∗ Institute for Financial Mathematics and Applied Number Theory, University of Linz, AT-4040 Linz, Austria † Institute for Financial Mathematics and Applied Number Theory, University of Linz, AT-4040 Linz, Austria

Utility maximization in multivariate Volterra Models

Abstract.

This paper is concerned with portfolio selection for an investor with power utility in multi-asset financial markets in a rough stochastic environment. We investigate Merton’s portfolio problem for different multivariate Volterra models, covering the rough Heston model. First we consider a class of multivariate affine Volterra models introduced in [E. Abi Jaber et al., SIAM J. Financial Math., 12, 369–409, (2021)]. Based on the classical Wishart model described in [N. Bäuerle and Li, Z., J. Appl. Probab., 50, 1025–1043 (2013)], we then introduce a new matrix-valued stochastic volatility model, where the volatility is driven by a Volterra-Wishart process. Due to the non-Markovianity of the underlying processes, the classical stochastic control approach cannot be applied in these settings. To overcome this issue, we provide a verification argument using calculus of convolutions and resolvents. The resulting optimal strategy can then be expressed explicitly in terms of the solution of a multivariate Riccati-Volterra equation. We thus extend the results obtained by Han and Wong to the multivariate case, avoiding restrictions on the correlation structure linked to the martingale distortion transformation used in [B. Han and Wong, H. Y., Finance Res. Lett., 39 (2021)]. We also provide existence and uniqueness theorems for the occurring Volterra processes and illustrate our results with a numerical study.

2020 Mathematics Subject Classification:

93E20, 60G22, 49N90, 60H20- Key words :

-

stochastic control, utility maximization, rough volatility, Volterra-Wishart model, Riccati-Volterra equations, non-Markovian

1. Introduction

Since the observation was made that the paths of realized volatilities are rougher than established volatility models would suggest, cf. [17], there is a growing research interest in developing new models that better fit empirical data. In [19], the popular Heston model [18] was adapted to the rough volatility framework by using a fractional process with Hurst index as driver of the volatility process. A more general class of volatility models covering the rough Heston model in [19] is obtained by modelling the volatility process as a stochastic Volterra equation of convolution type [1, 20, 5]. Although most of the literature about rough volatility is concerned with option pricing, there are some recent works dealing with Merton portfolio optimization in such models. While [10] and [5] are dealing with the Markowitz portfolio problem, the Merton portfolio problem is studied in [6, 2, 9].

Merton’s portfolio problem aims at maximizing an investor’s utility from terminal wealth with respect to his utility function. The problem for the classical Heston stochastic volatility model was explicitly solved in [27], based on the represenation result of [4], and solutions for affine stochastic volatility models were derived in [30]. In [3], the Merton problem was studied for a multi-asset financial market where the volatility is modeled by a matrix-valued Wishart process, using stochastic control theory. In the rough framework it is no longer possible to apply the classical stochastic control approach deriving the corresponding Hamilton-Jacobi-Bellman equation, due to the non-markovianity of the rough volatility processes. In order to circumvent this problem, in [2], Bäuerle and Desmettre use a finite dimensional approximation of the volatility process in order to cast the problem back into the classical framework. However, this only yields explicit solutions in case that there is no correlation between stock and volatility. Han and Wong [9] overcome this difficulty using a martingale distortion Ansatz and applying the martingale optimality principle to obtain an explicit solution for the optimal investment strategy in a mono-asset Volterra Heston model. In order to take into account several important stylized facts about real financial markets such as choice among multiple assets, roughness of the volatility, correlation between different stocks and leverage effects, i.e. correlation between a stock and its volatility, multivariate rough volatility models have recently been developed (cf. [23], [24], [1]). In [5], Abi Jaber et al. study the Markowitz portfolio problem for a class of multivariate affine Volterra models, that features correlation between the stocks and between a stock and its volatility.

In this paper we solve the Merton portfolio problem for an investor with a power-utility function for different multivariate Volterra models including the rough Heston model. The outline of the paper is as follows: Section 2 gives an overview of the calculus of convolutions and resolvents which is needed throughout the paper. In Section 3 we introduce a class of multivariate affine Volterra models studied in [1] and [5]. For such a market model we consider two different approaches to solve the Merton portfolio problem. We first adapt the martingale distortion transformation used in [9] to the multivariate case. However, as it is pointed out in [5], this only works if the correlation structure is highly degenerate. Inspired by the techniques used in [3], we then provide a solution for the Merton portfolio problem for a more general correlation structure using calculus of convolutions and resolvents. In Section 4 we introduce a more general market model where the volatility is a matrix-valued stochastic process. In our model we adapt the Wishart stochastic volatility model studied in [26] and [3] to the Volterra framework, defining the variance-covariance matrix as the solution of a matrix-valued Volterra-Wishart equation, thus extending the Heston model. Considering a matrix-valued volatility process allows us to take into account correlation between different assets. Despite the non-Markovianity of these settings, the optimal strategy can be expressed explicitly in terms of the solution of a multivariate Riccati-Volterra equation. In Section 5 we illustrate our results with a numerical example. Section 6 provides existence and uniqueness results for the appearing Volterra equations even in the matrix-valued case. Auxiliary results and longer proofs can be found in the Appendix.

2. Convolutions and resolvents

In this section we give a short overview of some important definitions and results from the calculus of convolutions and resolvents, that we are going to use frequently throughout the paper. We start by defining three different types of convolutions:

Definition 2.1 (Convolution of two functions).

[1, Chapter 2] Let and be functions defined on . Then the convolution of and is defined as

| (2.1) |

whenever the above expressions are well-defined.

This definition can of course be extended to matrix-valued functions. In this case it is important that the dimensions of the matrices are compatible.

Definition 2.2 (Convolution of a measurable function and a measure).

[1, Chapter 2] Let be a measurable function on and be a measure on of locally bounded variation. Then the convolutions and are defined as

| (2.2) |

for all for which the above integrals exist.

Definition 2.3 (Convolution of a measurable function and a local martingale).

[1, Chapter 2] Let be a -dimensional continuous local martingale and be a function. Then the convolution is defined as

| (2.3) |

Remark 2.4.

The above convolution is well-defined as an Itô-integral for any satisfying

If and there is a locally bounded process such that then the convolution is well defined for all .

The following lemma shows that also this type of convolution is associative.

Lemma 2.5.

Another useful concept related to the integral kernel are so called resolvents. We distinguish between resolvents of the first and the second kind.

Definition 2.6.

Let and be a -valued measure on . Then is called the resolvent of the first kind of if

| (2.5) |

where is the -dimensional identity matrix.

Definition 2.7.

For a kernel , is called the resolvent of the second kind of if

| (2.6) |

The following table (cf. [1]) gives an overview of some kernels and their corresponding resolvents of the first and second kind.

| Type | |||

|---|---|---|---|

| Constant | |||

| Fractional | |||

| Exponential | |||

| Gamma |

For a more detailed discussion of the topic we refer to [14].

