Non-Adaptive Stochastic Score Classification and

Explainable Halfspace Evaluation

Abstract

Sequential testing problems involve a complex system with several components, each of which is “working” with some independent probability. The outcome of each component can be determined by performing a test, which incurs some cost. The overall system status is given by a function of the outcomes of its components. The goal is to evaluate this function by performing tests at the minimum expected cost. While there has been extensive prior work on this topic, provable approximation bounds are mainly limited to simple functions like “k-out-of-n” and halfspaces. We consider significantly more general “score classification” functions, and provide the first constant-factor approximation algorithm (improving over a previous logarithmic approximation ratio). Moreover, our policy is non adaptive: it just involves performing tests in an a priori fixed order. We also consider the related halfspace evaluation problem, where we want to evaluate some function on halfspaces (e.g., intersection of halfspaces). We show that our approach provides an -approximation algorithm for this problem. Our algorithms also extend to the setting of “batched” tests, where multiple tests can be perfomed simultaneously while incurring an extra setup cost. Finally, we perform computational experiments that demonstrate the practical performance of our algorithm for score classification. We observe that, for most instances, the cost of our algorithm is within of an information-theoretic lower bound on the optimal value.

1 Introduction

The problem of diagnosing complex systems often involves running costly tests for several components of such a system. One approach to diagnose such systems is to perform tests on all components, which can be prohibitively expensive. A better and more practical approach involves sequential testing, where a policy tests components one by one until the system is diagnosed, while minimizing the expected cost of testing. Such sequential testing problems arise in a number of applications such as healthcare, manufacturing and telecommunucation; we refer to the surveys by [Ü04] and [Mor82] for more details.

Concretely, there are components, where each component is “working” independently with some probability. The outcome (working or failed) of each component can be determined by performing a test, which incurs some cost. The overall status of the system is given by a function of the outcomes of its components. The goal is to determine , where denotes the outcome of component . The objective is to minimize the expected cost of testing.

Perhaps the simplest and most commonly studied function is the AND-function (or series system), which involves testing if all the components are working, i.e., . In this case, it is well known that the natural greedy algorithm finds an optimal solution, see e.g., [But72]. An exact algorithm is also known for -out-of- functions, where we want to determine if at least a threshold number of components are working (i.e., ); this result is by [BD81]. More generally, in the halfspace evaluation problem, each component has a weight and we want to check whether the total weight of working components is above/below a threshold. [DHK16] obtained a constant-factor approximation algorithm for the halfspace evaluation problem (it is also known to be NP-hard).

In this paper, we obtain sequential testing algorithms with provable guarantees for much more general functions . In particular, we consider the stochastic score classification problem, introduced by [GGHK18], where components have weights as in the halfspace evaluation problem. We are also given multiple threshold values that partition the number line into disjoint intervals, and the goal is to identify the interval that the total weight lies in. For example, the intervals may correspond to the overall system status being poor/fair/good/excellent, and we want to identify the system status at minimum expected cost. Note that the halfspace evaluation problem is a special case of score classification when there are just intervals.

We also consider the problem of evaluating the intersection of halfspaces. Here, there are different halfspaces and we want to check whether all the halfspaces are satisfied (and if not, we also want to identify some violated halfspace). In fact, we consider a more general problem that involves evaluating an arbitrary function over the halfspaces.

Solutions to all these problems are sequential decision processes, where one component is tested at each step (after which its outcome is observed). This process continues until the function value is determined. We note that solutions in general are adaptive: the choice of the next component to test may depend on all previous outcomes. In practice, it is often preferable to use a non-adaptive solution, which is simply given by a priority list of components: tests are then performed in that fixed order until the function is evaluated. Non-adaptive solutions are simpler and faster to implement (compared to their adaptive counterparts) as the testing sequence needs to be constructed just once, after which it can be used for all input realizations. However, non-adaptive solutions typically cost more than adaptive ones. So, one would ideally like to find a non-adaptive solution of cost comparable to an optimal adaptive solution. A priori, it is not even clear if such a low cost non-adaptive solution exists (let alone finding it in polynomial time). The adaptivity gap, introduced by [DGV08], captures the worst-case ratio between the best non-adaptive and best adaptive solutions; note that this quantity is independent of computational efficiency.

Our main result is a non-adaptive algorithm for stochastic score classification that is a constant-factor approximation to the optimal adaptive solution. We also obtain a non-adaptive factor approximation algorithm for evaluating the intersection of halfspaces. Both these results involve efficient algorithms (in fact, nearly linear time) and also bound the adaptivity gaps.

We also consider a more general cost-structure, where multiple tests can be performed simultaneously while incurring an extra set-up cost. As discussed in [SS22], this feature is present in many practical applications as it allows batching tests to achieve economies of scale. Our results extend to this batch-cost setting as well.

1.1 Problem Definitions

In the following, for any integer , we use .

Stochastic Score Classification ().

