On Recovering the Best Rank- Approximation from Few Entries∗

Abstract

In this note, we investigate how well we can reconstruct the best rank- approximation of a large matrix from a small number of its entries. We show that even if a data matrix is of full rank and cannot be approximated well by a low-rank matrix, its best low-rank approximations may still be reliably computed or estimated from a small number of its entries. This is especially relevant from a statistical viewpoint: the best low-rank approximations to a data matrix are often of more interest than itself because they capture the more stable and oftentimes more reproducible properties of an otherwise complicated data-generating model. In particular, we investigate two agnostic approaches: the first is based on spectral truncation; and the second is a projected gradient descent based optimization procedure. We argue that, while the first approach is intuitive and reasonably effective, the latter has far superior performance in general. We show that the error depends on how close the matrix is to being of low rank. Both theoretical and numerical evidence is presented to demonstrate the effectiveness of the proposed approaches.

1 Introduction

Low-rank approximations and other related spectral methods are among the most fundamental and ubiquitous tools in data analysis. Their computational and statistical aspects have been studied extensively and are among the central themes in numerical analysis and multivariate statistics respectively. The classical approaches however face new challenges with massive data sets are being generated every day across diverse fields: gene expression analysis (see, e.g., Kluger et al., 2003), protein-to-protein interaction (see, e.g., Stelzl et al., 2005), MRI image analysis (see, e.g., Smith et al., 2004), and the analysis of large graphs and social networks (see, e.g., Clauset et al., 2004; Scott, 2017), to name a few. Scalable computation and valid statistical inferences in high dimensions for low-rank approximations are the subjects of fervent research interests in recent years.

Consider a data matrix . As Eckart-Young Theorem indicates, its best rank- approximation, denoted by hereafter, can be uniquely identified by its top singular values and their corresponding vectors, assuming that its th and th singular values are different for simplicity. From a statistical perspective, we are interested in how well properties of a data-generating model can be inferred from , be they principal components, statistical factors, empirical orthogonal functions, or else. Suppose that we are interested in estimating a parameter that can be represented by a matrix in the Frobenius norm . These analyses often tell us about the stochastic behavior of the “estimation error” . For example, if where ’s entries are independent variables, then so that is a consistent estimate of under the Frobenius norm whenever . Classical multivariate analysis has primarily focused on “thin” data matrices where (sample size) is large and (dimensionality or number of features) is small (see, e.g., Anderson, 2003). On the other hand, the emphasis of recent effort is on the so-called high dimensional paradigm where both and are large (see, e.g., Bai and Silverstein, 2010; Wainwright, 2019).

Similarly, from a computational perspective, tremendous progress has been made in the past couple of decades towards fast computation of low-rank approximations to when both and are large, and randomized algorithms have become increasingly popular for this purpose (see, e.g., Mahoney, 2011; Woodruff et al., 2014). The goal is to find an which may or may not be of rank that can approximate nearly as well as under suitable matrix norms. Typical guarantees, in terms of Frobenius norm, for instance, for the output from these algorithms take the form:

| (1.1) |

for a sufficiently small factor .

It is, however, worth noting a subtle distinction between these two perspectives. While from a computational point of view, we are interested in finding a “good” approximation to ; from a statistical viewpoint, the focus is often on itself rather than the original data matrix because captures the more stable and oftentimes more reproducible properties of an otherwise complicated data-generating model, even if the data matrix itself may not necessarily be of low rank. These two goals are closely connected yet could also be rather different. In particular, (1.1) cannot ensure that would inherit the nice statistical properties one may be able to establish for : unless can be well approximated by , (1.1) does not imply that is small so we may not be able to infer from (1.1) that is necessarily a “good” estimate of even if is known to be small. Consider, for example, the signal-plus-noise model discussed before. Recall that so that may be inconsistent even though is a consistent estimate of when at least for small s. Moreover, oftentimes has a rank much greater than and therefore unsuitable for situations where an exact rank- estimate is sought. Our work aims to fill in this gap between the two strands of fruitful research by investigating how well we can reconstruct from random sparsification of a general matrix , and therefore contributes to growing literature to unify both statistical and computational perspectives (see, e.g., Raskutti and Mahoney, 2016).

