The Weighted Generalised Covariance Measure

Abstract

We introduce a new test for conditional independence which is based on what we call the weighted generalised covariance measure (WGCM). It is an extension of the recently introduced generalised covariance measure (GCM). To test the null hypothesis of and being conditionally independent given , our test statistic is a weighted form of the sample covariance between the residuals of nonlinearly regressing and on . We propose different variants of the test for both univariate and multivariate and . We give conditions under which the tests yield the correct type I error rate. Finally, we compare our novel tests to the original GCM using simulation and on real data sets. Typically, our tests have power against a wider class of alternatives compared to the GCM. This comes at the cost of having less power against alternatives for which the GCM already works well. In the special case of binary or categorical and , one of our tests has power against all alternatives.

Keywords: conditional independence tests, weighted covariance, nonparametric regression, boosting, nonparametric variable selection

1 Introduction

Conditional independence is a key concept for statistical inference. Where already Dawid (1979) argued that different important statistical concepts can be unified using conditional independence, it has received more attention during the last years. This is mainly because conditional independence plays a prominent role in the context of graphical models and causal inference. As a consequence, conditional independence tests form the basis of many algorithms for causal structure learning, see for example Pearl (2009) or Peters et al. (2017).

In contrast to unconditional independence (see for example Josse and Holmes, 2016 for an overview), testing conditional independence is a hard statistical problem. In fact, it was recently proven by Shah and Peters (2020) that conditional independence is not a testable hypothesis. If the joint distribution of is absolutely continuous with respect to Lebesgue measure, then there is no test for the null hypothesis of and being conditionally independent given that has power against any alternative and at the same time controls the level for all distributions in the null hypothesis. A test for conditional independence therefore needs to make some assumptions to restrict the space of possible null distributions. In the following, we write for conditional independence of and given .

The review over nonparametric conditional independence tests for continuous variables by Li and Fan (2020) groups the tests into the following categories.

- Discretization-based tests:

- Metric-based tests:

-

Su and White (2014) construct tests using the smoothed empirical likelihood ratio. Su and White (2007) and Wang et al. (2015) propose tests based on conditional characteristic functions. Su and White (2008) introduce a test based on the weighted Hellinger distance between two conditional densities. A test proposed by Runge (2018) is based on conditional mutual information.

- Permutation-based two-sample tests:

- Kernel-based tests:

- Regression-based tests:

-

Many tests related to causal inference assume an additive noise model of the form

where and are independent of with mean zero. In this case, testing is equivalent to testing . Hence, a reasonable approach is to regress on and on and then test (unconditional) independence of the residuals, see for example Hoyer et al. (2009), Peters et al. (2014), Zhang et al. (2019), Zhang et al. (2017) and Ramsey (2014). Instead of testing independence of the residuals, Shah and Peters (2020) introduce a test based on the sample covariance of the residuals. In view of the hardness of conditional independence testing, an advantage of regression based tests is that they convert the problem of restricting the null hypothesis to choosing appropriate regression or machine learning methods, which may be more accessible in practice.

- Other tests:

-

Under the assumption that the conditional distribution of is known at least approximately, it is possible to restore type I error control, see Berrett et al. (2020) and Candès et al. (2018). Heinze-Deml et al. (2018) propose some additional tests in the setting of nonlinear invariant causal prediction. Azadkia and Chatterjee (2019) introduce a new non-parametric coefficient of conditional dependence, based on which they construct a new variable selection algorithm.

1.1 Our Contribution

We introduce a new regression-based conditional independence test, which is a non-trivial and often more powerful extension of the generalised covariance measure (GCM) introduced by Shah and Peters (2020). We call it the weighted generalised covariance measure (WGCM). For simplicity, assume that the random variables and take values in . The test statistic of the GCM is a normalised sum of the product of the residuals of (nonlinearly) regressing on and on . Hence, the GCM essentially tests if , where

For a more thorough treatment, see Section 2.1. Note that under the null hypothesis of , but we can also have under an alternative. Our WGCM however introduces an additional weight function. Instead of using the sum of the products of the residuals from the regression of on and on as the basis of the test statistic, we weight this sum with an additional weight function depending on . Thus, the idea of the WGCM is to test for some suitable weight function from the domain of to . We will propose two different methods of the WGCM. WGCM.fix tests for several fixed weight functions and aggregates the results. WGCM.est performs sample splitting and estimates a promising weight function on one part of the data and calculates the test statistic using this weight function on the other part of the data. To give conditions for the correct type I error rate of our tests, we can rely on the work of Shah and Peters (2020) and largely follow the proofs given there.

A bounded weight function satisfying exists if and only if is not almost surely equal to : If a.s., then for every bounded weight function ,

Conversely, if is not almost surely equal to , then for example

| (1) |

satisfies .

The two methods WGCM.fix and WGCM.est have power against a wider class of alternatives than the GCM, at the cost of typically being less powerful in situations where the GCM already works well. In view of the above considerations, we expect WGCM.fix and WGCM.est to be superior to GCM, when is equal to or close to , but is not. This can be supported by simulations.

Our main contributions are:

-

•

We introduce the two tests WGCM.fix and WGCM.est for conditional independence of two univariate random variables and given a random vector .

-

•

For both tests, we prove asymptotic guarantees for the level of the tests under appropriate conditions.

-

•

For both tests, we prove theorems justifying that WGCM.fix and WGCM.est have full asymptotic power against a wider class of alternatives compared to the GCM. In particular, for categorical and but continuous , WGCM.est leads to full asymptotic power against all alternatives.

-

•

We introduce extensions mWGCM.fix and mWGCM.est for the case of multivariate and and derive the corresponding results.

As in Shah and Peters (2020), our theoretical results allow for high-dimensional conditioning variables Z.

In the following, we give a more precise overview about which methods have power in which situations. Let be the collection of all distributions for that are absolutely continuous with respect to Lebesgue measure. For a distribution , let denote the expectation with respect to and consider the following subsets of distributions:

| (2) | ||||

| (3) | ||||

| (4) |

Moreover, for a fixed collection of bounded weight functions from to , let

| (5) |

By the argument prior to Equation (1), it follows that for a fixed with , we have

We will give conditions under which

1.1.1 Categorical Variables

Our tests are also applicable in the setting of categorical and and continuous . For simplicity, assume that and take values in and takes values in . In this case,

| (6) |

It follows that a distribution satisfies if and only if or using the notation (3) and (4), . Hence, for binary variables, we will give conditions under which the test WGCM.est has asymptotic power against all alternatives (see Section 2.2.3). Using dummy coding, this result can also be extended to arbitrary categorical and (see Appendix A.3).

1.1.2 A Concrete Example

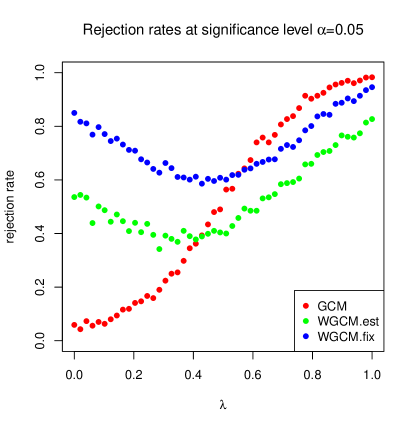

For , let . Consider the setting

| (7) | ||||

where , and are jointly independent. Clearly, and are not conditionally independent given . In Figure 1, we plot the rejection rates at level for the three methods GCM, WGCM.est and WGCM.fix for different values of . The rejection rates are calculated from simulation runs with samples. We see that GCM outperforms the other methods for high values of , which corresponds to settings where the function introducing the dependence is nearly linear. However, for small and moderate values of , the methods WGCM.est and WGCM.fix still have considerable power, whereas the power of the GCM rapidly decreases.

To understand the phenomenon, let us consider the cases of and more closely. Using the notation from before, we have

and

If , we have , so we expect the GCM to have power in this case, which is also supported by our simulation. If , however, , since , and are all equal to zero. Therefore, we do not expect the GCM to have power larger than the significance level in this case, which is also visible in the plot. On the other hand, in the case of , we have that

which is not almost surely equal to zero. Thus, we expect the two variants of the WGCM to have power. This is supported by the simulation.

1.2 Conventions and Notation

As most of the arguments are along the same lines as in Shah and Peters (2020), we also largely use the same notation.

We will use the following setting: Let , and be random vectors taking values in , and . For , let be i.i.d. copies of . Let , and be the data matrices with rows , and , respectively.

Whereas at some places, we will also consider categorical and , for most of the time, we assume that the joint distribution of is absolutely continuous with respect to Lebesgue measure. Let be the joint Lebesgue density of .

We say that and are conditionally independent given , written as

if one of the following two equivalent characterizations holds for Lebesgue almost all with :

-

1.

;

-

2.

,

see for example Section 3.1 in Dawid (1979).

Let be the collection of all distributions for that are absolutely continuous with respect to Lebesgue measure. Let be the set of distributions in such that and are conditionally independent given .

We use to denote the expectation of random variables under the probability distribution and we write for the corresponding probability measure . We denote indicator functions with or .

We write for the cumulative distribution function of a standard normal random variable, that is, for all , we have , where .

Let be a collection of probability distributions. For a sequence of random variables with laws determined by , we write if for all

We write if

For another sequence of strictly positive random variables, we write and if and , respectively.

For a random variable taking values in (a subset of) , we typically say for all instead of for all in the support of .

