Portfolio analysis with mean-CVaR and mean-CVaR-skewness criteria based on mean–variance mixture models

Abstract

The paper Zhao et al. (2015) shows that mean-CVaR-skewness portfolio optimization problems based on asymetric Laplace (AL) distributions can be transformed into quadratic optimization problems for which closed form solutions can be found. In this note, we show that such a result also holds for mean-risk-skewness portfolio optimization problems when the underlying distribution belongs to a larger class of normal mean–variance mixture (NMVM) models than the class of AL distributions. We then study the value at risk (VaR) and conditional value at risk (CVaR) risk measures of portfolios of returns with NMVM distributions. They have closed form expressions for portfolios of normal and more generally elliptically distributed returns, as discussed in Rockafellar & Uryasev (2000) and in Landsman & Valdez (2003). When the returns have general NMVM distributions, these risk measures do not give closed form expressions. In this note, we give approximate closed form expressions for the VaR and CVaR of portfolios of returns with NMVM distributions. Numerical tests show that our closed form formulas give accurate values for VaR and CVaR and shorten the computational time for portfolio optimization problems associated with VaR and CVaR considerably.

Keywords: Portfolio selection Normal mean–variance mixtures Risk measure Mean-risk-skewness EM algorithm

1 Introduction

Numerous empirical studies of asset returns suggest that their distributions deviate from the normal distribution, see Cont & Tankov (2004) and Schoutens (2003). In fact, it has been demonstrated in many papers that asset returns have fat tails and skewness, see Rachev et al. (2005) and Campbell, Lo & MacKinlay (1997) for example. The leptekortic features of empirical asset return data suggest that there are more realistic models than the normal distribution. It has been empirically demonstrated in numerous papers that the multivariate Generalized Hyperbolic (mGH) distributions and their sub-classes can describe multivariate financial data returns very well , see McNeil et al. (2015) and the references therein. The class of mGH distributions is a subclass of general normal mean–variance mixture (NMVM) models.

A return vector (here and from now on denotes transpose) of assets follows an NMVM distribution if

| (1) |

where is an dimensional standard normal random variable (here is the -dimensional identity matrix), is a non-negative scalar-valued random variable which is independent of , is a matrix, and are constant vectors which describe the location and skewness of respectively.

In general, in (1) can be any non-negative valued random variable. But if follows a Generalized Inverse Gaussian (GIG) distribution, the distribution of is called an mGH distribution, see McNeil et al. (2015) and Prause et al. (1999) for the delails of the GH distributions. When is an exponential random variable with parameter , follows an assymetric Laplace (AL) distribution, see Mittnik & Rachev (1993), Kozubowski & Rachev (1994), and Kozubowski & Podgórski (2001) for the definition and financial applications of AL distributions.

A GIG distribution has three parameters and and its density is given by

| (2) |

where is the modified Bessel function of the third kind with index for . The parameters in (2) satisfy and if and if and and if . The expected value of is given by

| (3) |

With in (1), the density function of has the following form

| (4) |

where denotes the Mahalanobis distance.

The GH distribution contains several special cases that are used frequently in financial modelling. For example, the case corresponds to a multivariate hyperbolic distribution, see Eberlein & Keller (1995) and Bingham & Kiesel (2001) for applications of this case in financial modelling. When , the distribution of is called a Normal Inverse Gaussian (NIG) distribution and Barndorff-Nielsen (1997) proposes NIG as a good model for finance. If and , the distribution of is a Variance Gamma (VG) distribution, see Madan & Seneta (1990) for the details of this case. If and , the distribution of is called the generalized hyperbolic Student distribution and Aas & Haff (2006) shows that this distribution matches the empirical data very well.

The mean-risk portfolio optimization problems based on NMVM models were discussed in the recent paper Shi & Kim (2021). They provided a method that transforms a high dimensional problem into a two-dimensional problem in their proposition 3.1. This enabled them to solve portfolio optimization problems associated with NMVM distributed returns more efficiently. When the returns have Gaussian distributions or more generally elliptical distributions, the VaR and CVaR risk measures have closed form expressions for portfolios of such returns, as shown in Owen & Rabinovitch (1983) and Landsman & Valdez (2003). For returns with more general NMVM distributions, these risk measures do not give closed form formulas. One of the goals of this paper is to provide approximate closed form formulas for risk measures for portfolios of NMVM distributed returns.

Remark 1.1.

We remark here that the NMVM models, which are more general than the mGH models, allow for models obtained by the multiple subordination techniques applied in Shirvani et al. (2021a) and Shirvani et al. (2021a) for example. The distributional class of mGHs has a specific structure of the subordinators and thus fixes the shape of the distributional tail behavior. NMVM includes the class of all distributions representing the unit increment of multivariate subordinated Lévy processes, see Shirvani et al. (2021b) for example. The number of subordinations changes the behavior of the tails of the distribution and can be used as a model parameter. In particular, the class of NMVM models includes multiple subordinated mGH. For example, if the first subordination determines the heavy tailedness and the skewness of the stock returns, the second subordination can be used to track transaction volume, and the third the ESG score of the company issuing the stock. As shown in Shirvani et al. (2021a) and Shirvani et al. (2021b), one subordination is not necessarily sufficient in financial modeling. These facts necessitate the need for the discussion of the general class of NMVM models.