To facilitate the storage, communication, or manipulation of a large data matrix, one often approximates the original data matrices with a more manageable amount of sketches. See Mahoney (2011); Woodruff et al. (2014) for recent reviews. A popular idea behind many of these approaches is sparsification—creating a sparse matrix by zeroing out some entries of the original data matrix. Sparse sketching of a large data matrix not only reduces space complexity but also allows for efficient computations. See, e.g., Frieze et al. (2004); Arora et al. (2006); Achlioptas and McSherry (2007); Drineas et al. (2008); Boutsidis et al. (2009); Mahoney and Drineas (2009); Drineas and Zouzias (2011); Achlioptas et al. (2013); Krishnamurthy and Singh (2013), among many others. In particular, we shall focus on matrix sparsification schemes that sample each entry of independently with a prescribed probability.

Denote by the indicator that the entry of is sampled and . Write where and we shall adopt the convention that in the rest of the paper. Many different sampling schemes have been developed in recent years so that the spectral error can be made small even with a tiny fraction of the entries sampled, e.g., . See, e.g., Arora et al. (2006); Achlioptas and McSherry (2007); Drineas and Zouzias (2011) among numerous others. Given the closeness of to , it is natural to consider estimating by the best rank- approximation of . We show that this is indeed a reasonable approach in light of the tight bounds controlled by under the spectral error. But more interestingly, we argue that for an arbitrary , by choosing s appropriately, we can derive a much better estimate of for all s. To this end, we introduce a sampling scheme and a companion rank- estimator of from . We show that can be bounded via the sampling error of instead of where . This leads to a significantly improved estimate of . In particular, if is of rank up to , then so that our estimator recovers exactly with high probability. This makes an immediate connection with the popular matrix completion problem where one seeks the exact recovery of a large matrix from partial observations of its entries (see, e.g., Candès and Recht, 2009; Gross, 2011; Recht, 2011)

Despite such a similarity, there are also significant distinctions between our results and those typical for matrix completion. For exact matrix completion, it is usually assumed that the rank of is small and known apriori, and that its singular vectors are incoherent so that each entry carries a similar amount of information. On the other hand, our approach does not make such stipulations and is generally applicable. As we shall show, remains a good estimate of even if is of full rank, and the incoherence condition can be done away with through carefully designed sampling schemes.

The rest of the paper is organized as follows. We first discuss the naïve approach to approximate by and show how it connects with existing results for matrix sparsification and completion in the next section. Section 3 introduces our sampling and estimation scheme for the improved approximation of . We complement the theoretical results with numerical experiments in Section 4 to further demonstrate the merits of our approach. Proofs of the main results are presented in Section 5 with more technical details relegated to the Appendix.

2 Naïve Estimate of

In the rest of the paper, we shall denote by , and the -th row, -th column, and entry of a matrix , respectively. Similarly, is the -th element of a vector . Following the convention, denotes the Frobenius norm, the spectral norm for a matrix and the norm for a vector, the element-wise infinity norm, the (vectorized) norm. We shall also write the inner product between two matrices as .

Most existing studies of the efficacy of sparsification algorithms focus on bounding the spectral error. For concreteness, consider a scheme that observes independently with probability

| (2.1) |

It is not hard to see that, from Chernoff’s bound, the total number of observed entries is within with high probability. Also, there exists a numerical constant such that

with probability at least , where (see, e.g., O’Rourke et al., 2018). In what follows, we shall use , and similarly , , etc., as generic numerical constants that may take different values at each appearance. Because

we have, under the above event,

In particular, whenever , we get

| (2.2) |

with probability at least . In light of such a bound on the spectral norm, it is natural to consider estimating by the respective best low-rank approximation of . The connection is made more precise by the following observation that links the closeness between and with the spectral error .

More specifically, for a matrix , its singular values are denoted by

Then we have

Lemma 1.

Let . If and , then there exists a numerical constant such that for any ,

Theorem 2.

Assume that each entry of is independently sampled from binomial trails with probability given by

If , then there exist numerical constants such that for any ,

with probability at least provided that

Theorem 2 justifies as a valid estimator of . It is worth noting that both the sample size requirement and error bound depend on the eigengap . This is inevitable since the eigengap characterizes the stability of best rank- approximation and in the extreme case where eigengap is 0, is not uniquely defined. We hereafter assume that .

It is instructive to revisit the signal-plus-noise model we discussed in the Introduction: where, to fix ideas, we assume that the signal is a rank-one square matrix with both and of unit length, and that the noise has independent entries. As noted before, it is of special interest to focus on the case when and there is a mismatch between the existing results from the statistical and computational sides. It is not hard to see that in this case and . In light of Theorem 2, this suggests that

Hence is consistent under the sample size requirement that . In particular, if for some , then the sample size requirement can be expressed as which means that a consistent estimate of can be obtained from a vanishing proportion () of the entries of .

