Procurements with Bidder Asymmetry in Cost and Risk-Aversion

Abstract

We propose an empirical method to analyze data from first-price procurements where bidders are asymmetric in their risk-aversion (CRRA) coefficients and distributions of private costs. Our Bayesian approach evaluates the likelihood by solving type-symmetric equilibria using the boundary-value method and integrates out unobserved heterogeneity through data augmentation. We study a new dataset from Russian government procurements focusing on the category of printing papers. We find that there is no unobserved heterogeneity (presumably because the job is routine), but bidders are highly asymmetric in their cost and risk-aversion. Our counterfactual study shows that choosing a type-specific cost-minimizing reserve price marginally reduces the procurement cost; however, inviting one more bidder substantially reduces the cost, by at least 5.5%. Furthermore, incorrectly imposing risk-neutrality would severely mislead inference and policy recommendations, but the bias from imposing homogeneity in risk-aversion is small.

Keywords: Asymmetric first-price procurements, Asymmetric risk-aversion, Identification and estimation, Statistical decision theory, Unobserved heterogeneity.

1 Introduction

This paper proposes a Bayesian method to analyze data from first-price (sealed-bid) procurements (FPP) with bidder-asymmetry in cost and risk-aversion. In particular, we consider a theoretical model of FPP with exogenous entry and type-symmetric Bayesian Nash Equilibrium bidding strategies. Here, a type of bidder refers to a pair of cost density and constant relative risk-aversion (CRRA) coefficient. For this setting, Campo (2012) identifies the model primitive (cost densities and CRRA coefficients) and proposes an indirect semiparametric estimation method. The empirical literature, however, has seldom considered asymmetry in both cost and risk-aversion. We, therefore, have limited empirical insights on the effects of asymmetric risk-aversion on procurement outcomes.

The main contribution of this paper is to develop a novel empirical procedure that produces reliable inference for asymmetric FPPs by combining and extending several state-of-the-art methods in the literature. First, the procedure explores the posterior distribution over the space of the model primitive by a Markov chain Monte Carlo (MCMC) algorithm (Kim, 2015). Second, we model the (procurement-specific) unobserved heterogeneity as additional latent components that are distributed jointly with the model primitive under the posterior so that we can integrate out the latent components via MCMC. This strategy to get around the difficulty of handling missing variables is known as data augmentation, which Li and Zheng (2009) and Aryal, Grundl, Kim, and Zhu (2018), among others, use to study auction markets. Third, we extend the boundary-value method of Fibich and Gavish (2011) to compute the type-symmetric equilibrium strategies for risk-averse bidders in FPPs and use it in our MCMC algorithm. Note that the literature has often used the backward-shooting method of Marshall, Meurer, Richard, and Stromquist (1994) to compute asymmetric bidding strategies, which is, however, shown to be inherently unstable near the boundary of the support; see Fibich and Gavish (2011). The boundary-value method is reliable everywhere and, therefore, is more suitable for evaluating likelihoods and conducting policy simulations.

In addition, our Bayesian method provides a natural framework for formal decision-making under parameter uncertainty. In particular, we consider the policymaker who wishes to choose a reserve price to minimize the (expected) procurement cost when there is uncertainty about the model primitives. Our decision method computes the procurement cost under a model primitive at a given, possibly type-specific, reserve price, which to our knowledge is the first in the empirical auction literature; see Kotowski (2018) for theoretical developments on this topic. For this step, we further extend the algorithm of Fibich and Gavish (2011) to accommodate binding reserve prices and evaluate the procurement cost by simulating equilibrium bids. The decision method then integrates out the model primitive by the posterior, resulting in the (posterior) predictive procurement cost at the said reserve price. Finally, our method selects a reserve price that gives the smallest predictive cost.

This solution is also coherent under the rationality axioms for a decision-maker in Savage (1954) and Anscombe and Aumann (1963). See also Kim (2013), Aryal and Kim (2013), Kim (2015), and Aryal, Grundl, Kim, and Zhu (2018) for applications of statistical decision theory in empirical auction design problems. This paper is the first to conduct such detailed counterfactual simulations for FPPs with asymmetric costs and risk-aversion.

Using our empirical method, we study a new dataset with FPPs from Russian public procurements conducted in 2014. (Charankevich (2021) investigates a sample of “open auctions” in the Russian procurements, which is different from the sample of FPPs that we analyze here.) In Russia, all government units purchase a wide range of goods and services through public procurements, which accounts for 7% of Russian GDP in 2014. Since the economic transition beginning in the 1990s, Russia has been revising the procurement system through several legislative changes and technological innovations to establish transparent competition among the suppliers to reduce the government expenditure. It is, therefore, critical for the policymaker to learn the economic fundamentals of the procurement system and evaluate alternative policy options for further improvements. We illustrate how the policymaker can achieve the goals applying our method to the data.

The Russian procurement system practices several allocation methods and selects one of them, e.g., FPP or “open auctions,” depending on the nature of the project and according to the relevant federal laws. For example, small projects (reserve price below \stackengine.64ex\stackengine.4exP OrFFL OrFFL500,000) must use an FPP. In total, there are 102 different categories in FPPs based on different goods and services. The categories are separate, each with its own market and a different set of suppliers. We choose one category to analyze by applying a set of selection criteria mostly concerning the sample size. We divide bidders into three types: type 1 (frequent) bidders bid in at least 10% of the procurements and type 3 (fringe) bidders only once, and type 2 are the remainders. Among the four categories complying with our selection criteria, we choose to analyze the category of “printing papers,” as it has the largest sample with 411 procurements. In the “printing papers” category, 1, 171, and 402 unique bidders are of types 1, 2, and 3, and we observe a total of 58, 625, and 402 bids, respectively.

On average, type 1 bidder bids lower than type 2, and type 2 lower than type 3. The differences in bids may arise because of differences in costs or risk-aversion. The posterior of the model parameters (model primitive) reveals that the ordering of risk-aversion is the opposite of the observed bid pattern. In particular, the CRRA coefficient of type 1 (frequent) bidder is roughly 0.2, whereas the coefficients of type 2 and 3 bidders are respectively 0.8 and 0.9. But, the predictive cost densities suggest that type 1 bidder tends to draw smaller costs than type 2, and type 2 smaller than type 3. Therefore, the difference between the cost densities is substantial enough to explain the bid pattern, despite the reversely ordered risk-aversion. Our analysis also finds no variation in the unobserved heterogeneity, which is consistent with the job of supplying papers being routine.

Our estimates of the model parameters are coherent with our findings in the counterfactual policy analysis. All bidders, except the most frequent bidder, exhibit high risk-aversion. So, the policymaker should prefer FPP to second-price procurements (SPP) (Holt, 1980) and choose a large reserve price in an FPP (Hu, Matthews, and Zou, 2010). In particular, we find that when a single reserve price is used for all bidders, the current mechanism is cost-minimizing. Recall also that when bidders are asymmetric, choosing a single reserve price would be suboptimal. Although there is no closed-form expression for the reserve prices as in Myerson (1981) due to risk-aversion, our method allows evaluating the procurement costs at different type-specific reserve prices. It recommends lowering the reserve price for type 1 by 4% from the current reserve price, but leaving other types’ prices unchanged. In that case, however, our method predicts a cost reduction only of 0.2%, suggesting that the current mechanism is effectively cost-minimizing.

In addition, we consider a scenario where the policymaker may invite an additional bidder in the spirit of Bulow and Klemperer (1996). For symmetric FPPs, the article implies that an FPP without a reserve price generates lower expected costs than optimally chosen reserve price but with one less bidder. We find that this insight holds in our context with bidders who are asymmetric in both cost densities and risk-aversion. In particular, adding one bidder of type 1, 2, and 3 reduces the predictive procurement cost by 6.2%, 5.8%, and 5.5%, respectively. Thus, even one additional fringe bidder substantially lowers the cost.

Moreover, we investigate the implications on the procurement cost and efficiency of incorrectly assuming either risk neutrality or an identical CRRA parameter for all bidders. When one ignores risk-aversion, small bids in the data inflate the left tail of the cost densities, which then tilts cost-minimizing reserve prices toward zero. As a result, the misspecified model selects a small reserve price, predicting 14.0% of cost-reduction. But, this result is misleading because the model with asymmetric CRRAs predicts a 15.2% of increase in the cost at that price. The misspecified model predicts that the efficient bidder wins with 33.2% of probability, whereas the model with asymmetric CRRAs predicts that the probability would be 6.0%. We find that the model with a common CRRA overall approximates our analysis with asymmetric CRRAs, except for overestimating type 1 bidder’s CRRA coefficient.

Nevertheless, one should not conclude that the model with identical risk-aversion always approximates the model with asymmetric risk-aversion because the approximation quality may depend on the model primitive, a priori unknown to the researcher. Our method with asymmetric CRRAs is not computationally more expensive than the model with a common CRRA. Therefore, there is no reason to impose homogeneity in CRRA coefficients. Finally, our analysis is robust to alternative definitions of bidder types, the prior over the parameter that indexes the cost densities, and the density specification of unobserved heterogeneity.

The paper proceeds as follows. Section 2 describes our model and its identification. Sections 3 and 4 present our data and econometric method, respectively. Section 5 discusses the empirical results and counterfactual analysis. Section 6 concludes with feasible extensions. The detailed information about data, computational detail, and additional results are in Supplementary Appendix (Aryal, Charankevich, Jeong, and Kim, 2022a).

2 Model and Identification

Consider a procurement that allocates a project to one of the bidders in the set with . Bidders submit their bids simultaneously, and the one with the lowest bid wins the project at a price equal to her bid, which we refer to as the first-price procurement (FPP). Let bidder ’s cost be , which follows the distribution and is independent of other bidders’ costs. We make the following assumptions on the cost distributions.

Assumption 1.

Bidder ’s cost distribution has a density on the support , and for two different bidders it can be that for some .

In addition, bidder exhibits constant relative risk-aversion (CRRA) with coefficient, .

Assumption 2.

Bidder ’s utility function is given by for consumption with the parameter , and it can be that if .

The CRRA specification has been widely used due to its convenient functional form in the auction literature, e.g., Bajari and Hortaçsu (2005), Lu and Perrigne (2008), Campo, Guerre, Perrigne, and Vuong (2011), and Aryal, Grundl, Kim, and Zhu (2018). Such convenience also allows the boundary-value method of Fibich and Gavish (2011) to accommodate bidder-specific risk-aversion in this paper, and one may compare the coefficients with previous estimates due to its prevalence.

If bidder wins the procurement at price , her utility is under Assumption 2. While the realizations of costs are bidders’ private information, cost distributions and risk-aversion parameters, , are assumed to be common knowledge. Bidder with cost chooses to maximize her expected utility given everyone else’s bidding strategy. Suppose all bidders other than bidder use strictly increasing equilibrium bidding strategies . Then bidder solves

Define , the inverse bidding strategy of bidder . Then, the optimal bid must satisfy the condition,

| (1) |

for all , implying a system of differential equations, which can be numerically solved with the boundary conditions and for all .

Since is unknown, the standard algorithm to solve (1), known as backward-shooting, starts with a guess of and adjusts its guess at each iteration (Marshall, Meurer, Richard, and Stromquist, 1994). Fibich and Gavish (2011), however, show that the backward-shooting algorithm is inherently unstable near the boundary and propose the boundary-value method to overcome the problem. We use their boundary-value method in our empirical method, where have to be evaluated at data points, including the ones near the boundary.

Identification.

Campo (2012) uses the exogenous variation in the bidder configuration to identify the parameters of interest. For completeness, we present the core intuition of the identification strategy in Campo (2012). Since are strictly increasing, the bid distribution of bidder is . Then, we can rewrite (1) as

| (2) |

where is the density of . Note that (2) in a procurement with gives

which gives Then, the exogenous variation in is sufficient for identification. For example, if we observe FPPs with , , and , we identify the CRRA coefficients as

where the right-hand side depends only on the bid densities that are directly identified from the data. Then, by substituting in (2), we identify the cost distributions.

Unobserved Heterogeneity.

Bidders may observe some aspects of the project that affect their costs (and hence their bids), which the researcher does not observe. Let denote such unobserved characteristics.

Assumption 3.

-

1.

with density on the support with a location normalization, e.g., is known.

-

2.

In procurement , is independent of bidder’s private cost, i.e., , for all bidders.

-

3.

The final cost for bidder with in procurement is given by .

Let be the distribution of for bidder and be the associated bidding strategies with the unobserved heterogeneity, . For and , where is bidder ’s equilibrium bidding strategy when ; see Liu and Luo (2017).

3 Russian Government Procurement

This section describes the institutional background of the government procurements in Russia, presents the dataset we analyze, and discusses the implications of the reserve price on our analysis in sections 4 and 5. In particular, the background description here identifies a few cases where observed bids might not be competitive and justifies the data we study as equilibrium outcomes after excluding those suspicious cases. It also motivates us to take cost-minimization as the primary policy objective in counterfactual analysis.

