Risk-averse Heteroscedastic Bayesian Optimization

Abstract

Many black-box optimization tasks arising in high-stakes applications require risk-averse decisions. The standard Bayesian optimization (BO) paradigm, however, optimizes the expected value only. We generalize BO to trade mean and input-dependent variance of the objective, both of which we assume to be unknown a priori. In particular, we propose a novel risk-averse heteroscedastic Bayesian optimization algorithm (RAHBO) that aims to identify a solution with high return and low noise variance, while learning the noise distribution on the fly. To this end, we model both expectation and variance as (unknown) RKHS functions, and propose a novel risk-aware acquisition function. We bound the regret for our approach and provide a robust rule to report the final decision point for applications where only a single solution must be identified. We demonstrate the effectiveness of RAHBO on synthetic benchmark functions and hyperparameter tuning tasks.

1 Introduction

Black-box optimization tasks arise frequently in high-stakes applications such as drug and material discovery [22, 17, 28], genetics [16, 27], robotics [5, 12, 25], hyperparameter tuning of complex learning systems [21, 13, 34], to name a few. In many of these applications, there is often a trade-off between achieving high utility and minimizing risk. Moreover, uncertain and costly evaluations are an inherent part of black-box optimization tasks, and modern learning methods need to handle these aspects when balancing between the previous two objectives.

Bayesian optimization (BO) is a powerful framework for optimizing such costly black-box functions from noisy zeroth-order evaluations. Classical BO approaches are typically risk-neutral as they seek to optimize the expected function value only. In practice, however, two different solutions might attain similar expected function values, but one might produce significantly noisier realizations. This is of major importance when it comes to actual deployment of the found solutions. For example, when selecting hyperparameters of a machine learning algorithm, we might prefer configurations that lead to slightly higher test errors but at the same time lead to smaller variance.

In this paper, we generalize BO to trade off mean and input-dependent noise variance when sequentially querying points and outputting final solutions. We introduce a practical setting where both the black-box objective and input-dependent noise variance are unknown a priori, and the learner needs to estimate them on the fly. We propose a novel optimistic risk-averse algorithm – RAHBO – that makes sequential decisions by simultaneously balancing between exploration (learning about uncertain actions), exploitation (choosing actions that lead to high gains) and risk (avoiding unreliable actions). We bound the cumulative regret of RAHBO as well as the number of samples required to output a single near-optimal risk-averse solution. In our experiments, we demonstrate the risk-averse performance of our algorithm and show that standard BO methods can severely fail in applications where reliability of the reported solutions is of utmost importance.

Related work.

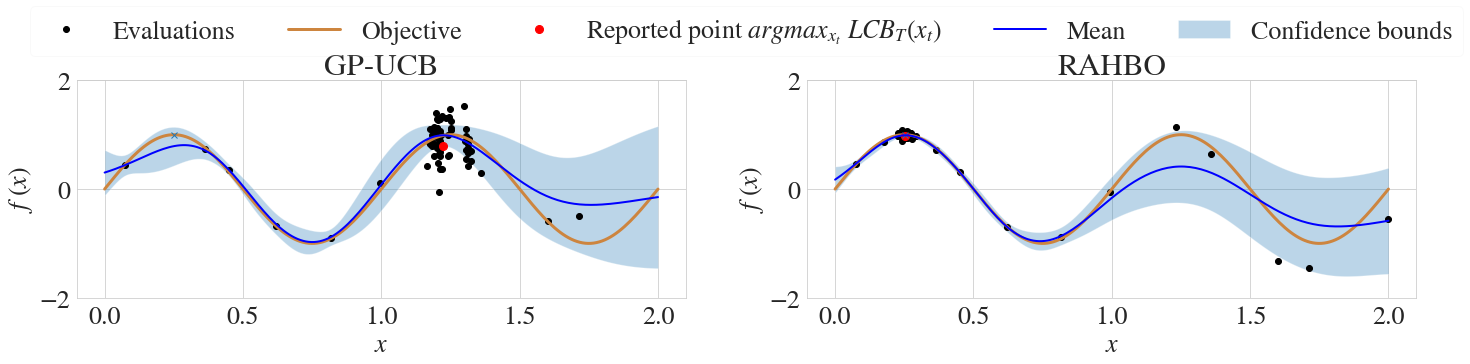

Bayesian optimization (BO) [26] refers to approaches for optimizing a noisy black-box objective that is typically expensive to evaluate. A great number of BO methods have been developed over the years, including a significant number of variants of popular algorithms such as GP-UCB [35], Expected Improvement [26], and Thompson Sampling [14]. While the focus of standard BO approaches is mainly on trading-off exploration vs. exploitation and optimizing for the expected performance, in this work, we additionally focus on the risk that is involved when working with noisy objectives, as illustrated in Figure 1.

The vast majority of previous BO works assume (sub-) Gaussian and homoscedastic noise (i.e., input independent and of some known fixed level). Both assumptions can be restrictive in practice. For example, as demonstrated in [15], the majority of hyperparameter tuning tasks exhibit heteroscedasticity. A few works relax the first assumption and consider, e.g., heavy-tailed noise models [31] and adversarially corrupted observations [8]. The second assumption is typically generalized via heteroscedastic Gaussian process (GP), allowing an explicit dependence of the noise distribution on the evaluation points [6, 10, 7, 20]. Similarly, in this work, we consider heteroscedastic GP models, but unlike the previous works, we specifically focus on the risk that is associated with querying and reporting noisy points.

Several works have recently considered robust and risk-averse aspects in BO. Their central focus is on designing robust strategies and protecting against the change/shift in uncontrollable covariates. They study various notions including worst-case robustness [9], distributional robustness [19, 30], robust mixed strategies [33] and other notions of risk-aversion [18, 11, 29], and while some of them report robust regret guarantees, their focus is primarily on the robustness in the homoscedastic GP setting. Instead, in our setting, we account for the risk that comes from the realization of random noise with unknown distribution. Rather than optimizing the expected performance, in our risk-averse setting, we prefer inputs with lower variance. To this end, we incorporate the learning of the noise distribution into the optimization procedure via a mean-variance objective. The closest to our setting is risk-aversion with respect to noise in multi-armed bandits [32]. Their approach, however, fails to exploit correlation in rewards among similar arms.

Contributions.

We propose a novel Risk-averse Heteroscedastic Bayesian optimization (RAHBO) approach based on the optimistic principle that trades off the expectation and uncertainty of the mean-variance objective function. We model both the objective and variance as (unknown) functions belonging to RKHS space of functions, and propose a practical risk-aware algorithm in the heteroscedastic GP setting. In our theoretical analysis, we establish rigorous sublinear regret guarantees for our algorithm, and provide a robust reporting rule for applications where only a single solution is required. We demonstrate the effectiveness of RAHBO on synthetic benchmarks, as well as on hyperparameter tuning tasks for the Swiss free-electron laser and a machine learning model.

2 Problem setting

Let be a given compact set of inputs ( for some ). We consider a problem of sequentially interacting with a fixed and unknown objective . At every round of this procedure, the learner selects an action , and obtains a noisy observation

| (1) |

where is zero-mean noise independent across different time steps . In this work, we consider sub-Gaussian heteroscedastic noise that depends on the query location.

Definition 1.

A zero-mean real-valued random variable is –sub-Gaussian, if there exists variance-proxy such that .

For a sub-Gaussian , its variance lower bounds any valid variance-proxy , i.e., . In case holds, is said to be strictly –sub-Gaussian. Besides zero-mean Gaussian random variables, most standard symmetric bounded random variables (e.g., Bernoulli, beta, uniform, binomial) are strictly sub-Gaussian (see [2, Proposition 1.1]). Throughout the paper, we consider sub-Gaussian noise, and in Section 3.3, we specialize to the case of strictly sub-Gaussian noise.

