dateenglish\monthname[\THEMONTH] \THEDAY, \THEYEAR

Joint FCLT for Sample Quantile and Measures of Dispersion for Functionals of Mixing Processes

?abstractname?

In this paper, we establish a joint (bivariate) functional central limit theorem of the sample quantile and the -th absolute centred sample moment for functionals of mixing processes. More precisely, we consider -near epoch dependent processes that are functionals of either -mixing or absolutely regular processes. The general results we obtain can be used for two classes of popular and important processes in applications: The class of augmented GARCH(,) processes with independent and identically distributed innovations (including many GARCH variations used in practice) and the class of ARMA(,) processes with mixing innovations (including, e.g., ARMA-GARCH processes). For selected examples, we provide exact conditions on the moments and parameters of the process for the joint asymptotics to hold.

2010 AMS classification: 60F05; 60F17; 60G10; 62H10; 62H20

JEL classification: C13; C14; C30

Keywords: asymptotic distribution; Bahadur representation; functional central limit theorem; near epoch dependence; mixing; (augmented) GARCH; ARMA; dependence; (sample) quantile; measure of dispersion; (sample) mean absolute deviation; (sample) variance

1 Introduction and framework

The focus of this paper is on the asymptotic theory of sample estimators of standard statistical quantities as rank, location and dispersion measures, for a very large class of widely used stationary processes. Such a theory is often needed for related statistical inference. The literature for sample quantiles has considerably developed (closely related to empirical processes) from the iid setting toward dependent random variables. In view of applications, it is also important to consider jointly the estimators of such standard statistical quantities. Fields of applications include dynamic systems (networks), (financial) econometrics, reliability, risk theory and management, quantitative finance, etc. For instance, dispersion measures, as e.g. the 2nd centred moment (named volatility in financial fields), are essential in economics for studying market fluctuations. This is why they are often introduced, via conditioning or jointly, in the econometric analysis of macroeconomic and financial data, to take into account the market state. Investigations on the relation between volatility estimators (a measure of dispersion) and Value-at-Risk (a quantile estimator) for time-series models are common in this field; see e.g. [14],[27], [38], [66, 67].

In the literature, the asymptotic behavior of each quantity has been investigated on its own, under some dependence structures. Limit theorems for sample quantiles have been proposed, inter alia, in the case of m-dependent or -mixing processes ([53], [54]), infinite-variance or non-linear processes ([30], [63]), and functionals of mixing processes ([61]). They are generally based on the use of the Bahadur representation developed in [4] for independent and identically distributed (iid) random variables (and refined by Kiefer in a sequence of papers), then extended (generally via coupling techniques) to linear and nonlinear processes, with various types of dependence (see e.g. [63, 64] and references therein).

For dispersion measures, there exist results for the mean absolute deviation (MAD) when considering strongly mixing processes ([52]), while the asymptotics of the sample variance can be found for various settings as examples in standard textbooks, see e.g. [1], [15], [58]. When considering more generally the autocovariance function of such estimators, we can mention, exemplarily, results for linear, bilinear or non-linear processes with regularly varying noise ([18], [19]), and for long-memory time series (e.g. [35] - and for a more complete overview [39] and references therein).

In this paper, we establish the joint asymptotics of the sample quantile and the -th absolute centred sample moment for functionals of strictly stationary processes , namely

assuming -mixing or absolutely regular, respectively, and near-epoch dependent. We briefly recall these dependence notions further below. Our limit theorem extends existing results on joint asymptotics in the case of an identically and independently distributed (iid) sample (see [14]). In particular, we establish an asymptotic representation for the -th absolute centred sample moment for stationary, ergodic, short-memory processes under minimal conditions (extending the results in [52] and [14]). Furthermore, our general results include two important popular classes of linear and nonlinear processes: The class of augmented GARCH(,) processes with iid innovations and ARMA(,) processes with mixing innovations. The former, introduced by Duan in [23], contains many well-known GARCH processes as special cases, of standard use, e.g. in quantitative finance and financial econometrics. Previous works on univariate CLTs and stationarity conditions for this class of GARCH processes are, among others, [3],[5],[34] and [40]. The class of ARMA processes includes the classical ARMA models with iid or white noise innovations (see e.g. [15], [12] for classical references on the topic), but also with mixing inovations. The earliest explicitly mentioned examples of ARMA processes with mixing innovations date back, to our knowledge, to [59], [60] considering ARMA models with ARCH errors. More widespreadly used in applications is the ARMA-GARCH model, which can be seen as an extension of the GARCH models to also have dynamics in the mean and not only in the variance process. First contributions on such types of processes can be found in [43], [44], [46]; more recent examples of applications are, e.g. [32, 55, 56]. Analogously to the class of augmented GARCH processes, there exist results in the literature on FCLTs for ARMA processes with mixing innovations (or even larger classes of linear processes), as e.g. [17], [50].

Classical and broad notions for (asymptotically vanishing) dependence of a process are known under the name of mixing (see [13] for an overview). Let us recall some notions of weak dependence related to the mixing coefficients. Let be a random process and denote the corresponding -algebra as .

Definition 1 (Mixing coefficients).

For any integer , let

The process is called strongly mixing if , -mixing or absolutely regular if , and -mixing if .

Note that, for a stationary time series, we can omit the in the definition of the mixing notions and simply set, w.l.o.g. , . Also, -mixing implies -mixing that implies -mixing, but the converse does not hold in general.

A drawback of mixing is that, in general, a functional that depends on an infinite number of lags of a mixing process will not be mixing itself. This gave rise to the introduction of the notion of -near-epoch dependence (-NED) (that goes back to [37] in the case of for an underlying -mixing process, even if not named NED there). It imposes additional structure on functionals of mixing processes enabling statistical inference for this larger class of processes. Alternatively, -NED is also called -approximation functional; see [9], [61].

Definition 2 (-NED, [2]).

For , a stationary process is called -NED on a process if, for ,

for non-negative constants such that as .

Note that, in the econometrics literature, a specific terminology is used for the rate of : If for some , one calls the process -NED of size and, if for some , geometrically -NED.

Finally, let us present some technical conditions on the marginal distribution function of the stationary process under study, and give the notation of the sample estimators for the two quantities of interest. We denote, whenever they exist, the probability density function (pdf) of by , with mean , variance , as well as, for any integer , the -th absolute centred moment, . The quantile of order of is defined as .

We impose four different types of conditions on the marginal distribution , as in the iid case (see [14]). First, we assume the existence of its finite -th moment for any integer . Then, the continuity or -fold differentiability of (at a given point or neighbourhood) for any integer , and the positivity of (at a given point or neighbourhood). Those conditions are named as:

Given a sample , with order statistics , let denote the sample quantile of order , namely

where and are the rounded-up integer-part and the nearest-integer of a real number , respectively.

The -th absolute centred sample moment is denoted by and defined, for , by

| (1) |

representing the empirical mean. Special cases of this latter estimator include the sample variance () and the sample mean absolute deviation around the sample mean ().