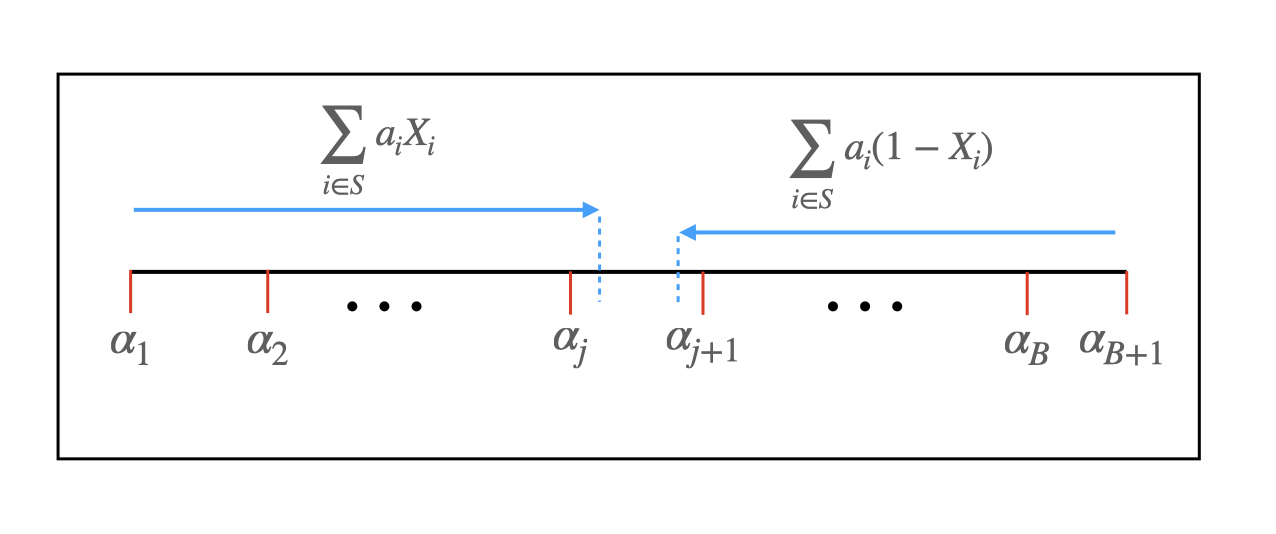

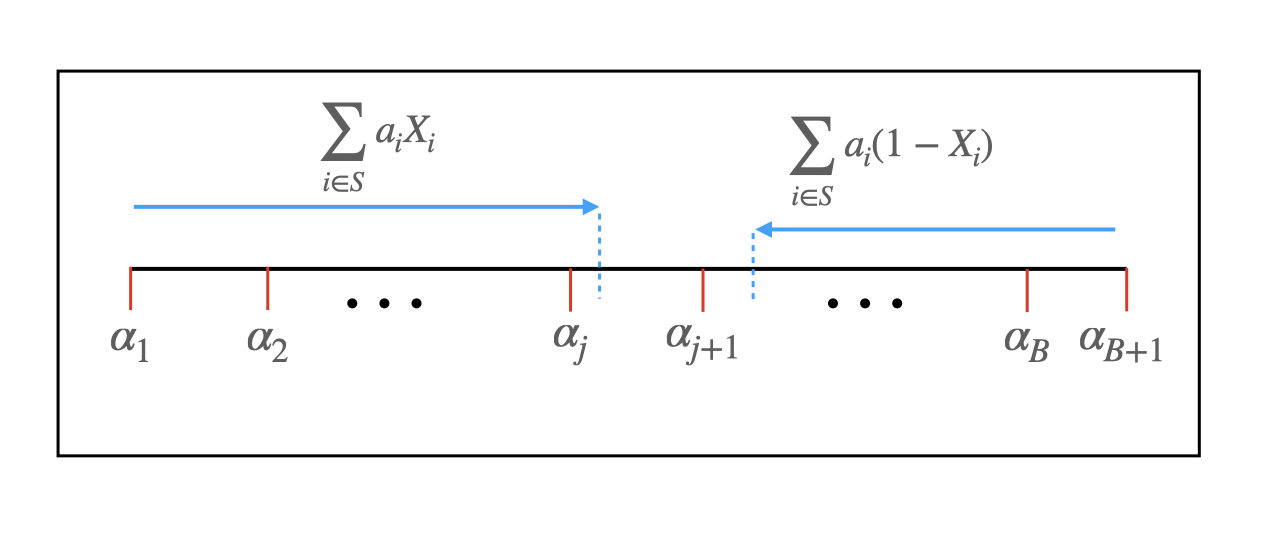

An instance consists of tests (a.k.a. items). Each item is associated with an independent random variable (r.v.) with . We use to denote the vector of all r.v.s. The algorithm knows the probability values s in advance, but not the random outcomes s. In order to determine the outcome of item , the algorithm needs to probe/test by incurring a cost . We are also given weights for all items , and the total weight of any outcome is denoted . In addition, we are given integer thresholds such that class corresponds to the interval . We assume that (resp. ) is the minimum (resp. maximum) total weight of any outcome. So, the intervals form a partition of possible weight outcomes. We want to evaluate the score classification function where precisely when , i.e. . The goal is to determine at minimum expected cost for testing.

Let denote the total weight of all items. For each class , we associate two numbers and . Note that for any outcome and class ,

| (1) |

In Appendix A, we show that any instance of with both positive and negative weights can be reduced to an equivalent instance with all positive weights. Henceforth, we assume (without loss of generality) that all weights s are non-negative. In this case, we also assume that and .

In our algorithm, it is convenient to introduce two (nonnegative) random rewards and associated with each item . Note that the total -reward (resp. -reward) corresponds to the total weight of working (resp. failed) items. For any subset of items, we define and .

Explainable Stochastic -Halfspace Evaluation (-d-).

An instance consists of random items as in , and halfspaces. For each , the halfspace is given by ; we set if the halfspace is satisfied and otherwise. Moreover, we are also given an aggregation function , and we want to evaluate . In other words, if we define the composite function , we want to evaluate . Furthermore, the problem asks for an “explanation”, or a witness of this evaluation. The definition of a witness is a bit technical, so it is deferred to §5. The goal is to evaluate along with a witness, at the minimum expected cost.

For example, when , -d- corresponds to evaluating the intersection of halfspaces; the witness in this case either confirms that all halfspaces are satisfied or identifies some violated halfspace. -d- also captures more general cases: given a target , we can check whether at least out of halfspaces are satisfied (using an appropriate ).

Batch Cost Structure.

This is a generalization of the basic (additive) cost structure, where any subset of items may be tested simultaneously by incurring an extra setup cost . Formally, the cost to simultaneously test a subset of items is . Note that setting , we recover the usual cost structure (as in and -d-), in which case there is no benefit to batching tests together. However, when is large, it is beneficial to perform multiple tests simultaneously because one can avoid paying the setup cost repeatedly. Here, a solution involves selecting a batch of items in each step (instead of a single item). Again, the goal is to evaluate the function (in or -d-) at minimum expected cost.

1.2 Results and Techniques

Our main result is the following algorithm (and adaptivity gap).

Theorem 1.1.

There is a non-adaptive algorithm for stochastic score classification with expected cost at most a constant factor times the optimal adaptive cost.

This result improves on the prior work from [GGHK18] in several ways. Firstly, we get a constant-factor approximation, improving upon the previous and ratios, where is the sum of weights, and the number of classes. Secondly, our algorithm is non-adaptive in contrast to the previous adaptive ones. Finally, our algorithm has nearly-linear runtime, which is faster than the previous algorithms.

An added benefit of our approach is that we obtain a “universal” solution that is simultaneously -approximate for all class-partitions. Indeed, the non-adaptive list produced by our algorithm only depends on the probabilities, costs and weights, and not on the class boundaries ; these values are only needed in the stopping condition.

Our second result is the following algorithm for -d-.

Theorem 1.2.

There is a non-adaptive algorithm for explainable stochastic -halfspace evaluation with expected cost times the optimal adaptive cost.

As a special case, we obtain a non-adaptive -approximation algorithm for (explainable) intersection of halfspaces. The stochastic intersection of halfspaces problem (in a slightly different model) was studied previously by [BLT21], where the solution may make errors with probability . Assuming that all probabilities , [BLT21] obtained an -approximation algorithm. Another difference from our model is that [BLT21] do not require a witness. So their policy can stop if it concludes that there exists a violated halfspace (even without knowing which one), whereas our policy can only stop after it identifies a violated halfspace (or determines that all halfspaces are satisfied). We note that our approximation ratio is independent of the number of variables and holds for arbitrary probabilities.

Next, we consider the more general batch-cost structure and show the following.

Theorem 1.3.

In the setting of batch-costs, there is a non-adaptive algorithm with:

-

•

approximation ratio for stochastic score classification.

-

•

approximation ratio for stochastic -halfspace evaluation.

To the best of our knowledge, this is the first constant approximation even for halfspace evaluation in the batched setting. Previously, [DGSÜ16] and [SS22] obtained constant-factor approximation algorithms for evaluating an AND-function in the batched setting.

Finally, we evaluate the empirical performance of our algorithm for score classification. In these experiments, our non-adaptive algorithm performs nearly as well as the previous-best adaptive algorithms, while being an order of magnitude faster. In fact, on many instances, our algorithm provides an improvement in both the cost as well as the running time. On most instances, the cost of our algorithm is within of an information-theoretic lower bound on the optimal value.

Overview of techniques.

To motivate our algorithm for , suppose that we have currently tested/probed a subset of items. Then, we can evaluate the score-classification function if and only if, there is some class such that

| (2) |

Indeed, if the above condition is satisfied then, irrespective of the outcomes of the untested items , we have and ; this uses the assumption that all weights are nonnegative. Using (1), we can then conclude that the function value . On the other hand, if the above condition is not satisfied for any class , we must continue testing as the function value cannot be determined yet. See Figure 1 for an example. Note that condition (2) is the same as and ; recall the definition of the and rewards. Our algorithm tries to achieve condition (2) at the minimum testing cost.

