Polymatrix Competitive Gradient Descent

Abstract

Many economic games and machine learning approaches can be cast as competitive optimization problems where multiple agents are minimizing their respective objective function, which depends on all agents’ actions. While gradient descent is a reliable basic workhorse for single-agent optimization, it often leads to oscillation in competitive optimization. In this work we propose polymatrix competitive gradient descent (PCGD) as a method for solving general sum competitive optimization involving arbitrary numbers of agents. The updates of our method are obtained as the Nash equilibria of a local polymatrix approximation with a quadratic regularization, and can be computed efficiently by solving a linear system of equations. We prove local convergence of PCGD to stable fixed points for -player general-sum games, and show that it does not require adapting the step size to the strength of the player-interactions. We use PCGD to optimize policies in multi-agent reinforcement learning and demonstrate its advantages in Snake, Markov soccer and an electricity market game. Agents trained by PCGD outperform agents trained with simultaneous gradient descent, symplectic gradient adjustment, and extragradient in Snake and Markov soccer games and on the electricity market game, PCGD trains faster than both simultaneous gradient descent and the extragradient method.

1 Introduction

Multi-agent optimization

is used to model cooperative and competitive behaviors of a group of interacting agents, each minimizing their respective objective function. These problems arise naturally in various applications, including robotics [1], distributed control [2] and socio-economic systems [3, 4]. More recently, multi-agent optimization has served as a powerful paradigm for the design of novel algorithms including generative modeling [5], adversarial robustness [6] and uncertainty quantification [7], as well as multi-agent reinforcement learning (MARL).

Simultaneous gradient descent and the cycling problem.

The most common approach for solving multi-agent optimization problems is simultaneous gradient descent (SimGD). In SimGD, all players independently change their strategy in the direction of steepest descent of their own cost function. However, this procedure often fails to converge, including in bilinear two-player games, where SimGD exhibits oscillatory and diverging behavior. This problem is addressed by numerous modifications of SimGD that are introduced through the lens of agent-behavior [8, 9, 10, 11, 12], variational inequalities [13], or the Helmholtz-decomposition [14, 15]. However, most of these methods require step sizes that are chosen inversely proportional to the strength of agent-interaction, limiting their convergence speed and stability.

Competitive gradient descent (CGD).

The updates of SimGD are Nash equilibria of a local game given by a regularized linear approximation of the agents’ losses. The authors of [16] argue that the shortcomings of SimGD arise from the inability of the linear approximation to account for agent interactions. For two-player optimization, they propose to use a bilinear approximation that allows the agents to take each other’s objectives into account when choosing an update. They show that the Nash equilibrium of the resulting regularized bilinear game has a closed form solution which provides the update rule of a new algorithm, named competitive gradient descent(CGD). Both theoretically and empirically, CGD shows improved stability properties and convergence speed, decoupling the admissible step size from the strength of player interactions. However, the algorithm presented therein is only applicable to the two-player setting.

CGD for more than two players.

Since the two-agent CGD update is given by the Nash equilibrium of a regularized bilinear approximation of both agents’ cost functions, a natural extension to -agent optimization would require an -th order multilinear approximation to capture all degrees of player interaction. However, this approach requires the solution of a system of -th order multilinear equations at each step. For , the resulting linear system of equations can be solved efficiently using the well developed tools from numerical linear algebra. In sharp contrast, the solution of -th order multilinear systems of equations is NP-hard in general Hillar and Lim [17]. Furthermore, existing heuristics such as alternating least squares (ALS) to solve multilinear systems do not offer nearly the same reliability, ease-of-use, and efficiency of optimal Krylov subspace methods available for systems of linear equations. In order to avoid this difficulty, we propose to use a local approximation given by a multilinear polymatrix game, where only interactions between pairs of agents are accounted for explicitly. This local approximation can then be solved using linear algebraic methods.

Our contributions.

In this work, we introduce polymatrix competitive gradient descent (PCGD) as a natural extension of gradient descent to multi-agent competitive optimization. The updates of PCGD are given by the Nash equilibria of a regularized polymatrix approximation of the local game. This approximation allows us to preserve the advantages of two-agent CGD in the multiagent setting, while still computing updates using the powerful tools of numerical linear algebra.

-

•

On the theoretical side, we prove local convergence of PCGD in the vicinity of local Nash equilibria, for multi-agent general-sum games. These results generalize the convergence results of CGD [16] from two-player zero-sum to -player general-sum games. In particular, PCGD guarantees convergence without needing to adapt the step sizes to the strength of agent interactions. Existing approaches based on simultaneous gradient descent need to reduce the step size to match the increases in competitive interactions to avoid divergence, requiring more hyperparameter tuning.

-

•

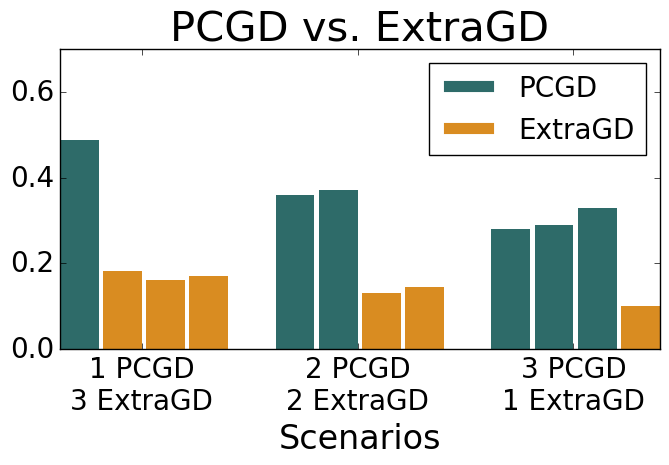

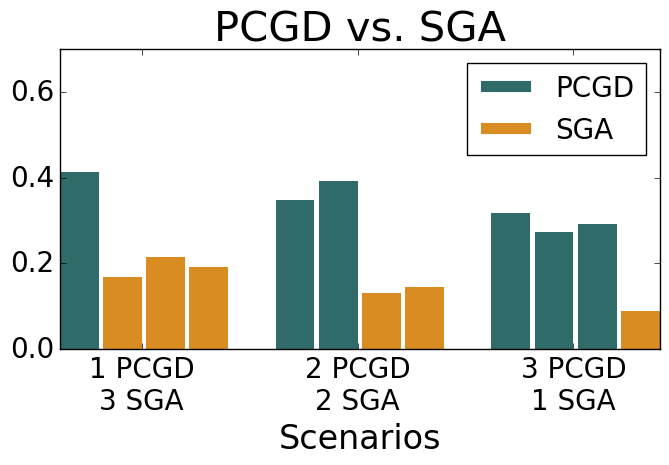

On the empirical side, we use PCGD for policy optimization in multi-agent reinforcement learning, and demonstrate its advantage in four-player snake and Markov soccer games. It is shown that, agents trained with PCGD, significantly outperform their SimGD, SGA, and Extragradient trained counterparts. In particular, PCGD trained agents win at more than twice the rate compared to SimGD, SGA, and Extragradient trained agents. This holds even in settings where the majority of agents are trained using non-PCGD methods, meaning the PCGD agent encounters a major distributional shift.

-

•

We also use PCGD for simulating strategic behavior in an economic market game that captures the essence of the real-world electricity market operating rules. We observe that PCGD improves the speed and stability of training, while reaching comparable reward. Thus, we can use PCGD as an effective tool to explore the behavior of self-interested agents in markets.

2 Polymatrix Competitive Gradient Descent

Setting and notation.