Optimization objective. Unlike the previous works that mostly focus on sequential optimization of in the homoscedastic noise case, in this work, we consider the trade-off between risk and return in the heteroscedastic case. While there exist a number of risk-averse objectives, we consider the simple and frequently used mean-variance objective (MV) [32]. Here, the objective value at is a trade-off between the (mean) return and the risk expressed by its variance-proxy :

| (2) |

where is a so-called coefficient of absolute risk tolerance. In this work, we assume is fixed and known to the learner. In the case of , maximizing coincides with the standard BO objective.

Performance metrics. We aim to construct a sequence of input evaluations that eventually maximizes the risk-averse objective . To assess this convergence, we consider two metrics. The first metric corresponds to the notion of cumulative regret similar to the one used in standard BO and bandits. Here, the learner’s goal is to maximize its risk-averse cumulative reward over a time horizon , or equivalently minimize its risk-averse cumulative regret:

| (3) |

where . A sublinear growth of with implies vanishing average regret as . Intuitively, this implies the existence of some such that is arbitrarily close to the optimal value .

The second metric is used when the learner seeks to simultaneously minimize the number of expensive function evaluations . Namely, for a given accuracy , we report a single "good" risk-averse point after a total of rounds, that satisfies:

| (4) |

Both metrics are important for choosing risk-averse solutions and which one is preferred depends on the application at hand. For example, risk-averse cumulative regret might be of a greater interest in online recommendation systems, while reporting a single point with high MV value might be more suitable when tuning machine learning hyperparameters. We consider both performance metrics in our experiments.

Regularity assumptions. We consider standard smoothness assumptions [35, 9] when it comes to the unknown function . In particular, we assume that belongs to a reproducing kernel Hilbert space (RKHS) (a space of smooth and real-valued functions defined on ), i.e., , induced by a kernel function . We also assume that for every . Moreover, the RKHS norm of is assumed to be bounded for some fixed constant . We assume that the noise is –sub-Gaussian with variance-proxy uniformly bounded for some constant values .

3 Algorithms

We first recall the Gaussian process (GP) based framework for sequential learning of RKHS functions from observations with heteroscedastic noise. Then, in Section 3.2, we consider a simple risk-averse Bayesian optimization problem with known variance-proxy, and later on in Section 3.3, we focus on our main problem setting in which the variance-proxy is unknown.

3.1 Bayesian optimization with heteroscedastic noise

Before addressing the risk-averse objective, we briefly recall the standard GP-UCB algorithm [35] in the setting of heteroscedastic sub-Gaussian noise. The regularity assumptions permit the construction of confidence bounds via GP model. Particularly, to decide which point to query at every round, GP-UCB makes use of the posterior GP mean and variance denoted by and , respectively. They are computed based on the previous measurements and the given kernel :

| (5) | |||

| (6) |

where , , and prior modelling assumptions are and .

At time , GP-UCB maximizes the upper confidence bound of , i.e.,

| (7) |

If the noise is heteroscedastic and -sub-Gaussian, the following confidence bounds hold:

Lemma 1 (Lemma 7 in [20]).

Here, stands for the parameter that balances between exploration vs. exploitation and ensures the validity of confidence bounds. The analogous concentration inequalities in case of homoscedastic noise were considered in [1, 14, 35].

Failure of GP-UCB in the risk-averse setting. GP-UCB is guaranteed to achieve sublinear cumulative regret with high probability in the risk-neutral (homoscedastic/heteroscedastic) BO setting [35, 14]. However, for the risk-averse setting in Eq. 2, the maximizers and might not coincide, and consequently, can be significantly larger than . This is illustrated in Figure 1, where GP-UCB most frequently chooses optimum of the highest risk.

3.2 Warm up: Known variance-proxy

We remedy the previous issue with GP-UCB by proposing a natural Risk-averse Heteroscedastic BO (RAHBO) in case of the known variance-proxy . At each round , RAHBO chooses the action:

| (9) |

where is from Lemma 1 and is from Eq. 2. In the next section, we further relax the assumption of the variance-proxy and consider a more practical setting when is unknown to the learner. For the current setting, the performance of RAHBO is formally captured in the following proposition.

Proposition 1.

Here, denotes the maximum information gain [35] at time defined via mutual information between evaluations and at points :

| (10) | |||

| (11) |

in case of heteroscedastic noise (see Section A.1.1). The upper bounds on are provided in [35] widely used kernels. These upper bounds typically scale sublinearly in ; for linear kernel , and in case of squared exponential kernel . While these bounds are derived assuming the homoscedastic GP setting with some fixed constant noise variance, we show (in Section A.1.3) that the same rates (up to a multiplicative constant factor) apply in the heteroscedastic case.

3.3 RAHBO for unknown variance-proxy

In the case of unknown variance-proxy, the confidence bounds for the unknown in Lemma 1 can not be readily used, and we construct new ones on the combined mean-variance objective. To learn about the unknown , we make some further assumptions.

Assumption 1.

The variance-proxy belongs to an RKHS induced by some kernel , i.e., , and its RKHS norm is bounded for some finite . Moreover, the noise in Eq. 1 is strictly –sub-Gaussian, i.e., for every .

As a consequence of our previous assumption, we can now focus on estimating the variance since and coincide. In particular, to estimate we consider a repeated experiment setting, where for each we collect evaluations , . Then, the sample mean and variance of are given as:

| (12) |

The key idea is that for strictly sub-Gaussian noise , yields unbiased, but noisy evaluations of the unknown variance-proxy , i.e.,

| (13) |

with zero-mean noise . In order to efficiently estimate , we need an additional assumption.

Assumption 2.

The noise in Eq. 13 is –sub-Gaussian with known and the realizations are independent between .

We note that a similar assumption is made in [32] in the multi-armed bandit setting. The fact that is known is rather mild as Assumption 1 allows controlling its value. For example, in case of strictly sub-Gaussian we show (in Section A.2) that . Then, given that , we can utilize the following (rather conservative) bound as a variance-proxy, i.e., .

RAHBO algorithm. We present our Risk-averse Heteroscedastic BO approach for unknown variance-proxy in Algorithm 1. Our method relies on building the following two GP models.

Firstly, we use sample variance evaluations to construct a GP model for . The corresponding and are computed as in Eqs. 5 and 6 by using kernel , variance-proxy and noisy observations . Consequently, we build the upper and lower confidence bounds and of the variance-proxy and we set according to Lemma 1:

| (14) | ||||

| (15) |

Secondly, we use sample mean evaluations to construct a GP model for . The mean and variance in Eqs. 6 and 5, however, rely on the unknown variance-proxy in , an we thus use its upper confidence bound truncated with :

| (16) |

where is corrected by since every evaluation in is an average over samples. This substitution of the unknown variance-proxy by its conservative estimate guarantees that the confidence bounds on also hold with high probability (conditioning on the confidence bounds for holding true; see Section A.3 for more details).

Finally, we define the acquisition function as , i.e., selecting at each round .

The proposed algorithm leads to new maximum information gains and for sample mean and sample variance evaluations. The corresponding mutual information in and is computed according to Eq. 11 for heteroscedastic noise with variance-proxy and , respectively (see Section A.4). The performance of RAHBO is captured in the following theorem.

Theorem 1.