The challenge however is that the class (of the realization ) is unknown: so we do not have a numeric threshold on the or rewards to aim for. If we knew the target and rewards then we could directly use constant-factor approximation algorithms for the stochastic covering knapsack problem from [DHK16] or [JLLS20]. In the stochastic covering knapsack () problem, given items with deterministic costs and random rewards, we want to minimize the expected cost to achieve a target total reward value. This is precisely what we would want to solve in (2) if the class was fixed.

We get around this issue (of not knowing class ) by coming up with a “universal” solution for that works for all targets simultaneously. Roughly speaking, we build two universal solutions and , corresponding to covering the and rewards respectively. Then, we interleave these two solutions so that the cost incurred in the combined solution is split evenly between and . The key step in building this universal solution lies in coming up with a non-adaptive solution for with the following guarantee: given any cost-budget and tolerance , there is a subset of items with cost such that for every adaptive solution of cost , the probability that has more reward than is at least . Our algorithm here relies on solving a logarithmic number of deterministic knapsack instances, where we use truncated expectations as the deterministic rewards. In order to choose the correct truncation threshold, we use the “critical scaling” idea from [JLLS20]. We note however that the details of our algorithm/analysis are different: we use properties of the fractional knapsack problem and our analysis doesn’t require martingale concentration inequalities as in [JLLS20].

1.3 Related Work

Sequential testing problems have been extensively studied in operations research and computer science; see e.g., surveys by [Mor82] and [Ü04]. When the function is an AND-function (equivalently, an OR-function), it is easy to easy to see that an optimal solution is non-adaptive. Moreover, [But72] proved that testing items in a greedy order is optimal in this case. For -out-of- functions, non-adaptive solutions are no longer optimal, and an optimal adaptive algorithm was obtained by [BD81]. A non-adaptive -approximation algorithm also follows from the work of [GGHK18]. The more general halfspace evaluation (a.k.a. linear threshold functions) is known to be NP-hard, and an adaptive -approximation algorithm was obtained in [DHK16]. A non-adaptive -approximation algorithm for halfspace evaluation can be inferred from [JLLS20].

Approximation algorithms are also known for evaluating certain other functions. In particular, [AHKU17] obtained a -approximation for monotone functions in “disjunctive normal form” with terms, and [KKM05] obtained a logarithmic approximation ratio for functions with both disjunctive and conjunctive normal form representations.

The problem was introduced by [GGHK18], who showed that it can be formulated as an instance of “stochastic submodular cover”. Then, using more general results ([INvdZ16, GK17]), they obtained an adaptive -approximation algorithm. Furthermore, [GGHK18] obtained an adaptive -approximation algorithm for by extending the approach of [DHK16] for halfspace evaluation. [GGHK18] also studied the unweighted special case of (where all weights ) and gave a slightly better -approximation algorithm. A main open question from this work was the possibility of a constant approximation for the general problem. We answer this in the affirmative. Moreover, our algorithm is non-adaptive: so we also bound the adaptivity gap.

Stochastic covering knapsack () is closely related to halfspace evaluation. Indeed, the results on halfspace evaluation in [DHK16] and [JLLS20] are based on this relation. We note that the results in [JLLS20] applied to the more general stochastic -TSP problem ([ENS17]). As noted earlier, we make use of some ideas from [JLLS20]. However, our algorithm/analysis is simpler and we obtain a nearly-linear time algorithm.

[DÖS+17] introduced sequential testing with batch costs and developed efficient heuristics (without performance guarantees). Subsequently, [DGSÜ16] obtained a constant-factor approximation algorithm for evaluating AND-functions under batch costs. Recently, [SS22] improved this result to a polynomial-time approximation scheme (PTAS). We are not aware of results for more general functions (even -out-of-) under batch costs.

More generally, non-adaptive solutions (and adaptivity gaps) have been used for various other stochastic optimization problems such as max-knapsack ([DGV08, BGK11]), matching ([BGL+12, BDH20]), matroid intersection ([GN13, GNS17]) and orienteering ([GM09, GKNR15, BN15]). Our result shows that this approach is also useful for .

Subsequent works.

After the preliminary version of this paper appeared, there have been some improved results on the unweighted special case of (where all weights are one). [PS22] and [Liu22] obtained approximation ratios of and , respectively. For the further special case with unit costs, [GHKL22] obtained a -approximation algorithm. All these algorithms also find non-adaptive solutions. We note our results are more general because they can handle arbitrary weights (as in halfspace evaluation).

1.4 Organization.

We start with some basic results on deterministic knapsack in §2. In §3, we present the non-adaptive algorithm for with a strong probabilistic guarantee. This result is then used to obtain all our algorithms: §4 is on , §5 is on -d- and §6 is on the batch-cost extensions. Finally, we present computational results in §7.

2 Preliminaries on Deterministic Knapsack

We first state some basic results for the deterministic knapsack problem. In an instance of the knapsack problem, we are given a set of items with non-negative costs and rewards , and a budget on the total cost. The goal is to select a subset of items of total cost at most that maximizes the total reward. The LP relaxation is the following:

The following algorithm solves the fractional knapsack problem and also obtains an approximate integral solution. Assume that the items are ordered so that . Let index the first item (if any) so that . Let which lies in . Define

Return as the optimal fractional solution and as an integer solution. We prove the following fact in the appendix for completeness.

Theorem 2.1.

Consider algorithm on any instance of the knapsack problem with budget .

-

1.

and so is an optimal LP solution.

-

2.

The derivative .

-

3.

Solution has cost and reward .

-

4.

is a concave function of .

3 Non-Adaptive Stochastic Covering Knapsack with Probabilistic Guarantee

Consider any instance of with items with deterministic costs and (independent) random rewards . An adaptive policy is a sequence of items, where the choice of the item depends on the observed rewards on the first items (as well as internal random outcomes). In contrast, a non-adaptive policy is simply a static sequence of the items. For any policy , let denote the corresponding sequence, where is the selected item. Note that s are random indices for an adaptive policy , whereas they are deterministic for a non-adaptive policy. We note that an adaptive policy may also use internal randomness in choosing items, i.e., the first items along with their observed rewards determine the probability distribution of the next item . We use to denote the random total reward collected by policy . We say that policy costs at most if the total cost of the (possibly random) items selected by is always at most . The main result of this section is a non-adaptive policy that achieves the following probabilistic guarantee relative to any adaptive policy.

Theorem 3.1.

Given a set of items with costs , random rewards , budget , and , Algorithm 1 returns a non-adaptive (i.e., fixed) subset such that

-

•

Cost guarantee: , and

-

•

Reward guarantee: for every adaptive policy of cost at most .

Moreover, the algorithm runs in time nearly-linear in .

We note that this result is stronger than typical “adaptivity gap” results which only bound the expected objective values of adaptive/nonadaptive policies. The fact that we have a probabilistic guarantee (rather than just expectation) turns out to be crucial in designing the algorithms for and -d-.

Our algorithm is based on solving a deterministic knapsack instance using the natural greedy algorithm . A key challenge in constructing the deterministic knapsack instance is the choice of deterministic rewards. To this end, we consider truncated expectations of the following form:

| (3) |

In order to keep the number of thresholds small (logarithmic instead of linear), we will only consider the following threshold values, also called scales.