We consider general multi-agent competitive optimization of the form

| (1) |

for functions , where . We denote the combined parameter vector of all players as , the simultaneous gradient as , and the game Hessian as

| (2) |

We denote as the block-diagonal part of , and as its block-off-diagonal part.

The multilinear polymatrix approximation.

Where SimGD and CGD compute updates as Nash equilibria of linear or multilinear approximations, we propose to instead use a multilinear polymatrix approximation of the form

| (3) |

By adding a quadratic regularization that expresses the limited confidence of the players in the accuracy of the local approximation for large , we obtain the local polymatrix game

| (4) |

Here and from now on, we stop explicitly denoting the dependence on the last iterate in order to simplify the notation. We will now derive the unique Nash equilibrium of this game.

Proposition 1.

The game in equation 4 has a unique Nash equilibrium given by

| (5) |

provided is sufficiently small for the inverse matrix to exist.

Proof.

A necessary condition for to be the Nash equilibrium is that for each ,

Therefore,

is the unique possible solution for small. This is a Nash equilibrium since

everywhere, a sufficient condition for fixed points to be Nash equilibria. ∎

Polymatrix competitive gradient descent (PCGD)

is obtained by using the Nash equilibrium of equation 5 as an update rule according to .

Input: objectives , parameters

Output:

By incorporating the interaction between the different players at each step, PCGD avoids the cycling problem encountered by simultaneous gradient descent. In particular, we will show in Section 3 that the local convergence of PCGD is robust to arbitrarily strong competitive interactions between the players, as described by the antisymmetric part of .

Why not use multi-linear approximation?

The authors of [16] propose to extend CGD to more than two players by using a full multilinear approximation of the objective function. For example, in a three-player game with objectives , the update would be the solution to the following game:

| (6) |

As shown in the trilinear approximation in equation 6, we start to consider interactions between groups of three or more agents captured by higher dimensional interaction tensors such as for each update. The optimality conditions obtained by differentiating the -th loss of the local game with respect to are given by a general system of multilinear equations and even deciding if a solution exists is NP-hard in general [17]. Existing approaches such as alternating least squares do not offer nearly the same reliability, ease-of-use, and efficiency as the well-developed tools for systems of linear equations. In contrast, the multilinear polymatrix approximation of equation 3 specializes to

| (7) |

in the special case of three players. The first term () is an update strictly in the direction of decreasing cost, or the self-minimization term. The second group of terms such as correspond to choosing an update with respect to what other agents’ choices might be, which we refer to as the interaction term. The third terms such as estimate the impact of other agents’ update on one’s objective. The fourth term, e.g. is the step size regularization. Contrary to the full multilinear approximation, the multilinear polymatrix approximation can be solved by using highly efficient algorithms for numerical linear algebra, such as Krylov subspace methods.

Practical implementation.

The update of Algorithm 1 is given in terms of the mixed Hessian, which scales quadratically in size with respect to the number of agent parameters. However, matrix-vector products can be computed as efficiently as the value of the loss function by combining forward and reverse mode automatic differentiation to compute Hessian vector products. Without access to mixed mode automatic differentiation, we employ the “double backprop trick” that computes matrix-vector products as . The quantity on the right can be evaluated by applying reverse-mode automatic differentiation twice. Using either of these methods, the computational cost of evaluating matrix-vector products in the mixed Hessian is, up to a small constant factor, no more expensive than the evaluation of the loss function.

We combine the fast matrix-vector multiplication with a Krylov subspace method for the solution of linear systems to compute the update of Algorithm 1. In our experiments, we use the conjugate gradient algorithm [18] to solve the system by solving the positive semi-definite system , where is the block-matrix we wish to invert. We terminate conjugate gradient after a relative decrease of the residual is achieved ( for some threshold ). To decrease the number of iterations needed, we use the solution of the previous updates as an initial guess for the next iteration of conjugate gradient. The number of iterations needed by the inner loop is highly problem-dependent. However, we observe that the updates of PCGD are often not much more expensive than SimGD in practice. In applications to reinforcement learning, the sampling cost often masks the computational overhead of PCGD.

3 Theoretical Results

We now provide theoretical results on the convergence of PCGD.

Definition 2 (Local Nash equilibrium).

We call a tuple of strategies a local Nash equilibrium if for each there exists an such that

| (8) |

We use the notation introduced in Section 2 and write the symmetric and nonsymmetric parts of the Hessian matrix as and . The matrices and can be seen as capturing the pair-wise collaborative and competitive parts of the game, respectively. To see this, we fix all agents but those with indices and obtain the game

| (9) |

Writing now and , we can write this game as the sum of a strictly collaborative potential game and a strictly competitive zero-sum game

| (10) | |||

| (11) |

The Hessian of the potential game in this decomposition is given by the restriction of to the strategy spaces of the -th and -th. The off-diagonal blocks of the Hessian, on the other hand, are given by the corresponding blocks of . We now state our main theorem.

Theorem 3.

Assume that each of the is twice continuously differentiable and let be a local Nash equilibrium for which the game Hessian is invertible. Then, for all , there exists an open neighborhood of such that PCGD converges at an exponential rate to .

The authors of [16] show that in the case of two-player, zero-sum games, the convergence of CGD is robust to strong agent-interaction as described by large off-diagonal blocks of the game Hessian, without lowering the step size. In stark contrast, methods such as extragradient [13], consensus optimization [12], or symplectic gradient adjustment [14] have to decrease the step size to counter strong agent interactions. The results presented here extend the results of [16] to general-sum games with arbitrary numbers of players and establish convergence of PCGD that is fully robust to the strength of the competitive interactions given by , without additional step size adaptation.

Having the ability to choose larger step sizes allows our algorithm to achieve faster convergence. The example below illustrates that in some games, e.g., multilinear games with pairwise zero-sum property, the step size can be arbitrarily large while PCGD still guarantees convergence.

Example 1.

Consider a four-player multilinear game with pairwise zero-sum interactions: . The simultaneous gradient is,

and game Hessian is

The origin is a stable fixed point since and is invertible. We have , so PCGD converges locally (in fact globally) to the origin for all !

We note that the step size of PCGD still needs to be adapted to the magnitude of . In the single-agent case, is the curvature of the objective which limits the size of step size for gradient descent. Thus it is expected that limits the step size of multi-agent generalizations of gradient descent.

We also remark that while we proved local convergence of PCGD to local Nash equilibria, an attractive point of the PCGD dynamics need not be a local Nash equilibrium if we consider general non-convex loss functions. A similar phenomenon was observed by Mazumdar et al. [19] in the context of simultaneous gradient descent and by Daskalakis and Panageas [20] in the context of optimistic gradient descent. These observations motivated some authors, such as Mazumdar et al. [21], to search for algorithms that only converge to local Nash equilibria. Others, such as Schäfer et al. [22] instead question the importance of local Nash equilibria as a solution concept in non-convex multi-agent games. A complete characterization of the landscape of attractors of PCGD is an interesting direction for future work.

4 Instantiation to Multi-Agent Reinforcement Learning

A fundamental challenge in multi-agent reinforcement learning is to design efficient optimization methods with provable convergence and stability guarantees. In this section, we instantiate how the proposed PCCD can be used for policy optimization in multiagent reinforcement learning. In particular, when deriving the policy updates, PCGD captures not only the agent’s own reward function, but also the effects of all other agents’ policy updates.

Multiagent Reinforcement Learning (MARL).