1.3 Outline

In Section 2, we describe the WGCM for univariate and . After a motivation as an extension of the GCM, we present two variants of the WGCM. The first variant WGCM.est is based on sample splitting to estimate a weight function, whereas the second variant WGCM.fix uses multiple fixed weight functions and aggregates the results. We provide Theorems justifying level and power of the methods. In Section 3, we compare our methods to the original GCM using simulation and also apply the methods to some real data sets in the context of variable selection. In the appendix, we show, how the WGCM can be extended to the case of multivariate and and present the proofs of our various results.

2 The Univariate Weighted Generalised Covariance Measure

In this section, we introduce the weighted generalised covariance measure (WGCM), which is an extension of the generalised covariance measure (GCM) recently introduced by Shah and Peters (2020). We first treat the case of and present different variants of the WGCM in this case. In Appendix A, we give extensions for multivariate and .

2.1 Prerequisites

We consider the same setup as in Section 3.1 of Shah and Peters (2020).

Let and . For any distribution , let and and for , define the functions and . Then, we can write

For , let and . Moreover, let and .

Let and be estimates of and , obtained by regression of , respectively on .

In the following, the dependence on and is sometimes omitted. The GCM by Shah and Peters (2020) uses the products of the residuals

as the basis of the test statistic

| (8) |

which is a normalised sum of the . Under the null hypothesis and suitable conditions on the convergence of and to and , the test statistic converges in distribution to a standard normal random variable, see Theorem 6 in Shah and Peters (2020).

The test statistic of the GCM is a normalised estimate of . Under the null hypothesis of , we have

using a.s. However, it is also possible to have and . Therefore, the GCM only has power against alternatives with , see Theorem 8 in Shah and Peters (2020).

By introducing an additional weight function in the test statistic, one can modify the set of alternatives against which the test has power. Let be a bounded measurable function. If we use the weighted product of the residuals

as the basis of the test statistic defined in (8), is now a normalised estimate of . Under the null hypothesis of , we still have

but now, the test has power against alternatives with . A weight function with exists if and only if is not almost surely equal to , see Equation (1). Typically, is unknown, so we do not know a suitable weight function. A possible strategy is to perform sample splitting and estimate a weight function on the first part of the sample (WGCM.est). This approach is treated next. Another approach is to calculate the test statistic for multiple weight functions and then to aggregate the results (WGCM.fix). This will be treated in Section 2.3.

2.2 WGCM with Estimated Weight Function (WGCM.est)

We have seen in Equation (1) that a desirable weight function for the WGCM is for example . We do not know in practice, but we can estimate it. We propose the following procedure:

Method 1 (WGCM.est)

Using one random sample split, create two independent data sets and . We use the data set to estimate a weight function and calculate the test statistic on the data set as in Section 2.1. For ease of notation, we still assume that consists of samples, whereas the size of the data set is arbitrary (but depends on ). The ratio between the sizes of the data sets and is difficult to choose in practice. We propose to estimate a weight function as follows:

-

1.

(Nonlinearly) regress on to get and on to get . Let and .

-

2.

(Nonlinearly) regress on to get which is an estimate of .

-

3.

Set .

The following two theorems do not assume this particular choice of based on the , but only require it to be estimated on a data set independent of . Note that the estimated weight function is not required to converge for . This is important, since under the null hypothesis, we have a.s. Thus, an estimate of of the form will typically not converge under the null hypothesis.

We consider the setting of Section 2.1 with the difference of replacing by

| (9) |

and redefine the test statistic (8) by

| (10) |

2.2.1 Distribution Under the Null Hypothesis

We will repeatedly use the quantities

| (11) | ||||||

| (12) |

The following theorem gives conditions under which the test statistic is asymptotically standard normal. In the case of constant weight function (and without sample splitting), it reduces to Theorem 6 in Shah and Peters (2020).

Theorem 1 (WGCM.est)

Let , , and be defined as in (11) and (12). Assume that the weight function is estimated on a data set independent of and let be defined as in (10). Assume that there exists such that for all we have for all . Define

-

1.

Let . Assume that , and . If there exists such that and if -almost surely there exists such that , then

-

2.

Let . Assume that , and . If there exists such that and if there exists such that for all , we have -almost surely , then

A proof can be found in Appendix C.

Remark 2

-

1.

An estimate of the form satisfies

so is satisfied.

-

2.

It would be desirable to do both the estimation of the weight function and calculating the test statistic on the full sample. However, the condition that the weight functions are estimated on an independent data set cannot be removed in general. If the weight function was allowed to depend on , one could take functions with . This would always lead to a positive test statistic, which would contradict the asymptotic normality under the null hypothesis.

-

3.

The conditions on the quantities , , and are reasonably weak. It is for example enough if and have mean squared prediction error (MSPE) of order , see Remark 7 in Shah and Peters (2020). An MSPE of order can for example be obtained for real-valued with bounded support if and are Lipschitz continuous, see for example Györfi et al. (2002), or for high-dimensional with sparse and linear and , see for example Bühlmann and van de Geer (2011). Moreover, the rates can also be satisfied using kernel ridge regression, see Section 4 of Shah and Peters (2020).

2.2.2 Power

In order to state a general power result, we need to make additional assumptions. We follow the path of Theorem 8 in Shah and Peters (2020) and assume that and have been estimated on another additional data set independent of and . This means that we have three independent data sets involved.

-

1.

An auxiliary data set to estimate and .

-

2.

The data set to calculate the test statistic.

-

3.

The data set to estimate the weight function .

Whereas the sample splitting, that is, the independence of the and is important in practice, the auxiliary data set to estimate and is mainly needed for technical reasons. In practice, it is usually recommended to use the original version of WGCM.est used in Section 2.2.1, see also Section 3.1.1. in Shah and Peters (2020) for a more detailed discussion.

Theorem 3 (WGCM.est)

Consider the setup of Theorem 1. Let , , and be defined as in (11) and (12) with the difference that and have been estimated on an auxiliary data set independent of and . Assume that there exists such that for all we have for all . For , let

Then, the following holds:

-

1.

Let . Assume that , and . Assume that there exists such that and that -almost surely there exists such that . Then, we have

where is defined in (8).

-

2.

Let . Assume that , and . If there exists such that and if there exists such that for all , we have -almost surely , then

A proof can be found in Appendix C.

Remark 4

If instead of estimating the weight function, one uses a fixed weight function , Theorem 3 implies that if , the test statistic is of order . That is, if , the WGCM with fixed weight function has asymptotic power against alternative .

We recommend to obtain by estimating , for example using Method 1. Recall the notation from (3). Fix , that is, is not almost surely equal to and assume that we can consistently estimate , wherever , that is

Defining

it follows that , because by the Cauchy-Schwarz inequality

Hence, with high probability, is bounded away from and we arrive at the following corollary.

Corollary 5 (WGCM.est)

Let , that is is not almost surely equal to . In the setting of Theorem 3, assertion 1., assume that

Then, for all ,

that is, WGCM.est has asymptotic power against alternative for any significance level .

Remark 6

Under the conditions of Corollary 5, WGCM.est has asymptotic power for alternatives . This is a larger class compared to the GCM, which has power against alternatives in the class , that is .

-

1.

However, with Method 1 our additional requirement that can be consistently estimated is not straightforward to verify, since there are two regressions involved. Intuitively, we will have that for the regression in step 1 of Method 1, is close to . Even if the regression method in 2 is consistent, we still need that it is also not too much affected by the difference between and . This will depend on the regression method applied in step 2.

-

2.

One could use the following observation to obtain an alternative method to estimate . By definition,

Hence, additionally to the functions and , one could try to also estimate the function using a regression of on . The consistency condition in Corollary 5 could then be replaced by consistency conditions for estimating , and which might be easier to justify than for the two-step approach of Method 1. However, the estimation of seems to be less reliable for finite samples using this method compared to using Method 1, which also leads to reduced power.

2.2.3 Binary Variables

If and are binary, we can use the same methodology to obtain a test that has asymptotic power 1 against any alternative, provided that the conditions of Theorem 5 and Corollary 5 hold.

Assume that and take values in . By (6), we have that a.s. if and only if . We thus obtain the following result for binary and .

Corollary 7 (WGCM.est, binary case)

Let and be binary and assume that the distribution of satisfies . In the setting of Theorem 3, assertion 1., assume that in probability. Then, for all ,

that is, WGCM.est has asymptotic power against alternative for any significance level .

Using dummy coding, this methodology can be extended to arbitrary categorical and variables, see Appendix A.3.

2.3 WGCM With Several Fixed Weight Functions (WGCM.fix)

We consider an alternative to the sample splitting approach. We calculate the test statistic for several fixed weight functions and aggregate the results. Consider the same setting as in Section 2.1. Let be bounded functions from . For , let be the vector of products of the residuals weighted by , that is,

Let be the test statistic of the WGCM based on the vector , that is,

| (13) |

where is the sample average of the coordinates of . Finally, let

For a fixed number of weight functions, the simplest approach would be to perform an individual test for each weight function and use Bonferroni correction to aggregate the -values. With the aggregated test statistic

the Bonferroni corrected -value is therefore

In this case, it is straightforward to obtain a variant of Theorem 1 (stating that is a conservative -value) and a variant of Theorem 3 (stating that the method has asymptotic power 1 if there exists with ).

However, we can also use more sophisticated methods to calculate a -value for . With fixed, it is possible to show that under the null hypothesis of (i.e. ), the vector converges to a multivariate Gaussian distribution. In fact, we go one step further and propose the same procedure as in Section 3.2 of Shah and Peters (2020), where the multivariate case of the (unweighted) GCM is treated. For technical reason, it is assumed that . We do not assume that is fixed, but it is allowed to grow with . Define

Let have a multivariate normal distribution with covariance matrix and mean . Let

and let be the quantile function of given . Note that is random and depends on the data. can be approximated by simulation. Recent results by Nadarajah et al. (2019) also allow to calculate analytically. For a significance level we propose the following test.