Consider any with and sampling model in Eq. 1 with unknown variance-proxy that satisfies Assumptions 1 and 2. Let denote the set of actions chosen by RAHBO (Algorithm 1) over T rounds. Set and according to Lemma 1 with , and . Then, the risk-averse cumulative regret of RAHBO is bounded as follows:

| (17) |

The risk-averse cumulative regret of RAHBO depends sublinearly on for most of the popularly used kernels. This follows from the implicit sublinear dependence on in and (the bounds in case of heteroscedastic noise replicate the ones used in Proposition 1 as shown in Sections A.1.2 and A.1.3). Finally, the result of Theorem 1 provides a non-trivial trade-off for number of repetitions where larger increases sample complexity but also leads to better estimation of the noise model. Furthermore, we obtain the bound for the number of rounds required for identifying an -optimal point:

Corollary 1.1.

Consider the setup of Theorem 1. Let denote actions selected by RAHBO over rounds. Then, with probability at least , the reported point where , achieves -accuracy, i.e., , after rounds.

The previous result demonstrates the sample complexity rates when a single risk-averse reported solution is required. We note that both Theorem 1 and Corollary 1.1 provide guarantees for choosing risk-averse solutions, and depending on application at hand, we might consider either one of the proposed performance metrics. We demonstrate use-cases for both in the following section.

4 Experiments

In this section, we experimentally validate RAHBO on two synthetic examples and two real hyperparameter tuning tasks, and compare it with the baselines. We provide an open-source implementation of our method.111https://github.com/Avidereta/risk-averse-hetero-bo

Baselines. We compare against two baselines: As the first baseline, we use GP-UCB with heteroscedastic noise as a standard risk-neutral algorithm that optimizes the unknown . As the second one, we consider a risk-averse baseline that uniformly learns variance-proxy before the optimization procedure, in contrast to RAHBO which learns the variance-proxy on the fly. We call it RAHBO-US, standing for RAHBO with uncertainty sampling. It consists of two stages: (i) uniformly learning via uncertainty sampling, (ii) GP-UCB applied to the mean-variance objective, in which instead of the unknown we use the mean of the learned model. Note that RAHBO-US is the closest to the contextual BO setting [18], where the context distribution is assumed to be known.

Experimental setup. At each iteration , an algorithm queries a point and observes sample mean and sample variance of observations . We use a heteroscedastic GP for modelling and a homoscedastic GP for . We set and , which is commonly used in practice to improve performance over the theoretical results. Before the BO procedure, we determine the GP hyperparameters maximizing the marginal likelihood. To this end, we use initial points that are same for all the baselines and are chosen via Sobol sequence that generates low discrepancy quasi-random samples. We repeat each experiment several times, generating new initial points for every repetition. We use two metrics: (a) risk-averse cumulative regret computed for the acquired inputs; (b) simple regret computed for inputs as reported via Corollary 1.1. For each metric, we report its mean two standard errors over the repetitions.