An -player Markov decision process is defined as the tuple where is the state space, is the action space of player . denote reward where is a bounded reward function for player ; is the discount factor and maps the state-action pairs to a probability distribution over next states. We use to denote the simplex. The goal of reinforcement learning is to learn a policy which maps a state and action to a probability of executing the action from the given state in order to maximize the expected return. In the n-player setting, the expected reward of each player is defined as,

| (12) |

which is a function associated with all players’ policy parameters . denotes the probability distribution of the trajectory and is the accumulated trajectory reward.

Each agent aims to maximize its expected reward in equation 12, i.e.,

| (13) |

PCGD for MARL training.

Equation 13 is an instantiation of the multi-agent competitive optimization setting defined in Section 2. Thus, we can use PCGD for the policy update,

| (14) |

where is the simultaneous gradient , and if the off-diagonal part of the game Hessian. In order to compute gradients and Hessian-vector-products, we rely on policy gradient theorems that allow us express the gradients and hessian-vector-products as expectations that can be approximated using sampled trajectories. The simplest approach to computing Hessian-vector products, which is applicable to any reward function , amounts to simply applying the policy gradient theorem twice, resulting in the expression, where

| (15a) | ||||

| (15b) | ||||

The downside of this approach, which can be seen as a competitive version of REINFORCE [23], is that it does not exploit the Markov structure of the problem, resulting in poor sample efficiency. To overcome this problem, Prajapat et al. [24] introduce a more involved competitive policy gradient theorem that expresses the mixed derivatives in terms of the Q-function.

| (16) |

| (17) |

This formulation allows us to use advanced, actor-critic-type approaches [25] to improve the sample efficiency. In our implementation, we use generalized advantage estimation (GAE) [26] in place of the function to calculate the gradient and Hessian terms. After sampling a batch of states, actions, and rewards from the replay buffer, we construct two pseudo-objectives, one for the first derivative terms and one for the mixed Hessian terms required for the PCGD update. Taking the gradient with respect to a single player of the one pseudo-objective gives us the desired single agent () terms for each player in the PCGD update, while taking the mixed derivative of the second pseudo-objective with respect to two different players using auto-differentiation gives us the desired polymatrix or interaction terms (.

