

1.0997

1.0519

1.0614

1.0423

1.049

1.0519

1.0614

1.0426

1.0492

(4.35%)

(3.48%)

(5.22%)

(4.61%)

(4.35%)

(3.48%)

(5.19%)

(4.59%)

AE

15.7474

15.2809

15.3664

15.1907

15.2544

15.2809

15.3664

15.1929

15.2561

(2.96%)

(2.42%)

(3.54%)

(3.13%)

(2.96%)

(2.42%)

(3.52%)

(3.12%)

ARE

2.8612

2.7669

2.7961

2.7537

2.7722

2.7669

2.7961

2.7541

2.7724

(3.30%)

(2.28%)

(3.76%)

(3.11%)

(3.30%)

(2.28%)

(3.74%)

(3.10%)

The improvement percentages show that both case 2 (e.g. for Corollary 1, SSE improvement is 5.22%) and case 3 (e.g., 4.61%) are better than the experiments show in Table 6 (e.g., 4.35%) but the case 1 (e.g., 3.48%) is worse. And the case 2 has the best improvement over all. Corollary 1 and Corollary 2 in the Non-iid model have almost the same improvement effects considering fluctuation due to the same scenario of these three cases.

3. Empirical Test for S&P 500 Call Option With Lévy Processes

As the last part of empirical test, three typical Lévy Processes we mentioned before are checked by optimal parameters searching. The comparison with previous Heston model is also considered.

For the data of S&P 500 option prices, we get the SSE values for these three Lévy processes for both in-sample and out-of-sample periods. The first step is to estimate the parameters for in-sample data, which is from September 4th 2012 to February 28th 2013. Gong and Zhuang (2016) use intelligent optimization Differential Evolution algorithm to calibrate the parameters for FFT estimation of Lévy processes dynamics. In our paper, the task is to make the SSE value be the minimum by using Matlab optimal function ”” due to the convenience of software toolbox.

As the initial parameter values for the optimal searching, results of Schoutens (2003) which calibrated the S&P 500 option index are referred. For the GH model, the initial values are , , , ; and the NIG model utilize , , , ; and the CGMY model use , , , for the initial parameters. All the estimations have upper bound and lower bound for the searching regions.

Table 7 below includes the parameters estimation and the corresponding SSE values.

The in-sample data comes from September 4th 2012 to February 28th 2013. These three typical Lévy processes have the equivalent order of magnitudes with the Heston model for the final SSE.

For the GH model, the initial values are , , , ; for the CGMY model use , , , for the initial parameters; and for the NIG model utilize , , , for the initial parameters based on results of Schoutens (2003). All the estimations have upper bound and lower bound for the searching regions. The greatest in-sample SSE result is 7.57 for GH model and the lowest is 4.13 for NIG model, the average is 6.21. According to Heston model, the greatest is 5.12 and lowest is 4.10 for in-sample with average 4.61. By comparison, the NIG model has the lowest answer in the 3 kinds of Lévy processes and very close to Heston model.

GH

NIG

CGMY

Heston SV model

SVJ model

model

model

model

estimate

estimate

-17.3388

19.999

15.6454

-15.421

0.3554

0.2295

-17.6347

-0.1667

C

4.47E-06

G

4.5725

M

6.8383

Y

1.9975

SSE

6.92

4.13

7.57

5.12

4.13

5.10

4.10

Table 7 shows that the biggest in-sample SSE result is 7.57 for GH model and the smallest is 4.13 for NIG model, the average is 6.21. From the final SSE results, we have that the Lévy processes have the equivalent order of magnitude of SSE values with the Heston model but slightly larger. According to the Heston model Panel A (we only consider Panel A for simplicity hereafter), the biggest is 5.12 and the smallest is 4.10 for in-sample with average of 4.61. By comparison, the NIG model has the smallest answers in the three kinds of Lévy processes and very close to the Heston model.

4.2 Out-of-sample Pricing Performance

1. Comparison of the BS model and the Heston Model

For the out-of-sample data, there are total option prices of the S&P 500 index. By using the parameters of in-sample estimation to evaluate, comparison for BS model and Heston model is in Table 8.

The out-of-sample period is from March 1, 2013 to August 30, 2013 of the S&P 500 index option prices. All models are using the parameters from in-sample estimations. The Heston model decreases the SSE value dramatically for the BS model for both implied volatility case and estimating volatility parameter case. Besides the SSE values, the Average Error (AE) and ARE means Average Relative Error (ARE) both have noticeable drops from the BS model to the Heston model for all cases.