3. A class of multivariate affine Volterra models

To start our investigation, we use the affine Volterra model introduced in [5, Chapter 4]. Let with scalar kernels on the diagonal. In our model we consider stocks and we assume that the price of the th stock has dynamics

| (3.1) |

where is a -dimensional Brownian motion and . For and such that if , the volatility is defined as a Volterra square-root process

| (3.2) |

Here is a deterministic function and is a -dimensional Brownian motion for which the correlation structure with is given by

| (3.3) |

where is a -dimensional Brownian motion independent of and . In accordance with [5], we assume that there exists a continuous -valued weak solution to (3.1)-(3.2) on some filtered probability space , satisfying the usual conditions. A function is completely monotone on if it is infinitely differentiable on and for all and . Under the assumption that for each , is completely monotone on and that there exists and such that

| (3.4) |

the existence of a unique in law -valued continuous weak solution of equation (3.2) is ensured by [1, Theorem 6.1] in case that for some (cf. [5, Remark 4.1]). For a discussion about existence of a solution for more general input curves , see [16]. Note that condition (3.4) is fulfilled for constant, non-negative kernels, fractional kernels of the form with , and exponentially decaying kernels with . The existence of defined via equation (3.1) follows from that of .

3.1. The optimization problem

A portfolio strategy is an valued, progressively measurable process, where represents the proportion of wealth invested into stock at time . Under a fixed portfolio strategy, the wealth process has dynamic

| (3.5) |

where . By we denote the set of admissible portfolio strategies. The conditions under which we consider a strategy to be admissible will be specified later. We want to solve the Merton portfolio optimization problem for power utility, i.e. our aim is to find the value function such that

| (3.6) |

where is the conditional expectation given . The parameter represents the relative risk aversion of the investor. Smaller correspond to higher risk aversion. A portfolio strategy for which the supremum is attained is called an optimal strategy. Seen as an optimization problem with state process this problem is non-Markovian and the standard stochastic control approach cannot be applied.

3.2. The martingale distortion transformation

Consider a one-dimensional market model where the risky asset is given by

and is a markovian process defined via the SDE

where and have correlation . In this setup, a candidate for the value function

can be obtained by solving the corresponding Hamilton-Jacobi-Bellman equation. The distortion transformation introduced in [4] uses the Ansatz

where the constant is defined as . With this choice of , the quadratic terms in the HJB equation cancel out, leading to a linear PDE for

where the Sharpe ratio is defined as . By the Feynman-Kac Theorem, can be written as

where under the probability measure with Radon-Nikodym density

is a standard Brownian motion.

In [6] Fouque and Hu showed that if the Sharpe-ratio is bounded and has bounded derivative, then the value process can be expressed as , where

even if the volatility process is non-Markovian. This approach is called the martingale distortion transformation and was first introduced in the seminal paper [4] and later transferred to a non-Markovian setting in [12]. The extension to the multi-asset case is straight forward in the case of a bounded risk premium (cf. [6], Remark 2.5.).

3.3. The degenerate correlation case

In this section we present an extension of the proof of [9] to the multivariate case for a degenerate correlation structure, i.e. we assume that the correlation in (3.3) is of the form for . Note that since in our model the risk premium is unbounded, we can not apply the results of [6]. As in the one dimensional case, the Ansatz

is inspired by the martingale distortion transformation described in the previous section. Here we use the short notation for . Define the diagonal matrices , , and recall that . Under the new probability measure defined via the Radon-Nikodym density

together with the new standard brownian motion under

an application of the exponential-affine transform formula in [1, Theorem 4.3] yields

| (3.7) | ||||

where denotes the conditional -expected variance and solves the Ricatti-Volterra equation

with . Thus we obtain

In order to find the value function and the optimal strategy, we show that the family fulfills the martingale optimality principle (cf. [22, 13, 9]), i.e. we show that:

-

(a)

for all ;

-

(b)

is a constant independent of ;

-

(c)

is a supermartingale for all and there exists such that is a martingale.

A family of processes with the above properties can now be used to compare the expected utilities of an arbitrary strategy and the strategy :

Thus the strategy is indeed our desired optimal portfolio strategy.

Definition 3.1.

In the setting described above, we say that a portfolio strategy is admissible if

-

(a)

the SDE (3.5) for the wealth process has a unique solution in terms of ;

-

(b)

for all ;

-

(c)

a.s.

The main result we get for the degenerate correlation case is the following, our proof enhances the arguments of the proof of [9, Theorem 3.3] to the multi-dimensional case:

Theorem 3.2.

Let be invertible and let be the unique, continuous non-continuable solution of the Riccati-Volterra equation

| (3.8) |

| (3.9) |

on the interval , given by Theorem 6.2111More details on can be found in Section 6.2.. Then satisfies the martingale optimality principle for , and the optimal portfolio strategy is given by

| (3.10) |

Proof: We show that fulfills the martingale optimality principle. For the first condition, note that and hence . Since is a constant independent of , is also independent of and thus also the second condition is satisfied. In order to show that also the third condition is fulfilled, we apply Itô’s formula on . Using Lemma C.1, this yields

with

Note that and since is a quadratic function in and we have . Solving the stochastic differential equation for yields

with

Now, since , is a non-increasing function. By our assumptions on the admissible strategies, and thus the stochastic exponential is a local martingale (which follows from the basic properties of the Dooléans-Dade exponential). Therefore we can find a sequence of stopping times with a.s. satisfying

Since , an application of Fatou’s Lemma yields that is a supermartingale for every arbitrary admissible strategy . It remains to show that is a true martingale for the optimal strategy . In this case and hence . is a martingale by Lemma B.3 and so is . In order to show that is admissible, we have to show that (a), (b), (c) of Definition 3.1 hold. Part (a) is true because (3.5) has a unique solution in terms of as is deterministic. For part (b) it suffices to show that

Inserting the explicit solution of the wealth process into the left-hand side and applying a combination of Doob’s maximal inequality together with Hölder’s inequality then leads to the desired result. Part (c) is true as our resulting optimal strategies are deterministic.∎

3.4. The general correlation case

For the case where the correlation in (3.3) is given by an arbitrary vector , the martingale distortion arguments from the previous section do not work anymore. Therefore, we develop a new approach inspired by the verification arguments used in [3] to solve the optimization problem for this more general correlation structure. In this setting we say that a portfolio strategy is admissible if

-

(a)

the SDE (3.5) for the wealth process has a unique strong solution;

-

(b)

for all ;

-

(c)

is bounded.

Remember that , , , . The main result we provide for this case is the following:

Theorem 3.3.

Proof: The proof is a straight forward adaption of the arguments from the proof of Theorem 4.2 to the vector-valued case. ∎

3.5. Comparison of the different approaches

The martingale distortion approach in section 3.3 yields the following solution for the Merton portfolio problem in the -dimensional affine Volterra model. The optimal portfolio strategy is given by

The value function can be written as

with

where is the solution of the Riccati-Volterra equation

| (3.14) |

For the approach in section 3.4 we get the following results. The optimal portfolio strategy is given by

The value function can be written as

with

where is the (unique, global) solution of the Riccati-Volterra equation

| (3.15) |

Lemma 3.4.

