Optimal pooling and distributed inference for the tail index and extreme quantiles

b Department of Decision Sciences, Bocconi University of Milan, via Roentgen 1, 20136 Milano, Italy

c Univ Rennes, Ensai, CNRS, CREST - UMR 9194, F-35000 Rennes, France)

Abstract

This paper investigates pooling strategies for tail index and extreme quantile estimation from heavy-tailed data. To fully exploit the information contained in several samples, we present general weighted pooled Hill estimators of the tail index and weighted pooled Weissman estimators of extreme quantiles calculated through a nonstandard geometric averaging scheme. We develop their large-sample asymptotic theory across a fixed number of samples, covering the general framework of heterogeneous sample sizes with different and asymptotically dependent distributions. Our results include optimal choices of pooling weights based on asymptotic variance and MSE minimization. In the important application of distributed inference, we prove that the variance-optimal distributed estimators are asymptotically equivalent to the benchmark Hill and Weissman estimators based on the unfeasible combination of subsamples, while the AMSE-optimal distributed estimators enjoy a smaller AMSE than the benchmarks in the case of large bias. We consider additional scenarios where the number of subsamples grows with the total sample size and effective subsample sizes can be low. We extend our methodology to handle serial dependence and the presence of covariates. Simulations confirm that our pooled estimators perform virtually as well as the benchmark estimators. Two applications to real weather and insurance data are showcased.

MSC 2010 subject classifications: 62G32, 62G30, 62F10, 62F12

Keywords: Extreme quantiles, heavy tails, distributed inference, pooling, tail index, testing

1 Introduction

The contemporary problem of efficient analysis of massive data has led to the development of the divide-and-conquer approach, which consists in dividing data into multiple samples that can be processed across several machines, before combining the results from subsamples on a central machine by making use of pooling techniques. In statistics, this strategy gives rise to distributed inference from many datasets, allowing to alleviate the computational challenges and constraints in storage imposed by the availability of extremely large datasets, or to handle data privacy issues as in banking and insurance. Pioneering contributions in the distributed framework focused on the regression mean and central parameters. In the last three years, distributed inferential procedures have been also developed for quantile estimation, mainly in a regression setup. Prominent among these contributions are Volgushev et al. (2019), Xu et al. (2020), and Wang and Ma (2021). The analyses therein concentrate on the statistical inference of ordinary conditional quantiles at fixed tail probability levels.

The estimation of extreme quantiles in a distributed computing setting, when their order tends to 1 as the total sample size goes to infinity, has not yet received any attention, however. More generally, distributed inference for tail quantities from the perspective of extreme value theory is still in its infancy. To the best of our knowledge, only tail index estimation has been recently explored in Chen et al. (2021) by taking a simple average of subsample tail index estimators as the final distributed estimator. From a broader perspective, the use of machine learning methods for extreme value analysis has started only very recently with, e.g., Ahmed et al. (2021) for extreme value statistics in semi-supervised models, Velthoen et al. (2021) for a gradient boosting procedure to estimate extreme conditional quantiles, and Aghbalou et al. (2021) for dimension reduction based on tail inverse regression.

In this article we go further than Chen et al. (2021) by addressing several important questions about distributed inference for the tail index, but also for extreme quantiles of heavy-tailed data. Our approach is based on the use of a general terminology and theory of pooling that encompasses distributed estimation from different samples whose distributions have a common target parameter, given in our setup by the tail index or an extreme quantile. Instead of naively averaging the estimators calculated from the available subsamples, it is of interest, both from a theoretical and a practical perspective, to construct a general class of weighted pooled estimators and to establish a fully data-driven inferential procedure integrating the optimal choice of weights. In particular, our overarching goal is to develop the asymptotic theory of the optimally pooled tail index and extreme quantile estimators, under weak technical conditions, covering both scenarios where the number of available subsamples is bounded or growing with the total sample size, as well as the general situation where the observed data can be dependent within and/or across subsamples. The pooling approach itself has a rich history dating back to Cochran (1937) for the estimation of the common mean of several samples. It is also encountered in the econometrics of panel data since the influential work of Theil (1954) and Zellner (1962). The idea of combining pooling and extreme value techniques has originally been suggested by Kinsvater et al. (2016), Asadi et al. (2018), and Vignotto et al. (2021) in climate science problems.

The first contribution of this paper is a joint asymptotic normality result for Hill estimators (Hill, 1975) calculated from a fixed number of samples with heavy-tailed data. In particular, we allow for different sample sizes, effective sample sizes, marginal distributions, and for dependence across samples. We apply this general result to design optimal pooling strategies of subsample Hill estimators for tail index estimation. We consider optimal weights that minimize either the asymptotic variance or the Asymptotic Mean Squared Error (AMSE) of the pooled estimator. These developments rely on a very general theory that we derive for a generic weighted pooled estimator built from subsample estimators for a common unknown parameter. This theory comes into play when the subsample estimators are jointly asymptotically normal, and can be biased and correlated. To the best of our knowledge, no such unrestricted approach has been fully investigated. We also construct bias-reduced versions of the proposed pooled tail index estimators. Then we discuss the problem of ultimate interest in extreme value analysis, which lies in estimating extreme quantiles either locally in each machine in the tail homogeneous setting of equal marginal tail indices, where tail quantiles are possibly only asymptotically proportional across subsamples, or globally by pooling subsample extreme quantile Weissman estimators (Weissman, 1978) in the more restrictive tail homoskedastic setting of asymptotically equivalent marginal tail quantiles. Our approach in both cases relies on a specific weighted geometric pooling scheme, particularly relevant for extreme quantiles, as opposed to arithmetic averaging naturally used for pooling ordinary quantiles (Knight and Bassett, 2003). Moreover, we explore inferential aspects of pooling for extreme values by constructing likelihood ratio-type tests for either tail homogeneity or tail homoskedasticity, as well as asymptotic confidence intervals for the tail index and extreme quantiles.

We also specialize the discussion to distributed inference as an important application of our general theory. In this particular case, due to computational costs or privacy restrictions, the data in sample number can only be processed by the th machine, with very restricted or no communication allowed between the machines, before an end user operating from a central machine conducts distributed inference from limited information transmitted by each machine. It is also assumed that the data is independent and identically distributed (i.i.d.) within and across machines. Under this setup, we examine and compare the asymptotic theory of the distributed tail index and extreme quantile estimators to the behavior of their respective benchmark Hill and Weissman estimators based on the unfeasible direct combination of subsamples. We extend this theory further by considering first the case when effective sample sizes are highly unbalanced among machines, and then the case of a growing number of machines with the total sample size . Finally, we tackle the problem of serial dependence within the data in the presence of covariates, showing how appropriately filtering the observations allows to recover the asymptotic theory from independent observations.