Recall the standard notation for the transpose of a vector and for the signum function. By , we denote the euclidean norm, and the usual -norm is denoted by . Moreover the notations , , and correspond to the convergence in distribution, almost surely, in probability and in distribution of a random vector in the d-dimensional Skorohod space . Further, for real-valued functions and , we write (as if and only if there exists a positive constant and a real number s.t. for all , and (as ) if, for all , there exists a real number s.t., for all , . Analogously, for a sequence of rv’s and constants , we denote by the convergence in probability to 0 of .

The structure of the paper is as follows. We present in Section 2 the main results on the bivariate FCLT for the sample quantile and the -th absolute centred sample moment for functionals of -mixing or absolutely regular processes. In Section 3, we apply our general results to the family of augmented GARCH(, ) processes and ARMA(,) processes with mixing innovations. Section 4 gathers auxiliary results needed for the proofs of the main results, but also of interest on their own: the asymptotic representation of the -th absolute centred sample moment and results on -NED of bounded and unbounded functionals. Finally, the proofs are given in Section 5. In Appendix A, we show how the conditions in the results of Section 3 translate for specific cases of well-known GARCH models, specifying under which conditions on the moments and parameters of the process these results hold. Further, in Appendix B, we recall univariate and multivariate (F)CLTs that we use in the proof of the main results.

2 The Bivariate FCLT

Let us state the main result. To ease its presentation, we introduce a trivariate normal random vector , functional of a random process , with mean zero and the following covariance matrix:

Theorem 3 (bivariate FCLT).

Consider a process that can be represented as a functional of a strictly stationary process and introduce the random vector

Assume for the marginals that the conditions , at and in a neighbourhood of and, for , at , are satisfied.

In terms of dependence, suppose that:

-

is -NED with constants , on a -mixing process with mixing coefficient , for some .

-

(D2)

For , is -NED with constants , for .

Then, we have, for ,

where is the 2-dimensional Brownian motion with covariance matrix defined, for any , by , where

being the trivariate normal vector (functional of ) with mean zero and covariance given in , all series being absolute convergent.

Remark 4.

-

1.

The conditions of Theorem 3 are those required to establish a univariate CLT for each component of , namely the sample quantile and the -th absolute centred sample moment. For the latter statistic, it requires first establishing a suitable representation, a new result on its own, presented in Proposition 13. Requiring and in a neighbourhood of corresponds to the conditions for the CLT of the sample quantile of a stationary process, which is -NED with constants on an absolutely regular process (thus also for a -mixing process) with mixing rate , for - see Corollary 1 in [61].

Further, the -NED with constants on a -mixing process with mixing rate , for , together with and the additional assumptions in the cases of ( at ) and (-NED with constants , on ), are sufficient conditions for the univariate CLT of the -th centred sample moment (using Theorem 1.2 in [17], which is a special case of Theorem 3.1 in [20]).

-

2.

Note that we have a trade-off between more restrictive mixing conditions on the underlying process and more restrictive moment conditions on . We make this explicit in Corollary 5.

-

3.

For , there can be an additional trade-off: In Corollary 6 we show that sufficient conditions for the -NED of are a balance between more restrictive moment conditions than and less restrictive NED conditions on (but more than -NED).

- 4.

We now present the different corollaries mentioned in Remark 4. In the first two, we illustrate the trade-off between more restrictive mixing and moment conditions. Note that, in Corollary 5, Condition (D1∗) replaces Condition (D1) of Theorem 3. In the subsequent two corollaries, we recover the CLT and the iid case as special cases from Theorem 3.

The result of Theorem 3 holds also true if we consider an underlying absolutely regular process , and slightly adapt the conditions:

Corollary 5.

Assume the setting and conditions of Theorem 3 with the following two changes:

-

•

Take and assume that the moment condition holds for an , instead of .

-

•

(D1∗) (instead of (D1)): The process is -NED with constants , on an absolutely regular process (instead of -mixing) with the same order of mixing coefficient, i.e. for some .

Then, the FCLT holds for as in Theorem 3.

Moreover, we can provide sufficient conditions to reduce the -NED of (condition (D2) in Theorem 3 and Corollary 5 respectively) to -NED of the process itself, as follows:

Corollary 6.

Note the following two extreme cases for choices of and in Corollary 6: Choosing , we get the most restrictive moment condition () in combination with -NED of , while, when choosing , we get the least restrictive moment condition () but needing -NED of at the same time. Only for , these two cases coincide.

Let us now turn to two special cases of Theorem 3 presented in Corollaries 7 and 8 and given for sake of completeness. Choosing in Theorem 3 provides the usual CLT, stated in Corollary 7:

Corollary 7.

We can also recover the CLT between the sample quantile and the -th absolute centred sample moment stated in the iid case; see [14], Theorem 4.1, which, of course, requires less restrictive conditions.

Corollary 8.

(Theorem 4.1 in [14]). Consider the series of iid rv’s with parent rv . Assume that satisfies and both conditions and in a neighbourhood of . Additionally, for , assume at . Then, the joint behaviour of the sample quantile (for ) and the -th absolute centred sample moment , is asymptotically bivariate normal:

| (3) |

where the asymptotic covariance matrix simplifies to

Idea of the proof -

Let us briefly sketch in three main steps the proof of Theorem 3 and, analogously, of Corollary 5, which is developed in Section 5.

-

•

First, we represent the sample quantile and -th absolute sample moment as sums of functionals of the process , so that has the following representation, based on , for a measurable function , with and , ,

For the sample quantile, we use its Bahadur representation, using a version given in [61, Theorem 1]. For that, we check that the NED, moments and mixing of the process are satisfied. These conditions are needed for approximating the sample quantile by an iid sample (and showing that the rest is asymptotically negligible). This approximation idea (coupling technique) dates back to the 70’s with Sen (see e.g. [63] for a brief historical review on the Bahadur representation). Next, we prove, under some conditions, a corresponding asymptotic representation for the -th absolute centred sample moment, extending results from [52] and [14]. Here, more work is involved as we consider not only the case when the mean is known but also an unknown mean. As such a representation is of interest on its own, we state it as a separate result, in Proposition 13.

-

•

Next, we have to ensure that each of the components of fulfil the conditions needed for a multivariate FCLT. Those include moment conditions on , for any , -NED of , as well as summability conditions of the mixing coefficients and constants . In particular, we show that the -NED condition on can be reduced to the -NED condition for the processes and .

- •

Note that, for the FCLT to hold for the very general class of stationary processes considered in this study, we will have to separately analyse the cases of -mixing (with moment condition ) and absolute regularity (with moment condition ) for . In each of the two cases, we need to introduce a different set of conditions for the FCLT to hold for , making sure that the mixing conditions on are inherited from those on . The -mixing case is done in the proof of Theorem 3, the absolute regularity one in the proof of Corollary 5.

3 Application to augmented GARCH and ARMA processes

We focus in this section on two classes of processes widely used in application, which fall within the framework of Theorem 3. By doing so, we provide new results when considering joint standard estimators for such processes. In Section 3.1 we consider the broad family of augmented GARCH(, ) processes with iid innovations, while, in Section 3.2, ARMA processes with dependent (absolutely regular) innovations; we also discuss an example, the ARMA-GARCH process. For the interested reader, we provide in Appendix A further specific examples of processes that fall in one of the two mentioned families and translate specifically the conditions on the moments and parameters of the process for the presented results to hold.