3.1 Institutional Background

All government bodies and public units in Russia purchase goods and services through government procurements. Examples of potential buyers include federal public authorities, regional governments, city councils, public hospitals, and schools. Hundreds of goods and services, e.g., car tires, hardcover textbooks, road maintenance, and printing papers, are traded via the official platform, “Unified Information System (UIS: zakupki.gov.ru).” (We use quotation marks to indicate field terms in their closest English translation. Moreover, procurement here is a general term referring to procuring something unless it comes with a technical qualifier, e.g., first-price procurement.) The public procurements are economically significant; according to the UIS, concluded contracts in 2014 add up to 5.47 trillion RUB (7% of Russian GDP, statistical.com).

Since the economic transition beginning in the 1990s, Russia has been revising the procurement system through several changes in legislation and modernizing it via technical innovations. Those reforms aim to reduce government spending and improve outcomes by creating a competitive environment for suppliers; especially by encouraging suppliers’ participation as well as eliminating corruption between government agents and suppliers. In particular, Federal Law No. 94-FZ (21 July 2005) laid a foundation for the current form of the system. The Law introduced the concept of “maximum (or initial contract) prices” and prohibited “closed procurements,” i.e., a negotiation inviting a single supplier, except for special cases such as projects involving state secrets.

Before the Law (94-FZ), the government agent overseeing the procurements had considerable freedom to choose a supplier and set a price. Therefore, the agent (buyer) could set a high price and select an “insider” (a supplier in collusion) to carry out the project at a cost lower than the price and share the margin. The legislation mandates that a “maximum price” must be chosen in such a way that participation of general suppliers is encouraged for “healthy competition,” and the price can still be justifiable given the nature of the project, market conditions, and historical data. For example, a buyer should be able to purchase comparable goods and services at the “maximum price” outside the procurement system. (The UIS provides protocols and official methods for setting a “maximum price” to handle different situations.) Section 3.3 below discusses the implications of “maximum price” for our analysis.

For projects with a “maximum price” above \stackengine.64ex\stackengine.4exP OrFFL OrFFL100,000 ($2,600), the procurer must select a supplier through a competitive procedure. The “maximum price” is then publicly announced, and any legal entity can participate with no entrance fee. The announcement should be placed at least four business days before the closing date if the “maximum price” is below \stackengine.64ex\stackengine.4exP OrFFL OrFFL250,000 (and seven days if above) to prevent buyers from selecting an “insider” by setting a tight deadline.

In addition, to improve transparency, by Federal Law No. 44-FZ (1 January 2014), the UIS publicly announces forthcoming procurements and maintains all procurement data, e.g., participants’ identities, their offers, and the winner for every procurement, and the UIS provides a platform to run a procurement. The system practices several allocation methods, including negotiation and contest, and one of them is “sealed-bid auction” in the field term. When the latter is implemented, bidders submit their initial documents in a sealed envelope (or online, but rarely in 2014). In the presence of all participants, then, each bidder makes a final decision on her bid and, finally, the procurer opens all the bids (Federal Law No. 44-FZ, article 78 of paragraph 3). Note that the procurer, here, is a government agency running procurements on behalf of buyers, other government agents. The lowest bidder wins at a price equal to her bid, if not higher than the “maximum price.” The mechanism is, therefore, the first-price procurement (FPP), where bidders know whom they oppose, and the “maximum price” plays the role of a reserve price in FPPs.

FPPs are used for cases with a “maximum price” below \stackengine.64ex\stackengine.4exP OrFFL OrFFL500,000, i.e., small projects. But, the penalty for a supplier in corruption, e.g., “insider,” is \stackengine.64ex\stackengine.4exP OrFFL OrFFL500,000 plus a full reimbursement of expenses. The supplier is also publicly marked as “unreliable” for two years. In addition, the fine for the government agent in corruption is \stackengine.64ex\stackengine.4exP OrFFL OrFFL50,000 with a three-year job suspension.

Despite all the legal devices to eliminate corruption, a buyer can still invite an “insider” only. For example, a buyer could deliberately make a typographical error, e.g., replacing a Cyrillic letter with a similar Latin letter in keywords. Then, only the insider can easily search for it in the system. Therefore, the cases with only one bidder can be suspicious. Even when multiple bidders appear in a procurement, there can be corruption. For example, the agent could invite shill bidders who submit bids with no chance of winning, e.g., bidding higher than the reserve price. Alternatively, the agent may manipulate submitted bids to increase the winning probability of the insider. Charankevich (2021) reports evidence of bid manipulation by exploring procurement outcomes and non-reported (or missing) bids in “open auctions,” which can be viewed as an oral-descending procurement. Considering all these, in our analysis, we exclude observations with only one bidder, bids above reserve prices, or missing bids to avoid those suspicious cases.

3.2 Data: category “printing papers”

The procurements with FPPs provide an ideal setting to study asymmetry in both cost densities and risk-aversion for the following reasons. First, bid data from FPPs allow us to identify the risk-aversion parameters. Second, FPPs are less prone to collusion among the bidders than oral-descending procurements because bidders do not observe other bidders’ behavior (Robinson, 1985). Third, since FPPs are used for projects with small budgets, they may attract small firms that are likely to be risk-averse (Herranz, Krasa, and Villamil, 2015). Indeed, the test of Jun and Zincenko (2022) rejects risk-neutrality in favor of risk-aversion (p-value ) for each symmetric FPPs, i.e., type 2 bidders only and type 3 bidders only with types defined below.

Finally, projects with small budgets are homogeneous and frequent, i.e., the bid preparation cost would be minimal, and the jobs are routine. To this end, we fail to reject the independence of any two randomly selected bids in the same FPP (p-value ) via the test used by Krasnokutskaya (2011) with 1,000 bootstrapped samples. For these reasons, the procurement-specific unobserved heterogeneity might not be substantial, which section 5 shall confirm from the data.

The UIS provides data on 42,828 FPPs in 2014 across 102 categories of different goods and services; see section S3.1 for the list of the categories and some statistics. We consider each category as an independent set of procurements because they are separated by industries with different sets of suppliers. Now, we explain how we select a category to analyze; see also section S3.1. In each category, first, we rule out all procurements with one bidder because they are vulnerable to corruption (section 3.1) and are not even bidding competition. We then exclude procurements with missing bids, which may arise due to bid manipulation (Charankevich, 2021). We also discard the procurements with bids larger than reserve prices because those bids could be shill bids as discussed or could signal that the reserve prices are set too low, violating the UIS protocols to select a reserve price.

After excluding these three cases, we group bidders into three types: in each category, type 1 bidders bid in at least ten percent of the FPPs, type 3 bidders bid once, and type 2 bidders are all the others. We define the bidder types by the participation rate because it is the only exogenous bidder-specific attribute in the data, besides their identities. (Section 5.3 considers alternative definitions.) Since the identification strategy relies on the variation in the bid for each type and bidder configuration, we sort out categories with at least 50 bids for each type to estimate the type-specific parameters. Four categories satisfy this condition. Among them, we analyze the one with the largest sample, which is the category of “printing papers” with procurements. (In the previous version of this paper, Aryal, Charankevich, Jeong, and Kim (2020) study the four categories separately, where the other ones have 228, 235, and 305 procurements.)

The category “printing papers” refers to white A4 paper for printing, copying, and faxing. A typical order specifies A4 white papers in packs of 500 sheets. The paper can vary from “regular white” of 92-94% (ISO) to “premium white” above 98% (ISO). A standard contract includes the delivery term that can range from 5 to 30 days and provision for the fulfillment of incomplete orders and replacement or exchange of damaged goods within 3 to 10 days after delivery. As mentioned above, any government unit can purchase the products, and any legal entity that can supply papers may bid in this category.

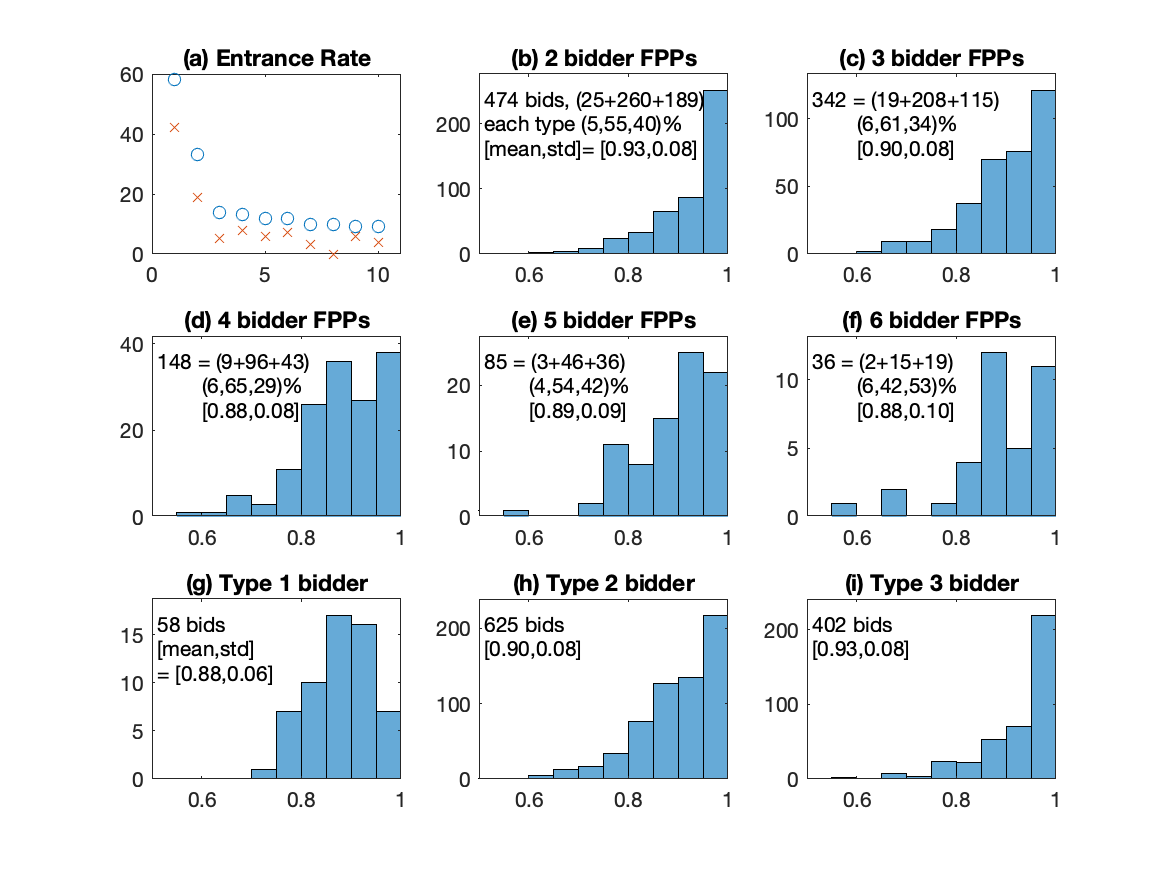

Now, we document some descriptive statistics of the data from the “printing papers” category. This category initially has 536 FPPs. Among them, we exclude 114 for having only one bid, three for missing bids, and eight for bids above the reserve price. Among the eight bids, five (three) were submitted by bidders who bid once (twice). No bidder repeats bidding above the reserve price, and no one wins with such a bid. In the sample of 411 procurements, we have one type 1 bidder who bids 58 times, 171 type 2 bidders with 625 bids, and 402 type 3 bidders. The second and third frequent bidders appear 33 and 14 times in the data. To assess how the type definition affects our analysis, in section 5.3 we change the definition of type 1 to include the second frequent bidder and then to also include the third frequent bidder. The entrance rate dramatically drops only for the first a few bidders; see the circles in Figure 1(a), suggesting that those bidders may differ from other bidders, i.e., asymmetry in model primitives. Section 5.3 also considers alternative type definitions based on how often each bidder wins; see the crosses in Figure 1(a).

Figure 1(b) shows the histogram of bids from procurements with two bidders. It has 474 bids and of them, i.e., %, are submitted by type bidders, respectively. The sample mean and standard deviation of the bids are 0.93 and 0.08. Panels (c)(f) similarly show the bid data for procurements with 3 to 6 bidders.

Recall that bidders know their competitors when bidding; see section 3.1. In the data, bidders appear to use the information on the competition. The bid distributions vary with the number of bidders, and there is a tendency that the average bid decreases in the number of bidders. We conduct the Kolmogorov-Smirnov (KS) test against the hypothesis that two marginal bid distributions are identical. The values are close to zero for all pairs involving the two bidder case (b) and for the pair of three bidder case (c) and four bidder case (d), rejecting the hypothesis of identical distributions. That is, we have some evidence that bidders appear to behave differently according to the competition level; section S3.2 gives more evidence. As the number of bidders grows, however, the bid distributions get harder to distinguish statistically. That might be because the bid weakly converges to the cost with the competition level. The number of bidders also gets noisier in measuring the competition because the bidder configuration becomes more variable when bidders are asymmetric.

On average, type 3 bidders bid higher than type 2 and type 2 higher than type 1 (panels (g)(i)). (For any pair of two types, the -value of the KS test is close to zero.) This pattern arises if type is either more efficient or more risk-averse than type . But, the cause of the pattern cannot be detected by reduced form analysis, motivating a structural approach.