What first distinguishes our contribution relative to earlier literature, and in particular to Chen et al. (2021) for tail index estimation, is that a detailed study is conducted for the case of a fixed number of subsamples with different sample sizes. These considerations are motivated by practical concerns. For example, the financial application in Chen et al. (2021) itself requires the rather small value and a ratio between lowest and highest subsample sizes roughly equal to , whereas their theory only considers the case as , with equal subsample sizes. We allow for general choices of weights in the pooling scheme, we construct bias-reduced versions of our pooled estimators, and we design inference procedures under very weak conditions that hold for any reasonable heavy-tailed model. We construct asymptotic variance-optimal and AMSE-optimal estimators, with meaningful comparisons between these optimally pooled estimators and the unfeasible benchmark Hill estimator. We revisit the case by providing, unlike Chen et al. (2021), a unified convergence result for tail index estimation that handles both bounded and unbounded effective sample sizes in the marginal Hill estimators. In particular, we carefully derive the correct expression of the asymptotic variance for the distributed Hill estimator, which should be different from the expression provided by Chen et al. (2021) in the case of unbalanced effective sample sizes. Moreover, this is the first work to implement the idea of geometric weighted extreme quantile pooling; our experience with simulated and real data indicates the superiority of the corresponding estimators over the arithmetically pooled competitors that suffer from substantially larger bias and variance.

The paper is organized as follows. Section 2 develops our general pooling theory for tail index and extreme quantile estimation, while Section 3 focuses on the special framework of distributed inference. Section 4 extends our methodology to handle serial dependence and the presence of covariates through filtering. Section 5 illustrates the usefulness of the proposed extreme value pooling and distributed inference methods through a simulation study and concrete applications to weather and insurance data. The supplement to this article contains additional theoretical results and all the proofs, with further details on our simulation study. Our methods and data have been incorporated into the open-source R package ExtremeRisks.

2 Pooling extreme value estimators

2.1 Pooled Hill estimators of the tail index

Let denote an dimensional random vector, and () denote independent copies of . We assume that the available data consists of the , for and , with being the total number of univariate data points available across all samples. We suppose that as . Table 1 provides a simple representation of the available data when .

| Vector | Available data | ||||||||

|---|---|---|---|---|---|---|---|---|---|

We focus on the general framework where the components of the random vector have continuous, right heavy-tailed distribution functions , with associated survival functions and tail quantile functions that satisfy For any , the function satisfies the second-order condition: is second-order regularly varying in a neighborhood of with index , second-order parameter and an auxiliary function having constant sign and converging to 0 at infinity, that is,

where the right-hand side should be read as when . In this condition is regularly varying with index (by Theorems 2.3.3 and 2.3.9 in de Haan and Ferreira, 2006), meaning that the larger is, the smaller the error in the approximation of the right tail of by a purely Pareto tail will be. All usual heavy-tailed distributions satisfy these conditions, see Table 2.1 in p.59 of Beirlant et al. (2004) for a detailed list of examples.

To incorporate the dependence between samples into the inference procedure, we assume an appropriate pairwise tail dependence structure based on the functions , for that are essentially the bivariate survival copulae of , namely: For any with , there is a function on such that

This condition imposes the existence of a limiting dependence structure in the joint right tail of and , given by the tail copula (see Schmidt and Stadtmüller (2006)). It can be viewed as a minimal assumption when it comes to assessing the dependence structure between extreme value estimators.

After ordering the data in the th sample as , (the notation is inspired by David and Nagaraja (2003)), we introduce the marginal Hill estimators which involve the top highest order statistics in each sample, for . The integer is the effective sample size in sample , and we set to be the total effective sample size in the vector of estimators . Our ultimate interest is in the case where the are equal to a common estimated by

The asymptotic distribution of any element within this class of estimators is stated in the following theorem, along with the joint asymptotic normality of , for .

Theorem 1.

Assume that conditions and hold. Suppose, without loss of generality, that , and then that with , , (with and ) and for any , as . Let the weight vector be such that and define a vector and symmetric matrix by

Then In particular, if , then

| with | |||

| and |

The matrix is positive definite if and only if is so, and hence we have the following results on optimal weights:

-

1.

(Variance-optimal weights) There is a unique solution to the minimization problem of subject to the constraint , which is

-

2.

(AMSE-optimal weights) There is a unique solution to the minimization problem of subject to the constraint , which is

The optimal value of is

Finally, if with , then the composite estimator is asymptotically equivalent to in the sense that .

The proof requires applying a very general pooling result in conjunction with the assumption that the sample sizes are asymptotically proportional (possibly unbalanced) and so are the effective sample sizes . This ensures that none of the imposes its limiting distribution to the others.

Remark 1 (Bias components across samples).

The structure of the asymptotic bias component is constrained by the second-order parameters : for all its components to be non-zero, the should be equal, because of the proportionality assumption on the ’s and the ’s with the fact that the functions are regularly varying with index . More specifically, if , then the th component of is 0 whenever . In the important special context of distributed inference (see Section 3), where all marginal distributions are the same, an asymptotic bias component will be present in every marginal.

2.2 Optimal choices of weights

The idea now is to use the pooled estimator in conjunction with the optimal choices of the weight vector . Since the resulting optimal values of weights depend on the asymptotic bias and variance components in view of Theorem 1, they should be estimated first. One convenient way of estimating the bias component, which hinges on and , is by assuming for some constant . Most commonly used heavy-tailed models satisfy this mild proportionality condition between and , see Table 1 in Girard et al. (2021b). Under this assumption, consistent estimators and of and are available and implemented in open-source software, for example in the R function mop from the package evt0. This yields an estimator of as Here the choice of in the estimator is arbitrary; for example, without any prior knowledge of the dependence structure, the naive weights seem reasonable.

Now, to estimate the covariance matrix, let and if and otherwise, and consider the estimator of the tail copula function defined as

[Here (resp. ) stands for the rank of (resp. ) among the observations (resp. ), namely, the first observations in sample (resp. ).] This is a modified version of the empirical upper tail copula in Equation (13) of Schmidt and Stadtmüller (2006). Adapting Lemma 7 from Stupfler (2019) shows that it is a locally uniformly consistent estimator of on under our technical conditions. Combining these tools, we arrive at the estimators

| and |

According to Theorem 1, the vectors of variance-optimal weights and AMSE-optimal weights can then be estimated by

Next, we provide the asymptotic properties of the composite pooled estimators based on these estimated optimal values of weights.

Corollary 1.

Work under the conditions of Theorem 1 with , , and for all . Assume that the matrix is positive definite (hence is). Assume further that, for all , is a consistent estimator of and . Then

Remark 2 (On the variance- and AMSE-optimal choices).