5 Numerical Experiments

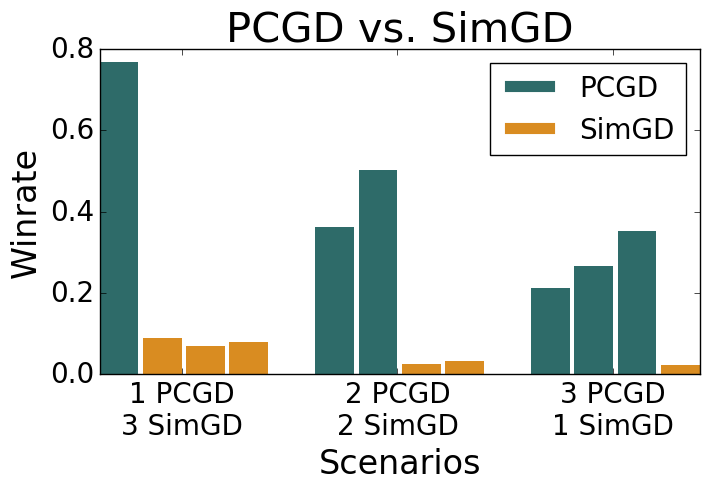

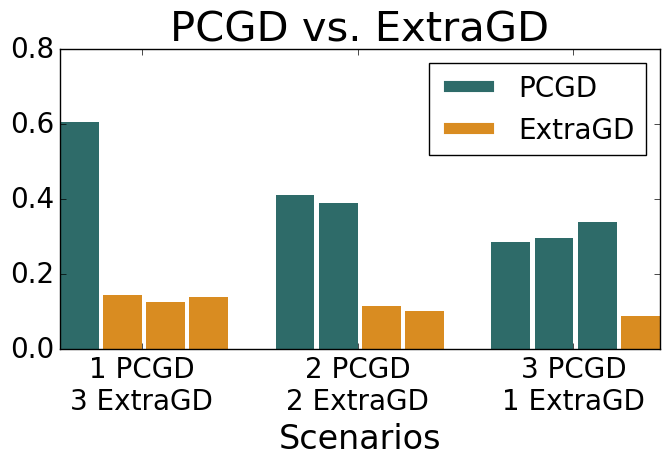

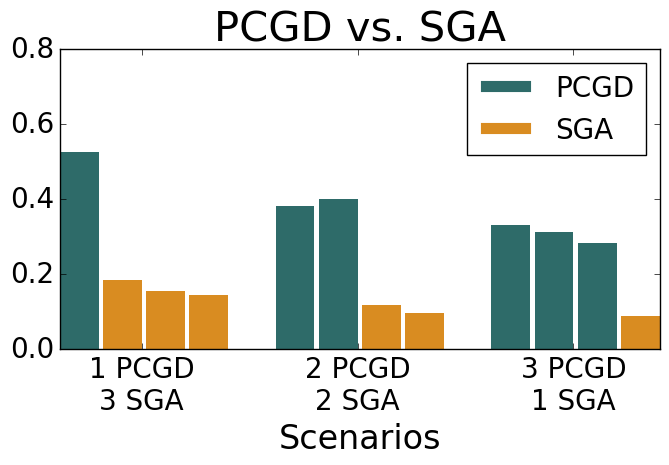

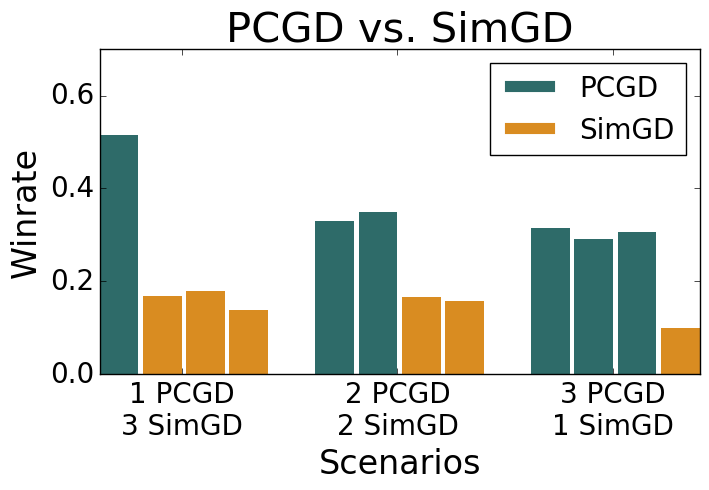

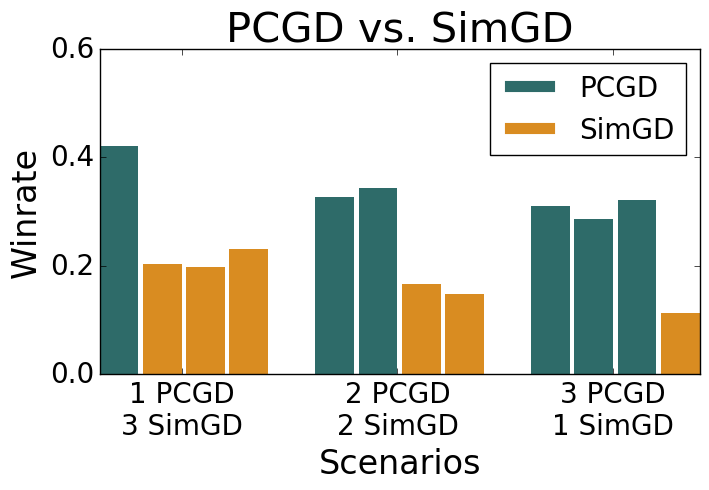

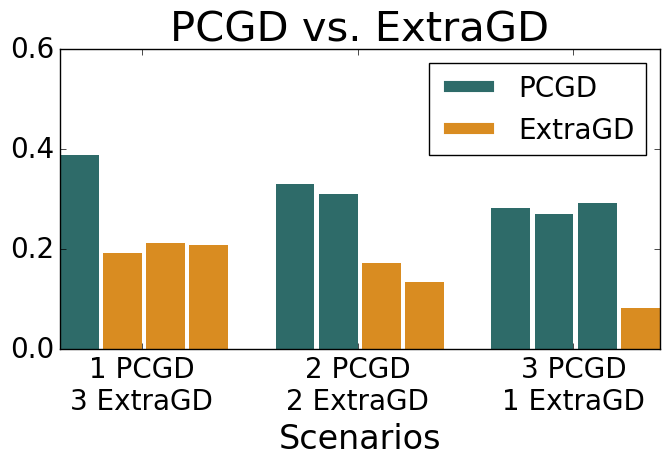

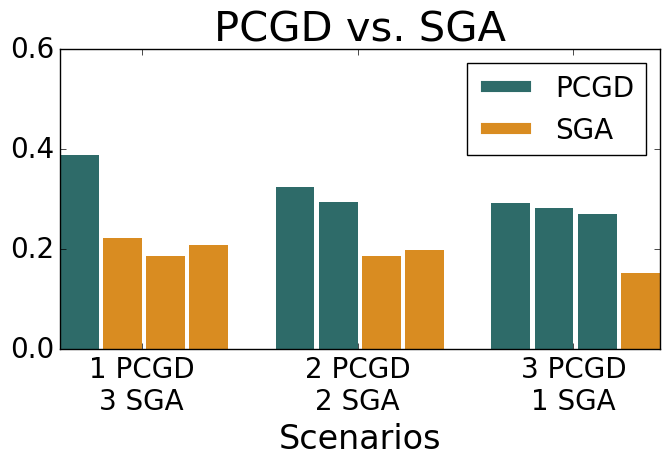

Snake and Markov Soccer.

We demonstrate our algorithm through numerical experiments on two games: Four-player Snake and four-player Markov Soccer. In the Snake game, four different snakes compete in a fixed space to box each other out, to consume a number of randomly-placed fruits, and to avoid colliding with each other or the walls. At each step of the game, each snake observes the 20-by-20 space around its head and decides whether to continue moving forward, to turn left, or to turn right. Agents are rewarded with from consuming a fruit and for a collision with either another snake’s body or a wall. Such a collision removes the snake from the game and the last snake alive receives another reward of . If a snake is removed from the game for colliding with another snake, that other snake receives a reward of for “capturing” the first snake. We build on the implementation of Snake as used by ML2 [27]. Four-player Markov Soccer is an extension of the two-player variant proposed by Littman [28] and consists of four players and a ball that are randomly initialized in a 8-by-8 field. Each agent is assigned to a goal and looks to pick up the ball or steal it from opposing players and score it in an opponent’s goal. The goal-scoring player is given , where all other players are penalized with ; in the case where a player own-goals, that player is penalized with -1, and all other players are given +0.

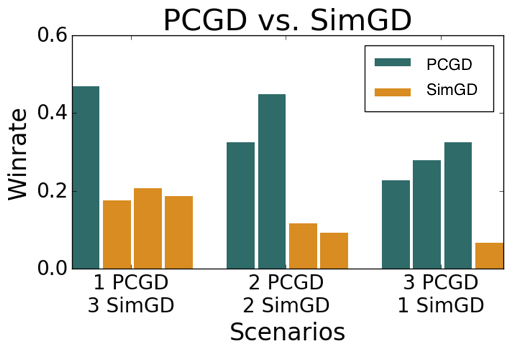

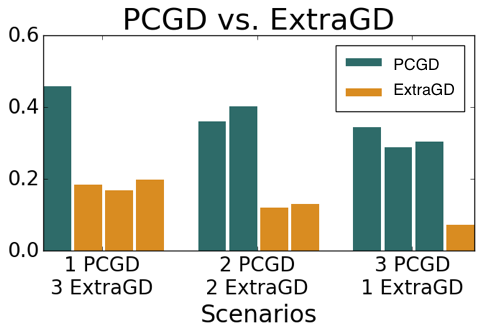

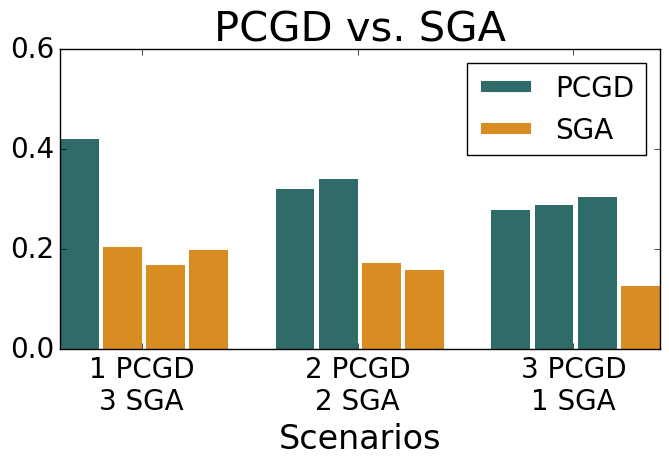

For both of these games, we take four policies and train them together with the same algorithm, once under PCGD and once under three other methods: SimGD, Extragradient, and Sympletic Gradient Ascent (SGA) ([29]). We then compare the policies generated by PCGD and one of the competing methods in three scenarios: playing 1 PCGD-trained agent against 3 competitor-trained agents; 2 PCGD-trained agents against 2 competitor-trained agents; and 3 PCGD-trained agents against 1 competitor-trained agent. As illustrated in Figures 1 and 2, we find that the PCGD trained agents show significantly higher winrate, even when facing major distributional shift in the case where a single PCGD agent plays against three agents trained using the same competing method.

Details about the implementation and choice of hyperparameters of the Snake game and Markov soccer are provided in the appendix.