Let and define . If is the unique global solution of the Riccati Volterra equation

then is the unique global solution of

.

Proof. First we show that .

Since is the unique solution of , we have

and thus has to be the unique solution of . ∎

Theorem 3.5.

Let . Then and for the value functions we have .

Proof. Recall that and . By the Lemma we have and the equality follows immediately. It remains to show that the value functions are equal. From Lemma 4.2 (Abi Jaber, affine Volterra processes) we know that

Using this fact, the value function reads

4. The Volterra-Wishart volatility model

In this section we present the Volterra-Wishart model which is a generalization of the Wishart volatility model described in [26] and [3] to the Volterra framework. In contrast to the class of models presented in the previous section, the volatility is now modeled as a matrix-valued stochastic process. The main advantage of using a matrix-valued volatility model is that this allows us to take into account the correlation between different stocks in our market and therefore extending the vector-valued model presented in the previous section. In contrast to the quadratic volatility models described in [5, Chapter 5] and [31], generalizing the Stein-Stein and Schöbel-Zhu model respectively, our model is an extension of the Heston model to the multivariate Volterra framework. The reason why we in particular investigate a Wishart model is that, besides being a straight forward generalisation of the popular Heston model, the additional degrees of freedom with regard to the stochastic correlation enable a better fit of market data while being still efficiently tractable, compare e.g. [33] and [34].

4.1. Market model and optimization problem

In our model the market consists of one riskfree asset with time-dependent, deterministic risk free rate and risky assets. The asset return vector process is defined via the stochastic differential system

| (4.1) |

where is a -dimensional Brownian Motion vector. The stochastic volatility process is given by the solution of the matrix-valued Volterra equation

| (4.2) | ||||

The integral kernel in the above equation is diagonal with scalar kernels . The deterministic initial value is assumed to be positive definite. The matrices and are responsible for the mean reversion, while matrix governs the volatility of the process which is driven by a Brownian motion matrix. In order to incorporate the leverage effect in our model, we allow the Brownian motions and to be correlated and we assume that with for and independent of . Thus for and another -dimensional Brownian motion vector independent of , we have

Under the assumption that the components of the kernel fulfill the condition

| (4.3) | ||||

Theorem 6.1 ensures the existence of a continuous, symmetric and positive definite -valued local weak solution to (4.1)-(4.2) on some filtered probability space , satisfying the usual conditions. For such a symmetric, positive definite matrix , by we denote the unique symmetric, positive definite matrix for which . Note that for we recover the classical Wishart model described in [3].

A portfolio strategy is an -valued, progressively measurable process, where represents the proportion of wealth invested into stock at time . Under a fixed portfolio strategy, the wealth process has dynamics

| (4.4) |

By we denote the set of admissible portfolio strategies.

Definition 4.1.

In our setting we say that a portfolio strategy is admissible if

-

(a)

the SDE (4.4) for the wealth process has a unique solution in terms of ;

-

(b)

for all ;

-

(c)

is bounded a.s.

We want to solve the Merton portfolio optimization problem for power utility, i.e. our aim is to find the value function such that

| (4.5) |

where is the conditional expectation. Again, the parameter represents the relative risk aversion of the investor. A portfolio strategy for which the supremum is attained is called an optimal strategy. As stated before, seen as an optimization problem with state process this problem is non-Markovian and the standard stochastic control approach cannot be applied.

4.2. The main result

We solve the Merton portfolio problem for the Volterra-Wishart model using a verification argument inspired by [3]. As it was pointed out in Section 3.3, the martingale distortion approach, used by [9] in the one dimensional case, can only be applied to the multivariate setting if the correlation structure is highly degenerate, i.e. . Since in our model we allow arbitrary correlation vectors , we have to use different techniques. The proof builds on ideas presented in [3] for the classical Wishart volatility model, yet we are facing serious technical challenges by doing that. In particular, in our case the stochastic volatility process is of convolution type and hence non-markovian, and therefore we cannot use Itô’s formula in order to show optimality of the candidate for the optimal strategy. In order to overcome this, we have to resort to the calculus of convolutions and resolvents. Note that the techniques we apply in our proof rely on the affine structure of the Volterra-Wishart convolution equation. Since the resulting calculations are rather involved, we present a condensed version of the proof here and the full proof can be found in Appendix A. Note that in contrast to the vector-valued cased, we cannot prove global existence of a week solution for the Volterra-Wishart process (4.2) and also the Riccati equation (4.6) can only be solved locally. Therefore we can only solve the Merton problem for a time horizon within the interval .

Theorem 4.2.

Assume that equation (4.2) has a positive definite, continuous weak solution on the interval . Let be the solution of the matrix Riccati-Volterra equation

| (4.6) |

with

| (4.7) |

on the interval , given by Theorem 6.4. Then for , , an optimal investment strategy for the Merton portfolio problem (4.5) is given by

| (4.8) |

and the value function can be written as

Sketch of Proof: In order to prove that is indeed the optimal portfolio strategy, we show that for

we have

-

(a)

for ,

-

(b)

for every other admissible strategy.

Proof of the equality (a): The SDE for the wealth process can be solved explicitly:

Introducing a new probability measure with Radon-Nikodym density

| (4.9) |

we obtain

where the matrix-valued, deterministic process is given by

Inserting the candidate for the optimal strategy , can be written in terms of

Let be the resolvent of the first kind of the integral kernel . Then by the associativity of the convolution and applying the fundamental theorem of calculus we obtain

Thus we can write as

We are interested in the expression . Under the probability measure , the process

is a -dimensional brownian motion by Girsanov’s theorem. The dynamics of the volatility process under can thus be written as

We insert the dynamics of into the expression and simplify using calculus of convolutions and resolvents. Finally, some terms cancel out and we end up with

Hence we obtain

Since is continuous, it is bounded and therefore the stochastic exponential is a true - martingale with expectation by Lemma B.1. Thus we get

This completes the first part of the proof.

Proof of the the inequality (b)

First note that standard techniques to prove the inequality like [27, Proposition 4.5] do not apply in our setting, since we can not use Itô’s formula due to the non-Markovianity of our volatility model. Therefore, we use a different approach writing an arbitrary strategy in terms of and some remainder .

To this end, let be an arbitrary admissible portfolio strategy. Define and write , where .