This is the first work to implement the idea of AMSE-optimal weights which should be favored in practice when the estimation bias is large enough, especially in the case of unequal sample fractions , as demonstrated below in Section 3.2 in the distributed inference framework. The solution using variance-optimal weights was actually suggested by Kinsvater et al. (2016), but their analog of Theorem 1 requires much stronger technical conditions. Besides, the use of their estimator for lacks a theoretical justification similar to Corollary 1. A different, variance-optimal convex combination (with nonnegative weights) is advocated in Dematteo and Clémençon (2016), also under much stronger technical conditions. Their solution does not coincide with ours in general, although this is not so clear-cut in the specific case of identical effective sample sizes. In this situation, at least when , the variance-optimal set of weights we propose is in fact a convex combination. For , a direct calculation provides irrespective of , corresponding to the naive average. For , the discussion is more complex and involves the identification of tail correlation matrices with a convex polytope that is a proper subset of the elliptope, a Riemannian quotient manifold representing the set of standard correlation matrices. As a consequence, pooling together Hill estimators with equal effective sample size can never outperform, in terms of asymptotic variance, a Hill estimator built from a pooled sample of independent data of equivalent total size. This would not necessarily be the case in general pooling problems, e.g., for positively correlated sample means. What can happen in the case remains unclear.

We conclude this section by discussing bias-reduced versions of the variance-optimal and AMSE-optimal pooled estimators, defined as

Corollary 2.

Under the conditions of Corollary 1, and

If the marginal distributions are equal across samples, then one can improve the estimation of the weights by pooling the second-order parameter estimators themselves. We shall explore this possibility in Section 3.2.

2.3 Weighted geometric pooling of extreme quantile estimators

We turn to extreme quantile estimation for a very small exceedance probability as . In each sample, we estimate by the extrapolated Weissman estimator of Weissman (1978):

where satisfies . The typical case is when is bounded, reflecting the challenging problem of estimating quantiles in the far tail where only a few or no observations are available in the neighborhood of . When the samples are believed or known to have the same tail index , it is natural to harness the power of pooling by substituting the weighted estimator in place of the individual estimator , to get

This improves on the traditional Weissman estimator in each sample by borrowing statistical strength across all samples. Going one step further, the marginal quantile estimators themselves can be pooled to gain more insight when the datasets have the same extreme quantiles, or equivalently, if one assumes that For any with , we have as . The validity of this assumption can be tested by applying the test of Padoan and Stupfler (2021) described in their Sections 3.3 and 5. Under assumption , the quantiles are all asymptotically equivalent and hence the estimators all estimate the same quantity. A straightforward way of combining these individual extreme quantile estimators would be to take again a weighted sum, as . This is most efficient when estimating central quantiles, see for example Knight and Bassett (2003). However, it is no longer the best possible solution when it comes to pooling the Weissman estimators, because the use of geometric weighted sums better suits the multiplicative and power structure of these extrapolated estimators (see Sections 5.1.1 for numerical evidence). The crucial point to note here is that the log-Weissman quantile estimator can be rewritten as

In the first term, which dominates since , the estimator now appears on the standard scale. This suggests the use of or, in other words,

This estimator is a weighted geometric (rather than arithmetic) mean of the . We conclude this discussion by deriving the asymptotic normality of and .

Theorem 2.

Work under the conditions and with the notation of Theorem 1 with and for all . Pick such that and as . Let be such that and . Then, for any ,

If moreover assumption holds then, for any ,

An analogue of Theorem 2 is feasible for optimally-pooled extreme quantile estimation where , since the asymptotic distribution of is governed by that of . Similar results can also be established when is replaced by the bias-reduced versions and , so they are omitted.

2.4 Inference using pooled extreme value estimators

Unless there are strong reasons to believe in the equality of tail indices (as is the case in the distributed inference setup of Section 3), it is crucial to justify this assumption by performing a statistical test before applying our pooled estimators. To do so, we briefly present here an approach motivated by testing for nested models. Suppose that is an dimensional Gaussian random vector with mean and known positive definite covariance matrix , and consider the testing problem of versus based on . The log-likelihood ratio deviance statistic for testing the validity of model is , with . In model , the statistic has a chi-square distribution with degrees of freedom. In our context, under the assumptions of Theorem 1 and if all the are 0 (see Remark 4 below for more discussion on this assumption), one has

| with |

This can be formulated by the approximation of the distribution of by the distribution. Given the estimator

one can obtain a deviance statistic for testing versus as

Therefore the test statistic compares the vector of estimates with an estimate of the variance-optimal pooled estimator on a scale adapted to the amount of dependence existing between the extremes of the vector . A somewhat different proposal, not motivated by a likelihood ratio test in nested models, is outlined in Kinsvater et al. (2016).

Our testing procedure, of asymptotic size , is to reject if , where is the th quantile of the chi-square distribution with degrees of freedom. The next corollary establishes the consistency of this test and gives a symmetric asymptotic confidence interval for the common tail index under .

Corollary 3.

Remark 3 (With asymptotic independence across subsamples).

An important subcase in practice is when pairs of data points taken from two different subsamples are asymptotically independent. This covers, for example, the distributed inference situation which will be discussed in Section 3. In this case, all tail copulae are identically zero, so one can estimate with . The test statistic becomes

This has the familiar look of a Pearson goodness-of-fit statistic, with the weight adjusting for the different rates of convergence of the . If all the are equal, then

In this setup, our proposed statistic bears some similarity with a test statistic studied in Einmahl et al. (2020) in the context of testing for the validity of a multivariate regular variation model that assumes equality of tail indices across marginal distributions.

Remark 4 (Inference and bias correction).

Typically, assuming to omit the asymptotic bias terms is sensible as long as the second-order parameters remain reasonably far away from 0. Based on finite-sample experiments with a total sample size , marginal Burr distributions and with both balanced and unbalanced samples, the confidence interval provided seems to perform very well when . Estimating the bias terms then is in fact detrimental, because of increased variability of the resulting interval estimator that is not accounted for in the estimated variance.

Remark 5 (Tail homogeneity and tail homoskedasticity).

When all the parameters are negative, as in Corollary 3, one has as , see the equation below Equation (2.3.23) in de Haan and Ferreira (2006). Testing versus is then exactly equivalent to testing

The testing procedure based on the statistic is therefore, under very mild conditions, exactly a test for asymptotic proportionality of marginal extreme quantiles. It can thus be used to detect tail homogeneity (equal tail indices and therefore asymptotically proportional tail quantiles) as opposed to tail heterogeneity (one marginal distribution having a heavier tail than the others). We discuss below the testing of the stronger property when all limits are equal to 1 in , corresponding to the asymptotic equivalence of extreme quantiles , and referred to as tail homoskedasticity.

Testing for tail homoskedasticity can be done directly using the Weissman estimators . Set and

A testing procedure of asymptotic size of versus

is to reject if . We establish this rigorously in our next result.

Corollary 4.