Method 2 (WGCM.fix)

Reject the null hypothesis if . The corresponding -value is given by

We need the following conditions on the errors and . Let .

-

(A1a)

;

-

(A1b)

;

-

(A2)

for some constants that do not depend on .

We obtain the following theorem. It is the adaptation of Theorem 9 in Shah and Peters (2020) to our setting.

Theorem 8 (WGCM.fix)

Let and let , , and be defined as in (11) and (12). Assume that there exist such that for all and there exists such that either (A1a) and (A2) or (A1b) and (A2) hold. Furthermore, assume that there exist (independent of ) such that for all and we have and . Assume that

| (14) | |||

| (15) |

Assume that there exist sequences and of real numbers such that

| (16) | |||

| (17) |

Then,

The proof can be found in Appendix D.

Remark 9

-

1.

If the errors and are sub-Gaussian with parameters bounded by some independent of , then by Lemma 39 in Appendix G, their product has a sub-exponential distribution, with parameters bounded independent of , see also Remark 10 in Shah and Peters (2020). A summary of results on sub-Gaussian and sub-exponential distributions can be found in Appendix G. If is sub-exponential with bounded parameters, then condition (A1a) is satisfied: By Definition 38, 2., there exists such that for all ,

For , we get that

Thus, we can choose such that for we have and set .

- 2.

The approach WGCM.fix always yields a lower -value than using Bonferroni correction. To see this, let , for a covariance matrix with for all . Then, we have for

By replacing with , and by , it follows that . As an immediate consequence of Theorem 3 and Remark 4, we get the following result on the power of WGCM.fix for a fixed number of weight functions. Recall the set from (5).

Corollary 10 (WGCM.fix)

Let . Let , , and be defined as in (11) and (12) with the difference that and have been estimated on an auxiliary data set independent of . Let be fixed. Assume that there exists such that for all and all , we have . Assume that , and as well as for all and . If for , that is if there exists such that , then for all ,

that is, WGCM.fix with fixed number of weight functions has asymptotic power against alternative for any significance level .

2.3.1 Choice of Weight Functions

We give a few heuristics on how to choose the weight functions in practice.

For a fixed alternative , a promising weight function satisfies . We know, that such a exists if and only if is not almost surely equal to .

Let us first assume that . For , define the functions

Then, we have that a.s. if and only if for all in the support of . To see this, define . Then,

If for all in the support of , then taking the derivative with respect to yields for all in the support of .

Therefore, it intuitively seems a good idea (in addition to the constant weight function ) to use the functions for some . In practice, one can for example take at the empirical -quantiles of . However, the choice of is a difficult problem. Theorem 8 allows for to be large compared to . However, if is too large, one is in danger of performing too many tests and loosing power again. This tradeoff makes the choice of difficult. In practice, we have experienced that a small number of weight functions is usually sufficient. For the experiments in Section 3, we will use weight functions.

For , one can for example take functions

where is the empirical -quantile of . This means that including the constant weight function , we have weight functions in total. For the experiments in Section 3, we will use weight functions per dimension of .

3 Experiments

We implement all our methods in R. Our implementations are based on the functions from the package GeneralisedCovarianceMeasure, see Peters and Shah (2019). Our code is available as the R-package weightedGCM on CRAN.

3.1 Detailed Comparison

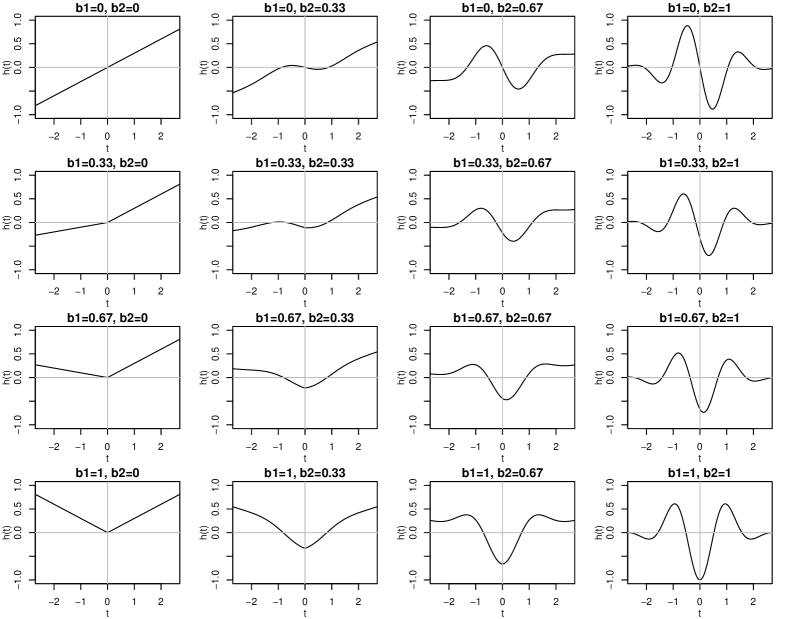

We have seen that for the introductory example in Section 1.1.2, the power of the GCM heavily depends on the function introducing the dependence, whereas WGCM.est and WGCM.fix are more stable in this respect. To investigate the observed effect more systematically, we consider a family of functions indexed by two parameters , where is a parameter for symmetry and is a parameter for wiggliness. Define

and let

Plots of the functions for various values of and can be found in Figure 2.

3.1.1 Null Hypothesis

We first look at the level of the tests under the null hypothesis in the following three settings, which are similar to Section 5.2 in Shah and Peters (2020):

-

(1D)

;

-

(10D.Add)

;

-

(10D.NonAdd)

;

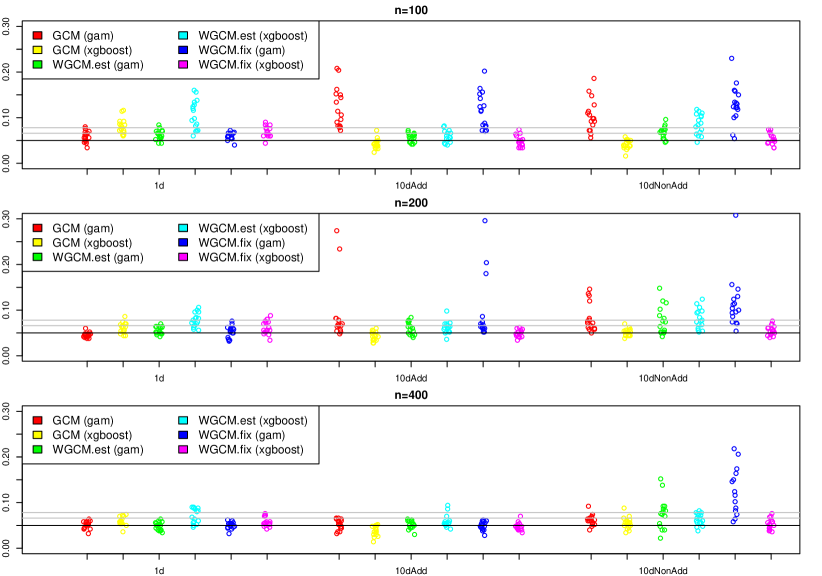

For every combination of , we simulate data sets with samples for each setting and perform the following tests:

-

(GCM)

The (unweighted) GCM by Shah and Peters (2020).

-

(WGCM.est)

The WGCM with one single estimated weight function, where of the samples are used to estimate the weight function.

-

(WGCM.fix)

The WGCM with fixed weight functions

where is the empirical -quantile of . Additionally, we take the constant weight function . We will use . This means we have a total of weight functions in the setting (1D) and weight functions in the settings (10D.Add) and (10D.NonAdd).

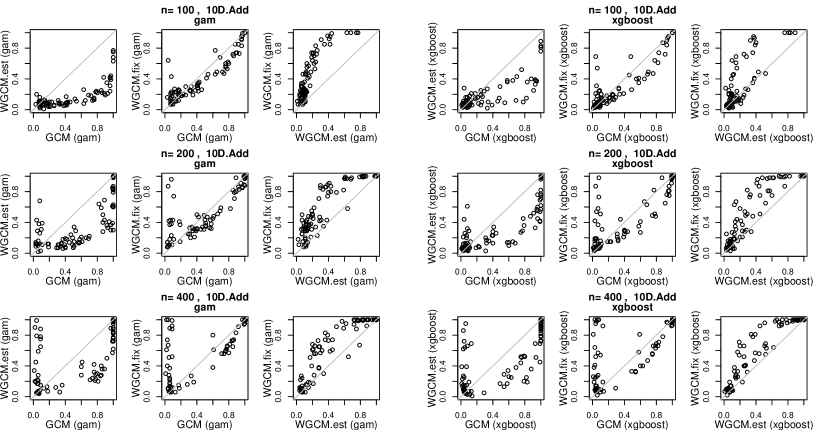

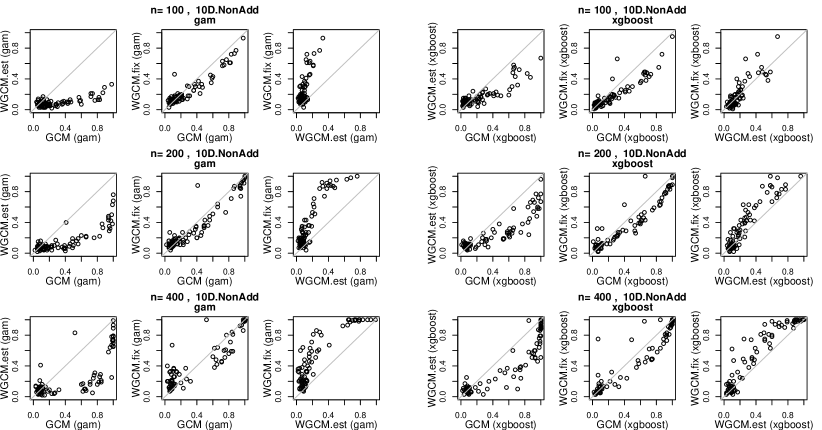

We perform all three tests both with regression splines using gam from the R package mgcv (see Wood, 2017) and with boosted regression trees using the package xgboost (see Chen and Guestrin, 2016 and Chen et al., 2021). For WGCM.est, we always use the same regression method both for step 1 and step 2 of Method 1 and for the calculation of the test statistic. Plots of the rejection rates at level can be found in Figure 3. For each combination of setting and method, we plot the rejection rate for all 16 combinations of and . The lower horizontal gray line denotes the individual one-sided test region at level for each dot based on a distribution. The upper horizontal gray line denotes the joint one-sided test region at level for each group of dots based on i.i.d. variables.