3.1 Bivariate FCLT for augmented GARCH(,) processes

Since the introduction of the ARCH and GARCH processes in the seminal papers by Engle, [24], and Bollerslev, [7], respectively, various GARCH modifications and extensions have been proposed and their statistical properties analysed (see e.g. [8] for an (G)ARCH glossary). Many such well-known GARCH processes can be seen as special cases of the class of augmented GARCH(, ) processes, established by Duan in [23].

An augmented GARCH(,) process satisfies, for integers and ,

| (4) | ||||

| (5) |

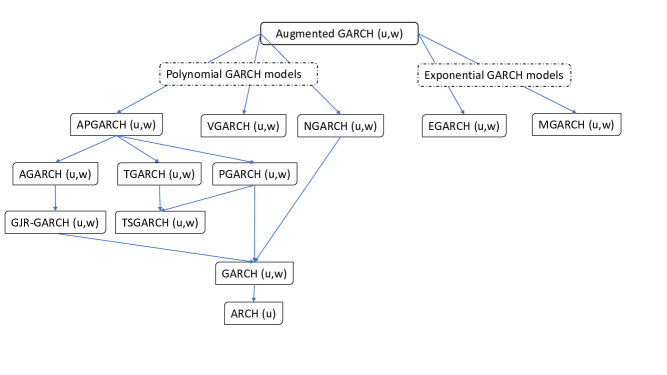

where is a series of iid rv’s with mean and variance , and , are real-valued measurable functions. Also, as in [40], we restrict the choice of to the so-called group of either polynomial GARCH(,) or exponential GARCH(,) processes (see Figure 1 in Appendix A for a representation of the hierarchy of these processes):

Clearly, for a strictly stationary solution to (4) and (5) to exist, the functions as well as the innovation process have to fulfil some regularity conditions (see e.g. [40], Lemma 1).

Alike, for the bivariate FCLT to hold, certain conditions on the functions , of the augmented GARCH(,) process of the family are needed, namely: Positivity of the functions used, (A), and boundedness in -norm for either the polynomial GARCH, , or exponential GARCH, , respectively, for a given integer ,

Note that Condition requires the to be bounded functions.

Remark 9.

By construction, from (4) and (5), and are independent (and is a functional of ). Thus, the conditions on the moments, distribution and density, could be formulated in terms of only. At the same time, this might impose some conditions on the functions (which might not be covered by , or ). Thus, we keep the conditions on as such, even if they might not be minimal.

Now, let us explain why and under which circumstances Theorem 3 holds.

It has been shown in the literature under which conditions the class of augmented GARCH(, ) processes fulfills the -NED.

More precisely, the conditions of geometric -NED on and are satisfied, on the one hand in the polynomial case under and via Corollary 2 in [40], on the other hand in the exponential case under and via Corollary 3 in [40].

This can be directly used to reframe the general FCLT given in Theorem 3 for the class of augmented GARCH(, ) processes:

and for polynomial, for exponential GARCH models respectively, are sufficient conditions for (D1) and (D2) in Theorem 3 to hold. Thus, Theorem 3 translates as follows:

Corollary 10.

Consider an augmented GARCH(,) process as defined in (4) and (5), which satisfies:

-

•

, both conditions at , and at for

-

•

, , and either for belonging to the group of polynomial GARCH, or for the group of exponential GARCH

Then, for , as , we obtain the FCLT

where the 2-dimensional Brownian motion, , has the same covariance matrix as in Theorem 3.

3.2 Bivariate FCLT for ARMA(,) processes

Similarly to the family of GARCH processes, ARMA (AutoRegressive - Moving Average) processes are widely used in applications (e.g. for financial time series). While GARCH models specify a structure of the conditional variance of the process, ARMA processes specify the conditional mean.

Recall that a general ARMA(,) process , for integers and , is a stationary process defined by

| (6) |

where is, in its most general form, a series of rv’s with mean and finite variance, the backward operator denotes the application , and and are polynomials of order and respectively, defined by () and (), such that and do not have any common root (to have a unique solution to (6)). A necessary and sufficient condition for to be causal, i.e. , with , is:

| (7) |

As already mentioned, various specifications of ARMA processes exist; we refer to [15], [12] and the survey article [33] for further references and examples. While the simplest case assumes iid innovations , mixing innovations have been introduced as they allow for broader applications. We can consider this general case thanks to the setup of Theorem 3 (and Corollary 5 respectively).

Note that the geometric -NED of ARMA(, ) processes with mixing innovations can be directly deduced from Theorem 3.1 in [50] under the causality condition (7). But, in contrast to the case of augmented GARCH(,) processes, we do not have results on the -NED of . So we establish this property in Lemma 19 (see Section 4), showing that the causality condition (7) is still sufficient. With these informations at hand, we can replace conditions (D1) and (D2) of Theorem 3 by specific conditions for the class of ARMA(, ) processes with mixing innovations, and state the following:

Corollary 11.

Consider a causal ARMA(,) process as defined in (6), such that:

-

•

Both conditions at hold, as well as at for

-

•

has either -mixing innovations (denoted ARMA-), or absolutely regular innovations (ARMA-) - in both cases with mixing coefficient of order , for some

-

•

satisfies for ARMA-, or , for any for ARMA-.

Then, for , as ,

where , the 2-dimensional Brownian motion, has the same covariance matrix as in Theorem 3.

Among ARMA processes with mixing innovations, the ARMA-GARCH process is a widespread example in applications (see e.g. [55, 56, 32]).

Example 12 (ARMA(, )-GARCH(,) process (for )).

A general ARMA(, )-GARCH(,) is defined as follows:

for an iid series with mean and variance .

Let us discuss the conditions of Corollary 11 applied to this class of processes.

-

•

Causality: For an ARMA(,)-GARCH(, ) to be causal, (7) needs to be fulfilled

-

•

Conditions on the marginal distribution: at as well as at for

-

•

Mixing innovations: The GARCH(,) process is known to be absolutely regular with geometric rate as long as it is strictly stationary, is absolutely continuous with Lebesgue density being strictly positive in a neighbourhood of 0, and for some ; see [42, Theorem 8] (the original result going back to [11]).

A necessary condition for the strict stationarity of the GARCH(,) process is known in the literature; see e.g. [10, Theorem 1.3]. A sufficient condition, easier to verify in practice, is: for (see [7]). -

•

Moment conditions: As the innovations are absolutely regular with geometric rate, the corresponding moment condition is for any . Necessary conditions for the existence of such moments depend on the specifications of the ARMA process and can be found e.g. in [46, Theorem 2.2]. In practice, a sufficient moment condition would be .

4 Auxiliary Results

In this section we present two different types of results. First, we provide in Proposition 13 an asymptotic representation of the -th absolute centred sample moment , for any integer . Then, in Lemmas 15, 16 and Corollary 18, we propose sufficient conditions such that the -NED property of is inherited for certain bounded and unfunctionals . We use them to establish the -NED of and , needed in the proof of Theorem 3. Additionally, Lemma 19 treats the specific case of the -NED of for any integer for ARMA(,) processes. Proofs of these results are deferred to Section 5.3.