Another interesting test case here is when is of rank up to so that . If, in addition, all entries of are of the same order so that , then it is not hard to see that

so that we have the following performance bound for as an approximation to under the Frobenius norm:

On the other hand, Theorem 2 indicates that

This immediately suggests that is a better estimate of by leveraging the fact that is small. Although this example shows the efficacy of as an estimate of , it also points to room for further improvement at least when is of low rank. In fact, with additional conditions, it may even be possible to recover a low-rank matrix exactly from !

For this to be possible, one usually assumes that is small and known apriori. Another essential concept is the so-called incoherence condition. Denote by its singular value decomposition. We say a rank- matrix is -incoherent if

Intuitively, the incoherence condition ensures that each entry of is of similar importance so that missing any one of them will not prevent us from being able to recover . Numerous tractable algorithms have been developed to reconstruct assuming that it is -incoherent and each of its entries is sampled independently with probability . See, e.g., Candès and Recht (2009); Candès and Tao (2010); Keshavan et al. (2010); Sun and Luo (2016) among many others. Interested readers are also referred to Davenport and Romberg (2016); Chen and Chi (2018) for a couple of recent surveys. For example, a natural approach is to reconstruct by the solution to

In particular, results from the recent work of Chen et al. (2020) indicate that we can recover exactly this way, with high probability, if

where is the condition number of .

These results immediately suggest that we can do even better than , albeit under additional assumptions. But can we do better than in general? Especially, can we do away with the incoherence assumption and the need to know apriori? We shall now argue that the answer is indeed affirmative.

3 Improved Estimate of

There are two main ingredients to our approach: sparsification with carefully chosen sampling probabilities to remove the need for incoherence; and an agnostic procedure based on projected gradient descent to estimate for any .

The fact that incoherence is closely related to the uniform sampling was noted first by Chen et al. (2015). They observed that a rank- matrix could be recovered exactly without the incoherence condition by taking

The difficulty of course is that it requires that be of rank . Nonetheless, motivated by the observation that

and

we shall consider sampling with probability

| (3.1) |

Compared with (2.1), we essentially replaced with which plays a similar role as when is indeed of rank . Unlike the factor , however, our choice of does not depend on . This is critical in allowing us to estimate for any from the sampled entries.

We shall now describe how to reconstruct from . Our approach is similar in spirit to Ge et al. (2017) and Chen et al. (2020). See also Jain and Kar (2017). Recall that is the solution to

It is clear by construction

so that we can consider minimizing . Any matrix with rank up to can be written as for some and so that this is equivalent to minimizing over the couple . However, decomposition is not unique. To overcome such an identifiable issue, we shall consider estimating by the solution to

| (3.2) |

where

and is a tuning parameter to be specified later.

The second term on the right-hand side of (3.2) forces so that if then and . Note that

When to be close to , then

so that the constraint on , and similarly that on , becomes inactive at least for a sufficiently small .

The objective function in (3.2) is non-convex jointly over . Nonetheless, it is natural to solve it by projected gradient descent with a good initialization. To this end, let be the projection on the convex set , that is

and

The intuition behind our approach is as follows. Write . In light of the discussion from the previous subsection, we may be able to exactly recover from . However, what we have is , with an extra term , and we now hope to be able to control the error bound for by the spectral error . The main advantage of our scheme is that we have tighter control of the perturbation than used in Theorem 2. Denote by

and

We have

Lemma 3.

Assume that each entry of is independently sampled from binomial trails with probability given by (3.1). If , then there exist numerical constants , with probability at least , such that

| (3.3) |

Further, an upper bound of gives us

| (3.4) |

It is worth pointing out that the sampling probability, and consequently is determined by instead of . As a result, is not determined by alone and the error bound above depends also on properties of . Compared with (2.2), for sufficiently large , describes how much tighter control we can have for than . By definition, , this means concentrates around its mean more tightly than . We are now in the position to present our main theoretical guarantee which shows that the quality of recovery indeed rests upon the perturbation of , not .

To this end, write and denote by

where is its SVD. Due to rotation symmetry, the difference between ad can be measured by

We have

Theorem 4.

A few remarks follow immediately. A benchmark case is when is of low rank. More specifically if , then and . From Theorem 4 and (3.3),

which implies that and consequently as . It is worth pointing out that if , the in the above inequality can be replaced by . In other words, the exact recovery of can be achieved without either the incoherence condition or knowing the precise value of apriori. Furthermore, if the incoherence condition indeed holds, the sample size requirement from Theorem 4 is comparable to those typical in the matrix completion literature.

In general, Theorem 4 and (3.4) suggests that whenever ,

| (3.5) | |||||

for large enough . This is to be compared with the bound given by Theorem 2:

It is clear that the bound in (3.5) is smaller because

and

To gain further insights of the difference between the two estimates of , we shall now take a closer look at these factors.

