A simple mechanism leading to first-order phase transitions in a model of tax evasion

Abstract

In this work we study a dynamics of tax evasion. We considered a fully-connected population divided in three compartments, namely honest tax payers, tax evaders and susceptibles, a class that is composed by honest tax payers that can become evaders. We consider a contagion model where the transitions among the compartments are governed by probabilities. Such probabilities represent the possible interactions among the indiviudals, as well as the government’s fiscalization. We show by analytical and numerical calculations that the emergence of tax evaders in the population is associated with an active-absorbing nonequilibrium first-order phase transition. In the absorbing phase only honest tax payers survive in the steady states of the model, and we observe a coexistence of the three subpopulations in the active phase.

keywords:

Dynamics of social systems, Econophysics, Computer simulations, Complex NetworksPACS Nos.: 05.10.-a, 05.70.Jk, 87.23.Ge, 89.75.Fb

1 Introduction

Socioeconomic problems have been recently the foccus of sociophysics researchers [1, 2]. The basic approach is usually dominated by agent-based models, which allow us to understand the emergente collective phenomena of such systems. Among the studied problems, one of great interest is tax evasion dynamics, which is interesting from the practical point of view because tax evasion remains to be a major predicament facing governments [3, 4, 5].

Economists studied models of tax evasion during several years [6, 7, 8, 9, 10, 11, 12, 13], and more recently physicists also became interested in the subject [14, 15, 16, 17, 18, 19, 20] (for recent reviews, see [3, 4, 21, 22]). The authors in [13] discussed that the management of tax arrears it’s not only the performance of the tax authorities of their duties to collect the debt, but also the formation of the system of economic relations that arise between the state (local government), business entities and individuals regarding the payment of fees. Regarding the Russian federation, a recent work verified that although the number of the on-site tax inspections is currently being reduced, it does not affect their performance efficiency as the tax control authorities select the auditees more thoroughly [23]. Microscopic models were recently developed. The authors in [20, 24] considered a system of nonlinear differential equations of the kinetic discretized Boltzmann type involving transition probabilities, and combined a tax system with a redistribution process. They showed that a inequality index (the Gini index) of the total population increases when the evasion level is higher, but does not depend significantly on the evasion spread.

Physics models based on the Ising model were proposed to analyze tax evasion dynamics [14, 15, 16]. These works analyze how enforcement rules, as well as agent-agent interactions can be combined to reduce tax evasion and tax evasion fluctuations. As an extension of such works, a recent paper proposed a diluted Ising model with competing interactions to model tax evasion dynamics [25]. The authors considered social variables such as the audit period and its effects over the percentage of evasion, in order to analyze the behavior of tax evasion in Colombia. They found that the magnetic field, representing general government policies, as well as the audit probability, must be complementary if a reduction in tax evasion is desired. Local temperatures and local magnetic fields were also considered in another work [18].

The author in [19] studied a more general spin-like model, considering a three-state model. Based on a kinetic exchange opinion model [26] together with the enforcement rules of the Zaklan model, it was found that below the critical point of the opinion dynamics the compliance is high, and the punishment rules have a small effect in the population. On the other hand, above the critical point of the opinion dynamics the tax evasion can be considerably reduced by the enforcement mechanism [19]. Considering a contagion epidemic-like model, a recent work [27] showed that the emergence of tax evaders in the population can be associated with an active-absorbing nonequilibrium continuous phase transition.

Rui Barbosa, a Brazilian diplomat, writer, jurist, and politician, said “To see triumph the nullities, see prosper the dishonor, see grow the injustice, to see agglomerate powers in the hands of the wicked, the man comes to discourage the virtue, laughing at the honor, ashamed to be honest” [28]. This is specially true in countries like Brazil, where there is a weak fiscalization and/or light punishment [29, 30]. This implies that social pressure of individuals’ contacts play an important role in the propagation of social norms, as discussed in recent works [31, 32].