4.1 Representation for the -th absolute centred sample moment

Let us state the asymptotic relation between the -th absolute centred sample moment with known and unknown mean, respectively. This enables us to compute the asymptotics of (given that the needed moments exist).

Proposition 13.

Consider a stationary and ergodic process that has ‘short-memory’, i.e.

.

Then, for any integer , assuming that the -th moment of exists and holds at for , we have the following asymptotics, as ,

| (8) |

4.2 -NED of functionals of

Here, we question under which conditions some bounded and unbounded functionals, as e.g. and , inherit the -NED of the process .

For bounded functionals, we can adapt the result proved for the -NED case (see [61], Lemma 3.5) to the -NED. For this, we introduce the ‘-variation condition’, a generalization of the variation condition for (that dates back to [21]) used in [61] (see therein Definition 1.4). As already noticed in [61], the (-)variation condition is similar to the notion of -continuity of [9] (Def. 2.10 therein).

Definition 14.

Let be a stationary process. For , a function satisfies the -variation condition (with respect to the distribution of ), if there exists a constant such that for any

Then, we can adapt Lemma 3.5 in [61] to the -NED case.

Lemma 15.

Let be -NED with constants , on a stationary process , and let be a function bounded by such that satisfies the 2-variation condition with constant . Then is -NED with constants .

Let us now consider the case of unbounded functions. In such a case, rather than considering -variation (or -continuity), we assume a certain geometry on these functions, namely convexity.

Lemma 16.

Let a process be -NED with constants on a stationary process .

Consider a positive, convex function with derivative such that, on , is convex and positive, and is convex with .

Then, a sufficient condition for the -NED of with constants is :

Remark 17.

For the reader interested in results on -NED in the case of unbounded functionals (which could be adapted to the -NED setting), we refer to [62], Lemma 2.1.7(i), under the assumption that the functional satisfies the 1-variation condition, and to [9], Proposition 2.11, under the assumption of 1-continuity.

Applying Lemma 16 for the function , , we obtain:

Corollary 18.

Let a process be -NED with constants on a stationary process . Then, for a given integer , a sufficient condition for the -NED of (with constants of order ) is, for any choice of s.t. ,

As an application, let us consider the class of ARMA(, ) processes, introduced in Section 3.2.

Lemma 19.

Let be a causal ARMA(, ) process as defined in (6). Then, for any integer , is geometrically -NED if .

We conclude this section with another application, which will be useful in the proof of Theorem 3, considering the indicator function , , in Lemma 15.

Example 20.

A sufficient condition for the function defined by (), to satisfy the -variation condition with respect to the distribution of , is the -Hölder continuity of the distribution function of .

Indeed, for , consider the expression

| (9) |

To deduce an upper bound for (9), note the following: For and , we have and, similarly, for with , it holds that . Thus, we can write

This implies, for the p-variation condition,

Therefore, satisfies the p-variation condition for any if is -Hölder-continous around (i.e., there exists a constant such that ).

Note that this result extends Example 1.5 in [61] for , where satisfies the Lipschitz-continuity.

5 Proofs

The main theorem is proven in Section 5.1, while the corollaries in Section 5.2. Proofs of the auxiliary results (presented in Section 4) are given in Section 5.3.

5.1 Proof of Theorem 3

As described in Section 2, the proof consists of three main steps. The first one, more involved, is split into two parts.

Step 1: Asymptotic representations for the two sample estimators

A Bahadur representation for the sample quantile

As explained in Section 2 the main idea in the Bahadur representation is to approximate the sample quantile by an equivalent estimator based on iid rv, i.e. showing that the dependence is asymptotically negligible.

The -NED of allows to approximate theses by functionals of finitely many , and the -variation condition ensures that this also holds for . Coupling techniques are then used to show that short-range dependent variables have the same behavior as iid ones (for this, mixing conditions are also necessary).

The choice of mixing conditions in Theorem 3 on the underlying process comes from the use of the Bahadur representation for NED processes as given in [61, Theorem 1], for which we need to verify the following conditions.

Let . It is straightforward to check that is non-negative, bounded, measurable, and non-decreasing in the second variable. The function also satisfies the variation condition uniformly in some neighbourhood of if it is Lipschitz-continuous. The latter follows from condition in a neighbourhood of .

The differentiability of and positivity of its derivative at are given by condition at .

The condition

is fulfilled as, by Assumption , is twice differentiable in .

As is stationary and -mixing (assumption ), , being a function of , is also stationary and ergodic.

Lastly, the process exactly fulfills the conditions on the mixing rate on the underlying process rate by :

Let . Then it holds that and as .

Further, the -NED is implied by the assumption of -NED (assumption ) at the exact same rate:

| (10) |

Thus, we can use the version of the Bahadur representation given in [61, Theorem 1], replacing (for our purposes) the exact remainder bound by , and write, as ,

| (11) |

Representation of the -th absolute centred sample moment

The representation is given in Proposition 13 (which proof can be found in Section 5.3). So, we simply need to check that the respective conditions (stationarity, finite -th moment, ergodicity and short-memory) are fulfilled. Let us explain why these conditions hold.

We have seen in above that is stationary.

The moment condition is fulfilled by assumption due to and, for , we have at by assumption too.

To prove the ergodicity and short-memory property,

we use a classical CLT for functionals of -mixing processes, [6, Theorem 21.1] (recalled in the appendix; see Theorem 22). It means to check that its conditions are fulfilled.

We have , by .

Moreover, as, by assumption , we have -NED with constants of the order , it holds for those constants that .

Finally, , since via the -mixing rate is assumed to be of order .

Step 2: Establishing the conditions needed for each component in view of the FCLT

Following the representation (8) of , we introduce tridimensional random vectors , for (anticipating their use in Step 3 for the FCLT of ), defined by

The idea is to apply the multivariate FCLT enunciated in Theorem 24, hence we have to verify that each random process , for , respectively, fulfills the conditions stated in Theorem 24, i.e.

-

(a)

Each process is -NED with constants , on a univariate process (the same for all components) which is, in our case, -mixing of order for any for a given .

-

(b)

For this choice of in (a), it must hold that , for all and for each .

-

(c)

as , for each .

Choosing , let us show that all the assumptions hold for each of the components of .

-

•

Condition (a): Let us first comment on the order of the -NED constants. For , by Assumption , it is of order . For , by in conjunction with Lemma 15, we have an order of . Finally, for , it is by Assumption . As and in and respectively, the required order is then fulfilled.

The mixing rate for , for , is, by Assumption , . As we chose , the required rate in Theorem 24 is for . Thus fulfills this requirement. -

•

Condition (b): We treat each component of , separately. By assumption of , it holds that (with , as chosen). Further, as is bounded, holds. Finally, holds using again .

- •

Step 3: Multivariate FCLT

Having checked the conditions for the FCLT (Theorem 24) in Step 2, we can now apply a trivariate FCLT for .