We see that with a sample size of and in the settings (1d) and (10dAdd), all the methods seem to perform reasonably well in the sense that the rejection rates are not significantly larger than . In the setting (10dNonAdd), the methods based on gam seem to reject too often. This was to be expected since gam assumes an additive structure. For lower sample size, some of the methods seem to reject too often also in the settings (1d) and (10dAdd). The guarantees for the level of the tests heavily rely on the quality of the approximation of and . Therefore, we suspect that the large rejection rates in some settings with and are due to the fact that some of the functions used in the simulation are too complex to be well approximated with the smaller sample sizes.

3.1.2 Alternative Hypothesis

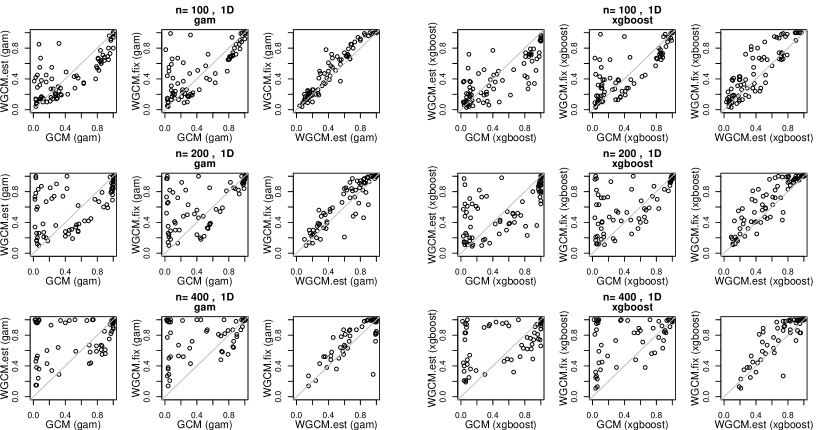

For the alternative, we consider the same settings (1D), (10D.Add), (10D.NonAdd), but modify them by adding to for some . We simulate 100 data sets for every combination of and and calculate the rejection rates of the methods GCM, WGCM.est and WGCM.fix both with gam and xgboost.

A significant difference to the simulations in Section 5.2 of Shah and Peters (2020) is that the function introducing the dependence is not just a linear function, but is also varied.

For each setting (1D), (10D.Add) and (10D.NonAdd), both regression methods gam and xgboost and sample sizes , we plot the rejection rates of the three methods GCM, WGCM.est and WGCM.fix against each other. Thus, each subplot consists of points, each corresponding to one combination of , , and , see Figures 4, 5 and 6.

Let us first look at the first, second, fourth and fifth columns of the plots. These plot the rejection rates of GCM against the rejection rates of WGCM.est and WGCM.fix, respectively. We see that the behavior of the GCM and the two variants of the WGCM is asymmetric. The part on the bottom right of the corresponding plots is free, indicating that there are no situations where the GCM has a very high and the WGCM a very low rejection rate. In contrast, we see situations where the WGCM has a high, but the GCM a low rejection rate (points in the top left). The effect gets more pronounced for larger sample size. Nevertheless, there are also many points below the diagonal connecting and . These indicate situations, where the GCM works better than the WGCM. To summarise, we see that indeed, the WGCM enlarges the space of alternatives against which the test has power. This comes at the cost of having less power in situations where the GCM already works well. In the setting (10D.NonAdd), the majority of the points lies below the diagonal in the plots comparing GCM to one of WGCM.fix and WGCM.est. As mentioned and observed in the simulations under the null hypothesis, we should not put too much trust in the results of (10D.NonAdd) with regression method gam. For the results using xgboost, it may also be possible that the picture would look more similar to the situations (1D) and (10D.Add) for larger sample size.

The third and sixth column of the plots compare the rejection rates of WGCM.est and WGCM.fix. We observe that WGCM.fix seems to perform better than WGCM.est, where the effect is more pronounced for (10D.Add) and (10D.NonAdd) than for (1D). However, by changing some parameters of the methods, for example the fraction of the samples used to estimate the weight function in WGCM.est and the number and type of weight functions for WGCM.fix, the picture could possibly look different.

3.2 Variable Selection and Importance

In this section, we briefly sketch how conditional independence tests allow to perform variable selection tasks.

Suppose we have a response variable and predictors , where all random variables take values in . For all , we can test

We expect the corresponding -value to be small if yields additional information for predicting that is not contained in . This can be seen as a generalization of the individual -tests in linear regression. We can then look, for which the variable is significant after a multiple testing correction. This approach is for example described in Watson and Wright (2019), where they compare it to a new method.

The following example is taken from Azadkia and Chatterjee (2019), where it appears as Example 7.4, with the difference that we only use a 50-dimensional and samples instead of a 1000-dimensional with samples. We use GCM, WGCM.est and WGCM.fix with xgboost for the regressions.

Example 1

Let be i.i.d. and let , where independent of . We simulate data sets with a sample size of . For each data set and all , we calculate a -value for using the three tests. After a multiple testing correction using Holm’s procedure (Holm, 1979), we observe that GCM never finds the correct set of predictors at significance level , but most often, it just finds and as significant variables. WGCM.est finds the correct set of predictors in 86 out of 100 cases and WGCM.fix even finds the correct predictors in 99 of the 100 cases. We use the same type of weight functions with as in Section 3.1.1 for WGCM.fix and for WGCM.est, we use of the samples to estimate the weight functions.

Hence, this example illustrates that the two variants of the WGCM can find more dependencies than the GCM. In the following, we also look at some real data sets.

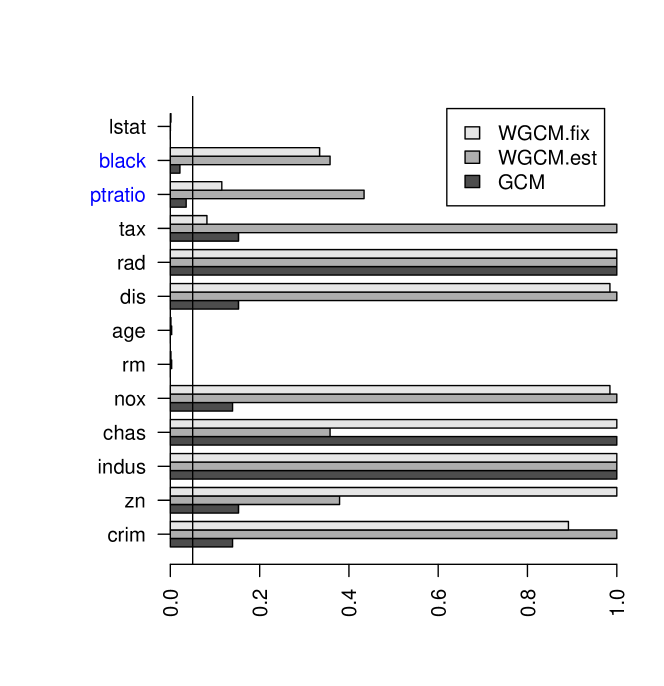

3.2.1 Boston Housing Data

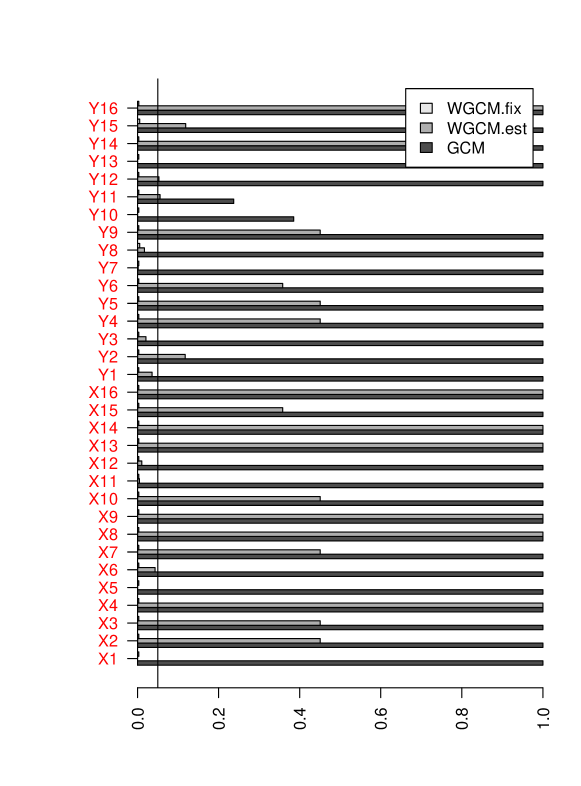

As a first example, we analyse the Boston housing data, see Harrison and Rubinfeld (1978). Among the set of 13 predictors, we want to find the most relevant ones to predict the target variable medv, which is the median value of owner-occupied homes. Plots of the -values after multiple testing correction using Holm’s method can be found in Figure 7. We performed all regressions using xgboost for GCM, WGCM.est and WGCM.fix

We see that in this case, the GCM finds significant variables at significance level , whereas WGCM.fix and WGCM.est only find . Hence, this is an example where the original GCM performs moderately better (in terms of power) than the new variants.