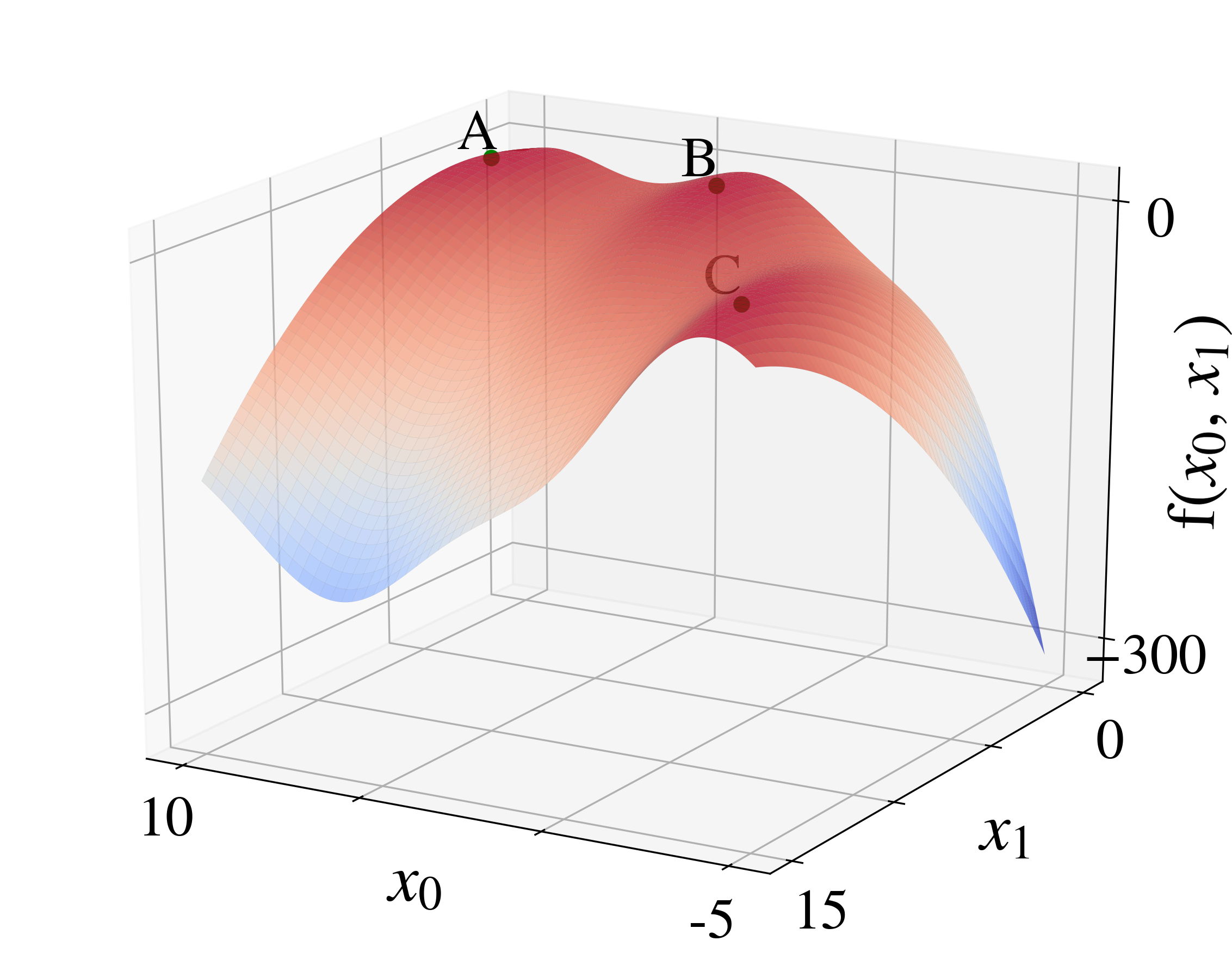

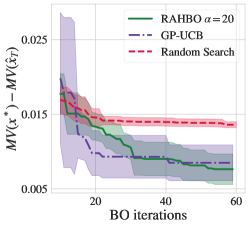

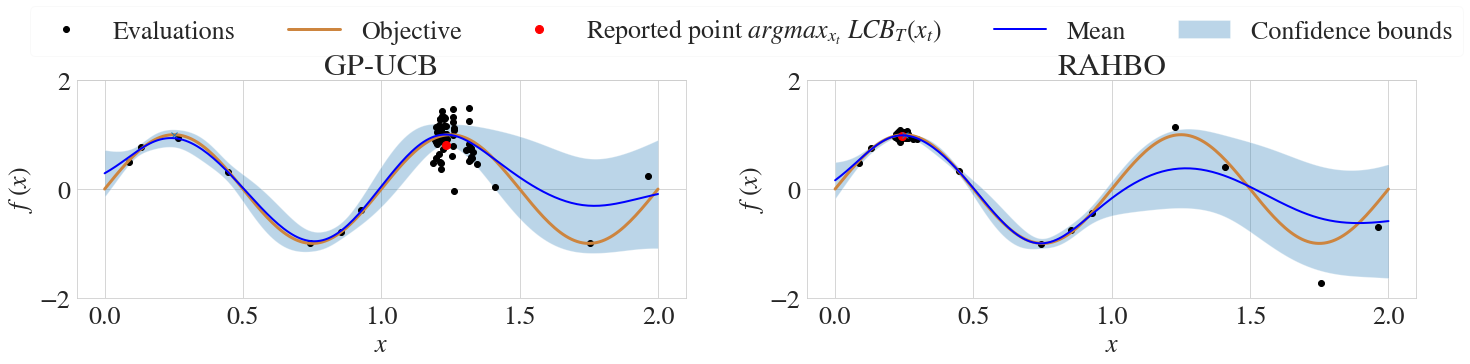

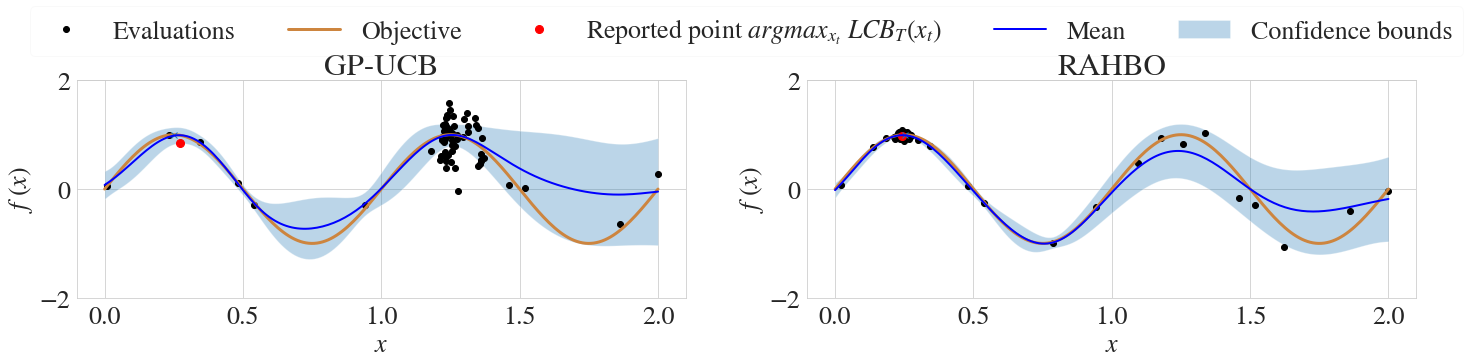

Example function We first illustrate the methods performance on a sine function depicted in Figure 2(a). This function has two global optimizers. We induce a heteroscedastic zero-mean Gaussian noise on the measurements. We use a sigmoid function for the noise variance, as depicted in Figure 2(a), that induces small noise on and higher noise on . We initialize the algorithms by selecting inputs at random and keep these points the same for all the algorithms. We use samples at each chosen . The number of acquisition rounds is . We repeat the experiment times for each method and show their average performances in Figure 2.