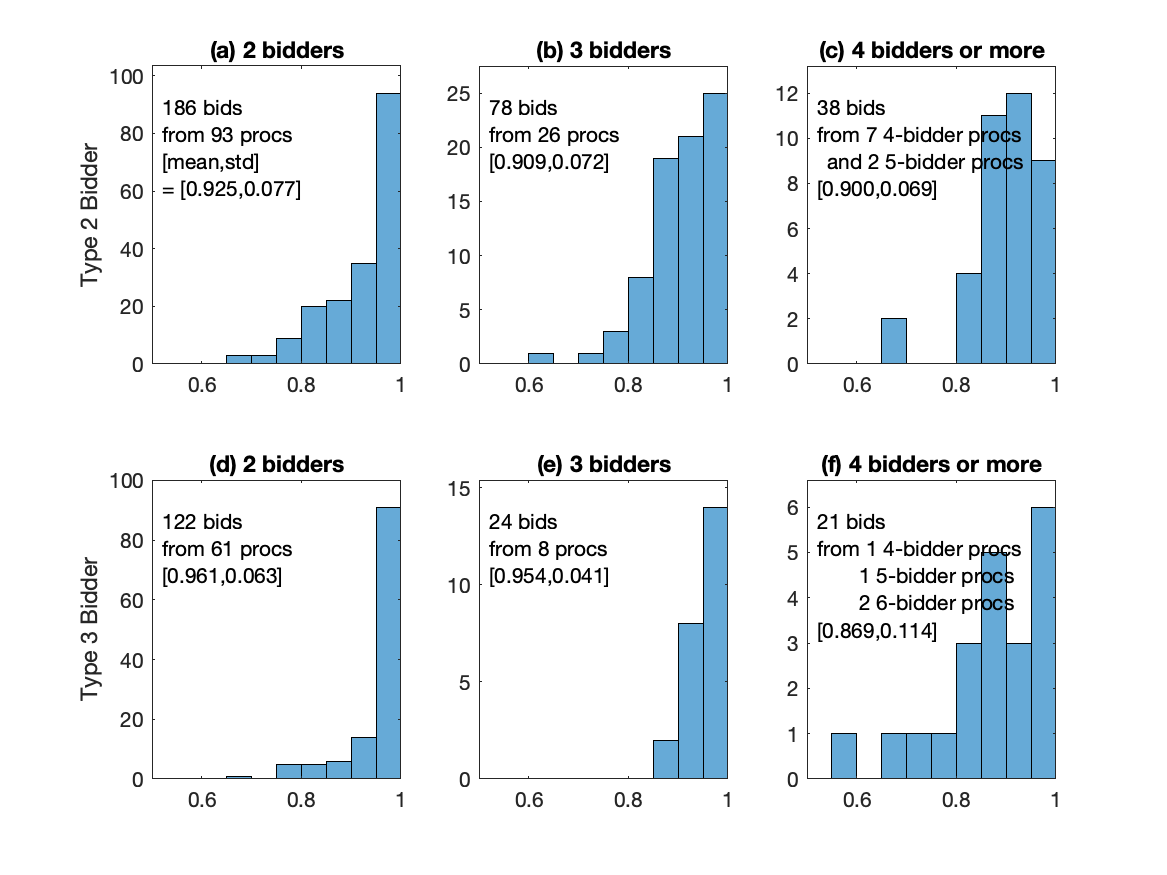

Figure 2 shows the bid histograms for symmetric procurements with only type 2 (3) bidders in the upper (lower) panels. Note that there is no symmetric procurements with type 1 bidder, as there is one type 1 bidder. The left and middle panels are for 2 and 3 bidder procurements and the right ones for the rest in the data. As discussed there, we conduct the KS test and get additional evidence that bidders’ behavior depends on the competition level, especially for the cases with sufficiently large bid samples.

Although we have excluded the procurements with bids above reserve prices, the high density near the reserve price may still seemingly suggest the presence of shill bids (no winning chance). According to the data, however, the bid of 0.99 gives a 14% chance of winning. Hence, the high density does not indicate shill bids. It is, instead, plausible that bidders’ optimal bids are actually near the reserve price because the reserve price has to be justifiable as a market price as discussed in section 3.1; see also section 3.3.

Finally, a group of suppliers may collude (not necessarily involving the government agent) to submit noncompetitive bids. Empirical methods to detect a bidding ring require bidders to be risk-neutral and a suspicious group of bidders to bid together in many procurements; see Schurter (2020) and references therein. It is infeasible to study a bidding ring using our data because even if the currently available methods may extend for risk-aversion, the dropping entrance rate in Figure 1(a) does not leave us any group of bidders jointly appearing in sufficiently many procurements. In particular, among 45 pairs of top ten frequent bidders, only eight have ever bid in the same procurements, but rarely: type 1 bidder met the frequent bidders times, respectively, and the and bidders met twice, the and bidders three times, and the and bidders five times.

3.3 Reserve Price

Recall that the reserve price is set sufficiently high to encourage suppliers’ participation and yet still justifiable as a market price to purchase comparable goods and services outside the procurement system. This description has three important implications on our analysis in the following sections. First, the procurement system does not use the reserve price to deter any bidder from entering, which alone might validate the reserve price as non-binding. Second, the description of the reserve price also implies that if a supplier incurred a cost higher than the reserve price, the cost is too high for the supplier to operate in the market, even outside the procurements. Hence, we do not consider such an inefficient supplier as a potential bidder in the procurement, and section 4 specifies the cost densities to have their support below the current reserve price, i.e., the latter is nonbinding. Third, in our policy simulations, when no bidder can bid below the counterfactual reserve price, we assume that the procurer carries out the job at the current reserve price; see section 5.2.

4 Inference Method

A set of bidders who can beat the reserve price is exogenously given for each procurement . Bidder with type has the CRRA coefficient and draws her cost from the cost distribution with density independently of other bidders. The cost density is strictly positive on , corresponding to the bid data normalized by the reserve price. Let , , and . Let be the bidding strategy when . That is, bidder bids where for all . When , bidder observes her cost and bid , which lies in . We model with the support of and Note that reflects the institutional feature that the reserve price does not exclude any bidder.

For estimation, we specify the cost density as

| (3) |

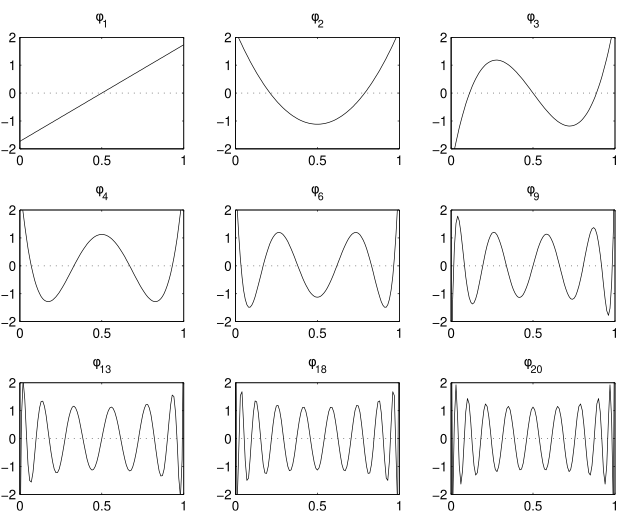

where is the vector of parameters and is the vector of the subsequent Legendre polynomials, defined on . Specifically, the -th entry in is given as where . The uniform component in (3) with the small weight ensures the density is strictly bounded away from zero.

Note that has extrema; see section S4 for graphs of for some s. As increases, the density of defined in (3) can approximate more complicated densities, i.e., the ones with many inflection points. Believing that the true cost densities are smooth, we put a smaller prior probability on larger by the prior with for all . Since the prior variance of decreases in , gets close to zero as increases, squeezing out the contribution of higher order components. Hence, cost densities with oscillations are less likely under our prior. Note that (3) is the uniform density at the prior mean of .

For the unobserved heterogeneity, we specify such that it implies

| (4) |

where the lower bound with such that , and the upper bound is set to 1 because the reserve price is non-binding, larger than the upper bound of the cost. To ensure that is sufficiently larger than zero, we restrict . This restriction implies the upper bound of , i.e., . We then use the uniform prior For the CRRA parameter, , we use a uniform prior , which excludes values near 1 to ensure that our computation does not fail due to the flat utility function, i.e., as . We collect the priors by where with and .

Conditional on , the bid in procurement has the density

| (5) |

for which we need to evaluate . To do so, section S5 modifies the boundary-value method to accommodate bidders with CRRA utility in FPPs, which Fibich and Gavish (2011) originally propose for risk-neutral bidders in high-bid auctions.

Then, the posterior density of the latent variables is given as

where , including bids and bidder configurations in the dataset. Once we have the posterior of the structural parameter , we are mostly interested in the posterior moments of important functions of . For a measurable function , its posterior moment is . The posterior mean () is often presented along with some uncertainty notions such as the posterior standard deviation, for which is also used. To evaluate the moments we first draws by a standard Markov chain Monte Carlo (MCMC) algorithm; see section S6. Then, we evaluate the moments by the MCMC draws, i.e., .