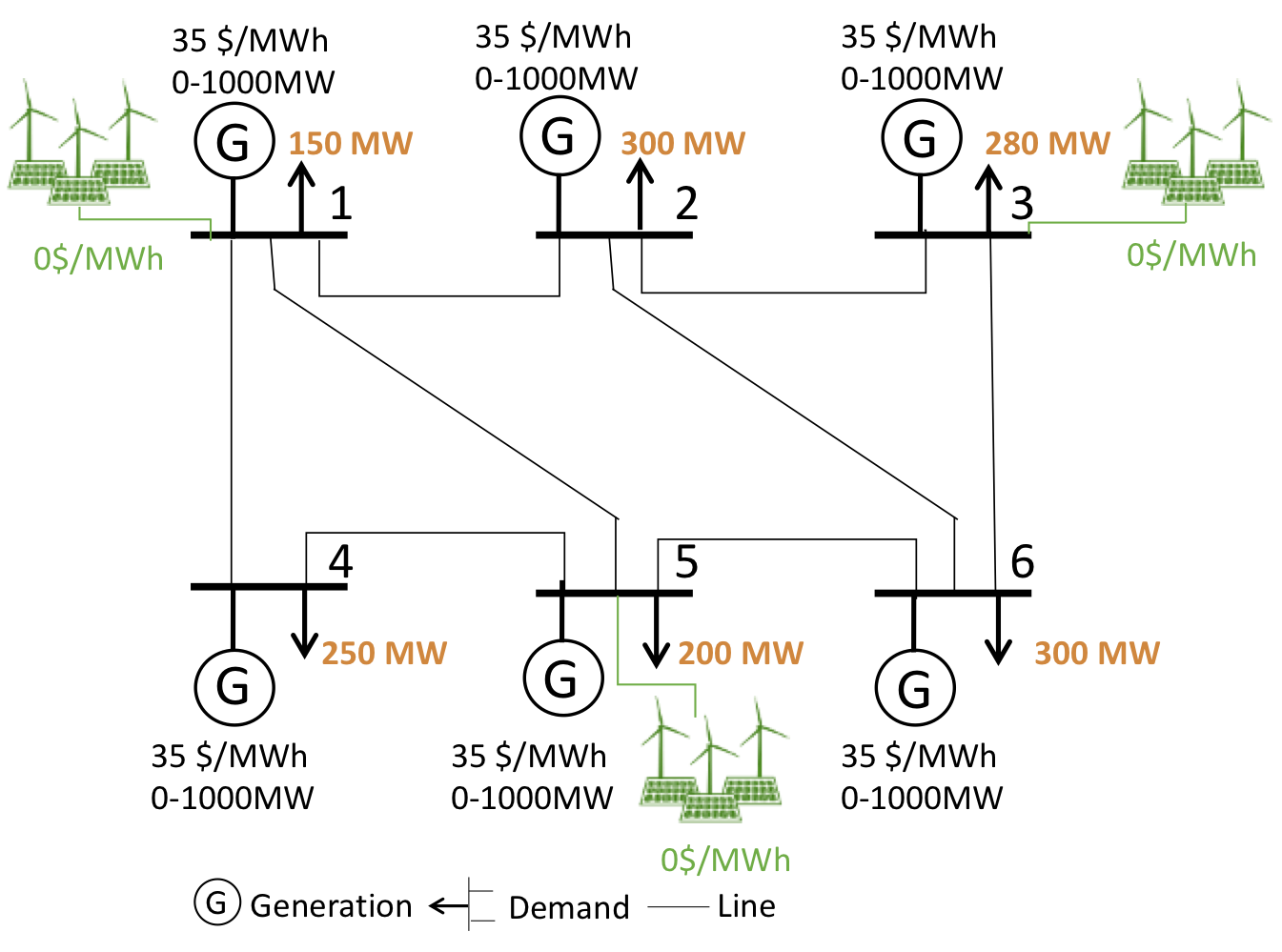

Electricity Market Simulation.

We also demonstrate the utility of PCGD for the simulation of strategic agent behavior in social-economic games. In particular, we consider an electricity market game where multiple generators compete for electricity supply and profit maximization following the setup in [3]. In the following, we explain how electricity market is modeled as a MARL game, by defining the state, action, and reward.

1) State and Actions. We follow the formulation in [3] where the system state is defined by that is the electricity demand at time across all nodes . For generator , its action includes two parts: the first part is the per unit production cost ($/MWh) and the second part is the supply capacity (MW). We assume that agents are strategic by physically or economically withholding supply from the market.

2) Reward: The goal of each generator is to maximize its profit, which can be written as,

where the first part represents market payment for generating unit of electricity and the second part reflects the production cost. In the above reward function, the scheduled supply quantity , and the unit electricity price at location (suppose generator locates in node ), are both decided by the system operator via solving the following optimization problem.

| (18a) | ||||

| s.t. | (18b) | |||

| (18c) | ||||

The objective function 18a aims to minimize the total system generation cost by deciding the power supply from each generator over horizon (e.g., 24 hours). The constraint in equation 18b collects the power grid equality constraints such as supply-demand balance and power flow equations; the constraint in equation 18c encodes physical limits, such as maximum generation capacity, i.e., and line flow limits. We refer the reader to [3] for more details.