Since is bounded by assumption, we can define a new probability measure with Radon-Nikodym density

| (4.10) |

by Lemma B.2. Analogously to the first part we obtain

with

and is like in the first part. Under the probability measure defined in (A.2), the process

is a -dimensional brownian motion by Girsanov’s theorem. Hence the dynamics of the volatility process under can be written as

Again we calculate inserting the dynamics of and using calculus of convolutions and resolvents. Some terms cancel out and this time we end up with

The term is equivalent to and since is positive definite and , it has to be less than or equal to . Thus, for the expectation we get

Note that the last inequality does not hold for the case . Since the stochastic exponential is a -martingale with expectation by Lemma B.1, we finally obtain

which completes the proof. ∎

5. Numerical examples

In this section we compute the optimal portfolio strategy numerically in two-dimensional examples. To begin, we consider a financial market with one riskfree asset and risky assets and an investment horizon of year. The parameters are taken from [25], where such a model is calibrated to real market data from the Standard and Poor’s 500 Index and 30-year Treasury bond. They obtained the following estimation for the model parameters:

and . Roughness of the model is obtained by taking an appropriate integration kernel. We choose a fractional kernel of the form

This corresponds to the rough Heston model in the one-dimensional case. The roughness of the volatility paths is determined by the parameter and for we recover the classical model. The parameter is linked to the Hurst parameter via the equation . In our example the investor has a power utility function