Under the conditions of Corollary 3 and for all , if is such that and as , then we have under , and as under . Moreover, under , if with then, for any and ,

The present test is more general than the one suggested in Section 3.3 of Padoan and Stupfler (2021), for which fairly strong integrability assumptions on the are unavoidable. The use of the log-scale is equivalent in theory to the relative scale employed in Theorem 2, but it tends to provide more accurate asymptotic confidence intervals for extreme quantiles, as indicated by e.g. Drees (2003).

3 The framework of distributed inference

Our general pooling theory naturally applies to the context of distributed inference. A restriction in this framework is that the individual data points cannot be processed with a standalone machine and very restricted or no communication is allowed between the machines. In particular, the end user operating from a central machine only has access to limited information, such as the subsample estimates and associated and , which is not sufficient for estimating the tail dependence structure between the different subsamples. We thus make the assumption that the data within and across machines are independent, that is, the are i.i.d. for and , with a common distribution satisfying the second-order condition .

3.1 Distributed estimation of the tail index

When the data are i.i.d., an obvious benchmark for the distributed estimator is the Hill estimator based on the unfeasible combination (due to computational or storage difficulties) of subsamples with effective sample size , that is, where are the order statistics of the random variables . Assume, as in Section 2.1, that the and the are asymptotically proportional but possibly unbalanced, i.e. and . Then, since is regularly varying with index , it is straightforward to show that the existence of , for any , is equivalent to the existence of , and that

Hence, we have the following corollary of Theorem 1.

Corollary 5.

Assume that condition holds. Suppose that and (with then ) for any , and then that with and , as . Let be such that . Then

where . If and then and so the above convergence remains valid for .

3.2 Variance-optimal and AMSE-optimal combinations

It is immediate that the variance-optimal weights are for all . Estimating by leads to the estimated weight vector . The variance-optimal distributed estimator is therefore a very convenient convex combination that has a much simpler expression than in the general setup of Section 2, due to the constraint of data independence across machines. Calculating this estimator only requires reporting each individual and to the central machine. Being a nonrandom convex combination, this estimator is immune to the instability issues caused by possible inaccurate estimation of optimal weights.nThe following result gives its asymptotic distribution.

Corollary 6.

Under the conditions and notation of Corollary 5,

Remark 6 (Asymptotic bias comparison).

The unfeasible Hill estimator has asymptotic bias . If and denotes the asymptotic bias of , then clearly when . Otherwise, the Hölder inequality for the conjugate exponents and provides . Equality holds if and only if , a constant independent of , i.e. . In other words, with equality if and only if either or for any , meaning that the sample fraction in each machine should be (asymptotically) the same for asymptotic bias equality to hold.

Theorem 3.

Under the conditions of Corollary 6 with , if and only if or for any . If moreover for any , we have in fact

This result states that adjusting the effective sample sizes such that is constant across machines produces a variance-optimal distributed estimator that is asymptotically equivalent to the unfeasible Hill estimator built from the combined subsamples. This is much stronger than only sharing the same asymptotic distribution, referred to as the oracle property by Chen et al. (2021) for the naive distributed estimator in the case (compare also with the results of Section 3.5). In the particular sector of insurance, according to Supplement B in Chen et al. (2021), insurance companies may be willing to communicate and might effectively use the same sample fraction. Yet, it is unlikely that such an adjustment can be performed in other sectors of activity, since each machine will pick its own following an appropriate selection rule based only on its subsample.

This difficulty with variance-optimal pooling motivates the focus on AMSE-optimal pooling in the frequent case of unequal sample fractions . The following result compares the resulting AMSE-optimal distributed estimator with the benchmark Hill estimator.

Theorem 4.

Under the conditions and notation of Corollary 5, set

Assume that the are not all equal to 1. Then if and only if , with

In the general situation where the marginal Hill estimators have unequal sample fractions , it is remarkable that the AMSE-optimal distributed estimator can actually have a smaller AMSE than the benchmark Hill estimator itself under the necessary and sufficient condition that the bias component is sufficiently large, as will be illustrated in Section 5.1.2. It should also be noted that Theorem 4 does not violate the minimax optimality property of the (benchmark) Hill estimator proved in Drees (1998) since it only states that the AMSE-optimal pooled estimator performs better than the Hill estimator within a certain class of heavy-tailed distributions.

To estimate the AMSE-optimal weights in this distributed inference context, we assume as in Section 2.2 that and note that

The estimators and in Section 2.2 of the second-order parameters and are restricted to each machine separately. We improve on these marginal estimators by using here the pooled versions and , which in turn leads to the bias component estimator where , and are three possibly random sets of weights. An obvious choice is for all three estimators. A more refined choice is variance-optimal weights for and for both and (recall that and use almost all the available observations in each machine). Set then

and define by replacing and in with and . We obtain the following result as an immediate consequence of Corollary 5.

Corollary 7.

Work under the conditions of Corollary 5 with and . Assume that, for all , is a consistent estimator of and . Then

A confidence interval based on this AMSE-optimal estimator (or on the variance-optimal estimator) can then be constructed exactly as in Section 2.4, and so we omit the details for the sake of brevity. This construction requires the knowledge of , , , that each individual machine has to communicate to the central machine.

We conclude this section by making use of the distributed inference-specific bias component estimator to define the following bias-reduced versions for both the variance- and AMSE-optimal pooled estimators and derive their asymptotic distributions:

Corollary 8.

Under the conditions of Corollary 7, and

3.3 Extreme quantile estimation

We are now ready to compare the weighted geometric distributed estimator of an extreme quantile , as well as its variance- and AMSE-optimal versions, to the classical unfeasible Weissman estimator obtained directly from the combined subsamples, each defined as

Corollary 9.

Work under the conditions of Corollary 5 with . Pick such that and , as . Let be such that and . Then

If moreover for any , then is asymptotically equivalent to . Finally, if the are not all equal to 1, then under the conditions of Corollary 7, has a smaller AMSE than if and only if , with the notation of Theorem 4.

3.4 Extension to the case of at least one, but not all, very low

It may happen that the ratio is quite large, owing to uncertainty in data-driven selection rules. One may then want to simply discard the marginal estimates with a very low from the pooling procedure, but these estimates will have very low bias if all machines have comparable sample sizes, and hence it is more sensible to incorporate them into the distributed estimators of the tail index and extreme quantiles. From an asymptotic point of view, we obtain the following result for the variance-optimal distributed estimators in this situation of extremely unbalanced effective sample sizes.

Theorem 5.

Assume that condition holds. Suppose that there is such that on the one hand, for any , with , and (with then ), and as ; and on the other hand, for any , is a nondecreasing sequence with , as and . Then, if and ,

If moreover and is such that and ,

| (1) |

as , then

The variance-optimal distributed estimators therefore possess, under suitable conditions, the same asymptotic properties as if they were calculated without incorporating the machines using a very low into the pooling procedure. Note that the first part of condition (1) automatically holds if in addition for any , and the second part of the condition on is obviously satisfied if, for any , is bounded. Bias reduction can be similarly carried out by focusing only on the machines having a large , so we omit the details for the sake of brevity.