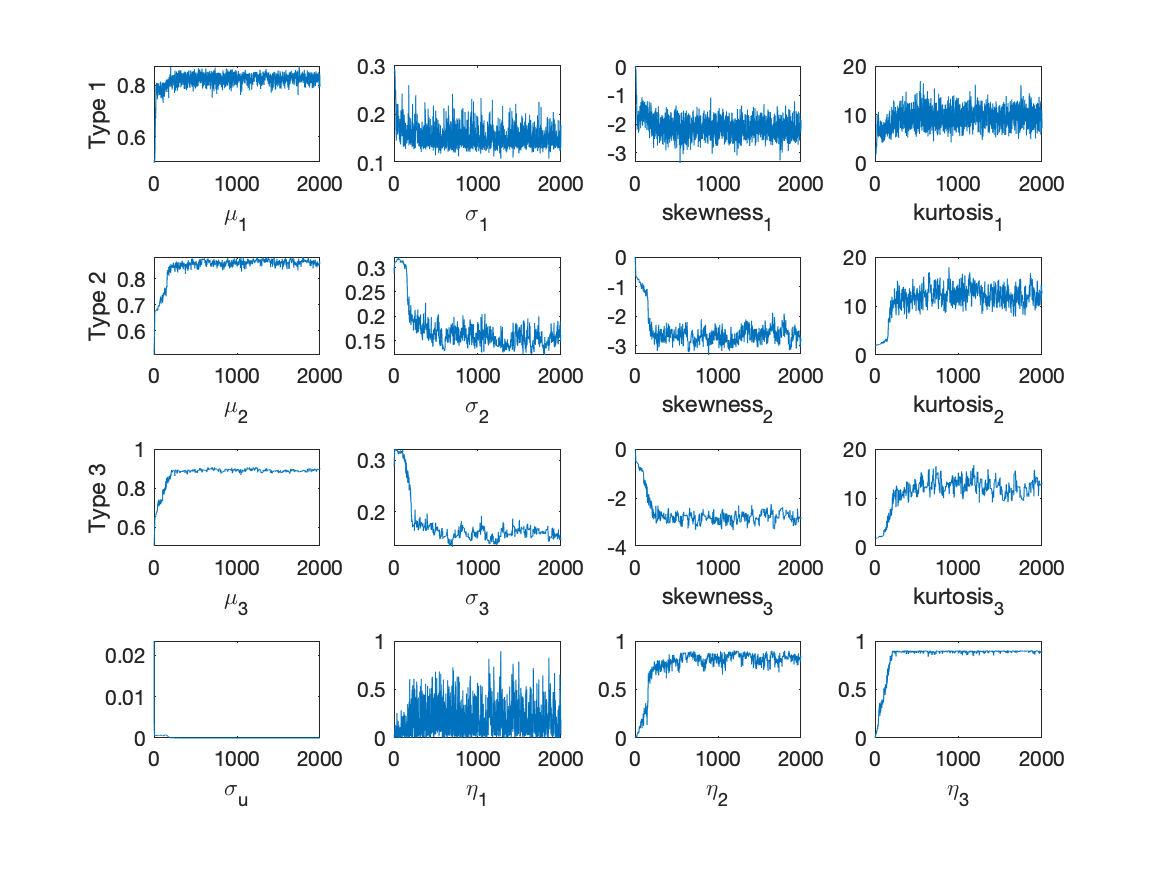

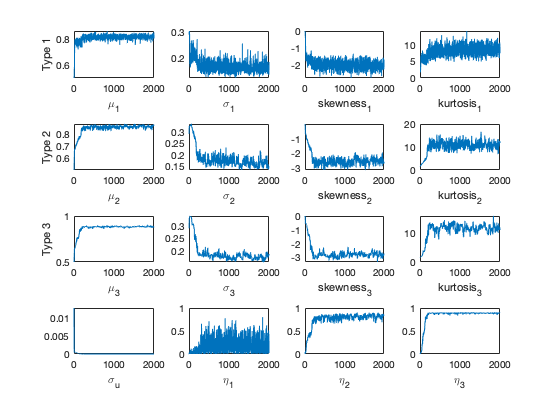

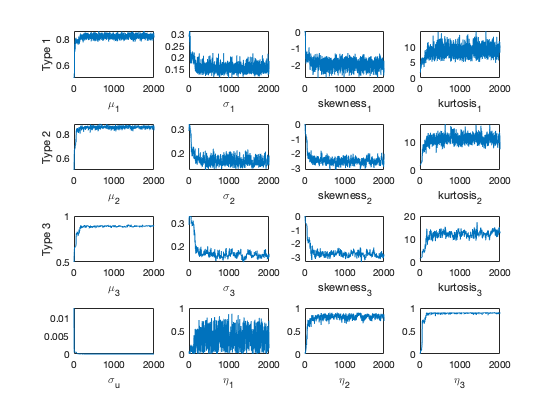

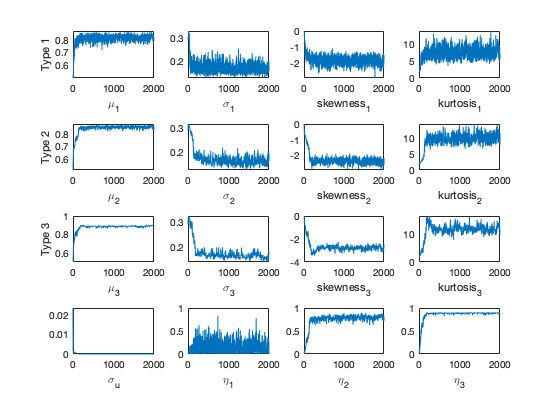

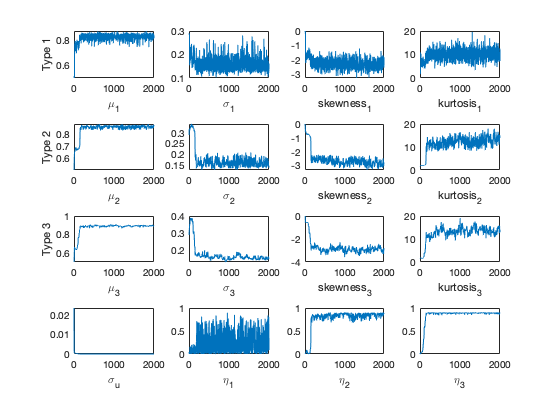

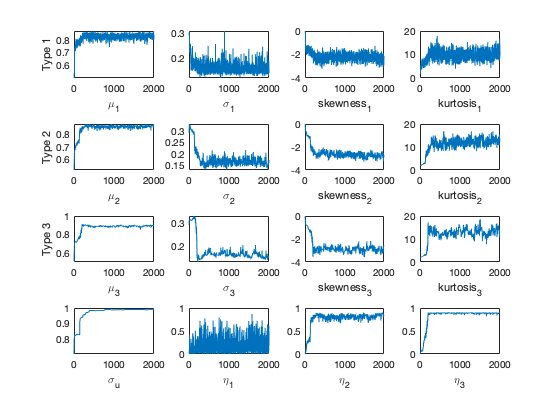

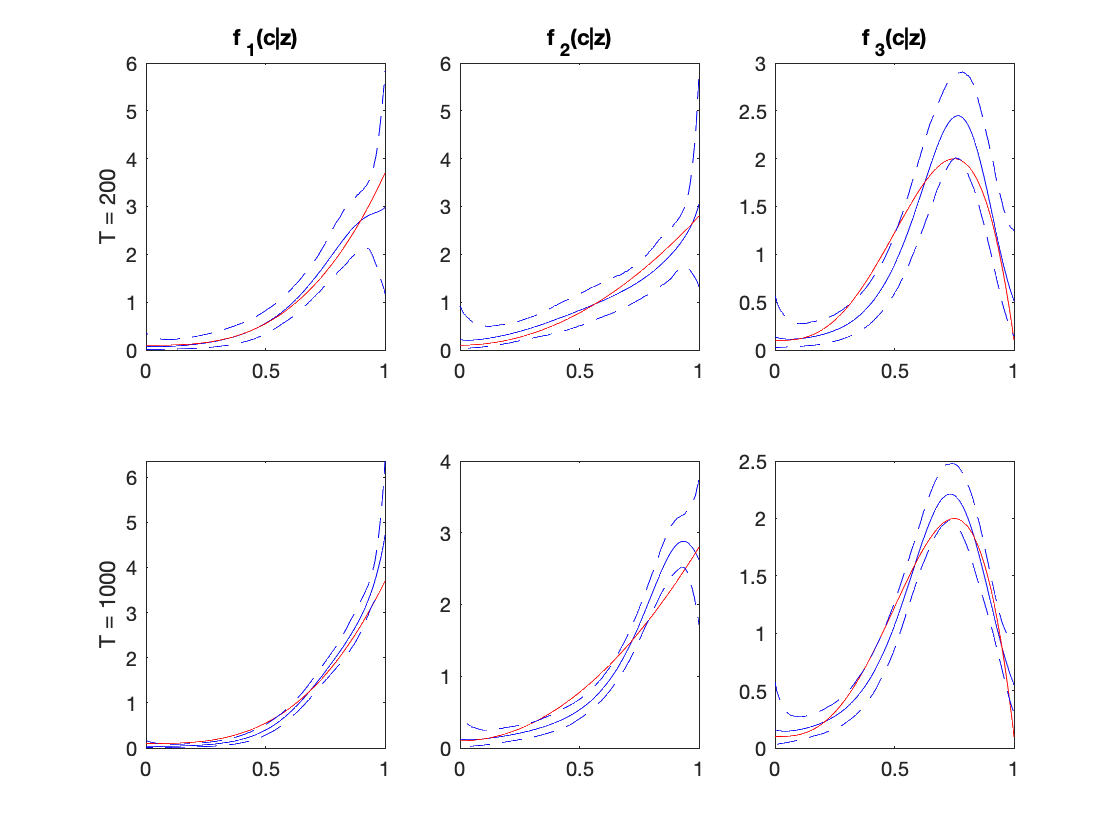

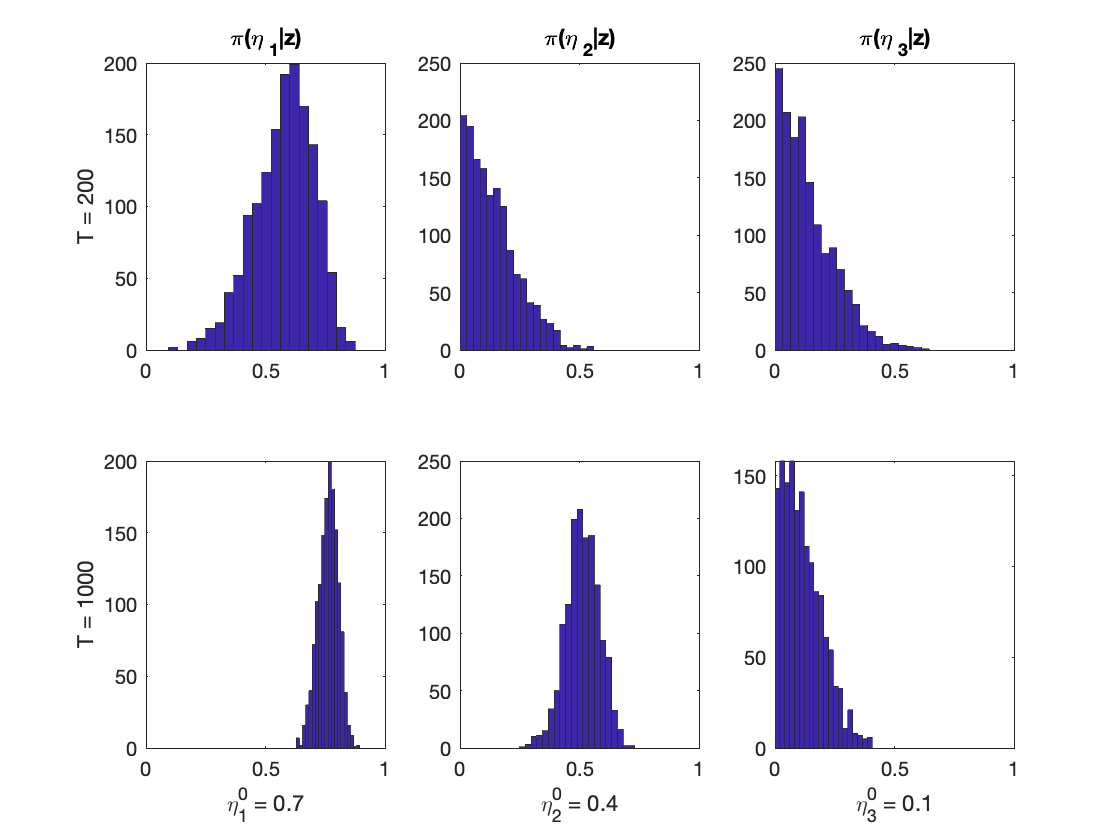

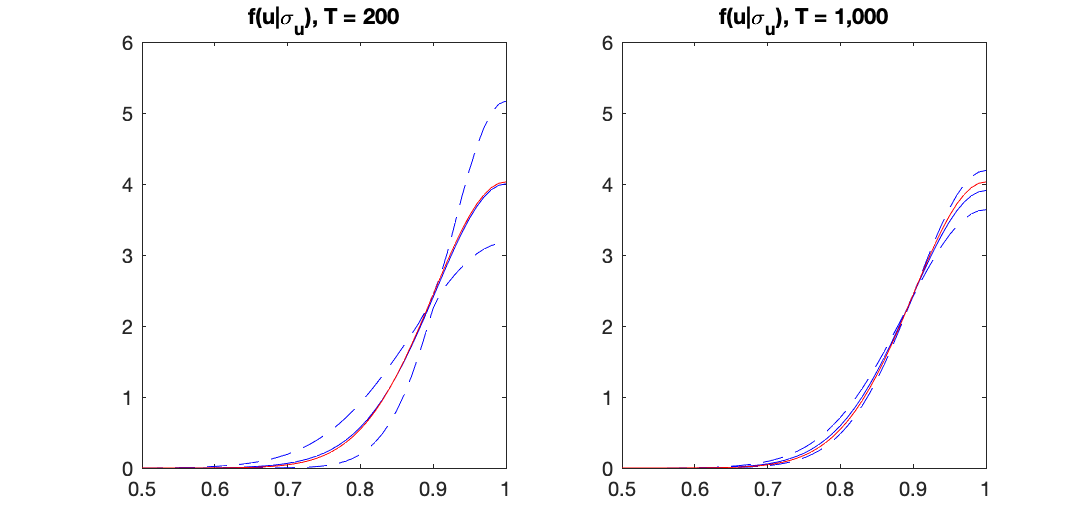

We conclude this section with a summary of section S7 that evaluates the performance of our method using simulated data. We consider three types of bidders, each with a different cost density and CRRA parameter, in FPPs with a substantial variation of bidder configurations: . We consider two cases: one with a substantial variation in the unobserved heterogeneity, , and the other with no variation . For each case, we consider two different sample sizes, for all s. Using those bid data we find that the MCMC traces are stable and converge quickly, and parameters are accurately estimated. As desired, the posterior of quantities of interests, such as and , becomes more precise around the true values, whether or , as the sample size increases.

5 Inference and Counterfactual Results

This section first summarizes the posterior distribution of the parameters of the model with asymmetric risk-aversion, and discusses the bias from two model misspecifications: imposing symmetric risk-aversion or ignoring risk-aversion altogether. Then, the section predicts procurement costs under counterfactual scenarios, and also quantifies the impacts of model misspecification in terms of procurement costs. Finally, the section concludes with some sensitivity analysis.

5.1 Posterior Inference

Asymmetric Risk-Aversion.

We sample from the posterior using the data discussed in section 3, allowing for bidder asymmetry in cost density and risk-aversion. The top block of Table 1 shows the posterior mean, standard deviation, and a 95% credible interval (2.5 and 97.5 percentiles) for each CRRA coefficient for and .

The estimates suggest that risk-aversion varies across the three types. Type 1 (most frequent) bidder is the least risk-averse, and type 3 (one-time) bidders are the most risk-averse. The posterior of has a considerable variation, and its mean is substantially smaller than the ones of and . The distribution of also differs from the one of , where the latter is more precise and (slightly) larger. Formally, the values of KS test are all close to zero, rejecting the hypothesis that and follow the identical marginal posterior distributions for . Section S8 discusses the use of KS test in Bayesian analysis.