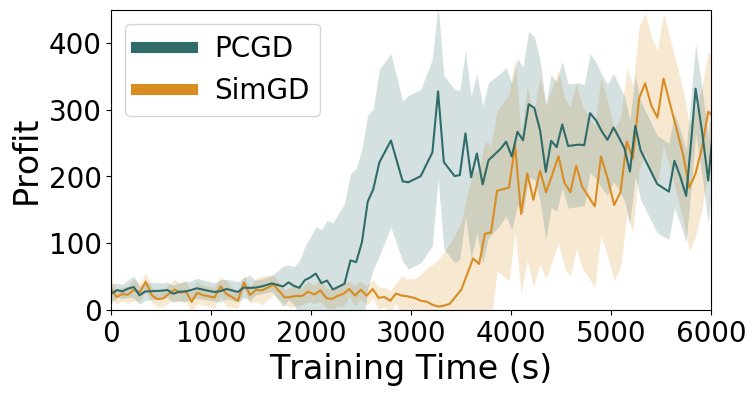

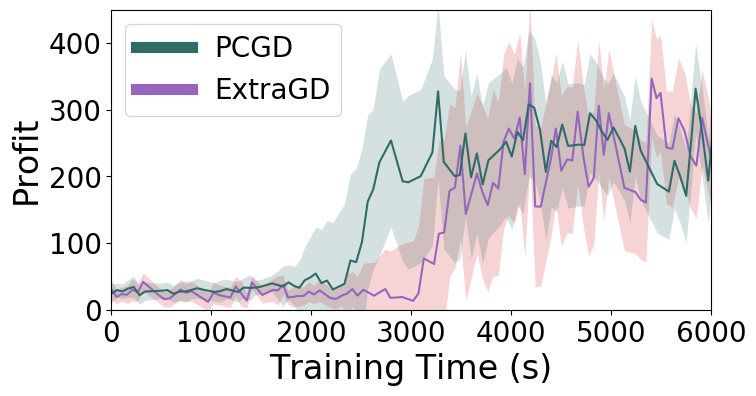

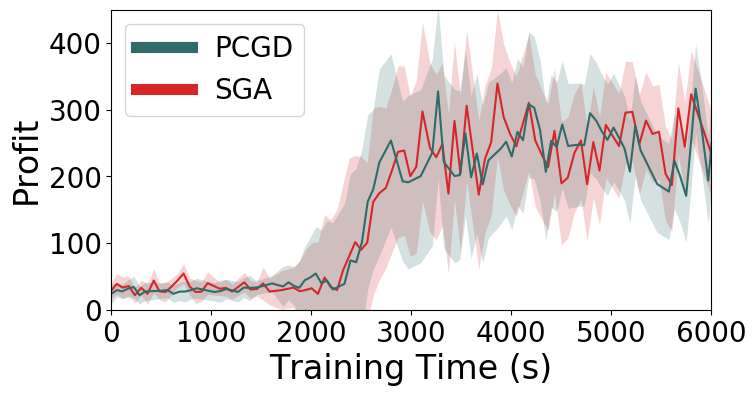

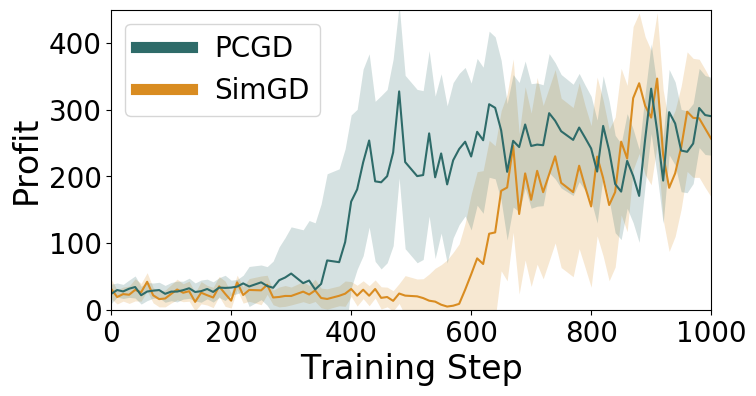

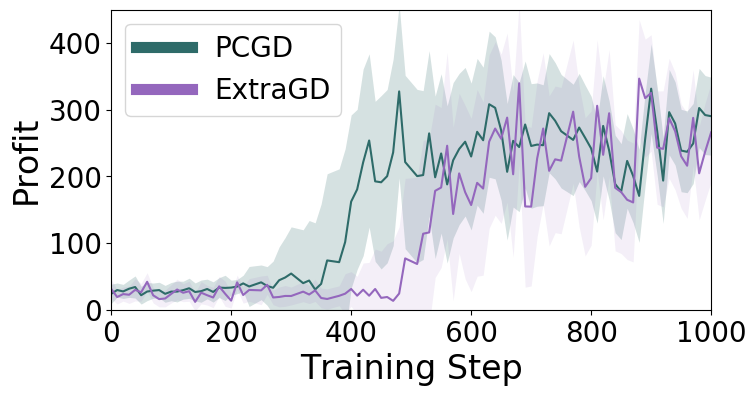

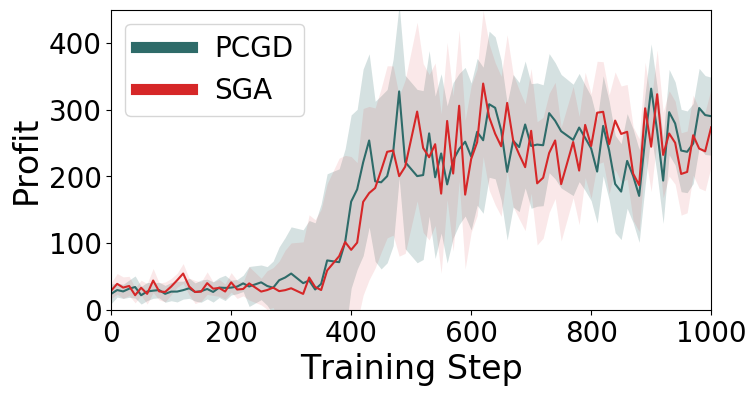

3) Learning algorithm: We use SimGD, SGA, ExtraGradient, and PCGD for simulating strategic behavior in the electricity market game. While all optimization methods achieve comparable reward in this game, we observe that PCGD converges significantly faster than both SimGD and Extragradient, and slightly faster than SGA. Despite the need of solving a linear system at each step of PCGD, this holds true when measuring cost in terms of either the number of iterations or total wall-clock time. This observation is explained by the fact that most of the iteration cost occurs when sampling from the policy, which has to be done only once per iteration.

6 Conclusion

In this work, we present a method for solving general sum competitive optimization of an arbitrary number of agents, named polymatrix competitive gradient descent (PCGD). We prove that PCGD converges locally in the vicinity of a local Nash equilibrium without having to reduce the step size to account for strong competitive player-interaction. We then apply our method towards a set of multi-agent reinforcement learning games, and show that PCGD produces significantly more performant policies on Markov Soccer and Snake, while achieving reduced training cost on an energy market game. PCGD provides an efficient and reliable computational tool for solving multi-agent optimization problems, which can be used for agent-based simulation of social-economical games, and also provides a powerful paradigm for new machine learning algorithm design that involves multi-agent and diverse objectives. A number of open questions remain for future work. While our present results show the practical usefulness of the polymatrix approximation, it might be inadequate for games with strong higher-order-interactions that are not captured by the polymatrix approximation and instead require the full multilinear approximation. Another open question is to better characterize the properties of solutions obtained by PCGD in collaborative games. PCGD agents beat agents trained by SimGD in our experiments, but in some applications we want agents to maximize a notion of social good. It is not clear what effect PCGD has on this objective.

Acknowledgements

AA is supported in part by the Bren endowed chair, Microsoft, Google, and Adobe faculty fellowships. FS gratefully acknowledge support by the Air Force Office of Scientific Research under award number FA9550-18-1-0271 (Games for Computation and Learning) and the Ronald and Maxine Linde Institute of Economic and Management Sciences at Caltech.

References

- Serrino et al. [2019] Jack Serrino, Max Kleiman-Weiner, David C Parkes, and Joshua B Tenenbaum. Finding friend and foe in multi-agent games. arXiv preprint arXiv:1906.02330, 2019.

- Marden and Shamma [2015] Jason R Marden and Jeff S Shamma. Game theory and distributed control. In Handbook of game theory with economic applications, volume 4, pages 861–899. Elsevier, 2015.

- Yu et al. [2007] Nanpeng Yu, Chen-Ching Liu, and Leigh Tesfatsion. Modeling of suppliers’ learning behaviors in an electricity market environment. In 2007 International Conference on Intelligent Systems Applications to Power Systems, pages 1–6. IEEE, 2007.

- Ruhi et al. [2017] Navid Azizan Ruhi, Krishnamurthy Dvijotham, Niangjun Chen, and Adam Wierman. Opportunities for price manipulation by aggregators in electricity markets. IEEE Transactions on Smart Grid, 9(6):5687–5698, 2017.

- Goodfellow et al. [2014] Ian J Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. Generative adversarial networks. arXiv preprint arXiv:1406.2661, 2014.

- Madry et al. [2017] Aleksander Madry, Aleksandar Makelov, Ludwig Schmidt, Dimitris Tsipras, and Adrian Vladu. Towards deep learning models resistant to adversarial attacks. arXiv preprint arXiv:1706.06083, 2017.

- Wang et al. [2020] Haoxuan Wang, Anqi Liu, Zhiding Yu, Yisong Yue, and Anima Anandkumar. Distributionally robust learning for unsupervised domain adaptation. arXiv preprint arXiv:2010.05784, 2020.

- Shalev-Shwartz and Singer [2007] Shai Shalev-Shwartz and Yoram Singer. Convex repeated games and fenchel duality. In Advances in Neural Information Processing Systems, page 1265–1272, 2007.

- Brown [1951] George W Brown. Iterative solution of games by fictitious play. Activity analysis of production and allocation, 13(1):374–376, 1951.

- Daskalakis et al. [2017] Constantinos Daskalakis, Andrew Ilyas, Vasilis Syrgkanis, and Haoyang Zeng. Training gans with optimism. arXiv preprint arXiv:1711.00141, 2017.

- Foerster et al. [2018] Jakob Foerster, Richard Y Chen, Maruan Al-Shedivat, Shimon Whiteson, Pieter Abbeel, and Igor Mordatch. Learning with opponent-learning awareness. In Proceedings of the 17th International Conference on Autonomous Agents and MultiAgent Systems, pages 122–130, 2018.

- Mescheder et al. [2017] Lars Mescheder, Sebastian Nowozin, and Andreas Geiger. The numerics of gans. In Advances in Neural Information Processing Systems, pages 1825–1835, 2017.

- Korpelevich [1977] GM Korpelevich. Extragradient method for finding saddle points and other problems. Matekon, 13(4):35–49, 1977.

- Balduzzi et al. [2018] David Balduzzi, Sebastien Racaniere, James Martens, Jakob Foerster, Karl Tuyls, and Thore Graepel. The mechanics of n-player differentiable games. In International Conference on Machine Learning, pages 354–363. PMLR, 2018.

- Ramponi and Restelli [2021] Giorgia Ramponi and Marcello Restelli. Newton optimization on helmholtz decomposition for continuous games. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 35, pages 11325–11333, 2021.