Using the Bahadur representation (11) of the sample quantile (ignoring the rest term for the moment), we can state:

| (12) |

where is the three-dimensional Brownian motion with covariance matrix , i.e. the components , satisfy the same dependence structure as for the random vector described in , with all series being absolutely convergent. By the multivariate Slutsky theorem, we can add to the asymptotics in (12) without changing the resulting distribution (since as ). Hence, we obtain, as ,

| (13) |

Then, we apply to (13) the multivariate continuous mapping theorem using the function with . Further, by Slutsky’s theorem once again, we can add to a rest of without changing the limiting distribution. So, we obtain, as ,

| (14) |

where follows from the specifications of above and the continuous mapping theorem.

5.2 Proofs of Corollaries

We consider corollaries in their order of appearance in the paper. We start with the proof of Corollary 5, where we need to show why Theorem 3 also holds in the case of an underlying absolutely regular process. The proof of Corollary 6 basically consists of establishing sufficient conditions for the -NED of , which will be done in (the proof of) Corollary 18 (proven in Section 5.3), thus we can omit it here. The proofs of corollaries 7, 8 and 10, are a direct consequence of Theorem 3, so can also be omitted. We end with the proof of Corollary 11 for which the main work consists of proving the -NED of , for ARMA processes.

Proof (Corollary 5).

The proof follows the one of Theorem 3, but we need to adapt (parts of) Steps 1b) and 2 to the setting of Corollary 5, i.e. for an underlying absolute regular process. Thus, we comment only on those two steps.

Step 1b): Representation of the -th absolute centred sample moment - Conditions.

Recall that such representation has been given in Proposition 13, so we simply need to check that the respective conditions, stationarity, finite -th moment, ergodicity and short-memory, are fulfilled.

Only the reasoning for the short-memory property differs from the one in Theorem 3:

To prove the ergodicity and short-memory property, we verify that the conditions for a CLT of are fulfilled.

Since absolute regularity implies strong mixing at the same rate, we consider the CLT for functionals of strongly mixing processes; see [36, Theorem 18.6.2], recalled in Appendix B.1, Theorem 23.

By choosing in that theorem, we check that the conditions stated there are fulfilled (recall that we defined in Corollary 5, ).

-

•

holds by (as );

-

•

holds as it is bounded by (since ), which is finite by the assumption of -NED with rate , i.e. ;

-

•

holds by construction (the choice of was made in a way that the sum is finite): ensures that and, by the choice of in the corollary, implies . We assume, w.l.o.g., that . We then have

As , , this quantity will always be bigger than and hence the infinite sum remains summable.

Hence Theorem 23 applies in this case for the process .

Step 2: Conditions for applying the FCLT (Theorem 24)

In Theorem 3, we used Theorem 24 as multivariate FCLT, which does not only cover the case of underlying -mixing processes, but also strong mixing. It means that we can also use it here. Therefore, it comes back to verify Condition , defined below, and Conditions (b) and (c) given in the proof of Theorem 3, Step 2.

-

-NED process with constants (changed from to , to avoid notational confusion) on a univariate process (the same for all components), which, in this case, is -mixing of order for any for a .

Note that, in comparison to the proof of Theorem 3, only the first condition has been adapted. Nevertheless, as the underlying mixing property is different, the proof of conditions (b) and (c) have also to be adapted.

Choosing in Theorem 24, we can show that all the assumptions hold for each of the components of .

-

•

Condition : The order of the -NED constants being the same as for the -mixing case, see and , the same arguments as in the proof of Theorem 3 hold. The mixing rate for is, by assumption , , which implies, by definition of , that it is also of order . Since we chose , we have (as ). The required rate in Theorem 24 is for a , thus fulfills this requirement.

-

•

Condition (b): We treat each component of , separately. By assumption of , it holds that . Further, as is bounded, . Finally, , using again the assumption of .

- •

Proof (Corollary 11).

Comparing the conditions of Corollary 11 with Theorem 3 or Corollary 5 respectively, we simply need to show why the causality (condition (7)), and or , are sufficient for the -NED of and with constants , and , , respectively. For , this follows directly by [50, Lemma 3.1] (by their result, a causal ARMA(,) is geometrically -NED). For , the geometric -NED has been exactly established through Lemma 19. Finally, as geometric -NED implies a rate of , the necessary rate for the application of Theorem 3 and Corollary 5, respectively, is attained.

5.3 Proofs of Auxiliary Results

We prove the auxiliary results of Section 4 in their order of appearance. We start by establishing the asymptotics of the -th absolute centred sample moment (Proposition 13). To do so, we need the following lemma, which extends Lemma 2.1 in [52] (case ) to any moment , as well as the iid case presented in Lemma A.1 in [14].

Lemma 21.

Consider a stationary and ergodic process with ‘short-memory’, i.e.

.

Then, for or , given that the 2nd moment of exists, or, for any integer , given that the -th moment of exists, it holds that, as ,

| (15) |

Proof.

The proof follows the lines of its equivalent in the iid case; see proof of Lemma A.1 in [14]. We recall briefly the main lines of the iid case for clarity, before mentioning the changes to be provided to obtain (15).

-

(i)

First, we rewrite the left hand side of equation (15) as

Defining the random variables and , we get a partition of with

such that the rest term can be defined as

-

(ii)

Then, we bound this rest term as

where denotes the cardinality of the set .

-

(iii)

Since it is shown in [52] that and we know that for any integer (as we are in the iid case), we have .

-

(iv)

Finally, we obtain by the strong law of large numbers

The argumentation for the proof in the dependent case needs to be adapted in points and , using the stationarity, ergodicity and short-memory of the process. By these three properties, it follows that holds for any integer (step ). Further, in , we use the ergodicity of the process, instead of the strong law of large numbers, to conclude that

Proof (Proposition 13).

Proposition 13 is an extension to the stationary, ergodic and short-memory case of Proposition A.1 in the iid case [14]. So, let us briefly comment on the differences compared to the iid case for the three different cases of :

Even integers - Recall that for the corresponding result in the iid case (see the proof of Proposition A.1 in [14]), we refered to the example 5.2.7 in [41]. Therein they only consider the iid case but in this case, the argumentation is still valid, when noticing that the convergence , for , holds for an ergodic, stationary, short-memory process too.

Case - The result cited in the iid case holds for ergodic, stationary time-series too; see [52, Lemma 2.1].

Odd integer - We point out the three differences to the corresponding proof in the iid case. First, as noticed above for even integers , the convergence , for , follows from the stationarity, ergodicity and short-memory of the process. Second, we use the ergodicity instead of the law of large numbers. Third, we use Lemma 21 instead of its counterpart in the iid case, Lemma A.1 in [14].

Proof (Lemma 15).

First, let us observe that

| (16) | ||||

| (17) |

where the first inequality follows from the fact that the conditional expectation minimizes the squared error over all measurable functions, i.e. for any measurable function , in particular for . For (16), we obtain by using the 2-variation condition,

For (17), using the boundedness of by , we have

Then, by the extended version of the Markov inequality and the fact that, by assumption, is -NED with constant , we obtain

from which we deduce that (17) can be bounded by . Hence, we can conclude that

Proof (Lemma 16).

We show the -NED of by directly estimating the constants. We start with the expression and comment line by line on the inequalities we use.