Measuring the risk of a financial position is a complex process. It is standard to assess the riskiness of a financial position by means of convex risk measures, see Frittelli & Gianin (2002), Föllmer & Schied (2002), Artzner et al. (1999). A convex risk measure is a convex function which is

-

(a)

Monotone: if almost surely.

-

(b)

Cash-invariant: for all .

Here denotes the class of random variables with finite moments (here, ). A convex risk measure satisfies the convexity property . A convex risk measure is called coherent if it satisfies the positive homogeneity property for any . The quantity can be viewed as the minimal capital that has to be added to the financial position to make it acceptable. A risk measure with the above two properties (a) and (b) is called a monetary risk measure, see Föllmer & Schied (2002). Monetary risk measures are also defined through an associated acceptable set. A subset of is called acceptable if and implies . A risk measure associated with an acceptable set is defined to be the minimum capital that has to be added to to make it acceptable, i.e.,

| (5) |

A risk measure can also be defined by (5) for a given acceptable set . For any risk measure , its associated acceptance set is given by . The risk measure can be recovered from as in (5). The concept of coherent risk measures was first introduced in the seminal paper Artzner et al. (1999), also see Malevergne & Sornette (2006). Convex risk measures were introduced and studied in Frittelli & Gianin (2002), Heath (2000), and Föllmer & Schied (2002).

A monetary risk measure is law invariant if whenever and are equal in distribution. The value at risk (VaR) is a law invariant monetary risk measure. For any , the value at risk at significance level is denoted by and its acceptance set is given by

The VaR is given by

| (6) |

where is the upper -quantile of . As pointed out in Artzner et al. (1999), the VaR lacks the subadditivity property. In particular, VaR is a non-convex function and portfolio optimization problems with it lead to multiple local extremes. Therefore portfolio optimization with VaR is computationally expensive.

Recently, the risk measure CVaR has become popular both in academia and in finance. The CVaR is a coherent risk measure (see, e.g., Acerbi & Tasche (2002)) and therefore has some favorable properties that VaR lacks. The conditional value at risk (average value at risk, tail value at risk, or expected shortfall) is defined for any as follows

Since is decreasing in , we clearly have . In fact, CVaR is the smallest coherent risk measure which is law invariant and dominates the VaR.

It is well known that a convex measure is law invariant if and only if

| (7) |

where

| (8) |

and is the space of probability measures on . A coherent risk measure is law invariant if and only if

| (9) |

for a subset of . For the details of these results see Kusuoka (2001), Dana (2005), and Frittelli & Gianin (2005).

Remark 1.2.

We remark here that the relations (7), (8), and (9) above show that any law invariant convex risk measure can be expressed in terms of CVaR. In Section 3 of this paper, we will discuss approximate closed form formulas for CVaR for portfolios of NMVM distributed returns. One can then use these formulas in place of CVaR in (7), (8), and (9) above and construct simpler expressions for any law invariant convex risk measure.

This paper is organized as follows. In Section 2, we study a mean-risk-skewness multi-objective optimization problem and provide closed form solutions for optimal portfolios when the return vectors follow a certain class of NMVM models. In Section 3, we give approximate closed form expressions for the risks of the portfolios of NMVM returns when the risk measures are coherent ones. In Section 4, we present the results of numerical tests of our results.

2 Closed form solutions for mean-risk-skewness optimal portfolios

As mentioned in the Abstract, Zhao et al. (2015) studies mean-CVaR-skewness optimization problems for AL distributions. The class of AL distributions considered in their paper have the mean–variance mixture form

| (10) |

for two real numbers and , where , and it is independent of the standard normal random variable . The characteristic function of is given by the formula (1) in their paper with replaced by . In this section and for the rest of the paper, we use “” to denote the equivalence in distribution of two random variables. “Skew” denotes the skewness of a random variable and “Kurt” denotes the kurtoses of a random variable.

In the multi-dimensional case, the AL distributions they have considered have the form , where now and is an matrix and is a dimensional standard normal random variable. For any portfolio , they calculated and as

| (11) |

where and are given as in (9), (11), and in (16) in their paper respectively. Note that here represents in their paper.

In their paper, they considered the mean-CVaR-skewness multi-objective problem

| (12) |

for any return . This problem can be written under general law invariant risk measure as follows:

| (13) |

Remark 2.1.