The optimal strategy consists of a constant term

and a time-depending term

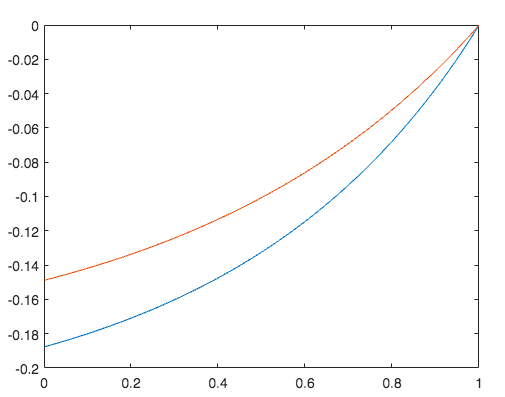

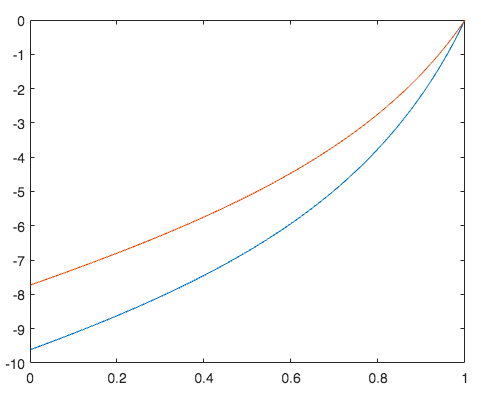

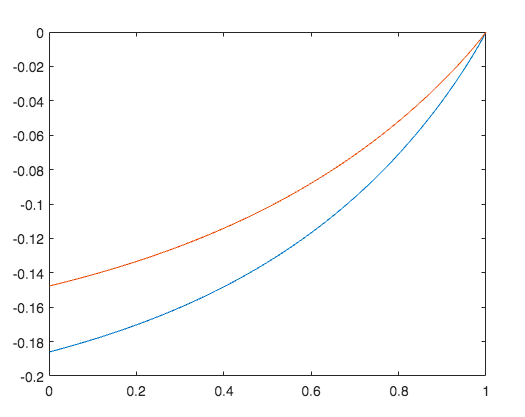

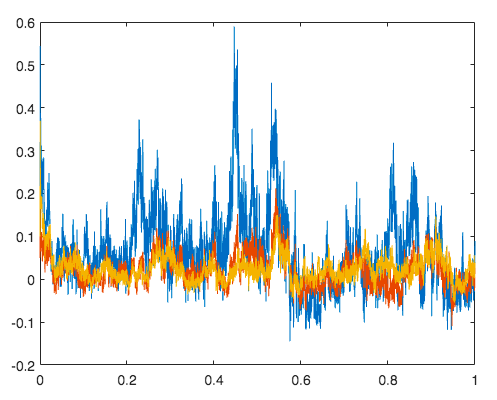

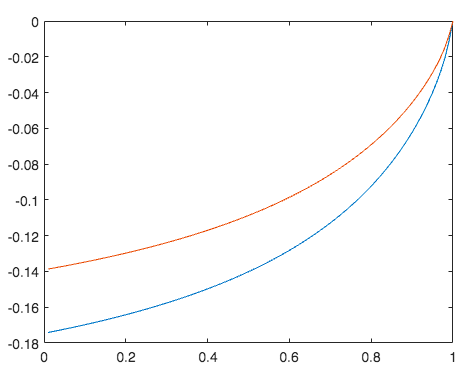

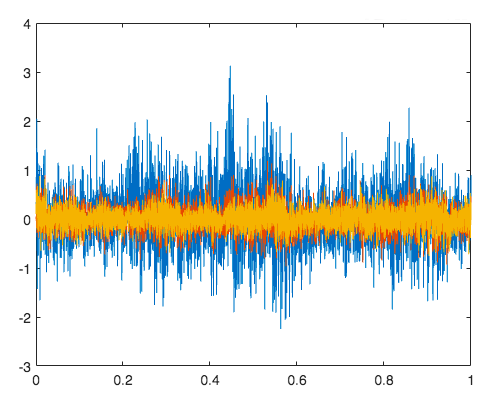

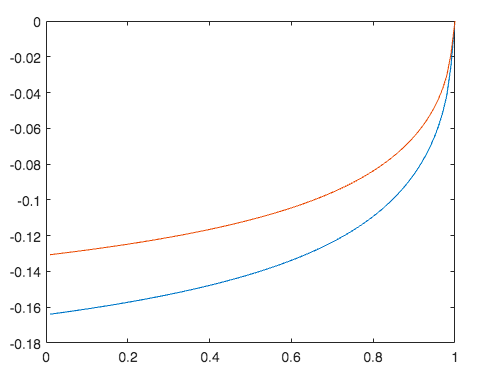

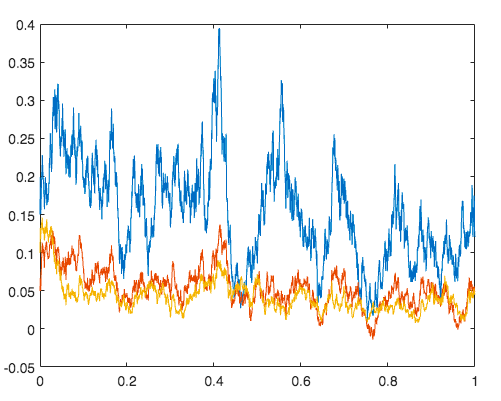

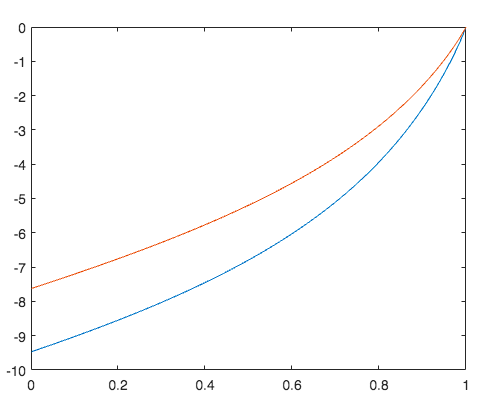

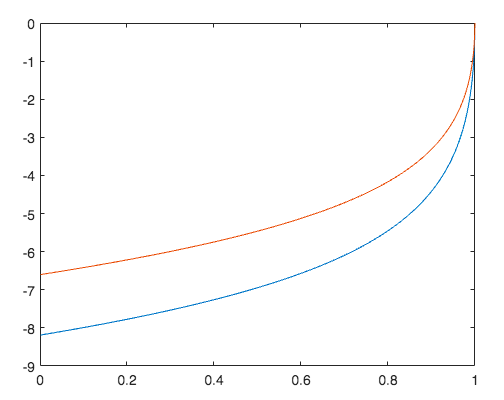

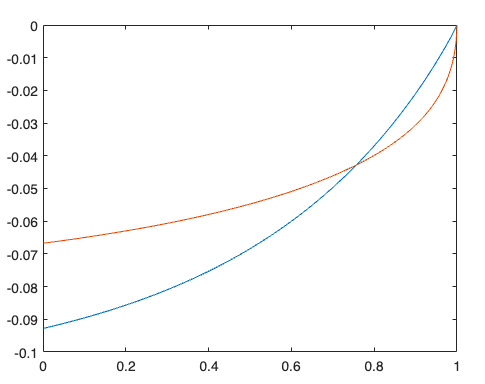

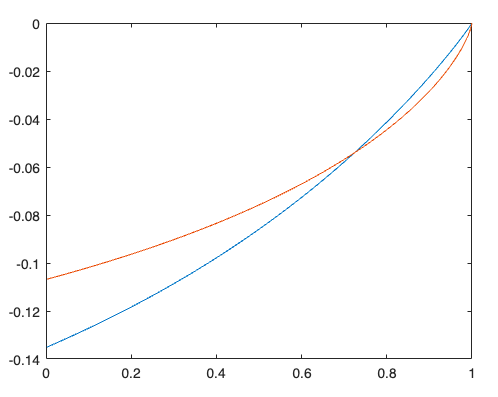

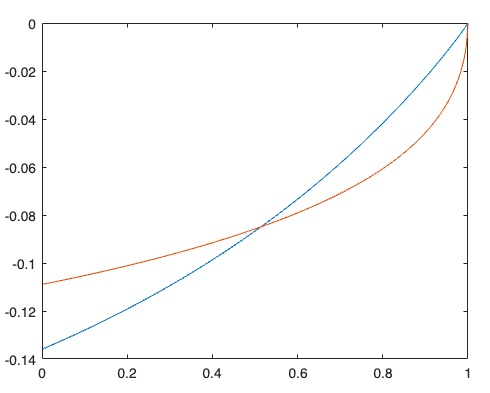

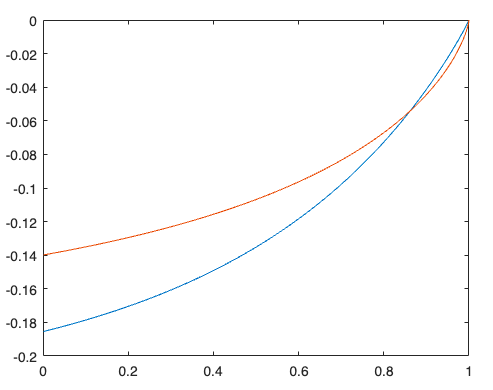

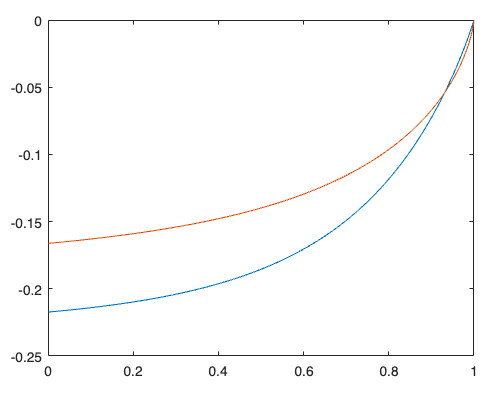

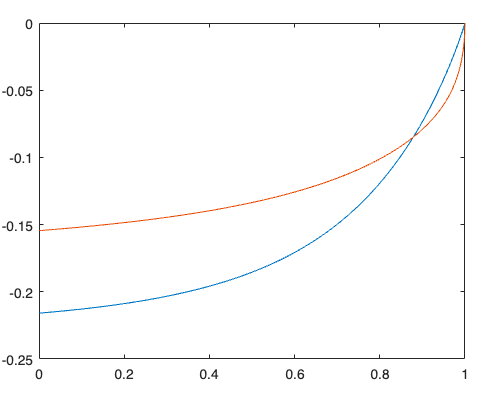

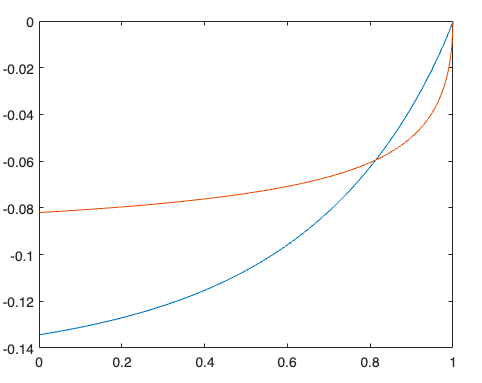

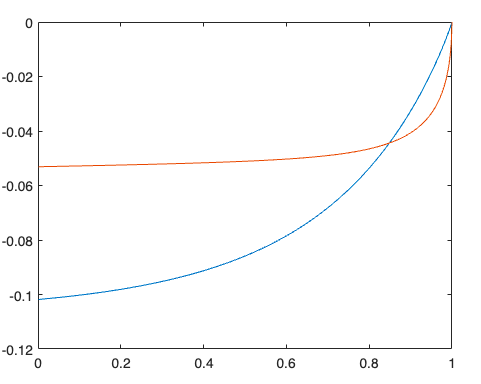

the hedging demand. Here the parameter is the market price of risk, is the relative risk aversion, is the correlation vector, is the Matrix governing the diffusion of the volatility process and is the solution of the matrix-valued Riccati-Volterra equation (4.6). In order to compute the hedging demand, we have to find the solution of equation (4.6). To this end we use the fractional Adams method developed in [28],[29] to obtain a numerical solution. The next diagram shows that if the roughness level , we recover the results of [3, Figure 1] for the classical Wishart model.

Figure 2 and 3 show that, in accordance with [3], the hedging demand for is negative. The lower the risk aversion of the investor, the more negative is his hedging demand. The roughness of the volatility of the assets also affects the hedging demand over time. Our illustrations show that the curvature of the hedging demand is increasing as the paths of the volatility become rougher.