Panel A (upbound=100)

Panel B (upbound=500)

BS

SV

SVJ

SV

SVJ

estimate

estimate

estimate

estimate

SSE

104.6249

6.6083

5.3216

6.5496

5.2743

5.5822

4.7935

5.6248

4.7672

AE

17.2347

2.9657

2.6315

2.9459

2.5960

2.7488

2.4067

2.7577

2.3761

ARE

2.4976

0.5995

0.4717

0.5856

0.4561

0.4342

0.3739

0.4557

0.3747

From the comparison, we see the Heston model decreases the SSE value dramatically for the BS model for both implied volatility case and estimating volatility case. The SSE values are 104.6249 of the BS model and 6.6083 for the Heston model of the first case with implied volatility estimates. Besides the SSE values, the Average Error (AE) and Average Relative Error (ARE) both have noticeable drops from the BS model to the Heston model for all cases. From the SV model to the SVJ model, improvements are 1%, 1%, and 2.3% on SSE, AE and ARE respectively for Panel A. That means the improvement with jumps contributing in calibration with the Heston models is small.

2. Comparison of the BS model and Non-iid Cases

With the same parameters setting for in-sample empirical tests, we obtain the out-of-sample results of non-iid jump cases in Table 9. The half years of out-of-sample non-iid cases empirical comparisons against the BS model are presented in Table 9.

The non-iid model uses those parameters estimated from in-sample data, and for each Corollary case the parameters are chosen from the Table 5. The out-of-sample empirical test is to have the option market prices of S&P 500 index from March 1, 2013 to August 30, 2013. For each case of non-iid model, there are two ways to choose the volatility parameter what are the implied volatility and the estimated volatility. Corollary 3 with auto-correlated non-iid is tested with both and for accuracy.

AE means Average Error, ARE means Average Relative Error. The percentages in the parenthesis are improvements according to the BS model prices.

BS

Cor 1

Cor 2

Cor 3 (n=50)

(n=15)

= 0.009

= 0.009

= 0.009

= 0.009

SSE

104.6249

104.5680

101.0453

104.5680

101.0452

104.5680

101.0453

104.5680

101.0453

(0.050%)

(3.417%)

(0.050%)

(3.417%)

(0.050%)

(3.417%)

(0.050%)

(3.417%)

AE

17.2347

17.2294

16.8378

17.2294

16.8378

17.2294

16.8378

17.2294

16.8378

(0.003%)

(2.276%)

(0.003%)

(2.276%)

(0.003%)

(2.276%)

(0.003%)

(2.276%)

ARE

2.4976

2.4967

2.4303

2.4967

2.4303

2.4967

2.4303

2.4967

2.4303

(0.036%)

(2.695%)

(0.036%)

(2.695%)

(0.036%)

(2.695%)

(0.036%)

(2.695%)

For the first case, we get the SSE results as for implied volatility and for estimated volatility cases. For the second case, the SSE results are and for implied volatility and estimated volatility cases respectively. For the third case, the estimation SSE results are for implied volatility and for estimated volatility cases when . Including the checking of AE and ARE values for out-of-sample, all the values are very close to the BS model results with only slight improvement.

Optional case for choosing according to the in-sample test, the same outcomes are obtained for out-of-sample with the previous case as . Both comparisons of in-sample and out-of-sample of non-iid cases suggest the fact that the non-iid assumption for the BS model only improve the performance of misspecific calibration very slightly.

Consistently, sensitivities for parameters and and the influence of combined movements in both are tested. Choosing the first days of out-of-sample for simplicity then the results are listed in Table 10. The improvement percentages keep the same change trends as we list in previous in-sample test. The case in Table 10 is the same case in Table 6 for the first day of in-sample data on varying the jumping size mean, variance and both.

For the first day of out-of-sample data, we analysis 3 cases of the non-iid model: First is to set increase from , to then stay, and the parameter is always unchanged; Second is to set fixed as , decrease from , to , then stay in ; Third case is to let increase from , to then stays, and simultaneously decreases from , to , then stays in . The corresponding cases are exactly as same as those for the first day of in-sample data in Table 6. AE means Average Error, ARE means Average Relative Error. The percentages in the parenthesis are improvements according to BS model prices.