We remark here that the problem (13) is a multi-objective problem, i.e., optimize both and simultaneously under the constraints In comparison, the relevant paper Akturk & Ararat (2020) discusses a static portfolio optimization problem also and their optimization problem is a single-objective problem.

Remark 2.2.

Such mean-risk-skewness portfolio optimization problem as in (13) have been studied in many papers in the past, see Konno & Suzuki (1995), Zhao et al. (2015), and the references therein, for example. This is because, as stated in the introduction of Konno & Suzuki (1995), many investors prefer a positively skewed distributions to a negative one and also larger skewed distributions compared to smaller skewed distributions if the mean and the risk are the same.

In their paper, they observe that CVaR, as was shown in the proof of their Theorem 2, is an increasing function of and Skew is a decreasing function of . They concluded, therefore, that minimizing gives the same solution as (12) above and also it translates into the quadratic optimization problem (17) in their paper.

In this paper, we take a different approach than Zhao et al. (2015) for the solution of the problem (12) above and obtain similar results for when is more general than and also when CVaR is replaced by a general law-invariant risk measure as in (13).

We first fix some notation. We denote by the column vectors of . We assume that is an invertable matrix. We write as linear combinations of , i.e., . We denote by the vector of the corresponding coefficients of such linear combination. As usual, we denote by the Euclidean norm of the vector . Also, for each NMVM distribution as above, we define

| (14) |

and we call the NMVM distribution associated with .

For any portfolio we define a transformation by , where is given by

| (15) |

In matrix form, this is written as . From now on, for any domain of portfolios , we denote by the image of under .

We start our discussions with the following simple lemma. In the following lemma, denotes a standard normal random variable that independent of the mixing distribution .

Lemma 2.3.

We have and . Therefore we have for any law invariant coherent risk measure whenever and are related by (15). Here is the cosine of the angle between and .

Proof.

Note that . We have and . Therefore . Since and is a law invariant risk measure, we have . Since and is positive homogeneous, we have . ∎

The above lemma shows that optimization problems under mean-risk-skewness criteria can be studied in the -coordinate system rather than the original -coordinate system. This has some advantage as will be seen shortly.

Below, we write the problem (13) in the -coordinate system as follows

| (16) |

where and .

Next, we will show that the problem (16) can be reduced to a quadratic optimization problem when satisfies certain conditions which are satisfied by AL distributions. We first need to calculate .

Proposition 2.4.

For any , we have

| (17) |

where , , and .

Proof.

Remark 2.5.

From Proposition 2.4, we observe that StD depends on through both and . However, both SKew and Kurt depend on only through the angle .

We need to calculate the derivative of with respect to . A straightforward calculation gives us

| (18) |

Remark 2.6.

Now we state the main result of this paper.

Theorem 2.7.

Proof.

From Lemma (2.3) above we have . Since from the constraint (20) we have . We conclude that is a function of under the constraint (20). From part (3) of Theorem 3.1 of Shi & Kim (2021) we conclude that is a non-decreasing function of . On the other hand, the condition on Skew ensures that SKew is an increasing function of . With the constraint , becomes a decreasing function of . Therefore decreasing minimizes and maximizes Skew simultaneously. To show (59), we form the Lagrangian . The first order condition gives

| (22) |

From this we get and since and , we obtain two equations and . The solution of these two equations give (21). ∎

For the remainder of this section, we give examples of the mixing distributions that satisfy condition (19).

Example 2.8.

We consider the case of gamma distributions with the density function

In this case we have and . We obtain

Thus, in this case satisfies the condition (19). Note that is an random variable and therefore also satisfies the condition (19). Thus for asymmetric Laplace distributions the problem (16) can be reduced to a quadratic optimization problem (20). This also shows that our Theorem 2.7 above extends Theorem 2 in Zhao et al. (2015) to the case of more general mean–variance mixture models.

Example 2.9.

Remark 2.10.

We should mention that in the above examples we only gave two classes of random variables that satisfy (19). However, the class of random variables that satisfy (19) is not restricted to these two types of random variables. One can check that the class of generalized inverse Gaussian random variables GIG also satisfies (19) for certain parameter values.

3 Portfolio optimization under mean-risk criteria

3.1 Recent results

The mean–variance portfolio theory was first introduced by Markowitz (1959) and since then it has been very popular for practitioners and scholars. However, the Markowitz portfolio theory neglects downside risk. It has been shown in many papers that downside risk can affect returns significantly, see Bollerslev & Todorov (2011) and Bali & Cakici (2004) for example. Because of this, many alternative risk measures have been the focus of academic research, see Chekhlov et al. (2005), Konno et al. (1993). Among downside risk measures, the VaR and CVaR have been extensively studied, see Rockafellar & Uryasev (2000) and Kolm et al. (2014).