3.5 The case of a large number of machines

Our results above do not consider the case when all the are low, possibly even bounded, whose treatment is substantially different. When all the are bounded in , consistency of the distributed estimators necessarily requires a growing number of machines with , namely . Otherwise, when is fixed, the pooled estimators will contain only a bounded number of summands. In this context, we require the following fundamental assumption. and the satisfy as . This condition means that the amount of data stored in each machine grows with , although the number of machines itself may grow at a much faster rate than the . While the condition ensures consistency, the condition is required to establish a precise control of the statistical errors arising in each machine. The proof is in this regard fundamentally different from the proofs of our theorems in the case of a fixed . Another important difference is that the weight vector now implicitly varies with , so restrictions are needed to define a class of admissible weights. For example, the pooled estimator corresponding to the weight is simply , which is not consistent when is bounded. We thus introduce a balanced allocation condition on . The weight vector satisfies as well as

This condition forbids from having constant components (with respect to ), meaning that the weight should be roughly evenly spread out across machines. It also prevents from taking very large values despite summing up to 1, which corresponds to a stabilization condition. Any weight vector satisfying , for all , will automatically fulfill . This encompasses the naive pooled estimator of , studied in Chen et al. (2021). The distributed estimator has the following asymptotic properties.

Theorem 6.

Under the conditions , and , if as and , then

Here denotes Euler’s Gamma function. If also as , then

[Note that necessarily by the Cauchy-Schwarz inequality.]

Remark 7 (Comparison with previous results for fixed ).

It is interesting to note that the asymptotic variance in Theorem 6 in fact matches the asymptotic variance in the case of fixed in Corollary 5, where the asymptotic variance is multiplied by

because . In the case , the right-hand side is nothing but . By contrast, the asymptotic bias term is substantially different.

Remark 8 (Comparison with Chen et al. (2021)).

Theorem 6 revisits and generalizes Theorems 1, 2 and 3 of Chen et al. (2021) in different directions: we deal with generic weighted distributed estimation instead of a naive pooling, we unravel not only the case of unbounded but also bounded (possibly unbalanced) in a single unified result, we handle the more realistic case of unbalanced sample sizes , all of this under the natural weaker version of Condition A in Chen et al. (2021). We also remark that the asymptotic variance obtained in Theorem 2 of Chen et al. (2021), with the naive weights for , is not correct. We fix the problem by proving that the asymptotic variance is in fact , where in general . This higher variance is not surprising because, in the case of unbalanced , machines with the lowest tend to provide less information than those with the largest , and therefore a loss of information should be expected in comparison with the case where all the are equal. This insight can be checked by considering, for example, a simple situation where is purely Pareto distributed with tail index , the number of machines is even, and for odd and for even. In this situation, each is in fact simply a sum of independent exponential random variables with mean and variance , and hence

This matches our result since and , so that . As such, the distributed Hill estimator with typically does not achieve the so-called “oracle property” claimed in Chen et al. (2021) even if or . In their terminology, this property holds when the distributed Hill estimator inherits the same speed of convergence and asymptotic distribution as the infeasible benchmark Hill estimator.

Remark 8 motivates the following corollary on the estimator with , which clearly satisfies condition .

Corollary 10.

Under conditions and , if as and , then

Therefore, as in the case of bounded , the distributed estimator with is asymptotically variance-optimal. It is this weighted estimator which possesses the “oracle property”.

We now turn to the asymptotic behavior of the geometrically weighted extreme quantile estimator . Perhaps surprisingly, this distributed estimator is in fact generally inconsistent when the are bounded, i.e. . The rationale is that, while the bias of the individual shape parameter estimators is small, and so averaging them out as creates a consistent estimator as the number of machines increases, the individual scale parameter estimators are fundamentally biased estimators of when is fixed. As such, the Weissman extrapolation of to the far tail in conjunction with can no longer be correctly applied. The workaround to ensure consistency of is to choose with as . With these growing , the distributed extreme quantile estimator is, as expected, consistent and asymptotically normal. These insights are summarized in the following result.

Theorem 7.

Work under the conditions of Theorem 6 with . Pick such that and as , and assume that

-

(i)

If the are bounded, i.e. , and for any , then does not converge to 1 in probability.

-

(ii)

If the are such that and as , then

Given that the are uniformly bounded, the assumption is exactly , which is guaranteed to hold in the typical case of interest in extreme value analysis. The extra assumption on the and compared to Theorem 6 ensures that the effective sample fractions are not too dissimilar across machines; it is satisfied if, for instance, . A weaker version of this condition already appears in Theorem 5.

4 Filtering to handle dependence and covariates

In practice, the data are often recorded with relevant covariates, or are stationary but weakly dependent in a way that can be modeled by a standard time series. Besides, when the share the same tail index, they typically have also asymptotically proportional extreme quantiles (see Remark 5). This suggests that can be modeled in many situations by a general location-scale model

| (2) |

where the unobserved noise vector has marginal tail quantile functions satisfying the conditions and , and its bivariate survival copulae satisfy . The functions and are unknown measurable functions of , for some . The covariates can be fully observed (in traditional regression settings) or partially or not at all observed (in a time series model which includes past unobserved innovations or volatility terms). The noise variable is assumed to be independent of . Let then the pairs , , be part of a strictly stationary sequence such that for and . The are assumed to be independent copies of as above. A reasonable idea to eliminate the heteroskedasticity and dependence in the data is to first estimate the location and scale components and of the model (under suitable identifiability and regularity conditions), and then filter the data to obtain residuals close to the unobserved errors . This results in residual-based Hill estimators These can be combined in a pooled version whose asymptotic normality can be proved under a high-level condition on the discrepancy between and .

Theorem 8.

Remark 9 (On the importance of filtering without pooling residuals).

One might argue that pooling directly the residuals themselves in a sample and applying the traditional Hill estimator may be more efficient. However, if the model is misspecified, heteroskedasticity could still remain in the residuals, and those with the largest scale might swamp the other residuals in the pooled sample, resulting thus in a large loss of estimation accuracy. Pooling the residual-based Hill estimates instead provides more protection against departures from the assumed location-scale model. Related points in the standard (non-pooling) context are discussed in Remarks 2 and 3 in Girard et al. (2021a).