By the definition of conditional expectation as minimizer in norm, and then the inequality , for , we can write

| (18) |

Denoting and using the mean value theorem, , we can bound the RHS of (18) as

hence, after noticing that is an increasing function and using the triangle inequality for the absolute value, it comes

| (19) |

Now, applying Jensen’s inequality (as is convex on by assumption), then, Hölder’s one, and finally the triangle inequality, the RHS of (19) can be bounded by

| (20) |

For the last step, notice that the composed function is convex: As is non-decreasing for , it holds by the convexity of the absolute value function:

where the second inequality follows by the convexity of on , which also holds by assumption. Consequently, we can apply Jensen’s inequality for conditional expectations to this compound function and obtain an equivalent expression for the RHS of (20):

Thus, combining all these calculations and inequalities, we can conclude that

where the last inequality holds using the assumptions -NED of and the -boundedness of .

Proof (Corollary 18).

We need to verify the conditions of Lemma 16 in the case of .

We compute and . Thus, we can verify the conditions one-by-one:

-

•

positive: yes, as a functional of the absolute value

-

•

convex: yes, as

-

•

positive for : Yes, as positive and positive for .

-

•

convex for : Yes, as , hence we have for (and for ) - which is positive for

-

•

convex for , for a choice of : As , we get for (and equal to for ) - which is, for all choices of , positive for .

Proof (Lemma 19).

The proof consists of three steps. First we show why is geometrically -NED. Then, we establish a sufficient condition for the geometric -NED of , namely the geometric -NED of , and, finally, we prove why this latter condition is fulfilled.

The process being a causal ARMA(, )-process, we can apply Theorem 3.1 from [50]. Choosing therein, we can conclude that is strong -NED with rate , for some , hence it is -NED with the same rate (compare Definitions 1.1 and 1.2 in [50]).

Since , equivalently , is -NED, we can apply Corollary 18. As it holds by assumption that , we choose and accordingly . Then, by Corollary 18, it holds that is geometrically -NED if is geometrically -NED.

Thus, the last and most involved part is to show this latter claim. For this, recall the representation of an ARMA process (which holds for an ARMA(, ) process satisfying (6), (7), see Lemma 3.1 in [50]):

| (21) |

Then, we apply a standard truncation argument (as e.g. done in [40], Lemma 1 for augmented GARCH(, ) processes): Define the truncated variable , which, by construction, is -measurable. Let . For any given integer , let us now verify the -NED of :

where the first equality follows from the -measurability of and the subsequent inequality because for any random variables and .

Thus, it is enough to prove the geometric -NED of to conclude the proof. Since we can write

where has a finite second moment by definition of the ARMA(, ) process, then, using (21), we obtain that, for a constant ,

for , hence the result.

?refname?

- [1] Anderson, T. W. The statistical analysis of time series. John Wiley & Sons, 1971.

- [2] Andrews, D. Laws of large numbers for dependent non-identically distributed random variables. Econometric Theory 4, 3 (1988), 458–467.

- [3] Aue, A., Berkes, I., and Horváth, L. Strong approximation for the sums of squares of augmented GARCH sequences. Bernoulli 12, 4 (2006), 583–608.

- [4] Bahadur, R. A note on quantiles in large samples. The Annals of Mathematical Statistics 37, 3 (1966), 577–580.

- [5] Berkes, I., Hörmann, S., and Horváth, L. The functional central limit theorem for a family of GARCH observations with applications. Statistics & Probability Letters 78, 16 (2008), 2725–2730.

- [6] Billingsley, P. Convergence of probability measures, 1st ed. John Wiley & Sons, 1968.

- [7] Bollerslev, T. Generalized autoregressive conditional heteroskedasticity. Journal of Econometrics 31, 3 (1986), 307–327.

- [8] Bollerslev, T. Glossary to ARCH (GARCH). CREATES Research Paper 49 (2008).

- [9] Borovkova, S., Burton, R., and Dehling, H. Limit theorems for functionals of mixing processes with applications to u-statistics and dimension estimation. Transactions of the American Mathematical Society 353, 11 (2001), 4261–4318.

- [10] Bougerol, P., and Picard, N. Stationarity of GARCH processes and of some nonnegative time series. Journal of econometrics 52, 1-2 (1992), 115–127.

- [11] Boussama, F. Ergodicité, mélange et estimation dans les modeles GARCH. PhD thesis, Université Paris 7, 1998.

- [12] Box, G. E., Jenkins, G. M., Reinsel, G. C., and Ljung, G. M. Time series analysis: forecasting and control. John Wiley & Sons, 2015.

- [13] Bradley, R. Basic properties of strong mixing conditions. A survey and some open questions. Probability surveys 2 (2005), 107–144.

- [14] Bräutigam, M., Dacorogna, M., and Kratz, M. Pro-cyclicality beyond business cycles. Mathematical Finance 33, 2 (2023), 308–341.

- [15] Brockwell, P. J., and Davis, R. A. Time series: theory and methods. Springer Science & Business Media, 1991.

- [16] Carrasco, M., and Chen, X. Mixing and moment properties of various GARCH and stochastic volatility models. Econometric Theory 18, 1 (2002), 17–39.

- [17] Davidson, J. Establishing conditions for the functional central limit theorem in nonlinear and semiparametric time series processes. Journal of Econometrics 106, 2 (2002), 243–269.

- [18] Davis, R., and Mikosch, T. The sample autocorrelations of heavy-tailed processes with applications to ARCH. The Annals of Statistics 26, 5 (1998), 2049–2080.

- [19] Davis, R. A., Mikosch, T., and Basrak, B. Sample ACF of multivariate stochastic recurrence equations with application to GARCH. Preprint, available at www. math. ku. dk/mikosch (1999).

- [20] De Jong, R. M., and Davidson, J. The functional central limit theorem and weak convergence to stochastic integrals I: weakly dependent processes. Econometric Theory 16, 5 (2000), 621–642.

- [21] Denker, M., and Keller, G. Rigorous statistical procedures for data from dynamical systems. Journal of Statistical Physics 44, 1-2 (1986), 67–93.

- [22] Ding, Z., Granger, C., and Engle, R. A long memory property of stock market returns and a new model. Journal of Empirical Finance 1, 1 (1993), 83–106.

- [23] Duan, J. Augmented GARCH (p, q) process and its diffusion limit. Journal of Econometrics 79, 1 (1997), 97–127.

- [24] Engle, R. Autoregressive conditional heteroscedasticity with estimates of the variance of united kingdom inflation. Econometrica: Journal of the Econometric Society 50, 4 (1982), 987–1007.

- [25] Engle, R., and Ng, V. Measuring and testing the impact of news on volatility. The Journal of Finance 48, 5 (1993), 1749–1778.

- [26] Geweke, J. Modeling the persistence of conditional variances: a comment. Econometric Reviews 5 (1986), 57–61.

- [27] Giot, P., and Laurent, S. Modelling daily value-at-risk using realized volatility and ARCH type models. Journal of empirical finance 11, 3 (2004), 379–398.

- [28] Giraitis, L., Leipus, R., and Surgailis, D. Recent advances in ARCH modelling. In Long Memory in Economics, G. Teyssière and A. Kirman, Eds. Springer, 2007, pp. 3–38.