In this work we extend a recent three-state model to analyze tax evasion dynamics. For this purpose, we considered mechanisms of social pressure and enforcement regime. Opinion dynamics models were considered recently to study the addoption of right/wrong behavior in societies [31, 32]. Here we adopt a distinct approach, considering an epidemic-like model, where the transition among the classes or compartments are ruled by probabilities [33, 34], to theoretically study the specific problem of tax evasion. We will see that the emergence of tax evaders in the population can be associated with a first-order nonequilibrium phase transition. The emergence of phase transitons in not usual in models of tax evasion [14, 15, 16, 17, 18, 19, 24, 25, 27]. In addition, to the best of our knowledge it is the first time that a first-order transition is observed in such models.

This work is organized as follows. In section 2 we define the model’s rules and the individuals presented in the population. After, in section 3 we discuss our analytical and numerical results. Finally, in section 4 we present our conclusions and final remarks.

2 Model

We considered a population of agents. Each individual () can be in one of three possible states at a given time step , represented by , and . In other words, represents the number of individuals in a given state, with . The state represents a honest tax payer, i.e., an individual 100 convinced of his/her honesty, who does not consider evasion. He/she is either habitually compliant or he/she is a recent evader who has become honest as a result of enforcement efforts or social norms. On the other hand, the state represents a cheater, i.e, an individual who is an evading tax payer. Whether a tax payer continues to evade depends on both enforcement and the effect of social interactions. Finally, the third state consists of taxpayers who are dissatisfied with the tax system (perhaps as a result of seeing others evade without being punished). These taxpayers are not actively evading, but they might if the perceived benefits of doing so exceed the perceived costs. For this group, evasion is an option, and so we classify them as susceptibles, i.e., they are susceptible to become evaders [10, 19, 27].

Following the model studied in [27], we consider an extra social interaction, namely interactions among honest tax payers and susceptible individuals . Due to social pressure of individuals, the susceptible agents hesitate and come back to the compartment. This new transition occurrs with probability . In addition, we keep the previous two social interactions and the enforcement regime [27]. The possible transitions are as follows:

| (1) | |||||

| (2) | |||||

| (3) | |||||

| (4) | |||||

| (5) |

As discussed in [27], Eq. (1) represents an encounter of a honest agent with an evader . In this case, with probability the honest individual becomes susceptible . The parameter can be viewed as the social pressure of evaders over honests. The transition occurrs to the susceptible state, i.e., we consider that the transition from honest to evader is not abrupt, as it is common in tax evasion models [14, 15, 16, 20, 24, 25]. The following transition, Eq. (2) represents a spontaneous transition from the susceptible state to the evader state . The enforcement affects the behavior of a susceptible individual through its effect on the perceived costs of evasion (cost-benefit analysis). Thus, we assume that some susceptible tax payers will perceive that the benefits of evasion exceed the costs of evasion in each period, leading these individuals to evade. This is represented by the probability . As discussed above, we consider that the transition from honest to evader is not abrupt: the honest individual first becomes susceptible and after he might become evader.

The new interaction rule is represented by Eq. (3). The susceptible agent can be persuaded by a honest one and hesitate to not become an evader . In such a case, the susceptible agent returns to the honest compartment with probability .

Eq. (4) represents the opposite transition in comparison with Eq. (1). In this case, it represents an encounter of an evader agent with a honest tax payer . In this case, with probability the evader agent becomes honest. The parameter can be viewed as the social pressure of honests over evaders. We can also consider that this last transition occurs to the state , but for simplicity we consider that the evaders go directly to the honest compartment.

Finnaly, Eq. (5) represents another enforcement effect. We consider that evaders become compliant after they are audited or when their perceptions regarding the costs and benefits of evasion change, either through experience or changing economic conditions [10]. This transition occurs with probability , that can be viewed as a measure of the efficiency of the government’s fiscalization. As in the previous case, one can also consider that some evaders might not be rehabilitated when they are audited, remaining susceptible rather than becoming honest, but for simplicity we will not consider those additional transitions.

In the next section we discuss the analytical and numerical results. We will show that the new mechanism represented by the hesitance of susceptible individuals to become evaders , under the influence of honest agents , leads to the emergence of a discontinuous nonequilibrium phase transition, which is absent for the special case where only continuous phase transitions were observed [27].