The condition on the discrepancy between and in Theorem 8 is typically satisfied as soon as the location and scale components and are estimated at a faster rate than . This can easily be checked theoretically in a variety of regression models, see Girard et al. (2021a) for examples. The presence of the denominator in the condition makes it also possible to handle heteroskedasticity. The ultimate interest in conditional extreme value modeling under (2) is to estimate extreme th quantiles of given , defined as by location equivariance and positive homogeneity of quantiles, where is the quantile function of . Given consistent estimators of and of , and using the Weissman estimator of from the residuals , one can then estimate by

When satisfies the condition described in Section 2.3, all associated quantiles become asymptotically equivalent and can then be estimated by a geometrically pooled estimator, which leads to the following location-scale estimator of :

Our final asymptotic result establishes the asymptotic normality of these two estimators.

Theorem 9.

Work under the conditions of Theorem 8 with for all . Pick such that and as . Let be such that and . Finally, assume that the estimators and satisfy and . Then, for any ,

which converges weakly to . If moreover holds then, for any ,

5 Finite-sample study

5.1 Simulation experiments

We investigate the finite-sample performance of our proposed inferential methodology, first in the general pooling framework for heavy-tailed distributions (Section 2) and then in the distributed inference framework (Section 3). To save space we only report a brief description of our simulated models and conclusions.

5.1.1 General setup: Pooling for tail index and extreme quantile inference

Dimensions were considered, with balanced, weakly unbalanced and strongly unbalanced sample sizes. Our statistical models had either unit Fréchet or absolute Student- (i.e. the absolute value of a Student-) marginal distributions with 1 degree of freedom. The dependence structure between margins was given by four copulae: the Clayton and Gumbel (Archimedean) copulae, and the Gaussian and Student copulae. The Clayton and Gaussian copulae are cases of asymptotic independence, while the Gumbel and Student copulae are cases of asymptotic dependence. All marginal distributions had equal tail indices .

Our first experiment, for a total sample size of across all subsamples, compares four pooled tail index estimators (naive, variance-optimal, AMSE-optimal, and AMSE-optimal with pooled second-order estimates as in the comment below Corollary 2) with the benchmark Hill estimator applied to the pooled dataset on each of the aforementioned models. We also compare the related four geometrically pooled extreme quantile estimators at level with the naive arithmetic mean of the Weissman estimators in each subsample and the benchmark Weissman estimator applied to the pooled dataset. We compute Monte Carlo approximations of the Mean Squared Error (MSE) and of the actual coverage probability for the asymptotic confidence intervals with nominal level arising from our asymptotic theory, see Corollaries 3 and 4 for our proposed estimators; for the Hill (resp. Weissman) estimator, we assume that the asymptotic distribution is normal with mean 0 and variance (resp. ), see Theorem 3.2.5, p.74 in de Haan and Ferreira (2006) (resp. Theorem 4.3.8, p.138 therein). The variance-optimal and AMSE-optimal estimators outperform by far the naive pooling estimator on the basis of the MSE, when there is strong unbalance between sample sizes. Differences in performance get larger as the unbalance increases. They also perform comparably to the Hill estimator on pooled data. At the inferential level, confidence intervals deduced using the variance-optimal and AMSE-optimal estimators are typically substantially narrower than those provided using naive pooling. When there is asymptotic independence between samples, the pooling methods and the benchmarks on pooled data both provide confidence intervals having correct coverage. This is no longer the case when substantial dependence is present, with the confidence intervals constructed using the benchmark Hill estimator having actual coverage that can be as low as . Conclusions about extreme quantile estimation are similar, with the added fact that geometrically pooled estimators outperform by far the naive arithmetic mean of Weissman estimators.

5.1.2 Distributed inference of extreme values

In our second experiment, we assume that the marginal distributions are i.i.d. Fréchet, absolute Student- or Burr distributed, with tail index . We consider dimensions in balanced and highly unbalanced setups. We compared again the tail index and extreme quantile estimators described in Section 5.1.1. The results suggest that our proposed variance-optimal and AMSE-optimal methods (with pooled second-order estimates) perform comparably to the unfeasible Hill and Weissman estimators applied to the pooled dataset and outperform the naive distributed estimators, with shorter confidence intervals having correct coverage, and lower MSE. Geometric pooling is clearly beneficial as far as extreme quantile estimation is concerned. The gain of using our proposed distributed estimators increases as the unbalance between sample sizes increases. The AMSE-optimal distributed estimator is also overall the best when sample fractions are unequal and substantially different.

5.2 Data analysis

We discuss two concrete applications of our methodology to insurance and rainfall data.

5.2.1 Distributed inference for car insurance data

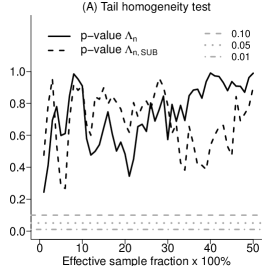

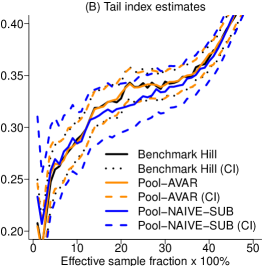

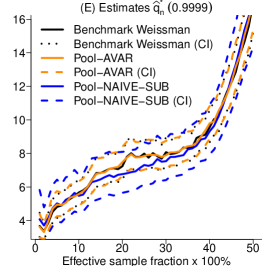

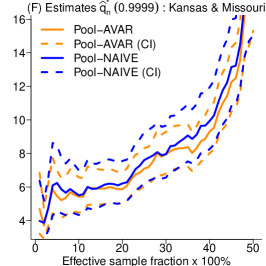

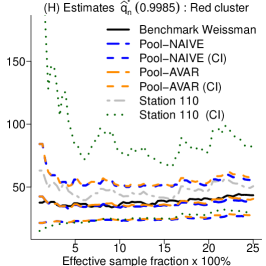

The first dataset comprises total claim amounts for car insurance companies in the five US states of Iowa (), Kansas (), Missouri (), Nebraska (), and Oklahoma () between January and February 2011, for a total sample size of . The choice of this dataset follows the same setup as in Chen et al. (2021) who assume that each company cannot share its data, making the calculation of Hill and Weissman estimates from pooled data inapplicable, but each company is willing to share its statistical analysis to enhance its appraisal of tail risk. Unlike Chen et al. (2021), however, our distributed inference method can handle the different subsample sizes and hence the full dataset, and allows to estimate extreme quantiles. Their analysis requires first a subsampling step to guarantee the same subsample sizes. We compare our results using the full data with those obtained from their method after subsampling at random 700 observations in each state, as described in Supplement B of Chen et al. (2021). As a benchmark, we use the hypothetical Hill and Weissman estimates, obtained directly from the combined data points. Results are given in Figure 1.

We first check the equality of tail indices by testing for tail homogeneity across the 5 states on full data and the subsampled data in each state, using the theory developed in Section 2.4 under the constraint of independence between subsamples (see Remark 3). From the p-values corresponding to our test statistic in Figure 1(A), we can comfortably conclude the equality of individual tail indices at the three significance levels and . It is remarkable that the p-values plot remains quite stable when moving from the full 5 samples of total size to the subsamples of total size . This indicates that the asymptotic chi-square regime is attained reasonably quickly.