- Schäfer and Anandkumar [2019] Florian Schäfer and Anima Anandkumar. Competitive gradient descent. In Proceedings of the 33rd International Conference on Neural Information Processing Systems, pages 7625–7635, 2019.

- Hillar and Lim [2013] Christopher J Hillar and Lek-Heng Lim. Most tensor problems are np-hard. Journal of the ACM (JACM), 60(6):1–39, 2013.

- O’Leary [1980] Dianne P O’Leary. The block conjugate gradient algorithm and related methods. Linear algebra and its applications, 29:293–322, 1980.

- Mazumdar et al. [2018] Eric Mazumdar, Lillian J Ratliff, and S Sastry. On the convergence of gradient-based learning in continuous games. arXiv preprint arXiv:1804.05464, 2018.

- Daskalakis and Panageas [2018] Constantinos Daskalakis and Ioannis Panageas. The limit points of (optimistic) gradient descent in min-max optimization. arXiv preprint arXiv:1807.03907, 2018.

- Mazumdar et al. [2019] Eric V Mazumdar, Michael I Jordan, and S Shankar Sastry. On finding local nash equilibria (and only local nash equilibria) in zero-sum games. arXiv preprint arXiv:1901.00838, 2019.

- Schäfer et al. [2020] Florian Schäfer, Anima Anandkumar, and Houman Owhadi. Competitive mirror descent. arXiv preprint arXiv:2006.10179, 2020.

- Williams [1992] Ronald J Williams. Simple statistical gradient-following algorithms for connectionist reinforcement learning. Machine learning, 8(3-4):229–256, 1992.

- Prajapat et al. [2021] Manish Prajapat, Kamyar Azizzadenesheli, Alexander Liniger, Yisong Yue, and Anima Anandkumar. Competitive policy optimization. UAI ’21: Proceedings of the 37th Conference on Uncertainty in Artificial Intelligence, 2021.

- Konda and Tsitsiklis [2000] Vijay R Konda and John N Tsitsiklis. Actor-critic algorithms. In Advances in neural information processing systems, pages 1008–1014, 2000.

- Schulman et al. [2015] John Schulman, Philipp Moritz, Sergey Levine, Michael Jordan, and Pieter Abbeel. High-dimensional continuous control using generalized advantage estimation. arXiv preprint arXiv:1506.02438, 2015.

- ML2 [2021] ML2. Marlenv, multi-agent reinforcement learning environment. http://github.com/kc-ml2/marlenv, 2021.

- Littman [1994] Michael L Littman. Markov games as a framework for multi-agent reinforcement learning. In Machine learning proceedings 1994, pages 157–163. Elsevier, 1994.

- Letcher et al. [2019] Alistair Letcher, David Balduzzi, Sébastien Racaniere, James Martens, Jakob Foerster, Karl Tuyls, and Thore Graepel. Differentiable game mechanics. The Journal of Machine Learning Research, 20(1):3032–3071, 2019.

- Ortega and Rheinboldt [2000] James M Ortega and Werner C Rheinboldt. Iterative solution of nonlinear equations in several variables. SIAM, 2000.

Appendix A Appendix

Appendix B Proof of theoretical results

A popular tool to establish local convergence of iterative solvers is Ostrowski’s theorem. We will use this classical theorem in the form of [29, Theorem 8], which is in turn an adaptation of [30, 10.1.3)].

Theorem 4 (Ostrowski).

Let be a continuously differentiable map on an open subset , and assume is a fixed point of . If all eigenvalues of are strictly in the unit circle of , then there is an open neighbourhood of such that for all , the sequence of iterates of converges to . Moreover, the rate of convergence is at least linear in .

Proof of Theorem 3.

In order to apply Theorem 4, we define the map

| (19) |

as the application of a single step of Algorithm 1. The fixed points of this map are exactly those points where . According to Theorem 4, PCGD converges locally to such a point , if

| (20) |

has eigenvalues in the unit circle. Here, is the antisymmetric part of the game Hessian and is the off-block-diagonal part of the symmetric part of , so that . Omitting from now on the argument , this holds if and only if the eigenvalues of satisfy

or equivalently,

Assume and let be any eigenvalue of with normalized eigenvector . By symmetry of and the antisymmetry of , we can write and with . In particular, implies . Writing for the off-block-diagonal part of , it holds moreover that

and thus

Here, we have exploited the general fact that the smallest eigenvalue of the block-diagonal part of a positive definite matrix is always at least as large as the smallest eigenvalue of the full matrix, as well as the assumption that is a local Nash equilibrium and thus is positive definite. The assumption that therefore implies . We obtain

It follows that

and so

| (21) |

Note that we cannot have since is assumed to be invertible, so this always holds if . Now assuming , the equation holds for any if since the LHS is negative and the RHS positive. Finally assume , and notice that implies

which is equivalent to equation 21. We have shown that the eigenvalues lies in the unit circle for any , and thus conclude the proof using Theorem 4. ∎

Appendix C Numerical experiment details

C.1 Snake Game Implementation

In the Snake game, four different snakes compete in a fixed 20x20 space to box each other out, to consume a number of randomly-placed fruits, and to avoid colliding with each other or the walls. Each snake is initialized with length 5, and can use their body to box out another snake. Snakes are initialized in either a clockwise or counter-clockwise spiral orientation, where each agent has a different initial orientation. We adapt the implementation of Snake by ML2 [27] by first rotating the observations such that the snake’s current direction corresponds to the top of the multi-channel observation matrix. Similarly, we adjust the action space to instead be three actions (no change in direction or no-op, turn left, or turn right) relative to the snake’s current orientation instead of the original five (no-op, up, down, left, right) global actions.

At each step of the game, each snake observes the 20-by-20 space centered at its head and decides whether to continue moving forward, to turn left, or to turn right. The observation vector is structured as a 4x20x20 tensor: the first channel denotes any cells corresponding to the current snakes body as 1, zero elsewhere; the second channel denotes any nearby grid cell with an of opponent snake’s body as 2, denotes any cells containing walls as 1, zero elsewhere. The third channel denotes any nearby fruits as 1, zero elsewhere, and the fourth channel denotes any cells containing nearby walls as 1, zero elsewhere. Agents are rewarded with from consuming a fruit, from capturing another snake, for colliding with either another snake’s body or a wall, and for being the last snake alive. Once a snake collides with a wall or another snake, it is eliminated from the game and its body is removed from the playing field. We terminate the game as soon a single snake wins, since continuing to optimize would become a single agent optimization problem.

Each agent policy maps the observation vector of the game to a categorical distribution of 5 outputs using a network with two hidden layers (64-32-5). Agents sample actions from a softmax probability function over this categorical distribution. For all of SimGD, Extragradient, SGA and PCGD scenarios, we trained the agents for 15000 epochs. At each epoch, we collected a batch of 32 trajectories. We used a learning rate of 0.001 and GAE for advantage estimation with and .