We still need to identify which scale to use as the threshold in (3). To this end, we first classify each scale as either rich or poor. Roughly speaking, in a rich scale, the optimal knapsack solution after cost still has large “incremental” reward, where is a parameter that will be fixed later. Formally, for any scale , let denote the optimal LP value function when the rewards are , i.e.,

The scale is called rich if the derivative , and it is called poor otherwise. The critical scale is the smallest scale that is poor, and so represents a transition from rich to poor: we will show later that this always exists. Informally, we can also view the critical scale as having derivative .

For our analysis, we will choose parameter .

We first show that the critical scale always exists.

Proof.

Proof. To prove that there is a smallest poor scale, it suffices to show that not all scales can be rich. We claim that the last scale cannot be rich. Suppose (for a contradiction) that scale is rich. Then, by concavity of (see property 4 in Theorem 2.1), we have . On the other hand, the total deterministic reward at this scale, . Thus, , a contradiction.

The next lemma proves the cost property.

Lemma 3.3.

For any scale , the cost . Hence, the solution returned by StochKnap has cost at most .

Proof.

Proof. Consider any scale . We have where is the integer solution from Theorem 2.1. It follows that ; note that we only consider items of cost at most (see Step 1 of Algorithm 1).

We now prove the reward property. For any adaptive policy of cost at most , w will show:

| (4) |

where is the solution from Algorithm 1. The probability above is taken over the randomness in the rewards as well as the choice of items in policy . This suffices to prove Theorem 3.1.

Let denote the (random) items selected by adaptive policy . Note that is a random subset as policy is adaptive. On the other hand, is a deterministic subset. We need to show that the probability that has more reward than is small. The key idea is to use the critical scale to argue that the following hold with large enough probability:

-

•

reward of is at most , and

-

•

reward of is at least .

For any subset of items, we use to denote the total observed reward in . We also use to be the scale immediately preceding the critical scale . (If then is undefined, and all steps involving can be ignored.)

Upper bounding reward of .

Define new random rewards:

| (5) |

Note that this is the truncated reward at scale , and for all items . We now show that any adaptive policy that selects items of cost (outside ) cannot get too much reward.

Lemma 3.4.

If is any adaptive policy of selecting items from with cost at most then . Hence, .

Proof.

Proof. Recall the definition of subset from Algorithm 1. This is an approximate solution to the deterministic knapsack instance on items (each of cost at most ) with rewards , where is the critical scale. The solution is constructed as follows (see Theorem 2.1). The items in are ordered greedily in non-increasing reward-to-cost ratio. Then, is the minimal prefix of with total cost at least the budget . Moreover, the derivative , where is the last item added to (in the greedy ordering).

As is a poor scale, the derivative . We now claim:

| (6) |

Clearly, every variable in has cost at most : so . Using the fact that is a prefix of in the greedy ordering (and is the last item in ),

Using , it now follows that , proving (6).

Now consider the adaptive policy . We also use to denote the (random) subset selected. Note that . The expected -reward of this policy is:

The third equality above uses the fact that are independent: so is independent of . Note that every outcome of has total cost at most . So, by (6), the total expected -reward . Combined with the above, we get

As s are non-negative, using Markov’s inequality, we have . Hence,

| (7) |

Now, observe that implies , which in turn implies . Combined with (7) this proves the first part of the lemma.

For the second part of the lemma, consider as the adaptive policy of cost at most . It follows that , as claimed.

Lower bounding reward of .

We first lower bound the expected reward.

Lemma 3.5.

If then for every outcome of .

Proof.

Proof. As , the rich scale exists. To reduce notation let be the reward at scale . Recall that the budget . Also, let and denote the optimal LP values of the knapsack instances (with items ) in scales and respectively. For any item , we have . We number the items in in the greedy order at scale , i.e., in decreasing order of . Let index the item so that the derivative . By Theorem 2.1, the cost of the first items, . Moreover,

| (8) |

Let denote the items in decreasing order of the ratio , which corresponds to scale . Note that the derivative equals the ratio of the first item (in the order ) such that ; see Theorem 2.1. From (8) and the fact that , it follows that the total cost of items with ratio at least is at least . Hence, we have .

Now, using the fact that is rich, we have . Therefore, . Furthermore, using the concavity of (see Theorem 2.1) and ,

| (9) |

By Theorem 2.1 (for the knapsack instance at scale ), the items have reward .

Now consider any outcome of the adaptive policy . The total cost . So, is always a feasible solution to the knapsack instance with budget . This implies ; recall that is the optimal LP value. Therefore,

The last inequality uses (9).

The following is a Chernoff-type bound.

Lemma 3.6.

We have , where .

Proof.

Proof.Recall that . Let . By Lemma 3.5, . Moreover, by our choice , we have . Note that implies . So it suffices to upper bound .

Let be some parameter. We have:

By convexity of we have for all . Taking expectation over , it follows that . Combined with the above,

Setting , the right-hand-side above is which completes the proof.

Wrapping up.

4 Score Classification Algorithm

We now provide a constant-factor approximation algorithm for , and prove Theorem 1.1. Recall that there are two random rewards and associated with each item . Moreover, a policy for can make progress by collecting either or reward. So, our algorithm (described formally in Algorithm 2) divides the cost incurred equally between “covering” and rewards. The non-adaptive list for is built in phases. In each phase , we select items of total cost . This is done by invoking the stochastic knapsack algorithm (Theorem 3.1) twice: using and rewards separately (with parameter ). Finally, the non-adaptive policy probes items in the order until it identifies the class.

Note that there are phases in Algorithm 2, and each phase calls algorithm StochKnap twice. As the running time of StochKnap is nearly-linear, so is the runtime of our algorithm.

Let NaCl denote the non-adaptive policy obtained in Algorithm 2 . We now analyze the expected cost of NaCl. We denote by an optimal adaptive solution for . To analyze the algorithm, we use the following notation.

-

•

: probability that NaCl is not complete by end of phase .

-

•

: probability that costs at least .

We can assume by scaling that the minimum cost is . So . When it is clear from context, we use and NaCl to also denote the random cost incurred by the respective policies. We also divide into phases: phase corresponds to items in after which its cumulative cost is between and . So, the items selected by in its first phases is the maximal prefix having cost at most . The following lemma forms the crux of the analysis.

Lemma 4.1 (Key lemma).

For any phase , we have where .

Using the cost property in Theorem 3.1, we get:

Lemma 4.2.

The total cost of NaCl in any phase is at most , where .

Proof.

Proof. The items in phase of NaCl are . Using Theorem 3.1 (with and ), the total cost of (resp. ) is . The lemma now follows.

Proof.

Proof of Theorem 1.1 This proof is fairly standard, see e.g., [ENS17]. By Lemma 4.2, the total cost until end of phase (in NaCl) is at most . Let below. Moreover, NaCl ends in phase with probability . As a consequence of this, we have

| (10) |

Similarly, we can bound the cost of the optimal adaptive algorithm as

| (11) |

where the final equality uses the fact that . Define . We have

where the first inequality follows from Lemma 4.1, the second inequality from (11), and the last inequality from the fact that . Thus, . From (10), we conclude . Setting and completes the proof.

4.1 Proof of Lemma 4.1

Fix any phase , and let be the set of remaining items (i.e., items that have not been added to the list in previous phases). Let denote the realizations of the items , i.e., the items probed in the first phases of NaCl. We further define the following conditioned on :

-

•

: probability that NaCl is not complete by end of phase .

-

•

: probability that costs at least , i.e., is not complete by end of phase .