3.2.2 Online News Popularity Data

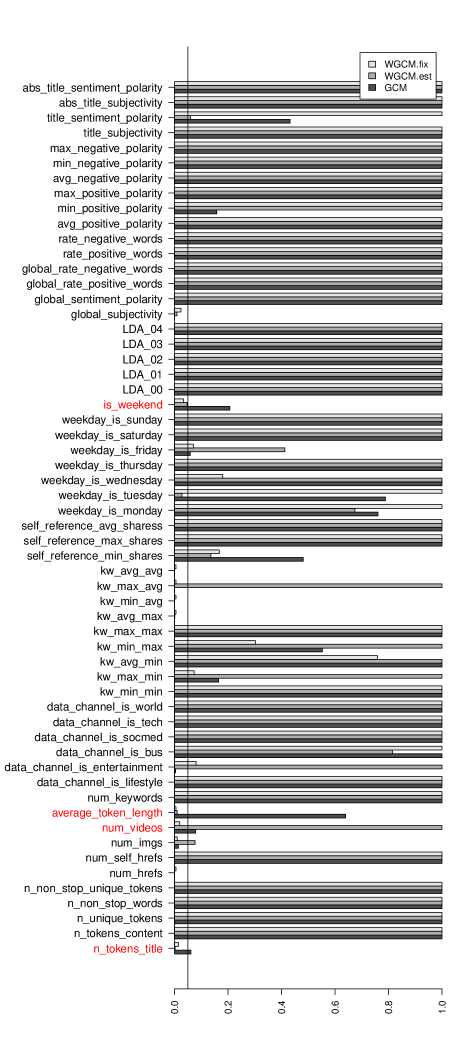

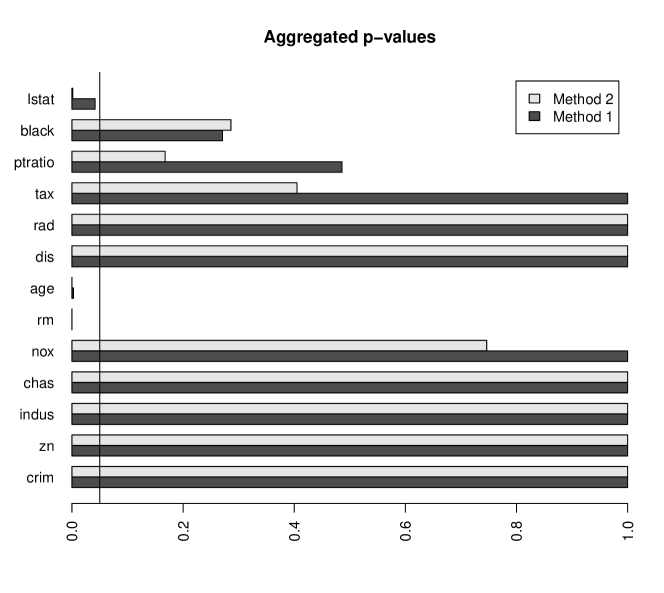

We analyse the online news popularity data set, see Fernandes et al. (2015). The data can be obtained from the UCI Machine Learning Repository, see Dua and Graff (2017). Removing missing values, we have observations of predictors and one target variable. Each observations corresponds to one article published by www.mashable.com. The target variable is the number of shares of the article, whereas the predictors are various features of the article, ranging from the number of words to sentiment scores. For the analysis, we take the log-transform of the target variable. Plots of the -values for the three methods can be found in Figure 8. We performed the regressions using xgboost for GCM, WGCM.est and WGCM.est.

We see that in this case, the GCM finds significant variables at significance level , whereas WGCM.est finds significant variables and WGCM.fix finds significant variables. Hence both versions of the WGCM perform slightly better (in terms of power) than the original GCM.

3.2.3 Wave Energy Converters Data

We look at the wave energy converters data set, available at the UCI Machine Learning Repository (Dua and Graff, 2017). The data set displays the (simulated) power output for different configurations of wave energy converters in different real wave scenarios, see Neshat et al. (2020). We restrict ourselves to the data of Tasmania. We have predictor variables, which consist of the and -coordinates of wave energy converters forming a wave farm. The target is the total power output of the farm. We randomly sample of the configurations in the data set. By symmetry, it seems reasonable that either no or all predictor variables are significant. In fact, with Holm’s method to adjust for multiple testing, GCM does not find any significant predictor at significance level , whereas WGCM.fix considers all predictors significant and WGCM.est finds significant predictors. Plots of the -values for the three methods can be found in Figure 9. In this case, the two WGCM methods are clearly superior to GCM (in terms of power).

4 Conclusion

We have introduced the weighted generalised covariance measure (WGCM) as a new test for conditional independence and we provide an implementation in the R-package weightedGCM, which is available on CRAN. The WGCM is based on the generalised covariance measure (GCM) by Shah and Peters (2020). We gave two versions of the WGCM in the setting of univariate and . Their generalisations to the setting of multivariate and can be found in Appendix A. To give guarantees for the correctness of the tests under appropriate conditions, we could benefit from the work by Shah and Peters (2020). We prove that WGCM.est and WGCM.fix have full asymptotic power against a broader class of alternatives than GCM. Finally, we compared our methods to the original GCM using simulation and on real data sets. We have seen for finite samples that our approach allows to enlarge the set of alternatives against which the test has power. This comes at the cost of having reduced power in settings where the GCM already performs well. An application in a variable selection task on real data sets confirmed that it depends on the data at hand which method is to be preferred. If the sample size is small and the form of the dependence is simple, the GCM will typically be the better choice. However, if the sample size is moderately large, choosing WGCM.fix or WGCM.est is typically beneficial.

4.1 Practical Issues

Choosing the optimal test among the GCM and the two versions of the WGCM remains a challenging task in practice, though it is always possible to perform several tests and use a multiple testing correction. It is worth mentioning that in principle, one could combine WGCM.est and WGCM.fix by including an estimated weight function together with the fixed weight functions of WGCM.fix. Such a case is implicitly covered by Theorem 14 in Appendix A.2. However, including an estimated weight function has the disadvantage that also the analysis of the fixed weight functions can only be done on half of the sample. For this reason, we think that performing the two tests WGCM.est and WGCM.fix individually and using Bonferroni correction is the better choice for combining the two tests.

Moreover, the randomness of the sample splitting for WGCM.est leads to the question how stable the test is with respect to this random split. We investigate this in Appendix B. Methods to aggregate -values obtained from multiple sample splits are for example treated in Meinshausen et al. (2009) and in DiCiccio et al. (2020). The -values obtained using such methods are more stable and provably controlling type I error. However, it is not clear how they affect the power of the test, even though the methods were found to improve power as well in other problems, see Meinshausen et al. (2009).

4.2 Outlook

There are many other open questions remaining. On the theoretical side, it would be desirable to give more concise results about the power properties of WGCM.est and WGCM.fix. For WGCM.est, Corollary 5 relies on the consistency of Method 1 to estimate , which is not straightforward to verify and depends on the regression method used. For WGCM.fix, it would be interesting to see, if there is a set of fixed weight functions with better properties than the ones described in Section 2.3.1.

On the practical side, there are many parameters that can be varied and whose effects could be inspected more closely. For WGCM.est, it would be desirable to have guidelines for the fraction of the data to be used to estimate the weight function. For WGCM.fix, the choice of the number of fixed weight functions is unknown for optimal power. However, our current default choice used in the empirical analysis seems to work reasonably well.

Also Method 1 to estimate the weight function could be investigated further. We do not claim our procedure to estimate to be optimal. It is simply a straightforward way how the conditions of Theorem 1 can be satisfied. However, there might be more powerful procedures. It could be worth investigating if a smoothed version of the sign is beneficial. This would have the advantage of giving less weight to values of for which the estimate of is close to and which are thus more likely to obtain the wrong sign. However, the smoothed version of the sign still has to be scaled in such a way that the conditions for the correct null distribution are satisfied.

Acknowledgments

We are grateful to Rajen D. Shah for pointing out that WGCM.est has power against all alternatives for binary and . We thank Rajen D. Shah and Jonas Peters for answering our questions about their paper Shah and Peters (2020). We also thank three referees and an action editor for helpful comments. The research of Julia Hörrmann is supported by ETH Foundations of Data Science. Peter Bühlmann received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation programme (grant agreement No. 786461).

A The Multivariate WGCM

In this section, we show how the methods of Section 2.3 can also be applied in the case of multivariate and . This can be done both in the context of fixed and of estimated weight functions.

A.1 Multivariate WGCM With Fixed Weight Functions (mWGCM.fix)

The procedure is again very similar to Section 3.2 of Shah and Peters (2020). The idea in the case of multivariate and stays the same, but we calculate the test statistic for every pair of and .

For any distribution and all and , define

Then, we can write

Let and .

Let and be estimates of and , obtained by regression of and , on . Note that is the th column of the data matrix , or equivalently the column of samples from the random variable .