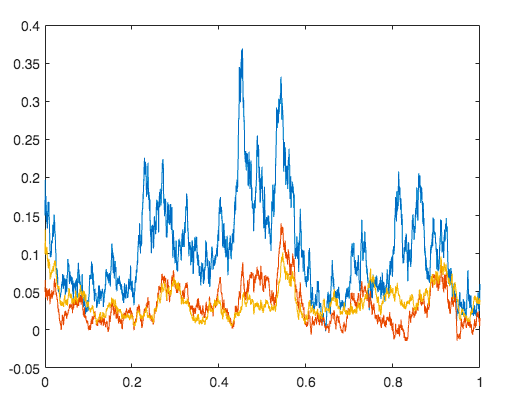

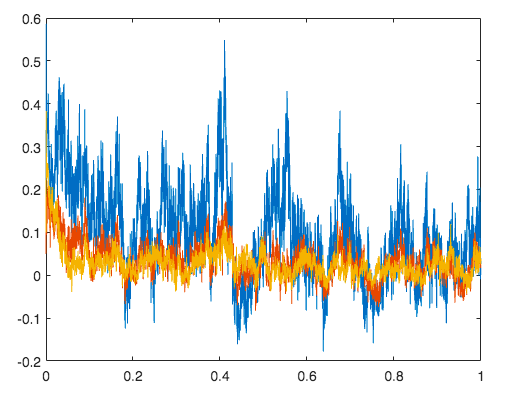

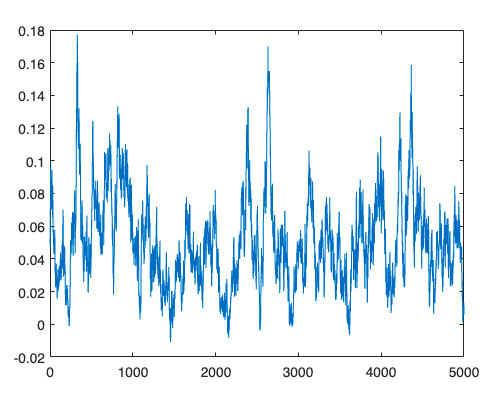

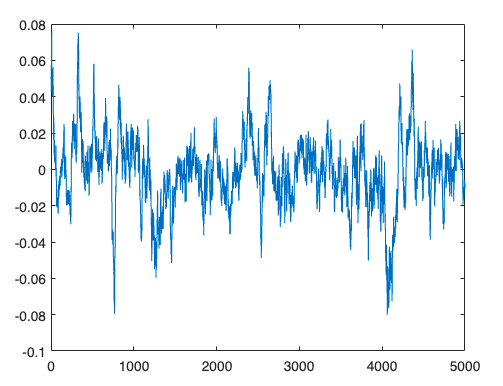

To have a comparison with another multivariate Volterra model, we adapt a numerical experiment from [5, Chapter 6] which was carried out for the Markowitz problem in a rough Stein-Stein model. Our aim is to investigate how the optimal investment strategy is affected on different time intervals within the investment horizon, if the investor can choose among a rough and a smooth asset with Hurst parameters . For this experiment we again use the parameters and as in the beginning of this section. Recall that the Hurst parameter is linked to the parameter in our integral kernels via . It turns out that as in [5], we end up with three distinct regimes:

-

(a)

: When the investment horizon is close to the end, the investor is selling a larger amount of the smooth asset than of the rough one.

-

(b)

: Here a transition of the investors behavior appears. First the agent prefers selling the rough asset but as the final horizon approaches, he prefers to sell the smooth asset.

-

(c)

: All the time until the transition point close to the maturity, the investor prefers selling the rough asset.

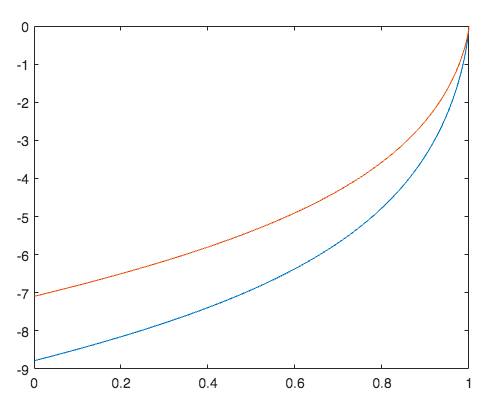

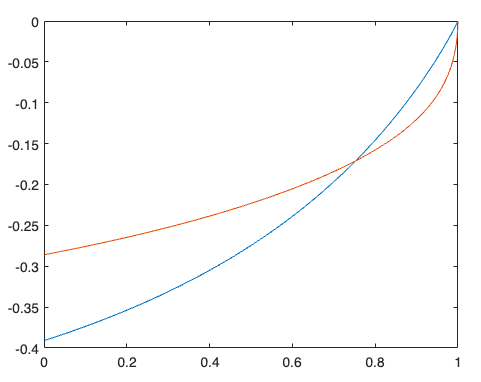

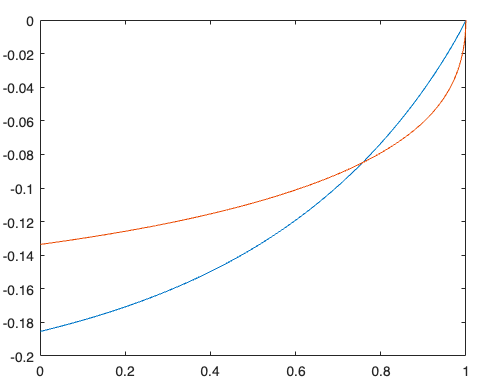

Our results are illustrated in Figure 5. As pointed out in [5], a possible interpretation of this transition could be that rough processes are more volatile than smooth processes in the short term but less volatile in the long term. Thus, when there is not much time left, the investor prefers rough assets to obtain some performance, whereas he favors the smooth asset on the long run. It turns out that the larger the difference of the roughness of the two assets becomes, the more the effect described above is pronounced. This means that if the second asset is very rough, the transition of the investors behavior happens earlier and the amount of rough assets the investor is selling decreases faster. In contrast to the Markowitz portfolio strategies studied in [5], we do not observe a structural difference in our portfolio strategies for different levels of asset correlation. While a positive asset correlation leads to a buy rough sell smooth strategy (cf. [32]) for the optimization problem in [5], in our case the correlation level only affects the extent to which the investor is selling both the smooth and the rough asset (see Figure 6). We want to point out that an average asset correlation of can be obtained by setting the non-diagonal entries of the matrices and to zero. Since our hedging demands are linear in terms of the vol-of-vol , the investors’ preferences are preserved in our model if is multiplied with constant, whereas in [AJMP21] the investor’s preferences do depend on the vol-of-vol. For completeness, this is illustrated in Figure 4.

6. Existence and uniqueness results for the Volterra equations

In this section we provide existence and uniqueness results for the Riccati-Volterra equations (4.6) and the stochastic Volterra equation (4.2).

6.1. Solution of the Volterra Wishart process

Previous research on stochastic Volterra equations has been carried out in the vector framework (cf. [5],[1]). For proving existence of a weak solution for the matrix-valued Volterra-Wishart equation (4.2), we use the vectorization operator in order to be able to resort to existing literature.

Theorem 6.1.

Proof: We cast the problem into the vector framework using the vectorization operator stacking the columns of a matrix on top of one another. This leads to the -valued stochastic Volterra equation

where

and

for some unitary matrix . We now show that and fulfill a linear growth condition.

with .

6.2. Solution of the Riccati Volterra equation

We use the concept of non-continuable solutions described in [1]. For an integral kernel and a function consider the Volterra integral equation

| (6.1) |

For , by a non-continuable solution of (6.1) we denote a pair with , such that satisfies (6.1) on and . A non-continuable solution is unique if for any and with satisfying (6.1) on , we have and on . If , we call a global solution of (6.1).

Theorem 6.2.