Note that is either or (as contains all realizations in the first phases). If (i.e., NaCl is complete before phase ) then as well: so, . On the other hand, if (i.e., NaCl does not complete before phase ) then we will prove

| (12) |

This would imply for all realizations . Taking expectation over then proves Lemma 4.1. It remains to prove Equation (12).

We denote by and the total reward obtained in the first phases by NaCl and respectively. We similarly define and . To prove Equation (12), we first use the reward-property in Theorem 3.1 to show that the probabilities and are small.

Lemma 4.3.

For , we have .

Proof.

Proof. Fix any and condition on realization . Let denote the total reward from the realizations in ; note that this is a deterministic value as we have conditioned on . Let be the items added in phase corresponding to -rewards (see Step 5 in Algorithm 2).

Observe that as corresponds to all items in the first phases and the items selected in phase is a superset of . (Recall that all rewards are non-negative.)

Let denote the adaptive policy obtained by restricting (conditional on ) to its first phases and items . In other words, if selects any item (in its first phases) then does not collect the reward of item but it continues to follow according to ’s realization in . Note that . Moreover, the cost of is at most .

Using the fact that is the solution of StochKnap with items , rewards , budget and (and Theorem 3.1), we have .

Combined with and , we have (conditioned on ),

Using this lemma, we prove Equation (12).

5 Explainable Stochastic -Halfspace Evaluation

We now consider -d- and prove Theorem 1.2. Recall that an instance of -d- also involves random items , but the function to be evaluated is different. In particular, there are halfspaces for . There is also an aggregation function , and we want to evaluate .

Furthermore, the problem asks for an “explanation”, or a witness of this evaluation. To define a witness, consider a tuple , where is the set of probed items, are the realizations of these items, and is a subset of halfspaces. This tuple is a witness for if the following conditions are satisfied:

-

•

The realizations of the probed items determine for all halfspaces . In other words, we can evaluate all the halfspaces using only the realizations of .

-

•

The values of completely determine . That is, has the same value for every with for .

In other words, a witness is a proof of the function value that only makes use of probed variables. The goal is to evaluate along with a witness (as defined above), at the minimum expected cost. We assume that checking whether a given tuple is a witness can be done efficiently.

The goal is to design a probing strategy of minimum expected cost that determines along with a witness. Before describing our algorithm, we highlight the role of a witness in stochastic -halfspace evaluation (by comparing to a model without witnesses). We also discuss the complexity of verifying witnesses for .

Solutions with/without witness. Solutions that are not required to provide a witness for their evaluation stop when they can infer that the function remains constant irrespective of the realizations of the remaining variables. For example, consider the stochastic intersection of halfspaces problem (as studied in [BLT21]). A feasible solution without a witness can stop probing when it determines that, with probability one, either halfspace or halfspace is violated (though it does not know precisely which halfspace is violated). Such a “stopping rule” may not be useful in situations where one also wants to know the identity of a violated halfspace (say, in order to take some corrective action). A solution with a witness (as required in our model) would provide one specific violated halfspace or conclude that all halfspaces are satisfied.

Verifying witnesses. We now address the issue of verifying whether a tuple is a witness for . Note that it is easy to check whether the values for suffice to evaluate all the halfspaces in . The challenge in verifying witnesses lies in confirming whether the values of completely determine . For some functions , such as intersection (i.e., all halfspaces must be satisfied) or -of- functions (i.e., at least of the halfspaces must be satisfied), this can be done efficiently. However, for a general aggregation function , verifying a witness may require the evaluation of at all points. While our algorithm works for any aggregation function , for a polynomial running time, we need to assume an efficient oracle for verifying witnesses.

Our algorithm for -d- is similar to that for , and is described in Algorithm 3. We introduce random rewards that help in evaluating the different halfspaces:

Then, we ensure that the cost incurred is spread uniformly to cover these different rewards. Again, the list-building algorithm proceeds in phases, where in each phase , we utilize the stochastic knapsack algorithm (Theorem 3.1) with budget for each of the rewards. This time, we set the parameter which enables us to show that our algorithm makes progress in covering all the rewards. Finally, the non-adaptive policy just probes items in the order of list until the realizations of the probed items form a witness for (which is verfied using the oracle).

The analysis is also similar to that for . Let NaCl denote the non-adaptive policy in Algorithm 3 and the optimal adaptive policy for -d-. We also define:

-

•

: probability that NaCl is not complete by end of phase .

-

•

: probability that costs at least .

Again, we assume by scaling that the minimum cost is ; so . We use and NaCl to also denote the random cost incurred by the respective policies. We also divide into phases: phase corresponds to items in after which its cumulative cost is between and . As before, we will show:

Lemma 5.1.

For any phase , we have where .

Using the cost property in Theorem 3.1, we get:

Lemma 5.2.

The total cost of NaCl in any phase is at most , where .

Proof.

Proof. The items in phase of NaCl are . For each and , using Theorem 3.1 (with and ), we obtain that the cost of subset is . The lemma now follows by combining the subsets .

The proof of Theorem 1.2 uses Lemma 5.1 and is identical to the proof of Theorem 1.1 (in §4). The only difference is that we have from Lemma 5.1, which results in the approximation guarantee.

It now remains to prove Lemma 5.1. Fix any phase , and let be the set of remaining items. Let denote the realizations of the items . As before, we also define the following conditioned on :

-

•

: probability that NaCl is not complete by end of phase .

-

•

: probability that costs at least , i.e., is not complete by end of phase .

As in the proof of Lemma 4.1, it suffices to prove

| (13) |

To this end, for any and , let and be the total reward obtained in the first phases by NaCl and respectively. We first use the reward-property in Theorem 3.1 to show:

Lemma 5.3.

For any and , we have .

Proof.

Proof. This is identical to the proof of Lemma 4.3, where we use random rewards (instead of ) and value (instead of ).

Using this lemma, we prove Equation (13). If finishes in phase , then there exists some witness where (i) is the set of items probed by until phase , (ii) the realizations of the items determine for all halfspaces , and (iii) the values completely determine . We further partition into

For any halfspace , define thresholds:

Note that for , we have if and only if .

Now, using the definition of and , we have:

-

C1.

for each , and

-

C2.

for each .

Let denote the set of 3-way-partitions of the halfspaces such that is completely determined by setting the coordinates in to and those in to . Note that for any witness as above, we have . Thus,

Note that if finishes by phase and for all and , then we can conclude that NaCl also finishes by phase (with the same witness as ). By Lemma 5.3 and union bound, we have . Hence,

Upon rearranging, this gives , which proves (13).

6 Sequential Testing with Batched Costs

In this section, we consider and -d- under batch-costs and prove Theorem 1.3. Recall that the batched cost structure involves an additional setup cost , where the cost to simultaneously test a subset is . The goal is to evaluate the function (corresponding to or -d-) at the minimum expected cost.

A solution in the batched setting is an adaptive sequence of subsets , where all items in are tested simultaneously in step . Note that these subsets are pairwise disjoint. If the function value is determined after step (i.e., using the outcomes of items ) then we stop after this step; else, we proceed to step by testing . Our algorithm is again non-adaptive: it fixes the sequence of subsets upfront, and the random outcomes are only used to determine when to stop. We divide the cost incurred by any solution into its total setup cost (i.e., times the number of batches used) and total testing cost (i.e., sum of costs over all items tested).