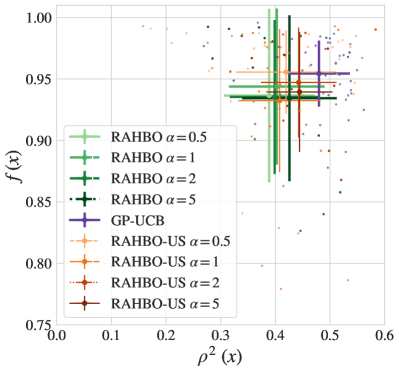

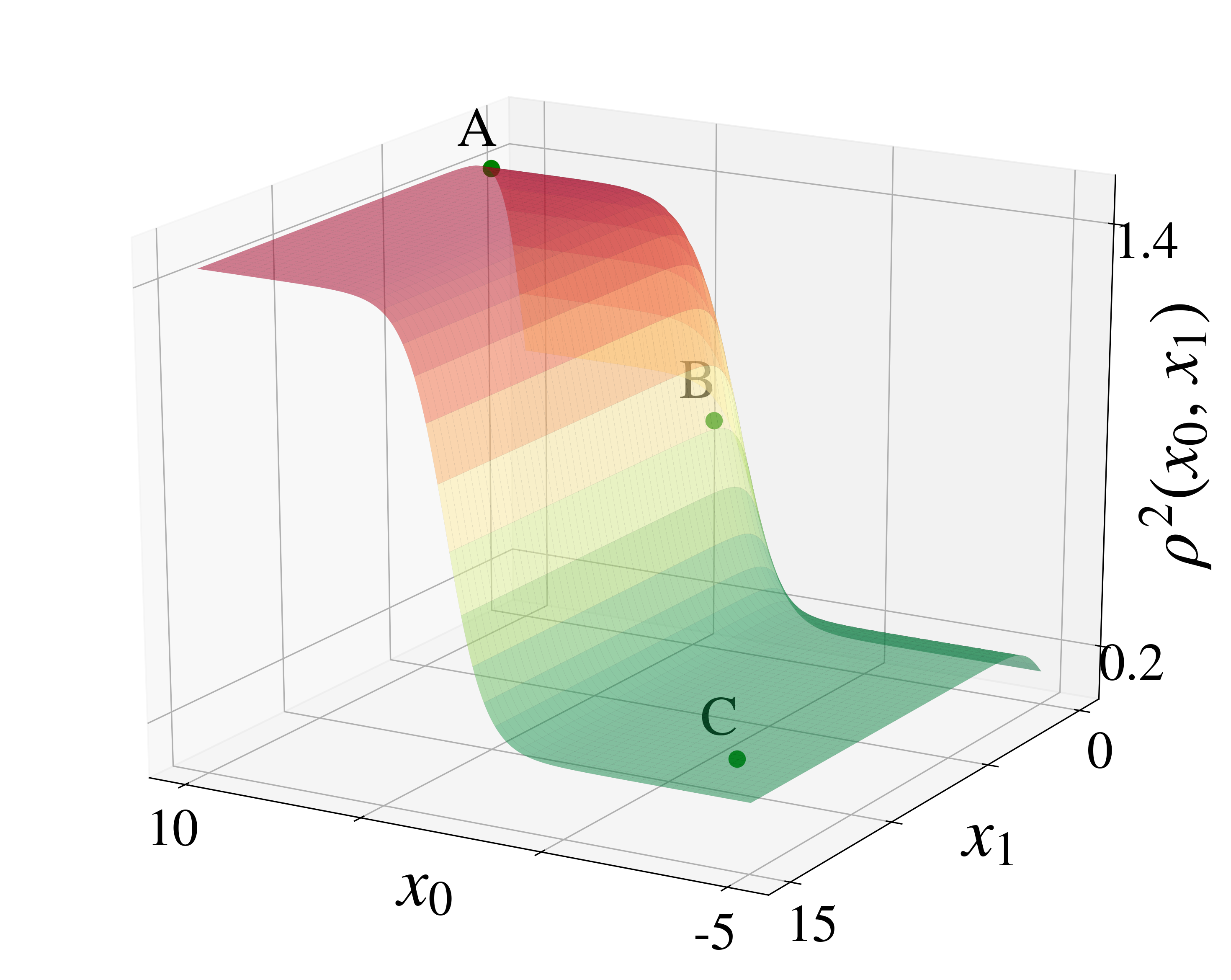

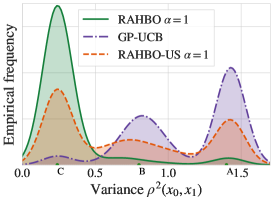

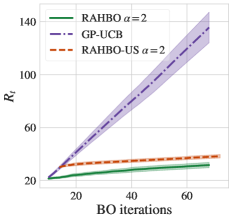

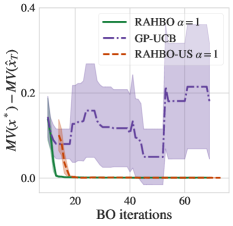

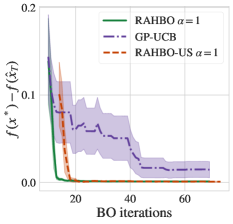

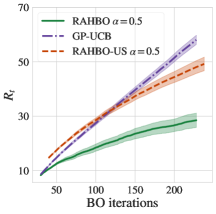

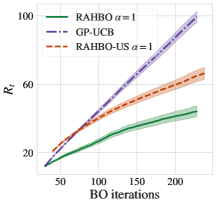

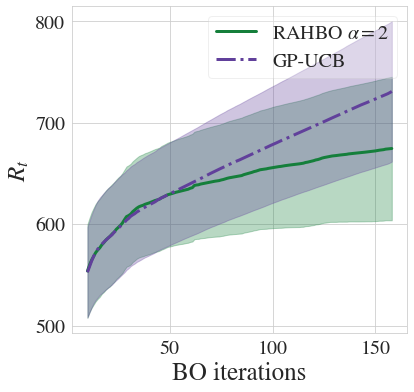

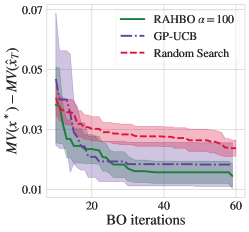

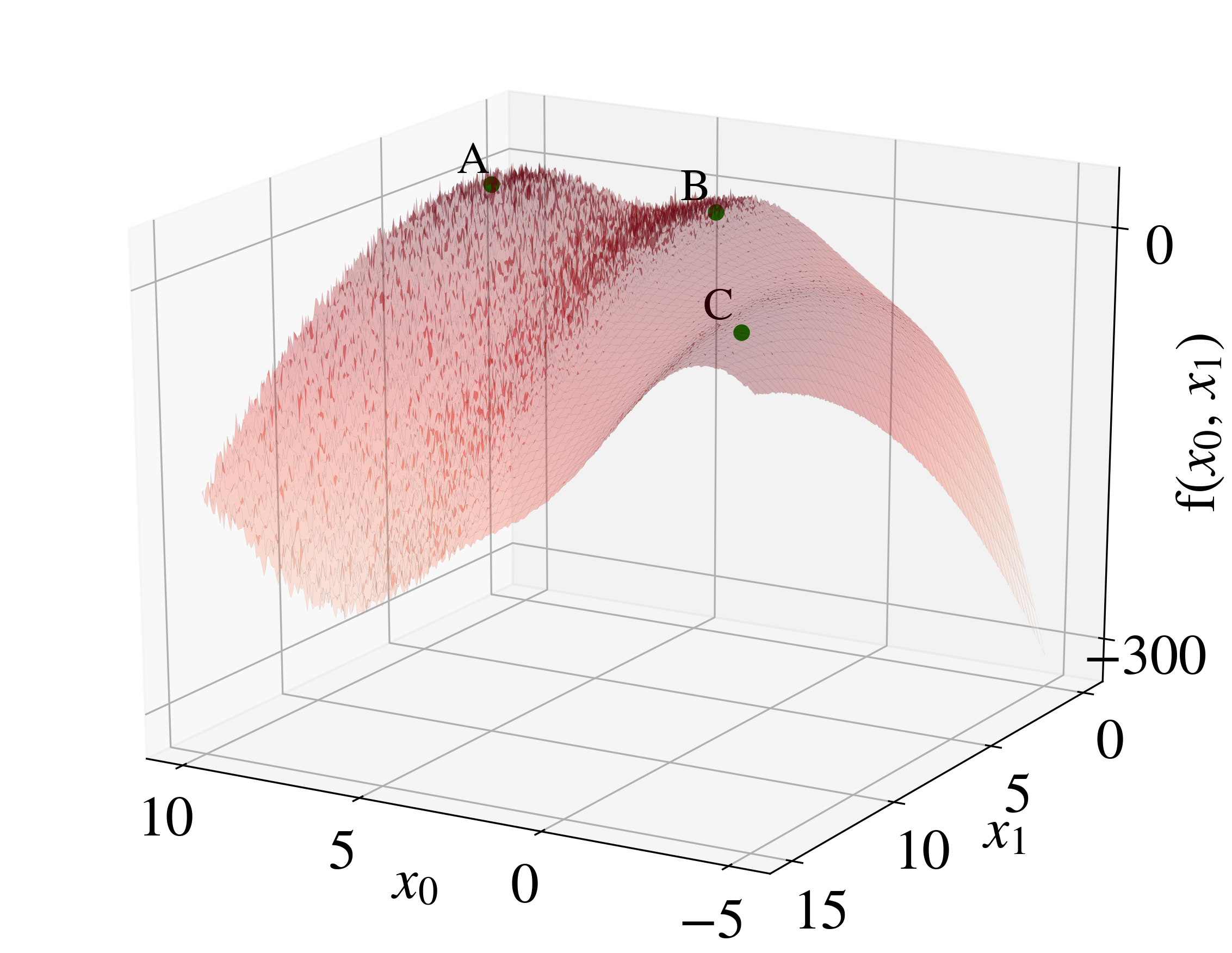

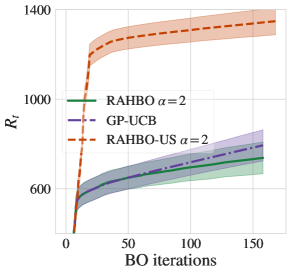

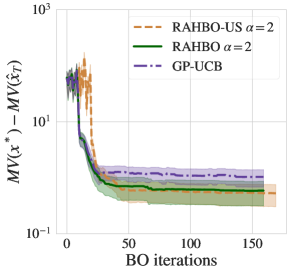

Branin benchmark Next, we evaluate the methods on the (negated) Branin benchmark function in Figure 1(a), achieving its optimum value at . The heteroscedastic variance function illustrated in Figure 1(b) defines different noise variances for the three optima. We initialize all algorithms by selecting inputs. We use samples to estimate the noise variance. The number of acquisition rounds is . We repeat BO times and show the results in Figures 5(a) and 1(c). Figure 1(c) provides more intuition behind the observed regret: UCB exploits the noisiest maxima the most, while RAHBO prefers smaller variance.

Tuning Swiss free-electron laser In this experiment, we tune the parameters of Swiss X-ray free-electron laser (SwissFEL), an important scientific instrument that generates very short pulses of X-ray light and enables researchers to observe extremely fast processes. The main objective is to maximize the pulse energy measured by a gas detector, that is a time-consuming and repetitive task during the SwissFEL operation. Such (re-)tuning takes place while user experiments on SwissFEL are running, and thus the cumulative regret is the metric of high importance in this application.

We use real SwissFEL measurements collected in [21] to train a neural network surrogate model, and use it to simulate the SwissFEL objective for new parameter settings . We similarly fit a model of the heteroscedastic variance by regressing the squared residuals via a GP model. Here, we focus on the calibration of the four most sensitive parameters.