In addition, there is no unobserved heterogeneity, , which is consistent with supplying A4 papers being routine. If present, any measurable variation in the unobserved heterogeneity should have led to a non-degenerate posterior of , even if the parametric assumption in (4) was incorrect. Section 5.3 also obtains a degenerate posterior of with a more flexible density of .

| Posterior | Posterior | Posterior | -value of KS test | |||

|---|---|---|---|---|---|---|

| Mean | St. Dev. | 95% Cred. Int. | ||||

| (1) | (2) | (3) | (4) | (5) | (6) | |

| Heterogeneous CRRA | 0.196 | 0.165 | [0.005, 0.596] | 0.000 | 0.000 | |

| 0.828 | 0.043 | [0.729, 0.893] | 0.000 | |||

| 0.891 | 0.009 | [0.867, 0.900] | ||||

| 0.000 | 0.000 | [0.000, 0.000] | ||||

| Homogeneous CRRA | 0.889 | 0.009 | [0.865, 0.900] | 0.000 | 0.000 | 0.000 |

| 0.000 | 0.000 | [0.000, 0.000] | ||||

| No CRRA | 0.066 | 0.001 | [0.064,0.068] | |||

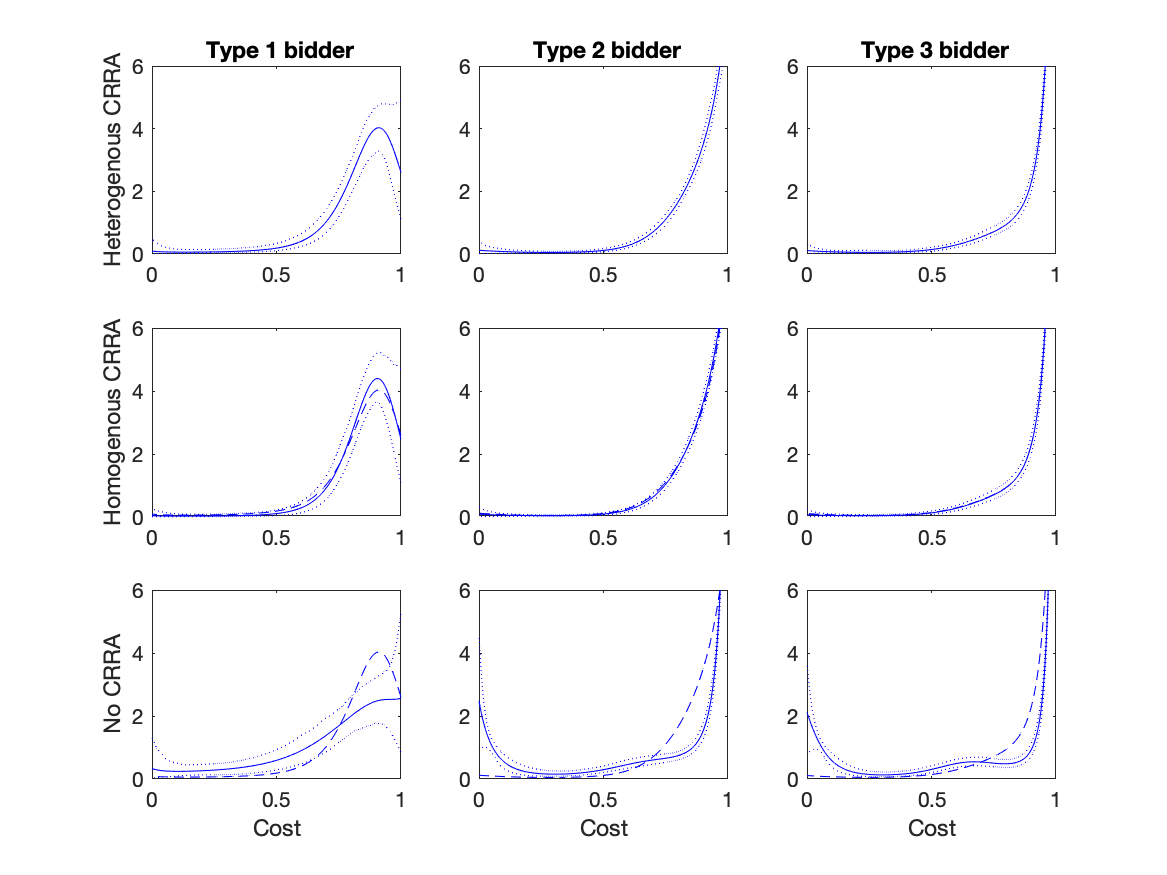

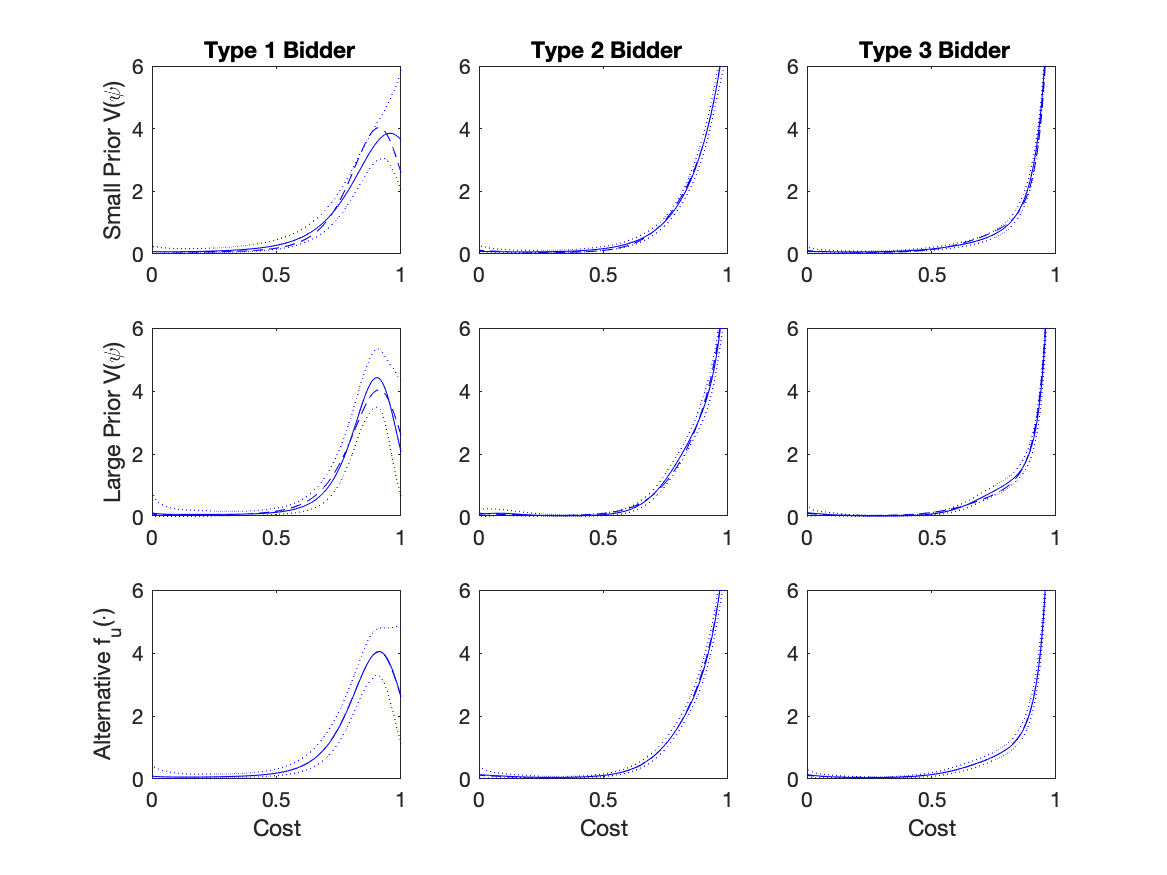

The top panels in Figure 3 show, for each type , the posterior mean of the cost density (3) at every point by a solid line and a 95% credible band around the predictive density by dotted lines. Bidders are asymmetric in the cost densities. Type 1 (frequent) bidder is more efficient in supplying papers than the other bidders, with type 3 (one-time) bidders being the least efficient. This prediction, especially for types 2 and 3, is precise, as indicated by the tight credible bands. Moreover, by the KS test, we reject the hypothesis that the posterior predictive cost distributions are identical for each pair of types; the relevant -values are all close to zero. Note that we apply the KS test to cost samples drawn from the predictive cost densities; see section S8.

Homogeneous Risk-Aversion.

We analyze the data again but imposing for all . The middle block of Table 1 summarizes the posterior distribution of , which precisely predicts that all bidders are highly risk-averse. Note that we reject the hypothesis that the posterior distribution of the constrained is identical to the posterior of from the upper block (heterogeneous CRRA) for each . For this constrained model, there is no unobserved heterogeneity as with asymmetric risk-aversion above. The middle panels of Figure 3 show the posterior predictive densities (solid) and 95% credible bands (dotted), where the dashed lines copy the predictive densities from the upper block for comparison. Imposing homogeneity in risk-aversion generates a slightly different predictive cost density for type 1 bidder, but the other types remain the same. The KS test with the 5% level rejects the hypothesis that the predictive cost distribution remains the same under the constraint for type 1 bidders.

Risk-Neutrality.

We repeat the exercise but restricting for all . Table 1 and Figure 3 (bottom) suggest that this misspecification induces an overestimation of unobserved heterogeneity and substantial bias in predicting cost densities; the more risk-averse, the larger the bias. Once we impose risk-neutrality, smaller bids in our sample must be justified by other model components, causing the bias pattern as we observe. For all , the KS test rejects, by -value , the hypothesis that the cost under follows the same predictive distribution as the cost without the constraint.

5.2 Counterfactual Analysis

Russia has constantly been updating the procurement system mainly to reduce government spending, as we mentioned in section 3.1. We, therefore, evaluate counterfactual scenarios by predictive procurement costs and investigate implications of misspecified risk-aversion. We also compute predictive costs and efficiency at other relevant policy options for comparison.

Decision Theoretic Approach.

Since we study the policymaker’s decision problem, we use a statistical decision-theoretic approach; see Berger (1985) for a survey. Note that Kim (2013) introduces the approach for empirical auction design and Aryal and Kim (2013), Kim (2015), and Aryal, Grundl, Kim, and Zhu (2018) use or extend for different contexts.

If the policymaker knows , he can choose an action , e.g., a reserve price, to minimize the (expected) procurement cost . Let . Choosing is infeasible, however, as is uncertain. The posterior represents the policymaker’s uncertainty about , combining his prior and the sample . Thus, he should choose

| (6) |

This is the idea of the Bayesian decision theory and it is similar to the usual expected utility theory. Choosing , known as a Bayes action, is rational under the axioms of Savage (1954) and Anscombe and Aumann (1963). A decision rule that maps every data to is optimal under a frequentist perspective (Bayes risk principle).

This approach formally considers the structure of the procurement cost and uncertainty and, therefore, it may incur smaller procurement costs than a ‘plug-in’ method. Since is unknown, the policymaker would choose some in practice. Consider a cost function that drops sharply before and slowly increases after . For this cost structure, the policymaker must prefer to for the same error, i.e., . Especially, if the cost is (almost) flat after , then, is (almost) equivalent to . The extent to which the policymaker prefers a large action must depend on the cost structure and amount of uncertainty. For example, if there is no uncertainty about , he would pick regardless of the cost structure. Alternatively, if the cost is flat after for all as in the case with a large number of bidders, he would choose . Solution (6) formalizes the idea of making a decision considering the cost structure and uncertainty. On the other hand, the plug-in approach, which is first popularized in empirical auctions by Paarsch (1997), chooses . That is, the plug-in approach regards the estimate as the true parameter in the decision problem, meaning that it ignores parameter uncertainty and the shape of the cost function (other than the fact that is a minimizer of .)

After formalizing uncertainty by the data and maintained assumptions (model and prior), is certainly the best action. So, no uncertainty notion comes with . Specifically, a credible interval represents uncertainty associated with , but is the action after integrating out by . We instead provide a credible interval of procurement cost at or other notable actions, which is natural because the cost is the outcome of interest and is still uncertain at . This is, however, different from the convention to construct a confidence interval around the plug-in estimate to consider the variation in random data in repeated sampling. The confidence interval is designed for testing a hypothesis like , which is a decision problem different from the policymaker’s problem.

We explain in section S9 our algorithm to evaluate the predictive procurement cost, , which integrates out and , respectively, by the posterior and the empirical distribution of , considering (stochastic) refinements of due to binding reserve prices.

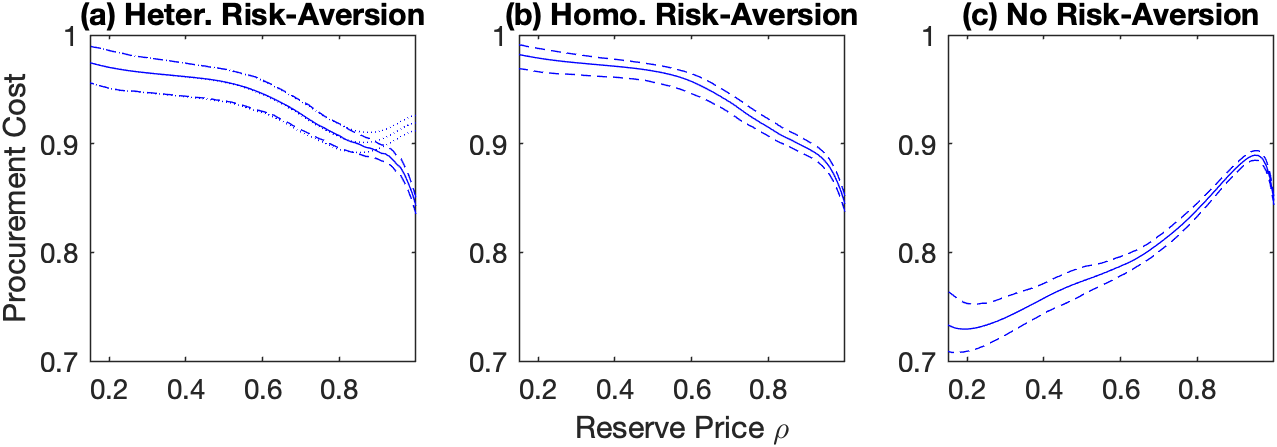

Common Reserve Prices.