For brevity, we shall assume for the discussion. Recall that . It is not hard to see that

If the entries of and are of similar order, then

Similarly, so that, from (3.5), there is more improvement over the naïve estimate when is close to being of rank .

On the other hand, it is instructive to consider the case when . In this case,

and on the other hand,

This implies that much better bound can be achieved by our approach as and increase.

4 Numerical Experiments

To complement the theoretical developments from the previous sections and further demonstrate the merits of our approach, we also conducted several sets of numerical experiments. In particular, we focused on several key operating characteristics of our method including the ability to recover low-rank matrices exactly; the impact of the target rank ; and the role of the eigengap . We consider estimating by the naïve estimate with generated according to (2.1), and by as the output from Algorithm 1 with generated according to (3.1). For a fair comparison, we adjusted of the sampling probability (2.1) (for naïve method) and (3.1) (for the improved estimate) to ensure that both methods sample the same number of entries on average. In our implementation of the projected gradient descent, was set to be . To accelerate the optimization, we used line search (the line_search function of scipy.optimize in Python) to determine the optimal stepsize. The stopping criterion was set to be . In what follows, we shall refer to the “relative error” as or , and the “spectral error” as or . All the results presented are based on 100 independent simulation runs.

In our first set of experiments, we set and generated as a low-rank matrix with additive noise . More specifically,

where is a Gaussian ensemble with entries independently sampled from the standard normal distribution, and ’s entries are independently from . The variance of is chosen such that .

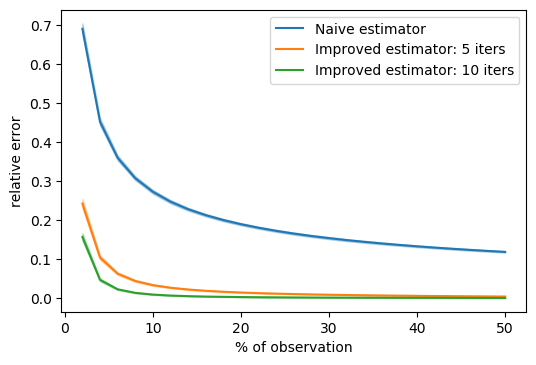

We began with the case where is of low rank. More specifically, we set and . In Figure 1, we plotted the relative error of and with the max number of iterations set to be or . It is clear that the relative error of both estimates decreases quickly with the increased sample size, as predicted by our theoretical results. But the relative error of decreases quickly to 0 while the error of the naïve estimate levels off around 0.15 even with as many as 50% of the entries observed. This highlights the ability of exact recovery for the improved approach as discussed in the previous section. Empirically, the projected gradient descent algorithm converges fairly quickly: there is little difference between setting the max number of iterations to 5 and 10, and 10 seems to suffice as a rule of thumb. In the rest of the experiments, we shall fix the max number of iterations at ten for consideration of computational speed.

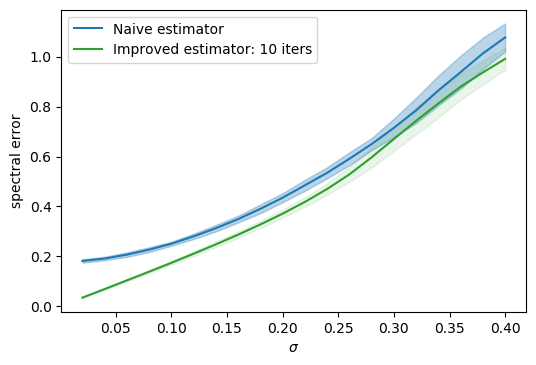

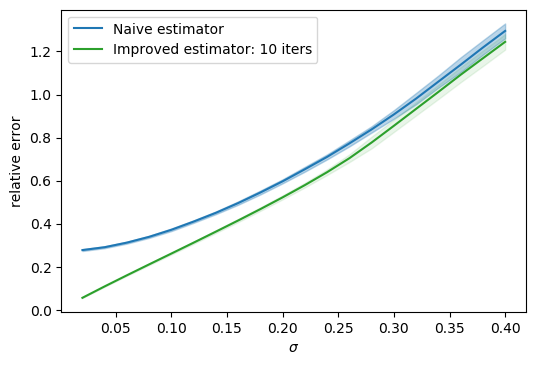

Next, we consider the case where is full rank yet we are primarily interested in its best rank approximations. To this end, we set . We adjusted of the sampling probability so that on average 10% of the entries were sampled. Figure 2 reports the mean and two-standard-deviance bands of both relative spectral and Frobenius errors from 100 simulation runs. A few interesting observations can be made. In particular, it is evident that is superior to the naïve estimator, in either error metric. Moreover, the naïve estimate is much more vulnerable to overshooting the “effective” rank of . Note that is “close” to being of rank . When consider estimating for , the performance of only deteriorates mildly with an increasing yet on the other hand, for the naïve estimate the impact is much more significant.