Our algorithm is a simple extension of Algorithms 2 and 3 for and -d- under the usual cost structure (no batches). Recall that both Algorithms 2 and 3 proceed in phases, where the items selected in each phase have cost . The multiplier for (Algorithm 2) and for -d- (Algorithm 3). Let . Then, the batched-cost algorithm does the following. For each phase , test subset in one batch. Note that the difference from the previous algorithms is that we start directly in phase instead of phase (and we test all items in a phase simultaneously). The reason we start with phase is that we do not want to incur the setup cost before the total testing cost is .

Analysis.

Let NaCl denote the non-adaptive policy above and the optimal adaptive policy, both under batch-costs. As before, we define:

-

•

: probability that NaCl is not complete by end of phase .

-

•

: probability that costs at least .

Lemma 6.1.

For any , we have where

Lemma 6.2.

The total testing cost of NaCl in any phase is at most .

We are now ready to prove Theorem 1.3. Note that uses at least one batch: so its setup cost is at least . The testing cost can be lower bounded as before, to get:

| (14) |

where we used the fact that .

Observe that with probability , NaCl completes in phase and has total cost at most . Moreover, for any , NaCl completes in phase with probability and has setup cost (corresponding to the number of batches used) and testing cost at most (by Lemma 6.2). Hence, we have

| (15) |

where the last inequality uses .

7 Computational Results

We provide a summary of computational results of our non-adaptive algorithm for the stochastic score classification problem. We conducted all of our computational experiments using Python 3.8 with a 2.3 GHz Intel Core i5 processor and 16 GB 2133MHz LPDDR3 memory. We use synthetic data to generate instances of for our experiments.

Instance Type.

We test our algorithm for three types of instances: stochastic halfspace evaluation (), unweighted stochastic score classification, and (weighted) stochastic score classification (). The cutoffs and the weights for the score function are selected based on the type of instance being generated and will be specified later.

Instance Generation.

We test our algorithm on synthetic data generated as follows. We first set . Given , we generate Bernoulli variables, each with probability chosen uniformly from . We set the costs of each variable to be an integer in . To select cutoffs (when ), we first select and then select the cutoffs (based on the value of ) uniformly at random in the score interval. For each we generate instances. For each instance, we sample realizations in order to calculate the average cost and average runtime.

Algorithms.

We compare our non-adaptive algorithm (Theorem 1.1) against a number of prior algorithms. For instances, we compare to the adaptive 3-approximation algorithm from [DHK16]. For unweighted instances, we compare to the non-adaptive algorithm from [GGHK18], which was shown to be a -approximation to the optimal adaptive policy by [PS22] and [Liu22]. For general instances, we compare to the adaptive -approximation algorithm from [GGHK18]. We would like to emphasize that we compare our single algorithm with other algorithms that are tailored to specific cases of . As a benchmark, we also compare to a naive non-adaptive algorithm that probes variables in a random order. We also compare to an information-theoretic lower bound (no adaptive policy can do better than this lower bound). We obtain this lower bound by using an integer linear program to compute the (offline) optimal probing cost for a given realization (see §C for details), and then taking an average over realizations.

Reported quantities.

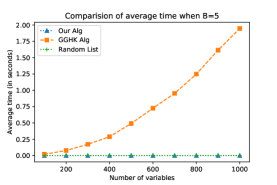

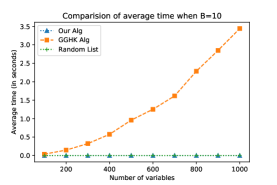

For every instance, we compute the cost and runtime of each algorithm by taking an average over independent realizations. For the non-adaptive algorithms, note that we only need one probing sequence for each instance (irrespective of the realization). On the other hand, adaptive algorithms need to find the probing sequence afresh for each realization. As seen in all the runtime plots, the non-adaptive algorithms are significantly faster.

For each instance type (, Unweighted and ), the plots in Figures 2-5 show the averages (for both cost and runtime) against the number of variables . Note that each point in these plots corresponds to an average over (i) the 10 instances of its type and (ii) the 50 sampled realizations for each instance.

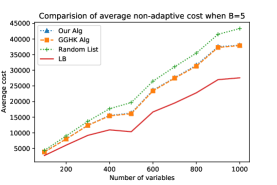

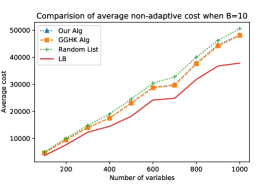

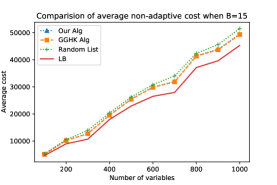

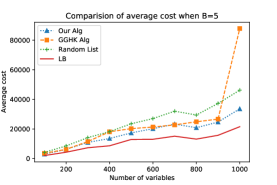

In Table 1, we report the average performance ratio (cost of the algorithm divided by the information-theoretic lower bound) of the various algorithms. For each instance type (, Unweighted and ), we report the performance ratio averaged over all values of (10 choices) and all instances (10 each). Values closer to demonstrate better performance. More detailed tables, with the average performance ratio for each value of , are in Appendix D.

| Instance Type | Our Alg. | GGHK Alg. | Random List |

|---|---|---|---|

| Unweighted , | |||

| Unweighted , | |||

| Unweighted , | |||

| , | |||

| , | |||

| , |

| Instance Type | Our Alg. | DHK Alg. | Random List |

|---|---|---|---|

Stochastic Halfspace Evaluation.

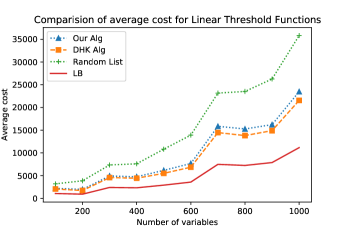

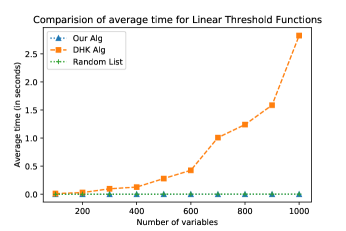

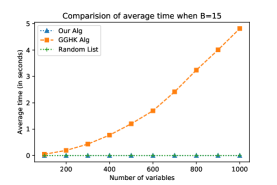

To generate an instance of , we set uniformly for all and select a cutoff value uniformly in the score interval. We plot the results in Figure 2. Our cost is about more than that of [DHK16], but our runtime is over faster for large instances.

Unweighted Stochastic Score Classification.

To generate instances of unweighted , we set for all . We choose , and then select the cutoffs (based on the value of ) uniformly at random in the score interval. We test our non-adaptive algorithm against the non-adaptive algorithm of [GGHK18] and a random query order. Since, all the algorithms are non-adaptive, there is no difference in their running time. So, we focus on the average cost comparison among the algorithms. We observe that the average cost incurred by our non-adaptive algorithm is comparable to that of the non-adaptive algorithm of [GGHK18], and both algorithms outperform a random query order. We plot the results in Figure 3

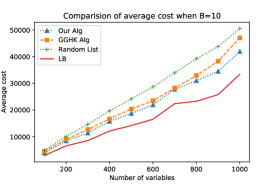

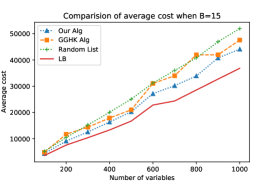

(Weighted) Stochastic Score Classification.

We test on instances with . The cutoff values are selected uniformly at random in the score interval. We plot results in Figures 4 and 5. In all cases, we observe that our non-adaptive algorithm beats the adaptive algorithm in both query cost and runtime; for e.g., when and our cost is less and our runtime is about faster.