For each let and let be functions from . We allow to grow with . We will work under the assumption that the functions are uniformly bounded for all , and . Let

Let be the vector of products of the residuals corresponding to and weighted by , that is,

Let be the test statistic of the WGCM based on the vector , that is,

| (18) |

with being the sample average of the coordinates of . Finally, let be the vector of all test statistics. We consider the maximum absolute value of the vector as a test statistic,

In summary, everything works similarly to the univariate case with the added complication of having expressions with three subscripts instead of one. Define by

Let have multivariate normal distribution with covariance and mean and let

Let be the quantile function of given . is random, depends on the data and can be approximated by simulation. We need similar conditions to (A1a), (A1b) and (A2) for Theorem 8. Let

Consider a sequence with .

-

(C1a)

for all , and ;

-

(C1b)

for all and ;

-

(C2)

for some constants that do not depend on .

We obtain the analogue of Theorem 8 (and also of Theorem 9 in Shah and Peters, 2020). For and , let

| (19) | |||

| (20) |

Theorem 11 (mWGCM.fix)

Let . Assume that there exist such that for all and there exists such that either (C1a) and (C2) or (C1b) and (C2) hold. Furthermore, assume that there exist (independent of ) such that for all , and and for all , we have and . Assume that

| (21) |

Assume that there exist sequences and as well as positive real numbers , , and possibly depending on such that for all ,

and such that

| (22) | |||

| (23) |

Then,

Remark 12

-

1.

The idea behind the sequences , , and is that they allow for a more general scaling than the simplified setting in the next item. Note that by , we have that , where and . If for example and are a.s. constant equal to some and , we can take and . In this case, conditions (22) and (23) are just conditions on the errors , scaled by their standard deviation and on , scaled by the error variance.

-

2.

Assume that there exists independent of such that for all , all and we have

(24) Then, we can replace by in conditions (C1a), (C1b) and (C2). Furthermore, we can replace the sequences , , and by in conditions (22) and (23) and we can replace condition (21) by

see also the next item.

If in addition to (24), we also have that the errors and have sub-Gaussian distributions with parameters uniformly bounded for all by some constant independent of , then using the same arguments as in Remark 9, condition (C1a) can be satisfied with constant independent of . Moreover, we have that . If for example both

then the modified versions of conditions (21), (22) and (23) are all satisfied.

-

3.

If there exists such that for all and all and we have

then inspection of the proof shows that condition (21) can be replaced by

In analogy to Corollary 10, we obtain the following result about the power of mWGCM.fix if , and all for and are fixed. For this, let and and define

| (25) | |||

| (26) |

Corollary 13 (mWGCM.fix)

Let . Let , , and be defined as in (19), (20), (25) and (26) with the difference that all and have been estimated on an auxiliary data set independent of . Let , and all for be fixed. Assume that there exists such that for all and all , we have . Assume that for all we have , and as well as for all and . If there exists and such that , then for all ,

that is, mWGCM.fix with fixed , and fixed number of weight functions for all and has asymptotic power against alternative for any significance level .

A.1.1 Choice of weight functions

As the simplest extension of the considerations in Section 2.3.1, we propose the following. For a fixed and every combination of and , use the same weight functions

where is the empirical -quantile of . This yields a total of weight functions, but the weight functions do not depend on and .

A.2 Multivariate WGCM With Estimated Weight Functions

The same procedure can be applied with estimated weight functions. We consider the same setting as in Section A.1.

The difference is that the weight functions have been estimated on an auxiliary data set independent of , obtained for example by sample splitting as in Section 2.2. For each , let , and for each , let

be functions from that have been estimated on . In general, we would recommend to set and use Method 1 to estimate . However, Theorem 14 even allows for to grow with . Let

As in Section A.1, define based on the weight functions

-

•

the vectors of weighted products of residuals ;

-

•

the test statistics of the individual WGCM;

-

•

the aggregated test statistic ;

-

•

the estimated covariance matrix ;

-

•

the multivariate normal vector and , the maximum absolute value of the components of ;

-

•

the quantile function of given .

We have the following variant of Theorem 11. Remark 12 also applies to this theorem.

Theorem 14 (mWGCM.est)

A proof can be found in Appendix E.

In the case of fixed , and if for all and , we have a combination of Corollary 5 and Corollary 13. We assume, that we use Method 1 to estimate . We denote the estimate of by . Note that we write and not , since for all .

Corollary 15 (mWGCM.est)

Let . Let , , and be defined as in (19), (20), (25) and (26) with the difference that all and have been estimated on an auxiliary data set independent of and . Let , be fixed and for all and . Assume that there exists such that for all , all and all , we have . Assume that for all we have , and as well as . Assume that there exists such that for all . If there exists and such that is not almost surely equal to and if can be consistently estimated in the sense that

then

that is, mWGCM.est with fixed , and fixed number of weight functions for all and has asymptotic power against alternative for any significance level .

A.3 Categorical Variables

The methodology for multivariate and can also be used to treat arbitrary categorical variables. This leads to a test that has asymptotic power 1 against any alternative, provided that the conditions of Corollary 15 are satisfied. Assume that takes values in and takes values in .

We can apply the methodology from Section A.1 and Section A.2 to the variables

Note that if and only if for all and for all ,

or equivalently if for all and for all , we have . In the same way as in the case of binary and in Section 2.2.3, we obtain that if and only if a.s., where and . In particular, we obtain the following version of Corollary 15.

Corollary 16 (mWGCM.est, categorical case)

Let and be categorical and assume that the distribution of satisfies . Let , , and be defined as in (19), (20), (25) and (26) with the difference that all and have been estimated on an auxiliary data set independent of and . Let , be fixed and for all and . Assume that there exists such that for all , all and all , we have . Assume that for all we have , and as well as . Assume that there exists such that for all . Since , there exists and such that is not almost surely equal to . If can be consistently estimated in the sense that

then

that is, mWGCM.est with fixed , and fixed number of weight functions for all and has asymptotic power against alternative for any significance level .

B Stability of WGCM.est with Respect to Sample Splitting

The procedure WGCM.est described in Section 2.2, depends on a random split of the sample. If one repeats the procedure several times, the -values will typically differ. In this section, we revisit the Boston housing data set, see Section 3.2.1, to investigate the effect of multiple sample splits for WGCM.est.

We repeat the analysis from Section 3.2.1 for independent splits of the sample and count for each of the predictors, how often the (Holm-corrected) -value is significant at level . A plot of the frequencies for each variable can be found in Figure 10.

We see that the variable rm is almost always significant, and the variables age and lstat are significant in more than of the cases. These were also the significant variables for WGCM.est in the original analysis in Section 3.2.1. However, the analysis indicates that the -values based on WGCM.est and hence also the number of significant variables is not very stable with respect to the randomness of the sample splitting. Depending on the split, it could well happen that only one or up to five variables are considered significant.

This leads to the question, how the -values based on WGCM.est can be made more stable. Methods to aggregate -values based on multiple sample splits have been developed in Meinshausen et al. (2009) and in DiCiccio et al. (2020). In the following, we apply the two approaches from Meinshausen et al. (2009) to the Boston housing data.

In the context of WGCM.est, let .

-

1.

Perform the test WGCM.est times with independent sample splits, obtaining -values .

-

2.

For , define the aggregated -value as

where is the empirical -quantile.

If the -values are asymptotically correct, then is also an asymptotically correct -value, see Theorem 3.1 Meinshausen et al. (2009).

However, one cannot simply search for yielding the lowest value of . Instead, for a fixed lower bound define

This is also an asymptotically correct -value, see Theorem 3.2 in Meinshausen et al. (2009).

For the Boston housing data set, we again apply the procedure from Section 3.2.1 for independent splits of the sample, but without applying Holm’s method. For each of the predictors, we calculate the corresponding aggregated -values with (Method 1) and with (Method 2). At the end, we apply Holm’s correction once to the -values from Method 1 and once to the -values from Method 2. Plots of the -values based on this procedure can be found in Figure 11. We see that for both aggregation methods, still the variables rm, age and lstat are significant.

In principle, applying WGCM.est with multiple sample splits is a good idea, as it makes the -values more stable. A caveat is however that especially in these variable importance examples, the runtime gets quite big, as there are already many tests involved in the procedure, even if only one sample split is used.

C Proofs of Section 2.2

In this section, we give the proofs of the Theorems on the univariate WGCM with single fixed and single estimated weight function.

C.1 A More General Result

To prove Theorem 1, we use the following more general result. Let . For and , define

To be more precise, is the set of measurable functions with those properties. For each , let

and let

| (27) |

Then, we have the following result under the null hypothesis:

Theorem 17

We also have a more general power result. Let . For and , let

C.2 Proofs

C.2.1 Proof of Theorem 17

Proof The proof closely follows the proof of Theorem 6 in Section D.1 in the supplementary material of Shah and Peters (2020). We will sometimes omit the dependence on and in the notation. We will repeatedly use limit theorems from Appendix F

Fix and write instead of . For , and , define

We first prove that

To simplify notation, we will abbreviate this in the following with

| (28) |

This is an application of Lemma 31, where the random variable corresponds to . Instead of the set of distributions for in Lemma 31, we look at the set of distributions determined by for where varies in and varies in . We have

and as well as

by assumption, so the lemma implies (28).

In the following, we will repeatedly apply Lemmas 32, 33 and 34 over the class of distributions for determined by in a similar fashion.

For , define

We first prove that

| (29) |

Observe that

| (30) |

with

In analogy to the notation of (28), we write for a sequence of random variables depending on ,

if for all ,

For , by the Cauchy-Schwarz inequality,

| (31) |

since is independent of and by assumption.

Next, we want to control and . For ,

Thus,

by assumption. Since is independent of , we get that

| (32) |

Thus, for all using Markov’s inequality,

Equation (32) and Lemma 34 applied to the variables with distributions determined by therefore imply that . Similarly, .