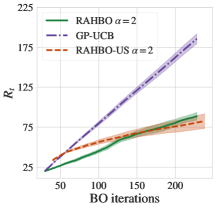

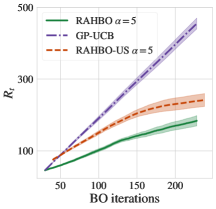

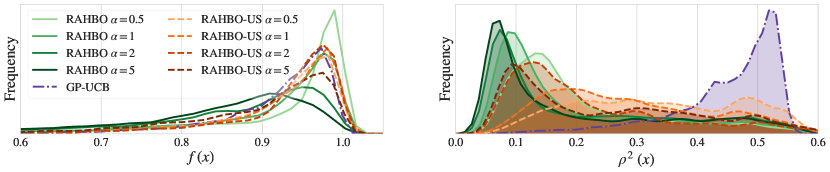

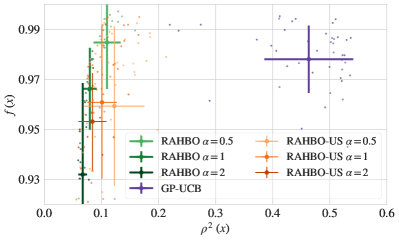

We report our comparison in Figure 4 where we also assess the effect of varying the coefficient of absolute risk tolerance . We use 30 points to initialize the baselines and then perform 200 acquisition rounds. We repeat each experiment 15 times. In Figure 4(a) we plot the empirical frequency of the true (unknown to the methods) values and at the inputs acquired by the methods. The empirical frequency for illustrates the tendency of risk-neutral GP-UCB to query points with higher noise, while risk-averse achieves substantially reduced variance and minimal reduction in mean performance. Sometimes, risk-neutral GP-UCB also fails to succeed in querying points with the highest -value. That tendency results in lower cumulative regret for RAHBO in Figures 4(c) and 4(d). We also compare the performance of the reporting rule from Corollary 1.1 in Figure 4(b), where we plot error bars with standard deviation both for and at the reported point . As before, RAHBO drastically reduces the variance compared to GP-UCB, while having only slightly lower mean performance. Additional results are presented in Figure 10 in Appendix.

Random Forest tuning BO is widely used by cloud services for tuning machine learning hyperparameters and the resulting models might be then used in high-stakes applications such as credit scoring or fraud detection. In k-fold cross-validation, the average metric over the validation sets is optimized – a canonical example of the repeated experiment setting that we consider in the paper. High across-folds variance is a practical problem [24] where the mean-variance approach might be beneficial.

In our experiment, we tune hyperparameters of a random forest classifier (RF) on a dataset of fraudulent credit card transactions [23].222https://www.kaggle.com/mlg-ulb/creditcardfraud It consist of 285k transactions with 29 features (processed due to confidentiality issues) that are distributed over time, and only 0.2% are fraud examples (see Appendix for more details). The search space for the RF hyperparameters is also provided in the Appendix. We use the balanced accuracy score and 5 validation folds, i.e., , and each validation fold is shifted in time with respect to the training data. We seek not only for high performance on average but also for low variance across the validation folds that have different time shifts with respect to the training data.

We initialize the algorithms by selecting 10 hyperparameter settings and keep these points the same for all algorithms. We use Matérn 5/2 kernels with Automatic Relevance Discovery (ARD) and normalize the input features to the unit cube. The number of acquisition rounds in one experiment is 50 and we repeat each experiment 15 times. We demonstrate our results in Figures 5(b) and 5(c) where we plot mean 2 standard errors. While both RAHBO and GP-UCB perform comparable in terms of the mean error, its standard deviation for RAHBO is smaller.

5 Conclusion

In this work, we generalize Bayesian optimization to the risk-averse setting and propose RAHBO algorithm aiming to find an input with both large expected return and small input-dependent noise variance. Both the mean objective and the variance are assumed to be unknown a priori and hence are estimated online. RAHBO is equipped with theoretical guarantees showing (under reasonable assumptions) sublinear dependence on the number of evaluation rounds both for cumulative risk-averse regret and -accurate mean-variance metric. The empirical evaluation of the algorithm on synthetic benchmarks and hyperparameter tuning tasks demonstrate promising examples of heteroscedastic use-cases benefiting from RAHBO.

Acknowledgements

This research has been gratefully supported by NCCR Automation grant 51NF40 180545, by ERC under the European Union’s Horizon grant 815943, SNSF grant 200021_172781, and ETH Zürich Postdoctoral Fellowship 19-2 FEL-47.

The authors thank Sebastian Curi, Mojmír Mutný and Johannes Kirschner as well as the anonymous reviewers of this paper for their helpful feedback.

References

- [1] Y. Abbasi-Yadkori. Online learning for linearly parametrized control problems. PhD thesis, Edmonton, Alberta, 2012.

- [2] J. Arbel, O. Marchal, and H. D. Nguyen. On strict sub-Gaussianity, optimal proxy variance and symmetry for bounded random variables. arXiv:1901.09188, 2019.

- [3] M. Balandat, B. Karrer, D. R. Jiang, S. Daulton, B. Letham, A. G. Wilson, and E. Bakshy. BoTorch: a framework for efficient Monte-Carlo Bayesian optimization. In Neural Information Processing Systems (NeurIPS), 2020.

- [4] E. Benhamou. A few properties of sample variance. arXiv:1809.03774, 2018.

- [5] F. Berkenkamp, A. Krause, and A. P. Schoellig. Bayesian optimization with safety constraints: Safe and automatic parameter tuning in robotics. arXiv:1602.04450, 2016.

- [6] M. Binois, R. B. Gramacy, and M. Ludkovski. Practical heteroscedastic Gaussian process modeling for large simulation experiments. Journal of Computational and Graphical Statistics, 2018.

- [7] M. Binois, J. Huang, R. B. Gramacy, and M. Ludkovski. Replication or exploration: Sequential design for stochastic simulation experiments. In Technometrics, 2019.

- [8] I. Bogunovic, A. Krause, and J. Scarlett. Corruption-tolerant Gaussian process bandit optimization. In Conference on Artificial Intelligence and Statistics (AISTATS), 2020.

- [9] I. Bogunovic, J. Scarlett, S. Jegelka, and V. Cevher. Adversarially robust optimization with Gaussian processes. In Neural Information Processing Systems (NeurIPS), 2018.

- [10] I. Bogunovic, J. Scarlett, A. Krause, and V. Cevher. Truncated variance reduction: A unified approach to Bayesian optimization and level-set estimation. In Neural Information Processing Systems (NeurIPS), 2016.

- [11] S. Cakmak, R. Astudillo, P. I. Frazier, and E. Zhou. Bayesian optimization of risk measures. In Neural Information Processing Systems (NeurIPS), 2020.

- [12] R. Calandra, A. Seyfarth, J. Peters, and M. P. Deisenroth. Bayesian optimization for learning gaits under uncertainty. Annals of Mathematics and Artificial Intelligence, 2016.

- [13] Y. Chen, A. Huang, Z. Wang, I. Antonoglou, J. Schrittwieser, D. Silver, and N. de Freitas. Bayesian optimization in Alphago. arXiv:1812.06855, 2018.

- [14] S. R. Chowdhury and A. Gopalan. On kernelized multi-armed bandits. In International Conference on Machine Learning (ICML), 2017.

- [15] A. I. Cowen-Rivers, W. Lyu, R. Tutunov, Z. Wang, A. Grosnit, R. R. Griffiths, H. Jianye, J. Wang, and H. B. Ammar. An empirical study of assumptions in Bayesian optimisation. arXiv:2012.03826, 2021.

- [16] J. González, J. Longworth, D. C. James, and N. D. Lawrence. Bayesian optimization for synthetic gene design. arXiv:1505.01627, 2015.

- [17] R.-R. Griffiths and J. M. Hernández-Lobato. Constrained Bayesian optimization for automatic chemical design using variational autoencoders. Chemical Science, 2020.

- [18] S. Iwazaki, Y. Inatsu, and I. Takeuchi. Mean-variance analysis in Bayesian optimization under uncertainty. In Conference on Artificial Intelligence and Statistics (AISTATS), 2021.

- [19] J. Kirschner, I. Bogunovic, S. Jegelka, and A. Krause. Distributionally robust Bayesian optimization. In Conference on Artificial Intelligence and Statistics (AISTATS), 2020.

- [20] J. Kirschner and A. Krause. Information directed sampling and bandits with heteroscedastic noise. In Conference On Learning Theory (COLT), 2018.