8 Conclusions

In this paper, we obtained the first constant-factor approximation algorithm for stochastic score classification, which significantly generalizes sequential testing algorithms for series systems, -of- functions and halfspaces. Our algorithm is non-adaptive and very efficient to implement. We also evaluated our algorithm empirically and compared it to previous approaches and an information-theoretic lower bound: in most cases, our algorithm provides an improvement in solution cost or runtime. Our approach also extends to other sequential testing problems such as intersection of halfspaces, and to the setting of batched tests.

Acknowledgements

A preliminary version of this paper (with the same title) appeared in the conference on Integer Programming and Combinatorial Optimization (IPCO), 2022.

References

- [AHKU17] Sarah Allen, Lisa Hellerstein, Devorah Kletenik, and Tonguç Ünlüyurt. Evaluation of monotone dnf formulas. Algorithmica, 77:661–685, 2017.

- [BD81] Yosi Ben-Dov. Optimal testing procedures for special structures of coherent systems. Management Science, 27(12):1410–1420, dec 1981.

- [BDH20] Soheil Behnezhad, Mahsa Derakhshan, and MohammadTaghi Hajiaghayi. Stochastic matching with few queries: (1-) approximation. In Proccedings of the 52nd Annual ACM SIGACT Symposium on Theory of Computing, pages 1111–1124, 2020.

- [BGK11] Anand Bhalgat, Ashish Goel, and Sanjeev Khanna. Improved approximation results for stochastic knapsack problems. In SODA, pages 1647–1665, 2011.

- [BGL+12] N. Bansal, A. Gupta, J. Li, J. Mestre, V. Nagarajan, and A. Rudra. When LP is the cure for your matching woes: Improved bounds for stochastic matchings. Algorithmica, 63(4):733–762, 2012.

- [BLT21] Guy Blanc, Jane Lange, and Li-Yang Tan. Query strategies for priced information, revisited. In Proceedings of the Thirty-second Annual ACM-SIAM Symposium on Discrete Algorithms (SODA 2021), page 1638–1650, 2021.

- [BN15] Nikhil Bansal and Viswanath Nagarajan. On the adaptivity gap of stochastic orienteering. Math. Program., 154(1-2):145–172, 2015.

- [But72] R Butterworth. Some reliability fault-testing models. Operations Research, 20(2):335–343, 1972.

- [DGSÜ16] Rebi Daldal, Iftah Gamzu, Danny Segev, and Tonguç Ünlüyurt. Approximation algorithms for sequential batch‐testing of series systems. Naval Research Logistics (NRL), 63, 2016.

- [DGV08] B. C. Dean, M. X. Goemans, and J. Vondrák. Approximating the stochastic knapsack problem: The benefit of adaptivity. Math. Oper. Res., 33(4):945–964, 2008.

- [DHK16] Amol Deshpande, Lisa Hellerstein, and Devorah Kletenik. Approximation algorithms for stochastic submodular set cover with applications to boolean function evaluation and min-knapsack. ACM Trans. Algorithms, 12(3), April 2016.

- [DÖS+17] Rebi Daldal, Özgür Özlük, Baris Selçuk, Zahed Shahmoradi, and Tonguç Ünlüyurt. Sequential testing in batches. Annals of Operations Research, 253:97–116, 2017.

- [ENS17] Alina Ene, Viswanath Nagarajan, and Rishi Saket. Approximation algorithms for stochastic k-tsp. In 37th IARCS Annual Conference on Foundations of Software Technology and Theoretical Computer Science, pages 27:27–27:14, 2017.

- [GGHK18] Dimitrios Gkenosis, Nathaniel Grammel, Lisa Hellerstein, and Devorah Kletenik. The Stochastic Score Classification Problem. In 26th Annual European Symposium on Algorithms (ESA), volume 112, pages 36:1–36:14, 2018.

- [GHKL22] Nathaniel Grammel, Lisa Hellerstein, Devorah Kletenik, and Naifeng Liu. Algorithms for the unit-cost stochastic score classification problem. Algorithmica, 84(10):3054–3074, 2022.

- [GK17] Daniel Golovin and Andreas Krause. Adaptive submodularity: A new approach to active learning and stochastic optimization. CoRR, abs/1003.3967, 2017.

- [GKNR15] Anupam Gupta, Ravishankar Krishnaswamy, Viswanath Nagarajan, and R. Ravi. Running errands in time: Approximation algorithms for stochastic orienteering. Math. Oper. Res., 40(1):56–79, 2015.

- [GM09] Sudipto Guha and Kamesh Munagala. Multi-armed bandits with metric switching costs. In Automata, Languages and Programming, 36th Internatilonal Colloquium (ICALP), pages 496–507, 2009.

- [GN13] Anupam Gupta and Viswanath Nagarajan. A stochastic probing problem with applications. In IPCO, pages 205–216, 2013.

- [GNS17] Anupam Gupta, Viswanath Nagarajan, and Sahil Singla. Adaptivity gaps for stochastic probing: Submodular and XOS functions. In Proceedings of the Twenty-Eighth Annual ACM-SIAM Symposium on Discrete Algorithms (SODA), pages 1688–1702, 2017.

- [INvdZ16] Sungjin Im, Viswanath Nagarajan, and Ruben van der Zwaan. Minimum latency submodular cover. ACM Trans. Algorithms, 13(1):13:1–13:28, 2016.

- [JLLS20] Haotian Jiang, Jian Li, Daogao Liu, and Sahil Singla. Algorithms and Adaptivity Gaps for Stochastic k-TSP. In 11th Innovations in Theoretical Computer Science Conference (ITCS), volume 151, pages 45:1–45:25, 2020.

- [KKM05] Haim Kaplan, Eyal Kushilevitz, and Yishay Mansour. Learning with attribute costs. In Proceedings of the Thirty-Seventh Annual ACM Symposium on Theory of Computing, page 356–365, 2005.

- [Liu22] Naifeng Liu. Two 6-approximation algorithms for the stochastic score classification problem. CoRR, abs/2212.02370, 2022.

- [Mor82] Bernard M. E. Moret. Decision trees and diagrams. ACM Comput. Surv., 14(4):593––623, December 1982.

- [PS22] Benedikt M. Plank and Kevin Schewior. Simple algorithms for stochastic score classification with small approximation ratios. CoRR, abs/2211.14082, 2022.

- [SS22] Danny Segev and Yaron Shaposhnik. A polynomial-time approximation scheme for sequential batch testing of series systems. Oper. Res., 70(2):1153–1165, mar 2022.

- [Ü04] Tonguç Ünlüyurt. Sequential testing of complex systems: a review. Discrete Applied Mathematics, 142(1):189–205, 2004.

Appendix A Handling Negative Weights

We now show how our results can be extended to the case where the weights may be positive or negative. For the stochastic score classification problem (), we provide a reduction from any instance (with aribtrary weights) to one with positive weights. Let be any instance of , and let (resp. ) denote the items with positive (resp. negative) weight. Note that we can re-write the total weight as follows:

| (16) |

Consider now a new instance with the variables for and for . The probabilities are for and for . The weights are for and for ; note that all weights are now positive. The costs remain the same as before. For any realization , the new weight is , using (16). Finally the class boundaries for the new instance are . It is easy to check that a realization in the new instance has class if and only if the corresponding realization has class in the original instance .

Explainable -halfspace evaluation.

To handle negative weights in -d-, we need to apply the above idea within the algorithm (it is not a black-box reduction to positive weights). At a high level, we use the fact that the algorithm simply interleaves the separate lists for each halfspace.