The risk measure CVaR was first studied in the context of portfolio optimization problems by Rockafellar & Uryasev (2000, 2002). They showed that a mean-CVaR optimization problem can be transformed into a linear programming problem that improves the efficiency of solving portfolio optimization problems associated with CVaR significantly. However, closed form approximate formulas are still more convenient and efficient and therefore we will discuss such formulas for them below.

For elliptical distributions, the VaR and CVaR have closed form expressions, as studied in Landsman & Valdez (2003). For the general class of NMVM models, these risk measures do not give closed form expressions. In this section, we will present approximate closed form formulas for them. Below, we start by discussing the properties of portfolios of NMVM distributed returns.

Let denote the return of assets and assume that has the NMVM distribution

| (23) |

where is a constant vector and the other symbols are as in the multi-dimensional case in (10) above. For any portfolio , we have

| (24) |

where is a standard normal random variable and . We will denote the density and distribution functions of the scalar valued random variables by and respectively for each portfolio . Then, according to formula of Hellmich & Kassberger (2011), the conditional value at risk of is given by

| (25) |

where the quantile-function is calculated by a root-finding method and the integral in (25) is calculated by numerical integration. Therefore, optimization problems like

| (26) |

in some domain of the set of portfolios are time consuming and computationally heavy. Another approach to solving the problem (26) was proposed in Rockafellar & Uryasev (2000, 2002). They introduced an auxiliary function

| (27) |

where is a real number and is the -dimensional probability density function of asset returns. They showed that

| (28) |

Since follows , the above can also be written as

| (29) |

With these, the optimization problem (26) becomes

| (30) |

Solving the problem (30) is also time consuming as one needs to calculate (29) numerically for each , and then for each the right-hand side of (30) needs to be minimized for .

The recent paper by Shi & Kim (2021) studies portfolio optimization problems with NMVM distributed returns. More specifically, they studied the optimization problem

| (31) |

for any coherent risk measure , where is a subset of the feasible portfolio set, , and is an -dimensional column vector in which each component equals one. They showed that the optimal solution to (31) can be expressed as

| (32) |

where

| (33) |

with

| (34) |

and

| (35) |

While this approach gives an expression for the optimal portfolio as in (32), one still needs to solve another optimization problem, namely (33).

In the following, we will show that (32) and (33) can be simplified further. We first fix some notation. Similar to the case of in Section 2, we write as a linear combination of as . We denote by the column vector formed by the corresponding coefficients of this linear combination. Also, for each NMVM distribution as in (23), we define

| (36) |

and we call the NMVM distribution associated with . In the -coordinate system, problem (31) can be written as

| (37) |

where and now .

The solution of (37) can be characterized by using the same idea as in Proposition 3.1 of Shi & Kim (2021). Below, we write down the optimal solution of (37) as a corollary of their result.

Corollary 3.1.

For any law invariant coherent risk measure , the solution of (37) is given by

| (38) |

where

| (39) |

with

| (40) |

and

| (41) |

Proof.

The proof follows from the same argument as in the proof of Proposition 3.1 of Shi & Kim (2021). In our case here, we have , and with this, their formula reduces to the solution in the corollary. ∎

3.2 Closed form approximations for risks

The result (32) reduces the high dimensional nature of the portfolio optimization problem (31) to two dimensions, as claimed in Shi & Kim (2021). In particular, this approach reduces the computational time of determining the optimal portfolio significantly, as claimed in their paper. In this section, we take an alternative approach and attempt to reduce the computational time of such optimization problems also. For this, we linearly transform the portfolio space into a different coordinate system.

The following simple lemma shows that to determine the optimal portfolio, one only needs to solve a low-dimensional optimization problem in, as explained in Remark 3.3 below.

Lemma 3.2.

For any coherent risk measure , we have

| (42) |

where

and is the angle between and .

Proof.

We have . Since is law invariant and cash invariant, we have . Now, since and is positive homogeneous, (42) follows. ∎

Remark 3.3.

Lemma (42) shows that the risk is dependent on . From now on we write

| (43) |

In the following lemma, we state some properties of .

Lemma 3.4.

For any coherent risk measure , the function is a decreasing, convex, and continuous function of in .

Proof.

The decreasing property of follows from Theorem 3.1 of Shi & Kim (2021). Here, for the sake of being self-contained, we present its proof. Take two . Then the subadditivity and monotonicity of implies

| (44) |

The convexity of follows from

| (45) |

for any . Since is a convex function, it is continuous in the interior of its domain, which is . ∎

Remark 3.5.

Remark 3.6.

We remark that in order to obtain high precision, the points need to be chosen to make as small as possible. However, this comes with a cost, as we need to calculate for each to obtain an approximate value of .

This proposition gives an accurate approximation for the value of the risk measure when the mesh of the corresponding partition is very small. However, as stated earlier, we need to calculate for many .

When the value of is relatively small, we can get an even simpler approximation, as stated in the following proposition. The next proposition gives an approximation for the risk measure in which one needs to calculate for only two values of to obtain a good approximation. In the following, we use the following notation .