- [21] J. Kirschner, M. Mutny, N. Hiller, R. Ischebeck, and A. Krause. Adaptive and safe Bayesian optimization in high dimensions via one-dimensional subspaces. In International Conference on Machine Learning (ICML), 2019.

- [22] K. Korovina, S. Xu, K. Kandasamy, W. Neiswanger, B. Poczos, J. Schneider, and E. P. Xing. Chembo: Bayesian optimization of small organic molecules with synthesizable recommendations. arXiv:1908.01425, 2019.

- [23] Y.-A. Le Borgne and G. Bontempi. Machine Learning for Credit Card Fraud Detection - Practical Handbook. Université Libre de Bruxelles, 2021.

- [24] A. Makarova, H. Shen, V. Perrone, A. Klein, J. B. Faddoul, A. Krause, M. Seeger, and C. Archambeau. Overfitting in Bayesian optimization: an empirical study and early-stopping solution. In ICLR Workshop on Neural Architecture Search, 2021.

- [25] A. Marco, P. Hennig, J. Bohg, S. Schaal, and S. Trimpe. Automatic LQR tuning based on Gaussian process global optimization. In International Conference on Robotics and Automation (ICRA), 2016.

- [26] J. Močkus. On Bayesian methods for seeking the extremum. In Optimization Techniques, 1975.

- [27] H. Moss, D. Leslie, D. Beck, J. González, and P. Rayson. BOSS: Bayesian optimization over string spaces. In Neural Information Processing Systems (NeurIPS), 2020.

- [28] D. M. Negoescu, P. I. Frazier, and W. B. Powell. The knowledge-gradient algorithm for sequencing experiments in drug discovery. INFORMS J. on Computing, 2011.

- [29] Q. P. Nguyen, Z. Dai, B. K. H. Low, and P. Jaillet. Value-at-risk optimization with Gaussian processes. In International Conference on Machine Learning (ICML), 2021.

- [30] T. Nguyen, S. Gupta, H. Ha, S. Rana, and S. Venkatesh. Distributionally robust Bayesian quadrature optimization. In Conference on Artificial Intelligence and Statistics (AISTATS), 2020.

- [31] S. Ray Chowdhury and A. Gopalan. Bayesian optimization under heavy-tailed payoffs. In Neural Information Processing Systems (NeurIPS), 2019.

- [32] A. Sani, A. Lazaric, and R. Munos. Risk-aversion in multi-armed bandits. In Neural Information Processing Systems (NeurIPS), 2012.

- [33] P. G. Sessa, I. Bogunovic, M. Kamgarpour, and A. Krause. Mixed strategies for robust optimization of unknown objectives. In Conference on Artificial Intelligence and Statistics (AISTATS), 2020.

- [34] J. Snoek, H. Larochelle, and R. P. Adams. Practical Bayesian optimization of machine learning algorithms. In Neural Information Processing Systems (NeurIPS), 2012.

- [35] N. Srinivas, A. Krause, S. Kakade, and M. Seeger. Gaussian process optimization in the bandit setting: No regret and experimental design. In International Conference on International Conference on Machine Learning (ICML), 2010.

Appendix A Appendix

Risk-averse Heteroscedastic Bayesian Optimization

(Anastasiia Makarova, Ilnura Usmanova, Ilija Bogunovic, Andreas Krause)

A.1 Details on Proposition 1

We first provide the proof of Proposition 1 for cumulative risk-averse regret Eq. 3 with known variance-proxy (see Definition 1) (Section A.1.1). We further provide data-independent bounds for (Section A.1.2) and maximum information gain (Section A.1.3) that together conclude the proof for sub-linear on regret guarantees for most of the popularly used kernels.

A.1.1 Proof Proposition 1

Proposition 1. Consider any with and sampling model from Eq. 1 with known variance-proxy . Let be set as in Lemma 1 with . Then, with probability at least , RAHBO attains cumulative risk-averse regret .

Proof.

The main steps of the proof are as follows: In Step 1, we derive the upper and the lower confidence bounds, and , on at iteration . In Step 2, we bound the instantaneous risk-averse regret . In Step 3, we derive mutual information in case of the heteroscedastic noise. In Step 4, we bound the sum of variances via mutual information . In Step 5, we bound the cumulative regret based on the previous steps.

Step 1:

On the confidence bounds for .

In case of known variance-proxy , the confidence bounds for at iteration can be directly obtained based on the posterior and for defined in Eqs. 5 and 6. Particularly, for defined in Eq. 8,

with the confidence bounds:

| (18) | |||

| (19) |

Step 2: On bounding the instantaneous risk-averse regret . We have

where the first inequality is due to the definition of confidence bounds, the second is due to the acquisition strategy and the equality further expands and Thus, the cumulative regret can be bounded as follows:

| (20) |

where the last inequality holds since is a non-decreasing sequence.

Step 3: On mutual information and maximum information gain .

Mutual information between the vector of evaluations at points and is defined by

where denotes entropy. Under the modelling assumptions and for the noise , the measurements are distributed as and , where is defined in Eq. 6. Hence, the entropy of each new measurement conditioned on the previous history is:

Therefore, the information gain for is:

| (21) |

Then, by definition of maximum information gain:

| (22) |

Step 4: On bounding .

| (23) |

where the first inequality follows from the Cauchy-Schwarz inequality. The second one is due to the fact that for any we can bound , that also holds for since for . The third inequality is due to .

A.1.2 Bounds for

We provide the bounds for the data-dependent that appear in the regret bound (see Eq. 8). Following our modelling assumptions and , the information gain is given as follows:

| (24) |

By definition then . On the other hand, defined in Lemma 1 can be expanded in a data-independent manner as follows:

| (25) |

A.1.3 Bounds for

Here, we show the relation between the information gains under heteroscedastic and homoscedastic noise. Note that for the latter the upper bounds are widely known, e.g., [35]. To distinguish between the maximum information gain for heteroscedastic noise with variance-proxy and the maximum information gain for homoscedastic noise with fixed variance-proxy , we denote them as and respectively. Recall that for some constant values .

Below, we show that with set to , that only affects the constants but not the main scaling (in terms of ) of the known bound for the homoscedastic maximum information gain.

| (26) | |||||

| (27) | |||||

| (28) |

where follows from Eq. 21. In , we lower bound the denominator and upper bound the numerator (due to monotonicity w.r.t. noise variance, i.e., ). In , we multiply by . In we use Bernoulli inequality since . The obtained expression can be interpreted as a standard information gain for homoscedastic noise and, particularly, with the variance-proxy set to due to . Finally, the upper bounds on typically scale sublinearly in for most of the popularly used kernels [35], e.g, for linear kernel , and for squared exponential kernel .

A.2 Tighter bounds for the variance-proxy .

Assumption 2 states that noise from Eq. 13 is -sub-Gaussian with variance-proxy being known. In practice, might be unknown. Here, we describe a way to estimate under the following two assumptions: the evaluation noise is strictly sub-Gaussian (that is already reflected in the Assumption 1) and the noise of variance evaluation is also strictly sub-Gaussian, that is, and .