Proof: The Riccati-Volterra equations (3.8) and (3.11) are both of the form

where is given by

with , and . Thus for , we get

with positive constants and . Here we have used the triangle inequality, the Cauchy-Schwarz inequality and the fact that for , we get . Now existence and uniqueness of a non-continuable solution follows directly from [1, Theorem B1]. ∎

In case that the matrix in equation (3.2) is diagonal, there exists even a global solution.

Theorem 6.3.

Assume that the matrix in the drift of the volatility process is a diagonal matrix, i.e. . Then the Riccati-Volterra equation (3.11) has a unique global solution if for all

Proof: If is a diagonal matrix, the matrix in equation (3.11) becomes a diagonal matrix of the form with . Now the vector valued equation (3.11) can be decomposed into real valued Riccati-Volterra equations such that for the th component of we obtain

| (6.2) |

By our assumptions and and therefore [10, Lemma A2] (cf. [8, Lemma A5]) guarantees the existence of a unique continuous global solution of the equation (6.2). Combining the component-wise solutions, we finally obtain the unique global solution of equation (3.11). ∎

A vectorization argument allows us to prove existence of a local solution for the matrix Riccati-Volterra equation (4.6).

Theorem 6.4.

The matrix Riccati-Volterra equation (4.6) has a unique non-continuable continuous solution .

Proof: We cast the problem into the vector framework using the vectorization operator stacking the columns of a matrix on top of one another. This leads to the -valued Riccati-Volterra equation

where denotes the Kronecker product. We now show that fulfills the growth condition

with positive constants amd .

For the first and the second term of this sum, we have

and

Since , we choose . For the third term, it holds that

One of the following statements must be true:

or

Without loss of generality we only treat the first case. Thus we obtain

The matrix is symmetric and thus its spectral decomposition can be written as for an orthogonal matrix . Let be the largest eigenvalue of . Since has only non-negative eigenvalues, is positive definite and so is . Since the trace of a matrix is the sum of its eigenvalues we have

and thus

Using the above facts, we obtain

Hence we have

leading to .

Now an application of [1, Theorem B2] yields the desired result. ∎

Appendix A Detailed proof of the main result

Proof: In order to prove that is indeed the optimal portfolio strategy, we show that for

we have

-

(a)

for ,

-

(b)

for every other admissible strategy.

We start with equation (a). The SDE for the wealth process can be solved explicitly and we obtain for an arbitrary admissible portfolio strategy

with .

Since is continuous by the continuity of , it is also bounded and thus we can define a new probability measure with Radon-Nikodym density

| (A.1) |

which is a martingale by Lemma B.2. Then we obtain

In the following, we denote the matrix-valued deterministic process by

Inserting the optimal strategy , we obtain

Under the probability measure defined in (A.1), the process

is a -dimensional brownian motion by Girsanov’s theorem. The dynamics of the volatility process under can thus be written as

Let be the resolvent of the first kind of the integral kernel . Then by the associativity of the convolution and applying the fundamental theorem of calculus we obtain

Here the last equality follows from equation (4.7). Thus we can write as

and consequently we have

We consider the term and substitute

This yields

We now simplify the terms , and using stochastic calculus of convolutions and resolvents.

ad (I):

ad (II):

ad (III):

The processes and are both continuous local martingales and and are locally bounded. Thus we can apply Lemma 2.5 to obtain

Combining the above results, we end up with

Hence we obtain

Since is continuous, it is bounded and therefore the stochastic exponential is a true - martingale with expectation by Lemma B.1. Thus we get

This completes the first part of the proof.

It remains to show the inequality (b) for arbitrary admissible portfolio strategies.

To this end, let be an arbitrary admissible portfolio strategy. Define and write , where . Since is bounded by assumption, we can define a new probability measure with Radon-Nikodym density

| (A.2) |

by Lemma B.2.

Analogously to the first part we obtain

We define

with

Under the probability measure defined in (A.2), the process

is a -dimensional brownian motion by Girsanov’s theorem.

Then the dynamics of the volatility process under can be written as

Therefore, we get

Combining the above results, we obtain

Since

three terms in the above sum cancel out and we end up with

Thus, for the expectation we get

The last inequality follows from the fact that is positive definite and . Since the stochastic exponential is a -martingale with expectation by Lemma B.1, we finally obtain

which completes the proof. ∎

Appendix B Martingale property of stochastic exponentials

In this section we proof the martingale property of the stochastic exponentials appearing in Section 3 and Section 4. The following lemma is an adaption of [1, Lemma 7.3] to the multivariate case.

Lemma B.1.

Let us denote

where is a deterministic process with values in and bounded by . Then is a martingale.

Proof: The process is a stochastic exponential of the form . Since is a non-negative local martingale, is a supermartingale by Fatou’s lemma. Thus, in order to show that is a true martingale, it suffices to show that for any . For a fixed we define the stopping times

The process is a uniformly integrable martingale for each , since the Novikov condition is fulfilled due to the boundedness of . Thus we get

By the theorem of dominated convergence, and thus, in order to show that , it is sufficient to prove that

Since is a martingale, we can define probability measures with Radon-Nikodym densities

By Girsanov’s theorem the process defined by

is a -dimensional Brownian motions under the measure . Furthermore, under we have with

Using the vectorization operator from Section 6, the above equation can be written as

where

and

for some unitary matrix . Using similar arguments as in the proof of Theorem 6.1, one can show that the drift and the diffusion term of the above equation fulfill the linear growth condition [1, condition (3.1)], i.e. we have

Note that the argument for the drift only works if the matrix is bounded. Choose sufficiently large that where for defined in (4.3). An application of [1, Lemma 3.1] yields the moment bound

for some constant independent of . The -Hölder seminorm of a function is defined as

Claim: For some constant independent of the following inequality holds:

Proof of Claim: We have to show that

or equivalently

Since for a vector we have for , it holds that the left-hand side is bounded by

Using the fact that the square of the supremum of a set of non-negative numbers equals the supremum of the squares, it remains to show that

Clearly

and since

we get

This completes the proof of the claim. ∎

We now show that as :

Since the constant is independent of we finally obtain

which completes the proof. ∎

Lemma B.2.

Let us denote

where is a deterministic process with values in and bounded by . Then is a martingale.

The next lemma is an enhancement of [5, Appendix C], the proof follows similar arguments.

Lemma B.3.

Let , be two independent -dimensional brownian motions and for let . Then the local martingale

is a true martingale.

Proof: Set . Then by the stochastic Fubini theorem we get

with

Since is a non-negative local martingale, is a supermartingale by Fatou’s lemma. Thus, in order to show that is a true martingale, it suffices to show that for any . For a fixed we define the stopping times

The stopped process is a uniformly integrable martingale for each , since the Novikov condition is fulfilled due to the boundedness of and . Thus we get

By the theorem of dominated convergence, and thus, in order to show that , it is sufficient to prove that

| (B.1) |

Since is a martingale, we can define probability measures with Radon-Nikodym densities

By Girsanov’s theorem the processes and defined by

are -dimensional Brownian motions under the measure . Furthermore, under we have

and under , the drift of satisfies a linear growth condition in for some constant independent of . Therefore an application of the generalized Grönwall inequality (cf. [7, Lemma 3.1]) yields the moment bound

where does not depend on . An application of Chebyshev’s inequality yields

This completes the proof. ∎

Appendix C Dynamics of the process

We derive the dynamics of the process appearing in the martingale distortion approach using Itô’s formula (cf. [9, Theorem 3.2]).