Proposition 3.7.

Any law invariant coherent risk measure can be approximated by

| (47) |

where is the angle between and .

Proof.

Remark 3.8.

The precision of the approximation (47) clearly depends on the properties of the risk measure . More specifically, the properties of in (43) determine the degree of accuracy of our approximation. The only information on that we know is its continuity, convexity, and the decreasing property as stated in Lemma 3.4. These are not sufficient to study the accuracy of the approximation for this proposition. However, our extensive numerical tests show that when is relatively small, which is usually the case for EM estimates of the NMVM models from empirical data, these approximations work pretty well.

The above proposition simplifies the computations of optimal portfolios considerably, as one only needs to evaluate at the two points and .

Remark 3.9.

Remark 3.10.

We remark that in optimization problems like , one can optimize instead and obtain an approximately optimal portfolio. Observe that can also be written as

| (49) |

Here, is a positive number, as is a decreasing function, as stated in Lemma 2.8. The minimization and maximization of functions of the form (49) were discussed in Landsman (2008) in detail, see also Owadally (2011) and Landsman & Makov (2016).

Remark 3.11.

As mentioned earlier, calculating the VaR and CVaR needs numerical procedures or Monte Carlo approaches for most models of asset returns. In the past, calculations of the VaR relied on linear approximations of the portfolio risks, see, e.g., Duffie & Pan (1997) and Jorion (1996)), or Monte Carlo simulation-based tools, see, e.g., Uryasev (2000), Bucay & Rosen (1999), and Pritsker (1997). Next, we present closed form approximations for them, as a corollary to Proposition 3.7.

Acerbi and Tasche (2010) defines to be the negative of the upper quantile

of , i.e., . When the random variable has a positive probability density function, we have and so . With this definition, VaR is a positive homogeneous monetary risk measure. The conditional value at risk is defined by . Then, for any portfolio , the CVaR of the loss and return are given by

| (50) |

respectively. When , a straightforward calculation shows that these risk measures have the closed form expressions

| (51) |

where is the cumulative distribution function of the standard normal random variable. When is elliptically distributed, one can also express these risk measures in closed form, as in equation (2) of Landsman and Valdez (2000).

Below, we discuss this risk measure for the class of random variables as this is sufficient to obtain expressions for these risk measures for general NMVM models, due to (42).

Denoting the probability density function of by , the probability density function of is given by

| (52) |

If , then has the following density function

| (53) |

where is the modified Bessel function of the third kind. Write and note that is the quantile of . By using the definitions of VaR and CVaR, we obtain the following relations:

Lemma 3.12.

We have

| (54) |

and

| (55) |

where is the cumulative distribution function of the standard normal random variable.

Proof.

Now, if we apply (42) to the risk measures VaR and CVaR, we obtain

| (56) |

and

| (57) |

where , , and satisfies (54). Therefore, optimization problems like or for some domain of portfolios involve computing (54) or (55) for each .

Below, we apply Proposition 2.8 and obtain simpler expressions for the VaR and CVaR.

Theorem 3.13.

The and can be approximated by the following and respectively

| (58) |

and

| (59) |

where and the constants are given by

| (60) |

where and with .

Proof.

The proof follows from Proposition (47). ∎

4 Numerical results

In this section, we numerically check the performance of our results. First, we fit the GH distribution to empirical data of five stocks by using the EM algorithm. For this, we use five years of price history of the stocks AMD, CZR, ENPH, NVDA, and TSLA from the 2nd of January 2015 to the 30th of December 2020. The following table gives a summary of this data

| Name | AMD | CZR | ENPH | NVDAC | TSLA |

|---|---|---|---|---|---|

| mean | 0.003121 | 0.002738 | 0.003218 | 0.002568 | 0.002432 |

| std | 0.040087 | 0.04008 | 0.056228 | 0.028707 | 0.034737 |

| min | -0.242291 | -0.37505 | -0.373656 | -0.187559 | -0.210628 |

| max | 0.522901 | 0.441571 | 0.424446 | 0.298067 | 0.198949 |

We apply the modified EM scheme to fit the daily log-returns of these stocks to 5-dimensional GH distributions. The algorithm is called multi-cycle, expectation, conditional estimation (MCECM) procedure, see McNeil et al. (2015) Meng & Rubin (1993) for the details of this algorithm. First, we fit the return data to the model . In this case, the estimated parameters for are