Next, we aim to prove

| (33) |

For this, it is enough to prove

| (34) |

by continuity of at .

Recall that

Since by (29), , it follows that . To prove (34), it therefore suffices to prove

| (35) |

For this, write

| (36) |

For , observe that and . Thus, we have

Observe that

by assumption. Furthermore, for all

similarly as before. Since by assumption, Lemma 34 implies that and thus,

| (37) |

Similarly, also . Moreover,

| (38) |

By Lemma 32, we have that for all

so

| (39) |

The second factor in (38) is equal to . This implies . In total, we get

| (40) |

For , we have

By (37), , so using (39), also

Similarly, . Combining this with (40) and (36), we get

With Lemma 32, we obtain that for all

and thus,

Since , we obtain

so (35) and (33) follow. Since , we get by Lemma 33 with (29)

This concludes the proof.

C.2.2 Proof of Theorem 1

Proof The statement 2. follows from Theorem 17 in the following way: For , and , let

with defined as in (27). By Theorem 17, we have

For the auxiliary data set , let be the sequence of functions estimated on . From the assumptions of Theorem 1, 2., we know that there exist such that for all , -almost surely for all we have . Since is independent of , we have

Using iterated expectations, it follows that

This concludes the proof of 2. The statement 1. can be proven in a similar fashion, but since we do not require uniformity over a collection , it is enough to have

| (41) |

Then, one can conclude using dominated convergence. To show (41), it is enough to a.s. have such that , so is allowed to depend on .

C.2.3 Proof of Theorem 18

Proof The proof is very similar to the proof of Theorem 17, see also the proof of Theorem 8 in Section D.3 in the supplementary material of Shah and Peters (2020). We will therefore only sketch the main steps. Apart from not assuming the null hypothesis anymore, a main difference is that we have a data set independent of on which and have been estimated.

Let

and

We first prove that (with the notation of (28) and (29))

| (42) |

For this, write

| (43) |

with , and defined as in (30). Similarly to (28), one can show that

The term can be controlled as in (31). For the term , replace conditioning on by conditioning on and similarly for . Since , we arrive at (42).

Next, we prove

| (44) |

which follows from Recall that

| (45) |

Since by (42), , we have

| (46) |

Next, we show

| (47) |

For this, write

exactly as in the proof of Theorem 17. By replacing conditioning on with conditioning on , one can show

in the same way as there. Using Lemma 32, one can show

so this implies (47).

C.2.4 Proof of Theorem 3

D Proof of Theorem 8

To prove Theorem 8, we use the strategy of the proof of Theorem 9 in Section D.4 of Shah and Peters (2020). We will heavily rely on results from Chernozhukov et al. (2013), which we summarise in the following.

D.1 Summary of Results on Gaussian Approximation of Maxima of Random Vectors

We present the following results in the form they are also presented in Section D.4.1 in Shah and Peters (2020), which are sometimes special cases of the corresponding results in Chernozhukov et al. (2013). There is the following difference to the results given there: We consider maxima of absolute values of random vectors instead of maxima of random vectors. The results for the maxima translate to the corresponding results for the absolute value by considering the vector instead of just the vector .

Assume , with for . Assume possibly depending on . Let . Let be a random vector taking values in with and and let be i.i.d copies of . Let

where is the th component of . We need the following conditions for some sequence with :

-

(B1a)

for all ;

-

(B1b)

for all ;

-

(B2)

There exist some constants such that .

The following Lemma corresponds to Corollary 2.1 in Chernozhukov et al. (2013) and Theorem 22 in Shah and Peters (2020):

Lemma 19

Assume that either (B1a) and (B2) or (B1b) and (B2) hold. Then, there exist constants depending only on and such that

The next Lemma corresponds to Lemma 24 in Shah and Peters (2020) and follows from Lemma C.1 in Section C.5 of Chernozhukov et al. (2013) (first statement) and is an application of Lemma A.1 in Section A.1 there (second statement).

Lemma 20

Again assume that either (B1a) and (B2) or (B1b) and (B2) hold. Let be the empirical covariance matrix of . Then, there exist constants depending only on and such that

The following lemma corresponds to Lemma 2.1 in Chernozhukov et al. (2013) and to Lemma 21 in Shah and Peters (2020).

Lemma 21

Let have a multivariate Gaussian distribution with and for all . Then, there exists a universal constant such that for all

Define the function

One may check by differentiating that is increasing in .111In Chernozhukov et al. (2013) and Shah and Peters (2020), the definition is . Although it is not essential for the proof, we consider it to be convenient for the function to be increasing in . The following Lemma corresponds to Lemma 3.1 in Chernozhukov et al. (2013) and to Lemma 23 in Shah and Peters (2020).

Lemma 22

Let and be centered multivariate Gaussian random vectors taking values in . Let have covariance matrix and have covariance matrix , such that for , we have . Let . Then, there exists a universal constant such that

-

1.

-

2.

Let and be the quantile functions of and . Then, for all

Note that 2. follows from 1. by observing that

so . Similarly, the second statement of 2. follows.

D.2 Proof of Theorem 8

We prove a slightly more general result, similar to Section C.1, since we later also want to apply a version of this theorem and its proof to estimated weight functions, see Appendix E.

For and , define

For , let and be the versions of and based on .

Theorem 23

Proof [Proof of Theorem 23] We closely follow Section D.4.2 in Shah and Peters (2020). In the following, we will often omit dependencies on , and and we will often write instead of there exists a constant independent of , and such that .

Fix and write . For , and let

We have for all

We will need the conditions (B1a)/(B1b) and (B2) to hold for the random vectors

This is guaranteed by (A1a)/(A1b) and (A2), since

Consider the definition (13) of . Write with

Write

It follows that

Define and define the matrix by

Note that the diagonal of consists of ones. Let be a random vector with distribution . Let and let be the quantile function of . Note that , , and all depend on and . Lemma 21 implies that the distribution function of is continuous, so for all , we have . Our goal is to bound

For this, define

Fix and . Let denote the symmetric difference. Using the triangle inequality and , we have

Let . By Lemma 22, implies . This means that if , we have that implies and implies . We obtain

In total, we obtain

For , define the event . Observe that , so on , we have that implies that and thus . Similarly, if , then we have . This implies that for all , we have

Therefore,

where the last line follows by reparametrisation. Now, we write

By Lemma 19, it follows that with independent of and . By Lemma 22, we get that , since . Since , we have

By Lemma 21, there exists such that

Combining , and , we get that

Similarly, also

In total, we obtain

Define

| (52) |

We first show, how to conclude with the help of Lemma 24 below. Take , such that . Then, we have and . Take , such that . Then, we have and

since and . The same argument works for the terms involving . It follows that

which concludes the proof.

Next, we prove the following Lemma that corresponds to Lemma 26 in Shah and Peters (2020).

Lemma 24

Proof Define for ,

We start with 1. As in the proof of Theorem 17, we can write with

Remember that , and . Using Cauchy-Schwarz, we have . By condition (48),

To control , we use Lemma 27, see below. For

for all . By condition (50), , so for any , there exists such that for all . We have that

by condition (50). Using bounded convergence (Lemma 34), we get that

Since are arbitrary, we get . Similarly, we also have . This concludes the proof of 1.

For 2., note that by definition and thus,

with

for . The first term is by Lemma 25 below. The second term is using Lemma 20. For the third term, write

Observe that by condition (A2), we have . Thus, . Using this and 1., we have

Together with Lemma 20, we obtain

| (53) |

In total, we get

Using Lemma 26 below with , we obtain . This proves 2.

For 3., Lemma 20 implies , so it is enough to show . Observe that

| (54) |

using Lemma 25 and (53). By 2. and Lemma 26, it follows that

This implies that also

| (55) |

Putting things together, we have

Using (54), Lemma 20 and (55), the first term is and the second term is also by (54). This proves 3.

It remains to prove the following Lemma corresponding to Lemma 27 in Shah and Peters (2020).

Lemma 25

For , let

Then,

Proof With , write for and

We show that the sum over each of the eight terms is individually. Since the terms on the right hand side of the inequality do not depend on anymore, this implies that the sum over the left hand side is . Note that by symmetry it is enough to control only one term in each line.

To start, observe

For the second term, . Observe that similarly to the proof of Theorem 17

using condition (49) and bounded convergence (Lemma 34), so

| (56) |

This can also be used for the third line. For the fourth line, we use Cauchy-Schwarz to write

The first factor is by (56) and the second factor is by Lemma 20, so the product is . Finally,

This completes the proof of Lemma 25 and thus also the proof of Theorem 8.

D.3 Some Additional Lemmas

The next two lemmas are also taken from Shah and Peters (2020), where they appear as Lemma 28 and Lemma 29.

Lemma 26

Let be a collection of distributions and for all , let be a random vector taking values in and let be a bounded sequence of positive numbers. Assume that . Let such that is in the interior of and let be continuously differentiable at with . Then,

Lemma 27

Let , be random matrices such that and the rows of are independent conditional on . Then, for all

for any .

E Proofs of Appendix A

In this section, we give the proofs of the results on the multivariate WGCM.

E.1 Proof of Theorem 11

As for Theorem 8, we prove a slightly more general result corresponding to Theorem 23. For a collection of weight functions , write

For and , define

For , let and be the versions of and based on .

Theorem 28

Let and let and be defined as in (19) and (20). Assume that there exist such that for all and there exists such that either (C1a) and (C2) or (C1b) and (C2) hold. Let such that for all the set is not empty. Assume that

| (57) |

Assume that there exist sequences and as well as positive real numbers , , and possibly depending on such that for all ,

and such that

| (58) | |||

| (59) |

Then,

E.1.1 Proof of Theorem 28

Proof The proof is along the same lines as the proof of Theorem 23 with the complication of having more indices. We therefore just present the parts that require extra care compared to the earlier proof.