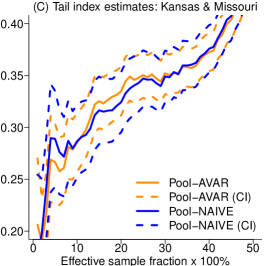

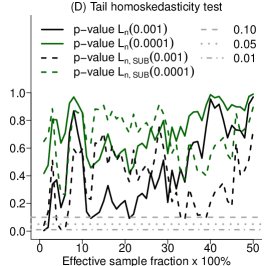

Figure 1(B) compares our variance-optimal distributed estimator , based on the full data, with the naive distributed estimator of Chen et al. (2021), which relies on the subsampled data, and with the benchmark Hill estimator along with their respective asymptotic confidence intervals. In contrast to the naive estimates and their associated confidence intervals, our optimal weighted estimates and their confidence intervals are, respectively, almost identical to the Hill estimates and their corresponding confidence intervals, as is to be expected from Theorem 3. Our variance-optimal confidence intervals are found to be around shorter than those of Chen et al. (2021). We arrive at a similar conclusion, in Figure 1(C), when restricting the analysis to the branches in Kansas and Missouri, whose subsample sizes and are strongly imbalanced, and using the full data from these states for both the variance-optimal and naive distributed estimates. Here, the variance-optimal confidence intervals are found to be roughly shorter than those relative to the naive estimator. The test theory of extreme quantile equivalence developed in Corollary 4 is implemented for the two extreme quantile levels and , resulting in the p-values from the test statistic displayed in Figure 1(D) for both full and subsampled data. The test overall allows to accept the assumption of tail homoskedasticity across states, with p-values getting higher as decreases. The rationale behind this behavior in this distributed setting is that, as extreme quantile levels increase, the shape of the approximating Pareto distribution gets more important relative to its scale. As such, because mere differences in scale can no longer be detected in the far tail as , the test actually becomes less powerful against the sub-alternative of proportional quantiles. Finally, the resulting variance-optimal distributed estimates and confidence intervals for extreme quantiles are found to be virtually indistinguishable from the ideal Weissman analogs, whereas they appreciably outperform the naive distributed competitors, as can be seen from Figure 1(E) and (F) for .

5.2.2 Pooling for regional inference on extreme rainfall

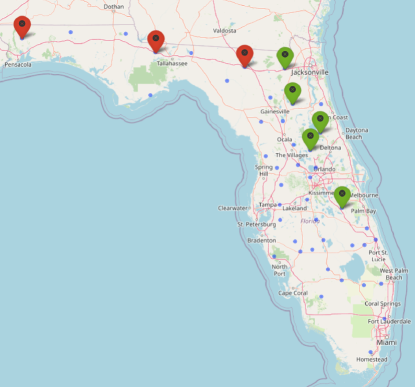

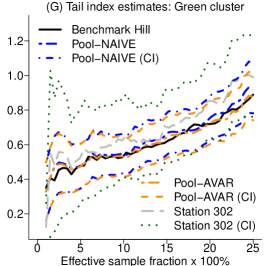

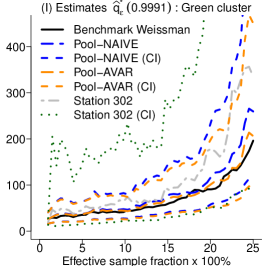

We explore regional inference on tail index and extreme quantiles of monthly rainfall in the state of Florida. An accurate assessment of these tail quantities is crucial for effective flood protection at minimal ecological damage and economic cost. Rainfall measurements are collected daily by the Florida Automated Weather Network at 49 gauge stations, over different periods between December 1997 and May 2021111See https://fawn.ifas.ufl.edu/data/fawnpub/.. We focus on the eight stations indicated with pin markers in the map in the top panel of Figure 2, whose aggregated monthly rainfall exhibit heavy-tailed distributions. The upper tail heaviness for each sample was ascertained in an exploratory analysis using moment and generalized Hill estimators (see e.g. Beirlant et al. (2004)). Individual sample sizes are rather short however, ranging from 172 to 281. The standard extreme value practice of individual extreme value inference will thus be subject to large uncertainty because of the limited amount of data at each site. By contrast, our optimal weighted pooling approach allows to reduce the uncertainty by borrowing tail information from homogeneous stations.

Our exploratory analysis shows first that the eight monthly time series are all stationary according to the classical KPSS and ADF tests. A first distinctive property is that the data for each station in the cluster of red pinned stations near the northern border of Florida are, in contrast to those in the green cluster close to the east coast, not autocorrelated according to the Ljung-Box test. The five time series in the green cluster of stations stretching along the east coast can be nicely fitted by simple seasonal ARMA models , where stands for a white noise process and denotes a constant, with , , and being respectively polynomials of degree in the lag operator and in . Following our theory in Section 4, the obtained residuals , for each station , are the basic tool for estimating tail indices. A second distinctive property is that the three stations in the red cluster have very similar Hill estimates between and , while the five stations in the green cluster also have similar Hill estimates between and , that are rather different from those in the red cluster.