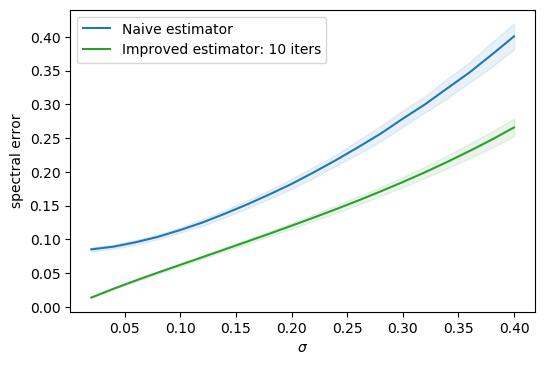

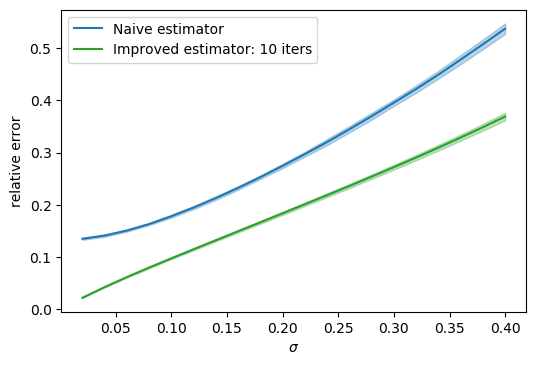

To further investigate the impact of the eigengap , we considered with varying from 0.02 to 0.4. Here serves as a proxy of the relative eigengap as . The results, again based upon 100 simulation runs, were summarized in Figure 3. It is interesting to note that the error increases as the relative eigengap decreases for both methods, but the impact on is minimal when compared with the naïve method, especially with increased sampling proportions.

In our final example, we computed both estimators to the waterfall image ***The original color version of image can be downloaded at https://media.cntraveler.com/photos/571945e380cf3e034f974b7d/master/pass/waterfalls-Seljalandsfoss-GettyImages-457381095.jpg.. The original image was converted into greyscale. The leading singular value of the matrix consisting of the pixel intensities accounts for 57.5% of the total variation. The best rank-10, rank-20, and rank-30 approximations explain 88.1%, 91.6%, and 93.0% of the variation respectively. We considered estimating the best rank- approximation to the image with , , and . For each , we set the max number of iteration to be 10 and sampled 10% pixels. Table 1 reports the mean and standard deviation of the “relative error” from 100 simulation runs. They again confirm that is a far more accurate estimate of .

| Target rank | Naïve Estimate | Improved Estimate |

|---|---|---|

| 5 | 0.290 (0.0017) | 0.118 (0.0036) |

| 10 | 0.432 (0.0012) | 0.154 (0.0018) |

| 20 | 0.609 (0.0009) | 0.174 (0.0012) |

| 30 | 0.738 (0.0009) | 0.184 (0.0010) |

To facilitate visual comparison between the improved and naïve methods, we now focus on the best rank- approximation of the image as shown in panel (a) of Figure 4. We fixed in the sampling probabilities so that the expected sampling proportion is 40%. One typical realization of both estimates is given in Panels (b) and (c) of Figure 4. For this specific realization, has a relative error 0.11. This is to be compared with the naïve method which has a relative error 0.37, which again is in agreement with our theoretical findings.

5 Proofs

Proof of Lemma 1.

By definition,

Observe that

We get

where we replaced with in the first inequality. Recall that

By Cauchy-Schwartz inequality,

Therefore,

In the case when , we can take to yield

Now consider the case when . Taking yields

Observe that

We have

Let and be their respective singular value decomposition. Then

By Davis-Kahan-Wedin’s Theorems,

so that

This implies that

∎

Proof of Lemma 3.

The proof relies on the following concentration bound.

Lemma 5.

Let be a fixed matrix and each entry of is independently sampled from binomial trails with probability given by (3.1). Then there exists a numerical constant such that

with probability at least , where .

In particular, consider applying Lemma 5 to . It is not hard to see that

and

By definition of , we get

where we used the fact that and thus the first claim follows.