Lemma C.1.

The process defined in (3.7) has dynamics

Here, for the second equality, we used the stochastic Fubini theorem from [15]. Next, we show that

We have

Here the last equality holds, since

Thus we get

where and .

Since , by Itô’s formula we obtain , i.e

The last equality holds, since in the degenerate correlation case we have the following identity:

∎

Acknowledgements

F. Aichinger and S. Desmettre are supported by the Austrian Science Fund (FWF) project F5507-N26, which is part of the Special Research Program Quasi-Monte Carlo Methods: Theory and Applications. We also thank Bingyan Han for useful discussions concerning Lemma B.3.

References

- [1] Abi Jaber, Eduardo and Larsson, Martin and Pulido, Sergio: Affine Volterra processes. The Annals of Applied Probability 29, 3155–3200 (2019)

- [2] Bäuerle, Nicole and Desmettre, Sascha: Portfolio optimization in fractional and rough Heston models. SIAM Journal on Financial Mathematics 11, 240–273 (2020)

- [3] Bäuerle, Nicole and Li, Zejing: Optimal portfolios for financial markets with Wishart volatility. Journal of Applied Probability 50, 1025–1043 (2013)

- [4] Zariphopoulou, Thaleia: A solution approach to valuation with unhedgeable risks. Finance and Stochastics 5, 61–82 (2001)

- [5] Abi Jaber, Eduardo and Miller, Enzo and Pham, Huyên: Markowitz portfolio selection for multivariate affine and quadratic Volterra models. SIAM Journal on Financial Mathematics 12, 369–409 (2021)

- [6] Fouque, Jean-Pierre and Hu, Ruimeng: Optimal portfolio under fractional stochastic environment. Mathematical Finance 29, 697–734 (2019)

- [7] Abi Jaber, Eduardo: Weak existence and uniqueness for affine stochastic Volterra equations with L1-kernels. Bernoulli 27, 1583–1615 (2021)

- [8] Gatheral, Jim and Keller-Ressel, Martin: Affine forward variance models. Finance and Stochastics 23, 501–533 (2019)

- [9] Han, Bingyan and Wong, Hoi Ying: Merton’s portfolio problem under Volterra Heston model. Finance Research Letters 39 (2021)

- [10] Han, Bingyan and Wong, Hoi Ying: Mean–Variance portfolio selection under Volterra Heston model. Applied Mathematics & Optimization 84, 683–710 (2020)

- [11] Fouque, Jean-Pierre and Sircar, Ronnie and Zariphopoulou, Thaleia: Portfolio optimization and stochastic volatility asymptotics. Mathematical Finance 27, 704–745 (2017)

- [12] Tehranchi, Michael: Explicit solutions of some utility maximization problems in incomplete markets. Stochastic Processes and their Applications 114, 109–125 (2004)

- [13] Jeanblanc, Monique and Mania, Michael and Santacroce, Marina and Schweizer, Martin: Mean-variance hedging via stochastic control and BSDEs for general semimartingales. The Annals of Applied Probability 22, 2388–2428 (2012)

- [14] Gripenberg, G. and Londen, S.-O. and Staffans, O.: Volterra integral and functional equations. Encyclopedia of Mathematics and its Applications, vol. 34. Cambridge University Press, Cambridge (1990)

- [15] Veraar, Mark: The stochastic Fubini theorem revisited. Stochastics 84, 543–551 (2012)

- [16] Abi Jaber, Eduardo and El Euch, Omar: Markovian structure of the Volterra Heston model. Statistics & Probability Letters 149, 63–72 (2019)

- [17] Gatheral, Jim and Jaisson, Thibault and Rosenbaum, Mathieu: Volatility is rough. Quantitative Finance 18, 933–949 (2018)

- [18] Heston, Steven L.: A closed-form solution for options with stochastic volatility with applications to bond and currency options. The Review of Financial Studies 6, 327–343 (1993)

- [19] El Euch, Omar and Rosenbaum, Mathieu: The characteristic function of rough Heston models. Mathematical Finance 29, 3–38 (2019)

- [20] Keller-Ressel, Martin and Larsson, Martin and Pulido, Sergio: Affine rough models. arXiv preprint arXiv:1812.08486 , (2019)

- [21] Diehl, Joscha and Friz, Peter K. and Gassiat, Paul: Stochastic control with rough paths. Applied Mathematics and Optimization 75, 285–315 (2017)

- [22] Hu, Ying and Imkeller, Peter and Müller, Matthias: Utility maximization in incomplete markets. The Annals of Applied Probability 15, 1691–1712 (2005)

- [23] Cuchiero, Christa and Teichmann, Josef: Markovian lifts of positive semidefinite affine Volterra-type processes. Decisions in Economics and Finance 42, 407–448 (2019)

- [24] Tomas, Mehdi and Rosenbaum, Mathieu: From microscopic price dynamics to multidimensional rough volatility models. arXiv preprint arXiv:1910.13338 , (2019)

- [25] Buraschi, Andrea and Porchia, Paolo and Trojani, Fabio: Correlation risk and optimal portfolio choice. Decisions in Economics and Finance 65, 393–420 (2010)

- [26] Gourieroux, Christian and Sufana, Razvan: Derivative pricing with Wishart multivariate stochastic volatility. Journal of Business & Economic Statistics 28, 438–451 (2010)

- [27] Kraft, Holger: Optimal portfolios and Heston’s stochastic volatility model: an explicit solution for power utility. Quantitative Finance 5, 303–313 (2005)

- [28] Diethelm, Kai and Ford, Neville J. and Freed, Alan D.: A predictor-corrector approach for the numerical solution of fractional differential equations. Nonlinear Dynamics 29, 3–22 (2002)

- [29] Diethelm, Kai and Ford, Neville J. and Freed, Alan D.: Detailed error analysis for a fractional Adams method. Numerical Algorithms 36, 31–52 (2004)

- [30] Kallsen, Jan and Muhle-Karbe, Johannes: Utility maximization in affine stochastic volatility models. International Journal of Theoretical and Applied Finance 13, 459–477 (2010)

- [31] Abi Jaber, Eduardo: The Laplace transform of the integrated Volterra Wishart process. Mathematical Finance 32, 309–348 (2022)

- [32] Glasserman, Paul and He, Pu: Buy rough, sell smooth. Quantitative Finance 20, 363–378 (2020)

- [33] Benabid, Anas and Bensusan, Harry and El Karoui, Nicole: Wishart stochastic volatility: Asymptotic smile and numerical framework. Stochastic Processes and their Applications (2008)

- [34] La Bua, Gaetano and Marazzina, Daniele: On the application of Wishart process to the pricing of equity derivatives: the multi-asset case. Computational Management Science 18, 149–176 (2021)