BS

Cor 1

Case 1

Case 2

Case 3

Cor 2

Case 1

Case 2

Case 3

SSE

0.5747

0.5572

0.5623

0.5521

0.5551

0.5572

0.5623

0.5523

0.5553

(3.05%)

(2.16%)

(3.93%)

(3.41%)

(3.05%)

(2.16%)

(3.90%)

(3.38%)

AE

16.2018

15.8389

15.9257

15.7393

15.7959

15.8389

15.9257

15.7425

15.7984

(2.24%)

(1.70%)

(2.85%)

(2.51%)

(2.24%)

(1.70%)

(2.83%)

(2.49%)

ARE

4.5028

4.3612

4.4041

4.345

4.3655

4.3612

4.4041

4.3461

4.3663

(3.14%)

(2.19%)

(3.50%)

(3.05%)

(3.14%)

(2.19%)

(3.48%)

(3.03%)

In summary, the non-iid model have no dramatic improvement of the BS model since the non-iid formulas are derived from the classic BS model with compound Poisson without uniform distributions. The underlying dynamic of of the asset is essentially same with only altering the i.i.d in the jumping size. That is why we should not expect too much improvement from the previous SVJ model.

3. Empirical Test for S&P 500 Call Option With Lévy Processes

From the in-sample estimations of parameters of three typical Lévy models, we empirically test the European call option price of S&P 500 index for the out-of-sample period. Table 11 includes the parameter estimation and the corresponding SSE values for the option prices.

The out-of-sample data comes from March 1st 2013 to August 30th 2013. These three Lévy processes have the equivalent order of magnitudes with Heston model for the final SSE. The greatest out-of-sample SSE estimation is 8.15 for CGMY model and the lowest is 5.81 for NIG model, the average is 7.13. According to Heston model, the greatest is 6.61 and lowest is 5.27 for out-of-sample with average 5.94. By comparison, and the NIG model has the lowest answer in the 3 kinds of Lévy processes and very close to Heston model as well.

GH

NIG

CGMY

Heston SV model

SVJ model

model

model

model

estimate

estimate

-17.3388

19.999

15.6454

-15.421

0.3554

0.2295

-17.6347

-0.1667

C

4.47E-06

G

4.5725

M

6.8383

Y

1.9975

SSE

7.43

5.81

8.15

6.61

5.32

6.55

5.27

Table 11 illustrates that the biggest out-of-sample SSE estimation is 8.15 of CGMY model and the smallest is 5.81 of NIG model, the average is 7.13. For the Heston models, the biggest is 6.61 and the smallest is 5.27 for out-of-sample with average of 5.94. All those parameters for the GH, NIG, CGMY models are derived from minimizing the SSE functions with proper ranges of each parameter. The SV and SVJ models with estimating volatility give the smallest SSE values 5.32 and 5.27 respectively, where the NIG model follows next with 5.81 SSE value.

By comparing these Lévy models with SV and SVJ models, Lévy processes have the equivalent order of magnitude of SSE values with Heston model for out-of-sample test, and the NIG model performances the lowest answers among the three typical Lévy processes and very close to the Heston model. This fact verifies the viewpoint of Geman et al. (2001) about the infinite arriving jump may represent the diffusion part as Heston model deals with. Furthermore, we have some stable features in the prediction of Lévy processes in the following subsection.

4.3 Two Scenario Calibrations for One Day Prediction of Lévy Processes

To detect the prediction of Lévy processes, another test about daily SSE computation is undertaken. We use 273 option prices of September 4th 2012 as in-sample data and 187 prices of the first day of second half year, March 1st 2013, as out-of-sample data. With the first day parameters, the out-of-sample results are listed in Table LABEL:3Levy1dayout as well. The SSE values are computed under two scenarios: using the first day parameters and using the first half year parameters.

Table LABEL:3Levy1dayout shows the parameter results of three Lévy processes for in-sample case.

For each model, table LABEL:3Levy1dayout consists of the first column that is the parameters for September 4th 2012 optimization, and the second column that lists the parameters of half year in-sample calibration. For the first column of the GH model, the SSE value in September 4th 2012 is 0.0415, and the SSE value for March 1st 2013 is 0.0845. The results of out-of-sample by using one day calibration parameters are more than double of in-sample SSE values. On the other side, the SSE value for the GH model on the second column is 0.02774, which means by using the first half year’s optimal parameters, the value becomes almost one quarter of the SSE value for March 1st 2013. The CGMY model does the same on the SSE. The effect of the NIG model is as dramatic as around fifteen-fold less since the SSE value changes from 0.2019 to 0.0139. Overall the NIG model based on the first half year’s optimal parameters performs the smallest SSE, and the CGMY based on September 4th 2012 optimization performs the biggest SSE for the one day of out-of-sample test.