and

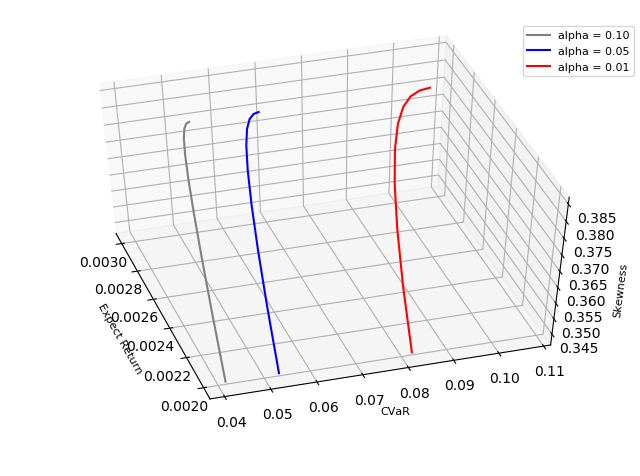

With these parameters, we have . We also have . As in Zhao et al. (2015), we consider returns . We take . For each , we calculate from , where and are given by (59). Then for each , we calculate from (17), from (50) and we plot in three-dimensional space. Table 2 gives a summary of the optimal portfolios and the corresponding skewness. Figure 1 is the mean-CVaR-skewness efficient frontier.

| Expect Return | 0.0020 | 0.0022 | 0.0024 | 0.0027 | 0.0029 |

|---|---|---|---|---|---|

| 0.077077 | 0.194069 | 0.31106 | 0.428051 | 0.545042 | |

| 0.252863 | 0.22433 | 0.195798 | 0.167265 | 0.138732 | |

| 0.067729 | 0.101723 | 0.135716 | 0.169709 | 0.203703 | |

| 0.399764 | 0.26734 | 0.134915 | 0.00249 | -0.12994 | |

| 0.202566 | 0.212539 | 0.222512 | 0.232485 | 0.242458 | |

| Skewness | 0.34231 | 0.370487 | 0.383957 | 0.385706 | 0.380047 |

In the second case, we fit the return data of the above listed five stocks to the model

The following table lists the numerical values for the parameters of our fit.

The values of and are as follows.

By using the definitions of and , we calculate them as follows.

Table 3 tests the performance of our Theorem 3.12. The value of the VaR is calculated by a numerical root finding method and also by using Theorem 3.12. It can be seen that the results match very well.

| Portfolio Weights | VaR | V | ||||

|---|---|---|---|---|---|---|

| = 0.1 | = 0.05 | = 0.01 | = 0.1 | = 0.05 | = 0.01 | |

| [0.1, 0.4, 0.2, 0.1, 0.2] | 0.027729 | 0.042165 | 0.082055 | 0.029828 | 0.044277 | 0.084206 |

| [0.2, 0.1, 0.5, 0.1, 0.1] | 0.038508 | 0.058196 | 0.112613 | 0.040006 | 0.059714 | 0.114193 |

| [0.1, 0.4, 0.1, 0.3, 0.1] | 0.02568 | 0.039183 | 0.076513 | 0.02816 | 0.041678 | 0.079054 |

| [0.3, 0.1, 0.3, 0.1, 0.2] | 0.03131 | 0.047384 | 0.091771 | 0.032775 | 0.048857 | 0.093264 |

| [0.1, 0.3, 0.1, 0.3, 0.2] | 0.025091 | 0.038256 | 0.074639 | 0.027397 | 0.040574 | 0.076994 |

In Table 4 we compare the numerical calculation of the CVaR with the performance of the approximation of the CVaR in Theorem 3.12. Again, it can be seen that the results match very well.

| Portfolio Weights | CVaR | CV | ||||

|---|---|---|---|---|---|---|

| = 0.1 | = 0.05 | = 0.01 | = 0.1 | = 0.05 | = 0.01 | |

| [0.1, 0.4, 0.2, 0.1, 0.2] | 0.050643 | 0.067315 | 0.111296 | 0.050654 | 0.067341 | 0.111366 |

| [0.2, 0.1, 0.5, 0.1, 0.1] | 0.069764 | 0.092505 | 0.152508 | 0.0698 | 0.092567 | 0.15264 |

| [0.1, 0.4, 0.1, 0.3, 0.1] | 0.04712 | 0.062719 | 0.103883 | 0.047136 | 0.062755 | 0.103972 |

| [0.3, 0.1, 0.3, 0.1, 0.2] | 0.056816 | 0.075369 | 0.124296 | 0.056815 | 0.075376 | 0.124327 |

| [0.1, 0.3, 0.1, 0.3, 0.2] | 0.04599 | 0.061195 | 0.10131 | 0.046 | 0.06122 | 0.101378 |

5 Conclusion

Zhao et al. (2015) showed that mean-CVaR-skewness portfolio optimization problems based on asymmetric Laplace distributions can be transformed into quadratic optimization problems. In this note, we extended their result and showed that mean-risk-skewness portfolio optimization problems based on a larger class of NMVM models can also be transformed into quadratic optimization problems under any law invariant risk measure. The critical step to achieve this was to transform the original portfolio space into another space by an appropriate linear transformation, a step which enabled us to express both the risk and skewness as functions of a single variable. By showing that any law invariant coherent risk measure is an increasing function and skewess is a decreasing function of this variable, we were able to transform the original optimization problem into a quadratic optimization problem as in Zhao et al. (2015). In the rest of this paper, we made use of this transformation to come up with approximate closed form formulas for law invariant risk measures and hence also for the VaR and CVaR. Our numerical tests show that such closed form approximations are accurate.