We consider a situation where the policymaker wishes to choose one reserve price and apply it to all bidders regardless of their types, i.e., . Figure 4(a) shows as a function of (solid line) and its 95 percent credible band (dashed lines), i.e., the 2.5 and 97.5 percentiles of under the posterior at every in the figure. The three dotted lines show the posterior predictive cost and its credible band if the policymaker implements the second-price procurements (SPP). When bidders are risk-averse, bidders bid more aggressively in an FPP than in an SPP. In particular, the figure shows that the FPP with results in lower costs than the SPP with the cost-minimizing reserve price. Panels (b) and (c) show the predictive costs under the models with homogeneous risk-aversion and no risk-aversion, respectively. When bidders are modeled to be risk-averse, the predictive cost is minimized at whether or not risk-aversion is type-specific. When risk-aversion is ignored, however, the method recommends a much smaller reserve price. This result follows from the fact that the cost densities in Figure 3 (bottom) falsely predict a large probability of small costs, especially for type 2 and 3 bidders, while these bidders would draw high costs more likely, Figure 3 (top).

The first block (common ) in Table S7 documents that the predictive procurement cost is 0.843 with a 95% credible interval of at the cost-minimizing reserve price , where the superscript indicates that the Bayes action is selected under the restriction of common reserve price. The table also shows that the efficient bidder wins the procurement with a 99.2% chance at . This prediction is similar even when risk-aversion is restricted to be homogeneous. Table S7 also shows that the model with risk-neutrality selects and predicts that the procurement cost would be 0.729 at , where the superscript is for risk-neutrality. That is, this misspecified model predicts of cost-reduction at , where 0.848 is the predictive cost at ; see the third block (for comparison) in Table S7. However, this prediction is misleading: the model with asymmetric CRRAs predicts the procurement cost of 0.971 at , increasing the cost by . At , moreover, the model under risk-neutrality also predicts that the efficient bidder would win with a 33.2% of chance, but the chance of allocation is only 3.6% under the model with asymmetric CRRAs. That is, if one ignores risk-aversion, the proposed policy will substantially increase the procurement cost, and most procurements will fail to find a supplier.

| Cost Min. | Predictive | Prob. that | Prob. of | |

|---|---|---|---|---|

| Reserve Price | Procurement Cost | Lowest Wins | Transaction, if | |

| (1) | (2) | (3) | (4) | |

| Common | ||||

| Heterogeneous CRRA | (1.00, 1.00, 1.00) | 0.843 [0.835, 0.850] | 0.992 [0.989, 0.996] | |

| Homogenous CRRA | (1.00, 1.00, 1.00) | 0.845 [0.837, 0.852] | 0.994 [0.993, 0.996] | |

| No Risk-Averson | (0.19, 0.19, 0.19) | 0.729 [0.708, 0.754] | 0.332 [0.301, 0.358] | 0.333 [0.303, 0.359] |

| Type-Specific | ||||

| Heterogeneous CRRA | (0.96, 1.00, 1.00) | 0.841 [0.834, 0.849] | 0.991 [0.989, 0.995] | |

| Homogenous CRRA | (1.00, 1.00, 1.00) | |||

| No Risk-Averson | (0.75, 0.20, 0.20) | 0.722 [0.703, 0.747] | 0.368 [0.335, 0.392] | 0.376 [0.344, 0.401] |

| For Comparison | ||||

| Heterogeneous CRRA | (0.19, 0.19, 0.19) | 0.971 [0.952, 0.987] | 0.036 [0.016, 0.059] | 0.036 [0.016, 0.059] |

| Heterogeneous CRRA | (0.75, 0.20, 0.20) | 0.965 [0.944, 0.980] | 0.060 [0.037, 0.087] | 0.063 [0.040, 0.091] |

| No Risk Aversion | (1.00, 1.00, 1.00) | 0.848 [0.843, 0.851] | 0.985 [0.982, 0.988] | |

| Additional Bidder | ||||

| Type 1 Bidder | 0.791 [0.775, 0.804] | 0.988 [0.981, 0.996] | ||

| Type 2 Bidder | 0.794 [0.782, 0.805] | 0.996 [0.994, 0.998] | ||

| Type 3 Bidder | 0.797 [0.784, 0.811] | 0.996 [0.993, 0.997] |

Type-Specific Reserve Prices.

Now, we consider the policymaker who can select type-specific reserve prices. The second block (type-specific ) in Table S7 shows that the model with asymmetric risk-aversion recommends , which may screen out type 1 (most frequent) bidder and this solution, , results in the predictive cost of 0.841, where the superscript indicates that the Bayes action is type-specific. But, the cost saving is marginal relative to the current cost of 0.843 at , suggesting that the predictive cost is flat in around 0.96 near one for and, therefore, any near one would be practically cost-equivalent.

When risk-aversion is restricted to be homogeneous, the method still chooses . However, ignoring risk-aversion introduces a large bias: the method selects at which it predicts the procurement cost of 0.722 ( of cost-saving), but the model with heterogeneous risk-aversion predicts the cost of 0.965 at ( of cost increase). Although efficiency is by assumption not of the first order interest for the policymaker, the efficiency measures predicted with risk-neutrality are also severely biased: the model with heterogeneous risk-aversion predicts that roughly 94% of procurements would fail to find a supplier through the mechanism.

Cost Reduction from Inviting an Additional Bidder.

Finally, we consider the case in which the buyer can invite one additional (genuine) bidder. Bulow and Klemperer (1996) show that inviting an additional bidder would improve the seller’s revenue more than choosing a revenue maximizing reserve price in a standard symmetric auction with risk-neutral bidders. But, it is unclear whether this finding would hold in our asymmetric model with risk-averse bidders.

We evaluate the predictive procurement cost at using the posterior with the model where bidders are heterogeneous in risk-aversion. When the buyer invites a type 1 bidder, i.e., type 1 bidder is added to all bidder configurations , our method predicts the cost of 0.791 with a 95% credible interval of . The predictive procurement cost in this case is 6.2% smaller than the predictive cost at , the first row in Table S7, with non-overlapping credible intervals. We have similar results when the procurer invites a bidder from other types. When the procurer invites one additional type 2 (3) bidder, the predictive cost would be 0.794 (0.797), which is a 5.8 (5.5)% of cost reduction, with a 95% credible interval of (of ).

Note that even if a fringe bidder (type 3) is invited, this bidder will lower the procurement cost more than selecting the cost-minimizing reserve price. Hence, we find that the insight of Bulow and Klemperer (1996) holds for the “printing papers” category of Russian procurements where bidders are asymmetric in both cost density and risk-aversion.

5.3 Sensitivity Analysis

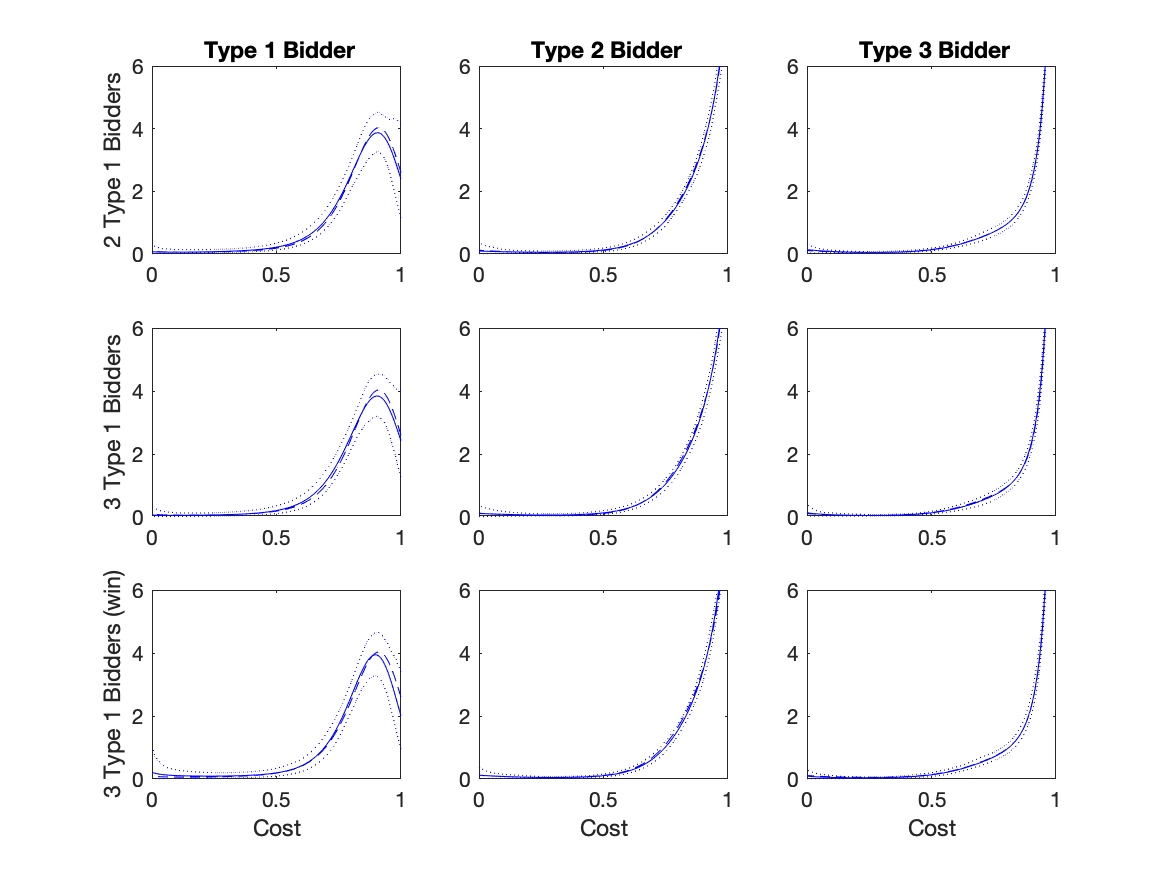

This subsection examines how sensitive our empirical findings are to the definition of bidder types and prior specifications. In this subsection, the main specification refers to the one with heterogeneous risk-aversion outlined in section 4, which gives the estimates in the top block of Table 1. We then consider six alternative specifications. The first (second) specification classifies the two (three) most frequent bidders as a type 1 bidder. Recall that the most (second-most) frequent bidder appears in the data 58 (33) times, but the frequency does not change much starting from the third frequent bidder, who appears 14 times; see Figure 1(a).

The type definitions here suggest that bidders’ entry depends on model primitives such as risk-aversion and cost density. To avoid resorting to any entry model, however, one might want to alternatively define the types, e.g., by how often they win. In our data, the two most frequent entrants are also the most frequent (42 and 19 times) winners. Thus, the analysis remains the same even if one defines type 1 bidder based on the winning rate for the first two bidders. However, the fourth entrant is the third (8 times) winner. The third specification, 3 Type 1 Bidders (win), defines type 1 bidders as the three most frequent winners. The winning rate does not drop after that; see Figure 1(a).

The prior variance of of the fourth (fifth) specification is four times smaller (larger) than the main specification; see the cost density (3) where we introduce . The last one adopts a more flexible density for the unobserved heterogeneity . Extending (4), we specify where , , and so that the distribution of unobserved heterogeneity is indexed by a three-dimensional parameter vector . Recall that the main specification indexes by a one-dimensional parameter with the restriction of ; see (4). Note that we use a flat prior for all the other parameters such as and in the main specification.

All the six alternative specifications produce predictive cost densities close to the ones under the main specification; see section S10.1. We test the hypothesis that the predictive distribution of type 1 bidder’s cost remains the same when we change the definition of type 1 bidder to include the second frequent bidder: Table 3 reports that the associated -value is 0.425, and we fail to reject the hypothesis at any conventional level. Similarly, we conduct the hypothesis testing for other types. Then, we repeat it for the other specifications. In all cases, we fail to reject the hypothesis that the predictive cost distribution remains the same.

| Cost , type | Unobserved Heterogeneity | ||||

|---|---|---|---|---|---|

| KS test, values | KS test | Predictive Distribution | |||

| Specifications | Type 1 | Type 2 | Type 3 | value | mean (stdev) [95% CI] |

| (1) | (2) | (3) | (4) | (5) | |

| (0) Main | NA | NA | 1.000 (0.000) [0.999,1.000] | ||

| (1) 2 Type 1 Bidders | 0.425 | 1.000 | 1.000 | 0.000 | 1.000 (0.000) [0.999,1.000] |

| (2) 3 Type 1 Bidders | 0.258 | 0.999 | 0.999 | 0.000 | 1.000 (0.000) [1.000,1.000] |

| (3) 3 Type 1 Bidders (wins) | 0.194 | 0.679 | 0.952 | 0.000 | 1.000 (0.000) [1.000,1.000] |

| (4) Small Prior | 0.105 | 0.789 | 0.716 | 0.000 | 1.000 (0.000) [0.999,1.000] |

| (5) Large Prior | 0.307 | 0.999 | 0.952 | 0.000 | 1.000 (0.000) [0.999,1.000] |

| (6) Alternative | 0.988 | 1.000 | 0.988 | 0.000 | 1.000 (0.000) [1.000,1.000] |

We also consider the predictive distribution of the unobserved heterogeneity . The KS test strongly rejects, with values close to zero, the hypothesis that the predictive distribution of under the main specification is the same as the distribution under the alternative specification for each of the six cases; see column (4) of Table 3. The specifications, however, unanimously predict that is practically degenerate at one: its mean and standard deviation are approximately one and zero; see column (5) of Table 3. This is an example to show that a statistically significant difference can be economically meaningless.