The change of SSE values indicates that the prediction error should be narrowed by using previous long period calibration parameters, not short period calibration as the one day optimal parameters. One more unexpected thing is that there are some negative values for the GH model estimation. By checking the model prices of the GH model, 42 negative values happened in the 272 prices of first day data, and the reason for the negative values comes from the iterating procedure. We further investigate all of these negative model prices are corresponding to very small market prices of S&P 500 index option. When we filter and keep all the positive 230 prices for the first day data, we notice the SSE value drops to 0.0352 from 0.0415 in Table LABEL:3Levy1dayout. Comparing results after filtering, both the total prices and SSE values drop 15% coincidentally. For the CGMY model and NIG model, we find no negative values for the model price estimation. In all, the unexpected happening about negative estimation does not affect the analyze for the total consideration. For out-of-sample data, we have 181 positive model prices in GH model from 187 items and the SSE value changes from 0.0845 in table LABEL:3Levy1dayout to 0.0836. The change percents of total prices and SSE are 3% and 1% respectively, changes are not different dramatically.

Intuitively, we may compare daily prediction results with previous Heston model. For the daily calibration, the parameter of Heston model are estimated by Matlab optimal function and listed in Table LABEL:Heston1daypara. With Heston models parameters, Table LABEL:3Levy1dayout and LABEL:Heston1daypara show the results and comparison of Lévy processes with previous Heston model.

Checking the four cases of the Heston model, the SSE values show oscillating behavior without clear pattern. For the SV model in the first case when we use implied volatility, the estimation of out-of-sample by using first day parameters has 0.0271 SSE value, and the SSE value becomes a slightly bigger 0.0278 for using first half year parameters. For the second case when we use estimated volatility, the SSE value varies from 0.0857 to 0.0202 with a drop. Extraordinarily, the SSE value in the third case of SVJ model is 7.4027 for using first day estimation parameters, which looks protrudingly large. However, three Lévy processes have the same shrinking trend when we use the long period data calibration parameters. For example, the NIG model has the change from 0.02019 to 0.0139 and lower than any Heston model we used. This indicates that Lévy processes have the more stable prediction with less errors as we expected.

In summary, the SSE values of Lévy processes have the same order of magnitude with Heston model we did before and even slightly greater. However, the one day prediction for out-of-sample data has a shrinking effect for the Lévy processes and more stable than Heston model. In articular, the NIG model has the lowest SSE value prediction within all the models.

5 Conclusion

Brownian motion is omnipresent in the financial economics, especially as a fundamental tool to simulate the dynamics of asset price movement over time. In the field of quantitative finance, the Black-Scholes-Merton model studies the option pricing formula that the underlying asset price follows geometric Brownian motion.

We follow the method of Bakshi et al. (1997) to first estimate parameters by the sum of squared error (SSE) for in-sample period of S&P 500 index. Other than the compound Poisson jumps, we also test the SSE results of non-iid cases numerically. The Heston model provides an excellent improvement of the BSM model which has fixed volatility. The advanced Heston models (SV, SVJ), which consider the volatility is a stochastic process, have the SSE value less than 10. By comparison, we find that the BSM model has the least performance consistently, and SV and SVJ models with estimated volatility have better results than SV and SVJ models with implied volatility by comparing those models with different periods of Bakshi et al. (1997).

Generally, the price activity has jumps which can be observed in the real financial market. Lévy processes are outstanding in terms of financial mathematics since their infinitely divisible, independent and stationary increments properties match financial market intuitively. For the model of exponential of Lévy process, the PIDE can be derived for the option pricing formula, but it is very hard to solve in a closed-form theoretically. Nevertheless, Fourier transform method can be used to solve the PIDE numerically due to the analogy of Lévy process’ characteristic function by Lévy-Khinchin theorem. In this paper, three typical cases of Lévy processes, GH model, NIG model and CGMY model, are calibrated by using fast Fourier transform (FFT) method numerically. Not only the parameter sensitivities of these Lévy processes are analyzed, but also all the SSE results of half year data are evaluated (below 10 as Heston model does). As a result, the NIG model has the better result than the GH and CGMY models for both in-sample and out-of-sample periods consistently. Meanwhile, for in-sample data, both NIG, SV and SVJ with estimated volatility models outperform the rest in terms of the least SSE value. For out-of-sample period, the SV and SVJ models with estimated volatility outperform the rest models and the NIG model follows next. Additionally, for one day prediction on March 1st 2013, we find that the NIG model is the best among all the models with the in-sample optimized parameters. Furthermore, the Lévy processes have the shrink effect and more stable prediction for chosen data. Beyond those analysis, the hedging problem with respect to the jumps is left for further study to investigate.