3 Results

In this section we consider the model on a fully-connected graph. Considering the densities of each state, namely (), we can write master equations for each density as follows:

| (6) | |||||

| (7) | |||||

| (8) |

where now , and denote the fractions of honest, susceptible and tax evader individuals, respectively. In addition, we also have the normalization condition

| (9) |

that is valid at each time step . For we recover the model strudied in [27].

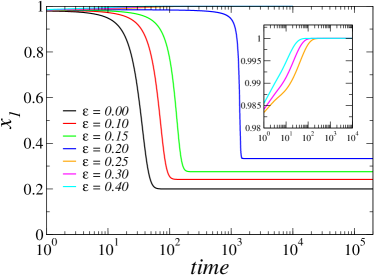

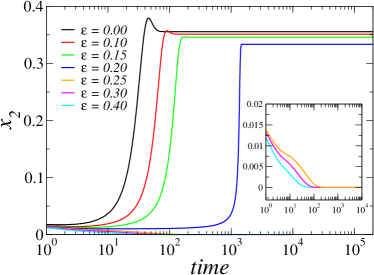

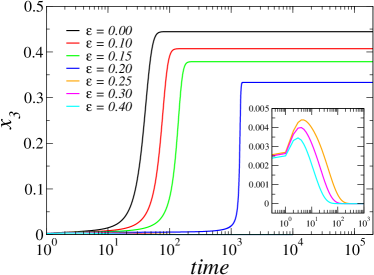

One can start analyzing the time evolution of the three classes of individuals. For this purpose, we numerically integrated Eqs. (6), (7) and (8). As initial conditions, we considered , and . In Fig. 1 we exhibit results for the time evolution of the fractions and . As is the new parameter of the model, we fixed , , and and plot graphics for typical values of . One observe that for increasing values of the final (steady state) fractions of susceptibles and evaders decrease, and for some cases they reach the steady state values . On the other hand, the stationary fraction of honest tax payers increases for increasing values of , and for sufficient large we have . This suggests the existence of a absorbing state, since if all the individuals in the populations are honests, the system remains frozen (see the rules given by Eqs. (1) - (5)). In the next we will obtain such absorbing state analytically.

In the steady states () we have that the three time derivatives of Eqs. (6) - (8) are zero. In such a case, Eq. (7) gives us

| (10) |

In addition, from Eq. (8) we have

| (11) |

From Eqs. (10) and (11), we have two solutions. The first one is given by , which means that there is no evaders in the long-time limit. If this solutions is valid, from Eq. (10) or (11) we have that . Thus, from the normalization condition Eq. (9) we have . This solution represents the above-mentioned absorbing phase, since there are only honest tax payers in the population, and the dynamics become frozen. This same absorbing phase was observed in the case [27].

On the other hand, the second solution of Eqs. (10) and (11) gives us a second order polynomial for of the type , where

| (12) | |||||

| (13) | |||||

| (14) |

For the limiting case we have and we recover the simple solution obtained in [27], namely . For , the second order polynomial gives us two solutions given by

| (15) |

Numerically, we can verify that the physically acceptable solution is given by the plus signal in Eq. (15). Substituting the normalization condition written as in Eq. (11), we can obtain

| (16) |

Given the solution of Eq. (15) with the plus signal, the stationary fraction of tax evaders can be obtained from Eq. (16).

Looking for the two obtained solutions in Eq. (15), and remembering that is not the order parameter (that is ), we expect the jumps at the critical point from the absorbing state solution to the solution given by Eq. (15). In such a case, taking in Eq. (15), we obtain the critical point,

| (17) |

Notice that for the limiting case , Eq. (17) recovers the result obtained in Ref. [27]. The behavior of Eq. (15) is typical of first-order phase transitions, as observed for example in opinion dynamics models [35], ecological dynamics [36, 37] and quantum spin system with long-range interaction [38]. Thus, taking into account the solutions given by and Eq. (15), we expect that the fraction of honests presents a jump at the critical points given by Eq. (17). In such a case, the order parameter also presents a discontinuity at . Taking into account the two solutions for the order parameter , namely and the other given by Eq. (16), we expect to observe nonequilibrium first-order phase transitions in the model at the critical points , obtained in the terms of the models’ parameters and given by Eq. (17). For we have a phase where the three fractions and coexist. On the other hand, for , the valid solution is given by . In this case, we are talking about a first-order active-absorbing transition [39, 40] that separates a phase where the tax evaders disappear of the population in the long-time limit and the population is formed only by honests, from a phase where there is a finite fraction of evaders in the long time. The susceptible agents also survive in the active phase, and they disappear in the absorbing phase. To the best of our knowledge, it is the first time that an active-absorbing nonequilibrium phase transition is observed in models of tax evasion. However, such kind of transition was observed in a wide range of systems, for example coupled opinion-epidemic dynamics [41], one-dimensional long-range contact processes [42], Ziff-Gulari-Barshad (ZGB) model [43, 44], granular systems [45], opinion dynamics [46, 47], naming games [48, 49], symbiotic contact process [50] and majority-vote model [51], among others.