Table 4 summarizes the posterior of the type-specific CRRA coefficients, for . Including the second frequent bidder in type 1 does not change the prediction on , but the third bidder, when classified as type 1, inflates the prediction on . However, that should be natural if the third bidder is similar to type 2 bidders as suggested by the entrance rate (Figure 1(a)) because type 2 bidders are highly risk-averse. Similarly, the specification defining the three most winning bidders as type 1 bidder predicts a high , which should also be natural because type 1 bidder includes the fourth frequent entrant, who is a type 2 bidder with a high risk aversion under the main specification.

The stronger prior on shrinks the prediction on toward zero, but the weaker prior on does not substantially change the prediction. The prediction on is more robust than because the bid samples of those types are 7 to 10 times larger than type 1. Overall, all the specifications give qualitatively the same prediction on : type 1 bidders are the least risk-averse, and the other bidders are highly risk-averse with . Note that the KS test rejects, at any conventional level, the hypothesis that the posterior of under the main specification equals the posterior of under the alternative specification for each of the six cases.

| Posterior mean (standard deviation) [95% credible interval] | |||

|---|---|---|---|

| Specifications | |||

| Main | 0.196 (0.165) [0.005,0.596] | 0.828 (0.043) [0.729,0.893] | 0.891 (0.009) [0.867,0.900] |

| 2 Type 1 Bidders | 0.196 (0.152) [0.007,0.548] | 0.819 (0.042) [0.736,0.888] | 0.891 (0.008) [0.872,0.900] |

| 3 Type 1 Bidders | 0.350 (0.176) [0.029,0.692] | 0.817 (0.042) [0.725,0.886] | 0.892 (0.008) [0.870,0.900] |

| 3 Type 1 Bidders (wins) | 0.597 (0.127) [0.331,0.823] | 0.865 (0.032) [0.779,0.899] | 0.888 (0.012) [0.856,0.900] |

| Small Prior | 0.141 (0.118) [0.005,0.443] | 0.798 (0.043) [0.704,0.869] | 0.890 (0.010) [0.863,0.900] |

| Large Prior | 0.242 (0.197) [0.006,0.720] | 0.842 (0.043) [0.740,0.898] | 0.891 (0.008) [0.870,0.900] |

| Alternative | 0.202 (0.162) [0.008,0.585] | 0.819 (0.041) [0.727,0.887] | 0.890 (0.010) [0.858,0.900] |

However, the statistically significant differences in the posterior distributions of between the specifications would not be large enough to induce an economically significant impact on the policymaker’s decision problem. When the policymaker applies a common reserve price to all bidders, our decision method selects the current reserve price as the cost-minimizing price under all the specifications, giving similar predictions on the procurement cost and the likelihood of the lowest bidder winning the procurement; see the upper block of Table 5. When the policymaker can choose bidder-specific reserve prices, our method selects different reserve prices for type 1 depending on the specification. As we discussed in the previous subsection, the predictive cost with the main specification is practically the same for near one at . All the alternative specifications produce similar predictive costs as a function of given . That is, the method could select any price near one, especially when the cost functions are evaluated by Monte Carlo, but all giving similar predictions on the outcome variables of interest; see the lower block of Table 5. All the specifications predict that the current mechanism is effectively cost-minimizing. Finally, we repeat the counterfactual analysis of inviting one additional bidder for each alternative specification and obtain predictions on the outcome variables of interest that are similar to the prediction under the main specification; see section S10.2.

| Cost Min. | Predictive | Probability that | |

| Reserve Price | Procurement Cost | Lowest Cost Bidder Wins | |

| (1) | (2) | (3) | |

| Common : | |||

| Main Spec | (1.00,1.00,1.00) | 0.843 (0.004) [0.835, 0.850] | 0.992 (0.002) [0.989, 0.996] |

| 2 Type 1 Bidders | (1.00,1.00,1.00) | 0.843 (0.004) [0.836, 0.850] | 0.991 (0.002) [0.988, 0.995] |

| 3 Type 1 Bidders | (1.00,1.00,1.00) | 0.843 (0.004) [0.836, 0.850] | 0.992 (0.002) [0.989, 0.996] |

| 3 Type 1 Bidders (wins) | (1.00,1.00,1.00) | 0.842 (0.004) [0.834, 0.849] | 0.994 (0.002) [0.991, 0.997] |

| Small Prior | (1.00,1.00,1.00) | 0.840 (0.004) [0.832, 0.848] | 0.992 (0.001) [0.989, 0.994] |

| Large Prior | (1.00,1.00,1.00) | 0.844 (0.004) [0.837, 0.850] | 0.992 (0.002) [0.989, 0.996] |

| Alternative | (1.00,1.00,1.00) | 0.843 (0.004) [0.836, 0.851] | 0.992 (0.002) [0.990, 0.996] |

| Type Specific : | |||

| Main Spec | (0.96,1.00,1.00) | 0.841 (0.004) [0.834,0.849] | 0.991 (0.001) [0.989,0.995] |

| 2 Type 1 Bidders | (0.93,1.00,1.00) | 0.841 (0.004) [0.832,0.849] | 0.986 (0.001) [0.984,0.989] |

| 3 Type 1 Bidders | (0.93,1.00,1.00) | 0.843 (0.005) [0.833,0.851] | 0.986 (0.002) [0.983,0.989] |

| 3 Type 1 Bidders (wins) | (1.00,1.00,1.00) | 0.842 (0.004) [0.834,0.849] | 0.994 (0.002) [0.991,0.997] |

| Small Prior | (0.95,1.00,1.00) | 0.838 (0.004) [0.830,0.846] | 0.991 (0.001) [0.988,0.993] |

| Large Prior | (0.95,1.00,1.00) | 0.843 (0.004) [0.835,0.850] | 0.991 (0.002) [0.988,0.994] |

| Alternative | (0.95,1.00,1.00) | 0.842 (0.004) [0.833,0.849] | 0.991 (0.001) [0.989,0.994] |

6 Concluding Remarks

We conclude this paper with a discussion about some possible extensions to our method. First, one may consider a non-separable unobserved heterogeneity instead of the separable one as introduced in Assumption 3-3. To be specific, if is discrete with a finite support and if is strictly increasing in for all , the bid distribution for with identifies the conditional bid distribution given for the given , following Hu, McAdams, and Shum (2013). Those identified conditional bid distributions at any in its finite support then identify with variation in following Campo (2012). In our data, 237 procurements out of , approximately 58%, have only bidders, and we do not consider this specification for estimation.

Second, one may treat bidders’ type as an additional parameter to estimate instead of fixing a type for each bidder. For example, An (2017) proposes a method to estimate bidder types. Our sample, however, does not meet its requirement. In particular, every bidder must appear at least in three different procurements. But, this is not the case in our data, where 84% of bidders enter once or twice. In our Bayesian setting, alternatively, we may model each bidder’s membership to a type as a random variable following the Dirichlet prior. This approach is standard with a range of applications, e.g., Dirichlet process mixture; see Ferguson (1973) and Escobar and West (1995) among others. If applied here, however, it would further complicate our method and substantially increase computing time.

Finally, a dataset may contain procurement-specific covariates, . We can also adapt the specification (3) to accommodate . In particular, let us use to denote (3) and for the cost density with . Let be a low-dimensional parametric density indexed by , where is a vector of parameters. For example, can be the exponential density with the mean . Then, we may specify the CDF of the cost by where and are the CDFs of and . To understand this specification, consider its log density, where . That is, this specification first approximates the cost density by the parametric family and reduces the error by the additional terms. Therefore, if the parametric family offers a good fit, need not be high dimensional for a given approximation quality. So, the specification is a parsimonious and yet flexible representation of the cost density with covariates. This approach has been used before, e.g., see Kim (2013), Aryal and Kim (2013), Kim (2015), and Aryal, Grundl, Kim, and Zhu (2018).

References

- (1)

- An (2017) An, Y. (2017): “Identification of First-Price Auctions with Nonequilibrium Beliefs: A Measurement Error Approach,” Journal of Econometrics, 200(2), 325–343.

- Anscombe and Aumann (1963) Anscombe, F. J., and R. J. Aumann (1963): “A Definition of Subjective Probability,” Annals of Mathematical Statistics, 34(1), 199–205.

- Aryal, Charankevich, Jeong, and Kim (2020) Aryal, G., H. Charankevich, S. Jeong, and D.-H. Kim (2020): “Procurements with Bidder Asymmetry in Cost and Risk-Aversion,” Working Paper. Available at SSRN: https://ssrn.com/abstract=3500268.

- Aryal, Charankevich, Jeong, and Kim (2022a) (2022a): “Procurements with Bidder Asymmetry in Cost and Risk-Aversion,” Supplementary Appendix.

- Aryal, Charankevich, Jeong, and Kim (2022b) (2022b): “Procurements with Bidder Asymmetry in Cost and Risk-Aversion,” Working Paper.

- Aryal, Grundl, Kim, and Zhu (2018) Aryal, G., S. Grundl, D.-H. Kim, and Y. Zhu (2018): “Empirical Relevance of Ambiguity in First Price Auctions,” Journal of Econometrics, 204(2), 189–206.

- Aryal and Kim (2013) Aryal, G., and D.-H. Kim (2013): “A Point Decision for Partially Identified Auction Models,” Journal of Business & Economic Statistics, 31(4), 384–397.

- Bajari and Hortaçsu (2005) Bajari, P., and A. Hortaçsu (2005): “Are Structural Estimates of Auction Models Reasonable? Evidence from Experimental Data,” Journal of Political Economy, 113(4), 703–741.

- Berger (1985) Berger, J. O. (1985): Statistical Decision Theory and Bayesian Analysis., Springer Series in Statistics. Springer, New York.

- Brooks, Giudici, and Philippe (2003) Brooks, S. P., P. Giudici, and A. Philippe (2003): “Nonparametric Convergence Assessment for MCMC Model Selection,” Journal of Computational and Graphical Statistics, 12(1), 1–22.

- Bulow and Klemperer (1996) Bulow, J., and P. Klemperer (1996): “Auctions Versus Negotiations,” The American Economic Review, 86(1), 180–194.

- Campo (2012) Campo, S. (2012): “Risk Aversion and Asymmetry in Procurement Auctions: Identification, Estimation and Application to Construction Procurements,” Journal of Econometrics, 168(1), 96–107.

- Campo, Guerre, Perrigne, and Vuong (2011) Campo, S., E. Guerre, I. Perrigne, and Q. Vuong (2011): “Semiparametric Estimation of First-Price Auctions with Risk-Averse Bidders,” Review of Economic Studies, 78(1), 112–147.

- Charankevich (2021) Charankevich, H. (2021): “Bid Manipulation in Open Procurement Auctions,” Ph.D. thesis, University of Virginia.

- Escobar and West (1995) Escobar, M. D., and M. West (1995): “Bayesian Density Estimation and Inference Using Mixtures,” Journal of the American Statistical Association, 90(430), 577–588.

- Ferguson (1973) Ferguson, T. S. (1973): “A Bayesian Analysis of Some Nonparametric Problems,” Annals of Statistics, 1(2), 209–230.

- Fibich and Gavish (2011) Fibich, G., and N. Gavish (2011): “Numerical Simulations of Asymmetric First-Price Auctions,” Games and Economic Behavior, 73(2), 479–495.

- Geweke (2005) Geweke, J. (2005): Contemporary Bayesian Econometrics and Statistics. John Wiley & Sons, Inc, Hoboken, New Jersey.

- Haario, Saksman, and Tamminen (2001) Haario, H., E. Saksman, and J. Tamminen (2001): “An Adaptive Metropolis Algorithm,” Bernoulli, 7, 223–242.

- Haario, Saksman, and Tamminen (2005) Haario, H., E. Saksman, and J. Tamminen (2005): “Componentwise Adaptation for High Dimensional MCMC,” Computation Statistics, 20, 265–273.

- Herranz, Krasa, and Villamil (2015) Herranz, N., S. Krasa, and A. P. Villamil (2015): “Entrepreneurs, Risk Aversion, and Dynamic Firms,” Journal of Political Economy, 125(5), 1133–1176.

- Holt (1980) Holt, C. A. (1980): “Competitive Bidding for Contracts under Alternative Auction Procedures,” Journal of Political Economy, 88(3), 433–445.

- Hu, Matthews, and Zou (2010) Hu, A., S. A. Matthews, and L. Zou (2010): “Risk Aversion and Optimal Reserve Prices in First- and Second-Price Auctions,” Journal of Economic Theory, 145(3), 1188–1202.

- Hu, McAdams, and Shum (2013) Hu, Y., D. McAdams, and M. Shum (2013): “Identification of First-Price Auctions with Non-separable Unobserved Heterogeneity,” Journal of Econometrics, 174(2), 186–193.

- Jun and Zincenko (2022) Jun, S. J., and F. Zincenko (2022): “Testing for Risk Aversion in First-Price Sealed-Bid Auctions,” Journal of Econometrics, 226, 295–320.

- Kim (2013) Kim, D.-H. (2013): “Optimal Choice of a Reserve Price under Uncertainty,” International Journal of Industrial Organization, 31(5), 587–602.