- [29] Glosten, L., Jagannathan, R., and Runkle, D. On the relation between the expected value and the volatility of the nominal excess return on stocks. The Journal of Finance 48, 5 (1993), 1779–1801.

- [30] Hesse, C. A Bahadur-type representation for empirical quantiles of a large class of stationary, possibly infinite-variance, linear processes. The Annals of Statistics (1990), 1188–1202.

- [31] Higgins, M., and Bera, A. A class of nonlinear ARCH models. International Economic Review 33, 1 (1992), 137–158.

- [32] Hoga, Y. Confidence intervals for conditional tail risk measures in arma–garch models. Journal of Business & Economic Statistics 37, 4 (2019), 613–624.

- [33] Holan, S. H., Lund, R., and Davis, G. The ARMA alphabet soup: A tour of ARMA model variants. Statistics Surveys 4 (2010), 232–274.

- [34] Hörmann, S. Augmented GARCH sequences: Dependence structure and asymptotics. Bernoulli 14, 2 (2008), 543–561.

- [35] Horváth, L., and Kokoszka, P. Sample autocovariances of long-memory time series. Bernoulli 14, 2 (2008), 405–418.

- [36] Ibragimov, I., and Linnik, Y. Independent and stationary sequences of random variables. Wolters, Noordhoff Pub., 1971.

- [37] Ibragimov, I. A. Some limit theorems for stationary processes. Theory of Probability & Its Applications 7, 4 (1962), 349–382.

- [38] Jeon, J., and Taylor, J. W. Using CAViaR models with implied volatility for value-at-risk estimation. Journal of Forecasting 32, 1 (2013), 62–74.

- [39] Kulik, R., and Soulier, P. Limit theorems for long-memory stochastic volatility models with infinite variance: partial sums and sample covariances. Advances in Applied Probability 44, 4 (2012), 1113–1141.

- [40] Lee, O. Functional central limit theorems for augmented GARCH (p, q) and FIGARCH processes. Journal of the Korean Statistical Society 43, 3 (2014), 393–401.

- [41] Lehmann, E. Elements of Large-Sample Theory. Springer Science & Business Media, 1999.

- [42] Lindner, A. Stationarity, mixing, distributional properties and moments of GARCH (p, q)–processes. In Handbook of financial time series, T. Mikosch, J. Kreiß, R. Davis, and T. Andersen, Eds. Springer, 2009, pp. 43–69.

- [43] Ling, S., and Li, W. K. On fractionally integrated autoregressive moving-average time series models with conditional heteroscedasticity. Journal of the American Statistical Association 92, 439 (1997), 1184–1194.

- [44] Ling, S., and Li, W. K. Limiting distributions of maximum likelihood estimators for unstable autoregressive moving-average time series with general autoregressive heteroscedastic errors. Annals of Statistics 26, 1 (1998), 84–125.

- [45] Ling, S., and McAleer, M. Necessary and sufficient moment conditions for the GARCH (r, s) and asymmetric power GARCH (r, s) models. Econometric theory (2002), 722–729.

- [46] Ling, S., and McAleer, M. Asymptotic theory for a vector ARMA-GARCH model. Econometric theory (2003), 280–310.

- [47] Milhøj, A. A multiplicative parameterization of ARCH models. Working Paper (1987).

- [48] Nelson, D. Conditional heteroskedasticity in asset returns: A new approach. Econometrica: Journal of the Econometric Society 59, 2 (1991), 347–370.

- [49] Pantula, S. Modeling the persistence of conditional variances: A comment. Econometric Reviews 5 (1986), 79–97.

- [50] Qiu, J., and Lin, Z. The functional central limit theorem for linear processes with strong near-epoch dependent innovations. Journal of mathematical analysis and applications 376, 1 (2011), 373–382.

- [51] Schwert, G. Why does stock market volatility change over time? The Journal of Finance 44, 5 (1989), 1115–1153.

- [52] Segers, J. On the asymptotic distribution of the mean absolute deviation about the mean. arXiv:1406.4151 (2014).

- [53] Sen, P. K. Asymptotic normality of sample quantiles for m-dependent processes. The annals of mathematical statistics (1968), 1724–1730.

- [54] Sen, P. K. On the Bahadur representation of sample quantiles for sequences of -mixing random variables. Journal of Multivariate analysis 2, 1 (1972), 77–95.

- [55] Song, J., and Kang, J. Parameter change tests for arma–garch models. Computational Statistics & Data Analysis 121 (2018), 41–56.

- [56] Spierdijk, L. Confidence intervals for arma–garch value-at-risk: The case of heavy tails and skewness. Computational statistics & data analysis 100 (2016), 545–559.

- [57] Taylor, S. Modelling financial time series. Wiley, New York, 1986.

- [58] Van der Vaart, A. Asymptotic statistics. Cambridge University Press, 1998.

- [59] Weiss, A. A. ARMA models with ARCH errors. Journal of time series analysis 5, 2 (1984), 129–143.

- [60] Weiss, A. A. Asymptotic theory for ARCH models: estimation and testing. Econometric theory (1986), 107–131.

- [61] Wendler, M. Bahadur representation for u-quantiles of dependent data. Journal of Multivariate Analysis 102, 6 (2011), 1064–1079.

- [62] Wendler, M. Empirical U-Quantiles of Dependent Data. PhD thesis, Ruhr-Universität Bochum, 2011.

- [63] Wu, W. B. On the Bahadur representation of sample quantiles for dependent sequences. The Annals of Statistics 33, 4 (2005), 1934–1963.

- [64] Wu, Y., Yu, W., and Wang, X. The bahadur representation of sample quantiles for ?-mixing random variables and its application. Statistics 55, 2 (2021), 426–444.

- [65] Zakoian, J.-M. Threshold heteroskedastic models. Journal of Economic Dynamics and Control 18, 5 (1994), 931–955.

- [66] Zumbach, G. Correlations of the realized volatilities with the centered volatility increment. http://www.finanscopics.com/figuresPage.php?figCode=corr_vol_r_VsDV0, 2012. [Online; accessed 01-September-2023].

- [67] Zumbach, G. Discrete Time Series, Processes, and Applications in Finance. Springer Science & Business Media, 2012.

?appendixname? A Examples of Augmented GARCH models

In this section we review some well-known examples of augmented GARCH(,) processes and discuss which conditions these models need to fulfil for the bivariate asymptotics of Corollary 10 to be valid, in view of applications.

Recalling the specific conditions mentioned in Corollary 10, note that the continuity and differentiability conditions, , , each at , and at for , remain the same for the whole class of augmented GARCH processes. Contrary to that, the moment condition imposes different restrictions on the parameters of the underlying process, depending on the given augmented GARCH(, ) process. To our knowledge, there exists no general result for the class of augmented GARCH(, ) describing the necessary conditions of the process for a given moment to exist: E.g. in [34] the case of augmented GARCH(,) processes is considered, see Corollary 1 and Proposition 1 therein, and in [45] the GARCH() and APGARCH(,), see Theorem 2.1 and Theorem 3.2 therein. Sufficient but not necessary conditions, which are easier to verify in practice, follow from results in [28] as mentioned in [42], Proposition 2.