References

- Aas & Haff (2006) Aas, K. & Haff, I. H. (2006). The generalized hyperbolic skew Student’s -distribution. Journal of Financial Econometrics, 4, 275–309

- Acerbi & Tasche (2002) Acerbi, C. & Tasche, D. (2002). On the coherence of expected shortfall. Journal of Banking & Finance, 26, 1487–1503

- Akturk & Ararat (2020) Akturk, T. D. & Ararat, C. (2020). Portfolio optimization with two coherent risk measures. Journal of Global Optimization, 597–626

- Artzner et al. (1999) Artzner, P., Delbaen, F., Eber, J. M., & Heath, D. (1999). Coherent measures of risk. Mathematical Finance, 9, 203–228

- Bali & Cakici (2004) Bali, T. G. & Cakici, N. (2004). Value at risk and expected stock returns. Financial Analysts Journal, 60, 57–73

- Barndorff-Nielsen (1997) Barndorff-Nielsen, O. E. (1997). Processes of normal inverse Gaussian type. Finance and Stochastics, 2, 41–68

- Bingham & Kiesel (2001) Bingham, N. H. & Kiesel, R. (2001). Modelling asset returns with hyperbolic distributions. Return Distributions in Finance, 1–20. Elsevier

- Bollerslev & Todorov (2011) Bollerslev, T. & Todorov, V. (2011). Tails, fears, and risk premia. The Journal of Finance, 66, 2165–2211

- Bucay & Rosen (1999) Bucay, N. & Rosen, D. (1999). Credit risk of an international bond portfolio: A case study. ALGO Research Quarterly, 2, 9–29

- Chekhlov et al. (2005) Chekhlov, A., Uryasev, S., & Zabarankin, M. (2005). Drawdown measure in portfolio optimization. International Journal of Theoretical and Applied Finance, 8, 13–58

- Cont & Tankov (2004) Cont, R. & Tankov, P. (2004). Nonparametric calibration of jump-diffusion option pricing models. The Journal of Computational Finance, 7, 1–49

- Dana (2005) Dana, R. A. (2005). A representation result for concave Schur concave functions. Mathematical Finance: An International Journal of Mathematics, Statistics and Financial Economics, 15, 613–634

- Duffie & Pan (1997) Duffie, D. & Pan, J. (1997). An overview of value at risk. Journal of Derivatives, 4, 7–49

- Eberlein & Keller (1995) Eberlein, E. & Keller, U. (1995). Hyperbolic distributions in finance. Bernoulli, 281–299

- Föllmer & Schied (2002) Föllmer, H. & Schied, A. (2002). Convex measures of risk and trading constraints. Finance and Stochastics, 6, 429–447

- Frittelli & Gianin (2002) Frittelli, M. & Gianin, E. R. (2002). Putting order in risk measures. Journal of Banking & Finance, 26, 1473–1486

- Frittelli & Gianin (2005) Frittelli, M. & Gianin, E. R. (2005). Law invariant convex risk measures. Advances in Mathematical Economics, 33–46. Springer

- Hammerstein (2010) Hammerstein, E. (2010). Generalized hyperbolic distributions: Theory and applications to CDO pricing. Ph.D. thesis

- Heath (2000) Heath, D. (2000). Back to the future. Plenary lecture. First World Congress of the Bachelier Finance Society, Paris

- Hellmich & Kassberger (2011) Hellmich, M. & Kassberger, S. (2011). Efficient and robust portfolio optimization in the multivariate generalized hyperbolic framework. Quantitative Finance, 11, 1503–1516

- Jorion (1996) Jorion, P. (1996). Risk2: Measuring the risk in value at risk. Financial Analysts Journal, 52, 47–56

- Kolm et al. (2014) Kolm, P. N., Tütüncü, R., & Fabozzi, F. J. (2014). 60 years of portfolio optimization: Practical challenges and current trends. European Journal of Operational Research, 234, 356–371

- Konno et al. (1993) Konno, H., Shirakawa, H., & Yamazaki, H. (1993). A mean-absolute deviation-skewness portfolio optimization model. Annals of Operations Research, 45, 205–220

- Konno & Suzuki (1995) Konno, H. & Suzuki, K. (1995). A mean–variance-skewness portfolio optimization model. Journal of the Operation Research Society of Japan, 38

- Kozubowski & Podgórski (2001) Kozubowski, T. J. & Podgórski, K. (2001). Asymmetric Laplace laws and modeling financial data. Mathematical and Computer Modelling, 34, 1003–1021