Define

We will need to apply the results from Section D.1 to the random vectors

The conditions (B1a)/(B1b) and (B2) are satisfied by (C1a)/(C1b) and (C2) using that

In exactly the same way as in the proof of Theorem 8, the theorem can be reduced to the following lemma:

Lemma 29

Let and let and be defined analogously to the proof of Theorem 23. Then,

-

1.

;

-

2.

;

-

3.

.

The proof of this Lemma is similar to the proof of Lemma 24. Extra care has to be taken in part 1. for the control of , where . For this, one also uses Lemma 27 to write for all

for all . From this, one can proceed as in the proof of Lemma 24. The rest of the proof of Lemma 29 also works as before, with the difference that

With this definition, the equivalent of Lemma 25 is the following:

Lemma 30

The idea of the proof of this lemma is similar to the proof of Lemma 25, but due to the slight difference in the definition of , we redo the proof. For all and and omitting the dependence on from the second line on, we can write

We control the sum over all fifteen terms individually. By symmetry, it is enough to control one term in each line. For the first term, observe that

We have that

| (60) |

by condition (57).

For the second line, we have

We show that the maximum of the sum over the second term is . Let . Then,

Using condition (59), we have

We can conclude using bounded convergence (Lemma 34) that

| (61) |

For the third and the fourth line, we can write

so this can be controlled as the term before. For the fifth line, by Cauchy-Schwarz .

The first factor is by (60). The second factor is by Lemma 20, so the product is .

E.2 Proof of Theorem 14

Proof Theorem 14 follows from Theorem 28 just as Theorem 1 followed from Theorem 17. In the setting of Theorem 28, for and , and , let

Then, we have

For the functions estimated on the auxiliary data set , we know that for all , -almost surely for all , we have . Since is independent of , we have

with . Using iterated expectations, we have

F Limit Theorems

The following three results are taken from Section D.2 in the supplementary material of Shah and Peters (2020). They are versions of the central limit theorem, the weak law of large numbers and Slutsky’s Lemma that hold uniformly over a collection of distributions .

Lemma 31 (Lemma 18 in Shah and Peters (2020))

Let be a family of distributions such that for all the random variable satisfies and . Assume that there exists such that . Let be i.i.d. copies of and define . Then, we have

Lemma 32 (Lemma 19 in Shah and Peters (2020))

Let be a family of distributions. For , let be a random variable with law determined by and for all . Let be i.i.d. copies of and let . Assume that there exists such that . Then, for all

Lemma 33 (Lemma 20 in Shah and Peters (2020))

Let be a family of distributions that determine the law of the random variables and . Assume that

Then, the following holds:

-

1.

If , then

-

2.

If , then

The next lemma is taken from Section D.5 in Shah and Peters (2020).

Lemma 34 (Lemma 25 in Shah and Peters (2020))

Let be a family of distributions that determine the law of the random variables . If and if there exists such that for all we have , then

G Sub-Gaussian and Sub-Exponential Distributions

We summarise some results on sub-Gaussian and sub-exponential distributions, see for example Sections 2.5 and 2.7 in Vershynin (2018).

Definition 35 (Definition 2.5.6 and Proposition 2.5.2 in Vershynin (2018))

A random variable with is called a sub-Gaussian random variable if one of the following equivalent conditions is satisfied. For the parameters , there exists an absolute constant such that for all , property implies property with parameter .

-

1.

There exists such that for all

-

2.

There exists such that

-

3.

There exists such that for all

The sub-Gaussian norm of is defined as

Example 2 (Example 2.5.8 in Vershynin (2018))

A random variable is sub-Gaussian with

where is an absolute constant.

A bounded random variable is sub-Gaussian with

Lemma 36 (Exercise 2.5.10 in Vershynin (2018))

Let be sub-Gaussian random variables and let . Then, there exists an absolute constant such that

Corollary 37

Let be sub-Gaussian random variables and assume that . Then,

Proof For all , by Markov’s inequality

Definition 38 (Definition 2.7.5 and Proposition 2.7.1 in Vershynin (2018))

A random variable is called a sub-exponential random variable if one of the following equivalent conditions is satisfied. For the parameters , there exists an absolute constant such that for all , property implies property with parameter .

-

1.

There exists such that for all

-

2.

There exists such that

-

3.

There exists such that for all

The sub-exponential norm of is defined as

Lemma 39 (Lemma 2.7.7 in Vershynin (2018))

If and are sub-Gaussian random variables, then is a sub-exponential random variable and

References

- Azadkia and Chatterjee (2019) Mona Azadkia and Sourav Chatterjee. A simple measure of conditional dependence. arXiv preprint arXiv:1910.12327. To appear in the Annals of Statistics, 2019.

- Berrett et al. (2020) Thomas B. Berrett, Yi Wang, Rina Foygel Barber, and Richard J. Samworth. The conditional permutation test for independence while controlling for confounders. Journal of the Royal Statistical Society: Series B, 82(1):175–197, 2020.

- Bühlmann and van de Geer (2011) Peter Bühlmann and Sara van de Geer. Statistics for High-Dimensional Data: Methods, Theory and Applications. Springer Series in Statistics. Springer, Berlin Heidelberg, 2011. ISBN 9783642201912. URL https://books.google.ch/books?id=lTvHNAEACAAJ.

- Candès et al. (2018) Emmanuel Candès, Yingying Fan, Lucas Janson, and Jinchi Lv. Panning for gold: Model-X knockoffs for high-dimensional controlled variable selection. Journal of the Royal Statistical Society: Series B, 80(3):551–577, 2018.

- Chen and Guestrin (2016) Tianqi Chen and Carlos Guestrin. Xgboost: A scalable tree boosting system. Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, 2016.

- Chen et al. (2021) Tianqi Chen, Tong He, Michael Benesty, Vadim Khotilovich, Yuan Tang, Hyunsu Cho, Kailong Chen, Rory Mitchell, Ignacio Cano, Tianyi Zhou, Mu Li, Junyuan Xie, Min Lin, Yifeng Geng, and Yutian Li. xgboost: Extreme Gradient Boosting, 2021. URL https://CRAN.R-project.org/package=xgboost. R package version 1.4.1.1.

- Chernozhukov et al. (2013) Victor Chernozhukov, Denis Chetverikov, and Kengo Kato. Gaussian approximations and multiplier bootstrap for maxima of sums of high-dimensional random vectors. The Annals of Statistics, 41(6):2786–2819, 2013.

- Dawid (1979) Alexander Philip Dawid. Conditional independence in statistical theory. Journal of the Royal Statistical Society. Series B, 41(1):1–31, 1979.

- DiCiccio et al. (2020) Cyrus J. DiCiccio, Thomas J. DiCiccio, and Joseph P. Romano. Exact tests via multiple data splitting. Statistics & Probability Letters, 166:108865, 2020.

- Doran et al. (2014) Gary Doran, Krikamol Muandet, Kun Zhang, and Bernhard Schölkopf. A permutation-based kernel conditional independence test. In Proceedings of the Thirtieth Conference on Uncertainty in Artificial Intelligence, pages 132–141, Arlington, Virginia, USA, 2014. AUAI Press.

- Dua and Graff (2017) Dheeru Dua and Casey Graff. UCI machine learning repository, 2017. URL http://archive.ics.uci.edu/ml.

- Fernandes et al. (2015) Kelwin Fernandes, Pedro Vinagre, and Paulo Cortez. A proactive intelligent decision support system for predicting the popularity of online news. In Proceedings of the 17th EPIA 2015 - Portuguese Conference on Artificial Intelligence, September, Coimbra, Portugal, 2015.

- Fukumizu et al. (2008) Kenji Fukumizu, Arthur Gretton, Xiaohai Sun, and Bernhard Schölkopf. Kernel measures of conditional dependence. Advances in Neural Information Processing Systems 20, pages 489–496, 2008.

- Györfi et al. (2002) László Györfi, Michael Kohler, A. Krzyzak, and Harro Walk. A Distribution-Free Theory of Nonparametric Regression. Springer Series in Statistics. Springer, New York, 2002.

- Harrison and Rubinfeld (1978) David Harrison and Daniel L Rubinfeld. Hedonic housing prices and the demand for clean air. Journal of Environmental Economics and Management, 5(1):81–102, 1978.

- Heinze-Deml et al. (2018) Christina Heinze-Deml, Jonas Peters, and Nicolai Meinshausen. Invariant causal prediction for nonlinear models. Journal of Causal Inference, 6(2):20170016, 2018.

- Holm (1979) Sture Holm. A simple sequentially rejective multiple test procedure. Scandinavian Journal of Statistics, 6(2):65–70, 1979.

- Hoyer et al. (2009) Patrik Hoyer, Dominik Janzing, Joris M Mooij, Jonas Peters, and Bernhard Schölkopf. Nonlinear causal discovery with additive noise models. In D. Koller, D. Schuurmans, Y. Bengio, and L. Bottou, editors, Advances in Neural Information Processing Systems, volume 21. Curran Associates, Inc., 2009.

- Huang (2010) Tzee-Ming Huang. Testing conditional independence using maximal nonlinear conditional correlation. The Annals of Statistics, 38(4):2047 – 2091, 2010.

- Josse and Holmes (2016) Julie Josse and Susan Holmes. Measuring multivariate association and beyond. Statistics Surveys, 10:132 – 167, 2016.

- Li and Fan (2020) Chun Li and Xiaodan Fan. On nonparametric conditional independence tests for continuous variables. WIREs Computational Statistics, 12(3):e1489, 2020.