We focus here on solely explaining how, depending on the specifications (4) and (5) of the process, the conditions, for polynomial GARCH or for exponential GARCH respectively, translate differently in the various examples.

For this, we introduce in Table 1 a non-exhaustive selection of different augmented GARCH(,) models, providing for each the corresponding volatility equation, (5), and the specifications of the functions and . We consider 10 models that belong to the group of polynomial GARCH () and two examples of exponential GARCH (). As the nesting of the different models presented is not obvious, we give a schematic overview in Figure 1. An explanation of the abbreviations and authors of the different models can be found at the end of Appendix A.

| standard formula for | corresponding specifications of in (5) | ||

|---|---|---|---|

| Polynomial GARCH | |||

| APGARCH family | |||

| AGARCH | |||

| GJR-GARCH | |||

| GARCH | |||

| ARCH | |||

| TGARCH | |||

| TSGARCH | |||

| PGARCH | |||

| VGARCH | and | ||

| NGARCH | and | ||

| Exponential GARCH | and | ||

| MGARCH | |||

| EGARCH |

Note that in Table 1 the specification of is the same for the whole APGARCH family (only the change), whereas for the two exponential GARCH models, it is the reverse. The general restrictions on the parameters are as follows: for , . Further, the parameters in the GJR-GARCH (TGARCH) are denoted with an asterix (with a plus or minus) as they are not the same as in the other models.

In Tables 2 and 3, we present how the conditions or translate for each model. Table 2 treats the specific case of an augmented GARCH(,) process with , whereas Table 3 treats the general case for arbitrary .

In Table 2 we consider in the first column the conditions for the general -th absolute centred sample moment, . We also specifically look at the standard cases of the sample MAD () and the sample variance () as measure of dispersion estimators respectively, presented in the second and third column.

For the selected polynomial GARCH models, the requirement in condition will always be fulfilled. Thus, we only need to analyse the condition .

| augmented | |||

|---|---|---|---|

| GARCH (, ) | |||

| APGARCH | |||

| AGARCH | |||

| GJR-GARCH | |||

| GARCH | |||

| ARCH | |||

| TGARCH | |||

| TSGARCH | |||

| PGARCH | |||

| VGARCH | for any : | ||

| NGARCH | |||

| MGARCH | for any : and | ||

| EGARCH | for any : and | ||

Lastly, we present in Table 3 how the conditions or respectively translate for those augmented GARCH(,) processes - this is the generalization of Table 2. As, in contrast to Table 2, we do not gain any insight by considering the choices of or , we only present the general case, .

When , we need to consider coefficients for . In case they are not defined, we set them equal to 0.

| augmented | |

|---|---|

| GARCH (,) | |

| APGARCH | |

| AGARCH | |

| GJR-GARCH | |

| GARCH | |

| ARCH | |

| TGARCH | |

| TSGARCH | |

| PGARCH | |

| VGARCH | |

| NGARCH | |

| MGARCH | and |

| EGARCH | and |

Note that, in Table 2 (and also Table 3), the restrictions on the parameter space, given by or respectively, are the same as the conditions for univariate FCLTs of the process itself (see [5], [34]). For , they coincide with the conditions for e.g. -mixing with exponential decay (see [16]).

Details on the Processes -

In the following we give an overview over the acronyms, authors and relation to each other of the augmented GARCH processes. The restrictions on the parameters, if not specified differently, are for , .

-

•

APGARCH: Asymmetric power GARCH, introduced by Ding et al. in [22]. One of the most general polynomial GARCH models.

-

•

AGARCH: Asymmetric GARCH, defined also by Ding et al. in [22], choosing in APGARCH.

-

•

GJR-GARCH: This process is named after its three authors Glosten, Jaganathan and Runkle and was defined by them in [29]. For the parameters it holds that and .

-

•

GARCH: Choosing all in the AGARCH model (or in the GJR-GARCH), gives back the well-known GARCH(,) process by Bollerslev in [7].

-

•

ARCH: Introduced by Engle in [24]. We recover it by setting all .

-

•

TGARCH: Choosing in the APGARCH model leads us the so called threshold GARCH (TGARCH) by Zakoian in [65]. For the parameters it holds that .

- •

-

•

PGARCH: Another subfamily of the APGARCH processes is the Power-GARCH (PGARCH), also called sometimes NGARCH (i.e. non-linear GARCH) due to Higgins and Bera in [31].

-

•

VGARCH: The volatility GARCH (VGARCH) model by Engle and Ng in [25] is also a polynomial GARCH model but is not part of the APGARCH family.

-

•

NGARCH: This non-linear asymmetric model is due to Engle and Ng in [25], and sometimes also called NAGARCH.

- •

-

•

EGARCH: This model is called exponential GARCH, introduced by Nelson in [48].

Then we give a schematic overview of the nesting of the different models in Figure 1.

?appendixname? B FCLT and CLTs used in the proofs

For the sake of completeness and to ease the understanding within the proofs, we cite here the multivariate FCLT as well as the two univariate CLTs to which we resort to.

B.1 Univariate FCLTs

Let us first state the FCLT for functionals of -mixing processes.

Theorem 22 (Theorem 21.1 in [6]).

Suppose that the process is -mixing and its mixing rate satisfies .

Then, for a given function , consider the process and assume it to have mean 0 and finite variance. Suppose further, there exist random variables of the form such that . Then the series

converges absolutely.

If , then it holds:

A corresponding FCLT for functionals of strong-mixing processes is the following:

Theorem 23 (Theorem 18.6.2 in [36]).

Suppose that the process is strong mixing with mixing rate .

Then, for a given function , consider the process and assume it to have mean 0 and finite variance.

Suppose that, for some ,

, and

. Then the series

converges.

If , then it holds:

B.2 Multivariate FCLTs

We state here the multivariate FCLT that we used in the proof of Theorem 3. It comes from [20] (Theorem 3.1)/ [17] (a multivariate version of Theorem 1.2), but adapted to our needs, as explained in Remark 25.

Theorem 24.

Consider a d-dimensional stationary random process where each of the components is an -NED process with constants , with respect to the same (univariate) process , which is either -mixing of order for , , or -mixing of order for , - where, for this choice of , it must hold that . Further, assume that , , as .

Then, the series converges (coordinatewise) absolutely and a FCLT holds for :

where the convergence takes place in the d-dimensional Skorohod space and is a d-dimensional Brownian motion with covariance matrix , i.e. it has mean 0 and

.

Remark 25.

The conditions of our multivariate FCLT are similar to those stated in the univariate FCLT of [17] (see Theorem 1.2 therein). Their result is not restricted to stationary processes, but, for us, this is sufficient. This is why our conditions, by stationarity, will hold uniformly in . It is also the reason why we do not need, in the definition of -NED, a constant depending on the time of the process. Theorem 1.2 of [17] is a special case of Theorem 3.1 of [20], and this latter theorem has a multivariate equivalent presented in Theorem 3.2 in [20]. Combining these two ideas, we present in Theorem 24 a special case of Theorem 3.2. of [20].