References

- Amin and Ng (1993) Amin, K. I., Ng, V. K., 1993. Option valuation with systematic stochastic volatility. The Journal of Finance 48, 881–910.

- Bakshi et al. (1997) Bakshi, G., Cao, C., Chen, Z., 1997. Empirical performance of alternative option pricing models. The Journal of Finance 52, 2003–2049.

- Bakshi and Chen (1997) Bakshi, G. S., Chen, Z., 1997. An alternative valuation model for contingent claims. Journal of Financial Economics 44, 123–165.

- Barndorff-Nielsen (1977) Barndorff-Nielsen, O., 1977. Exponentially decreasing distributions for the logarithm of particle size. Proceedings of the Royal Society of London. A. Mathematical and Physical Sciences 353, 401–419.

- Barndorff-Nielsen and Blaesild (1981) Barndorff-Nielsen, O., Blaesild, P., 1981. Hyperbolic distributions and ramifications: Contributions to theory and application. In: Statistical distributions in scientific work, Springer, pp. 19–44.

- Barndorff-Nielsen (1997) Barndorff-Nielsen, O. E., 1997. Processes of normal inverse gaussian type. Finance and Stochastics 2, 41–68.

- Bates (1991) Bates, D. S., 1991. The crash of ’87: Was it expected? the evidence from options markets. The Journal of Finance 46, 1009–1044.

- Bates (1996) Bates, D. S., 1996. Jumps and stochastic volatility: Exchange rate processes implicit in deutsche mark options. The Review of Financial Studies 9, 69–107.

- Black and Scholes (1973) Black, F., Scholes, M., 1973. The pricing of options and corporate liabilities. Journal of Political Economy 81, 637–654.

- Blaesild and Sørensen (1992) Blaesild, P., Sørensen, M., 1992. ” Hyp”: A Computer Program for Analyzing Data by Means of the Hyperbolic Distribution. University of Aarhus, Department of Theoretical Statistics.

- Broadie et al. (2009) Broadie, M., Chernov, M., Johannes, M., 2009. Understanding index option returns. The Review of Financial Studies 22, 4493–4529.

- Câmara and Li (2008) Câmara, A., Li, W., 2008. Jump-diffusion option pricing without iid jumps. Available at SSRN: https://ssrn.com/abstract=1282882 or http://dx.doi.org/10.2139/ssrn.1282882 .

- Carr et al. (2002) Carr, P., Geman, H., Madan, D. B., Yor, M., 2002. The fine structure of asset returns: An empirical investigation. The Journal of Business 75, 305–332.

- Carr and Wu (2004) Carr, P., Wu, L., 2004. Time-changed lévy processes and option pricing. Journal of Financial Economics 71, 113–141.

- Christoffersen et al. (2009) Christoffersen, P., Heston, S., Jacobs, K., 2009. The shape and term structure of the index option smirk: Why multifactor stochastic volatility models work so well. Management Science 55, 1914–1932.

- Constantinides et al. (2008) Constantinides, G. M., Jackwerth, J. C., Perrakis, S., 2008. Mispricing of s&p 500 index options. The Review of Financial Studies 22, 1247–1277.

- Cont and Tankov (2003) Cont, R., Tankov, P., 2003. Financial modelling with jump processes, vol. 2. CRC press.

- Cont and Voltchkova (2005) Cont, R., Voltchkova, E., 2005. Integro-differential equations for option prices in exponential lévy models. Finance and Stochastics 9, 299–325.

- Cooley and Tukey (1965) Cooley, J. W., Tukey, J. W., 1965. An algorithm for the machine calculation of complex fourier series. Mathematics of Computation 19, 297–301.

- Cox et al. (1985) Cox, J. C., Ingersoll Jr, J. E., Ross, S. A., 1985. A theory of the term structure of interest rates. Econometrica 53, 385–408.

- Duffie et al. (2000) Duffie, D., Pan, J., Singleton, K., 2000. Transform analysis and asset pricing for affine jump-diffusions. Econometrica 68, 1343–1376.

- Florescu et al. (2014) Florescu, I., Mariani, M. C., Sewell, G., 2014. Numerical solutions to an integro-differential parabolic problem arising in the pricing of financial options in a levy market. Quantitative Finance 14, 1445–1452.