For the second claim, let be its singular value decomposition,

Hence,

This implies that

with probability at least . ∎

Proof of Theorem 4.

In the rest of the proof, we shall omit in for brevity. Let

We shall then write , and . Moreover, denote by

Our analysis relies on the follow two technical lemmas.

Lemma 6.

Assume that and such that

There exists a numerical constant such that, with probability at least , if

| (5.1) |

then

and otherwise,

provide that .

Lemma 6 verifies the so-called local descent condition from Chen and Wainwright (2015). It states that, if , will have an acute angle with and shows similar behavior to a convex function. It implies that if , then it is necessarily true that

so that, to bound , it suffices to do so for .

Lemma 7.

Under the conditions in Lemma 6, there exists a numerical constant such that

with probability at least provide .

We shall now use these lemmas to prove that for any

| (5.2) |

and

| (5.3) |

We shall do so by induction. In fact, when , it suffices to verify (5.2). In light of Lemma 3 and Lemma 1, we have

with probability at least provided that

Then, (5.2) follows immediately from Lemma 6 and Lemma 42 of Ge et al. (2017).

Now assume that (5.2) and (5.3) hold for , we show that the same is true for . We shall first verify (5.3). Because the projection is contractive, we have

where we used Lemma 7.

In light of above two inequalities, we have,

It is clear that (5.2) also continues to hold for in light of the inequality above and the Lemma 3. The first claim of Theorem 4 follows immediately.

The second claim also follows, in light of the following bound:

Lemma 8.

Under the assumptions of Theorem 4,

Proof of Lemma 6.

For brevity, we shall omit the subscript in what follows. Denote by . Observe that

and

Therefore,

| (5.7) | |||||

We now bound each of the term on the rightmost hand side to show that it can be lower bounded by .

Bounding (5.7):

The term (5.7) can be bounded in a similar way as Ge et al. (2016). However, since we are dealing with different instead of uniform sampling in Ge et al. (2016), new concentration inequalities are needed.

Denote by , , and

It is clear that

and

Thus, by Cauchy-Schwartz inequality

We shall make use of the following concentration inequalities:

Lemma 9.

In light of Lemma 9, we have

| (5.8) |

Bounding (5.7):

It is not hard to see that . Thus, by rewriting and , we have

where we used the result that is symmetric from Lemma 6 of Ge et al. (2017). The first term on the righthand side can be bounded by

where the last inequality follow from the fact that .

Bounding (5.7):

Observe that

| (5.9) |

The first term on the righthand side can be bounded by

where we made use of the facts that, for two arbitrary matrices and ,

Note that by definition and . This implies that

In summary, we have

Together, the bounds for (5.7), (5.7) and (5.7) imply that

Denote by

where we again used the result that is symmetric from Lemma 6 of Ge et al. (2017) and the fact that .

This implies

| (5.10) |

Note that

| (5.11) |

We get

In light of (5.11), if

| (5.13) |

then

Together with (5.13), we get

In light of (5), we have

The case when (5.13) does not hold can be handled in a similar fashion: since

tegother with (5), we have

∎

Proof of Lemma 7.

By Cauchy-Schwartz inequality, for any such that ,

| (5.14) | |||||

The first term of (5.14) can be bounded by

In the last line, we used the fact that and the Cauchy-Schwartz inequality. We shall need the following concentration inequality.

Lemma 10.

Assume that each entry of is independently sampled from binomial trails with probability given by (3.1). There exists a numerical constant such that, for any matrices ,

with probability at least provided that .

By Lemma 10

where we used the facts that

and

Here, we used the definition of ,

Similarly, we can bound the second term on the righthand side of (5.14) by

where we used the fact that

in the last inequality.

The last term of (5.14) can be bounded by

where we used the facts that

| (5.15) |

and same bound for due to symmetry.

In summary, we have

The claim then follows from a similar bound for . ∎

Appendix A Proofs of Lemmas

Proof of Lemma 5.

Note that

It is not hard to see that

A similar bound can be derived for . On the other hand,

An application of Theorem 4.9 of Latała et al. (2018) yields

∎

Proof of Lemma 8.

Proof of Lemma 9.

The first claim is a generalization of Theorem 4.1 from Candès and Recht (2009), and its proof follows a similar idea. Write its SVD and denote by and . We first bound , where

and is the orthogonal projection on . As shown by Candès and Recht (2009),

for an arbitrary matrix , and

| (A.1) |

where , or is the orthogonal projection onto the column space of , or , and is the -th standard basis.