One can also estimate the limiting case above which there is no phase transition anymore. Taking in Eq. (17), we have

| (18) |

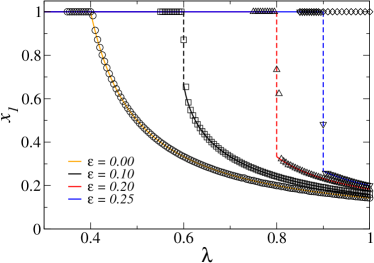

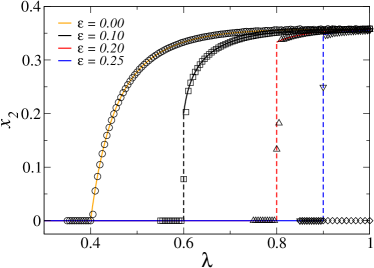

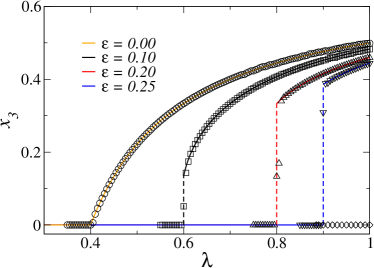

To test the above analytical results, we performed numerical simulations of the model in a fully-connected graph. In Fig. 2 we exhibit the stationary fractions and as functions of for typical values of . The fixed parameters are , and . The full lines are the analytical results for and given by Eqs. (15), (11) and (16), respectively, and the symbols were obtained from simulations with population size . For the simulations, the distance between two data points is , except for the case where , for better visualization (see the black diamonds in Fig. 2). The analytical and numerical results are in excellent agreement. The limiting case was obtained from the expressions of Ref. [27], and they are exhibited only for comparison with the cases where . As previous discussed, in the absence of the hesitance represented by the probability , the model undergoes a continuous phase transition. On the other hand, in the presence of the interaction among honests and susceptibles, the transition is of first-order type. Notice that, for the parameters considered in Fig. 2, we have from Eq. (18) . Thus, we expect that for the system does not undergoes a phase transition, which is exact we observe in Fig. 2 for (see the black diamonds).

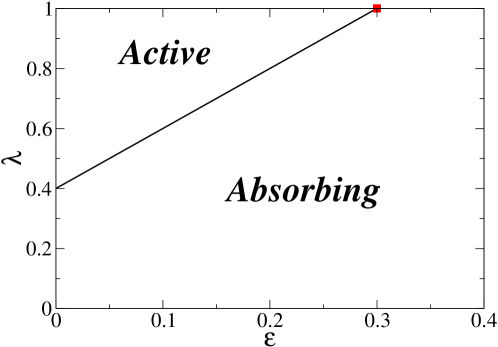

To summarize the results, we exhibit in Fig. 3 the phase diagram of the model in the plane vs for fixed parameters , and , separating the Absorbing and Active phases. The full (black) line is given by Eq. (17), and the (red) square represents the critical point given by Eq. (18), which represents the above-discussed limiting case.

4 Concluding remarks

In this work, we have studied the dynamics of tax evasion based on a contagion model. The model consists of three distinct compartments, namely honest tax payers, tax evaders and susceptibles, an intermediate compartment between honests and evaders. We considered a fully-connected population, and we introduce a new transition probability in the model of Ref. [27], that can be related to the hesitance of susceptible individuals to become evaders, due to social influence of honest tax payers.