- Geman et al. (2001) Geman, H., Madan, D. B., Yor, M., 2001. Time changes for lévy processes. Mathematical Finance 11, 79–96.

- Gong and Zhuang (2016) Gong, X., Zhuang, X., 2016. Option pricing for stochastic volatility model with infinite activity lévy jumps. Physica A: Statistical Mechanics and its Applications 455, 1–10.

- Hansen (1982) Hansen, L. P., 1982. Large sample properties of generalized method of moments estimators. Econometrica: Journal of the Econometric Society pp. 1029–1054.

- He and Zhu (2018) He, X.-J., Zhu, S.-P., 2018. A closed-form pricing formula for european options under the heston model with stochastic interest rate. Journal of Computational and Applied Mathematics 335, 323–333.

- Heston (1993) Heston, S. L., 1993. A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies 6, 327–343.

- Hirsa (2016) Hirsa, A., 2016. Computational methods in finance. CRC Press.

- Hull and White (1987) Hull, J., White, A., 1987. The pricing of options on assets with stochastic volatilities. The Journal of Finance 42, 281–300.

- Kienitz and Wetterau (2012) Kienitz, J., Wetterau, D., 2012. Financial modelling: Theory, implementation and practice with MATLAB source. John Wiley & Sons.

- Kwok et al. (2012) Kwok, Y. K., Leung, K. S., Wong, H. Y., 2012. Efficient options pricing using the fast fourier transform. In: Handbook of computational finance, Springer, pp. 579–604.

- Lee and Hannig (2010) Lee, S. S., Hannig, J., 2010. Detecting jumps from lévy jump diffusion processes. Journal of Financial Economics 96, 271–290.

- Lewis (2000) Lewis, A., 2000. Option valuation under stochastic volatility with mathematica code.

- Li et al. (2006) Li, H., Wells, M. T., Yu, C. L., 2006. A bayesian analysis of return dynamics with lévy jumps. The Review of Financial Studies 21, 2345–2378.

- Li and Li (2015) Li, O. X., Li, W., 2015. Hedging jump risk, expected returns and risk premia in jump-diffusion economies. Quantitative Finance 15, 873–888.

- Lord et al. (2008) Lord, R., Fang, F., Bervoets, F., Oosterlee, C. W., 2008. A fast and accurate fft-based method for pricing early-exercise options under lévy processes. SIAM Journal on Scientific Computing 30, 1678–1705.

- Loretan and Phillips (1994) Loretan, M., Phillips, P. C., 1994. Testing the covariance stationarity of heavy-tailed time series: An overview of the theory with applications to several financial datasets. Journal of Empirical Finance 1, 211–248.

- Lux (2000) Lux, T., 2000. On moment condition failure in german stock returns: an application of recent advances in extreme value statistics. Empirical Economics 25, 641–652.

- Merton (1976) Merton, R. C., 1976. Option pricing when underlying stock returns are discontinuous. Journal of Financial Economics 3, 125–144.

- Merton et al. (1973) Merton, R. C., et al., 1973. Theory of rational option pricing. Theory of Valuation pp. 229–288.

- Ornthanalai (2014) Ornthanalai, C., 2014. Levy jump risk: Evidence from options and returns. Journal of Financial Economics 112, 69–90.

- Rouah (2013) Rouah, F. D., 2013. The Heston Model and Its Extensions in Matlab and C. John Wiley & Sons.

- Schoutens (2003) Schoutens, W., 2003. Lévy processes in finance: pricing financial derivatives. John Wiley & Sons.

- Scott (1987) Scott, L. O., 1987. Option pricing when the variance changes randomly: Theory, estimation, and an application. Journal of Financial and Quantitative Analysis 22, 419–438.

- Scott (1997) Scott, L. O., 1997. Pricing stock options in a jump-diffusion model with stochastic volatility and interest rates: Applications of fourier inversion methods. Mathematical Finance 7, 413–426.

- Shreve (2004) Shreve, S. E., 2004. Stochastic calculus for finance II: Continuous-time models, vol. 11. Springer Science & Business Media.

- Strang (1994) Strang, G., 1994. Wavelets. American Scientist 82, 250–255.

- Wong and Guan (2011) Wong, H. Y., Guan, P., 2011. An fft-network for lévy option pricing. Journal of Banking & Finance 35, 988–999.

- Zaevski et al. (2014) Zaevski, T. S., Kim, Y. S., Fabozzi, F. J., 2014. Option pricing under stochastic volatility and tempered stable lévy jumps. International Review of Financial Analysis 31, 101–108.