Observe that

| (A.2) | |||||

It is easy to verify that , then

We can derive similar result for . Together with (A.1), we have

| (A.3) |

For any matrix , we have

It’s easy to verify that

by expanding and the fact that , are symmetric.

Therefore

Here, is a transformation from to , but we can view it as a linear transformation from to by vectorizing a matrix into a -dimensional vector. Actually, in the view of space,

where is vectorizing transformation.

Then we can apply matrix Bernstein inequality. We have

and notice that

we can always assume

Together with (A.3),

therefore,

| (A.4) |

Observe that

where we used (A.2) for the first and last inequality on the righthand side. Therefore,

Together with (A.4), by matrix Bernstein inequality,

| (A.5) |

with probability at least , provided that

Note that by definition,

Together with (A.5), we have

We now turn to the second claim. Denote by

two vectors and

a matrix. We can assume

as we only care those . It’s easy to verify that

and

where we used the fact that and . Same bound can be derived for .

Observe that

where we used the facts that

and, similarly, for the last inequality.

Together with the fact that

we get

provided

∎

Proof of Lemma 10.

Let’s first look at the case where and are vectors,

| (A.6) |

We shall first bound

| (A.7) |

Observe that

and

where we used the facts that and .

By Bernstein inequality,

with probability at least , provided that .

References

- Achlioptas and McSherry (2007) Dimitris Achlioptas and Frank McSherry. Fast computation of low-rank matrix approximations. Journal of the ACM (JACM), 54(2):9, 2007.

- Achlioptas et al. (2013) Dimitris Achlioptas, Zohar S Karnin, and Edo Liberty. Near-optimal entrywise sampling for data matrices. In Advances in Neural Information Processing Systems, pages 1565–1573, 2013.

- Anderson (2003) T.W. Anderson. An Introduction to Multivariate Statistical Analysis. Wiley Series in Probability and Statistics. Wiley, 2003. ISBN 9780471360919.

- Arora et al. (2006) Sanjeev Arora, Elad Hazan, and Satyen Kale. A fast random sampling algorithm for sparsifying matrices. In Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques, pages 272–279. Springer, 2006.

- Bai and Silverstein (2010) Zhidong Bai and Jack W Silverstein. Spectral analysis of large dimensional random matrices, volume 20. Springer, 2010.

- Boutsidis et al. (2009) Christos Boutsidis, Michael W Mahoney, and Petros Drineas. An improved approximation algorithm for the column subset selection problem. In Proceedings of the twentieth annual ACM-SIAM symposium on Discrete algorithms, pages 968–977. SIAM, 2009.

- Candès and Recht (2009) Emmanuel J Candès and Benjamin Recht. Exact matrix completion via convex optimization. Foundations of Computational mathematics, 9(6):717, 2009.

- Candès and Tao (2010) Emmanuel J Candès and Terence Tao. The power of convex relaxation: Near-optimal matrix completion. IEEE Transactions on Information Theory, 56(5):2053–2080, 2010.

- Chen and Chi (2018) Yudong Chen and Yuejie Chi. Harnessing structures in big data via guaranteed low-rank matrix estimation: Recent theory and fast algorithms via convex and nonconvex optimization. IEEE Signal Processing Magazine, 35(4):14–31, 2018.

- Chen and Wainwright (2015) Yudong Chen and Martin J Wainwright. Fast low-rank estimation by projected gradient descent: General statistical and algorithmic guarantees. arXiv preprint arXiv:1509.03025, 2015.

- Chen et al. (2015) Yudong Chen, Srinadh Bhojanapalli, Sujay Sanghavi, and Rachel Ward. Completing any low-rank matrix, provably. The Journal of Machine Learning Research, 16(1):2999–3034, 2015.

- Chen et al. (2020) Yuxin Chen, Yuejie Chi, Jianqing Fan, Cong Ma, and Yuling Yan. Noisy matrix completion: Understanding statistical guarantees for convex relaxation via nonconvex optimization. SIAM Journal on Optimization, 30(4):3098–3121, 2020.

- Clauset et al. (2004) Aaron Clauset, Mark EJ Newman, and Cristopher Moore. Finding community structure in very large networks. Physical review E, 70(6):066111, 2004.

- Davenport and Romberg (2016) Mark A Davenport and Justin Romberg. An overview of low-rank matrix recovery from incomplete observations. IEEE Journal of Selected Topics in Signal Processing, 10(4):608–622, 2016.

- Drineas and Zouzias (2011) Petros Drineas and Anastasios Zouzias. A note on element-wise matrix sparsification via a matrix-valued bernstein inequality. Information Processing Letters, 111(8):385–389, 2011.