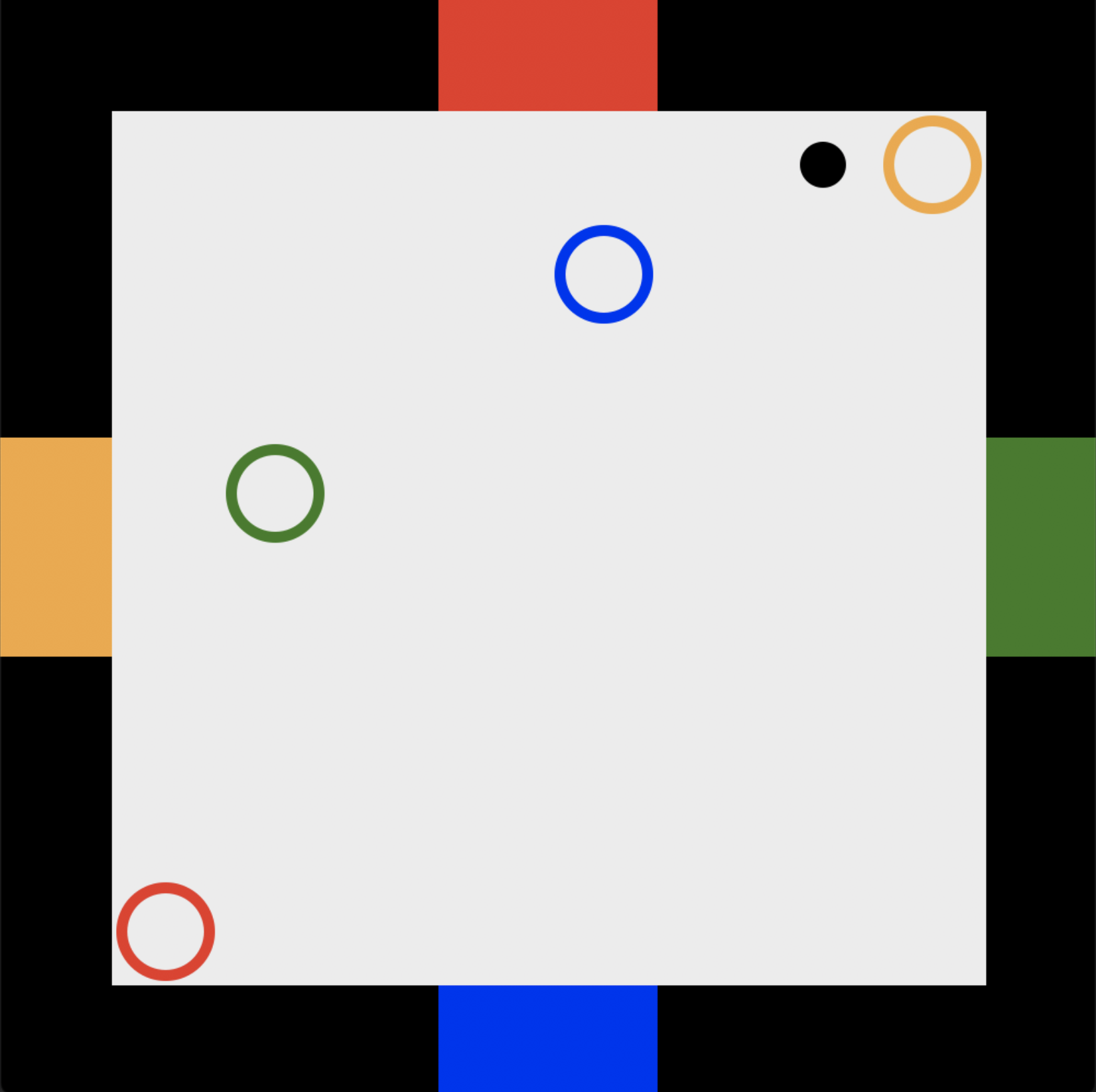

C.2 Markov Soccer Game Implementation

The setup of the four-player Markov soccer is shown in the left. It ist based on the two-player variant [28] and is played between four players that are each randomly initialized in one of the 8x8 grid cells. The ball is also randomly initialized in one of the 8x8 grid cells. Each agent is assigned a goal and are supposed to pickup the ball (by moving into the ball’s grid location or stealing it from another player) and place it in one of their three opponents goals. Agents are allowed to move left, right, up, or down, or to stand still. If one player holds the ball and another agent’s move would put it into the position of the ball-holding agent, the second agent successfully steals the ball, and both agents keep their original positions.

At each step of the game, agent actions are collected and processed in a random order; thus, it is possible that multiple steals can happen in a single round. The game ends if the player holding the ball moves into a goal, and the goal scoring player is rewarded with , the player who was scored on is penalized with , and all other players are penalized with .

Given a clockwise order of players , where is the location of the player with the top goal, with the rightmost goal, with the bottom goal, and with the left side goal, the local state vector of each player with respect to other players is defined as:

where are defined as the relative position of the current player to some other item in horizontal and vertical offsets, and where are the goals of players and . The observation state of each player is then as follows:

Each agent policy maps the observation vector of the game to a categorical distribution of 5 outputs using a network with two hidden layers, the first with 64 neurons, the second with 32. Agents sample actions from a softmax probability function over this categorical distribution. For all of SimGD, Extragradient, SGA and PCGD scenarios, we trained the agents for 20000 epochs. At each epoch, we collected a batch of 16 trajectories. We used a learning rate of 0.01 and GAE for advantage estimation with and .

C.2.1 Electricity Market Game Implementation

The implementation of electricity market game follows Fig. 8, where the system is a standard 6-bus system from [4]. The demand at each bus is set to be . Each bus can have one or more generators assigned to it. In our experiments, we place one high marginal-cost generator (e.g., coal or gas generator) at each of the six buses, which has a fixed capacity bid of 1000 units and a constant marginal cost of 35 units. This ensures that the market optimization problem is always feasible and makes the game environment more robust to randomly sampled bids learning agents might make during training.

We place the three learning generators at each of Buses 1, 3, and 5, and train the agents together under both PCGD, SimGD, ExtraGD and SGA. We further add a flag to indicate whether that bus is under load, affected by the price. Without loss of generality, this framework can simulate the effect of both elastic and inelastic electricity demand. The load flag is set based on the previously calculated electricity price (LMP) at that bus: if the price at that bus exceeds a certain threshold, the flag is set to 1; otherwise, it is set to 0. For inelastic demand single-stage repeated game, we set the LMP load thresholds at each bus as infinity. For elastic demand multi-stage game, we set the LMP load thresholds at certain positive values and can be different across buses. For our experiments, the LMP load thresholds for each bus are [25, 25, 25, 35, 30, 25]. Once the LMP at certain bus exceeds the LMP load threshold, the demand at that bus is reduced by half.

Each trajectory of this electricity market game goes as follows: We initialize load states randomly (0 or 1) at each bus: standard demand or reduced demand status. For each step, each of the three learning agents observes the load state of the environment, a 6-vector containing the load state flags of Buses 1 through 6, and submits a bid for the maximum capacity that they are willing to generate. This bid is capped from 0 to 10000 generation units. The market solver collects these bids and solves the market optimization problem in equation 18 to determine: (i) the electricity price at each bus and the (ii) quantity to be generated per generator . From the results of the market optimization algorithm, we calculate profit for each learning agent and return it as immediate reward. Profit at each step is divided by a constant factor of 50 to stabilize learning in this game. At the end of each step, the electricity price at each bus is used to update system states (i.e., demand state) for the next game step. Finally, to create a finite horizon, at each step the game has a fixed probability of ending. For our experiments this probability is , giving the game an expected length of 5 steps.

Each agent’s policy is parameterized as a Gaussian policy, where the mean is the output from 2 two-hidden layer neural network (128 neurons each layer) and the standard deviation is fixed at 25. Each player samples a bid for its maximum generation capacity from this Gaussian distribution. For all optimization methods, players were trained for 1000 episodes. In each epoch, we collected 64 trajectories per update step. We used a learning rate of 0.001 and GAE for advantage estimation with and , as we optimize over non-discounted profit.

C.3 Computational Resources

All experiments were implemented and trained on Amazon AWS P3 instances with an Nvidia V100 Tensor Core GPU.