In such a case, we derive the mean-field master equations that allow us to analyze the dynamics and the steady-state properties of the model. For the limiting case the model undergoes a continuous nonequilibrium phase transition from an active phase, where the three compartments coexist in the population, to an absborbing phase where all individuals are honests [27]. For the present case, our analytical and numerical results show that the introduction of only a new parameter, , leads the system to undergoes nonequilibrium first-order phase transitions at critical points that depend on the other four parameters of the model ( and ). In other words, the presence of the above-mentioned hesitance turns the continuous phase transition into a discontinuous one. Since it is not usual to observe even continuous phase transitions in models of tax evasion, the present model presents theoretical interest for the Statistical Physics and Complex Systems community.

We built a phase diagram of the model. Such phase diagram shows the existence of two states, namely the Absorbing state and the Active state. The nature of such phases are completely distinct: whereas in the Active phase we have the coexistence of the 3 populations (, and ), in the Absorbing phase only the honest tax payers () survive in the stationary states, leading to a frozen state that is characteristic of an Absorbing state [39]. In addition, the transition between those two states can be of continuous type (for ) or first-order type (for ).

As future extensions, it can be considered the inclusion of heterogeneities in the population, as the presence of special agents like contrarians individuals [47, 52, 53], zealots or sttuborn individuals [31, 32, 54, 55, 56] and opinion leaders [57, 58, 59]. The presence of distinct kinds of noises can also be considered [60, 61, 62], among others. The properties of this model in various lattices and networks would also be interesting to analyze.

Acknowledgments

The author acknowledges financial support from the Brazilian scientific funding agencies Conselho Nacional de Desenvolvimento Científico e Tecnológico (CNPq, grant number 310893/2020-8) and Fundação Carlos Chagas Filho de Amparo à Pesquisa do Estado do Rio de Janeiro (FAPERJ, grant number 203.217/2017).

References

- [1] Econophysics and Sociophysics: Trends and Perspectives, edited by B. K. Chakrabarti, A. Chakraborti and A. Chatterjee (Wiley-VCH, Berlin, 2006).

- [2] D. Stauffer, S. Moss de Oliveira, P. M. C. de Oliveira, J. S. Sá Martins, Biology, Sociology, Geology by Computational Physicists (Elsevier, Amsterdam, 2006).

- [3] K. M. Bloomquist, A Comparison of Agent-Based Models of Income Tax Evasion, Soc. Sci. Comput. Rev. 24, 411 (2006).

- [4] M. Pickhardt, A. Prinz, Behavioral dynamics of tax evasion - A survey, J. Econ. Psychol. 40, 1 (2013).

- [5] J. Andreoni, B. Erard, J. Feinstein, Tax compliance, J. of Economic Literature 36, 818 (1998).

- [6] S. Gachter, “Moral Judgments in Social Dilemmas: How Bad is Free Riding?” Discussion Papers 2006-03 CeDEx, University of Nottingham, 2006.

- [7] B. S. Frey, B. Togler, Managing Motivation, Organization and Governance, IEW-Working Papers 286, Institute for Empirical Research in Economics, University of Zurich, 2006.

- [8] H. Follmer, Random economies with many interacting agents, J. Math. Econ. 1, 51 (1974).

- [9] J. Slemrod, Cheating Ourselves: The Economics of Tax Evasion, J. Econ. Perspect. 21, 25 (2007).

- [10] J. S. Davis, G. Hecht, J. D. Perkins, Social Behaviors Enforcement and Tax Compliance, Account. Rev. 78, 39 (2003).

- [11] M. Wenzel, The impact of outcome orientation and justice concerns on tax compliance: The role of taxpayers’ identity., J. Appl. Psychol. 87, 629 (2002).

- [12] C. Hood, Privatizing UK tax law enforcement?, Public Administration 64, 319 (1986).

- [13] S. V. Salmina, Y. M. Galimardanova, A. R. Khafizova, Tax Debt Individual Customers in the Russian Federation, Mediterranean Journal of Social Sciences, 5(24), 412 (2014), Retrieved from

- [14] G. Zaklan, F. Westerhoff, D. Stauffer, Analysing tax evasion dynamics via the Ising model, J. Econ. Interact. Coord. 4, 1 (2009).