(i) Reformulation of the sample variance. We first rewrite the sample variance defined in Eq. 12 as the average over squared differences over all pairs :

(ii) Variance of the sample variance . In Eq. 29, we show that sample variance can be written in terms of the noise . In [4] (see Eq. (37)), it is shown that for i.i.d observations , sampled from a distribution with the 2nd and 4th central moments and , respectively, the variance of the sample variance can be computed as follows:

Since is strictly –sub-Gaussian, the latter can be further adapted as

(iii) Due to being strictly sub-Gaussian, i.e., , the derivation above also holds for the variance-proxy :

(iv) Bound 4th moment . The 4th moment can expressed in terms of the distribution kurtosis that is bounded under our assumptions. Particularly, kurtosis is measure that identifies the tails behaviour of the distribution of ; for normallly distribute and for strictly sub-Gaussian random variable (see [2]). This implies

(v) Bound variance-proxy. There

In case of the known bound , we bound the unknown as follows:

A.3 Method details: GP-estimator of variance-proxy

According to the Assumption 2, variance-proxy is smooth, and is -sub-Gaussian with known variance-proxy . In this case, confidence bounds for follow the ones derived in Lemma 1 with based on . Particularly, we collect noise variance evaluations Then the estimates for and for follow the corresponding estimates for . Particularly,

| (32) | ||||

| (33) |

A.4 Proof of Theorem 1

Theorem 1.

Consider any with and sampling model in Eq. 1 with unknown variance-proxy that satisfies Assumptions 1 and 2. Let denote the set of actions chosen by RAHBO (Algorithm 1) over T rounds. Set and according to Lemma 1 with , and . Then, the risk-averse cumulative regret of RAHBO is bounded as follows:

| (34) |

Proof. The main steps of our proof are as follows: In Step 1, we derive the upper and the lower confidence bounds, and , on at iteration . In Step 2, we bound the instantaneous risk-averse regret . In Step 3, we derive mutual information both for function and variance-proxy evaluations. In Step 4, we bound the sum of variances via mutual information. In Step 5, we bound the cumulative regret based on the previous steps.

Step 1: On confidence bounds for .

(i) On confidence bounds for . According to Eq. 33, with probability the following confidence bounds hold with set according to Lemma 1:

(ii) On confidence bounds for . Here we adapt confidence bounds introduced in Eq. 18-(19) since Eq. 5 relies on the unknown variance-proxy incorporated into . Conditioning on the event that is upper bounded by defined in (i), the confidence bounds for with probability are:

| (35) | |||

| (36) |

(iii) On confidence bounds for . Finally, combining (i) and (ii) and using the union bound, with probability , we get with

| (37) | |||

| (38) |

Step 2: On bounding the instantaneous regret.

First, we bound instantaneous regret of a single measurement at point , but with unknown variance-proxy as follows:

| (39) |

The second inequality is due to the acquisition algorithm. The last equality is due to the fact that by definition, as well as

Note that at each iteration we take measurements, hence the total number of measurements is . Thus, we can bound the cumulative regret by

| (40) |

Step 3: On bounding maximum information gain.

We follow the notion of information gain computed assuming that with (Eq. 12). Under the modelling assumptions , and

with variance-proxy , the information gain is:

| (41) |

We define the corresponding maximum information gain

| (42) |

Analogously, for with the posterior the information gain is defined as:

| (43) |

Then, the corresponding maximum information gain is as follows:

| (44) |

where is again a set of size with points .

Step 4: On bounding

and

We repeat the corresponding derivation for known , recalling that :

| (45) |

Here, the first inequality follows from Cauchy-Schwarz inequality and the fact that The latter holds by the definition of , particularly:

then and That implies

The second inequality in Eq. 45 is due to the fact that for any we can bound , that also holds for since for any

Similarly, we bound

| (46) |

in the above we define

Step 5: On bounding cumulative regret

Combining the above three steps together, we obtain with probability

| (47) |

A.5 Proof of Corollary 1.1

Corollary 1.1 Consider the setup of Theorem 1. Let denote actions selected by RAHBO over rounds. Then, with probability at least , the reported point where , achieves -accuracy, i.e., , after rounds.

Proof.

We select the maximizer of over the past points :

since adding a constant does not change the solution. We denote Then we obtain the following bound

| (48) |

In the above, the first inequality holds with high probability by definition , the second inequality is due to and therefore The third inequality holds since with high probability, and the fourth is due to for every , since is selected via Algorithm 1.

Recalling Eq. 47, note that the following bounds hold:

| (49) |

Combining the above Eq. 49 with Section A.5 we can get the following upper bound

Therefore, for samples with we finally obtain

∎

A.6 Experimental settings and extended results

Implementation and resources

We implemented all our experiments using Python and BoTorch [3].333https://botorch.org/ We ran our experiments on an Intel(R) Xeon(R) CPU E5-2699 v3 @ 2.30GHz machine.

A.6.1 Example function

We provide additional visualizations for the example sine function in Fig. 6. These examples demonstrate that exploration-exploitation trade-off (as in GP-UCB) might not be enough to prefer points with lower noise and GP-UCB might tend to acquire points with higher variance. In contrast, RAHBO, initialized with the same point, prefers points with lower risk inherited in noise.

A.6.2 Branin

We provide additional visualizations, experimental details and results. Firstly, we plot the noise-perturbed objective function in Fig. 7 in addition to the visualization in Fig. 1(c). In Fig. 8, we plot cumulative regret and simple mean-variance regrets that extends the results in Fig. 5(a) with RAHBO-US. The general setting is the same as described for Fig. 5(a): we use initial samples, repeat each evaluation times, and RAHBO-US additionally uses samples for learning the variance function with uncertainty sampling. During the optimization, RAHBO-US updates the GP model for variance function after every acquired point.

A.7 Random Forest tuning

Experiment motivation:

Consider the motivating example first: the optimized RF model will be exploited under the data drift over time, e.g., detecting fraud during a week. We are interested not only in high performance on average but also in low variance across the results. Particularly, the first can be a realization of the decent result in the first days and unacceptable result in the last days, and the latter ensures lower dispersion over the days while keeping a reasonable mean. In this case, when training an over-parametrized model that is prone to overfitting (to the training data), e.g., Random Forest (RF) with deep trees, high variance in validation error might be observed. In contrast, a model that is less prone to overfitting can result into a similar validation error with lower variance.

RF specifications:

We use scikit-learn implementation of RF. The RF search spaces for BO are listed in Table 1 and other parameters are the default provided by scikit-learn. 444https://scikit-learn.org/stable/modules/generated/sklearn.ensemble.RandomForestClassifier.html During BO, we transform the parameter space to the unit-cube space.

Dataset:

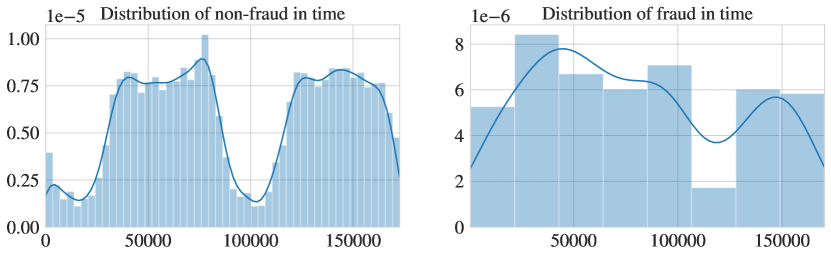

We tune RF on a dataset of fraudulent credit card transactions [23] originally announced for Kaggle competition.555https://www.kaggle.com/mlg-ulb/creditcardfraud It is a highly imbalanced dataset that consists of 285k transactions and only 0.2% are fraud examples. The transactions occurred in two days and each has a time feature that contains the seconds elapsed between each transaction and the first transaction in the dataset. We use the time feature to split the data into train and validation sets such that validation transactions happen later than the training ones. The distribution of the fraud and non-fraud transactions in time is presented in Fig. 9.

In BO, we collect evaluation in the following way: we fix the training data to be the first half of the transactions, and the rest we split into 5 validation folds that are consecutive in time. The RF model is then trained on the fixed training set, and evaluated on the validations sets. We use a balanced accuracy score that takes imbalance in the data into account.

task hyperparameter search space RandomForest n_estimators [, ] max_features [, ] max_depth [, ]

A.7.1 Tuning Swiss free-electron laser (SwissFEL)