- Kim (2015) (2015): “Flexible Bayesian Analysis of First-Price Auctions Using a Simulated Likelihood,” Quantitative Economics, 6, 429–461.

- Kotlarski (1966) Kotlarski, I. (1966): “On Some Characterization of Probability Distributions in Hilbert Spaces,” Annali di Matematica Pura ed Applicata, 74(1), 129–134.

- Kotowski (2018) Kotowski, M. H. (2018): “On Asymmetric Reserve Prices,” Theoretical Economics, 13(1), 205–237.

- Krasnokutskaya (2011) Krasnokutskaya, E. (2011): “Identification and Estimation of Auction Models with Unobserved Heterogeneity,” Review of Economic Studies, 78(1), 293–327.

- Li and Vuong (1998) Li, T., and Q. Vuong (1998): “Nonparametric Estimation of the Measurement Error Model Using Multiple Indicators,” Journal of Multivariate Analysis, 65(2), 139–165.

- Li and Zheng (2009) Li, T., and X. Zheng (2009): “Entry and Comptetition Effects in First-Price Auctions: Theory and Evidence from Procurement Auctions,” Review of Economic Studies, 76, 1397–1429.

- Liu and Luo (2017) Liu, N., and Y. Luo (2017): “A Nonparametric Test for Comparing Valuation Distributions in First‐Price Auctions,” International Economic Review, 58(3), 857–887.

- Lu and Perrigne (2008) Lu, J., and I. Perrigne (2008): “Estimating Risk Aversion from Ascending and Sealed-Bid Auctions: The Case of Timber Auction Data,” Journal of Applied Econometrics, 23(7), 871–896.

- Marshall, Meurer, Richard, and Stromquist (1994) Marshall, R., M. Meurer, J. Richard, and W. Stromquist (1994): “Numerical Analysis of Asymmetric First Price Auctions,” Games and Economic Behaviour, 7, 193–220.

- Myerson (1981) Myerson, R. B. (1981): “Optimal Auction Design,” Mathematics of Operations Research, 6(1), 58–73.

- Paarsch (1997) Paarsch, H. (1997): “Deriving an Estimate of the Optimal Reserve Price: An Application to British Columbian Timber Sales,” Journal of Econometrics, 78, 333–357.

- Robert and George (2004) Robert, C. P., and C. George (2004): Monte Carlo Statistical Methods. Springer, 2 edn.

- Robinson (1985) Robinson, M. (1985): “Collusion and the Choice of Auction,” Rand Journal of Economics, 16, 141–145.

- Savage (1954) Savage, L. (1954): Foundation of Statistics. Wiley, reissued in 1972 by Dover, New York.

- Schurter (2020) Schurter, K. (2020): “Identification and Inference in First-Price Auctions with Collusion,” Working Paper.

- Szegö (1975) Szegö, G. (1975): Orthogonal Polynomials. American Mathematical Society, 4 edn.

- van der Vaart (1998) van der Vaart, A. W. (1998): Asymptotic Statistics, Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, New York.

Supplementary Appendix

S1 Roadmap

This supplementary appendix provides additional materials. The order of the contents in this appendix closely follows the order in the main paper, Aryal, Charankevich, Jeong, and Kim (2022b).

Section S2 proves Lemma 1 in section 2 in the main paper. Section S3 provides a complete list of 102 categories, for each of which the section presents some additional statistics. The section then explains the selection criteria by which we choose the “printing papers” category. Then, the section documents further evidence that bidders bid depending on the level of competition for the category.

The next five sections in this appendix discuss details about the computational algorithms used in our estimation method; see sections 4 and 5 in the main paper. In particular, section S4 plots graphs of several Legendre polynomial basis functions that we use to specify the cost densities, and section S5 provides computational details on solving the asymmetric equilibria and evaluating the likelihood in a Markov chain Monte Carlo (MCMC) method. Section S6 explains the MCMC algorithm that we use, and section S7 presents the estimation results with simulated data. Section 4 in the main paper has a summary of the findings from this section. Section S8 discusses how the Kolmogorov-Smirnov (KS) test are used to examine if multiple MCMC outcomes are drawn from the same (posterior) distribution.

S2 Proof of Lemma 1

Consider any bidder configuration with , and let be the joint distribution of bids submitted by bidders in . Note that is directly identified from the bid data generated from procurements with . By Theorem 1 in Krasnokutskaya (2011), then, we can identify the marginal bid distribution of bidder when there is no unobserved heterogeneity, i.e., , for all and the distribution of the unobserved heterogeneity, . By Lemma 2 in Campo (2012), then, we can identify the risk-aversion coefficient and the cost distribution for bidder , using when exogenously varies.

S3 Data

This section explains the selection criteria that we use to choose a category to analyze. Then, we provide additional statistical evidence that bidders in the category “printing papers” bid depending on the level of competition.

S3.1 Selecting a Category

The Russian government uses the first-price procurement (FPP) (along with several other allocation methods) to buy goods and services from private bidders. Tables S1 to S4 list all the 102 categories for which FPPs were used in 2014. Some categories have names that are too long to fit in the table, in which case their full names appear below the table along with their identification numbers (ID). It is evident that the categories are in different industries with separate markets. The tables show the total numbers of procurements, bids, and bidders in each category in columns (1), (2), and (3), respectively. For example, the second job category, “educational service,” has 763 procurements in total, where 1,079 bidders submit a total of 1,607 bids. (As in the paper, we use double quotation marks to indicate field terms in their closest English translation.) Columns (4), (5), and (6) show the numbers of procurements with only one bidder, unrecorded bids, and bids larger than the reserve price, respectively. In the second category, “educational service,” 292 procurements have only one bidder, two procurements have missing bids, and 14 procurements have at least one bid larger than the reserve price.

| Number (#) of | # of procs | # of | # of bids | |||||||||

| procurements, | 1 bid only, | remaining | submitted by | |||||||||

| bids, | missing bids, | procs | type (1,2,3) | |||||||||

| Category | bidders | bids | (%) | bidders | ||||||||

| ID | Names | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) |

| 1 | car tires | 272 | 609 | 448 | 83 | 0 | 12 | 177 | (65%) | 0 | 199 | 293 |

| 2 | educational services* | 763 | 1607 | 1079 | 292 | 2 | 14 | 458 | (60%) | 0 | 629 | 647 |

| 3 | training courses | 211 | 461 | 325 | 81 | 0 | 7 | 123 | (58%) | 0 | 162 | 198 |

| 4 | construction: other building r | 1259 | 3471 | 2285 | 257 | 1 | 36 | 975 | (77%) | 0 | 1601 | 1525 |

| 5 | metrology services | 443 | 671 | 372 | 280 | 1 | 27 | 154 | (35%) | 0 | 150 | 222 |

| 6 | IT and computer services* | 467 | 897 | 716 | 153 | 0 | 22 | 293 | (63%) | 0 | 201 | 493 |

| 7 | wooden office furniture | 209 | 510 | 412 | 47 | 1 | 7 | 154 | (74%) | 0 | 141 | 298 |

| 8 | M&R cars | 290 | 626 | 518 | 65 | 0 | 19 | 206 | (71%) | 0 | 146 | 362 |

| 9 | garbage collection | 278 | 550 | 431 | 100 | 0 | 17 | 166 | (60%) | 0 | 145 | 277 |

| 10 | system maintenance | 1430 | 2947 | 1703 | 298 | 1 | 80 | 1053 | (74%) | 0 | 1463 | 996 |

| 11 | advanced professional training | 719 | 1363 | 652 | 366 | 2 | 12 | 339 | (47%) | 0 | 599 | 360 |

| 12 | construction: admin and busine | 590 | 1519 | 1128 | 129 | 2 | 25 | 439 | (74%) | 0 | 553 | 774 |

| 13 | Internet and regional network | 770 | 1414 | 534 | 315 | 1 | 31 | 427 | (55%) | 208 | 526 | 295 |

| 14 | other drugs | 329 | 596 | 218 | 140 | 0 | 8 | 181 | (55%) | 55 | 277 | 105 |

| 15 | engineering evaluation and res | 701 | 1775 | 1204 | 197 | 2 | 21 | 482 | (69%) | 0 | 730 | 781 |

| 16 | other design and engineering s | 324 | 907 | 675 | 58 | 1 | 14 | 252 | (78%) | 0 | 293 | 504 |

| 17 | milk | 289 | 585 | 442 | 79 | 0 | 9 | 202 | (70%) | 0 | 172 | 314 |

| 18 | other personal services | 685 | 1500 | 1256 | 198 | 2 | 21 | 466 | (68%) | 0 | 308 | 934 |

| 19 | inventorying and certification | 396 | 1124 | 558 | 82 | 0 | 12 | 305 | (77%) | 95 | 565 | 359 |

| 20 | other workshops and training c | 217 | 432 | 315 | 106 | 1 | 4 | 106 | (49%) | 0 | 109 | 206 |

| 21 | general medical checkup and ex | 828 | 1498 | 874 | 446 | 0 | 20 | 366 | (44%) | 0 | 620 | 386 |

| 22 | other entertaining services | 327 | 722 | 545 | 74 | 0 | 16 | 238 | (73%) | 0 | 243 | 364 |

| 23 | sanitation improvement* | 336 | 814 | 702 | 70 | 0 | 25 | 246 | (73%) | 0 | 144 | 528 |

| 24 | M&R lifting and conveying mac | 541 | 1056 | 585 | 163 | 2 | 29 | 349 | (65%) | 0 | 518 | 297 |

| 4 | construction: other building repairing |

|---|---|

| 11 | advanced professional training for employees with higher education |

| 12 | construction: admin and business buildings, bus and railway stations, airports |

| 13 | Internet and regional network services |

| 15 | engineering evaluation and research* |

| 16 | other design and engineering services |

| 19 | inventorying and certification of non-housing stock |

| 20 | other workshops and training courses |

| 21 | general medical checkup and examination services |

| 24 | M&R lifting and conveying machines |

| Number (#) of | # of procs | # of | # of bids | |||||||||

| procurements, | 1 bid only, | remaining | submitted by | |||||||||

| bids, | missing bids, | procs | type (1,2,3) | |||||||||

| Category | bidders | bids | (%) | bidders | ||||||||

| ID | Names | (1) | (2) | (3) | (4) | (5) | (6) | (7) | (8) | (9) | (10) | (11) |

| 25 | motor fuel | 626 | 1015 | 514 | 294 | 0 | 16 | 319 | (51%) | 0 | 399 | 291 |

| 26 | out-of-schedule public transpo | 398 | 681 | 537 | 167 | 0 | 16 | 220 | (55%) | 0 | 186 | 297 |

| 27 | office and school plastic supp | 221 | 564 | 401 | 41 | 0 | 5 | 176 | (80%) | 0 | 224 | 289 |

| 28 | medical lab services* | 279 | 438 | 283 | 168 | 0 | 6 | 109 | (39%) | 0 | 121 | 144 |

| 29 | copier P&A | 581 | 1623 | 1030 | 93 | 3 | 16 | 471 | (81%) | 0 | 756 | 719 |

| 30 | computer P&A* | 357 | 862 | 644 | 95 | 3 | 10 | 250 | (70%) | 0 | 277 | 452 |

| 31 | office and school plastic supp | 340 | 932 | 564 | 51 | 2 | 8 | 279 | (82%) | 33 | 437 | 377 |

| 32 | individual car M&R | 212 | 435 | 371 | 58 | 0 | 11 | 143 | (67%) | 0 | 95 | 251 |

| 33 | M&R IT equipment | 418 | 1019 | 839 | 87 | 1 | 14 | 318 | (76%) | 0 | 262 | 629 |

| 34 | A/C equipment | 390 | 1270 | 911 | 48 | 2 | 18 | 322 | (83%) | 0 | 475 | 653 |

| 35 | ground-based vehicles insuranc | 389 | 1125 | 85 | 74 | 1 | 46 | 273 | (70%) | 671 | 170 | 40 |

| 36 | off-the-shelf software and use | 316 | 624 | 473 | 103 | 0 | 11 | 202 | (64%) | 0 | 174 | 319 |

| 37 | lead-free gasoline, sulfur con | 314 | 517 | 311 | 147 | 1 | 8 | 158 | (50%) | 0 | 178 | 173 |

| 38 | advanced professional training | 380 | 575 | 308 | 274 | 1 | 4 | 101 | (27%) | 12 | 110 | 163 |

| 39 | security services | 1378 | 3448 | 1921 | 336 | 3 | 59 | 988 | (72%) | 0 | 1841 | 1096 |

| 40 | subscription for newspapers, m | 356 | 671 | 130 | 114 | 0 | 15 | 228 | (64%) | 229 | 230 | 64 |

| 41 | subscription for domestic news | 371 | 703 | 121 | 112 | 2 | 20 | 243 | (65%) | 254 | 251 | 46 |

| 42 | property and assets evaluation | 591 | 1695 | 773 | 133 | 3 | 9 | 446 | (75%) | 0 | 1078 | 445 |

| 43 | architectural design | 211 | 610 | 411 | 50 | 0 | 5 | 156 | (74%) | 0 | 279 | 270 |

| 44 | construction completion* | 1379 | 3492 | 2579 | 327 | 6 | 64 | 994 | (72%) | 0 | 1191 | 1799 |