- [15] G. Zaklan, F. W. S. Lima, F. Westerhoff, Controlling tax evasion fluctuations, Physica A 387, 5857 (2008).

- [16] F. W. S. Lima, G. Zaklan, A multi-agent-based approach to tax morale, Int. J. Mod. Phys. C 19, 1797 (2008).

- [17] T. Llaccer, F. J. Miguel, J. A. Nogueira, E. Tapia, An agent-based model of tax compliance: An application to the Spanish case, Adv. Complex Syst. 16, 1350007 (2013).

- [18] G. Seibold, M. Pickhardt, Lapse of time effects on tax evasion in an agent-based econophysics model, Physica A 392, 2079 (2013).

- [19] N. Crokidakis, A three-state kinetic agent-based model to analyze tax evasion dynamics, Physica A 414, 321 (2014).

- [20] M. J. Bertotti, G. Mondanese, Mathematical models describing the effects of different tax evasion behaviors, Journal of Economic Interaction and Coordination 13, 351 (2018).

- [21] S. Hokamp, L. Gulyás, M. Koehler, S. Wijesinghe, Agent-based modeling and tax evasion: Theory and application, Agent-based Modeling of Tax Evasion: Theoretical Aspects and Computational Simulations 2018, Wiley Online Library.

- [22] G. Seibold, From Spins to Agents: An Econophysics Approach to Tax Evasion, Agent-based Modeling of Tax Evasion: Theoretical Aspects and Computational Simulations, 315-336, Wiley Online Library, (2018).

- [23] S. V. Salmina, A. R. Khafizova, I. V. Salmin, Arrangement and Performance of On-Site Tax Auditing in the Russian Federation, Mediterranean Journal of Social Sciences, 6(3), 732 (2015), Retrieved from

- [24] M. L. Bertotti, G. Modanese, Microscopic models for the study of taxpayer audit effects, Int. J. Mod. Phys. C 27, 1650100 (2016).

- [25] J. Giraldo-Barreto, J. Restrepo, Tax evasion study in a society realized as a diluted Ising model with competing interactions, Physica A 582, 126264 (2021).

- [26] S. Biswas, A. Chatterjee, P. Sen, Disorder induced phase transition in kinetic models of opinion dynamics, Physica A 391, 3257 (2012).

- [27] R. M. Brum, N. Crokidakis, Dynamics of tax evasion through an epidemic-like model, Int. J. of Mod. Phys. C 28, 1750023 (2017).

- [28]

- [29] I. Utsumi, Tax Evasion in Brazil, available on-line at http://thebrazilbusiness.com /article/tax-evasion-in-brazil.

- [30] Introduction to Politics of the Developing World, Fifth Edition, edited by W. A. Joseph, M. Kesselman, J. Krieger (Wadsworth, Bostonm, 2010).

- [31] M. F. Laguna, G. Abramson, S. Risau-Gusman, J. R. Iglesias, Do the right thing, J. Stat. Mech. 2010, P03028 (2010).

- [32] M. F. Laguna, G. Abramson, J. R. Iglesias, Compelled to do the right thing, Eur. Phys. J. B 86, 202 (2013).

- [33] N. T. J. Bailey, The Mathematical Theory of Infectious Diseases and Its Applications (New York: Hafner Press, New York, 1975).

- [34] N. Crokidakis, S. M. D. Queirós, Probing into the effectiveness of self-isolation policies in epidemic control, J. Stat. Mech. 2012, P06003 (2012).

- [35] S. Biswas, Mean-field solutions of kinetic-exchange opinion models, Phys. Rev. E 84, 056106 (2011).

- [36] A. Windus, H. J. Jensen, Allee effects and extinction in a lattice model, Theor. Popul. Biol. 72, 459 (2007).

- [37] A. Windus, H. J. Jensen, Phase transitions in a lattice population model, J. Phys. A: Math. Theor. 40, 2287 (2007).

- [38] M. Jo, J. Um, B. Kahng Nonequilibrium phase transition in an open quantum spin system with long-range interaction, Phys. Rev. E 99, 032131 (2019).

- [39] J. Marro, R. Dickman, Nonequilibrium Phase Transitions in Lattice Models (Cambridge University Press, Cambridge, England, 1999).