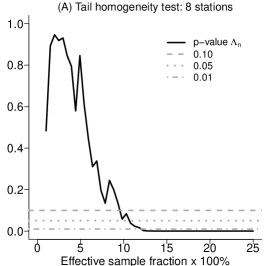

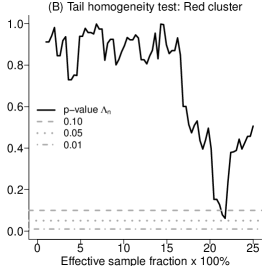

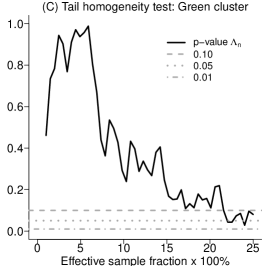

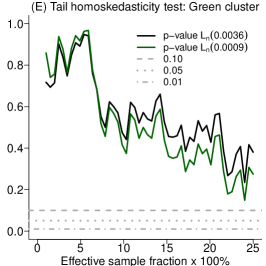

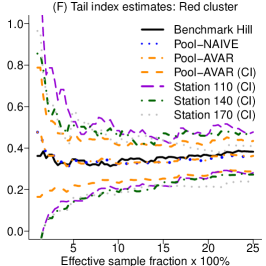

This motivates testing for equal tail indices in the separate red and green clusters of stations. First, that the eight stations do not have the same tail index is confirmed by the tail homogeneity test in Figure 2(A), where the plot of p-values from the test statistic becomes clearly very stable below the three significance levels and . By contrast, we can comfortably conclude the equality of tail indices in both red and green clusters from the tail homogeneity tests in Figure 2(B) and (C). This justifies the in-group tail homogeneity between the stations in each cluster besides their geographical proximity. Even more strongly, the tail homoskedasticity test implemented in Figure 2(D) and (E), for the two extreme quantile levels and , allows to accept the assumption of extreme quantile equivalence across stations in each cluster. Therefore, the Hill and Weissman estimators of the common tail index and extreme quantiles , respectively, could be directly calculated from the combined data in each cluster. However, it should be clear that the key question of inference based on these ideal estimators remains open in this particular application. Indeed, combining subsamples in each cluster of stations results in a single sample of asymptotically dependent (rainfall) data for which the asymptotic theory of both Hill and Weissman estimators is still unavailable in the extreme value literature. Our regional pooled estimators come with a satisfactory solution, reducing substantially the huge uncertainty inherent to local inference at each site, as can be seen from Figure 2(F)-(I). For the red cluster, Figure 2(F) shows that both naive and variance-optimal pooled estimators of are very close to the benchmark Hill estimator, while the asymptotic variance-optimal confidence intervals are quite stable and remarkably narrower relative to the Hill-based confidence intervals obtained individually from each subsample. We arrive at the same conclusion for the green cluster in Figure 2(G), where both pooling-type confidence intervals appear to be much tighter than the individual Hill-based confidence interval obtained from the largest subsample. Likewise, when estimating the extreme quantile of order , the individual Weissman-based confidence interval obtained from the largest subsample in Figure 2(H) and (I), for raw data in the red cluster and for residuals in the green cluster, tends to be unstable and twice as wide as our pooling confidence intervals, owing to the reduction of uncertainty in the latter. It is also worth noticing that the variance-optimal pooled estimator is closer to the benchmark Weissman estimator than the naive pooled competitor.

References

- Aghbalou et al. (2021) Aghbalou, A., F. Portier, A. Sabourin, and C. Zhou (2021). Tail inverse regression for dimension reduction with extreme response. arXiv:2108.01432.

- Ahmed et al. (2021) Ahmed, H., J. H. J. Einmahl, and C. Zhou (2021). Extreme value statistics in semi-supervised models. CentER Discussion Paper; Vol. 2021-007.

- Asadi et al. (2018) Asadi, P., S. Engelke, and A. C. Davison (2018). Optimal regionalization of extreme value distributions for flood estimation. Journal of Hydrology 556, 182–193.

- Beirlant et al. (2004) Beirlant, J., Y. Goegebeur, J. Segers, and J. L. Teugels (2004). Statistics of Extremes: Theory and Applications. Wiley.

- Chen et al. (2021) Chen, L., D. Li, and C. Zhou (2021). Distributed inference for the extreme value index. Biometrika, to appear.

- Cochran (1937) Cochran, W. G. (1937). Problems arising in the analysis of a series of similar experiments. Supplement to the Journal of the Royal Statistical Society 4, 102–118.

- David and Nagaraja (2003) David, H. A. and H. N. Nagaraja (2003). Order Statistics (Third edition). Wiley Series in Probability and Statistics.

- de Haan and Ferreira (2006) de Haan, L. and A. Ferreira (2006). Extreme Value Theory: An Introduction. Springer.

- Dematteo and Clémençon (2016) Dematteo, A. and S. Clémençon (2016). On tail index estimation based on multivariate data. Journal of Nonparametric Statistics 28, 152–176.

- Drees (1998) Drees, H. (1998). Optimal rates of convergence for estimates of the extreme value index. Annals of Statistics 26, 434–448.

- Drees (2003) Drees, H. (2003). Extreme quantile estimation for dependent data, with applications to finance. Bernoulli 9, 617–657.

- Einmahl et al. (2020) Einmahl, J. H. J., F. Yang, and C. Zhou (2020). Testing the multivariate regular variation model. Journal of Business & Economic Statistics, to appear.

- Girard et al. (2021a) Girard, S., G. Stupfler, and A. Usseglio-Carleve (2021a). Extreme conditional expectile estimation in heavy-tailed heteroscedastic regression models. Annals of Statistics, to appear.

- Girard et al. (2021b) Girard, S., G. Stupfler, and A. Usseglio-Carleve (2021b). On automatic bias reduction for extreme expectile estimation. https://hal.archives-ouvertes.fr/hal-03086048v2.

- Hill (1975) Hill, B. M. (1975). A simple general approach to inference about the tail of a distribution. Annals of Statistics 3, 1163–1174.

- Kinsvater et al. (2016) Kinsvater, P., R. Fried, and J. Lilienthal (2016). Regional extreme value index estimation and a test of tail homogeneity. Environmetrics 27, 103–115.

- Knight and Bassett (2003) Knight, K. and G. W. Bassett (2003). Second order improvements of sample quantiles using subsamples. Unpublished manuscript.

- Padoan and Stupfler (2021) Padoan, S. and G. Stupfler (2021). Joint inference on extreme expectiles for multivariate heavy-tailed distributions. Bernoulli, to appear. Available at https://hal.inria.fr/hal-02902667v2.

- Schmidt and Stadtmüller (2006) Schmidt, R. and U. Stadtmüller (2006). Non-parametric estimation of tail dependence. Scandinavian Journal of Statistics 33, 307–335.

- Stupfler (2019) Stupfler, G. (2019). On a relationship between randomly and non-randomly thresholded empirical average excesses for heavy tails. Extremes 22, 749–769.

- Theil (1954) Theil, H. (1954). Linear Aggregation of Economic Relations. North Holland Publishing Company, Amsterdam.

- Velthoen et al. (2021) Velthoen, J., C. Dombry, J.-J. Cai, and S. Engelke (2021). Gradient boosting for extreme quantile regression. arXiv:2103.00808.

- Vignotto et al. (2021) Vignotto, E., S. Engelke, and J. Zscheischler (2021). Clustering bivariate dependencies of compound precipitation and wind extremes over Great Britain and Ireland. Weather and Climate Extremes 32, 100318.

- Volgushev et al. (2019) Volgushev, S., S.-K. Chao, and G. Cheng (2019). Distributed inference for quantile regression processes. The Annals of Statistics 47, 1634–1662.

- Wang and Ma (2021) Wang, H. and Y. Ma (2021). Optimal subsampling for quantile regression in big data. Biometrika 108, 99–112.

- Weissman (1978) Weissman, I. (1978). Estimation of parameters and large quantiles based on the largest observations. Journal of the American Statistical Association 73, 812–815.

- Xu et al. (2020) Xu, Q., C. Cai, C. Jiang, F. Sun, and X. Huang (2020). Block average quantile regression for massive dataset. Statistical Papers 61, 141–165.

- Zellner (1962) Zellner, A. (1962). An efficient method of estimating seemingly unrelated regressions and tests for aggregation bias. Journal of the American Statistical Association 57, 348–368.