- Kozubowski & Rachev (1994) Kozubowski, T. J. & Rachev, S. T. (1994). The theory of geometric stable distributions and its use in modeling financial data. European Journal of Operational Research, 74, 310–324

- Kusuoka (2001) Kusuoka, S. (2001). On law invariant coherent risk measures. Advances in Mathematical Economics, 83–95. Springer

- Landsman (2008) Landsman, Z. (2008). Minimization of the root of a quadratic functional under a system of affine equality constraints with application to portfolio management. Journal of Computational and Applied Mathematics, 220, 739–748

- Landsman & Makov (2016) Landsman, Z. & Makov, U. (2016). Minimization of a function of a quadratic functional with application to optimal portfolio selection. Journal of Optimization Theory and Applications, 308–322

- Landsman & Valdez (2003) Landsman, Z. M. & Valdez, E. A. (2003). Tail conditional expectations for elliptical distributions. North American Actuarial Journal, 7, 55–71

- Lo & MacKinlay (1997) Lo, A. W. & MacKinlay, A. C. (1997). Maximizing predictability in the stock and bond markets. Macroeconomic Dynamics, 1, 102–134

- Madan & Seneta (1990) Madan, D. B. & Seneta, E. (1990). The variance gamma (VG) model for share market returns. Journal of Business, 511–524

- Malevergne & Sornette (2006) Malevergne, Y. & Sornette, D. (2006). Extreme financial risks: From dependence to risk management. Springer-Verlag

- Markowitz (1959) Markowitz, H. M. (1959). Portfolio Selection: Efficient Diversification of Investments, volume 16

- McNeil et al. (2015) McNeil, A. J., Frey, R., & Embrechts, P. (2015). Quantitative Risk Management: Concepts, Techniques and Tools–Revised Edition. Princeton University Press

- Meng & Rubin (1993) Meng, X. L. & Rubin, D. B. (1993). Maximum likelihood estimation via the ECM algorithm: A general framework. Biometrika, 80, 267–278

- Mittnik & Rachev (1993) Mittnik, S. & Rachev, S. T. (1993). Modeling asset returns with alternative stable distributions. Econometric Reviews, 12, 261–330

- Owadally (2011) Owadally, I. (2011). An improved closed-form solution for the constrained minimization of the root of a quadratic functional. Journal of Computational and Applied Mathematics, 4428–4435

- Owen & Rabinovitch (1983) Owen, J. & Rabinovitch, R. (1983). On the class of elliptical distributions and their applications to the theory of portfolio choice. The Journal of Finance, 38, 745–752

- Prause et al. (1999) Prause, K. et al. (1999). The generalized hyperbolic model: Estimation, financial derivatives, and risk measures. Ph.D. thesis

- Pritsker (1997) Pritsker, M. (1997). Evaluating value at risk methodologies: Accuracy versus computational time. Journal of Financial Services Research, 12, 201–242

- Rachev et al. (2005) Rachev, S. T., Stoyanov, S. V., Biglova, A., & Fabozzi, F. J. (2005). An empirical examination of daily stock return distributions for US stocks. Data Analysis and Decision Support, 269–281. Springer

- Rockafellar & Uryasev (2000) Rockafellar, R. T. & Uryasev, S. (2000). Optimization of conditional value-at-risk. Journal of risk, 2, 21–42

- Rockafellar & Uryasev (2002) Rockafellar, R. T. & Uryasev, S. (2002). Conditional value-at-risk for general loss distributions. Journal of Banking & Finance, 26, 1443–1471

- Schoutens (2003) Schoutens, W. (2003). Lévy processes in finance: Pricing financial derivatives. Wiley Online Library

- Shi & Kim (2021) Shi, X. & Kim, Y. S. (2021). Coherent risk measures and normal mixture distributions with applications in portfolio optimization. International Journal of Theoretical and Applied Finance (IJTAF), 24, 1–18

- Shirvani et al. (2021a) Shirvani, A., Rachev, T. S., & Fabozzi, F. J. (2021a). Multiple subordinated modeling of asset returns: Implications for option pricing. Rev Quant Finan Acc, 156, 1329–1342

- Shirvani et al. (2021b) Shirvani, A., Stoyanov, S., & Fabozzi, F. e. a. (2021b). Equity premium puzzle or faulty economic modelling? Rev Quant Finan Acc, 156, 1329–1342

- Uryasev (2000) Uryasev, S. (2000). Conditional value-at-risk: Optimization algorithms and applications. Proceedings of the IEEE/IAFE/INFORMS 2000 Conference on Computational Intelligence for Financial Engineering (CIFEr) (Cat. No. 00TH8520), 49–57. IEEE

- Zhao et al. (2015) Zhao, S., Lu, Q., Han, L., Liu, Y., & Hu, F. (2015). A mean-CVaR-skewness portfolio optimization model based on asymmetric Laplace distribution. Annals of Operations Research, 226, 727–739