- [40] H. Hinrichsen, Adv. Phys. 49 (2000) 815.

- [41] M. A Pires, A. L. Oestereich, N. Crokidakis, Sudden transitions in coupled opinion and epidemic dynamics with vaccination, J. Stat. Mech. 2018, 053407 (2018).

- [42] C. E. Fiore, M. J. de Oliveira, Robustness of first-order phase transitions in one-dimensional long-range contact processes, Phys. Rev. E 87, 042101 (2013).

- [43] M. M. de Oliveira, M. G. E. da Luz, C. E. Fiore, Generic finite size scaling for discontinuous nonequilibrium phase transitions into absorbing states, Phys. Rev. E 92, 062126 (2015).

- [44] M. M. de Oliveira, S. G. Alves, S. C. Ferreira, Continuous and discontinuous absorbing-state phase transitions on Voronoi-Delaunay random lattices, Phys. Rev. E 93, 012110 (2016).

- [45] B. Néel, I. Rondini, A. Turzillo, N. Mujica, R. Soto, Dynamics of a first-order transition to an absorbing state, Phys. Rev. E 89, 042206 (2014).

- [46] A. L. Oestereich, M. A. Pires, N. Crokidakis, Three-state opinion dynamics in modular networks, Phys. Rev. E 100, 032312 (2019).

- [47] J. P. Gambaro, N. Crokidakis, The influence of contrarians in the dynamics of opinion formation, Physica A 486 465 (2017).

- [48] N. Crokidakis, E. Brigatti, Discontinuous phase transition in an open-ended Naming Game, J. Stat. Mech. 2015, P01019 (2015).

- [49] M. A. Neto, E. Brigatti, Discontinuous transitions can survive to quenched disorder in a two-dimensional nonequilibrium system, Phys. Rev. E 101, 022112 (2020).

- [50] C. I. N. Sampaio Filho, T. B. dos Santos, N. A. M. Ara’ujo, H. A. Carmona, A. A. Moreira, J. S. Andrade, Jr., Symbiotic contact process: Phase transitions, hysteresis cycles, and bistability, Phys. Rev. E98, 062108 (2018).

- [51] H. Chen, C. Shen, H. Zhang, G. Li, Z. Hou, J. Kurths, First-order phase transition in a majority-vote model with inertia, Phys. Rev. E 95, 042304 (2017).

- [52] S. Galam, Contrarian deterministic effect: the hung elections scenario, Physica A 333, 453 (2004).

- [53] M. B. Gordon, M. F. Laguna, S. Gonçalves, J. R. Iglesias, Adoption of innovations with contrarian agents and repentance, Physica A 486, 192 (2017).

- [54] S. Galam, F. Jacobs, The role of inflexible minorities in the breaking of democratic opinion dynamics, Physica A 381, 366 (2007).

- [55] S. Galam, Sociophysics: a review of Galam models, Int. J. Mod. Phys. C 19, 409 (2008).

- [56] M. Mobilia, On the role of zealotry in the voter model, J. Stat. Mech. 2007, P08029 (2007).

- [57] N. Boccara, Models of opinion formation: Influence of opinion leaders, Int. J. Mod. Phys. C 19, 93 (2008).

- [58] M. Zhu, G. Xie, Leader’s opinion priority bounded confidence model for network opinion evolution, AIP Conference Proceedings 1864, 020060 (2017).

- [59] Q.-Hui Liu, F.-Mao Lu, Q. Zhang, M. Tang, T. Zhou, Impacts of opinion leaders on social contagions, Chaos 28, 053103 (2018).

- [60] M. S. de la Lama, I. G. Szendro, J. R. Iglesias, H. S. Wio, Van Kampen’s expansion approach in an opinion formation model, Eur. Phys. J. B 51, 435 (2006).

- [61] M. S. de la Lama, J. M. López, H. S. Wio, Spontaneous emergence of contrarian-like behaviour in an opinion spreading model, Europhys. Lett. 72, 851 (2005).

- [62] C. Anteneodo, N. Crokidakis, Symmetry breaking by heating in a continuous opinion model, Phys. Rev. E 95, 042308 (2017).