- Drineas et al. (2008) Petros Drineas, Michael W Mahoney, and Shan Muthukrishnan. Relative-error cur matrix decompositions. SIAM Journal on Matrix Analysis and Applications, 30(2):844–881, 2008.

- Frieze et al. (2004) Alan Frieze, Ravi Kannan, and Santosh Vempala. Fast monte-carlo algorithms for finding low-rank approximations. Journal of the ACM (JACM), 51(6):1025–1041, 2004.

- Ge et al. (2016) Rong Ge, Jason D Lee, and Tengyu Ma. Matrix completion has no spurious local minimum. Advances in Neural Information Processing Systems, pages 2981–2989, 2016.

- Ge et al. (2017) Rong Ge, Chi Jin, and Yi Zheng. No spurious local minima in nonconvex low rank problems: A unified geometric analysis. In Proceedings of the 34th International Conference on Machine Learning-Volume 70, pages 1233–1242. JMLR. org, 2017.

- Gross (2011) David Gross. Recovering low-rank matrices from few coefficients in any basis. IEEE Transactions on Information Theory, 57(3):1548–1566, 2011.

- Jain and Kar (2017) Prateek Jain and Purushottam Kar. Non-convex optimization for machine learning. Foundations and Trends® in Machine Learning, 10(3-4):142–336, 2017.

- Keshavan et al. (2010) Raghunandan H Keshavan, Andrea Montanari, and Sewoong Oh. Matrix completion from a few entries. IEEE transactions on information theory, 56(6):2980–2998, 2010.

- Kluger et al. (2003) Yuval Kluger, Ronen Basri, Joseph T Chang, and Mark Gerstein. Spectral biclustering of microarray data: coclustering genes and conditions. Genome research, 13(4):703–716, 2003.

- Krishnamurthy and Singh (2013) Akshay Krishnamurthy and Aarti Singh. Low-rank matrix and tensor completion via adaptive sampling. In Advances in Neural Information Processing Systems, pages 836–844, 2013.

- Latała et al. (2018) Rafał Latała, Ramon van Handel, and Pierre Youssef. The dimension-free structure of nonhomogeneous random matrices. Inventiones mathematicae, 214(3):1031–1080, 2018.

- Mahoney (2011) Michael W Mahoney. Randomized algorithms for matrices and data. Foundations and Trends® in Machine Learning, 3(2):123–224, 2011.

- Mahoney and Drineas (2009) Michael W Mahoney and Petros Drineas. Cur matrix decompositions for improved data analysis. Proceedings of the National Academy of Sciences, 106(3):697–702, 2009.

- O’Rourke et al. (2018) Sean O’Rourke, Van Vu, and Ke Wang. Random perturbation and matrix sparsification and completion. arXiv preprint arXiv:1803.00679, 2018.

- Raskutti and Mahoney (2016) Garvesh Raskutti and Michael W Mahoney. A statistical perspective on randomized sketching for ordinary least-squares. The Journal of Machine Learning Research, 17(1):7508–7538, 2016.

- Recht (2011) Benjamin Recht. A simpler approach to matrix completion. Journal of Machine Learning Research, 12(12), 2011.

- Scott (2017) John Scott. Social network analysis. Sage, 2017.

- Smith et al. (2004) Stephen M Smith, Mark Jenkinson, Mark W Woolrich, Christian F Beckmann, Timothy EJ Behrens, Heidi Johansen-Berg, Peter R Bannister, Marilena De Luca, Ivana Drobnjak, and David E Flitney. Advances in functional and structural mr image analysis and implementation as FSL. Neuroimage, 23:S208–S219, 2004.

- Stelzl et al. (2005) Ulrich Stelzl, Uwe Worm, Maciej Lalowski, Christian Haenig, Felix H Brembeck, Heike Goehler, Martin Stroedicke, Martina Zenkner, Anke Schoenherr, and Susanne Koeppen. A human protein-protein interaction network: a resource for annotating the proteome. Cell, 122(6):957–968, 2005.

- Sun and Luo (2016) Ruoyu Sun and Zhi-Quan Luo. Guaranteed matrix completion via non-convex factorization. IEEE Transactions on Information Theory, 62(11):6535–6579, 2016.

- Wainwright (2019) M.J. Wainwright. High-Dimensional Statistics: A Non-Asymptotic Viewpoint. Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, 2019. ISBN 9781108571234. URL https://books.google.com/books?id=tMKIDwAAQBAJ.

- Woodruff et al. (2014) David P Woodruff et al. Sketching as a tool for numerical linear algebra. Foundations and Trends® in Theoretical Computer Science, 10(1–2):1–157, 2014.