Consider any halfpsace with both positive and negative weights. Let and denote the items with positive and negative weight respectively (for halfspace ). We then rephrase as the following halfspace .

Correspondingly, we define two non-negative rewards and (for halfspace ) as follows.

Note that after probing a subset , the total (resp. ) reward corresponds to a lower (resp. upper) bound on the left-hand-side of the modified halfspace , which allows us to evaluate the original halfspace . The rest of the algorithm remains the same as in §5. The analysis also remains the same.

Appendix B Proof of Theorem 2.1

Recall the setting of Theorem 2.1. We are given a set of items with non-negative costs and rewards , along with a budget . The goal is to select a subset of items of total cost at most that maximizes the total reward. The following is a natural LP relaxation of the knapsack problem where the objective is expressed as a function of the budget .

The following algorithm solves the fractional knapsack problem and also obtains an approximate integral solution. Assume that the items are ordered so that . Let index the first item (if any) so that . Let which lies in . Define

Return as the optimal fractional solution and as an integer solution. We restate Theorem 2.1 for completeness.

Theorem B.1.

Consider algorithm on any instance of the knapsack problem with budget .

-

1.

and so is an optimal LP solution.

-

2.

The derivative .

-

3.

Solution has cost and reward .

-

4.

is a concave function of .

Proof.

Proof. Let be an optimal LP solution. If , we are done. Suppose that , and assume without loss of generality that ; else we can obtain a greater reward by raising . Let be the smallest index such that : note that is well defined by the definition of . Let be the largest index with : note that such an index must exist as . Moreover, by definition of our solution . As , we have from above. Define a new solution

Above, . Intuitively, we are redistributing cost from item to . Note that the cost of the new solution . Moreover, the reward

where we used which follows from and the ordering of items. Finally, by choice of , either or . It follows that is also an optimal LP solution. Repeating this process, we obtain that is also an optimal LP solution. This completes the proof of property (1).

For property (2), observe that

as desired.

Since , we have and , proving property (3).

Finally, using property (2) and the non-increasing order of the items, it follows that is a concave function. This proves property (4).

Appendix C An Information-Theoretic Lower Bound for

Here, we present an information theoretic lower bound for . Recall that an instance of consists of independent Bernoulli random variables , where variable is with probability , and its realization can be probed at cost . The score of the outcome is where for all . Additionally, we are given thresholds which define intervals where . These intervals define a score classification function ; precisely when . The goal is to determine at minimum expected cost.

Let correspond to a realization of the variables . Furthermore, suppose that ; that is, under realization , the score lies in . Let correspond to the set of probed variables. Recall that is a feasible solution for under realization when the following conditions on the and rewards of hold: and where and . Thus, the following integer program computes a lower bound on the probing cost needed to conclude that .

| minimize | ||||

| subject to | (17) | |||

where , for , is a binary variable denoting whether is probed. Let denote the optimal value of (17). Then, is an information-theoretic lower bound for the given instance. We note that (17) only provides a lower bound on the probing cost for realization , and is not a formulation for the given instance.

Appendix D Additional Tables

Here we give more detailed tables for the average performance ratio (cost of the algorithm divided by the information-theoretic lower bound) of the various algorithms. For each instance type (, Unweighted and ) and each value of , we report the performance ratio averaged over all instances (10 each). Values closer to demonstrate better performance.

| Our Alg. | GGHK Alg. | Random List | |

|---|---|---|---|

| Our Alg. | GGHK Alg. | Random List | |

|---|---|---|---|

| 100 | 1.31 | 1.30 | 1.39 |

| 200 | 1.26 | 1.25 | 1.32 |

| 300 | 1.15 | 1.15 | 1.26 |

| 400 | 1.27 | 1.26 | 1.40 |

| 500 | 1.32 | 1.31 | 1.40 |

| 600 | 1.21 | 1.20 | 1.28 |

| 700 | 1.21 | 1.20 | 1.36 |

| 800 | 1.20 | 1.20 | 1.28 |

| 900 | 1.24 | 1.23 | 1.29 |

| 1000 | 1.29 | 1.29 | 1.36 |

| Our Alg. | GGHK Alg. | Random List | |

|---|---|---|---|

| 100 | 1.12 | 1.11 | 1.15 |

| 200 | 1.16 | 1.16 | 1.20 |

| 300 | 1.21 | 1.20 | 1.34 |

| 400 | 1.09 | 1.09 | 1.14 |

| 500 | 1.12 | 1.12 | 1.16 |

| 600 | 1.13 | 1.13 | 1.17 |

| 700 | 1.15 | 1.15 | 1.25 |

| 800 | 1.12 | 1.12 | 1.14 |

| 900 | 1.11 | 1.11 | 1.16 |

| 1000 | 1.10 | 1.10 | 1.15 |

| Our Alg. | GGHK Alg. | Random List | |

|---|---|---|---|

| 100 | 1.56 | 1.97 | 2.47 |

| 200 | 1.55 | 1.46 | 2.42 |

| 300 | 1.59 | 1.69 | 2.19 |

| 400 | 1.61 | 2.07 | 2.31 |

| 500 | 1.38 | 1.65 | 1.95 |

| 600 | 1.63 | 1.72 | 2.41 |

| 700 | 1.63 | 1.55 | 2.35 |

| 800 | 1.74 | 1.87 | 3.39 |

| 900 | 1.64 | 1.78 | 2.54 |

| 1000 | 1.60 | 3.69 | 2.26 |

| Our Alg. | GGHK Alg. | Random List | |

|---|---|---|---|

| 100 | 1.35 | 1.55 | 1.73 |

| 200 | 1.29 | 1.37 | 1.57 |

| 300 | 1.34 | 1.53 | 1.79 |

| 400 | 1.35 | 1.44 | 1.76 |

| 500 | 1.35 | 1.46 | 1.77 |

| 600 | 1.36 | 1.44 | 1.83 |

| 700 | 1.30 | 1.28 | 1.71 |

| 800 | 1.37 | 1.46 | 1.79 |

| 900 | 1.39 | 1.54 | 1.82 |

| 1000 | 1.26 | 1.46 | 1.58 |

| Our Alg. | GGHK Alg. | Random List | |

|---|---|---|---|

| 100 | 1.23 | 1.36 | 1.47 |

| 200 | 1.20 | 1.54 | 1.39 |

| 300 | 1.22 | 1.43 | 1.52 |

| 400 | 1.25 | 1.39 | 1.56 |

| 500 | 1.22 | 1.26 | 1.53 |

| 600 | 1.19 | 1.38 | 1.38 |

| 700 | 1.25 | 1.41 | 1.50 |

| 800 | 1.19 | 1.51 | 1.46 |

| 900 | 1.26 | 1.29 | 1.46 |

| 1000 | 1.23 | 1.31 | 1.46 |

| Our Alg. | DHK Alg. | Random List | |

|---|---|---|---|

| 100 | 2.21 | 1.85 | 4.14 |

| 200 | 2.14 | 1.61 | 6.28 |

| 300 | 2.36 | 1.66 | 6.79 |

| 400 | 2.28 | 1.66 | 7.15 |

| 500 | 2.26 | 1.75 | 7.58 |

| 600 | 2.13 | 1.74 | 5.70 |

| 700 | 2.12 | 1.81 | 4.80 |

| 800 | 2.12 | 1.76 | 5.13 |

| 900 | 2.10 | 1.77 | 4.75 |

| 1000 | 2.11 | 1.85 | 3.96 |